aca reinsurance program and the 3rs presented by : karl ideman ©2011 pool administrators inc. 1

TRANSCRIPT

©2011 Pool Administrators Inc.

ACA Reinsurance Program and the 3Rs

Presented by : Karl Ideman

1

©2011 Pool Administrators Inc.

The 3 Rs

– Addressing ACA and the 3 Rs:• Reinsurance• Risk corridors• Risk adjustment

– Potential transitional issues and interim changes related to exchanges under three scenarios

• Best Case• Mid Case• Worst Case

2

©2011 Pool Administrators Inc.

Items of Interest• HHS released Standards and Proposed Rules on July 13th

with 75 days for Comments Related to the 3 Rs• Permanent Risk Adjustment• Temporary Reinsurance• Temporary Risk Corridors

• Proposed Approaches by HHS follow traditional NAIC Model methodology

• Transitional Issues for each State:– How and Why to quickly establish a State Reinsurance

Program?• The markets thrive or at least they survive

– What might happen if a State does not?• The markets may fail!

3

©2011 Pool Administrators Inc.

Three New “Risk Sharing” Mechanisms

1. Permanent Risk Adjustment will compensate insurers when they write high risk business in the individual or in the small employer market either inside or outside the exchange(s);

2. Temporary Reinsurance will compensate insurers when they pay claims for individual high risks either inside or outside the exchange(s);

3. Temporary Risk Corridors will limit the extent of issuer gains or losses inside the exchange

4

©2011 Pool Administrators Inc.

Same Rates for Comparable Benefits

4. Issuers must consider all enrollees of non-grandfathered individual plans and non-grandfathered small employer plans offered inside and outside of the Exchange as

members of a single risk pool in each respective market with the same base rates for comparable benefits.

5

Individual MarketReinsurance Contributions

Reinsurance PaymentsRisk Adjustment

Small Group MarketReinsurance Contributions

OnlyRisk Adjustment

No

Su

bsi

die

s N

o T

ax Cre

dit

s

Ou

tsid

e E

xch

ange

Mu

st p

rovi

de

ess

en

tial

be

ne

fits

Can

se

ll b

ron

ze a

nd

cat

astr

op

hic

pla

ns

IndividualReinsurance Contributions

Reinsurance PaymentsRisk Adjustment

Risk Corridors

SHOPSmall Employer 1-100*

*state option: 1-50 for years 2014-2015

Reinsurance Contributions OnlyRisk Adjustment

Risk Corridors

Inside Exchange

QHPs

Sub

sidies

Tax Cred

its

Subject to ALL QHP Requirements

No Risk Corridor

No Risk Adjustment

Reinsurance Contributions Only

- Exempt from majority of new market reforms- Individual and Small Group Plans Not Subject to

Single Risk Pool requirement

GRANDFATHERED

No Risk Corridor

No Risk Adjustment

Reinsurance Contributions Only

Self-Funded

No Risk Corridor

No Risk Adjustment

Reinsurance Contributions Only

Large Group

©2011 Pool Administrators Inc.

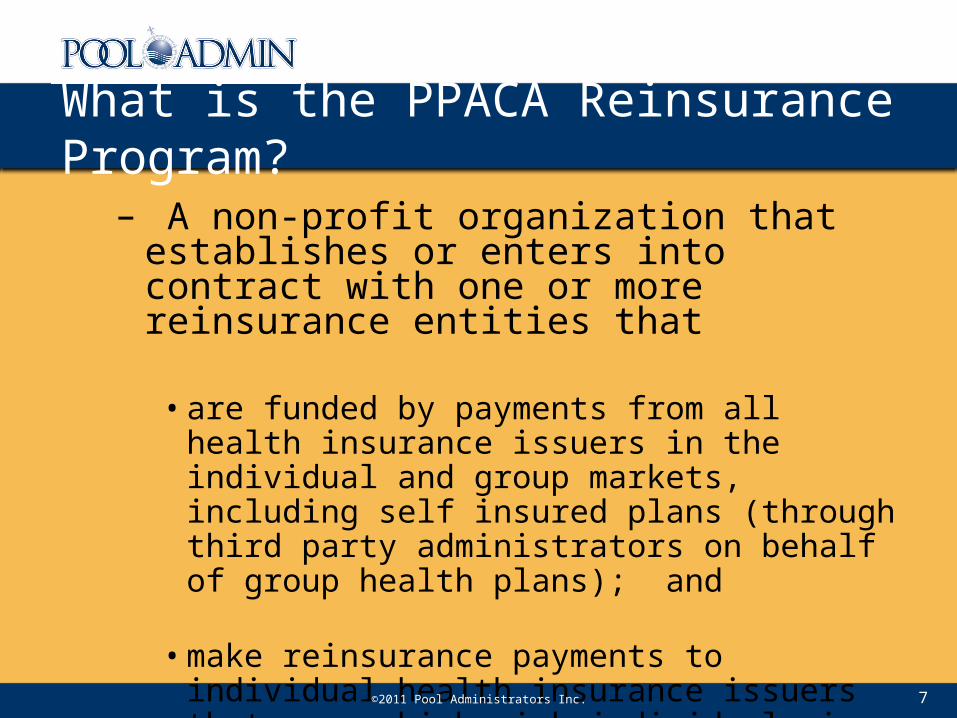

What is the PPACA Reinsurance Program?

– A non-profit organization that establishes or enters into contract with one or more reinsurance entities that

• are funded by payments from all health insurance issuers in the individual and group markets, including self insured plans (through third party administrators on behalf of group health plans); and

• make reinsurance payments to individual health insurance issuers that cover high risk individuals in the individual market (excluding grandfathered plans)

7

©2011 Pool Administrators Inc.

How Will Reinsurance Be Administered In 2014?

• Notice of Proposed Rule Making (NPRM) has been issued with Proposed Rules

– Final Rules will be produced some time in 2012.

– We already know that the proposed rules follow traditional reinsurance administration methods now followed by this non-profit state legislated program

8

©2011 Pool Administrators Inc.

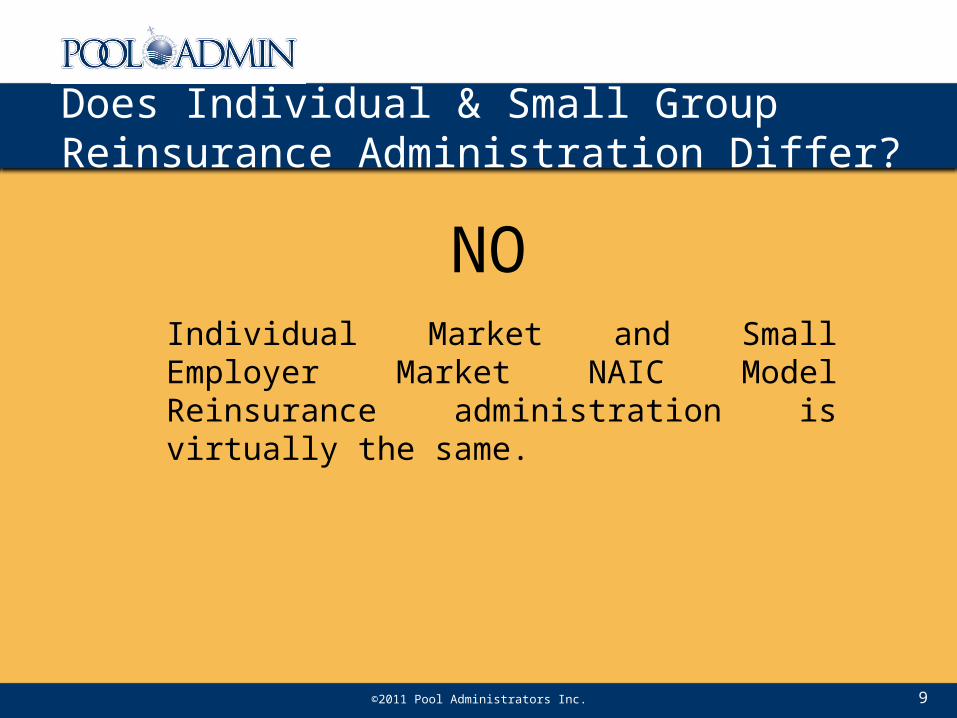

Does Individual & Small Group Reinsurance Administration Differ?

9

Individual Market and Small Employer Market NAIC Model Reinsurance administration is virtually the same.

NO

©2011 Pool Administrators Inc.

How MIGHT the PPACA Reinsurance Program Work?

10

The PPACA Reinsurance Program MIGHT work much the same as the NAIC Model.

©2011 Pool Administrators Inc.

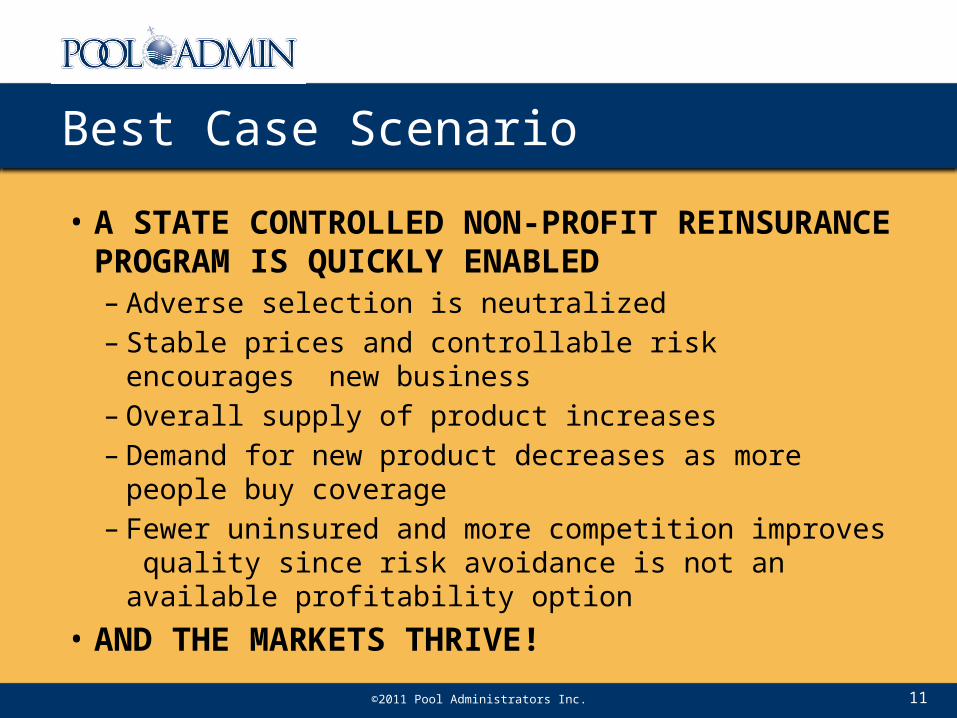

Best Case Scenario

• A STATE CONTROLLED NON-PROFIT REINSURANCE PROGRAM IS QUICKLY ENABLED– Adverse selection is neutralized– Stable prices and controllable risk encourages new

business– Overall supply of product increases– Demand for new product decreases as more people buy

coverage– Fewer uninsured and more competition improves quality

since risk avoidance is not an available profitability option• AND THE MARKETS THRIVE!

11

©2011 Pool Administrators Inc.

Mid Case Scenario

• A STATE CONTROLLED NON-PROFIT REINSURANCE PROGRAM IS QUICKLY ENABLED– and the Wild Cards Appear

• the Individual Mandate is repealed but Individual guarantee issue survives, and

• Insurers are unable to price to the level of risk they assume

– but the State is able to balance the markets through reinsurance and risk adjustment

• AND THE MARKETS SURVIVE !12

©2011 Pool Administrators Inc.

Worst Case Scenario

• A STATE NON-PROFIT REINSURANCE PROGRAM IS NOT ENABLED (FEDERAL FALLBACK)– However, the Wild Cards appear– Adverse Selection runs rampant– Federal market mechanisms and their related market

controls are not flexible enough to balance the markets– Health Plans exit the markets– Overall supply decreases and adverse selection tightens

its grip in the death spiral

• AND THE MARKETS MAY FAIL! 13

©2011 Pool Administrators Inc.

Important Planning Considerations

• The Non-Profit Reinsurance Program can be State controlled regardless of the status of the Exchange

• The proposed rules allow states to coordinate their high risk pools with their reinsurance programs after 2014

14

©2011 Pool Administrators Inc.

Important Planning Considerations

• A State should follow a simple, safe and cost effective implementation approach for reinsurance– Use the existing high risk pool or reinsurance pool

infrastructure wherever possible– Use the proven NAIC Model for Reinsurance by converting

small group provisions into individual market provisions and allow options for prospective, retrospective and selective ceding of individual risks

– All this proven infrastructure and simple flexibility will help but effective reinsurance will still be very challenging because of the volatility of dumping and the untried nature of commercial risk adjustment

15

©2011 Pool Administrators Inc.

Important Timing Considerations

• Risk Adjustment is already behind Schedule and Reinsurance should be designed and tested in tandem so both can be tested against the risk corridor methodology and then applied to the MLR before Issuers have to file their rates based on the MLR

– Oct 2011: Methodology for 3 Rs defined Too Late Already – Jun 2012 Software developed and input data collected – Jan 2013 RA and Reinsurance modeled Drop Dead Date– Jul 2013 Latest date for issuers to submit filings – Jan 2014 Enrollment Begins

16

©2011 Pool Administrators Inc. 17

Contact:Karl IdemanPool Administrators Inc.Phone: 860-306-9936Email: [email protected]

Questions?