aaron bar - the dynamic wind energy market & the impact on blade technology

TRANSCRIPT

Analyst PRESENTATION

The Dynamic Wind

Energy Market and

Impact on Blade

Technology

Aaron Barr

August 30, 2014

Contents

22016 Sandia Wind Turbine Blade Workshop

August, 2016

Global wind energy market dynamics

– Long-term market forecast by region

– Long term United States demand driven by PTC extension

– Economies of scale accelerate LCOE gains in North America

– Traditional markets to drive installs, while new markets emerge

Blade market and technology trends

– Recent mergers and acquisitions will impact blade technology

– Historically MW-limited markets see 3MW movement

– Best in class products defined by blades

– Modular portfolio strategies lead to rapid turbine proliferation

– Blade lengths will continue to grow in all regions

– Blade technology prospects and impact on LCOE

– Blades a central focus of O&M technology development

Delivering renewableenergy insight

8 September 2016 3

Global wind energy

market dynamics

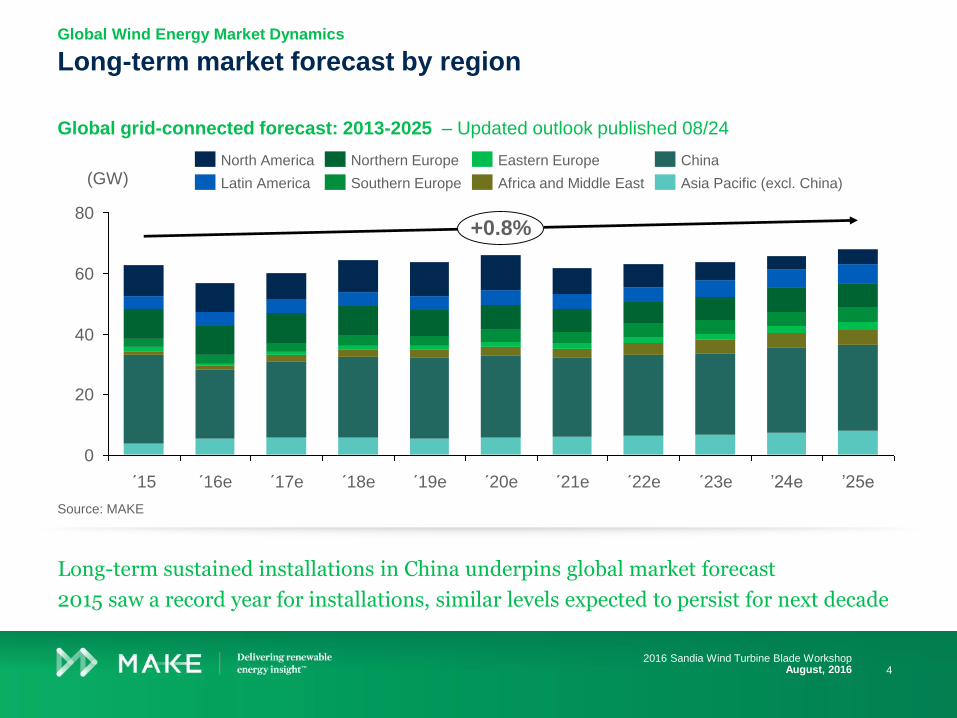

Global grid-connected forecast: 2013-2025 – Updated outlook published 08/24

Long-term market forecast by regionGlobal Wind Energy Market Dynamics

Source: MAKE

Long-term sustained installations in China underpins global market forecast

2015 saw a record year for installations, similar levels expected to persist for next decade

42016 Sandia Wind Turbine Blade Workshop

August, 2016

80

40

20

60

0

´20e´18e´15

+0.8%

´23e´22e

(GW)

´21e´19e´17e´16e ’24e ’25e

China

Latin America Southern Europe

North America

Asia Pacific (excl. China)Africa and Middle East

Northern Europe Eastern Europe

United States market outlook, 2013-2025e (GW) – Updated outlook published 08/24

Long term United States demand driven by PTC extensionGlobal Wind Energy Market Dynamics

52016 Sandia Wind Turbine Blade Workshop

August, 2016

0

2

12

6

10

4

8

GW

Grid

Co

nn

ecte

d

+14%-31%

-22%-17%

-26%+9%

2024e

+24%

2025e

+4%

-11%

2023e2018e 2019e 2022e2017e 2020e2015 2021e2016e

StrongerWeaker

Transmission

PTC

Retirements

LCOE

C&I demand

CPP/RES

Gas prices

Solar power

Ba

rrie

rsD

rive

rs

Regional economies of scale in North America

Economies of scale accelerate LCOE gains in North America

Contributors and benefits of regional scale

Global Wind Energy Market Dynamics

Contributors to regional growth and scale

Excellent and consistent wind resources

Limited terrain complexity – flat sites

Large tracts of land with few constraints

Infrastructure – transmission and rail

Local supply chain – turbines, services, equipment

Benefits of regional scale

Capital equipment savings – local network of cranes,

trucks and equipment

Turbine pricing – Familiarity reduces risk to OEMs

and allows for lower turbine pricing

BOP pricing – well understood foundation and road

design and construction reduces BOP costs

Experience – Money and time savings due to

experienced local network of installers

O&M savings – Highly trained and fluid network of

technicians lead to cost savings in maintenanceNote: Unsubsidized LCOE. Local assumptions for debt, equity, CAPEX, CF, wind

Source; MAKE

Installation centers of Texas and the Midwest benefit from experience of 17+ GW

LCOE lessons learned from the “Wind Belt” are now being applied to emerging markets

62016 Sandia Wind Turbine Blade Workshop

August, 2016

30

35

40

45

50

55

60

65

70

75

80

85

90

0 2 4 6 8 10 12 14 16 18 20 22 24

LC

OE

–U

SD

/MW

h

Midwest

66

Total cumulative GW

83

Northeast

47

58

Texas

Canada

US Average

2015 annual

installations (GW)

Top 20 markets: New capacity 2016e-2025e

Traditional markets to drive installs, while new markets emerge

Top 20 emerging markets by regions: 2015-25e

Global Wind Energy Market Dynamics

Note: “Emerging” countries with less than 1GW installed at YE2015

Source: MAKE

China, US and Germany to contribute 60% to global installs over next decade

Significant growth expected in emerging markets of Africa and the Middle East

72016 Sandia Wind Turbine Blade Workshop

August 2016

0 20 40 60 28010080

Canada

France

South Africa

(GW)

Netherlands

Turkey

Sweden

Australia

Others

Mexico

India

Japan

Brazil

Germany

U.S.

China

United Kingdom

73263

7

6

5

4

3

2

0

1

+20.9%

´25e´24e´23e´22e´21e´20e´17e ´18e´16e´15 ´19e

(GW)

Delivering renewableenergy insight

8 September 2016 8

Blade market and

technology trends

Diverging technical paths within OEM M&A

Recent mergers and acquisitions will impact blade technology

Technology acquisitions to secure blade IP

Lower

CAPEXVarious options

Higher

CAPEX

Blade

Materials Glass Carbon

Blade

Sourcing3rd party

suppliers

Vertically

integrated

Blade

StructureShells

& web

Single

infusion

Pitch

Systems Electric Hydraulic

Converter

TypesPartial

Power

Full

Power

Tower

technology Steel Concrete

Blade market and technology trends

Source: MAKE, Espacenet

Only includes USPTO filings made prior to acquisitions

Looming industry consolidation will force tough technical choices in blade technology

M&A will lead to restriction of some blade innovation through exclusive access to IP

92016 Sandia Wind Turbine Blade Workshop

August 2016

NordexAccionaGamesaSiemens

8 20

3

11

7

18Modwind

Patent

Applications

Rodpack

Granted

Patents

29

Blade

Dynamics

10

28GE acquired

Deployment TBD

Vestas acquired

Not evident in products

Senvion acquired

Use in offshore 74.4m blade,

Note: CAPEX: Capital expenditure on either component or factory level

Orders for 3MW products on the rise in US

Historically MW-limited markets see 3MW movement

3MW capacity factors are catching up

Blade market and technology trends

Note: Orders shown only include those with known turbine types

Orders shown may not include balance of PTC Safe Harbor orders

Note: Gross capacity factor at 8.5m/s

Construction cost given at a plant level – 150MW plant assumed

BOP and O&M cost savings for larger turbines, combined with economies of scale have blurred the lines between MW-limited and turbine-limited markets

102016 Sandia Wind Turbine Blade Workshop

August, 2016

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Announced

Orders*

4,80212,870

20142012

8,402*

2013

8,5891,128

2015

>3.5MW2.3-2.791.0-1.79MW 1.8-2.29 2.8-3.49

58.4

55.7 55.7

V110-2.0

-5%

58.4

V136-3.45

3.XMW

-6%

2.XMW

Construction cost savings are significant

150

200

250

300

350

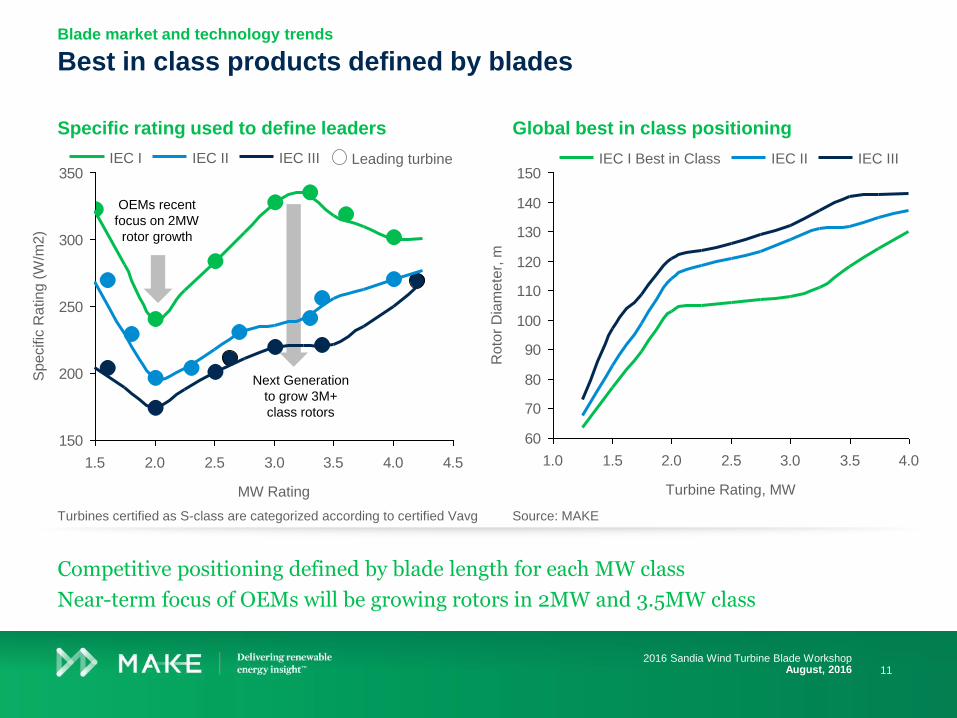

1.5 2.0 2.5 3.0 3.5 4.0 4.5

Specific

Rating

(W

/m2)

MW Rating

Specific rating used to define leaders

Best in class products defined by blades

Global best in class positioning

Blade market and technology trends

Competitive positioning defined by blade length for each MW class

Near-term focus of OEMs will be growing rotors in 2MW and 3.5MW class

112016 Sandia Wind Turbine Blade Workshop

August, 2016

IEC I IEC IIIIEC II Leading turbine

OEMs recent

focus on 2MW

rotor growth

Next Generation

to grow 3M+

class rotors

60

70

80

90

100

110

120

130

140

150

1.0 1.5 2.0 2.5 3.0 3.5 4.0

Ro

tor

Dia

me

ter,

mTurbine Rating, MW

IEC I Best in Class IEC II IEC III

Source: MAKETurbines certified as S-class are categorized according to certified Vavg

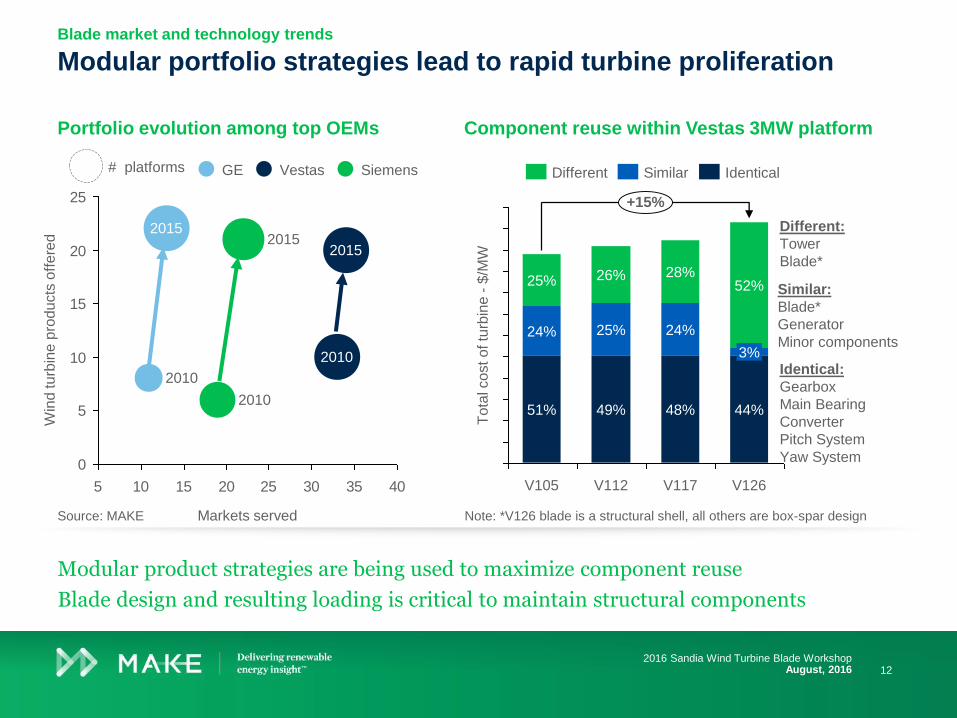

Portfolio evolution among top OEMs

Modular portfolio strategies lead to rapid turbine proliferationBlade market and technology trends

Modular product strategies are being used to maximize component reuse

Blade design and resulting loading is critical to maintain structural components

122016 Sandia Wind Turbine Blade Workshop

August, 2016

Component reuse within Vestas 3MW platform

Note: *V126 blade is a structural shell, all others are box-spar design

0

5

10

15

20

25

5 10 15 20 25 30 35 40

Markets served

2015

2010

2015

2015

2010

2010

Win

d turb

ine p

roducts

off

ere

d

SiemensVestasGE# platforms

Source: MAKE

26%

V105

51%

24%

25%

To

tal co

st o

f tu

rbin

e -

$/M

W

24%

28%

V112

49%

25%

+15%

V126

44%

3%

52%

V117

48%

IdenticalSimilarDifferent

Similar:

Blade*

Generator

Minor components

Identical:

Gearbox

Main Bearing

Converter

Pitch System

Yaw System

Different:

Tower

Blade*

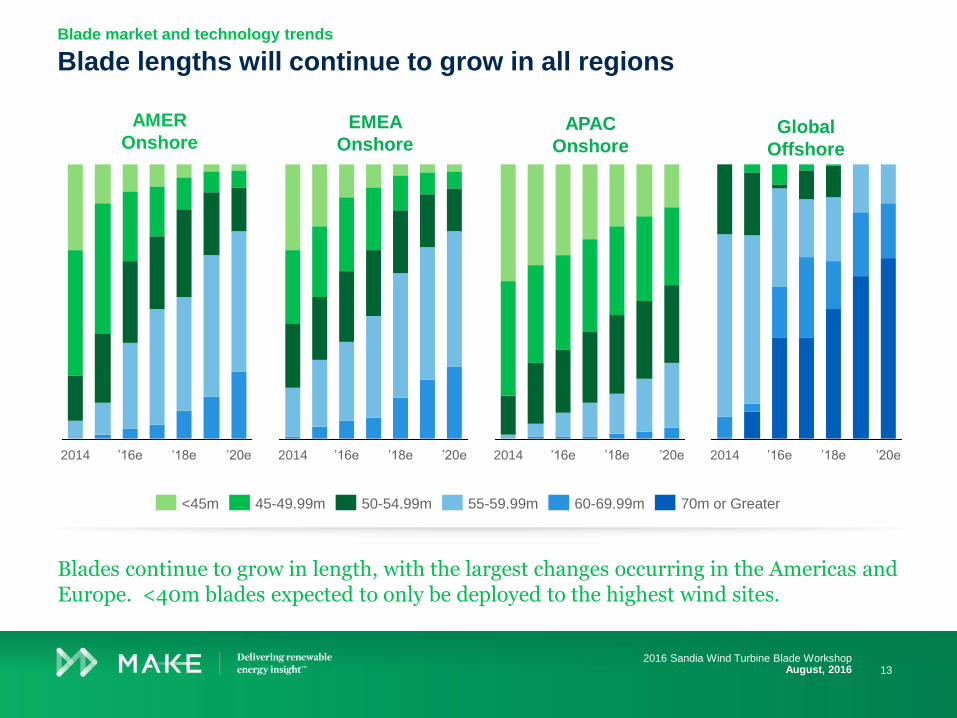

Blade lengths will continue to grow in all regionsBlade market and technology trends

Blades continue to grow in length, with the largest changes occurring in the Americas and Europe. <40m blades expected to only be deployed to the highest wind sites.

132016 Sandia Wind Turbine Blade Workshop

August, 2016

AMER

OnshoreEMEA

OnshoreAPAC

Onshore

2014 ’20e’18e’16e

45-49.99m 70m or Greater60-69.99m<45m 55-59.99m50-54.99m

’20e’16e ’18e2014 ’16e ’18e2014 ’20e ’20e2014 ’16e ’18e

Global

Offshore

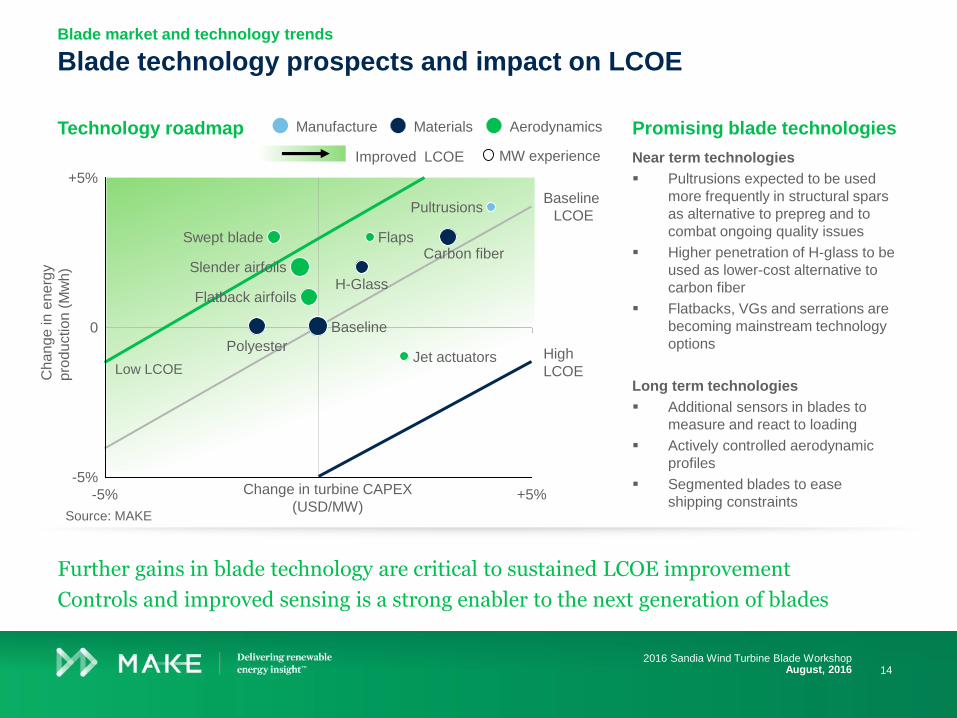

0

High

LCOE

Baseline

LCOE

-5% +5%

-5%

+5%

Carbon fiber

Baseline

Flatback airfoils

Swept blade

Slender airfoils

Jet actuators

Flaps

Polyester

H-Glass

Pultrusions

Technology roadmap Promising blade technologies

Near term technologies

Pultrusions expected to be used

more frequently in structural spars

as alternative to prepreg and to

combat ongoing quality issues

Higher penetration of H-glass to be

used as lower-cost alternative to

carbon fiber

Flatbacks, VGs and serrations are

becoming mainstream technology

options

Long term technologies

Additional sensors in blades to

measure and react to loading

Actively controlled aerodynamic

profiles

Segmented blades to ease

shipping constraints

Blade technology prospects and impact on LCOEBlade market and technology trends

Source: MAKE

Further gains in blade technology are critical to sustained LCOE improvement

Controls and improved sensing is a strong enabler to the next generation of blades

142016 Sandia Wind Turbine Blade Workshop

August, 2016

Chang

e in e

nerg

y

pro

du

ction

(M

wh)

Change in turbine CAPEX

(USD/MW)

Improved LCOE MW experience

AerodynamicsManufacture Materials

Low LCOE

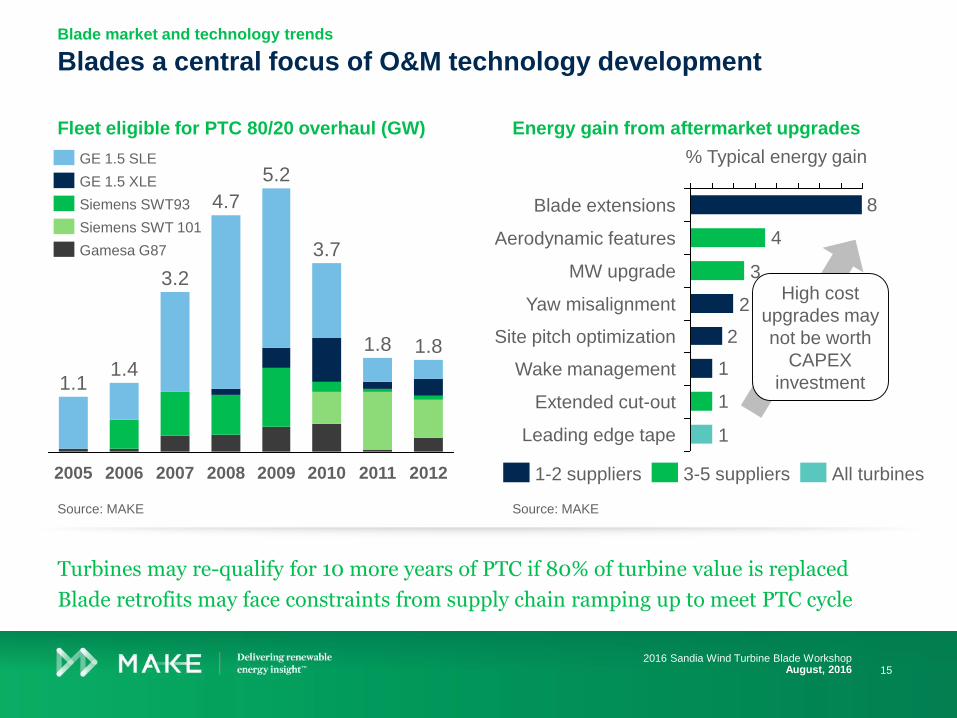

Fleet eligible for PTC 80/20 overhaul (GW)

Blades a central focus of O&M technology development

Energy gain from aftermarket upgrades

Blade market and technology trends

Source: MAKE Source: MAKE

Turbines may re-qualify for 10 more years of PTC if 80% of turbine value is replaced

Blade retrofits may face constraints from supply chain ramping up to meet PTC cycle

152016 Sandia Wind Turbine Blade Workshop

August, 2016

1.1

5.2

3.2

2006 2009

4.7

1.8

2005

1.8

2011 20122010

3.7

20082007

1.4

Siemens SWT 101

Siemens SWT93

GE 1.5 SLE

GE 1.5 XLE

Gamesa G87

1

1

1

2

2

3

4

8

% Typical energy gain

Leading edge tape

Extended cut-out

Wake management

Site pitch optimization

Yaw misalignment

MW upgrade

Aerodynamic features

Blade extensions

All turbines3-5 suppliers1-2 suppliers

High cost

upgrades may

not be worth

CAPEX

investment

Contact

consultmake.com

© 2016 MAKE Consulting A/S. All rights reserved. Reproduction or distribution of this report in any form without prior written permission is strictly forbidden.

Violation of the above restrictions will be subjects to legal action under the Danish Arbitration Act. The information herein is taken from sources considered

reliable, but its accuracy and completeness are not warranted, nor are the opinions, analyses and forecasts on which they are based. MAKE Consulting A/S

cannot be held liable for any errors in this report, neither can MAKE Consulting A/S be liable for any financial loss or damage caused by the use of the

information presented in this report.

Denmark

Sønder Allé 9

DK-8000

Aarhus

T +45 7026 6628

U.S.

117 N. Jefferson Street

Suite 400

Chicago, IL 60661

T +1 312 441 9590

U.S.

225 Franklin Street

26th floor

Boston, MA 02110

T +1 978 448 3186

China

Level 26, Shanghai

Times Sq. Office Tower,

Shanghai 200021

T +86 21 5117 9329

Germany

Neuer Wall 10

20354

Hamburg

T +49 40 822 15 3111

Aaron Barr

162016 Sandia Wind Turbine Blade Workshop

August, 2016