accounting for vat.pdf

TRANSCRIPT

You must show the VAT claimed as a separate total in your purchase records.

The basic T- account transaction is as follows:

Transaction (VAT Rate is 15%)

List of typical “business records” include:• Annual accounts, including profit and loss accounts• Bank statements and deposit slips• Cashbooks and other account books• Purchase invoices and copy sales invoices• VAT Credit or debit notes• Orders and delivery notes• Purchase and sales books• Records of daily takings such as till rolls• Import and export documents• Business correspondence• Your VAT account

These notes are for guidance only. They reflect the Law and the Department’s position at the time of publication. They do not replace the Legislation or affect your Rights of Appeal about your tax position.

If in doubt, consult the Inland Revenue Department, VAT Section.Each leaflet covers just one topic. Other leaflets you may find useful include:

What is VAT?Should I be registered for VAT?

How to register for VAT?After RegistrationBasic Supply RulesMixed Supply RulesAccounting for VATReporting the VAT

Penalties and Offences under the VAT ActVAT Legislative Overview

VAT and the ConsumerFiling VAT Returns

VAT DocumentsInput Tax DeductionsVAT & Entertainment

Transitional Provisions

You can get further help and copies of forms and information leaflets from the Inland Revenue Department in Castries, Vieux Fort and Soufriere or The VAT Section, Manoel Street, Castries.

For further information contact us at:

Tel: (758) 468 1420Email: [email protected]

Website: www.vat.gov.lc

© Ministry of FinanceInland Revenue Department

April 2012

Accounting for VAT1.

Business buys goods to sell for cash VAT Inclusive - $3,000 + 450 VAT2. Business sells goods for cash - $6,000 + $900 VAT3. Business sells foods on credit - $5,000 + 750 VAT4. Business imports foods to sell on credit - $30,000 + $4,500 VAT

Date Invoice # Supplies / Sales Output tax Total

Standard -rate Other rate Zero-rate Exempt

Total

INVOICE/Custom DATE

INVOICE/ Entry

SUPPLIER'S TIN# SUPPLIER

TAXABLE VALUE VAT TOTAL

Total

Input Tax $ Output Tax $ Domestic purchases Supply of goods/services

Imports Debit note issued

Debit note received Credit note received

Credit note issued Bad debt recovered

Bad debt Goods taken for non-business

Adjustments for errors etc

Adjustments for errors etc

Total Input tax allowable

Total output tax

Less Input tax allowable

Tax payable/creditable

Date Invoice # Supplies / Sales Output tax Total

Standard -rate Other rate Zero-rate Exempt

Total

INVOICE/Custom DATE

INVOICE/ Entry

SUPPLIER'S TIN# SUPPLIER

TAXABLE VALUE VAT TOTAL

Total

Input Tax $ Output Tax $ Domestic purchases Supply of goods/services

Imports Debit note issued

Debit note received Credit note received

Credit note issued Bad debt recovered

Bad debt Goods taken for non-business

Adjustments for errors etc

Adjustments for errors etc

Total Input tax allowable

Total output tax

Less Input tax allowable

Tax payable/creditable

Date Invoice # Supplies / Sales Output tax Total

Standard -rate Other rate Zero-rate Exempt

Total

INVOICE/Custom DATE

INVOICE/ Entry

SUPPLIER'S TIN# SUPPLIER

TAXABLE VALUE VAT TOTAL

Total

Input Tax $ Output Tax $ Domestic purchases Supply of goods/services

Imports Debit note issued

Debit note received Credit note received

Credit note issued Bad debt recovered

Bad debt Goods taken for non-business

Adjustments for errors etc

Adjustments for errors etc

Total Input tax allowable

Total output tax

Less Input tax allowable

Tax payable/creditable

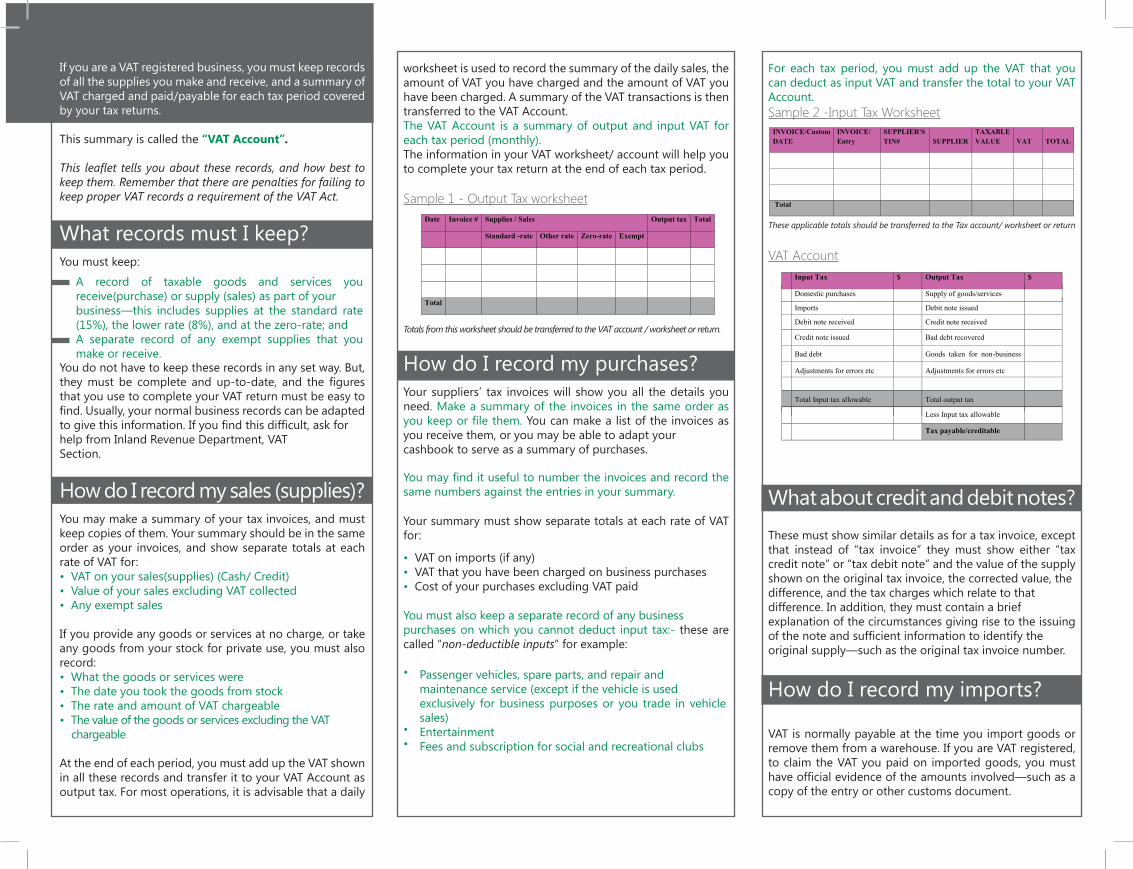

A record of taxable goods and services you receive(purchase) or supply (sales) as part of your business—this includes supplies at the standard rate (15%), the lower rate (8%), and at the zero-rate; andA separate record of any exempt supplies that you make or receive.

Passenger vehicles, spare parts, and repair and maintenance service (except if the vehicle is used exclusively for business purposes or you trade in vehicle sales)EntertainmentFees and subscription for social and recreational clubs

For each tax period, you must add up the VAT that you can deduct as input VAT and transfer the total to your VAT Account.Sample 2 -Input Tax Worksheet

These applicable totals should be transferred to the Tax account/ worksheet or return

VAT Account

What about credit and debit notes?These must show similar details as for a tax invoice, except that instead of “tax invoice” they must show either “tax credit note” or “tax debit note” and the value of the supply shown on the original tax invoice, the corrected value, the difference, and the tax charges which relate to that difference. In addition, they must contain a brief explanation of the circumstances giving rise to the issuing of the note and sufficient information to identify the original supply—such as the original tax invoice number.

How do I record my imports?

VAT is normally payable at the time you import goods or remove them from a warehouse. If you are VAT registered, to claim the VAT you paid on imported goods, you must have official evidence of the amounts involved—such as a copy of the entry or other customs document.

worksheet is used to record the summary of the daily sales, the amount of VAT you have charged and the amount of VAT you have been charged. A summary of the VAT transactions is then transferred to the VAT Account. The VAT Account is a summary of output and input VAT for each tax period (monthly).The information in your VAT worksheet/ account will help you to complete your tax return at the end of each tax period.

Sample 1 - Output Tax worksheet

Totals from this worksheet should be transferred to the VAT account / worksheet or return.

How do I record my purchases?Your suppliers’ tax invoices will show you all the details you need. Make a summary of the invoices in the same order as you keep or file them. You can make a list of the invoices as you receive them, or you may be able to adapt your cashbook to serve as a summary of purchases.

You may find it useful to number the invoices and record the same numbers against the entries in your summary.

Your summary must show separate totals at each rate of VAT for:

• VAT on imports (if any)• VAT that you have been charged on business purchases • Cost of your purchases excluding VAT paid

You must also keep a separate record of any business purchases on which you cannot deduct input tax:- these are called “non-deductible inputs” for example:

•

• •

If you are a VAT registered business, you must keep records of all the supplies you make and receive, and a summary of VAT charged and paid/payable for each tax period covered by your tax returns.

This summary is called the “VAT Account”.

This leaflet tells you about these records, and how best to keep them. Remember that there are penalties for failing to keep proper VAT records a requirement of the VAT Act.

What records must I keep?You must keep:

You do not have to keep these records in any set way. But, they must be complete and up-to-date, and the figures that you use to complete your VAT return must be easy to find. Usually, your normal business records can be adapted to give this information. If you find this difficult, ask for help from Inland Revenue Department, VAT Section.

How do I record my sales (supplies)?You may make a summary of your tax invoices, and must keep copies of them. Your summary should be in the same order as your invoices, and show separate totals at each rate of VAT for:• VAT on your sales(supplies) (Cash/ Credit)• Value of your sales excluding VAT collected• Any exempt sales

If you provide any goods or services at no charge, or take any goods from your stock for private use, you must also record:• What the goods or services were• The date you took the goods from stock• The rate and amount of VAT chargeable• The value of the goods or services excluding the VAT chargeable

At the end of each period, you must add up the VAT shown in all these records and transfer it to your VAT Account as output tax. For most operations, it is advisable that a daily