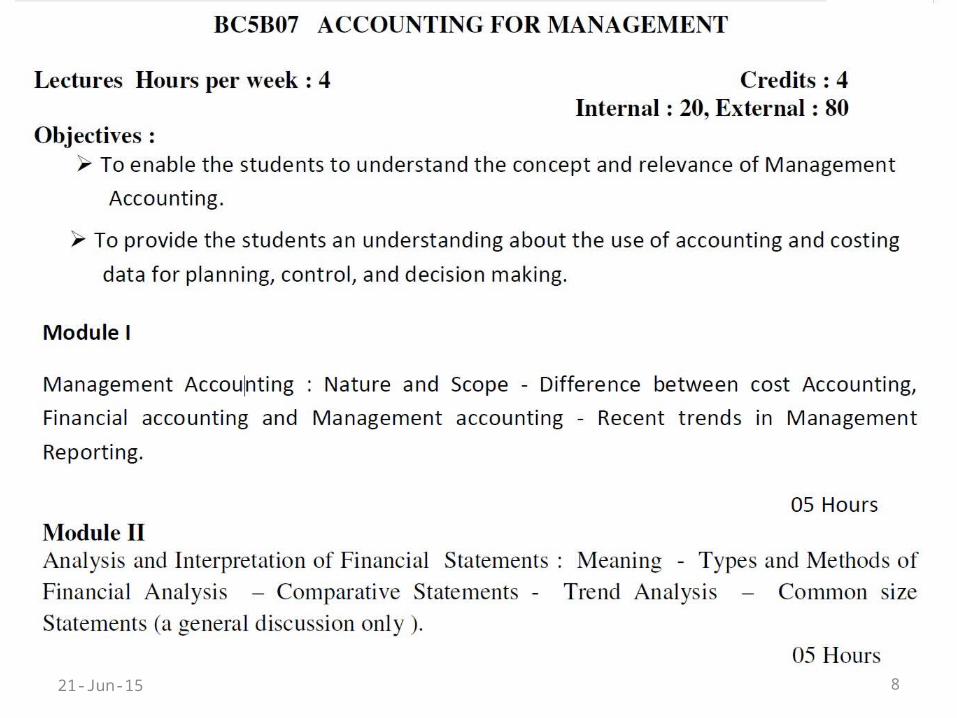

accounting for management

TRANSCRIPT

Accounting for Management

BC5B07, Hours 4, Credits 4

Santhosh Thannikat

2

Semester 1

21-Jun-15

3

Semester 2

21-Jun-15

4

Semester 3

21-Jun-15

5

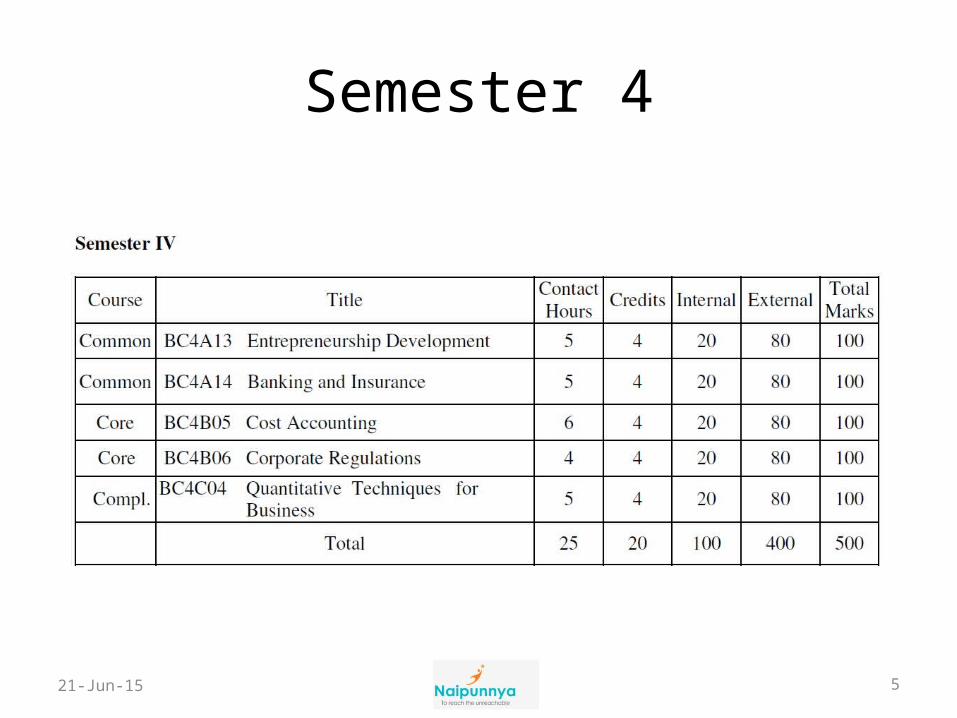

Semester 4

21-Jun-15

6

Semester 5

21-Jun-15

7

Semester 6

21-Jun-15

821-Jun-15

921-Jun-15

1021-Jun-15

11

Introduction

• Limitations of Fin Accounting– Historical– Cost centre– Control over resources’ utilisation– Efficiency measurement– Pricing– Cost comparison– Decision making

21-Jun-15

12

Definition

• Accounting for management decision making• Combination of Financial Accounting and Cost

Accounting• Helping management functions viz. POSDCORB• Presentation of accounting information to help

mgmt in policy making and decision making • Any accounting form which enables more

efficient business

21-Jun-15

13

Characteristics

• Accounting information• Decision making objective• Cause and effect relationship analysed to increase efficiency• Uses special tools

– Standard costing– Budgetary Control– Ration Analysis…

• Quantitative / Qualitative information• Multi disciplinary• Accounting for future• No fixed forms

21-Jun-15

14

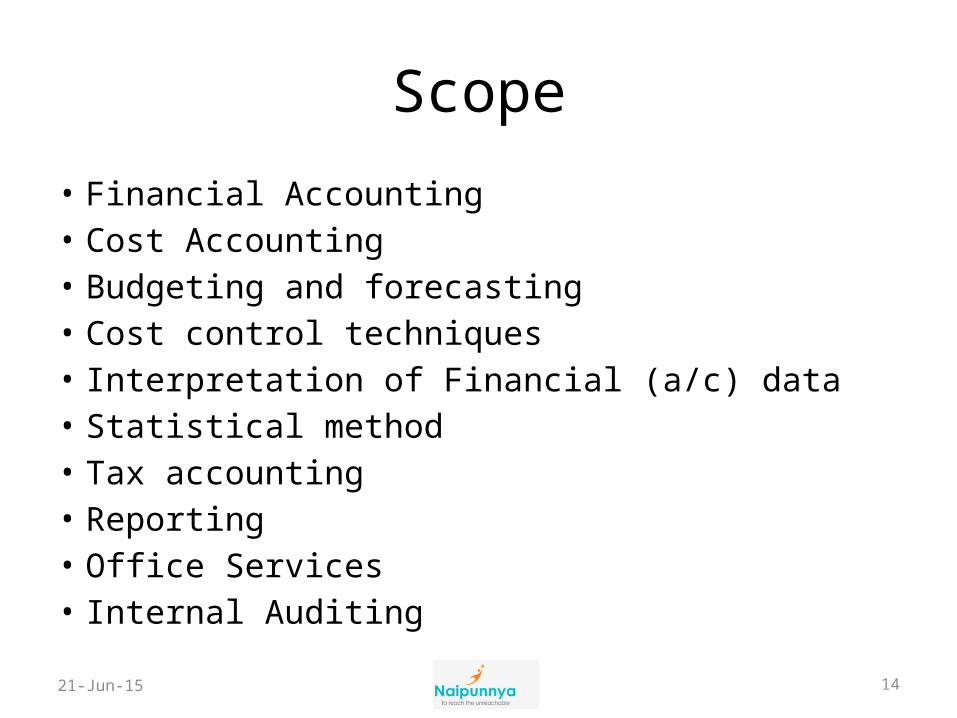

Scope

• Financial Accounting• Cost Accounting• Budgeting and forecasting• Cost control techniques• Interpretation of Financial (a/c) data• Statistical method• Tax accounting• Reporting• Office Services• Internal Auditing21-Jun-15

15

Objectives

• Help in decision making and Planning• Interpreting Financial Statements• Cost controlling and internal disciplines• Coordinates• Motivating employees• To help policy formation• Reporting

21-Jun-15

16

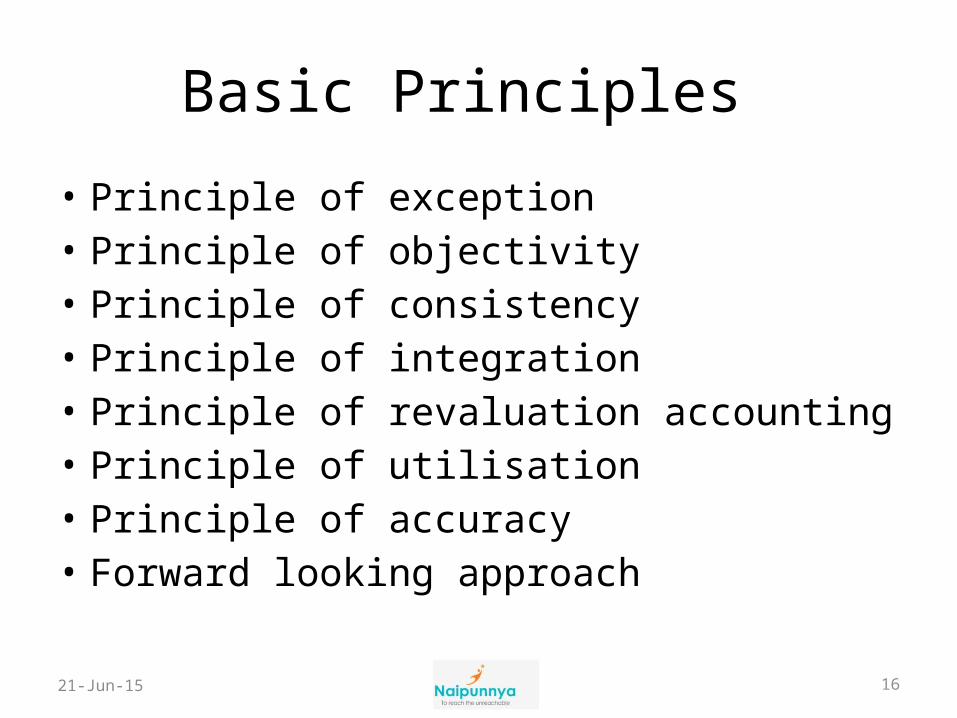

Basic Principles

• Principle of exception• Principle of objectivity • Principle of consistency• Principle of integration• Principle of revaluation accounting• Principle of utilisation• Principle of accuracy• Forward looking approach 21-Jun-15

17

Functions

• Planning and forecasting• Modification and verification of data• Analysis and interpretation of data• Communication• Helping in co-ordination• Helping in decision making

21-Jun-15

18

Comparison

Financial Accounting• Compulsory• Records historical data• To ascertain P&L / BS• Lays more emphasis on accuracy• Based on accepted accounting

principles and conventions• Limited scope• External parties are users• Audit is more compulsory • Stock is valued at cost or market

price

Management Accounting• Optional• For future plans and operations• For mgmt decision making• Emphasis on quick and prompt

reporting• Not based on rigid principles but as per

requirement• Wide scope• Mgmt are the users• Audit is not compulsory• No principles followed for the valuation

of stock

21-Jun-15

19

Comparison with Costing

Cost accounting• Purpose of cost control of

products / services• Limited scope with

ascertain cost and control• Uses only quantitative info.• Deals with cost• Historical and current data• Peceeds mgmt acctg.

Management Accounting• Purpose is to enable

decision making• Vast scope with fin. Acc.,

costing, budgeting etc.• Both• Cost and revenue• Related to the future• Starts from Cost Acctg.

21-Jun-15

20

Advantages

• Proper planning• Effective control• Increased efficiency• Measurement of performance• Maximising profitability• Increase in production• Better customer service• Quick decision making• Improves standard of living• Economic development21-Jun-15

21

Limitations

• Based on accounting information• Lack of adequate knowledge• Cannot replace management• Personal judgement• Costly• Evolutionary stage• Resistance to change

21-Jun-15

22

Tools and Techniques• Financial Accounting and Policy• Financial Analysis• Historical Cost Accounting• Budgetary Control• Standard Costing• Marginal Costing• Decision Accounting (Opportunity Cost)• Revaluation Accounting• Management Information System (MIS)• Statistical Techniques and Operations Research• Responsibility Accounting• Other techniques

21-Jun-15

23

Installation of Management Accounting System

• Preparation of organisational manual• Preparation of forms and returns• Requisite staffing• Classifying accounts and integrating the

system• Introducing Standard Costing technique• Setting up budgetary control system• Introducing operations research techniques

21-Jun-15

24

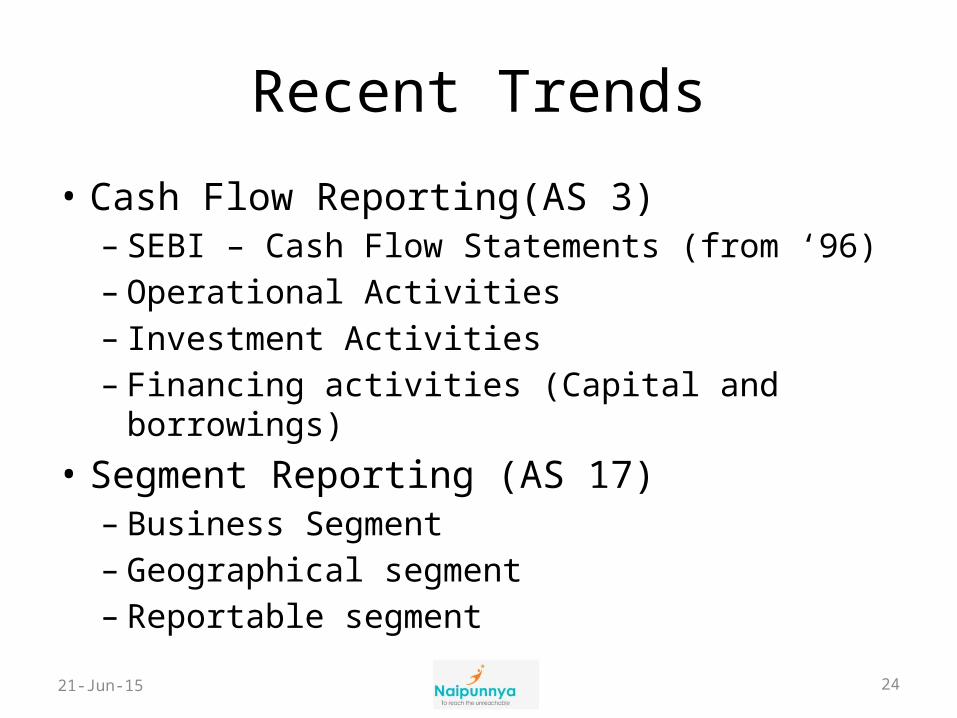

Recent Trends

• Cash Flow Reporting(AS 3)– SEBI – Cash Flow Statements (from ‘96)– Operational Activities– Investment Activities– Financing activities (Capital and borrowings)

• Segment Reporting (AS 17)– Business Segment– Geographical segment– Reportable segment

21-Jun-15

25

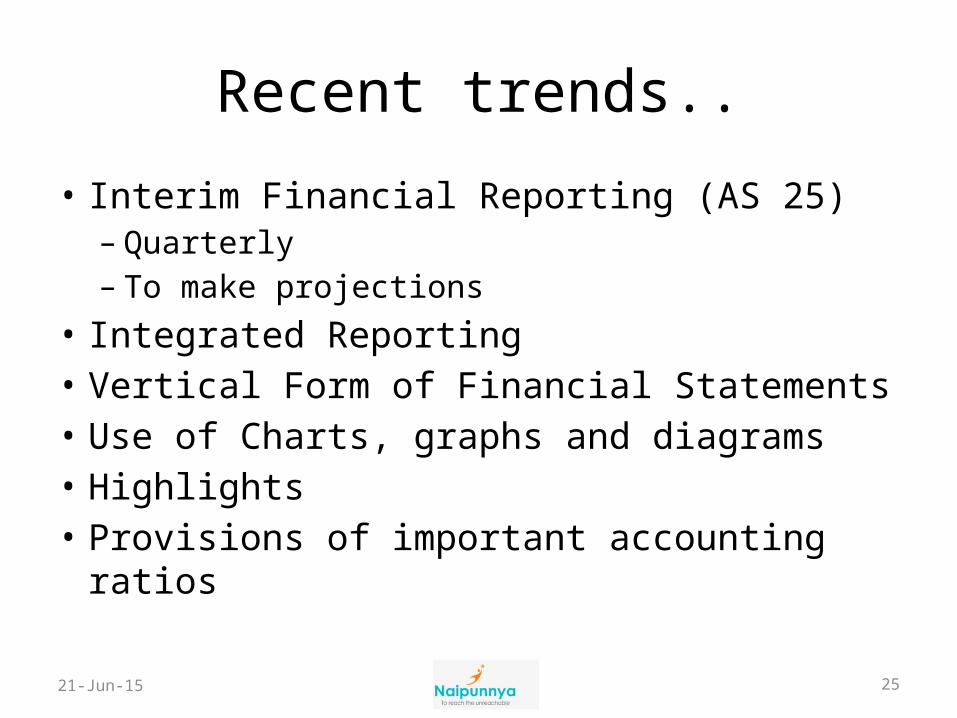

Recent trends..

• Interim Financial Reporting (AS 25)– Quarterly– To make projections

• Integrated Reporting• Vertical Form of Financial Statements• Use of Charts, graphs and diagrams• Highlights• Provisions of important accounting ratios

21-Jun-15