absolute return partners 2012 investment outlook

DESCRIPTION

Absolute Return Partners 2012 Investment OutlookTRANSCRIPT

Absolute Return Partners LLP Absolute Return Partners LLP

2012 Outlook2012 Outlook

December 2011December 2011

Part 1Part 1

The The EurozoneEurozone CrisisCrisis

2

3

The eurozone crisis continues unabatedlyThe eurozone crisis continues unabatedly

Throwing money at the problem is no longer a viable option Throwing money at the problem is no longer a viable option –– the the numbers are simply too big;numbers are simply too big;

Germany holds the key to a lasting solution;Germany holds the key to a lasting solution;

It has to choose between:It has to choose between:

i.i. Monetisation;Monetisation;

ii.ii. Fiscal union;Fiscal union;

iii.iii. Withdrawal.Withdrawal.

Germany cannot say Germany cannot say ‘‘NeinNein’’ to all of them! to all of them!

4

Bailing out Italy is not an optionBailing out Italy is not an option

Source: Morgan Stanley

The Italian government bond market is EuropeThe Italian government bond market is Europe’’s largests largest

5

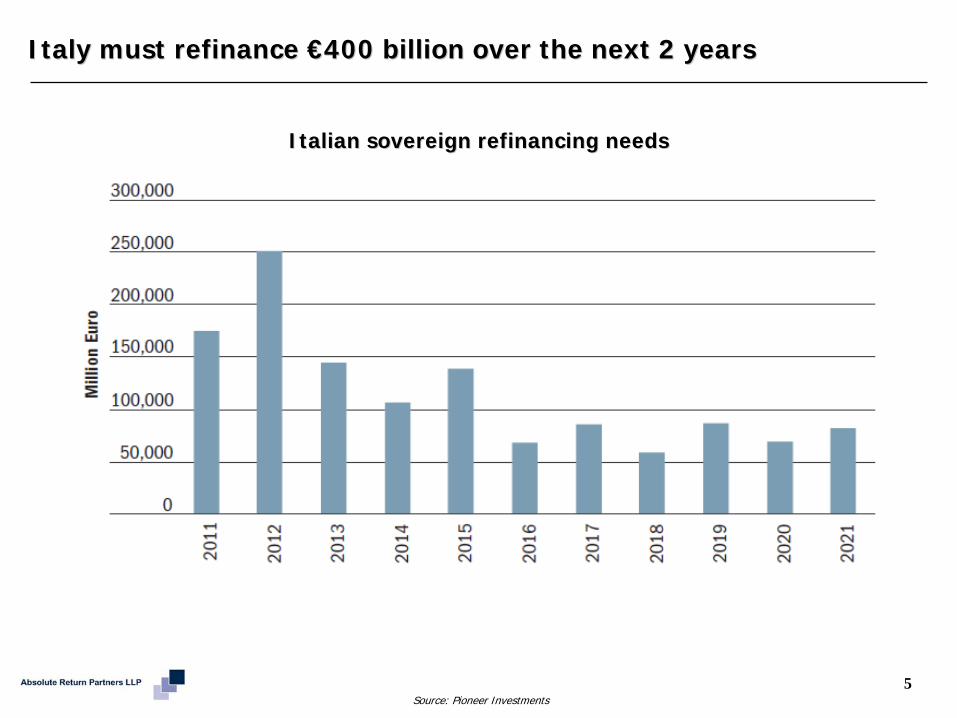

Italy must refinance Italy must refinance €€400 billion over the next 2 years 400 billion over the next 2 years

Source: Pioneer Investments

Italian sovereign refinancing needsItalian sovereign refinancing needs

6

Is there room for monetisation?Is there room for monetisation?

Source: Banca d’Italia, Daily Telegraph

Italian monetary aggregates turning negativeItalian monetary aggregates turning negative

Part 2Part 2

EuropeEurope’’s Bankss BanksThe Biggest Story of 2012?The Biggest Story of 2012?

7

8

European banks could be the main story of 2012European banks could be the main story of 2012

European banks must raise tier 1 capital ratios to 9% by 30 JuneEuropean banks must raise tier 1 capital ratios to 9% by 30 June 2012;2012;

EBA estimates a total of EBA estimates a total of €€106 billion of new capital will be required;106 billion of new capital will be required;

With virtually all banks selling well below (stated) book value,With virtually all banks selling well below (stated) book value, and with and with pressure on earnings, few are keen to raise new equity capital;pressure on earnings, few are keen to raise new equity capital;

The alternative is to delever;The alternative is to delever;

Morgan Stanley estimates Morgan Stanley estimates €€1.51.5--2.5 trillion of deleveraging over next 18 2.5 trillion of deleveraging over next 18 months (3months (3--5% of total assets);5% of total assets);

Barclays Capital puts the number as high as 10%;Barclays Capital puts the number as high as 10%;

Political pressure to continue domestic lending;Political pressure to continue domestic lending;

The only solution? Cut back on nonThe only solution? Cut back on non--domestic lending. domestic lending.

9

Difficult to raise new equity when earnings are under pressureDifficult to raise new equity when earnings are under pressure

Source: Barclays Capital

2012 consensus earnings for European banks2012 consensus earnings for European banks

10

Assets may have to shrink by as much as 10% to meet 9% targetAssets may have to shrink by as much as 10% to meet 9% target

Source: Barclays Capital

Banks in peripheral Europe must shrink the mostBanks in peripheral Europe must shrink the most

11

Asia is exposed to European bank deleveragingAsia is exposed to European bank deleveraging

Source: Morgan Stanley

European banks have USD 1.6 trillion total exposure to Asia ex JEuropean banks have USD 1.6 trillion total exposure to Asia ex JapanapanAs of June 2011As of June 2011

12

……but Asia is only a small part of total lending originated in Eurbut Asia is only a small part of total lending originated in Europeope

Source: Barclays Capital

European banksEuropean banks’’ geographical location of assetsgeographical location of assets

13

Global trade is at risk from European bank deleveragingGlobal trade is at risk from European bank deleveraging

Source: Barclays Capital

Latin America trade finance loans, Q3 11

Spain and France dominate trade financeSpain and France dominate trade finance

14

Eastern European exporters are very exposed to the EUEastern European exporters are very exposed to the EU

Source: Morgan Stanley

Emerging market exports to EuropeEmerging market exports to Europe

15

Where will European banks be inclined to exit?Where will European banks be inclined to exit?

Source: Barclays Capital

Banks more likely to pull out where nonBanks more likely to pull out where non--performing loans are high performing loans are high

Part 3Part 3

Investment RecommendationsInvestment Recommendations

16

Source: Morgan Stanley. Data as of 30 November 2011.17

ShillerShiller P/E ratios for Emerging Markets vs. S&P 500P/E ratios for Emerging Markets vs. S&P 500

Neither US nor EM equities look particularly cheap at this pointNeither US nor EM equities look particularly cheap at this point

US P/E ratios are 30% above the median and the emerging market discount has all but evaporated.

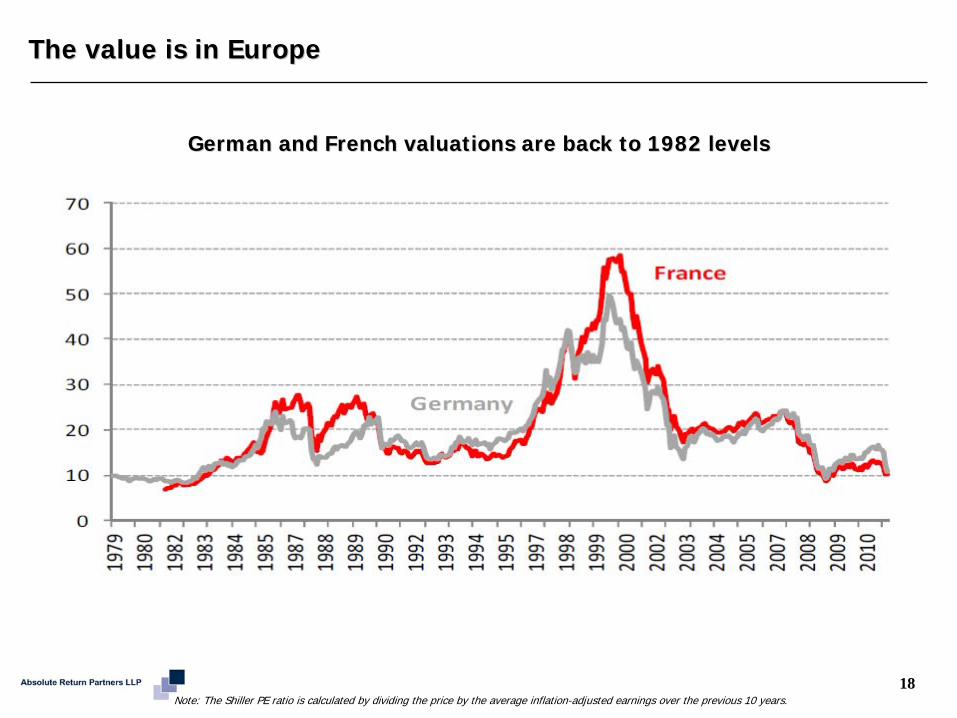

The value is in EuropeThe value is in Europe

Note: The Shiller PE ratio is calculated by dividing the price by the average inflation-adjusted earnings over the previous 10 years. 18

German and French valuations are back to 1982 levelsGerman and French valuations are back to 1982 levels

Source: Blackrock, Oriel Securities. Based on FTSE All Share Index as at 7 September, 2011. 2012 P/E = 8.9.

LongLong--term returns are negatively correlated with entryterm returns are negatively correlated with entry--point P/Espoint P/Es

19

UK valuations consistent with attractive long term returnsUK valuations consistent with attractive long term returns

Investment Conclusion # 1Investment Conclusion # 1

20

Overweight UK and stronger eurozone markets (ex financials) primarily for valuation reasons but also because a eurozone resolution is expected within 12 months;

Underweight US and emerging markets as economic growth will disappoint;

Underweight (most) commodities as EM weakness will take its toll on energy and metals in particular.

21Source: Kingdon Capital Management, JP MorganNote: Shaded areas indicate U.S. recession

High yield spreads are significantly above long term averagesHigh yield spreads are significantly above long term averages

High Yield Spread to 5High Yield Spread to 5--Year US TreasuriesYear US Treasuries

22Source: Kingdon Capital Management, JP MorganNote: Shaded areas indicate U.S. recession

Adjusted spreads are near record highs Adjusted spreads are near record highs

Spreads measured as % of total yieldSpreads measured as % of total yield

23

Default rates are near 25 year lowsDefault rates are near 25 year lows

Source: Kingdon Capital Management, JP MorganNote: Shaded areas indicate U.S. recession

High Yield Default RateHigh Yield Default Rate

Investment Conclusion # 2Investment Conclusion # 2

24

Corporate balance sheets in much better shape than sovereign and household balance sheets;

Overweight both US and European credit (ex financials);

Investment grade is attractive but the real value is to be found in high yield;

Focus on US high yield near term (less macro risk) but be prepared to switch to European high yield as 2012 progresses.

25

Recommended weightings (next 12 months)Recommended weightings (next 12 months)

26

This document has been issued by Quartet Capital Partners LLP (“Quartet”), which is authorised and regulated by the Financial Services Authority (“FSA”). The information in this document does not constitute, or form part of, any offer to sell or issue, or any offer to purchase or subscribe for shares, nor shall this document or any part of it or the fact of its distribution form the basis of or be relied upon in connection with any contract. This financial promotion and the products and services it describes are directed at professional clients or eligible counterparties only. Retail clients may not rely on the information contained here and should seek independent professional advice. Quartet has not taken any steps to ensure that the securities or products referred to in this document are suitable for any particular investor and no assurance can be given that the stated investment objectives will be achieved. Quartet may, to the extent permitted by law, act upon or use the information or opinions presented herein, or the research or analysis on which it is based, before the material is published.

Past performance is not indicative of future results, which may vary. The value of investments and the income derived from investments can go down as well as up. Future returns are not guaranteed, and a loss of principal may occur. Opinions expressed are current opinions as of the date appearing in this material only. No part of this material may, without Quartet’s prior written consent, be (i) copied, photocopied or duplicated in any form, by any means, or (ii) distributed to any person that is not an employee, officer, partner, or authorised agent of Quartet.

Any examples contained here are provided for illustrative purposes only and are not actual results. If any assumptions used do not prove to be true, results may vary substantially. Some strategies may include the use of derivatives which often involve a high degree of financial risk because a relatively small movement in the price of the underlying security which may result in a disproportionately large movement in the price of the derivative and are not suitable for all investors. No representation regarding the suitability of these instruments and strategies for a particular investor is made.

Where applicable, emerging markets securities may be less liquid and more volatile and are subject to a number of additional risks, including but not limited to currency fluctuations and political instability. Specific transactions involving overseas securities or products may involve currency fluctuations which may affect the value of a specific investment or strategy. Any opinions and/or estimates expressed reflect the author’s judgment as of the date of this presentation and are subject to change without notice. They may involve a number of assumptions that may not prove to be valid so actual results may vary substantially. Any reference to a specific company, security or product does not constitute a recommendation to buy, sell, hold or directly invest in a company or its securities or a named product.

Please be aware that Quartet does not provide tax advice to its clients. All investors are strongly urged to consult their tax and legal advisors regarding any potential transactions or investments. There is also no assurance that the tax status or treatment of a proposed transaction or investment will continue in the future and tax treatment or status may be changed by law or government action in the future or on a retroactive basis. Prospective investors should inform themselves as to any applicable legal requirements and taxation and exchange control regulations in the countries of their citizenship, residence or domicile which might be relevant.

The law may restrict distribution of this document in certain jurisdictions; therefore, persons into whose possession this document comes should inform themselves about and observe any such restrictions. This document, the information contained herein, and any oral or other written information disclosed or provided in connection with this document is strictly confidential and may not be reproduced or redistributed, in whole or in part, nor may its contents be disclosed to any other person under any circumstances without the prior written consent of a partner of Quartet.

Quartet Capital Partners LLP is a Limited Liability Partnership registered in England and Wales No OC345770.

Registered Office Address: 16 Water Lane, Richmond, Surrey TW9 1TJ.

A list of members is available for inspection at the registered office.

Copyright © 2011, Quartet Capital LLP. All rights reserved.

Risk WarningRisk Warning