accounting & financial management introduction to managerial accounting larry ross, ph.d....

TRANSCRIPT

Accounting & Financial

Management

Introduction to Managerial Accounting

Larry Ross, Ph.D.Barnett School of Business & Free EnterpriseFlorida Southern College @ Lakeland, FL

2014 BMI II ~ Managerial Accounting

Learning Objectives

At the end of this session you will be able to:

1. Relate accounting’s role to club management

2. Determine the financial “health” of the club

3. Assess the club’s level of financial performance

4. Apply the CVP model as a decision-making tool

5. Compare and contrast the advantages and disadvantages of leasing

2014 BMI II ~ Managerial Accounting

Sources of Information

Accounting for Club Operations Ch. 2,5,6,9 & 11

Contemporary Club Management 3rd ed. Ch. 11

Uniform System of Financial Reporting for Clubs

White Papers on Club Management, VIII:16

2014 BMI II ~ Managerial Accounting

4 Major Topics

1. Key Accounting Terms &

Principles

2. Financial analysis using Ratios

3. Decision-making with CVP

Analysis

4. Impact of the decision to lease

2014 BMI II ~ Managerial Accounting

The Accounting Function

Information-oriented

1)External Users

2)Internal Uses

Support Function

2014 BMI II ~ Managerial Accounting

6 Branches of Accounting1. Financial Accounting2. Cost Accounting3. Managerial Accounting4. Tax Accounting5. Auditing6. Accounting Info Systems

2014 BMI II ~ Managerial Accounting

Generally Accepted Accounting Principles

(GAAP)

Cost Principle Going Concern Unit of Measurement Objective Evidence Full Disclosure

2014 BMI II ~ Managerial Accounting

Generally Accepted Accounting Principles

(GAAP)

Consistency Matching Conservatism Materiality Cash Basis vs. Accrual

2014 BMI II ~ Managerial Accounting

Accounting BasicsFundamental Accounting

Equation (A = L + ME) Assets Liabilities Member’s Equity

PermanentTemporary

2014 BMI II ~ Managerial Accounting

Typical ASSET Accounts

Cash Accounts Receivable Food & Beverage Inventory Prepaid Expenses Fixed Assets (Building &

Equipment)

2014 BMI II ~ Managerial Accounting

Typical Liability Accounts

Accounts Payable Accrued Expenses Unearned Income Note Payable Mortgage Payable

2014 BMI II ~ Managerial Accounting

Typical Equity Accounts

Capital Stock

Designated net Assets

Undesignated net Assets

2014 BMI II ~ Managerial Accounting

Typical Revenue Accounts

Membership dues Initiation fees Food revenue Beverage revenue Rentals and other

revenue

2014 BMI II ~ Managerial Accounting

Typical Expense Accounts

Food cost Beverage cost Entertainment expense Administrative & general Energy costs

The Balance Sheet

Also called the Statement of Financial

Position

2014 BMI II ~ Managerial Accounting

Statement of Financial Position

“Snapshot” of account balances

A = L + OE Balanced via the

Proprietorship Accounts

Indicates financial “health”

2014 BMI II ~ Managerial Accounting

What can We Learn from the Statement of Financial

Position

Horizontal Analysis

Vertical Analysis

Base-year Comparisons

Ratio Analysis

The Income Statement

Also called the Statement of

Activities

2014 BMI II ~ Managerial Accounting

Statement of Activities

“Video” of financial activity

Profit = Revenue – Expenses

Closed-out to Member’s Equity

Indicates financial performance

2014 BMI II ~ Managerial Accounting

What can We Learn from the Statement of

Activities

Departmental Statements Operating Statistics

Multi-year trendsGeographic & size divisions

Analysis of Income Statement

Statement of Cash Flows

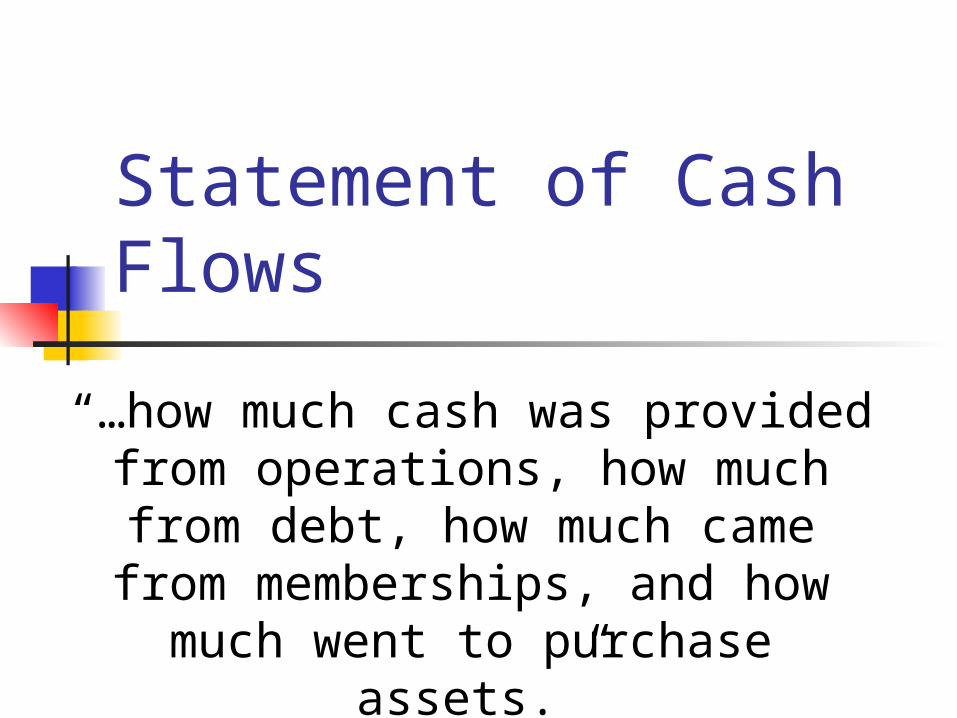

“…how much cash was provided from operations, how much from

debt, how much came from memberships, and how much

went to purchase assets.”

2014 BMI II ~ Managerial Accounting

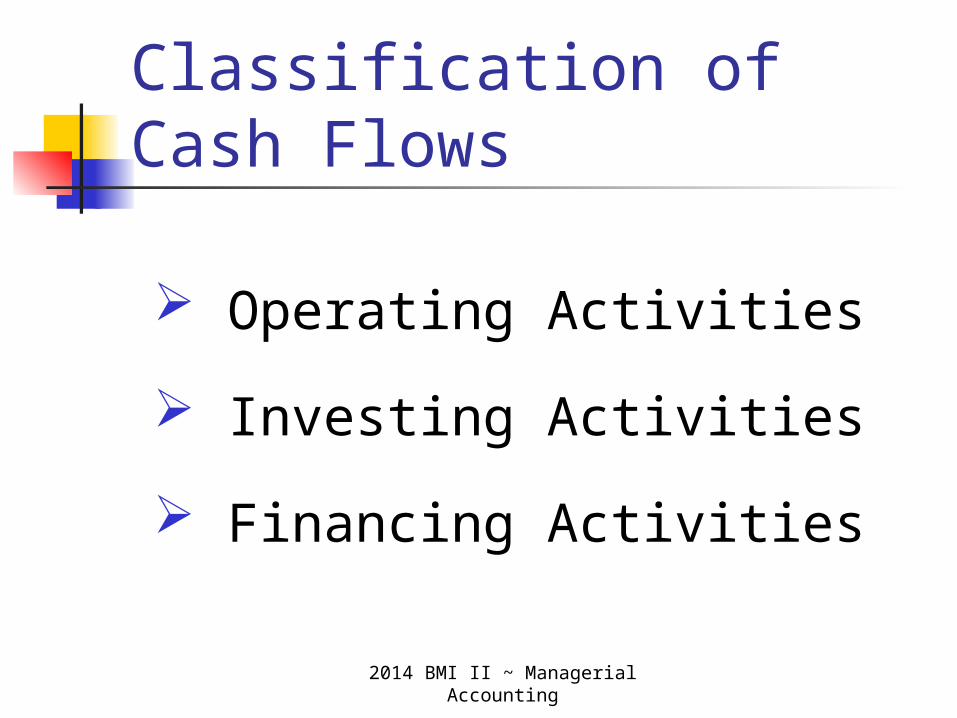

Classification of Cash Flows

Operating Activities

Investing Activities

Financing Activities

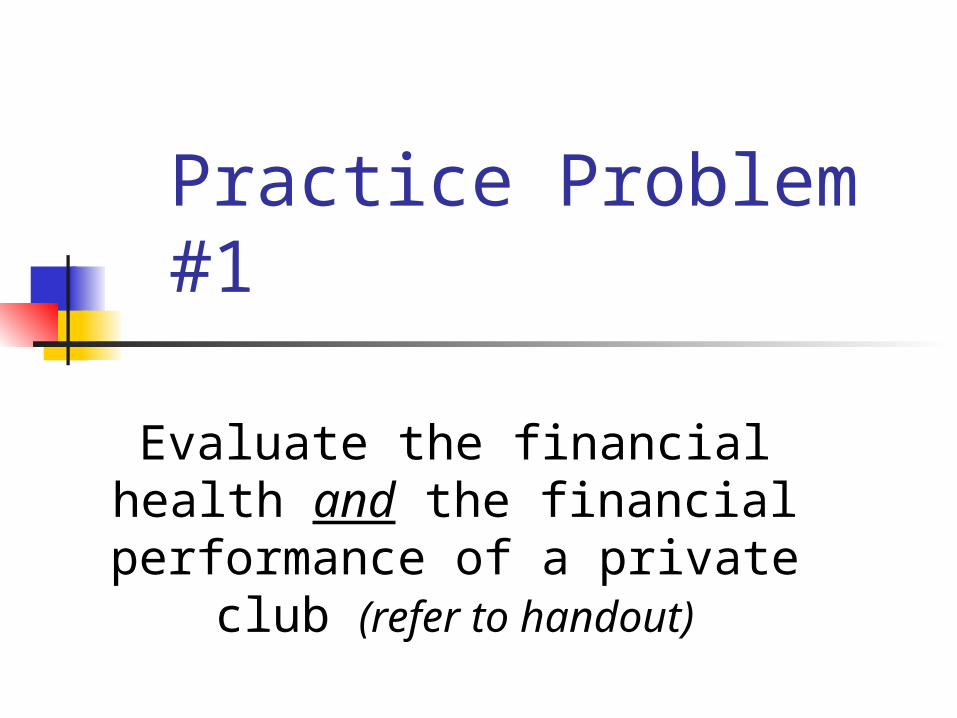

Practice Problem #1

Evaluate the financial health and the financial

performance of a private club (refer to handout)

2014 BMI II ~ Managerial Accounting

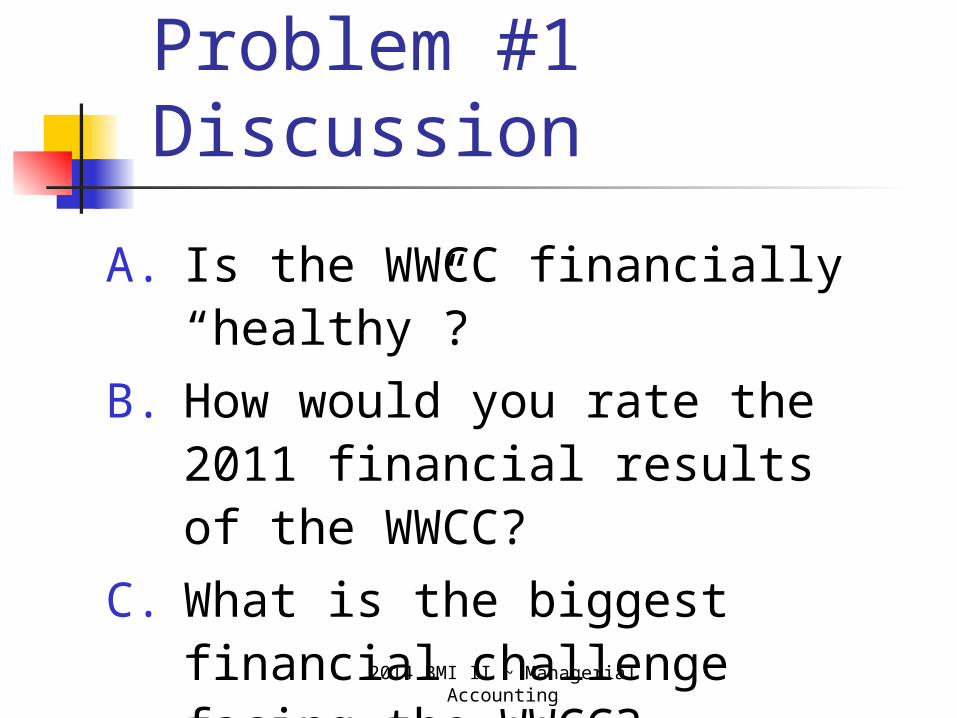

Problem #1 Discussion

A. Is the WWCC financially “healthy”?

B. How would you rate the 2011 financial results of the WWCC?

C. What is the biggest financial challenge facing the WWCC?

Ratio Analysis

“. . .interpret the reported facts to discover aspects. . .

that could otherwise go unnoticed.”

2014 BMI II ~ Managerial Accounting

Ratio Analysis

Four Key Elements: 2 Indicators – Performance & Health

3 Sources of Information

3 Groups of Users

5 Types of Ratios

2014 BMI II ~ Managerial Accounting

Ratio Analysis

Standards of Comparison Historical Past

Industry Averages

Budget

2014 BMI II ~ Managerial Accounting

Ratio Analysis3 Different Users – different

uses1. Creditors

Secured Unsecured

2. Owners/Members3. Managers

2014 BMI II ~ Managerial Accounting

5 Classes of Ratios1. Liquidity: short-term

2. Solvency: long-term

3. Activity: productivity

4. Profitability: conversion

5. Operating: industry-specific

2014 BMI II ~ Managerial Accounting

Ratio Analysis: Liquidity

Current Ratio

Acid-test Ratio

Accounts Receivable Turnover

Average Collection Period

2014 BMI II ~ Managerial Accounting

Ratio Analysis: Solvency

Solvency Ratio

Debt-to-Equity

Number times Interest Earned

Fixed Charge Coverage

2014 BMI II ~ Managerial Accounting

Ratio Analysis: Activity

Inventory Turnover

Fixed Asset Turnover

Total Asset Turnover

Paid Occupancy

Rounds of Golf

2014 BMI II ~ Managerial Accounting

Ratio Analysis: Profitability

Gross Profit Margin

Operating Efficiency Ratio

Return on Assets

Return on Member’s Equity

2014 BMI II ~ Managerial Accounting

Ratio Analysis: Operating

Sales Mix Average Food Check Food Cost Percent Beverage Cost Percent Labor Cost Percent

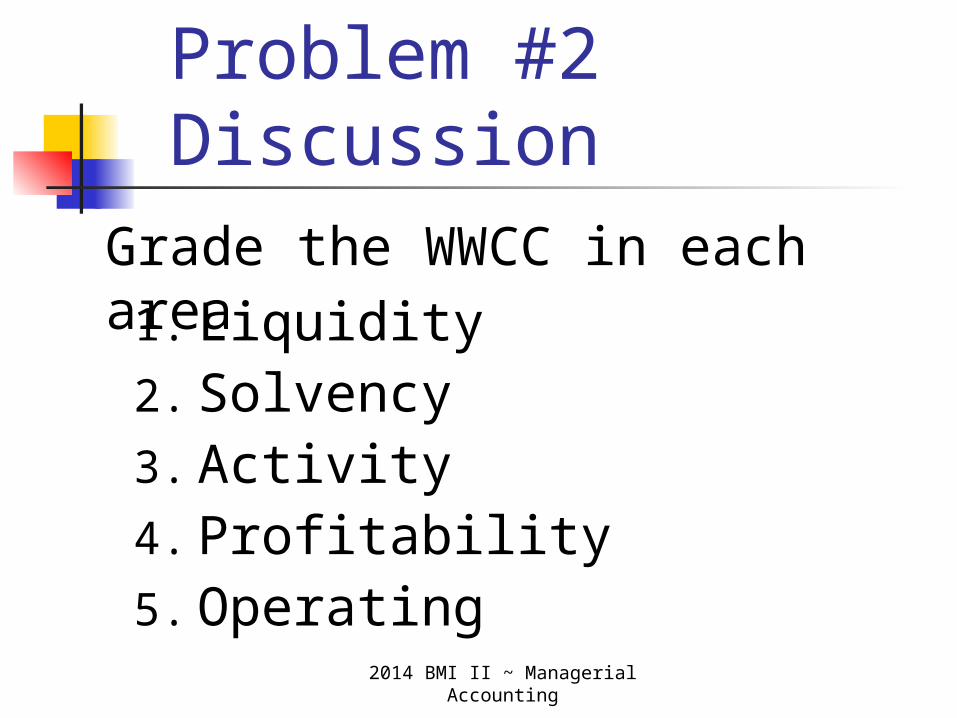

Practice Problem #2

Analyze the financial health and financial performance of the Whistling Wind Country Club using all 5 classes of

ratios.

2014 BMI II ~ Managerial Accounting

Problem #2 Discussion

1. Liquidity2. Solvency3. Activity4. Profitability5. Operating

Grade the WWCC in each area

Applying Cost Concepts

“. . . Something of value given up in order to achieve a specific

outcome.”

2014 BMI II ~ Managerial Accounting

Cost/Volume/Profit Analysis

C/V/P is an expression of the relationship between various costs, sales volume, and profit.

2014 BMI II ~ Managerial Accounting

C/V/P Assumptions

Fixed costs remain fixed.

Variable costs vary in direct proportion to volume.

Revenues vary in direct proportion to volume.

Mixed costs can be divided.

Joint costs can be allocated.

Only considers quantitative factors.

2014 BMI II ~ Managerial Accounting

C/V/P RelationshipsRevenue

Total Cost

Fixed Cost

Variable Cost

$

Volume

2014 BMI II ~ Managerial Accounting

C/V/P Equations Income = Revenue -

Expenses I = R - E Revenue = Price * Quantity

R = P * Q Expenses = Variable Cost +

Fixed E = (V* Q) + F

I = (P*Q) - [(V*Q) + F)]

2014 BMI II ~ Managerial Accounting

C/V/P Equations I = (P*Q) - [(V*Q) + F)]

I = Q*(P-V) - F

IBE + F = Q*CM

Q = F CM

Practice Problem #3

Analyze the decision to build a Wii Fitness Facility at the

Whistling Wind Country Club

2014 BMI II ~ Managerial Accounting

Problem #3 Discussion1. How many new fitness members are necessary for

the fitness facility to break even?2. If you could outsource the salaried supervisor to a

“Wii Pro” who charges for lessons and therefore lower the fixed costs by $40,000, how many members would be necessary (all other things stay the same) to break even?

3. If the board requires a 12% return on capital investments, how many new fitness facility memberships are necessary?

4. A study determines that at most 420 new members would join, what would the price of membership need to be?

Lease Accounting

“. . .an agreement conveying the right to use resources for

specified purposes for a limited time.”

2014 BMI II ~ Managerial Accounting

Advantages of Leases Conserve working capital Less “red tape” Easier to change equipment Less impact on financial

ratios Reduces need for capital

budget

2014 BMI II ~ Managerial Accounting

Disadvantages of Leases

No beneficial residual value

Higher cost

Additional costs of early termination

2014 BMI II ~ Managerial Accounting

Classification of Leases Operating Leases Capital Leases

Title transfer provision Bargain purchase provision Economic life provision Value recovery provision

Practice Test Questions

20 items from the accounting topics that

were covered. . .