a study of the repayment performance of the microfinance borrower households of the ahon sa hirap...

TRANSCRIPT

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)

1. Research question and hypotheses

2. Theoretical model

3. Empirical model

4. Empirical results

5. Concluding notes and recommendations

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)

1.1 Three introductory remarks on the motivation and context of the research

1. Research question and hypotheses

(a) Proceeding from an interest in the poverty reduction agenda of microfinance, the present

study aims to contribute to a better understanding of how poorer microfinance

borrower households experience loan repayment difficulties.

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)

1.1 Three introductory remarks on the motivation and context of the research

1. Research question and hypotheses

(b) The research studies the repayment performance of borrower households of the Ahon sa Hirap Inc.

(ASHI), a social mission-oriented Philippine microfinance institution (MFI).

*** In September 2013, ASHI had:20 branches in Laguna, Rizal, Metro Manila,

Antique and Aklan26,801 borrower-members

Outstanding loan portfolio of PHP 229.7 million

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)

1.1 Three introductory remarks on the motivation and context of the research

1. Research question and hypotheses

(c) The study makes use of Progress out of Poverty Index (PPI) data.

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)

1.2 (A) General research question:

Does the empirical evidence with regard to the repayment performance of ASHI borrower households conform to theoretical expectations based on the repayment model of Gonzalez (2008) as the latter is augmented by some analytical expectations?

1. Research question and hypotheses

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)

1.2 (B) Specific research question:

Does a greater likelihood that an ASHI borrower household is officially poor (based on its PPI score) increase the probability that it does not pay in full one of its weekly loan obligations?

1. Research question and hypotheses

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)

1.3 In formulating the research question and generating research hypotheses, the research theoretical frame identifies the following five main factors that determine or that are associated with weekly loan obligation non-payment:

a. General repayment capacity of borrower HH

b. Loan appraisal processes of ASHI

c. Borrower HH use of ASHI loans

d. HH adverse economic shocks

e. Group lending structures and MFI competition

1. Research question and hypotheses

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)

1.4 (A) Primary research hypothesis:

A lower ASHI borrower household PPI score (indicating that the said household has a greater likelihood of being officially poor) increases the probability that it does not pay in full a weekly loan obligation.

1. Research question and hypotheses

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)

1.4 (B) Secondary research hypotheses:

1. A greater number of years of membership in ASHI on the part of a borrower household decreases the probability that it does not pay in full a weekly loan obligation.

2. Greater social cohesion of the ASHI borrower center of the borrower household—as indicated by greater member attendance in center meetings—decreases the probability of non-payment.

3. Stronger presence of MFI competitors of ASHI increases the probability of non-payment.

1. Research question and hypotheses

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)

A. The borrower household chooses the optimal level of effort, consumption and saving, respectively, in each period of a two-period lifetime.

> Household optimization problem:

Max W = [ U1 ( c1 , e1 ) + β U2 ( c2 , e2)] c1, c2, e1, e2, b1, a1

where ct = consumption in period t et = effort in period t b1 = amount of loan received in period one a1 = stock of assets at end of period one

2. Theoretical model

2.1 Gonzalez (2008) model of repayment behavior: Basic structure

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)

B. Household can choose to repay the loan it receives in period one and this allows it to avail of another loan in period two. Conversely, it can choose to default on its period one loan at the cost of losing access to a loan in period two.

C. The household is later assumed to be subject to an adverse economic shock in period one and the effect of the latter on its utility-maximizing behavior is analyzed.

D. After an adverse economic shock, if the borrower household still chooses to repay its loan, it needs to generate additional repayment capacity by engaging in “costly actions.”

2. Theoretical model

2.1 Gonzalez (2008) model of repayment behavior: Basic structure

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)

E. Given all the foregoing, there are four repayment/ default scenarios that frame the utility-maximizing behavior of the household:

(i) the repayment scenario with no adverse economic shock

(ii) the default scenario with no adverse economic shock,

(iii) the repayment scenario after an adverse economic shock, and

(iv) the default scenario after an adverse economic shock.

2. Theoretical model

2.1 Gonzalez (2008) model of repayment behavior: Basic structure

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)

A. Discussion of effect of lower level of borrower household productivity z1 and/ or asset ownership a0

> The initial planned level of consumption c1* tends to decrease as household z1 and/ or a0 decrease.

> The lower level of c1*—particularly if it is already close to the minimum subsistence level of consumption cMin—makes default more likely.

2. Theoretical model

2.2 Gonzalez (2008) model of repayment behavior: Four analytical extensions

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)

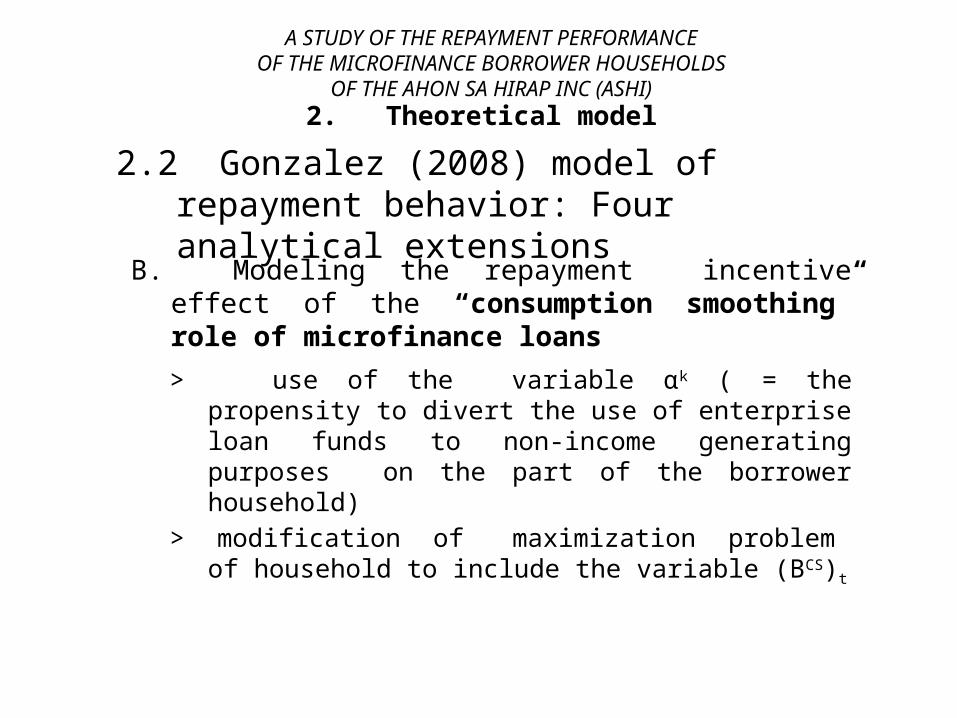

B. Modeling the repayment incentive effect of the “consumption smoothing” role of microfinance loans

> use of the variable αk ( = the propensity to divert the use of enterprise loan funds to non-income generating purposes on the part of the borrower household)

> modification of maximization problem of household to include the variable (BCS)t

2. Theoretical model

2.2 Gonzalez (2008) model of repayment behavior: Four analytical extensions

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)

C. Modeling the repayment incentive effect of group lending structures

> use of the variable (BSK)t ( = net benefits derived by the borrower household from its microfinance-associated social capital endowment )

> modification of maximization problem of household to include the variable (BSK)t

2. Theoretical model

2.2 Gonzalez (2008) model of repayment behavior: Four analytical extensions

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)

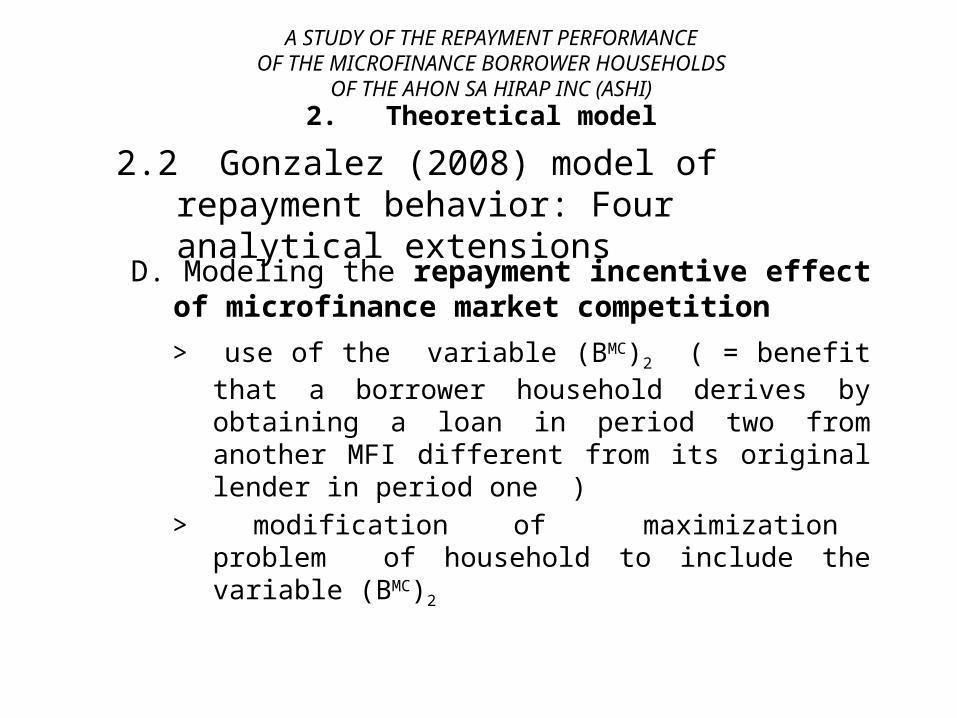

D. Modeling the repayment incentive effect of microfinance market competition

> use of the variable (BMC)2 ( = benefit that a borrower household derives by obtaining a loan in period two from another MFI different from its original lender in period one )

> modification of maximization problem of household to include the variable (BMC)2

2. Theoretical model

2.2 Gonzalez (2008) model of repayment behavior: Four analytical extensions

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)

*** The model incorporates a number of key perspectives drawn from the microfinance literature with regard to:

A. Perceived limits to the poverty reduction impact of microfinance

B. Concerns for the “over-indebtedness” of microfinance borrowers as a whole

C. Improved understanding of how microfinance benefits borrower households

2. Theoretical model

2.3 Gonzalez (2008) model of repayment behavior and its analytical extensions: Concluding remarks

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

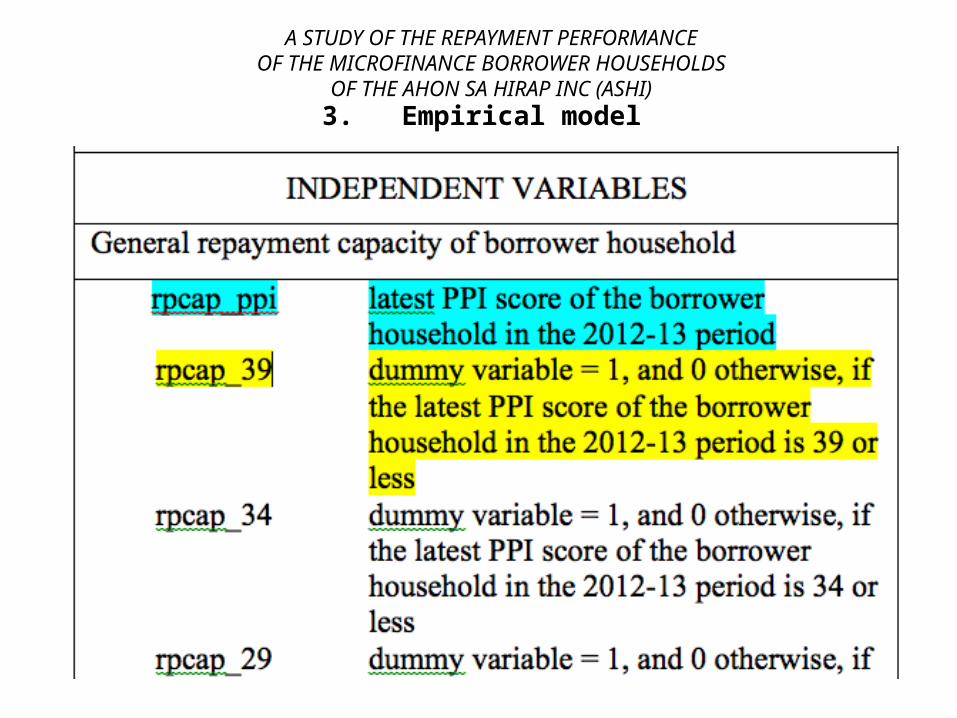

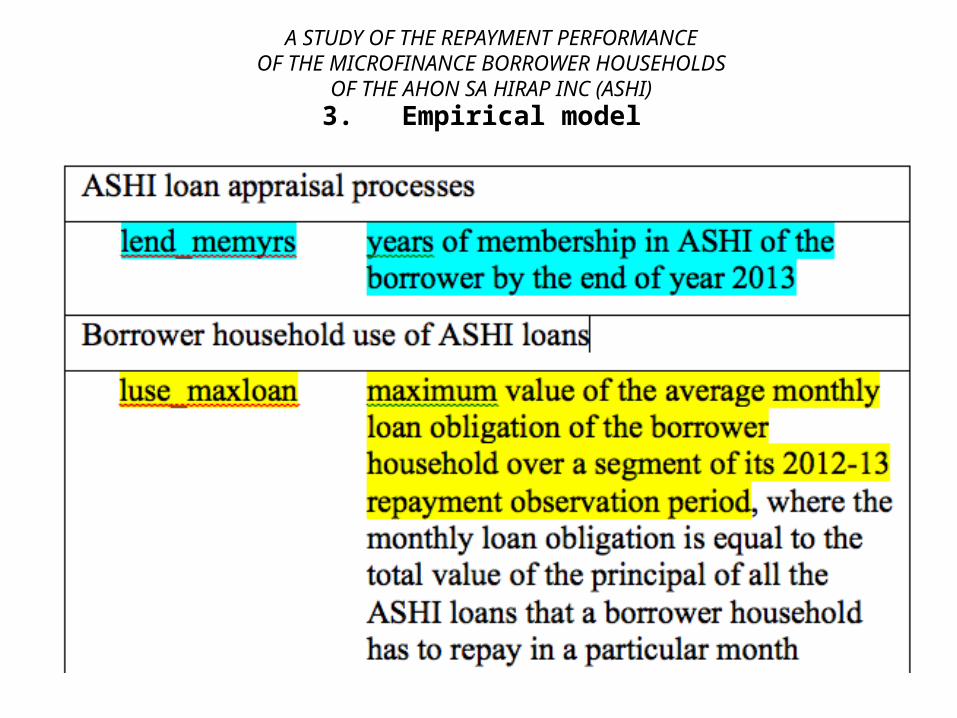

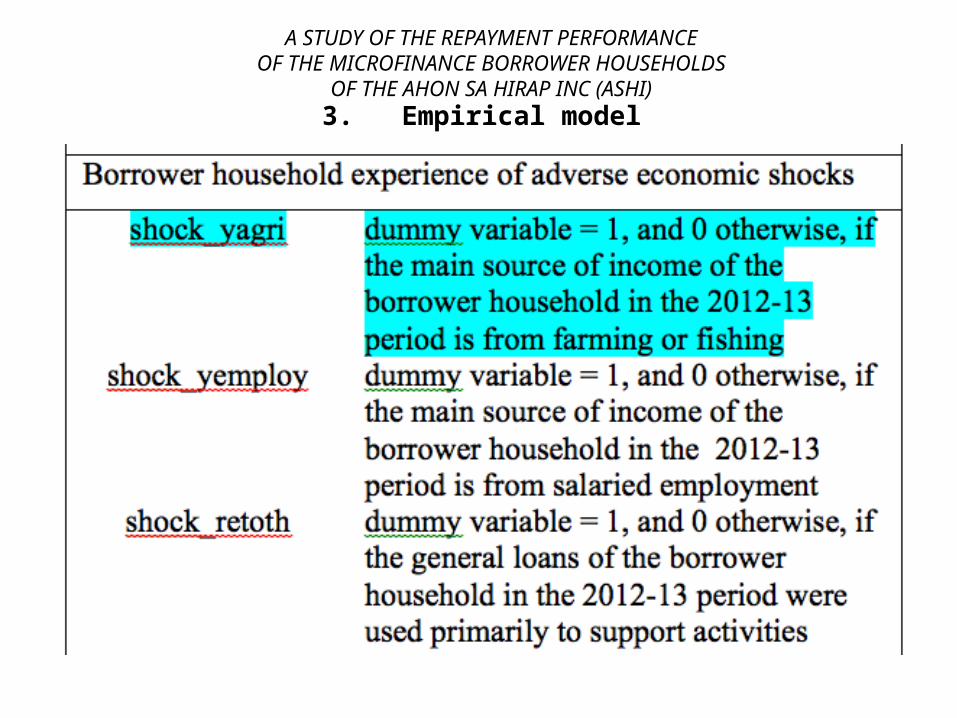

OF THE AHON SA HIRAP INC (ASHI)3. Empirical model

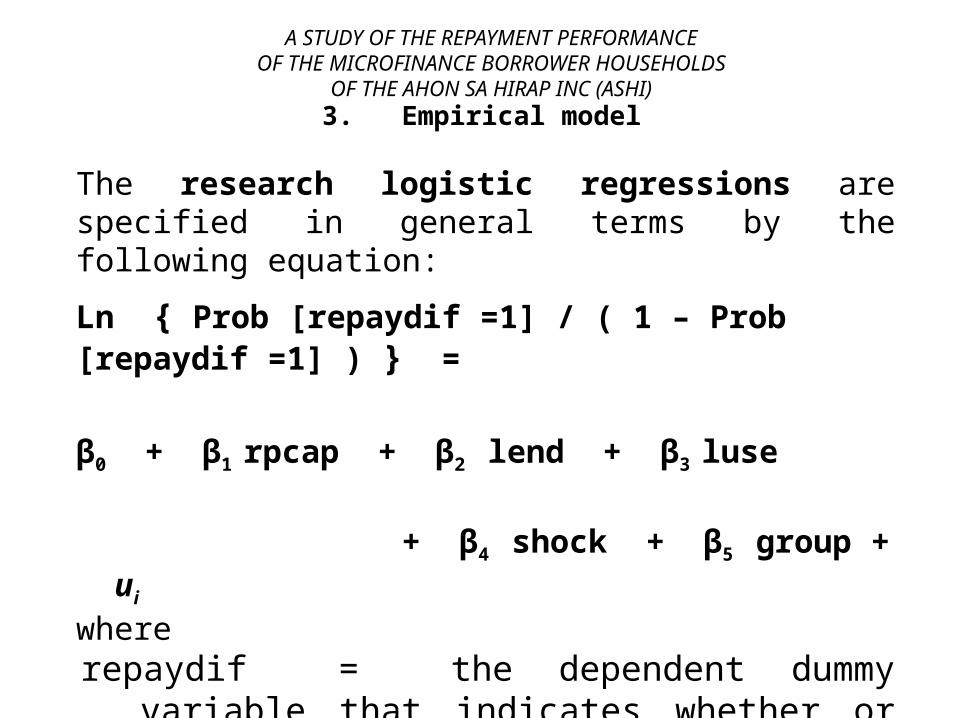

The research logistic regressions are specified in general terms by the following equation:

Ln { Prob [repaydif =1] / ( 1 – Prob [repaydif =1] ) } =

β0 + β1 rpcap + β2 lend + β3 luse

+ β4 shock + β5 group + ui whererepaydif = the dependent dummy variable that indicates

whether or not the borrower household has not paid in full one of its weekly loan obligations

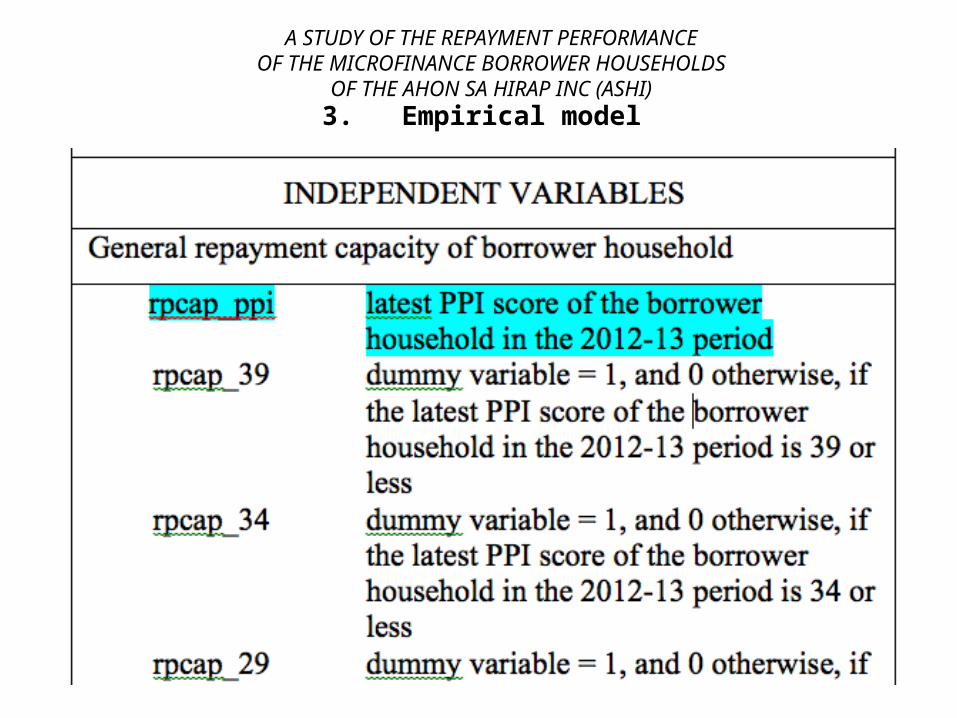

rpcap = a variable that represents the general repayment capacity of the borrower household

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)3. Empirical model

The research logistic regressions are specified in general terms by the following equation:

Ln { Prob [repaydif =1] / ( 1 – Prob [repaydif =1] ) } =

β0 + β1 rpcap + β2 lend + β3 luse

+ β4 shock + β5 group + ui wherelend = a variable that represents the effectiveness of

ASHI loan appraisal processes luse = a vector of variables that measures the total

amount of ASHI loans that a borrower household avails of and the purposes for which it uses the said loans

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)3. Empirical model

The research logistic regressions are specified in general terms by the following equation:

Ln { Prob [repaydif =1] / ( 1 – Prob [repaydif =1] ) } =

β0 + β1 rpcap + β2 lend + β3 luse

+ β4 shock + β5 group + ui whereshock = a vector of variables associated with the

borrower household’s possible experience of adverse economic shocks

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)3. Empirical model

The research logistic regressions are specified in general terms by the following equation:

Ln { Prob [repaydif =1] / ( 1 – Prob [repaydif =1] ) } =

β0 + β1 rpcap + β2 lend + β3 luse

+ β4 shock + β5 group + ui wheregroup = a vector of variables that indicates the strength

of the social cohesion of the borrower center of the borrower household, as well as the degree of competition faced by ASHI from other MFIs

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)3. Empirical model

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)3. Empirical model

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)3. Empirical model

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)3. Empirical model

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)3. Empirical model

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)3. Empirical model

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)3. Empirical model

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)3. Empirical model

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)3. Empirical model

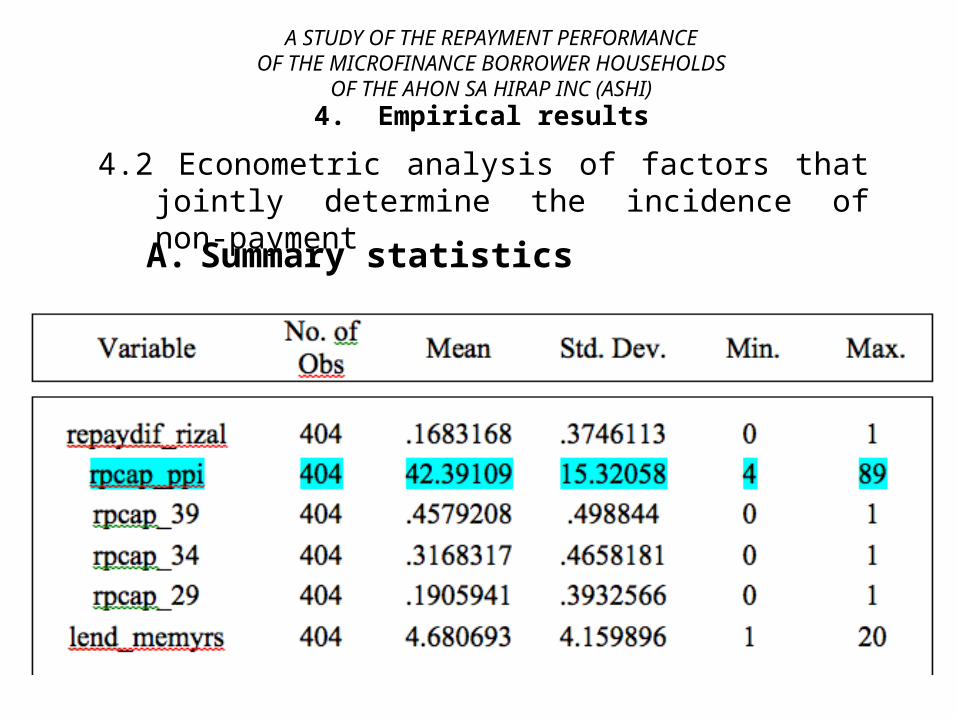

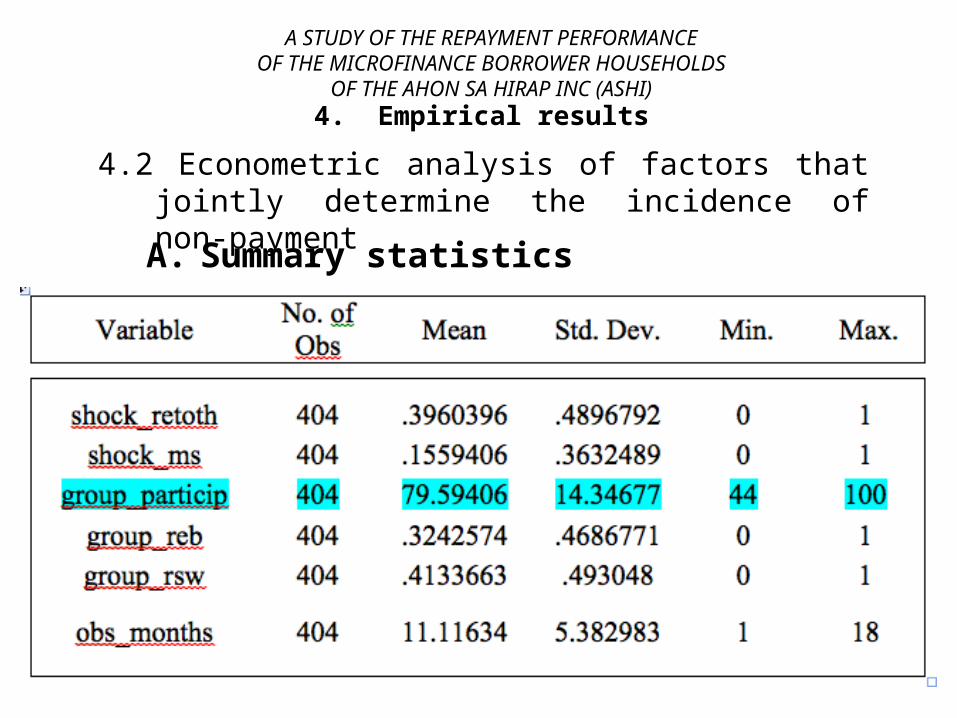

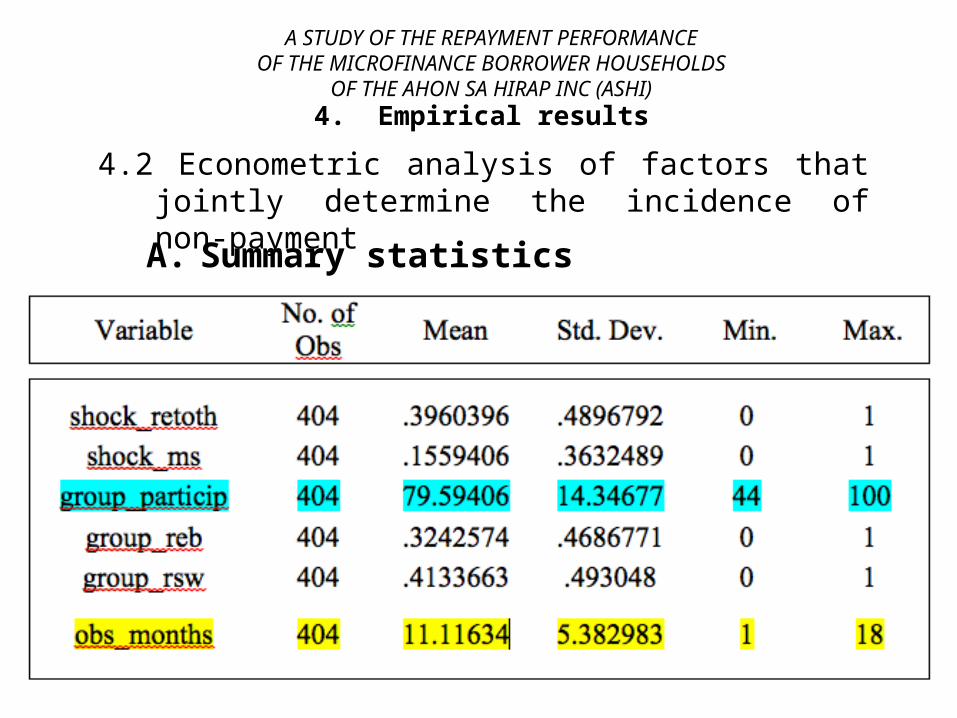

Some notes on data collection:1. Data for the empirical analysis was collected from November to December 2013.

2. Three ASHI branches in Rizal were chosen for data-gathering: the Rizal West branch (RWB), the Rizal Southwest branch (RSW), and the Rizal East branch (REB).

3. Data on 404 borrower households was collected, 131 from the REB, 167 from the RSW and 106 from the RWB.

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)

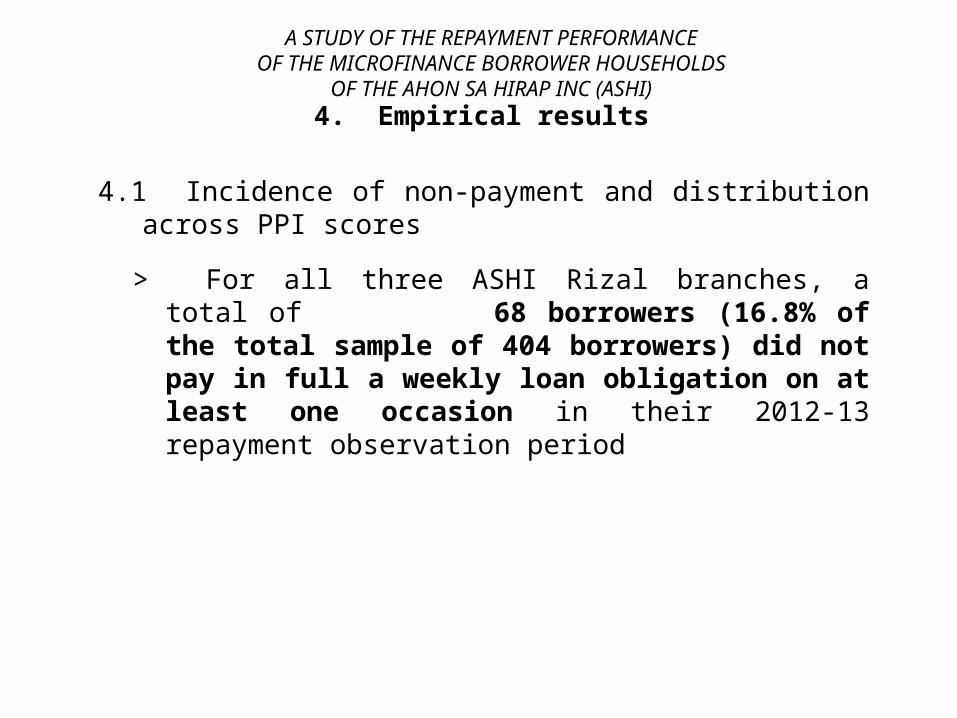

4.1 Incidence of non-payment and distribution across PPI scores

> For all three ASHI Rizal branches, a total of 68 borrowers (16.8% of the total sample of 404 borrowers) did not pay in full a weekly loan obligation on at least one occasion in their 2012-13 repayment observation period

4. Empirical results

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)

4.1 Incidence of non-payment and distribution across PPI scores

4. Empirical results

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)

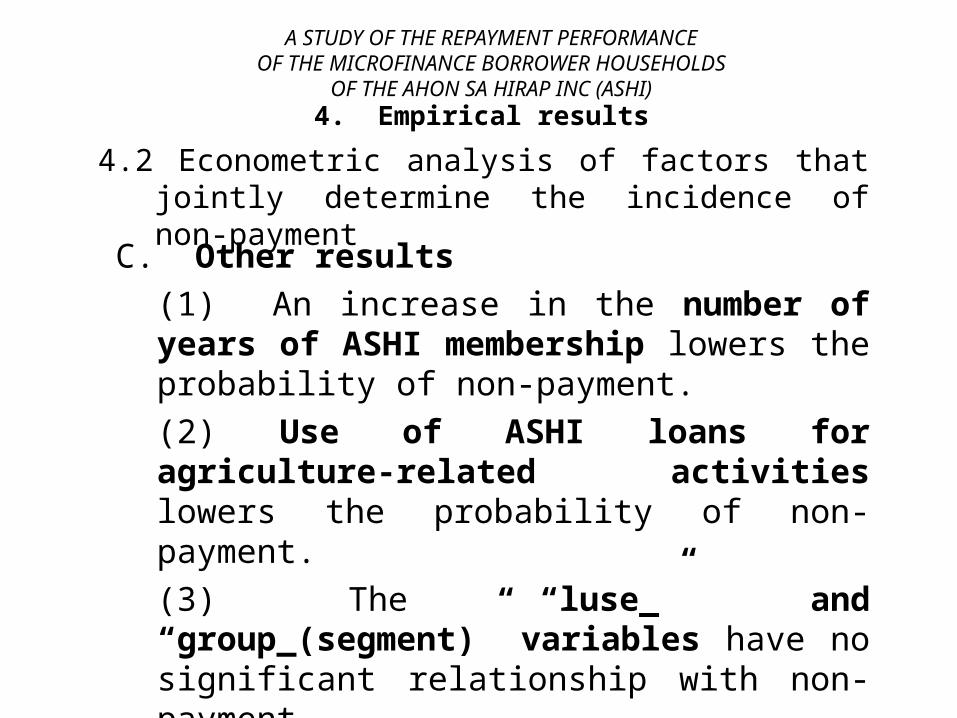

4.2 Econometric analysis of factors that jointly determine the incidence of non-payment

4. Empirical results

A. Summary statistics

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)

4.2 Econometric analysis of factors that jointly determine the incidence of non-payment

4. Empirical results

A. Summary statistics

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)

4.2 Econometric analysis of factors that jointly determine the incidence of non-payment

4. Empirical results

A. Summary statistics

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)

4.2 Econometric analysis of factors that jointly determine the incidence of non-payment

4. Empirical results

A. Summary statistics

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)

4.2 Econometric analysis of factors that jointly determine the incidence of non-payment

4. Empirical results

A. Summary statistics

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)

4.2 Econometric analysis of factors that jointly determine the incidence of non-payment

4. Empirical results

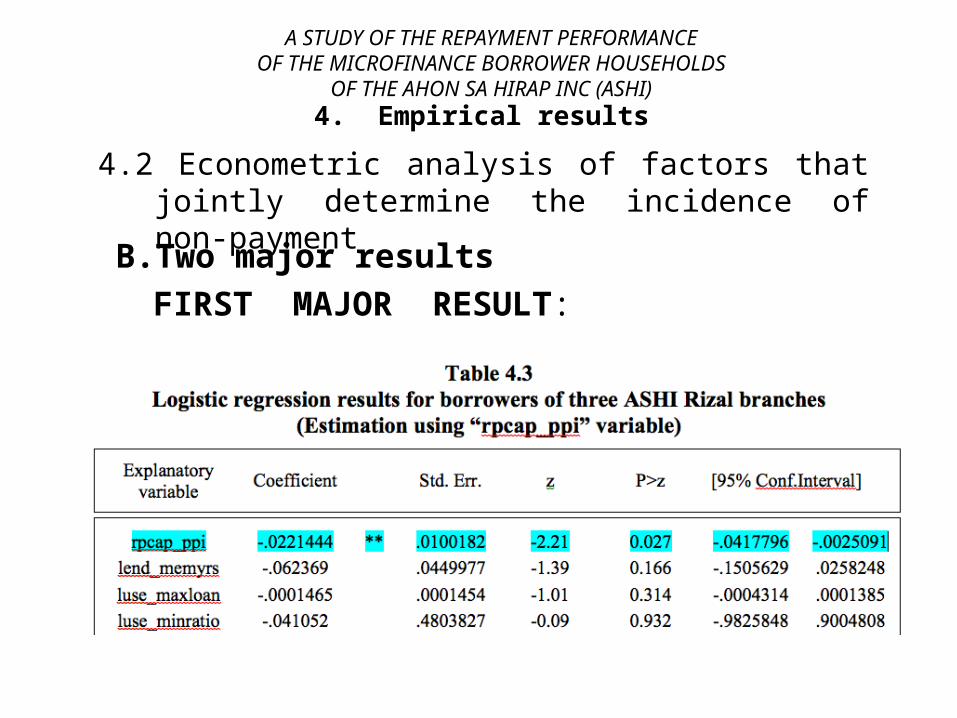

B.Two major resultsFIRST MAJOR RESULT: Confirming the primary hypothesis of the research, there is evidence of a statistically significant negative relationship between the probability of non-payment and the PPI score of the concerned borrower household.

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)

4.2 Econometric analysis of factors that jointly determine the incidence of non-payment

4. Empirical results

B.Two major resultsFIRST MAJOR RESULT:

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)

4.2 Econometric analysis of factors that jointly determine the incidence of non-payment

4. Empirical results

B.Two major resultsFIRST MAJOR RESULT:

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)

4.2 Econometric analysis of factors that jointly determine the incidence of non-payment

4. Empirical results

B.Two major results:SECOND MAJOR RESULT: An increase in the social cohesion of the borrower center of the borrower household—as measured by the degree of attendance at borrower center meetings—significantly decreases the probability of non-payment.

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)

4.2 Econometric analysis of factors that jointly determine the incidence of non-payment

4. Empirical results

B.Two major results:SECOND MAJOR RESULT:

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)

4.2 Econometric analysis of factors that jointly determine the incidence of non-payment

4. Empirical results

C. Other results(1) An increase in the number of years of ASHI membership lowers the probability of non-payment.(2) Use of ASHI loans for agriculture-related activities lowers the probability of non-payment.(3) The “luse_” and “group_(segment)” variables have no significant relationship with non-payment.(4) The control variable “obs_months” is significantly related to non-payment.

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)

5.1 The research results are consistent with the results of previous research surveyed in the review of literature.

5.2 The research results provide validation of the repayment model of Gonzalez (2008) and the analytical extensions of the model.

5. Concluding notes and recommendations

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)

5.3 The research results suggest that loan repayment difficulties—understood in terms of a borrower household not being able to or not wanting to pay in full a weekly loan obligation—affects a significant minority of ASHI borrower households.

Poorer borrower households, moreover, are shown to be more likely to experience these loan repayment difficulties.

5. Concluding notes and recommendations

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)

5.4 The research theoretical framework emphasizes that repayment performance does not reveal the whole dynamic of loan repayment difficulties. To uncover the latter, future research needs to examine the “costly actions” that borrower households resort to in paying back their loans.

5. Concluding notes and recommendations

A STUDY OF THE REPAYMENT PERFORMANCEOF THE MICROFINANCE BORROWER HOUSEHOLDS

OF THE AHON SA HIRAP INC (ASHI)

5.5 More research on the repayment difficulties borne by poorer microfinance borrower households vis-à-vis those who are more well-off can provide important insights with regard to the welfare impact of microfinance.

The latter can help interested stakeholders maximize the positive impact of microfinance and minimize its negative consequences.

5. Concluding notes and recommendations

THANK YOU!