abg basel 3 seminar - seb group · pdf fileabg . basel 3 . seminar. oct 6. th, 2010. 2. ... eu...

TRANSCRIPT

Anders Kvist Head

of Group Treasury

ABG Basel 3

Seminar

Oct 6th, 2010

2

Transmission of financial crisis to the

real economyResulting inability to absorb

increasing trading and credit losses

nor to re-intermediate large off-balance sheet exposures

Excessive on-

and off-balance sheet leverage

Low capitalisation, thin equity cushions, deteriorating quality of

banks’

capital sources

Insufficient liquidity buffers

of most financial institutions, which

ultimately turned to central banks for refinancing

Interconnectedness of systemic institutions

through an array of complex and sometimes non-

transparent transactions

Procyclical

deleveraging

of banks exacerbated negative effects of

financial and RE crisis on the real economy

Basel Committee’s key concerns for the global banking sector

BA

SE

LII

IR

EG

UL

AT

OR

YF

RA

ME

WO

RK

:A

NO

VE

RV

IEW

Source J.P.Morgan

3

•

Timetable too aggressive in light of magnitude of change Second round of consultation & QIS required

•

Extended phase in & grandfathering of utmost importance

•

Leverage Ratio strongly opposed (SBA and, finally, EBF agreed. IIF disagrees but support no fixed minimum)

•

Capital Base

-

Write-up of written down hybrid Tier 1 capital securities must be allowed

-

Net pension fund deficits should not be deducted from equity

•

Credit Valuation Adjustments (CVA)

-

Proposed capital add-on for OTC derivatives strongly opposed

•

Liquidity Coverage Ratio

-

Concept OK but run-off assumptions much too pessimistic and liquid asseteligibility much to narrow. Covered bond holdings must be given more credit.

•

Net stable Funding Ratio

-Too prescriptive and conservative. No fixed ratio should be required

SEB´s

consultative response largely agreed

√√√(√)

√

√√

(√)

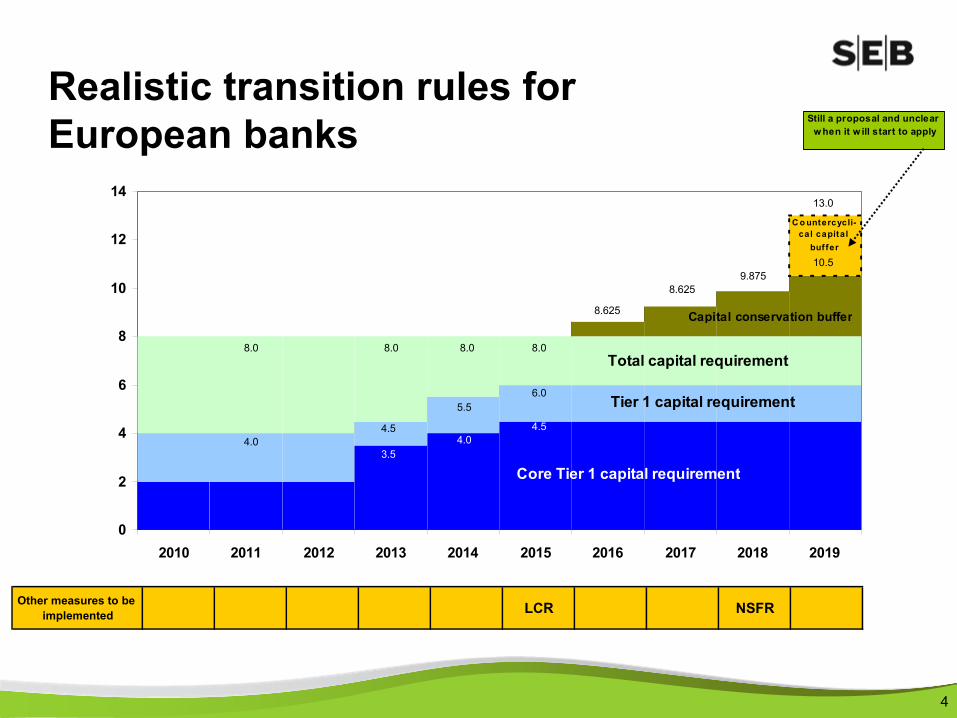

Realistic

transition

rules

for European banks

0

2

4

6

8

10

12

14

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

3.5

4.5

8.0

C o untercycli-cal capital

buf fer

8.0

5.5

4.04.5

6.0

8.0

Core Tier 1 capital requirement

Tier 1 capital requirement

Capital conservation buffer8.625

8.6259.875

10.5

13.0

Total capital requirement8.0

4.0

Still a proposal and unclear w hen it w ill start to apply

Other measures to be implemented LCR NSFR

4

Redefine bank capital

Introduce supplementary leverage ratios

Liquidity & funding ratios

Adjust for cyclical & systemic effects

Capture additional risk exposures

Basel III and impact on Nordic banks Five key areas of new regulation

1

2

3

4

5

5

13,9 14,3

12,111,7

14,514,7

Dec 2009 Jun 2010

Total capital ratio, %Tier I capital ratio, %Core Tier I

Capital adequacy without transitional floor

SEK bnCapital base 107.3

103.9RWA 730

714

EU stress tests and Basel III

Tier 1 ratio in EU stress test

Benchmark scenario: 11.8%

Adverse scenario: 10.7%

+sovereign shock: 10.3%

Basel III

Core tier 1 well above the aggregate of the required minimum plus conservation buffer and maximum countercyclical buffer

Combined effect of the redefined capital base and RWAs

of 100-

150bps on CT1 in 2012E

SEB’s

capitalisation more than adequate

6

7

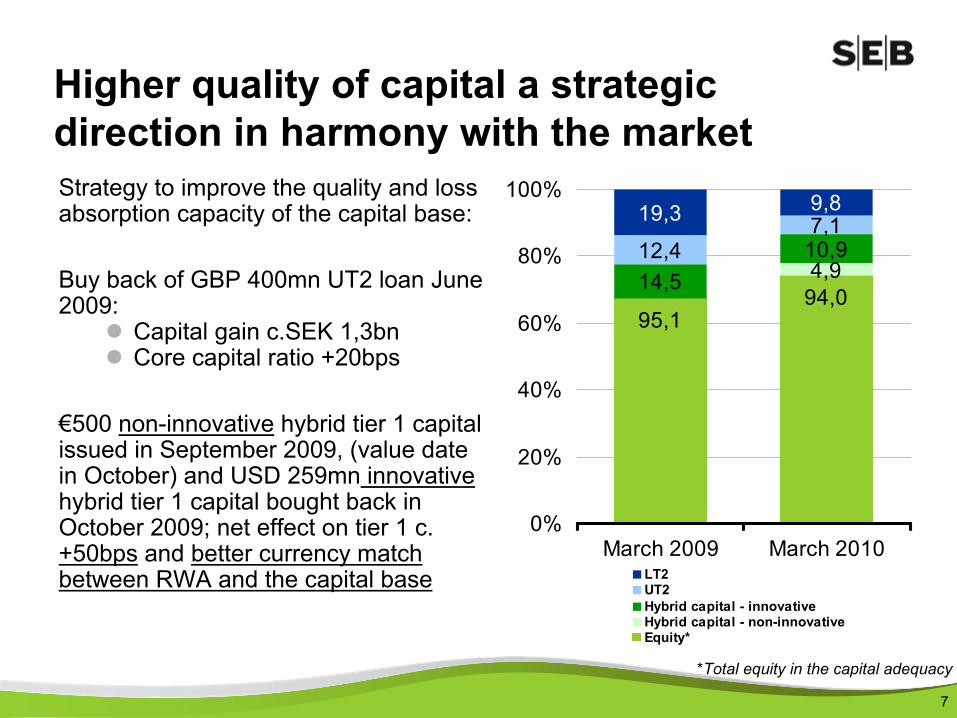

Higher quality of capital a strategic direction in harmony with the marketStrategy to improve the quality and loss absorption capacity of the capital base:

Buy back of GBP 400mn UT2 loan June 2009:

Capital gain c.SEK

1,3bn

Core capital ratio +20bps

€500 non-innovative

hybrid tier 1 capital issued in September 2009, (value date in October) and USD 259mn

innovative

hybrid tier 1 capital bought back in October 2009; net effect on tier 1 c. +50bps

and better currency match

between RWA and the capital base

95,194,04,914,5

10,912,47,119,3 9,8

0%

20%

40%

60%

80%

100%

March 2009 March 2010LT2UT2Hybrid capital - innovativeHybrid capital - non-innovativeEquity*

*Total equity in the capital adequacy

Capital management conclusions●

SEB has a large buffer to any new benchmark requirements

SEB can wait for details of non-common equity components to develop and the investment market’s acceptance of these

No conclusions for contingent capital and hybrid tier 1 capital yet

Size/Design of countercyclical and systemic (?) buffers still unclear

●

The buffer on top of all regulatory buffers can be small

Most potential scenarios already covered

●

Very unclear role for Tier 2 capital going forward

●

Normalization of dividend in accordance with dividend policy preferred route for returning capital as of now

8

SEB’s

balance sheet liquidity is structurally strong

Assets Equity & Liabilities

Balance sheet structure (June 2010)

Funding <1 year

Funding, remaining maturity

>1 year

Cash & Lending

Financial Institutions

Deposits from the publicOther

Lending

Net Bond portfolio

Equity

Short-term and Liquid

assets

Stable funding

Short-term funding

“Banking book”

Net Other trading

Deposits Financial

Institutions

Household Lending

9

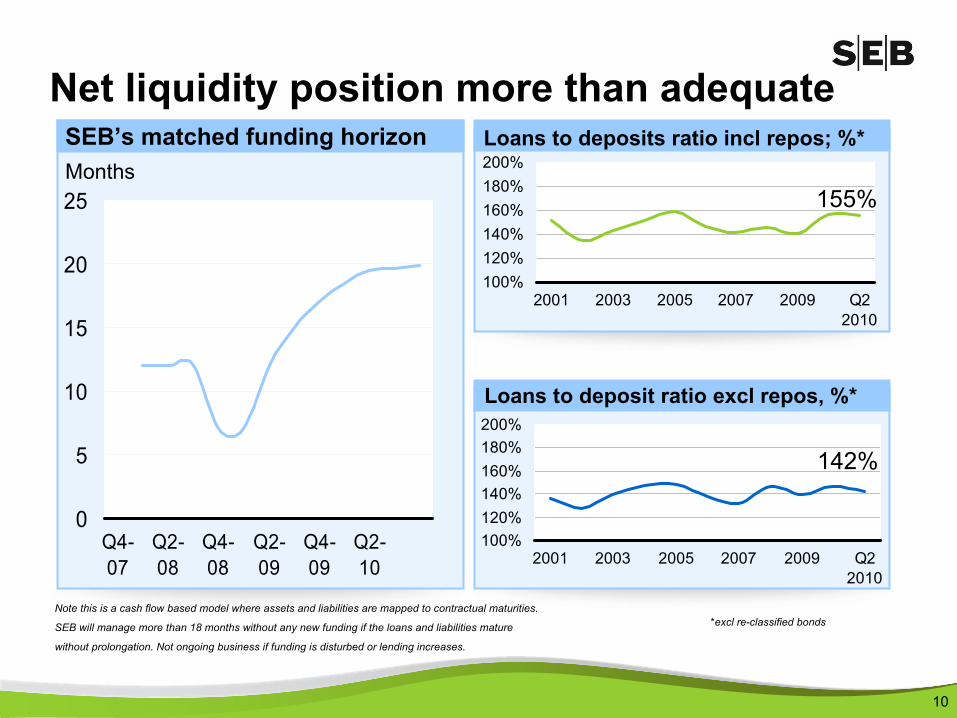

Loans to deposits ratio incl

repos; %*

Net liquidity position more than adequateSEB’s

matched funding horizon

Months

100%120%140%160%180%200%

2001 2003 2005 2007 2009 Q22010

155%

0

5

10

15

20

25

Q4-07

Q2-08

Q4-08

Q2-09

Q4-09

Q2-10

Loans to deposit ratio excl repos, %*

100%120%140%160%180%200%

2001 2003 2005 2007 2009 Q22010

142%

*excl

re-classified

bondsNote this is a cash flow based model where assets and liabilities are mapped to contractual maturities.

SEB will manage more than 18 months without any new funding if the loans and liabilities mature

without prolongation. Not ongoing business if funding is disturbed or lending increases.

10

Funding structure SEB Group, SEK 1,580bn, June 2010

Schuldscheins and Reg Bonds 1,3%

Mortgage Covered Bonds Germany

2,5%

Subordinated debt 2,0%

Deposits - General Public 42,2%

Senior debt 6,3%

Public Covered Bonds Germany 4,4%

CPs/CDs 10,8%

Deposits - Central Banks 7,6%

Mortgage Covered Bonds Sweden 10,1%

Deposits - Financial Institutions 13,0%

11

Managing NSFR●

Issuance of Swedish and German covered bonds and create cover pools for other loan classes

●

Increase and/or prolong deposit volume by either attracting new volumes or incentivizing

customers to transfer funds from mutual funds

●

Restructure lending by shortening duration or transfer corporate

lending to bonds that are kept in SEB’s

balance sheet

●

“Externalize”

lending by either securitizing parts of loan portfolio or assisting large corporates

to replace credit from SEB with bonds issued

to third parties (public issues or private placement)●

Reduce trading portfolios

●

Reduce credit facilities●

Issuance of senior unsecured debt

12

No rush –

and we still think it is a too rigid framework not fit for the Nordic markets

Managing Liquidity Coverage Ratio (LCR)●

SEB has a high quality liquidity portfolio in SEK and EUR

●

Further build-up of liquidity reserves can easily be funded by using the untapped potential in the mortgage cover pool

●

In addition, significant international Commercial Paper borrowing capacity

●

All collateral normally eligible for central bank borrowing purposes should qualify as liquidity reserve assets for the purposes of LCR

●

Local Swedish regulatory approach desirable

13

Requirements easy to meet –

but we would encourage a framework more geared to covered bonds

Liquidity management conclusions•

SEB has a diversified and functional funding starting point with

access

to all relevant funding markets

-

The transitional rules proposed means that the current liquidity management strategy remains valid

•

Customer Pricing will more accurately reflect costs of Capital-

On and off balance sheet consumption

-

Liquidity

•

The proposed Basel III framework remains structurally misaligned

to the robust Nordic funding markets

-

Too little credit given to covered bonds

-

Too little credit given to the robustness of corporate deposit

14

15

Summary

Redefine bank capital

Changes to capital definitions in line with SEB’s

current conservative risk and capital management

Under both the current and new rules, SEB remains among the best

capitalised banks in Europe

SEB’s

relative position vs. European peers is likely to improve as the impact of the new rules on SEB is estimated to be smaller than the European average–

New rules reflect full benefits of current high common equity component within Core Tier 1

A combined effect of the redefined capital base and RWAs

of 100-150bps on SEB’s

CT1 in 2012E

Capture additional risk exposures

Further details on proposed changes required for detailed assessment

Introduce supplementary leverage ratios

SEB within top quartile of European banking universe and within top half of Nordic banks due to high capital levels and minimal relative off balance sheet and credit derivative exposures

Liquidity & funding standards

Impact of Liquidity and Funding Ratios highly dependent on continued refinements by Committee

Long transition times allow ample time to adapt business model –

should Nordic characteristicse

not be recognized

Adjust for cyclical & systemic effects

In line with SEB’s

current dividend policy which is already based on a “through the cycle”

payout ratio–

Flexibility to be adjusted depending on “point in time”

capitalisation level

Proposed regulatory changes reinforce a more robust view on capital, echoing SEB’s

own capital and risk management strategy. All buffer capital requirements have not been set yet.

16