access to credit and women entrepreneurship: evidence … · access to credit and women...

TRANSCRIPT

M. Jahangir Alam Chowdhury University of Dhaka 1

Access to Credit and Women

Entrepreneurship: Evidence from

Bangladesh

M. Jahangir Alam Chowdhury

University of Dhaka

Dhaka, Bangladesh

M. Jahangir Alam Chowdhury University of Dhaka 2

Outline

Introduction

Research Question

Methodology

Results

Conclusion

M. Jahangir Alam Chowdhury University of Dhaka 3

Introduction

Access to capital has been recognized as one of

the factors that contribute to the higher level of

welfare of households.

The credit constraint has a gender characteristic

Women are more likely to be constrained than

men

Entrepreneurship is considered as one of the

factors that help poor people to escape poverty.

M. Jahangir Alam Chowdhury University of Dhaka 4

Introduction

The limitations of the formal financial sector and

the informal financial sector in providing financial

services, especially credit, to poor and women

encouraged various microcredit programs to evolve

in Bangladesh.

M. Jahangir Alam Chowdhury University of Dhaka 5

Introduction : Microcredit

Microcredit is instalment based small

collateral free loans for the purpose of poverty

alleviation.

Micro-credit was first initiated in 1976 in

Chittagong as part of an action research

program.

Target of the Micro-credit Summit 1997 –

reaching 100 Million of World’s Poorest

Families by 2007.

M. Jahangir Alam Chowdhury University of Dhaka 6

Introduction: Microcredit

Target of the Micro-credit Summit 2006 – Ensuring credit for 175 million of the world's poorest families, especially the women of those families, are receiving credit for self-employment and other financial and business services by the end of 2015.

Target of the Micro-credit Summit 2006 – Bringing 100 million families rise above the US$1.25 a day threshold adjusted for purchasing power parity (PPP), between 1990 and 2015.

M. Jahangir Alam Chowdhury University of Dhaka 7

Introduction : Microfinance Sector in Bangladesh

Items 2011

No of branches 17,851

No. of employees 231,098

Number of active members (in million) 33.06

Women members 93%

Number of active borrowers (in million) 27.17

Amount of Loan Outstanding (USD Million ) 3,588

Net savings of members (USD Million) 2,386

M. Jahangir Alam Chowdhury University of Dhaka 8

Research Question

Does an access to microcredit contribute to the

development of women entrepreneurship?

M. Jahangir Alam Chowdhury University of Dhaka 9

Previous Evidence

Chowdhury (2008) indicate that the participation in the microcredit programs does not promote women entrepreneurship.

Limitations:

The sample size is small (N=920)

the survey of the study was conducted in only one of the main seventeen districts in the country.

It uses pipeline control to take care of the selection bias problem.

Probit technique is used.

M. Jahangir Alam Chowdhury University of Dhaka 10

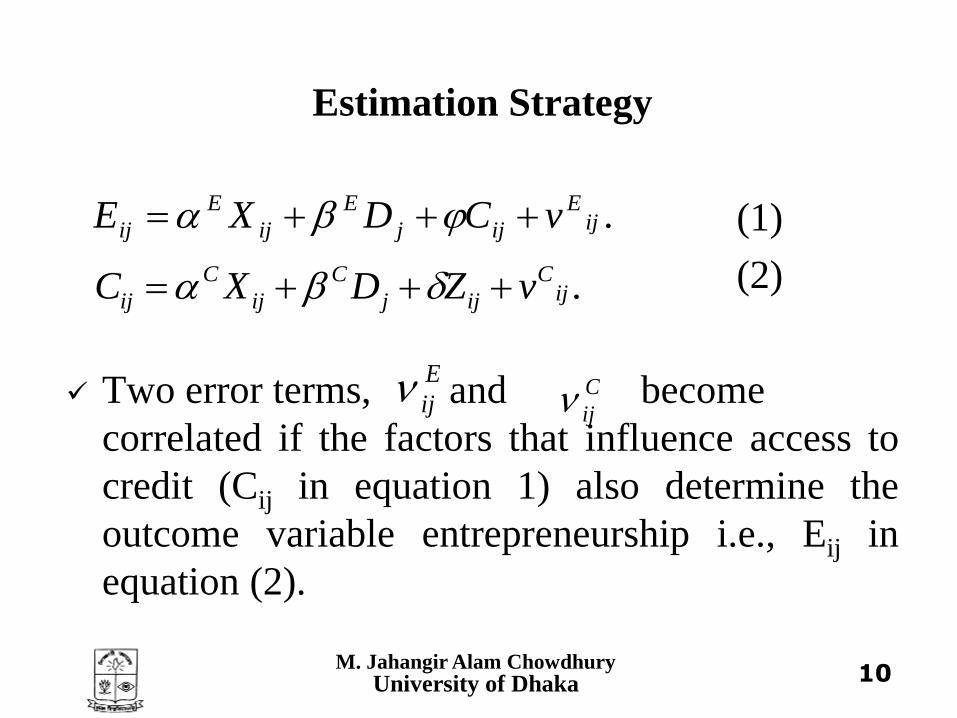

Estimation Strategy

(1)

(2)

Two error terms, and become

correlated if the factors that influence access to

credit (Cij in equation 1) also determine the

outcome variable entrepreneurship i.e., Eij in

equation (2).

.ijE

ijj

E

ij

E

ij vCDXE

.ijC

ijj

C

ij

C

ij vZDXC

E

ij C

ij

M. Jahangir Alam Chowdhury University of Dhaka 11

Estimation Strategy: Identification

Since and are not correlated, I use the instrumental variable (IV) technique.

The land ownership of the household is used as an instrument as it is a criteria that is followed by MFIs in Bangladesh.

Table 1: Microcrdit Program Participation and Land Ownership Criterion

E

ij C

ij

Microcredit

Program

Participation

Land Ownership

Less than 50 Decimals

Total

Yes No

Yes 2,641 (86.11%) 426 (13.89%) 3,067

No 6,628 (72.25%) 2,546 (27.75%) 9,174

Total 9,269 2,972 12,241

M. Jahangir Alam Chowdhury University of Dhaka 12

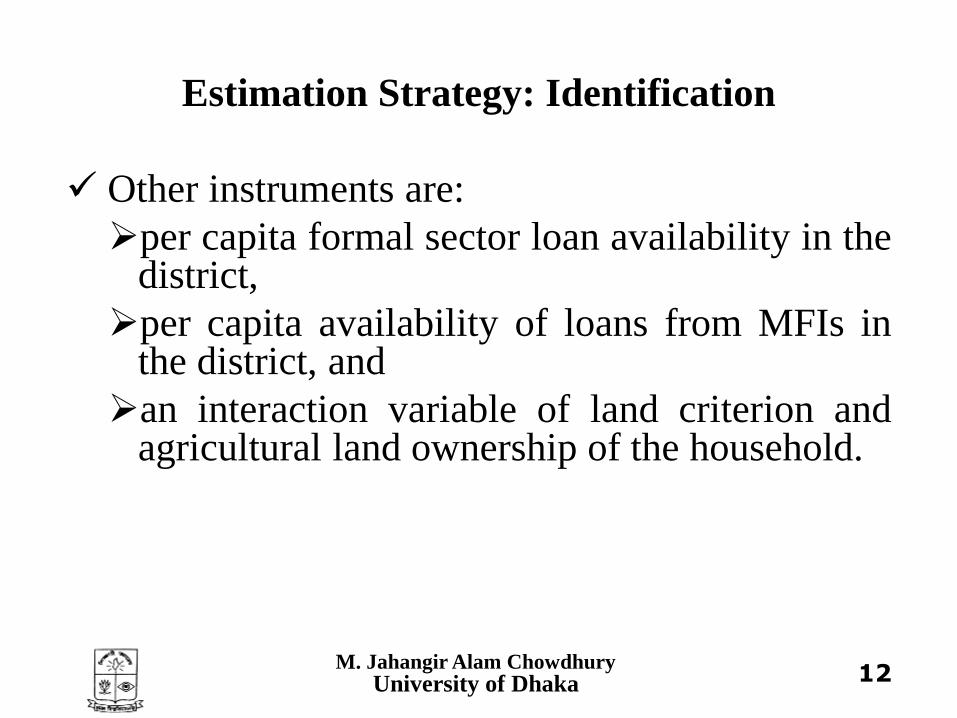

Estimation Strategy: Identification

Other instruments are:

per capita formal sector loan availability in the district,

per capita availability of loans from MFIs in the district, and

an interaction variable of land criterion and agricultural land ownership of the household.

M. Jahangir Alam Chowdhury University of Dhaka 13

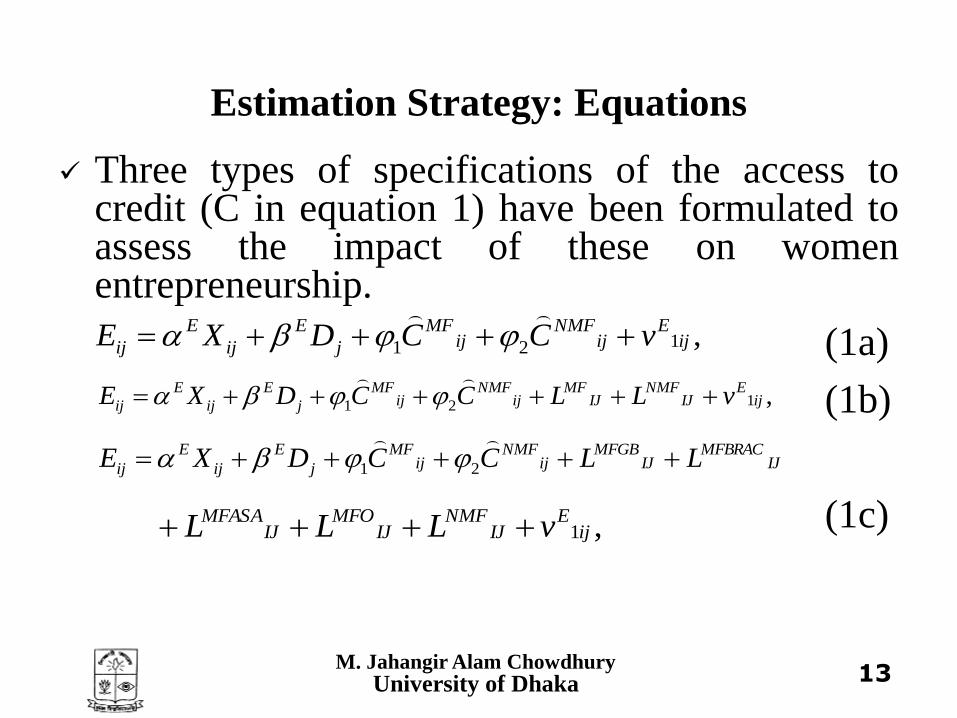

Estimation Strategy: Equations

Three types of specifications of the access to credit (C in equation 1) have been formulated to assess the impact of these on women entrepreneurship.

(1a)

(1b)

(1c)

IJMFBRAC

IJMFGB

ijNMF

ijMF

j

E

ij

E

ij LLCCDXE

21

,1ijE

IJNMF

IJMFO

IJMFASA vLLL

,121 ijE

ijNMF

ijMF

j

E

ij

E

ij vCCDXE

,121 ijE

IJNMF

IJMF

ijNMF

ijMF

j

E

ij

E

ij vLLCCDXE

M. Jahangir Alam Chowdhury University of Dhaka 14

Data

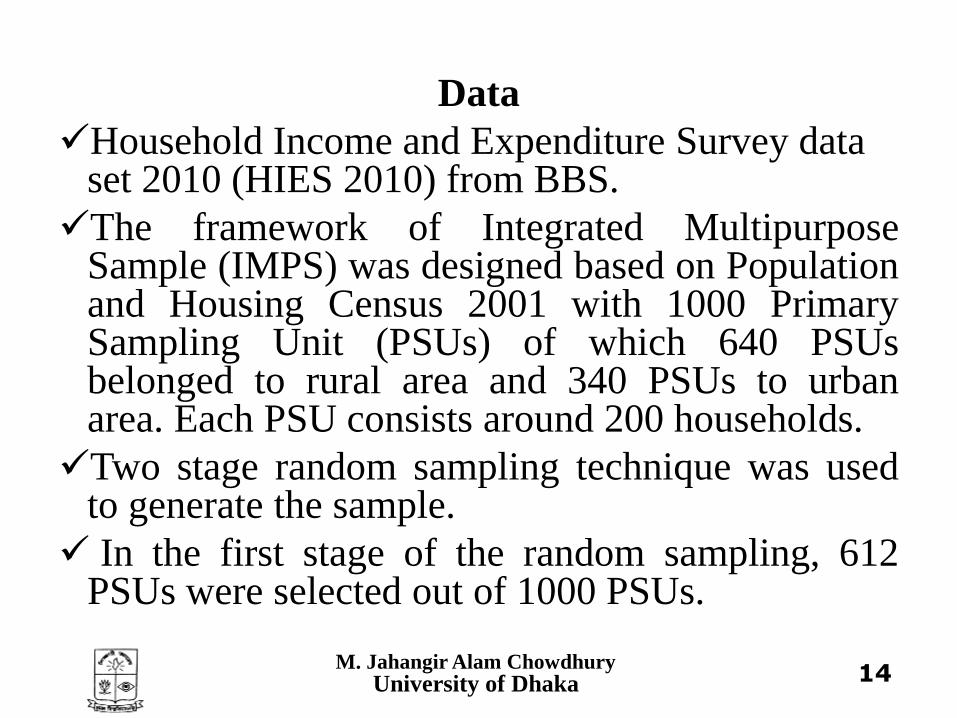

Household Income and Expenditure Survey data set 2010 (HIES 2010) from BBS.

The framework of Integrated Multipurpose Sample (IMPS) was designed based on Population and Housing Census 2001 with 1000 Primary Sampling Unit (PSUs) of which 640 PSUs belonged to rural area and 340 PSUs to urban area. Each PSU consists around 200 households.

Two stage random sampling technique was used to generate the sample.

In the first stage of the random sampling, 612 PSUs were selected out of 1000 PSUs.

M. Jahangir Alam Chowdhury University of Dhaka 15

Data

In the second stage, 20 households were randomly selected from each of the selected 612 PSUs. In total, HIES 2010 collected data from 12,240 households (N=12,240).

Table 3: Entrepreneurs by sex

Gender Entrepreneur Total

Yes No

Male 3,352

(20.99%)

12,621

(89.12%)

15,973

Female 267

(1.55%)

17,010

(98.45%)

17,277

Total 3,619 29,631 33,250

M. Jahangir Alam Chowdhury University of Dhaka 16

Results: Specification Testing

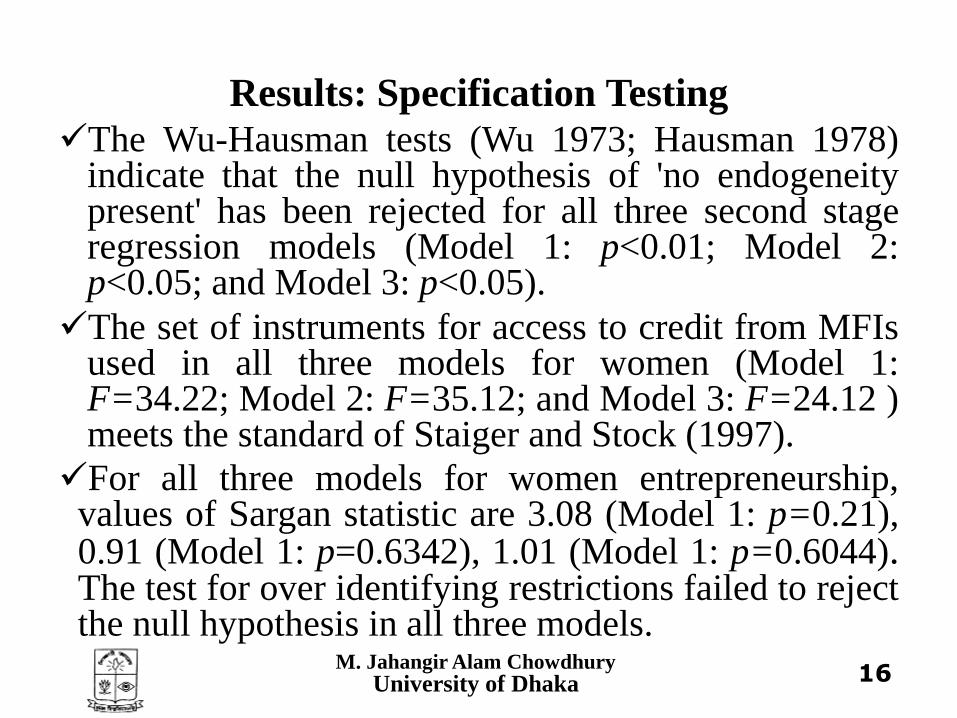

The Wu-Hausman tests (Wu 1973; Hausman 1978) indicate that the null hypothesis of 'no endogeneity present' has been rejected for all three second stage regression models (Model 1: p<0.01; Model 2: p<0.05; and Model 3: p<0.05).

The set of instruments for access to credit from MFIs used in all three models for women (Model 1: F=34.22; Model 2: F=35.12; and Model 3: F=24.12 ) meets the standard of Staiger and Stock (1997).

For all three models for women entrepreneurship, values of Sargan statistic are 3.08 (Model 1: p=0.21), 0.91 (Model 1: p=0.6342), 1.01 (Model 1: p=0.6044). The test for over identifying restrictions failed to reject the null hypothesis in all three models.

M. Jahangir Alam Chowdhury University of Dhaka 17

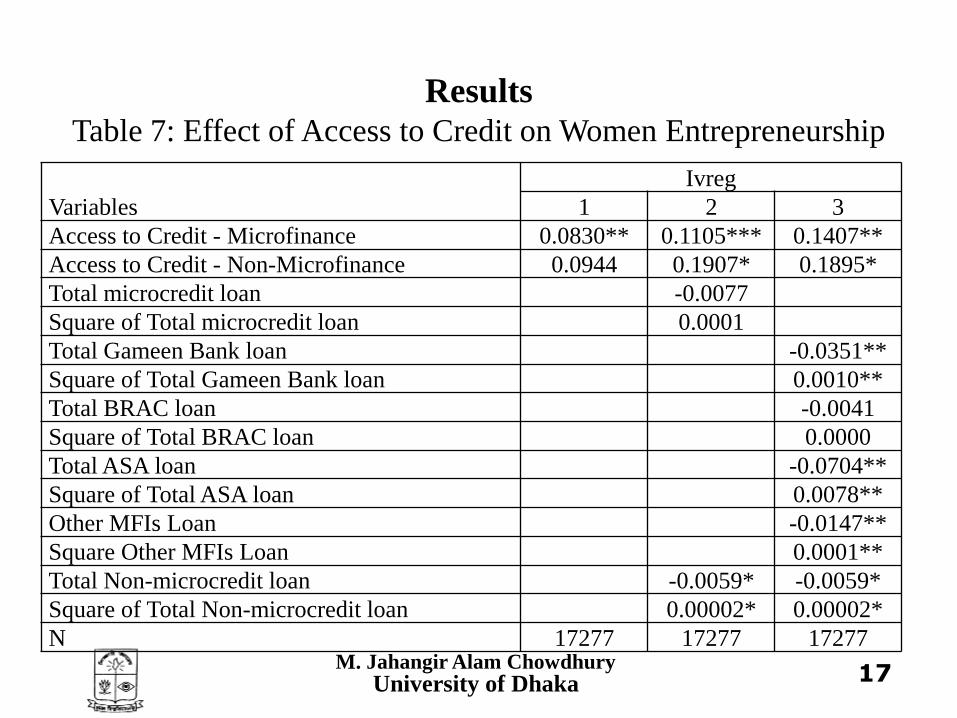

Results

Table 7: Effect of Access to Credit on Women Entrepreneurship

Variables

Ivreg

1 2 3

Access to Credit - Microfinance 0.0830** 0.1105*** 0.1407**

Access to Credit - Non-Microfinance 0.0944 0.1907* 0.1895*

Total microcredit loan -0.0077

Square of Total microcredit loan 0.0001

Total Gameen Bank loan -0.0351**

Square of Total Gameen Bank loan 0.0010**

Total BRAC loan -0.0041

Square of Total BRAC loan 0.0000

Total ASA loan -0.0704**

Square of Total ASA loan 0.0078**

Other MFIs Loan -0.0147**

Square Other MFIs Loan 0.0001**

Total Non-microcredit loan -0.0059* -0.0059*

Square of Total Non-microcredit loan 0.00002* 0.00002*

N 17277 17277 17277

M. Jahangir Alam Chowdhury University of Dhaka 18

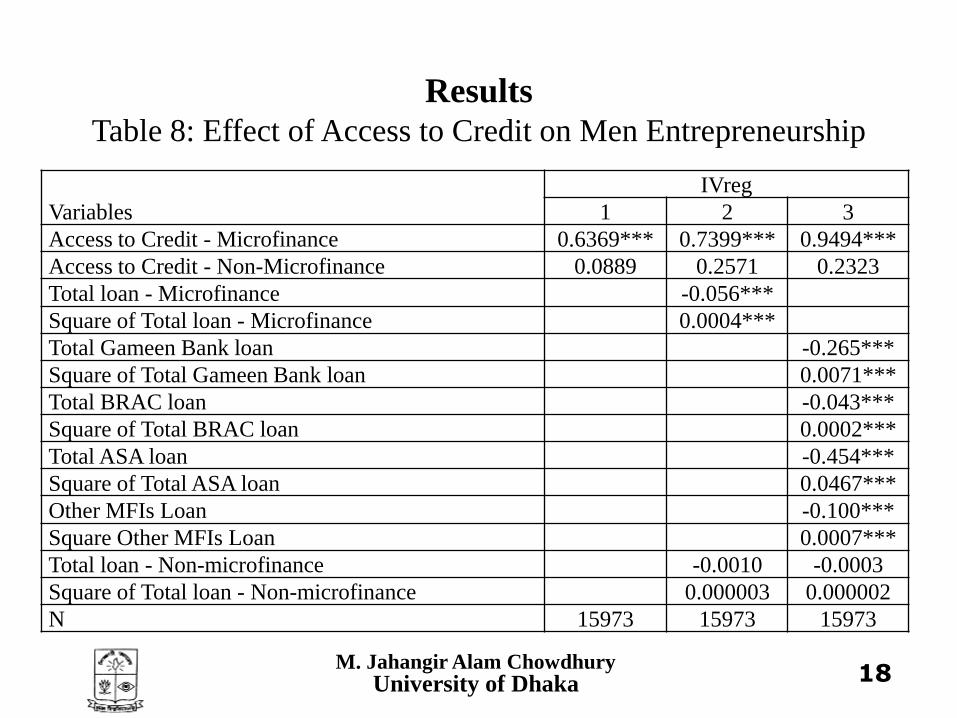

Results Table 8: Effect of Access to Credit on Men Entrepreneurship

Variables

IVreg

1 2 3

Access to Credit - Microfinance 0.6369*** 0.7399*** 0.9494***

Access to Credit - Non-Microfinance 0.0889 0.2571 0.2323

Total loan - Microfinance -0.056***

Square of Total loan - Microfinance 0.0004***

Total Gameen Bank loan -0.265***

Square of Total Gameen Bank loan 0.0071***

Total BRAC loan -0.043***

Square of Total BRAC loan 0.0002***

Total ASA loan -0.454***

Square of Total ASA loan 0.0467***

Other MFIs Loan -0.100***

Square Other MFIs Loan 0.0007***

Total loan - Non-microfinance -0.0010 -0.0003

Square of Total loan - Non-microfinance 0.000003 0.000002

N 15973 15973 15973

M. Jahangir Alam Chowdhury University of Dhaka 19

Conclusions

Non-credit effects compared to credit effects of microfinance program participation are more important for women entrepreneurship.

Most of the loans from different microfinance sources are not significant determinants of women entrepreneurship.

The loans from Grameen Bank and non-microfinance sources significantly determine women entrepreneurship.

However, these two types of loans are not positively effective for women entrepreneurship when sizes are small.

M. Jahangir Alam Chowdhury University of Dhaka 20

Conclusions

The reality is that the sizes of loans which women take from microfinance and non-microfinance sources are small.

Non-credit aspects of microfinance program participation of women also help significantly positively male members of households in becoming entrepreneurs.

Loans from different microfinance sources are significantly more effective for men than women in terms of becoming entrepreneurs.

Loans from microfinance and non-microfinance sources significantly increase the total market value of businesses of men and those of households.

M. Jahangir Alam Chowdhury University of Dhaka 21

Thanks