a random walk down wall street - american university€¦ · a random walk down wall street ... as...

TRANSCRIPT

FIN 614 Capital Market Efficiency

Professor Robert B.H. Hauswald

Kogod School of Business, AU

1/25/2011 Market Efficiency © Robert B.H. Hauswald 2

A Random Walk Down Wall Street

• From theory of return behavior to its practice• Capital market efficiency: the hypothesis, forms

– information aggregated: markets conform to theory

– price behavior and empirical evidence

– common misconceptions and "arbitrage"

• Investment techniques: beat the markets?

– common practice: fundamental and technical analysis

– Of (Wo)Men and Mice: chartists, momentum players, contrarians and other wild beasts

1/25/2011 Market Efficiency © Robert B.H. Hauswald 3

Capital Market Efficiency

• Efficient capital market: current market prices fully reflect available information– costless trading rules do not consistently beat the market

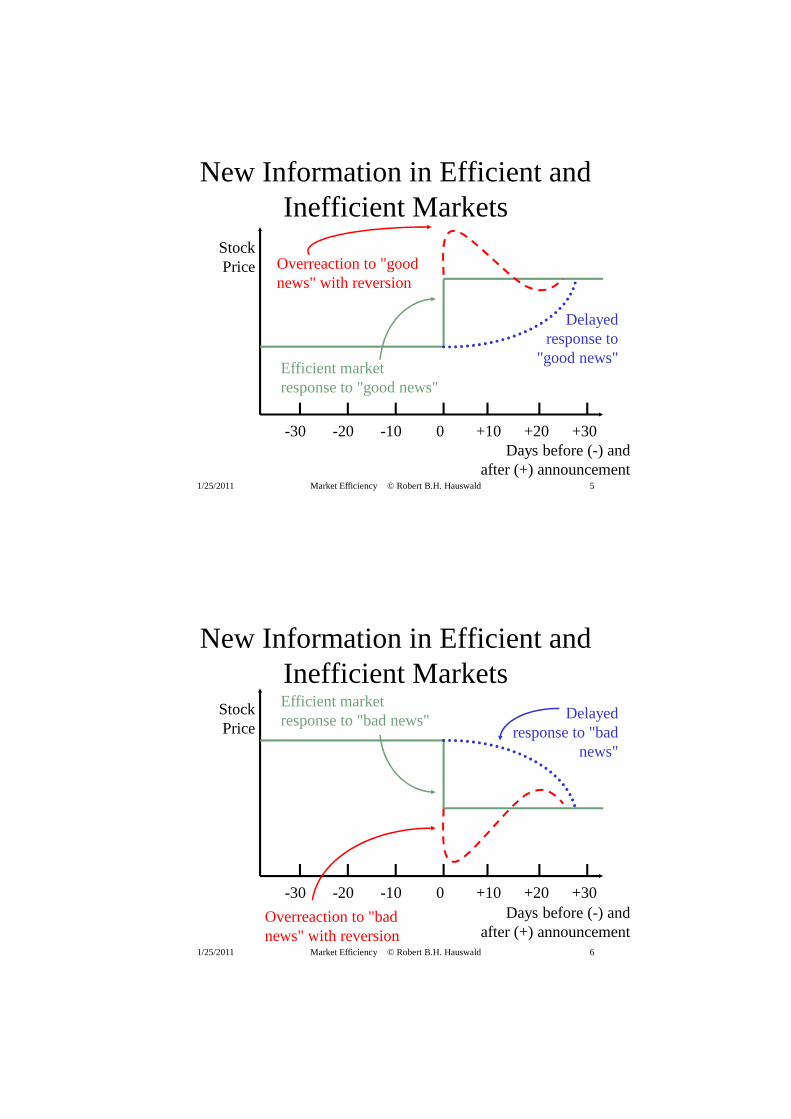

• Price behavior in an efficient market– stock price reaction to news in efficient and inefficient markets:

nearly instantaneous vs. delayed – difference?

• The Efficient Market Hypothesis (EMH)– securities represent zero NPV investments: they are expected to

return just their exact risk-adjusted rate– modern (US) stock markets are, as a practical matter, efficient

• Causes of market efficiency: information disclosure– competition among investors and traders, trading regulation

1/25/2011 Market Efficiency © Robert B.H. Hauswald 4

Efficient Capital Markets

• An efficient capital market is one in which stockprices fully reflect available information.

• The EMH has implications for investors and firms.

– Since information is reflected in security prices quickly,knowing information when it is released does aninvestor no good.

– Firms should expect to receive the fair value forsecurities that they sell. Firms cannot profit fromfooling investors in an efficient market.

1/25/2011 Market Efficiency © Robert B.H. Hauswald 5

New Information in Efficient and Inefficient Markets

Stock Price

-30 -20 -10 0 +10 +20 +30Days before (-) and

after (+) announcement

Efficient market response to "good news"

Overreaction to "good news" with reversion

Delayed response to

"good news"

1/25/2011 Market Efficiency © Robert B.H. Hauswald 6

Stock Price

-30 -20 -10 0 +10 +20 +30Days before (-) and

after (+) announcement

Efficient market response to "bad news"

Overreaction to "bad news" with reversion

Delayed response to "bad

news"

New Information in Efficient and Inefficient Markets

1/25/2011 Market Efficiency © Robert B.H. Hauswald 7

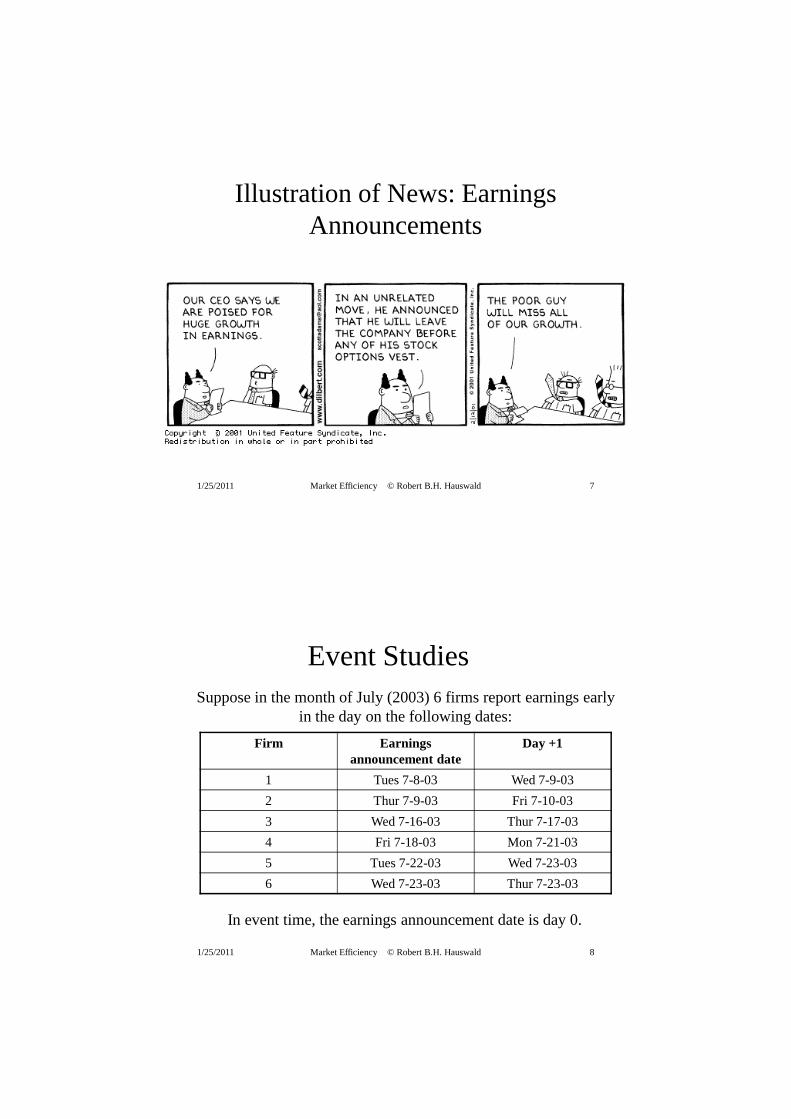

Illustration of News: Earnings Announcements

1/25/2011 Market Efficiency © Robert B.H. Hauswald 8

Event StudiesSuppose in the month of July (2003) 6 firms report earnings early

in the day on the following dates:

Firm Earnings announcement date

Day +1

1 Tues 7-8-03 Wed 7-9-03

2 Thur 7-9-03 Fri 7-10-03

3 Wed 7-16-03 Thur 7-17-03

4 Fri 7-18-03 Mon 7-21-03

5 Tues 7-22-03 Wed 7-23-03

6 Wed 7-23-03 Thur 7-23-03

In event time, the earnings announcement date is day 0.

1/25/2011 Market Efficiency © Robert B.H. Hauswald 9

Event Studies

-5 -4 -3 -2 -1 0 +1 +2 +3 +4 +5

Event Time (in days)

10%

-10%

0%

5%

-5%

Cum

ulat

ive

Abn

orm

al R

etur

n

The actual return minus the expected return

Abnormal return

Abn

orm

al R

etur

n

Could just be the market index return for the day, or the market index return times the beta of the

firm reporting the earnings announcement (CAPM)

The positive jump on day 0 implies that the earnings news was, on average for these firms, better than expected: adjusting for market movements!

Because the line is flat after day 0, the market seems to fully incorporated the earnings news on the event day: no additional upward or downward price trend is seen

Response to Democratic Victory in 2006

10

1/25/2011 Market Efficiency © Robert B.H. Hauswald 11

Different Types of Efficiency

• Weak Form– Security prices reflect all information found in past

prices and volume.

• Semi-Strong Form– Security prices reflect all publicly available

information.

• Strong Form– Security prices reflect all information—public and

private.

1/25/2011 Market Efficiency © Robert B.H. Hauswald 12

Weak FormMarket Efficiency

• Security prices reflect all information found inpast prices and volume.– if the weak form of market efficiency holds, then

technical analysis (extrapolation) is of no value.

– often weak-form efficiency is represented as

Pt = Pt-1 + Expected return + random error t

• Since stock prices only respond tonewinformation, which by definition arrivesrandomly, stock prices are said to follow arandom walk.

1/25/2011 Market Efficiency © Robert B.H. Hauswald 13

Semi-Strong Form Market Efficiency

• Security Prices reflect all publiclyavailable information.

• Publicly available information includes:– Historical price and volume information

– Published accounting statements.

– Information found in annual reports.

1/25/2011 Market Efficiency © Robert B.H. Hauswald 14

Strong FormMarket Efficiency

• Security Prices reflect all information– public and private: even inside information!

• Strong form efficiency incorporates weakand semi-strong form efficiency.

• Strong form efficiency says thatanythingpertinent to the stock and known to at leastone investor is already incorporated into thesecurity’s price.

1/25/2011 Market Efficiency © Robert B.H. Hauswald 15

Three Different Information Sets

All informationrelevant to a stock

Information setof publicly available

information

Informationset of

past prices

1/25/2011 Market Efficiency © Robert B.H. Hauswald 16

Three Approaches to Security Selection

Technical Analysis• historical price and volume movements can identify price

patterns from which future prices can be forecast

Fundamental Analysis

• Forecast future free cash flows, find PV of these to estimate security’s Intrinsic Value, buy if Intrinsic value is greater than price of security ("Margin of Safety")

Efficient Market Selection

• Assumes Fundamental Analysis works so well that current market prices will be equal to their Intrinsic Value, buy and hold, earn a return for risk bearing not security selection

1/25/2011 Market Efficiency © Robert B.H. Hauswald 17

Investment Research

1/25/2011 Market Efficiency © Robert B.H. Hauswald 18

Views Contrary to Market Efficiency

• Stock Market Crash of 1987– The market dropped between 20 percent and 25 percent

on a Monday following a weekend during which little surprising information was released.

• Temporal Anomalies– Turn of the year, —month, —week.

• Speculative Bubbles– Sometimes a crowd of investors can behave as a single

squirrel.

1/25/2011 Market Efficiency © Robert B.H. Hauswald 19

The Evidence

• The record on the EMH is extensive, and inlarge measure it is reassuring to advocates ofthe efficiency of markets.

• Studies fall into three broad categories:1. Are changes in stock prices random? Are there

profitable "trading rules"?

2. Event studies: does the market quickly andaccurately respond to new information?

3. The record of professionally managed investmentfirms.

1/25/2011 Market Efficiency © Robert B.H. Hauswald 20

Are Changes in Stock Prices Random?

• Can we really tell?– Psychologists and statisticians believe that most people

want to see patterns even when faced with pure randomness.

– People claiming to see patterns in stock price movements are probably seeing optical illusions.

• A matter of degree– Even if we can spot patterns, we need to have returns that

beat our transactions costs.

• Random stock price changes support weak-form efficiency

1/25/2011 Market Efficiency © Robert B.H. Hauswald 21Market Efficiency - 8

Technical Analysis

• The market is inefficient, long live the market!!!!• Castles in the air: mania, bubbles, panics, crashes

– Tulip bulb craze in 1634, South sea trade in 1711– 1929 stock price valuation: INVESTMENT POOLS– Growth stocks in 1961, NIFTY 50 in 1972– High tech in 2000?– stick to your fundamentals?

• Technical analysts: prices reflect "sentiment" – prices reflect more than fundamental values– prices are driven by prevailing market sentiments

1/25/2011 Market Efficiency © Robert B.H. Hauswald 22

Misinformation or Marketing?

• Chartists: predict future from past prices• Mechanical trading rules: head & shoulders/flags,

pennants, support, resistance levels, accumulation levels, corrections, waves, breakthroughs– "Hold the winners, sell the losers"– "Switch into 'Strong' stocks"– "Don't fight the tape"

• Computers jazz up technical analysis– belief: past prices and volume reveal information– prices react slowly over long periods of time to new

information or changes in investor sentiment

1/25/2011 Market Efficiency © Robert B.H. Hauswald 23

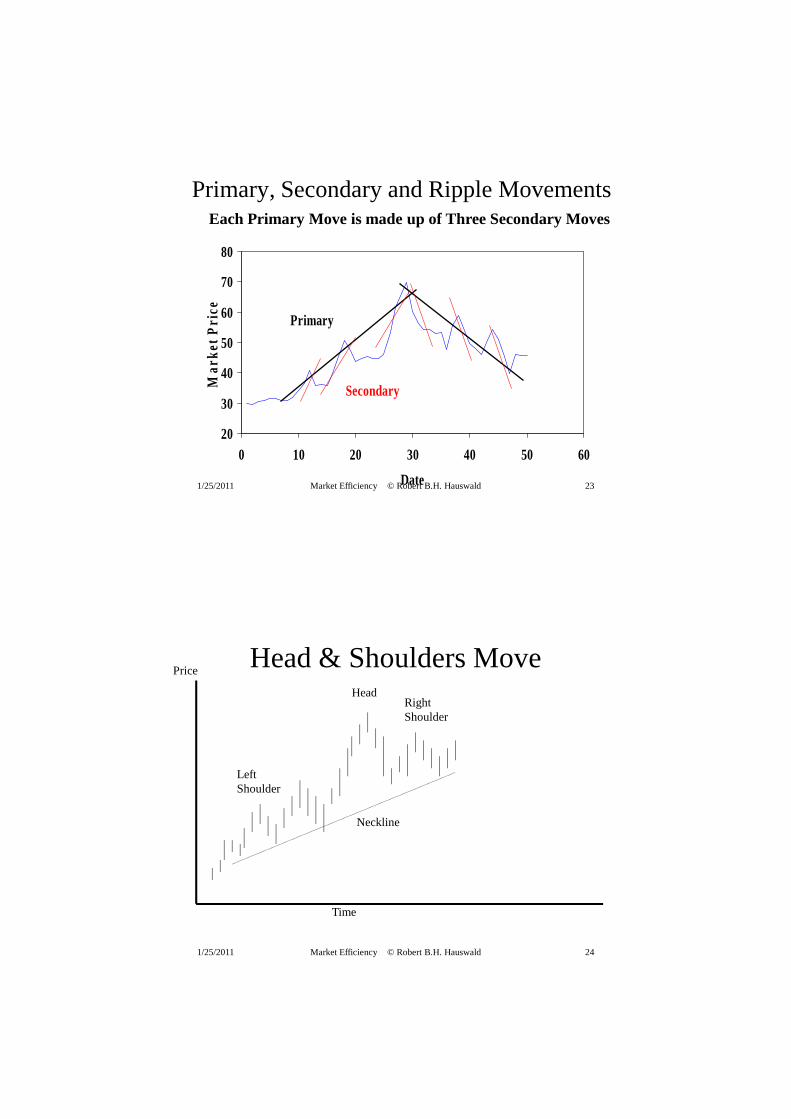

Primary, Secondary and Ripple Movements

20

30

40

50

60

70

80

0 10 20 30 40 50 60

Date

Mar

ket

Pri

ce

Primary

Secondary

Each Primary Move is made up of Three Secondary Moves

1/25/2011 Market Efficiency © Robert B.H. Hauswald 24

Head & Shoulders Move

LeftShoulder

HeadRightShoulder

Neckline

Time

Price

1/25/2011 Market Efficiency © Robert B.H. Hauswald 25

Support & Resistance Levels

25

30

35

40

45

50

0 20 40 60 80 100

Date

Pri

ce

Resistance Level

Support Level

1/25/2011 Market Efficiency © Robert B.H. Hauswald 26

Momentum Players

• Motto: "sell the losers, keep the winners"• Past trends up or down will continue as the

information is slowly absorbed by the market – or as the wave of optimism or pessimism spreads

through the market

• Suggests that the series of returns should show positive autocorrelation (correlation over time)– price increases should tend to be followed by price

increases, and price decreases should tend to be followed by price decreases

• Cyclical patterns and volatility: look at recent price plots

1/25/2011 Market Efficiency © Robert B.H. Hauswald 27

Contrarians at the Gates!

• Assumption: investors overreact to good and bad news– investors are irrational?

• Advice is to buy on bad news and sell on good news– returns should exhibit negative serial dependence because price

reversals are more likely than continuances of price changes

• PLOT of actual and simulated stock prices: Figure 13.5– then trade!

• Weekly closing of the Dow-Jones Industrials, 1955-1956

==> Garbagein, Garbage out

1/25/2011 Market Efficiency © Robert B.H. Hauswald 28

Evidence on EMH: Weak Form

• Technical analysis (past prices!) should not work if the market moved in a true random fashion; so test– chartists vs. random walk: market is semi-strong efficient

• random walk: price changes should be uncorrelated and prices should look like a random walk – without patterns and all-over the place– statistical evidence: plots, correlations, statistical tests– long term profitability of technical trading rules– horse races of different trading strategies

• NO evidence in support of Technical Analysis– net of trading costs and risk adjustment!

1/25/2011 Market Efficiency © Robert B.H. Hauswald 29

Why Technical Analysis FailsS

tock

Pric

e

Time

Investor behavior tends to eliminate any profit opportunity associated with stock price patterns.

If it were possible to make big money simply by finding "the pattern" in the stock price movements, everyone would do it and the profits would be competed away.

Sell

Sell

Buy

Buy

1/25/2011 Market Efficiency © Robert B.H. Hauswald 30

Tests of Semi-Strong and Strong Forms

• Which forms, if any, are supported by statistical examination of the data?

– test different versions against trading strategies

– theory meets practice: how could both be right?

• Recall two adjustments that we need to make1. Risk adjustment: concomitant problem of incorrect

risk adjustment

2. Transaction costs: need to subtract trading costs from dollar returns – mechanical trading incurs high costs

1/25/2011 Market Efficiency © Robert B.H. Hauswald 31

Fees and Transaction Costs

1/25/2011 Market Efficiency © Robert B.H. Hauswald 32

Testing the Semi-Strong EMH

• Using public information, can one generate risk-adjusted trading profits?

• Investigate accounting changes based strategies– should we buy stock in companies that announces

change of accounting policy – buy stock based on firms’ choice of LIFO vs FIFO– if prices (inflation) are rising, LIFO accounting leads to

higher cash flows because of lower taxes – but it produces lower net income.

• "Fooling" investors by changes in accounting?– Not this one

1/25/2011 Market Efficiency © Robert B.H. Hauswald 33

Event Studies Tests

• Event Studies are tests of the semi-strong form of market efficiency, i.e., whether– prices reflect all publicly available information.

• Event studies examine prices and returns over time– particularly around the arrival of new information– test for evidence of underreaction, overreaction,

early reaction, delayed reaction around the event– adjusting for market-wide effects: idiosyncratic

returns in response to "relevant" new information

1/25/2011 Market Efficiency © Robert B.H. Hauswald 34

Event Study Results

• Event study methodology has been applied to a large number of events including:– Dividend increases and decreases; earnings announcements– Mergers; capital-structure changes; new issues of stock– Capital spending; R&D

• The studies generally support the view that the market is semistrong-from efficient.– markets may even have some foresight into the future– news tends to leak out in advance of public

announcements.

1/25/2011 Market Efficiency © Robert B.H. Hauswald 35

The Record on Mutual Funds

• If the market is semistrong-form efficient, then no matter what publicly available information mutual-fund managers rely on to pick stocks, their average returns should be the same as those of the average investor in the market as a whole.

• We can test efficiency by comparing the performance of professionally managed mutual funds with the performance of a market index.

1/25/2011 Market Efficiency © Robert B.H. Hauswald 36

The Record of Mutual Funds

Taken from Lubos Pastor and Robert F. Stambaugh, "Mutual Fund Performance and Seemingly Unrelated Assets," Journal of Financial Exonomics, 63 (2002).

-2.13%

-8.45%

-5.41%

-2.17% -2.29%

-1.06%-0.51%-0.39%

All funds Small-companygrowth

Other-aggressive

growth

Growth Income Growth andincome

Maximumcapital gains

Sector

1/25/2011 Market Efficiency © Robert B.H. Hauswald 37

Evidence on Strong EMH Form

• Stock prices reflect all publicly AND privately available information: implies what?

• Mutual funds excess returns– are fund managers are either better at picking stocks than

most people? access to private information?– after adjusting for risk and transaction costs: managers

apparently NOT better at picking stocks on average

• Insider trading: do insiders earn excess returns?– Yes, if returns calculated from time of purchase or sale

rather than from time of announcement of purchase or sale

1/25/2011 Market Efficiency © Robert B.H. Hauswald 38

Past Performance and Beating the Market…

1/25/2011 Market Efficiency © Robert B.H. Hauswald 39

The Forms of Market Efficiency

• Weak efficiency: you cannot beat the market by knowing past prices and trading on this knowledge– supported by evidence after risk and trading cost

adjustments

• Semi-strong efficiency: you cannot consistently beat the market using publicly available information– most controversial form of the theory: largely supported

• Strong efficiency: no (public or private) information of any kind can be used to beat the market– evidence shows this form does not hold– so become an insider?

1/25/2011 Market Efficiency © Robert B.H. Hauswald 40

EMH Misconceptions

• Capital market history shows:1. prices respond very rapidly to new information2. future prices changes are difficult to predict3. mispriced stocks (accurately predictable future price

level): difficult to identify and exploit

• Market efficiency does not mean irrelevance of– investment decisions: the risk/return trade-off still applies– rather: you cannot expect to consistently "beat the market"

on a risk-adjusted basis using costless trading strategies

• The EMH does not say prices are random; but rather– price changes in an efficient market are random and

independent: they cannot be predicted before they happen

1/25/2011 Market Efficiency © Robert B.H. Hauswald 41

Conclusions• Markets are reasonably efficient

– evidence supports weak and semi-strong forms of market efficiency but not strong form

• Implication for trading: to make excess profits– need information no one else has, or– ability to process available information much better

• There are market anomalies, BUT– little evidence that they produce large dollar profits consistently

after adjusting for risk and transaction costs– many an "arbitrage strategy" is NOT riskless!

• Implications: beating the market is hard, so– do your homework: get information first and diversify– avoid transaction costs, minimize taxes, corporate governance

1/25/2011 Market Efficiency © Robert B.H. Hauswald 42

The Take-Away