accounting for service concession agreements (ppps) · 2016-07-27 · accounting for service...

TRANSCRIPT

Accounting for Service Concession agreements (PPPs) Seminar on Accounting reforms in the Public

Sector: IPSAS/EPSAS

Brussels, May 13, 2016

Thomas Müller-Marqués Berger, EY Germany

Page 2

Agenda

► Overview of service concession arrangements (SCAs) or public-

private partnerships (PPPs)

► IPSAS 32: Accounting for SCAs/PPPs

Page 3

Overview of SCAs/PPPs

Page 4

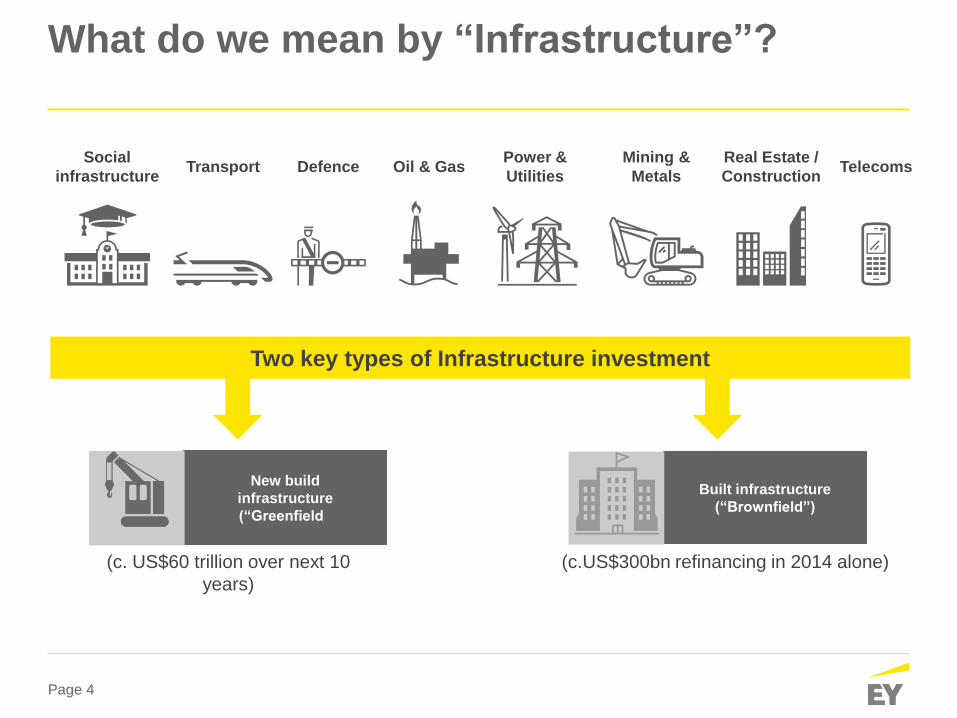

What do we mean by “Infrastructure”?

Two key types of Infrastructure investment

(c. US$60 trillion over next 10

years)

(c.US$300bn refinancing in 2014 alone)

New build

infrastructure

(“Greenfield”)

Built infrastructure

(“Brownfield”)

Real Estate /

Construction

Social

infrastructure Transport Oil & Gas

Power &

Utilities

Mining &

Metals Defence Telecoms

Page 5

What are the key trends driving global infrastructure investment and activity?

Changing

technology,

patterns and

smart

infrastructure

Rapid growth in

emerging

markets

Decommissioning

of Infrastructure

Resilient

cities

Globalization

of supply

chains

Clean energy

and renewables

Digital agenda

Major

events

Capital Agenda

Page 6

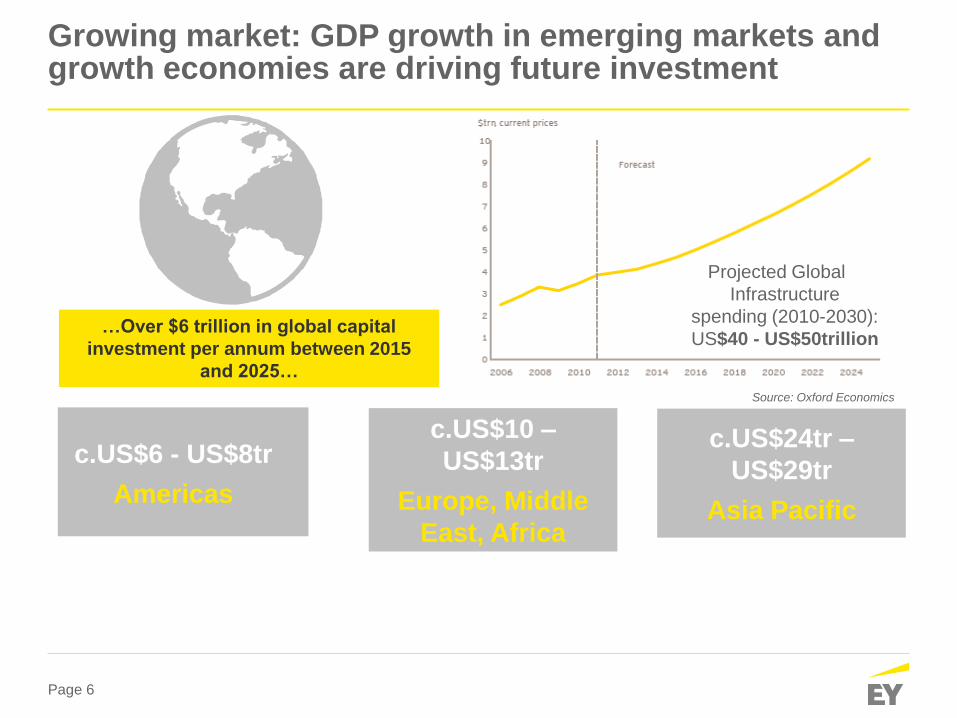

Growing market: GDP growth in emerging markets and growth economies are driving future investment

Projected Global

Infrastructure

spending (2010-2030):

US$40 - US$50trillion

$60bn p.a. Addressable Market with a Whole-of-firm approach

(c.1% of spend)

c.US$6 - US$8tr

Americas

c.US$24tr –

US$29tr

Asia Pacific

c.US$10 –

US$13tr

Europe, Middle

East, Africa

…Over $6 trillion in global capital

investment per annum between 2015

and 2025…

Source: Oxford Economics

Page 7

What’s driving governments to use PPPs?

Key Trends

► Growth. Population growth and urbanisation continue to spur demand

for infrastructure and services

► Funding Gap. Inability of governments to finance current and future

infrastructure assets

► Budgetary pressure. Achievement of community expectations whilst

avoiding debt or adverse budgetary impacts

► Maintenance. Governments must upgrade, replace, and build out

essential infrastructure assets for the community

► Investment. Diversifying financial portfolios with investors seeking

asset classes for long-term investments yielding steady, positive

returns

► Innovation. Innovation and technology have allowed private sector to

bring expertise and new practices to the public sector

Page 8

Accounting for SCAs/PPPs

Page 9

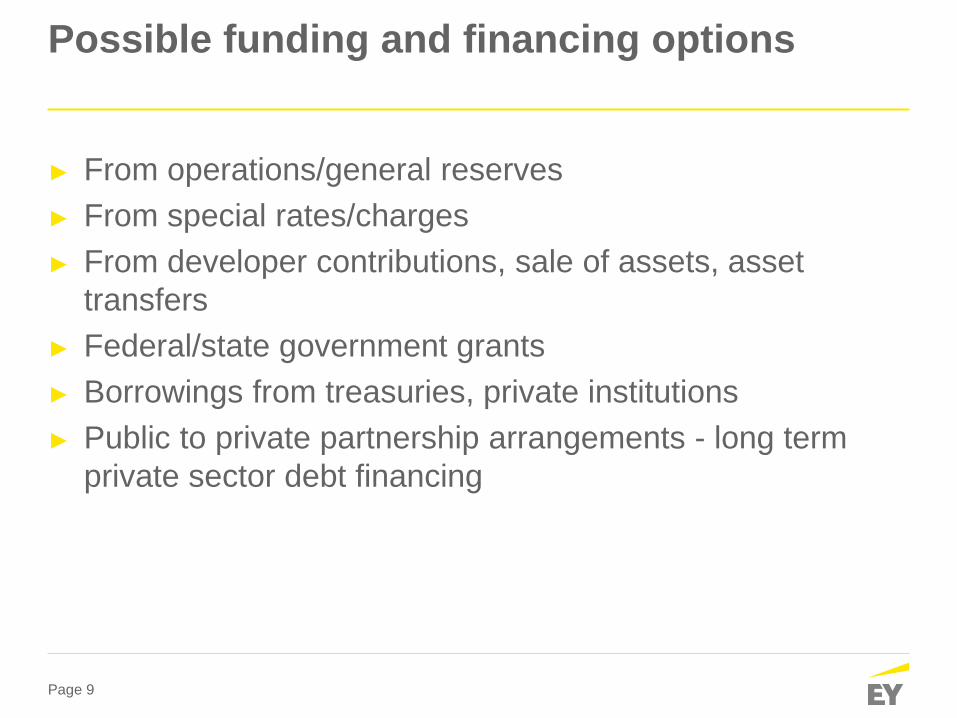

Possible funding and financing options

► From operations/general reserves

► From special rates/charges

► From developer contributions, sale of assets, asset

transfers

► Federal/state government grants

► Borrowings from treasuries, private institutions

► Public to private partnership arrangements - long term

private sector debt financing

Page 10

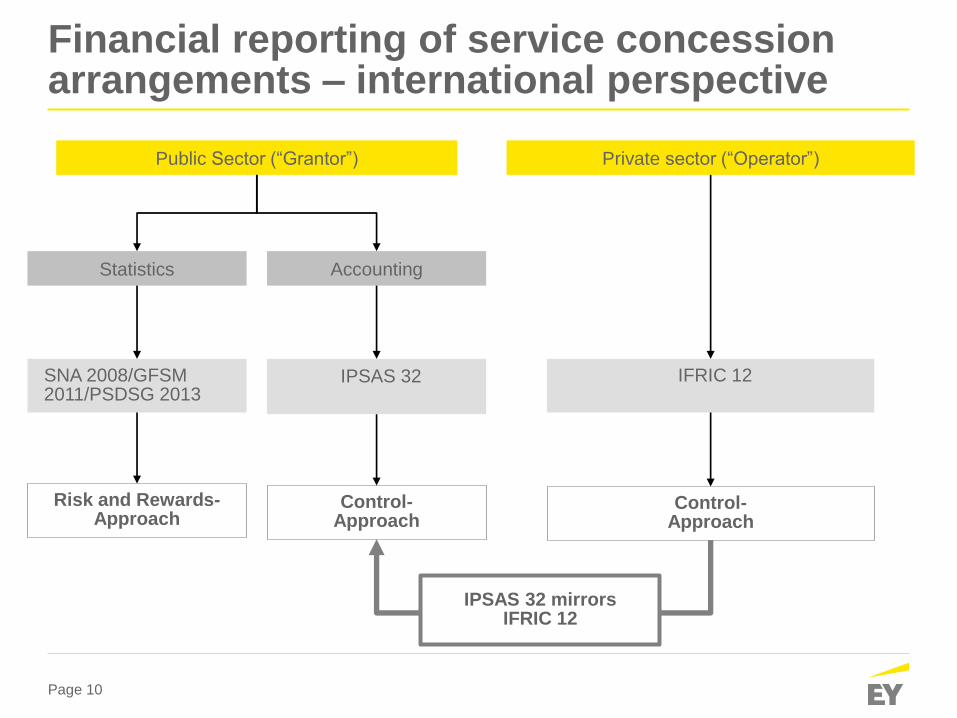

Financial reporting of service concession arrangements – international perspective

Public Sector (“Grantor”) Private sector (“Operator”)

IFRIC 12

Statistics Accounting

SNA 2008/GFSM 2011/PSDSG 2013

IPSAS 32

Control- Approach

Risk and Rewards-Approach

Control- Approach

IPSAS 32 mirrors IFRIC 12

Page 11

Accounting approaches for PPPs Risks and rewards vs control

Risk and Rewards Approach

Control Approach

Accounting ownership of an asset lies with the party that:

► carries the risks, benefits and burden in connection with the asset.

Accounting ownership of an asset lies with the party that:

► controls what services the private sector partner must provide, to whom and what price and

► has control over the residual value of the asset

Accounting Ownership Relevant Standards

► IFRIC 4/IAS 17

► IPSAS 13

► GFSM 2010

► ESA 95/2010

►IFRIC 12

►IPSAS 32

Typically construction risk

and asset availability risk are

transferred to the private

sector entity; while service

demand risk is not

=> In that case PPP scheme

is booked as service

arrangement, i.e. no service

concession asset, no liability

E.g. IPSAS 32 requires:

► Recognition of service concession asset based upon ‘power to control and regulate’ the use of the asset

► Recognition of obligations as either a financial liability or as deferred income

Accounting in Practice

Page 12

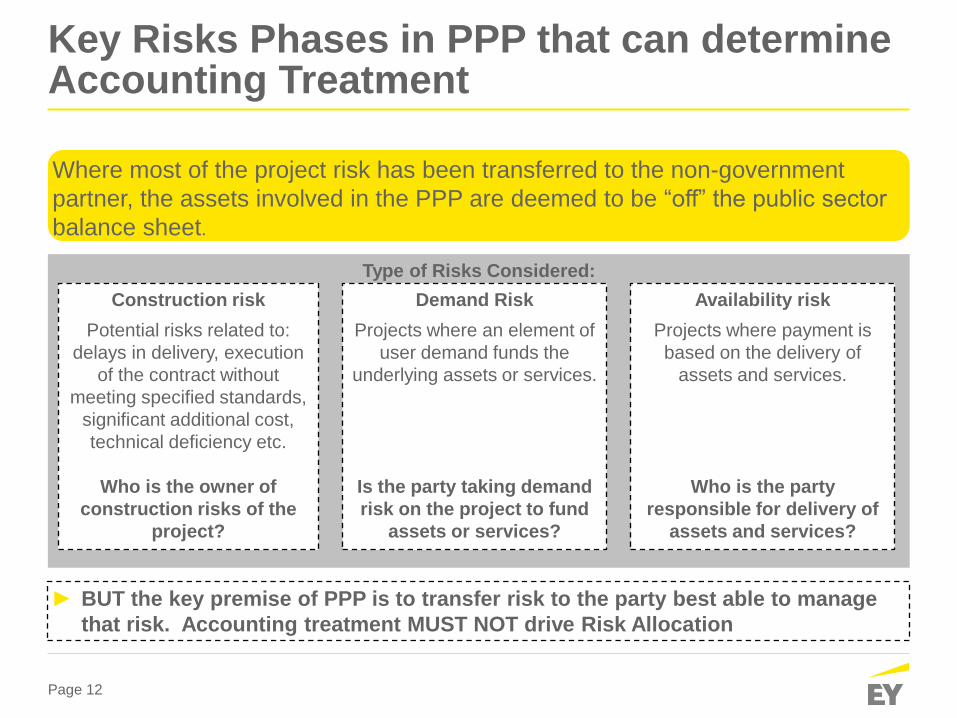

Key Risks Phases in PPP that can determine Accounting Treatment

Where most of the project risk has been transferred to the non-government

partner, the assets involved in the PPP are deemed to be “off” the public sector

balance sheet.

Type of Risks Considered:

Construction risk

Potential risks related to:

delays in delivery, execution

of the contract without

meeting specified standards,

significant additional cost,

technical deficiency etc.

Who is the owner of

construction risks of the

project?

Availability risk

Projects where payment is

based on the delivery of

assets and services.

Who is the party

responsible for delivery of

assets and services?

Demand Risk

Projects where an element of

user demand funds the

underlying assets or services.

Is the party taking demand

risk on the project to fund

assets or services?

► BUT the key premise of PPP is to transfer risk to the party best able to manage

that risk. Accounting treatment MUST NOT drive Risk Allocation

Page 13

“On” and “Off” Balance Sheet Treatment

Off-Balance sheet

► Implies accounting only for the annual

payments it makes to the PPP

operator, and not for the assets and

liabilities of the project, including its

debt

► It is attractive as long-term obligations

under PPPs do not appear under

government’s financial

statements/budget and help to keep

government net debt within the

reference value

► However credit rating agencies are

now challenging this view in

government ratings

On-Balance sheet

► On-balance sheet treatment implies

the recording of total liabilities when

the project commences or at

commercial acceptance

► Typically reported through “liability”

(deferred revenue) with the investment

in PPP assets recorded from the

outset and amortized over the project

life

► Implies that it consequently increases

gross liabilities recognised on balance

sheet. Net-effect is balanced by

recognition of an asset

Page 14

Accounting Requirements of IPSAS 32

Page 15

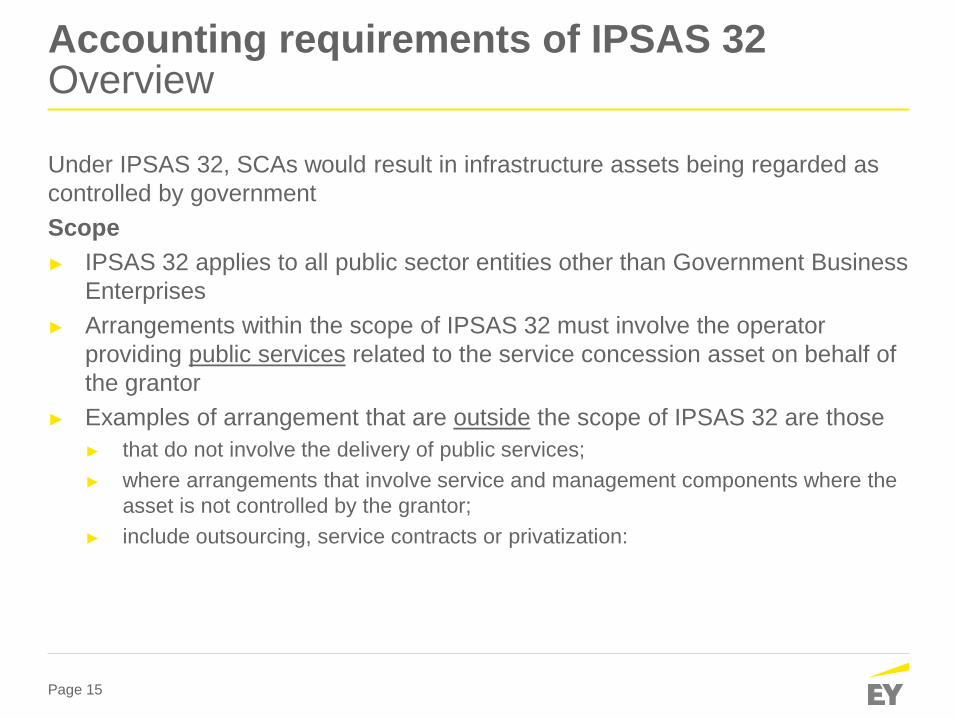

Accounting requirements of IPSAS 32 Overview Under IPSAS 32, SCAs would result in infrastructure assets being regarded as

controlled by government

Scope

► IPSAS 32 applies to all public sector entities other than Government Business

Enterprises

► Arrangements within the scope of IPSAS 32 must involve the operator

providing public services related to the service concession asset on behalf of

the grantor

► Examples of arrangement that are outside the scope of IPSAS 32 are those

► that do not involve the delivery of public services;

► where arrangements that involve service and management components where the

asset is not controlled by the grantor;

► include outsourcing, service contracts or privatization:

Page 16

Accounting requirements of IPSAS 32 Overview Definitions

► Service Concession Arrangement is a binding arrangement between a

grantor and an operator in which

► the operator uses the service concession asset to provide a public service on

behalf of the grantor for a specified period of time; and

► the operator is compensated for its services over the period of the service

concession arrangement.

► A grantor is the entity that grants the right to use the service

concession asset to the operator

► An operator is the entity that uses the asset to provide public

services subject to the grantor´s control of the asset

► A service concession asset is an asset used to provide public

services in a service concession arrangement that

► is provided by the operator (construct/develop/acquire or existing asset)

► is provided by the grantor (existing asset or update)

Page 17

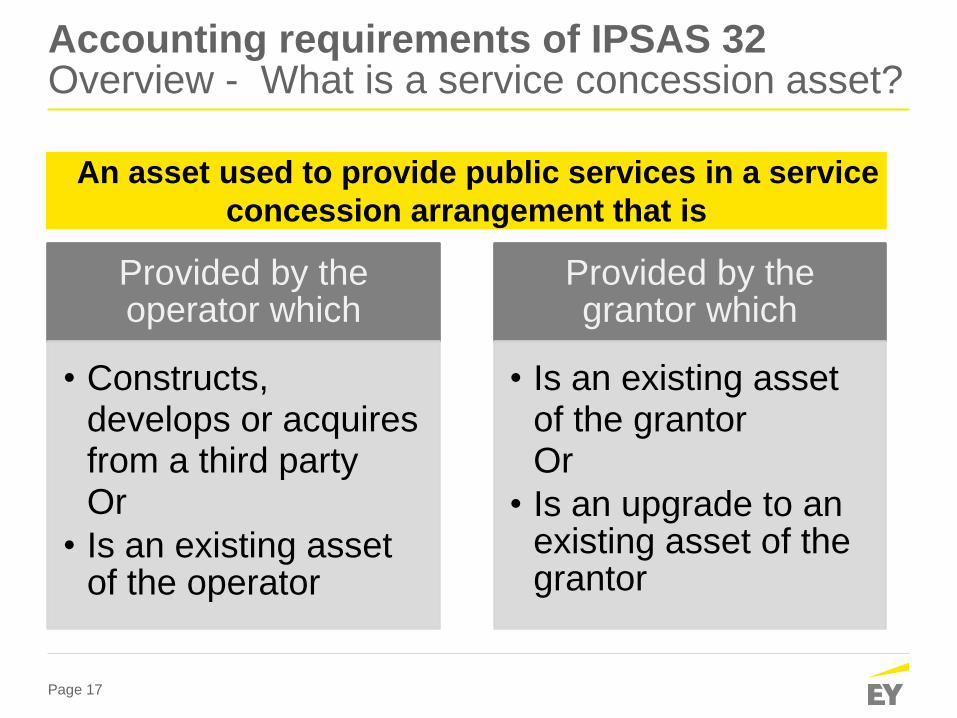

Accounting requirements of IPSAS 32 Overview - What is a service concession asset?

►An asset used to provide public services in a service

concession arrangement that is

Provided by the operator which

• Constructs, develops or acquires from a third party Or

• Is an existing asset of the operator

Provided by the grantor which

• Is an existing asset of the grantor Or

• Is an upgrade to an existing asset of the grantor

Page 18

Accounting requirements of IPSAS 32 Accounting for service concession asset Recognition

► A government recognizes an asset in its financial statements

when (IPSAS 32.9):

► The grantor controls or regulates the services to be provided by the

operator

and

► The grantor controls any significant residual interest in the asset at the

end of the arrangement

► However: the recognition criteria in IPSAS 17/ IPSAS 31 have

to be fulfilled

► it is probable that future economic benefits associated with the item will

flow to the entity

► the cost or fail value of the item can be measured reliably

-> e.g. during construction period: progress reports by the operator (AG23).

Page 19

Accounting requirements of IPSAS 32 Accounting for service concession asset

Measurement

► Initial measurement of the asset is at fair value does not

constitute revaluation under IPSAS 17 Property, Plant and

Equipment / IPSAS 31 Intangible Assets (IPSAS 32.11)

► After initial recognition, the asset shall be accounted for as a

separate class of assets in accordance with IPSAS 17 or

IPSAS 31, as appropriate

► historical cost method

► revaluation method

► In cases where an existing asset is subject to a SCA, the

grantor shall reclassify the asset

► the requirement of IPSAS 32.11 does not apply to reclassifications,

i.e. no re-measurement at fair value in this case (AG24)!

Page 20

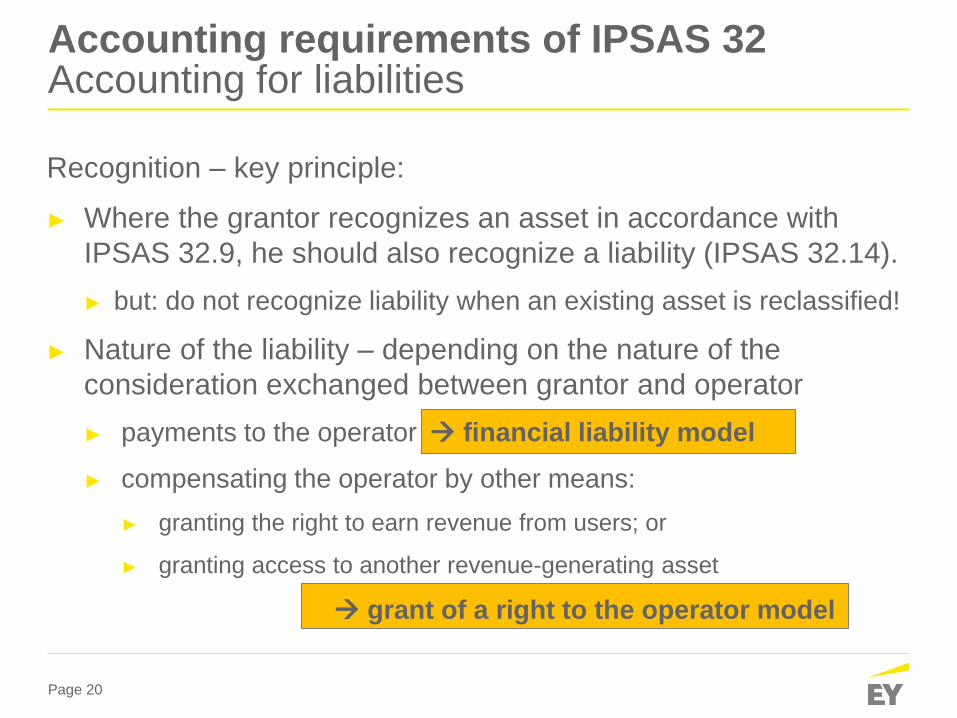

Recognition – key principle:

► Where the grantor recognizes an asset in accordance with

IPSAS 32.9, he should also recognize a liability (IPSAS 32.14).

► but: do not recognize liability when an existing asset is reclassified!

► Nature of the liability – depending on the nature of the

consideration exchanged between grantor and operator

► payments to the operator financial liability model

► compensating the operator by other means:

► granting the right to earn revenue from users; or

► granting access to another revenue-generating asset

grant of a right to the operator model

Accounting requirements of IPSAS 32 Accounting for liabilities

Page 21

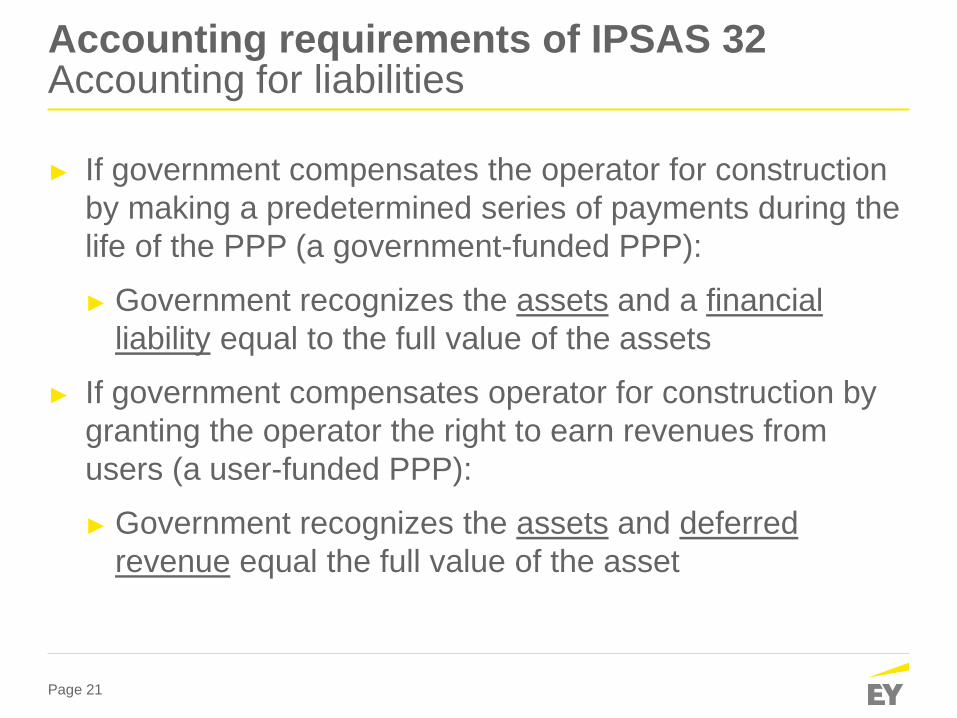

Accounting requirements of IPSAS 32 Accounting for liabilities

► If government compensates the operator for construction

by making a predetermined series of payments during the

life of the PPP (a government-funded PPP):

► Government recognizes the assets and a financial

liability equal to the full value of the assets

► If government compensates operator for construction by

granting the operator the right to earn revenues from

users (a user-funded PPP):

► Government recognizes the assets and deferred

revenue equal the full value of the asset

Page 22

Accounting requirements of IPSAS 32 Accounting for liabilities

Measurement:

► The liability recognized shall be initially measured at the same

amount as the service concession asset (IPSAS 32.15)

It is likely that the government’s gross debt increases by the amount of the

liability, while net worth remains unchanged

► Subsequent measurement is depending on the nature of

the liability

► Financial liability model: measurement according to IPSAS 29 (IPSAS

32.20)

► Grant of a right model: the grantor shall account for the liability as the

unearned portion of the revenue arising from the exchange of assets with

the operator (IPSAS 32.24).

► For mixed arrangements: it is necessary to account separately for each

part of the total liability recognized (IPSAS 32.27).

Page 23

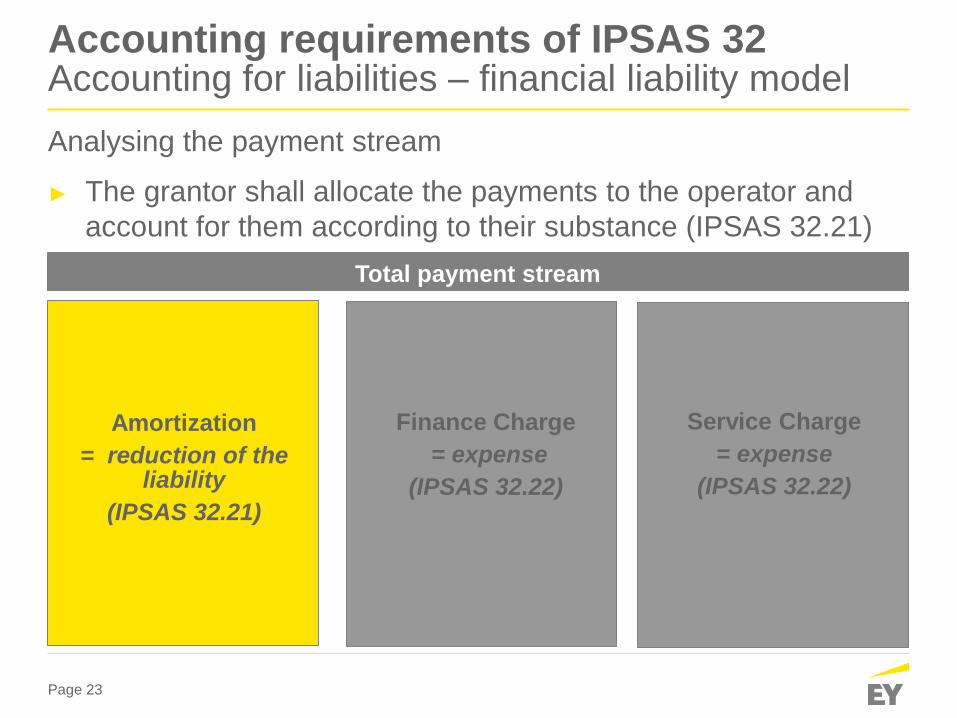

Accounting requirements of IPSAS 32 Accounting for liabilities – financial liability model

Analysing the payment stream

► The grantor shall allocate the payments to the operator and

account for them according to their substance (IPSAS 32.21)

Amortization

= reduction of the liability

(IPSAS 32.21)

Finance Charge

= expense

(IPSAS 32.22)

Service Charge

= expense

(IPSAS 32.22)

Total payment stream

Page 24

Accounting requirements of IPSAS 32 Accounting for liabilities – financial liability model

How to allocate the payment streams (IPSAS 32.23):

► Asset and service components are separately identifiable:

► service components shall be allocated by reference to the relative fair

values of the asset and the services

► Asset and service components are not separately identifiable:

► the service component of payments to the operator is determined using

estimation techniques (similar transactions observable?)

► i.e. the fair value of the asset (IPSAS 32.11) is determined by using

estimation techniques (AG31) assessment of comparable assets

► Service component is recognized evenly over the term of the

arrangement – best correspondents to service provision

► only in cases when specific expenses are required to be separately

compensated, and timing is known, these are recognized as incurred

(AG46)

Page 25

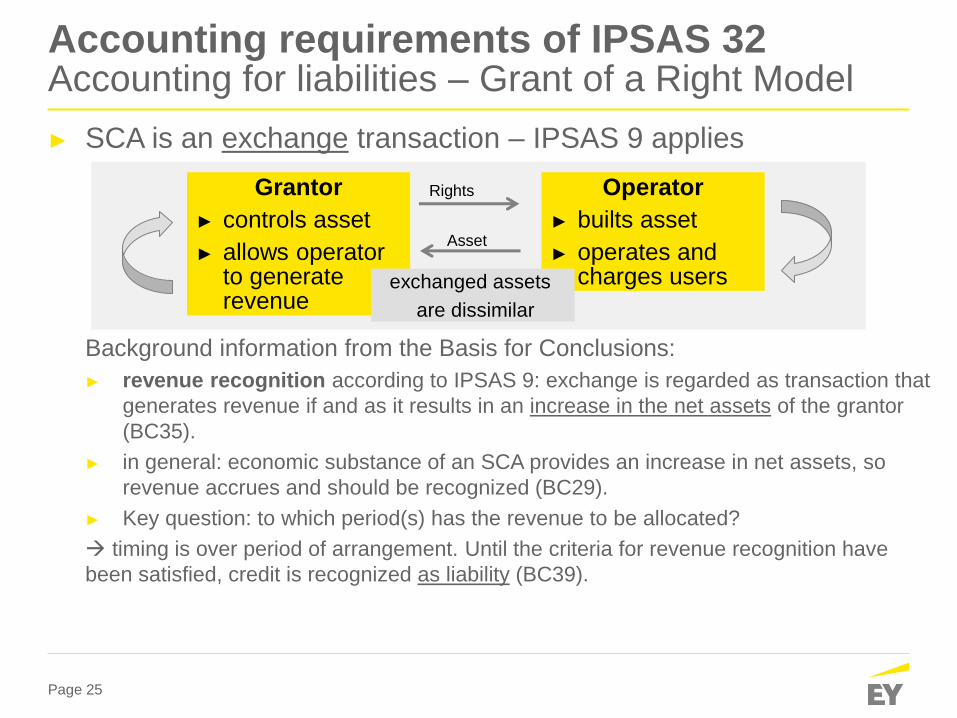

► SCA is an exchange transaction – IPSAS 9 applies

Background information from the Basis for Conclusions:

► revenue recognition according to IPSAS 9: exchange is regarded as transaction that

generates revenue if and as it results in an increase in the net assets of the grantor

(BC35).

► in general: economic substance of an SCA provides an increase in net assets, so

revenue accrues and should be recognized (BC29).

► Key question: to which period(s) has the revenue to be allocated?

timing is over period of arrangement. Until the criteria for revenue recognition have

been satisfied, credit is recognized as liability (BC39).

Accounting requirements of IPSAS 32 Accounting for liabilities – Grant of a Right Model

Grantor

► controls asset

► allows operator to generate revenue

Operator

► builts asset

► operates and charges users

Rights

Asset

exchanged assets

are dissimilar

Page 26

Accounting requirements of IPSAS 32 Accounting for liabilities – grant of a right model

► General principle (IPSAS 32.24): the grantor shall account for

the liability recognized in accordance with para.14 as the

unearned portion of the revenue arising from the exchange of

assets

► As the right granted to the operator is effective for the period of the

arrangement, the grantor does not recognize revenue from the

exchange immediately (IPSAS 32.26; under ED 43: “performance

obligation”)

the grantor earns the benefit associated with the assets received in

exchange for the right granted to the operator over the period of the

arrangement (AG47)

► The revenue is recognized according to the economic substance

of the service concession arrangement, and the liability is reduced

as revenue is recognized

Page 27

EY Contacts

Thomas, Global Leader of EY’s IPSAS Sector

Group, was the German Board Member of the

IPSASB (2009-2014), since 2016 he is the

Chairman of the IPSASB CAG. Besides that,

Thomas is Chairman of the Public Sector

Committee (PSC) of the Federation of Euro-

pean Accountants (Fédération des Experts

Comptables Européens - FEE).

Thomas has many years of worldwide exper-

ience in auditing and advising governments as

well as public and municipal companies, and

European organisa-tions including Eurostat. In

2009-2010 he was also appointed as external

IPSAS expert for the temporary “DAS Think

Tank” of the European Court of Auditors. Since

2013, Thomas is a member of the Accounting

Advisory Group of the European Commission.

As FEE PSG chair, he contributed to both Euro-

stat Task Forces “EPSAS Governance” and

“EPSAS Standards”. Currently, he represents

FEE at the EPSAS Working Group and Cells.

Thomas Müller-Marqués Berger German Certified Public Accountant

Partner

Global Leader International Public Sector

Accounting

Phone: +49 711 9881 15844

Mobile: +49 160 939 15844

Fax: +49 181 3943 15844

thomas.mueller-marques.berger

@de.ey.com

Ernst & Young GmbH

Wirtschaftsprüfungsgesellschaft

Mittlerer Pfad 15

70499 Stuttgart

ey.com