accelerate your business through search & native innovation

TRANSCRIPT

CO

PY

RIG

HT

© Y

AH

OO

2017

CO

PY

RIG

HT

© Y

AH

OO

2016

CO

PY

RIG

HT

© Y

AH

OO

2017

BRIAN HEDRICKDIRECTOR, PERFORMANCE STRATEGY

ACCELERATE YOUR BUSINESS THROUGH SEARCH & NATIVE INNOVATION

1

CO

PY

RIG

HT

© Y

AH

OO

2017

CO

PY

RIG

HT

© Y

AH

OO

2017

2

Today’s presentation contains information that is confidential and proprietary to Yahoo

CONFIDENTIALITY & PRIVACY

All confidential information being shared today is subject

to terms and conditions of your non-disclosure agreement

(or other agreement that contains confidentiality

provisions) with Yahoo.

As a recognized leader in developing privacy-enhancing

tools for consumers and a member of the NAI and DAA,

Yahoo understands the importance of consumer trust and

privacy.

Yahoo and its partners provide transparency about our

data collection and use practices and extend several tools

to empower consumers to manage their experience. We

are also now among the first in the world to support Do

Not Track.

CO

PY

RIG

HT

© Y

AH

OO

2017

CO

PY

RIG

HT

© Y

AH

OO

2017

THE STATE OF MEDIA

3

CO

PY

RIG

HT

© Y

AH

OO

2017

CONTENT CONSUMPTION IS EVOLVING. DIGITAL DOMINATES TIME SPENT, BUT SMARTPHONES ALONE WILL BEGIN TO THREATEN TV’S PREVIOUS DOMINANCE

4

4:31 4:11 4:01

2:162:12 2:08

2:15 2:54 3:17

2013 2015 2017

AVG. TIME SPENT PER DAY IN (HOURS:MINS)

Source: eMarketer, September 2016

Smartphon

ePC

TV

Decline: -12%▼

Decline: -4%▼

Growth: +47%▲

CO

PY

RIG

HT

© Y

AH

OO

2017

TRADITIONAL TV WATCHING STILL PEAKS DURING PRIME TIME

6AM - 9AM 9AM – 12PM 12PM – 3PM 3PM – 6PM 6PM – 9PM 9PM – 12AM 12AM – 3AM 3AM – 6AM

% O

F T

V V

IEW

ER

SH

IP

Prime time

peak

8-9PM

Source: TV viewing levels for YTD, P13+, Nielsen, September 2015

W E E K D A Y

W E E K E N D

WEEKDAY VS. WEEKEND | TV RATINGS BY HOUR

5

CO

PY

RIG

HT

© Y

AH

OO

2017

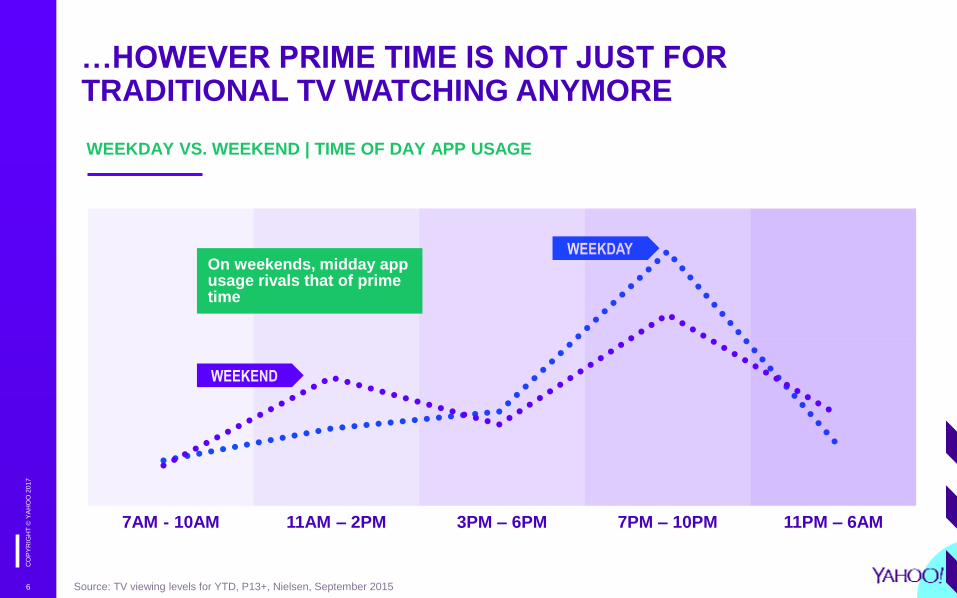

…HOWEVER PRIME TIME IS NOT JUST FOR TRADITIONAL TV WATCHING ANYMORE

Source: TV viewing levels for YTD, P13+, Nielsen, September 2015

WEEKDAY VS. WEEKEND | TIME OF DAY APP USAGE

% O

F T

OT

AL

AP

P S

ES

SIO

NS

WEEKDAY

WEEKEND

7AM - 10AM 11AM – 2PM 3PM – 6PM 7PM – 10PM 11PM – 6AM

On weekends, midday app usage rivals that of prime time

6

CO

PY

RIG

HT

© Y

AH

OO

2017

58%24%

16%2%

FULL

SAMPLE 55%

24%

19%

3%

MILLENNIALS

65%

24%

10% 1%

GEN X’ERS

TV + Laptop TV +

Phone

Phone + Laptop All 3

TV + LAPTOP IS THE MOST COMMON MULTITASKING METHOD

7Source: Nielsen Biometric Day in the Life

CO

PY

RIG

HT

© Y

AH

OO

2017

UNSURPRISINGLY, WITH THE PREVALENCE OF MULTITASKING DURING PRIME TIME, DEVICE SWITCHING IS MORE FREQUENT FOR BOTH GROUPS FROM 7-10PM

8Source: Nielsen Biometric Day in the Life

G E N X ’ E R S

9.2switches per

hour

M I L L E N N I A L S

8.7switches per

hour

CO

PY

RIG

HT

© Y

AH

OO

2017

MILLENNIALS ARE CONSIDERABLY MORE PROFICIENT THAN GEN X’ERS AT MULTI-TASKING DURING PRIME TIME

9

EMOTIONAL RESPONSE TO MULTITASKING- DURING PRIME TIME

Source: Nielsen Biometric Day in the Life

Gen X’ers respond the least emotionally to multitasking during prime

time, potentially making this a difficult audience to reach and engage

emotionally for advertisers.

64

53

32

40

32 3229

N/A

Gen X’ers

Millennials

TV + Laptop TV + Phone Laptop + Phone All 3

CO

PY

RIG

HT

© Y

AH

OO

2017

ALTHOUGH TV IS THE DEVICE USED THE MOST, SMARTPHONES ACTUALLY RECEIVE THE HIGHEST AMOUNT OF “PRIMARY ATTENTION”

10

PERCENT OF TIME USING DEVICE AS THE

PRIMARY DEVICE - DURING PRIME TIME

Source: Nielsen Biometric Day in the Life

94% of the time that a Smartphone is being

touched during these hours, it is being used

as the primary device.

SM

AR

TP

HO

NE

94%

TV

83%

LA

PT

OP

80%

CO

PY

RIG

HT

© Y

AH

OO

2017

CO

PY

RIG

HT

© Y

AH

OO

2017

DIGITAL IS WINNING THE BATTLE FOR CONSUMER ATTENTION WHEN IT COMES TO ADVERTISING

11

% OF TIME CONSUMER ATTENTION DIVERTED

TO ANOTHER DEVICE WHEN AD APPEARED

57% 15%25%

Source: Nielsen Biometric Day in the Life

CO

PY

RIG

HT

© Y

AH

OO

2017

CO

PY

RIG

HT

© Y

AH

OO

2017

12

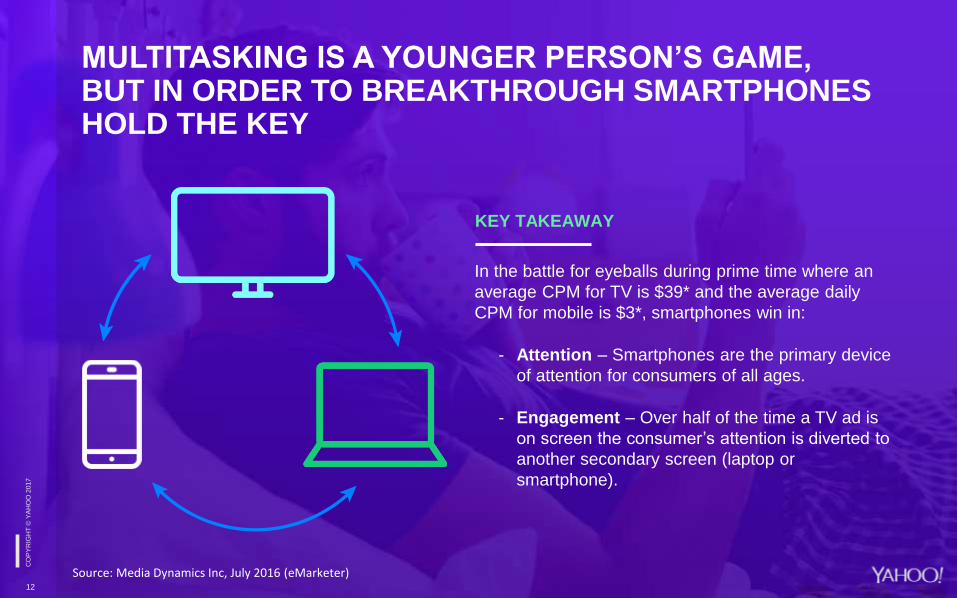

MULTITASKING IS A YOUNGER PERSON’S GAME, BUT IN ORDER TO BREAKTHROUGH SMARTPHONES HOLD THE KEY

In the battle for eyeballs during prime time where an

average CPM for TV is $39* and the average daily

CPM for mobile is $3*, smartphones win in:

- Attention – Smartphones are the primary device

of attention for consumers of all ages.

- Engagement – Over half of the time a TV ad is

on screen the consumer’s attention is diverted to

another secondary screen (laptop or

smartphone).

KEY TAKEAWAY

Source: Media Dynamics Inc, July 2016 (eMarketer)

CO

PY

RIG

HT

© Y

AH

OO

2017

MOBILE SHOPPERS WILL BE VIRTUALLY SYNONYMOUS WITH DIGITAL SHOPPERS BY 2020

13

184.4

220.2

100

200

2015 2016 2017 2018 2019 2020

US Mobile Shoppers (Millions)

88.5%

98.4%

70%

2016 2017 2018 2019 2020

US Mobile Shoppers as a Percent of

Digital Shoppers, 2016-2020

DEFINITION:

Ages 14+; mobile shoppers are internet users who have browsed,

researched or compared products digitally via any device during

the calendar year but have not necessarily bought digitally98.4%

Source: US Ecommerce Performance StatPack: Including Mobile Performance Yory Wurmser | December 23, 2016

CO

PY

RIG

HT

© Y

AH

OO

2017

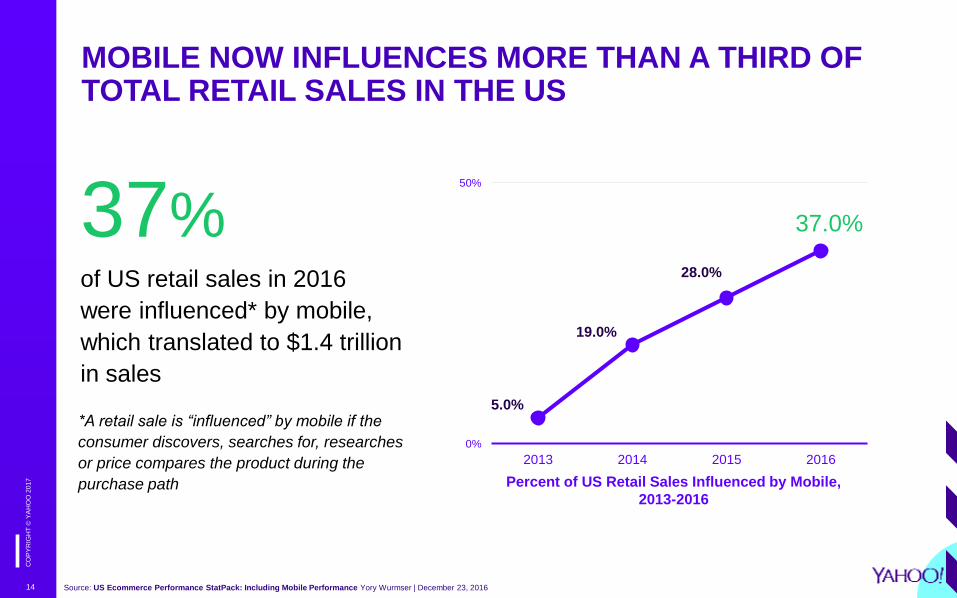

MOBILE NOW INFLUENCES MORE THAN A THIRD OF TOTAL RETAIL SALES IN THE US

14

*A retail sale is “influenced” by mobile if the

consumer discovers, searches for, researches

or price compares the product during the

purchase path

37%of US retail sales in 2016

were influenced* by mobile,

which translated to $1.4 trillion

in sales5.0%

19.0%

28.0%

[]

0%

50%

2013 2014 2015 2016

Percent of US Retail Sales Influenced by Mobile,

2013-2016

37.0%

Source: US Ecommerce Performance StatPack: Including Mobile Performance Yory Wurmser | December 23, 2016

CO

PY

RIG

HT

© Y

AH

OO

2017

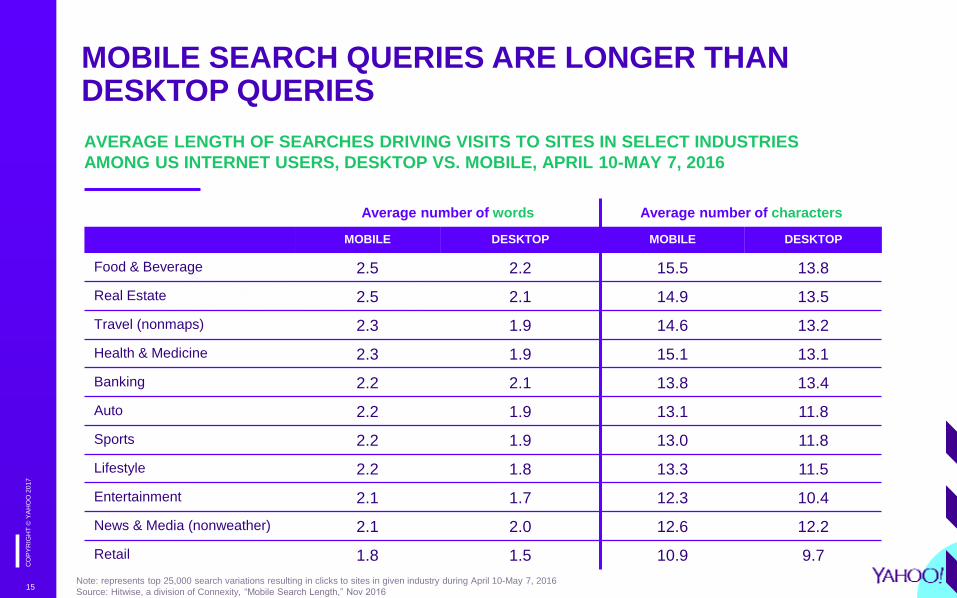

MOBILE SEARCH QUERIES ARE LONGER THAN DESKTOP QUERIES

15

AVERAGE LENGTH OF SEARCHES DRIVING VISITS TO SITES IN SELECT INDUSTRIES

AMONG US INTERNET USERS, DESKTOP VS. MOBILE, APRIL 10-MAY 7, 2016

Average number of words Average number of characters

MOBILE DESKTOP MOBILE DESKTOP

Food & Beverage 2.5 2.2 15.5 13.8

Real Estate 2.5 2.1 14.9 13.5

Travel (nonmaps) 2.3 1.9 14.6 13.2

Health & Medicine 2.3 1.9 15.1 13.1

Banking 2.2 2.1 13.8 13.4

Auto 2.2 1.9 13.1 11.8

Sports 2.2 1.9 13.0 11.8

Lifestyle 2.2 1.8 13.3 11.5

Entertainment 2.1 1.7 12.3 10.4

News & Media (nonweather) 2.1 2.0 12.6 12.2

Retail 1.8 1.5 10.9 9.7

Note: represents top 25,000 search variations resulting in clicks to sites in given industry during April 10-May 7, 2016

Source: Hitwise, a division of Connexity, “Mobile Search Length,” Nov 2016

CO

PY

RIG

HT

© Y

AH

OO

2017

ALTHOUGH MOBILE IS KEY, DESKTOP IS STILL IMPORTANT FOR CONVERSIONS

16

US RETAIL ECOMMERCE WEBSITE TRAFFIC VS. REVENUE

SHARE, BY DEVICE, Q2 2016 (% OF TOTAL)

Note: represents activity tracked by Adobe, broader industry metrics may vary

Source: Adobe, “2016 Mobile Retail Report; eMarketer calculations, Oct 25, 2016

Tablet

9%

Desktop

59%

Smartphone

32%

Traffic Share

Tablet

9%

Desktop

75%

Smartphone

16%

Revenue Share

CO

PY

RIG

HT

© Y

AH

OO

2017

THE REASON: SMARTPHONES LAG DESKTOPS AND TABLETS IN ADD-TO-CART AND CONVERSION RATES

17

US ADD-TO-CART VS TOTAL RETAIL ECOMMERCE

CONVERSION RATES, BY DEVICE, Q2 2016

Note: represents activity tracked by Adobe, broader industry metrics may vary; read as 1.0% of total smartphone

visits result in an order, while 16% of smartphone visitors who ad items to their cart make a purchase

Source: Adobe, “2016 Mobile Retail Report; eMarketer calculations, Oct 25, 2016

SMARTPHONE TABLET DESKTOP

Add-to-cart 16% 22% 26%

Total 1.0% 2.0% 2.8%

CO

PY

RIG

HT

© Y

AH

OO

2017

TECHNOLOGY

Technology to help you reach

audiences at scale both on and off

Yahoo.

DATA

The most complete set of signals

from sources including mail, search,

content, mobile app usage and

social.

CONTENT

Leading news, sports, finance and

lifestyle properties for brand building

and content marketing.

18

CO

PY

RIG

HT

© Y

AH

OO

2017

CO

PY

RIG

HT

© Y

AH

OO

2017

19

WHAT IS YAHOO GEMINI?

THE PERFORMANCE AND

RELEVANCE OF

SEARCH

+

THE EXTENSIVE SCALE

AND CREATIVITY OF

NATIVE

BUY MANAGE OPTIMIZE

CO

PY

RIG

HT

© Y

AH

OO

2017

CO

PY

RIG

HT

© Y

AH

OO

2017

20

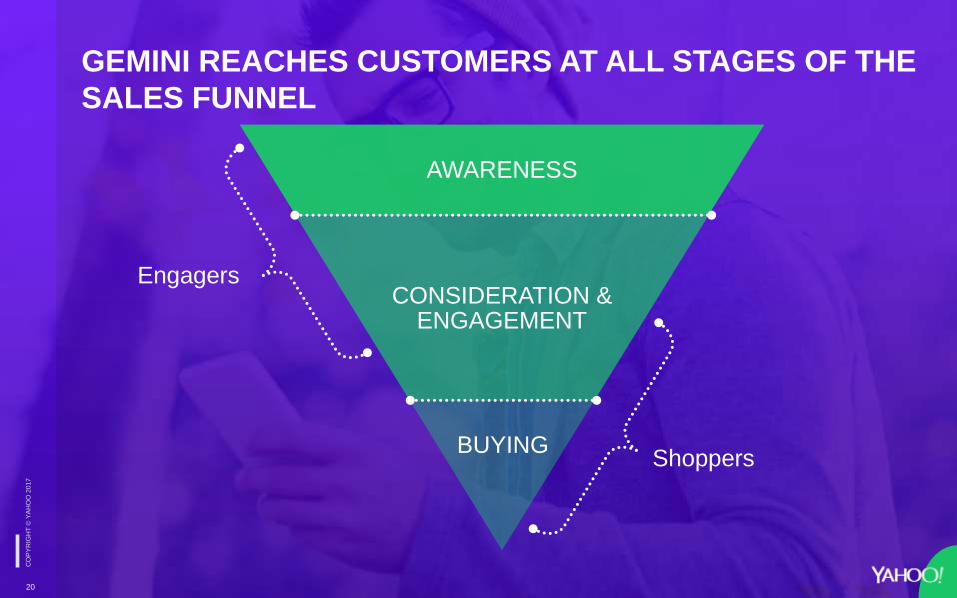

GEMINI REACHES CUSTOMERS AT ALL STAGES OF THE

SALES FUNNEL

AWARENESS

CONSIDERATION & ENGAGEMENT

BUYINGShoppers

Engagers

CO

PY

RIG

HT

© Y

AH

OO

2017

YAHOO IS CONNECTED TO CONSUMERS

AT EVERY POINT IN THEIR JOURNEY

165 BILLION DATA EVENTS

21

daily from 1 billion consumers visiting

our site each month

APPS

SEARCH

CONTENT

SOCIAL

Source: Yahoo internal data

CO

PY

RIG

HT

© Y

AH

OO

2017

22

POWERFUL DATA POINTS FOR A MORE COMPLETE

UNDERSTANDING OF YOUR AUDIENCE

LOCATION

from registration data

PREFERENCES FOR

TRAVEL, RETAIL & MORE

from email data

CROSS-DEVICE IDENTITYfrom mobile data

FAVORITE CONTENT

from web data & 720k apps

RECENT STORE VISITS

from mobile geolocation data

ON AND OFFLINE PURCHASES

from email data

PURCHASE INTENT

from search queries

PASSIONS & INTERESTS

from Tumblr

CO

PY

RIG

HT

© Y

AH

OO

2017

CO

PY

RIG

HT

© Y

AH

OO

2017

23

TARGET YOUR MOST VALUABLE AUDIENCE

WITH CUSTOM AUDIENCES

•Demographic

•Geographic

•Interest

YAHOO DATA

•Website actions

•Mobile device IDs

•Email list

•In app action

•Lookalike modeling

YOUR DATA

•Page visits

•Site visits

•Cart abandonment

SITE RETARGETING

•Custom segments

•Email lists

3rd PARTY DATA

= exclusive to

CO

PY

RIG

HT

© Y

AH

OO

2017

AMPLIFY YOUR EFFICIENCYApply Audience Targeting to Search to improve campaign efficiency

24

Advertisers in the pilot saw the

following results for their audience

targeted traffic:

CONVERSION

RATES

90%

200%CLICK THROUGH

RATES

COST PER

ACQUISTION

30%

*Audience traffic compared to non-audience trafficSource: Yahoo internal data

CO

PY

RIG

HT

© Y

AH

OO

2017

25

RETAILER TARGETS QUALIFIED CUSTOMERS,

DRIVES EFFICIENCY

CO

PY

RIG

HT

© Y

AH

OO

2017

Increase in

CTR

Increase in

Conversion Rate

Savings in

CPA

225% 51%230%

Using Custom Audience in Search a big box store grew conversions and increased efficiency*

*Results from comparison between audience targeted vs. non audience targeted traffic Source: Yahoo internal data

CO

PY

RIG

HT

© Y

AH

OO

2017

DRIVE MORE TRAFFIC WITH SEARCH ON NATIVEAdd an image to your search campaigns to maximize your impact on Yahoo Gemini. Extend

your reach and target customers that searched for your products on native supply with

Search on Native.

26

CPC

50%

CLICKS

20%

Hotels in San Francisco

Hotel DealsGreat prices in San Francisco

Source: Yahoo internal data

CO

PY

RIG

HT

© Y

AH

OO

2017

…WITH COMPREHENSIVE

MEASUREMENT TOOLS

Scalable, open and actionable

measurement to understand your

campaign impact.

…INTO ACTIONABLE

INSIGHTS & TARGETING

Turning data into insights that help

you better understand your

customers and prospects.

TURNING SUPERIOR DATA…

The most complete set of signals

from sources including mail, search,

content, mobile app usage and

social.

27

CO

PY

RIG

HT

© Y

AH

OO

2017

CO

PY

RIG

HT

© Y

AH

OO

2017

28

RECAP

PLAN FOR THE

MULTI-TASKER

LEVERAGE

DATA &

INSIGHTS TO

PLAY UP AND

DOWN THE

FUNNEL

DOUBLE DOWN

ON THE

MOBILE

EXPERIENCE

advertising.yahoo.com

CO

PY

RIG

HT

© Y

AH

OO

2017

CO

PY

RIG

HT

© Y

AH

OO

2016

CO

PY

RIG

HT

© Y

AH

OO

2017

THANK YOU

29