academy academy 3 current assets 2,150,000 450,000 less: current liabilities600,000 450,000bank...

TRANSCRIPT

PRIME A

CADEMY

1

The Society of Auditors and Prime Academy

Final Model exam- September 2016

Financial Reporting- Paper 1

Question No 1 is Compulsory answer any five of the remaining questions

Working notes should form part of the respective answers

Wherever necessary candidates can make assumptions and disclose the same by

way of a note

(4 x 5 M = 20 M)

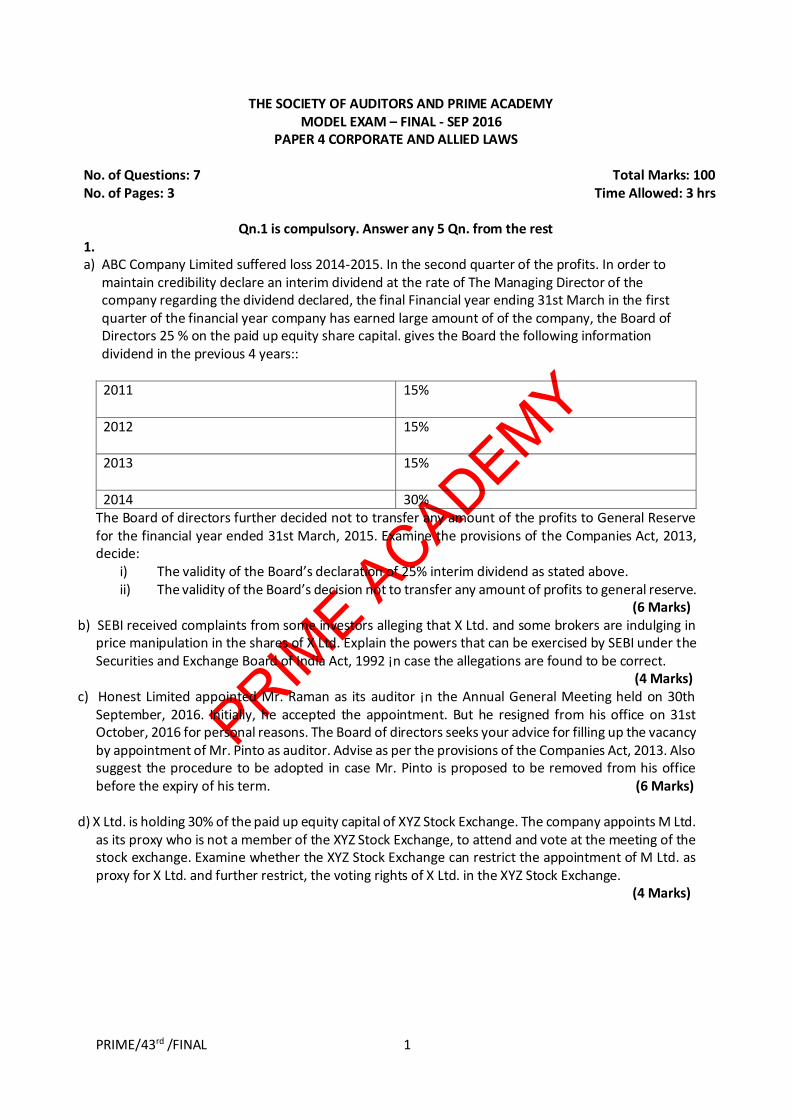

1(a) Z Limited ordered 13,000 kg. of chemicals at ` 90 per kg. The purchase price includes

excise duty of `5 per kg. in respect of which full CENVAT credit is admissible. Further, state

VAT is leviable at ` 2.5 per kg on purchase price. Freight incurred amounted to ` 30,000.

Normal transit loss is 4%. The company actually received 12,400 kg and consumed 10,000 kg.

of chemicals. The company has received trade discount later on in the form of their credit

note of Re. 1 per kg. The chemicals were delivered in containers. The containers were not

reusable, hence sold for Rs. 500. The administrative expenses incurred to bring the

chemicals were Rs. 10,000. Compute the value of inventory and allocate the material cost as

per AS 2.

1(b) Huge Ltd. acquired at the start of the financial year a fixed asset from USA at a price of

US $ 1,25,000 and made a down payment of US $ 25,000. The exchange rate was Rs. 61.50

per dollar at the date of transaction.The balance amount was payable in 4 equal half yearly

instalments with interest @ 8% per annum. The exchange rates on due dates of instalment

have been Rs. 61.60; Rs. 61.80; Rs. 61.90; and Rs. 62.10. The asset was under

construction during the period of six months from its acquisition. Ascertain the amount to

be capitalized and the gain or loss to be recognized in each of the years.

1(c) Dynamic Ltd. invested in the shares of another company on 31st

October, 2015 at

a cost of Rs. 4,50,000. It also earlier purchased Gold of Rs. 5,00,000 and Silver of

Rs. 2,25,000 on 31st March, 2013. Market values as on 31st March, 2016 of the above

investments are as follows: Shares Rs.3,75,000; Gold Rs.7,50,000 and Silver Rs.4,35,000.

How will the above investments be shown in the books of account of Dynamic Ltd. for the

year ending 31st March, 2016 as per the provision of AS13?

1(d) On 1st January, 2015, Sahara Ltd. Sold equipment for Rs.6,14,460. The carrying

amount of the equipment on that date was Rs. 1,00,000.The sale was a part of the package

under which Help Ltd. leased the asset to Sahara Ltd. for ten years term.

The economic life of the asset is estimated as 10 years. The minimum lease rents payable by

the lessee has been fixed at Rs. 1,00,000 payable annually beginning from 31st

PRIME A

CADEMY

2

December, 2015. The incremental borrowing interest rate of Sahara Ltd. is estimated at

10% p.a. Calculate the net effect on the Statement of Profit and Loss in the books of Sahara

Ltd.

2 . M Ltd. Acquired 12,000 shares in D Ltd. For rs. 1,70,000 on July 1,1988. The balance sheets

of the two companies on 31st March 1989 were as follows:( 16 Marks )

M Ltd D Ltd

M Ltd D Ltd

Liabilities Rs. Rs. Assets Rs. Rs.

Share Capital :

Goodwill 300,000 70,000

(share of Rs. 10 each) 1,000,000 300,000 Land and Buildings 400,000 100,000

General Reserve 420,000 50,000 Plant and machinery 500,000 100,000

Profit and loss account 260,000 85,000 Investments 170,000 -

Loan from D Ltd (incl.

interest)

57,500 -

Stock

200,000 40,000

Bills Payable 80,000 60,000 Book Debts 300,000 85,000

Creditors 182,500 42,000 Cash And Bank

Balances

80,000 62,000

Bills receivable 50,000 30,000

Loan to M Ltd - 50,000

20,00,000 5,37,000

20,00,000 5,37,000

On April 1, 1988, the Profit and loss account of D ltd stood at Rs. 40,000 out of which a dividend

of 15% for the year 1987-88 on the then capital of Rs. 2,00,000 was paid in September 1988. At

the same time, a bonus issue of one share (fully paid) for every two shares held, was also made

out of General Reserve. Bills Payable of D Ltd, represent bills issued in favour of M Ltd. Which

company still held Rs. 40,000 of the bills accepted by D ltd. The entire closing stock of D Ltd.

Represents goods supplied by M Ltd. At cost plus 20%.M Ltd. and D Ltd. agreed that, with

effect from July 1,1988, for services rendered M ltd. should charge Rs.500 p.m. from D Ltd.

Entries for this were not made when the accounts were drawn up. The loan to M Ltd. was made

by D ltd. on April 1, 1988.

Prepare the consolidated balance sheet of the two companies as at 31st March 1989.

3. As on 31st March,1989, 1/3 of the capital of Zed ltd. had been lost,not counting Goodwill. On

that date, the position was as follows: (16 Marks )

Rs. Rs.

Goodwill

200,000

Other Fixed Assets: Cost 2,000,000

Less: Depreciation 500,000 1,500,000

PRIME A

CADEMY

3

Current Assets

450,000

2,150,000

Less: Current Liabilities 600,000

Bank Loan 450,000 1,050,000

1,100,000

There was a capital reserve totalling Rs. 1,00,000. The capital consisted of equity shares and

10% preference shares in the ratio of 3:2, both shares being of Rs.100 each, fully paid.

It was found that the fixed assets needed further depreciation to the extent of Rs.1,50,000 and

the current assets were worth Rs. 4,00,000. A scheme of reconstruction was framed and

received all requisite approvals and sanctions; the main features were the following:-

(a) The preference shares were to be converted into 14% redeemable preference shares,

four new shares being issued for five old shares and 1/5 of the arrears of dividend which

was last paid for the year ending 31st March, 1985 was to be paid in cash.

(b) Equity shares were to be reduced to Rs. 10 each, fully paid.

(c) For every two equity shares held, each equity shareholder was to subscribe for one

equity share of Rs.10 each, fully paid.

(d) Of the profit earned in future, atleast 50% would be retained by the company.

Pass Journal entries and draft the balance sheet of the company after the scheme is

implemented.

4(a) Comment in case of following two situations: ( 8 Marks )

Company A is a listed company and has three Subsidiaries Company X, Company Y

and Company Z. As on 31st March 2014, the net worth of Company A is Rs.

600 crore, net worth of Company X is Rs. 100 crore, Company Y is Rs. 400 crore and

Company Z is Rs. 210 crore. All the three subsidiaries are non-listed public

companies.

(i) During the financial year 2015-16, Company A has sold off its investment in

Company Y on 31st December, 2015. Therefore, Company Y is no longer a

subsidiary of Company A for the purposes of preparation of financial statements as

on 31 March 2016.Should Company Y prepare its financial statements as per the

Companies (Accounting Standards) Rules, 2006 or the Companies (Indian

Accounting Standards) Rules, 2015?

(ii) During the financial year 2016-17, Company A has sold off its investment in

Company Z on 31st December 2016, therefore company Z is no longer a subsidiary

of Company A for the purposes of preparation of financial statements as on 31st

March 2017.Should Company Z prepare its financial statements as per the

Companies (Accounting Standards) Rules, 2006 or the Companies (Indian

Accounting Standards) Rules, 2015?

PRIME A

CADEMY

4

4(b) Comment on the following two situations with respect to Schedule III of the

Companies Act 2013:

( 8 Marks )

(i) Y Ltd purchased goods on 24 months credit but the creditor has the call option that

can be exercised after 15 months. On the reporting date such trade payable was

outstanding for 4 months (i.e payable after 20 months from the reporting date) Is the

trade payable current or non-current?

(ii) Where should the balances with banks to the extent held as margin money or

security against the borrowings, guarantees, other commitments be disclosed?

5(a) The Capital structure of Define Ltd . is as under: ( 8 Marks )

80,00,000,Equity shares of Rs 10 each = Rs 800Lacs

1,00,000, 12% Preference shares of Rs 250 each = 250Lacs

1,00,000, 10% Debentures of Rs 500 each = 500Lacs

Term loans from Bank @ 10% = Rs 450Lacs

The company’s statement of Profit & Loss for the year showed PAT of Rs 100lacs after

appropriating Equity dividend @ 20%. The company is in the 40% tax bracket. Treasury

bonds carry 6.5% interest and beta factor for the company may be taken as 1.5. The long

run market rate of return may be taken as 16.5%.Calculate Economic Value Added.

5(b) A Company announced a stock appreciation right on 01/04/2010 for each of its 525

employees. The scheme gives the employees the right to claim cash payment equivalent to

excess on market price of company’s shares on exercise date over the exercise price Rs 125 per

share in respect of 100 shares, subject to condition of continuous employment for 3 years. The

SAR is exercisable after 31/03/2013 but before 30/06/2013. The fair value of SAR was Rs 21 in

2010-11, Rs 23 in 2011-12, and Rs 24 in 2012-13. In 2010-11 the company estimates that 2% of

the employees shall leave the company annually. This was revised to 3% in 2011-12. Actually, 15

employees left the company in 2010-11, 10 in 2011-12 and 8 in left in 2012-13. The SAR

therefore actually vested to 492 employees. On 30/06/13, when the SAR was exercised, the

intrinsic value was Rs 25 per share . Show provision for SAR a/c by fair value method ( 8 Marks )

6(a) The capital structure of M/s XYZ Ltd on 31st March 2015 was as follows:

Rs. In Lacs

Equity share capital 18000 shares of Rs. 100 each 18

12% Preference capital 5000 shares of Rs. 100 each 5

12% secured Debentures 5

Reserves 5

PRIME A

CADEMY

5

PBIT during the year 7.2

Tax rate 40%

Generally the return on equity shares of this type of industry is 15%

Subject to:

(a) The profit after tax covers fixed interest and fixed dividends atleast four times.

(b) The Debt Equity ratio is atleast 2.

(c) Yield on shares is calculated at 60% of distributed profits and 10% of undistributed

profits.

The company has been paying regularly an equity dividend of 15%. The risk premium for

dividends is generally assumed at 1% and find out the value of equity dividends of the company.

( 12 Marks )

6 (b ) A mutual Fund raised 100 lakh on April 1,2015 by issue of 10 lakh units of Rs. 10per unit.

The fund invested in several capital market instruments to build a portfolio of Rs. 90 Lacs. The

initial expenses amounted to Rs. 7 lac.During April 2015, the fund sold certain securities of cost

Rs. 38 Lacs for 40 Lacs and purchased certain other securities for Rs. 28.2 lacs. The fund

management expenses for the month amounted to Rs. 4.5 lacs of which Rs. 0.25 Lacs was in

arrears. The dividend earned was Rs. 1.2 lacs. 75% of the realized earnings were distributed.

The market value of the portfolio on 30/04/2015 was Rs.100.9 Lacs. Determine NAV per unit

( 4 Marks )

7. Answer any four of the following: (4 x 4M= 16M)

(a) List down any four key differences between Ind AS-1presentation of Financial statements

and existing notified AS-1 disclosure of accounting policies.

(b) X Ltd had the following items under “Reserves and Surplus” in the Balance Sheet as on 31st

March 2015:

Particulars Rs. in Lacs

Securities Premium 50

Capital Reserve 30

General Reserve 21

The Company had accumulated loss of Rs 120 Lacs , on the same day , which it had disclosed

under the head “ statement of Profit & Loss “ as an asset in the Balance Sheet.

Comment on the correctness of this treatment in line with Schedule III to the Companies Act

2013.

PRIME A

CADEMY

6

( c ) Write a short note on other comprehensive income.

(d) write a short note on Corporate Social Responsibility according to the Companies Act 2013.

( e ) Explain the concept of fair value with reference to Indian Accounting Standards.

PRIME A

CADEMY

PRIME/43rd /FINAL 1

THE SOCIETY OF AUDITORS AND PRIME ACADEMY 43rd SESSION MODEL EXAM – FINAL – FINANCIAL REPORTING

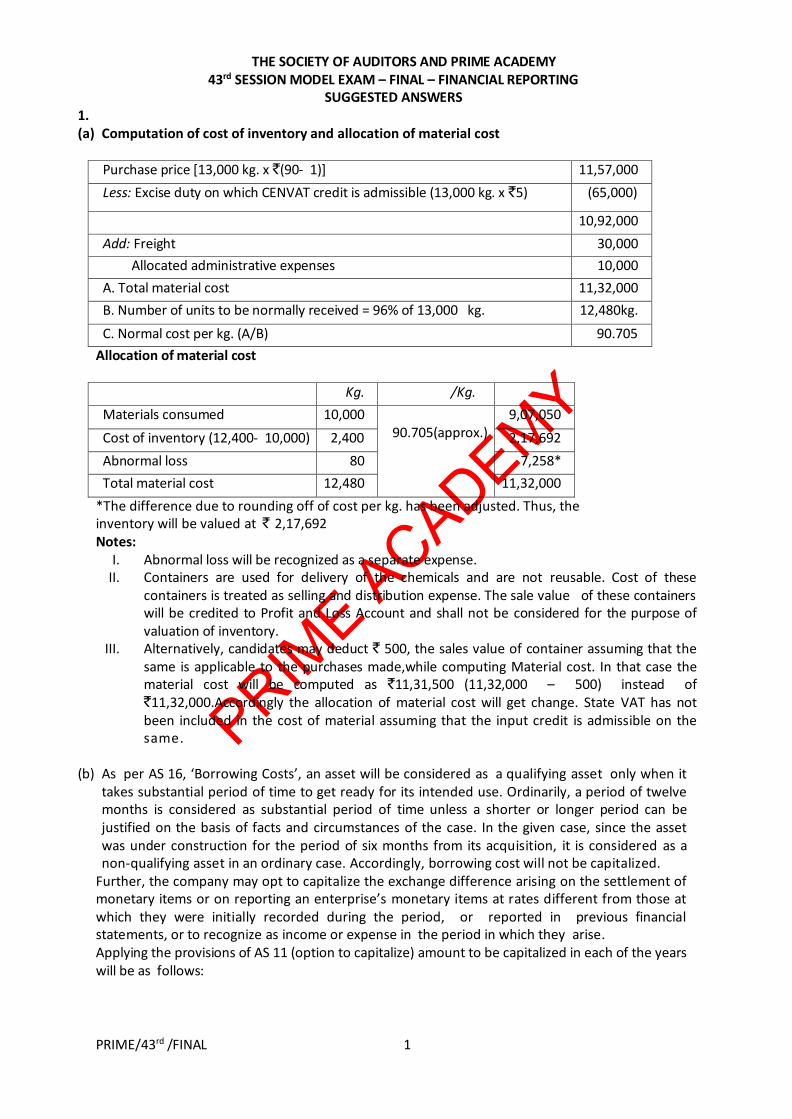

SUGGESTED ANSWERS 1. (a) Computation of cost of inventory and allocation of material cost

Purchase price [13,000 kg. x `(90- 1)] 11,57,000

Less: Excise duty on which CENVAT credit is admissible (13,000 kg. x `5) (65,000)

10,92,000

Add: Freight 30,000

Allocated administrative expenses 10,000

A. Total material cost 11,32,000

B. Number of units to be normally received = 96% of 13,000 kg. 12,480kg.

C. Normal cost per kg. (A/B) 90.705

Allocation of material cost

Kg. /Kg.

Materials consumed 10,000 90.705(approx.)

9,07,050

Cost of inventory (12,400- 10,000) 2,400 2,17,692

Abnormal loss 80 7,258*

Total material cost 12,480 11,32,000

*The difference due to rounding off of cost per kg. has been adjusted. Thus, the inventory will be valued at ` 2,17,692 Notes:

I. Abnormal loss will be recognized as a separate expense. II. Containers are used for delivery of the chemicals and are not reusable. Cost of these

containers is treated as selling and distribution expense. The sale value of these containers will be credited to Profit and Loss Account and shall not be considered for the purpose of valuation of inventory.

III. Alternatively, candidates may deduct ` 500, the sales value of container assuming that the same is applicable to the purchases made,while computing Material cost. In that case the material cost will be computed as `11,31,500 (11,32,000 – 500) instead of `11,32,000.Accordingly the allocation of material cost will get change. State VAT has not been included in the cost of material assuming that the input credit is admissible on the same.

(b) As per AS 16, ‘Borrowing Costs’, an asset will be considered as a qualifying asset only when it

takes substantial period of time to get ready for its intended use. Ordinarily, a period of twelve months is considered as substantial period of time unless a shorter or longer period can be justified on the basis of facts and circumstances of the case. In the given case, since the asset was under construction for the period of six months from its acquisition, it is considered as a non-qualifying asset in an ordinary case. Accordingly, borrowing cost will not be capitalized.

Further, the company may opt to capitalize the exchange difference arising on the settlement of monetary items or on reporting an enterprise’s monetary items at rates different from those at which they were initially recorded during the period, or reported in previous financial statements, or to recognize as income or expense in the period in which they arise. Applying the provisions of AS 11 (option to capitalize) amount to be capitalized in each of the years will be as follows:

PRIME A

CADEMY

PRIME/43rd /FINAL 2

Purpose ` Amount to be

capitalized `

Interest to be charged to

profit and loss account ̀

Initial cost at the time of acquisition of fixed asset

US $ 1,25,000 x Rs 61.50

76,87,500

On payment of 1st instalment US $ 25,000 x (61.60 - 61.50)

2,500

Interest paid with 1st instalment (1,00,000 x 8% x 6/12)x61.60

2,46,400

On payment of 2nd instalment US $ 25,000 x (61.80 - 61.50)

7,500

Interest paid with 2nd instalment (75,000 x 8% x 6/12) x 61.80

1,85,400

Exchange difference on closing balance of long term foreign currency

US $ 50,000 x (61.80 - 61.50)

15,000

At the end of the year 1 77,12,500 4,31,800

On payment of 3rd instalment

US $ 25,000 x (61.90 - 61.80)

2,500

Interest paid with 3rd instalment (50,000 x 8% x 6/12) x 61.90

1,23,800

On payment of 4th instalment

US $ 25,000 x (62.10 - 61.80)

7,500

Interest paid with 4th instalment (25,000 x 8% x 6/12) x 62.10

62,100

At the end of the year 2 10,000 1,85,900 The entire amount of exchange difference of ̀35,000 (25,000 + 10,000) will be capitalized to ‘Fixed Asset account’. This capitalized exchange difference will be depreciated over the useful life of the asset.

(c) As per AS 13 ‘Accounting for Investments’, if the shares are purchased with an intention to hold for short-term period then investment will be shown at the market value. In the given

case, shares purchased on 31st October, 2015, will be valued at ` 3,75,000 as on 31st March, 2016.Gold and silver are generally purchased with an intention to hold it for long term period until and unless given otherwise. Hence, the investment in gold and silver(purchased on

31st March, 2013) shall continue to be shown at cost as on 31st March, 2016 i.e., ` 5,00,000 and `2,25,000 respectively, though their realizable values have been increased. Thus the shares, gold and silver will be shown at ` 3,75,000, ` 5,00,000 and `2,25,000 respectively and hence, total investment will be valued at `11,00,000 in the books of account of

Dynamic Ltd. for the year ending 31st March, 2016 as per provisions of AS 13.

(d) Net effect on the Statement of Profit and Loss in the year of sale in the books of Lessee (Sahara Ltd.) For calculation of net effect on the statement of profit and loss on sale of equipment, it has to be judged whether lease is an operating lease or finance lease. The lease term is for 10 years which covers the entire economic life of the equipment. At the inception of the lease, the present value of the minimum lease payments (MLP) is ̀6,14,400 [` 1,00,000 x 6.144 (Annuity factor of Re. 1 @10% for 10 years)] and amounts to at least substantially all of the fair value (sale price i.e.`6,14,460) of the leased equipment. Thus lease is a finance lease. As per para 48 of AS 19 “Leases”, if a sale and leaseback transaction results in a finance lease, profit of ` 5,14,460 (Sale value ` 6,14,460 less carrying amount` 1,00,000) will not be recognized as income in the year of sale in the books of lessee i.e. Sahara Ltd. It should be deferred and amortised over the lease term in proportion to the depreciation of the leased asset.

PRIME A

CADEMY

PRIME/43rd /FINAL 3

Therefore, assuming that depreciation is charged on straight line basis, Sahara Ltd. will recognize depreciation of ` 61,446 per annum for 10 years (` 6,14,460/ 10) and amortise profit of ̀5,14,460 over the lease term of 10 years, i.e. ` 51,446 p.a. The net effect is a debit of ( ̀61,446 - ̀51,446) ` 10,000 p.a. to the Statement of Profit and Loss, for 10 years as covered under the lease term. Note: Had there been no sale and lease back transaction, the Statement of Profit and Loss for each year (covered in the lease term) would have been charged by(` 1,00,000/10) ̀10,000, towards depreciation. Thus, the sale and lease back transaction will have no impact on profit or loss account to be reported by the lessee (vendor in the sales transaction) over the lease period.

2.

Consolidated Balance Sheet of M Ltd. & its subsidiary D Ltd. as on 31st March 1989

Liabilities ` ` Assets ` ̀

Share Capital

Authorised ? Fixed Assets

Issued and Subscribed : Goodwill

100000 Equity shares of ` 10 each fully paid

1,000,000 M Ltd 300,000

Minority Interest 175,200 D Ltd 70,000

Reserves and Surplus 370,000

General reserve 420,000 Less: Capital reserve on consolidation

76,375 293,625

Profit & loss account

Balance as per M ltd's balance Sheet

260,000 Land and buildings

less: capital receipt M Ltd 400,000

15% Dividend on 12000 shares wrongly credited earlier

18,000 D Ltd 100,000 500,000

242,000

add: Charged to D ltd for services 4,500 Plant and machinery

add: M Ltd share of D ltd's profit 34,425 M Ltd 500,000

280,925 D Ltd 100,000 600,000

less: Unrealised Profit 6,667 274,258

Current liabilities and provisions Current Assets Loans and Advances

Current Liabilities Current Assets

Bills payable Stock

M Ltd 80,000 M Ltd 200,000

D Ltd 60,000 D Ltd 40,000

140,000 240,000

less: Mutual Owing 40,000 100,000 Less: unrealised profit 6,667 233,333

Creditors Book Debts

M Ltd 182,500 M Ltd 300,000

D Ltd 42,000 224,500 D Ltd 85,000 385,000

Provisions 0 Cash and Bank balance

M Ltd 80,000

D Ltd 62,000 142,000

PRIME A

CADEMY

PRIME/43rd /FINAL 4

Loans and Advances

Bills Receivable

M Ltd 50,000

D Ltd 30,000

80,000

Less: Mutual Owing 40,000 40,000

2,193,958 2,193,958

Working note 1:

D Ltd's profit and loss account

` `

To Dividend for 1987-88 30,000.00 By Balance b/d 40,000.00

To balance c/d 92,500.00 By Net Profit for the year 82,500.00

(Working note (ii) ) (Balancing figure)

1,22,500.00 1,22,500.00

Working Note 2:

` Balance of D ltd's Profit and Loss Account as on 1st April 1988

85,000

Add: Interest on Loan to M Ltd not yet accounted for

7,500 correct closing balance

92,500

Working Note 3: Capital Profits Balance of D Ltd's Profit and Loss Account as on 1st April 1988

40,000 Less: Dividend paid out of the above balance

30,000

Balance left

10,000 Add: Profit for the three months

ie till July 1,1988,` 82500 * 3/12

20,625 Add: D Ltd's general Reserve after bonus issue

50,000

80,625

M ltd's share ` 80625 * 60/100

48,375 Working Note 4: current Profits

` profit after 1st July 1988( ` 82500*9/12)

61,875

Less: Amount credited to M Ltd for services rendered

4,500 ` 500 * 9

correct post- acquisition profit

57,375 M ltd's share

` 57375 * 60/100

34,425 Working Note 5: Minority Interest

` Paid up value of 40% shares in D Ltd

1,20,000

PRIME A

CADEMY

PRIME/43rd /FINAL 5

Add: 40% of capital Profits

32,250 (` 80625 *40/100)

Add: 40% of current Profits

22,950 ` 57375 * 40/100

1,75,200 Working Note 6: Capital Reserve on consolidation:

` Paid up value of D Ltd's share held by M Ltd

1,80,000

Add: M ltd share of capital Profits

48,375 Working Note (iii)

2,28,375

less: Amount paid for the shares 170000 less: Dividend received out of pre-acquisition profit 18000 1,52,000

Capital reserve on consolidation

76,375

Working Note 7: Unrealised profit on stock

6,667 ` 40000*20/120

3.

Suppose total loss is ` X

Then, the capital lost is ` X – ` 1,00,000 because there is a capital reserve of ` 1,00,000.

Capital of the company is ` 3 (X – 1,00,000) or ` 3X – ` 3,00,000

Then,

3X – 3,00,000= 11,00,000 + X – 1,00,000

Or 3X – X = 11,00,000 – 1,00,000 + 3,00,000

Or 2X = 13,00,000

Hence, X = 6,50,000

Thus loss is ` 6,50,000 and total share capital is

= ` 3( 6,50,000 – 1,00,000) = ` 16,50,000 of which,

Equity share capital = ` 1,65,000 * 3/5 = ` 9,90,000 and

Preference share capital = ` 1,65,000 * 2/5 = ` 6,60,000

Balance Sheet of Zed ltd (Before Reconstruction)

Liabilities ̀ Assets ̀ ̀

Equity share capital

9,90,000 Goodwill

2,00,000

10% preference share capital 6,60,000 Other fixed assets: Cost 20,00,000 Capital reserve

1,00,000 Less: Depreciation 5,00,000 15,00,000

Bank Loan

4,50,000 Current Assets

4,50,000

Current liabilities

6,00,000 Profit and Loss Account( bal fig) 6,50,000

28,00,000

28,00,000

Contingent Liability: Preference dividend in arrears for four years amounting to ` 2,64,000

PRIME A

CADEMY

PRIME/43rd /FINAL 6

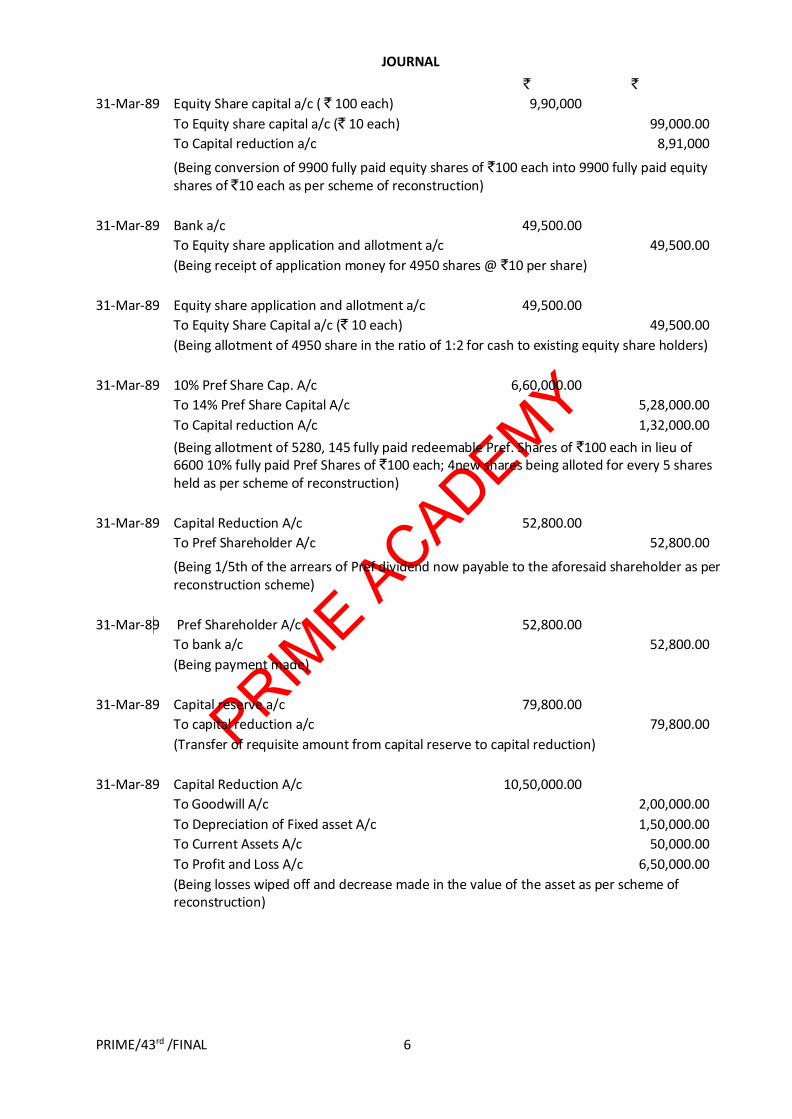

JOURNAL

` `

31-Mar-89 Equity Share capital a/c ( ` 100 each) 9,90,000

To Equity share capital a/c (` 10 each)

99,000.00

To Capital reduction a/c

8,91,000

(Being conversion of 9900 fully paid equity shares of `100 each into 9900 fully paid equity shares of ̀ 10 each as per scheme of reconstruction)

31-Mar-89 Bank a/c

49,500.00

To Equity share application and allotment a/c 49,500.00

(Being receipt of application money for 4950 shares @ `10 per share)

31-Mar-89 Equity share application and allotment a/c 49,500.00

To Equity Share Capital a/c (` 10 each) 49,500.00

(Being allotment of 4950 share in the ratio of 1:2 for cash to existing equity share holders)

31-Mar-89 10% Pref Share Cap. A/c 6,60,000.00

To 14% Pref Share Capital A/c

5,28,000.00

To Capital reduction A/c

1,32,000.00

(Being allotment of 5280, 145 fully paid redeemable Pref. Shares of `100 each in lieu of 6600 10% fully paid Pref Shares of `100 each; 4new shares being alloted for every 5 shares held as per scheme of reconstruction)

31-Mar-89 Capital Reduction A/c 52,800.00

To Pref Shareholder A/c

52,800.00

(Being 1/5th of the arrears of Pref dividend now payable to the aforesaid shareholder as per reconstruction scheme)

31-Mar-89 Pref Shareholder A/c 52,800.00

To bank a/c

52,800.00

(Being payment made)

31-Mar-89 Capital reserve a/c

79,800.00

To capital reduction a/c

79,800.00

(Transfer of requisite amount from capital reserve to capital reduction)

31-Mar-89 Capital Reduction A/c 10,50,000.00

To Goodwill A/c

2,00,000.00

To Depreciation of Fixed asset A/c

1,50,000.00

To Current Assets A/c

50,000.00

To Profit and Loss A/c

6,50,000.00

(Being losses wiped off and decrease made in the value of the asset as per scheme of reconstruction)

PRIME A

CADEMY

PRIME/43rd /FINAL 7

Balance Sheet of Z ltd as at 31st March, 1989 (After Reconstruction)

Liabilities ` ̀ Assets ̀ ̀

Share Capital

Authorised ? Fixed Assets

Issued and Subscribed : Goodwill 2,00,000.00

5280 14% Redeemable Pref Shares of `100 each fully paid

5,28,000.00 Less: Amount writtenoff under scheme of reconstruction

(2,00,000.00)

-

14850 Equity Shares of `10 each Fully Paid

1,48,500.00 6,76,500.00 Other Fixed Assets 20,00,000.00

Reserves and Surplus Less: Depreciation (5,00,000.00)

Capital Reserve 20,200.00 Less: Additional Depreciation

(1,50,000.00)

13,50,000.00

Secured loans Current Assets Loans and Advances

Bank Loans 4,50,000.00 Current Assets 3,96,700.00

Loans and Advances - 3,96,700.00

Current Liabilities and Provisions

Current Liabilities 6,00,000.00

Provisions - 6,00,000.00

17,46,700.00 17,46,700.00

4 (a) The Companies (Indian Accounting Standards) Rules, 2015, states that the following

companies shall comply with Ind AS for the accounting periods beginning on or after 1st

April, 2016, with the comparatives for the periods ending on 31st March, 2016, or thereafter, namely:- (a) companies whose equity or debt securities are listed or are in the process of being listed on

any stock exchange in India or outside India and having net worth of rupees five hundred crore or more;

(b) companies other than those covered by point (a) above and having net worth of rupees five hundred crore or more;

(c) holding, subsidiary, joint venture or associate companies of companies covered by point (a) and (b) as the case may be;

Further, the Companies (Indian Accounting Standards) Rules, 2015, states that for the purposes of calculation of net worth of companies, the following principles shall apply, namely:-

(a) the net worth shall be calculated in accordance with the stand-alone financial statements of

the company as on 31st March, 2014 or the first audited financial statements for accounting period which ends after that date;

(b) for companies which are not in existence on 31st March, 2014 or an existing company falling

under any of thresholds specified for the first time after 31st March, 2014, the net worth shall be calculated on the basis of the first audited financial statements ending after that date in respect of which it meets the thresholds specified.

PRIME A

CADEMY

PRIME/43rd /FINAL 8

The companies meeting the specified thresholds for the first time at the end of an accounting year shall apply Ind AS from the immediate next accounting year in the manner specified above. Once a company starts following Ind AS either voluntarily or mandatorily on the basis of criteria specified, it shall be required to follow Ind AS for all the subsequent financial statements even if any of the criteria specified in the rule does not subsequently apply to it. In view of the above requirements, Company A meets the criteria as specified the Companies

(Indian Accounting Standards) Rules, 2015, on 31st March, 2014. Accordingly, the Companies (Indian Accounting Standards) Rules, 2015, will become applicable to

the Company on mandatory basis from accounting periods commencing 1st April, 2016. A holding, subsidiary, joint venture or associate company of a Company to which the Companies (Indian Accounting Standards) Rules, 2015 applies will be required to follow the Companies (Indian Accounting Standards) Rules, 2015 for preparing and presenting its financial statements. In the abovementioned case, Company A has net worth of more than ` 500 crore in the financial

year ending 31st March 2014. Therefore, ordinarily Company A along with its subsidiaries will have to apply Indian Accounting Standards (Ind ASs) for preparing financial statements

fortheaccountingperiodscommencing1st April, 2016, except in situations Case A as discussed below:

A Company A has sold its investment in subsidiary Company Y on 31st December, 2015, in consequence of which Company Y is no longer subsidiary of Company A as at the

beginning of 1st April, 2016. Therefore, the Companies (Indian Accounting Standards) Rules, 2015 will not be applicableto Company Y. Therefore, Company Y would continue to prepare financial statements for accounting periods commencing April 1, 2016 under the Companies (Accounting Standards) Rules, 2006.

B Company A has sold its investment in subsidiary Company Z on 31st December,

2016; therefore, Company Z was a subsidiary of Company A as at the beginning of 1st April,

2016. Company Z being subsidiary of Company A as at the beginning of 1st April, 2016,

would have to prepare financial statements for the accounting periods commencing 1st April, 2016 as per the Companies (Indian Accounting Standards) Rules, 2015.

(b) (a) Under instant case the call option is exercisable within 12 months of reporting date (15

months minus 4 months), and accordingly the company does not have an unconditional right to defer settlement of the liability for at least twelve months after the reporting date, and therefore same are to be classified as current trade payables.

(b) These are required to be disclosed under cash and cash equivalents separately in notes to accounts under Schedule III, however same is in conflict with the requirements of AS 3 “Cash Flow Statements” as they are neither in nature of demand deposits, nor readily available for use by the company, accordingly do-not meet the definition of cash equivalents. Hence the said items should also be included as ‘other bank balances’ under cash and bank balances along with FDR having balance maturity period of more than 12 months.

5. (a) Computation of Economic Value Added

Particulars ` in lakhs

Profit before Interest and Taxes (from W.N.1) 578.33 Less: Interest (50 + 45) (95.00)

483.33 Less: Taxes (193.33)

290 Add: Interest (net of tax) [95 x (1 - 0.40)] 57 Net Operating Profit After Taxes 347 Less: Cost of Capital (WACC x Capital Employed) (2,000 x 12.95%) (259.00) Economic Value Added 88.00

PRIME A

CADEMY

PRIME/43rd /FINAL 9

Working Notes:

1. Calculation of Profit Before Tax

Particulars Computation ` in lakhs

Profit before Interest and Taxes Balancing figure 578.33

Less: Interest on Debentures 10% x ` 500 lakhs (50.00)

Interest on Bank Term Loan 10% x ` 450 lakhs (45.00)

Profit Before Tax (` 290.00 ÷ 60%) 483.33

Less: Tax @ 40% (` 290.00 ÷ 60%) x 40%

(193.33)

Profit after Tax 290.00

Less: Preference Dividend 12% x ` 250 lakhs (30.00)

Residual earnings for equity shareholders

260.00

Less: Equity Dividend 20% x ` 800 lakhs (160.00)

Net balance in Profit and Loss Account Given 100.00

1. Computation of Cost of Equity :

= Risk Free Rate + Beta x (Market Rate – Risk Free Rate) = 6.5% + 1.5 (16.5% - 6.5%) = 21.5%

2. Cost of Debt

Interest ` 45 lakhs Less: Tax (40%) (` 18 lakhs)

Interest after Tax ` 27 lakhs

27 Cost of Debt = 6%

450 3. Computation of Weighted Average Cost of Capital

Component Amount Ratio Individual Cost WACC

Equity ` 800 lakhs

800 ÷ 2000 =0.40 Ke = 21.5 8.6

Preference ` 250 lakhs

250 ÷2000 = 0.125 Ke = 12 1.5

Debt (500+ 450) ` 950 lakhs

950 ÷ 2000 = 0.475 Ke = 6 2.85

Total ` 2,000 lakhs

Ke 12.95%

5 (b) Provision of SARs A/c (For 2010-11)

To Balance c/d 3,42,860 By Employee Compensation Expense

3,42,860

3,42,860 3,42,860

Provision of SARs A/c (For 2011-12) To Balance c/d 7,43,667 By Balance b/d 3,42,860

By Employee Compensation Expenses

4,00,807

7,43,667 7,43,667 Provision of SARs A/c (For 2013-14)

To Balance c/d 11,80,800 By Balance b/d 7,43,667

By Employee Compensation Expenses

4,37,133

11,80,800 11,80,800 Provision of SARs A/c (For 2013-14)

To Bank (49,200 x 25)

12,30,000 By Balance b/d 11,80,800

By Employee Expenses 49,200

12,30,000 12,30,000

PRIME A

CADEMY

PRIME/43rd /FINAL 10

The Provision for SAR is a liability as settlement of SAR is through cash payment equivalent to an excess of market price of company’s shares on exercise date over the exercise price.

Working Notes: Year 2010-11 Number of employees to whom SARs were announced = 525 employees Total estimated SARs, to be vested at the end of the vesting period, as on 2010-11

= (525 -15 x 0.98 x 0.98) x 100 SARs = 48,980 SARs Fair value of SARs = 48,980 SARs ` 21 = ` 10,28,580 Vesting period = 3 years Recognised as expense in 2010–11 = ` 10,28,580 / 3 years = ` 3,42,860 Year 2011-12 Total number of employees after three years, on the basis of the estimation in 2011-12

= [(525 – 15 - 10) x 0.97] x 100 SARs = 48,500 SARs Fair value of SARs = 48,500 SARs ` 23 = ` 11,15,500 Vesting period = 3 years No. of years expired = 2 years Cumulative value of SARs to recognize as expense

= 11,15,500/3 2 = ` 7,43,667 SARs recognize as expense in 2011–12

= ` 7,43,667 – ` 3,42,860 = ` 4,00,807 Year 2012-13 Fair value of SARs = ` 24 SARs actually vested = 492 employees 100 = 49,200 SARs Fair value = 49,200 SARs ` 24 = ̀ 11,80,800 Cumulative value to be recognized = ` 11,80,800 Value of SARs to be recognized as an expense = ` 11,80,800 – ` 7,43,667 = ` 4,37,133 Year 2013–14 Cash payment of SARs = 49,200 SARs ` 25 = ` 12,30,000 Value of SARs to be recognized as an expense in 2013–14

= ` 12,30,000 – ` 11,80,800 = ` 49,200

6. (a)

Calculation of Profit After Tax ` `

Profit Before Interest and Tax (PBIT) 7,20,000

Less : Debenture Interest ( 500000 * 12/100) (60,000)

Profit Before Tax (PBT) 6,60,000

less : Tax @ 40% (2,64,000)

Profit after Tax (PAT) 3,96,000

less : Preference dividend ( 500000*12/100) 60000

less : Equity Dividend (1800000 * 15/100) 270000 (3,30,000)

Retained Earnings ( Undistributed Profit) 66,000

PRIME A

CADEMY

PRIME/43rd /FINAL 11

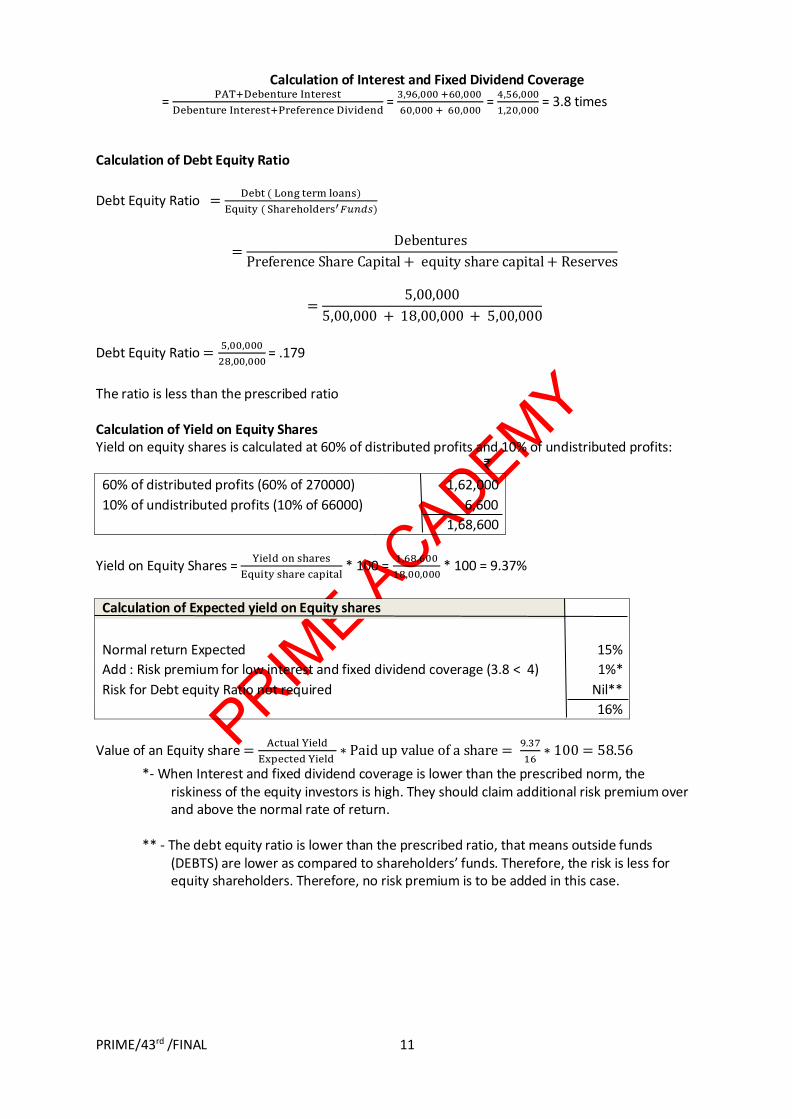

Calculation of Interest and Fixed Dividend Coverage

= PAT+Debenture Interest

Debenture Interest+Preference Dividend =

3,96,000 +60,000

60,000 + 60,000 =

4,56,000

1,20,000 = 3.8 times

Calculation of Debt Equity Ratio

Debt Equity Ratio =Debt ( Long term loans)

Equity ( Shareholders′ 𝐹𝑢𝑛𝑑𝑠)

=Debentures

Preference Share Capital + equity share capital + Reserves

=5,00,000

5,00,000 + 18,00,000 + 5,00,000

Debt Equity Ratio =5,00,000

28,00,000 = .179

The ratio is less than the prescribed ratio Calculation of Yield on Equity Shares Yield on equity shares is calculated at 60% of distributed profits and 10% of undistributed profits:

`

60% of distributed profits (60% of 270000) 1,62,000

10% of undistributed profits (10% of 66000)

6,600

1,68,600

Yield on Equity Shares = Yield on shares

Equity share capital * 100 =

1,68,600

18,00,000 * 100 = 9.37%

Calculation of Expected yield on Equity shares

Normal return Expected 15%

Add : Risk premium for low interest and fixed dividend coverage (3.8 < 4) 1%*

Risk for Debt equity Ratio not required Nil**

16%

Value of an Equity share =Actual Yield

Expected Yield ∗ Paid up value of a share =

9.37

16∗ 100 = 58.56

*- When Interest and fixed dividend coverage is lower than the prescribed norm, the riskiness of the equity investors is high. They should claim additional risk premium over and above the normal rate of return.

** - The debt equity ratio is lower than the prescribed ratio, that means outside funds

(DEBTS) are lower as compared to shareholders’ funds. Therefore, the risk is less for equity shareholders. Therefore, no risk premium is to be added in this case.

PRIME A

CADEMY

PRIME/43rd /FINAL 12

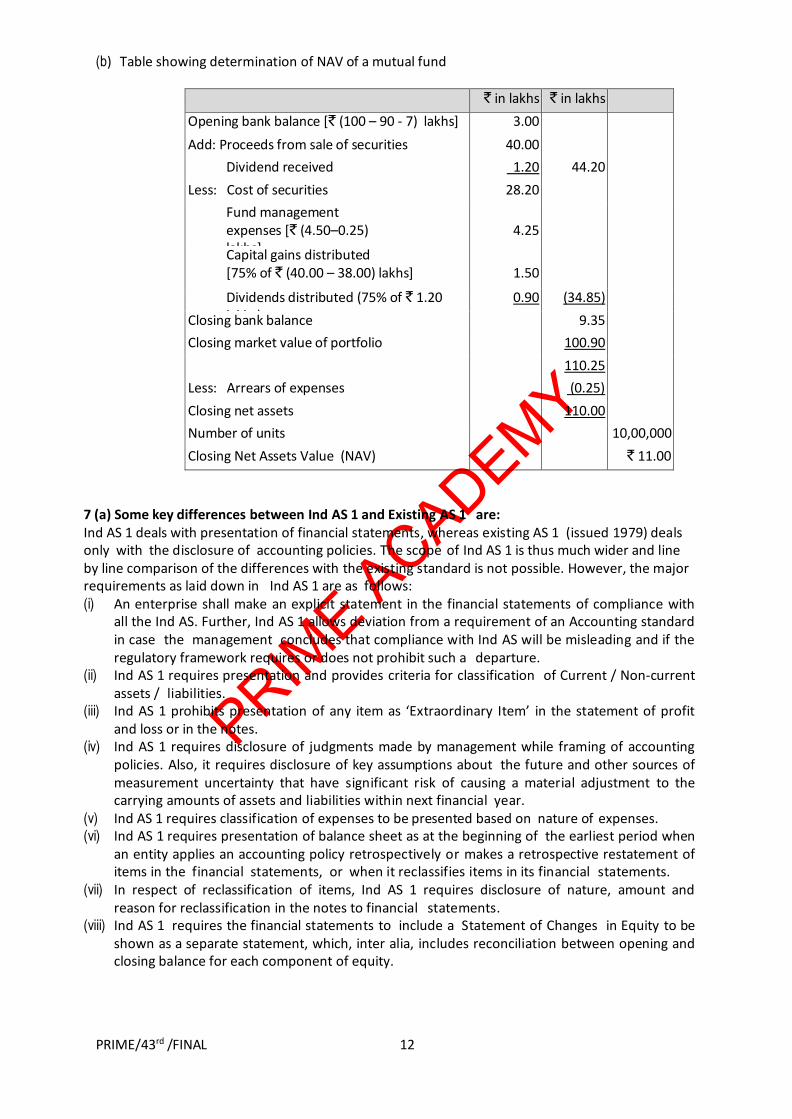

(b) Table showing determination of NAV of a mutual fund

` in lakhs ` in lakhs

Opening bank balance [` (100 – 90 - 7) lakhs] 3.00

Add: Proceeds from sale of securities 40.00

Dividend received 1.20 44.20

Less: Cost of securities 28.20

Fund management expenses [` (4.50–0.25) lakhs]

4.25

Capital gains distributed [75% of ` (40.00 – 38.00) lakhs]

1.50

Dividends distributed (75% of ` 1.20 lakhs)

0.90 (34.85)

Closing bank balance 9.35

Closing market value of portfolio 100.90

110.25

Less: Arrears of expenses (0.25)

Closing net assets 110.00

Number of units 10,00,000

Closing Net Assets Value (NAV) ` 11.00

7 (a) Some key differences between Ind AS 1 and Existing AS 1 are: Ind AS 1 deals with presentation of financial statements, whereas existing AS 1 (issued 1979) deals only with the disclosure of accounting policies. The scope of Ind AS 1 is thus much wider and line by line comparison of the differences with the existing standard is not possible. However, the major requirements as laid down in Ind AS 1 are as follows: (i) An enterprise shall make an explicit statement in the financial statements of compliance with

all the Ind AS. Further, Ind AS 1 allows deviation from a requirement of an Accounting standard in case the management concludes that compliance with Ind AS will be misleading and if the regulatory framework requires or does not prohibit such a departure.

(ii) Ind AS 1 requires presentation and provides criteria for classification of Current / Non-current assets / liabilities.

(iii) Ind AS 1 prohibits presentation of any item as ‘Extraordinary Item’ in the statement of profit and loss or in the notes.

(iv) Ind AS 1 requires disclosure of judgments made by management while framing of accounting policies. Also, it requires disclosure of key assumptions about the future and other sources of measurement uncertainty that have significant risk of causing a material adjustment to the carrying amounts of assets and liabilities within next financial year.

(v) Ind AS 1 requires classification of expenses to be presented based on nature of expenses. (vi) Ind AS 1 requires presentation of balance sheet as at the beginning of the earliest period when

an entity applies an accounting policy retrospectively or makes a retrospective restatement of items in the financial statements, or when it reclassifies items in its financial statements.

(vii) In respect of reclassification of items, Ind AS 1 requires disclosure of nature, amount and reason for reclassification in the notes to financial statements.

(viii) Ind AS 1 requires the financial statements to include a Statement of Changes in Equity to be shown as a separate statement, which, inter alia, includes reconciliation between opening and closing balance for each component of equity.

PRIME A

CADEMY

PRIME/43rd /FINAL 13

(ix) Ind AS 1 requires that an entity shall present a single statement of profit and loss, with profit or loss and other comprehensive income presented in two sections. The sections shall be presented together, with the profit or loss section presented first followed directly by the other comprehensive income section.

(x) As per Ind AS 1, an entity shall include certain comparative information for understanding the current period’s financial statements.

(xi) Ind AS 1 clarifies that long term loan arrangement need not be classified as current on account of breach of a material provision, for which the lender has agreed to waive before the approval of financial statements for issue.

(b) In accordance with Note 6(B) given under part I of Schedule III to the Companies Act, 2013,the debit balance of Profit and Loss (after all allocations and appropriations), if any, shall be shown as a negative figure under the head ‘Surplus’. Similarly the balance of ‘Reserves and Surplus’ after adjusting negative balance of surplus, shall be shown under the head ‘Reserves and Surplus’, even if the resulting figure is in negative. In this case, the debit balance of `120 lakhs, exceeds the total of all the reserves i.e. `101 lakhs. Negative balance of `19 lakhs of “Reserves and Surplus” after adjusting debit balance of ‘Profit and Loss’ should be disclosed on the face of Balance Sheet under the sub-heading “Reserves and Surplus” under the heading “Shareholders’ Fund”. Thus the treatment done by the company is incorrect.

(c) Other comprehensive income comprises items of incomes and expenses (including

reclassification adjustments) that are not recognized in profit or loss as required or permitted by other Ind Ass.The standard requires an entity to disclose reclassification adjustments and income tax relating to each component of other comprehensive income. Reclassification adjustments are th amounts reclassified to profit or loss in the current period that were previously recognized in other comprehensive income. The other comprehensive income section shall present line items for amounts of other comprehensive income in the period , classified by nature (including share of the other comprehensive income of associates and joint ventures accounted for using the equity method ) and grouped into those that, in accordance with other Ind AS :

A. Will not be reclassified subsequently to profit or loss ; and B. Will be classified subsequently to profit or loss when specific conditions are met.

(d) Corporate Social Responsibility (CSR) Reporting is an information communiqué with respect to

discharge of social responsibilities of corporate entity. Through ‘CSR Report’ the corporate enterprises disclose the manner in which they are discharging their social responsibilities. More specifically, it is addressed to the public or society at large, although it can be squarely used by other user groups also. Section 135 of the Companies Act, 2013 mandated the companies fulfilling the criteria mentioned in the said section to spend certain amount of their profit on activities as specified in the Schedule VII to the Act. Companies not falling within that criteria can also spend on CSR activities voluntarily. However, besides the requirements of constitution of a CSR committee and a CSR policy, the corporate entities should also take care that expenditure incurred for CSR should not be the expenditure incurred for the activities in the ordinary course of business. If expenditure incurred is for the activities in the ordinary course of business, then it will not be qualified as expenditure incurred onCSR activities.

(e) Cost vs. Fair value Cost basis: The term cost refers to cost of purchase, costs of conversion on other costs incurred in bringing the goods to its present condition and location. Assets are recorded at the amount of cash or cash equivalents paid or the fair value of the other consideration given to acquire them at the time of their acquisition. Liabilities are recorded at the amount of proceeds received in exchange for the obligation, or in some circumstances (for example, income taxes), at the amounts of cash or cash equivalents expected to be paid to satisfy the liability in the normal course of business.

PRIME A

CADEMY

PRIME/43rd /FINAL 14

Fair value:Fair value of an asset is the amount at which an enterprise expects to exchange an asset between knowledgeable and willing parties in an arm’s length transaction. Fair value concept requires a lot of estimation and to the extent, it is subjective in nature. Accounting Standards are generally based on historical cost with a very few exceptions: AS 2 “Valuation of Inventories”– Inventories are valued at net realizable value (NRV) if cost of inventories is more than NRV. AS 10 “Accounting for Fixed Assets”– Items of fixed assets that have been retired from active use and are held for disposal are stated at net realizable value if their net book value is more than NRV. AS 13 “Accounting for Investments”– Current investments are carried at lower of cost and fair value. The carrying amount of long term investments is reduced to recognize the permanent decline in value. AS 15 “Employee Benefits”– The provision for defined benefits is made at fair value of the obligations. AS 26 “Intangible Assets”– If an intangible asset is acquired in exchange for shares or other securities of the reporting enterprise, the asset is recorded at its fair value, or the fair value of the securities issued, whichever is more clearly evident.

AS 28 “Impairment of Assets”– Provision is made for impairment of assets.

PRIME A

CADEMY

(1)43F/SFM

Total No. of Printed Pages – 5 Total Marks – 100

Total No. of Questions – 7 Time Allowed – 3 Hours

THE SOCIETY OF AUDITORS & PRIME ACADEMY

Final - Model Exam - September 2016

Strategic Financial Management

Questions No.1 is compulsory.

Attempt any five out of the remaining six questions.

Wherever appropriate, suitable assumptions should be made and indicated in the answer by the candidate.

Working Notes should form part of the answer.

1. (a) Swastik Ltd manufacturers of special purpose machine tools, have two divisions that are peri-odically assisted by visiting teams of consultants. The Management is worried about the steady increase of expenses in this regard over the years. An analysis of last year’s expenses reveals: Consultants remuneration Rs.2,50,000; Travel & Conveyance Rs.1,50,000; Accommodation Ex-penses Rs.600,000; Boarding Charges Rs.2,00,000; Special Allowances Rs.50,000. The manage-ment estimates accommodation expenses to increase by Rs.2,00,000 annually. As part of a cost reduction drive, Swastik Ltd are proposing to construct a consultancy centre to take care of the accommodation requirements of the consultants. This center will additionally save the company Rs.50,000 in boarding charges and Rs.2,00,000 in the cost of Executive Training Programs hith-erto conducted outside the Company’s premises every year. The following details are available regarding the construction and maintenance of the new center. Land: At a cost of Rs. 8,00,000 already owned by the Company, will be used. Construction cost: Rs. 15,00,000 including special furnishings. Cost of annual maintenance Rs.1,50,000 Construction cost will be written off over 5 years being the useful life. Assuming that the write off of construction cost as aforesaid will be accepted for tax purposes, that the rate of tax will be 50% and that the desired rate of return is 15% you are required to analyse the feasibility of the proposal and make recommendation.

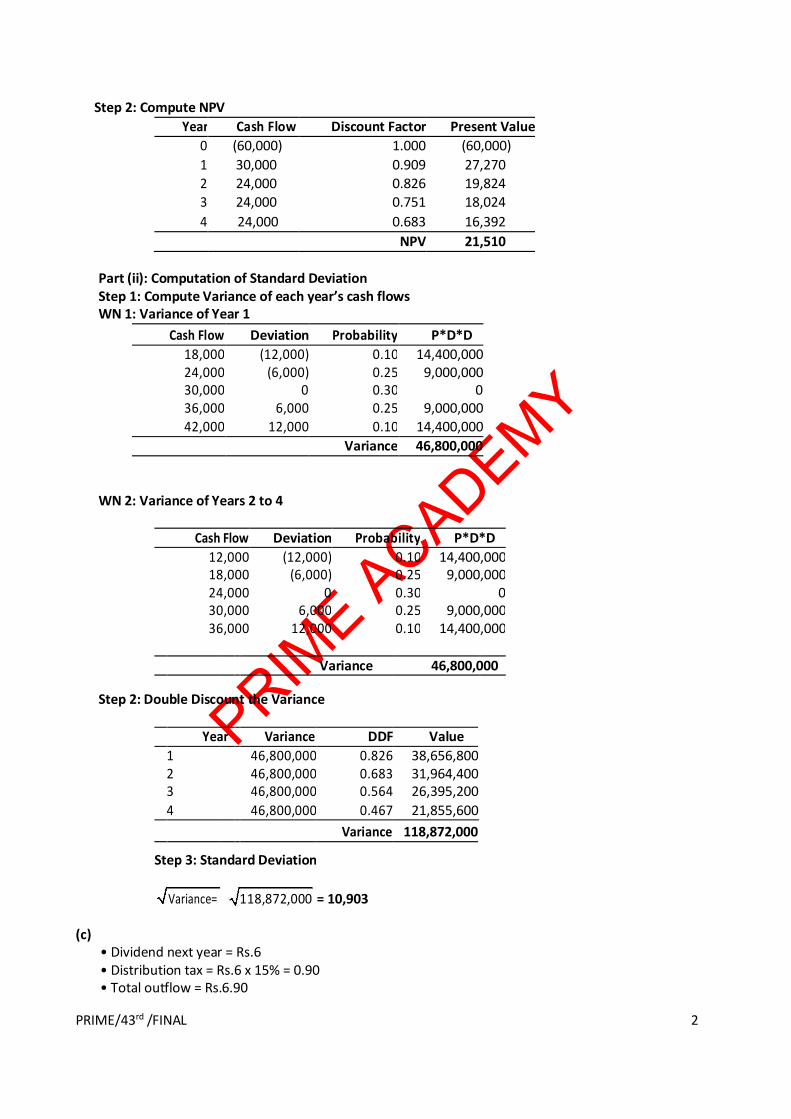

b. Investment in a four-year project is Rs.60,000, and expected CFAT carry the following probability distribution. Cash flows for each period is uncorrelated.

Probability CF (Rs.)Year 1

CF (Rs.)Year 2 to 4

0.10 18,000 12,0000.25 24,000 18,0000.30 30,000 24,0000.25 36,000 30,0000.10 42,000 36,000

Required: (i) Compute the NPV of the Project, assuming a discount rate of 10% . (ii) Compute standard deviation

PRIME A

CADEMY

(2)43F/SFM

c. X Ltd will pay Rs. 6 as dividend one year from today. The current market price of the share is Rs.90/-. This dividend will grow at 5% annually forever. Dividend distribution tax is 15% of the amount distributed. Compute cost of equity.

d. An investor is seeking the price to pay for a security, whose standard deviation is 3.00 per cent. The

correlation coefficient for the security with the market is 0.8 and the market standard deviation is 2.2 per cent. The return from government securities is 5.2 per cent and from the market portfolio is 9.8 per cent. The investor knows that, by calculating the required return, he can then determine the price to pay for the security. What is the required return on the security?

(4 x 5 = 20 marks)

2. (a) Sun Moon Mutual Fund (Approved Mutual Fund) sponsored open-ended equity oriented scheme “Chanakya Opportunity Fund”. There were three plans viz. ‘A’ – Dividend Re-investment Plan, ‘B’ – Bonus Plan & ‘C’ – Growth Plan.At the time of Initial Public Offer on 1.4.1995, Mr. Anand, Mr. Bacchan & Mrs. Charu, three investors invested Rs. 1,00,000 each & chosen ‘B’, ‘C’ & ‘A’ Plan respectively.The History of the Fund is as follows:Date Div (%) Bonus Plan A Plan B Plan C28.07.1999 20 30.70 31.40 33.4231.03.2000 70 5 : 4 58.42 31.05 70.0531.10.2003 40 42.18 25.02 56.1515.03.2004 25 46.45 29.10 64.2831.03.2004 1 : 3 42.18 20.05 60.1224.03.2005 40 1 : 4 48.10 19.95 72.4031.07.2005 53.75 22.98 82.07

On 31st July all three investors redeemed all the balance units. Calculate annual rate of return to each of the investors.Consider: 1. Long-term Capital Gain is exempt from Income tax. 2. Short-term Capital Gain is subject to 10% Income tax. 3. Security Transaction Tax 0.2 per cent only on sale/redemption of units. 4. Ignore Education Cess

b. (i) Identify the action to be taken in respect of the following situations?

Stock beta Stock position Stock Value (Rs.lakh) Hedge needed0.8 Long 2 Full1.2 Long 5 Full0.9 Short 1 Full1.0 Long 2 50%1.3 Short 4 110%

(ii) Consider the following data relating to KM stock. KM has a beta of 0.7 with NIFTY. Each Nifty contract is equal to 200 units. KM now quotes at Rs.150 and the Nifty futures is 5600 Index points. You are long on 12,000 shares of KM in the spot market. How many futures contracts will you have to take?

(2 x 8 = 16 marks)

PRIME A

CADEMY

(3)43F/SFM

3. (a) Bask PLC is a UK based importer. It has accepted an invoice for $ 350,000/- from a Florida supplier. The money is payable in six months. Exchange rates and money market rates in London are:

$/£ Spot 1.5865 - 1.59056 months Forward 1.5505 - 1.5545

(a) Compute and show how a money-market hedge can be put in place.

(b) Determine whether forward contract would be advantageous.

Money market ratesDeposit Loan

$ 5% 7%£ 7% 9%

3. (b) XYZ Limited borrows £ 15 Million of six months LIBOR + 10.00% for a period of 24 months. The company anticipates a rise in LIBOR, hence it proposes to buy a Cap Option from its Bankers at the strike rate of 8.00%. The lump sum premium is 1.00% for the entire reset peri-ods and the fixed rate of interest is 7.00% per annum. The actual position of LIBOR during the forthcoming reset period is as under:

Reset Period LIBOR 1 9.00% 2 9.50% 3 10.00%

You are required to show how far interest rate. Risk is hedged through Cap Option. For cal-culation, work out figures at each stage up to four decimal points and amount nearest to £. It should be part of working notes. (2 x 8 = 16 marks)

4. (a) Fair finance, a leasing company, has been approached by a prospective customer intending to acquire a machine whose Cash Down price is Rs. 3 crores. The customer, in order to leverage his tax position, has requested a quote for a three year lease with rentals payable at the end of each year but in a diminishing manner such that they are in the ratio of 3 : 2 : 1.Depreciation can be assumed to be on straight line basis and Fair Finance’s marginal tax rate is 35%. The target rate of return for Fair Finance on the transaction is 10%.Required: Calculate the lease rents to be quoted for the lease for three years.

4. (b) M. Co. Ltd., is studying the possible acquisition of N Co. Ltd., by way of merger. The follow-ing data are available in respect of the companies: Particulars M Co. Ltd. N Co. Ltd. Earnings after tax (Rs.) 80,00,000 24,00,000 Number of equity shares 16,00,000 4,00,000 Market value per share (Rs.) 200 160

(i) Compute pre-merger EPS and PEM of both companies(ii) If the merger goes through the exchange of equity and the exchange ratio is based on the

current market price, what is the new earnings per share for M Ltd.? (iii) What is the gain or loss in (ii) above?(iv) N Co Ltd., wants to be sure that the earnings available to its shareholders will not be di-

minished by the merger. What should be the exchange ratio in that case? (2 x 8 = 16 marks)

PRIME A

CADEMY

(4)43F/SFM

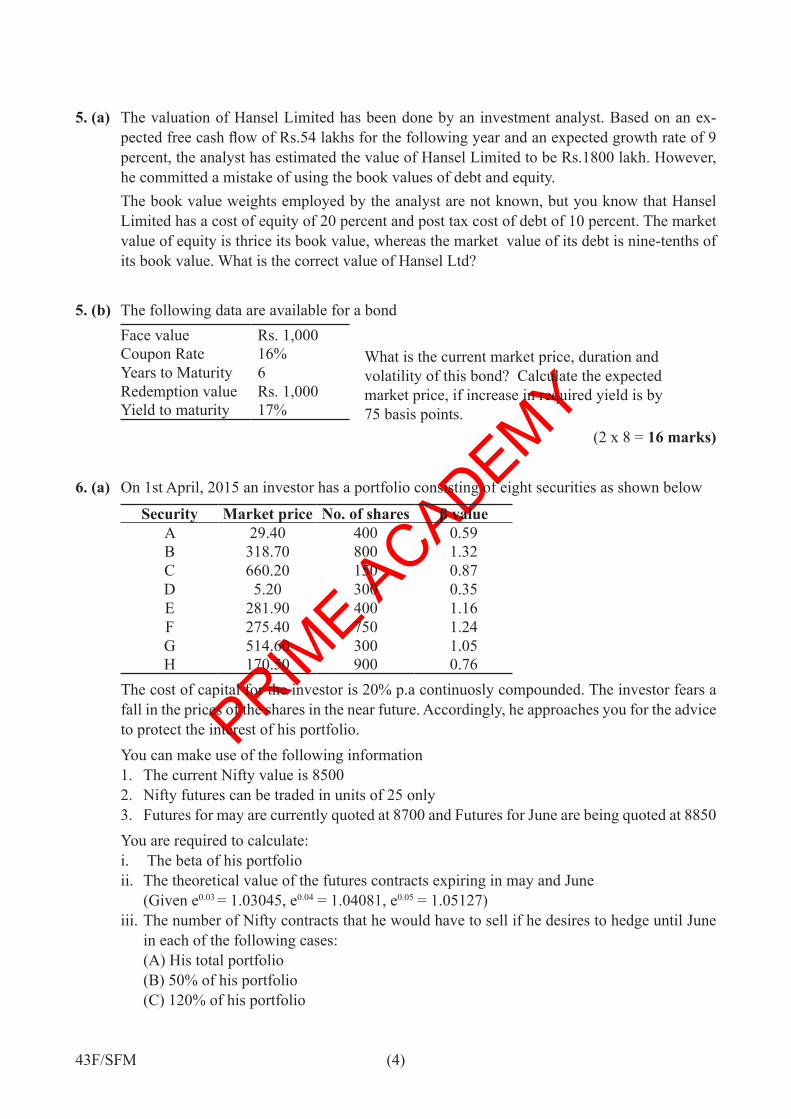

5. (a) The valuation of Hansel Limited has been done by an investment analyst. Based on an ex-pected free cash flow of Rs.54 lakhs for the following year and an expected growth rate of 9 percent, the analyst has estimated the value of Hansel Limited to be Rs.1800 lakh. However, he committed a mistake of using the book values of debt and equity.

The book value weights employed by the analyst are not known, but you know that Hansel Limited has a cost of equity of 20 percent and post tax cost of debt of 10 percent. The market value of equity is thrice its book value, whereas the market value of its debt is nine-tenths of its book value. What is the correct value of Hansel Ltd?

5. (b) The following data are available for a bondFace value Rs. 1,000

What is the current market price, duration and volatility of this bond? Calculate the expected market price, if increase in required yield is by 75 basis points.

Coupon Rate 16%Years to Maturity 6Redemption value Rs. 1,000Yield to maturity 17%

(2 x 8 = 16 marks)

6. (a) On 1st April, 2015 an investor has a portfolio consisting of eight securities as shown below

Security Market price No. of shares β valueA 29.40 400 0.59B 318.70 800 1.32C 660.20 150 0.87D 5.20 300 0.35E 281.90 400 1.16F 275.40 750 1.24G 514.60 300 1.05H 170.50 900 0.76

The cost of capital for the investor is 20% p.a continuosly compounded. The investor fears a fall in the prices of the shares in the near future. Accordingly, he approaches you for the advice to protect the interest of his portfolio.You can make use of the following information1. The current Nifty value is 85002. Nifty futures can be traded in units of 25 only3. Futures for may are currently quoted at 8700 and Futures for June are being quoted at 8850You are required to calculate:i. The beta of his portfolioii. The theoretical value of the futures contracts expiring in may and June (Given e0.03 = 1.03045, e0.04 = 1.04081, e0.05 = 1.05127)iii. The number of Nifty contracts that he would have to sell if he desires to hedge until June

in each of the following cases:(A) His total portfolio(B) 50% of his portfolio(C) 120% of his portfolio

PRIME A

CADEMY

(5)43F/SFM

6. (b) On January 1,2013 an investor has a portfolio of 5 shares as given below:Security Price No. of Shares Beta

A 349.30 5,000 1.15B 480.50 7,000 0.40C 593.52 8,000 0.90D 734.70 10,000 0.95E 824.85 2,000 0.85

The cost of capital to the investor is 10.5% per annum.You are required to calculate:(i) The beta of his portfolio. (2 x 8 = 16 marks)

7. Write short notes on the following:1. What are the factors you will consider in selecting your Mutual fund? 2. Name four alternatives to dividend.3. What is the difference between national Capital Budgeting and International Capital Budgeting?4. Explain briefly:

i) Yield to maturityii) Deep discount bond. (4 x 4 = 16 marks)

PRIME A

CADEMY

PRIME/43rd /FINAL 1

THE SOCIETY OF AUDITORS AND PRIME ACADEMY

43rd SESSION MODEL EXAM – FINAL – STRATEGIC FINANCIAL MANAGEMENT SUGGESTED ANSWERS

1. (a) Step 1: Initial Outflow (Rs. Lakhs)

Construction Cost: 15.0 The cost of the land is irrelevant since it represents a sunk cost. Market value of land is rel-evant because it’s an opportunity cost. However, it is assumed that the company has no inten-tion of selling the land. Hence the market value of land is not relevant.

Step 2: In-between Cash flows (Rs. lakhs)

Details Note 1 2 3 4 5

Savings in accommodation costs 8 10 12 14 16 Savings in boarding charges 0.5 0.5 0.5 0.5 0.5 Savings in training programs 2.0 2.0 2.0 2.0 2.0

Less : Annual Maintenance Cost (1.5) (1.5) (1.5) (1.5) (1.5) Less : Depreciation 1 (3.0) (3.0) (3.0) (3.0) (3.0) Profit Before Tax 6.0 8.0 10.0 12.0 14.0

Tax 3.0 4.0 5.0 6.0 7.0

Profit After Tax 3.0 4.0 5.0 6.0 7.0

Cash flow after Tax 6.0 7.0 8.0 9.0 10.0 WN 1: With capital expenditure at Rs.15 lakhs and life 5 years, the annual depreciation is Rs.3 lakhs. Step 3: Terminal Flow: NIL Step 4: Capital Budgeting Analysis Statement (Disc Fact 15%)

Year CF DF DCF

0 (15) 1.000 (15.00) 1 6.0 0.870 5.21 2 7.0 0.756 5.29 3 8.0 0.658 5.26 4 9.0 0.572 5.15 5 10.0 0.497 4.92 Conclusion: Since NPV of the project is NPV 10.83 Positive, the project should be accepted.

(b)

Part (i): Computation of NPV

Step 1: Compute Expected Value of Cash Flows

Cash Flows Expected Value

Probability Year 1 Year 2 to 4 Year 1 Year 2 to 4 0.10 18,000 12,000 1,800 1,200 0.25 24,000 18,000 6,000 4,500 0.30 30,000 24,000 9,000 7,200 0.25 36,000 30,000 9,000 7,500 0.10 42,000 36,000 4,200 3,600

Total 30,000 24,000

PRIME A

CADEMY

PRIME/43rd /FINAL 2

Step 2: Compute NPV

Year Cash Flow Discount Factor Present Value

0 (60,000) 1.000 (60,000)

1 30,000 0.909 27,270

2 24,000 0.826 19,824 3 24,000 0.751 18,024

4 24,000 0.683 16,392

NPV 21,510

Part (ii): Computation of Standard Deviation Step 1: Compute Variance of each year’s cash flows WN 1: Variance of Year 1

Cash Flow Deviation Probability P*D*D

18,000 (12,000) 0.10 14,400,000 24,000 (6,000) 0.25 9,000,000 30,000 0 0.30 0 36,000 6,000 0.25 9,000,000 42,000 12,000 0.10 14,400,000

Variance 46,800,000

WN 2: Variance of Years 2 to 4

Cash Flow Deviation Probability P*D*D

12,000 (12,000) 0.10 14,400,000 18,000 (6,000) 0.25 9,000,000 24,000 0 0.30 0 30,000 6,000 0.25 9,000,000 36,000 12,000 0.10 14,400,000

Variance 46,800,000

Step 2: Double Discount the Variance

Year Variance DDF Value

1 46,800,000 0.826 38,656,800 2 46,800,000 0.683 31,964,400 3 46,800,000 0.564 26,395,200

4 46,800,000 0.467 21,855,600

Variance 118,872,000

Step 3: Standard Deviation

= 10,903

Variance= 118,872,000 (c)

• Dividend next year = Rs.6 • Distribution tax = Rs.6 x 15% = 0.90 • Total outflow = Rs.6.90

PRIME A

CADEMY

PRIME/43rd /FINAL 3

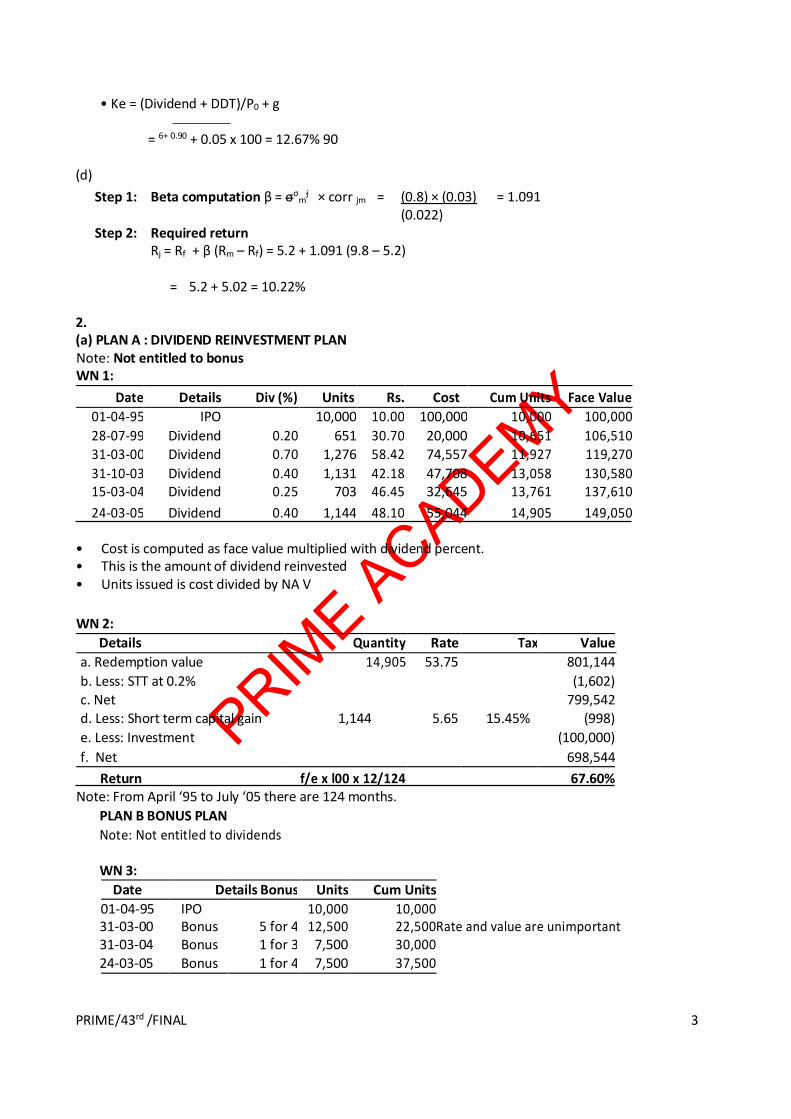

• Ke = (Dividend + DDT)/P0 + g

= 6+ 0.90 + 0.05 x 100 = 12.67% 90 (d)

Step 1: Beta computation β = σσm

j × corr jm = (0.8) × (0.03) = 1.091

Step 2: Required return (0.022)

Rj = Rf + β (Rm – Rf) = 5.2 + 1.091 (9.8 – 5.2)

= 5.2 + 5.02 = 10.22% 2. (a) PLAN A : DIVIDEND REINVESTMENT PLAN Note: Not entitled to bonus WN 1:

Date Details Div (%) Units Rs. Cost Cum Units Face Value

01-04-95 IPO 10,000 10.00 100,000 10,000 100,000

28-07-99 Dividend 0.20 651 30.70 20,000 10,651 106,510 31-03-00 Dividend 0.70 1,276 58.42 74,557 11,927 119,270

31-10-03 Dividend 0.40 1,131 42.18 47,708 13,058 130,580 15-03-04 Dividend 0.25 703 46.45 32,645 13,761 137,610

24-03-05 Dividend 0.40 1,144 48.10 55,044 14,905 149,050 • Cost is computed as face value multiplied with dividend percent. • This is the amount of dividend reinvested • Units issued is cost divided by NA V

WN 2:

Details Quantity Rate Tax Value

a. Redemption value 14,905 53.75 801,144

b. Less: STT at 0.2% (1,602) c. Net 799,542 d. Less: Short term capital gain 1,144 5.65 15.45% (998)

e. Less: Investment (100,000)

f. Net 698,544

Return f/e x l00 x 12/124 67.60% Note: From April ‘95 to July ‘05 there are 124 months.

PLAN B BONUS PLAN

Note: Not entitled to dividends WN 3:

Date Details Bonus Units Cum Units

01-04-95 IPO 10,000 10,000 31-03-00 Bonus 5 for 4 12,500 22,500 Rate and value are unimportant 31-03-04 Bonus 1 for 3 7,500 30,000

24-03-05 Bonus 1 for 4 7,500 37,500

PRIME A

CADEMY

PRIME/43rd /FINAL 4

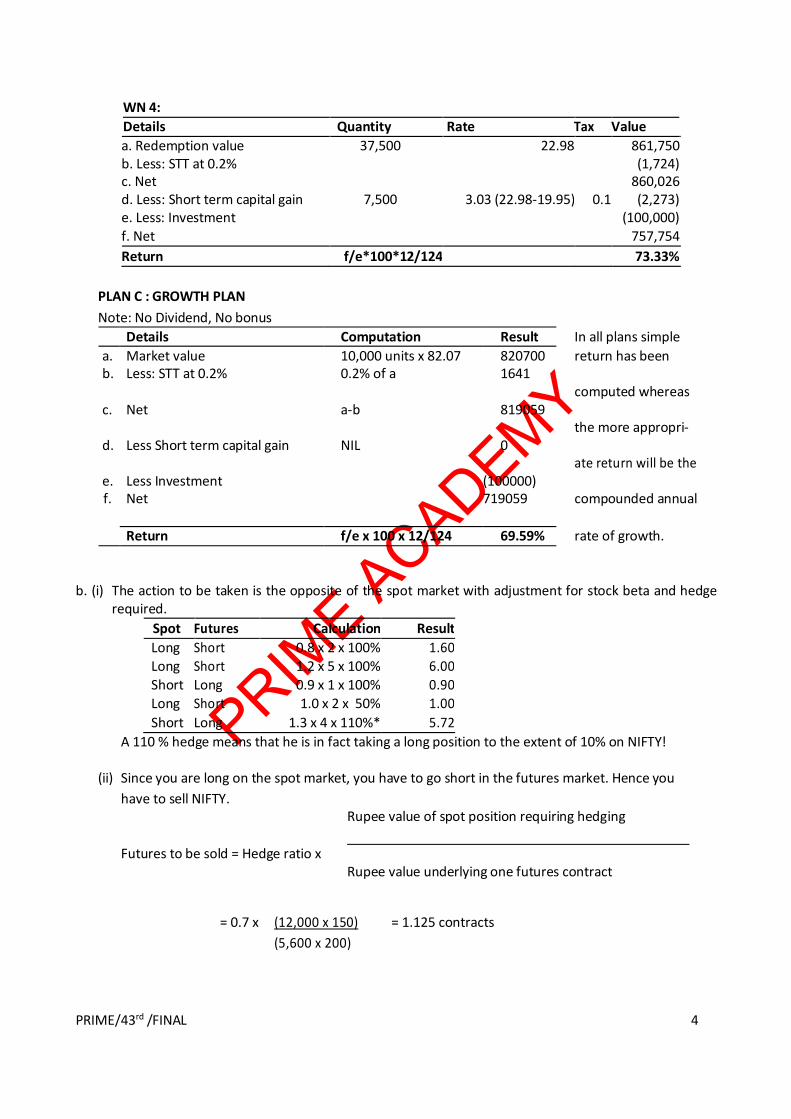

WN 4:

Details Quantity Rate Tax Value

a. Redemption value 37,500 22.98 861,750 b. Less: STT at 0.2% (1,724) c. Net 860,026 d. Less: Short term capital gain 7,500 3.03 (22.98-19.95) 0.1 (2,273) e. Less: Investment (100,000) f. Net 757,754

Return f/e*100*12/124 73.33%

PLAN C : GROWTH PLAN

Note: No Dividend, No bonus

Details Computation Result In all plans simple

a. Market value 10,000 units x 82.07 820700 return has been b. Less: STT at 0.2% 0.2% of a 1641

computed whereas

c. Net a-b 819059

the more appropri-

d. Less Short term capital gain NIL 0

ate return will be the

e. Less Investment

(100000)

compounded annual

f. Net 719059

rate of growth.

Return f/e x 100 x 12/124 69.59%

b. (i) The action to be taken is the opposite of the spot market with adjustment for stock beta and hedge

required.

Spot Futures Calculation Result

Long Short 0.8 x 2 x 100% 1.60 Long Short 1.2 x 5 x 100% 6.00

Short Long 0.9 x 1 x 100% 0.90 Long Short 1.0 x 2 x 50% 1.00

Short Long 1.3 x 4 x 110%* 5.72

A 110 % hedge means that he is in fact taking a long position to the extent of 10% on NIFTY!

(ii) Since you are long on the spot market, you have to go short in the futures market. Hence you

have to sell NIFTY. Rupee value of spot position requiring hedging

Futures to be sold = Hedge ratio x

Rupee value underlying one futures contract

= 0.7 x (12,000 x 150) = 1.125 contracts

(5,600 x 200)

PRIME A

CADEMY

PRIME/43rd /FINAL 5

3. (a)

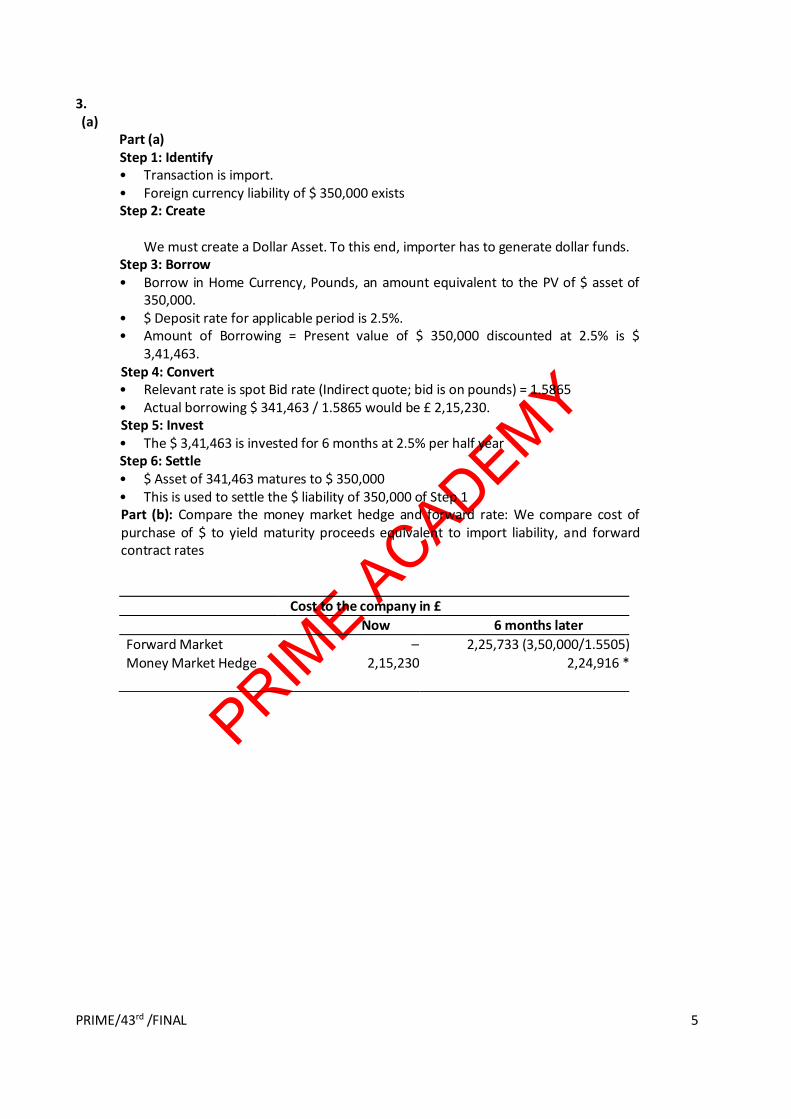

Part (a) Step 1: Identify • Transaction is import. • Foreign currency liability of $ 350,000 exists Step 2: Create

We must create a Dollar Asset. To this end, importer has to generate dollar funds. Step 3: Borrow • Borrow in Home Currency, Pounds, an amount equivalent to the PV of $ asset of

350,000. • $ Deposit rate for applicable period is 2.5%. • Amount of Borrowing = Present value of $ 350,000 discounted at 2.5% is $

3,41,463. Step 4: Convert • Relevant rate is spot Bid rate (Indirect quote; bid is on pounds) = 1.5865 • Actual borrowing $ 341,463 / 1.5865 would be £ 2,15,230. Step 5: Invest • The $ 3,41,463 is invested for 6 months at 2.5% per half year Step 6: Settle • $ Asset of 341,463 matures to $ 350,000 • This is used to settle the $ liability of 350,000 of Step 1 Part (b): Compare the money market hedge and forward rate: We compare cost of purchase of $ to yield maturity proceeds equivalent to import liability, and forward contract rates

Cost to the company in £

Now 6 months later

Forward Market – 2,25,733 (3,50,000/1.5505) Money Market Hedge 2,15,230 2,24,916 *

PRIME A

CADEMY

PRIME/43rd /FINAL 6

*(Since there is an initial outflow in £s, we have to compute the future value of these funds, based on an imputed cost at the borrowing rate of 9% for six months) Decision: Maturity value of the cost of £-funds under money market hedge is lower than quantum of £s involved for performing forward exchange contract at 1.5505. Hence we must opt for money market hedging. 3. (b)

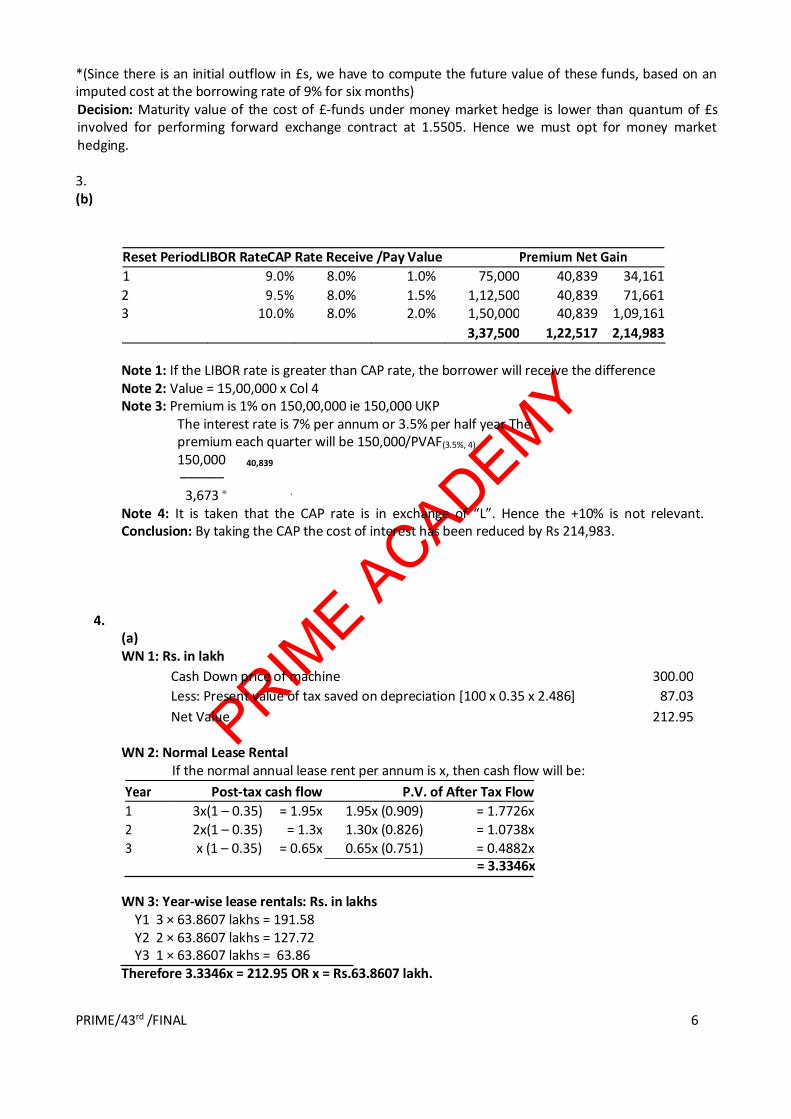

Reset PeriodLIBOR RateCAP Rate Receive /Pay Value Premium Net Gain

1 9.0% 8.0% 1.0% 75,000 40,839 34,161

2 9.5% 8.0% 1.5% 1,12,500 40,839 71,661 3 10.0% 8.0% 2.0% 1,50,000 40,839 1,09,161

3,37,500 1,22,517 2,14,983

Note 1: If the LIBOR rate is greater than CAP rate, the borrower will receive the difference Note 2: Value = 15,00,000 x Col 4 Note 3: Premium is 1% on 150,00,000 ie 150,000 UKP

The interest rate is 7% per annum or 3.5% per half year The premium each quarter will be 150,000/PVAF(3.5%, 4) 150,000 40,839 –––––– 3,673 = .

Note 4: It is taken that the CAP rate is in exchange of “L”. Hence the +10% is not relevant. Conclusion: By taking the CAP the cost of interest has been reduced by Rs 214,983.

4. (a) WN 1: Rs. in lakh

Cash Down price of machine 300.00

Less: Present value of tax saved on depreciation [100 x 0.35 x 2.486] 87.03

Net Value 212.95

WN 2: Normal Lease Rental If the normal annual lease rent per annum is x, then cash flow will be:

Year Post-tax cash flow P.V. of After Tax Flow

1 3x(1 – 0.35) = 1.95x 1.95x (0.909) = 1.7726x

2 2x(1 – 0.35) = 1.3x 1.30x (0.826) = 1.0738x 3 x (1 – 0.35) = 0.65x 0.65x (0.751) = 0.4882x

= 3.3346x

WN 3: Year-wise lease rentals: Rs. in lakhs Y1 3 × 63.8607 lakhs = 191.58 Y2 2 × 63.8607 lakhs = 127.72 Y3 1 × 63.8607 lakhs = 63.86

Therefore 3.3346x = 212.95 OR x = Rs.63.8607 lakh.

PRIME A

CADEMY

PRIME/43rd /FINAL 7

(b)

Part (i) Details Acquirer (M) Target (N)

(a) Earnings After Tax 8,000,000 2,400,000 (b) Number of Shares 1,600,000 400,000

(c) Market Price 200 160 (d) Earnings Per Share [(a) / (b)] 5 6

(e) PEM (a / d) 40.00 26.67

Part (ii) Post Merger EPS XYZ ABC Combined

(a) Earnings After Tax 8,000,000 2,400,000 10,400,000 (b) Number of Shares 1,600,000 320,000 1,920,000

(c) Earnings Per Share [(a) / (b)] 5.42

Part (iii): New EPS/Adjusted EPS 5.42 4.336 Old EPS 5 6

Gain/Loss GAIN LOSS

Part (iv): The exchange ratio to ensure that EPS stays in tact is the ratio of EPS namely 6:5

5. a)

Step 1: Computation of Ko 54L / (Ko-9%) = 1800 L Hence Ko = 12%

Step 2: Computation of BV weights

Source BV Weight Cost Wt x Cost Equity S 20% 0.2 S Debt 1-S 10% 0.1 - 0.1S

Total 1 0.12

Hence, 0.2S + 0.10 - 0.1S = 0.12

Or, 0.1S = 0.02 Or, S=0.2

Hence weight of Equity is 0.2 and that of Debt is 0.8

Step 3: Computation of WACC based on MV weights

Source BV MV WT Cost WtxCost

Equity 0.2 0.6 0.454545455 20% 0.0909 MV thrice BV Debt 0.8 0.72 0.545454545 10% 0.0545 MV is 0.9 BV

1.32 0.1454

Step 4: Revised value of the firm 54L / (0.1454-0.09) = 972.97.

PRIME A

CADEMY

PRIME/43rd /FINAL 8

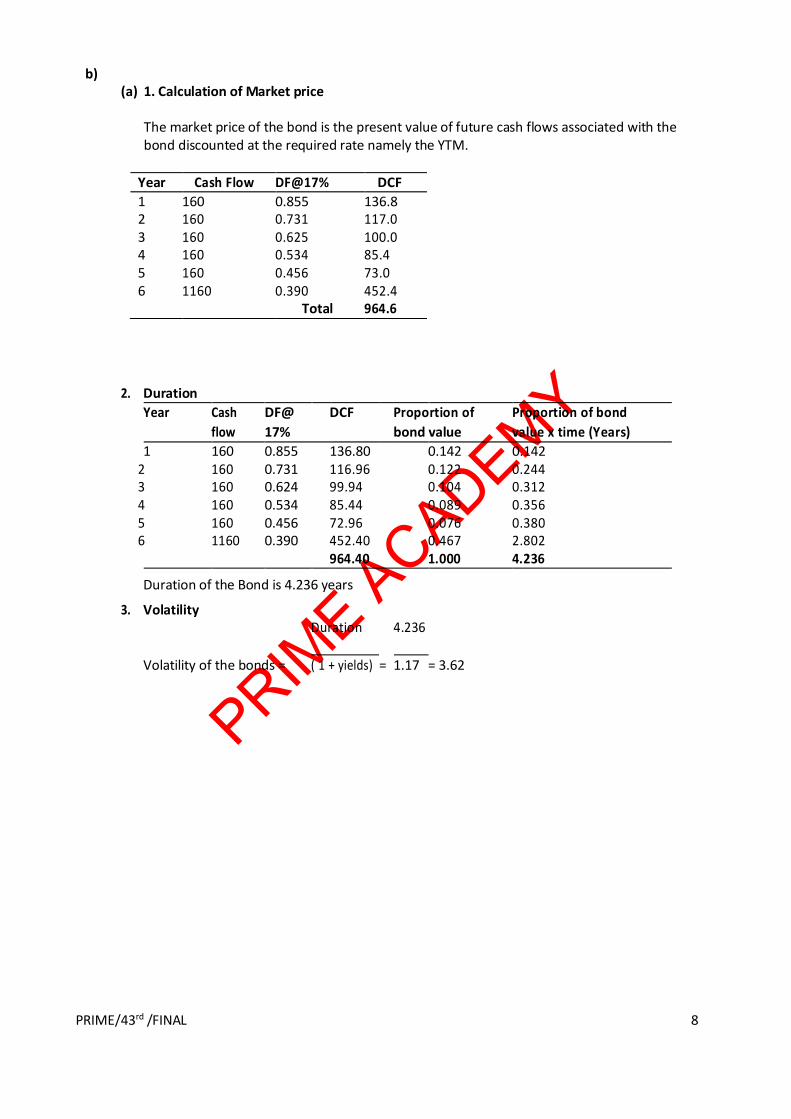

b) (a) 1. Calculation of Market price

The market price of the bond is the present value of future cash flows associated with the bond discounted at the required rate namely the YTM.

Year Cash Flow DF@17% DCF

1 160 0.855 136.8 2 160 0.731 117.0 3 160 0.625 100.0 4 160 0.534 85.4 5 160 0.456 73.0 6 1160 0.390 452.4

Total 964.6

2. Duration

Year Cash DF@ DCF Proportion of Proportion of bond

flow 17% bond value value x time (Years)

1 160 0.855 136.80 0.142 0.142 2 160 0.731 116.96 0.122 0.244 3 160 0.624 99.94 0.104 0.312 4 160 0.534 85.44 0.089 0.356 5 160 0.456 72.96 0.076 0.380 6 1160 0.390 452.40 0.467 2.802 964.40 1.000 4.236

Duration of the Bond is 4.236 years

3. Volatility Duration 4.236

Volatility of the bonds = = 3.62

=

( 1 + yields) 1.17

PRIME A

CADEMY

PRIME/43rd /FINAL 9

The expected market price if increase in required yield is by 75 basis points.

Price will fall by Rs. 960.26 × 0.75 (3.62/100) = Rs. 26.07 New Market Price Rs. 960.26 – Rs. 26.07 = Rs. 934.19

6. (a)

(i) Beta of the Portfolio

Security MP No. of Shares Total Inv. Weights Beta Wt. Beta

A 29.40 400 11760 0.01 0.59 0.006977123 B 318.70 800 254960 0.26 1.32 0.338425461 C 660.20 150 99030 0.10 0.87 0.086636935 D 5.20 300 1560 0.00 0.35 0.000549047 E 281.90 400 112760 0.11 1.16 0.1315316 F 275.40 750 206550 0.21 1.24 0.25755141 G 514.60 300 154380 0.16 1.05 0.16300367

H 170.50 900 153450 0.15 0.76 0.117272864

994450 1.10

(ii) Theoretical value of futures contract

Theoretical Value = Current Value x ert For May =

8500 x e0.20 x 2/12

= 8500 x e0.03 = 8758.825 For June = 8500 x e0.20 x 3/12

= 8500 x e0.05 = 8935.795

(iii) Computation of number of Contracts to be hedged:

Value Requiring hedging x Hedge Ratio x Beta –––––––––––––––––––––––––––––––––––– Nifty Value x Multiplier

Full Hedge : 994450 x 100% x 1.10

= 4.94 Contracts

––––––––––––––––– 8850 x 25

50% Hedge : 994450 x 50% x 1.10 ––––––––––––––––– = 2.47Contracts

8850 x 25

120% Hedge : 994450 x 120% x 1.10

= 5.93 Contracts

–––––––––––––––––

8850 x 25

PRIME A

CADEMY

PRIME/43rd /FINAL 10

(b)

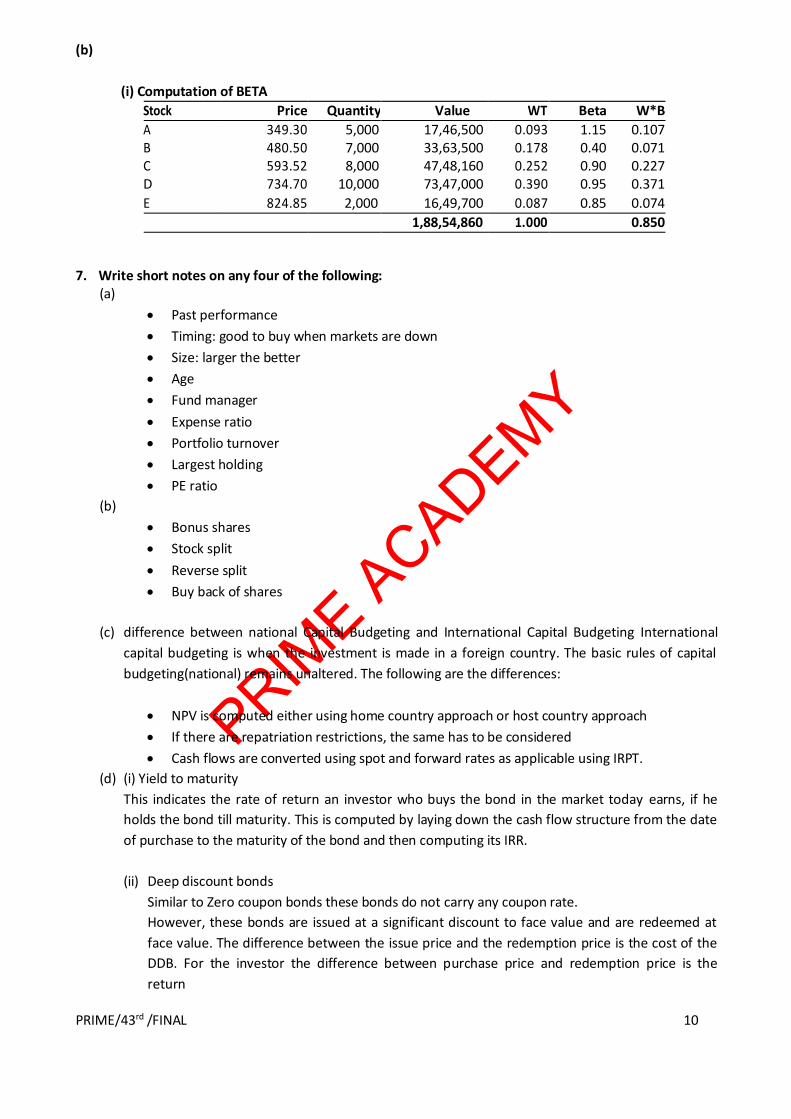

(i) Computation of BETA

Stock Price Quantity Value WT Beta W*B

A 349.30 5,000 17,46,500 0.093 1.15 0.107 B 480.50 7,000 33,63,500 0.178 0.40 0.071 C 593.52 8,000 47,48,160 0.252 0.90 0.227 D 734.70 10,000 73,47,000 0.390 0.95 0.371

E 824.85 2,000 16,49,700 0.087 0.85 0.074

1,88,54,860 1.000 0.850

7. Write short notes on any four of the following:

(a)

Past performance

Timing: good to buy when markets are down

Size: larger the better

Age

Fund manager

Expense ratio

Portfolio turnover

Largest holding

PE ratio

(b)

Bonus shares

Stock split

Reverse split

Buy back of shares

(c) difference between national Capital Budgeting and International Capital Budgeting International

capital budgeting is when the investment is made in a foreign country. The basic rules of capital

budgeting(national) remains unaltered. The following are the differences:

NPV is computed either using home country approach or host country approach

If there are repatriation restrictions, the same has to be considered

Cash flows are converted using spot and forward rates as applicable using IRPT.

(d) (i) Yield to maturity

This indicates the rate of return an investor who buys the bond in the market today earns, if he

holds the bond till maturity. This is computed by laying down the cash flow structure from the date

of purchase to the maturity of the bond and then computing its IRR.

(ii) Deep discount bonds

Similar to Zero coupon bonds these bonds do not carry any coupon rate.

However, these bonds are issued at a significant discount to face value and are redeemed at

face value. The difference between the issue price and the redemption price is the cost of the

DDB. For the investor the difference between purchase price and redemption price is the

return

PRIME A

CADEMY

PRI

ME

/43r

d

/FI

NA

L 11

PRIME A

CADEMY

PRIME/43rd /FINAL 1

The Society of Auditors and Prime Academy Model Exam – FINAL - Sep 2016

Advanced Auditing and Professional Ethics No. of Questions: 7 Total Marks: 100 No. of Pages: 2 Time Allowed: 3 hrs

Question 1 is Compulsory

Answers any Five Questions from the rest 1.

a) You are the Statutory auditor of XYZ Ltd. In the month of May 2016 due to earth quake the inventory worth 50 Lakhs was lying in the warehouse was totally destroyed. The financial statements of the company had not been adopted till the date of the earth quake. The management of the company argues that since the loss occurred in the year 2016-17, no provision for the loss needs to be made in the financial statements of 2015-16. Comment as Statutory Auditor. (5 marks)

b) As the Team leader for the audit of a closely held public limited company, you have been asked by the Engagement Partner, to report on the existence of related party transactions. What are records, documents and other possible sources of informations which you would ask your team to inspect and check. (5 marks)

c) Mr.Kannan is a freshly qualified Chartered Accountant of the May 2016 batch, who has started practice. He has been appointed as the statutory auditor of a private limited company for the first time. What are the audit techniques that he would have adopted apart from the conventional audit procedures such as posting, casting, vouching. (5 marks)

d) As the auditor of a large multi locational company, during the planning process how would you identify the inherent risk at the account balance and class of transaction level. (5 marks)

2.

a) A mid sized pharma company having a turnover of Rs.75 crores has developed an ERP tailor made to meet its requirements. All transaction are processed and the final accounts are generated through the system.The management is of the view that the books need not be printed and audit can be conducted on the computer. The ERP has a module for query based reports. As a statutory auditor enumerate the procedures you would adopt to conduct the audit. (6 marks)

b) As a tax auditor, which are the accounting ratios required to be mentioned in the report in case of manufacturing entities? Explain in detail any one of the above ratios and how does it help the tax auditor in his analytical review. (5 marks)

c) Write a short note on Corporate Governance. ( 5 marks)

3. a) Describe the procedure for verification of the following balances appearing in the account books

of a bank: i. Drafts paid without advice ii. Branch adjustment account (6 Marks)

b) Write a short note on True and Fair Cost of Production. (5 marks) c) “Surprise Checks” help the auditors to ascertain whether the Internal control system is operating

effectively in a company or not.” Discuss. (5 marks)

4. a) During the audit of Airwave Telecom Ltd., you come across a report of the Internal auditor of a

fraud involving agents and the management to the tune of 5 Crores. This report was not shared with you, but you came across the report in one of the files which was made available for audit.

PRIME A

CADEMY

PRIME/43rd /FINAL 2

With reference to the companies Act 2013, what will be your approach and how will you report the fraud. (6 marks)

b) Comment on the following situation: The Board of Directors of Polite Ltd. made an aggregate of online contribution of ` 37.5 lakhs to a National Defense Fund for the financial year ending on31st March, 2015. All the contribution of the fund is used for the welfare of the members of the Armed Forces and their dependents. The average net profit of the company during the three immediately preceding financial years was ` 476 lakhs. The manager of the company is of the view that the maximum contribution that can be made to a National Defense Fund is ` 35.7 lakhs and, therefore, the company is violating the provisions of the Companies Act, 2013. (6 marks)

c) While doing the audit of consolidated financial statements, which current period adjustments are

to be taken into account. (4 marks)

5. a) Ever Bright Batteries Ltd., having turnover of 500 Crores, has appointed M/s ABC as the sole

statutory auditors for 2016-17. Till last year, M/s DEF were also one of the joint auditors along with M/s ABC. Mention the steps that should be taken by M/s ABC before commencing the audit. (4 marks)

b) As auditor of Go Slow Ltd. What steps will you take to ensure that the dividend has been paid only out of profits. (4 marks)

c) The Managing Director of X Ltd is concerned about the high attrition rate in his company. As the Internal auditor he requests you to analyse the causes for the same. What factor would you consider in such analysis. (4 marks)

d) What are the liabilities of the auditor u/s 35 of the Companies Act 2013, for making an untrue statement in the report (as an expert forming a part of the prospectus) (4 marks)

6. Comment on the following with reference to the ca act 1949 and the schedules thereto:

a) M/s QRS, a firm in practice, develops a website qrs.com. The color chosen for the website is a very bright yellow and the web site was to run on a “push” technology where the names of the partners of the firm and the major clients were to be displayed on the web site. (4 marks)

b) Rahul Junior cleared the CA final in November 2015 and started practice in December 2015. Rahul was able to set up a flourishing practice by sheer hard work. In August 2016 he got an offer to join Ta start up as a CFO with a monthly salary of Rs. 1lakh. He accepted the offer and converted his practice into a partnership firm by taking a Fresh CA as his partner. Rahul neither intimated the Institute nor obtained permission from the Institute for his employment. Will Rahul be held guilty under the CA ACT?

c) Priya a Chartered Accountant has sent letters under certificate of posting to the previous auditor informing him her appointment as an auditor before the commencement of audit by . Is she guilty of professional misconduct? Give your views with reasons in brief.

d) Mr. Annamalai a Chartered Accountant certified the financial statements of a company in which his wife is a Director holding substantial interest.

7. Write short notes on any 4 of the following:

a) Powers and duties of an auditor of a Multi State Cooperative society. b) Reporting on the Compliance engagement c) Classification of frauds by NBFC d) Scope of peer review e) Hap hazard Sampling (4 x 4 = 16 Marks)