a new approach to analyzing credit and bankruptcy risk...

TRANSCRIPT

A NEW APPROACH TO ANALYZING CREDIT AND BANKRUPTCY RISKCFA INSTITUTE: 64th ANNUAL CONFERENCEEDINBURGH, SCOTLAND,10 MAY 2011

Tim Gaumer, CFADirector of Fundamental Research Thomson ReutersDirector of Fundamental Research, Thomson Reuters

AGENDA

• CREDIT RISK MODEL– STRUCTURAL MODEL (MERTON APPROACH)– RATIO ANALYSIS

MINING TEXT DOCUMENTS– MINING TEXT DOCUMENTS– ESTIMATING LOSS GIVEN DEFAULT– CDS MARKET– COMBINATION RESULTS

• Q & A

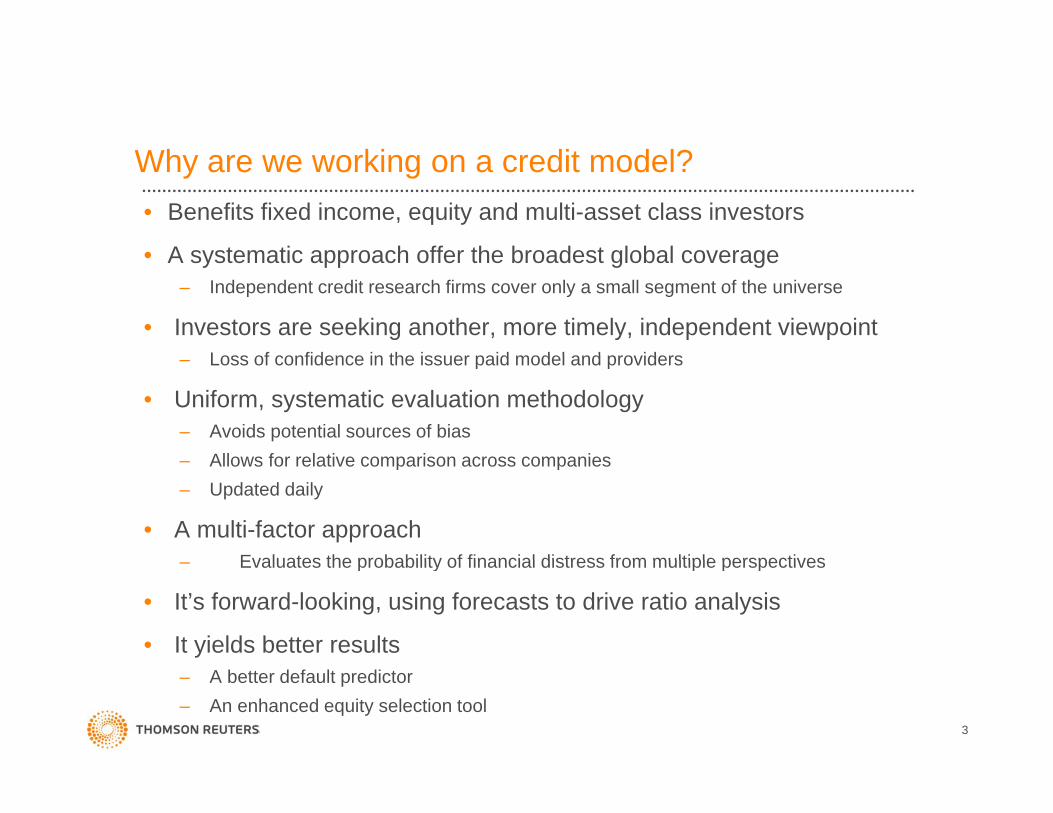

Wh ki dit d l?Why are we working on a credit model?• Benefits fixed income, equity and multi-asset class investors

• A systematic approach offer the broadest global coverage• A systematic approach offer the broadest global coverage– Independent credit research firms cover only a small segment of the universe

• Investors are seeking another, more timely, independent viewpointLoss of confidence in the iss er paid model and pro iders– Loss of confidence in the issuer paid model and providers

• Uniform, systematic evaluation methodology– Avoids potential sources of bias

Allows for relative comparison across companies– Allows for relative comparison across companies– Updated daily

• A multi-factor approachEvaluates the probability of financial distress from multiple perspectives– Evaluates the probability of financial distress from multiple perspectives

• It’s forward-looking, using forecasts to drive ratio analysis

• It yields better results– A better default predictor– An enhanced equity selection tool

3

StarMine Credit Risk: Analytics built on Thomson Reuters content

C dit i k t i ti b bilit f d f ltCredit risk metrics – rating, probability of default

For trading, investment management, risk management

StarMine Credit Risk g

5 Powerful component models il bl i di id ll t th

Component ModelsCDS modelLoss Given Default

Sophisticated analytics that allow clear

available individually or together

StarMine Analytics

SmartEstimates Implied

Financial Ratios

Text Mining

Structural(Merton)

Volatility

Text processing &

Capital structure

Incorporates text estimates

Sophisticated analytics that allow clear drill-down

Thomson Reuters Source Data

I/B/E/S Thomson Reuters

Reuters News

SmartEstimates+ SmartRatios

Implied CDS Spread

Reuters

StreetEventsTranscripts

DataScope Fixed

Text processing &document scoring

Filings SECAPI

Incorporates text, estimates, and other unique, high-quality content

I/B/E/S Estimates

Thomson Reuters CDS Spreads

Reuters Fundamentals

DataScope Fixed Income & Equities

4

AGENDA

• CREDIT RISK MODEL– STRUCTURAL MODEL (MERTON APPROACH)– RATIO ANALYSIS

MINING TEXT DOCUMENTS– MINING TEXT DOCUMENTS– ESTIMATING LOSS GIVEN DEFAULT– CDS MARKET– COMBINATION RESULTS

• Q & A

Merton/Structural model:A standard approach that works well

Input Effect on default probabilityLeverage (debt/assets) Higher leverage increases D.P.Asset volatility Higher asset volatility increases D.P.Asset growth rate Higher growth rate decreases D.P.

• Uses option pricing theory to estimate market value of a firm’s assets.

s

A possible asset value path

(random walk with drift)

• Models a company’s equity as a call option on its assets.

• Probability of default equates to probability that asset value of Va

lue of Asset

Distribution ofasset value at horizon

probability that asset value of firm will fall below the default point (~liabilities). i.e., probability that the option expires worthless

Market A0

Default Point

Probabilityexpires worthless.

• We use a 1-year horizon. Time

of default

6

Our Structural Credit Risk (SCR) improves on the ( ) pMerton model with a number of innovative features

• Optimized leverage, volatility, and drift inputs.• e.g. different treatment of balance sheet liabilities for certain companies in

the financials sector.

• Employs region-specific adjustments to default rates

• Leverages StarMine Val-Mo model as an input• helps predict the upward or downward direction of future drift of the assets

7

StarMine SCR’s default prediction rate outperforms p pthe Altman Z-score, and basic Merton model

1 0

0 7

0.8

0.9

1.0ptured

in

e

0.4

0.5

0.6

0.7

Defau

lts Ca

pkiest Q

uintile

0.1

0.2

0.3

0.4

Fraction

of

Ris

0.0

0.1

All firms Financial sector firms

StarMine SCR Basic Merton Model Altman Z

8

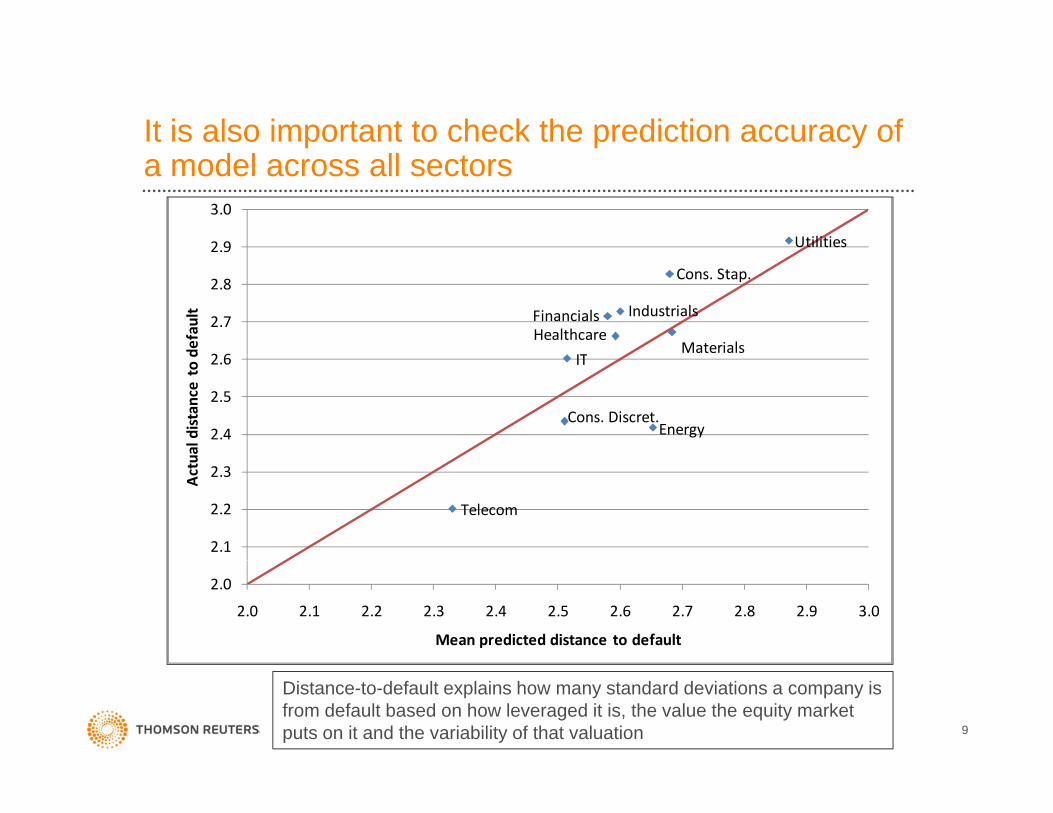

It is also important to check the prediction accuracy of a model across all sectors

2.9

3.0

Utilities

2 6

2.7

2.8

default

ITMaterials

Industrials

Cons. Stap.

HealthcareFinancials

2.4

2.5

2.6

ual distance to d IT

EnergyCons. Discret.

2.1

2.2

2.3Actu

Telecom

2.0

2.0 2.1 2.2 2.3 2.4 2.5 2.6 2.7 2.8 2.9 3.0

Mean predicted distance to default

9

Distance-to-default explains how many standard deviations a company is from default based on how leveraged it is, the value the equity market puts on it and the variability of that valuation

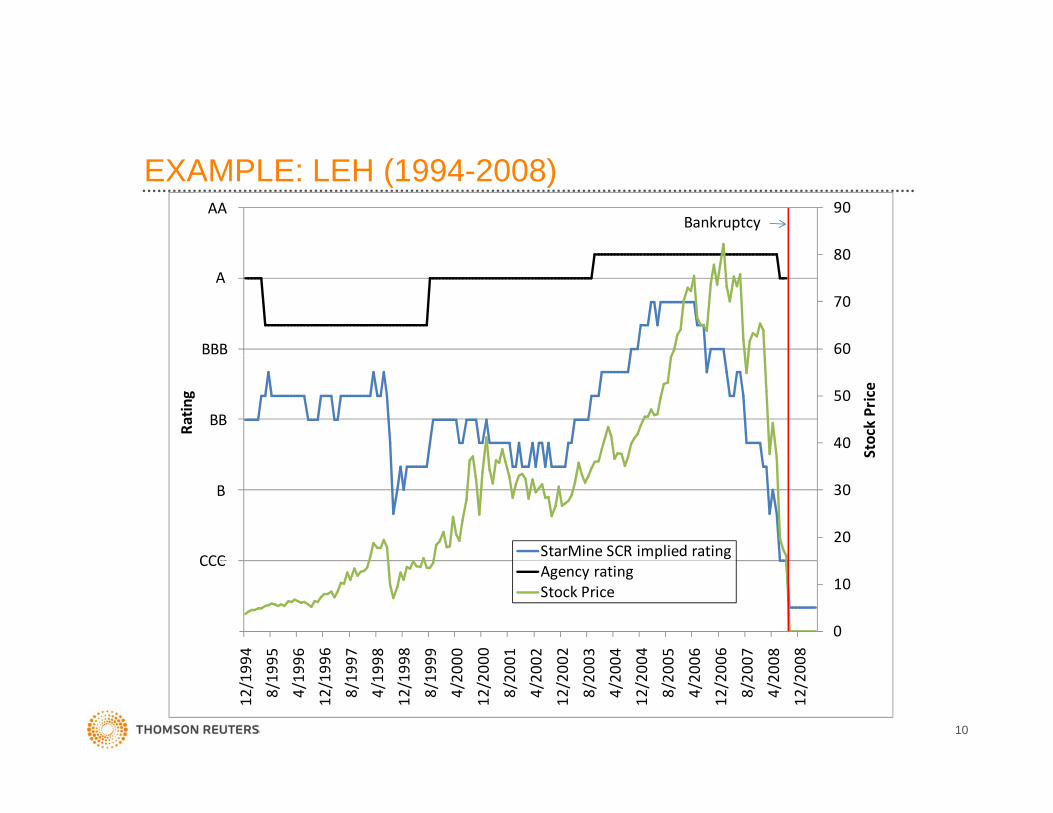

EXAMPLE: LEH (1994-2008)

80

9024AABankruptcy

60

70

80

18

21A

BBB

40

5015

Stock Price

Rating

BB

20

30

9

12

StarMine SCR implied rating

B

CCC

0

10

6

9

94 95 96 96 97 98 98 99 00 00 01 02 02 03 04 04 05 06 06 07 08 08

Agency ratingStock Price

CCC

10

12/199

8/19

9

4/19

9

12/199

8/19

9

4/19

9

12/199

8/19

9

4/20

0

12/200

8/20

0

4/20

0

12/200

8/20

0

4/20

0

12/200

8/20

0

4/20

0

12/200

8/20

0

4/20

0

12/200

A SCR model can be used in several different contexts• Fixed Income:

– Measuring the riskiness of fixed income assets relative to their prices and yields

• Equity Selection:– Screening for “quality” stocks with low default risk

• Cross-asset Arbitrage:Comparing StarMine SCR defa lt probabilities ith CDS– Comparing StarMine SCR default probabilities with CDS spreads (riskiness)

11

It can also be used to improve equity portfolio performance

7Combining StarMine Val‐Mo with StarMine SCR

6

7

Val‐Mo OnlyVal‐Mo Reduced to Merton Portfolio SizeVal‐Mo Filtered by StarMine SCR

4

5

Sharpe

Ratio

2

3

Ann

ualized

0

1

1998 1999 2000 2001 2002 2003 2004 2005 2007 2008 O ll1998 1999 2000 2001 2002 2003 2004 2005 2007 2008 Overall

12

AGENDA

• CREDIT RISK MODEL– STRUCTURAL MODEL (MERTON APPROACH)– RATIO ANALYSIS

MINING TEXT DOCUMENTS– MINING TEXT DOCUMENTS– ESTIMATING LOSS GIVEN DEFAULT– CDS MARKET– COMBINATION RESULTS

• Q & A

Financial ratios for predicting firm failure can be grouped i t l t i W t f h

Profitability Coverage Growth

into several categories. We create scores for each.

Profitability(e.g., Return on Capital, Profit

Margin)

Leverage(e.g., Net

Debt/Equity)

Coverage(e.g.,

EBITDA/Interest, CashFlow/Debt)

Liquidity(e.g., quick ratio,

Cash/Debt)

Growth(e.g., ROE

expansion, stability of EPS growth)

Industry-specific

SmartRatios Score&

specific Information

Country/Region

Probability of Defaulteffects

14

SmartRatios Credit RiskComponents KeyProfi tabi l i ty Scores 91‐100 (lowest risk)

Score PD

0 015% Leverage Scores 71‐90Coverage Scores 31‐70Liquidi ty Scores 11‐30Growth Scores 1‐10 (highest ri sk)

78100=lowest risk

0.015%(AA‐)

15

Incorporates both forward-looking (via SmartEstimate) and trailing ratios

SmartRatios Credit RiskComponents KeyProfi tabi l i ty Scores 91‐100 (lowest risk)

Score PD

0 015% Leverage Scores 71‐90Coverage Scores 31‐70Liquidi ty Scores 11‐30Growth Scores 1‐10 (highest ri sk)

78100=lowest risk

0.015%(AA‐)

16

Incorporates both forward-looking (via SmartEstimate) and trailing ratios

Incorporates industry-specific ratios where appropriate

SmartRatios Credit RiskComponents KeyProfi tabi l i ty Scores 91‐100 (lowest risk)

Score PD

0 015% Leverage Scores 71‐90Coverage Scores 31‐70Liquidi ty Scores 11‐30Growth Scores 1‐10 (highest ri sk)

78100=lowest risk

0.015%(AA‐)

17

Incorporates both forward-looking (via SmartEstimate) and trailing ratios

Incorporates industry-specific ratios where appropriate

Incorporates often over-looked items

Ratios based on StarMine SmartEstimates are more predictive than trailing ratios

80%

Value of SmartRatiosHit Rate: % of Failures Identified among High Risk (bottom 20%) Firms

60%

70%

80%

entif

ied

ms

40%

50%

f Fai

lure

s Id

eig

h R

isk

Firm

10%

20%

30%

Hit

Rat

e: %

of

amon

g H

i

0%

10%

FY0 FY1 SmartRatio

FY0 FY1 SmartRatio

FY0 FY1 SmartRatio

H

Earnings/Assets Debt/Equity Cash Flow/Interest

18

Industry-specific ratios: Some industries need special consideration

Ratios Banks Insurance Retail Airlines Utilities Oil & Gas All Others

Profitability Return on Capital √ √ √ √ √ √ √Profit Margin √ √ √ √ √ √ √U li d L √ √ √ √ √ √ √Unrealized Losses √ √ √ √ √ √ √Change in LIFO Reserve √ √ √ √ √ √ √Operating Leverage √Combined Ratio √Break‐even load √Passenger load √Generation Cost √

Leverage Assets/Equity √ √ √ √ √ √ √Unfunded Pension Liab √ √ √ √ √ √Net Debt/Equity √ √ √ √ √ √Tier 1 Capital Ratio √Loans/Deposits √

Coverage EBTIDA/Interest √ √ √ √ √ √Free Cash Flow/Debt √ √ √ √ √ √EBIT/Interest √ √ √ √ √ √Non‐performing Loans √Loan‐loss provision √Other Real‐Estate Owned √

Liquidity Cash/Debt √ √ √ √ √ √ √Short‐term Debt/ Total Debt √ √ √ √ √ √ √Quick Ratio √ √ √ √ √Change in Quick Ratio √ √ √ √ √Change in Reserve √Fuel Reserve √

19

Proven reserves √

Growth Normalized ROE Growth √ √ √ √ √ √ √Standard Deviation of EPS Growth √ √ √ √ √ √ √Standard Deviation of Revenue Growth √ √ √ √ √ √ √Same‐Store Sales Growth √

Incorporating industry-specific metrics adds value

20

For global large-cap equities, both Sharpe Ratio and R t i i k t k l d dReturns increase as more risky stocks are excluded

StarMine Val‐Mo Long‐only Portfolio Filtered by SmartRatios Model PDGlobal Top 2000, Jan 1998 ‐May 2009

35%

40%

1.40

1.60

cileReturn

p , y

Annualized Sharpe

Annualized Return

20%

25%

30%

0 80

1.00

1.20

urn of Top

Dec

of Top

Decile

R

10%

15%

20%

0.40

0.60

0.80

nnua

lized

Retu

alized

Sha

rpe o

0%

5%

0.00

0.20

3 31 1 75 1 09 0 73 0 50 0 36 0 25 0 16 0 09

An

Ann

ua

21

3.31 1.75 1.09 0.73 0.50 0.36 0.25 0.16 0.09

StarMine SmartRatios Model PD Cutoff (%)

BBB+BBBBBB‐BB+BB+BBBB‐BB‐B

S R i M d l dSmartRatios Model advantages

• Forward looking via StarMine SmartEstimates

• Incorporates industry-specific ratios

• Includes often overlooked information (e.g., unrealized losses)

• More timely (updated daily)More timely (updated daily)

• Broader coverage (~35,000 companies globally), including financial sector.

22

AGENDA

• CREDIT RISK MODEL– STRUCTURAL MODEL (MERTON APPROACH)– RATIO ANALYSIS

MINING TEXT DOCUMENTS– MINING TEXT DOCUMENTS– ESTIMATING LOSS GIVEN DEFAULT– CDS MARKET– COMBINATION RESULTS

• Q & A

Text mining of company documents can predict financial failure

• Identify linguistic content that provides best discrimination between fi th t f il th th t d tfirms that fail vs. those that do not

• Apply sophisticated machine learning algorithms to these high-dimensional data to provide unique and powerful failure

di tipredictions

24

T Mi i C di Ri kText Mining Credit RiskDocuments (news, transcripts, filings)

FULL Numerical representation of documentsp , g )

“good i

ClearForest Calais

covenantgood

morning apple …doc1 0 1 1 …doc2 1 1 0 …doc3 1 0 0morning…

…potentially violating the covenants…”

potential,violat,the,covenant,

Stem words. Remove high frequency words Chop

doc3 1 0 0 …… … … … …

Bag-of-words

potential violat,…,

words. Chop into unique words and phrases Select most

valuable k-mers

tcredit f il

Officers t d

Make Date Company

Probability of Default

date1 A 0 0011Machine L i

covenant facil arrested …doc1 0 0 1 …doc2 1 0 0 …doc3 1 1 0 …

… … … … …

predictionsdate1 A 0.0011date1 B 0.0132date1 C 0.0578

… … …

Learning Algorithm

… … … … …

25

8-K filings are more numerous, and more timely (4

# of Documents per year by filing type

g , y (days vs 90 days allowed) than statements

120000

140000

160000

80000

100000

f Docum

ents

20000

40000

60000# o

0

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

10K and 10Q Filings 8‐Ks Filings

SarbOxReg FD 26

Statements = 10K & 10Q

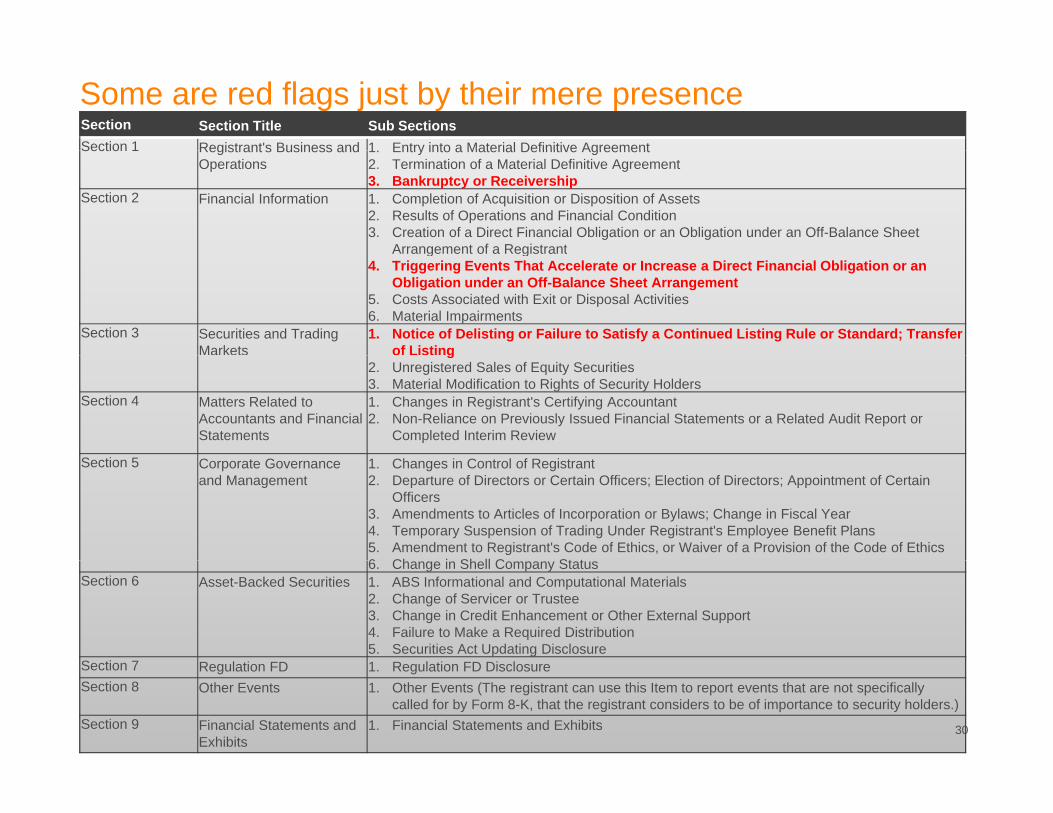

There are many sections (types) of 8-KsSection Section Title Sub SectionsSection 1 Registrant's Business and 1 Entry into a Material Definitive AgreementSection 1 Registrant s Business and

Operations1. Entry into a Material Definitive Agreement2. Termination of a Material Definitive Agreement3. Bankruptcy or Receivership

Section 2 Financial Information 1. Completion of Acquisition or Disposition of Assets2. Results of Operations and Financial Condition3. Creation of a Direct Financial Obligation or an Obligation under an Off-Balance Sheet

Arrangement of a Registrant

1. Notice of Delisting or Failure to Satisfy a Continued Listing Rule or Standard;

Arrangement of a Registrant4. Triggering Events That Accelerate or Increase a Direct Financial Obligation or an Obligation

under an Off-Balance Sheet Arrangement5. Costs Associated with Exit or Disposal Activities6. Material Impairments

Section 3 Securities and Trading Markets

1. Notice of Delisting or Failure to Satisfy a Continued Listing Rule or Standard; Transfer of Listing

Transfer of Listing g

2. Unregistered Sales of Equity Securities3. Material Modification to Rights of Security Holders

Section 4 Matters Related to Accountants and Financial Statements

1. Changes in Registrant's Certifying Accountant2. Non-Reliance on Previously Issued Financial Statements or a Related Audit Report or

Completed Interim Review

S ti 5Section 5 Corporate Governance and Management

1. Changes in Control of Registrant2. Departure of Directors or Certain Officers; Election of Directors; Appointment of Certain

Officers3. Amendments to Articles of Incorporation or Bylaws; Change in Fiscal Year4. Temporary Suspension of Trading Under Registrant's Employee Benefit Plans5. Amendment to Registrant's Code of Ethics, or Waiver of a Provision of the Code of Ethics6 Ch i Sh ll C St t6. Change in Shell Company Status

Section 6 Asset-Backed Securities 1. ABS Informational and Computational Materials2. Change of Servicer or Trustee3. Change in Credit Enhancement or Other External Support4. Failure to Make a Required Distribution5. Securities Act Updating Disclosure

Section 7 R l ti FD 1 R l ti FD Di lSection 7 Regulation FD 1. Regulation FD DisclosureSection 8 Other Events 1. Other Events (The registrant can use this Item to report events that are not specifically

called for by Form 8-K, that the registrant considers to be of importance to security holders.)Section 9 Financial Statements and

Exhibits1. Financial Statements and Exhibits 27

Some are red flags just by their mere presenceSection Section Title Sub SectionsSection 1 Registrant's Business and 1 Entry into a Material Definitive AgreementSection 1 Registrant s Business and

Operations1. Entry into a Material Definitive Agreement2. Termination of a Material Definitive Agreement3. Bankruptcy or Receivership

Section 2 Financial Information 1. Completion of Acquisition or Disposition of Assets2. Results of Operations and Financial Condition3. Creation of a Direct Financial Obligation or an Obligation under an Off-Balance Sheet

Arrangement of a Registrant

1. Notice of Delisting or Failure to Satisfy a Continued Listing Rule or Standard;

Arrangement of a Registrant4. Triggering Events That Accelerate or Increase a Direct Financial Obligation or an Obligation

under an Off-Balance Sheet Arrangement5. Costs Associated with Exit or Disposal Activities6. Material Impairments

Section 3 Securities and Trading Markets

1. Notice of Delisting or Failure to Satisfy a Continued Listing Rule or Standard; Transfer of Listing

Transfer of Listing g

2. Unregistered Sales of Equity Securities3. Material Modification to Rights of Security Holders

Section 4 Matters Related to Accountants and Financial Statements

1. Changes in Registrant's Certifying Accountant2. Non-Reliance on Previously Issued Financial Statements or a Related Audit Report or

Completed Interim Review

S ti 5Section 5 Corporate Governance and Management

1. Changes in Control of Registrant2. Departure of Directors or Certain Officers; Election of Directors; Appointment of Certain

Officers3. Amendments to Articles of Incorporation or Bylaws; Change in Fiscal Year4. Temporary Suspension of Trading Under Registrant's Employee Benefit Plans5. Amendment to Registrant's Code of Ethics, or Waiver of a Provision of the Code of Ethics6 Ch i Sh ll C St t6. Change in Shell Company Status

Section 6 Asset-Backed Securities 1. ABS Informational and Computational Materials2. Change of Servicer or Trustee3. Change in Credit Enhancement or Other External Support4. Failure to Make a Required Distribution5. Securities Act Updating Disclosure

Section 7 R l ti FD 1 R l ti FD Di lSection 7 Regulation FD 1. Regulation FD DisclosureSection 8 Other Events 1. Other Events (The registrant can use this Item to report events that are not specifically

called for by Form 8-K, that the registrant considers to be of importance to security holders.)Section 9 Financial Statements and

Exhibits1. Financial Statements and Exhibits 28

Some are red flags just by their mere presenceSection Section Title Sub SectionsSection 1 Registrant's Business and 1 Entry into a Material Definitive AgreementSection 1 Registrant s Business and

Operations1. Entry into a Material Definitive Agreement2. Termination of a Material Definitive Agreement3. Bankruptcy or Receivership

Section 2 Financial Information 1. Completion of Acquisition or Disposition of Assets2. Results of Operations and Financial Condition3. Creation of a Direct Financial Obligation or an Obligation under an Off-Balance Sheet

Arrangement of a Registrant

1. Notice of Delisting or Failure to Satisfy a Continued Listing Rule or Standard;

Arrangement of a Registrant4. Triggering Events That Accelerate or Increase a Direct Financial Obligation or an

Obligation under an Off-Balance Sheet Arrangement5. Costs Associated with Exit or Disposal Activities6. Material Impairments

Section 3 Securities and Trading Markets

1. Notice of Delisting or Failure to Satisfy a Continued Listing Rule or Standard; Transfer of Listing

Transfer of Listing g

2. Unregistered Sales of Equity Securities3. Material Modification to Rights of Security Holders

Section 4 Matters Related to Accountants and Financial Statements

1. Changes in Registrant's Certifying Accountant2. Non-Reliance on Previously Issued Financial Statements or a Related Audit Report or

Completed Interim Review

S ti 5Section 5 Corporate Governance and Management

1. Changes in Control of Registrant2. Departure of Directors or Certain Officers; Election of Directors; Appointment of Certain

Officers3. Amendments to Articles of Incorporation or Bylaws; Change in Fiscal Year4. Temporary Suspension of Trading Under Registrant's Employee Benefit Plans5. Amendment to Registrant's Code of Ethics, or Waiver of a Provision of the Code of Ethics6 Ch i Sh ll C St t6. Change in Shell Company Status

Section 6 Asset-Backed Securities 1. ABS Informational and Computational Materials2. Change of Servicer or Trustee3. Change in Credit Enhancement or Other External Support4. Failure to Make a Required Distribution5. Securities Act Updating Disclosure

Section 7 R l ti FD 1 R l ti FD Di lSection 7 Regulation FD 1. Regulation FD DisclosureSection 8 Other Events 1. Other Events (The registrant can use this Item to report events that are not specifically

called for by Form 8-K, that the registrant considers to be of importance to security holders.)Section 9 Financial Statements and

Exhibits1. Financial Statements and Exhibits 29

Some are red flags just by their mere presenceSection Section Title Sub SectionsSection 1 Registrant's Business and 1 Entry into a Material Definitive AgreementSection 1 Registrant s Business and

Operations1. Entry into a Material Definitive Agreement2. Termination of a Material Definitive Agreement3. Bankruptcy or Receivership

Section 2 Financial Information 1. Completion of Acquisition or Disposition of Assets2. Results of Operations and Financial Condition3. Creation of a Direct Financial Obligation or an Obligation under an Off-Balance Sheet

Arrangement of a Registrant

1. Notice of Delisting or Failure to Satisfy a Continued Listing Rule or Standard;

Arrangement of a Registrant4. Triggering Events That Accelerate or Increase a Direct Financial Obligation or an

Obligation under an Off-Balance Sheet Arrangement5. Costs Associated with Exit or Disposal Activities6. Material Impairments

Section 3 Securities and Trading Markets

1. Notice of Delisting or Failure to Satisfy a Continued Listing Rule or Standard; Transfer of Listing

Transfer of Listing g

2. Unregistered Sales of Equity Securities3. Material Modification to Rights of Security Holders

Section 4 Matters Related to Accountants and Financial Statements

1. Changes in Registrant's Certifying Accountant2. Non-Reliance on Previously Issued Financial Statements or a Related Audit Report or

Completed Interim Review

S ti 5Section 5 Corporate Governance and Management

1. Changes in Control of Registrant2. Departure of Directors or Certain Officers; Election of Directors; Appointment of Certain

Officers3. Amendments to Articles of Incorporation or Bylaws; Change in Fiscal Year4. Temporary Suspension of Trading Under Registrant's Employee Benefit Plans5. Amendment to Registrant's Code of Ethics, or Waiver of a Provision of the Code of Ethics6 Ch i Sh ll C St t6. Change in Shell Company Status

Section 6 Asset-Backed Securities 1. ABS Informational and Computational Materials2. Change of Servicer or Trustee3. Change in Credit Enhancement or Other External Support4. Failure to Make a Required Distribution5. Securities Act Updating Disclosure

Section 7 R l ti FD 1 R l ti FD Di lSection 7 Regulation FD 1. Regulation FD DisclosureSection 8 Other Events 1. Other Events (The registrant can use this Item to report events that are not specifically

called for by Form 8-K, that the registrant considers to be of importance to security holders.)Section 9 Financial Statements and

Exhibits1. Financial Statements and Exhibits 30

Some are red flags just by their mere presenceSection Section Title Sub SectionsSection 1 Registrant's Business and 1 Entry into a Material Definitive AgreementSection 1 Registrant s Business and

Operations1. Entry into a Material Definitive Agreement2. Termination of a Material Definitive Agreement3. Bankruptcy or Receivership

Section 2 Financial Information 1. Completion of Acquisition or Disposition of Assets2. Results of Operations and Financial Condition3. Creation of a Direct Financial Obligation or an Obligation under an Off-Balance Sheet

Arrangement of a Registrant

1. Notice of Delisting or Failure to Satisfy a Continued Listing Rule or Standard;

Arrangement of a Registrant4. Triggering Events That Accelerate or Increase a Direct Financial Obligation or an

Obligation under an Off-Balance Sheet Arrangement5. Costs Associated with Exit or Disposal Activities6. Material Impairments

Section 3 Securities and Trading Markets

1. Notice of Delisting or Failure to Satisfy a Continued Listing Rule or Standard; Transfer of Listing

Transfer of Listing g

2. Unregistered Sales of Equity Securities3. Material Modification to Rights of Security Holders

Section 4 Matters Related to Accountants and Financial Statements

1. Changes in Registrant's Certifying Accountant2. Non-Reliance on Previously Issued Financial Statements or a Related Audit Report or

Completed Interim Review

S ti 5Section 5 Corporate Governance and Management

1. Changes in Control of Registrant2. Departure of Directors or Certain Officers; Election of Directors; Appointment of

Certain Officers3. Amendments to Articles of Incorporation or Bylaws; Change in Fiscal Year4. Temporary Suspension of Trading Under Registrant's Employee Benefit Plans5. Amendment to Registrant's Code of Ethics, or Waiver of a Provision of the Code of Ethics6 Ch i Sh ll C St t6. Change in Shell Company Status

Section 6 Asset-Backed Securities 1. ABS Informational and Computational Materials2. Change of Servicer or Trustee3. Change in Credit Enhancement or Other External Support4. Failure to Make a Required Distribution5. Securities Act Updating Disclosure

Section 7 R l ti FD 1 R l ti FD Di lSection 7 Regulation FD 1. Regulation FD DisclosureSection 8 Other Events 1. Other Events (The registrant can use this Item to report events that are not specifically

called for by Form 8-K, that the registrant considers to be of importance to security holders.)Section 9 Financial Statements and

Exhibits1. Financial Statements and Exhibits 31

Extensive news coverage in Developed Europe

0 50 100 150 200 250 300 350 400

# of Securities per Month

0 50 100 150 200 250 300 350 400

NorwayFrance

GermanyUnited Kingdom

NetherlandsSpain

SwedenItaly

Switzerland

GreeceDenmarkBelgiumFinlandAustria

0 2 000 4 000 6 000 8 000 10 000 12 000 14 000 16 000 18 000

LuxembourgIcelandIreland

Portugal

0 2,000 4,000 6,000 8,000 10,000 12,000 14,000 16,000 18,000

# of Articles per Month

32

Combining signals from multiple textual sources g g pproduces a stronger credit model

1

Performance increases when using multiple sources of textual data

0.6

0.8

y Ratio

0.2

0.4

Accuracy

0

Statements News Transcripts All 3 Sources

33

*Performance may change as model is finalized

$24

Comparison of Agency Rating and TR Model Componentsfor Chesapeake Corp

AAA

Text mining can raise red flags early on8/17/2007 – Transcript

A l t I t k it ' till i

$18

$21

investment grade threshold

Agency Rating

TR Merton Model Equivalent Rating

TR Text Model Equivalent Rating

S k P i

AA

A

Analyst: I take it you're still in compliance with all of your covenants there. And have you spoken to any of your creditors about refinancing any of the credit terms?

$12

$15

ck Price

Stock Price

BBB

BB

credit terms?

11/30/2007 - Transcript

CEO: There is a reasonable ibilit th t ill t

$6

$9 Stoc

B

CCC

possibility that we will not be able to comply with these covenants …

08/31/2008 – 10-Q

$0

$3

/ / / / / / / / /

CC

C

Based on current projections we are likely to not be in compliance with the financial covenants under the Credit required…. These matters raise

1/07 4/07 7/07 10/07 1/08 4/08 7/08 10/08 1/09

34

qsubstantial doubt about our ability to continue as a going concern

AGENDA

• CREDIT RISK MODEL– STRUCTURAL MODEL (MERTON APPROACH)– RATIO ANALYSIS

MINING TEXT DOCUMENTS– MINING TEXT DOCUMENTS– ESTIMATING LOSS GIVEN DEFAULT– CDS MARKET– COMBINATION RESULTS

• Q & A

Loss Given Default (LGD) is a common parameter inLoss Given Default (LGD) is a common parameter in risk models• Definition:

LGD = 1 – recovery rate= 1 – post-default price/redemption price

(where the post-default price refers to the price quoted one th ft th d f lt t d d ti imonth after the default event, and redemption price

normally takes value as $100)

• Usage in Modeling Credit Risk:

Expected loss = exposure * default probability * LGD

36

StarMine LGD: Incorporates high-level macro data to specific bond-level data

Macro-level: Treasury yields and spreads, VIXMacro level: Treasury yields and spreads, VIX

Industry-level: Industry Aggregate PDPD

Company-level: SmartRatiosSmartRatiosComponents

Bond-level: seniority & capital

structurestructure

StarMine Loss Given Default 37

AGENDA

• CREDIT RISK MODEL– STRUCTURAL MODEL (MERTON APPROACH)– RATIO ANALYSIS

MINING TEXT DOCUMENTS– MINING TEXT DOCUMENTS– ESTIMATING LOSS GIVEN DEFAULT– CDS MARKET– COMBINATION RESULTS

• Q & A

CDS Model: Analyze the CDS market’s view of dit i kcredit risk

• Reduced form modeling approach which uses all daily pricing data to derive a PD curvederive a PD curve

• Create CDS market-implied values, compare with StarMine forecasts.– Input: StarMine PD + StarMine LGD

Output: StarMine fair value CDS– Output: StarMine fair value CDS– Input: observed CDS price + StarMine LGD (or ISDA LGD)– Output: CDS market-implied PD

P d t t t f PD• Produce term structure of PD– Group similar companies, fit hazard rate function to their CDS, apply same

shape to like companies w/o CDS

39

The CDS market is often more responsiveExample: Goldman Sachs

Comparison of StarMine CDS‐implied PD and Structural model PD

200

240

10%

12%

120

160

6%

8%

k Price

y of D

efau

lt

804%

Stock

Prob

ability

0

40

0%

2%

2/08 4/08 6/08 8/08 10/08 12/08 2/09 4/09 6/09

40

/ / / / / / / / /

CDS implied PD Structural model PD Stock Price

AGENDA

• CREDIT RISK MODEL– STRUCTURAL MODEL (MERTON APPROACH)– RATIO ANALYSIS

MINING TEXT DOCUMENTS– MINING TEXT DOCUMENTS– ESTIMATING LOSS GIVEN DEFAULT– CDS MARKET– COMBINATION RESULTS

• Q & A

Incorporating information from multiple data sources adds considerable value

Power of Combining Financial Ratio, Equity Price (Merton), & Text DataHIT Rate: % Failures Predicted among High Risk (bottom 20%) Firms

95%

100%

cted

g g ( )

25% improvement

30% improvementin MISS Rate

85%

90%

of Failures Pred

icHigh Risk Firm

s

49% improvementin MISS Rate

in MISS Rate

75%

80%

HIT Rate: %

oam

ong H

70%

Text model Financial Ratio model

Merton model Financial Ratio + Merton + Text

42

What did we learn about credit default prediction?• It is possible to systematically predict credit events more accurately than credit agencies Altman Z- or Ohlson O-scores (and many creditthan credit agencies, Altman Z- or Ohlson O-scores (and many credit analysts). We learned...

– Incorporating information from multiple perspectives improves upon any single source of data or type of analysisany single source of data or type of analysis

– You can often be more responsive by incorporating market intelligence embedded in CDS and stock prices

Incorporating textual analytics from several sources can flag– Incorporating textual analytics from several sources can flag problems before they show up in the numbers. And, text is underused from a quant perspective

– There is great value in using more forward-looking timely– There is great value in using more forward-looking, timely information

– Used to filter out the most risky stocks, it also adds value to equity portfoliosportfolios

43

Thank You! Q&A

• For a copy of this presentation, please drop off your business

card or visit www.starmine.com/cfaevent

• To request access to our white papers, visit:

www starmine com/whitepaperswww.starmine.com/whitepapers

44