accounting & financial analysis

TRANSCRIPT

Accounting & Financial Accounting & Financial AnalysisAnalysis

An IntroductionAn Introduction

Prof. Raman ChawlaProf. Raman Chawla

What is accountingWhat is accounting

Accounting is the art of identifying, Accounting is the art of identifying, recording, classifying and summarizing recording, classifying and summarizing in a significant manner and in terms of in a significant manner and in terms of money transactions and events which money transactions and events which are, in part at least of a financial are, in part at least of a financial character and interpreting the result character and interpreting the result thereof.thereof.

Accounting is a system in which all the Accounting is a system in which all the financial transaction are recorded in a financial transaction are recorded in a proper and system way.proper and system way.

Characteristics of Characteristics of financial accountingfinancial accounting Accounting is an art- Art is that part of knowledge which helps Accounting is an art- Art is that part of knowledge which helps

us in attaining our aim. Accounting helps us in attaining our us in attaining our aim. Accounting helps us in attaining our aim of ascertaining the financial results by showing the best aim of ascertaining the financial results by showing the best way of recording, classifying and summarizing the business way of recording, classifying and summarizing the business transaction.transaction.

Recording, Classifying and summarizing- It provides Recording, Classifying and summarizing- It provides information about all the transactions of financial in nature, information about all the transactions of financial in nature, recorded in journal, classifying in forms of ledgers, preparation recorded in journal, classifying in forms of ledgers, preparation of trial balance for checking the accuracy of accounts.of trial balance for checking the accuracy of accounts.

In terms of money-Only those transaction are recorded which In terms of money-Only those transaction are recorded which are in terms of money.are in terms of money.

Interpreting the results- It provide the tools for their analysis, Interpreting the results- It provide the tools for their analysis, through which various parties of business obtain information through which various parties of business obtain information related to them. related to them.

Objectives or functions Objectives or functions of accountingof accounting Knowledge of sales and purchaseKnowledge of sales and purchase Providing information of closing stockProviding information of closing stock Knowledge of financial positionKnowledge of financial position Information related for working capitalInformation related for working capital Knowledge of profit & loss of the businessKnowledge of profit & loss of the business Provide information to various partiesProvide information to various parties Provide Information about embezzlement & fraudsProvide Information about embezzlement & frauds Evidence in court.Evidence in court.

Functions of Functions of AccountingAccounting It keeps a complete record of business transactions.It keeps a complete record of business transactions. It provides complete information concerning the businessIt provides complete information concerning the business.. It provides a check on the arithmetical accuracy of books It provides a check on the arithmetical accuracy of books

of accounts.of accounts. It discloses the operating results .It discloses the operating results . It makes possible a meaning full comparison of operating It makes possible a meaning full comparison of operating

and financial performance over a period of time and and financial performance over a period of time and enable the businessman to evaluate the progress of his enable the businessman to evaluate the progress of his business.business.

It also enables a business man to plan and control his It also enables a business man to plan and control his operations.operations.

It reduces the chances of committing fraud.It reduces the chances of committing fraud. Past details with regard to any account are easily and Past details with regard to any account are easily and

accurately obtainable in this system. accurately obtainable in this system.

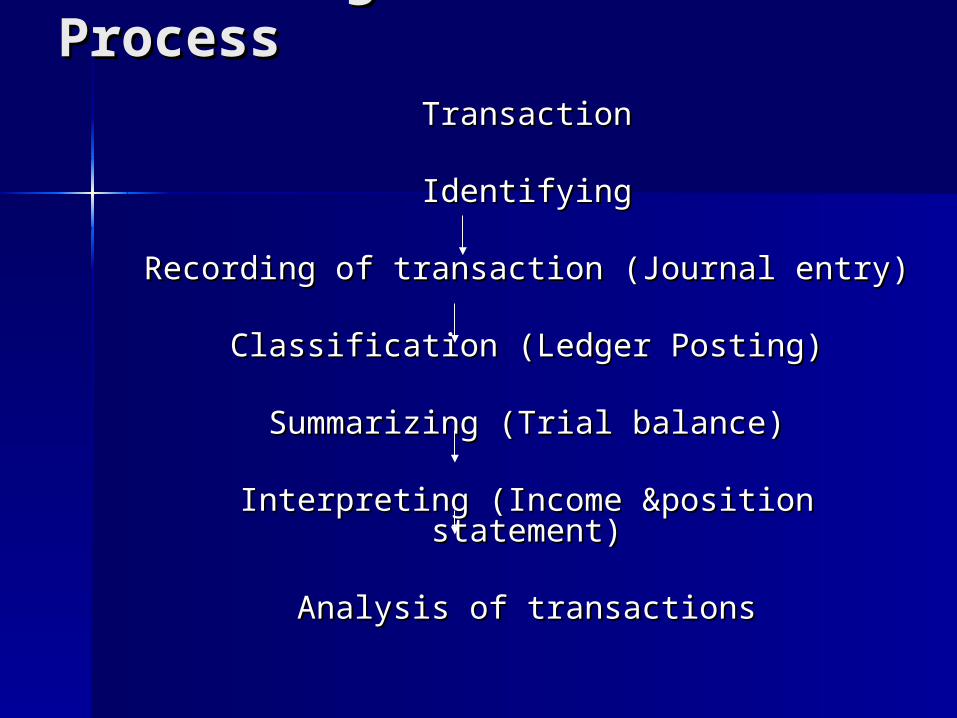

Accounting Accounting ProcessProcess

TransactionTransaction

IdentifyingIdentifying

Recording of transaction (Journal entry)Recording of transaction (Journal entry)

Classification (Ledger Posting)Classification (Ledger Posting)

Summarizing (Trial balance)Summarizing (Trial balance)

Interpreting (Income &position statement)Interpreting (Income &position statement)

Analysis of transactionsAnalysis of transactions

Branches of Branches of AccountingAccounting Financial Accounting:- It is Financial Accounting:- It is

concerned with recording and concerned with recording and processing the financial processing the financial transactions which affect the transactions which affect the financial position of the business. financial position of the business. It leads to the preparation of It leads to the preparation of income statement & position income statement & position statement of the business.statement of the business.

Cost accountingCost accounting

Cost accounting is the process of Cost accounting is the process of accounting for costs. It is a accounting for costs. It is a systematic procedure for determining systematic procedure for determining the unit cost of output produced or the unit cost of output produced or services rendered. The primary services rendered. The primary functions of cost accounting are to functions of cost accounting are to ascertain the cost of a product and to ascertain the cost of a product and to help the management in the control help the management in the control of cost. of cost.

Management Management accountingaccounting It is concerned with the collecting It is concerned with the collecting

systematically and regularly all systematically and regularly all such information as will help to such information as will help to the management in discharging the management in discharging its functions of planning, control, its functions of planning, control, decision making, etc. this is also decision making, etc. this is also named as accounting for named as accounting for management. management.

Users of accounting Users of accounting informationinformation

Internal sources Internal sources

OwnersOwners

ManagementManagement

EmployeesEmployees

External PersonsExternal Persons CreditorsCreditors

GovernmentGovernment InvestorsInvestors

ResearchesResearches LendersLenders

ConsumerConsumer Tax DepartmentTax Department

Cont…Cont…

Owner – A person who is interested Owner – A person who is interested in accounting information to know in accounting information to know about the profit or loss of the about the profit or loss of the business, financial position, amount business, financial position, amount of expenses, amount of capital and of expenses, amount of capital and its size, value of obligations, its size, value of obligations, amount to be paid to the suppliers, amount to be paid to the suppliers, details of purchase or sale.details of purchase or sale.

ManagementManagement The management needs The management needs

information from accounting for information from accounting for successful, efficient and smooth successful, efficient and smooth running of business operations. The running of business operations. The management can evaluate the management can evaluate the progress and future plans based on progress and future plans based on accounting information. Shot term accounting information. Shot term and long term plans can be and long term plans can be prepared on the basis of financial prepared on the basis of financial information.information.

EmployeesEmployees

Employees are interested in Employees are interested in accounting information of the accounting information of the business as their welfare scheme business as their welfare scheme like bonus, salaries, fringe like bonus, salaries, fringe benefits, provident funds, benefits, provident funds, Gratuity etc. Gratuity etc.

Creditors / Supplier Creditors / Supplier Creditors are those parties that Creditors are those parties that

provide a firm with raw materials, provide a firm with raw materials, goods and services on credit way. goods and services on credit way. They are interested to know They are interested to know about the credit worthiness about the credit worthiness status, financial positions of the status, financial positions of the current year.current year.

GovernmentGovernment

Government has collected sales Government has collected sales tax, income tax, excise duty and tax, income tax, excise duty and other taxes from the business. other taxes from the business. For this it is necessary that proper For this it is necessary that proper accounts are made available to accounts are made available to the government.the government.

investorsinvestors Investors provide risk capital to Investors provide risk capital to

the business. They are interested the business. They are interested in accounting information to know in accounting information to know about the survival, prosperity, about the survival, prosperity, profitability, and ability to pay profitability, and ability to pay dividend. dividend.

Researchers Researchers

The researchers are interested in The researchers are interested in interpreting the financial interpreting the financial statements of the concern for a statements of the concern for a given objective.given objective.

LendersLenders Lenders are the persons who Lenders are the persons who

provide the loan to the business. provide the loan to the business. They are interested to know They are interested to know about the use of money, interest about the use of money, interest and how safe the funds are?and how safe the funds are?

consumersconsumers Consumers are interested in Consumers are interested in

buying goods at the reasonable buying goods at the reasonable price. price.

Generally Accepted Generally Accepted Accounting principles Accounting principles (GAAP)(GAAP)

Business Entity ConceptBusiness Entity Concept Going Concern conceptGoing Concern concept Dual Aspect ConceptDual Aspect Concept Cost conceptCost concept Money measurement ConceptMoney measurement Concept Accounting period ConceptAccounting period Concept Matching ConceptMatching Concept Accrual conceptAccrual concept

Business entity Business entity conceptconcept Business is treated as a unit or entity Business is treated as a unit or entity

apart from its owner. The owner of an apart from its owner. The owner of an organization is always considered to organization is always considered to be separate and distinct from the be separate and distinct from the business which he controls. that is business which he controls. that is why, the capital of the owner is why, the capital of the owner is always entered in liability side of always entered in liability side of balance sheet. It is considered as the balance sheet. It is considered as the creditor of the business.creditor of the business.

Going concern conceptGoing concern concept It is assumed that the business will It is assumed that the business will

exist for the foreseeable future and exist for the foreseeable future and transactions are recorded from this transactions are recorded from this point of view. It should continue to point of view. It should continue to operate at its present scale in the operate at its present scale in the foreseeable future. foreseeable future.

Dual Aspect Concept Dual Aspect Concept Financial accounting has dual Financial accounting has dual

aspect of recording. Every debit aspect of recording. Every debit has its corresponding credit & has its corresponding credit & every credit has its corresponding every credit has its corresponding debit. The modern accounting debit. The modern accounting system basically based on dual system basically based on dual aspect of accounting. aspect of accounting.

Cost concept Cost concept The underlying idea of cost concept is The underlying idea of cost concept is

that-that- Assets is recorded at the price paid to Assets is recorded at the price paid to

acquire it, that is, at cost, and..acquire it, that is, at cost, and.. This cost is the basis for all subsequent This cost is the basis for all subsequent

accounting for the asset. accounting for the asset. The change in the real worth of an asset The change in the real worth of an asset

with the passage of time is not ordinarily with the passage of time is not ordinarily recorded in the account books.recorded in the account books.

Money measurement Money measurement conceptconcept The money concept underlines the The money concept underlines the

fact that in accounting every worth fact that in accounting every worth recording event, happening or recording event, happening or transaction is recorded in terms of transaction is recorded in terms of money. In other words, a fact or a money. In other words, a fact or a happening which cannot be happening which cannot be expressed in terms of money is not expressed in terms of money is not recorded in the accounting books.recorded in the accounting books.

Accounting period Accounting period conceptconcept

Accounts choose some shorter Accounts choose some shorter and convenient time for the and convenient time for the measurement of income. Twelve-measurement of income. Twelve-month period is normally adopted month period is normally adopted for this purpose. this time interval for this purpose. this time interval is called accounting period.is called accounting period.

Matching conceptMatching concept It is based on the determination of the It is based on the determination of the

profit & loss of a particular accounting profit & loss of a particular accounting period is the process of matching the period is the process of matching the revenue earned during the period and revenue earned during the period and the expenses incurred during the the expenses incurred during the period to obtain such revenue.period to obtain such revenue.

Accrual concept Accrual concept

Under this method revenue recognition Under this method revenue recognition depends on its realization and not depends on its realization and not actual receipt. Likewise costs are actual receipt. Likewise costs are recognized when they are incurred and recognized when they are incurred and not when paid. not when paid.

Accounting conventionsAccounting conventions ConsistencyConsistency Full disclosureFull disclosure ConservatismConservatism

ConsistencyConsistency The convention of consistency aims at The convention of consistency aims at

making the financial statements more making the financial statements more comparable and useful. The comparable and useful. The convention holds that in accounting convention holds that in accounting processes, all concepts, principles processes, all concepts, principles and measurement approaches should and measurement approaches should be applied in a similar or consistent be applied in a similar or consistent way from one period to another way from one period to another period.period.

Full disclosureFull disclosure This convention specifies that there This convention specifies that there

should be complete and understandable should be complete and understandable reporting in the financial statements of reporting in the financial statements of all significant information relating to the all significant information relating to the economic affairs of the entity. All economic affairs of the entity. All information which is of material interest information which is of material interest to the users of the accounting to the users of the accounting information should be disclosed in information should be disclosed in accounting statements. accounting statements.

ConservatismConservatism This is the policy of playing safe. This is the policy of playing safe.

Accounting permits for making Accounting permits for making reserves to face the uncertainty reserves to face the uncertainty situations of the business.situations of the business.

Double entry systemDouble entry system

It is a common system of book-keeping It is a common system of book-keeping whereby the two aspects of every whereby the two aspects of every transaction i.e., It is based on the dual transaction i.e., It is based on the dual aspect conceptaspect concept. . This method of writing This method of writing every transaction in two different accounts every transaction in two different accounts on opposite sides for equal value is known on opposite sides for equal value is known as the double entry system of book keeping. as the double entry system of book keeping. This is the most accurate, complete and This is the most accurate, complete and scientific system of accounting.scientific system of accounting.

Advantages of double entry Advantages of double entry systemsystem

It keeps a complete record of business transactions.It keeps a complete record of business transactions. It provides complete information concerning the businessIt provides complete information concerning the business.. It provides a check on the arithmetical accuracy of books It provides a check on the arithmetical accuracy of books

of accounts.of accounts. It discloses the operating results .It discloses the operating results . It makes possible a meaning full comparison of operating It makes possible a meaning full comparison of operating

and financial performance over a period of time and enable and financial performance over a period of time and enable the businessman to evaluate the progress of his business.the businessman to evaluate the progress of his business.

It also enables a business man to plan and control his It also enables a business man to plan and control his operations.operations.

It reduces the chances of committing fraud.It reduces the chances of committing fraud. Past details with regard to any account are easily and Past details with regard to any account are easily and

accurately obtainable in this system. accurately obtainable in this system.

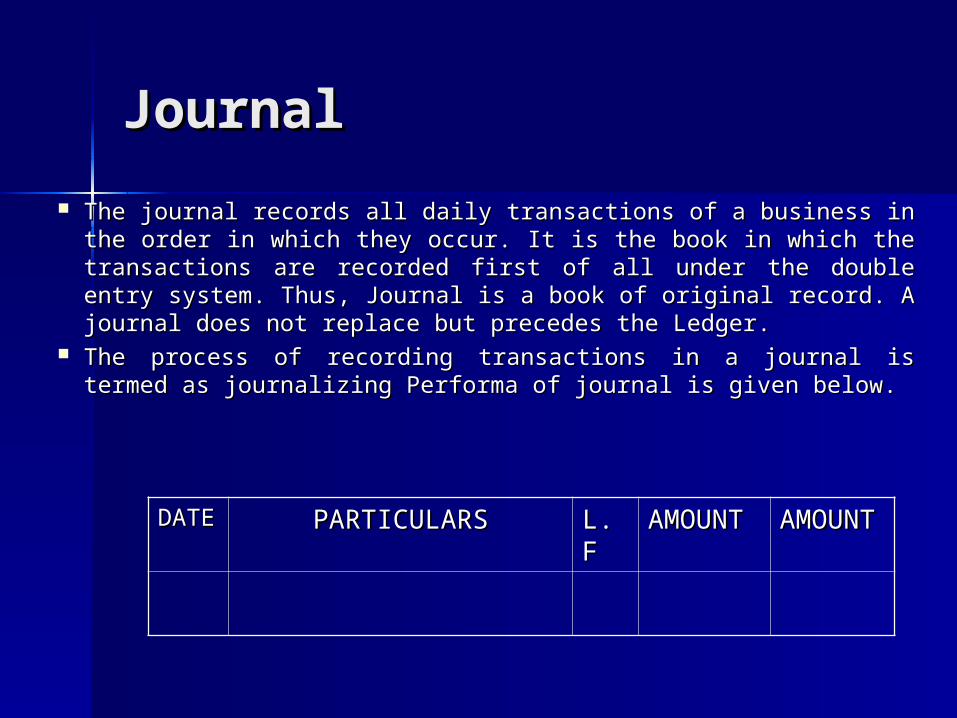

JournalJournal The journal records all daily transactions of a business in the order The journal records all daily transactions of a business in the order

in which they occur. It is the book in which the transactions are in which they occur. It is the book in which the transactions are recorded first of all under the double entry system. Thus, Journal is recorded first of all under the double entry system. Thus, Journal is a book of original record. A journal does not replace but precedes a book of original record. A journal does not replace but precedes the Ledger.the Ledger.

The process of recording transactions in a journal is termed as The process of recording transactions in a journal is termed as journalizing Performa of journal is given below.journalizing Performa of journal is given below.

DATDATEE

PARTICULARSPARTICULARS L.FL.F AMOUNAMOUNTT

AMOUNAMOUNTT

ExplanationExplanation

1. Date: The date on which the transaction was 1. Date: The date on which the transaction was entered is recorded here.entered is recorded here.

2. Particulars: The two aspect of transaction are 2. Particulars: The two aspect of transaction are recorded in this column,i.e, the details regarding recorded in this column,i.e, the details regarding accounts which have to be debited and credited.accounts which have to be debited and credited.

L.F: It means ledger folio. The transactions entered in L.F: It means ledger folio. The transactions entered in the journal are later on posted to the ledger. the journal are later on posted to the ledger. Procedure regarding posting the transactions in the Procedure regarding posting the transactions in the ledger has been explained in the succeeding chapter.ledger has been explained in the succeeding chapter.

Debit. In this column, the amount to be debited is Debit. In this column, the amount to be debited is enteredentered

Credit. In this column, The amount to be credited is Credit. In this column, The amount to be credited is shownshown

Golden rules of Golden rules of accountingaccounting

Real account- Debit what comes in, Real account- Debit what comes in, Credit what goes out.Credit what goes out.

Personal account- Debit the Personal account- Debit the receivers, Credit the givers.receivers, Credit the givers.

Nominal account- Debit the Nominal account- Debit the expenses & losses, Credit the expenses & losses, Credit the incomes & gains.incomes & gains.

LedgerLedger The second important part of The second important part of

accounting cycle of double entry accounting cycle of double entry system is the classification of system is the classification of transactions i.e. posting in the ledger transactions i.e. posting in the ledger book.book.

The ledger is the main book of The ledger is the main book of account, and it is in this book that all account, and it is in this book that all the business transactions would the business transactions would ultimately find their place under their ultimately find their place under their place under their respective accounts place under their respective accounts in a duly classified form. in a duly classified form.

Need and importance Need and importance of ledgerof ledger The information regarding any account can be The information regarding any account can be

obtained one place.obtained one place. It saves time.It saves time. It provides information of total purchases, sales and It provides information of total purchases, sales and

the status of return for a particular period.the status of return for a particular period. The information of account receivables and payable The information of account receivables and payable

can be obtained known from it.can be obtained known from it. The information of income and expenditure can be The information of income and expenditure can be

obtained separatelyobtained separately.. The information of assets and liabilities of the concern The information of assets and liabilities of the concern

can be obtainedcan be obtained.. It helps in the preparation of trial balance and balance It helps in the preparation of trial balance and balance

sheet. sheet.

Trial balanceTrial balance A trial balance is a statement of A trial balance is a statement of

debit and credit balances debit and credit balances extracted from all ledgers with a extracted from all ledgers with a view to ascertain arithmetic view to ascertain arithmetic accuracy of the posting of all accuracy of the posting of all transactions into the respective transactions into the respective ledgers. ledgers.

DefinitionDefinition The first list of balances, which is added The first list of balances, which is added

and totaled, called a trial balance.and totaled, called a trial balance. A trial balance is a list of all the balances A trial balance is a list of all the balances

standing on the ledger accounts of the standing on the ledger accounts of the concern at any given date.concern at any given date.

Objectives of trial Objectives of trial balancebalance Test of arithmetical accuracy of ledger Test of arithmetical accuracy of ledger

accountsaccounts To observe the application of the rules To observe the application of the rules

of double entry systemof double entry system Summary of ledger accountSummary of ledger account Basis for preparing final accountsBasis for preparing final accounts Useful for making adjustmentsUseful for making adjustments

Errors disclosed by Errors disclosed by trial balancetrial balance If books of accounts are properly If books of accounts are properly

maintained according to the principles of maintained according to the principles of double entry system both the debit and double entry system both the debit and credit side of the trial balance must credit side of the trial balance must equal to each other. In case both sides equal to each other. In case both sides are not equal, there is bound to be are not equal, there is bound to be certain error in accounting. The trial certain error in accounting. The trial balance in case of disagreement is said balance in case of disagreement is said to be out of balance. Following errors are to be out of balance. Following errors are responsible for disagreement of trial responsible for disagreement of trial balance.balance.

Cont..Cont.. Errors of additions and subtractions- these Errors of additions and subtractions- these

errors make trial balance ‘out of balance’. errors make trial balance ‘out of balance’. Errors of additions and subtractions may occur Errors of additions and subtractions may occur in the subsidiary books or in the ledger account in the subsidiary books or in the ledger account or even in the trial balance itself. The trial or even in the trial balance itself. The trial balance will disclose the errors. These errors balance will disclose the errors. These errors may be enumerated as under-may be enumerated as under-

Errors in the amount column of cash book.Errors in the amount column of cash book. Errors in the balancing of cash bookErrors in the balancing of cash book Errors in the subsidiary booksErrors in the subsidiary books Wrong totaling and balancing of ledger Wrong totaling and balancing of ledger

accounts accounts Wrong totaling in trial balance. Wrong totaling in trial balance.

Cont….Cont…. Posting at the wrong side of an account-Posting at the wrong side of an account-

In case the posting is made at the wrong side In case the posting is made at the wrong side of any specific account, the trial balance will of any specific account, the trial balance will not tally.not tally.

Entering incorrect amount-Entering incorrect amount- This error may This error may occur, when we copy wrong figures, in any occur, when we copy wrong figures, in any type of book of account. Ex. Writing 59 in type of book of account. Ex. Writing 59 in place of 95 or 123 in place of 321.place of 95 or 123 in place of 321.

Cont..Cont.. Errors of omission-Errors of omission- All the omissions taking All the omissions taking

place in posting or in the trial balance will place in posting or in the trial balance will throw out the trial balance. Following are the throw out the trial balance. Following are the examples of such errors: examples of such errors:

1. If an item has not been posted at all from 1. If an item has not been posted at all from subsidiary books to ledger.subsidiary books to ledger.

2. If the balance of any ledger account has 2. If the balance of any ledger account has not been posted to trial balance.not been posted to trial balance.

Wrong posting in the trial balance- Wrong posting in the trial balance- IfIf the the debit balance of an account has been posted debit balance of an account has been posted at the credit side of trial balance or the credit at the credit side of trial balance or the credit balance has been posted at the debit side of balance has been posted at the debit side of the trial balance.the trial balance.

Limitations of trial balanceLimitations of trial balanceErrors not disclosed by trial Errors not disclosed by trial balancebalance Trial balance is taken as test of arithmetical Trial balance is taken as test of arithmetical

accuracy. If both the side of trial balance are accuracy. If both the side of trial balance are equal to each other, we assume that there is equal to each other, we assume that there is no mistake in the posting of journal and no mistake in the posting of journal and subsidiary books to ledger accounts, in subsidiary books to ledger accounts, in carrying forward balances of ledger accounts to carrying forward balances of ledger accounts to trial balance and even in the balancing of trial balance and even in the balancing of ledger accounts. This assumption is correct but ledger accounts. This assumption is correct but should never be taken as conclusive proof of should never be taken as conclusive proof of accuracy. It means that there are certain errors accuracy. It means that there are certain errors which remain undetected by trial balance. Both which remain undetected by trial balance. Both the debit and credit side of trial balance may the debit and credit side of trial balance may be equal in spite of certain mistakes of be equal in spite of certain mistakes of omissions and principles. There are as….omissions and principles. There are as….

Cont..Cont.. Errors of omission in the original record-TheErrors of omission in the original record-The

entire transaction is not recorded in the books of entire transaction is not recorded in the books of accounts, we omit to the transaction. Ex – goods accounts, we omit to the transaction. Ex – goods returned by Mohan were taken into the stock but the returned by Mohan were taken into the stock but the return was not entered in the books. return was not entered in the books.

Errors of principle- Errors of principle- Errors of principles may be Errors of principles may be committed, if we debit or credit a wrong account due committed, if we debit or credit a wrong account due to our ignorance. The accountant does not have the to our ignorance. The accountant does not have the understanding of the accounting concepts and understanding of the accounting concepts and commits errors. Ex- purchase of building is capital commits errors. Ex- purchase of building is capital expenditure and building account should be debited expenditure and building account should be debited but if the accountant debits purchases account but if the accountant debits purchases account instead of building account, errors of principles will be instead of building account, errors of principles will be there in account.there in account.

Cont..Cont.. Compensating errors- Compensating errors- It is justIt is just possible that the effect possible that the effect

of certain error is neutralized by the effect of another of certain error is neutralized by the effect of another error. the combined effect of the two errors will equalize error. the combined effect of the two errors will equalize the debit and credit side of trial balance in spite of errors. the debit and credit side of trial balance in spite of errors. Ex-sale of goods to Mohan for Rs. 100 was debited to Ex-sale of goods to Mohan for Rs. 100 was debited to Mohan‘s account with Rs. 10 only. Rs. 100. received from Mohan‘s account with Rs. 10 only. Rs. 100. received from Sohan was credited to Sohan’s account with Rs. 10 only. Sohan was credited to Sohan’s account with Rs. 10 only. In the first error, Mohan’s account was debited with Rs. In the first error, Mohan’s account was debited with Rs. 10 only, whereas it should have been debited with Rs. 10 only, whereas it should have been debited with Rs. 100. it means that Rs. 90 was debited short. The effect of 100. it means that Rs. 90 was debited short. The effect of the error in the trial balance will be that the total of the the error in the trial balance will be that the total of the debit side will be Rs.90 lesser. The second error Sohan’s debit side will be Rs.90 lesser. The second error Sohan’s account has been credited with Rs. 10. whereas it should account has been credited with Rs. 10. whereas it should have been credited with Rs. 100. it shows that Rs. 90 have been credited with Rs. 100. it shows that Rs. 90 have been written lesser at the credit side of Sohan’s have been written lesser at the credit side of Sohan’s account. As per the effect of this error, the total of the account. As per the effect of this error, the total of the credit column of trial balance will becredit column of trial balance will be lesser by Rs. 90.. lesser by Rs. 90..

Cont…Cont… In correct account in the original book-In correct account in the original book- If If

the name of wrong account are used in the journal or the name of wrong account are used in the journal or subsidiary books, trial balance will not be able to subsidiary books, trial balance will not be able to direct it . Ex- sale of goods to Amit Rs. 100. was direct it . Ex- sale of goods to Amit Rs. 100. was debited in the books of amitabh.debited in the books of amitabh.

Posting to wrong account- Posting to wrong account- If the posting If the posting from the debit side or credit side of cash book or from from the debit side or credit side of cash book or from purchases book or sales book or returns book is made purchases book or sales book or returns book is made to wrong account but at the correct amount, both the to wrong account but at the correct amount, both the debit and credit side of trial balance will equal in spite debit and credit side of trial balance will equal in spite of these errorsof these errors..

Depreciation Depreciation Loss in the value and utility of assets due Loss in the value and utility of assets due

to their constant use of and expiry of time to their constant use of and expiry of time is termed as depreciation.is termed as depreciation.

Depreciation is gradual and permanent Depreciation is gradual and permanent decrease in the value of assets from any decrease in the value of assets from any cause.cause.

Depreciation may be defined as permanent Depreciation may be defined as permanent and continuing diminution in the quality, and continuing diminution in the quality, quantity or the value of an asset. quantity or the value of an asset.

Special features of Special features of depreciationdepreciation Depreciation is loss in the value of assets.Depreciation is loss in the value of assets. Loss should be gradual and constant.Loss should be gradual and constant. Depreciation is the exhaution of the Depreciation is the exhaution of the

effective life of business.effective life of business. Depreciation is the normal feature.Depreciation is the normal feature. Maintenance of assets is not depreciation.Maintenance of assets is not depreciation. It is continuing decrease in the value of It is continuing decrease in the value of

assets..assets..

Word related with Word related with depreciationdepreciation Obsolescence – Sometimes new inventions throw Obsolescence – Sometimes new inventions throw

away the existing machine and equipments as away the existing machine and equipments as obsolete (useless) although the old machines and obsolete (useless) although the old machines and equipments are not completely useless. Loss due to equipments are not completely useless. Loss due to the useless of old machine and equipment is known as the useless of old machine and equipment is known as obsolescence.obsolescence.

Depletion – the firm may possess certain minerals Depletion – the firm may possess certain minerals wealth such as coal, oil, ore etc. The more we extract wealth such as coal, oil, ore etc. The more we extract mineral wealth from these mines the more mines are mineral wealth from these mines the more mines are depleted. Decrease in mineral wealth of the mines is depleted. Decrease in mineral wealth of the mines is termed as depletion.termed as depletion.

Amortization – the word amortization is used to show Amortization – the word amortization is used to show loss in the value of intangible assets. These assets are loss in the value of intangible assets. These assets are goodwill , patents and preliminary expenses etc. these goodwill , patents and preliminary expenses etc. these assets are written off over certain period. assets are written off over certain period.

Fluctuation Fluctuation Increase and decrease in the Increase and decrease in the

market value of assets is known market value of assets is known as fluctuation. as fluctuation.

Causes of depreciationCauses of depreciation

By constant useBy constant use By expiry of timeBy expiry of time By obsolescenceBy obsolescence By depletionBy depletion Permanent fall in price Permanent fall in price By accidentsBy accidents

Need for charging Need for charging depreciationdepreciation For determining of net profit or net lossFor determining of net profit or net loss For showing assets at fair and true For showing assets at fair and true

value in the balance sheet value in the balance sheet Provisions of funds for replacement of Provisions of funds for replacement of

assetsassets Ascertaining accurate cost of productionAscertaining accurate cost of production Distribution of dividend out of profit onlyDistribution of dividend out of profit only Avoiding over payment of income taxAvoiding over payment of income tax

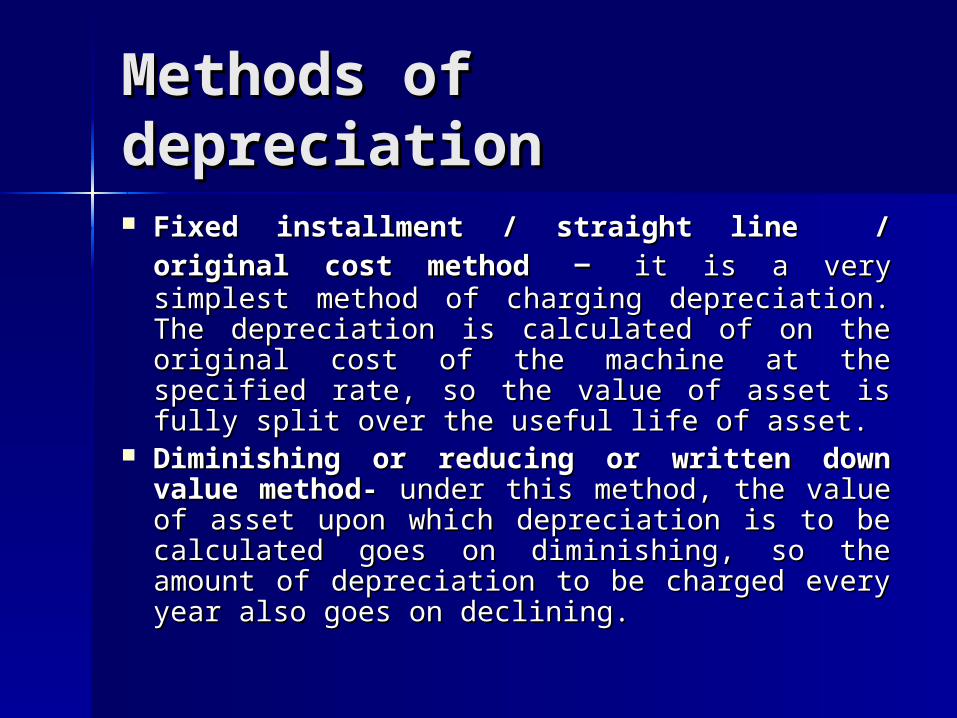

Methods of Methods of depreciationdepreciation Fixed installment / straight line / original Fixed installment / straight line / original

cost methodcost method – – it is a very simplest method of it is a very simplest method of charging depreciation. The depreciation is charging depreciation. The depreciation is calculated of on the original cost of the calculated of on the original cost of the machine at the specified rate, so the value of machine at the specified rate, so the value of asset is fully split over the useful life of asset.asset is fully split over the useful life of asset.

Diminishing or reducing or written down Diminishing or reducing or written down value method- value method- under this method, the value under this method, the value of asset upon which depreciation is to be of asset upon which depreciation is to be calculated goes on diminishing, so the amount calculated goes on diminishing, so the amount of depreciation to be charged every year also of depreciation to be charged every year also goes on declining. goes on declining.

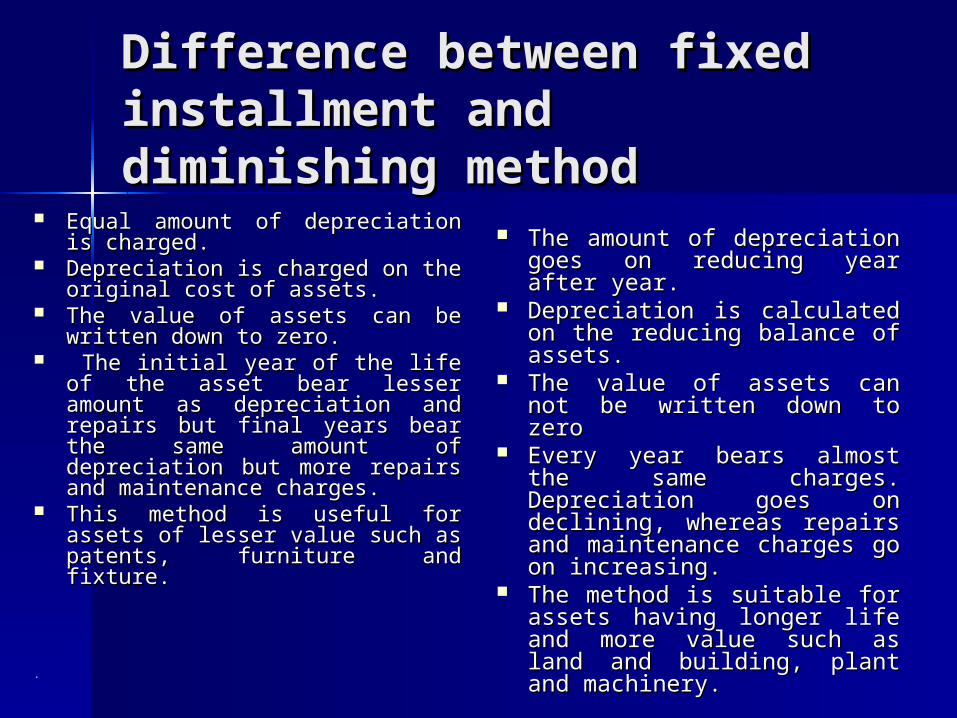

Difference between fixed Difference between fixed installment and diminishing installment and diminishing methodmethod

Equal amount of depreciation is Equal amount of depreciation is charged.charged.

Depreciation is charged on the Depreciation is charged on the original cost of assets.original cost of assets.

The value of assets can be The value of assets can be written down to zero.written down to zero.

The initial year of the life of the The initial year of the life of the asset bear lesser amount as asset bear lesser amount as depreciation and repairs but final depreciation and repairs but final years bear the same amount of years bear the same amount of depreciation but more repairs depreciation but more repairs and maintenance charges.and maintenance charges.

This method is useful for assets This method is useful for assets of lesser value such as patents, of lesser value such as patents, furniture and fixture. furniture and fixture.

..

The amount of depreciation The amount of depreciation goes on reducing year after goes on reducing year after year.year.

Depreciation is calculated on Depreciation is calculated on the reducing balance of the reducing balance of assets.assets.

The value of assets can not The value of assets can not be written down to zerobe written down to zero

Every year bears almost the Every year bears almost the same charges. Depreciation same charges. Depreciation goes on declining, whereas goes on declining, whereas repairs and maintenance repairs and maintenance charges go on increasing.charges go on increasing.

The method is suitable for The method is suitable for assets having longer life and assets having longer life and more value such as land and more value such as land and building, plant and building, plant and machinery.machinery.

ACCOUNTING ACCOUNTING STANDARDSSTANDARDS

Accounting bodies all over the world Accounting bodies all over the world have tried to achieve some uniformity have tried to achieve some uniformity in the accounting policies by in the accounting policies by prescribing certain accounting prescribing certain accounting standards in order to narrow the standards in order to narrow the range of alternatives available to an range of alternatives available to an organization in respect of collection organization in respect of collection and presentation of accounting and presentation of accounting information.information.

International International accounting standardaccounting standard Accounting bodies throughout the world are Accounting bodies throughout the world are

striving to achieve a reasonable degree of striving to achieve a reasonable degree of uniformity in the accounting policies by uniformity in the accounting policies by prescribing certain accounting standards with prescribing certain accounting standards with respect to the collection and presentation of respect to the collection and presentation of accounting information. To formulate the accounting information. To formulate the accounting standards, they have established a accounting standards, they have established a committee called the International Accounting committee called the International Accounting standards committee (IASC) in 1973.Accounting standards committee (IASC) in 1973.Accounting bodies of most of the countries, including the bodies of most of the countries, including the institute of chartered accountants of India, are institute of chartered accountants of India, are the members of this bodies. the members of this bodies.

Objectives of Objectives of committeecommittee

i) formulating, publishing and i) formulating, publishing and promoting the use of the accounting promoting the use of the accounting standards worldwide,standards worldwide,

ii) To work for improvement.ii) To work for improvement.

The IASC has so far issued forty one The IASC has so far issued forty one accounting standardaccounting standard

Indian accounting Indian accounting standardsstandards

Recognizing the need to harmonized the Recognizing the need to harmonized the diverse accounting policies and practices diverse accounting policies and practices prevalent in India. The institute of chartered prevalent in India. The institute of chartered accountants of India constituted an accounting accountants of India constituted an accounting standard board (ASB) on 21standard board (ASB) on 21stst april,1977.The april,1977.The main function of ASB is to frame accounting main function of ASB is to frame accounting standards which would be formally issued standards which would be formally issued under the authority of the council of the under the authority of the council of the institute of chartered accountants.institute of chartered accountants.

Importance of accounting Importance of accounting standardsstandards

The role of mandatory accounting The role of mandatory accounting standards in presenting clear-cut account standards in presenting clear-cut account on a uniform basis can not on a uniform basis can not overemphasized. The standards overemphasized. The standards represent the ideal practice of accounting represent the ideal practice of accounting and ensure comparability of accounts and ensure comparability of accounts because of uniformity in the presentation. because of uniformity in the presentation. Hence, such accounts are bound to show Hence, such accounts are bound to show the clear position of the state of affairs.the clear position of the state of affairs.

Accounting standards Accounting standards issued by ASB of ICAIissued by ASB of ICAI

The ASB of the institute of The ASB of the institute of chartered accountants of India, chartered accountants of India, has in line with the international has in line with the international standards, issued twenty nine standards, issued twenty nine standards to be followed by its standards to be followed by its members while auditing the members while auditing the accounts of companies. These accounts of companies. These are – are –

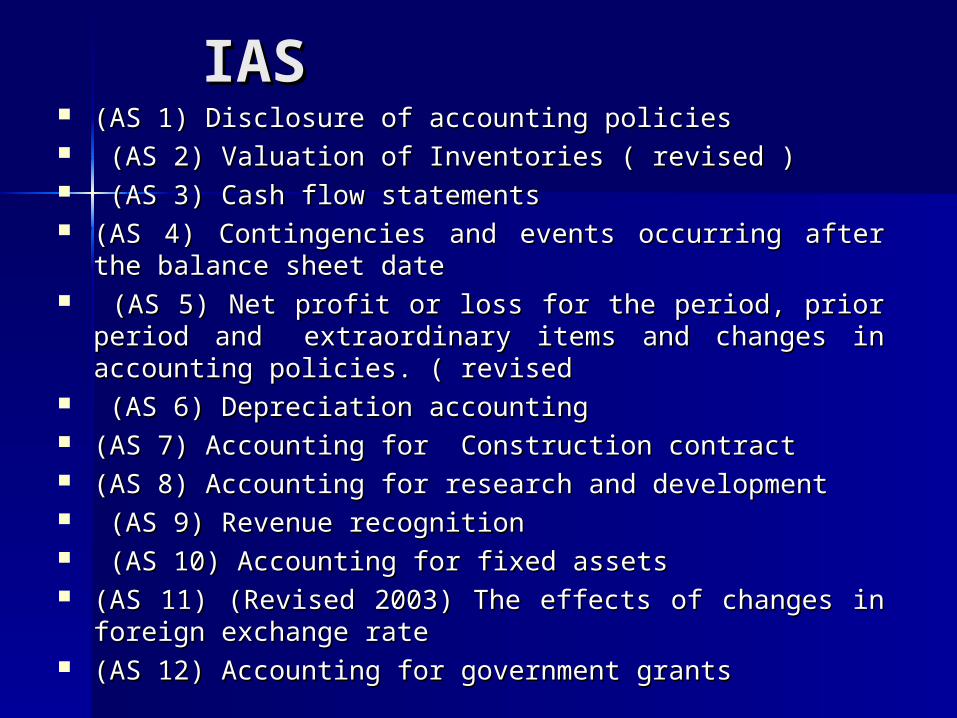

IASIAS (AS 1) Disclosure of accounting policies (AS 1) Disclosure of accounting policies (AS 2) Valuation of Inventories ( revised )(AS 2) Valuation of Inventories ( revised ) (AS 3) Cash flow statements(AS 3) Cash flow statements (AS 4) Contingencies and events occurring after the (AS 4) Contingencies and events occurring after the

balance sheet datebalance sheet date (AS 5) Net profit or loss for the period, prior period and (AS 5) Net profit or loss for the period, prior period and

extraordinary items and changes in accounting policies. extraordinary items and changes in accounting policies. ( revised( revised

(AS 6) Depreciation accounting (AS 6) Depreciation accounting (AS 7) Accounting for Construction contract(AS 7) Accounting for Construction contract (AS 8) Accounting for research and development(AS 8) Accounting for research and development (AS 9) Revenue recognition(AS 9) Revenue recognition (AS 10) Accounting for fixed assets(AS 10) Accounting for fixed assets (AS 11) (Revised 2003) The effects of changes in foreign (AS 11) (Revised 2003) The effects of changes in foreign

exchange rateexchange rate (AS 12) Accounting for government grants(AS 12) Accounting for government grants

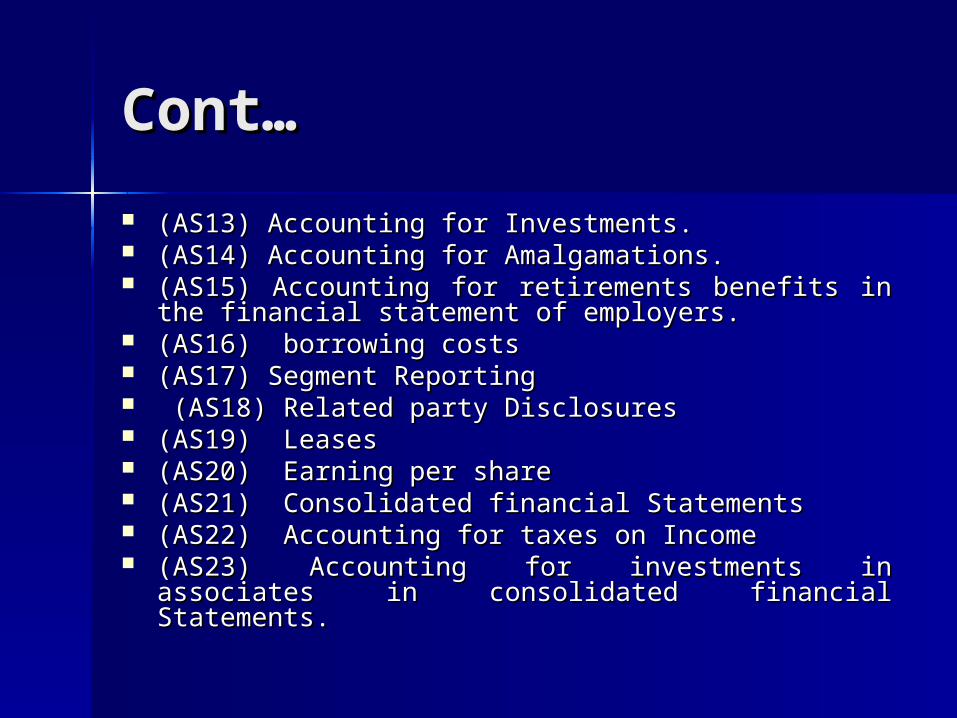

Cont…Cont… (AS13) Accounting for Investments.(AS13) Accounting for Investments. (AS14) Accounting for Amalgamations.(AS14) Accounting for Amalgamations. (AS15) Accounting for retirements benefits in the (AS15) Accounting for retirements benefits in the

financial statement of employers.financial statement of employers. (AS16) borrowing costs(AS16) borrowing costs (AS17) Segment Reporting(AS17) Segment Reporting (AS18) Related party Disclosures(AS18) Related party Disclosures (AS19) Leases(AS19) Leases (AS20) Earning per share(AS20) Earning per share (AS21) Consolidated financial Statements(AS21) Consolidated financial Statements (AS22) Accounting for taxes on Income(AS22) Accounting for taxes on Income (AS23) Accounting for investments in associates in (AS23) Accounting for investments in associates in

consolidated financial Statements.consolidated financial Statements.

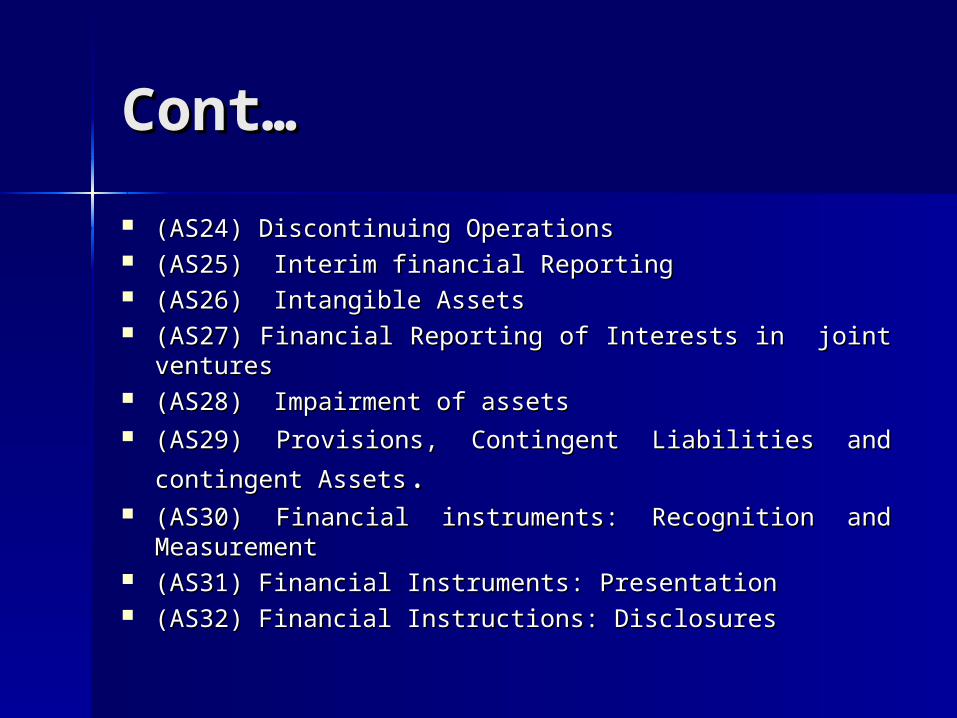

Cont…Cont… (AS24) Discontinuing Operations(AS24) Discontinuing Operations (AS25) Interim financial Reporting(AS25) Interim financial Reporting (AS26) Intangible Assets(AS26) Intangible Assets (AS27) Financial Reporting of Interests in joint ventures(AS27) Financial Reporting of Interests in joint ventures (AS28) Impairment of assets(AS28) Impairment of assets (AS29) Provisions, Contingent Liabilities and contingent (AS29) Provisions, Contingent Liabilities and contingent

AssetsAssets.. (AS30) Financial instruments: Recognition and (AS30) Financial instruments: Recognition and

MeasurementMeasurement (AS31) Financial Instruments: Presentation(AS31) Financial Instruments: Presentation (AS32) Financial Instructions: Disclosures(AS32) Financial Instructions: Disclosures

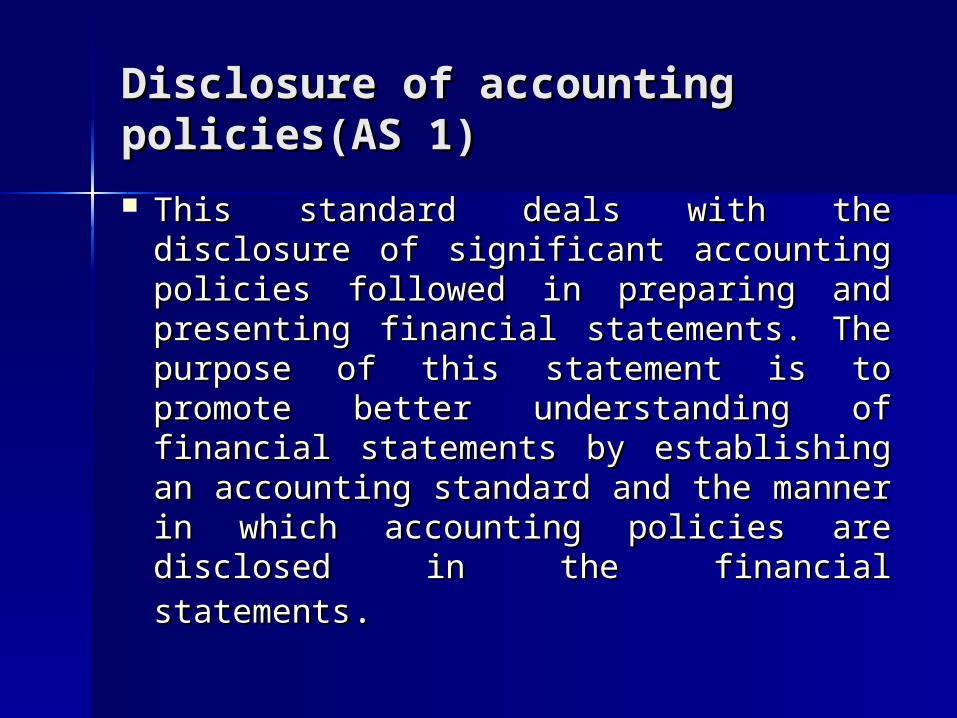

Disclosure of accounting Disclosure of accounting policies(AS 1)policies(AS 1) This standard deals with the disclosure This standard deals with the disclosure

of significant accounting policies of significant accounting policies followed in preparing and presenting followed in preparing and presenting financial statements. The purpose of financial statements. The purpose of this statement is to promote better this statement is to promote better understanding of financial statements understanding of financial statements by establishing an accounting standard by establishing an accounting standard and the manner in which accounting and the manner in which accounting policies are disclosed in the financial policies are disclosed in the financial statementsstatements..

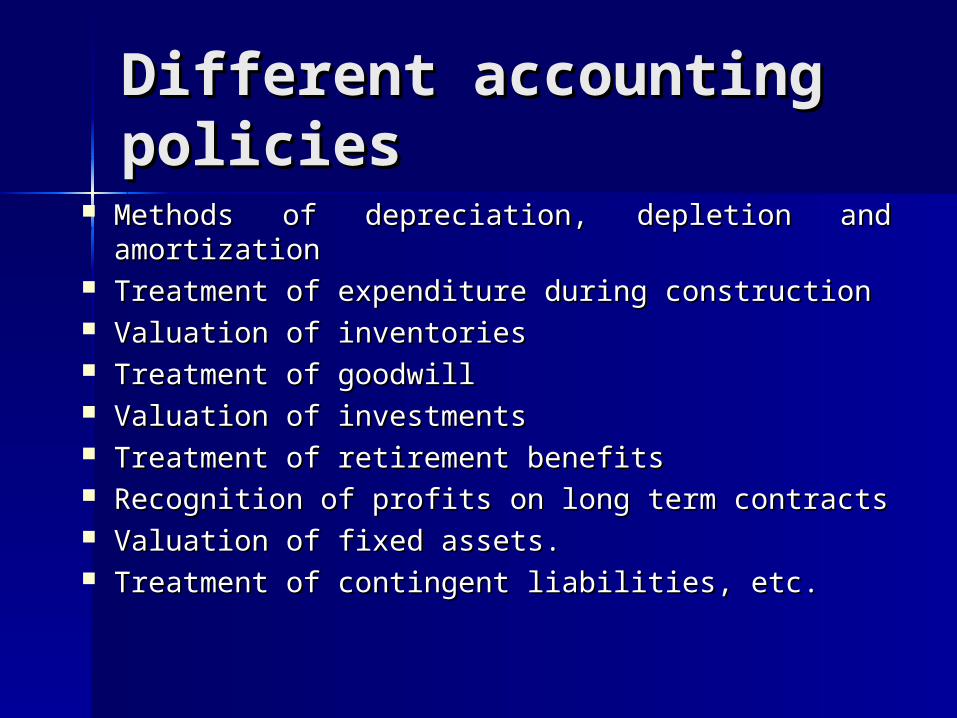

Different accounting Different accounting policies policies

Methods of depreciation, depletion and Methods of depreciation, depletion and amortizationamortization

Treatment of expenditure during constructionTreatment of expenditure during construction Valuation of inventoriesValuation of inventories Treatment of goodwillTreatment of goodwill Valuation of investmentsValuation of investments Treatment of retirement benefitsTreatment of retirement benefits Recognition of profits on long term contractsRecognition of profits on long term contracts Valuation of fixed assets.Valuation of fixed assets. Treatment of contingent liabilities, etc.Treatment of contingent liabilities, etc.

As-2 valuation of inventoriesAs-2 valuation of inventories

The object of this standard is to determine The object of this standard is to determine the value at which inventories are carried the value at which inventories are carried in financial statements until the related in financial statements until the related revenue recognized. Inventories includes revenue recognized. Inventories includes all those which are held for sale in the all those which are held for sale in the ordinary course of business, used in the ordinary course of business, used in the process of production for such sale or in process of production for such sale or in the form of materials or supplies to the form of materials or supplies to consumed in production process or in the consumed in production process or in the rendering of services. rendering of services.

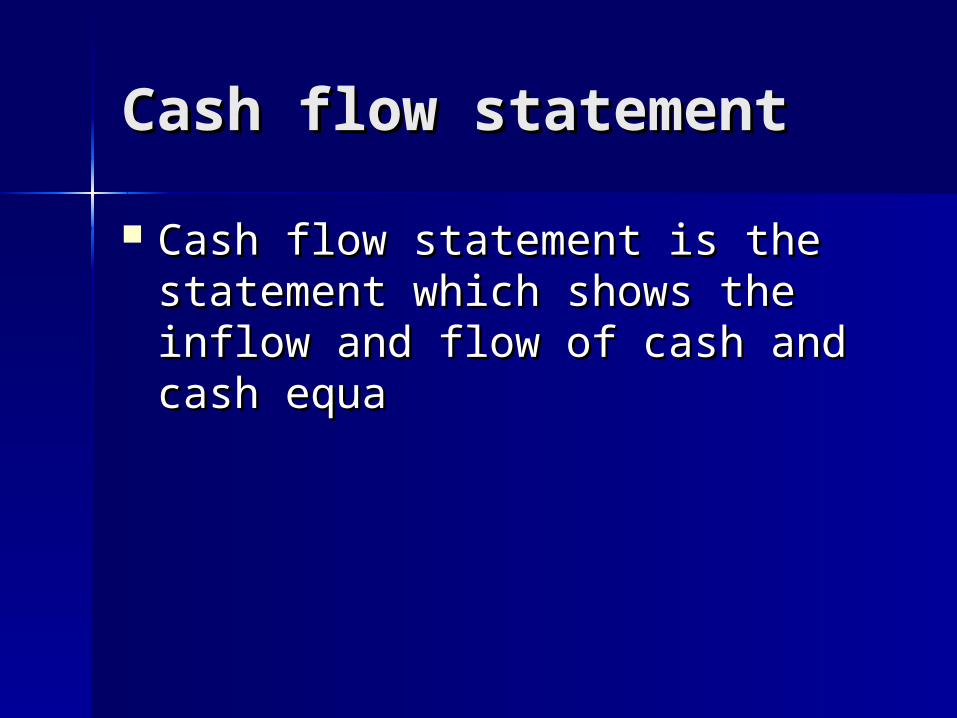

As-3 Cash flow statements As-3 Cash flow statements

In this accounting standard the cash flow In this accounting standard the cash flow statement should report cash flows during statement should report cash flows during the period classified by operating, investing the period classified by operating, investing and financial activities and cash and cash and financial activities and cash and cash equivalents. Which are explained as below:-equivalents. Which are explained as below:-

Cash comprises of cash and demand deposit Cash comprises of cash and demand deposit with bankswith banks

Cash equivalents are short term, highly liquid Cash equivalents are short term, highly liquid investments are readily convertible into cashinvestments are readily convertible into cash

Cash flows are inflows and outflows of cash Cash flows are inflows and outflows of cash and cash equivalents.and cash equivalents.

As-4 contingencies and events As-4 contingencies and events occurring after the balance sheet occurring after the balance sheet

This standard deals with the treatment of a) This standard deals with the treatment of a) contingencies and b) events occurring after the balance contingencies and b) events occurring after the balance sheet dare, where- sheet dare, where-

a) a contingency is a condition or situation, the ultimate a) a contingency is a condition or situation, the ultimate outcome of which, gain or loss, will be known or outcome of which, gain or loss, will be known or determined only on the occurrence, or non occurrence, of determined only on the occurrence, or non occurrence, of one or more uncertain future eventsone or more uncertain future events. . It is restricted to It is restricted to conditions or situations at the balance sheet , conditions or situations at the balance sheet , the financial effects of which is to be determined the financial effects of which is to be determined by future events which may or may not occurby future events which may or may not occur

As-5 NAs-5 Net profit or loss for the et profit or loss for the periodperiod The object of this standard is to prescribe The object of this standard is to prescribe

the classification and disclosure of the classification and disclosure of certain items in the statement of profit certain items in the statement of profit and loss so that all enterprises prepare and loss so that all enterprises prepare and present such a statement on a and present such a statement on a uniform basis. This enhances the uniform basis. This enhances the comparability of the financial statements comparability of the financial statements of an enterprise over time and with the of an enterprise over time and with the financial statements of other enterprisesfinancial statements of other enterprises..

As-6 As-6 Depreciation accountingDepreciation accounting Depreciation is a measure of the wearing out, Depreciation is a measure of the wearing out,

consumption or other loss of the value of a consumption or other loss of the value of a depreciable asset arising from use or obsolescence depreciable asset arising from use or obsolescence through technology and market changes. The through technology and market changes. The standard deals with depreciation accounting and standard deals with depreciation accounting and applies to all depreciable assets, expect the applies to all depreciable assets, expect the following items to which special considerations following items to which special considerations apply:- forests, plantations and similar apply:- forests, plantations and similar regenerative natural resourcesregenerative natural resources, expenditure on , expenditure on research and development, goodwill, live research and development, goodwill, live stock, land unless it has a limited useful life stock, land unless it has a limited useful life the enterprise.the enterprise.

As-7 As-7 accounting for accounting for construction contractconstruction contract The standard deals with accounting for The standard deals with accounting for

construction contract in the financial construction contract in the financial statements of contracts in the financial statements of contracts in the financial statements of contractors. The statements of contractors. The principal problem relating to principal problem relating to accounting for construction contracts accounting for construction contracts is the allocation of revenues and is the allocation of revenues and related costs to accounting periods related costs to accounting periods over the duration of the contract.over the duration of the contract.

AS-8 Accounting for Research AS-8 Accounting for Research and development and development

This standard has been This standard has been withdrawn and included is AS-26.withdrawn and included is AS-26.

AS-9 Revenue RecognitionAS-9 Revenue Recognition

This standard deals with the bases This standard deals with the bases for recognition of revenue in the for recognition of revenue in the statement of profit and loss of an statement of profit and loss of an enterprise. It is concerned with the enterprise. It is concerned with the recognition of revenue arising in recognition of revenue arising in the course of ordinary activities of the course of ordinary activities of the enterprise from sale of goods the enterprise from sale of goods and the rendering of services, the and the rendering of services, the use of other resources.use of other resources.

AS-10 Accounting for AS-10 Accounting for Fixed AssetsFixed Assets This standard in the financial This standard in the financial

statements and providing statements and providing information with regard to cost, information with regard to cost, life span, depreciation, life span, depreciation, revaluation and carrying amount revaluation and carrying amount (w.d.v) of such assets. (w.d.v) of such assets.

AS-11 (Revised)AS-11 (Revised)the effect of changes in foreign the effect of changes in foreign exchange rates exchange rates

The objective of this standard is to The objective of this standard is to show the effects of changes in foreign show the effects of changes in foreign branches. Foreign currency branches. Foreign currency transactions should be expressed in transactions should be expressed in the enterprise’s reporting currency the enterprise’s reporting currency and the financial statements of foreign and the financial statements of foreign branches should be translated into the branches should be translated into the enterprise’s reporting currency in enterprise’s reporting currency in order to include them in the financial order to include them in the financial statements of the enterprise.statements of the enterprise.

AS-12: Accounting for AS-12: Accounting for Government Grants Government Grants AS-12 deals with accounting for AS-12 deals with accounting for

government grants, subsidies, government grants, subsidies, cash incentives and duty cash incentives and duty drawbacks etc. however, this drawbacks etc. however, this standard does not deals with standard does not deals with government assistance other than government assistance other than in the form of government grants in the form of government grants and government participation. and government participation.

AS-13 Accounting for AS-13 Accounting for investmentsinvestments It deals with the accounting treatment of It deals with the accounting treatment of

investments in respect of its investments in respect of its classification, cost, carry amount, classification, cost, carry amount, disposal and disclosure. However, this disposal and disclosure. However, this standard does not deal with:-standard does not deal with:-

Investments by way of operating or Investments by way of operating or financial lease.financial lease.

Investments of life insurance enterprisesInvestments of life insurance enterprises Mutual funds and public financial Mutual funds and public financial

institution and banks.institution and banks.

AS-14 Accounting for AS-14 Accounting for AmalgamationAmalgamation It aims to provide accounting It aims to provide accounting

treatment on amalgamation and the treatment on amalgamation and the treatment of goodwill or reserves treatment of goodwill or reserves arising there. As per AS 14 there are arising there. As per AS 14 there are two types of amalgamations:-two types of amalgamations:-

Amalgamation in the nature of merger Amalgamation in the nature of merger Amalgamation in the nature of Amalgamation in the nature of

purchase. purchase.

AS-15 Accounting for AS-15 Accounting for retirement benefits in the retirement benefits in the financial statements of financial statements of employersemployers This standard deals with the This standard deals with the

accounting treatment of accounting treatment of retirement benefits such as retirement benefits such as provident fund, superannuation provident fund, superannuation dun, pension benefits, Gratuity, dun, pension benefits, Gratuity, encashment of earned leave and encashment of earned leave and other retirement benefits. other retirement benefits.

AS-16 Borrowing CostsAS-16 Borrowing Costs It deals with the treatment of It deals with the treatment of

borrowing costs such as interests borrowing costs such as interests and other costs incurred in and other costs incurred in connection with the borrowing of connection with the borrowing of funds.funds.

AS-17 Segment AS-17 Segment ReportingReporting AS-17 seeks to establish guidelines AS-17 seeks to establish guidelines

and to prescribe rules for financial and to prescribe rules for financial information about the different information about the different types of products and services in types of products and services in which the firms deals in, called which the firms deals in, called Business Segment and covering Business Segment and covering various geographical areas called various geographical areas called Geographical segment.Geographical segment.

AS-18 Related Party AS-18 Related Party DisclosuresDisclosures AS-18 prescribes guidelines AS-18 prescribes guidelines

regarding disclosure requirements regarding disclosure requirements of related transactions, related of related transactions, related party includes:party includes:

Holding companies, Subsidiaries Holding companies, Subsidiaries and fellow subsidiariesand fellow subsidiaries

Associates and Joint venturesAssociates and Joint ventures

AS-19 LeasesAS-19 Leases It deals with the accounting It deals with the accounting

treatment of lease transactions in treatment of lease transactions in the books of both parties. As per the books of both parties. As per the standard the leases have the standard the leases have classified in two categories:- classified in two categories:- Financial LeasesFinancial Leases

Operating LeasesOperating Leases

AS-20 Earning Per AS-20 Earning Per ShareShare The objective of this standard is The objective of this standard is

to prescribe principles for the to prescribe principles for the determination and presentation of determination and presentation of earning per share which will earning per share which will improve the comparison of improve the comparison of performance among different performance among different enterprises. enterprises.

AS-21 Consolidated AS-21 Consolidated Financial Statement Financial Statement AS 21 Prescribes guidelines, rules AS 21 Prescribes guidelines, rules

and procedure to prepare and procedure to prepare consolidated financial statements consolidated financial statements for group of enterprises under the for group of enterprises under the control of a parent.control of a parent.

AS-22 Accounting For AS-22 Accounting For Taxes on IncomeTaxes on Income AS-22 deals with the accounting AS-22 deals with the accounting

treatment of taxes on income. It treatment of taxes on income. It prescribes guidelines and principles prescribes guidelines and principles for determination of an amount of tax for determination of an amount of tax expense or tax savings on the total expense or tax savings on the total profits of an enterprise in respect of profits of an enterprise in respect of an accounting period and disclosure an accounting period and disclosure of such amount in the financial of such amount in the financial statements. statements.

AS-23 Accounting for Investments in AS-23 Accounting for Investments in Associates in Consolidated Financial Associates in Consolidated Financial StatementsStatements

This standard deals with the This standard deals with the investments in associates in the investments in associates in the preparation and presentation of preparation and presentation of consolidated financial statements consolidated financial statements of an investor of an investor

AS-24 Discontinuing AS-24 Discontinuing OperationsOperations This standard prescribes guidelines for This standard prescribes guidelines for

reporting information about discontinuing reporting information about discontinuing operations thereby enhancing the ability operations thereby enhancing the ability of users of financial statements to make of users of financial statements to make projections of an enterprise’s cash flows, projections of an enterprise’s cash flows, earning-generating capacity and financial earning-generating capacity and financial position by segregating information about position by segregating information about discontinuing from information about discontinuing from information about continuing operations.continuing operations.

AS-25 Interim financial AS-25 Interim financial ReportingReporting AS-25 aims to prescribe minimum AS-25 aims to prescribe minimum

contents of an interim financial contents of an interim financial report and to prescribe principles report and to prescribe principles for recognition and measurement for recognition and measurement in a complete financial in a complete financial statements for an interim period.statements for an interim period.

AS-26 Intangible AS-26 Intangible AssetsAssets The main objectives of AS-26 is to The main objectives of AS-26 is to

prescribe the accounting prescribe the accounting treatment for intangible assets treatment for intangible assets that are not dealt with specifically that are not dealt with specifically in another accounting standard. in another accounting standard.

AS-27 Financial Reporting of AS-27 Financial Reporting of Interests in joint venturesInterests in joint ventures

The objective of this standard is The objective of this standard is to set out principles and to set out principles and procedures for accounting for procedures for accounting for interests in joint ventures and interests in joint ventures and reporting of joint ventures assets, reporting of joint ventures assets, liabilities, incomes and expenses liabilities, incomes and expenses in the financial statements of in the financial statements of investors.investors.

AS-28 Impairment of AS-28 Impairment of AssetsAssets AS 28 aims to prescribe principles AS 28 aims to prescribe principles

to ensure that assets are shown to ensure that assets are shown at an amount which is not more at an amount which is not more than the recoverable amount. The than the recoverable amount. The excess of carrying amount( Book excess of carrying amount( Book Value) over the recoverable Value) over the recoverable amount from sale or use of asset amount from sale or use of asset is known as impairment loss. is known as impairment loss.

AS-29 Provisions, contingent AS-29 Provisions, contingent Liabilities and Assets Liabilities and Assets

The main objective of this The main objective of this standard is to ensure appropriate standard is to ensure appropriate recognition and measurement recognition and measurement criteria for provisions and criteria for provisions and contingent liabilities by providing contingent liabilities by providing sufficient information in the sufficient information in the financial statement.financial statement.

AS-30 Financial Instruments AS-30 Financial Instruments Recognition and MeasurementsRecognition and Measurements

An enterprise recognizes a An enterprise recognizes a financial assets or a financial financial assets or a financial assets or a financial liability on its assets or a financial liability on its balance sheet when the balance sheet when the enterprise became a party to the enterprise became a party to the contractual provisions of contractual provisions of instrument. instrument.

AS-31 Financial Instruments AS-31 Financial Instruments -Presentation-Presentation This standard has been set out This standard has been set out

broadly in line of IAS-32 broadly in line of IAS-32 establishes various principles.establishes various principles.

For presenting financial For presenting financial instruments as liabilities or instruments as liabilities or equity.equity.

Inventory ValuationInventory Valuation Inventories are the stock of Inventories are the stock of

product a company is product a company is manufacturing for sale or buying manufacturing for sale or buying for resale including the parts, for resale including the parts, components or materials that components or materials that make the product.make the product.

Classification of Classification of Inventories Inventories 1) Raw Materials: these are the basis 1) Raw Materials: these are the basis

inputs that are converted into inputs that are converted into finished product through production finished product through production process. process.

2) Work in Progress: this part of 2) Work in Progress: this part of inventories comprises semi produced inventories comprises semi produced of incomplete units of product. it of incomplete units of product. it includes cost such as material, direct includes cost such as material, direct labour and factory overheads etc.labour and factory overheads etc.

3) Finished Goods: Goods produced 3) Finished Goods: Goods produced and completed and ready for sale.and completed and ready for sale.

Objectives of Objectives of inventories valuationinventories valuation Determination of inventory valuation.Determination of inventory valuation. Determination of financial position.Determination of financial position. Estimating working capital Estimating working capital

requirements.requirements. To maintain an ideal balance b/w To maintain an ideal balance b/w

production and sales.production and sales.

Methods of taking Methods of taking inventoryinventory Periodic inventory method:- under this Periodic inventory method:- under this

method value of inventory is ascertained method value of inventory is ascertained by physical counting and checking of all by physical counting and checking of all items of inventory at the year end and the items of inventory at the year end and the same is verified from the book entry. same is verified from the book entry.

Perpetual inventory method:-this method Perpetual inventory method:-this method involves continues recording of addition to involves continues recording of addition to or reduction in material, work in progress or reduction in material, work in progress and finished goods on the day to day and finished goods on the day to day basisbasis. .

Methods of valuation Methods of valuation inventoriesinventories First in First out FIFOFirst in First out FIFO Last in First out LIFOLast in First out LIFO Highest in First out HIFOHighest in First out HIFO Base Stock MethodBase Stock Method Simple Average Cost MethodSimple Average Cost Method Weighted average cost MethodWeighted average cost Method Standard cost methodStandard cost method Specific identification cost methodsSpecific identification cost methods Replacement cost Replacement cost Lower cost methodLower cost method Retail Inventory methodRetail Inventory method

Accounting treatment Accounting treatment of intangible assetsof intangible assets AS per accounting standard 26 an AS per accounting standard 26 an

intangible assets is an identifiable intangible assets is an identifiable non monetary asset without non monetary asset without physical substance held for use in physical substance held for use in the production or sale of goods or the production or sale of goods or services or for rental to other or services or for rental to other or for administrative. for administrative.

conceptconcept Enterprise frequently pay for Enterprise frequently pay for

acquisition and development of acquisition and development of intangible assets. These may intangible assets. These may relate to scientific or technical relate to scientific or technical knowledge, design and system. knowledge, design and system. Licenses, market knowledge, trade Licenses, market knowledge, trade marks, brand name and computer marks, brand name and computer software, patents, copy rights, software, patents, copy rights, marketing rights and goodwill etc.marketing rights and goodwill etc.

Salient featuresSalient features As item may be recognized as an intangible As item may be recognized as an intangible

asset if following three conditions are satisfied.asset if following three conditions are satisfied. Identifiability :- an asset is identifiable if it Identifiability :- an asset is identifiable if it

separate or arises from contractual or other separate or arises from contractual or other legal rights.legal rights.

Control over an asset :- control provides to Control over an asset :- control provides to enjoy economic benefits of an asset.enjoy economic benefits of an asset.

Future economic benefits :- the future Future economic benefits :- the future economic benefits flowing from an intangible economic benefits flowing from an intangible asset may include revenue from the sale of asset may include revenue from the sale of products or services resulting from the use of products or services resulting from the use of the asset by the company.the asset by the company.

Final AccountsFinal Accounts Final accounts refers to the final Final accounts refers to the final

statements of accounts prepared in order statements of accounts prepared in order to ascertain and report the results of the to ascertain and report the results of the financial activities of a business. Having financial activities of a business. Having prepared the trial balance, which prepared the trial balance, which establishes the accuracy of books of establishes the accuracy of books of accounts, the next step is to ascertain accounts, the next step is to ascertain the operating result and financial the operating result and financial position of the business. For this position of the business. For this purpose, the final accounts are prepared, purpose, the final accounts are prepared, which include mainly the trading and which include mainly the trading and profit and loss account, also called as profit and loss account, also called as income statement and balance sheetincome statement and balance sheet

Objectives of preparing final Objectives of preparing final accountsaccounts To calculate profit or loss at the end of To calculate profit or loss at the end of

accounting year.accounting year. To ascertain financial position of the To ascertain financial position of the

business at the end of the year.business at the end of the year. To make a comparative study of changes To make a comparative study of changes

taken place in assets and liabilities.taken place in assets and liabilities. To calculate or decide capital employed .To calculate or decide capital employed . Legal compulsion of preparing final Legal compulsion of preparing final

accounts.accounts.

Trading accountTrading account Trading account is an account Trading account is an account

through which it is ascertained as to through which it is ascertained as to how much profit has been earned or how much profit has been earned or losses have been sustained through losses have been sustained through purchase and sale of goods within purchase and sale of goods within specified period. The result of specified period. The result of trading account is named as gross trading account is named as gross profit or gross loss. profit or gross loss.

Profit and loss accountProfit and loss account Profit and loss account is an account, which is Profit and loss account is an account, which is

prepared to calculate the final profit and loss prepared to calculate the final profit and loss of the business. All operating expenses and of the business. All operating expenses and other non operating income and expenditure other non operating income and expenditure and losses are charged to P&L account to find and losses are charged to P&L account to find out the net profit. Operating expenses such as out the net profit. Operating expenses such as office and administration expenses, selling office and administration expenses, selling and distribution expenses and financial and distribution expenses and financial charges are in direct in nature and incurred to charges are in direct in nature and incurred to carry on business profitably. Non operating carry on business profitably. Non operating income such as a dividends received and income such as a dividends received and interest received etc. and non operating interest received etc. and non operating expenses such as donation paid are also expenses such as donation paid are also charged to P/L accountcharged to P/L account

Balance sheetBalance sheet A balance sheet may be defined as ‘a A balance sheet may be defined as ‘a

statement drawn upon a given date, statement drawn upon a given date, generally at the end of each accounting generally at the end of each accounting year, to measure the exact financial year, to measure the exact financial position of the business, setting forth position of the business, setting forth the various assets and liabilities of the the various assets and liabilities of the concern at this date’. On the other hand concern at this date’. On the other hand “The balance sheet is a statement at a “The balance sheet is a statement at a particular date showing on one side the particular date showing on one side the trader’s property and possessions and trader’s property and possessions and on the other hand liabilities” on the other hand liabilities”

Difference b/w Difference b/w balance sheet and balance sheet and

trial balancetrial balance Trial balancesTrial balances It is a list of It is a list of

balances of all balances of all ledgerledger

Its object is to Its object is to check the check the arithmetical arithmetical accuracy of the accuracy of the ledger.ledger.

Balance sheetBalance sheet It is a statement It is a statement

of assets and of assets and liabilities.liabilities.

Its object is to Its object is to reveal at a glance reveal at a glance the financial the financial position of the position of the business business concerns.concerns.

Cont…Cont… It includes the opening It includes the opening

stockstock It is prepared whenever It is prepared whenever

desireddesired

It does not give It does not give information about the information about the net profit or net loss.net profit or net loss.

It is not necessary to It is not necessary to prepare the trial prepare the trial balance. balance.

It includes the closing It includes the closing stock stock

It is usually prepared at It is usually prepared at the end of a trading the end of a trading period or accounting period or accounting year.year.

It gives information It gives information about the profits and the about the profits and the capital balance includes capital balance includes the profit.the profit.

Preparation of balance Preparation of balance sheet is necessary to sheet is necessary to complete the accounting complete the accounting process.process.

Cont..Cont.. It is generally It is generally

prepared without prepared without giving effect to giving effect to any adjustment.any adjustment.

It contains the It contains the heading debit heading debit and credit.and credit.

It can not be It can not be prepared without prepared without making making adjustmentsadjustments

It contains the It contains the headings headings liabilities and liabilities and assets. assets.

AdjustmentsAdjustments Closing stock – As the value of closing Closing stock – As the value of closing

inventories is ascertained at the inventories is ascertained at the accounting year, it appears as an accounting year, it appears as an adjustment. It should be credited to adjustment. It should be credited to trading a/c and shown in the assets side trading a/c and shown in the assets side of the B/S. of the B/S.