a practical guide 2015 england & wales charities · pdf filea practical guide 2015 england...

TRANSCRIPT

A Practical Guide 2015

England & WalesCharities

Contents

Introduction to UK200Charities & Education Group

Map of UK200Charities & Education Group members and useful contacts

Charity Governance and Conflicts of Interest

Public Benefit

Charities and Risk Management

Charity Accounting and Financial Reporting

Charity Accounting and Financial Reporting – SORP 2015

Charity Tax

Charitable Incorporated Organisations

Charities and Financial Investment

2

3

4 – 8

9

10 – 15

16 – 19

20 - 29

30 – 34

35

36 – 39

Introduction to UK200Group Charites & Education Group

About the guide

It is becoming increasingly challenging forcharities to keep up to date with the rulesand regulations governing the sector.Changes to the Charities Act andCompanies Act have resulted in a tightercompliance and governance framework,with the drive for greater transparency inoperation and reporting an underlyingtheme.

Further, the Charity Commission isfocussing more on its regulatory role andthis is set against the near halving of itsbudget.

The taxes and VAT regimes are underconstant review, with frequent changesmade to the underlying rules, exemptionsand thresholds. Whilst the introduction ofthe new Charities SORP 2015 (FRS 102),introduces the most significant change toaccounting and financial reporting for thesector in a decade.

The aim of this guide is to summarise the key changes and impact of the newSORP (“Statement of RecommendedPractice”) and to provide an overview ofsome of the key principles impactingcharity taxation and VAT. In addition, theguide reaffirms best practice in charityRisk Management and reviews latestguidance in respect of Conflicts ofInterest, Public Benefit and InvestmentManagement.

Introduction to UK200Group

The UK200Group is a nationwideassociation of independent CharteredAccountants and Lawyers, providingaccess to specialist expertise and crossfertilisation of ideas and experienceacross a wide range of specialist areas.The principle objective of the Group is toprovide the benefits of strength in depthin specialist and technical areas normallyavailable only to the national firms.The UK200Group has a strong Charitiesand Education Group which providestraining and guidance to its members inthe form of seminars, newsletters andtechnical releases. Members are charityspecialists who offer a broad range ofsupport including:

Audit and Accounting

As well as statutory audit, internal auditand year end statutory accountspreparation, we provide guidance andadvice to ensure compliance withregulatory requirements and best practice.

Business and Strategic Planning

Effective strategic planning isfundamental to all organisations.Heightened funding and “commercial”challenges along with the drive towardsgreater transparency, with theintroduction of the requirements of thenew SORP and the Charities Act 2011,have made this particularly pertinent forcharities. Charities are also required topublicly report their strategic goals andobjectives, and their achievementstowards meeting these. We are able toassist organisations in preparing theirplans through facilitated discussion andthe provision of tailored documentation.

Management Accounting and Reporting

Timely and accurate managementaccounting information is essential to theongoing management of any charity. Weare able to support charities by eitherhelping to embed the skills and processesneeded internally or by providing morehands-on assistance with the setting ofKPI’s, budgets and cash flow forecastsand the preparation of monthly orquarterly management information.

Risk Management, Governance andGeneral Compliance

Risk management is a key factor ingovernance and integral to the managementof charities. Our support includes assistingclients with the identification, documentationand on-going review of risk, and compliancewith best practice in governance.

This handbook has been prepared for general interest and it is important to obtain professional advice on specificissues. We believe the information contained in it to be correct. While all possible care is taken in the preparation ofthis handbook, no responsibility for loss occasioned by any person acting or refraining from acting as a result of thematerial contained herein can be accepted by the UK200Group, or its member firms or the authors.

UK200Group is an association of separate and independently owned and managed chartered accountancy andlawyer firms. UK200Group does not provide client services and it does not accept responsibility or liability for theacts or omissions of its members. Likewise, the members of UK200Group are separate and independent legalentities, and as such each has no responsibility or liability for the acts or omissions of other members.

Version 1 – August 2015

2 UK200Group England & Wales Charities 2015

Taxation and VAT

We provide a full range of VAT andtaxation advice. Whilst the area oftaxation is becoming increasinglycomplex, a great many charities are ableto take advantage of exemptions frommost forms of income and capital taxes,but need to ensure that the appropriateconditions are met.

This guide is not intended as a definitiveguide to all aspects of charity accounting,taxation, law or best practice incompliance. Whilst, the guide highlightssome of the key areas requiringconsideration, appropriate professionaladvice should be taken by Trustees as thecircumstances warrant.

Chairman – Andy MalpassUK200Charities & Education GroupPartner at Whittingham Riddell LLP

Andy heads up the Charities andEducation group at Whittingham RiddellLLP and is Chair of the UK200GroupCharities and Education Committee. Heworks with a broad range of charities andeducational organisation, includingAcademies and Independent Schools.Andy has extensive experience of auditand internal audit compliance andprovides advice on governance and riskmanagement, financial planning,budgeting and strategy. He is often calledupon to speak at local and national charityconferences and seminars and regularlywrites for the professional press.

Andy joined Whittingham Riddell LLPfrom Pricewaterhouse Coopers where hespent 13 years working in both the UK andAustralia.

UK200Group Charities & Education Group members

UK200Group England & Wales Charities 2015 3

UK200Charities & Education Group3 Wesley HallQueens RoadAldershotHants GU11 3NPTel: 01252 401050 or 01252 [email protected]

Useful Contacts

The following organisations are usefulpoints of contact for readers wishing toobtain information or clarification onissues covered in this report, either at thedate of publication or in the future.

Charity Commission for England & WalesPO Box 1227Liverpool L69 3UGwww.charitycommission.gov.uk

HM Revenue & CustomsPO Box 205Bootle L69 9AZGeneral enquiries 0300 123 1073www.gov.uk

Office of Scottish Charity Regulator(OSCR)9 Riverside DriveDundee DD1 4NYGeneral enquiries 01382 220446www.oscr.org.uk

Office of the Third Sector2nd FloorAdmiralty ArchSouth SideThe MallLondon SW1A 2WHTel: 020 7276 1234www.thirdsector.co.uk

Seven Investment Management (7IM)125 Old Broad StreetLondon EC2N 1ARTel: 0203 102 9861www.7im.co.uk

LONDON

BIRMINGHAM M

CARDIFF

NEWCASTLE

STIRLING

SCARBOROUGH

BELFAST

BANBURY

BRIDGEND

CAMBRIDGE

CHELMSFORD

CHELTENHAM

CHICHESTER

COLCHESTER

GODALMING

GRIMSBY

HULL

HUNTINGDON

LEEDS

LETCHWORTHGARDEN CITY

LEWES

MIDDLESBROUGH

SALISBURY

SEAFORD

SHEWSBURY

SOUTHAMPTON

STOCKTON-ON-TEES

STRATFORD-UPON-AVON

SWANSEA WATFORD

WITNEY

UK200Charities & Education Group memberfirms, refer to website www.uk200group.co.ukfor full contact details

Charity Governance & Conflicts of Interest

Governance

There is an abundance of guidanceavailable to trustees issued by the CharityCommission and others providing detailsof the numerous responsibilities oftrustees in relation to governance. Twokey pieces of guidance and reporting areconsidered below.

Published in July 2008; The Hallmarks ofan effective charity is still best practicewith regards to governance. It sets outthe standards which help trustees toimprove the effectiveness of their charity,and the principles that the CharityCommission’s regulatory framework existsto support. The six hallmarks are:

Clear about its purposes and directionAn effective charity is clear about itspurposes, mission and values and usesthem to direct all aspects of its work.

A strong boardAn effective charity is run by a clearlyidentifiable board or trustee body thathas the right balance of skills andexperience, acts in the best interests ofthe charity and its beneficiaries,understands its responsibilities and hassystems in place to exercise them properly.

Fit for purposeThe structure, policies and procedures ofan effective charity enable it to achieve itspurposes and mission and deliver itsservices efficiently.

Learning and improvingAn effective charity is always seeking toimprove its performance and efficiency,and to learn new and better ways ofdelivering its purposes. A charity'sassessment of its performance, and of theimpact and outcomes of its work, willfeed into its planning processes and willinfluence its future direction.

Financially sound and prudentAn effective charity has the financial andother resources needed to deliver itspurposes and mission, and controls anduses them so as to achieve its potential.

Accountable and transparentAn effective charity is accountable to thepublic and others with an interest in the

charity (stakeholders) in a way that istransparent and understandable. There are a number of other codes andstandards of good practice which arereflected in guidance created for manydifferent organisations; e.g. NationalHousing Federation’s publication“Excellence in Governance” and, “GoodGovernance: a Code for the Voluntary andCommunity Sector” which is jointlyowned by NCVO, ACEVO, SCC, ICSA &WCVA and supported by the CharityCommission.

The underlying principle which is integralto these codes and standards is theprinciple of equality and diversity;

Equality is about creating a fairer societywhere everyone can participate and havethe opportunity to fulfil their potential.

Diversity is about respecting, valuing andcelebrating aspects that make us uniqueas individuals – recognising that wecontribute to society because of thoseaspects, not in spite of them. Diversityshould be recognised in all its formsincluding age, gender, faith, race, sexualorientation, disability, experience andthinking.

Impact of poor governance

Each year the Charity Commission issuesits report on investigations andcompliance casework. The 2013-14 report‘Tackling abuse and mismanagement’highlighted the most common types ofabuse and mismanagement as:

> Financial mismanagement and financialcrime

> Concerns about safeguarding> The risk of abuse for terrorist related

purposes> Serious governance failures> Concerns about charities’ independence> Concerns about charities abusing their

charitable status> Concerns about fundraising.

The Commission’s Statement of RegulatoryApproach, published in its annual reportand accounts for 2013-14, emphasisesrobust regulation and prioritises theirwork to promote trustees’ compliancewith charity law. It makes clear that theyare enhancing the rigour with which theyhold charities accountable.

An important part of the Commission’snew approach, is that the Commission isbecoming more proactive in identifyingand acting on concerns about charities.

The Commission has:

> Changed its approach to monitoringcharities that have been told to improvetheir compliance and governance

> Improved its work to follow up onconcerns raised during or shortly afterregistration

> Taken steps to recover lost funds,including, where appropriate, takingrestitution action.

Many of the problems identified by theCommission have their roots in basicgovernance failures. Poor governanceexposes charities to risk, hampers them infurthering their aims, and contributes toan environment in which abuse can becommitted and go unnoticed. No systemof control can guarantee a charity is fullyprotected against serious incidents orwilful criminal exploitation. But byfulfilling their duties and putting solidgovernance controls in place, trustees candramatically reduce the risk of abuse,protect their charity from harm andensure it furthers its purposes in line withits governing document.

At the heart of good governance is sounddecision making. Good decision makingmeans:

> Acting in good faith and exclusively inthe charity’s interests

> Acting within the trustees’ powers> Managing conflicts of interest> Being properly informed> Where relevant, seeking appropriate

advice.

Sometimes, concerns arise in connectionwith transactions and dealings betweenthe charity and a trustee or bodies closelyconnected to a trustee, for example loansbetween the charity and a trustee.Concerns can arise, when, for example,there is no record of the transaction beingproperly discussed by the non-conflictedtrustees, no written agreements, noindependent advice taken or where thetransactions are not reviewed for longperiods of time.

When a problem has arisen, trustees must

4 UK200Group England & Wales Charities 2015

UK200Group England & Wales Charities 2015 5

> Governance

respond appropriately, including reportingthe incident to the Charity Commission.This demonstrates to donors, funders andbeneficiaries that the trustees are notignoring the issues, but protecting theircharity’s interests. It therefore mitigatesthe potential reputational damageassociated with the adverse incident. Iftrustees fail to respond appropriately, thismay be deemed to be mismanagement.

The Commission’s regulatory approach isreflected in the guidance issued to trustees.They have recently consulted on andreissued guidance on conflicts of interest,and also consultated on and revised theCharity Commission’s core guidance ontrusteeship (The essential trustee).

The most significant change proposed to“The essential trustee” is a new explanationof what the Commission expects oftrustees. Commission guidance currentlydistinguishes between legal requirements(what trustees ‘must’ do) and goodpractice (what trustees ‘should’ do). Sometrustees and their advisors have beenunclear whether they need to follow thespecified good practice; some have treatedthis good practice as merely optional.

This was never the Commission’sintention. Many of the examples of goodpractice are applications of wider legalrequirements that trustees must meet.Trustees who don’t follow the specifiedgood practice are at risk of breachingtheir legal duties.

The Commission wants to make it clearerthat it expects trustees to comply withspecified good practice unless they canjustify not doing so (for example bycomplying in a different way). If trusteescan’t justify why they haven’t followedgood practice, the Commission is likely totreat this as misconduct or mismanagement.

It is important that all trustees are familiarwith the guidance available and we wouldconsider the following to be essentialreading.

> Internal financial controls for charities:http://bit.ly/1BQMqVl

> It’s your decision: charity trustees anddecision making: http://url6.org/bDGX

> The essential trustee: what you need toknow: http://url6.org/bDGY

> Conflicts of interest:http://url6.org/bDGZ

> Hallmarks of an effective charity:http://url6.org/bDHa

> Charity Finance Group Charity Fraudguide: http://bit.ly/1AgUNHI

> Fraud and financial crime:http://url6.org/bDHc

Further reading designed to providesupport to trustees in particular areas,includes:

> Protecting vulnerable groups includingchildren: http://url6.org/bDHd

> Safeguarding children:http://url6.org/bDHe

> Charities and terrorism:http://url6.org/bDHf

> Protecting charities from abuse forextremist purposes:http://url6.org/bDHg

> Due diligence monitoring and end useof funds: http://bit.ly/1Ph7lmA

> Holding moving and receiving fundssafely: http://url6.org/bDHi

> Managing charity assets and resources:http://url6.org/bDHj

> Reporting serious incidents - guidancefor trustees: http://bit.ly/1wKG828

> Speaking out: campaigning andpolitical activity by charities:http://bit.ly/1z2keJQ

> Charities, elections and referendums:http://url6.org/bDHl

> Electoral Commission guidance onCharities and Campaigning:http://bit.ly/1oWLlQQ

Report produced by:Sue Foster and Mark Filsell, Knill James

Sue heads the Charities and Educationteam at Knill James, and is on theUK200Group Charities and EducationCommittee. Sue and Mark act for anumber of charities and not-for-profitorganisations together with independentschools and academies providing auditand assurance services and advising ongovernance issues, risk management andinternal control procedures.

Sue and Mark speak at charity, educationaland academy seminars providing trusteeswith updates on technical and governanceissues.

Conflicts of Interest

As the independent regulator for charitiesin England and Wales, it is the job of theCharity Commission to ensure thattrustees comply with the followingresponsibilities:

> Act in the interests of the charity> Operate in a manner consistent with the

charity’s purpose> Act with due care and diligence> Ensure that the charity complies with

relevant legislation.

As such, they have issued guidance toensure that trustees do not putthemselves in any position where theirduties as a trustee may conflict with anypersonal interest they may have. Thefollowing is a summary of theCommission’s guide for charity trustees inrespect of ‘Conflicts of Interest’.

What is a conflict of interest?

A conflict of interest is any situation inwhich a trustee’s personal interests orloyalties could, or could be seen to,prevent the trustee from making adecision only in the best interests of thecharity; for example, if a trustee (or afamily member or business partner):

> Receive payment from the charity forgoods or services supplied, or as anemployee

> Make a loan to the charity> Own a business that enters into a

contract with the charity> Use the charity’s services> Enter into some other financial

transaction with the charity.

Conflicts of interest are common incharities and having a conflict of interestdoesn’t mean that the trustee has donesomething wrong. However, action needsto be taken to prevent them frominterfering with the trustee’s ability tomake a decision only in the best interestsof the charity.

Each charity should:

> Identify conflicts of interest> Prevent any conflict of interest from

affecting a decision> Record any conflict of interest.

Identifying conflicts of interest

Each individual trustee must avoid puttingthemselves in a position where their dutyto act only in the best interests of thecharity could conflict with any personalinterest they may have. Individual trusteesmust identify and declare any conflict ofinterest and the trustee body must ensurethat any conflict of interest does notprevent them from making a decision onlyin the best interests of the charity.

A conflict of interest can relate not only toa trustee’s personal interests but also tothe interests of those connected to them.The list of connected persons is wide andincludes child, parent, grandchild,grandparent, brother or sister and spouseor civil partner.

It is good practice to have a writtenconflicts of interest policy and register ofinterests as these can help individualtrustees and the trustee body to identifyconflicts of interest promptly. The CharityCommission has given guidance as towhat should be included in such a policyand this is included in Table A.

A register of interests should includerelevant business and pecuniary interestsand the Board of Trustees should ensurethat their register of interests is kept up todate through regular review.

The trustee body should considerconflicts of interest prior to appointmentof a trustee. Where prospective trusteesare likely to be subject to serious orfrequent conflicts of interest then thetrustees should consider seriously whetherthat trustee should be appointed.

Conflicts of interest usually arise whereeither:

> There is a potential financial benefitdirectly to a trustee or indirectlythrough a connected person; or

> A trustee’s duty to the charity maycompete with a duty or loyalty theyowe to another organisation or person.

Although declaring conflicts of interest isprimarily the responsibility of the affectedtrustee, the trustee body should havestrong systems in place to ensure trusteesare aware of their duty to declare them.

The Charity Commission expect trusteesto have a standard agenda item at thebeginning of each trustee meeting todeclare any actual or potential conflict ofinterest.

Preventing conflicts of interestfrom affecting decision making

Having identified a conflict of interest,trustees must ensure that any potentialeffect on decision making is eliminated.They would normally do this by:

> Finding an alternative way forwardwhich doesn’t involve the conflict ofinterest

> Take appropriate steps to manage theconflict (see below).

Trustees must follow any legal orgoverning document requirements whichsay how the conflict of interest must behandled.

Trustee benefit – withdraw from decisionmaking

Where there are no legal or governingdocument provisions about managingconflicts of interest, then it is expectedthat a trustee should be absent from anydiscussion that could lead to the trustee’sbenefit. The individual should not voteand should be absent for initialdiscussions, decisions and anysubsequent discussion or decision on theissue.

Conflict of loyalty – withdraw fromdecision making

Where there are no legal or governingdocument provisions and where there is aconflict of loyalty but the trustee does notstand to gain any benefit, then it is up tothe trustees as to the best course ofaction to take. The trustee concerned maybe asked to:

> Withdraw (as above) > Stay in the meeting but not participate> Participate in the discussion.

The trustees should always be able toshow that they have made their decisionin the best interest of the charity.

6 UK200Group England & Wales Charities 2015

> Conflicts of Interest

Record the conflict of interest

It is expected that the charity keeps awritten record within the minutes of anyconflict of interest and how it was dealtwith. This would normally include:

> The nature of the conflict> Which trustee(s) were affected> If any conflicts were declared in

advance> An outline of the discussion> Whether anyone withdrew from the

discussion> How the trustees took the decision in

the best interests of the charity.

It is recommended, and in most cases it isa requirement, that details of paymentsand benefits to charity trustees andpeople connected to them are includedwithin the charity’s annual accounts.

If you get it wrong

Problems in charities are often caused bypoorly managed conflicts of interest andabout 90% of Charity Commissioninvestigations involve a conflict ofinterest. If you fail to identify and dealwith conflicts of interest:

> The trustees’ decision may be invalidand could be open to challenge

> Trustees might have to refund anypayment they received from the charity,even if the charity also benefitted fromthe arrangement

> Trustees might have to make good anyloss the charity suffers

> The Charity Commission will takeregulatory action where it’s necessaryto protect the charity from further harmor to deal with any misconduct ormismanagement by the trustees.

Trustees should be aware of thesignificant negative effects that a badlymanaged conflict of interest can have onthe charity’s reputation and on publictrust and confidence generally. Whendealing with conflicts of interest, trusteesshould be aware of how the situation mayappear to someone from outside thecharity, and make sure that policies andprocedures are in place which will allowtrustees to demonstrate that suchsituations have been dealt with properly.

> Conflicts of Interest

Conflict of Interest Policy - Table A*

As a minimum, a conflicts of interest policy should:

> Define conflicts of interest> Explain that trustees have a personal responsibility to declare conflicts of

interest if they are to fulfil their legal duty to act only in the best interests ofthe charity

> Give an account of what the charity’s governing document says about conflictsof interest

> Define all interests that trustees should declare, including business andpersonal interests and those of their spouse, partner, family and close relatives

> Define trustee benefits and highlight the requirement to obtain legal authoritybefore any transaction involving trustee benefit is undertaken

> Include guidance on the procedures to follow when a trustee is subject to aconflict of interest, such as: l Recording trustee interests in the charity’s register of interestsl Declaring interests at the beginning of each meetingl Removing the trustee concerned from the decision making processl Recording details of the discussions and decisions made

> Set out how and by whom the policy will be monitored and enforced> Be widely communicated and understood within the charity> Be part of a wider policy framework, for example a trustee handbook.

* is an extract from the Charity Commission Guidance

UK200Group England & Wales Charities 2015 7

8 UK200Group England & Wales Charities 2015

> Conflicts of Interest

Report produced by:David Robertson, Partner with AndersonBarrowcliff LLP

David is a member of the UK200GroupCharity and Education committee andchairs the UK200Group Academiesnational training day. He has over 20years’ experience of auditing and advisingcharities and not-for-profit organisationsand specialises in education; academies,independent schools and Sixth Form andFE colleges. He is an audit committeemember at his local university and afinance advisor for a FE College.

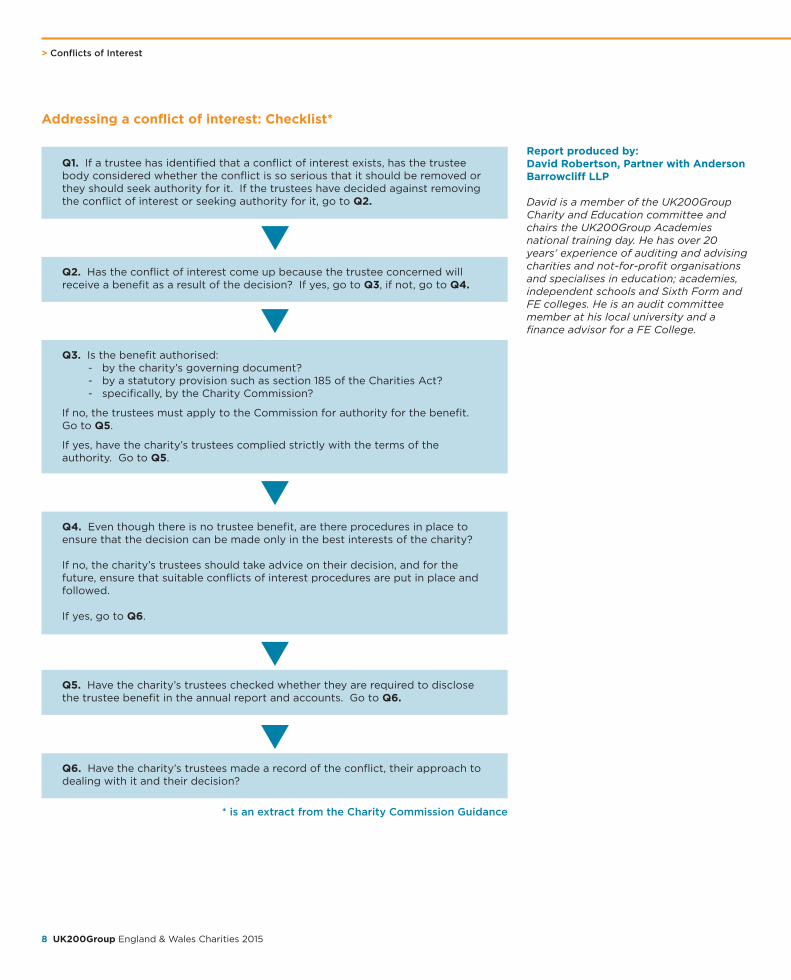

Addressing a conflict of interest: Checklist*

Q1. If a trustee has identified that a conflict of interest exists, has the trusteebody considered whether the conflict is so serious that it should be removed orthey should seek authority for it. If the trustees have decided against removingthe conflict of interest or seeking authority for it, go to Q2.

Q3. Is the benefit authorised:- by the charity’s governing document?- by a statutory provision such as section 185 of the Charities Act?- specifically, by the Charity Commission?

If no, the trustees must apply to the Commission for authority for the benefit.Go to Q5.

If yes, have the charity’s trustees complied strictly with the terms of theauthority. Go to Q5.

Q4. Even though there is no trustee benefit, are there procedures in place toensure that the decision can be made only in the best interests of the charity?

If no, the charity’s trustees should take advice on their decision, and for thefuture, ensure that suitable conflicts of interest procedures are put in place andfollowed.

If yes, go to Q6.

Q2. Has the conflict of interest come up because the trustee concerned willreceive a benefit as a result of the decision? If yes, go to Q3, if not, go to Q4.

Q5. Have the charity’s trustees checked whether they are required to disclosethe trustee benefit in the annual report and accounts. Go to Q6.

Q6. Have the charity’s trustees made a record of the conflict, their approach todealing with it and their decision?

q

q

q

q

q

* is an extract from the Charity Commission Guidance

Public BenefitThe Charities Act 2006 refers to the factthat all charities must provide a publicbenefit and must satisfy the public benefittest. However, the legislation contains nostatutory definition of public benefit.

Whilst there is no statutory guidance onthe public benefit “test”, the CharityCommission was given a new regulatoryobjective – known as the public benefitobjective – which involves promotingawareness and understanding of theoperation of the public benefit requirement.

Revised Guidance was issued at the endof 2013, following a decision of the UpperTribunal in a case involving the IndependentSchools Council as a result of which theGuidance previously issued by the CharityCommission had to be amended andsections of that guidance withdrawn.

The current Public Benefit Guidanceissued by the Charity Commission is splitinto three as follows:

1 The first part explains the legalrequirements that a charity’s purposesmust be for the public benefit

2 The second part explains the meaningof public benefit in the context ofrunning a charity

3 The third part explains the requirementfor a charity trustee to report on howthey have carried out the charity’spurposes for the public benefit.

The three part Guidance does not laydown the law but rather explains how thelaw is interpreted and applied by theCommission. Individual decisions arebased on the facts of a given case.Charity trustees must be aware of theCommission’s Public Benefit Guidanceand have taken it into account, where it isrelevant, and only depart from it wherethey have good reason. Taking each partof the revised current Guidance in turn:

1 What Public Benefit Means

Charities have to have charitablepurposes only:

i) These are set out in the descriptions inthe Charities Act 2006; and

ii) A charitable purpose must be for thepublic benefit. This is split into two:

a) The “benefit aspect” whichmeans that the purpose must be

beneficial and any detriment must notoutweigh the benefit. If it is not clearthat a purpose is beneficial theCommission may ask for evidence

b) The “public aspect” by which itmust benefit the public in general or asufficient section of it. Whether asufficient section of the public benefitmay depend on the specific purposeand in some cases people living in aspecific geographical area will besufficient. It is also possible to decidewho can benefit by reference to“protected characteristics” such asage, disability or religion. TheCommission will decide whether asection of the public is “sufficient” ona case by case basis and there aredifferent rules for poverty charitieswhich may not require the “public”aspect of the test to be satisfied.

Further, any personal benefits receivedshould be no more than “incidental” tocarrying out a charity’s purpose.

2 What Public Benefit Means in theContext of Running a Charity

Charity trustees have a duty to carry out acharity’s purposes for the public benefit.That the charity’s purposes are beneficialshould be understood by the trustees andthe purposes should be carried out so asto benefit the public in that way.

In doing this:

i) The risk of harm should be identifiedand minimised; and any harm whicharises should be a minor consequenceof carrying out the purpose

ii) Trustees should know who canproperly benefit and give properconsideration to the full range of waysin which the charity’s purposes can becarried out. This includes havingproper reasons for so doing, notexcluding the poor and making surethat the decision is within the rangethat trustees could make. There arespecial considerations for membershipcharities and for charges for serviceswhere charges should generally beaffordable to people of modest meansand the level of provision for the poor“must be more than minimal or token”.

There are also special considerations with

regard to physical access to a charity’sfacilities and whether these can berestricted.

3 The Requirement to Report

This sets out the duty that charitytrustees must report on how they havecarried out the charity’s purposes for thepublic benefit. This must be reported inthe trustees’ annual report and there aredifferent rules for “smaller” charities thanfor “larger” charities.

For smaller charities, charity trusteesmust include a brief summary of the mainactivities undertaken by the charity tocarry out its charitable purposes for thepublic benefit and a statement as towhether they have had regard to theCommission’s Guidance when exercisingany powers or duties to which it is relevant.

For larger charities there are moredetailed requirements.

This third requirement means that thepublic benefit requirement is reported byreference to the charity’s purposes and itis for the trustees to demonstrate that therequirements have been fulfilled.

Recently the Charity Commission haspublished its letter to the IndependentSchools Council stating its position onissues relating to the public benefit ofindependent schools. The Commissionmakes it clear that it does not favour anew statutory duty for independent schoolsbut rather that it is considering its Guidanceand the inclusion of more examples ofreporting on sharing sports, arts or musicfacilities so that charitable schools areencouraged to consider what they aredoing and how they report in this area. Itis understood that this revised guidancewill be published and promoted to charitableschools. This emphasises the approach ofthe Commission that trustees are free tomake decisions about how they carry outtheir legal duties in a way which isappropriate for the individual circumstancesof their charity, and that the Commissiondoes not wish to be prescriptive.

Report produced by:Mark Lewis – Lodders Solicitors LLPBio on page 35

UK200Group England & Wales Charities 2015 9

10 UK200Group England & Wales Charities 2015

Charities and Risk Management

The management of risk forms a key partof the day to day operation of a charityand is fundamental to the wider strategicconsiderations of the Board of Trustees.The formal consideration of and reportingof risk by charities, is not only consistentwith good governance and good practicebut, is also a legal requirement for thosecharities which require an audit.

The risks which charities face will varyaccording to their size, nature and thecomplexity of their activities andoperations, whilst the finances of a charitywill also have a significant bearing on riskin the wider sense. The larger and morediverse the operations of a charity, themore difficult the identification, recordingand management of risk becomes.Accordingly, the risk managementprocesses will need to be tailored to thespecific circumstances of each individualcharity. This guidance considers:

> The Basics of Risk Management> Legal Reporting Requirements> Types of Risk> Identifying and Managing Risk> Recording Risk Assessment – example

risk registers.

The Basics of Risk Management

Identifying and managing risk is essentialto the trustees achieving their keyobjectives and sustaining the charity’sfinancial wellbeing and safeguarding itsunderlying assets. By managing riskeffectively, trustees can help ensure that:

> Significant risks are known andmonitored, allowing trustees andmanagement to make informeddecisions

> Opportunities can be explored anddeveloped on an informed basis

> Strategic planning can be enhancedand improved as broader consequencesare considered and evaluated.

Legal Reporting Requirements

The ultimate responsibility for themanagement and control of a charity sitswith the trustees and their involvement inthe risk management process is essential.Whilst, aspects of the risk managementprocess will be delegated within most, ifnot all charities, trustees should consider

and review the key aspects of the riskmanagement process on an ongoing basisand formally minute their considerationsat least annually.

Charities that are required by law to havetheir accounts audited must make a riskmanagement statement in their trustees’annual report confirming that: “thecharity trustees have given considerationto the major risks to which the charity isexposed and satisfied themselves thatsystems or procedures are established inorder to manage those risks”.

Smaller charities which fall below the auditthreshold, whilst not required to make arisk management statement in theirTrustees’ Annual Report, are encouragedto do so as a matter of best practice.

Business Review

Incorporated charities, other than smallcompanies as defined by company law,must also include a business review intheir annual directors’ (i.e. Trustees’)report for accounting periodscommencing on or after 1 January 2016.To be a small company at least 2 of thefollowing conditions must be met:

> Annual income must be £10.2m or less(previously £6.5m or less)

> Total assets on the balance sheet mustbe £5.1m or less (previously £3.26m orless)

> The average number of employees mustbe 50 or fewer.

The business review must contain adescription of the principal risks anduncertainties facing the charitable company.

Purpose

The purpose of the risk managementstatement is to give the readers of theannual trustees report an insight into:

> How the charity approaches themanagement of risk

> An understanding of the major risks towhich the charity is exposed

> Proposals for further developments inthe management of risk.

Form and content

The form and content of the risk

management statement will reflect thesize and complexity of the charity but as aminimum should include:

> An acknowledgement of the trustees’responsibility

> An overview of the risk identificationprocess

> An indication that the major risksidentified have been reviewed andassessed

> Confirmation that control systems havebeen established to manage those risks.

The level of involvement by trusteesshould be sufficient for them to be able tomake the required risk managementstatement with reasonable confidence.

Detailed approach to reporting

Larger charities and those with morecomplex activities may, as a matter ofbest practice, wish to adopt a moredetailed approach to reporting in theannual report. The Charity Commissionguidance on the structure and principleswhich those adopting a more expansiveapproach to reporting should consider isas follows:

> A description of the major risks faced> The links between the identification of

major risks and the operational andstrategic objectives of the charity

> Procedures that extend beyond thefinancial risk to encompass operational,compliance and other categories ofidentifiable risk

> The link between risk assessment andevaluation to the likelihood of itsoccurrence and impact should theevent occur

> A description of the risk assessmentprocesses and monitoring that areembedded in management andoperational processes

> Trustees’ review of the principal resultsof risk identification processes and howthey are evaluated and monitored.

Types of Risk

All charities face a level of risk both interms of their day to day operation and inthe wider sense of their existence. Majorrisks are those risks that would have amajor impact on the charity and aprobable or highly probable likelihood ofoccurring.

UK200Group England & Wales Charities 2015 11

> Charities and Risk Management

There are many examples of riskclassification which charities can adopt inhelping them to identify the major risks towhich they are exposed. The followingrisks categories provide a guide to thesort of categories that trustees would beexpected to consider:

> Mission/objectivese.g. aims/objectives do not accord withconstitution, activities and futuredevelopments restricted by objects,inappropriate/lack of strategy andforward planning.

> Governance and managemente.g. inappropriate organisationalstructure, difficulty recruiting trustees,poor relationship between trustees andmanagement, conflict of interest,inadequate reporting to trustees.

> Law and regulation (compliance)e.g. failure to operate within objects,objects not considered charitable, adverseCharity Commission visit, penaltiesimposed, breach of statutory requirements(Health and Safety Legislation, CharitiesAct, Companies Act etc.).

> External factorse.g. political change, social anddemographic changes, public perception,adverse publicity, Acts of God.

> Operational factorse.g. poor service quality, competitionand pricing, supplier/customerdependency, contract risk, security ofassets, lack of operational planning andcontrol, lack of written policies andprocedures.

> Human resourcese.g. loss of key members of staff,difficulty in recruitment, poor staffvetting procedures, low staff morale,lack of formal terms and conditionspoor training.

> Environmentale.g. planning applications, contamination.

> Technologye.g. need to invest in new technology,failure of key software/hardware, poorsystems selection, lack of IT disasterrecovery planning, over reliance onsupplier.

> Financiale.g. weak/ineffective financialprocedures and controls, inadequatebudgeting and reporting, lack of capitalexpenditure planning.

> Taxatione.g. breach of trading limits forCorporation Tax and or VAT, poor GiftAid procedures, lack of VAT planning.

> Funds and fundraisinge.g. lack of reserves policy, fundingdeficit, falling income levels, failure tocomply with donor requirements, poorcontrol over fundraising, lack ofinvestment policy.

> Fraude.g. lack of consideration of fraud risk,poor staff education and training,inappropriate response to fraud, poorinternal controls, lack of segregation ofduties.

The categorisation of risk and the specificrisks attributed will vary according to thesize and complexity of the charity andsmaller charities may consider simplifyingtheir risk model by combining some of thecategories.

Identifying and Managing Risk

There are many models/exampleprocesses which trustees’ may adopt infulfilling their obligations. They are allsimilar in that they set out a number ofstages to be considered and trusteesmust select the model which is mostsuited to the particular circumstances oftheir charity. The stages which trustees’must work through should effectivelyaddress the specific requirements of thestatement which they are required tomake annually. These are as follows:

Establish a risk policy

Risk is inherent in all activities and mayarise as a consequence of a positivedecision to do something, or from inaction.Charities will have differing risk profilesaccording to their size, nature and thecomplexity of their activities, andoperations will have different capacities toabsorb or tolerate risk. Not only will acharity need to understand its toleranceto risk but will also need to understand itsoverall risk profile, the balance between

higher and lower risk activities.

These considerations will form the basisof the trustees decision making in respectof the level of risk they are willing toaccept, and from a starting point of whichto undertake the initial risk assessmentand determine the policy in respect ofrisk. The trustees will need tocommunicate the boundaries and limitsset by their policy to ensure that there is aclear understanding through theorganisation of acceptable andunacceptable risks.

Identify the major risks

The identification of risks is best achievedby involving the trustees and members ofmanagement and staff who have adetailed knowledge of the day to dayoperations of the charity. The wider theinput the more comprehensive theassessment is likely to be. Achievingstructured input can be difficult and maybest be achieved by holding a series ofworkshops to gather information andideas. If the charity has subsidiaries orbranches, risk identification must extendto them.

Examples of the general types of risks towhich a charity may be exposed are listedabove, and these can be used as astarting point/checklist. However, it isimportant that the process of riskidentification is specific to the charity andnot simply viewed as a generic exercise.

Assess the impact of identified risks

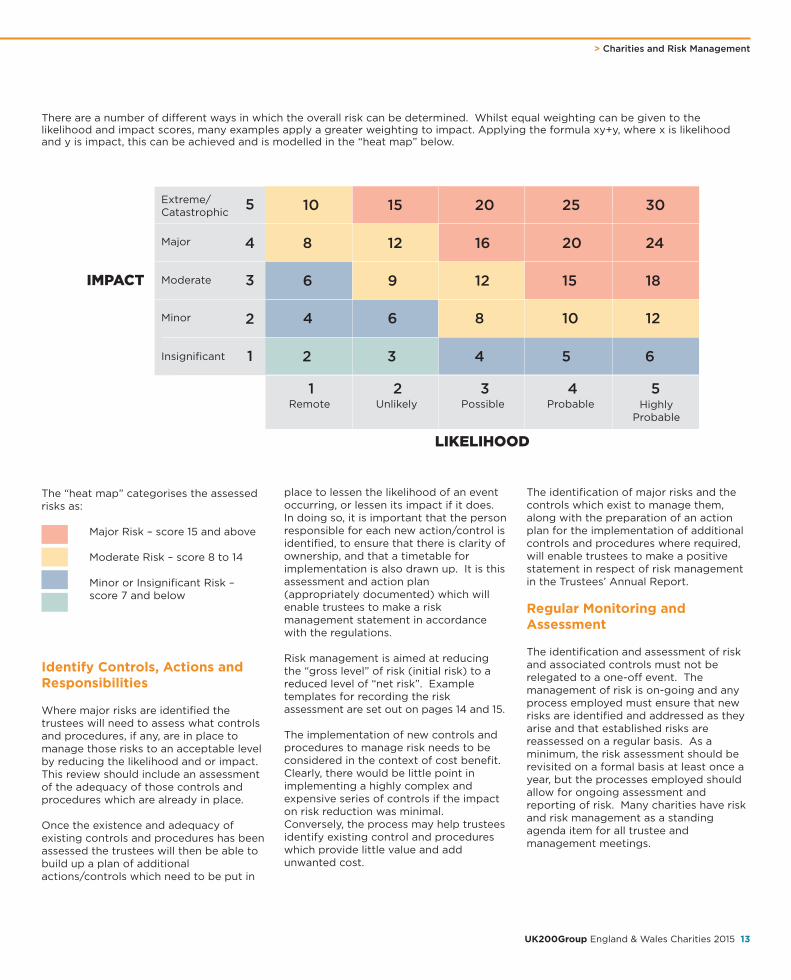

The requirement for trustees to report onrisk management is focussed on “major”risk. Accordingly it is important that oncerisks have been identified they are putinto perspective in respect of their relativeimportance by considering the severity ofimpact and the likelihood of occurrence.There are various models which considerthis. The following scoring matrix onpage 12, which is included in the CharityCommission guidance, is one such modelwhich attempts to give an overall scorefor each risk identified.

12 UK200Group England & Wales Charities 2015

> Charities and Risk Management

IMPACT

Description Score Example

Insignificant 1 l no impact on service/reputationl complaint unlikelyl litigation risk low

Minor 2 l slight impact on service/reputationl complaint possiblel litigation possible

Moderate 3 l some service disruptionl potential adverse publicity – avoidablel complaint probablel litigation probable

Major 4 l service disruptedl adverse publicity not avoidablel complaint probablel litigation probable

Extreme/Catastrophic 5 l service interrupted for significant timel major adverse publicity not avoidablel major litigation expectedl resignation of senior management and boardl loss of beneficiary confidence

LIKELIHOOD

Description Score Example

Remote 1 l may only occur in exceptional circumstances

Unlikely 2 l expected to occur in a few circumstances

Possible 3 l expected to occur in some circumstances

Probable 4 l expected to occur in many circumstances

Highly Probable 5 l expected to occur frequently

The “heat map” categorises the assessedrisks as:

Major Risk – score 15 and above

Moderate Risk – score 8 to 14

Minor or Insignificant Risk – score 7 and below

Identify Controls, Actions andResponsibilities

Where major risks are identified thetrustees will need to assess what controlsand procedures, if any, are in place tomanage those risks to an acceptable levelby reducing the likelihood and or impact.This review should include an assessmentof the adequacy of those controls andprocedures which are already in place.

Once the existence and adequacy ofexisting controls and procedures has beenassessed the trustees will then be able tobuild up a plan of additionalactions/controls which need to be put in

> Charities and Risk Management

There are a number of different ways in which the overall risk can be determined. Whilst equal weighting can be given to thelikelihood and impact scores, many examples apply a greater weighting to impact. Applying the formula xy+y, where x is likelihoodand y is impact, this can be achieved and is modelled in the “heat map” below.

IMPACT

LIKELIHOOD

Extreme/Catastrophic

Remote Unlikely Possible Probable HighlyProbable

Major

Moderate

Minor

Insignificant

10 15 20 25 30

8 12 16 20 24

6 9 12 15 18

4 6 8 10 12

2 3 4 5 6

1 2 3 4 5

5

4

3

2

1

place to lessen the likelihood of an eventoccurring, or lessen its impact if it does.In doing so, it is important that the personresponsible for each new action/control isidentified, to ensure that there is clarity ofownership, and that a timetable forimplementation is also drawn up. It is thisassessment and action plan(appropriately documented) which willenable trustees to make a riskmanagement statement in accordancewith the regulations.

Risk management is aimed at reducingthe “gross level” of risk (initial risk) to areduced level of “net risk”. Exampletemplates for recording the riskassessment are set out on pages 14 and 15.

The implementation of new controls andprocedures to manage risk needs to beconsidered in the context of cost benefit.Clearly, there would be little point inimplementing a highly complex andexpensive series of controls if the impacton risk reduction was minimal.Conversely, the process may help trusteesidentify existing control and procedureswhich provide little value and addunwanted cost.

The identification of major risks and thecontrols which exist to manage them,along with the preparation of an actionplan for the implementation of additionalcontrols and procedures where required,will enable trustees to make a positivestatement in respect of risk managementin the Trustees’ Annual Report.

Regular Monitoring andAssessment

The identification and assessment of riskand associated controls must not berelegated to a one-off event. Themanagement of risk is on-going and anyprocess employed must ensure that newrisks are identified and addressed as theyarise and that established risks arereassessed on a regular basis. As aminimum, the risk assessment should berevisited on a formal basis at least once ayear, but the processes employed shouldallow for ongoing assessment andreporting of risk. Many charities have riskand risk management as a standingagenda item for all trustee andmanagement meetings.

UK200Group England & Wales Charities 2015 13

> Charities and Risk Management

Recording Risk Assessment

In order for risk management to be effective and allow trustees to formally evidence their assessment of risk, it is essential that theassessment is appropriately recorded. Many charities do so by adopting a form of risk register/matrix. There is no prescribed formatwhich charities must adopt and the form and content will vary depending upon the size of a charity. The following are examples ofrisk register templates which have been adopted:

Example Format 1

Structure,skills andconduct of theBoard ofTrustees andmanagementcommittees isinappropriate

Weak orineffectivefinancialcontrols andinadequatefinancialplanning andforecasting

1

2

5

4

10

12

NoneFormal reviewandassessment ofBoardstructure,training andskills – annually

Formal review of strategy –annually

Formal Reviewand approval of budgets –annually

Formal review of managementaccounts andvariance analysis -monthly

Board ofTrustees

FinanceManager/Board ofTrustees

Low

Low

Review of structureand constitutionalchange to ensurethat the Boardcontains thenecessaryexperience andskills/skills audit

Terms of referenceand reporting linesclearly defined

Appropriate trainingand advisorysupport in place

Recruitment process

Organisation chartand clearunderstanding ofroles andresponsibilities

Budgets linked tobusiness planningand objectives

Timely and accuratemonitoring andreporting

Proper costingprocedures forproduct or servicedelivery

Adequate skillsbase to produceand interpretbudgetary andfinancial report

Procedures toreview and actionbudget/cash flowvariances

Risk Factor Risk Risk Gross Control Net Responsibility Monitoring Further Likelihood Impact Risk Procedure Risk Process/

1 - 5 1 - 5 Score L/M/H Review Date

e.g. Governance and Management

e.g. Financial

14 UK200Group England & Wales Charities 2015

> Charities and Risk Management

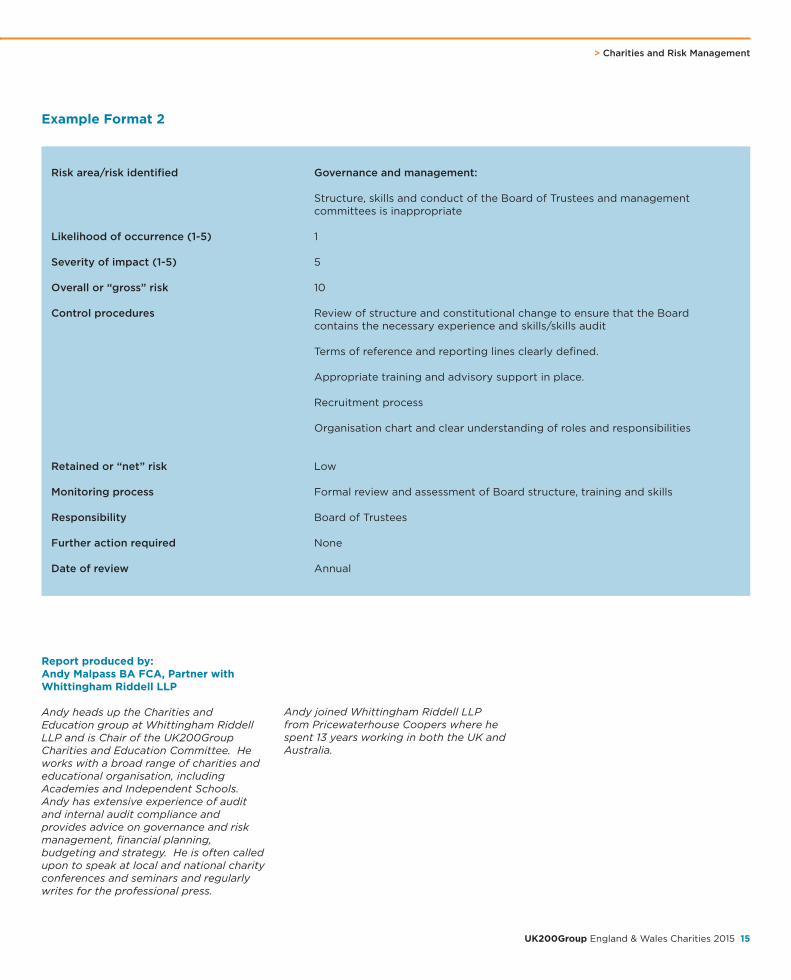

Example Format 2

Risk area/risk identified Governance and management:

Structure, skills and conduct of the Board of Trustees and management committees is inappropriate

Likelihood of occurrence (1-5) 1

Severity of impact (1-5) 5

Overall or “gross” risk 10

Control procedures Review of structure and constitutional change to ensure that the Board contains the necessary experience and skills/skills audit

Terms of reference and reporting lines clearly defined.

Appropriate training and advisory support in place.

Recruitment process

Organisation chart and clear understanding of roles and responsibilities

Retained or “net” risk Low

Monitoring process Formal review and assessment of Board structure, training and skills

Responsibility Board of Trustees

Further action required None

Date of review Annual

Report produced by:Andy Malpass BA FCA, Partner withWhittingham Riddell LLP

Andy heads up the Charities andEducation group at Whittingham RiddellLLP and is Chair of the UK200GroupCharities and Education Committee. Heworks with a broad range of charities andeducational organisation, includingAcademies and Independent Schools.Andy has extensive experience of auditand internal audit compliance andprovides advice on governance and riskmanagement, financial planning,budgeting and strategy. He is often calledupon to speak at local and national charityconferences and seminars and regularlywrites for the professional press.

UK200Group England & Wales Charities 2015 15

Andy joined Whittingham Riddell LLPfrom Pricewaterhouse Coopers where hespent 13 years working in both the UK andAustralia.

Charity Accounting and Financial Reporting

Introduction

Charity accounting and reportingrequirements applicable to England andWales are primarily dictated by theCharities Act 2011 and the Statements ofRecommended Practice (known under theacronym SORP).

The SORP issued in 2005 has beenreplaced by SORP 2015 and the detailedreporting requirements have beenamended to be in line with changes to UKGenerally Accepted Accounting Principles(GAAP) imposed by the adoption ofFinancial Reporting Statement 102 (FRS102). The new provisions apply foraccounting periods beginning on or after 1 January 2015. The details of SORP 2015and the changes it introduces are set outin the section of this handbook entitled“Charity accounting and financialreporting – SORP 2015”.

The areas covered in this section are asfollows:

> Accounting records > Annual statutory accounts and trustees’

annual report> Annual return> Summary of accounts and report

production and filing requirements> External scrutiny.

Overriding principle

In order to benefit from the special taxstatus granted to charities and to fulfil theprinciples of public accountability andtransparency required of them, allcharities are required to not only maintainaccounting records and prepare accounts,but also to make the accounts available tothe public on request.

(If the particular charity is also required toprepare a trustees’ annual report then thishas to be made available too.)

This duty is in addition to any other filingrequirements under the Charities orCompanies Act or by any other principalregulators (exempt charities). To assist indefraying the cost of the provision above,the trustees are permitted to make areasonable charge to cover incidentalssuch as copying and postage.

Accounting Records

All charities must comply with thefollowing requirements in respect of thepreparation and maintenance ofaccounting records:

> Prepare and maintain accountingrecords. These records which willinclude cash books, invoices, receipts,bank statements, wage details etc mustbe retained for at least 6 years (as setout in the Charities Act)

> Where gift aid payments are received,records must be maintained for six yearsincluding the details of substantial donors,in accordance with HMRC requirements.

Annual Statutory Accountsand Trustees’ AnnualReport

Requirement to prepare and fileaccounts

All Charities are required to prepareannual accounts in some form and areobliged to make them available to thepublic, upon request, together with, ifrequired, a trustees’ annual report. Theavailability to the public of the accountsand the trustees’ annual report is neededto underpin the principle of publicaccountability and transparency of Charities.

Also as a matter of public record, certaininformation has to be filed with theCharity Commission. The amount ofinformation depends entirely on the levelof income of the Charity, apart fromCharitable Incorporated Organisations(CIOs) which are required to file an annualreturn, trustees’ annual report and accountsregardless of the level of their income.

Basis of preparation of accounts

Receipts and Payments Accounts

Receipts and payments accounts can beprepared by non-company Charities witha gross income of £250,000 or lessduring the financial year with thefollowing items contained within them:

> Receipts and payments account> Statement of assets and liabilities

> Notes to the accounts (where appropriate)> Trustees’ annual report.

Charities with a gross income of £250,000or less can opt to prepare accounts on anaccruals basis.

Charity Commission guidance on thepreparation of receipts and paymentsaccounts, in the form of its ‘receipts andpayments accounts pack (CC16)’ isavailable on the Commission website.

Accruals Accounts

All charitable companies, non-companyCharities with a gross income exceeding£250,000 and those Charities whererequired by their underlying constitution,must prepare in each financial year anannual report and accounts based uponthe accruals concept with the followingkey components:

> Statement of Financial Activity (“SOFA”)(including an income and expenditureaccount - where appropriate)

> Balance sheet (also known as thestatement of financial position)

> Cash flow statement (where required *)> Notes to the accounts> Trustees’ annual report.

* SORP 2015 effective from 1 January 2015has been initially designed in 2 partsallowing small charities to take advantageof the FRSSE and not prepare a cash flow,however this standard is being withdrawnin 2016 and after that date all charities willneed to follow the new FRS 102 formatwhich includes a requirement for a cashflow – (refer to page 20 for section onSORP 2015).

Such accounts for Charities are normallyrequired to show a true and fair view.Charities are required to apply themethods and principles of the SORP andthe regulations when preparing theirfinancial statements.

Charity Commission guidance on thepreparation of accruals accounts in theform of its ‘accruals accounts pack (CC17)’is available on the Commission website.

Group Accounts

Under the provisions of the Charities Act2011, Charities with subsidiaries must

16 UK200Group England & Wales Charities 2015

prepare group accounts to consolidate theaccounts of the Charity and any subsidiaries,if the income of the group, after eliminatingintra-group transactions and consolidationadjustments, exceeds £1,000,000 foraccounting periods ending on or after 31 March 2015 (previously £500,000).These accounts are prepared on theaccruals basis and in accordance with theSORP and comprise:

> Group SoFA> Group income and expenditure account

– if appropriate> Group and charity only balance sheet> Group and charity only cash flow –

where required > Notes to the accounts> Trustees’ annual report.

Trustees’ Annual Report

All registered charities must prepare atrustees’ annual report (TAR). Some ofthe basic contents are mandatory for allcharities but the bigger the charity themore comprehensive the informationshould be. The purpose of the TAR is toexplain the aims of the charity and how itis going about achieving them. It does nothave to be complicated, particularly forthe smaller charity, but it should enablethe reader of the accounts to understandhow the money was raised, spent and,crucially, what difference it made.

The TAR is structured under the followingheadings for all charities:

> Reference and administration details ofthe charity, its trustees and advisers

> Structure, governance and management> Objectives and activities> Achievements and performance> Financial review> Any funds held as custodian trustees on

behalf of others – if appropriate> Public benefit.

In addition for larger charities, (thosesubject to statutory audit) must include:

> Plans for future periods

and for group accounts:

> Relationship between the charity andrelated parties including subsidiaries

> Significant activities through thesubsidiaries (under objectives andactivities)

> Differentiation in achievements andperformance between the charity andthe subsidiary

> Financial position of the charity andsubsidiary (under financial review).

The detailed legal requirements for thetrustees’ annual report are set out in theCharities (Accounts and Reports)Regulations 2008 which underpins therecommendations of the Charities SORP.

Excepted and Exempt Charities

These charities are not required to file theirtrustees’ annual report or accounts with theCharity Commission, but may be requiredto file elsewhere in accordance with theirprinciple regulators (exempt charities).The basic requirements to keep accountingrecords and to prepare accounts whichare available to the public on request do,however, have to be met.

Annual Return

Charity trustees, by law, must keep thecharity’s registered details up-to-date.

Small charities with a gross income of£10,000 or less do this utilising an annualinformation update form. If the charity’sincome is more than £10,000, an annualreturn must be completed. The annualreturn should be compiled when theaccounts for the period are finalised andsigned using the information contained inthem to complete the form.

Annual Information Update

This requests basic information about thecharity including trustee details anddetails of its area(s) of operation.

Annual Return

This comprises the following basicinformation:

> Registered charity number (andcompany number if applicable)

> Charity’s bank or building society details- account name, number and sort code

> Trustees’ details - names, dates of birthand contact details

> Details of the main contact at the charity > Number of volunteers and employees at

the charity.

The following additional information isalso required:

Financial information

> Start and end dates of the financialperiod you are reporting on

> Total income and spending for the period > The amount spent outside England and

Wales.

Information on aims and activities

> A description of activities in thereporting period (around 100 words)

> Information about what the charity does> Locations where the charity worked in

the period.

Where the charity’s income is > £25,000the following digital copies (PDF format)will also be required:

> The charity’s accounts, agreed by thetrustees

> Independent examiner or auditor’s report> Trustees’ annual report> A list of any serious incidents that took

place in the year, even if alreadyreported to the Charity Commission.

There is no longer any requirement forlarger charities to complete the SummaryInformation Return (SIR).

Summary of Changes to Annual Return

For the annual return for 2015 the CharityCommission is introducing three newquestions to be answered by all charitiesthat complete the annual return.

> In the reporting period how muchincome did you receive from:

l Contracts from central or local government to deliver services

l Grants from central or local government

> Does your charity have a policy onpaying its staff?

> Has your charity reviewed its financialcontrols during the reporting period?

The Charity Commission have producedguidance to accompany these newquestions.

UK200Group England & Wales Charities 2015 17

> Charity Accounting and Financial Reporting

Filing Deadline

Charity Commission

The deadline for filing accounts and reports with the Charity Commission is within 10 months of the end of each financial reportingperiod.

Companies House

Incorporated charities must also file their accounts and trustees annual report with Companies House within 9 months of the year end.

18 UK200Group England & Wales Charities 2015

Summary of Accounts and Report Production and Filing RequirementsSet out below is a table summarising the accounts and report production and reporting requirements for Charities of different sizes:

1 Registered charities with income below £10k are asked to complete and file an update form.

2 Accrual basis of accounts preparation if corporate charity, income >£250k or required by governing document.

There is a link on the charity commission website for information on, and to access, the annual return which is as followshttp://bit.ly/1ylbmMk

Reporting Requirements Prepare Prepare File Annual File Annual Report Serious Receipts and Accounts Annual Report & Return Incidents PaymentsReport Report Accounts Accounts

IncomeCIOs Y Y Y Y - <£250k

Other charities:

Unregistered Y - Y - - Y

Income < £10k Y Y - Y - 1

Income £10k to £25k Y Y Y Y - Y

Income £25k to £250k Y Y Y Y Y Y

Income £250k to £1m* Y Y Y Y Y 2

Income 1m* Y Y Y Y Y 2

> Charity Accounting and Financial Reporting

UK200Group England & Wales Charities 2015 19

> Charity Accounting and Financial Reporting

Income level Requirement Note

Up to £25,000 None Unless governing documents require independent examination or audit*

£25,001 to £250,000 Independent examination Unless governing documents require audit*

£250,001 to £1,000,000** Independent examination Unless governing documents require audit*And gross assets < £3.26m by qualified examiner only

£250,001 to £1,000,000** Statutory auditAnd gross assets > £3.26m

> £1,000,000** Statutory audit

* Incorporated charity – In addition to governing document, 10% of members can request an audit

** For year ends on or before 30 March 2015, the upper threshold was £500,000.

Report produced by Eric Williams FCA,Principal with Edmund Carr LLP andTheresa Rees, Partner at ReesRussell LLP

Eric Williams FCA, Principal withEdmund Carr LLPEric heads up the Charities department atEdmund Carr LLP and is a member of theUK200Group Charities & EducationCommittee. He has had experience of abroad range of Charities and not-for-profit organisations and has extensiveexperience in audit services.

Theresa Rees, Partner at ReesRussell LLPTheresa is a member of the UK200GroupCharities & Education Committee hasworked with a wide range of charitiesencompassing the very small to charitieswith a national presence. Her charityclients operate across a broad sector andinclude those focussed on people (theyoung, the sick and the disadvantaged),places (areas of natural beauty both in theUK and overseas) and churches & faithbased activities.

External Scrutiny

Charity Accounting and Financial Reporting – SORP 2015

Introduction

The new Charity Statement ofRecommended Practice (“SORP”) bringsthe first significant change to accountingand financial reporting for the charity andnot-for-profit sector in a decade.

In 2013 the Financial Reporting Councilissued a new accounting standard, FRS102, to replace all existing accountingstandards. Since the SORP puts theaccounting standards into the specificcontext of the charity and not-for-profitsector, revisions to the existing SORP(SORP 2005) were needed.

The new Charities SORP, “Charities SORP(FRS 102)”, applies to all charities thatprepare their financial statements on theaccruals basis, unless they are small, andchoose to, adopt the “Charities SORP(FRSSE)”.

The Financial Reporting Standard forSmall Entities (“FRSSE”) is a less onerousaccounting standard which is available forsmall entities. To reflect this standard anadditional SORP (Charities SORP(FRSSE)) was also issued.

For most charities the first reportingperiod for which the new SORP will applywill be the year ending 31 December 2015or 31 March 2016. The first set of financialstatements compiled under the newSORPs will need to include comparativeswhich are restated for the new accountingregulations, as well as reconciliations ofthe opening comparative balance sheet,the closing comparative balance sheetand the comparative surplus/(deficit)reported under the current SORP andthose reported under the new SORP.Additionally, each change in accountingpolicy will need to be described andexplained in the notes to the financialstatements.

The SORP is in a modular format withrequirements for larger charities beingincluded in a separate section. Terms usedthroughout are “must”, should” and “may”making its requirements easilyunderstandable.

Choosing to adopt theFRSSE

The SORP (FRSSE) can be used bycharities who meet the small companythresholds, as set out below:

A charity qualifies as small where anytwo of the following three criteria aremet in both the current and precedingfinancial years:

> Gross income of less than £6.5m> Balance sheet total of less than

£3.26m> Average number of employees less

than 50.

Whilst the requirements of the SORP(FRSSE) are much less onerous (see keyareas of change below) the FRSSE (andconsequentially the SORP (FRSSE)) willbe revised shortly which could result infurther changes for those who choose toadopt this SORP. Therefore many charitiesthat are eligible for adopting the SORP(FRSSE) may in fact choose to adoptSORP (FRS 102) instead.

Charities should seek professional advicewhen deciding which SORP to adopt,where the choice is applicable.

The Trustees’ Annual Report

The new SORP continues to stress theimportance of Trustees’ providing abalanced annual report, covering theimpact, as well as the outputs of thecharity during the year.

The main changes noted for all charitiesare:

> An explanation of the policy forholding reserves, including stating theamount of the reserves held and thereasons for holding them. Actualreserves should be compared to thepolicy and any differences explained.Where funds are in deficit, the reportshould explain why and set out thesteps being taken to eliminate thedeficit

> A separate category of identifiedreserves can be established withinunrestricted reserves. Where Trusteeshave decided that holding reserves isunnecessary, the report must disclose

this fact as well as providing thereasons behind this decision. Thisfollows the good practice which manycharities have already established

> For any charities with more than 50Trustees, all Trustees names must nowbe disclosed.

The main changes noted for largercharities are:

> An explanation of social investmentpolicies, explaining how anyprogramme related investment hascontributed to the achievements of thecharity’s aims and objectives

> In addition to reporting the significantcharitable activities undertaken, anexplanation of the financial effect ofsignificant events is required

> A description of the principal risks anduncertainties facing the charity, asidentified by the Trustees, together witha summary of their plans and strategiesfor managing those risks

> Arrangements for setting the pay andremuneration of key managementpersonnel1 and any benchmarks,parameters or criteria used in settingtheir pay

> A charity which makes largefundraising payments in advance mustexplain the basis upon which thepayments are made and the effect onfundraising ratios must be qualtified.

20 UK200Group England & Wales Charities 2015

1 Key management personnel are “thosepersons having authority andresponsibility for planning, directing andcontrolling the activities of the charity,directly or indirectly, including anyDirectors of the charity. This definitionincludes Trustees and those seniormanagement personnel to whom theTrustees have delegated significantauthority or responsibility in the day-to-day running of the charity.

The Statement of FinancialActivity (SoFA)

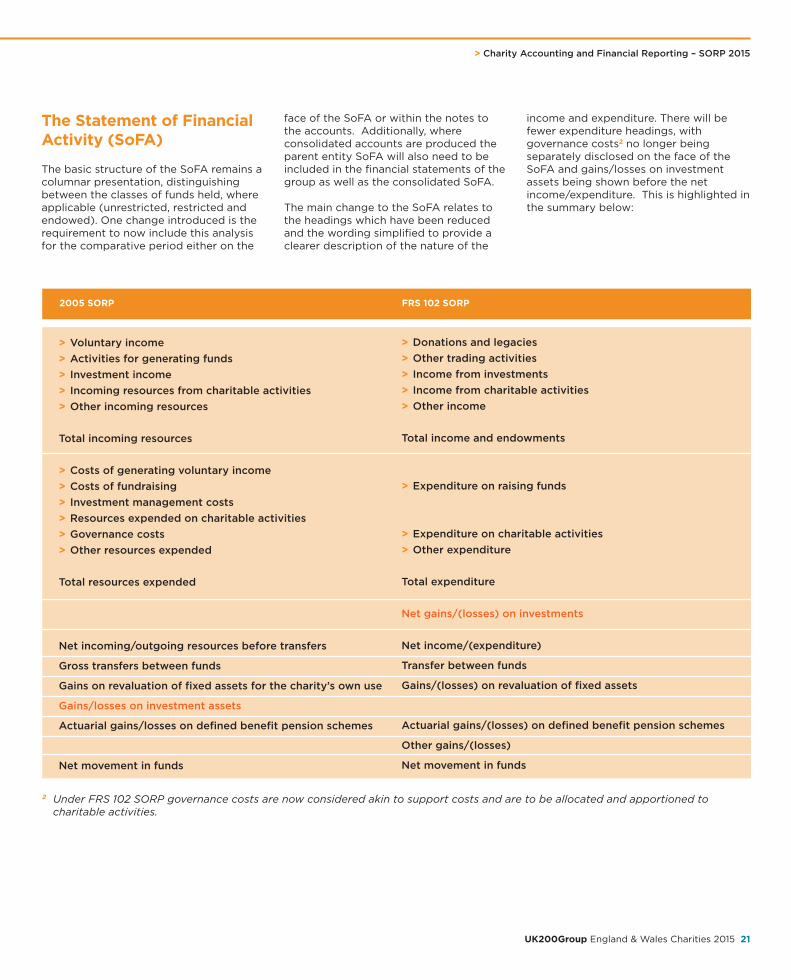

The basic structure of the SoFA remains acolumnar presentation, distinguishingbetween the classes of funds held, whereapplicable (unrestricted, restricted andendowed). One change introduced is therequirement to now include this analysisfor the comparative period either on the

face of the SoFA or within the notes tothe accounts. Additionally, whereconsolidated accounts are produced theparent entity SoFA will also need to beincluded in the financial statements of thegroup as well as the consolidated SoFA.

The main change to the SoFA relates tothe headings which have been reducedand the wording simplified to provide aclearer description of the nature of the

income and expenditure. There will befewer expenditure headings, withgovernance costs2 no longer beingseparately disclosed on the face of theSoFA and gains/losses on investmentassets being shown before the netincome/expenditure. This is highlighted inthe summary below:

UK200Group England & Wales Charities 2015 21

> Charity Accounting and Financial Reporting – SORP 2015

2005 SORP FRS 102 SORP

> Voluntary income> Activities for generating funds> Investment income> Incoming resources from charitable activities> Other incoming resources

Total incoming resources

> Costs of generating voluntary income> Costs of fundraising> Investment management costs> Resources expended on charitable activities> Governance costs> Other resources expended

Total resources expended

Net incoming/outgoing resources before transfers

Gross transfers between funds

Gains on revaluation of fixed assets for the charity’s own use

Gains/losses on investment assets

Actuarial gains/losses on defined benefit pension schemes

Net movement in funds

> Donations and legacies> Other trading activities> Income from investments> Income from charitable activities> Other income

Total income and endowments

> Expenditure on raising funds

> Expenditure on charitable activities> Other expenditure

Total expenditure

Net gains/(losses) on investments

Net income/(expenditure)

Transfer between funds

Gains/(losses) on revaluation of fixed assets

Actuarial gains/(losses) on defined benefit pension schemes

Other gains/(losses)

Net movement in funds

2 Under FRS 102 SORP governance costs are now considered akin to support costs and are to be allocated and apportioned to charitable activities.

> Charity Accounting and Financial Reporting – SORP 2015

The Balance Sheet

The format of the balance sheet isunchanged under the new SORP otherthan the definitive requirement to presenta revaluation reserve on the face of thebalance sheet where such a reserve exists.There is also an opportunity to include areserve fund (continuity fund) as aseparate unrestricted fund and anydefined pension benefit surplus/deficitcan be disclosed as a separate pensionreserve.

There are, however some changes to howbalance sheet items should be accountedfor and the details of these are included inthe summary of key changes (later in thissection).

Transitional arrangements

SORP 2015 provides a one-offopportunity to simplify the preparation ofthe opening balance sheet andcomparative figures, when reportingunder it for the first time. In particular, acharity may elect to measure a fixed asset(including buildings) on the date oftransition at its fair value and use that fairvalue as its deemed cost at that date.

Charities will need to weigh-up the cost ofobtaining such valuations and the likelyincreased depreciation charge against thepotential benefit.

Cash Flow Statement

Unlike the previous SORP, FRS 102 SORPdoes not contain an exemption for smallentities from preparing a cash flowstatement. Therefore, unless a charity isable to, and chooses to adopt the FRSSESORP, it will have to prepare a cash flowstatement.

Subsidiaries of charities (whether tradingor charitable) are able to take advantageof the disclosure exemptions permitted byFRS 102 and not prepare a cash flowstatement.

A template for the cash flow statementand associated notes as required underthe new SORP is shown below:

22 UK200Group England & Wales Charities 2015

Total funds £ Prior year funds £ Note

Cash flows from operating activities: x x Note 1

Net cash provided by (used in) operating activities A A

Cash flows from investing activities:> Dividends, interest & rents from investments X X> Proceeds from the sale of property, plant & equipment X X> Purchase of property, plant & equipment (x) (x)> Proceeds from sale of investments X X> Purchase of investments (x) (x)

Net cash provided by (used in) investing activities B B

Cash flows from financing activities:> Repayments of borrowing (x) (x)> Cash inflows from new borrowing X X> Receipt of endowment X X

Net cash provided by (used in) financing activities C C

Change in cash and cash equivalents in the reporting period =A+B+C =A+B+C

Cash and cash equivalents at the beginning of the reporting period X X Note 2

Change in cash and cash equivalents due to exchange rate movements X X

Cash and cash equivalents at the end of the reporting period x x Note 2

Statement of cash flows

UK200Group England & Wales Charities 2015 23

> Charity Accounting and Financial Reporting – SORP 2015

Current year Prior year£ £

Net income/(expenditure) for the reporting period x x(as per the statement of financial activities)

Adjustments for:

> Depreciation charges x x

> Gains/(losses) on investments x x

> Dividends, interest & rents from investments (x) (x)

> Loss/(profit) on sale of fixed assets x x

> (Increase)/decrease in stocks (x) (x)

> (Increase)/decrease in debtors (x) (x)

> Increase/(decrease) in creditors x x

Net cash provided by (used in) investing activities x x

Note 1 – Reconciliation of net income/(expenditure) to net cash from operating activities

Current year Prior year£ £

Cash in hand x x

Notice deposits (less than three months) x x

Overdraft facility repayable on demand x x

Total cash and cash equivalents X X

Note 2 – Analysis of cash and cash equivalents

Prior year Cash flow Other non-cash changes Current year£ £ £ £

Cash at bank and in hand x x x x

Debt:

Finance leases x x x x

Due within one year x x x x

Debt falling due after more than one year x x x x

Net Funds x x x x

Analysis of changes in net funds

> Charity Accounting and Financial Reporting – SORP 2015

Disclosure of Trustee andStaff Remuneration,Related Party and OtherTransactions

The main changes in the FRS 102 SORP are:-

Related parties