acacia mining plc total economic and tax …/media/files/a/acacia/reports/2015/...acacia mining’s...

TRANSCRIPT

Acacia Mining plc total economic and tax contributions in Tanzania, 2014 Prepared for Acacia Mining plc April 2015

Acacia Mining’s total economic and tax contributions in Tanzania, 2014

(Page intentionally left blank)

Acacia Mining plc’s total economic and tax contributions in Tanzania, 2014

EY | i

Executive summary

This report provides estimates of Acacia Mining plc’s (Acacia Mining plc is hereinafter referred

to as Acacia) economic contribution in Tanzania. This is the third annual EY analysis of the

company’s economic contribution.1” The direct impacts are for Acacia’s operations in 2014; the

estimates of related economic activity in Tanzania use multipliers developed in EY’s previous

studies. Acacia owns and operates three gold mines in Tanzania: Bulyanhulu, Buzwagi, and

North Mara. The economic impact analysis described in this report finds that Acacia’s

Tanzanian entities support economic activity across a wide range of industries in Tanzania,

including thousands of jobs with suppliers and other businesses and millions of dollars of

government revenue.

Table ES-1 summarizes the key findings of the analysis. Acacia’s total direct, indirect, and

induced economic contribution in Tanzania in 2014 included nearly 54,000 jobs, approximately

US$459 million of labour income, and nearly US$678 million of value added (GDP). In total,

including direct, indirect, and induced taxes paid by Acacia, its employees, suppliers, and other

affected businesses, Acacia’s total tax contribution in 2014 was an estimated US$179 million.

The overall employment multiplier (including indirect and induced economic activity) is 12, which

can be interpreted as, for each direct Acacia employee, 11 additional jobs are supported in the

broader Tanzanian economy. This multiplier is consistent with the high output per worker

experienced in the mining industry.

In general, the economic and fiscal contributions estimated in this analysis can be expected to

change in proportion to changes in Acacia’s direct employment, labour income, and value

added in future years. The estimates would also be affected by changes in the nature of capital

investment expenditures or the industry distribution of Acacia’s supplier purchases.

Table ES-1 Estimated economic and fiscal contributions of Acacia in Tanzania, 2014

Millions of 2014 US dollars; total number of employees

Direct

Indirect & induced

Total

Wage employment 4,443 49,500 53,943

Labour income $141 $320 $459

Value added (GDP) $190 $488 $678

Tanzania taxes, net of anticipated VAT refunds $118 $61 $179

Note: Figures may not sum due to rounding. Including self-employed proprietors, the estimated total employment impact is 76,943 workers. Source: EY analysis based on Acacia data and publicly available economic data for Tanzania. Data provided by Acacia management were not independently audited by EY.

Specific findings of the analysis include the following:

► Acacia is a high-wage employer. In 2014, Acacia employed more than 4,400 workers in

Acacia Mining plc’s total economic and tax contributions in Tanzania, 2014

EY | ii

Tanzania and paid wages and benefits totaling US$141 million. On average, employees

received more than US$31,000 in wages and benefits.

► Acacia provides jobs to Tanzanian nationals. Of Acacia’s 4,443 full and part-time wage

employees in Tanzania, 4,161 (94%) were Tanzanian nationals, on average.2 The

proportion of Acacia employees who are Tanzanian nationals is consistent with other mining

companies in Tanzania.3 Tanzanian nationals employed by Acacia received an average

annual wage of nearly US$16,400 (26.7 million TSH)—which remained unchanged from

2013. The average annual wage for Tanzanian nationals employed by Acacia in 2014 was

higher than the average earnings of US$1,525 (2.5 million TSH) for Tanzanian workers

throughout the economy in 2014, and higher than the average wage of the Tanzanian

mining industry of approximately US$1,000 (1.6 million TSH).

► Acacia has a strong Tanzanian supply chain. In 2014, Acacia’s Tanzanian entities

purchased US$488 million of goods and services from other Tanzanian businesses for use

by its Tanzania operations. These purchases of Tanzanian goods and services accounted

for 71% of total supplier purchases made by Acacia’s Tanzanian entities in 2014, compared

to 58% in 2013. Of this amount, US$99 million was purchased from businesses located in

the same region as Acacia’s mines.

► Acacia’s supply-chain spending supported 30,500 indirect wage-earning jobs.

Acacia’s supplier spending supported jobs across all sectors of the Tanzanian economy,

with the most jobs concentrated in the trade, transportation, and other services sectors.

► Consumption spending by Acacia and supplier employees supported an additional

19,000 induced jobs. These jobs, related to consumption spending by Acacia and supplier

employees on food, clothing, housing, and other goods and services, supported jobs that

were concentrated in the agriculture and trade sectors.

► Acacia’s total contribution to Tanzanian GDP in 2014 was approximately US$678

million. This level of total GDP contribution is equivalent to approximately 2% of total

Tanzanian GDP in 2014. Overall, the mining sector contributed 3.3% to the Tanzanian GDP

in 2013.4

► Acacia paid more than US$65 million in taxes and royalties in Tanzania in 2014.

Approximately 63% of Acacia’s direct Tanzanian tax payments was related to corporate

income taxes and royalties, while the remaining 37% was related to unrecovered VAT,

customs & excise taxes, payroll taxes, and other levies. The amount of tax paid by Acacia

declined by approximately US$6 million (8%) from 2013 to 2014.

► Acacia’s total government revenue contribution per employee is approximately 20

times higher than the national average. Per employee, Acacia contributes US$14,700 of

direct taxes and royalties, compared to approximately US$700 per worker economy-wide.

► Acacia’s employees contribute additional tax revenue. In 2014, Acacia’s employees

paid an estimated US$53 million in taxes. The majority (72%) of the estimated employee tax

Acacia Mining plc’s total economic and tax contributions in Tanzania, 2014

EY | iii

impact results from individual income taxes and social security contributions paid by

employees. Employees also paid significant amounts of VAT, excise, and other taxes on

consumption spending.

► Acacia’s economic activity resulted in indirect and induced tax impacts of US$61

million, for a total tax contribution of US$179 million.

► Acacia invests in its local communities. In 2014, Acacia’s social investments in Tanzania

totaled US$10.9 million, supporting a variety of education, infrastructure, water and

sanitation initiatives, primarily in the communities surrounding Acacia’s mines. Of this

amount, US$8.5 million related to Acacia’s Maendeleo Fund.

Acacia Mining plc’s total economic and tax contributions in Tanzania, 2014

EY | iv

Contents

1. Introduction ......................................................................................................................... 1

2. Estimating Acacia’s total economic and tax contribution – study methodology and current

literature ............................................................................................................................. 3

2.1 Study methodology ...................................................................................................... 3

2.2 Studies of mining economic multiplier effects ............................................................... 6

3. Acacia’s direct contributions in Tanzania in 2014 ................................................................ 7

3.1 Gross value added (GDP) ............................................................................................ 7

3.2 Employment ................................................................................................................. 8

3.3 Employee compensation/labour income ......................................................................10

3.4 Tanzania taxes paid and collected ..............................................................................11

4. Acacia’s indirect and induced economic and tax contributions, 2014 .................................13

4.1 Acacia’s direct, indirect, and induced economic contributions .....................................13

4.2 Acacia’s direct, indirect, and induced tax contributions ...............................................18

5. Acacia’s social investments, 2014 ......................................................................................21

6. Study limitations .................................................................................................................23

7. Conclusion .........................................................................................................................25

Appendix. Acacia Economic and fiscal contribution comparison 2013 and 2014 .......................26

References ...............................................................................................................................27

Endnotes ...................................................................................................................................28

Acacia Mining’s total economic and tax contributions in Tanzania, 2014

EY | 1

Acacia’s total economic and fiscal contribution in Tanzania,

2014

1. Introduction

The economic impact of Acacia’s gold production extends beyond its mines and employees.

The following is an update of prior EY analyses based on detailed 2012 and 2013 economic and

operating information for Acacia. The following direct impacts are for Acacia's operations in

2014; the estimates of related economic activity in Tanzania use multipliers developed in the

2012 analysis.

Acacia was created from Barrick Gold Corporation in an initial public offering in 2010. Acacia

was known as African Barrick Gold until November 2014. Acacia owns and operates three gold

mines in Tanzania—Bulyanhulu, Buzwagi, and North Mara. These mines are in the Lake Zone

of Tanzania, located near Lake Victoria in the northwest region.5

Acacia acquired Aviva Mining Kenya Ltd (AMKL) from Aviva Corporation (Aviva) in October

2012, and thereby acquired AMKL’s interests in the West Kenya Project through the Lonmin

Joint Venture with AfriOre International, a subsidiary of South African-based platinum producer

Lonmin Plc. Acacia also acquired AMKL’s right to earn up to a 75% interest in a second joint

venture with Advance Gold Corporation. The licenses occupy 2,208 square kilometres of the

highly-prospective Ndori Greenstone belt in Kenya, which forms part of the Archaean Tanzanian

Craton. Previous exploration identified significant potential for gold, as well as copper, lead, and

zinc. The license areas have been divided into two large gold camps, known locally as the

Kakamega Dome Camp and the Lake Zone Camp.

Acacia’s oldest and largest mine, Bulyanhulu, has been in production since 2001 and produced

234,786 troy ounces of gold during 2014. Copper is produced as a co-product at both

Bulyanhulu and Buzwagi. Table 1 summarizes Acacia’s mine operations in Tanzania, including

2014 production and anticipated mine life.

Table 1 Overview of Acacia mines Gold amounts in troy ounces

First year of production

2014 production

Proven and probable reserves

Expected end of mine life

Bulyanhulu 2001 234,786 9,530,000 2045 (34 years)

Buzwagi 2009 210,063 898,000 2024 (5 years)

North Mara 2002 273,803 2,047,000 2019 (9 years)

Total

718,652 12,475,000

Source: Acacia data. Mine life dates were provided by Acacia Management. Data provided by Acacia were not

independently audited by EY.

In 2013, mining comprised 3.3% of Tanzanian GDP and employed over 15,000 workers,

supported by a gold mining sector that ranked fourth in Africa in terms of production volume.6

Acacia Mining’s total economic and tax contributions in Tanzania, 2014

EY | 2

Gold is the largest mineral commodity in Tanzania, with gold exports comprising 89% of the

value of total mineral exports in 2014.7 Figure 1 illustrates Acacia’s share of Tanzania gold

production from 1998 through 2014. Acacia opened three mines between 2001 and 2005. Over

the period, Tanzania’s gold mining sector was also rapidly expanding, with production

increasing nearly 75% over five years and 2005 production levels more than 11 times higher

than in 1998. Between 2001 and 2005, Acacia averaged 26% of total Tanzanian production.

Since 2006, Acacia has produced, on average, just over half of all of Tanzania’s gold.

Figure 1 Acacia and total Tanzanian gold production, 1998-2014 Millions of troy ounces

* 2014 total Tanzanian gold production data are not yet available. 2014 represents only Acacia gold production for the

year. 49% represents Acacia’s average share of Tanzanian gold production from 2005-2013.

Source: US Geological Survey; Acacia data. Data provided by Acacia management were not independently audited

by EY.

Mining is a highly capital-intensive sector requiring substantial up-front and ongoing capital

investments. Because of the long-term nature of mining investments, once a mine has achieved

consistent profitability, it can contribute to the local economy for years to come. Acacia's

Bulyanhulu mine, for instance, contains more than 9.5 million troy ounces of proven and

probable gold reserves. Due to the estimated long life of the Bulyanhulu mine, the economic

and fiscal benefits related to the mine’s operations will continue through that period.

The following sections detail Acacia’s direct contributions to the Tanzanian economy and its

citizens through its mine operations as well as additional related economic activity.

0.0

0.5

1.0

1.5

2.0

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Millio

ns o

f tr

oy o

un

ces

Acacia gold production Non-Acacia gold production in Tanzania

2001-2004

Acacia avg. prod.: 315,500 t oz Acacia avg. share: 23%

2005-2014* Acacia avg. prod.: 668,208 t oz

Acacia avg. share: 49%

Acacia Mining’s total economic and tax contributions in Tanzania, 2014

EY | 3

2. Estimating Acacia’s total economic and tax contribution – study

methodology and current literature

2.1 Study methodology

Acacia’s total economic contribution consists of three elements, described below.

1. Direct contribution. Acacia’s direct contribution includes the total number of wage

employees and amount of employee compensation (gross wages and salaries, employer

payroll taxes, and other employee costs) at its Tanzanian entities, including mines and

support offices. The direct contribution also includes the total amount of GDP attributed to

Acacia’s Tanzanian operations and tax payments by Acacia and Acacia employees.

2. Indirect contribution. The indirect contribution is the supplier-related Tanzanian economic

activity that results from Acacia’s purchases of goods and services, including spending on

contractors and social investments in local communities. Purchases from other Tanzanian

businesses providing engineering services, utilities, telecommunications, information

services, and other operating inputs support employment in these industries. In turn, these

suppliers purchase operating inputs, which support additional rounds of indirect economic

contributions.

3. Induced contribution. The induced economic contribution reflects the contribution from

employee spending. Employees at Acacia’s mines and support offices and employees at

other businesses indirectly affected by Acacia’s operations use a portion of their incomes to

purchase goods and services from Tanzanian businesses. These transactions support

employment at businesses such as retailers, restaurants, and service companies.

Figure 2 shows the three components of the total economic contribution. The left-hand side of

the diagram shows the components of Acacia’s direct contribution, including mining,

administrative, and exploration operations in Tanzania. Each of these activities creates

additional economic impacts through two primary channels: (1) domestic input purchases and

(2) payments to employees and proprietor income (labour income). Domestic input purchases

support additional indirect economic contributions as Acacia purchases goods and services

from Tanzanian businesses. The labour income earned by Acacia and supplier employees

creates induced effects resulting from consumer spending.

Acacia Mining’s total economic and tax contributions in Tanzania, 2014

EY | 4

Figure 2 Overview of the components of economic contribution

Components of Acacia’s direct contribution Multiplier drivers

Related economic activity

The magnitude of economic contribution in Tanzania is determined by several factors, including

supplier relationships with businesses in the country. This impact can be expressed using an

“economic multiplier” which is equal to the total economic impact per unit of direct impact. The

economic multipliers in this study were estimated using the 2007 Social Accounting Matrix

(SAM) for Tanzania, published by the Purdue University Global Trade Analysis Project (GTAP),

publicly available data reported by the Tanzanian National Bureau of Statistics (NBS), and

operations and supplier purchase information provided by Acacia. (A SAM represents all

economic flows in an economy, “taking into account the patterns of production and demand, and

various institutional relationships.”8)

Figure 3 details the relationships between the data inputs (including source information), steps

in the analysis, and the results that are described in this report.

Several key inputs to the economic and tax contribution analysis have been updated to reflect

Acacia’s 2014 operations, including employment, employee compensation, the level of supplier

purchases, and taxes paid.

The multipliers applied in the following analysis have not been re-estimated and are based on a

detailed analysis of Acacia’s operations and Tanzanian economic and tax data from 2012. For

further details please see the November 2013 EY report prepared for Acacia.

Acacia’s exploration activities

Acacia’s Tanzania administrative offices in

Dar es Salaam

Acacia’s TZ gold mines:

Bulyanhulu, Buzwagi, &

North Mara

Indirect effect (supplier-related)

TZ input purchases

TZ input purchases

TZ input purchases

Induced effect (consumption-related)

TZ labour income

TZ labour income

TZ labour income

Acacia Mining’s total economic and tax contributions in Tanzania, 2014

EY | 5

Figure 3 Diagram of analysis inputs, intermediate results, and outputs

J. 2014 ratios of taxes to economic activity

USD of tax collections per USD of economic activity (e.g.

personal income)

K. Total tax contribution Total tax contribution =

I + (G-F)*J

F. Direct economic contribution

2014 Acacia data on direct impacts (employment, employee compensation, sales, and input

purchases)

D. Derivation of Acacia

indirect & induced impacts

E. Estimation of “total

effects” multipliers

by industry, for gross value added (GDP), labour income,

and employment

C. 2014 Acacia supplier data

domestic and total supplier purchases by type of purchase

A. National input-output (I-O) & statistical data

TZ National Bureau of Statistics and the Purdue University Global Trade Analysis Project (GTAP)

B. National I-O table unadjusted multipliers

for each industry

G. Total economic contribution

Total economic contribution = E * F

I. Direct tax contribution

H. 2014 Acacia tax data Direct business taxes paid by

Acacia & income taxes paid by Acacia employees

Mu

ltip

lier

derivatio

n

Co

ntr

ibutio

n e

stim

ate

s

Key

Reported output

Intermediate step

Input

Acacia Mining’s total economic and tax contributions in Tanzania, 2014

EY | 6

2.2 Studies of mining economic multiplier effects

While there is not a significant body of Tanzanian economic impact analysis using economic

multipliers, several studies in Tanzania and in peer countries have been identified to inform this

analysis of Acacia’s contributions to the Tanzanian economy.

A review of Tanzania- and mining-related economic multiplier studies found a relatively small

range of mining direct and indirect output multipliers, varying from 1.0 to 2.0. Employment and

labour income multipliers estimated in the reviewed studies were distributed over a wider

range–from 1.3 to 11.1 for employment, and from 1.2 to 5.7 for labour income. Other literature

considered the implications for multiplier effects of agrarian-based economies and the mining

industry’s capital-intensive nature.

The most similar study to this analysis was of the economic contributions of a Ghanaian gold

mine, which estimated the direct, indirect, and induced economic contributions of gold mining

activities, based on the GTAP database of economic relationships.9 Further, the Ghana and

Tanzania economies share certain similarities, with predominantly agrarian economies and

large (or growing) mining sectors. The Ghana study found a total gold mining employment

multiplier of 28.4 and a labour income multiplier of 5.5.

Most of the current economic studies for Tanzania and comparison countries include only the

indirect (supplier-related) economic contribution. These studies report mining-sector

employment multipliers ranging from 1.3 to 21.0. In general, mining sector multipliers reported

for other countries in Africa tend to be higher than the multipliers reported for Tanzania. Some

studies of mining sector economic contributions in Tanzania cite the limited supply of locally-

produced operating inputs purchased by the Tanzanian mining industry as a contributing factor

to the low estimated indirect multipliers.

Of the eight economic multiplier studies examined, only two studies included estimates of the

induced (consumption-related) economic impacts. The Ghana study estimated that employment

related to induced activity comprised 26% of the total employment impact.10

Acacia Mining’s total economic and tax contributions in Tanzania, 2014

EY | 7

3. Acacia’s direct contributions in Tanzania in 2014

This section presents Acacia’s direct contributions to the Tanzanian economy in 2014 through

its operations and investment activities, presenting a snapshot of Acacia’s operations during the

year. Much of Acacia’s operations are annual impacts, producing economic activity during each

year of the mine’s life. Based on Acacia’s current projections, the company anticipates operating

its largest mine in Tanzania through at least 2045.

The economic and fiscal contributions presented in this report are described in terms of four key

indicators: (1) employment, (2) employee compensation/labour income, (3) gross value added

(GDP), and (4) tax payments. Each of these indicators is described in detail in the following

sections, illustrating how Acacia’s operations contribute directly to the Tanzanian economy.

Highlights of Acacia’s direct contribution include:

► Acacia’s Tanzanian entities were mostly staffed by Tanzanian workers—Tanzanian

nationals made up 94% of Acacia’s employees in Tanzania in 2014. This proportion is

consistent with the share of employees at other miners located in Tanzania who are

Tanzanian nationals.

► Acacia’s direct contribution to GDP in Tanzania was US$190 million in 2014—a 21% decline

from Acacia’s 2013 direct contribution to GDP of US$240 million. This decline reflected

lower employment and lower tax payments.

► The average annual gross wage received by Tanzanian nationals employed by Acacia was

approximately US$16,400 (26.6 million TSH)—far in excess of the overall Tanzanian

average gross wage for paid employees of approximately US$1,000 (1.6 million TSH).11

► In 2014, Acacia paid approximately US$65 million in Tanzanian taxes, including US$41

million of corporate income taxes and royalties, US$16 million of employer payroll taxes, and

US$8 million of indirect taxes, including anticipated unrecoverable VAT, customs duties,

excise taxes, and other levies.

3.1 Gross value added (GDP)

During 2014, Acacia’s operating expenditures totaled nearly US$878 million in payments to

employees as wages and benefits, to the government as taxes, and to communities as

purchases from local suppliers. The composition of Acacia’s expenditures in Tanzania is shown

in Figure 4.

Gross value added (reported as GDP) is the broadest measure of economic activity included in

this analysis. The sum of gross value added across all industries is equivalent to a country’s

GDP. Acacia’s contribution to GDP is the sum of its payments to labour, capital, and

government (indirect taxes). In 2014, Acacia’s direct GDP was an estimated US$190 million.

Acacia Mining’s total economic and tax contributions in Tanzania, 2014

EY | 8

Figure 4 Composition of Acacia’s expenditures, 2014

Millions of 2014 US dollars

Source: Acacia data. Data provided by Acacia management were not independently audited by EY.

3.2 Employment

The employment estimates are reported in terms of two major classifications of jobs: (1) wage

employment and (2) proprietors, described below.

1. Wage employment: As defined by the Tanzania NBS, wage employment includes regular

employees and casual workers. Regular employees are permanent and temporary

employees who have been employed on a weekly or monthly basis for more than one

month.12 Casual workers are defined as persons receiving daily wages.

2. Proprietors: Proprietors are self-employed individuals who own or manage a business or

other such establishment. Proprietors do not include subsistence farmers.

Acacia’s direct employment is the average number of Tanzanian and international wage

employees at Acacia’s Tanzania locations in 2014. These figures are based on the monthly

number of paid employees, provided by Acacia, and are shown in terms of total headcount, not

full-time equivalents (FTEs). In 2014, Acacia directly employed 4,443 wage employees in

Tanzania, accounting for 98% of Acacia’s total employment across all countries. Figure 5 shows

the geographic distribution of Acacia’s employment in Tanzania in 2014. The Bulyanhulu mine

has the largest share of employment, employing 52% of Acacia’s total workforce in Tanzania.

Corp. income tax, royalties, net VAT payments, and customs & excise taxes; $49mm (6%)

Suppliers, contractors & communities; $688mm (78%)

Employee payroll costs, incl. taxes; $141mm (16%)

Total

$878mm

Acacia Mining’s total economic and tax contributions in Tanzania, 2014

EY | 9

Figure 5 Average Acacia’s employment in Tanzania, by Tanzanian entity in 2014

Note: The Tulawaka site closed on July 30, 2013. The 2 employees shown in the figure are the average number of employees during the year. Figures may not appear to sum due to rounding of average monthly headcounts. Source: Acacia data. Data provided by Acacia management were not independently audited by EY.

On average, 94% (4,161 employees) of Acacia’s total 4,443 employees in Tanzania during 2014

were Tanzanian nationals. Studies of Tanzania’s governance and oversight of the mining sector

have cited the perception of limited job opportunities for Tanzanian nationals at mining

operations due to the high number of international employees working on-site.13 However, this is

changing over time as Tanzania’s mining sector develops and companies continue to invest in

employee training, resulting in a more skilled domestic workforce and more job opportunities for

Tanzanians.14

According to a report published by the Tanzanian Ministry of Energy and Metals (MEM) in 2011,

Tanzanian nationals made up 90% of employment at both the Bulyanhulu and Buzwagi mines in

2009.15 During the period 2014, Acacia increased relative employment of Tanzanians at the

Bulyanhulu mine to 94%, while the percentage of Buzwagi employees who are Tanzanian has

increased to 96%.16 Over the past five years, the share of Acacia’s employees in Tanzania that

are Tanzanian nationals has increased from 90% to 94% while that of expatriates decreased

Dar es Salaam 127

Bulyanhulu 2,318

Buzwagi 901

North Mara 1,042

Exploration 53

Tulawaka

2

Acacia Mining’s total economic and tax contributions in Tanzania, 2014

EY | 10

from 10% to 6% in the same period. In other words, expatriates’ share of Acacia employment

declined by approximately 40% from 2010 to 2014.

The composition of Acacia’s employment in Tanzania from 2010 to 2014 is shown in Table 2.

Table 2 Composition of Acacia’s employment in Tanzania, 2010-2014

2010 2011 2012 2013 2014

Tanzanian nationals 4,184 4,650 4,953 4,691 4,161

Foreign nationals 490 538 517 394 283

Total Acacia employees in Tanzania 4,674 5,188 5,470 5,084 4,443

% Tanzanian nationals 90% 90% 91% 92% 94%

Source: Acacia data. Data provided by Acacia management were not independently audited by EY.

Note: 2014 data reflect average headcount across the entire year. As of year-end 2014, the share of

Acacia employees who were Tanzanian nationals had increased to 94.1%.

Acacia operations are also supported by a significant number of mining, engineering, security,

and construction contractors who work on-site at Acacia mines and facilities. In 2014, Acacia

reported US$92 million in contractor spending related to the 3,517 contractors working on-site at

Acacia’s mines, of which 3,320 (94%) were Tanzanian nationals. These contractors are

employed by other businesses (as opposed to independent contractors contracted as

individuals) and therefore these contracts are categorized as purchased services.

3.3 Employee compensation/labour income

Total employee compensation includes salaries, wages, and benefits. Salaries and wages are

defined as gross wages before deducting employee individual income tax. Benefits include

employer-contributed health insurance and retirement benefits, employer social security

contributions and payroll tax (skills and development levy), and the value of other employee

costs including training, meals, and travel. As shown in Figure 6, in 2014, Acacia’s employees in

Tanzania earned a total of US$141 million in compensation. This amount includes US$16

million of employer payroll taxes paid by Acacia in Tanzania, of which US$6 million was paid on

salaries to international employees. Further, according to data provided by Acacia, a significant

amount of individual income tax was paid by Tanzanian employees in 2014—US$21 million

(57% of individual income tax paid by all Acacia employees in Tanzania).

The average wage for Tanzanian nationals employed by Acacia in Tanzania was nearly

US$16,400 in 2014. Of total take-home wages paid by Acacia to employees in Tanzania, more

than half (54%) was paid to Tanzanian nationals.

Acacia Mining’s total economic and tax contributions in Tanzania, 2014

EY | 11

Figure 6 Composition of Acacia’s employee compensation in Tanzania, 2014

Millions of 2014 US dollars

Note: Employee taxes include individual income tax withholding and social security contributions. Employer payroll

taxes include employer social security contributions and skills and development levy payments.

Source: Acacia data. Data provided by Acacia management were not independently audited by EY.

3.4 Tanzania taxes paid and collected

Acacia’s tax contribution has three components: (1) direct taxes paid by Acacia, including

corporate income taxes and royalties, as well as indirect taxes on operations such as value-

added tax, payroll taxes, import duties and fuel levies; (2) individual income taxes paid by

Acacia’s employees; and (3) taxes withheld from suppliers and contractors and remitted by

Acacia on their behalf.

In 2014, Acacia paid US$141 million in Tanzanian taxes and royalties, as shown in Figure 7.

Corporate income taxes and royalties comprised 63% of taxes paid by Acacia (and, more

broadly, 37% of total taxes paid or collected by Acacia). Acacia paid $41 million in royalties and

paid no corporate income tax to the Tanzanian government. Under the Mining Tax Act of 2010,

Tanzania increased gold royalties from 3% to 4% and broadened the royalty base from net

value to gross sales (total revenue from domestic sales and exports).

Indirect taxes shown in Figure 7 include net VAT payments, fuel levies, environmental fees and

charges, and import duties. The net VAT payments included for Acacia are 2014 VAT payments

on inputs, net of expected refunds. Tanzania currently charges an 18% VAT for standard-rated

supplies. Exports of goods and services are subject to a 0% VAT. Fuel levies are assessed at

US$200,000 per site for Acacia properties.

Payroll taxes paid by Acacia in Figure 7 include social security contributions and skills and

development levy payments. Social security contributions are paid by both employers and

$0

$20

$40

$60

$80

$100

$120

$140

$160

Employee payroll taxes, $16mm

Employer taxes, $38mm

Take-home salaries & wages, $87mm

$141mm

Acacia Mining’s total economic and tax contributions in Tanzania, 2014

EY | 12

employees in Tanzania, with each contributing 10% of gross salary to the National Social

Security Fund.

In addition to the taxes paid by Acacia, Acacia withheld US$38 million on behalf of its

employees in 2015—an estimated US$12 million for employee social security contributions, and

more than US$25 million for individual income tax withholding. Individual income taxes are

assessed over five brackets, with a top marginal rate of 30%. Allowable deductions include

social security contributions and certain health care costs. At the average wage level earned by

Acacia employees, the average statutory individual income tax rate is 27%. The estimated

US$25 million of individual income taxes withheld by Acacia in 2014 was 27% of total taxable

employee earnings, in-line with the average statutory rate. Based on average wages in the

Tanzanian economy (US$1,525), the average nationwide statutory tax rate on individual income

is 4%. Acacia also withheld and remitted US$9 million in withholding taxes on behalf of its

suppliers.

Figure 7 Distribution of Acacia 2014 taxes paid or withheld

Millions of 2014 US dollars; total 2014 taxes paid or withheld by Acacia = $113 million

Note: Indirect taxes include anticipated unrecoverable VAT payments, import duties, fuel levies, environmental levies,

and other charges and fees. Payroll taxes paid by Acacia include employer social security contributions and skills and

development levy payments.

Source: Acacia data. Data provided by Acacia management were not independently audited by EY.

$9mm

$38mm

$8mm

$16mm

$41mm

Supplier spending withholding tax

Payroll taxes

Indirect tax

Payroll taxes paid by Acacia

Corporate income tax & royalties

Taxes paid by Acacia

Taxes withheld on behalf of employees

Tax collected and remitted by Acacia

Acacia Mining’s total economic and tax contributions in Tanzania, 2014

EY | 13

4. Acacia’s indirect and induced economic and tax contributions, 2014

Acacia’s contributions to the Tanzanian economy extend beyond the mine gates. As described

in Section 3, Acacia generates indirect and induced economic activity through its purchases

from Tanzanian suppliers and the local consumer spending of their employees. Further, this

activity results in additional taxable sales and income. Highlights of the total economic

contributions include:

► For every direct employee at Acacia’s mines and administrative offices in Tanzania, there

were approximately 11 paid employees and 5 self-employed individuals supported in the

broader economy. On average, these workers earned US$5,970 of labour income in 2014,

compared to an economy-wide average of US$1,525 (in 2014 US dollar terms) as reported

in the 2006 labour force survey.17

► Approximately 71% of the US$688 million of purchases of services and supplies made by

Acacia’s Tanzanian entities were from domestic suppliers.

► Approximately 92% of Acacia’s US$688 million of total procurement expenditures in 2014—

over US$633 million—were of a recurring nature, including operating input purchases and

sustaining capital investments. The remaining 8% was for investment in mine expansion and

development.

► Economic activity related to Acacia’s operations in Tanzania generated a total of nearly

US$179 million of tax payments by businesses and individuals.

4.1 Acacia’s direct, indirect, and induced economic contributions

In 2014, Acacia’s total economic contribution, including supplier and consumer spending

impacts, was an estimated US$678 million of GDP, of which US$460 million was labour income

(income earned by wage employees and proprietors), as shown in Table 3. Through supplier

purchases, Acacia’s activities generated US$290 million of indirect GDP, including US$180

million of labour income for an estimated 35,300 wage and self-employed workers in Tanzania.

Consumer spending by Acacia and supplier employees at local retailers, grocers, and other

businesses supported an estimated additional 37,200 wage employees and sole proprietors,

earning a total of US$138 million in labour income (averaging approximately US$3,700 per

worker; 6.1 million TSH).

The analysis presents employment impacts separately for wage employment and full

employment, which includes wage and self-employed workers. Depending on the types of

businesses from which suppliers and individuals purchase goods and services, the number of

jobs in each category may differ. For example, domestic purchases from large multinational

firms create wage employment opportunities in Tanzania, compared to additional demand for

local personal services, which are more likely to create opportunities for entrepreneurs.

Table 3 Acacia’s total economic contributions in Tanzania, 2014 Millions of 2014 US dollars; number of employees

Acacia Mining’s total economic and tax contributions in Tanzania, 2014

EY | 14

Direct contribution

Indirect contribution

(supplier spending)

Induced contribution

(employee spending)

Total contribution

Wage employment 4,443 30,500 19,000 53,943

Labour income $141 $180 $138 $459

Value added (GDP) $190 $290 $198 $678

Addendum: Full employment (Wage employment & proprietors) 4,443 35,300 37,200 76,943

Note: Direct employee headcount does not include contractors. Contractors are included as indirect contributions. Full employment includes wage employees and proprietors (self-employed individuals). Figures may not sum due to rounding. Source: EY analysis based on Acacia data. Data provided by Acacia management were not independently audited by EY.

In their economic benefits report, MEM states that mines have “significant potential to act as a

catalyst for local business development due to the demand it generates for goods and

services.”18 Acacia makes significant purchases of goods and services to support its annual

operations, much of which is from Tanzanian businesses. As shown in Figure 8, Acacia’s

Tanzanian entities purchased US$488 million of goods and services from within Tanzania

related to its operations, accounting for 71% of total input purchases. Of this amount, US$99

million was provided by suppliers that are located near the purchasing mine or in the closest

regional/major town. The remaining US$389 million was purchased from businesses operating

within Tanzania, but outside of the immediate impact area or closest regional/major town

surrounding the mine. Further, according to data provided by Acacia, 47% ($230 million) of the

US$488 million of Tanzanian purchases were purchased from Tanzanian-owned businesses.

Domestic purchases of goods and services generated rounds of supplier purchases, which

resulted in an estimated US$290 million of indirect GDP in Tanzania.

Acacia’s Tanzanian capital investments in 2014 are included in Acacia’s total Tanzania

procurement of US$488 million, shown in Figure 8. During 2014, Acacia invested nearly

US$194 million to develop new sites or expand existing projects. These expenditures included

capitalized exploration and evaluation costs and mine site development and expansion. Major

expansion projects create a one-time catalyst for the economy, creating temporary but important

jobs at the mine development site.

Acacia Mining’s total economic and tax contributions in Tanzania, 2014

EY | 15

Figure 8 Location of Acacia’s suppliers for operating inputs and capital expenditures,

2014

Total 2014 supplier purchases = US$688 million

Note: The immediate impact area, as defined by Acacia, includes the surrounding communities as well as the nearest regional or major town. Businesses within the immediate impact area are shown as “Same region as mine” purchases. Purchases from suppliers outside of the immediate impact area are shown as “Other TZ regions”. Source: Acacia data. Acacia data were not independently audited by EY.

The types of goods and services that Acacia’s Tanzanian entities purchases from Tanzanian

businesses create different impacts in the economy. The level of indirect impact primarily

depends on two factors: (1) the amount of goods or services that are purchased domestically

and (2) the average levels of output per worker for each industry. The total level of output per

worker in each industry reflects the dependence on labour for production. For example, the

mining sector is capital intensive and has a very high output per worker, compared to the

national average for all industries. Alternatively, most service sectors have low output per

worker because they rely on labour to produce their product and generate revenue. The

composition of purchases made by Acacia’s Tanzanian entities in 2014 is displayed in Figure 9,

classified by activity or product of the supplier. Purchases of machinery and equipment from

Tanzanian wholesalers are classified within the service sector as trade. Machinery and

equipment manufactured in Tanzania would be classified within the industrial sector.

Other TZ regions, $389mm

Same region as mine, $99mm

Tanzania, $488mm

South Africa, $51mm

International, $136mm

Rest of Africa $13mm

Acacia Mining’s total economic and tax contributions in Tanzania, 2014

EY | 16

Figure 9 Distribution of purchases of Tanzania-supplied goods and services by Acacia’s

Tanzanian entities, by sector, 2014

Total 2014 purchases from Tanzanian suppliers by Acacia’s Tanzanian entities = US$488million

Note: The industrial sector includes mining, manufacturing, utilities, and construction. The service sector includes trade, transportation, and communication; financial services; business and professional services; health, educations, and public administration; and other services. Source: EY analysis of data provided by Acacia. Acacia data were not independently audited by EY.

Figure 10 shows the distribution of the estimated direct, indirect, and induced wage employment

impacts by major industry sector. The majority of the indirect wage employment is within the

trade and transportation, financial services, and other services sectors. In 2014, approximately

8% of Acacia’s total purchases were for sustaining capital at Acacia’s mines and Tanzanian

offices. This investment includes replacement equipment, capitalized improvements to buildings

and facilities, and other sustaining capital. Domestic purchases of equipment are frequently

through a Tanzanian wholesaler selling equipment that was manufactured elsewhere and

imported into Tanzania. This activity generates employment in the wholesale trade industry,

classified as trade and transportation.

Acacia’s Tanzanian entities are supported by a significant number of mining, engineering,

security, and construction contractors who work on-site at Acacia mines and facilities. Contract

employment is classified as a purchased service and is included in the indirect wage

employment impact. In 2014, Acacia reported US$92 million in contractor spending related to

the 3,517 contractors working on-site at Acacia’s mines, of which 3,320 (94%) were Tanzanian

nationals.

Induced consumption-related employee spending reflects the household purchasing distribution

in Tanzania. The largest share of induced wage employment is in the agricultural sector.

According to the GTAP model, agriculture products make up nearly 62% of the total domestic

Agriculture, 2%

Industrial, 43% Service, 55%

Total

$488mm

Acacia Mining’s total economic and tax contributions in Tanzania, 2014

EY | 17

goods and services purchased by households. Induced jobs are also supported in the trade

sector (through spending at retail stores) and other services (which includes personal services,

entertainment, restaurants, and hotels), as well as for financial services, manufacturing, and

healthcare and education.

Figure 10 Distribution of estimated direct, indirect and induced wage employment, 2014

Note: The figure does not include the estimated number of proprietors in each industry. “Other services” includes

personal services, recreation and entertainment, and hospitality and food service. “Trade & transport” includes retail

and wholesale trade, transportation services, and communications services.

Source: EY analysis based on Acacia data. Data provided by Acacia management were not independently audited by

EY.

The estimated wage employment multiplier of 12 can be interpreted as, for each direct Acacia

employee, 11 wage employees are supported through indirect and induced economic activity,

totaling 12 employees overall. Including proprietors, the employment multiplier increases to 17

(i.e. for every one direct Acacia employee, there are an estimated 16 additional wage and self-

employed positions supported in the broader Tanzanian economy).

Figure 11 compares the estimated employment impacts for wage employment and full

employment, including proprietors. The majority of the indirect impact related to supplier

purchases is comprised of direct wage employees. The analysis assumes that the companies

that Acacia directly purchases goods and services from in Tanzania are not sole

proprietorships. However, the additional rounds of supplier purchases (Acacia’s direct suppliers

purchasing from other Tanzanian businesses) add an estimated 4,800 proprietors.

Self-employed labour accounts for 18,200 jobs out of the induced employment impact of 37,200

jobs. As employees spend their incomes in the local economy, it is likely that they purchase

-

2,000

4,000

6,000

8,000

10,000

12,000

Induced employment

Indirect employment

Direct employment, Acacia

Acacia Mining’s total economic and tax contributions in Tanzania, 2014

EY | 18

food and personal services from individuals who own their own businesses such as restaurants,

convenience stores, personal service businesses, and construction contractors.

Figure 11 Comparison of estimated employment impacts, 2014

Note: Full employment includes wage employees and proprietors (self-employed persons, excluding subsistence farmers). Source: EY analysis based on data provided by Acacia. Data provided by Acacia management were not independently audited by EY.

4.2 Acacia’s direct, indirect, and induced tax contributions

In 2014, Acacia paid US$65 million in Tanzanian taxes and royalties. In addition to paying an

estimated US$38 million in individual income taxes and social security contributions, Acacia’s

employees paid approximately US$15 million in other taxes and fees, including VAT and excise

taxes on their purchases. Taxes paid by Acacia and Acacia’s employees collectively make up

Acacia’s direct tax impact, totaling US$118 million in 2014.

Suppliers and businesses that sell to Acacia and supplier employees also pay taxes on their

sales and incomes related to the increased demand for their goods and services. Businesses

and individuals paid an estimated US$61 million in taxes related to indirect and induced

economic activity.

In Tanzania, tax payments were approximately 16% of total labor income (wages and benefits)

in 2014. In that year, VAT, customs duties, and excise taxes paid by businesses and individuals

totaled 6% of total labor income.19 Payroll taxes include social security and skills and

development levy payments. In 2014, these taxes totaled an estimated 1% of labor income.

4,443

30,500

19,000

53,943

35,300 37,200

76,943

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

Direct Indirect Induced Total

Wage employment

Full employment

Acacia Mining’s total economic and tax contributions in Tanzania, 2014

EY | 19

Table 4 Acacia’s total tax contribution, 2014

Millions of 2014 US dollars

Direct Tax

Paid by Acacia

Paid by Acacia

employees Indirect &

induced tax Total tax

Corporate income tax & royalties $41.3 $ -- $6.2 $47.5

Individual income tax -- 25.4 9.6 35.0

Value-added tax (VAT) 0.9 6.1 13.7 20.7

Customs & excise 5.6 7.3 16.6 29.6

Payroll taxes 15.8 12.5 2.0 30.3 Technical services withholding tax and other taxes & fees

1.6 1.4 12.5 15.5

Total taxes $65.3 $52.7 $60.7 $178.6

Note: The direct VAT paid by Acacia reported above is the estimated VAT paid on input purchases that will be unrecovered by Acacia through refunds. Payroll taxes include social security contributions and the skills & development levy. Technical services withholding taxes collected and remitted by Acacia are not included in the direct tax impacts. These taxes are included in the indirect tax impact, as the liability of the suppliers. “Other taxes and fees” include capital gains taxes, as well as business license fees, motor vehicle license, and other similar taxes and fees. Figures may not sum due to rounding. Source: EY analysis based on Acacia data. Data provided by Acacia management were not independently audited by EY.

Overall, tax payments by Acacia’s Tanzanian entities comprised 37% of the total estimated tax

impact, shown in Figure 12. Of the total, 23% were corporate income tax and royalty payments

paid by Acacia. Estimated unrecoverable VAT and customs and excise duties paid by Acacia

comprised a combined 4% of the total tax impact of $179 million. Other taxes paid by Acacia

included payroll taxes, fuel levies and taxes paid to local governments, totaling 10% of

estimated taxes overall.

In order to properly quantify the contribution of Acacia’s VAT payments to the Tanzanian

economy, this analysis assumes that Acacia’s direct VAT contribution consists only of those

VAT payments not recovered through refunds. Acacia estimates that VAT claims of nearly

$930,000 will be disallowed. This amount has increased since 2013, when unrecovered VAT

totaled nearly $620,000.

Acacia Mining’s total economic and tax contributions in Tanzania, 2014

EY | 20

Figure 12 Composition of Acacia’s total tax contribution from operations, 2014

Total 2014 tax impact = US$179 million

Note: Percentages shown are percentages of the total estimated tax impact of US$179 million. Figures may not appear to sum due to rounding. Source: EY analysis based on Acacia data and data published in Tanzania’s national accounts. Data provided by Acacia management were not independently audited by EY.

The US$61 million of taxes related to indirect and induced economic activity accounted for 34%

of the total tax impact. The US$9 million of tax withheld by Acacia on behalf of suppliers is

included as an indirect tax impact. Other indirect and induced tax impacts were estimated using

the ratios of Tanzania-wide tax collections to Tanzania personal income. Customs and excise

taxes made up the largest share of indirect and induced tax impacts at 27%. VAT comprised

23% of the total. Other indirect and induced taxes include taxes and fees such as business and

motor vehicle license fees, employer payroll taxes (including social security and the skills

development levy), and capital gains taxes.

Corporate income tax &

royalties 23%

Customs & VAT 4%

Other taxes 10%

Paid by Acacia employees

29%

Indirect and induced tax

34%

Acacia taxes 37%

Acacia Mining’s total economic and tax contributions in Tanzania, 2014

EY | 21

5. Acacia’s social investments, 2014

Beyond economic contributions, Acacia made substantial social investments that can have long-

lasting health, education, and infrastructure benefits in Tanzania. In 2014, Acacia invested a

total of US$10.9 million in its Tanzania corporate responsibility program with US$8.5 million

being spent on the Maendeleo Fund and US$2.4 million on wider community relations and mine

site community, as summarized in Table 5. Of the US$8.5 million Maendeleo Fund spending,

US$2.6 million (31%) was invested in infrastructure, US$2.5 million (30%) went towards

education programs, and US$1.3 million (15%) was used to improve water & sanitation access.

Beyond the Maendeleo Fund, Acacia invested an additional US$2.4 million in social programs,

for a total of US$10.9 million in social investment spending in 2014.

Table 5 Summary of Acacia’s 2014 social contributions in Tanzania

Thousands of 2014 US dollars

North Mara Buzwagi Tulawaka Bulyanhulu Corporate Discovery Total

Maendelo Fund spending

Donations $164 $3 $0 $0 $0 $137 $304 Education $1,857 $154 $57 $317 $127 - $2,513 Infrastructure $482 $2,066 $0 $0 $0 $35 $2,584 Water & Sanitation $730 $0 $39 $276 $0 $212 $1,257 Health $366 $0 $0 $0 $0 $403 $769 Livelihood support $632 $50 $18 - $27 - $726 Other $283 $0 - - $34 - $317

Total Maendeleo Fund spending $4,514 $2,273 $114 $592 $188 $787 $8,469 CSR site operation costs

- - - - - - $2,389

Total community investment $4,514 $2,273 $114 $592 $188 $787 $10,858

Note: Figures may not appear to sum due to rounding. “CSR site operation costs” include spending on Village Benefit

Implementation Agreements (VBIAs).

Source: EY analysis based on data provided by Acacia Data provided by Acacia management were not independently audited by EY.

This social investment spending is included in Acacia’s $488 million of supplier spending in

Tanzania and is captured in the resulting indirect and induced contributions. However, the long-

term impact of these investments resulting from, for example, access to medical facilities and

potable water are not estimated in this study.

Acacia’s Maendeleo Fund supports a wide variety of projects in Tanzania with a primary focus

being the communities that live around the Acacia mines and exploration sites. Some of these

projects have short-term, one time impacts. The fund was established in 2011 as part of

commitment to promoting sustainable development in Tanzania. Funding priority is given to

investments that support community development and capacity building, access to health,

education, water and environmental projects within communities surrounding our operations.

Acacia Mining’s total economic and tax contributions in Tanzania, 2014

EY | 22

Since its inception, the Acacia Maendeleo Fund has invested US$27.4 million in community

development initiatives across a range of areas including education, health, water and

Sanitation, infrastructure, and livelihoods. The following sections describe three of the largest

Maendeleo Fund projects in more detail.

Infrastructure: Infrastructure social investments were the largest single area of Maendeleo

Fund spending in Tanzania in 2014, at nearly US$2.6million.

During 2014, Acacia supported road maintenance in 6 villages in North Mara. In the Buzwagi

area, Acacia also carried out a Kahama roads project and invested in a community alternative

road project.

Education: Education social investments were the second largest single area of Maendeleo

Fund spending in Tanzania in 2014, at nearly US$2.5 million.

During 2014, Acacia supported infrastructure upgrades in schools within Bulyanhulu, North

Mara, Buzwagi and Tulawaka. This included construction and renovations of dormitories,

classrooms, laboratories, teacher houses and libraries. Acacia also participated regionally and

nationally in the CAN EDUCATE program and supported scholarships and sponsorships in

North Mara.

Water: Ensuring clean, safe water, quality, and access has been another area of emphasis in

Acacia’s social investment spending in Tanzania. Access to potable water is particularly

challenging in rural Tanzanian communities.

Acacia is focused on ensuring that communities around its mine sites have access to clean

water and safe drinking water. One example of Acacia’s work in this area is the Community pipe

water supply project and water boreholes program.

The impacts of social investments are difficult to quantify. While the direct contributions of

spending on water infrastructure—payments to construction workers and materials suppliers, for

instance—have estimable impacts that are reflected in the economic impact estimates, there

are also a variety of positive externalities created by Acacia’s social investment spending. The

improved education that a Tanzanian child receives may not be reflected in the Tanzanian

economy for many years. Likewise, it is difficult to determine the number of Tanzanians who can

now make homes in areas of Mara that have newfound access to fresh water. Acacia’s social

investment spending and other metrics provide the best indicators of benefits in the short term.

Quantifying the impact of social investments requires follow-up studies and the collection of

social baselines. This analysis does not attempt to quantify the socioeconomic and health

outcomes of Acacia’s social investments.

Acacia Mining’s total economic and tax contributions in Tanzania, 2014

EY | 23

6. Study limitations

Readers should be aware of several limitations of this analysis.

► Assumptions underlying key multiplier model inputs. The direct economic and tax

contributions reflect 2014 client data. Two key inputs to the multiplier analysis have been

held constant from the analysis of Acacia’s 2012 economic and tax contributions in

Tanzania: 1) economic input-output data for Tanzania and 2) Acacia’s industry distribution of

supplier purchases. Changes to the ratio of taxes paid to personal income would cause

proportionate changes in the estimates of taxes paid by Acacia employees, indirect taxes,

and induced taxes.

The 2012 aggregate supplier spending information provided by Acacia was, in some cases,

disaggregated into purchases from specific industries using the industry average

composition of mining industry inputs from the GTAP model. The distribution of input

purchases and import percentages by industry used in this analysis were based on 2012

information provided by Acacia and industry averages for the mining sector in the GTAP

model. Significant changes to Acacia’s distribution of supplier purchases would result in a

different industry distribution of indirect and induced employment, labor income, and value

added (GDP), depending on the labour- or capital-intensity of the supplier industry.

► Tanzania input-output model. This analysis relies on GTAP's 2007 SAM of the Tanzanian

economy, which is a product of the broader “Africa 2” database that models economies and

international trade flows in Africa and the rest of the world. The documentation underlying

GTAP economic modeling and the variety of studies based on GTAP information—including

the NGGL Ghana gold mining study that is comparable in scope and subject matter to this

analysis—suggest that the 2007 Tanzania data provide a strong foundation for this analysis.

Certain elements of the GTAP 2007 matrix are based on the Tanzanian 1992 input-output

table (the most recent comprehensive input-output matrix that was constructed from survey

data and published by the Tanzania NBS). This matrix has been extrapolated to 2007 using

2007 national accounts data.

► Supplier purchases from foreign-owned businesses operating in Tanzania. Acacia’s

supplier purchases in Tanzania include purchases from foreign businesses operating in

Tanzania. If these suppliers are simply domestic wholesalers of equipment that was

manufactured abroad, the indirect impact would be overstated for those suppliers because

the manufacturing activity did not occur in Tanzania.

► Classification of Acacia’s on-site contractors. Based on information provided by Acacia,

contractors working on-site for Tanzanian entities are mostly employed by separate supplier

firms, in roles not generally filled by direct Acacia employees. Because these workers are

employees of a service firm and not employed by Acacia as individuals working as

independent contractors, Acacia’s expenditures on service contracts are classified as non-

labour input purchases and not employee costs. As a result, the contractor employees are

captured within the indirect job estimate. The multiplier model is sensitive to the transfer of

Acacia Mining’s total economic and tax contributions in Tanzania, 2014

EY | 24

jobs between Acacia employees and contracted workers. Replacing Acacia employees with

contractors to complete the same work would increase the economic multipliers, shifting

jobs from direct to indirect, while reducing reliance on contractors would decrease the

economic multipliers (shifting jobs from indirect to direct). However, the total contribution

levels would be the same under either scenario.

► Formal versus informal economic sector activity. Employment data in Tanzania reflects

several types of employment, including formal wage and salary employees, self-employed

proprietors, unpaid family helpers, and subsistence farmers (or “traditional agriculture”). The

estimated employment multipliers are sensitive to the definition of employment. The primary

employment results presented in this analysis reflect only wage and salary employment but

if other types of employment are considered, the estimated employment impacts are larger

than those shown in this analysis.

► Residency assumption. The estimated induced contributions and tax impacts assume that

all employees of Acacia’s Tanzania operations live in Tanzania. This assumption means that

all labour income is saved or spent within the country (accounting for imports), and is fully

taxable within Tanzania.

Acacia Mining’s total economic and tax contributions in Tanzania, 2014

EY | 25

7. Conclusion

This report analyzes the total economic and tax contributions of Acacia’s operations and

investment activities in Tanzania during 2014. The report provides a snapshot of the economic

activity created by Acacia in terms of GDP, labour income, and employment. Because of the

size of Acacia’s Tanzanian operations and the importance of the mining sector to Tanzania’s

economy, the estimated contributions are substantial, with estimated total direct, indirect and

induced GDP equivalent to approximately 2% of Tanzania’s overall GDP in 2014.

This report finds that Acacia’s total economic contribution included nearly US$680 million of

GDP, of which approximately US$460 million was labour income earned by nearly 77,000 wage

employees and self-employed individuals. If Acacia’s Tanzanian entities continue to operate at

2014 levels in Tanzania, much of this economic activity would be anticipated to occur annually,

as recurring operating input purchases and capital investment spending comprised 92% of

Acacia’s total procurement spending during 2014.

During 2014, Acacia’s Tanzanian entities paid a total of US$65 million in Tanzanian taxes, with

Acacia employees paying an additional US$53 million on their incomes, purchases, and

property. Indirect and induced economic activity from Acacia’s operations resulted in an

estimated US$61 million in taxes. Acacia’s total government revenue contribution per employee

in 2014 was 20 times higher than the national average. Per employee, Acacia paid nearly

US$14,700 of direct taxes and royalties, compared to approximately US$700 per worker

economy-wide.

In 2014, Acacia’s social investments in Tanzania through its Maendeleo Fund totaled US$8.5

million, supporting a variety of education, infrastructure and water and sanitation initiatives,

primarily in the communities surrounding Acacia’s mines and throughout the Lake Zone of

Tanzania. The Maendeleo Fund concentrates on community development through the

construction of medical facilities, increased access to potable water, improved schools, and

other infrastructure and programming initiatives. Beyond its Maendeleo Fund spending, Acacia

made additional social investments of US$2.4 million, bringing its total social investment

spending in Tanzania in 2014 to US$10.9 million. This spending provides both one-time and

long-term benefits to the residents of these communities.

Acacia Mining’s total economic and tax contributions in Tanzania, 2014

EY | 26

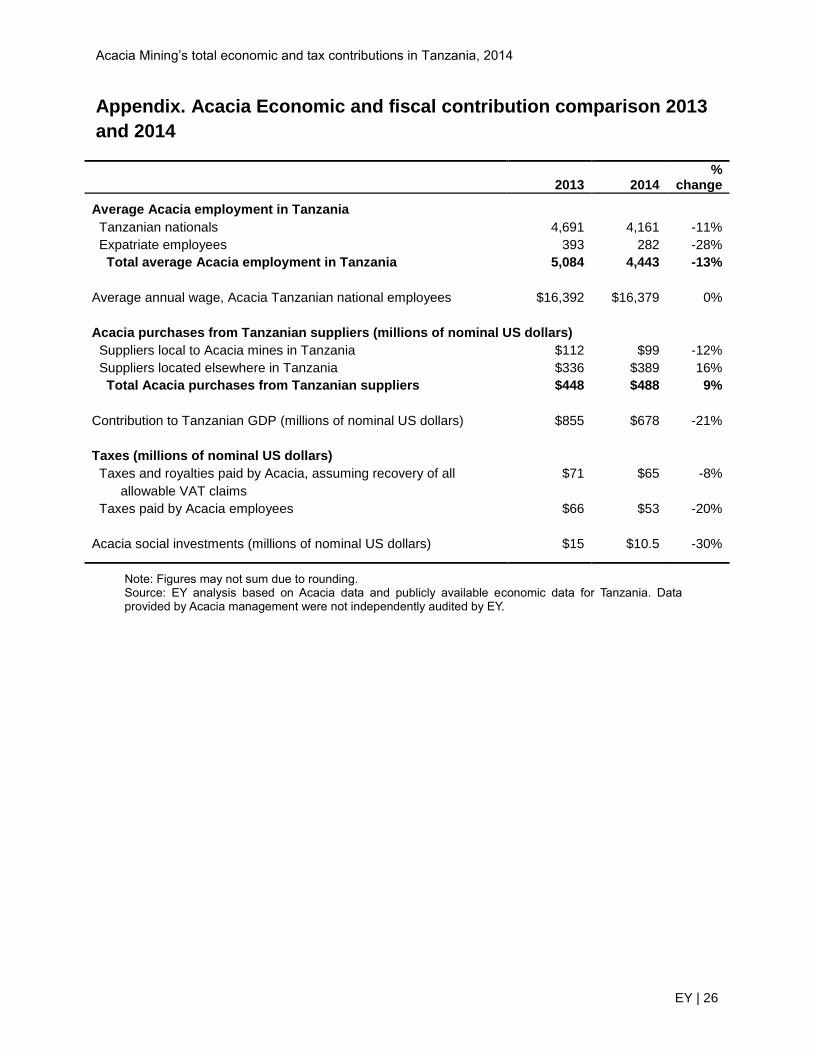

Appendix. Acacia Economic and fiscal contribution comparison 2013

and 2014

Note: Figures may not sum due to rounding. Source: EY analysis based on Acacia data and publicly available economic data for Tanzania. Data provided by Acacia management were not independently audited by EY.

2013 2014

% change

Average Acacia employment in Tanzania

Tanzanian nationals 4,691 4,161 -11%

Expatriate employees 393 282 -28%

Total average Acacia employment in Tanzania 5,084 4,443 -13%

Average annual wage, Acacia Tanzanian national employees $16,392 $16,379 0%

Acacia purchases from Tanzanian suppliers (millions of nominal US dollars)

Suppliers local to Acacia mines in Tanzania $112 $99 -12%

Suppliers located elsewhere in Tanzania $336 $389 16%

Total Acacia purchases from Tanzanian suppliers $448 $488 9%

Contribution to Tanzanian GDP (millions of nominal US dollars) $855 $678 -21%

Taxes (millions of nominal US dollars)

Taxes and royalties paid by Acacia, assuming recovery of all

allowable VAT claims

$71 $65 -8%

Taxes paid by Acacia employees $66 $53 -20%

Acacia social investments (millions of nominal US dollars) $15 $10.5 -30%

Acacia Mining’s total economic and tax contributions in Tanzania, 2014

EY | 27

References

“A Golden Opportunity?: How Tanzania is Failing to Benefit from Gold Mining.” Curtis, Mark and Tandu

Lissu. Commissioned by Christian Council of Tanzania (CCT), et al. 2009.“GTAP Data Bases: GTAP

Africa 2 Data Base.” May 31, 2013. https://www.gtap.agecon.purdue.edu/

databases/Africa/v2/default.asp.

Kapstein, Ethan and Rene Kim. "The Socioeconomic impact of Newmont Ghana Gold Limited."

Sponsored by Newmont Ghana Gold Limited. Prepared by Steward Redqueen. June 2011.

http://www.newmont.com/sites/default/files/Socio_Economic_Impact_of_Newmont_Ghana_Gold_July

_2011_0.pdf?bcsi_scan_7f73a9d1b05f4e20=jOfagWWqRO82y98WXEQ8QrxWvHckAAAAvfVLhQ==&

bcsi_scan_filename=Socio_Economic_Impact_of_Newmont_Ghana_Gold_July_2011_0.pdf.

“Tanzania Investment Benefits Study.” United Republic of Tanzania Ministry of Energy and Minerals.

Prepared by Oxford Policy Management. September 2011.

http://www.opml.co.uk/sites/opml/files/Investment%20Benefits%20Report%20for%20MEM.pdf.

Thurlow, James and Peter Wobst. “Poverty-Focused Social Accounting Matrices for Tanzania.”

International Food Policy Research Institute. March 2003.

http://www.ifpri.org/sites/default/files/publications/tmdp30.pdf.

Wobst, Peter. “A 1992 Social Accounting Matrix (SAM) for Tanzania.” International Food Policy Research

Institute. August 1998. http://www.ifpri.org/sites/default/files/publications/tmdp30.pdf.

“World Development Indicators.” The World Bank. 2013. http://data.worldbank.org/.

Acacia Mining’s total economic and tax contributions in Tanzania, 2014

EY | 28

Endnotes

1 Further to the approval of shareholders at its General Meeting held on 26 November 2014, African Barrick Gold plc

changed its name to Acacia Mining plc (LSE: ACA) with immediate effect. Trading in shares under the new name Acacia Mining plc started at the commencement of trading on 27 November 2014. The Company's International Securities Identification Number remains unchanged. 2 In this study, all employment figures are reported as total headcount, not as full-time equivalents (FTEs).

3 Tanzania Minerals Audit Agency

4 2014 Tanzania GDP data by industry are not yet available.

5 Tulawaka is owned as part of a joint venture with MDN Inc. in which Acacia has a 70% stake.

6 “Tanzania Economic Condition” National Bureau of Statistics Tanzania see p.12

7 “Tanzania Economic Condition” , National Bureau of Statistics Tanzania see p.197

8 Thurlow, James and Peter Wobst. “Poverty-Focused Social Accounting Matrices for Tanzania.” International Food

Policy Research Institute. March 2003. See p.i. 9 Kapstein, Ethan and Rene Kim. "The Socioeconomic impact of Newmont Ghana Gold Limited." Sponsored by

Newmont Ghana Gold Limited. Prepared by Steward Redqueen. June 2011. See p.31-32. 10

Kapstein, Ethan and Rene Kim. "The Socioeconomic impact of Newmont Ghana Gold Limited." Sponsored by Newmont Ghana Gold Limited. Prepared by Steward Redqueen. June 2011. See p.31-32. 11

The average wage of $16,400 for Tanzanians employed by Acacia in 2013 is includes take-home pay as well as payroll and income taxes paid by the employee (i.e. gross wages). For economy-wide Tanzania wage information, see p.82 of “2006 Integrated Labour Force Survey.” Tanzania National Bureau of Statistics. 12

“Employment and earnings survey: Analytical Report 2007.” Tanzania National Bureau of Statistics. November 2012. See p.1-2. 13

See: “Tanzania Investment Benefits Study.” United Republic of Tanzania Ministry of Energy and Minerals. Prepared by Oxford Policy Management. September 2011 and “A Golden Opportunity?: How Tanzania is Failing to Benefit from Gold Mining.” Curtis, Mark and Tandu Lissu. Commissioned by Christian Council of Tanzania (CCT), et al. 2009. 14

Acacia invested $4,438,000 in education initiatives in 2013. See Table 5. 15

See “Tanzania Investment Benefits Study”, p.54. 16

Employment data provided by Acacia 17

“2006 Integrated Labour Force Survey.” Tanzania National Bureau of Statistics. See p.82. Value is inflated to nominal 2014 terms using the Tanzania inflation rate. 18

See “Tanzania Investment Benefits Study”, p.59. 19

EY analysis based on Tanzania Revenue Authority data.