account disclosures for personal accounts - onewest bank · 2018 spring 1.25% apy premium money...

TRANSCRIPT

onewestbank.com

Account Disclosures for Personal Accounts

88024 Personal Account Disclosure R2.indd 2 1/23/18 4:41 PM

4026-05/18

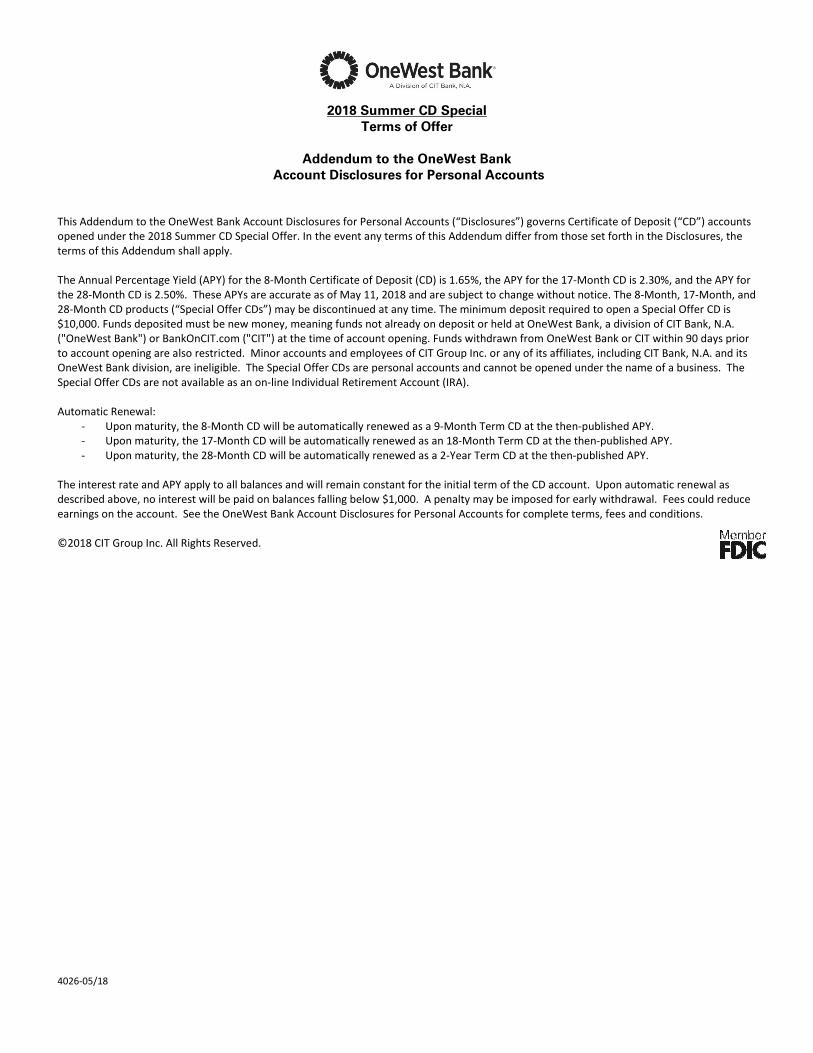

2018 Summer CD Special

Terms of Offer

Addendum to the OneWest Bank

Account Disclosures for Personal Accounts

This Addendum to the OneWest Bank Account Disclosures for Personal Accounts (“Disclosures”) governs Certificate of Deposit (“CD”) accounts

opened under the 2018 Summer CD Special Offer. In the event any terms of this Addendum differ from those set forth in the Disclosures, the

terms of this Addendum shall apply.

The Annual Percentage Yield (APY) for the 8-Month Certificate of Deposit (CD) is 1.65%, the APY for the 17-Month CD is 2.30%, and the APY for

the 28-Month CD is 2.50%. These APYs are accurate as of May 11, 2018 and are subject to change without notice. The 8-Month, 17-Month, and

28-Month CD products (“Special Offer CDs”) may be discontinued at any time. The minimum deposit required to open a Special Offer CD is

$10,000. Funds deposited must be new money, meaning funds not already on deposit or held at OneWest Bank, a division of CIT Bank, N.A.

("OneWest Bank") or BankOnCIT.com ("CIT") at the time of account opening. Funds withdrawn from OneWest Bank or CIT within 90 days prior

to account opening are also restricted. Minor accounts and employees of CIT Group Inc. or any of its affiliates, including CIT Bank, N.A. and its

OneWest Bank division, are ineligible. The Special Offer CDs are personal accounts and cannot be opened under the name of a business. The

Special Offer CDs are not available as an on-line Individual Retirement Account (IRA).

Automatic Renewal:

- Upon maturity, the 8-Month CD will be automatically renewed as a 9-Month Term CD at the then-published APY.

- Upon maturity, the 17-Month CD will be automatically renewed as an 18-Month Term CD at the then-published APY.

- Upon maturity, the 28-Month CD will be automatically renewed as a 2-Year Term CD at the then-published APY.

The interest rate and APY apply to all balances and will remain constant for the initial term of the CD account. Upon automatic renewal as

described above, no interest will be paid on balances falling below $1,000. A penalty may be imposed for early withdrawal. Fees could reduce

earnings on the account. See the OneWest Bank Account Disclosures for Personal Accounts for complete terms, fees and conditions.

©2018 CIT Group Inc. All Rights Reserved.

4028-06/18

2018 Spring 1.25% APY Premium Money Market Account Promotion

Terms of Offer

Addendum to the OneWest Bank

Account Disclosures for Personal Accounts

This Addendum to the OneWest Bank Account Disclosures for Personal Accounts (“Disclosures”) governs Premium Money

Market Accounts opened under the 2018 Spring 1.25% APY Premium Money Market Account Promotion offer. In the event any

terms of this Addendum differ from those set forth in the Disclosures, the terms of this Addendum shall apply.

Limited time offer of a promotional 1.25% Annual Percentage Yield (“APY”) on new Premium Money Market Accounts

(“PMMAs”) opened between March 19, 2018 and June 30, 2018. The 1.25% APY will be paid on PMMAs opened under this offer

for the first 12 months after the account is opened (the “Promotional Period”), provided the following requirements are met:

1. The new PMMA is opened with a minimum of $10,000 not on deposit or held at OneWest Bank, a division of CIT Bank,

N.A. (“OneWest Bank”) or BankOnCIT.com (“CIT”) at the time of account opening. Funds withdrawn from OneWest

Bank or CIT within 90 days prior to account opening are also restricted.

2. A principal balance of between $10,000 and $500,000 is maintained in the subject PMMA each day during the

Promotional Period. The principal balance is defined as the end-of-day PMMA account balance, exclusive of any

interest earned.

Only one promotional PMMA can be opened per customer within a 12-month period. Retirement accounts, minor accounts,

and employees of CIT Group Inc. or any of its affiliates, including CIT Bank, N.A. and its OneWest Bank division, are ineligible for

this offer. The PMMA is a personal account only and cannot be opened in the name of a business.

The 1.25% APY will be paid on your qualified PMMA each of the first twelve months the account is open, after confirmation

each day that your PMMA principal balance is between $10,000 and $500,000. If the end-of day PMMA account balance falls

below $10,000 or exceeds $506,250 (which includes the additional interest on a $500,000 principal balance earned over one

year at 1.25% APY), the interest rate and APY will revert to the then current regular published interest rate and APY for the

applicable balance tier. The promotional rate will be reinstated on the day after the PMMA end-of-day account balance again

falls within the balance range stated in the previous sentence.

After the end of the Promotional Period, the PMMA will revert to the then current regular published rates for all balance tiers.

Current published APYs, effective as of March 19, 2018, are: 0.15% APY on balances below $1,000; 0.15% APY on balances of

$1,000 - $4,999; 0.15% APY on balances of $5,000 - $9,999; 0.25% APY on balances of $10,000 - $24,999; 0.40% APY on

balances of $25,000 - $49,999; 0.50% APY on balances of $50,000 - $99,999; 0.60% APY on balances of $100,000 - $9,999,999;

and 0.60% APY on balances of $10,000,000 or more. APYs applicable after the end of the Promotional Period, and on PMMAs

that are not eligible for this promotion or which become ineligible because the principal balance falls outside of the specified

range, are variable and may change at any time without prior notice. Fees could reduce earnings on the account. A monthly

service fee of $10 will apply for the PMMA if the average monthly balance falls below $10,000. Contact a banking office for

complete terms, fees and conditions.

Restriction on deposits: For the duration of the Promotional Period, you may not deposit or transfer to your PMMA any funds

that are on deposit or held at OneWest Bank or CIT. OneWest Bank reserves the right to reverse any deposits it determines

violate this restriction.

© 2018 CIT Group Inc. All rights reserved.

I. DEPOSIT ACCOUNT AGREEMENT

WELCOME TO ONEWEST BANKBanking with OneWest Bank 1Additional Services to Consider 1Ways to Access your Account 1

YOUR AGREEMENT WITH US Our Agreement 2Amendments and Changes in Account Terms 2FDIC Insurance 2Governing Law 2Consent to Receive Telephone Calls/Texts & SMS Messages 3

INFORMATION ABOUT YOU AND YOUR ACCOUNTS WITH USCustomer Identification Program 3Credit Verification 3Telephone and E-Mail Monitoring 3

ACCOUNT OWNERSHIPSome General Information 3Transfer/Assignment 4Personal Accounts in General 4Payable-on-Death and Totten Trust Accounts 4

GENERAL INFORMATION ABOUT TYPES OF ACCOUNTSChecking, Savings and Money Market Products Offered 4Checking Subaccounts 4Certificate of Deposit Products Offered 5

PAYMENT OF OVERDRAFTSMaintaining an Available Balance 5Payment of Overdrafts 5Fees Associated with Overdrafts 5Overdraft Protection 5

ABOUT OUR POSTING ORDERGeneral Posting Order 6Credit and Debit Categories for Posting 6Determination of Posting Order 6Posting Order and Overdraft Fees 6

DEPOSITS AND COLLECTIONSAccepting Items for Deposit 6Verification and Collection 7Items Sent for Collection 7Lost Items 7Remotely Created Checks and Demand Drafts 7Delivery of Deposits and Verification 8Endorsements 8Identifying Your Account for Deposits 8Correction of Deposit Errors 8Returned Items/Transactions 9Depositing or Cashing Substitute Checks 9

88024 Personal Account Disclosure R2.indd 4 1/23/18 4:41 PM

FUNDS AVAILABILITY POLICYYour Ability to Withdraw Funds 9Longer Delays May Apply 9Special Rules for New Accounts 10Deposits Made Via Automated Clearing House Transactions 10Holds on Other Funds 10Foreign Items 10

WITHDRAWALS AND CHECK CASHINGCashing Checks Payable to You 11Cashing Your Checks Payable to Others 11Check Stock 11Converting Checks to Electronic Debits 11Examining Checks 11Voluntary Disclosure of Your Account Number 12Large Cash Withdrawals 12Paying Checks Drawn on Your Account 12Post-Dated Checks 12Missing Date or Stale-Dated Checks 12Substitute Checks and Image Replacement Copies 13Returning Unpaid Items to You 13

SUBSTITUTE CHECKS AND YOUR RIGHTSWhat is a Substitute Check? 13What are Your Rights Regarding Substitute Checks? 13How do you Make a Claim for a Refund? 14

COMMUNICATIONS, NOTICES AND STATEMENTS WE MAY SEND YOUAbout Sending Communications, Notices and Statements to You 14Delivery of Communications About Changes 14Check Images 15Change of Address 15Changes in Ownership and Authorized Signers 15

PROTECTING YOUR ACCOUNTSPrecautions You Should Take 15Closing a Compromised Account 16Lost or Stolen Checks 16

REPORTING UNAUTHORIZED TRANSACTIONS AND PROBLEMSTypes of Unauthorized Transactions 16Reviewing Statements and Reporting Unauthorized Use of Your Account 16Not Reporting Unauthorized Transactions Timely 16Our Investigation of Your Unauthorized Transaction 17Our Maximum Liability 17

FOREIGN CHECKS AND TRANSACTIONSWhat is a Foreign Item? 17Being Careful About Accepting Foreign Items 17Converting Currency and Exchange Rates 17Checks or Other Items in Foreign Currency 17

OTHER TERMS AND CONDITIONSAutomatic Transfer Service 18Using Your Checks and Pre-printed Deposit Slips 18

88024 Personal Account Disclosure R2.indd 5 1/23/18 4:41 PM

Compliance 18 Prohibition on Funding of Unlawful Internet Gambling 18Conflicting Claims to Funds or Other Property 19Closing an Account 19Death or Incompetence 19Facsimile Signature 19Fees and Charges 20Indemnification 20Legal Process Items 20Multiple Signatures Not Required 20Withdrawal Notice 20Power of Attorney 20Retaining Records 21Right of Refusal 21Right to Set-Off 21Stop Payments 21Inactive and Unclaimed Accounts 22Severability 22

ELECTRONIC FUND TRANSFER AGREEMENT AND DISCLOSUREElectronic Check Conversion 22Automated Teller Machine (“ATM”) and Debit Cards 22Telephone Banking 23Preauthorized/Automatic Transfers 24Online Banking/Mobile Banking 24Limitations 24Record of Your Transactions 24Our Liability for Failing to Make Transfers 24Your Liability for Unauthorized Electronic Fund Transfers 25How to Stop Preauthorized Transfers from Your Account 25Lost or Stolen Card/PIN or Unauthorized Transaction 26In Case of Errors or Questions About Your Electronic Transfers 26Fees 26Business Days 26Privacy 26Change in Terms/ Termination of Service 27

WIRE TRANSFERS AND OTHER FUNDS TRANSFERSGeneral Provisions 27Related Fees 27About Fedwire 27Sending Wire Transfers 27Error Resolution and Cancellation Rights for Consumer Int’l Wire Transfers 29Receiving Wire Transfers and Certain Other Funds Transfers 29ACH Debits and Credits 29International Wire and ACH Transactions 30General Foreign Wire Transfer Information 30

INCOME TAX WITHHOLDING 31

RESOLUTION OF DISPUTESResolution of Disputes: Arbitration Agreement 31Small Claims 32Commencing an Arbitration 32Powers and Qualifications of Arbitrators 32No Class Action or Joinder of Parties 32

88024 Personal Account Disclosure R2.indd 6 1/23/18 4:41 PM

SAFE DEPOSIT/SAFEKEEPING AGREEMENT AND DISCLOSUREDuties 33Access 33Default 34Remedies 34Notices 34Termination 35Joint Owners 35Relocation of Box 35Liability 35

II. CONSUMER PRODUCTS AND FEES

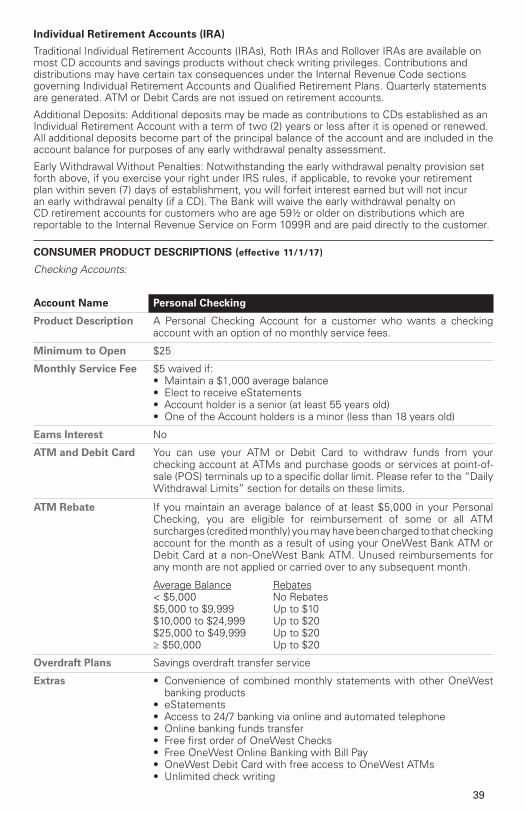

CHECKING, SAVINGS, MONEY MARKET AND CD ACCOUNT DISCLOSURESAverage Balance 36Statements 36Additional Rate Information 36Interest Compounding, Calculating and Crediting 36ATM and Debit Cards 36Daily Withdrawal Limits 37Savings and Money Market Accounts Are Limited Transaction Accounts 37Additional CD Account Disclosures 37Early Withdrawal Penalties 37Early Withdrawals Without Penalties 38Grace Period 38Renewals 38Additional Deposits 38Maturity Date and End of Term 38Individual Retirement Accounts (IRA) 39

CONSUMER PRODUCT DESCRIPTIONSPersonal Checking 39Premium Checking 40OneAccount Checking 41Personal Savings 42Green Savings 43Premium Money Market 44Certificate of Deposit 45

88024 Personal Account Disclosure R2.indd 7 1/23/18 4:41 PM

I. DEPOSIT ACCOUNT AGREEMENT

WELCOME TO ONEWEST BANK, A DIVISION OF CIT BANK, N.A.

Banking with OneWest Bank

At OneWest Bank, a division of CIT Bank, N A (“OneWest”), we deliver friendly, personalized banking services, One Person at a Time® OneWest was founded as a regional bank dedicated to customer service and a commitment to our community We pride ourselves as a bank with a strong capital foundation, conservative management and a consistent focus on providing value to our customers

Thank you for banking with OneWest Bank We look forward to serving you

Additional Services to Consider

After you open your account, please consider these optional services that can help you manage your account

• Debit Card. Use your debit card to pay for purchases at merchants that accept debit cards,to make deposits at OneWest Bank ATMs and to withdraw cash from ATMs

• Direct Deposit. Have your paycheck, retirement benefits or other payments depositedelectronically into your checking or savings account

• Online Banking. Helps you manage your finances Here are some of the things you can dousing our Online Banking: (1) check your account balances and review transaction history;(2) transfer funds between your accounts; (3) receive your statements and paid checks online,then review or print them at your convenience; (4) reorder checks and change your address;and (5) place stop payments on checks you’ve written

• Online Bill Pay Service. Pay and receive your bills electronically

• Mobile Banking. Access your accounts from your mobile phone or other portable device,including the ability to scan and deposit checks remotely (a service known as “mobile remotedeposit capture”)

• Automatic Transfer Service. Helps make saving easier by automatically transferring fundsfrom your checking account to your savings account

• Overdraft Protection Service. Protects you from overdrafts and from us having to returnchecks you have written by automatically transferring available funds from your savingsaccount to your checking account

Ways to Access Your Account

You can access your account and get information about our accounts and services: • At our Branches and at OneWest Bank ATMs

• Through our Online Banking at www onewestbank com

• Through our Customer Contact Center at 877 741 9378 (877-PH-1-WEST)

• Through our downloadable mobile banking application

You can locate our nearest branch or ATM on our website at www onewestbank com or by calling us at 877 741 9378

1

88024 Personal Account Disclosure R2.indd 1 1/23/18 4:41 PM

YOUR AGREEMENT WITH US

Our Agreement

This “Account Disclosures for Personal Accounts” document is designed for use with OneWest Bank’s companion disclosures, fee schedules and any applicable product or service addenda (together referred to as the “Agreement”) This Agreement explains OneWest Bank’s consumer deposit accounts and other related services we make available to you, as well as the terms and fees that govern these accounts and services By signing and returning the signature card for your account, you confirm that you have received this Agreement, and that you have reviewed, understood and agreed to the terms and conditions, fees and other information contained therein We may add to, delete or change the terms of this Agreement at any time subject to applicable law Except as indicated herein, we will inform you of changes that affect your rights and obligations Throughout this Agreement, the words “you,” “your” and “yours” refer to the account owner or owners Each person who signs the signature card is an owner of the account opened under this Agreement “We,” “us,” “the Bank” and “our” refer to OneWest Bank

This Agreement contains important information about your accounts You are responsible for ensuring that all authorized signers on your account are familiar with this Agreement We recommend you retain a copy of this Agreement (and any other notices the Bank provides you regarding changes to this Agreement) for as long as you maintain an account with us This Agreement does not apply to any accounts you may have with CIT Bank, N A ’s internet bank (www BankOnCIT com)

DISPUTE RESOLUTION/ARBITRATION AGREEMENT

THIS AGREEMENT INCLUDES OUR INTENT TO ARBITRATE ANY DISPUTES BETWEEN YOU AND THE BANK INSTEAD OF HAVING SUCH DISPUTES RESOLVED THROUGH A COURT TRIAL BEFORE A JUDGE OR JURY PLEASE READ THE RESOLUTION OF DISPUTES SECTION OF THIS AGREEMENT CAREFULLY

Amendments and Changes in Account Terms

We may change (add to, delete or alter) the terms of this Agreement with you at any time without prior notice, unless prior notice is required by law We will notify you of any such changes by mailing, e-mailing or delivering a notice, a statement message or an amended Agreement to any of you at the last address (location or e-mail) on file for you, your account or the service in question, or by posting the information in our offices, on our website or otherwise making it available to you

FDIC Insurance

Funds in your deposit accounts are generally insured up to $250,000 per depositor by the Federal Deposit Insurance Corporation (FDIC) The FDIC provides separate coverage for deposits held in different account ownerships such as: (1) individual or single ownership accounts; (2) joint ownership accounts; (3) revocable trust accounts (including pay-on-death accounts); (4) corporations, partnerships and unincorporated association accounts; and (5) certain individual retirement accounts To calculate your deposit insurance coverage, use the FDIC’s Electronic Deposit Insurance Estimator (EDIE) at www fdic gov/edie For questions about FDIC coverage limits and requirements visit www fdic gov/deposit/deposits or call toll-free at 1-877-ASK-FDIC

CIT Bank, N A and OneWest Bank, a division of CIT Bank, N A , are the same FDIC-insured institution Deposits held under each name are not separately insured, but are combined to determine whether a depositor has exceeded the $250,000 federal deposit insurance limit, per depositor for each account ownership category For purposes of calculating aggregate deposits held in OneWest Bank, a division of CIT Bank, N A , you should include deposits held in CIT Bank, N A

Governing Law

This Agreement, and your account(s), are governed by the laws and regulations of the United States and, to the extent applicable, the laws of the State of California, without regard to conflict of law principles If state and federal law are inconsistent, or if state law is preempted by federal

2

88024 Personal Account Disclosure R2.indd 2 1/23/18 4:41 PM

law, federal law governs Unless otherwise provided in this Agreement, your accounts and services will be subject to applicable clearinghouse, Federal Reserve Bank and correspondent bank rules You agree that we do not have to notify you of a change in those rules, except to the extent required by law

Consent to Receive Telephone Calls/Text & SMS Messages

When you provide us with your residential, business or mobile phone number you are deemed to have expressly consented to receiving telephone calls and text or SMS messages to such numbers You also consent to receipt of such calls or messages made by us using an auto dialer and/or prerecorded or artificial voice messages to you to provide banking services

INFORMATION ABOUT YOU AND YOUR ACCOUNTS WITH US

Customer Identification Program

IMPORTANT INFORMATION ABOUT PROCEDURES FOR OPENING A NEW ACCOUNT

To help the government fight the funding of terrorism and money laundering activities, federal law requires all financial institutions to obtain, verify and record information that identifies each person opening an account In some cases we may also be required to ascertain the identity of the beneficial owners of certain accounts

When you open an account, we will ask for your name, address, date of birth and other information that will allow us to identify you or the beneficial owners of the account We will also ask to see your driver’s license and/or other identifying documents

In those instances where we are unable to complete identity verification using information from a third-party, we may at our discretion: (1) request that you provide acceptable additional documentation or information and (2) block deposit and withdrawal activity on the account until such time as the identity verification has been satisfactorily completed In those instances where identity verification is not satisfactorily completed within a reasonable period of time after account opening and/or our notification to you of the same, we may, at our option, close the account and mail the proceeds to you in the form of a bank check

Credit Verification

By opening an account with the Bank, by agreeing to be an owner or signer on an account or obtaining any other service from us, you (and, if acting in a representative capacity, individually and for such entity or principal) agree that we may obtain account experience information or credit information about you from consumer or credit reporting agencies and/or by any other means where permitted by law We may do so at the time you open the account, at any time while your account is open, or after your account is closed if you owe us any amounts related to your account If you do not handle your account in a satisfactory manner and/or it is necessary for us to charge off your account as a loss, we will report such negative information to check or credit reporting agencies

Telephone and E-Mail Monitoring

We may randomly monitor (and may also record) customer service telephone conversations and electronic communications to ensure that you receive courteous and efficient service When you, or anyone you authorize, communicate with us, you agree that your call or e-mail may be monitored and/or recorded without further notice to you

ACCOUNT OWNERSHIP

Some General Information

When you open an account with us, we may rely on information you give us and we maintain in our records From this information we determine the type and ownership of the account opened If you ask us to make a change to this information or any change to your account, and we agree to the change, the change will not be effective until we have had a reasonable period of time to

3

88024 Personal Account Disclosure R2.indd 3 1/23/18 4:41 PM

act on the new information For example, if you ask us to change one or more signers on your account, the request will not be effective until we have had enough time to review your request and act on it If we ask you to give us additional documents or information, and you do not do so promptly, we may close your account When we accept a deposit to an account or permit a withdrawal, we may rely upon the current ownership of the account, the information currently in our records, and the terms of this Agreement at the time we process the transaction We are not obligated to inquire about the source or ownership of any funds we receive for deposit or about the use of funds withdrawn

When we permit a withdrawal from an account at the request of any signer (or the agent of any signer, as applicable), in accordance with the Agreement, the withdrawal is a release and discharge of the Bank from all claims regarding the withdrawal If you open an account in the names of two or more individuals, and we later determine that one or more of them have not completed our account opening documents (or provided us with certain requested information), you agree to hold us harmless for our reliance on your initial instructions We may in our discretion either: (1) treat the account as being owned by all persons in whose names the account was opened or (2) treat the account as being owned solely by the persons who have completed our account opening documents If we treat the account as owned by all persons in whose names the account was opened, we may permit any non-signing person to withdraw funds from the account or take any other action without any liability to you We may require you at any time to close the account in order to remove a co-owner, terminate joint ownership or change a payable-on-death (POD) or trust designation

Transfer/Assignment

All accounts are nontransferable except upon the books and records of the Bank We may require surrender of the evidence of account You may not grant, transfer or assign any of your rights to any account without prior written consent of the Bank We are not required to accept or recognize an attempted assignment of your account or any interest in it

Personal Accounts in General

Accounts such as individual, joint account (with or without right of survivorship), payable-on-death (POD), etc are intended for personal, family or household purposes and may not be used for business or commercial purposes If personal accounts are being used for business or commercial purposes, we reserve the right to either close the account or request that you present business documentation to substantiate the existence of the business and change the account to an appropriate business account type

Payable-on-Death (POD) and Totten Trust Accounts (ITF)

Payable-on-death and Totten Trust accounts are accounts which are payable on request to one or more depositors during their lifetimes and, upon the death of the last depositor, to one or more designated beneficiaries or payees If there is more than one surviving beneficiary or payee, each will receive an equal share of the account unless the signature card provides differently We may require joint instructions of, or payments to, all beneficiaries or payees

GENERAL INFORMATION ABOUT TYPES OF ACCOUNTS

Checking, Savings and Money Market Products Offered

We offer a range of checking (both variable rate interest bearing and non-interest bearing), variable rate savings and money market accounts (with limited check writing) that will suit the banking needs of consumers Please refer to the “Consumer Products” section for account details and eligibility For our current rates, please visit www onewestbank com or stop by one our branches

Checking Subaccounts

The following applies to all checking accounts For regulatory reporting and reserve purposes, we divide checking accounts into two subaccounts: a checking subaccount and a savings subaccount If your checking account earns interest, we will pay the same interest rate on both subaccounts If it does not earn interest, no interest will be paid on either subaccount

4

88024 Personal Account Disclosure R2.indd 4 1/23/18 4:41 PM

In either case, your account will continue to operate, from your perspective, as one account We may establish a threshold for the balance maintained in the checking subaccount and may transfer funds periodically from one subaccount to the other to meet that threshold and cover transactions against your account Your account statements will not reflect the existence of the subaccounts, and our periodic reallocation of funds between subaccounts will not affect your ability to withdraw funds, the interest rate (if any), fees or other features of your checking account You agree that we may treat the subaccounts as one and the same account if we receive a levy, subpoena or other legal process regarding either subaccount or your checking account

Certificate of Deposit Products Offered

We offer a range of certificate of deposit accounts with a variety of terms Please refer to the “Consumer Products and Fees” section for account details and eligibility For our current rates, please visit www onewestbank com or stop by one our branches

PAYMENT OF OVERDRAFTS

Maintaining an Available Balance

It is your responsibility to make sure that your account contains sufficient available funds at the time a check drawn against your account comes in for payment, and when you make a withdrawal or transfer, authorize a debit card purchase or other debit transaction of any kind If you are uncertain of your available balance, please contact us, check your account balance at any OneWest ATM, access our Online Banking Service at www onewestbank com, or use our Mobile Banking App If you do not have sufficient available funds on deposit in your account to cover a debit transaction, we may return the item unpaid or, in our discretion, authorize and pay the transaction creating an overdraft

Payments of Overdrafts

We are not obligated to pay any item presented for payment against your account if your account does not have sufficient available funds If we pay a transaction by overdrawing your account, we are not obligated to continue paying such transactions and creating or increasing overdrafts in the future We may stop paying checks and other items which create overdrafts at once without notice to you You are liable to us to repay immediately any overdrafts on your account whether you created them or not If you do not pay us, and we take collection action against you, you agree to pay for any costs of collection We may terminate, without notice, any account with excessive insufficient funds activity, and report the account to a consumer-reporting agency

Fees Associated with Overdrafts

There are fees associated with each transaction that we either pay, which results in an overdraft, or do not pay (and return unpaid) which would have resulted in an overdraft had we paid it (usually due to insufficient or unavailable funds) Such fees may apply to overdraft transactions created by check, recurring debit card transactions, automated clearing house (ACH) debit and by certain other electronic means as permitted by law We will not charge a fee on overdraft transactions that we pay that are created by one-time debit card transactions or ATM transactions No more than four (4) overdrafts fees (due to insufficient or unavailable funds) per account will be charged in any one day Overdraft fees will not be charged on overdrafts less than $5 00 Refer to the “Consumer Fee Schedule” for additional overdraft fee information

Overdraft Protection

The Bank offers the following overdraft protection service:

Savings Overdraft Transfer Service - With this service, you authorize the Bank to make transfers of available funds automatically from your savings or money market account to cover overdrafts in your checking account Transfers from your savings or money market account are made in the exact amount of the overdraft Each transfer counts as one of the six (6) limited transactions you are allowed each month from your savings or money market account Please refer to the “Savings and Money Market Accounts are Limited Transaction Accounts” paragraph for further details You must enroll into this service Refer to the “Consumer Fee Schedule” for any fees associated with this service

5

88024 Personal Account Disclosure R2.indd 5 1/23/18 4:41 PM

ABOUT OUR POSTING ORDER

General Posting Order

We ordinarily post items within certain debit “categories” from the lowest to highest dollar amount, regardless of the order in which they occur or we receive them Refer to “Credit and Debit Categories for Posting” below for more information

Credit and Debit Categories for Posting

We may establish, at our discretion, different categories of debits and credits, and then determine posting orders within each category A category may include more than one type of debit or credit Debit categories may include checks, debit card purchases, withdrawals (in-person, via ATM, preauthorized and online), payments and various fees Credits that may be included in a credit category for posting may include teller deposits, direct deposits and other types of credits For example, we may treat ATM withdrawals and debit card purchases as one category, and on-us checks as another category, and then post ATM withdrawals and debit card purchases before we process and post checks We may change categories and orders within categories at any time without notice

We may change our posting order at any time without notice to you We may give preference to debits payable to us On your account statement we do not necessarily report debits and credits in the order that we posted them to your account

Determination of Posting Order

We do not post credits and debits to your account in the order in which they occur or we receive them Sometimes they are not posted to your account on the same day that they occur For example, when you write a check or use your debit card to make a purchase, the merchant or the person or business from whom you made the purchase may not present the check or debit charge to us for payment until several days later We may treat credits and debits to your account which we receive on any day as if we received all of them at the end of that day and post them in the order we determine

Posting Order and Overdraft Fees

Some posting orders may result in more overdraft items and returned items fees than other posting orders We may choose our processing and posting orders regardless of whether additional fees may result

You can avoid overdraft fees by making sure that your account always contains sufficient available funds to cover all of your withdrawals and debits You may also want to consider our Savings Overdraft Transfer Service as a possible way to avoid certain overdraft fees See the “Overdraft Protection” section for additional information

DEPOSITS AND COLLECTIONS

Accepting Items for Deposit

We may accept items for deposit, accept items for collection only, refuse items for deposit or return all or part of any deposit If we accept checks or other items for deposit to your account or cash them, you are responsible for the checks and other items if there is a subsequent problem with them

• We may accept a check or other item for deposit to your account from anyone We do not haveto question the authority of the person making the deposit

• We may refuse to accept for deposit to your account items payable to another person

• If we cash a check or other item for you or deposit it to your account and it is not paid for anyreason, we will charge your account for the amount of the check or other item, even if thiscauses your account to become overdrawn

6

88024 Personal Account Disclosure R2.indd 6 1/23/18 4:41 PM

• All deposits are subject to our subsequent verification and adjustment, even if you have alreadywithdrawn all or part of the deposit

• If we accept checks or other items for deposit or collection, we act only as your collectionagent and assume no responsibility beyond ordinary care We are not responsible for errorsand delays made by other institutions in the collection process

• When you send us deposits by mail, we treat them as received at the time we receive actualdelivery of the deposit If you place deposits in our night depository, we treat them as receivedwhen we remove the deposits from the depository

• If you give us cash that we later determine to be counterfeit, we will charge your account forthe amount we determine to be counterfeit

• You will not knowingly deposit items into your account that do not have either a true originalsignature of the person on whose account it is drawn or an authorized reproduction of thatperson’s signature

Verification and Collection

We may deduct funds from your account if an item is lost, stolen or destroyed in the collection process, if it is returned to us unpaid or if it was improperly paid, even if this causes your account to become overdrawn

Items Sent for Collection

We and other institutions may refuse to accept a check or other item for deposit or may accept it on a collection basis only This often occurs with foreign, questionable or damaged items If we accept an item for collection, we will send it to the institution upon which it is drawn, but will not credit your account for the amount until we receive the funds from the other institution If we elect to credit your account before then, we may charge the amount back against your account if we do not receive payment for any reason even if this causes your account to be overdrawn We may impose a fee in connection with sending and receiving items for collection (e g , by charging your account or deducting the fee from the amount remitted) Other institutions that send or receive items for collection involving your account also may impose a fee for their services

Lost Items

We act only as your collection agent when receiving items for deposit or encashment You should be aware that we reserve the right to reverse the credit for any deposited item or charge your account for cashed items should they become lost, mutilated, or destroyed while in the process of collection If we do not reverse a credit, you agree to assist us in collecting the amount of any lost items by providing us with such information and other assistance as we request We may charge your account when a photocopy or other substitute for a check you have written is presented to us for payment in place of a lost original, unless a stop payment order is in effect for the check

Remotely Created Checks and Demand Drafts

If you provide your account number to a third party in order to charge your account by means of one or more remotely created checks or demand drafts (i e , items which do not bear your actual signature, but purport to be drawn with your authorization), you authorize us to pay such items, even though they do not contain your signature and may exceed the amount you authorized to be charged This provision shall not obligate us to honor such items We may refuse to honor such items without cause or prior notice, even if we have honored similar items previously You agree to indemnify, defend and hold us harmless from every loss, expense and liability related to a claim that such items were not authorized (e g , as to their amount and payee) by you

You may not deposit remotely created checks or demand drafts to an account with us without our prior, express written consent If you do deposit remotely created checks or demand drafts to your account you agree that we may place a hold or otherwise restrict your account, or any other account you hold with us, in an amount we deem necessary should any such item be returned unpaid for any reason or returned to us with a claim that the item was unauthorized You agree that the amount of funds subject to hold and the duration of such hold shall be determined solely by us in our discretion

7

88024 Personal Account Disclosure R2.indd 7 1/23/18 4:41 PM

Delivery of Deposits and Verification

You may present deposits to us through various channels including one of our branches, ATMs, night depositories, mail, mobile remote deposit capture or other means that we may make available We may use the channel and time of delivery to determine when you receive credit for the deposit If we credit your account for the amount shown on the deposit ticket or other transmittal, the credit is subject to subsequent verification by us and our determination of the deposit amount is final

If you provide an endorsement on an item deposited to your account, such endorsement must adhere to all federal and state law requirements as well as banking industry practice If we authorize you to use a deposit envelope, you authorize us to open the envelope in your absence and credit the amount indicated on the deposit ticket contained therein to your account subject to subsequent verification of the contents If you make your deposit through a night depository, you agree to exercise reasonable care in opening, closing and properly securing the depository If you make a deposit using mobile remote deposit capture, the terms of the Online Banking Agreement will also govern the deposit

Endorsements

You authorize the Bank to supply your endorsement on any item that the Bank accepts for collection, payment or deposit to your account You also authorize the Bank to collect any unendorsed item that is made payable to you without first obtaining your endorsement, provided the item was deposited to your account The Bank may refuse to pay or cash any item or accept any item for deposit or collection unless it is able to verify to its satisfaction that all of the necessary endorsements are present on the item For example, the Bank may require that all payees or persons to whom the item is endorsed be present at the time that an item is presented to the Bank for payment, encashment, deposit or collection

If you issue or deposit a check that contains a carbon band, printing, endorsements or other material on the back of the check outside the area extending 1½ inches from the trailing edge of the check, that material could also interfere with endorsements by other banks and cause delays in returning the check Therefore, you agree that the Bank shall not be liable to you for, and you will indemnify and hold the Bank harmless from any and all claims, loss, costs and expenses (including reasonable attorneys’ fees and the costs of litigation) that the Bank or you may incur as a result of the late return of a check caused by carbon band, printing, endorsements or other material on the back of any check drawn on or deposited to your account that extend outside the area extending 11/2 inches from the trailing edge of the check The trailing edge is defined as the left side of the check when viewing it from the front

Identifying Your Account for Deposits

You are responsible for correctly identifying the account to which you want funds deposited or payments made We may credit a deposit to an account based solely on the account number listed on the deposit slip or other instruction to credit an account, even if the name on the deposit slip or other instruction differs from the name on the account You are responsible for any cost, loss or damage caused by your failure to properly identify the account to which a deposit is to be made

Correction of Deposit Errors

When we receive your deposits, we may provisionally credit your account for the amount indicated on the deposit slip or other transmittal, subject to later verification by us You must ensure that the amount indicated on the deposit ticket or other transmittal is correct even if you did not prepare the instruction If we later determine that the amount indicated on the deposit ticket or other transmittal is incorrect, we may make the appropriate debit or credit adjustment to your account However, if in our determination the error on the deposit ticket or other transmittal was inadvertent and is less than our standard adjustment amount, we will not adjust the amount of deposit to your account unless you notify us of the error within one year of the date of your periodic statement that shows the deposit After this notification period has expired and you have not brought any error to our attention, the deposit amount indicated on the statement will be considered final

8

88024 Personal Account Disclosure R2.indd 8 1/23/18 4:41 PM

Returned Items/Transactions

If we are notified that an item you cashed or deposited is being returned unpaid, we may attempt to re-clear the item at our discretion, place a hold on the funds in question (refer to the “Funds Availability Policy” section) or charge your account for the amount (and any interest earned on it), whether or not the return or notice of non-payment is proper or timely This also applies to checks drawn on us which are not paid for any reason, and to checks that are returned to us in accordance with any law, regulation or rule (including a clearinghouse rule) We may assess a fee for each returned item and notify you of the return orally, electronically or in writing

If we receive an affidavit or a declaration under penalty of perjury stating that an endorsement on an item deposited to your account is forged, that the item contains an alteration or that there has been a breach of warranty in connection with the item, we may charge the item back against your account or place a hold on the funds pending an investigation, without prior notice to you

Depositing or Cashing Substitute Checks

You agree that you will not, without our prior permission, cash or deposit “substitute checks” as defined by federal law or Image Replacement Documents (“IRDs”) that purport to be substitute checks and have not been previously endorsed by a bank If you cash or deposit such an item, you give us the same warranties and indemnities that we would give under applicable law as a reconverting bank You further agree to reimburse us for losses, costs, damages and attorneys’ fees we may incur as a result of such action If you provide us with an electronic representation of a substitute check for deposit into your account instead of an original check, you agree to reimburse us for all losses, costs and damages we incur because the resulting substitute check (from the electronic representation) does not meet the requirements for legal equivalence or causes duplicate payments

FUNDS AVAILABILITY POLICY

Your Ability to Withdraw Funds

Our policy is generally to make funds from your check deposits with us available to you on the first business day we are open after the day we receive your deposit Once the funds are available, you can withdraw the funds in cash and we will use the funds to pay checks you have written Cash and incoming wire transfers will be available on the day we receive the deposit For determining the availability of your deposits, every day is a business day, except Saturday, Sunday and Federal holidays If we receive your deposit at one of our branches on a day other than a business day or on a day we are not open, the deposit will be considered received on the next business day

If you make a deposit at one of our automated teller machines (ATM) or via mobile remote deposit capture before 3:00 PM on a business day we are open, we will consider that the day of deposit If you make a deposit at one of our night depositories before 8:00 AM on a business day we are open, we will consider that the day of deposit Deposits made after these times will be considered received on the next business day Times may vary slightly by location and will be posted on affected ATMs and night depositories Cash deposits at our ATMs will be available on the next business day following the day we receive the deposit

Longer Delays May Apply

In some cases, we will not make all of the funds that you deposit by check available to you the next business day after we receive your deposit Funds you deposit by check may be delayed for a longer period of time under certain circumstances, including the following:

• We believe a check you deposit will not be paid

• You deposit checks totaling more than $5,000 on any one day

• You redeposit a check that has been returned unpaid

• You have overdrawn your account repeatedly in the last six months

• There is an emergency, such as failure of computer or communications equipment

9

88024 Personal Account Disclosure R2.indd 9 1/23/18 4:41 PM

We will notify you if we delay your ability to withdraw funds for any of these reasons, and we will tell you when the funds will be available They will generally be available no later than the seventh business day after the date of your deposit If we decide to take this action after you have left the premises, we will mail you the notice by the following business day after we receive your deposit If you will need the funds from a deposit right away, you should ask us when the funds will also be available

Special Rules for New Accounts

If you are a new client, the following special rules apply during the first 30 calendar days that your account is open Funds from cash and wire transfers to your account will be available on the day we receive the deposit The first $5,000 of a day’s total deposits of cashier’s, certified, teller’s, traveler’s and federal, state and local government checks will be available on the first business day after the day of your deposit if the deposit meets certain conditions For example, the checks must be payable to you The excess over $5,000 will be available on the seventh business day after the day of your deposit If your deposit of these checks (other than a U S Treasury check) is not made in person to one of our employees, the first $5,000 will not be available until the second (2nd) business day after the day of your deposit Funds from all other check deposits will be available on the seventh business day after the day of your deposit

Deposits Made Via Automated Clearing House Transactions

For funds deposited by an Automated Clearing House (ACH) transaction you initiate with OneWest Bank (where the funds come from your account at another bank for deposit to your OneWest Bank account), we may place a hold on such deposited funds for a period of 5 business days

Funds Deposited by an ACH transaction you initiate through another US financial institution (where the funds are sent from your account at another bank for deposit to your OneWest Bank account) are credited and available as of the business day OneWest Bank receives the funds from your bank

OneWest Bank reserves the right to place an extended hold on any deposits that are believed to be fraudulent or are suspicious

Holds on Other Funds

If we cash a check for you that is drawn on another bank, we may withhold availability of a corresponding amount of funds that are already in your account Those funds will be available at the time funds from the check we cashed would have been available if you had deposited it If we accept for deposit a check that is drawn on another bank, we may make funds from the deposit available for withdrawal immediately, but delay your availability to withdraw a corresponding amount of funds that you have on deposit in another account with us The funds in the other account would then not be available for withdrawal until the time periods that are described elsewhere in this disclosure for the type of check that you deposited

Foreign Items

This funds availability policy section does not apply to foreign checks which may be subject to longer holds before funds are available For additional information see the Foreign Checks and Transactions section

10

88024 Personal Account Disclosure R2.indd 10 1/23/18 4:41 PM

WITHDRAWALS AND CHECK CASHING

Cashing Checks Payable to You

We may occasionally refuse to cash a check payable to you (for example, if we doubt the collectability of a check) If we do cash such a check and it is returned to us unpaid for any reason at any time, we may deduct the amount of the check from your account (including any related fee) even if this causes your account to become overdrawn We may cash checks payable to any signer on your account when endorsed by any other signer If you request that we cash a check for you, we may apply the proceeds of the check encashment to any fees, overdrafts and other amounts you owe us

Cashing Your Checks Payable to Others

If a person wants to cash your check in one of our branches, we may:

• require identification satisfactory to us,

• charge them a fee for cashing the check; and

• impose additional requirements, such as requiring their fingerprint on the check, verifying the validity of the check with you, and/or posing questions designed to verify the identity of the payee(s) or person(s) to whom the item is endorsed

If the person with your check fails or refuses to satisfy our requirements, we may refuse to cash the check We are not liable to you for refusing to cash the check or for charging a check-cashing fee

Check Stock

You agree to bear the costs, losses and damages as a result of your use of check stock that contains defects, such as printing inaccuracies, faulty magnetic ink, faulty encoding or duplicate check numbers You also agree to bear the risk of loss if: you elect to have your checks printed by a vendor that has not been approved by us; you use check stock or features (including security features) that cause important data to disappear or be obscured when converted to an electronic image during the check collection and return process; or you write your check in a way that causes critical data to disappear or to be obscured when converted to an electronic image

Converting Checks to Electronic Debits

Some businesses convert checks that you give them into electronic debits and then send us the electronic debit for the transaction amount When we receive the electronic debit, we charge it to your account We may receive the electronic debit to your account immediately after the business enters the transaction, so you may incur an overdraft fee if you do not have sufficient funds in your account to cover the amount of the check Since the check is not sent to us, we do not have a copy of your check We list these electronic debits on your account statement If the business uses your check to initiate an electronic debit at the point of sale, the business should give you notice of the conversion of the check and return the voided check to you You should treat the voided check with care because someone else who obtains possession of it could use the information to initiate additional debits against your account

Examining Checks

We receive many checks for deposit and encashment each business day Compliance with expedited funds availability regulations require us to use automated check processing procedures which may not allow us time to examine every check presented Although we may visually review a sample of checks presented from time to time, reasonable commercial standards do not require us to do so We may select some checks for review based on certain criteria that we may establish and change at our discretion Using automated check processing procedures means that most checks are processed on the basis of the MICR (Magnetic Ink Character Recognition) line printed along the bottom edge of the check, and are not individually examined for dates, maker signatures, endorsements, etc You agree that we will have exercised ordinary care if we examine only those items that we have identified according to the criteria that we may establish at our discretion

11

88024 Personal Account Disclosure R2.indd 11 1/23/18 4:41 PM

When we do visually examine any check, we may disregard any restrictive instructions or notations (e g , pay only on two or more signatures) We may return the item unpaid if, in our opinion, it does not bear a signature matching any specimen signature we have on file for your account You agree that we will not be liable to you for honoring any check bearing a signature that resembles, in our opinion, the specimen signature on file with us Since we do not individually examine most checks, it is important for you to secure your checks, promptly review your account statement and immediately report any suspicious or unauthorized activity to us You agree that automated processing of your checks is reasonable and that you accept responsibility for preventing and reporting forgeries, alterations and other unauthorized uses of your checks or accounts You further agree that the exercise of ordinary care will not require us to detect forgeries or alterations that could not be detected by a person observing reasonable commercial standards We may elect in some cases to make further inquiries about certain checks that are presented for payment against your account In these instances, if we are unable to contact you to determine with reasonable certainty that you authorized these payments, we may either pay the checks or return them unpaid without any liability to you

Voluntary Disclosure of Your Account Number

If you voluntarily disclose your account number to another person through any means, you are deemed to authorize each item, including electronic debits, which result from your disclosure We may pay these items and charge your account

Large Cash Withdrawals

We reserve the right to limit the amount of cash you may withdraw at a branch due to the limited amount of currency on hand If we do not have sufficient cash for a large withdrawal, we may offer to make payment with a bank check or wire transfer, or at our sole discretion, make arrangements for a later cash payment If you intend to make a large cash withdrawal you must provide us with reasonable advance notice so that we can make arrangements to have the cash available or inform you that your request cannot be accommodated If we determine that your request can be accommodated, we will assume no responsibility to provide personal protection for customers who elect to carry large sums of money off our premises In some cases we may require that you make arrangements to receive large cash withdrawals at our central cash vault or other location designated by us via armored transport service acceptable to us and at your risk and expense

Paying Checks Drawn on Your Account

We may debit your account for a check or other item drawn on your account either on the day it is presented to us for payment or on the day we receive notice that the item has been deposited for collection at another financial institution - whichever is earlier If you do not have sufficient available funds to cover the item, we will decide whether to return it or to pay it and overdraw your account We may determine your balance and make our decision on an insufficient funds item at any time between our receipt of the item or notice and the time we must return the item We are required to determine your account balance only once during this time period When you deposit checks or other items that are drawn on another account with us, we may treat such items as presented to us for payment on the business day that they are received by our department that processes checks drawn on the other account

Post-Dated Checks

We generally do not accept post-dated checks (i e , a check with a date in the future) However, if one is presented for payment, we may pay the check and charge it to your account even if it is presented for payment before the date stated on the check If you do not want us to pay a stale- dated or postdated check, you must place a stop payment order on it Refer to “Stop Payments” in the “Other Terms and Conditions” section of this booklet

Missing Date or Stale-Dated Checks

Regardless of the date on a check you have written, whether missing or stale-dated (a date more than 6 months in the past), we may pay or reject the check (at our discretion) whenever it is presented for payment You agree that we are not required to identify stale-dated checks, checks with missing dates or to seek your permission to pay them If you do not want us to pay

12

88024 Personal Account Disclosure R2.indd 12 1/23/18 4:41 PM

any check for any reason, you must place a stop payment order on the check Refer to “Stop Payments” in the “Other Terms and Conditions” section of this booklet

Substitute Checks and Image Replacement Copies

In some cases, we may be sent a copy of your original check with representation that the original is lost or stolen accompanied by an indemnification from a financial institution, an Image Replacement Document (IRD), a substitute check or an image of your check, instead of the original item We may act upon presentment of an indemnified copy, IRD, substitute check or image of your check and pay these items against your account, just as if the original item had been presented Except as provided in the Check 21 Act, we will incur no liability to you or anyone else if the original item is later presented to and paid by us

Returning Unpaid Items to You

If we decide not to pay a check or other item drawn on your account, we may return the original, an image or a copy of the item, or we may send an electronic notice of return and keep either the original, an image, or a copy of the item in our records If we send an electronic notice of return, you agree that any person who receives that electronic notice may use it to make a claim against you to the same extent and with the same effect as if we had returned the original item

SUBSTITUTE CHECKS AND YOUR RIGHTS

The following provisions explain some of the rights a consumer has under a federal law often referred to as “Check 21 ” Check 21 was enacted to increase the efficiency of the U S check clearing system The check clearing system has historically relied heavily on the physical transport of paper checks between banks Check 21 allows banks to create substitute checks and present them electronically to other banks instead of the original check This reduces the transport of checks among banks and facilitates the electronic collection of checks

What is a Substitute Check?

To make check processing faster, federal law permits banks and businesses to replace original checks with “substitute checks ” These checks are similar in size to original checks with a slightly reduced image of the front and back of the original check The front of a substitute check states: “This is a legal copy of your check You can use it the same way you would use the original check ” You may use a substitute check as proof of payment just like the original check Some or all of the checks that you receive back from us may be substitute checks This notice describes rights you have when you receive substitute checks from us The rights in this notice do not apply to original checks or to electronic debits to your account However, you have rights under other laws with respect to those transactions

What are your Rights Regarding Substitute Checks?

In certain cases, federal law provides a special procedure that allows you to request a refund for losses you suffer if a substitute check is posted to your account (for example, if you think that we withdrew the wrong amount from your account or that we withdrew money from your account more than once for the same check) The losses you may attempt to recover under this procedure may include the amount that was withdrawn from your account and fees that were charged as a result of the withdrawal (for example, bounced check fees) The amount of your refund under this procedure is limited to the amount of your loss or the amount of the substitute check, whichever is less You also are entitled to interest on the amount of your refund if your account is an interest- bearing account If your loss exceeds the amount of the substitute check, you may be able to recover additional amounts under other laws If you use this procedure, you may receive up to $2,500 of your refund (plus interest if your account earns interest) within 10 business days after we received your claim and the remainder of your refund (plus interest if your account earns interest) not later than 45 calendar days after we received your claim We may reverse the refund (including any interest on the refund) if we later are able to demonstrate that the substitute check was correctly posted to your account

13

88024 Personal Account Disclosure R2.indd 13 1/23/18 4:41 PM

How do you Make a Claim for a Refund?

If you believe that you have suffered a loss relating to a substitute check that you received and that was posted to your account, please contact us You may call us at 877 741 9378 or write to us at P O Box 471, Santa Monica, CA 90406-0471 You must contact us within 40 calendar days of the date that we mailed (or otherwise delivered by a means to which you agreed) the substitute check in question or the account statement showing that the substitute check was posted to your account, whichever is later We will extend this time period if you were not able to make a timely claim because of extraordinary circumstances Your claim must include: (1) a description of why you have suffered a loss (for example, you think the amount withdrawn was incorrect); (2) an estimate of the amount of your loss; (3) an explanation of why the substitute check you received is insufficient to confirm that you suffered a loss; and (4) a copy of the substitute check and/or the following information to help us identify the substitute check: the check number, the name of the person to whom you wrote the check, the amount of the check

COMMUNICATIONS, NOTICES AND STATEMENTS WE MAY SEND YOU

About Sending Communications, Notices and Statements to You

You should promptly review all notices, account statements and other communications (hereafter referred to as “communications”) we send you Many communications will inform you of changes affecting your rights and obligations When we send communications we may:

• address notices to one account owner;

• destroy communications that are sent to you and returned to us as being undeliverable, along with any accompanying checks and other items;

• mail a communication for pickup that remains unclaimed to the address reflected in our records for your account or destroy it;

• authorize the post office or an agent to destroy communications along with accompanying checks and other items that the post office informs us are undeliverable;

• send communications to you at the electronic or street address we have in our records for your account; and

• stop sending communications to you until a new address is provided to us if we reasonably believe that the address we have in our records for your account is wrong

We are not responsible for communications (including enclosed checks) lost while not in our possession If you have requested that we hold your account statements at a branch, the statements shall be deemed to have been delivered to you at the time that they are available to you at the branch

Delivery of Communications about Changes

When we inform you of changes affecting your accounts, rights and obligations, we do so by delivering or making the communication available to you In some cases, we may post a notice of a change in our branches or on our website Otherwise, we may mail the communication regarding a change to you at the address currently in our records or via text message, e-mail, secure messaging or other means (if you have agreed to such method) We may provide a communication as a message on your statement or as a statement insert If a communication of a change is returned to us as undeliverable, or if we stop sending communications to you because previous communications (including account statements) we sent you were returned to us as undeliverable, you understand that copies of such communications can be requested at our branches You agree to these methods of delivery and that changes covered in these communications are effective and binding on you A communication sent to any one account owner is deemed notice to all account owners

14

88024 Personal Account Disclosure R2.indd 14 1/23/18 4:41 PM

Check Images

Check imaging is provided for all checking and any savings or money market account products with check writing privileges All checking and applicable savings or money market accountholders will receive electronically-produced images of the fronts of all checks, including check clearing information, for proof of payment Cancelled check images (front and back) will be stored for seven (7) years, but the actual cancelled checks will not be returned to you If a copy of the front or back of a specific check is necessary, you may request it by calling us at 877 741 9378 or visiting one of our branches Refer to the “Consumer Fee Schedule” for fees related to check copies

Change of Address

You agree to notify us immediately of any change of address We may require that you notify us of any change of address in writing You may request to change your address by calling us at 877 741 9378, visiting one of our branches, or visiting our website at www onewestbank com We may update your mailing address if we receive information from the postal service or a reliable third party that you have moved and have a new address

Changes in Ownership and Authorized Signers

You agree to notify us immediately in writing of any change in your name or the authorized signers on your account We will require a new signature card before any change in ownership or authorized signers becomes effective We may rely solely on our account records to determine the ownership of your account

If the authorized persons on your account change, we may continue to honor items and instructions given earlier by any previously authorized person(s) until we receive specific notice from you in writing not to do so A new or updated signature card, by itself, does not constitute notice to terminate any pre-existing payment or transfer plan In some instances we may require you to close your account or provide us with stop payment orders in order to prevent transactions from occurring There may be a delay in implementing a change in the authorized signers on our records, and you agree that we will be given a reasonable opportunity to make the necessary changes

PROTECTING YOUR ACCOUNTS

Precautions You Should Take

To help prevent fraud and identity theft as well as protect your assets, we recommend that you take the following precautions:

• Do not preprint your driver’s license number, Social Security number or taxpayer identification number on your checks

• Notify us immediately if your debit card or any document containing your identification is lost or stolen

• If your new OneWest Bank ATM or Debit Card does not arrive within a reasonable period of time, call us at the number included in this document

• Blank, paid or cancelled checks for your account and account statements should be safely stored, and, when appropriate, destroyed or shredded before discarding

• Do not share your PIN or any account access password (e g , online banking) with anyone; do not write your PIN on your card or keep it with your card

• Keep accurate records of your account transactions and reconcile your statements as soon as they are made available to you

• Contact us immediately at 877 741 9378 if there are any discrepancies on your statement that you cannot explain or if you do not receive a statement when expected

• If using our mobile banking service, protect your mobile phone or other device with a passcode or other security feature to prevent anyone other than you from accessing your accounts

• Additional information about protecting your accounts is available on www onewestbank com

• Sign up for eStatements in lieu of receiving paper statements in the mail

15

88024 Personal Account Disclosure R2.indd 15 1/23/18 4:41 PM

Closing a Compromised Account

If you or we suspect that your account is or may be compromised (including any unauthorized transactions on the account), we may recommend that you close your account and open a new account If we recommend that you close your account and you do not do so, we are not liable to you for subsequent losses or damages on the account due to unauthorized transactions When you open a new account, you are responsible for notifying any third parties that need to know your new account number

Lost or Stolen Checks

You agree to notify us immediately whenever checks are lost or stolen We will close the account and transfer the balance and any account privileges to a new account of the same type Checks drawn on the “old” account will be returned unpaid unless a timely request is made in writing to pay a particular check(s) The written request must include the check number, dollar amount and the payee name

You must also take precautions in safeguarding your blank checks Notify us immediately if you believe your checks have been lost or stolen If you are negligent in safeguarding your checks, you may bear all or a portion of the loss unless we failed to use ordinary care and substantially contributed to the loss

REPORTING UNAUTHORIZED TRANSACTIONS AND PROBLEMS

Please note that different notice and liability rules apply to certain electronic fund transfers and substitute checks See the sections entitled “Electronic Funds Transfer Agreement and Disclosure” and “Substitute Checks and Your Rights” in this document

Types of Unauthorized Transactions

Some examples of unauthorized transactions or potential problems include: suspected fraud; missing deposits; missing, stolen or unauthorized checks or other withdrawal orders; checks or other withdrawal orders bearing an unauthorized signature, endorsement or alteration; illegible images; encoding errors made by you or us; and counterfeit checks

Reviewing Statements and Reporting Unauthorized Use of Your Account

When we make an account statement available to you, we are required to provide sufficient information to enable you to identify the items paid If we return the paid items, provide an image of the paid items or describe the paid items by item number, amount, and the date of payment, such information shall be treated as sufficient information for the purposes of this Agreement You agree to promptly and carefully examine all statements, notices and paid items that we send or otherwise make available to you and report any discrepancies, problems or unauthorized transactions to us immediately You must promptly report and reimburse us for any erroneous credit You agree that within 30 calendar days after we mail or otherwise make a statement or transaction notice available to you, you must report to us any problem or unauthorized transactions including (without limitation) a claim for credit or refund due for an erroneous debit, a missing signature, an unauthorized signature or an alteration It is agreed that the mailing date for statements is the first business day following the statement date or the date we otherwise make the information available to you

Not Reporting Unauthorized Transactions Timely

If you do not notify us within the time frame specified above, it is agreed that we will conclusively presume that the stated balance is correct regarding debits described on the statement This means that we are released from all liability for the items charged to your account, and for all other transactions or matters covered by the statement If you don’t report to us missing debit items, unauthorized signatures, alterations or other suspected misuse of your account, in addition to any rights we have by law, the Bank will not be responsible for any subsequent forgeries, altered check or other fraudulent uses of your account by the same person that occur after you have been afforded a reasonable period of time (not exceeding 30 calendar days) after we send a statement containing information about the first forgery, alteration or fraudulent transaction

16

88024 Personal Account Disclosure R2.indd 16 1/23/18 4:41 PM

Our Investigation of Your Unauthorized Transaction

If you report to us that a forgery, alteration or other unauthorized transaction has occurred, you agree to cooperate with us in the investigation of your claim You agree to provide us with an affidavit containing the information we require concerning the transaction You also agree to assist us in identifying and prosecuting the suspected wrongdoer(s) You agree that we have a reasonable period of time to investigate the facts surrounding any loss you claim, and that we are under no obligation to provisionally credit your account during our investigation

Our Maximum Liability

Our maximum liability is the lesser of your actual damages proved or the amount of the missing deposit, forgery, alteration or other unauthorized withdrawal, reduced in all cases by the amount of the loss that could have been avoided by your use of ordinary care We are not liable to you for any consequential losses or damages of any kind, including loss of profits or attorneys’ fees incurred by you

FOREIGN CHECKS AND TRANSACTIONS

What is a Foreign Item?

A foreign item is a check or other item in any currency (including United States dollars) that is drawn on a bank or branch of a bank located outside of the United States A foreign currency is any currency other than United States dollars Some foreign items are payable in United States dollars Some are payable in a foreign currency

Being Careful About Accepting Foreign Items

You should be careful about accepting foreign items because they are not subject to United States laws or regulations A foreign item may be returned unpaid much later than checks or other items that are drawn on banks located in the United States If a foreign item is returned to us unpaid or there is some other problem with the foreign item, you are responsible for the item and you may incur a loss

Converting Currency and Exchange Rates

If you conduct a transaction in a currency other than U S dollars, the merchant, network or card association that processes the transaction may convert any related debit or credit into U S dollars in accordance with its policies When we decide to convert a transaction, we may determine in our discretion the currency exchange rate and then assign that currency exchange rate to your transaction without notice to you You agree to this procedure and accept our determination of the currency exchange rate The conversion rate may be different from the rate in effect on the date of your transaction and the date it is posted to your account We may impose a charge equal to 1% of the transaction amount (including credits and reversals) for each transaction that you conduct outside the United States or in a foreign currency

Checks or Other Items in Foreign Currency