about the project - national food security...

TRANSCRIPT

About the ProjectThe need for monitoring and analysis of emerging food scenarios is important for India both because ofsignificant dependence of output on the monsoon rains and the fact that globally India is one of the majorconsumers of food crops influencing markets. Management of agriculture from a public policy perspectiverequires organisation of this information and analysis as inputs to policy making.

Against this backdrop the National Food Security Mission (NFSM), Ministry of Agriculture, commissioned a3–Year study to National Council of Applied Economic Research (NCAER) in 2011–12 to bridge thisimportant gap in analytical inputs for understanding the emerging agricultural scenarios both in the short-termof one or two quarters and also in the medium to longer term.

Accordingly, the agricultural outlook and situation analysis undertaken in this study refers to the main cropbased food items: cereals (specifically rice, wheat, jowar, bajra, maize and overall coarse grains), pulses (gram,tur), selected fruits and vegetables (banana, potato, onion), sugarcane and edible oils (groundnut, rapeseed/mustard, soybean). In addition the analysis also covers milk, one livestock product.

The three main outputs of the proposed work are:

(1) A Quarterly Agricultural Outlook Report that integrates the assessment of key indicators relating toagriculture with a focus on food sectors. The reports will include assessment of the current situation oninputs, output and market conditions and also forecasts of key indicators for the full year based on modelsdeveloped for the purpose.

(2) A Semi-annual Agricultural Outlook Report which provides a longer term perspective for the food sector.These reports will present an analysis of alternative scenarios of output and consumption for the food cropstaking into account the available information and based on the suitable economic models that permitlonger term projections.

(3) Monthly briefings on the prevailing agricultural conditions.

ImplementationNCAER has set up a study team to carry out the study.

An advisory committee has been formed to provide broad guidance to the implementation of the study. TheCommittee comprises of Dr Shekhar Shah, DG, NCAER as Chair, Dr Ashok Gulati, Chairman, Commissionon Agricultural Costs and Prices, Prof. Ramesh Chand, Director, National Centre for Agricultural Policy(NCAP), New Delhi and Prof. Mahendra Dev, Director, Indira Gandhi Institute for Development Research(IGIDR), Mumbai. Representative from FAO and DFID are Special Invitees to the Committee meetings.

A Technical Support Group comprising of key officers from different departments of the government andexperts has also been formed to interact with the study team to improve the work under the study.

Agricultural Outlook and Situation Analysis Reports

AGRICULTURAL OUTLOOK AND SITUATION ANALYSIS REPORTS

ii

Agricultural Outlook and Situation Analysis Reports

Quarterly Agricultural Outlook ReportOctober–December 2013

Under the Project Sponsored by The National Food Security MissionMinistry of Agriculture

March, 2014

Prepared by

National Council of Applied Economic Research11, I.P. Estate, New Delhi 110 002agrioutlookindia.ncaer.org

AGRICULTURAL OUTLOOK AND SITUATION ANALYSIS REPORTS

iv

AGRICULTURAL OUTLOOK AND SITUATION ANALYSIS REPORTS

vi

AGRICULTURAL OUTLOOK AND SITUATION ANALYSIS REPORTS

viii

The advance estimates of national accounts project overall growth of GDP at 4.9 per centin 2013–14, higher than the 4.5 per cent growth estimated in the previous year. Whileoverall economic growth remained low in agriculture and allied sectors registered a sharpimprovement in output. Favourable monsoon rainfall helped to improve agriculturalsector’s production prospects. Although excess rainfall towards the end of monsoon periodin some of the eastern and central India led to crop damage, the late rains helped improveprospects of the rabi crops with reported increases in sown area of the rabi crops. In fact,nearly all the estimated increase in foodgrain output in 2013–14, as per the 2nd AdvanceEstimates (AE) of the Ministry of Agriculture is in the rabi season.

The report also provides an assessment based on rainfall data and trend growth in outputof food commodities. As the official estimates are still subject to further revisions based onthe new data, we have provided these estimates for a comparison as the model basedestimates are valuable when they are obtained before the final estimates are available. As aresult of higher crop production, the year also saw deceleration in overall inflation rate andfood inflation especially towards the end of 2013. International market prices haveremained stable and lower in 2013 as compared to the previous year in a number ofcommodities. Although lower prices reflect adequate supplies to meet the globalrequirements at the present levels of consumption, they also point to the need for morecompetitive production of commodities to benefit from export demand. The exchange ratedepreciation provided some cushion to exports, but they also raise the cost of importedinputs and food commodities such as edible oils. Some of the production estimates aresummarised below:

� The 2nd AE of agricultural production for 2013–14 have raised the output estimatesof foodgrains to 263.2 million tonnes from the final estimates of 257.1 million tonnesin 2012–13. The estimates based on trend and rainfall provide higher estimate of267–272 million tonnes of foodgrain production. The main difference in the twoestimates is in the case of kharif rice and bajra production. The final estimates are likelyto be between the lower end of this range and the 2nd AE.

� Production of rice is placed at 106.2 million tonnes by the 2nd AE, marginal increaseover 105.2 million tonnes in the previous year. In the case of wheat, the 2nd AE placeproduction at 95.6 million tonnes, about 2 million tonnes more than the harvest in2012–13. Our estimates are for a production of 97.5 million tonnes. As per the 2ndAE, production of coarse grains in 2013–14 is estimated at 41.6 million tonnes, upfrom about 40 million tonnes in the previous year. Our assessment is higher at44.1–44.5 million tonnes mainly because of higher production estimate of bajra.

� Pulses production is estimated by the 2nd AE at 19.8 million tonnes, close to ourassessment of 19.4–19.7 million tonnes.

� Among the major oilseeds, production of groundnut is projected by the 2nd AE at 9.1million tonnes, up from a low 4.7 million tonnes in the previous year. In the case ofsoybean, the 2nd AE of production, the 2013–14 output is about 2 million tonnes

Highlights

ix

lower than the revised estimate of 14.67 million tonnes in the previous year. Therapeseed and mustard production is projected to be maintained at about 8 milliontonnes. The overall production of nine major oilseeds is projected at 33 million tonnes,up from 30.9 million tonnes in the previous year. The estimates based on rainfall andtrend data indicate production of the nine major oilseeds at 36.22 million tonnes.While the two estimates are close in the case of rapeseed and mustard, the differencesare greater in the other cases. The main difference is in the case of kharif oilseeds.

� Sugarcane production is 345.9 million tonnes, up from 341.77 million tonnes in theprevious year. The estimates based on trend and rainfall place production in 2013–14at 353.8–356 million tonnes.

� The output of onion in 2013–14 is estimated to have increased to 18–19 milliontonnes, up from 16.8 million tonnes in the previous year. Potato production isestimated at 44.8–46.4 million tonnes, marginally higher than the production estimatefor the previous year. In the case of milk, production is estimated to increase by 4.3–4.5per cent in 2013–14 over the 132.43 million tonnes production in the previous year.

The price scenario during the year has generally reflected production conditions. The year-on-year increase in the Wholesale Price Index (WPI) for food articles dropped from closeto 19 per cent between August and November 2013 to below 14 per cent in December2013 as the impact of kharif harvest began to have an impact on prices. In the case ofonion, the price rise dropped from the height of triple digit annual rates to double digitrate by December 2013 and further to 8.8 per cent in January 2014. A key feature of theoverall price scenario is the stable prices of food commodities in the international markets.The FAO Food Price Index has shown negative year-on-year changes throughout 2013 asglobal production recovered from the drought effects of the previous year. Short-termprojections of the food price scenario indicates that year-on-year food inflation, based onWPI, may remain at 6–7 per cent in the next 2–3 months.

Using the data from FAO and also consumption expenditure surveys of the NationalSample Survey Organisation, the present report also draws attention to the trends in foodconsumption. While there is a trend increase in the per capita consumption of calories andfats improvement in the consumption of proteins has been marginal over the years. Morestriking is the change in terms of sources of nutrition: per capita consumption of livestockproducts is rising and becoming a growing source of calories and proteins relative tovegetable sources. The trends are similar in rural and urban areas. The changing trendsreflect changing consumer preferences and also availability of food commodities.

AGRICULTURAL OUTLOOK AND SITUATION ANALYSIS REPORTS

x

The study team wishes to acknowledge the support of Mr Ashish Baahuguna, Secretary,Department of Agriculture and Cooperation, to our work. He has encouraged the studyteam to improve the contents of these reports throughout the course of this study. Dr J.S.Sandhu, Agriculture Commissioner and Mr S. Lohiya, Joint Secretary (Crops), haveprovided guidance in the conduct of the study. A number of officials in the agricultureministry have participated in the meetings and other interactions held in the context of thepresent study and contributed to our understanding of the issues related to theperformance of the sector.

Reports of FAO, OECD, USDA, ABARES, IGC, and a number of other agencies havebeen referred in this report. We acknowledge the information and insights that have beenvaluable to us in the preparation of this report.

The advisory committee for the report and the technical support group have providedinputs during the course of this project on Agricultural Outlook and Situation AnalysisReports commissioned by the National Food Security Mission.

We are grateful to the experts who have contributed to our understanding of issues relatingto different aspects of the food sector. We have listed at the end of this report thepresentations that were made by these experts during the period of October 2013–March2014.

Acknowledgements

xi

Study Team

Shashanka Bhide (Project Leader), A. Govindan, Saurabh Bandyopadhyay,Mondira Bhattacharya, Laxmi Joshi, S.K. Mondal, V.P. Ahuja, Amar Singh, PalashBarua, Charu Jain, Himani Gupta, Praveen Sachdeva, Prem Mohan Srivastava,Rahul Thakur and Abjitej Kodali. J.S. Punia has coordinated production of thisreport.

AGRICULTURAL OUTLOOK AND SITUATION ANALYSIS REPORTS

xii

Preface . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .v

Foreword . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .vii

Highlights . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .ix

Acknowledgements and Study Team . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .xi

List of Tables . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .xv

List of Figures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .xvii

I. Overview of the Domestic Agriculture Outlook . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1

II. Overview of the Global Food Outlook . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .11

III. Factors Influencing Food Outlook . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .25

IV. Commodity Outlook Assessment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .45

IV.1 Rice . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .45

IV.2 Wheat . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .49

IV.3 Coarse Grains . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .53

IV.4 Pulses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .55

IV.5 Edible Oilseeds and Oils . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .59

IV.6 Sugarcane and Sugar . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .66

IV.7 Potato . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .72

IV.8 Onion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .80

IV.9 Banana . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .89

IV.10 Milk . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .97

V. Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .103

Contents

xiii

xiv

I.1 2013–14 Crop Forecasts (Million Tonnes) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .5

I.2 Year-on-Year Inflation Trend in Major Food Commodities: WPI % change YOY . . . . . . . . . . . . . . . . . . . .7

I.3a Recent Trends in Food Prices: WPI and International Price, % YOY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .8

I.3b Projections of Wholesale Prices in Delhi Based on Harmonic Analysis: % Change YOY . . . . . . . . . . . . . . .8

I.3c Projections of National Level WPI Based on ARIMA Models: % Change YOY and MOM . . . . . . . . . . .9

I.4 Supply-Demand Balances for Selected Food Commodities (Thousand Tonnes) . . . . . . . . . . . . . . . . . . . . . .9

II.1 Global Production Forecasts for Major Food Commodities (Million Tonnes) . . . . . . . . . . . . . . . . . . . . . . .13

II.2 CBOT Futures Price Quotes US$/MT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .20

III.1 Per Capita Income Growth During the Recent Decades . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .26

III.2 Agri-Policy Developments during October 2013 to January 2014 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .44

IV.1.1 Government Operations in Rice . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .47

IV.1.2 Supply and Demand Balance for Rice (Thousand Tonnes) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .48

IV.2.1 Government Operations in Wheat . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .50

IV.2.2 Supply and Demand Balance for Wheat (Thousand Metric Tonnes) . . . . . . . . . . . . . . . . . . . . . . . . . . . . .52

IV.3.1 Demand Supply Balance Sheet for Maize (Thousand Tonnes) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .55

IV.4.1 Demand and Supply Balance Sheet for Pulses (Thousand Tonnes) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .59

IV.5.1 Sowing of Rabi Oilseeds (Lakh Hectare): 2013 and 2014 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .59

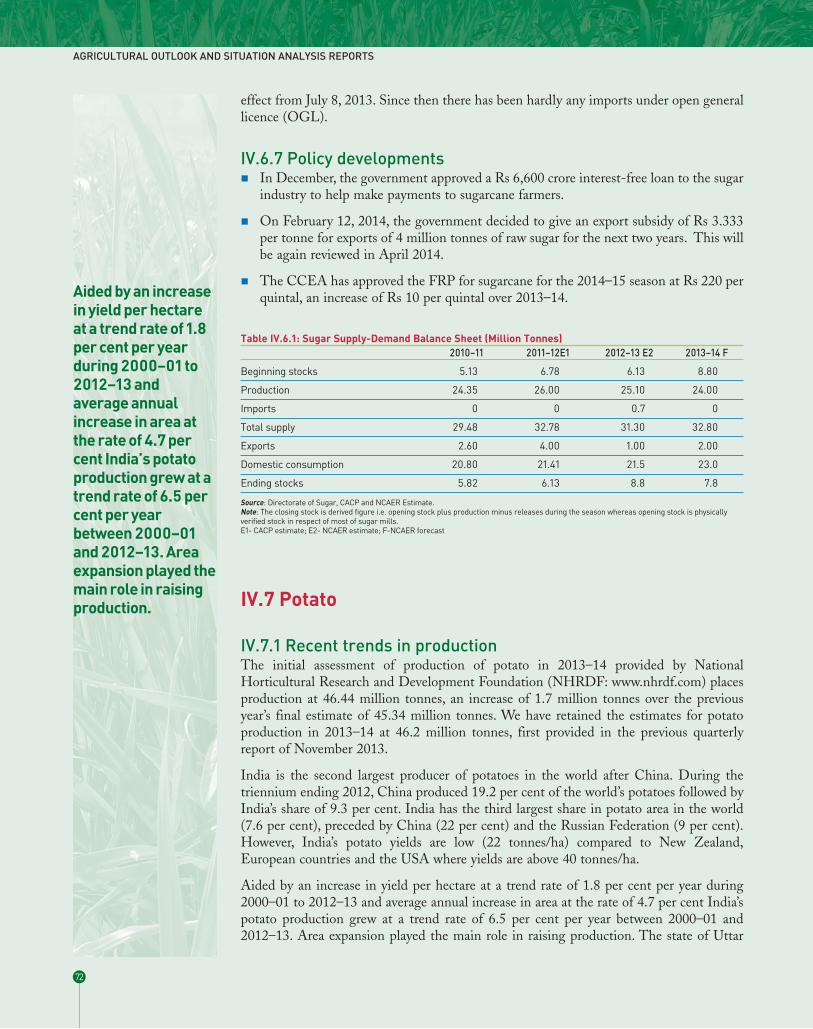

IV.6.1 Sugar Supply-Demand Balance Sheet (Million Tonnes) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .72

IV.7.1 Trends in Area, Production and Yield in Major Potato Producing States and Share of States in Area and Production . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .73

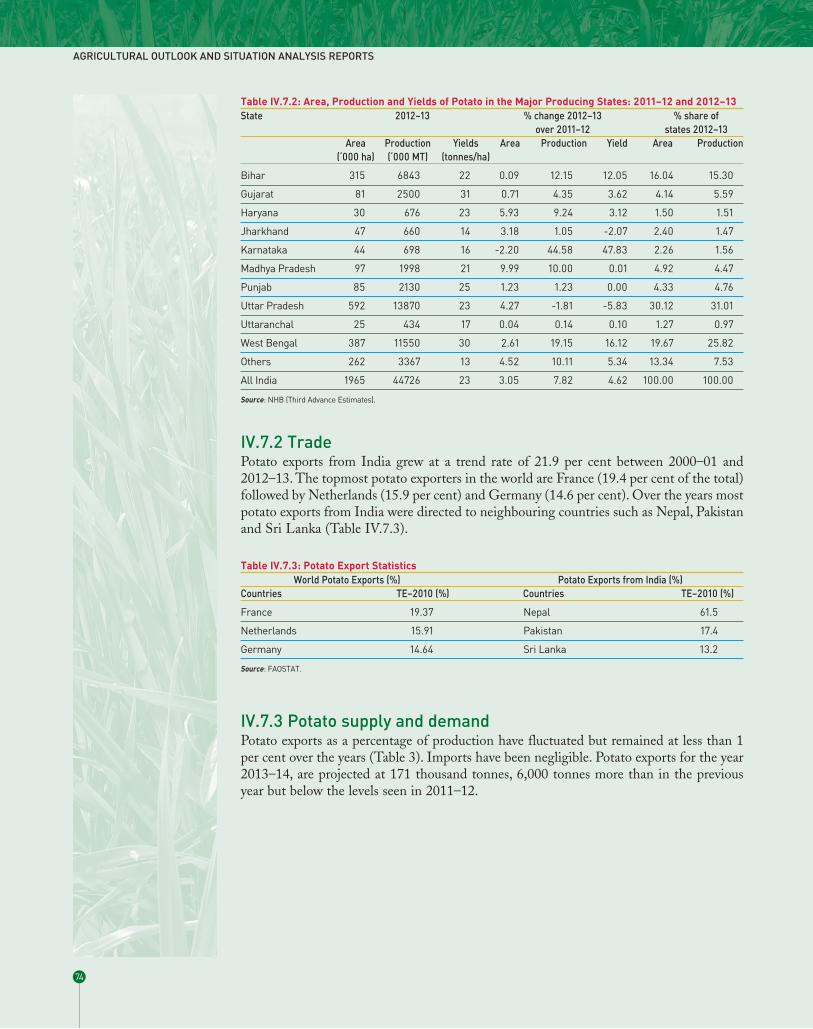

IV.7.2 Area, Production and Yields of Potato in the Major Producing States: 2011–12 and 2012–13 . . . . . . . . . .74

IV.7.3 Potato Export Statistics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .74

IV.7.4 Potato Supply and Demand (Thousand Tonnes) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .75

IV.7.5 Potato Market Arrivals and Prices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .79

IV.7.6 Futures Prices of Potato . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .79

IV.8.1 Onion Production Statistics: Major States . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .81

IV.8.2 State-wise Area, Production and Yield of Onion: 2012–13 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .82

IV.8.3 Season-wise Area, Production and Yield of Onion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .82

List of Tables

xv

IV.8.4 Onion Export Statistics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .83

IV.8.5 Onion Supply and Demand (Thousand Tonnes) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .83

IV.9.1 Area, Production and Yield of Banana in the Major Producing States and All-India level . . . . . . . . . . . . .90

IV.9.2 Banana Export Trends . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .91

IV.9.3 Banana Supply and Demand (Thousand Tonnes) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .91

IV.9.4 Monthly Price Differential – Wholesale & Retail . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .94

IV.10.1 Milk Production and Yield 2012–13 – Major Indian States . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .98

IV.10.2 Per Capita World Dairy Consumption (Kg/Year) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .99

IV.10.3 WPI of Milk Relative to the Selected Other Livestock Products and Inputs: 2004–05=100 . . . . . . . . . . .101

List of Tables

xvi

I.1 GDP Growth – Agriculture& Allied vs. Overall . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .2

I.2 Agricultural Production Trends . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .2

I.3 Food Inflation Exceeds Overall Inflation Rate . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .7

II.1 Global Price Trend of Major Commodities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .16

II.2 Stocks-to-Use Ratio of Major Agricultural Commodities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .22

III.1a Trend in Cereal Consumption – Rural . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .26

III.1b Trend in Cereal Consumption – Urban . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .27

III.2 Trends in Per Capita Rice Consumption . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .27

III.3 Trends in Per Capita Wheat Consumption . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .28

III.4 Trends in Per Capita Consumption of Coarse grains . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .28

III.5 Trends in Per Capita Consumption of Pulses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .29

III.6 Trends in Per Capita Edible Oil Consumption . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .29

III.7 Changes in the Composition of Edible Oils in Consumption . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .30

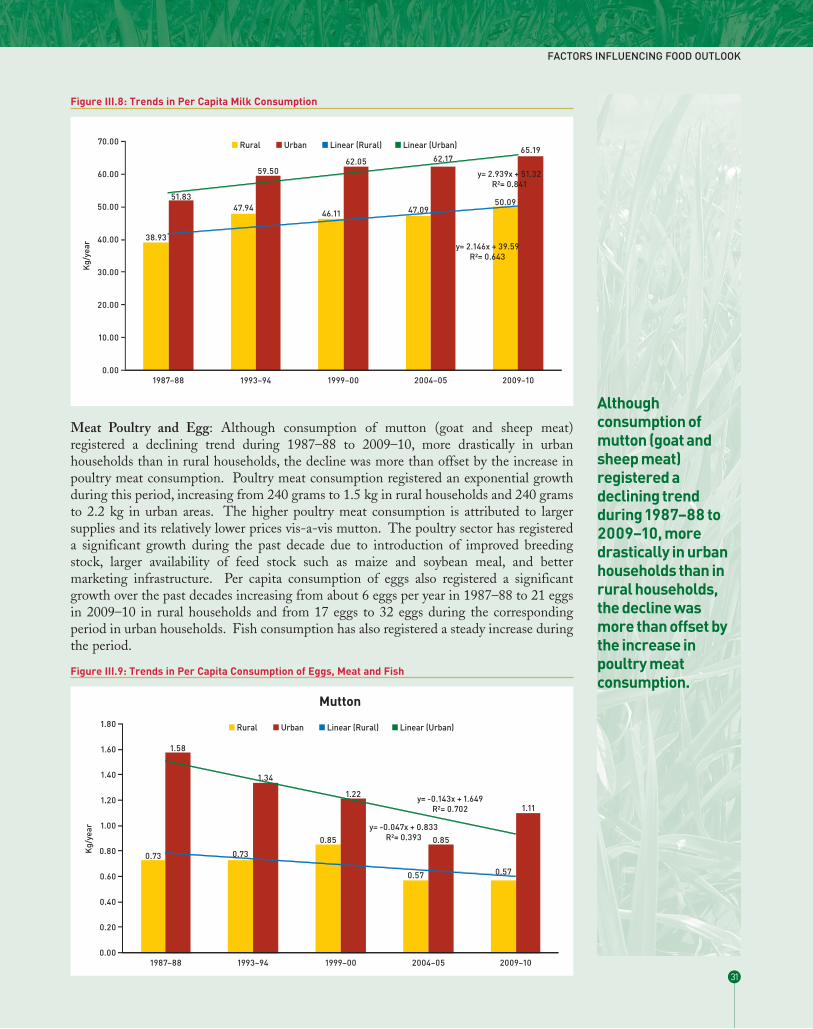

III.8 Trends in Per Capita Milk Consumption . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .31

III.9 Trends in Per Capita Consumption of Eggs, Meat and Fish . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .31

III.10 Trends in Per Capita Consumption of Onion, Potato and Banana . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .33

III.11 Trends in Per Capita Consumption of Calories, Protein and Fats . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .35

III.12 Trends in Composition of Calories: Animal and Vegetable Products . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .35

III.13 Trends in Composition of Per Capita Calorie Intake by Type of Food . . . . . . . . . . . . . . . . . . . . . . . . . . . .36

III.14 Trends in Composition of Per Capita Calorie Intake by Type of Food: % of Calorie Intake . . . . . . . . . . . .36

III.15 Trends in Per Capita Protein Intake by Animal and Vegetable Sources . . . . . . . . . . . . . . . . . . . . . . . . . . . .38

III.16 Trends in Per Capita Protein Intake by Type of Food . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .38

III.17 Trends in the Composition of Protein Intake by Type of Food: % of Protein . . . . . . . . . . . . . . . . . . . . . . .39

III.18 Per Capita Nutrient Intake in India, China and US . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .41

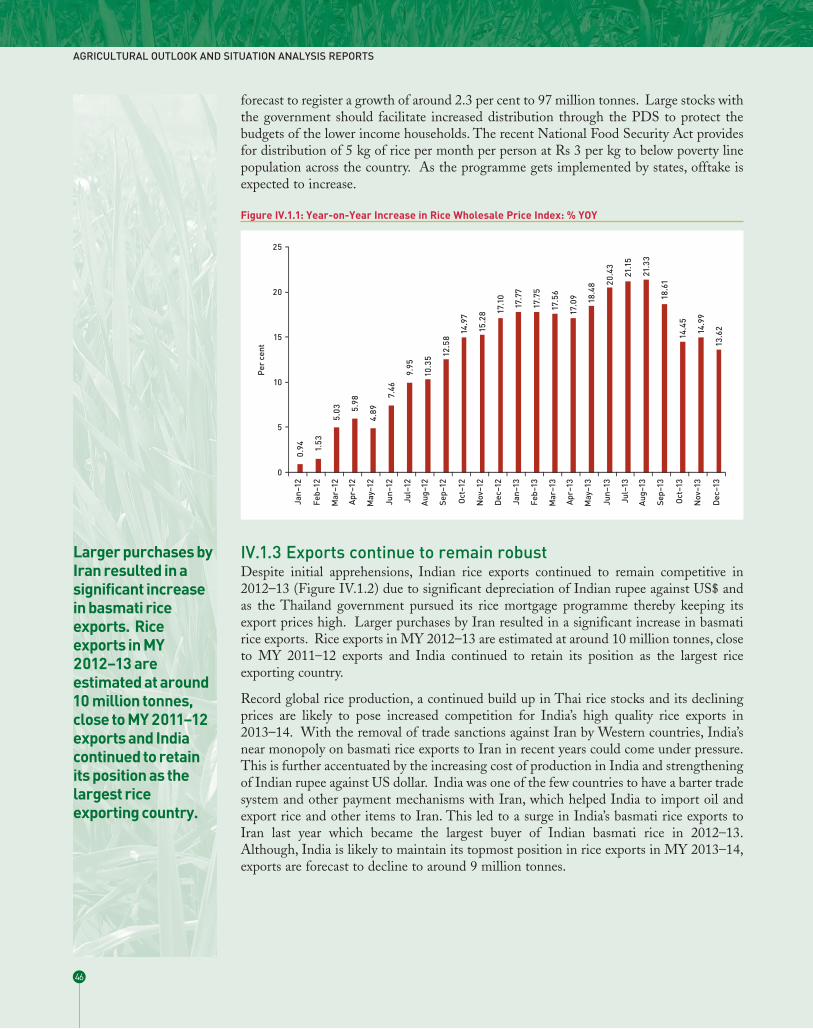

IV.1.1 Year-on-Year Increase in Rice Wholesale Price Index: % YOY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .46

IV.1.2 Rice Export Price – India vis-a-vis International . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .47

IV.1.3 Government Rice Stocks – Actual vs. Buffer Norm . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .48

IV.2.1 Wheat Price Inflation: WPI (% YOY) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .50

IV.2.2 Indian Wholesale Wheat Price vis-à-vis US SRW Wheat Price FOB . . . . . . . . . . . . . . . . . . . . . . . . . . . .51

IV.2.3 Government Wheat Stocks – Actual vs. Buffer Norm . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .52

IV.3.1 Coarse Grain Production Trend . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .54

IV.3.2 Maize Price Comparison US vs. India . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .55

List of Figures

xvii

IV.4.1 Trend in Area, Yield, and Production of Pulses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .56

IV.4.2 Trend in Pulse Production by Type . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .57

IV.4.3 Trend in Minimum Support Prices for Pulses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .57

IV.4.4 Wholesale Price Inflation Trend in Pulses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .58

IV.5.1 Edible Oil Production and Consumption . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .60

IV.5.2 Oilseed and Vegetable Oil Price Inflation (YoY % Change) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .61

IV.5.3 Wholesale Price Index of Rapeseed and Mustard, Palm Oil and International Price of Palm Oil (YOY % Change) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .61

IV.5.4 Arrival and Prices of Groundnut in Gondal market in Rajkot District of Gujarat . . . . . . . . . . . . . . . . . . .62

IV.5.5 Arrival and Prices of Soybean . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .62

IV.5.6 Arrival and Prices of Rapeseed and Mustard . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .64

IV.5.7 Total Imports of Edible Oils (Oil Year from Nov–Oct) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .65

IV.5.8 Share of Different Oils in Total Imports . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .65

IV.6.1 Sugarcane Area, Production and Yield Trends . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .67

VI.6.2 Sugarcane and Sugar Production Trend . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .68

IV.6.3 Indian Sugar Cycle . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .68

IV.6.4 All India Sugar Price and Year-on-Year Change in WPI of Sugar . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .69

IV.6.5 Fair Average Price (FRP) for Sugarcane and Actual Price Paid to Famers . . . . . . . . . . . . . . . . . . . . . . . . .70

IV.6.6 Sugar Beginning Stocks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .71

IV.7.1 Area, Production and Yield of Potato in India . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .73

IV.7.2 WPI Trends in Potato . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .75

IV.7.3 Comparison between Average % YoY of WPI from 2006 to 2011 and % YoY of 2012 over 2013 . . . . . . .76

IV.7.4 Wholesale Prices of Potato in Selected Cities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .77

IV.7.5 Retail Prices of Potato in Selected Cities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .77

IV.7.6 Per day Average Arrivals of Potatoes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .78

IV.8.1 Area, Production and Yield of Onion in India . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .81

IV.8.2 Wholesale Price Index of Onion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .84

IV.8.3 Comparison between Average % YoY of WPI from 2006 to 2011 and % YoY of 2012 over 2013 . . . . . . .84

IV.8.4 Wholesale Prices of Onion in Cities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .85

IV.8.5 Retail Prices of Onion in Metro Cities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .86

IV.8.6 Per Day Average Arrivals of Onion in Selected Wholesale Markets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .87

IV.9.1 Area, Production and Yield of Banana . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .90

IV.9.2 WPI of Banana Relative to WPI of Fruits and Food Articles . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .92

List of Figures

xviii

IV.9.3 Comparison between Average % YoY of WPI from 2006 to 2011 and % YoY of 2012 over 2013 . . . . . . .92

IV.9.4 Wholesale Prices of Banana in Selected Cities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .93

IV.9.5 Retail Prices of Banana in Selected Cities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .94

IV.9.6 Per Day Average Arrivals of Bananas . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .95

IV.10.1 Compound Decadal Growth Rate of Milk Production . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .97

IV.10.2 Average Milk Yield/day . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .99

IV.10.3 Trends in the WPI for Milk and Foodgrains: % YOY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .100

IV.10.4 FAO International Dairy Price Index – % change YOY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .101

List of Figures

xix

xx

I.1 Economic Growth Sluggish, but Agricultural GrowthUpbeatImproved agricultural growth has contributed to achieving a higher growth rate of theeconomy in the current year as compared to 2012–13. The Advance Estimates of India’snational income statistics, the first official estimates for India’s GDP for 2013–14 releasedon Feb 7, 2014, indicate that the economy grew at an annual rate of 4.9 per cent followingan even slower growth rate of 4.5 per cent in the previous year. Agricultural growth hasbeen projected at 4.6 per cent as compared to a mere 1.4 per cent in 2012–13.

A number of agencies were predicting a modest growth of the economy in the current year.The Reserve Bank of India (RBI) in its Second Quarter Review of Monetary Policy2013–14 scaled down India’s economic growth forecast for FY 2013–14 to 5 per cent fromthe earlier projection of 5.5 per cent, citing downside risk stemming from domesticconstraints. The International Monetary Fund (IMF) and the Asian Development Bank(ADB) were pegging growth somewhat lower.

A highly favourable south west monsoon in 2013 resulted in higher production of mostkharif grains, pulses and oilseeds. The first advance estimates of agricultural productionby the Ministry of Agriculture, released towards the end of September 2013, placed khariffoodgrain production at 129.32 million tonnes, above the 128.2 million tonnes in theprevious year. However, the 2nd AE released in February 2014, have dropped the khariffoodgrain production to 128.4 million tonnes, just above the 2012–13 estimates.Nevertheless, the first assessment of the overall production of crop output for the full year2013–14 shows that foodgrain output for the year is expected to be a new record exceeding263 million tonnes.

Combined with estimated higher production of oilseeds, fruits and vegetables, other crops,livestock products (primarily milk), and forestry and fisheries resulted in an overallagricultural and allied sector year-on-year GDP growth rate of 4.6 per cent for 2013–14.The Economic Advisory Council of the Prime Minister (EAC) in September 2013 hadprojected agricultural sector’s GDP growth rate in FY 2013–14 at 4.8 per cent comparedto less than 2 per cent in 2012–13 on the basis of normal monsoon rains.

PART I

Overview of the DomesticAgriculture Outlook

1

The 2nd AE releasedin February 2014,have dropped thekharif foodgrainproduction to 128.4million tonnes, justabove the 2012–13estimates.Nevertheless, thefirst assessment ofthe overallproduction of cropoutput for the fullyear 2013–14 showsthat foodgrain outputfor the year isexpected to be a newrecord exceeding263 million tonnes.

AGRICULTURAL OUTLOOK AND SITUATION ANALYSIS REPORTS

2

Figure I.1: GDP Growth – Agriculture & Allied vs. Overall

Figure I.2: Agricultural Production Trends

Rice Wheat C. Grains Pulses Total Sugarcane Potato Onion Bannana MilkOilseeds

2008–09 99.18 80.68 40.03 14.57 27.72 285.03 34.40 13.57 26.20 112.202009–10 89.09 80.80 33.55 14.66 24.88 292.30 36.60 12.16 26.50 116.402010–11 95.98 86.87 43.40 18.24 32.48 342.38 42.30 15.12 29.80 121.802011–12 105.31 94.88 42.04 17.09 29.80 361.07 41.48 17.51 28.46 127.902012–13 105.24 93.51 40.04 18.34 30.94 341.20 42.48 16.82 30.28 133.002013–14 # 106.19 95.60 41.64 19.77 32.98 345.92 44.80 18.00 30.90 138.10

# Final Estimate for rice, wheat, coarse grains, pulses, oilseeds and sugarcane.

I.2 Excess Rains Temper Kharif ProspectsDespite a favourable monsoon in 2013, the 2nd advance estimate of crop productionbrought out in February 2014 by the Ministry of Agriculture pegged 2013–14 khariffoodgrain production at 128.4 million tonnes, with only a marginal increase over 2012–13production of 128.1 million tonnes. A 0.4 million tonne decline in rice production,estimated at 92 million tonnes was offset by higher production of maize. Some of thedownward revision in production estimates from the 1st AE appears to be related to theadverse impact of the super cyclone Phailin which hit India’s eastern coast on October 12,2013 and subsequent heavy rains in Andhra Pradesh and Orissa raising the likelihood ofsome reduction in the initial assessment of kharif production.

Kharif pulses production is estimated to have increased by 0.3 million tonnes in 2013–14reaching 6.25 million tonnes. Tur (pigeon pea) and Moong (green gram) contributed tohigher production although Urd (black gram) output was lower in the present kharifseason.

The 2013–14 kharif oilseed production is estimated 1.2 million tonnes higher at 22.0million tonnes as per the 2nd AE with most of the increase coming from groundnut.Unseasonal heavy rains coinciding with soybean harvest in central India is reported to havecaused serious damage to soybean crop, leading to an estimated decline of 2.2 milliontonnes, as per the 2nd AE, from the previous harvest of 14.7 million tonnes.

Sugarcane output, which reaches the harvesting stage towards the end of the kharif seasonis estimated to be 345.9 million tonnes in 2013–14, 4 million tonnes higher than 2012–13.The estimates production for 2013–14 remains lower than the previous peak harvest of361 million tonnes in 2011–12.

I.3 Rabi Outlook PromisingThe above normal monsoon rains in most parts of the county in 2013 and its latewithdrawal provided favourable conditions for the planting of rabi crops. Although rainfallin the sowing period of Oct–December 2013 was below long period average (LPA) in thenorth west region, rabi planting was not affected adversely. Progressive rabi crop plantingdata shows a significant increase in wheat area and some increases in oilseed and pulsesarea but a marginal decline in coarse gain area. Growing conditions have been favourable.Rainfall during January has been above LPA in the northwest and central regions whererabi crop is important. Water storage in major reservoirs in early January at 105.15 BCMis significantly higher than a year ago level of 84.92 BCM and the 10 year average level of85.17 BCM, benefiting the mostly irrigated rabi crops. As a result, production of most rabicrops, is expected to higher in 2013–14 as compared to the previous year.

The overall economic environment in terms of prices paid by the farmers has been mixedfor rabi season. The energy prices have registered significant increase during the year2013–14 with both diesel and electricity prices rising at double digit rate over the previousyear. The wage rates have also shown significant increase during the year. The fertiliser andpesticide prices have increased at modest rate of less than 5 per cent over the previous yearand the WPI for manufactured products as whole also registered an increase of less than 5per cent. The rupee depreciated by about 14 per cent over the previous year during thesecond half of the year providing some support to agricultural exports but also makingimports expensive. Thus, while some of the key inputs such as fertilisers and machineryprices remained relatively stable, labour and energy inputs became expensive.

OVERVIEW OF THE DOMESTIC AGRICULTURE OUTLOOK

3

The above normalmonsoon rains inmost parts of thecounty in 2013 andits late withdrawalprovided favourableconditions for theplanting of rabicrops. Althoughrainfall in the sowingperiod ofOct–December 2013was below longperiod average (LPA)in the north westregion, rabi plantingwas not affectedadversely.Progressive rabicrop planting datashows a significantincrease in wheatarea and someincreases in oilseedand pulses area but amarginal decline incoarse gain area.Growing conditionshave beenfavourable. Rainfallduring January hasbeen above LPA inthe northwest andcentral regionswhere rabi crop isimportant.

The 2nd AE for 2013–14 places rabi production of foodgrains at 134.84 million tonnesabove the 129.06 million tonnes harvested in 2012–13. It is also the highest ever rabiharvest of foodgrains. The increase is contributed by cereals (4.64 million tonnes) andpulses (1.4 million tonnes). Among the rabi cereals, wheat is projected to contribute 2.09million tonnes to the increased production and gram accounts for 1 million tonnes of theincreased production of 1.4 million tonnes of pulses in 2013–14 over the previous year.Thus, even though kharif production is expected to show marginal improvement over theprevious year’s kharif season, the late withdrawal of rains at the end of south-westmonsoon helped improve area under rabi crops and also yields.

The production of nine major oilseeds as a whole in 2013–14 is now placed at 33 milliontonnes, up from 31 million tonnes in 2012–13. Rapeseed and mustard is projected toincrease by 0.22 million tonnes in the current year over the harvested 8.03 million tonnesin the previous year.

Among the fruits and vegetables covered in this report, our estimate of production ofpotato is 44.8 million tonnes, about the same as the 3rd AEs of production of 44.7 milliontonnes in 2012–13. Although, at an overall level rains in the south-west monsoon seasonwere favourable, the rainfall was not favourable in the eastern and north-eastern regions.However, the present estimates of production for 2013–14 available from NationalHorticulture Board are higher at 46.4 million tonnes. In the case of onion, production isestimated to exceed 18 million tonnes, about 1.5 million tonnes higher than in 2012–13.Adequate rainfall in the monsoon period helped improve production of onions in thecurrent year. The present estimates for 2013–14 available from NHRDF place productionof onions at 19 million tonnes. In the case of banana, our estimates place production at30.9 million tonnes, significantly higher than the estimated production (NHRDF) of 24.9million tonnes in 2012–13. We have retained the estimated milk production of138.1–138.4 million tonnes in 2013–14 lower than the targeted 139.7 million tonnes.

While the official estimates of production are now available for 2013–14, they are still notfinal as the rabi crop is yet to be harvested. For a comparison we have provided estimatesof production of food commodities for both the kharif and rabi seasons of 2013–14 basedon the statistical analysis of trends in output and the impact of rainfall during the cropseason. There are some significant deviations in estimates in some cases such as kharif rice,bajra and soybean where assessments based on trend and rainfall exceed the 2nd AE.

AGRICULTURAL OUTLOOK AND SITUATION ANALYSIS REPORTS

4

While the officialestimates ofproduction are nowavailable for2013–14, they arestill not final as therabi crop is yet to beharvested. For acomparison we haveprovided estimatesof production of foodcommodities forboth the kharif andrabi seasons of2013–14 based onthe statisticalanalysis of trends inoutput and theimpact of rainfallduring the cropseason. There aresome significantdeviations inestimates in somecases such as kharifrice, bajra andsoybean whereassessments basedon trend and rainfallexceed the 2nd AE.

OVERVIEW OF THE DOMESTIC AGRICULTURE OUTLOOK

5

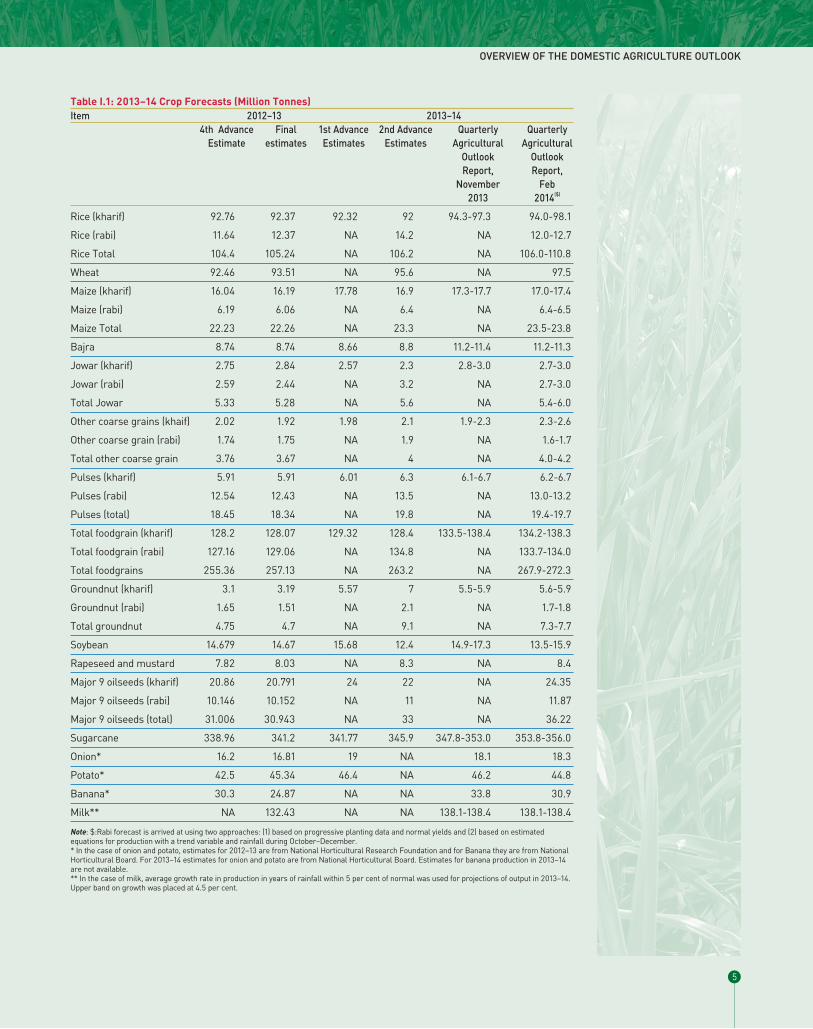

Table I.1: 2013–14 Crop Forecasts (Million Tonnes)Item 2012–13 2013–14

4th Advance Final 1st Advance 2nd Advance Quarterly QuarterlyEstimate estimates Estimates Estimates Agricultural Agricultural

Outlook OutlookReport, Report,

November Feb2013 2014($)

Rice (kharif) 92.76 92.37 92.32 92 94.3-97.3 94.0-98.1

Rice (rabi) 11.64 12.37 NA 14.2 NA 12.0-12.7

Rice Total 104.4 105.24 NA 106.2 NA 106.0-110.8

Wheat 92.46 93.51 NA 95.6 NA 97.5

Maize (kharif) 16.04 16.19 17.78 16.9 17.3-17.7 17.0-17.4

Maize (rabi) 6.19 6.06 NA 6.4 NA 6.4-6.5

Maize Total 22.23 22.26 NA 23.3 NA 23.5-23.8

Bajra 8.74 8.74 8.66 8.8 11.2-11.4 11.2-11.3

Jowar (kharif) 2.75 2.84 2.57 2.3 2.8-3.0 2.7-3.0

Jowar (rabi) 2.59 2.44 NA 3.2 NA 2.7-3.0

Total Jowar 5.33 5.28 NA 5.6 NA 5.4-6.0

Other coarse grains (khaif) 2.02 1.92 1.98 2.1 1.9-2.3 2.3-2.6

Other coarse grain (rabi) 1.74 1.75 NA 1.9 NA 1.6-1.7

Total other coarse grain 3.76 3.67 NA 4 NA 4.0-4.2

Pulses (kharif) 5.91 5.91 6.01 6.3 6.1-6.7 6.2-6.7

Pulses (rabi) 12.54 12.43 NA 13.5 NA 13.0-13.2

Pulses (total) 18.45 18.34 NA 19.8 NA 19.4-19.7

Total foodgrain (kharif) 128.2 128.07 129.32 128.4 133.5-138.4 134.2-138.3

Total foodgrain (rabi) 127.16 129.06 NA 134.8 NA 133.7-134.0

Total foodgrains 255.36 257.13 NA 263.2 NA 267.9-272.3

Groundnut (kharif) 3.1 3.19 5.57 7 5.5-5.9 5.6-5.9

Groundnut (rabi) 1.65 1.51 NA 2.1 NA 1.7-1.8

Total groundnut 4.75 4.7 NA 9.1 NA 7.3-7.7

Soybean 14.679 14.67 15.68 12.4 14.9-17.3 13.5-15.9

Rapeseed and mustard 7.82 8.03 NA 8.3 NA 8.4

Major 9 oilseeds (kharif) 20.86 20.791 24 22 NA 24.35

Major 9 oilseeds (rabi) 10.146 10.152 NA 11 NA 11.87

Major 9 oilseeds (total) 31.006 30.943 NA 33 NA 36.22

Sugarcane 338.96 341.2 341.77 345.9 347.8-353.0 353.8-356.0

Onion* 16.2 16.81 19 NA 18.1 18.3

Potato* 42.5 45.34 46.4 NA 46.2 44.8

Banana* 30.3 24.87 NA NA 33.8 30.9

Milk** NA 132.43 NA NA 138.1-138.4 138.1-138.4

Note: $:Rabi forecast is arrived at using two approaches: (1) based on progressive planting data and normal yields and (2) based on estimatedequations for production with a trend variable and rainfall during October–December.* In the case of onion and potato, estimates for 2012–13 are from National Horticultural Research Foundation and for Banana they are from NationalHorticultural Board. For 2013–14 estimates for onion and potato are from National Horticultural Board. Estimates for banana production in 2013–14are not available.** In the case of milk, average growth rate in production in years of rainfall within 5 per cent of normal was used for projections of output in 2013–14.Upper band on growth was placed at 4.5 per cent.

I.4 Food Inflation WeakensYear-on-year headline inflation, measured by Wholesale Price Index after peaking 7.52 percent in November 2013, abated to 6.16 per cent in December compared to 7.31 per cent ayear ago, aided by drop in food inflation. Annual food inflation in December 2013 measuredby WPI of food articles abated to 13.7 per cent from 19.9 per cent a month ago, supportedlargely by lower prices of onion and rice (Figure I.4 and Table I.2). Rice price inflationdeclined marginally to 13.62 per cent in December from 15 per cent in November, whereasonion price increase on annual basis fell sharply to 39.6 per cent, the lowest in the past 13months, following increased market arrival from the late kharif crop. Wheat and milk pricesstrengthened modestly, whereas pulses, vegetable oil, and sugar prices showed decline.

Food inflation in the Short-runWith price rise of most food products, particularly of onion, cereals, pulses, vegetable oils,and sugar showing a declining trend, food inflation is expected to further moderate in theshort-run which may help in bringing down the overall inflation rate (Table I.3a). Twoapproaches were adopted for the short-term projections of price inflation of major fooditems, which are summarized in Tables I.3b–I.3c.

The highlights of the price environment are:

� The domestic and international prices show a contrasting pattern in the case ofaggregate food price index and in some specific sectors such as rice, wheat, maize andsoybean. The international prices show a declining pattern relative to the situation ayear back, the domestic prices are at elevated levels relative to previous year.

� Only in the case of groundnut oil the domestic prices show a declining pattern whileinternational prices are rising.

� The differences in domestic and international price trends are influenced by outputfluctuations, price support policies, exchange rate fluctuations and also level ofintegration with the international markets. In the case of soybean and groundnutdomestic production scenario presents a contrasting situation, with output registeringsharp increase in the case of groundnut and showing some uncertain gains in soybean.The rapeseed and mustard oil shows similar trend in domestic and internationalmarkets and in the case of palm oil difference appears to be the exchange rate wedge.

� In the case of vegetables, while overall WPI is showing lower annual increase, in thecase of potato, price rise is significant indicating supply side pressures.

� The projections of domestic prices for the next 3–4 months indicating moderate orsoftening inflationary pressures in the case of wheat, pulses, onion and edible oils as agroup, in the case of wholesale prices in Delhi or national WPI indices.

� In the case of rice and milk the two approaches of projection indicate continuedfirmness in the price scenario.

� In the case of potato and onion the projections show contrasting patterns: the pricescenario in Delhi shows softening trends for potato but at national level the pricescenario appears to show upward pressures. In the case of onion the patterns are quitethe opposite. This mixed picture suggests that prices would show moderate increase,year-on-year basis, in the case of these two vegetables, but demand pressures willremain to maintain the upward pressures.

Overall, the food prices are likely to show annual 7–8 per cent increase in the short-term.

AGRICULTURAL OUTLOOK AND SITUATION ANALYSIS REPORTS

6

With price rise ofmost food products,particularly of onion,cereals, pulses,vegetable oils, andsugar showing adeclining trend, foodinflation is expectedto further moderatein the short-runwhich may help inbringing down theoverall inflation rate.

OVERVIEW OF THE DOMESTIC AGRICULTURE OUTLOOK

7

Table I.2: Year-on-Year Inflation Trend in Major Food Commodities: WPI % Change YOYMonths Food Articles Rice Wheat Pulses Potato Onion Milk Veg Oils SugarJan ’12 -0.68 0.94 -3.42 11.01 -23.15 -75.62 12.33 9.43 2.54Feb 6.12 1.53 -3.95 7.86 -2.22 -48.66 11.70 7.65 4.07Mar 10.11 5.03 -0.58 10.10 18.43 -24.06 15.29 9.94 2.87Apr 10.92 5.98 5.97 11.29 59.30 -11.03 15.68 11.18 3.16May 10.63 4.89 6.75 16.77 72.17 -8.05 11.90 10.37 5.24Jun 10.91 7.46 6.76 20.59 84.91 -9.46 7.46 9.52 7.13Jul 10.17 9.95 6.44 28.57 73.24 -10.05 8.01 10.85 9.38Aug 9.34 10.35 12.97 34.54 70.74 -20.71 6.68 10.91 16.91Sep 8.06 12.58 18.87 28.98 52.45 -24.69 6.45 10.71 19.87Oct 6.72 14.97 19.78 19.86 49.13 -9.12 6.35 9.38 18.88Nov 8.80 15.28 23.25 18.77 67.85 16.55 6.18 9.76 15.48Dec 10.63 17.10 23.63 16.25 58.03 72.79 6.15 9.20 9.84Jan ’13 12.35 17.77 21.87 15.89 73.10 125.17 4.52 7.54 10.09Feb 11.95 17.75 21.81 13.95 50.14 182.36 4.52 7.04 10.49Mar 8.63 17.56 19.35 10.84 15.80 110.74 4.42 3.60 9.35Apr 6.08 17.09 13.55 10.52 -0.63 90.83 4.04 2.01 8.67May 8.25 18.48 12.37 5.95 1.28 94.28 4.46 0.89 7.10Jun 10.27 20.43 13.94 1.59 -8.38 114.76 4.08 0.07 6.93Jul 12.29 21.15 13.64 -7.43 -6.13 146.43 3.02 -2.23 2.20Aug 19.17 21.33 9.38 -14.70 -15.25 272.54 6.02 -2.86 -4.75Sep 18.68 18.61 7.31 -13.42 -12.28 335.88 5.77 -2.72 -7.39Oct 18.34 14.45 7.88 -10.72 0.17 293.29 5.64 -0.27 -8.21Nov 19.93 14.99 7.21 -10.56 26.71 190.34 6.25 -0.07 -8.41Dec 13.68 13.62 7.93 -7.19 54.65 39.56 6.93 -1.20 -5.99

Figure I.3: Food Inflation Exceeds Overall Inflation Rate

AGRICULTURAL OUTLOOK AND SITUATION ANALYSIS REPORTS

8

Table I.3a: Recent Trends in Food Prices: WPI and International Price, % YOY Item WPI % Change YOY International Prices % Change YOY

Oct–13 Nov–13 Dec–13 Jan–14 Oct–13 Nov–13 Dec–13 Jan–14

Food Price Index 12.8 13.9 9.6 6.3 -4.8 -4.6 -3.6 -4.5

Food articles 18.3 19.7 13.7 8.8

Food products 2.3 2.4 1.8 1.5

Cereals 11.4 11.3 10.2 9.3

Rice 14.5 15.0 13.6 13.4 -22.5 -24.0 -20.9 -23.1

Wheat 7.9 7.0 7.9 7.1 -9.2 -15.0 -16.2 -17.9

Jowar 2.9 9.4 8.8 8.2

Bajra 13.9 8.0 0.1 -0.5

Maize 6.4 7.4 4.0 -1.7 -37.3 -38.1 -36.0 -34.5

Pulses -10.7 -9.9 -7.2 -6.1

Gram -23.9 -25.5 -23.5 -22.4

Tur 0.6 3.9 9.2 8.8

Groundnut seed -10.8 -19.5 -23.5 -28.9

Rapeseed & Mustard seed -15.6 -14.3 -12.2 -9.5

Soybean 10.9 13.9 10.2 10.1 -16.4 -10.6 -8.6 -9.5

Vegetables 80.2 97.7 57.3 16.6

Potato 0.2 35.0 54.7 21.7

Onion 293.3 201.2 39.6 6.6

Fruits 15.8 13.6 9.1 5.3

Banana 30.5 16.6 16.4 14.0 -2.3 -1.6 -2.2 -0.6

Groundnut oil -2.2 -4.0 -11.0 -12.9 42.8 42.7 18.4 22.1

R & M oil -0.9 -0.8 0.3 0.6 -17.0 -14.9 -15.4 -21.2

Palm oil 3.4 7.4 5.8 6.2 -0.7 9.0 11.4 -0.9

Edible oils -0.3 0.2 -1.2 -2.0

Sugar -8.2 -7.7 -6.0 -5.2 -8.1 -4.9 -8.9 -8.4

Grain mill products 7.9 7.5 5.1 2.8

Milk 5.6 6.9 6.9 7.2

Note: International prices: IMF.

Table I.3b: Projections of Wholesale Prices in Delhi based on Harmonic Analysis: % Change Year-on-YearJan–14 Feb–14 Mar–14 Apr–14

Rice 5.8 5.7 5.7 5.7

Wheat 4.2 4.2 4.2 4.3

Tur -9.7 -9.9 -10.0 -10.0

Gram -23.6 -23.7 9.6 9.9

Urd 4.5 4.6 4.6 4.6

Masur -13.0 -14.1 -14.8 -14.8

Onion 88.7 86.9 82.8 10.4

Potato -18.1 -20.6 -20.0 -16.4

Sugar -9.1 -10.0 -10.6 -10.7

Soy oil 13.2 15.9 18.3 20.6

Palm oil 21.1 23.7 25.8 27.4

Milk 13.1 13.0 12.8 12.7

I.5 Supply-Demand Balance SummaryPart IV of the report discusses the short-term scenario for specific food commodities.Summary of the scenario that is developing in the supply-demand balance sheet of thefood commodities is summarised in Table I.4.

In arriving at the supply-demand balances, we have taken opening stock and closing stockfor rice and wheat based on accounting of government operations in foodgrains; in the caseof edible oils and sugar, closing stocks are residual as we specify domestic use based pasttrends. In the other cases, closing stocks are specified at the same level as the notionalbeginning stocks.

OVERVIEW OF THE DOMESTIC AGRICULTURE OUTLOOK

9

Table I.3c: Projections of National Level WPI based on ARIMA Models: % Change Year-on-Year andMonth over MonthCommodity % YOY % MOM

Actual Projected Actual ProjectedJan–14 Feb–14 Mar–14 Apr–14 Jan–14 Feb–14 Mar–14 Apr–14

Rice 13.4 13.3 12.5 12.6 -0.2 0.4 0.5 0.8

Wheat 7.1 7.6 7.6 5.6 0.2 0.9 -0.8 -2.7

Jowar 8.2 7.9 1.7 1.6 0.2 1.2 -0.4 1.0

Bajra -0.5 -1.2 -0.4 0.2 1.1 -0.3 0.9 2.9

Maize -1.7 0.6 2.4 1.3 -2.7 1.9 1.7 -0.7

Gram -22.4 -20.1 -16.7 -16.6 -1.3 -3.0 -1.6 -1.8

Tur 8.8 8.8 4.4 3.3 -1.1 0.7 -0.2 1.3

Pulses -6.1 -4.7 -2.9 -1.9 -0.1 -1.2 -0.1 1.1

Onion 6.6 -26.9 -22.0 -28.2 -16.6 -23.8 -19.0 -14.5

Potatoes 21.7 15.1 35.6 23.4 -23.0 -12.2 8.6 7.2

Groundnut seed -28.9 -28.2 -27.8 -28.0 -0.2 -1.4 0.5 1.3

Rape Mustard seed -9.5 -9.5 -5.7 -2.4 -0.1 -3.2 -2.9 0.0

Soyabean 10.1 9.8 3.3 -6.9 -1.5 -0.9 0.7 1.9

Edible oils -2.0 -2.8 -1.9 -1.2 -0.7 -1.2 -0.6 0.9

Food articles 8.8 9.1 10.3 10.2 -2.7 0.6 0.5 2.6

Food products 1.5 1.3 2.1 2.3 -0.4 -0.1 0.1 1.0

Food sector 6.2 6.4 7.3 7.1 -1.9 0.4 0.2 1.8

Table I.4: Supply-Demand Balances for Selected Food Commodities (Thousand Tonnes)Item/ Marketing year Rice Wheat Maize Pulses Edible oils Sugar Onion Potato

2013–14 2014–15 2013–14 2013–14 2013–14 2013–14 2013–14 2013–14

A. Supply side

Beginning stocks 23,000 19,000 550 1,964 1,643 8,800 657 2,450

Production 106,500 97,500 23,500 19,700 10,000 24,500 18,300 44,800

Imports 0 0 0 3,500 10,300 0 10 0

Total supply 129,500 116,500 24,050 25,164 21,943 33,300 18,967 47,250

B. Demand side

Exports 9,000 4,000 3,000 200 100 2000 1,000 250

Domestic use 98,000 92,500 19,850 23,000 19,200 23,000 17,310 44,550

Utilisation 107,000 96,500 22,850 23,200 19,300 25,000 18,310 44,800

C. Closing stocks 22,500 20,000 1200 1,964 2,643 8,300 657 2,450

Note: IThe supply demand balances are for the marketing year 2013–14 in all the cases except wheat, which is for MY 2014–15.

The balance sheet indicates the significant level of beginning and closing stocks in the caseof rice, wheat and sugar and relatively low stocks in the other cases. While adjustments toproduction or demand shocks are likely to be absorbed through trade or consumption inthe case of pulses and edible oils, the low stock position (even when estimated notionallyin the absence of data) reflects the vulnerability of consumption to production shocks inthe case of onion and potatoes.

AGRICULTURAL OUTLOOK AND SITUATION ANALYSIS REPORTS

10

PART II

Overview of the Global FoodOutlook

11

II.1 Economy Poised for a Modest GrowthThe global economy continues to grow at a moderate pace, in large part due to weakerprospects in many emerging market economies, with a modest acceleration of growthanticipated in 2014. The International Monetary Fund (IMF) currently forecasts globaleconomic growth in 2014 at 3.6 per cent compared to 2.9 per cent in 2013. Growthcontinues to disappoint in major emerging market economies, reflecting, to varyingdegrees, infrastructure bottlenecks and other capacity constraints, slower external demandgrowth, lower commodity prices, financial stability concerns, and, in some cases, weakerpolicy support.

On the positive side, in early December 2013, The World Trade Organisation (WTO)reached its first ever worldwide trade reform deal pertaining to trade facilitation at a make-or-break meeting at Bali. The deal also includes agriculture provisions that encourage theeliminationof export subsidies and better administration of tariff-rate quotas. Experts saythe new trade agreement could boost global economic output by as much as $1 trillion andcreate 21 million jobs, most of those in developing countries. India succeeded in securinga waiver on providing agriculture subsidies in the WTO forum.

II.2 Global Agricultural Outlook

II.2.1 Production further upGlobal agricultural outlook for 2013–14 continues to remain upbeat. Since our lastQuarterly Outlook Report ( July–September), there have been further upward revisions in2013–14 global production of wheat, coarse grains, oilseeds, vegetable oils, and sugar.However, global rice production was revised downward by 3 to 7 million tonnes by variousagencies due to a worsening of crop prospects in China and India, the two largestproducers (Table II.1).

� The FAO has revised its 2013–14 wheat production upward to 710.8 million tonnes,the USDA to 712.7 million tonnes and IGC to 698.0 million tonnes, record highs,from the 2012–13 production of 659.6, 656.2 and 655 million tonnes, respectively.

� World rice production in 2013–14 was revised downward to 494.2 million tonnes byFAO, 471.1 million tonnes by USDA, and 471 million tonnes by IGC from itsSeptember estimate, but still a record high.

� 2013–14 world coarse grain production has been revised significantly upward, about130 million tonnes above the 2012–13 level to 1295 million tonnes by FAO, 1,259million tonnes by USDA, and 1,248 million tonnes by IGC, with most of the increaseconfined to maize.

� Global oilseed production forecast for 2013–14 was revised significantly upward by all

In early December2013, The WorldTrade Organisation(WTO) reached itsfirst ever worldwidetrade reform dealpertaining to tradefacilitation at amake-or-breakmeeting at Bali. Thedeal also includesagricultureprovisions thatencourage theeliminationof exportsubsidies and betteradministration oftariff-rate quotas.Experts say the newtrade agreementcould boost globaleconomic output byas much as $1 trillionand create 21 millionjobs, most of those indevelopingcountries. Indiasucceeded insecuring a waiver onprovidingagriculturesubsidies in the WTOforum.

agencies from its earlier forecast. The revised estimates with the 2012–13 estimates inparentheses in million tonnes are: FAO – 503 (482) and USDA – 506 (474). U.S.soybean production was revised upward to 89.5 million tonnes from the Septemberestimate of 85.7 million tonnes. Reflecting higher oilseed production, 2013–14 globaledible oil production has also been revised upward to 169 million tonnes by USDA, 8.4million tonnes above the 2012–13 production, with most of the increase in palm oil,soybean oil, and sunflower seed oil.

Global wheat production in 2013–14 is forecast to increase by around 8 per cent with mostof the increase confined to the Black Sea region (the Russian Federation, Ukraine andKazakhstan) following severe drought conditions in the previous year. Significant increasein wheat production is reported in Canada, Australia, and European Union, partly offsetby lower production in the United States, China, and India. In the United States inparticular, production is estimated to decline by about 6.2 per cent reflecting droughtconditions throughout the growing season in many major winter wheat areas.

Global rice production for 2013–14, despite some downgrading in recent months in Indiaand China due to weather related problems, is forecast at a record as a result of expandedarea. Higher production is expected in all major producing countries except in Chinamainly due to an increase in planted area driven by higher government support prices.

Driven largely by a sharp increase in maize production in the U.S., the world’s largestmaize producing country, from the drought-plagued output of the previous year, globalcoarse grains production in 2013–14 is estimated at a record. Maize production in theUnited States rebounded by about 30 per cent to 354 million tonnes from its drought-reduced level in the previous year. In China and India, the consistent growth in maizeproduction in recent years has continued in 2013–14. Maize production in other majorproducing countries such as European Union, Ukraine, Canada, and Indonesia is forecastto increase to record levels, whereas in Brazil and Argentina production is likely to declinefrom the 2012–13 record levels due to an expected fall in the area in response to prevailinglower world corn prices.

AGRICULTURAL OUTLOOK AND SITUATION ANALYSIS REPORTS

12

Global wheatproduction in2013–14 is forecastto increase byaround 8 per centwith most of theincrease confined tothe Black Sea region(the RussianFederation, Ukraineand Kazakhstan)following severedrought conditions inthe previous year.

Global riceproduction for2013–14, despitesome downgradingin recent months inIndia and China dueto weather relatedproblems, is forecastat a record as aresult of expandedarea.

USDA projects world oilseeds production in 2013–14 to rise further to a record of around506 million tonnes, largely due a significant increase in soybeans, rapeseed, and sunflowerseed. In the United States, despite weather related problem in major producing areas,soybean production is estimated at a near record level of 89.5 million tonnes, an increaseof 7 million tonnes over the previous year. Relatively favourable returns to soybeans areforecast to result in an expansion of the area planted to soybeans in Brazil and Argentina,primarily at the expense of the area planted to corn. As a result, soybean production inthese countries is forecast to rise to record levels assuming favourable weather conditions.A significant increase in rapeseed production is Canada would take world rapeseedproduction to a record 70 million tonnes. World sunflower seed production is forecast torise by 13 per cent in 2013–14 to a record 43.7 million tonnes, largely driven by higherproduction in the Black Sea region and the European Union.

OVERVIEW OF THE GLOBAL FOOD OUTLOOK

13

Table II.1: Global Production Forecasts for Major Food Commodities (Million Tonnes)FAO USDA IGC ABARES

Wheat

2011–12 702.4 697.3 695 695

2012–13 659.6 656.2 655 655

2013–14 710.8 (709.8) 712.7 (708.9) 698.0 (693.0) 705 (695)

Rice

2011–12 486.1 465.8 465 NA

2012–13 489.1 469 469 NA

2013–14 494.2 (497.2) 471.1(476.8) 471 (474) NA

Maize

2011–12 888.4 886 877 886

2012–13 875.2 862.9 863 863

2013–14 1001.3 (983) 966.9 (956.7) 950 (943) 964 (957)

All Coarse grains

2011–12 1164.5 1151.3 1156 1151

2012–13 1156.3 1132.5 1135 1131

2013–14 1294.8 (1285.3) 1259.2 (1245.5) 1248 (1237) 1254 (1247)

Total Oilseeds

2011–12 454.7 446.3 NA 445

2012–13 481.5 474.1 NA 470

2013–14 502.5 (NA) 505.9 (495.1) NA 498 (487)

Total Vegetable oils

2011–12 183.6 157.5 NA 153

2012–13 190.2 160.8 NA 156

2013–14 199.3 (NA) 169.2 (167.3) NA 165 (164)

Sugar ( Raw equivalent)

2011–12 175.2 161.9 NA 174.3

2012–13 179.6 172 NA 183.6

2013–14 180.2 (NA) 174.9 NA 181.6 (181.1)

Milk

2011–12 742.2 529.7 NA NA

2012–13 765.6 544.1 NA NA

2013–14 780.3 (NA) 553.7 NA NA

World vegetable oil production in 2013–14 is forecast by USDA at a record 169 milliontonnes, up almost 8 million tonnes from the 2012–13 production, with most of theincrease in palm oil (Indonesia), soybean oil (Argentina and Brazil), rapeseed oil (Canada)and sunflower seed oil (Ukraine and Russia). Oil production from the group of annualoilseed crops is estimated to rise by around 5.0 million tonnes and the perennial oil seedcrop, mainly oil palm is forecast to add around 3.0 million tonnes to global vegetable oilproduction.

Global production outlook for pulses in major exporting countries has further improvedsince our last report. World production of dry peas, one of the leading pulses traded inglobal market, is estimated to have increased significantly in all major exporting countriessuch as Canada, Australia, and the United States in 2013–14. Canadian dry peaproduction estimate for 2013–14 has been revised upward at 3.8 million tonnes, up 13 percent from the previous year’s production, as lower harvested area has been offset by recordyields. US dry pea production is forecast to increase by 21 per cent to 700,000 tonnesmainly due to a 30 per cent increase in planted area. Australian field pea production in2013 is estimated at 397,100 tonnes, an increase of 24 per cent over 2012.

Canadian lentil production is estimated to rise by 11 per cent to 1.7 million tonnes. Thisis largely due to estimate of record yield, which more than offsets lower harvested area. TheUS lentil production is forecast to decline by 26 per cent to 200,000 tonnes due to declinein planted area. Australian lentil production in 2013 is estimated at 246,250 tonnes, anincrease of 34 per cent over the previous year.

Canadian chickpea production for 2013–14 is estimated to rise by 6 per cent to 171,000tonnes, due to above average yield estimates for the second consecutive year. 2013–14. USchickpea production is forecast at 150,000 metric tonnes, unchanged from the 2012–13level. Australian desi chickpea production in 2013 is estimated to have declined by about26 per cent to 541,290 tonnes due to poor growing conditions. This was marginally offsethigher kabuli chickpea production which increased by 26 per cent to 97,930 tonnes.

2013–14 pulse production in Myanmar, a major supplier of tropical pulses such as urd(black matpe), tur (pigeon pea), etc. is estimated at 4.8 million tonnes, marginally higherfrom the 2012–13 level.

While ABARES forecasts 2013–14 world sugar production to decline marginally to 181.6million tonnes from 183.6 million tonnes the previous year, FAO estimates a marginalincrease in production at 180.2 million tonnes. Production is forecast to be lower inEurope, the United States, India and Mexico but higher in Brazil, Thailand and China.

FAO forecasts world milk production in 2013 to grow by 1.9 per cent to 780 milliontonnes – with Asia, particularly India, expected to account for most of the increase. Returnto favourable seasonal conditions in main dairy exporting countries such as New Zealand,United States and European Union and lower feed grain prices will also contribute tohigher production.

II.2.2 Consumption upbeatWheat consumption is forecast to increase in 2013–14 from the low level of the previousyear due to larger production and lower prices with food use accounting for most of theincrease. Developing countries are likely to account for the bulk of the wheat food useincrease. Expected lower prices of feed wheat substitutes, such as corn, are expected tomoderate the extent of the increase in feed wheat demand with most of the increaseconfined to European Union, whereas in the US and China feed use is likely to decline.USDA estimates total global wheat consumption to increase by around 1.9 per cent to

AGRICULTURAL OUTLOOK AND SITUATION ANALYSIS REPORTS

14

Global productionoutlook for pulses inmajor exportingcountries has furtherimproved since ourlast report. Worldproduction of drypeas, one of theleading pulsestraded in globalmarket, is estimatedto have increasedsignificantly in allmajor exportingcountries such asCanada, Australia,and the United Statesin 2013–14.

While ABARESforecasts 2013–14world sugarproduction to declinemarginally to 181.6million tonnes from183.6 million tonnesthe previous year,FAO estimates amarginal increase inproduction at 180.2million tonnes.

FAO forecasts worldmilk production in2013 to grow by 1.9per cent to 780million tonnes – withAsia, particularlyIndia, expected toaccount for most ofthe increase.

699.3 million tonnes, FAO by 1.4 per cent to 696.1 million tonnes and IGC by 2.8 percent to 692 million tonnes.

Despite a marginal downward revision from the earlier forecast, global 2013–14 riceconsumption is projected at a record 473.0 million tonnes by USDA and 471 milliontonnes by IGC, up about 1 per cent from a year earlier. However, FAO estimate of2013–14 rice consumption is 489 million tonnes, up 2.6 per cent from the 2012–13 level.India, China and Nigeria account for most of the projected increase in global consumptionin 2013–14.

World coarse grains consumption in 2013–14 is forecast to reach a record of around 1.2billion tonnes, driven by an expected increase in the feed use, particularly maize. Total feedutilization of coarse grains in 2013–14 is currently forecast by FAO to increase by around6 per cent to 700 million tonnes which reflects recovery in world supplies and lower pricesof major coarse grains. Total maize consumption (including food, feed and industrial use)consumption is forecast by USDA to rise by 9 to 10 per cent to a record level of around935 million tonnes, with United States and China accounting for the largest increasefollowed by Mexico, Russia, and Ukraine. Barley consumption is forecast by USDA to riseby around 8 million tonnes to 141 million tonnes.

Total industrial use of maize (mostly for production of ethanol) is projected by theInternational Grains Council to approach 262 million tonnes, 6 per cent higher than in theprevious season. Most of the increase is expected to be in the United States, where assumingno change to ethanol blending mandates, ethanol producers are expected to respond toimproved producer margins during 2013–14 as maize prices are expected to moderate.

World oilseeds crush, exclusive of oil palm, is forecast by USDA to increase by 4 to 5 percent in 2013–14 to around 415 million tonnes, driven by high demand for protein mealsand vegetable oils. Most of the increase will be in soybeans (up 5 per cent to 240 milliontonnes) followed by sunflower (up 13 per cent to 37 million tonnes) and rapeseed/mustard(up 3 per cent to 64 million tonnes).

Larger supplies combined with the fall in international prices are likely to stimulate globalvegetable oil demand. As a result, world consumption is forecast to increase by 6 per centin 2013–14 to 165 million tonnes by the USDA, with both food consumption and to alesser extent industrial use of vegetable oils (primarily biodiesel) increasing. Food usegrowth is likely to remain confined to China and India. Given its competitive pricerelative to other oils, palm oil would remain the growth leader, followed by soy, rape andsunflower seed oil. National biofuel regulations, border measures and certificationrequirements will continue to influence markets for biodiesel and their feedstock. TheEuropean Union is likely to increase domestic biodiesel production in response to theintroduction in late 2013 of import duties on biodiesel from Argentina and Indonesia.

Despite a likely marginal decline in production, ABARES forecasts world sugarconsumption to increase by 2.2 per cent in 2013–14 to a record 176.8 million tonnes,driven by expected income growth, particularly in China, Indonesia, India and Brazil.Large supplies and lower international and domestic prices due to large carryover stocksare expected to underpin consumption.

II.2.3 Price trend mixedWorld commodity prices presented a mixed picture during the past quarter with wheat,maize, soybean oil, soybean meal, and sugar showing a downward trend while rice,soybeans and palm oil prices strengthening. Nevertheless, most commodity prices in recent

OVERVIEW OF THE GLOBAL FOOD OUTLOOK

15

World coarse grainsconsumption in2013–14 is forecastto reach a record ofaround 1.2 billiontonnes, driven by anexpected increase inthe feed use,particularly maize.Total feed utilizationof coarse grains in2013–14 is currentlyforecast by FAO toincrease by around 6per cent to 700million tonnes whichreflects recovery inworld supplies andlower prices of majorcoarse grains.

Larger suppliescombined with thefall in internationalprices are likely tostimulate globalvegetable oildemand.

AGRICULTURAL OUTLOOK AND SITUATION ANALYSIS REPORTS

16

A record cereal cropthis year has helpedto improve the globalsupply situation,weighing on theinternational pricesof wheat and maize.

The FAO Food PriceIndex averaged206.7 points inDecember 2013,nearly unchangedfrom November, as asharp increase indairy prices andfirming meat valuesdue to increasingdemand from Chinaand Japan largelybalanced out a steepdecline in sugarquotations and lowercereal and oil prices.Over the full 2013year, the Indexaveraged 209.9points, down 1.6 percent from 2012, butstill the third highestannual value onrecord.

months were significantly below a year-ago prices. A record cereal crop this year has helpedto improve the global supply situation, weighing on the international prices of wheat andmaize. Prices for soybeans have trended higher during recent months, underpinned by firmbuying interest from leading importers, which more than offset pressure from prospects forbumper outturns in all of the world’s main exporters. Palm oil prices in recent months hasstrengthened and exceeded a year-ago price due to strong global import demand, includingfor biodiesel production, and below-expectation output in Southeast Asia followingexcessive rainfall (Figure II.1). Improved harvesting operations in Brazil, the world’slargest sugar producer and exporter, and speculations of a possible surge of exports fromBrazil and India, owing to the weakening of currencies against the US dollar caused a slidein sugar prices.

The FAO Food Price Index averaged 206.7 points in December 2013, nearly unchangedfrom November, as a sharp increase in dairy prices and firming meat values due toincreasing demand from China and Japan largely balanced out a steep decline in sugarquotations and lower cereal and oil prices. Over the full 2013 year, the Index averaged209.9 points, down 1.6 per cent from 2012, but still the third highest annual value onrecord.

Figure II.1: Global Price Trend of Major Commodities

OVERVIEW OF THE GLOBAL FOOD OUTLOOK

17

AGRICULTURAL OUTLOOK AND SITUATION ANALYSIS REPORTS

18

II.2.4 Price outlook bearish

Generally increased wheat supplies and the expected drop in maize prices should see someweakening in world wheat prices during the rest of MY 2013–14 and MY 2014–15. Mostobservers (ABARES, the Economist Intelligence Unit) feel the world wheat indicatorprice (US #2 HRW) to fall by 9 to 10 per cent to $ 310 to $315 per tonne in 2013–14 andfurther to below $300 per tonne in 2014–15. For medium and lower protein wheatvarieties, including feed wheat, prices on world markets are expected to decline by morethan the fall in the indicator price.

With rice availabilities set to remain comfortable next year, international prices should easefurther in 2014. Thailand’s large sell off of government rice stocks and record exportablesupplies in Asia with record and near record stocks in Thailand and India, respectively arebearish factors.

The world coarse grains indicator price (US corn, fob Gulf ) is forecast by ABARES to fallby 29 per cent in 2013–14 to US$220 a tonne. This mostly reflects a record corn harvestin the United States. A proposed lowering of 2014 ethanol blending requirements in theUS and news of a number of overseas customs rejections of imported US maize on fearsof genetic modification provided negative pressure on prices in recent weeks. With onlylimited scope for growth in the U.S. fuel ethanol market, the potential outlets for therecord crop in 2013 therefore appear limited and the heavier stocks outlook should meaneven lower prices in the months ahead.

Soybean prices are expected to ease gradually in coming months against the backdrop ofample and improving supplies, especially in the world’s major exporters. The EconomistIntelligence Unit forecasts 2014 average US export prices (US # 2 Yellow fob Gulf basis)to decline by around 8 per cent year-on-year. There is likely to a strengthening in soybeanoil price through the end of the first quarter of 2014 in unison with palm oil price beyondwhich prices are expected to moderate.

With palm oil production entering its seasonal decline and with the possibility of a furtherdowngrading of production prospects in Indonesia, the palm oil market is now in a morebullish phase. This phase is expected to continue until the end of the January–Marchquarter of 2014, beyond which production will start to increase seasonally. According toexperts, palm oil prices could hit a more than one-year high at over $900 per tonne byMach 2014 rising faster than previously expected on strong demand from the biofuelindustry, mainly in Indonesia, before declining. Recent higher prices have led to asignificant reduction in the discount of palm oil to other vegetable oils, which is now at itslowest level since mid-2010. Typically, soybean oil price is on an average $200 per tonneabove palm oil which is only $75 per tonne now.

Global prices of dry peas, lentils, and chick peas are expected to fall in 2013–14 due to largersupplies and carryover stocks in major exporting countries such as Canada. The average priceof Canadian dry peas is expected to fall from the 2012–13 level, due to expectations for muchlarger carry-out stocks in 2013–14, projected by Agriculture and Agri-Food Canada.Average price is forecast to range between Canadian $ 265–295 against the previous year’sC$ 340 per tonne. The overall average price of Canadian lentils in 2013–14 is also forecastto be lower in the range of C$ 390–420 against C$ 440 per tonne in 2012–13 due to anexpected rise in carry-out stocks. Canadian chickpea price in 2013–14 is forecast at C$590–620 per tonne against $690 in 2012–13 due to higher world and Canadian supplies.

Given the relatively optimistic view of the supply fundamentals, and on the basis of furtherstock growth, there is likely to be limited price recovery in sugar in 2014, unless growing

OVERVIEW OF THE GLOBAL FOOD OUTLOOK

19

Generally increasedwheat supplies andthe expected drop inmaize prices shouldsee some weakeningin world wheatprices during therest of MY 2013–14and MY 2014–15.

Soybean prices areexpected to easegradually in comingmonths against thebackdrop of ampleand improvingsupplies, especiallyin the world’s majorexporters.

With palm oilproduction enteringits seasonal declineand with thepossibility of afurther downgradingof productionprospects inIndonesia, the palmoil market is now in amore bullish phase.