a simple approach to determining the super-efficient

TRANSCRIPT

Journal of Business & Leadership: Research, Practice, and Journal of Business & Leadership: Research, Practice, and

Teaching (2005-2012) Teaching (2005-2012)

Volume 4 Number 1 Journal of Business & Leadership Article 2

1-1-2008

A Simple Approach To Determining The Super-Efficient A Simple Approach To Determining The Super-Efficient

Investment Portfolio Investment Portfolio

Jeff Grover Dynamics Research Corporation

Angeline M. Lavin University of South Dakota

Follow this and additional works at: https://scholars.fhsu.edu/jbl

Part of the Business Commons, and the Education Commons

Recommended Citation Recommended Citation Grover, Jeff and Lavin, Angeline M. (2008) "A Simple Approach To Determining The Super-Efficient Investment Portfolio," Journal of Business & Leadership: Research, Practice, and Teaching (2005-2012): Vol. 4 : No. 1 , Article 2. Available at: https://scholars.fhsu.edu/jbl/vol4/iss1/2

This Article is brought to you for free and open access by the Peer-Reviewed Journals at FHSU Scholars Repository. It has been accepted for inclusion in Journal of Business & Leadership: Research, Practice, and Teaching (2005-2012) by an authorized editor of FHSU Scholars Repository.

G rover and La vin Jo um a l o f Bus iness & L~,ld ~ r,; hip R~s~a rc h . Praclr ce and Teac hin g

"oos. Vo l 4 . No . 1. 1-9

A SIMPLE APPROACH TO DETERMINING THE SUP ER-EFFlCJENT INVESTMENT PORTFOLIO

Je ff G ro ver, Dyna mi cs Research Corpora tion Angeline M. Lavin , Uni vers ity o f South Dakota

This paper presents a simple approach to !Hod ern Portfolio Th eory that makes th e process m ore understand able and accessible to students. Th e m ethodology is a jive-st ep process that hegins ll'ith th e calculation of m ean return s, excess returns, betas, unsystematic risk, and excess returns over beta and th en ~ystematically rank s a set of funds to determine a super-efficient optimal portfolio. Data from th e TIAA -CR E F family of funds 1va s employed in thi s stud y but th e analysis

can be applied to any distinct set of mwua/ funds. Thi s linear optimizati on m eth odology, based on the Elton, Gruber, Braum and Goet:ma11n (2003) m ethodology, is a straightfon vard tool that can he use d to teach stud ent s th e un de rlyi ng

constructs of modern portfolio theOIJ ' because it enables th e stud ent s to learn by pe1jorming th e analys is th emse lves. Thi s rese ar ch 111ill also benefit mlllua/ fund investors because it can he widely applied to h elp in vestors m ake better asset

allocation decisions.

Since Markowitz first o ri g inated the concept of port fo lio inves ting in the la te 1950s, portfo lio theo ry has ex ploded . Although Markowitz's mean-variance (M V) optimi za ti on is conceptua ll y intuiti ve, the process is computa ti ona ll y co mpl ex. Despite it s co mplex iti es, meanvari ance optimi za tion is a fund ame nta l building block of portfo li o theory, and it is impo rtant fo r s tudents to understand bo th the theo ry and process behind portfo li o optimiza tion. As more so phi s ti ca ted so ftware and more po werful co mput er resources become ava il abl e, the nature of optimization continues to inc rease in co mplex it y. Pro fess iona l fin ancia l consult ant s , ri sk ana lys ts, and academi cs continue to push the fro nti ers o f portfo lio optimiza tion knowledge and theory, caus ing the process to become even more co mplex from the po int of view o f a student leaming the materi a l fo r the firs t tim e.

Optimiza tio n teclllliques are difficult to s implify and teach in undergrad ua te finance and inves tments courses, which oft en mea ns tha t finance s tudent s are no t exposed to problems that require MV optimi za ti on. This paper illustrates how an ex isting s implifi ed linear approach to optimiza ti on can be adapted to teach the co nstruc ts o f fund selection and portfo lio optimi za tio n using an integrated framework . The intent is to c learl y expla in the inte rre la tionship of the three uni fy ing cons truc ts in portfo li o optimizati on (the Markowitz Po rtfo li o Model (MPM ), Modem Portfo lio Theo ry (MPT), and the Capit a l Asse t Pri c ing Model (CAPM )) so that students o f fin ance can be tter understand them in the contex t o f a risk and expected re rum marke t environment. The unique feature of thi s study is the development o f a s imple mathe mati ca l process fo r evaluating bo th fund va lu ati on and portfo li o optimiza ti on s imultaneously. S ince the CAPM is a linear process, its ri sk and rerum re la tio ns can be es tablished in linea r assoc iati on with each o ther, and it can be used to demonstra te fund eva lua tion due to its simpli c ity. A lthough Sharpe ( 1972) simplified Markowitz's MV optimizati on by us ing the

assum ptio n o f a ri sk-free securi ty co mbined with the Sharpe Ratio max imi za ti o n methodo logy, co mplex ity is stil l inherent in the p rocess, whi ch prese nts a lea m ing constrai nt to stu dents.

To reduce co mpl ex it y, the opti mi za tio n construct ca n be demo nstrated by utili z ing the eq uiva lent mean-be ta computed op tima l po rt foli o tha t Elt on. G ruber, Brown and Goetzmann (2003) deve loped and ex plai ne I. This si ngleindex model me thodo logy is parti cul arl y interes tin g because it enables the c rea ti o n of th e sa me optima l portfo li o as the S harpe 1972 methodo logy wi th minimal lea rnin g co nstra ints . Elton e t ~d (2003) demonstrate an optima l procedu re fo r port fo lio selection as an a lte rnative method for the co mplex it y of fo recas ting the covariance s truc ture of re tums. Firs t, they present a rankin g crite rio n to ra nk securiti es se lected fo r the optimal portfo lio and then d iscuss employing the ranki ng methodo logy to fo rm the optimal portfo li o. In addi ti on, they prese nt a demonstrat io n o f the linear process to use in fom1ing the opt imal portfo li o. Thi s method e lim ina tes the need fo r non- linear optim iza tion .

Thi s p 1e r rep li cates the demo nstra ti on fro m Elton eta! (2003) us ing se lec ted fund data in a format that is accessible to s tudents and has the po tenti a l to enhance c lassroom leaming though hands-on app lica tion. The unique co nt ributi on o f thi s paper is the va li dation o fthe Elton et al (2003) methodo logy with the standard Sharpe ( 1972) max im ization optimi za ti on technique, which is the benchmark fo r portfo lio opti mization .

PO RTFOLIO THEORY

T he Markowitz Portfo li o Mode l (M PM ), cap ital marke t theory (CMT) . and fund pric ing are the three sub-cons truc ts th at comprise MPT. Markow it z ( 1952) bui lt hi s port folio mode l on seve ra l assumption · with respect to in ves tor beha vio r: (I) in ves to rs co ns ider a ltem ati ve in ves tme nts based on a log- norma l p robabi lity distri buti on o f re rum s, (2) inves to rs ma xtmi ze o ne- period ex pected uti lit y and the ir

1

Grover and Lavin: A Simple Approach To Determining The Super-Efficient Investment P

Published by FHSU Scholars Repository, 2008

Grover and Lav in

u11lit y curves demo ns trate dimini shin g marg ina l wea lth , (3) investo rs es timate portfo li o risk on the bas is o f va riabi lity or re turns, (4) in ves to rs make in ves tme nt decis io ns based so le ly on ri sk and expected re tu m , (5) and fo r a g iven leve l o f ri sk, In ves to rs p refer hi g her re rums.

T he M PM o pe ra tes in ri sk-expected re turn space. The ex pected ra te o f re turn fo r a po rtfo li o o f in ves tme nts is si mpl y the weighted avera ge o f the respecti ve rates o f re turns o f the indi v id ua l in ves tments in the po rtfo lio, and the Markowit z po rtfo lio standa rd devia tion is co mputed as a fun c ti o n of the weig hted averages o f the indi vid ua l va riances sq uared plus the weighted cova ri ances be tween the fund s in the po rtfo li o. Equa ti o n I is kJ1 own as the no n- linear q uad ratic func ti o n Markowitz ( 19 52) standard dev iati o n:

N N N

CT~ = I(x,2CTn+ I I(x,x1CT,J ( I ) i ,. J t= l j = l k~t

where, _I(, = the we ight of va ri able i or j, CTu = the

covar iance o f vari:-~bl e i wi th j , and CT,2 = the va ri ance o f

va riabl e i.

a. T he Efficie nt Frontier. The e ffi c ient fro nti er is the co mb1na ti o n of fund s tha t has the max imum re tu m with the minimum level of ri sk. T he concave effi c ie nt fronti er fun c ti o n is den vcd from the quadratic equati on fo r the s tandard deviati o n as reported in Equa tion ( I) . A n infinite number of we ighted portfolios lie benea th this fro nti er. In ri sk-ex pected re turn space, the p011fo lios o n the fro nti er domin ate those b<' low the frontier. The fronti er is de fin ed s tarting wi th a minimum va ria nce p011fo lio a t the bo ttom le ft o f the arc and ending w ith a m::tximum re tum po rtfo li o at the to p ri ght o f the arc . The dominant o r tange nt po rtfo lio li es bet ween the two e nd points of the a rc and has the attribut e or max imum re turn fo r a minimum leve l o f ri sk. In ves tor utilit y theo ry s uggests tha t a ll in ves to rs wou ld se lect thi s tangent portfo li o because o f thi s charac te ri s tic. MPT is a na tural extens io n o f thi s co ns truc t. A ll po rtfo lios o n thi s fro ntier are e !Ticicnt but the tan gent po rtfo lio is " sup e r effi c ient" beca use it provides the in ves to r with the g rea tes t re turn fo r the minimum amount of ri sk.

b. Moder n Portfolio Theot-y. MPT ex tends the MPM by inc luding the fo ll owin g additional ass umptio ns co ncerning investors: ( I) in ves to rs arc Markow it z e ffi c ient ::tnd pre fer target points o n the effi c ient fro nt ie r, i.e. , they ca n se lec t uni que levels o f ri sks, (2) in ves to rs pre fer the tange nt po rtfo lio , (3) in vesto rs can bo rrow at the ris k-free rate , and (4 ) the capi tal marke ts are in equi librium . Introduc tio n of the ri sk- free asset is an impo rtant dis tinc ti o n o f MPT. The riskfree asset is unique in tha t it ( I) has no ri sk, (2) docs not corre la te wi th ri sky assets, and (3) li es o n the expected re turn ax is in ri sk and expec ted re turn space. T he cova riance of the ri sk-free asse t w ith othe rs in a po rtfo lio o f ri sky assets is zero. The standard devia ti o n o f a po11 fo li o that co mbines the ri sk- free asset wi th ri sky asse ts is in linea r pro porti on

2

Joumal of Business & Leadership: Research, Practi ce and Teaching 2008, Vol. 4, No. I, 1-9

with that o f the risky asse t po rtfo lio. Given the addition o f the ri sk- free asse t, the ray, repo rted in Figure I , can be drawn fro m the ri sk-free asset to the e ffic ient frontier due to the linea rity im posed by the conditio n that the risk-free asse t has a zero standard deviati o n. When this ray is drawn tange nt to, o r ex tends to the fro ntier, it touches the super e ffi c ient po rtfo lio , whi ch aga in domina tes all others in riskex pected return space. Bo th risk and expected return increase in a linea r fashi o n a lo ng thi s ray, which beco mes know as the capital a lloca ti on line (CAL). When the tangent po rtfo lio is the marke t portfo li o, it becomes the capital market line (CML), whi ch beco mes the new frontier. The CA L and CML a re both linear models, and their expected re l'urns are deri ved by adding the standard deviation of the ri sky po rtfo lio times the marke t ri sk marke t premium of the ri sky po rtfo li o to the ri sk- free asse t return .

c. Cap ita! Asse t Pricing Model. A natural ex tens ion o f the CM L is the security marke t line (SM L) , in troduced by S harpe ( 1972), whi ch va lues the ex pected rel'um o f indi vid ua l funds in re lati o nship to those that make up the marke t portfo li o o f a ll kJ1own fund s. By ex tension, subst itu ting the sta ndard deviati on of the combined po rtfo lio o f fund s w ith the covar iance o f the indiv idual fund with the marke t po rtfo lio, the CAP M ca n eva luate these funds re lative to the marke t 1 n tf oli o. The ex pec ted return is the ri sk- free return p lus a marke t ri sk premium multipli ed by the cova ri ance fac tor (beta). T he ac tu al re turn ca n be compared to the expec ted return to determine if the fund' s ri skadj us ted return is underva lued , properl y va lued, o r overva lued re lative to the marke t port fo lio.

Optimizatio n is a rare econom ic phenomeno n tha t ex is ts onl y when a portfo li o is es tab lished in ri sk-expected return space so that the optima l fu nd mi x resu lts in effi c ient po rtfo li o re turns, or a portfo lio that provides the hig hes t re turn fo r a g ive n amo unt o f ri sk. Capital a ll oca tio n across different fund c lasses is a key in ves to r dec is ion. A lthough theore tica ll y appea li ng, the Markowitz methodo logy, which is quadratic in nat ure, p resents com puta tiona l constraints that make it diffi cult to app ly in prac tice. M arkowitz's c riti ca l ins ight was the rea liza ti on th at the co- move ment o f funds wi th each o the r is mo re impo rt ant than indi vidual fund cha racteri sti cs when forming a po rtfo lio o f nmds.

Elton, Gruber, and Padberg ( 1976) attempted to opcrationa li ze MPT, whi ch a lthough mea nt to be a prac tica l too l, had primari ly developed as a no rmati ve, theore tical cons truct. They sugges ted th at the implementatio n diffi culties fo r portfo li o ma nagers were caused by the fo ll owing: ( I) es tim ating the corre lati on matrices, (2) the time and costs in generating effi c ient quadra tic po rtfo lios, and (3) the necessity o f unde rs tand ing th e ri sk-return tradeo ffs ex pressed as co-va riances and standard deviations.

T his paper provides a prac tica l appli ca ti on o f the s ing leindex linea r mode l proposed by E lto n, G ruber and Padberg ( 1977) that sa tis fi es the o rig in a l conditiona l boundaries of the Ma rkowitz mode l. T his s ing le- index model uses the

2

Journal of Business & Leadership: Research, Practice, and Teaching (2005-2012), Vol. 4 [2008], No. 1, Art. 2

https://scholars.fhsu.edu/jbl/vol4/iss1/2

G rover and Lavin

re lationship between a s in gle market index and a s ingle security in de termining va luati ons and portf oli o e ffi c iency. Sharpe (1994) confirmed the abilit y of his S harpe ratto to identify the optimal portfolio out of a population o f random portfolios. The ab ilit y to eva luate multipl e capital c lasses . with speed and ease is an espec ia ll y benefic t ~ l c haracten sttc of thi s methodo logy. The empirica l inten t o f thts s tud y IS to detennine the optimal portfo li o co mbinati on o f a des ignated portfo lio of fund s utiliz ing the portfo li o optimi za:io n construc ts disc ussed above and den ved fro m M P r.

METHODOLOGY

Current Practitioner Limitations

A search of current software tha t a llows fin ance student to perfom1 optimization teclmiques re turned a limited number of cost e ffecti ve po rtfo li o optimiza ti on services. T he methodology proposed in thi s paper seeks to overco me these limita tions by fo llowing the Elton, e t a l (2003) linea r methodo logy to provide a user-fri endl y algebrai c a lgorithm combined wi th an eas il y adaptab le Mi croso ft Exce l spreadsheet app li cation. The int ent is to have the student download monthl y fund c los ing pri ces fro m T IAACREF.org or another mutual fund pro vider and monthl y risk-free rates and market index c los ing pri ces fro m a so urce such as finan ce.yahoo.co m.

The method presented in this paper does no t req uire quadratic (Jackso n and Staunt on, 1999) or s impl ex optimi za tion eng ines to obtain optimal co nvergence. Se lec ti on o f the po rt fo li o with the max imum Sharpe Ra ti o inherentl y acco mpli shes the sa me objecti ve as the optimiza tion teclmique if the po rtfo lio holder chooses the portfo lio wi th max imum re turn and minimum ri sk. Furthermore, thi s method a llows fo r the in c lus io n of severa l fund s in the analys is, whi ch ex tend s the two-asset exa mple developed fo r c lass room usc by Am o ld, Na il and N ixo n (2006).

Fund Family Selection

The T IAA-CREF famil y o f funds was se lected fo r tl1i s eva lua ti on. TIAA-C REF is a major provide r o f defined contributi on retirement plans to the academi c co mmunit y. Rugh (2003) reports tha t TI AA-C REF is tl1e larges t pens io n provider in the U.S ., manag in g $300 billion in to ta l assets for more than two milli on indi viduals. The p lans, whi ch are provided through the e mpl oyer of the respecti ve in ves to r, a re referred to as retirement (or g roup re tireme nt ) annuit y contracts. In ves tment amounts a re dependent on co ntrac tua l agreements betwee n the empl oyee and e mpl oyer and are specifi ed in the contract. Typica ll y, co ntributi ons a rc made on a tax-deferred bas is, whi ch means that pre- tax do ll a rs fund the accounts, but the employee pays taxes o n wi thdrawa ls. The info rn1a tio n was obt a ined fro m the T IAAC REF websi te, www.tiaa

c ref.org/perfonnance/retirementldata/i ndex. html . (Note: thi s web location is subj ec t to be ing moved).

3

Joum 31 of Bus iness & Leaders hip : ResC3 rch. Pracu cc and Teachin g 2008. Vol 4. No. I . 1-9

Sim ple Techniques for Determining an Optimal Pot·tfolio

This mode l will use the s imple teclmiques of Elton, e t a l (2003) to de termine an optima l portfo li o. Impli c it in this process is the identifi catio n of undervalued fund s acco rding to the paramete rs o f S harpe's 1972 s ingle- index CAP M. The identifi ca ti on o f these fund s is inherent in the Elto n, e t a l. ( 1976) me thodo logy, whi ch makes it very c lea r why a f1md does o r does no t ent er into an optima l portfo lio. The Elton methodo logy ca lcul a tes mea n returns, excess re rum s, betas, unsys tema ti c risk, and excess re turns over beta and then syste mat ica ll y ranks the inc lu ded securiti es to detem1ine an optima l portfo li o. The e limina ti on o f overva lued funds and the optimiza ti on o f underva lu ed fund s are inherent in th is ranking process. Thus, the CAPM is the benchm ark fo r fu nd inc lus ion.

Review of Fund Va luatio n using th e CAPM 1\lethodology

The va lua ti o n process as de termined b y the CAPM is impli c it in the Elt on, e t a l (2003) optimi za ti on process. The

CAPM is de fin ed as E(R) = R1 + /3, (Rm - Rr ) , wher e the

ex pec ted return equ als to the average risk free return plus the prod uc t o f the beta of fundi and the diffe re nce in th e average m arke t re turn min us the average ri sk free re turn . Il e re, fund va lua ti on is s im ply de te rmined by two fa cto rs: ( I ) the expec ted o r marke t de mande d re turn Gnd (2 ) the rea li zed re turn o f the fund . If the rea lized return is g reater ( less) th an the ex pected re turn , then the fund is und erpri ced (overpri ced) . If th e two re turn s a re eq ua l, then the fund IS

properl y pri ced .

Formation of the Optimal Portfo li o

T he portfo li o fo rm at io n proceeds by construct ing a rankin g syste m using a s in g le co mputed number to de tem1ine the fund s that s hould be inc luded in the optimal po rtfo li o . T hi s process utili zes the assumpti on th:ll the s in gle- index mod el accura te ly descri bes the co- mo\'e ment be tween these funds, and thi s descripti on can be de ri \·ed us in g a s ingle number (beta) as the unit o f measurement. Thus, the ci t irabi lity of any fund is di rect ly relat ed to its excess re t11 rn to beta (Treynor) rati o. The excess re turns are measured by the difference be twee n the expected return o n the fund and the ri sk- free ra te o f inte res t, as measured by the 13-week Treas ury bi ll . This rati o measures the additi onal re turn on the fund (beyond tha t o flered by a risk-free asset) pe r unit o fno ndivers ifiable r isk. The form o f this ra tio makes it easy interpre t and has led to its wide acceptance b y in ves tors as a n exp lanat ion of the re latio nship be tween ri sk and rewa rd . T his is known as the Treynor measure ( 1965) and is illu stra ted tn Equa ti on 2:

(R., - R., ) fJ,

(2)

3

Grover and Lavin: A Simple Approach To Determining The Super-Efficient Investment P

Published by FHSU Scholars Repository, 2008

rover a11d l:lV in

wh<..:rc, R; - th e expected return on fund i, R J = the return

on a ri sk- fr ee fund , and f]; = the expected change in the rate

o f r<..:turn on fundi as~oc iat cd with a I 'X, ch ::~ n gc in the market index rate of return .

Thi~ excess re turn lo beta rati o (Rati o) ranking represents the dcs ir:lbilit y o f an y fund in a portfo li o. Therefore, if one fund with 3 certa in Rati o is included in an optimal po rtfo li o, all others with a hi gher ratio would a lso be inc lu ded. Conversely, iflunds with hi gher Rati os arc exc lu ded, then fund s with lower Rati os are exc luded. Since th e sing le- index rn de l is :l s~umcd to represent the cova ri ance structure of the fund s for thi s s tud y, fund s will be inc luded or exc luded acco rding to thi s Ratio . The quantit y o f fun

ds se lec ted will depend on ::1 uni que cul -o ffra lc such th at

fund s with hi gher ratios arc in c luded and those with lower Rati os arc exc lu ded.

Rules for Po•·tfolio Inclusion

T he fo ll owing rul es or co nstra int s w<..: rc used to dclt.:r min <..: whi ch funds to inc lude in the optim:ll portfoli o: ( I) determine the rati o for eac h fund in th e fund l~ mil y and ra nk from highes t to lowes t and (2) cs t::~ b l i s h th e optimal portfo li o that co nsists o f inv <..:s ting in a ll fund~ for whi ch the ra ti o is grea ter than a parti cul a r cut -o iTpo int. T hi s is done by rankin g the sec ur iti es in ascendi ng order by the Ra ti o. Once ranked, these va lues arc th <..: n compared to the cul -o lT rat c, which is dctcrrni11Cd by inspec ti on. Those fund s with v::~ l u cs

<..:qua l to and above the cut -o ff rate arc i11 c lu dcd and th ose less th <1 n the cut -o fT rate arc exc luded fro m the ca lcul a ti on process. O nce th e inc luded st.:curiti cs arc de lcnnin cd, an optim al po rtf oli o mi x o f thc~e fund s is determined. T he dt.: tcnnina li n o f the cuto fTpo inl lo r fund in clusion versus exc lusion is described as part o f the fi ve-s tep process in the fo ll owin g secti on.

PRA C'l ' ICUM

To illustrate the methodology, the fi ve-s tep p roccs~

( in c lud ing sub-steps) used to constru ct an optima l T li\J\ C REF VJ ri ab lc annuit y retirement fund po rt fo li o is ex plained

in th1 s ~ee l ion. The T IAJ\ - 'REF fund s include th e T li\i\ Rea l Es tate fun d and th e C REI: Global , Soc ial, Stock,

Eq uit y, Gro wth , lnOati on-lin kcd Bond , Money Market, and Bond h111d . T he Rus~c ll 3000 (ARUA) was selected as the

mark et index, and th e C hi cago Board Options Exchange ( ' 130 1~) index (1\ IRX), JS the 13-Wcck TrcJsury- Bi ll . T li\J\ -C IZEF used th e Ru ssell 3000 as its benchmark non d1V1dcnd-y icldi ng index, and th e T IAA-C REF fund s do not product.: d ividends. T he AJRX Treas ury- Bi ll Index was se lec ted because it reports actual annu a l di sco unt ra1cs, whi ch makes th e co nvers ion to monthl y return s slri.l ightfo rwa rd. Ex planati on o f the fi ve s tep ~ in the process fo ll ows :

4

Joumal of 13u sin css & Lcackr ship : Resea rch, Pracli ce and Teaching 2008, Vol. 4, No. I, 1-9

S tep I

The 6 1-beg inJling o f the month clos ing prices from Decernbcr 200 I 10 December 2006 fo r " RUA and 1\ IRX ind ices were eo ll ec ted fr m fin ance.yahoo.com and the T IAA -CREF retirement fund family data from www.tiaacref. org. The data was uploaded into Microso ft Excel and 60 months o f lognormal returns fo r " RUA and for each TIAACREF fund s were computed us ing Equati on]:

In [~)* 100 S,_l

(3)

where, S, is th e fund c lose pri ce al tim e I and S,_1 is the

price at 1- l . The ave rage ri sk- free rate, /? f, was co mputed

by co nvertin g annua l d iscount rates lo monthl y di scount rates by d ivid in g eac h annua l valu e by 12 and then

averag ing the monthl y ra tes to determine R1 using

Equ ati on (4) :

N /? I I I / 12 f~ l

N

whi ch i ~ the average ex p<..:eted relum on the risk-free fund

where /? r = th e average di sco unt rat e o f th e I ]-wee k U.S .

T rcnsury- Bi ll usin g th e same da le ran •c of the fund s.

Step 2

(4)

The average mea n returns ( R;) fo r each fu nd i and the

market index, 1< ,, art.: co mputed from the In rclums using

Eq uati on 5·

R /,f/ 1

(5)

N

where R; = the ex pec ted rc l.um on fun d i and R,. = the

average ex pected return on th e market in dex m, " RU A, and N = number of obsc l-va li ons. T hese values were computed and reported in Range 13 3: 8 I I in Tab le I .

b. Covariances of each fund with the market index, 0',~ ,

arc co mputed as 0',2; = 0'} - J3/ 0',;,, whi ch is the variance

of fundi minus the product o f the beta squared of the fund

and the va ri ance o f the mJrk c l index. Note: II ere, CT ~ is

co nsidered unsys temati c ri sk. (Sec Elt on c t a l (2003) pp. I 34-35 for an ex planati on and fo rmal proo f lo r the

4

Journal of Business & Leadership: Research, Practice, and Teaching (2005-2012), Vol. 4 [2008], No. 1, Art. 2

https://scholars.fhsu.edu/jbl/vol4/iss1/2

Grover and Lavin

computa tion o f CJ :; ). Co variances for each variable with the

Russe ll 3000 marke t index were computed and reported in the Range C3: C II in Table I.

2 (} .

c. Beta, /3; = ---f , or systematic risk, is co mputed as (Jill

the covari ance o f the fund w ith the marke t di vided by the variance o f the marke t. The be ta fo r each fund was computed and reported in the Range 0 3: 0 II in T able I .

d . Marke t Premium, Mr. is computed as (R, - R 1 ) ,

where R; = the average re turn on fund i minus the average

risk-free ra te o f rerum. These va lues were co mputed and reported in the Range E3:E II in T able I.

e. The Capita l Asset Pric ing Mode l (CAP M), Rcmr , is

computed as R 1 + A1 p * /3;, the average re turn o f the ri sk

free asset plus the product o f the marke t premium and the beta o f asse t i. These va lues were co mp ut ed and reported in the Range F3 :FII in T able I .

f. Market index vari ance, uJ1 , is co mputed as in

Equa tion 6:

(6)

where m = popula tion mea n of a marke t index and R; = ith

value o f re turn R, a nd r. ;~ 1 (R, - R111

)2 = summ ati on o f a ll

the squared diffe rences between the R; values and m . The

computed va lue of 12.9 46 is reported in T able I.

Step 3

a. X 1 is computed as X 1= CJ;, , unsystemati c ri sk, o r the

vari ance o f a fund 's move ment that is no t assoc iated with the movement o f the marke t index. These va lu es are reported in the Range G 3:G II in Table I .

R; - R1 __ ____.::..__ , the market

/3; b. x2 is computed as x2

premium o f fund i di vided be ta . These va lues a re reported in the Range H3 :HII in T able I.

Step 4

This step beg ins by so rting X2 in descending orde r so that the max imum row value is the s ta rting number o f the co lumn. Then, the fo ll owing s teps are taken:

5

Jouma l of Bus1n ess & Leaders hip : Resear ch, Practi ce and Teachi ng 2008 . Vo l. 4 , No. I, 1-9

. (7?, - R; )/3, a. XJ ts co mputed as X1 =

1 , the ma rket

u;, premi um mult ip lied by the be ta o f fu ndi di vided by X1. T hese va lues are reported in the Range 13: !7 in Tab le I .

b X . · d X /3,2

I b f ~ . . 4 IS co mpute as 4 = - ?- , t 1e e ta o ,u nd 1

(5 ; ;

squared , di vided by X1. T hese va lues are reported in the Ra nge 13 :17 in T ab le I .

X . d ~ (7?, - R r )/3,

c. 5 ts co mpu te as X5 = L... 2

, the surn o f } = I C5 e;

the product o f the marke t premium and the beta o f fundi d ivided by the cova ri ance o f the fund wit h the marke t index . T hi s fun cti o n is cumul ati ve where it beg ins wi th the initi al row va lu e and then c umul a tes subseq uent va lues o f X3.

T hese va lues are reported in the Ra nge K3:K7 in T ab le I.

d X . d ~ /3,2

I . h . I I . . 6 IS compute as L_. --:2, W 1\C IS t 1e CUlllU at J\ 'e

;= I (J" ej

sum o f X4 from j = I to i. T his fun c tion is cumul ati ve w here it beg ins with the in it ia l row va lue and then cum ulates subsequent va lues o fX 4 . T hese va lu es are rep011ed in the R:m ge L3 :L7 in Tab le I.

e. Co mpute C *:

I . Calculate C, , whi ch takes the fo rm as prese nted in

Eq uati on 7:

C, (7)

\vhere 0",;1

is the variance of the nu1rk ct index and a-~ is

the unsys tet na tic ri sk. T hi s func ti on is the produc t o f the va ria nce o f the ma rke t ind ex and the sum o f X1 divided by

o ne p lus the produ ct o f u,;, and Xr,. These va lu es are

reported in the Ra nge M3:1'v !7 in Table I .

2. De termi ne C* , which is computed by e \·a lu ating

co lumn M fo r the fu nd w ith the hi ghes t C, va lue. The

da ta in co lum n M has a lread y been ordered us in g the ru les fo r portfo lio inc lus ion JS described pre\' ious ly. C* is the des igna ted brea k po int fo r fund inc lusio n in the op tima l po rt fo lio . Fu nds tha t were equal to and above C * in co lu mn M were re tained , and fu nds that were be low C* we

re e limina ted fro m the portfo lio . r o r this se t of dJta,

the hi ghest fund va lue , C*, was 0.688. The C, va lues are

reported in Table I .

5

Grover and Lavin: A Simple Approach To Determining The Super-Efficient Investment P

Published by FHSU Scholars Repository, 2008

( •l t , v n .t1u l l .t \ ' 111

Sit·p S ( 'ou \fl'lr r f Opfiu ral l'or ·ffoli o

( 'o llljlllf l' / ., ,111d .\ , /\ ff l ' l ( ' l IS t k fc lllllllL' d ;111d fil l'

''"'"

' ' " ' I

L' I ' 11110 11 Ill III L' ll fllllll . d IHHihdi ll :Il l ' ld l' lllii 'IL' d , i l ll'

111 \' l' ~ llll\ ' 111 jl l'

i l '

l' lll :lgL· P I fil l' IL' I :IIII l' d lilll lf. S IS c: d c u i ;IIL' tf b y

''" "fllllll i ) ', /, :1s s l 1oW 11 111 hlu:illl >ll X

N I ) /.,

Jl, ( (1<, () .', fl, ( 'l (X)

\\' li l' ll' /,IS lfJL' f11 lldll t' l ll f'l l it' fll' l : i o l ILIIItf 1 d1 Y11fc: d IJ y J\ 1 IIHillipli L'

d hv I I IL' ddki cll l 'l' ill' l \ l 'L'l'll X,. : 111d ( ' * . \\' l11 c li 1s IIH·

lii

) '

li L·s l ( ·, v; il u L· I il l· IIH I IVIdii .d / ., \ '; iluL'S :li t' IL' fH ll ll'lllll 11i c

ICiii ) ',L' Nl N 7 .111d lliL' II ''"""' c d l o /,will II'' l l' l)(\ lf nllli

ll' ll

X

111 l .d 1k I

l dl' ll lill c: il lll ll o f 1l 1e I : lll )~l' lll l 'lll li ol1 o . .\ ,, lli l'

fl l'

l l

l' lll :l)'.l ' Ill 111 \'l'S I Ill L':IL II l1111tf , I ~ L' l llllfll il l'l l USIII )'

lqll

.

ill ll /1 1)

IOtuu.d ,, 1 Hu ..., ln t.'"" & I e.td l· "'l up R ~..· :-.t.:. u L. il , l 'r :u.: ltc ·and '!\ :at.:l tt ll )'

•. OOX. Vo> l ·1 . No I , I 1)

% X

J (0) I ~ -, uulr11ltd

w il L' ' · L': lc l l /.,, h11 1

111 tf1

Y

idu :d /, v; ii(I L'S h tu :il ll lll ( 1J) d e i L' IIII ill eS lli e Je l :iii Ye

III

VCS

IIII elll lll l'; l rli lund , Wli l' ll' l l i l' \Ve lg lli .S Oll lli e i11di vid u :d

llli lll

s

'" '"' S\1111 I ll l\ IIC IO l' ll ~ lll l' I OO' Y, , II I YeSI III 'Ill

II

IS

111lf1ll il .llll Ill 111\ll' lli a l I IllS :lli :J i ySI S I · l 1es Oil lh e

.IS~ lllilflli ll lllli , illli L:

p :ISI

V: lll ;lll lC lllV: II I:II ICl' Sliti L: Illl e o f

lli

L·s,· IUI I( I s

\\' ill coll llllii C /lilli e' luliii L' . ' I li e X, v :du cs :1re

I C fl llli l'l llll I il l' l { : ll>ge () ) ( >7 I ll I ;dJk: I . w hil e I li e Sl/111 or '"L' .\' , ·, ' ' ll' lllll il' d "' LL· II (> X I tl dlu~ 1 1 : il c ! Iies e

(' iil l' til dillli\S , /, " \\' <I S ('() lllfll il l' d : I ~ ! ,, X

()()11

/

(0 . .1\'/ *((> ·1 :o I 0 r, x~ )) :IIHII L' fl ll i l c d "' Ce ll N1 . T h e

v;du

c

.\ 'ol IS l OII l lliii L' tf ;1.s () 1) . 1(, ) ~· I X /.1 (> 1)-1 :111d l e flO il c d

111

(

'v ii () \ 111 l .1hk I /\s SII )' ) 'L'.\ Il'l l h y l ·ll o11 , L' l a l (_()0\) ,

! Il lS Stllllilllll \\ Ill hl' l d L'III IL: il h illi l' le'S UII s :Jl lll l'I'L' tf b y

ljll:idl ,ill l lli ll )'l :lllll lllll )'

'J':Jitil' I : l'r a r li <'tllll l{ l'\11 11\

It I) II ~ · N ()

Slop S11·p S1vp I :-, il' p 'i ~ l l' p o;

'·• .,. I I

\ , IJ l .t!Ji l' li ( . I . \ ' ()

~ ~· IC "''t ,\ \,, J

11.\i\ 1\t·. ol hl. i ll' ll X 1.1 lll ol ll II 'll'i II >I/ (1 1111 1 1111' 1 11111111 1111. 1 1 11111111 111 1'1 I ' I X 'l· l 'iH" ,

( ' 1(1 1· ( ,)p!J ,tl 11/11 l j,,., 111'1'1 II 'i 11 1 II.' 'i'l Ill X II l(,(l() III II II II IIII I 0111· 1 II IIII I 11 1111 1111\(, 11 '1 ",

1 '1(1 1 Sm t . .! 11 '1' 1 •1 0'1 1 II I ii.' 0 1.'.' 0 .' IX I \\1 I '1'111 IlOilo IIIIIIX 1)(1'1(1 IIIII' II 'i '" llllio\ ~ 1 'i" "

( ' !(I I Sl11r k (1 () /1 '-1 111h 11.'1·1 () lh.l () >j,q 'l X 1\ I 'l II 011 11 lllllllo ()I)(, I 011 1 / Oh· l ' Ill) 11 I 1·1",

( ' 1 (1 ·1· "'t '"' Y ll ~· I ' \ '>.'X 0.'/ \ 111 ·111 0 .'XIl 'I ·IX I 1 .1 1/ II II II I 0 OOS 1)(1/1 III JI) II loXX llll llo (1(,[)",

( !(I I ( 11 \1\\ lh 011'111 ·I //X II lio'l II 11 1 II \1 1/ l 'llllo II IIIIo Stq• I ,. , II ioXX 1(,') 1 I Ilii OII",

( '1\ 11 II Hn11d II '\'ill I ll}ll II II III II I I / 11 1 / 1 \ 1.'/ l ·l ioX

Ill (!(I

I

t\ l n 1H·} II I XII 1111 .10 0011.' II II '1 II 10\ II IIII o 1 1 11.'

II

( ' 1

(1 ·1 Ho 11d II ·IIIX Il l (,(, 110 11 (I ,' () ) Il l ')'} I .'W I ._, ')X.1

I a hk I N ul' ' ' :

( I) I o~h lc I I" 11\ I t it- s I il l· : tL< tll lllil :ll lll ll ul' 1 li e· l' lll fllll l'. il ll' Sull s o f I Ill· pi .IL IIL 'lll\1 <'\l' l l l'<' II hq • 111 s \I 11 h Sll' p • hv t. d c u l. illll g

,I\ L' l oi ) ' e· ll 'ltiiii S l11 1 t': ll II l u11d ;u1d c 11tl s Willi Sll'p ') h y t'll ll l fli llllt ) ' I hL· llfl lllii ,d f' ll ill ll lll l 11 L' l )' Ii i.\ l o 1 I il L' s · ln ln l I 1111ds ilf !li t '

l l t\ t\ ( ' 1 ~ 1 · 1 · I III II I

( 1 ) S i l' p .) lt \1\ .S IS i s o l llt l' l o ll ll \\' 11 1) ~

S i v p .1: 1 , 1l1 v c: d rul.ill (l ll ll l'l li l' :1\ 'L' I :IJ' L' 111 :11 k c l (0 · I K')) .111d '"k II L'l' ll' IIIIII S (0 _)()\ ), :11 11ll lll· ii\ L' I ,I)'l ' ll 'ltllll S ollh c

lt111d s u l lhl' 11 /\ t \ ( ' 1.: 1· 1· lu11d s, N, ,

Sll' p .' h • 1 il l' c: d cul :tlll ' " u l 1 li e 111 :11 k L· f v: lll .lll l'L' ( I ! .1>·1(, ) . ,

S i v p .1 , , t. d rul :tli< \11 t >l lli c·t · i >V; II I:IIl l'l'S <> fll1 e l'u11d s \V illilll c lli:llkl' l lll tlv .\,0: .,;

6

Journal of Business & Leadership: Research, Practice, and Teaching (2005-2012), Vol. 4 [2008], No. 1, Art. 2

https://scholars.fhsu.edu/jbl/vol4/iss1/2

G rover and Lavin

Step 2.d ., ca lcul ati ons of betas, /J;; and

Step 2.e ., ca lculation o f marke t premiums, MP ; and

Step 2. f. , ca lcula tio n o f the CAPMs. Next, Step 3 consists o f the fo llowing:

Step 3.a. , the calcul ati on o f X 1 and Step 3. b ., the calculatio n o f X2 .

Nex t, Step 4 consis ts of the fo llowing: Step 4 .a., the ca lcula tio n o f X3,

Step 4 .b. , the ca lcul ati on o fX4 ,

Step 4. c ., the ca lcul ati o n o f X5,

Step 4 .d ., the ca lcul atio n o fX 6 ,

Step 4 .e .l ., the ca lcul ati on o f C, and Step 4 .e.2 ., the calcula ti on o f the maxim um va lue o f C,.

Nex t, Step 5 consists o f the fo llowing: Step 5.a., the ca lcul ati on o f Z, and

Joum ol o f Bus iness & Leo dership : Researc h. Practice and Teac hing 2008. Vo l. 4. No . I . 1-9

Step 5.b. , the ca lcul a ti on o f X; , which inc ludes the summi ng o f the Z,' s. (3) TIAA IL-B ond is the T IAA inOation-linked bond fund .

T he identificati on o f the super-effic ient or OIJtimal portfo lio mix for the T IAA-CREF funds is shown in Figure I , whi ch is integra ted with the e ft~ c i ent fronti er. T he fund weights of the super e ffi c ient portfo li o , using data from December 200 I to December 2006 , are as fo llows: T IAA Rea l Estate: 94 .58 percent , CR EF Socia l: 2.35 p rcent. CREF G loba l: 1.35 percent, C REF Stoc k: 1.14 percent , and CREF Equity: 0.60 percent, for a to ta l o f 100 percent. Oa tes

for tJ1e first set o f weight s Fixed . We used data from August 2003 to August 2008 to va li da te the s tabi lit y o f the mode l and we obtained s imilar results. T he we ights us ing the 2003-2008 data are the fo ll owing : T !AA Real Estate: 94.88 percent , C R.EF Soc ial: 2. 13 percent , C R.EF G loba l: 1.3 -1 percent , C R.EF S tock: 1. 1 I percent , and CR.EF Equit y: 0.53 percent , for a to tal o f I 00 percent.

Figure I: Effici ent Fronti er

0.82%

E o.81 % :::J Qi 0.81% a: ~080% ro

~ 0.8 0% <(

0.79%

0.47%

Figure 1 No tes:

•

• 0.47%

Efficient Frontier

• • • • •

0.48% 0.48%

Standard Deviation

( I) This is the effi c ient fronti e r with the tangent portfoli o shown.

• • •

0.49% 0.49%

(2) The percent ages are tJ1e portfo li o we ighted average monthl y re turn s on the Y -ax is and the Markowitz ( 1952) deri ved s tandard devia ti ons on the X-ax is as calcula ted using the s in gle-index linea r model. (3) The ray fro m the risk-free asse t to the super e ffi c ient portfo lio is not shown due to sca ling issues. T he average ri sk- free return is 0 .203% .

7 7

Grover and Lavin: A Simple Approach To Determining The Super-Efficient Investment P

Published by FHSU Scholars Repository, 2008

C..1 O\ c1 dnJ L. .Jv1n Joum.1l of Bu Si ness & Lcatk rshq1 R~searc h , PrJclicc and Teachin g 2008, Vol 4, No. I , 1-9

(-1 ) T hi s Exce l based supe r e lfi c ie nl portfoli o we1ghted th e T IAA Rea l Estate 9-1 .58%, the CREF Soc tJI :!.35°o. C R I: P G loba l 1 . 35~0 , CREF Stoc k 1. 1-l"u, an d CR.EP Equit y 0.60%, for a to ta l o f' I 00° o.

l'

o \'a

li date that thi s opttm almi x is indeed th e super l'ITi c tent port fol1 o, the s tng le- modeln on-lincar optimi zati on tec hn1que was performed, and the result s were identi ca l to th ose reported 111 Tab le I. T he opt imtzati on algo rith m is reported 111 1\pp end tx A.

SUJ\11\l AR\' AND CONC LUS IO NS

'I h1 s paper provides s trc11gh tf o rward co mputatt on:t l 1cs ults for an e fTic1ent T IAA -C REF port fol1 o o pt11 nal mi x of

funds

u ~ 1n g the Elto n. etc. al. , (2003 ) linea r optimi zat ion met hod. Us 1ng the co nstru cts o f MPf\1 , MPT, and CAPM , a tcJc h1ng too ltlt at e na b le~ the sea mless Int egrati on o f these co nstructs 1s pro\' tded. 'J he paper includes a ge nera l blended dtsc uss ton of' th ese tl1ree co n,tr ucts, bn efl y hi g hl1 ght s current researc h 111 MV opt tmi za tt on nnd fund \'alu atwn

me tlwds, \'a lucs fu nds from a se le cted fund farml y, cstabl rshcs a po rtfo lro mtx of these un derva lued fu nds,

lr nearly optr lllltes th ts por tfo lt o, and re port s the fin dtn gs. A no n-It near optr rn iZJ tt on a lgtm thm tha t \'a ltdatcs the linear mode l, wh rch IS a uniqu e co ntnbutt on to the fi e ld o f 1n1estn1 ent lt tc raturc, is a lso rnc luded. In add 1t 1011 to the 1n1tr :tl op tl lll iZa tto n result s, the po rtlo l1o was rc-opttmrzed us1ng cu rrent dc~ta, and the re-opttlll iZat lon y1e lded Similar

result s, 11 htch sugges ts mode l s ta bil11:att on.

r he Intent o f thi s paper \\'3S tO 0Ut fll1C J model th at opc ratJOna lt zes a sunp lis tt c approac h to MI'T T hi s me th odo logy ts n lin>s tcp process th Jt 1n c ludcs c;- dcul at mg

mean rctums, excess return s, betas, unsys temati C n sk, exce~s rc

tums O\e r beta, an d th en sys tcmattca ll y ra nktng the T IAA

CRFF t:1m dy of Cu nds to dctcrn1 1nc a super-e rf i cient optima l port fo liO. 1 he elrmm:llton of O\ erva lu ed fu nds and the

op t1l11 1Z:1t to n o f underva lued fund s 1s 1nil ercnt in tht s ra nktn g process. Thi s linea r optim1za tr on methodol ogy is an easy- to

usc li near too l th at ca n be used to rn odc l the underl ying MPT constru cts. \V InJe thts opttmtza ti on process 1s based ent ire ly nn htstorr cil l data, studcnb can rep! reate thi s s tud y usi ng proJec ted data sets. When ustn g h1sto rrca l data, 11 IS

rmpo r1ant to keep in mind that pas t pc:rfo nn ance may not be tndtcatt\'e of fu tu re resul ts.

R EFEREN C ES

Arnold, 1., 1 Na t! and T. N ixon 2006. Getting t\ lore O ut of ' I wo-Asse t Port foli os. J ournal of Applied Fin a nce,

Sp n ng. Sumrner, 72-8 1.

1-lton, E. and tv! . (] ru ber 1997. Modem Portf oli O Theo ry, 1950 to Date. Jo umal of Ba nkin g and Finan ce, 2 1 ( I L 12). 1 7 ~ 3- 1 759.

8

Elt on, 1 ~., tv! . Gruber and M . Pad berg 1976. S im ple Criteria for Opt1 mal Port fo lro Se lec ti on. Jou rn a l of Finance, X I (5 ), 134 1- 13 57.

----- 1977. SHnpl e Rul es for Opt rrn all' ortfoli o Selection: The t\ lu ltt Group Case. Jo umal of Fina ncial and Q uantit a tiv e Ana lys is, X II (3), 329-345.

~ ! to n , [ ., tvl. Gruber, Brown, S. and Goctzmann, W. 2003 . J\ Iodern Portfo lio Theor y a nd Investment Anal ys is. John Wil ey & Son, Inc., New Yo rk.

Jac kso n, M. and M .D. Staunt on 1999. Quad rati c l'rogr:11nrnin g Appli ca ti ons in f-i nance Using Excel. Th e Journa l of th e O pera tio na l Researc h Society, 50 ( 12), 1256- 1266.

Ma rkow tt z, II. 1952 . Ponfo!to Se lect ion. Jour nal of Finan ce, March, 77-9 1.

, I 959. Por tfo li o Se lec tion : Effic ient Diversification of Inves tm ents, John \\' dey & Sons, Inc., New Yo rk .

Rugh, J. 2003. Participant Co ntnbu tt ons and Asset AllocatiOns Dur1ng the Rece nt Bull and Bea r Market: E\'tdencc from T IAA-CRE F. Be nefit s Q uarterly , 55-

67

Sharpe, W. 19!i6. t\ lutual f-und l'u fo1rna ncc. Journal of B u ~in ess, 39, 11 9-131\.

Sktrpe. W. 1907. I\ Strnp lrficd t\1ndc l of l'o11 fo lio Analys is . i\

l an agcment Science, 13,277-293

Sharpe, \V 1972. Sll nple Strategies fo r Po rtfoli o Dtvcrs rfi ca t1on: Comme nt. Jo ur nal of Finance, VII

( I ), 127-129.

S1m plc Strategtes for Portfo li o D1vC1'sdi ca ti on: Commen

t, A Correc twn J ourn a l of Fina nce, VII (3) ,

773

Sharpe,\\'. 1994 , fhe Sharvc Ratrn Juumal of Purt{o lio J\lan agcmentScie nce,2 1 (!), 49-5X.

T IAJ\-CR I· F. http twww. tr aa-cre f.org/perforrnancc, re t lfC l11Cl1 tJ data/1 ndex. ht mJ, retn c\'cd on Ja nuary 3, 2007.

Treynor, J. L. 1965. !l ow to Rate: Ma rngc rn ent of l n\'cstmc nt Funds. Harvard Bu siness Review, 43 , (J anuary-February), 63-7 5.

Y:tl wol Finance. htt p:// fi nancc.ya hoo.co m, retrieved on Janu ary 3, 2007.

8

Journal of Business & Leadership: Research, Practice, and Teaching (2005-2012), Vol. 4 [2008], No. 1, Art. 2

https://scholars.fhsu.edu/jbl/vol4/iss1/2

Grover and Lavin

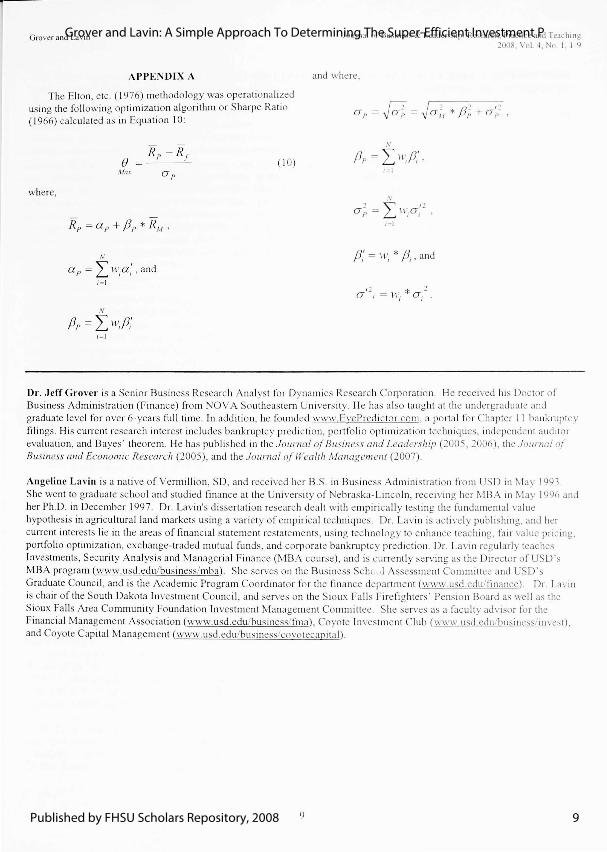

APPENDIX A

The Elton, e tc. ( 1976) methodo logy was operati ona li zed us ing the fo ll owing optimization a lgo rithm or S harpe Rati o ( 1966) ca lcul ated as in Equati on I 0 :

where,

N

ap= I w,a; , and i = l

N

/]p =I W;/3: i= l

( I 0)

Jnumal o f Bus iness & Lcatkr , hir Re,c arc h. Practice and Teach1n g 2008. Vo l ~ . Nn I . 1-9

and where.

,v

fJp =I ,, .,/3,'. 1 ~ 1

"' a-;, = I \\·.a-:"

t = i

/],' = \1 ', * /3;, and

12 * 2 a- I = \ "; CY; .

Dr. Jeff Grover is a Seni o r Bus iness Resea rch A nalys t for D ynami cs Resea rch Corporati on. He rece ived his Doctor o f Business Ad ministrati on (Finance) from NOV A Southeastem Uni ve rs it y. He has a lso taught at the undergradu ate and g raduate level for over 6-yea rs full time. In add it ion , he fo unded www. Eve Pred ic to r. com, a po rt ed fo r Chapter II bankruptcy filin gs. Hi s current researc h int eres t inc ludes bankruptcy predi c ti on, portfo li o opti mizati on tec hn iqu es, indepe nde nt aud ito r evaluation, and Bayes' theo rem . He has publi shed in the Journal of Business and Leadership (2005 , 2006), the Joum ol of Business and Economic Research (2005) , and the Journal of Wealth Management (2007) .

Angeline Lavin is a na ti ve o f Vermilli on, SO, and received her B.S. in Bus iness Admini s tra tio n fro m U Din ~ l ay I 993. She went to graduate schoo l and s tudied fin ance a t the Uni vers it y o f Neb ras ka- Linco ln. rec ei, ·ing her MBA in 1ay 1996 and her Ph.D. in December 1997. Dr. Lavin 's dissert ation research d ea lt w ith empirica ll y tes ting the fu ndamenta l va lue hypothesis in agricultura l land marke ts us ing a va ri e ty of empiri ca l techni ques . Dr. La vin is act ive ly pub lishing, and her current interests li e in the a reas of fin anc ia l s ta tement res ta teme nts, us ing tec hno logy to enJ1ance teaching, fa ir va lue pri c ing, portfo lio optimizatio n, exchange- traded mutual funds, and co rpo rat e bankru ptcy pred iction . Dr. Lavin regul arl y teaches Inves tments, Securit y Analysis and Manageria l Finance (MB A co urse), and is currentl y serving as the Directo r o f USD 's MB A progra m (www. usd .edu/b us iness/mba) . She serves on the Bus iness Scht ,, I Assessment Comm ittee and US D 's G raduate Co uncil , and is the Academi c Progra m Coo rdina to r fo r the fin ance department www.usd .edu/ fin ance) . Dr. La vin is cha ir of the South Dako ta In ves tment Co unc il , and serves on the S io ux Fa ll s Fire fi ghte rs' Pens io n Board as we ll as the Sioux Falls Area Co nullllnity Foundatio n Inves tme nt Management Comm ittee. S he serves as a fa c ult y advisor fo r the Financial Management Associa tion (www.usd .edu/bus iness/ fma) , Coyote Inves tm ent C lu b (www.usd. ed u/bus incss /inves t) , and Coyo te Cap ital Management (vAvw.usd .edulb usiness /eovo tecapita l) .

9 9

Grover and Lavin: A Simple Approach To Determining The Super-Efficient Investment P

Published by FHSU Scholars Repository, 2008