acc3200 job order costing. learning objectives describe the key differences between job order...

TRANSCRIPT

ACC3200Job Order Costing

Learning ObjectivesDescribe the key differences between job order costing and

process costing.

Describe the source documents used to track direct material and indirect labor costs to the job cost sheet.

Calculate a predetermined overhead rate and use it to apply manufacturing overhead cost to jobs.

Describe how costs flow through the accounting system in job order costing.

Calculate the cost of goods manufactured and cost of goods sold.

Job Order versus Process Costing

Description Job Order Costing Process CostingType of product

Unique products and services, such as a custom-built ship.

Homogeneous products and services, such as cans of soda

Manufacturing approach

Customized to the needs of the customer or client

Mass-production of products in series of standardized processes

Cost accumulation

Costs accumulated by job or customer

Costs accumulated by process

Major cost report

Job cost sheet for each unique unit, customer, or job

Production report for each major production process

Job Order Costing versus Process Costing

2-3

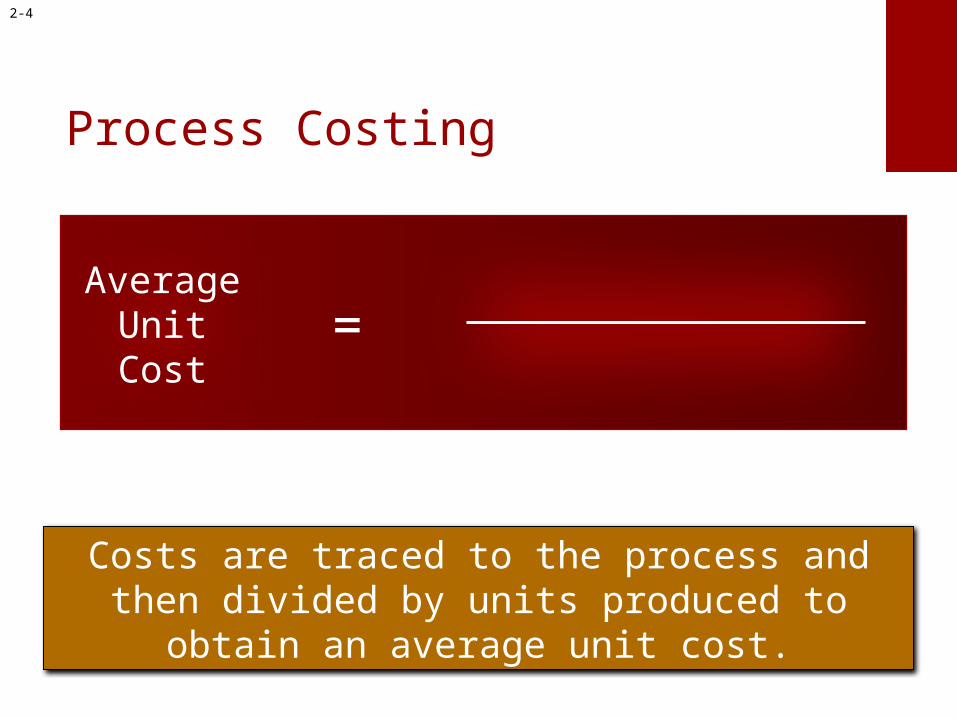

Process Costing

Costs are traced to the process and then divided by units produced to obtain an average unit cost.

AverageUnitCost

=

2-4

Manufacturing Cost Categories

2-5

Assignment of Manufacturing Costs to Jobs

2-6

Materials Requisition Form

Materials Requisition Number: MR #5236 Date 8/11/2008Job Number #2719Description: Simpson Home, Lot #79, Cambridge Subdivision

Material Description Quantity Unit Cost Total Cost2 X 6 Exterior Studs 6,362 board ft. 0.50$ 3,181$ 2 X 6 Double Plate 2,600 board ft. 0.49 1,274 2 X 6 Pressure Treated 450 board ft. 0.68 306 2 X 4 Interior Studs 5,400 board ft. 0.21 1,134 2 X 4 Pressure Treated 300 board ft. 0.35 105 Total Cost 6,000$

Authorized Signature

2-7

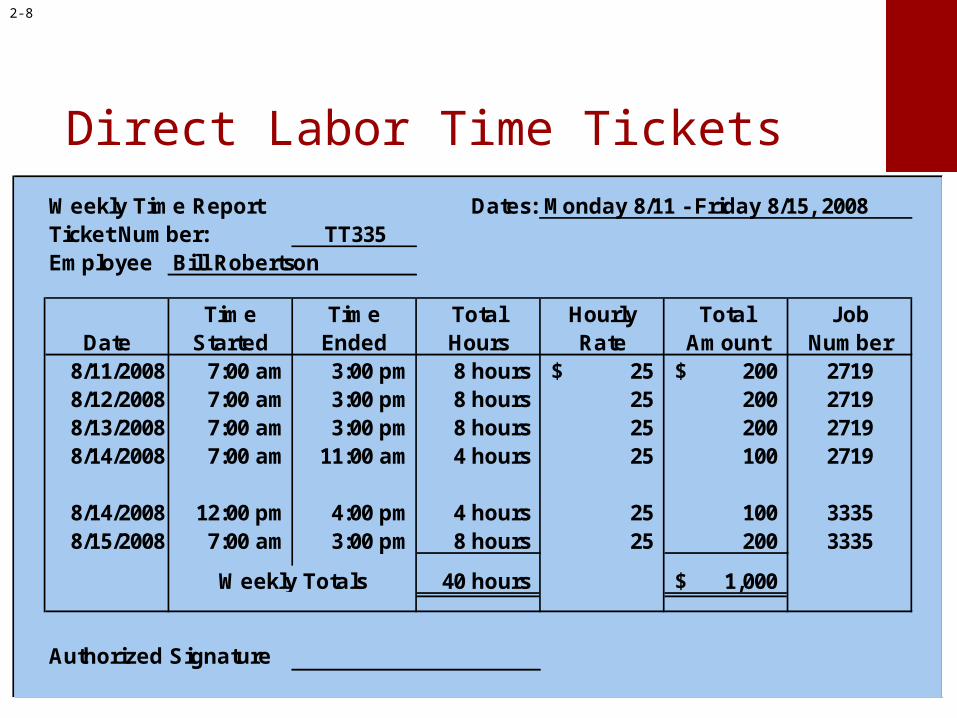

Direct Labor Time TicketsWeekly Time Report Dates: Monday 8/11 - Friday 8/15, 2008Ticket Number: TT335Employee Bill Robertson

Time Time Total Hourly Total JobDate Started Ended Hours Rate Amount Number

8/11/2008 7:00 am 3:00 pm 8 hours 25$ 200$ 27198/12/2008 7:00 am 3:00 pm 8 hours 25 200 27198/13/2008 7:00 am 3:00 pm 8 hours 25 200 27198/14/2008 7:00 am 11:00 am 4 hours 25 100 2719

8/14/2008 12:00 pm 4:00 pm 4 hours 25 100 33358/15/2008 7:00 am 3:00 pm 8 hours 25 200 3335

40 hours 1,000$

Authorized Signature

Weekly Totals

2-8

Job Cost Sheet

Job Number #2719Date Started: 7/12/2008Date Completed:Description: Simpson Home, Lot #79, Cambridge Subdivision

AppliedDirect Materials Direct Labor Manufacturing Overhead

Req. No. Amount Ticket Hours AmountMR #5236 6,000$ TT335 300 700$

2-9

Manufacturing overhead is applied to jobs that are in process. An allocation base, such as direct labor

hours, direct labor dollars, or machine hours, is used to assign manufacturing overhead to individual jobs.

Manufacturing overhead is applied to jobs that are in process. An allocation base, such as direct labor

hours, direct labor dollars, or machine hours, is used to assign manufacturing overhead to individual jobs.

We use an allocation base to apply manufacturing overhead because:

1. It is impossible or difficult to trace overhead costs to particular jobs.

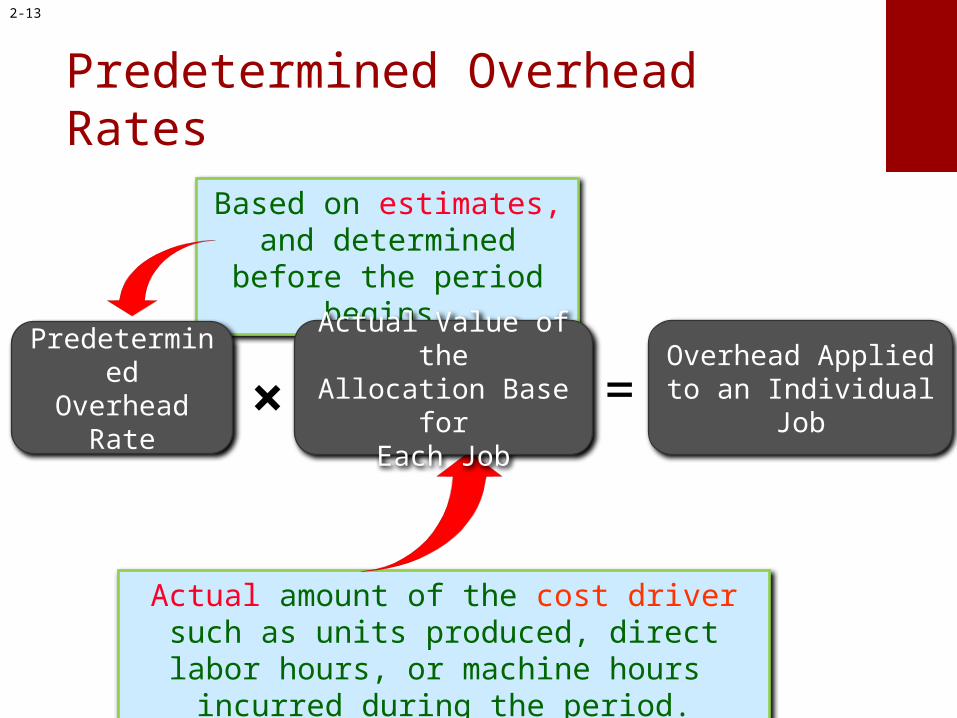

Predetermined Overhead Rates

2-10

Predetermined Overhead Rates

The predetermined overhead rate (POHR) used to apply overhead to jobs is determined

before the period begins using estimates.

PredeterminedOverhead

Rate

Ideally, the allocation base is a cost driver that causes overhead.

=

2-11

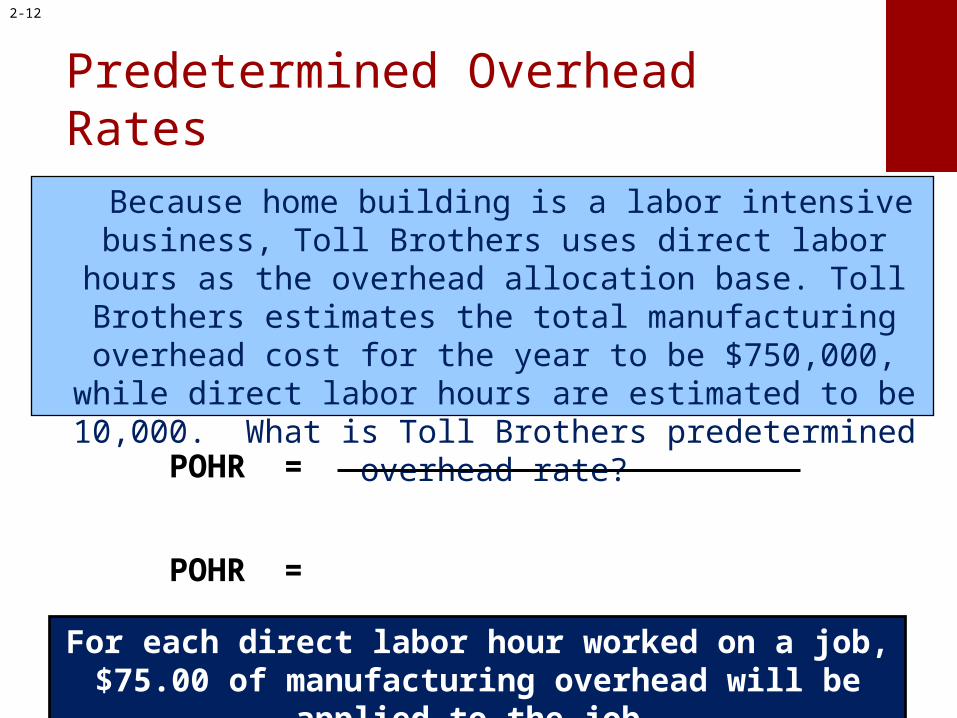

Predetermined Overhead Rates

Because home building is a labor intensive business, Toll Brothers uses direct labor hours as the overhead allocation

base. Toll Brothers estimates the total manufacturing overhead cost for the year to be $750,000, while direct labor

hours are estimated to be 10,000. What is Toll Brothers predetermined overhead rate?

For each direct labor hour worked on a job, $75.00 of manufacturing overhead will be applied to the job.

POHR =

POHR =

2-12

Actual amount of the cost driver such as units produced, direct labor hours, or machine

hours incurred during the period.

Based on estimates, and determined before the

period begins.

Predetermined Overhead Rates

=× Overhead Applied

to an Individual Job

PredeterminedOverhead

Rate

Actual Value of theAllocation Base for

Each Job

2-13

Job Number #2719Date Started: 7/12/2008Date Completed:Description: Simpson Home, Lot #79, Cambridge Subdivision

AppliedDirect Materials Direct Labor Manufacturing Overhead

Req. No. Amount Ticket Hours Amount Hours Rate AmountMR #3345 8,000$ TT335 28 700$ 28 75$ 2,100$ MR #3372 6,000 TT340 90 2,250 90 75 6,750 MR #4251 4,500 TT385 90 2,250 90 75 6,750 MR #4827 5,500 TT425 52 1,300 52 75 3,900 MR #5236 6,000 TT445 40 1,000 40 75 3,000

30,000$ 300 7,500$ 300 75 22,500$

Predetermined Overhead RatesOverheadApplied

to Job #2719

PredeterminedOverhead

Rate =Actual Direct Labor

Hours for Job #2719×

2-14

Job Number #2719Date Started: 7/12/2008Date Completed:Description: Simpson Home, Lot #79, Cambridge Subdivision

AppliedDirect Materials Direct Labor Manufacturing Overhead

Req. No. Amount Ticket Hours Amount Hours Rate AmountMR #3345 8,000$ TT335 28 700$ 28 75$ 2,100$ MR #3372 6,000 TT340 90 2,250 90 75 6,750 MR #4251 4,500 TT385 90 2,250 90 75 6,750 MR #4827 5,500 TT425 52 1,300 52 75 3,900 MR #5236 6,000 TT445 40 1,000 40 75 3,000

30,000$ 300 7,500$ 300 75 22,500$

Direct Materials Cost 30,000$ Direct Labor Cost 7,500 Applied Manufacturing Overhead 22,500 Total cost 60,000$

Cost Summary

Predetermined Overhead Rates

2-15

Recording the Flow of Costs in Job Order Costing

2-16

Purchases 150,000 Issued to production 150,000Raw Materials Inventory

10,000 Manufacturing Overhead 140,000

Work in Process Inventory

Recording the Purchase and Issue of Materials

Toll Brothers purchased $150,000 in raw materials on account. Toll Brothers withdraws $150,000 worth of materials from

inventory, $100,000 for Job #2719 (Simpson home), $40,000 for Job #3335 (Flintstone Home) and $10,000 for supplies.

2-17

Recording Labor Costs

Toll Brothers incurs $55,000 in labor costs, $30,000 for Job #2719 (Simpson home), $20,000 for Job

#3335 (Flintstone Home) and $5,000 for indirect labor.

5,000 Manufacturing Overhead

50,000 Work in Process Inventory

2-18

Recording Actual Manufacturing Overhead

In addition to indirect materials and indirect labor, Toll Brothers incurs other manufacturing overhead costs including:• Salary paid to construction site supervisor, $12,000.• Salary owed to a construction engineer, $8,000.• Property taxes owed but not yet paid, $6,000.• Expired insurance premium for construction, $4,000.• Depreciation on construction equipment, $18,000.

Actual AppliedIndirect materials 10,000Indirect labor 5,000

Manufacturing Overhead

2-19

Recording Applied Manufacturing Overhead

Toll Brothers applies manufacturing overhead to jobs using a predetermined overhead rate of $75 per direct labor

hour. Time tickets for the month show a total of 800 direct labor hours, 600 hours for Job #2719 (Simpson home) and

200 hours for Job #3335 (Flintstone Home).

Direct Overhead AppliedJob # Labor Hrs Rate Overhead

Simpson home 2719 600 75$ 45,000$ Flintstone home 3335 200 75 15,000 Total direct labor hours 800 60,000$

2-20

Recording Actual and Applied Manufacturing Overhead

The difference is closed to cost of goods sold.

Actual Applied MOH MOH =/

Actual AppliedIndirect materials 10,000 Applied OH 60,000Indirect labor 5,000Supervisor salary 12,000Engineer salary 8,000Property taxes 6,000Insurance expense 4,000Depreciation 18,000

Manufacturing Overhead

60,000 Work in Process Inventory

2-21

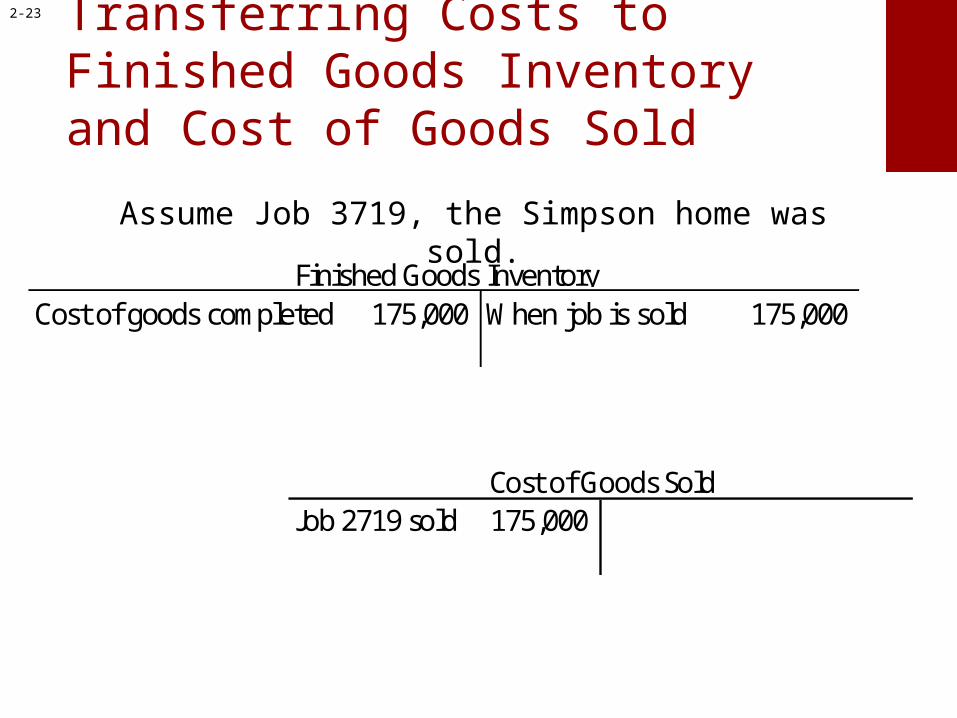

Transferring Costs to Finished Goods Inventory and Cost of Goods Sold

Job Number #2719Date Started: 7/12/2008Date Completed:Description: Simpson Home, Lot #79, Cambridge Subdivision

Direct Materials Cost 100,000$ Direct Labor Cost 30,000 Applied Manufacturing Overhead 45,000 Total cost 175,000$

Cost Summary

Summary section of job cost sheet for

Job #2719 after all costs are

updated.

Direct material 140,000 Job 2719 completed 175,000 Direct labor 50,000 Applied MOH 60,000 Balance 75,000

Work in Process Inventory

Cost of goods completed 175,000 Finished Goods Inventory

2-22

Transferring Costs to Finished Goods Inventory and Cost of Goods Sold

Cost of goods completed 175,000 When job is sold 175,000 Finished Goods Inventory

Job 2719 sold 175,000 Cost of Goods Sold

Assume Job 3719, the Simpson home was sold.

2-23

Recording Nonmanufacturing CostsIn addition to manufacturing costs, Toll Brothersincurs non-manufacturing overhead costs.1. Commissions to sales agent, $20,000.2. Advertising expense, $5,000.3. Depreciation on office equipment, $6,000.4. Other selling and administrative expenses, $4,000.

These non-manufacturing costs would be recorded in individual expense accounts, including

commission expense, advertising expense, depreciation expense, and other expenses. The total of the selling and administrative expense would be subtracted from gross margin on the

income statement.

2-24

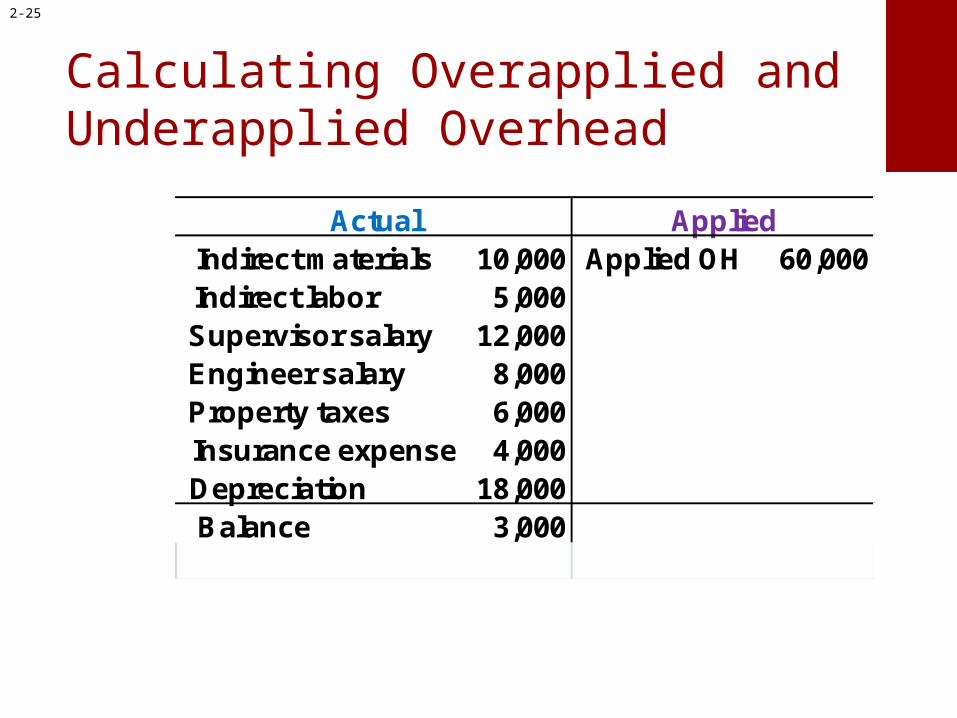

Calculating Overapplied andUnderapplied Overhead

Actual AppliedIndirect materials 10,000 Applied OH 60,000Indirect labor 5,000Supervisor salary 12,000Engineer salary 8,000Property taxes 6,000Insurance expense 4,000Depreciation 18,000Balance 3,000

2-25

Disposing of Overapplied and Underapplied Overhead

The most common method for disposing of the balance in Manufacturing Overhead is to make

a direct adjustment to Cost of Goods Sold.

OverappliedManufacturing

Overhead(credit balance)

UnderappliedManufacturing

Overhead(debit balance)

DecreasesCost of Goods

Sold

IncreasesCost of Goods

Sold

2-26

Summary of Recorded Manufacturing and Nonmanufacturing Costs

2-27

Cost of Goods Manufactured Report

Beginning raw materials inventory -$ Plus: Raw material purchases 150,000 Less: Indirect materials (10,000) Less: Ending raw materials inventory - Direct materials used 140,000 Direct labor 50,000 Manufacturing overhead applied 60,000 Total current manufacturing costs 250,000 Plus: Beginning work in process inventory - Less: Ending work in process inventory (75,000) Cost of goods manufactured 175,000

Toll BrothersCost of Goods Manufactured Report

2-28

Cost of Goods Manufactured Report

Sales revenue 275,000$ Cost of goods sold Beginning finished goods inventory -$ Plus: Cost of goods manufactured 175,000 Less: Ending finished goods inventory - Unadjusted cost of goods sold 175,000 Plus: Underapplied manufacturing overhead 3,000 178,000 Gross profit 97,000 Selling and administrative expenses 35,000 Net income from operations 62,000$

Toll BrothersIncome Statement

2-29

SupplementJournal Entries for Job Order Costing

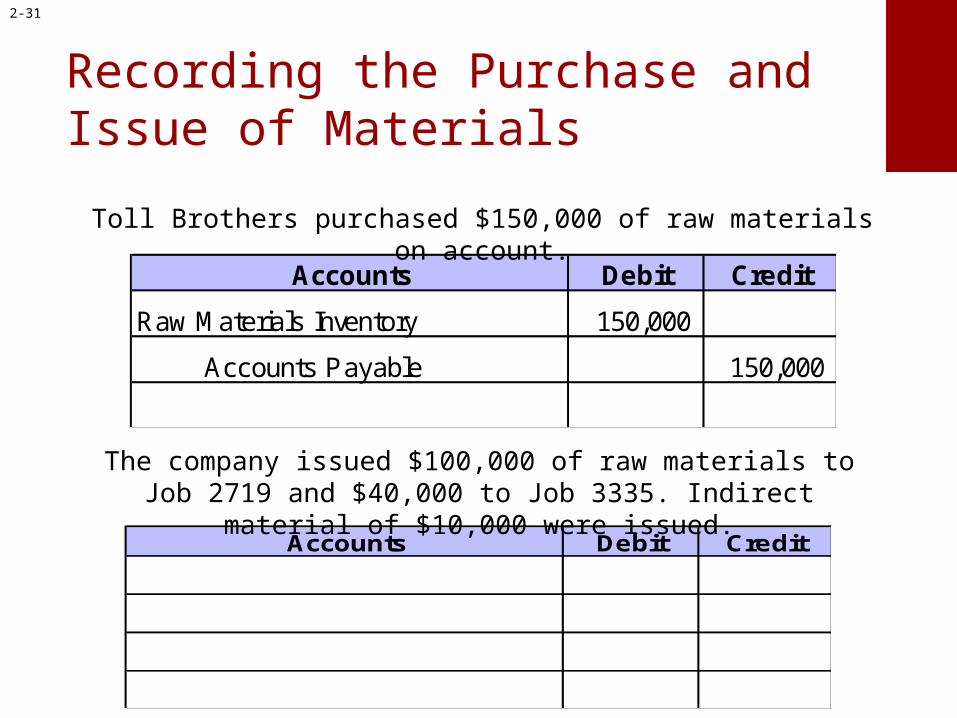

Recording the Purchase and Issue of Materials

Debit Credit

Raw Materials Inventory 150,000

Accounts Payable 150,000

Accounts

Debit CreditAccounts

Toll Brothers purchased $150,000 of raw materials on account.

The company issued $100,000 of raw materials to Job 2719 and $40,000 to Job 3335. Indirect material of $10,000 were issued.

2-31

Recording Labor Costs

Debit CreditAccounts

Direct labor on Job 2719 30,000$ Direct labor on Job 3335 20,000 Indirect labor 5,000 Total 55,000$

The following labor costs were incurred during the period.

2-32

Recording Actual Manufacturing Overhead

The following overhead costs were incurred during the period.

Actual AppliedSupervisor salary 12,000Engineer salary 8,000Property taxes 6,000Insurance expense 4,000Depreciation 18,000

Manufacturing Overhead

Debit CreditAccounts

2-33

Recording Applied Manufacturing Overhead

Here is how we applied overhead during the period.Direct Overhead Applied

Job # Labor Hrs Rate OverheadSimpson home 2719 600 75$ 45,000$ Flintstone home 3335 200 75 15,000 Total direct labor hours 800 60,000$

Debit CreditAccounts

2-34

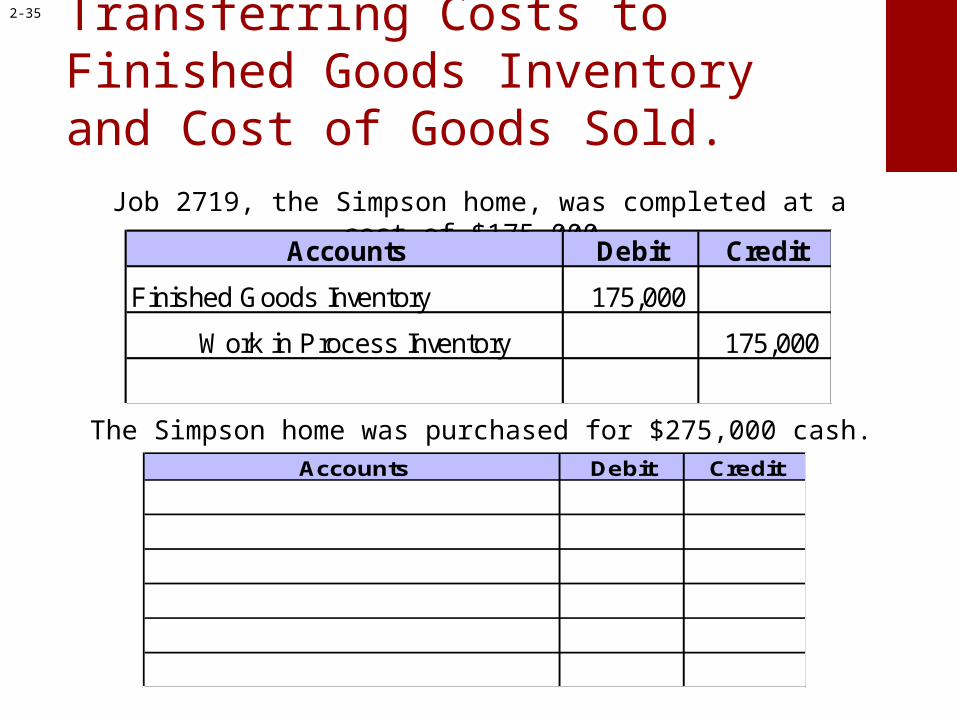

Transferring Costs to Finished Goods Inventory and Cost of Goods Sold.Job 2719, the Simpson home, was completed at a cost of $175,000.

Debit Credit

Finished Goods Inventory 175,000

Work in Process Inventory 175,000

Accounts

The Simpson home was purchased for $275,000 cash.Debit CreditAccounts

2-35

Recording Nonmanufacturing Costs

Debit Credit

Commission Expense 20,000

Commissions Payable 20,000

Advertising Expense 5,000

Prepaid Advertising 5,000

Accounts

Toll Brothers incurs non-manufacturing overhead costs.1. Commissions to sales agent, $20,000.2. Advertising expense, $5,000.3. Depreciation on office equipment, $6,000.4. Other selling and administrative expenses, $4,000.

Debit CreditAccounts

2-36

Overapplied or Underapplied Manufacturing Overhead

At the end of the period, Toll Brothers has a $3,000 debit balance in the Manufacturing Overhead account (underapplied overhead).

Debit CreditAccounts

2-37

End of Topic 5