accounting grade 11- chapter 4 recording of transaction ii

TRANSCRIPT

1

Recording of Transactions - II

Questions For Practice

Short Answers

1. Briefly state how the cash book is both journal and a ledger.

Ans) Cash book is journal in the sense that all cash transactions are primarily recorded in the cash book with narration and therefore, these

are posted to the relevant accounts in the ledger. Cash book is also ledger in the sense that it serves the purpose of cash account and bank

account (in case of triple column cash book)

2. What is the purpose of contra entry?

Ans) The purpose of Contra Entry is to record reverse or offset an entry on the other side of an account. If a debit entry is recorded in an

account, contra entry will be recorded on the credit side and vice-versa.

Debit and credit aspects of a single transaction are entered in the same account, but in different columns. Each entry in this case is viewed as

a contra entry of the other.

3. What are special purpose books?

Ans) Special purpose books are :

1. Cash Book

2. Purchases Book

3. Purchases Return (Return Outwards) Book

4. Sales Book

5. Sales Return (Return Inwards) Book

6. Journal Proper

4. What is petty cash book? How it is prepared?

Ans) Businesses generally keep small amounts of cash to meet small miscellaneous payments such as entertainment expenses and stationery

costs. Such payments are generally recorded in the book called as petty cash. It is prepared by imprest system whereby an amount is paid in

advance called as 'Float' & it is a fixed amount. This is the maximum amount of cash that can be held at any time. Each time cash level runs

low, the petty cash imprest is injected with cash by drawing a cheque. The amount of reimbursement is equal to the expenses paid through

petty cash since the time of last reimbursement. Petty cash balance after reimbursement reverts to back to the level of the float.

2

5. Explain the meaning of posting of journal entries?

Ans) Posting is the process of transferring the entries from the books of original entry (journal) to the

ledger. In other words, posting means grouping of all the transactions in respect to a particular account at one place for meaningful conclusion

and to further the accounting process.

6. Define the purpose of maintaining subsidiary journal.

Ans) Subsidiary books are maintained because it may be impossible to record each transaction into the ledger as it occurs. Subsidiary books

record the details of the transactions and therefore help the ledger to become brief. Future reference and any desired analysis becomes easy

as transactions of similar nature are recorded together in subsidiary books.

7. Write the difference between return Inwards and return outwards.

Ans ) Return Outwards:

Faulty or wrong goods that the business returns back to suppliers.

Return Inwards:

Faulty or wrong goods that the customers return back to the business

8. What do you understand by ledger folio?

Ans ) Ledger folio is page number of an entry in the company's ledger. A ledger folio in accounting is often abbreviated LF.

9. What is difference between trade discount and cash discount?

Ans)

Cash Discount Trade Discount

Is a reduction granted by

supplier from the invoice

price in consideration of

immediate or prompt

payment

Is a reduction granted by

supplier from the list price

of goods or services on

business consideration re:

buying in bulk for goods

and longer period when in

terms of services

3

As an incentive in credit

management to

encourage prompt

payment

Allowed to promote the

sales

Not shown in the

supplier bill or invoice

Shown by way of

deduction in the invoice

itself

Cash discount account is

opened in the ledger

Trade discount account is

not opened in the ledger

Allowed on payment of

money

Allowed on purchase of

goods

It may vary with the time

period within which

payment is received

It may vary with the

quantity of goods

purchased or amount of

purchases made

10. Write the process of preparing ledger from a journal.

Ans) The complete process of posting from journal to ledger is as follows:

Step 1 : Locate in the ledger, the account to be debited as entered in the journal.

Step 2 : Enter the date of transaction in the date column on the debit side.

Step 3 : In the ‘Particulars’ column write the name of the account through

which it has been debited in the journal.

Step 4 : Enter the page number of the journal in the folio column and in the

journal write the page number of the ledger on which a particular account appears.

Step 5 : Enter the relevant amount in the amount column on the debit side.

It may be noted that the same procedure is followed for making the entry on

the credit side of that account to be credited. An account is opened only once

4

in the ledger and all entries relating to a particular account is posted on the

debit or credit side, as the case may be.

11. What do you understand by Imprest amount in petty cash book?

Ans) Imprest amount in petty cash book an amount paid in advance called as 'Float' & it is a fixed amount. This is the maximum amount of

cash that can be held at any time. Each time cash level runs low, the petty cash imprest is injected with cash by drawing a cheque. The amount

of reimbursement is equal to the expenses paid through petty cash since the time of last reimbursement. Petty cash balance after

reimbursement reverts to back to the level of the float.

Long Answers

1. Explain the need for drawing up the special purpose books.

Ans) A small business may be able to record all its transactions in one book only, i.e., the journal. But as the business expands and the

number of transactions becomes large, it may become cumbersome to journalise each transaction. For quick, efficient and accurate recording

of business

transactions, Journal is sub-divided into special journals. Many of the business transactions are repetitive in nature. They can be easily

recorded in special journals, each meant for recording all the transactions of a similar nature. For example, all cash transactions may be

recorded in one book, all credit sales transactions in another book and all credit purchases transactions in yet another book and so on.

These special journals are also called daybooks or subsidiary books. Transactions that cannot be recorded in any special journal are recorded

in journal called the Journal Proper. Special journals prove economical and make division of labour possible in accounting work.

Q.2. What is n Cash Book? Explain the types of cash book.

Ans) Cash book is used to record cash receipts and cash payments side by side. Cash book is ruled like a ledger account with the debit and

credit sides and the balance represents cash in hand at the end of accounting period. Besides being a book of original entry, the Cash Book

also serves as a ledger account. As such there is no need to open a separate cash account in the ledger. The basic form of Cash Book

remaining the same, additional columns may be provided on either side, if necessary. Cash book may be of following types: (i) Simple Cash

Book — Simple Cash Book has only one amount column on each side. This book serves the purpose of cash account. It is suited to concerns

which have only cash transactions. (ii) Two-column Cash Book — Two-column Cash Book has two amount columns: one for cash and another

for Bank on each side. This book serves the purpose of cash account as well as Bank account. It is suited to concerns which have cash

transactions and banking transactions. A business concern need not maintain a separate account for the banking transactions. At the end of

the accounting period the cash book reveals not only cash in hand but balance at bank also. There may be a two-column cash book containing

cash column and discount column also. On the debit side, all cash receipts and discount allowed to customers arc recorded. On the credit side,

5

all cash payments and discount received from creditors are recorded (iii) Three-column Cash Book —Three-column Cash Book is prepared

when there are a large number of cash and banking transactions. This Cash Book has three amount columns on each side, namely: cash

column, bank column and discount column. (iv) Petty Cash Book —In order to make the task of the cashier easy. A petty cashier is appointed

and handed over a small sum of money. He meets out small payments like stationery, postage, conveyance cartage etc. At the end of the

given period, the petty cashier submits the account to the cashier who reimburses him for payments.

Q.3. What is contra entry ? How can you deal this entry while preparing double column Cash Book?

Ans) Contra Entry is an entry which is recorded to reverse or offset an entry on the other side of an account. If a debit entry is recorded in an

account, contra entry will be recorded on the credit side and vice-versa.

Debit and credit aspects of a single transaction are entered in the same account, but in different columns. Each entry in this case is viewed as

a contra entry of the other.

Just like cash transactions, all payments into the bank are recorded on the left side and all withdrawals/

payments through the bank are recorded on the right side of two column cash book. When cash is

deposited in the bank or cash is withdrawn from the bank, both the entries are recorded in the two column cash book. This is so because both

aspects of the transaction appear in the two column cash book itself. When cash is paid into the bank, the amount deposited is written on the

left side in the bank column and at the same time the same amount is entered on the right side in the cash column. The reverse entries are

recorded when cash is withdrawn from the bank for use in the office. Against such entries the word C, which stands for contra is written in the

L.F. column indicating that these entries are not to be posted to the ledger account.

Q.4. What is petty cash book ? Write the Advantages of petty cash book.

Ans) Petty cash book may be defined as a specialised cash book which is used by a petty cashier to record all the small payments such as

cartage. postage. stationery. conveyance etc. Following are the advantages of maintaining a petty cash book : (1) Saving of time — The head

cashier is not bothered to make petty expenses and record their entries. This saves his time which can be utilised for other important matters.

(2) Saving of labour— Petty Cash Book saves the labour of head cashier in recording each and every entry in Cash Book and posting them to

the ledger accounts. (3) Simple to adopt —This is a simple method. Imprest system of petty cash facilitates its easy use. (4) Lesser mistakes

Since the petty cash book is maintained separately. the possibility of mistakes is reduced. The head cashier can check the accuracy of every

entry. (5) Control over payments — The head cashier supervises the maintenance of petty cash book and verifies the different payments from

vouchers This reduces the chances of fraud and wrong payment.

Q.5. Describe the advantages of sub-dividing the journal.

Ans)Following arc the advantages of sub-division of journal i.e.. subsidiary books :

6

(1)The most important advantage of the sub-division of journal is that it permits division of labour which is very necessary in a large

organisation. The process of recording can be divided among several persons. each of whom is responsible for particular type of transactions.

(2)Since, there is a separate book for each class of transactions. The information relating to each class of transactions is available at one

place. Sub-division of journal provides classified information. Periodical details of important business transactions can be known very easily.

(3)Various accounting processes may be undertaken simultaneously because of the use of a number of books. This will lead to the work being

completed quickly and efficiently. (4)Errors and mistakes if any, in entering transactions can be located easily from subsidiary books. (5)There

is less wastage of stationery- because there will be no repetition of journal entries. The record can be made much briefer and a great amount of

clerical effort and stationery can be saved.

Q.6. What do you understand by balancing of account ?

Ans) Accounts in the ledger are periodically balanced, generally at the end of the accounting period, with the object of ascertaining the net

position of each amount. Balancing of an account means that the two sides are totaled and the difference between them is shown on the side,

which is shorter in order to make their totals equal. The words ‘balance c/d’ are written against the amount of the difference between the two

sides. The amount of balance is brought (b/d) down in the next accounting period indicating that it is a continuing account, till finally settled or

closed.

Numerical Questions

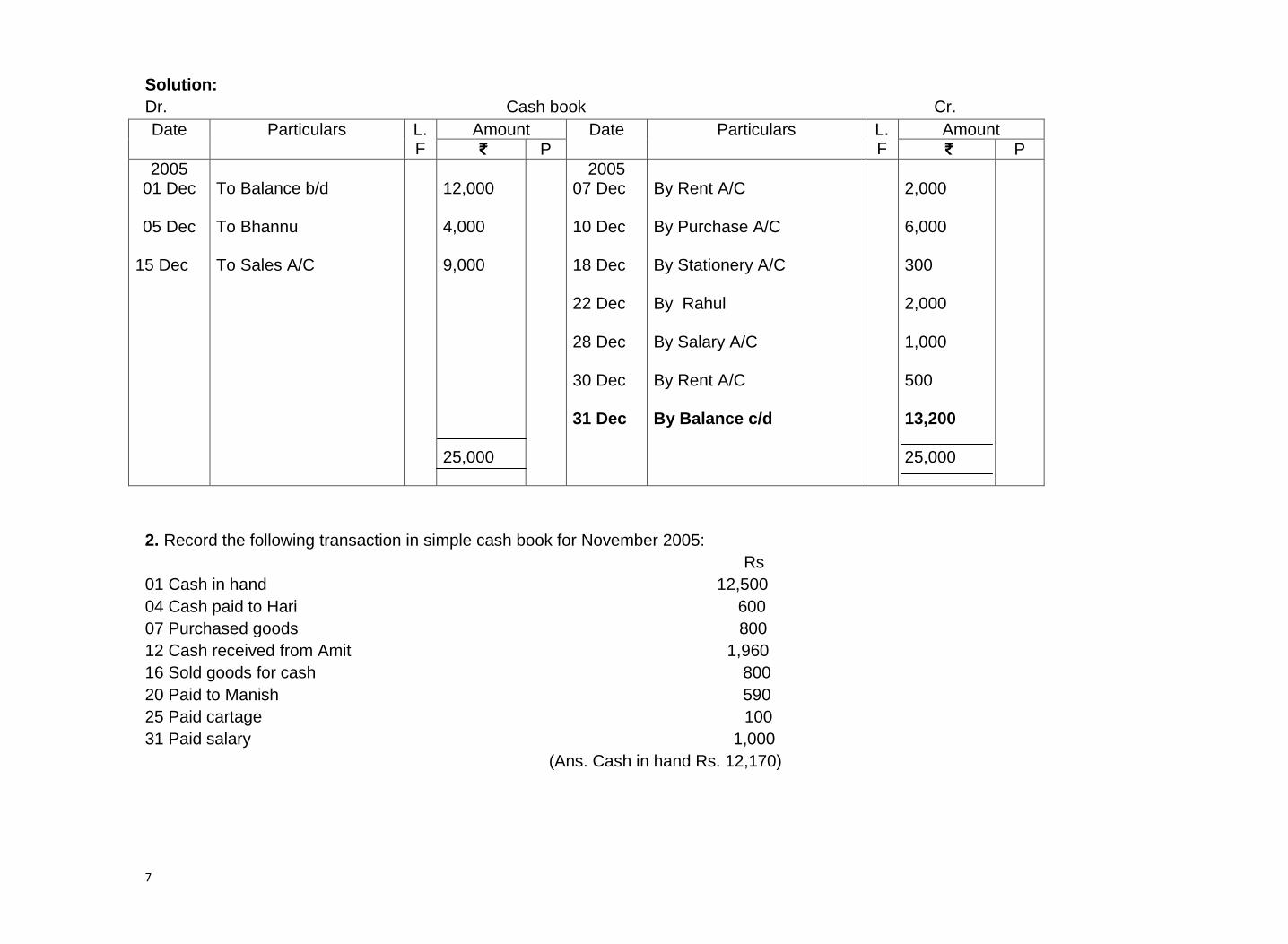

1. Enter the following transactions in a simple cash book for December 2005:

Rs.

01 Cash in hand 12,000

05 Cash received from Bhanu 4,000

07 Rent Paid 2,000

10 Purchased goods Murari for cash 6,000

15 Sold goods for cash 9,000

18 Purchase stationery 300

22 Cash paid to Rahul on account 2,000

28 Paid salary 1,000

30 Paid rent 500

(Ans. Cash in hand Rs. 13,200)

7

Solution:

Dr. Cash book Cr.

Date Particulars L.F

Amount Date Particulars L.F

Amount

₹ P ₹ P

2005 01 Dec

05 Dec

15 Dec

To Balance b/d To Bhannu To Sales A/C

12,000 4,000 9,000 25,000

2005 07 Dec 10 Dec 18 Dec 22 Dec 28 Dec 30 Dec 31 Dec

By Rent A/C By Purchase A/C By Stationery A/C By Rahul By Salary A/C By Rent A/C By Balance c/d

2,000 6,000 300 2,000 1,000 500 13,200 25,000

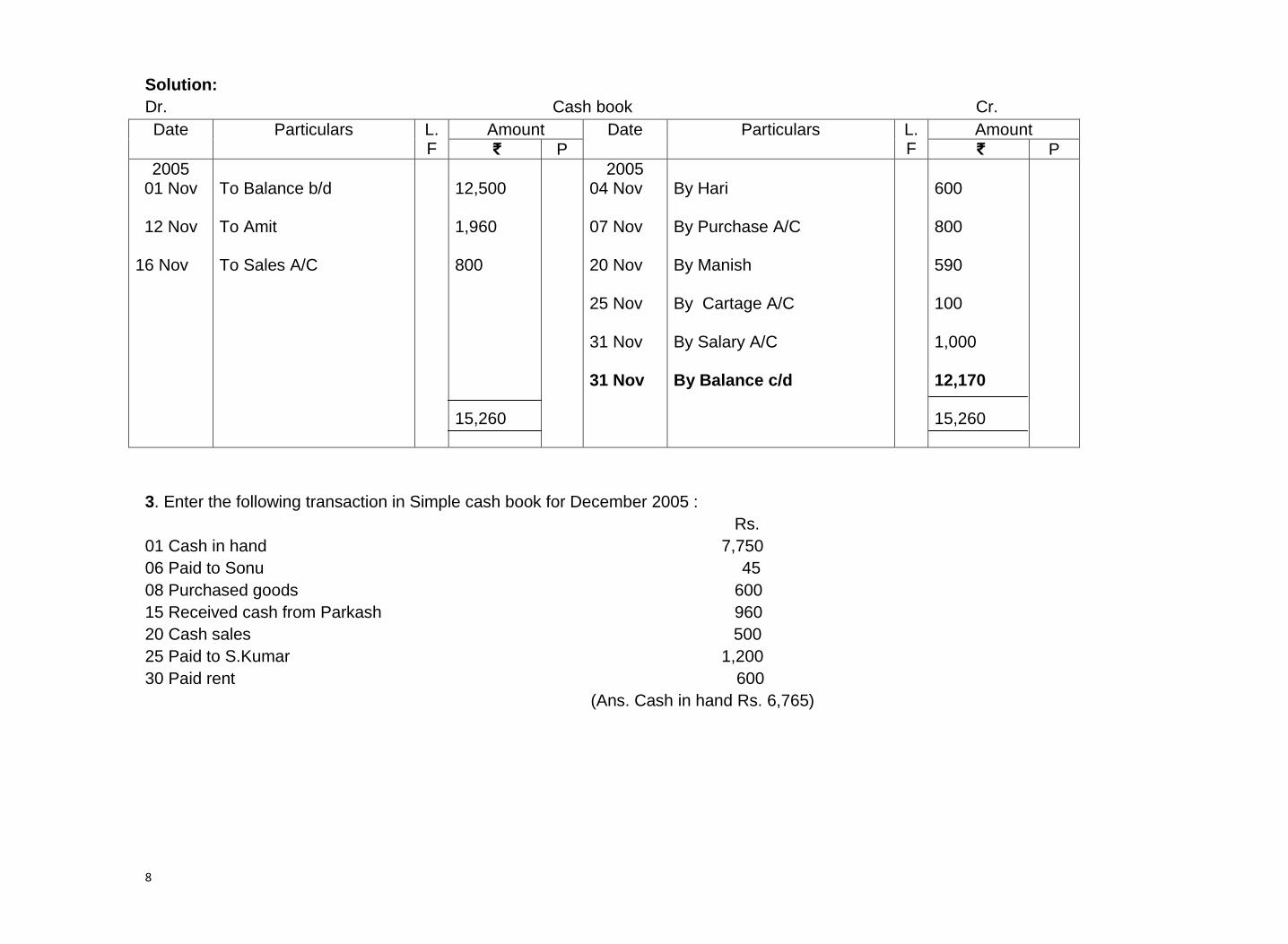

2. Record the following transaction in simple cash book for November 2005:

Rs

01 Cash in hand 12,500

04 Cash paid to Hari 600

07 Purchased goods 800

12 Cash received from Amit 1,960

16 Sold goods for cash 800

20 Paid to Manish 590

25 Paid cartage 100

31 Paid salary 1,000

(Ans. Cash in hand Rs. 12,170)

8

Solution:

Dr. Cash book Cr.

Date Particulars L.F

Amount Date Particulars L.F

Amount

₹ P ₹ P

2005 01 Nov

12 Nov

16 Nov

To Balance b/d To Amit To Sales A/C

12,500 1,960 800 15,260

2005 04 Nov 07 Nov 20 Nov 25 Nov 31 Nov 31 Nov

By Hari By Purchase A/C By Manish By Cartage A/C By Salary A/C By Balance c/d

600 800 590 100 1,000 12,170 15,260

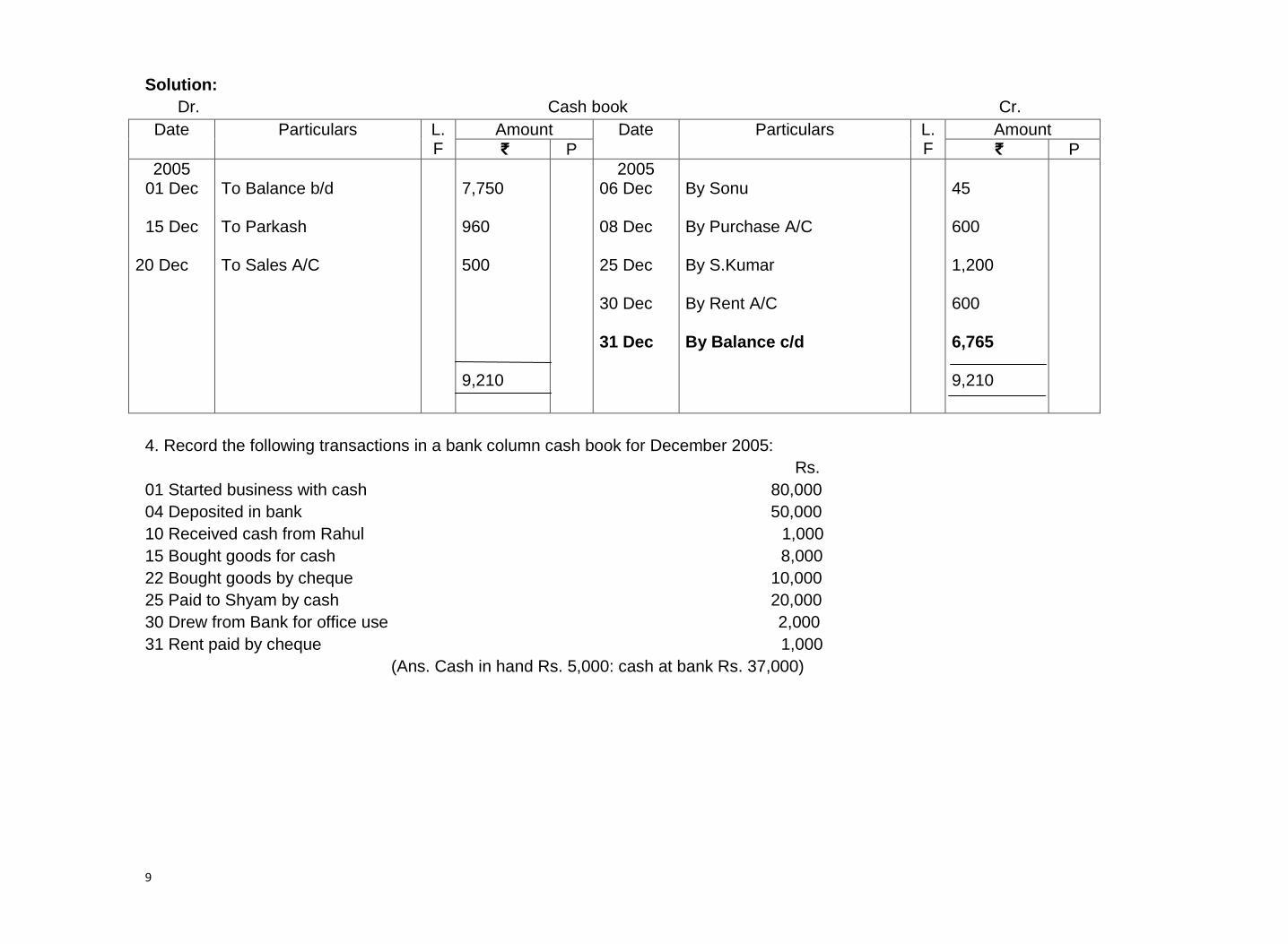

3. Enter the following transaction in Simple cash book for December 2005 :

Rs.

01 Cash in hand 7,750

06 Paid to Sonu 45

08 Purchased goods 600

15 Received cash from Parkash 960

20 Cash sales 500

25 Paid to S.Kumar 1,200

30 Paid rent 600

(Ans. Cash in hand Rs. 6,765)

9

Solution:

Dr. Cash book Cr.

Date Particulars L.F

Amount Date Particulars L.F

Amount

₹ P ₹ P

2005 01 Dec

15 Dec

20 Dec

To Balance b/d To Parkash To Sales A/C

7,750 960 500 9,210

2005 06 Dec 08 Dec 25 Dec 30 Dec 31 Dec

By Sonu By Purchase A/C By S.Kumar By Rent A/C By Balance c/d

45 600 1,200 600 6,765 9,210

4. Record the following transactions in a bank column cash book for December 2005:

Rs.

01 Started business with cash 80,000

04 Deposited in bank 50,000

10 Received cash from Rahul 1,000

15 Bought goods for cash 8,000

22 Bought goods by cheque 10,000

25 Paid to Shyam by cash 20,000

30 Drew from Bank for office use 2,000

31 Rent paid by cheque 1,000

(Ans. Cash in hand Rs. 5,000: cash at bank Rs. 37,000)

10

Solution:

Dr. Bank Column Cash book Cr.

Date Particulars L.F Amount Date Particulars L.F Amount

Cash ₹

Bank ₹

Cash ₹

Bank ₹

2005 01 Dec

04 Dec

10 Dec 30 Dec

To Balance b/d To Cash A/C To Rahul To Bank A/C

©

©

80,000 1,000 2,000 83,000

50,000

50,000

2005 04 Dec 15 Dec 22 Dec 25 Dec 30 Dec 30 Dec 31 Dec

By Bank A/C By Purchase A/C By Purchase A/C By Shyam By Cash A/C By Rent A/C By Balance c/d

©

©

50,000 8,000 20,000 5,000 83,000

10,000 2,000 1,000 37,000 50,000

5. Prepare a double column cash book with the help of following information for December 2005 :

Rs.

01 Started business with cash 1,20,000

03 Cash paid into bank 50,000

05 Purchased goods from Sushmita 20,000

06 Sold goods to Dinker and received a cheque 20,000

10 Paid to Sushmita cash 20,000

14 Cheque received on December 06, 2005 deposited into bank

18 Sold goods to Rani 12,000

20 Cartage paid in cash 500

22 Received cash from Rani 12,000

27 Commission received 5,000

30 Drew cash for personal use 2,000

(Ans. Cash in hand Rs. 64,500 : Cash at bank Rs. 70,000)

11

Solution:

Dr. Double Column Cash book Cr.

Date Particulars L.F Amount Date Particulars L.F Amount

Cash ₹

Bank ₹

Cash ₹

Bank ₹

2005 01 Dec

03 Dec

06 Dec 14 Dec 22 Dec 27 Dec

To Balance b/d To Cash A/C To Dinker To Cash A/C To Rani To Commission A/C

©

©

1,20,000 20,000 12,000 5,000 1,57,000

50,000

20,000

70,000

2005 03 Dec 10 Dec 14Dec 20 Dec 30 Dec 31 Dec

By Bank A/C By Sushmita By Bank A/C By Cartage A/C By Drawings A/C By Balance c/d

©

©

50,000 20,000 20,000 500 2,000 64,500 1,57,000

70,000 70,000

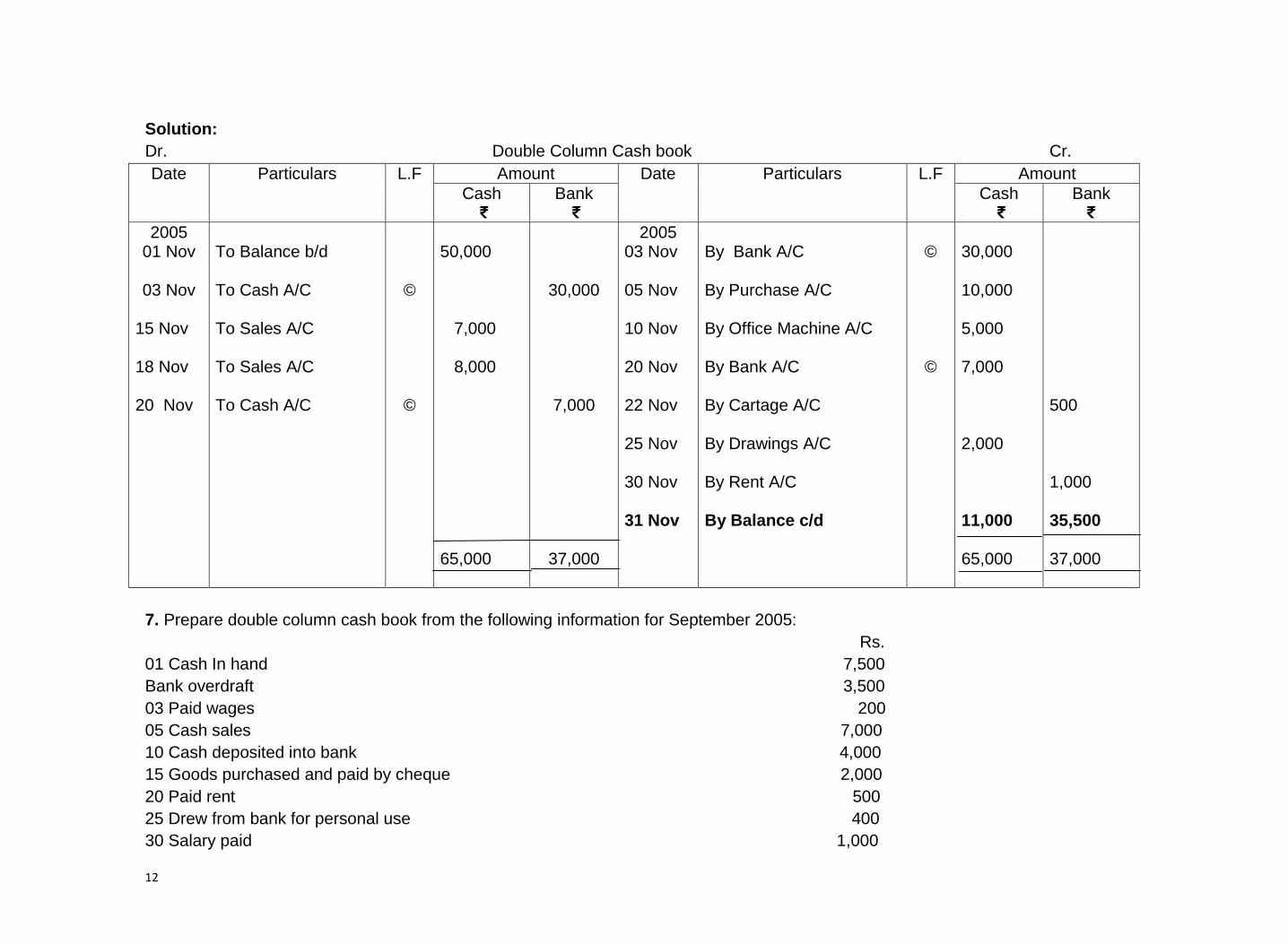

6. Enter the following transactions in double column cash book of M/s Ambica Traders for November 2005:

Rs.

01 Commenced business with cash 50,000

03 Opened bank account with ICICI 30,000

05 Purchased goods for cash 10,000

10 Purchased office machine for cash 5,000

15 Sales goods on credit from Rohan and received cheque 7,000

18 Cash sales 8,000

20 Rohan’s cheque deposited into bank

22 Paid cartage by cheque 500

25 Cash withdrawn for personal use 2,000

30 Paid rent by cheque 1,000

(Ans. Cash in hand Rs. 11,000, Cash at bank Rs. 35,500)

12

Solution:

Dr. Double Column Cash book Cr.

Date Particulars L.F Amount Date Particulars L.F Amount

Cash ₹

Bank ₹

Cash ₹

Bank ₹

2005 01 Nov

03 Nov

15 Nov 18 Nov 20 Nov

To Balance b/d To Cash A/C To Sales A/C To Sales A/C To Cash A/C

©

©

50,000 7,000 8,000 65,000

30,000

7,000

37,000

2005 03 Nov 05 Nov 10 Nov 20 Nov 22 Nov 25 Nov 30 Nov 31 Nov

By Bank A/C By Purchase A/C By Office Machine A/C By Bank A/C By Cartage A/C By Drawings A/C By Rent A/C By Balance c/d

©

©

30,000 10,000 5,000 7,000 2,000 11,000 65,000

500 1,000 35,500 37,000

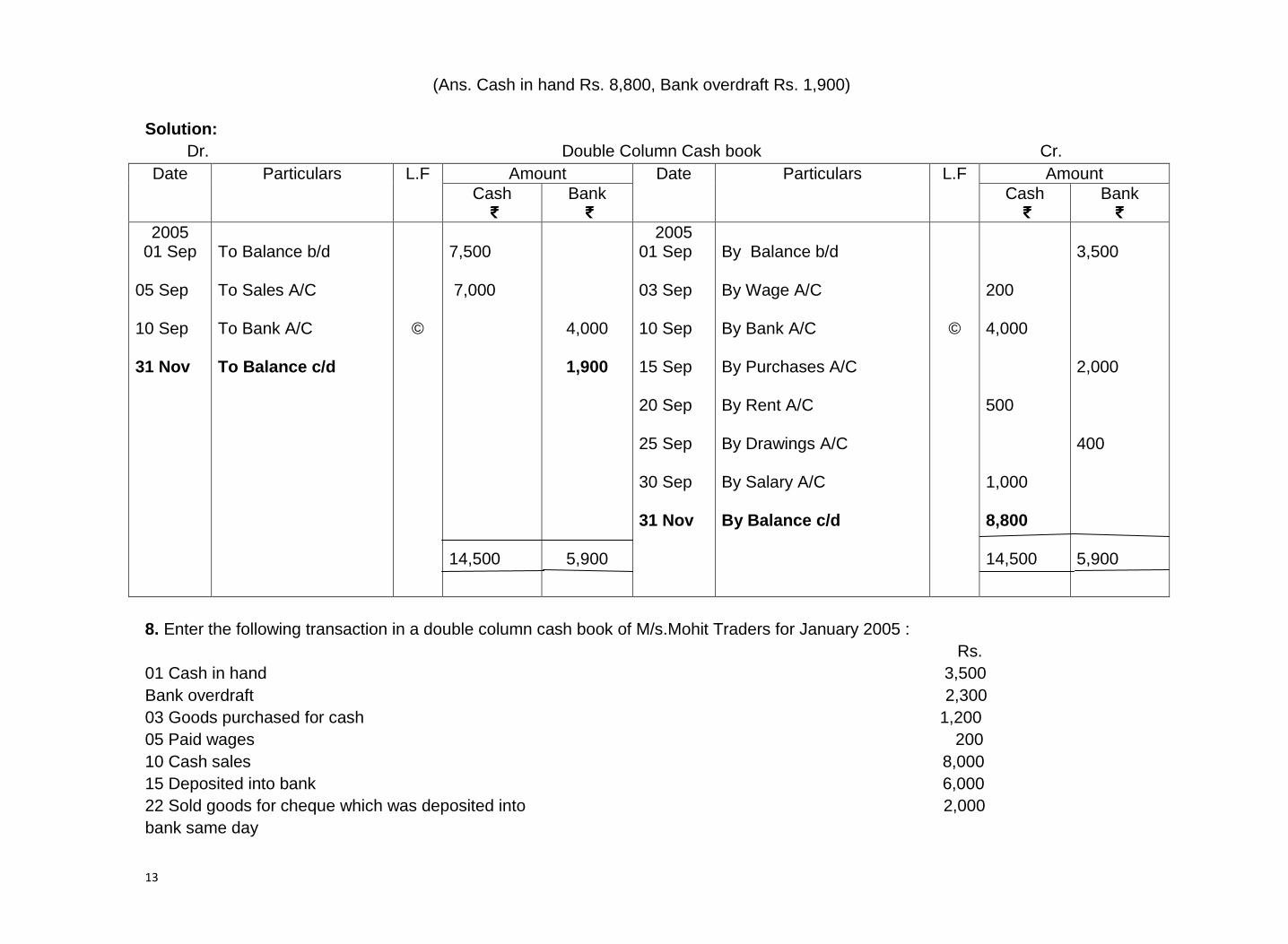

7. Prepare double column cash book from the following information for September 2005:

Rs.

01 Cash In hand 7,500

Bank overdraft 3,500

03 Paid wages 200

05 Cash sales 7,000

10 Cash deposited into bank 4,000

15 Goods purchased and paid by cheque 2,000

20 Paid rent 500

25 Drew from bank for personal use 400

30 Salary paid 1,000

13

(Ans. Cash in hand Rs. 8,800, Bank overdraft Rs. 1,900)

Solution:

Dr. Double Column Cash book Cr.

Date Particulars L.F Amount Date Particulars L.F Amount

Cash ₹

Bank ₹

Cash ₹

Bank ₹

2005 01 Sep

05 Sep 10 Sep 31 Nov

To Balance b/d To Sales A/C To Bank A/C To Balance c/d

©

7,500 7,000 14,500

4,000

1,900

5,900

2005 01 Sep 03 Sep 10 Sep 15 Sep 20 Sep 25 Sep 30 Sep 31 Nov

By Balance b/d By Wage A/C By Bank A/C By Purchases A/C By Rent A/C By Drawings A/C By Salary A/C By Balance c/d

©

200 4,000 500 1,000 8,800 14,500

3,500

2,000 400 5,900

8. Enter the following transaction in a double column cash book of M/s.Mohit Traders for January 2005 :

Rs.

01 Cash in hand 3,500

Bank overdraft 2,300

03 Goods purchased for cash 1,200

05 Paid wages 200

10 Cash sales 8,000

15 Deposited into bank 6,000

22 Sold goods for cheque which was deposited into 2,000

bank same day

14

25 Paid rent by cheque 1,200

28 Drew from bank for personal use 1,000

31 Bought goods by cheque 1,000

(Ans. Cash in hand Rs. 4,100 Cash at bank Rs. 2,500)

Solution:

Dr. Double Column Cash book Cr.

Date Particulars L.F Amount Date Particulars L.F Amount

Cash ₹

Bank ₹

Cash ₹

Bank ₹

2005 01 Jan

10 Jan 15 Jan 22 Jan

To Balance b/d To Sales A/C To Cash A/C To Sales A/C

©

3,500 8,000 11,500

6,000

2,000

8,000

2005 01 Jan 03 Jan 05 Jan 15 Jan 25 Jan 28 Jan 31 Jan 31 Jan

By Balance b/d By Purchases A/C By wages A/C By Bank A/C By Rent A/C By Drawings A/C By Purchases A/C By Balance c/d

©

1,200 200 6,000 4,100 11,500

2,300

1,200 1,000 1,000 2,500 8,000

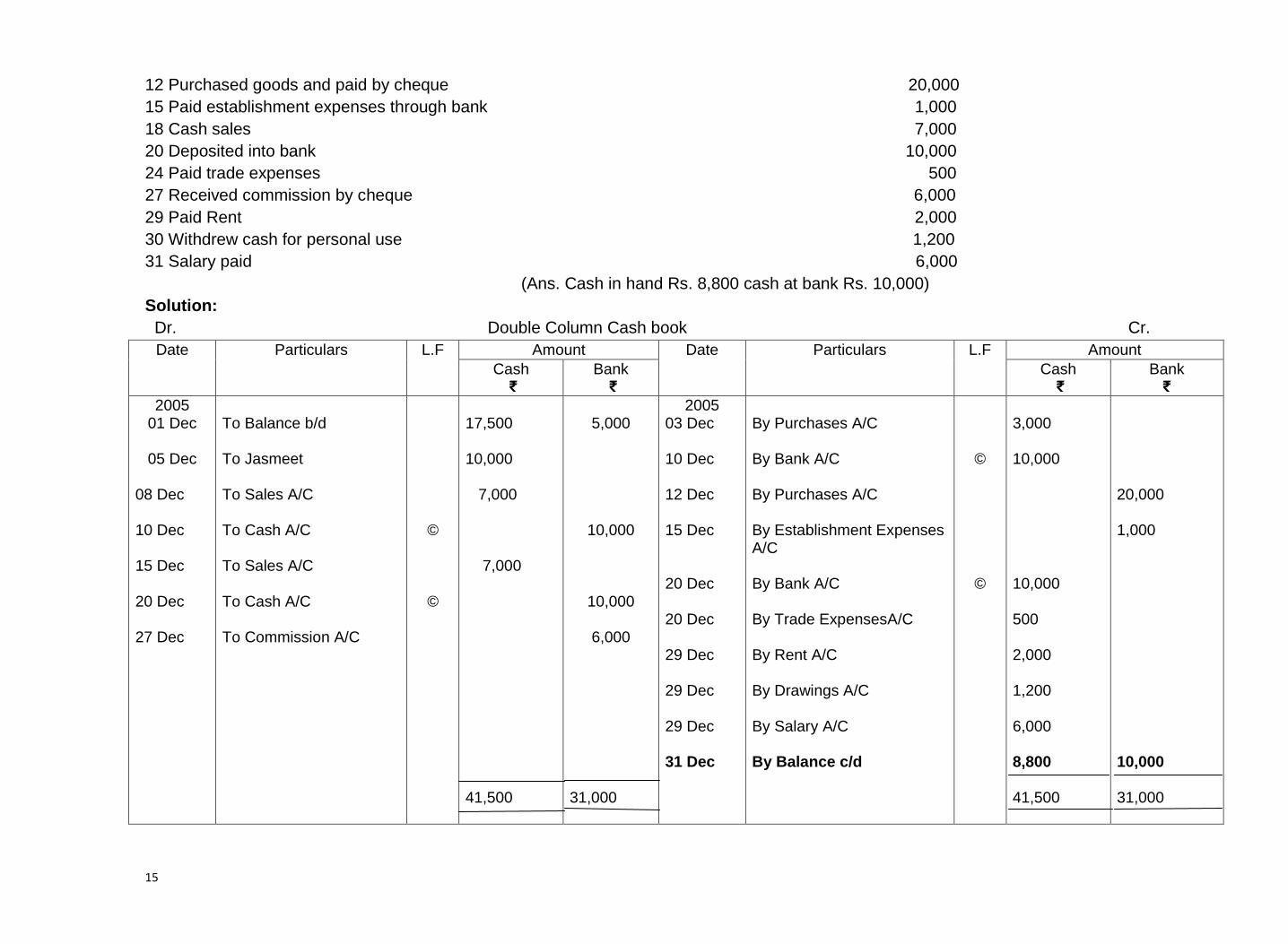

9. Prepare double column cash book from the following transactions for the year December 2005:

Rs.

01 Cash in hand 17,500

Cash at bank 5,000

03 Purchased goods for cash 3,000

05 Received cheque from Jasmeet 10,000

08 Sold goods for cash 7,000

10 Jasmeet’s cheque deposited into bank

15

12 Purchased goods and paid by cheque 20,000

15 Paid establishment expenses through bank 1,000

18 Cash sales 7,000

20 Deposited into bank 10,000

24 Paid trade expenses 500

27 Received commission by cheque 6,000

29 Paid Rent 2,000

30 Withdrew cash for personal use 1,200

31 Salary paid 6,000

(Ans. Cash in hand Rs. 8,800 cash at bank Rs. 10,000)

Solution:

Dr. Double Column Cash book Cr.

Date Particulars L.F Amount Date Particulars L.F Amount

Cash ₹

Bank ₹

Cash ₹

Bank ₹

2005 01 Dec

05 Dec

08 Dec 10 Dec 15 Dec 20 Dec 27 Dec

To Balance b/d To Jasmeet To Sales A/C To Cash A/C To Sales A/C To Cash A/C To Commission A/C

©

©

17,500 10,000 7,000 7,000 41,500

5,000

10,000

10,000

6,000

31,000

2005 03 Dec 10 Dec 12 Dec 15 Dec 20 Dec 20 Dec 29 Dec 29 Dec 29 Dec 31 Dec

By Purchases A/C By Bank A/C By Purchases A/C By Establishment Expenses A/C By Bank A/C By Trade ExpensesA/C By Rent A/C By Drawings A/C By Salary A/C By Balance c/d

©

©

3,000 10,000 10,000 500 2,000 1,200 6,000 8,800 41,500

20,000 1,000 10,000 31,000

16

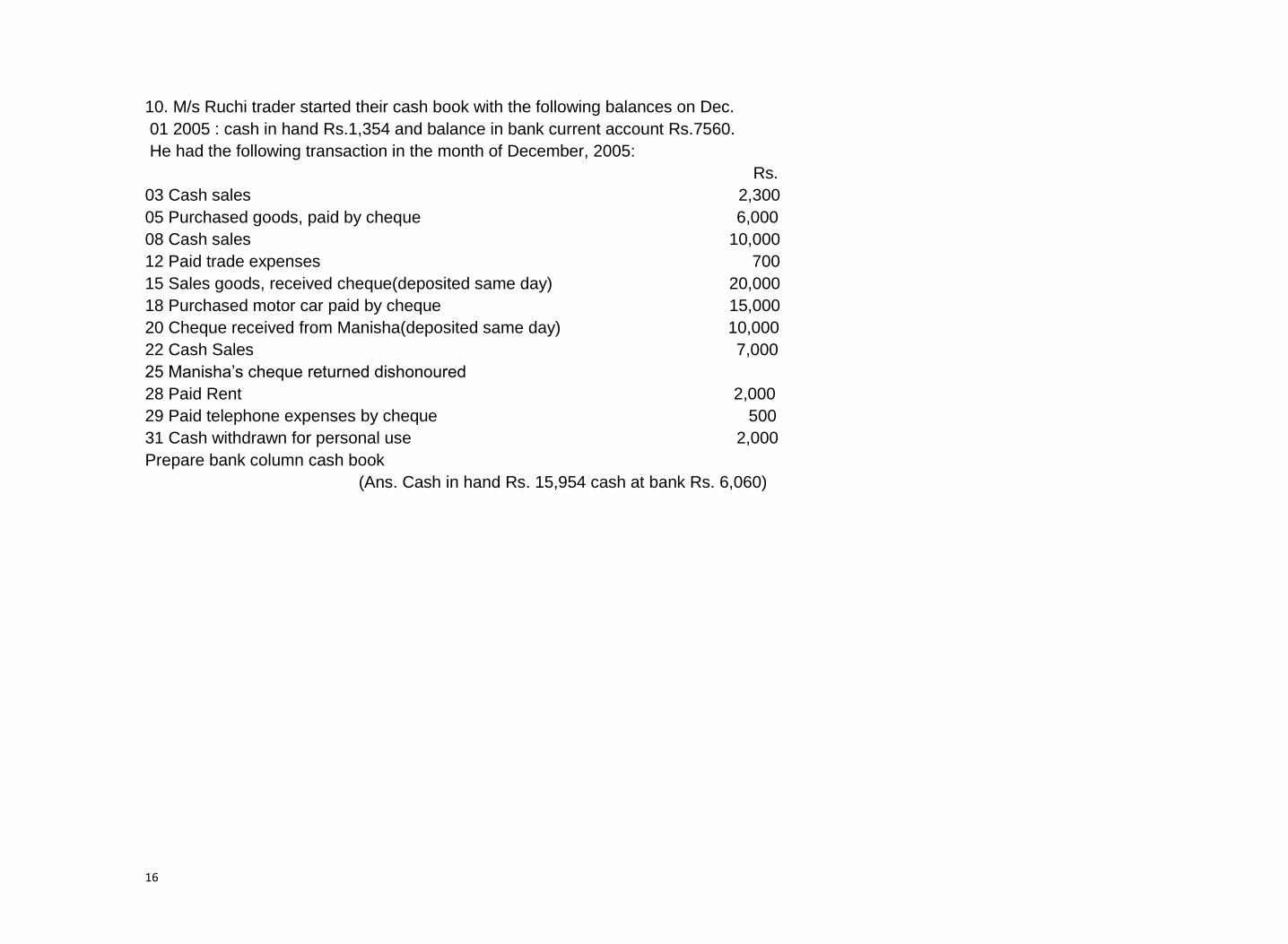

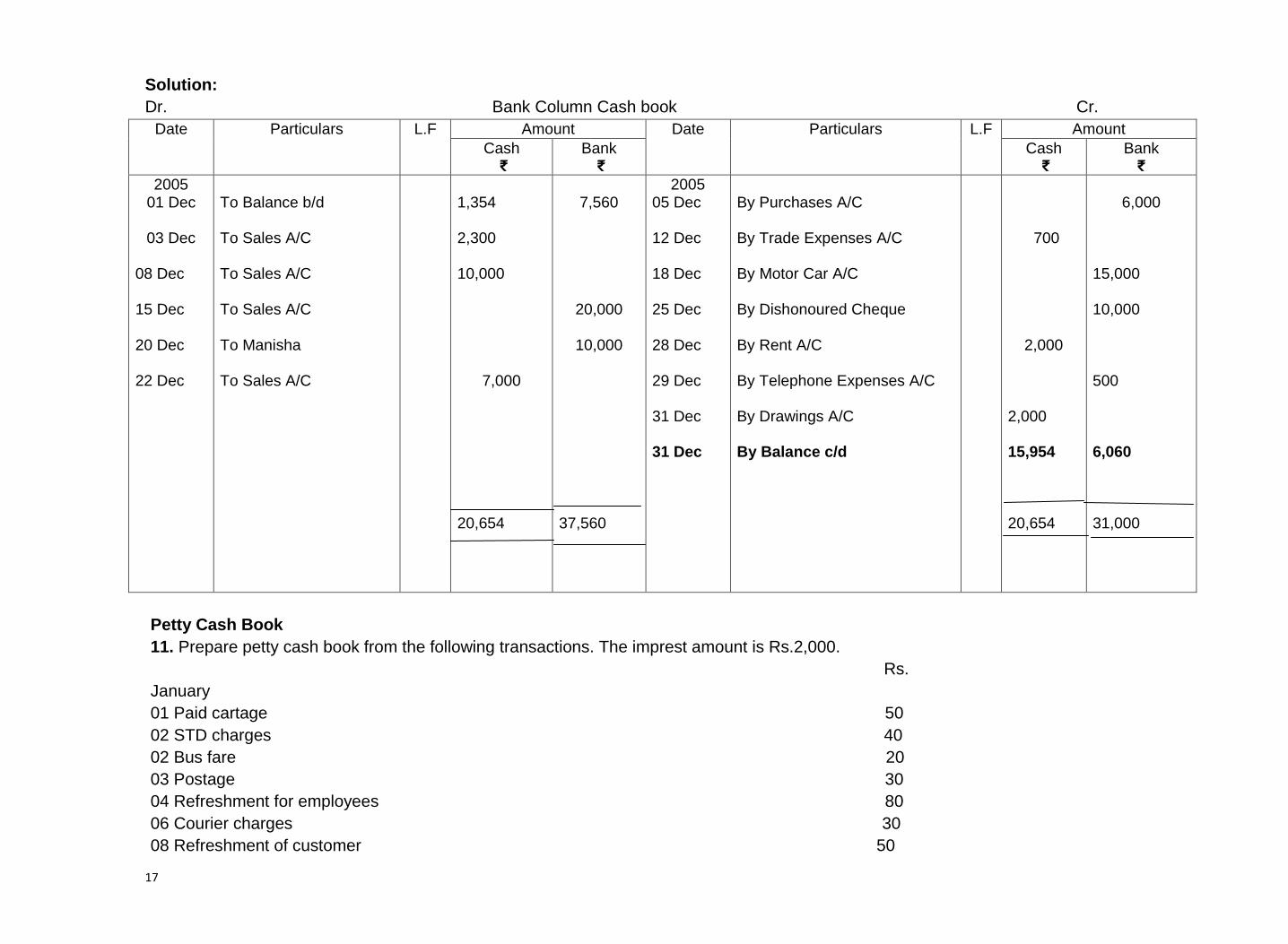

10. M/s Ruchi trader started their cash book with the following balances on Dec.

01 2005 : cash in hand Rs.1,354 and balance in bank current account Rs.7560.

He had the following transaction in the month of December, 2005:

Rs.

03 Cash sales 2,300

05 Purchased goods, paid by cheque 6,000

08 Cash sales 10,000

12 Paid trade expenses 700

15 Sales goods, received cheque(deposited same day) 20,000

18 Purchased motor car paid by cheque 15,000

20 Cheque received from Manisha(deposited same day) 10,000

22 Cash Sales 7,000

25 Manisha’s cheque returned dishonoured

28 Paid Rent 2,000

29 Paid telephone expenses by cheque 500

31 Cash withdrawn for personal use 2,000

Prepare bank column cash book

(Ans. Cash in hand Rs. 15,954 cash at bank Rs. 6,060)

17

Solution:

Dr. Bank Column Cash book Cr.

Date Particulars L.F Amount Date Particulars L.F Amount

Cash ₹

Bank ₹

Cash ₹

Bank ₹

2005 01 Dec

03 Dec

08 Dec 15 Dec 20 Dec 22 Dec

To Balance b/d To Sales A/C To Sales A/C To Sales A/C To Manisha To Sales A/C

1,354 2,300 10,000

7,000 20,654

7,560

20,000

10,000

37,560

2005 05 Dec 12 Dec 18 Dec 25 Dec 28 Dec 29 Dec 31 Dec 31 Dec

By Purchases A/C By Trade Expenses A/C By Motor Car A/C By Dishonoured Cheque By Rent A/C By Telephone Expenses A/C By Drawings A/C By Balance c/d

700

2,000 2,000 15,954 20,654

6,000

15,000 10,000 500 6,060 31,000

Petty Cash Book

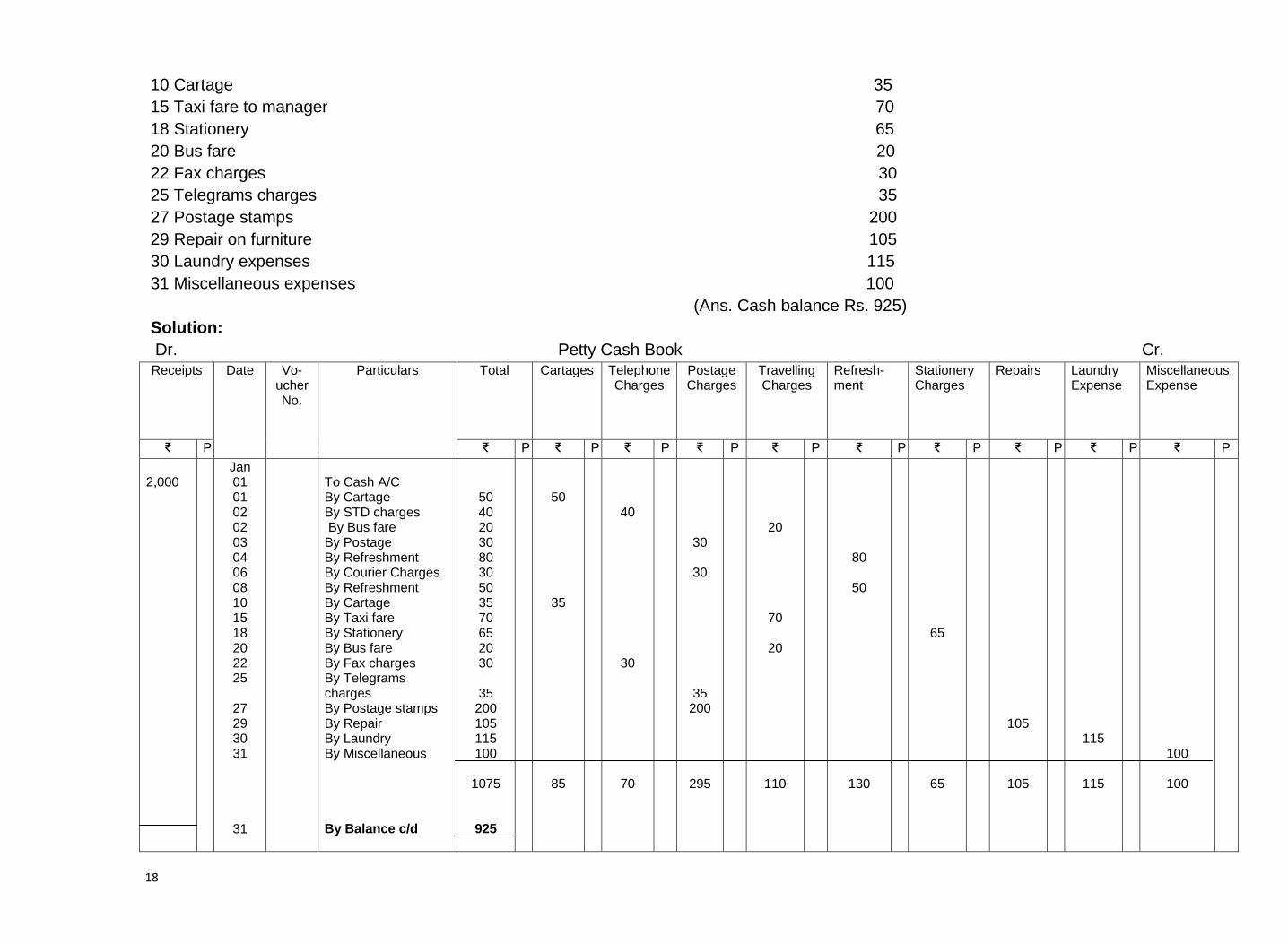

11. Prepare petty cash book from the following transactions. The imprest amount is Rs.2,000.

Rs.

January

01 Paid cartage 50

02 STD charges 40

02 Bus fare 20

03 Postage 30

04 Refreshment for employees 80

06 Courier charges 30

08 Refreshment of customer 50

18

10 Cartage 35

15 Taxi fare to manager 70

18 Stationery 65

20 Bus fare 20

22 Fax charges 30

25 Telegrams charges 35

27 Postage stamps 200

29 Repair on furniture 105

30 Laundry expenses 115

31 Miscellaneous expenses 100

(Ans. Cash balance Rs. 925)

Solution:

Dr. Petty Cash Book Cr. Receipts Date Vo-

ucher No.

Particulars Total Cartages Telephone Charges

Postage Charges

Travelling Charges

Refresh-ment

Stationery Charges

Repairs Laundry Expense

Miscellaneous Expense

₹ P ₹ P ₹ P ₹ P ₹ P ₹ P ₹ P ₹ P ₹ P ₹ P ₹ P

2,000

Jan 01 01 02 02 03 04 06 08 10 15 18 20 22 25

27 29 30 31

31

To Cash A/C By Cartage By STD charges By Bus fare By Postage By Refreshment By Courier Charges By Refreshment By Cartage By Taxi fare By Stationery By Bus fare By Fax charges By Telegrams charges By Postage stamps By Repair By Laundry By Miscellaneous By Balance c/d

50 40 20 30 80 30 50 35 70 65 20 30

35 200 105 115 100

1075

925

50

35

85

40

30

70

30

30

35 200

295

20

70

20

110

80

50

130

65

65

105

105

115

115

100

100

19

2,000 925 1075

Feb 01 01

To Balance b/d To Cash

2,000

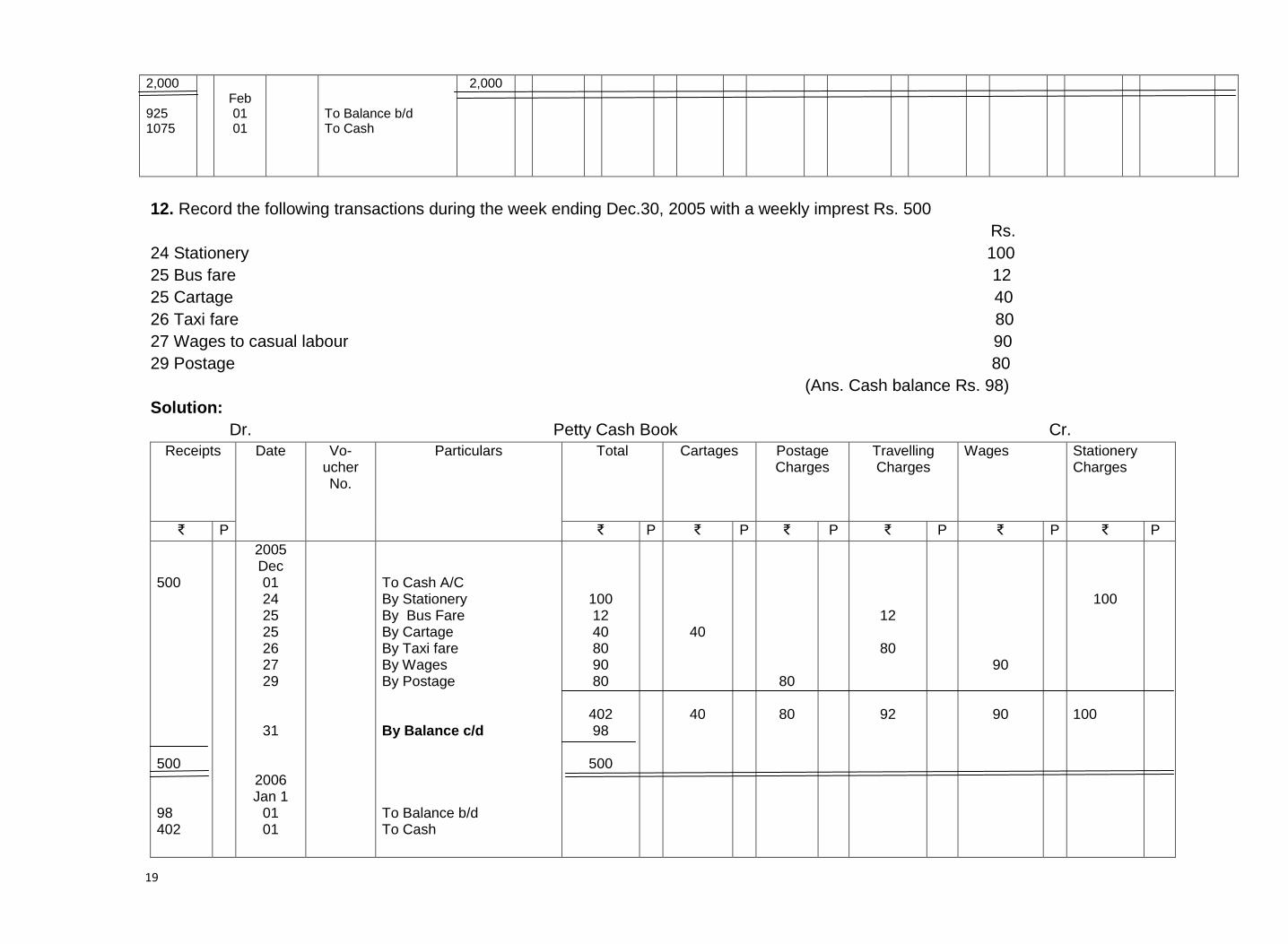

12. Record the following transactions during the week ending Dec.30, 2005 with a weekly imprest Rs. 500

Rs.

24 Stationery 100

25 Bus fare 12

25 Cartage 40

26 Taxi fare 80

27 Wages to casual labour 90

29 Postage 80

(Ans. Cash balance Rs. 98)

Solution:

Dr. Petty Cash Book Cr.

Receipts Date Vo-ucher No.

Particulars Total Cartages Postage Charges

Travelling Charges

Wages Stationery Charges

₹ P ₹ P ₹ P ₹ P ₹ P ₹ P ₹ P

500 500 98 402

2005 Dec 01 24 25 25 26 27 29

31

2006 Jan 1

01 01

To Cash A/C By Stationery By Bus Fare By Cartage By Taxi fare By Wages By Postage By Balance c/d To Balance b/d To Cash

100 12 40 80 90 80

402 98

500

40

40

80

80

12

80

92

90

90

100 100

20

Other Subsidiary Books

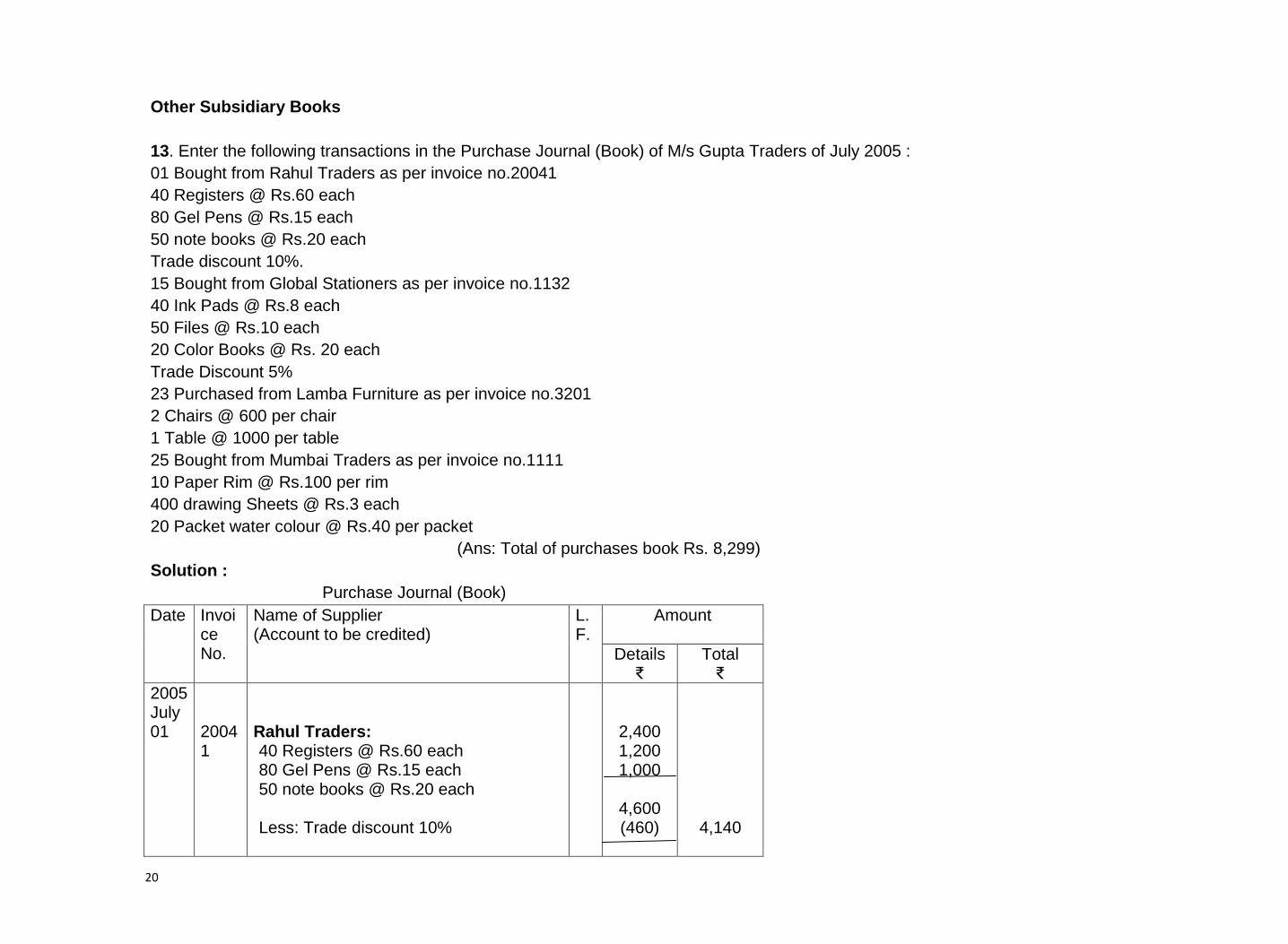

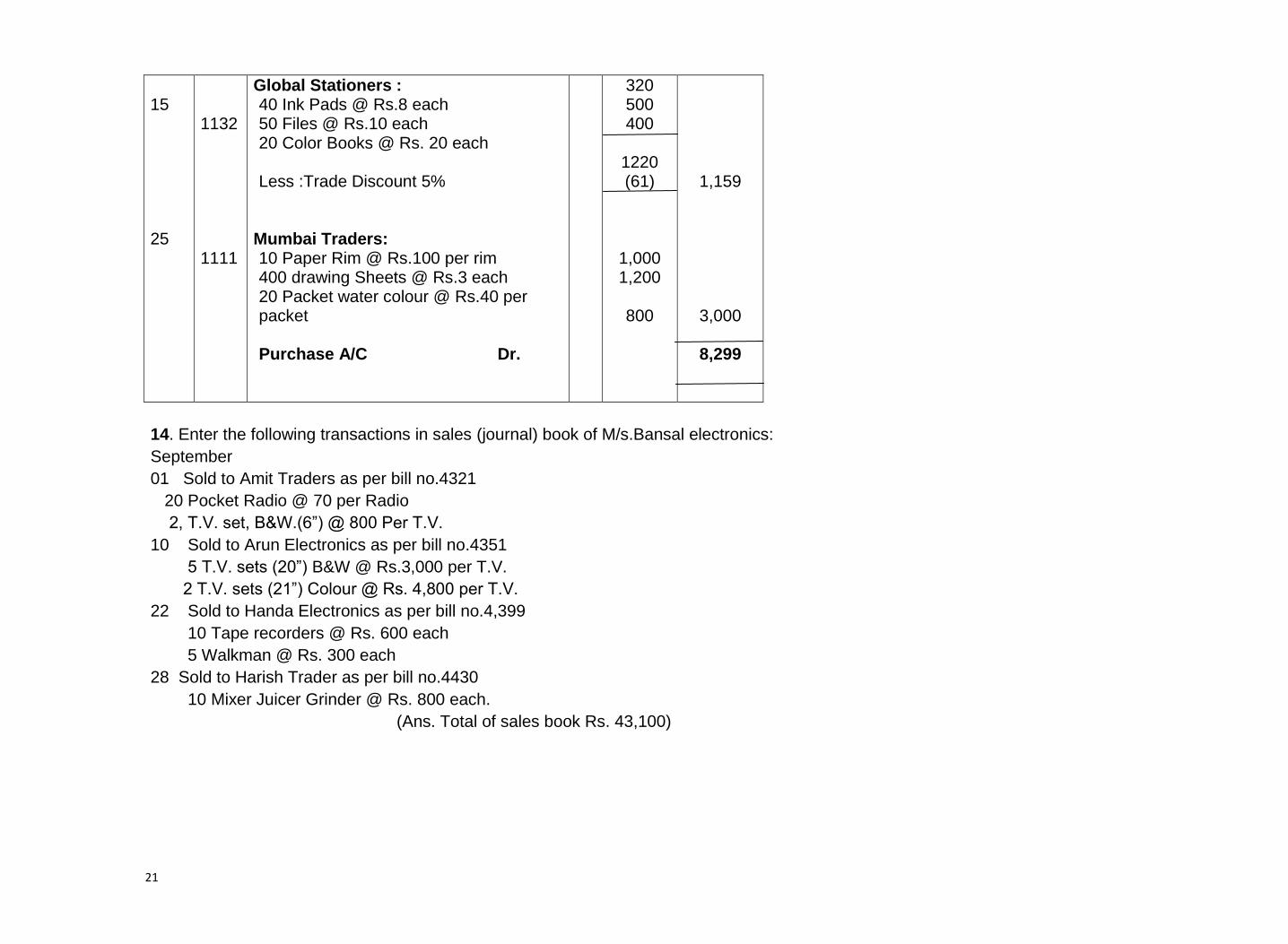

13. Enter the following transactions in the Purchase Journal (Book) of M/s Gupta Traders of July 2005 :

01 Bought from Rahul Traders as per invoice no.20041

40 Registers @ Rs.60 each

80 Gel Pens @ Rs.15 each

50 note books @ Rs.20 each

Trade discount 10%.

15 Bought from Global Stationers as per invoice no.1132

40 Ink Pads @ Rs.8 each

50 Files @ Rs.10 each

20 Color Books @ Rs. 20 each

Trade Discount 5%

23 Purchased from Lamba Furniture as per invoice no.3201

2 Chairs @ 600 per chair

1 Table @ 1000 per table

25 Bought from Mumbai Traders as per invoice no.1111

10 Paper Rim @ Rs.100 per rim

400 drawing Sheets @ Rs.3 each

20 Packet water colour @ Rs.40 per packet

(Ans: Total of purchases book Rs. 8,299)

Solution :

Purchase Journal (Book)

Date Invoice No.

Name of Supplier (Account to be credited)

L.F.

Amount

Details ₹

Total ₹

2005 July 01

20041

Rahul Traders: 40 Registers @ Rs.60 each 80 Gel Pens @ Rs.15 each 50 note books @ Rs.20 each

Less: Trade discount 10%

2,400 1,200 1,000

4,600 (460)

4,140

21

15 25

1132 1111

Global Stationers : 40 Ink Pads @ Rs.8 each 50 Files @ Rs.10 each 20 Color Books @ Rs. 20 each Less :Trade Discount 5%

Mumbai Traders: 10 Paper Rim @ Rs.100 per rim 400 drawing Sheets @ Rs.3 each 20 Packet water colour @ Rs.40 per packet Purchase A/C Dr.

320 500 400

1220 (61)

1,000 1,200

800

1,159

3,000

8,299

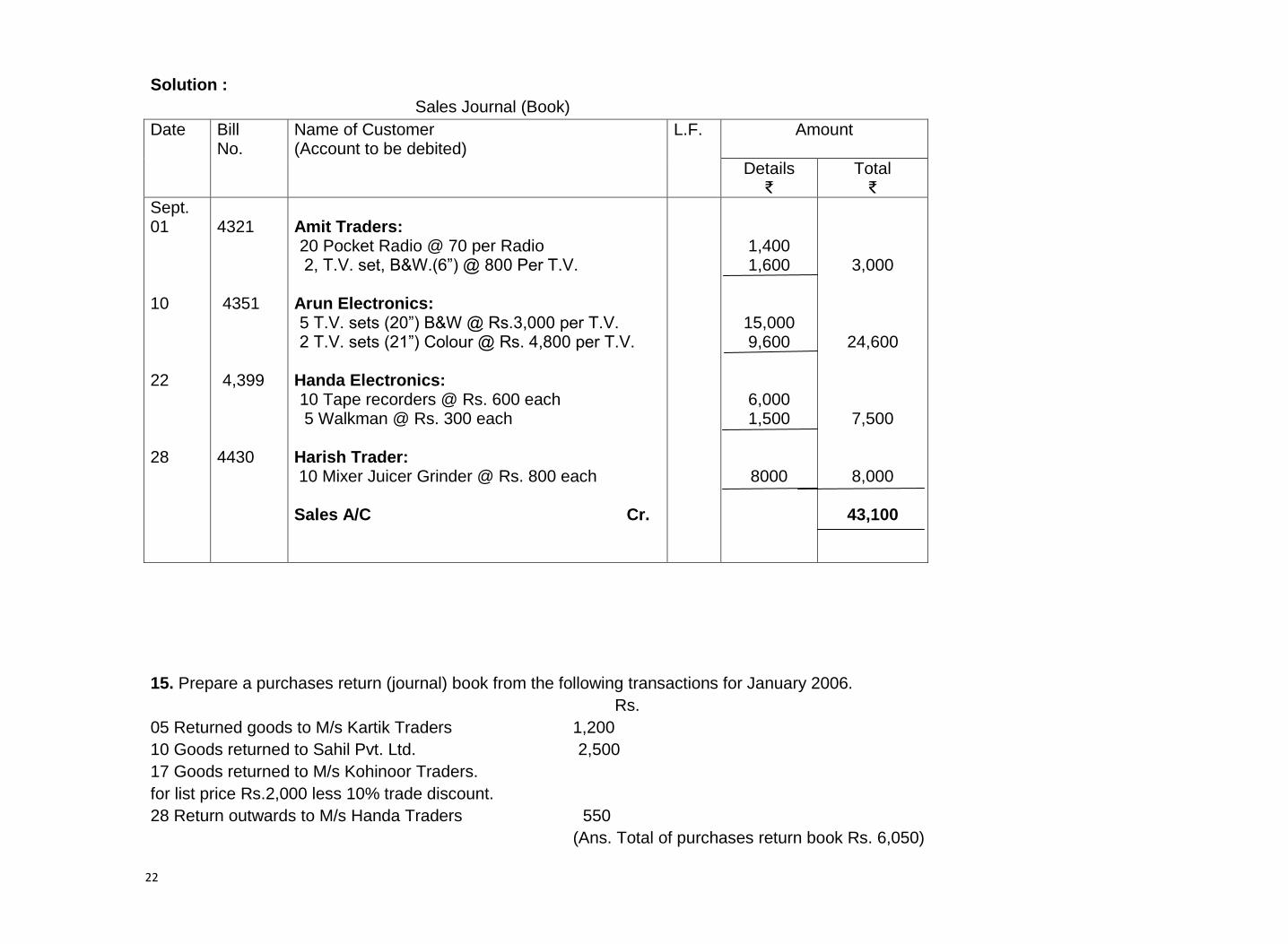

14. Enter the following transactions in sales (journal) book of M/s.Bansal electronics:

September

01 Sold to Amit Traders as per bill no.4321

20 Pocket Radio @ 70 per Radio

2, T.V. set, B&W.(6”) @ 800 Per T.V.

10 Sold to Arun Electronics as per bill no.4351

5 T.V. sets (20”) B&W @ Rs.3,000 per T.V.

2 T.V. sets (21”) Colour @ Rs. 4,800 per T.V.

22 Sold to Handa Electronics as per bill no.4,399

10 Tape recorders @ Rs. 600 each

5 Walkman @ Rs. 300 each

28 Sold to Harish Trader as per bill no.4430

10 Mixer Juicer Grinder @ Rs. 800 each.

(Ans. Total of sales book Rs. 43,100)

22

Solution :

Sales Journal (Book)

Date Bill No.

Name of Customer (Account to be debited)

L.F. Amount

Details ₹

Total ₹

Sept. 01 10 22 28

4321 4351 4,399

4430

Amit Traders: 20 Pocket Radio @ 70 per Radio 2, T.V. set, B&W.(6”) @ 800 Per T.V.

Arun Electronics: 5 T.V. sets (20”) B&W @ Rs.3,000 per T.V. 2 T.V. sets (21”) Colour @ Rs. 4,800 per T.V.

Handa Electronics: 10 Tape recorders @ Rs. 600 each 5 Walkman @ Rs. 300 each

Harish Trader: 10 Mixer Juicer Grinder @ Rs. 800 each Sales A/C Cr.

1,400 1,600

15,000 9,600

6,000 1,500

8000

3,000

24,600

7,500

8,000

43,100

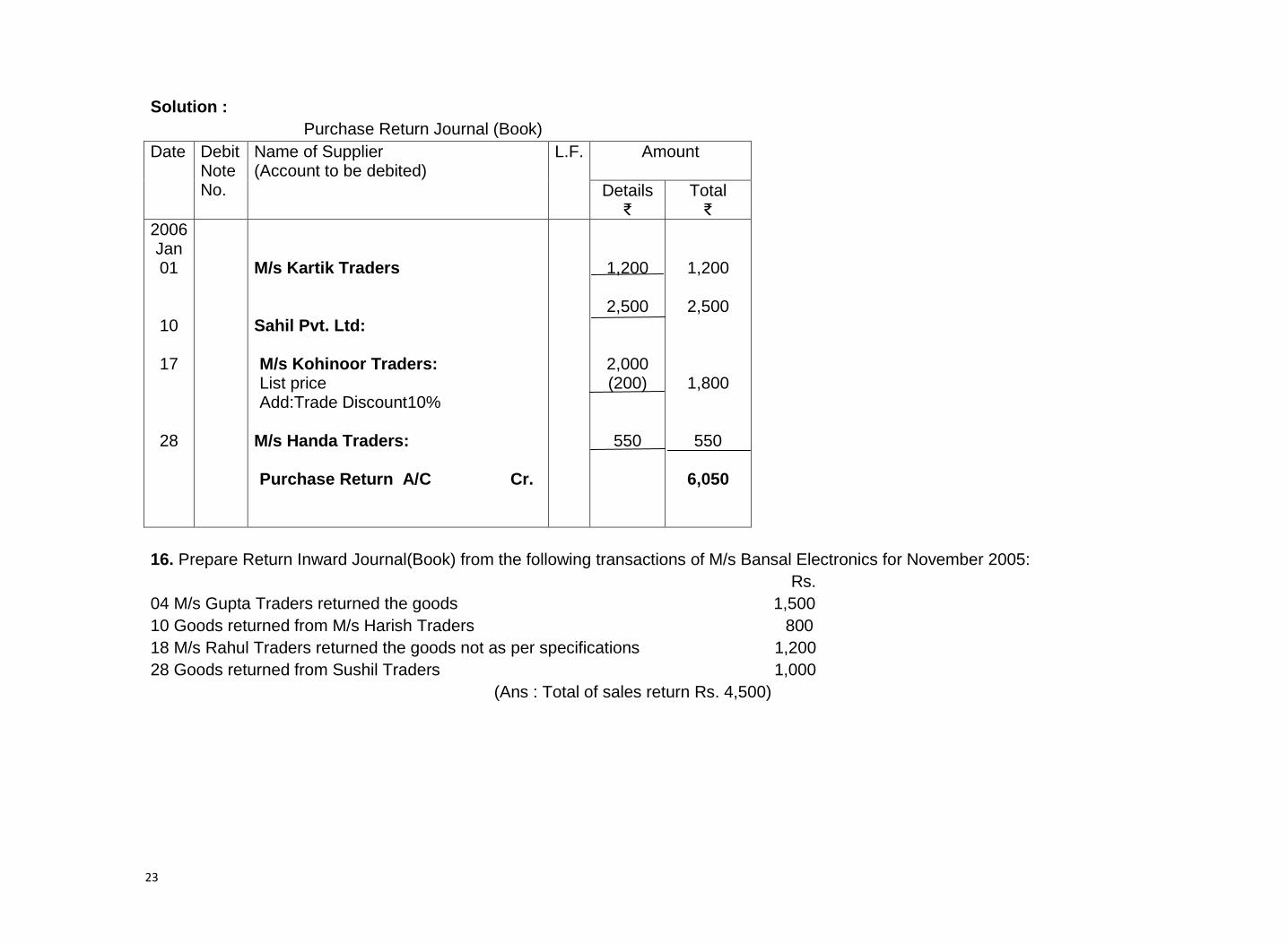

15. Prepare a purchases return (journal) book from the following transactions for January 2006.

Rs.

05 Returned goods to M/s Kartik Traders 1,200

10 Goods returned to Sahil Pvt. Ltd. 2,500

17 Goods returned to M/s Kohinoor Traders.

for list price Rs.2,000 less 10% trade discount.

28 Return outwards to M/s Handa Traders 550

(Ans. Total of purchases return book Rs. 6,050)

23

Solution :

Purchase Return Journal (Book)

Date Debit Note No.

Name of Supplier (Account to be debited)

L.F. Amount

Details ₹

Total ₹

2006 Jan 01

10

17

28

M/s Kartik Traders Sahil Pvt. Ltd: M/s Kohinoor Traders: List price Add:Trade Discount10%

M/s Handa Traders: Purchase Return A/C Cr.

1,200

2,500

2,000 (200)

550

1,200

2,500

1,800

550

6,050

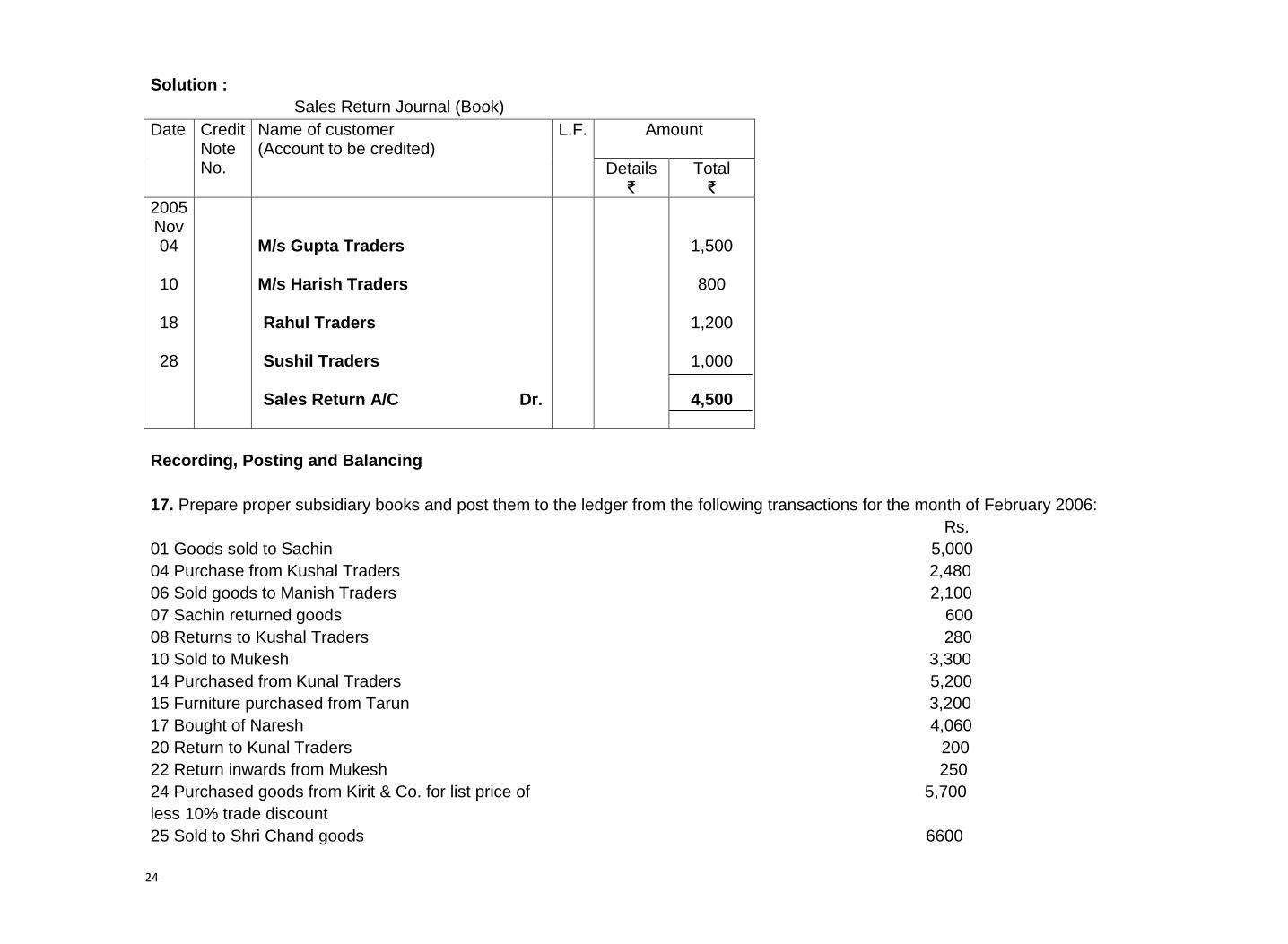

16. Prepare Return Inward Journal(Book) from the following transactions of M/s Bansal Electronics for November 2005:

Rs.

04 M/s Gupta Traders returned the goods 1,500

10 Goods returned from M/s Harish Traders 800

18 M/s Rahul Traders returned the goods not as per specifications 1,200

28 Goods returned from Sushil Traders 1,000

(Ans : Total of sales return Rs. 4,500)

24

Solution :

Sales Return Journal (Book)

Date Credit Note No.

Name of customer (Account to be credited)

L.F. Amount

Details ₹

Total ₹

2005 Nov 04

10

18

28

M/s Gupta Traders M/s Harish Traders Rahul Traders Sushil Traders Sales Return A/C Dr.

1,500

800

1,200

1,000

4,500

Recording, Posting and Balancing

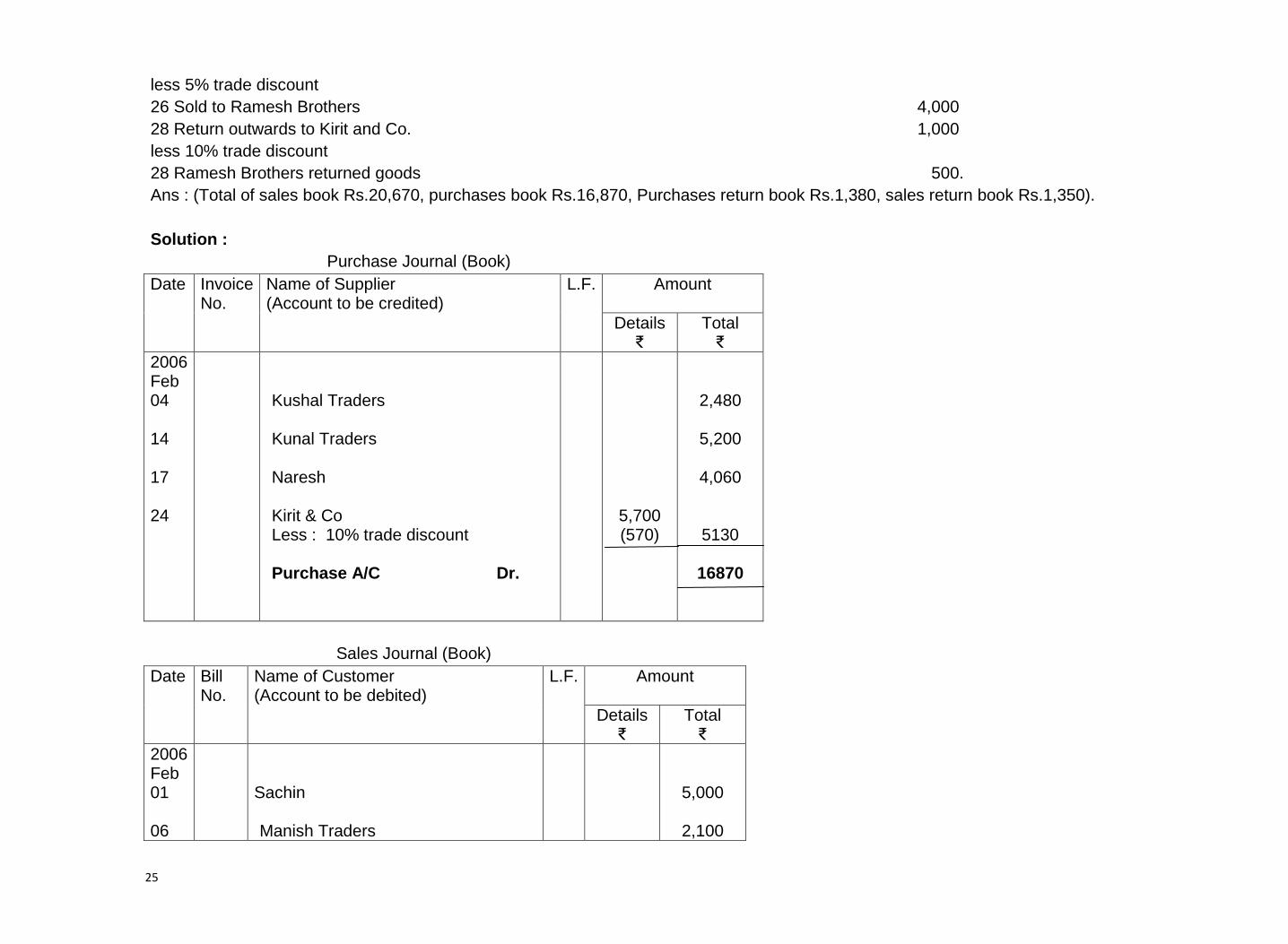

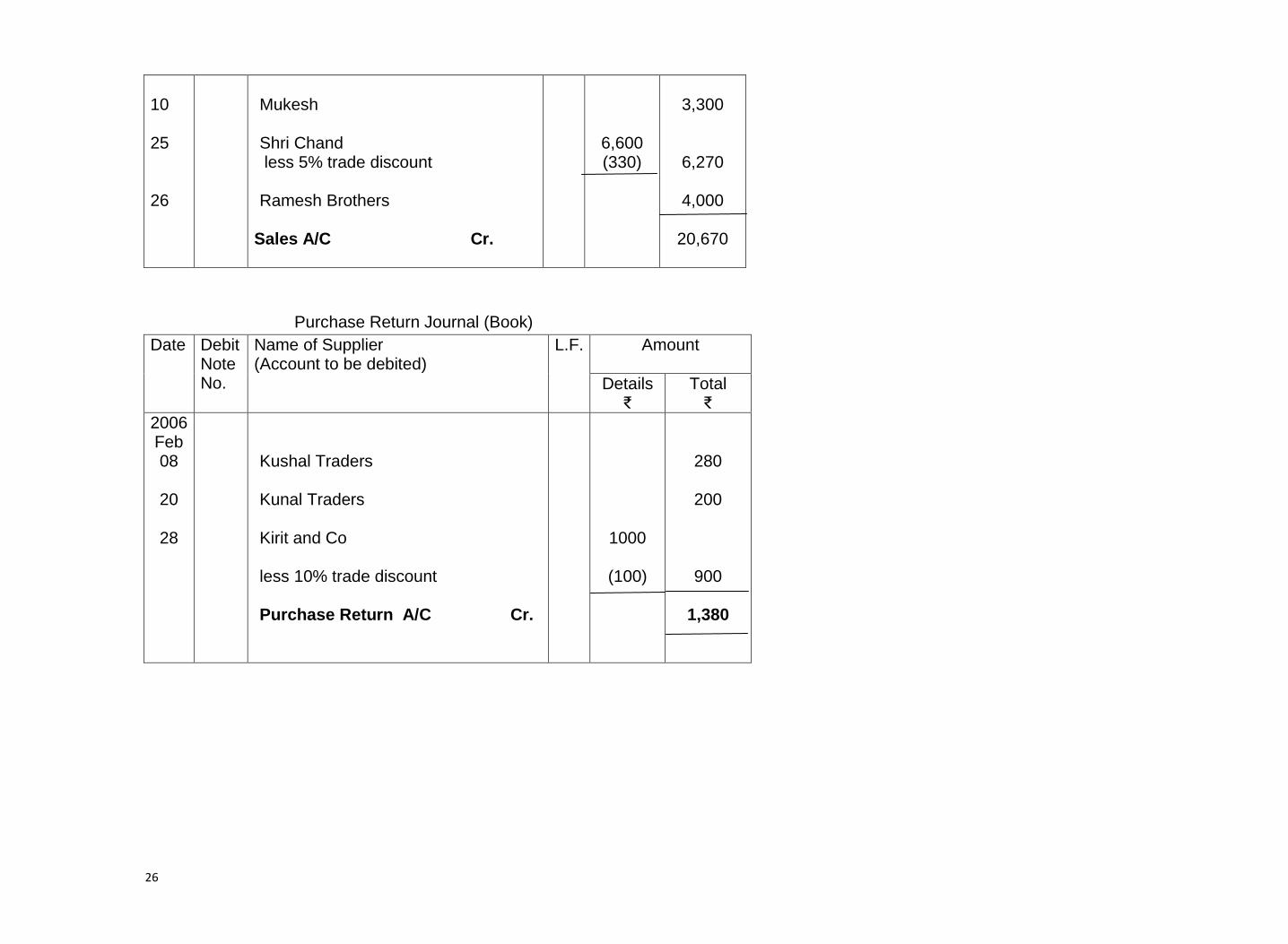

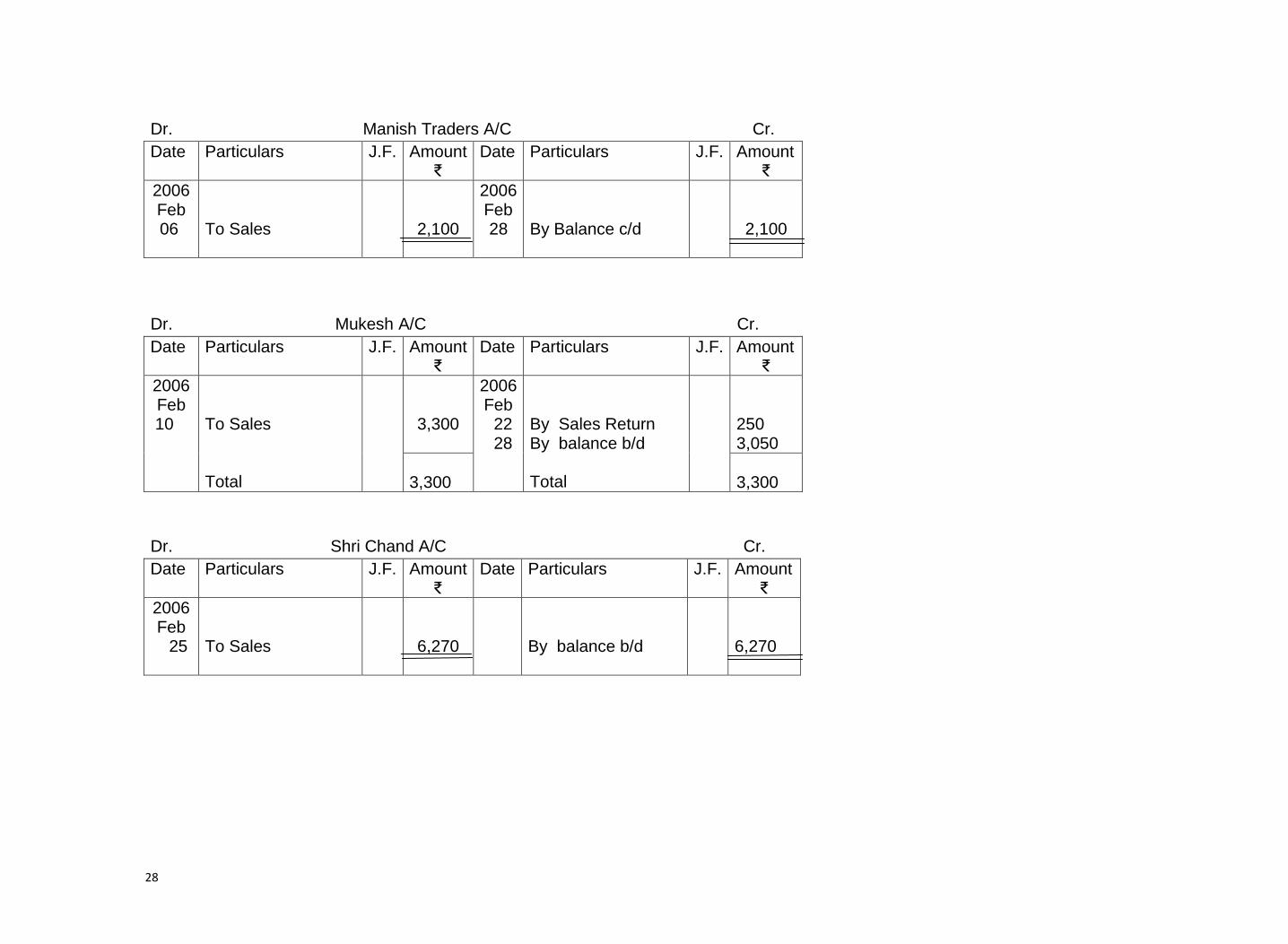

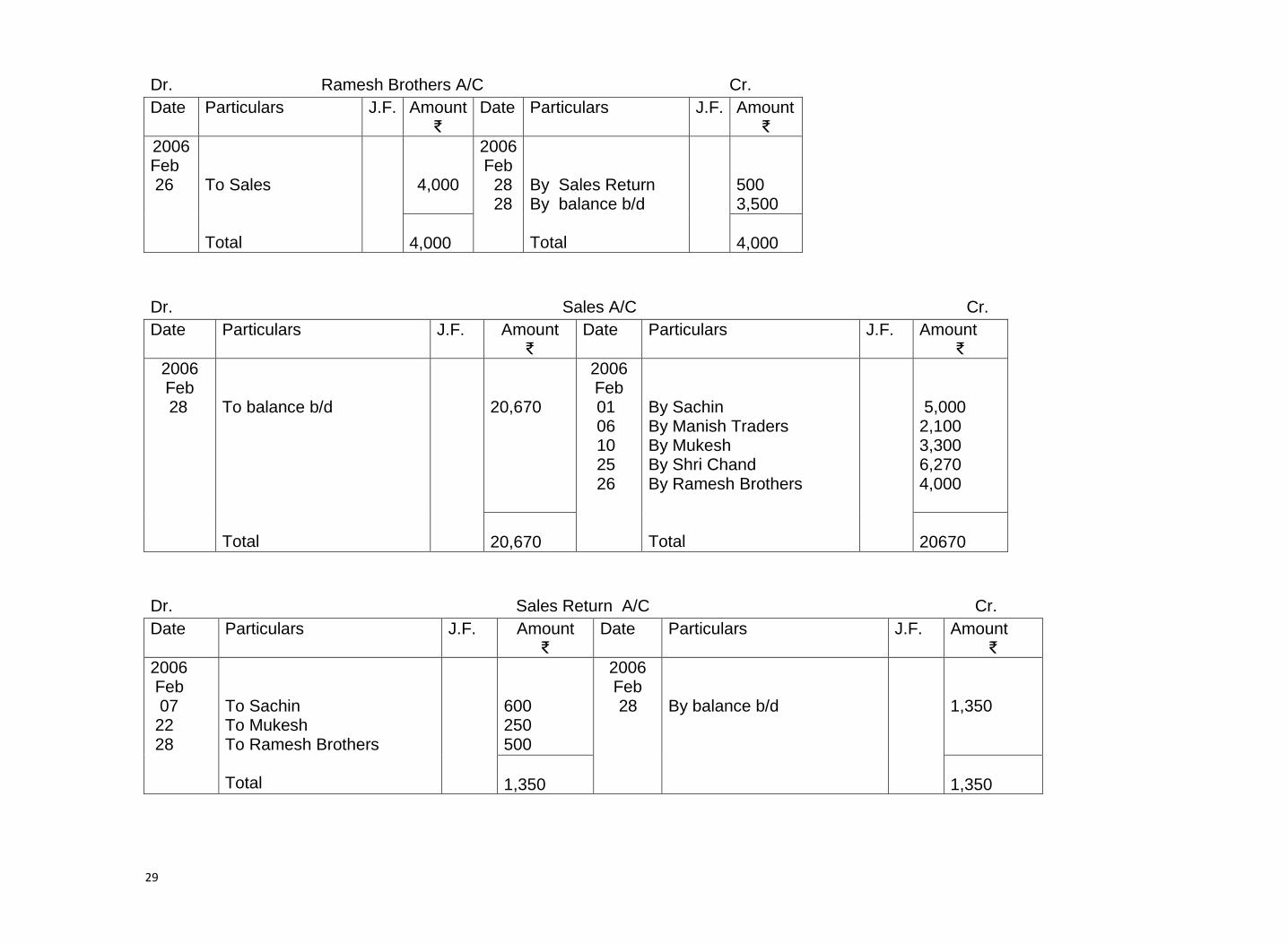

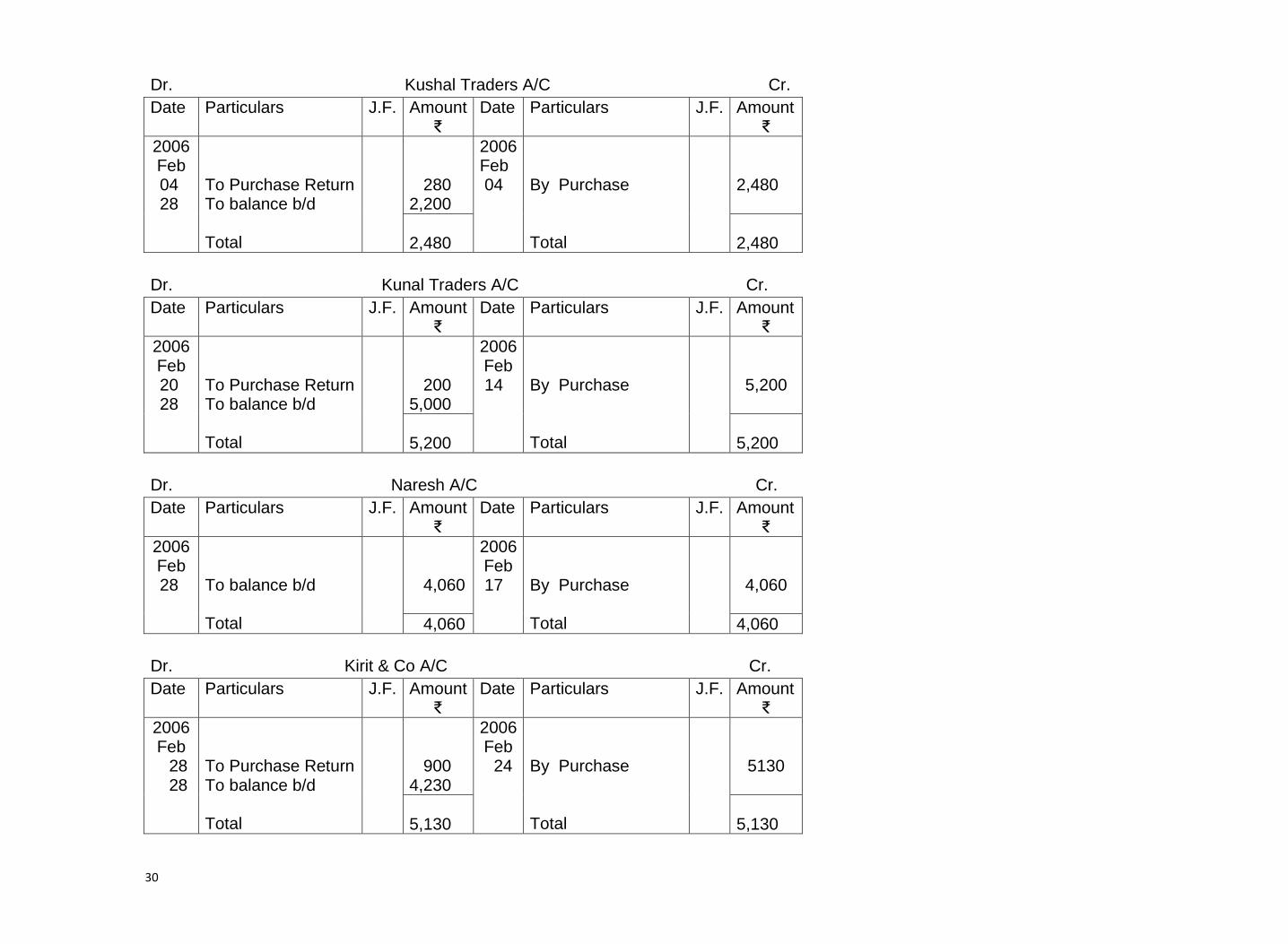

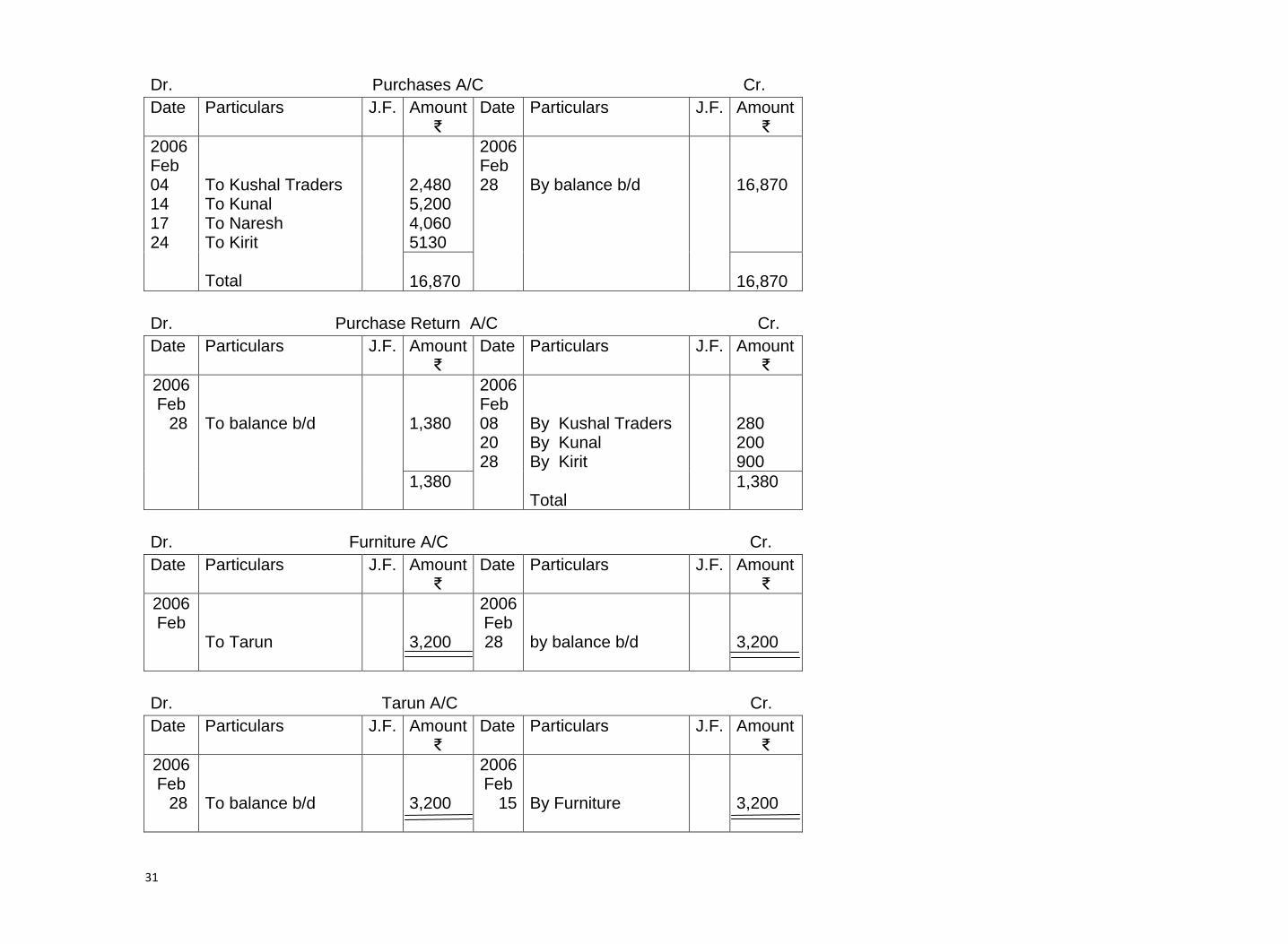

17. Prepare proper subsidiary books and post them to the ledger from the following transactions for the month of February 2006:

Rs.

01 Goods sold to Sachin 5,000

04 Purchase from Kushal Traders 2,480

06 Sold goods to Manish Traders 2,100

07 Sachin returned goods 600

08 Returns to Kushal Traders 280

10 Sold to Mukesh 3,300

14 Purchased from Kunal Traders 5,200

15 Furniture purchased from Tarun 3,200

17 Bought of Naresh 4,060

20 Return to Kunal Traders 200

22 Return inwards from Mukesh 250

24 Purchased goods from Kirit & Co. for list price of 5,700

less 10% trade discount

25 Sold to Shri Chand goods 6600

25

less 5% trade discount

26 Sold to Ramesh Brothers 4,000

28 Return outwards to Kirit and Co. 1,000

less 10% trade discount

28 Ramesh Brothers returned goods 500.

Ans : (Total of sales book Rs.20,670, purchases book Rs.16,870, Purchases return book Rs.1,380, sales return book Rs.1,350).

Solution :

Purchase Journal (Book)

Date Invoice No.

Name of Supplier (Account to be credited)

L.F. Amount

Details ₹

Total ₹

2006 Feb 04 14 17 24

Kushal Traders Kunal Traders Naresh Kirit & Co Less : 10% trade discount Purchase A/C Dr.

5,700 (570)

2,480

5,200

4,060

5130

16870

Sales Journal (Book)

Date Bill No.

Name of Customer (Account to be debited)

L.F. Amount

Details ₹

Total ₹

2006 Feb 01 06

Sachin Manish Traders

5,000

2,100

26

10 25 26

Mukesh Shri Chand less 5% trade discount Ramesh Brothers

Sales A/C Cr.

6,600 (330)

3,300

6,270

4,000

20,670

Purchase Return Journal (Book)

Date Debit Note No.

Name of Supplier (Account to be debited)

L.F. Amount

Details ₹

Total ₹

2006 Feb 08

20

28

Kushal Traders Kunal Traders Kirit and Co less 10% trade discount

Purchase Return A/C Cr.

1000

(100)

280

200

900

1,380

27

Sales Return Journal (Book)

Date Credit Note No.

Name of customer (Account to be credited)

L.F. Amount

Details ₹

Total ₹

2006 Feb 07

22

28

Sachin

Mukesh Ramesh Brothers

Sales Return A/C Dr.

600

250

500

1,350

Journal Proper

Date Particulars L.F Amount

Debit ₹

Credit ₹

2006 Feb 15

Furniture A/C To Tarun (Being furniture purchased from Tarun )

3,200

3,200

Dr. Sachin A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 Feb

01

To Sales Total

5,000

2006 Feb 07

By Sales Return By balance b/d Total

6,00 4,400

5,000

5,000

28

Dr. Manish Traders A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 Feb

06

To Sales

2,100

2006 Feb 28

By Balance c/d

2,100

Dr. Mukesh A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 Feb

10

To Sales Total

3,300

2006 Feb 22 28

By Sales Return By balance b/d Total

250 3,050

3,300

3,300

Dr. Shri Chand A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 Feb

25

To Sales

6,270

By balance b/d

6,270

29

Dr. Ramesh Brothers A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 Feb 26

To Sales Total

4,000

2006 Feb 28 28

By Sales Return By balance b/d Total

500 3,500

4,000

4,000

Dr. Sales A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 Feb

28

To balance b/d Total

20,670

2006 Feb

01 06 10 25 26

By Sachin By Manish Traders By Mukesh By Shri Chand By Ramesh Brothers Total

5,000 2,100 3,300 6,270 4,000

20,670

20670

Dr. Sales Return A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 Feb 07 22 28

To Sachin To Mukesh To Ramesh Brothers Total

600 250 500

2006 Feb

28

By balance b/d

1,350

1,350

1,350

30

Dr. Kushal Traders A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 Feb

04 28

To Purchase Return To balance b/d Total

280 2,200

2006 Feb 04

By Purchase Total

2,480

2,480

2,480

Dr. Kunal Traders A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 Feb

20 28

To Purchase Return To balance b/d Total

200 5,000

2006 Feb 14

By Purchase Total

5,200

5,200

5,200

Dr. Naresh A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 Feb

28

To balance b/d Total

4,060

2006 Feb 17

By Purchase Total

4,060

4,060 4,060

Dr. Kirit & Co A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 Feb

28 28

To Purchase Return To balance b/d Total

900 4,230

2006 Feb 24

By Purchase Total

5130

5,130

5,130

31

Dr. Purchases A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 Feb 04 14 17 24

To Kushal Traders To Kunal To Naresh To Kirit Total

2,480 5,200 4,060 5130

2006 Feb 28

By balance b/d

16,870

16,870

16,870

Dr. Purchase Return A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 Feb

28

To balance b/d

1,380

2006 Feb 08 20 28

By Kushal Traders By Kunal By Kirit Total

280 200 900

1,380 1,380

Dr. Furniture A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 Feb

To Tarun

3,200

2006 Feb 28

by balance b/d

3,200

Dr. Tarun A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 Feb

28

To balance b/d

3,200

2006 Feb 15

By Furniture

3,200

32

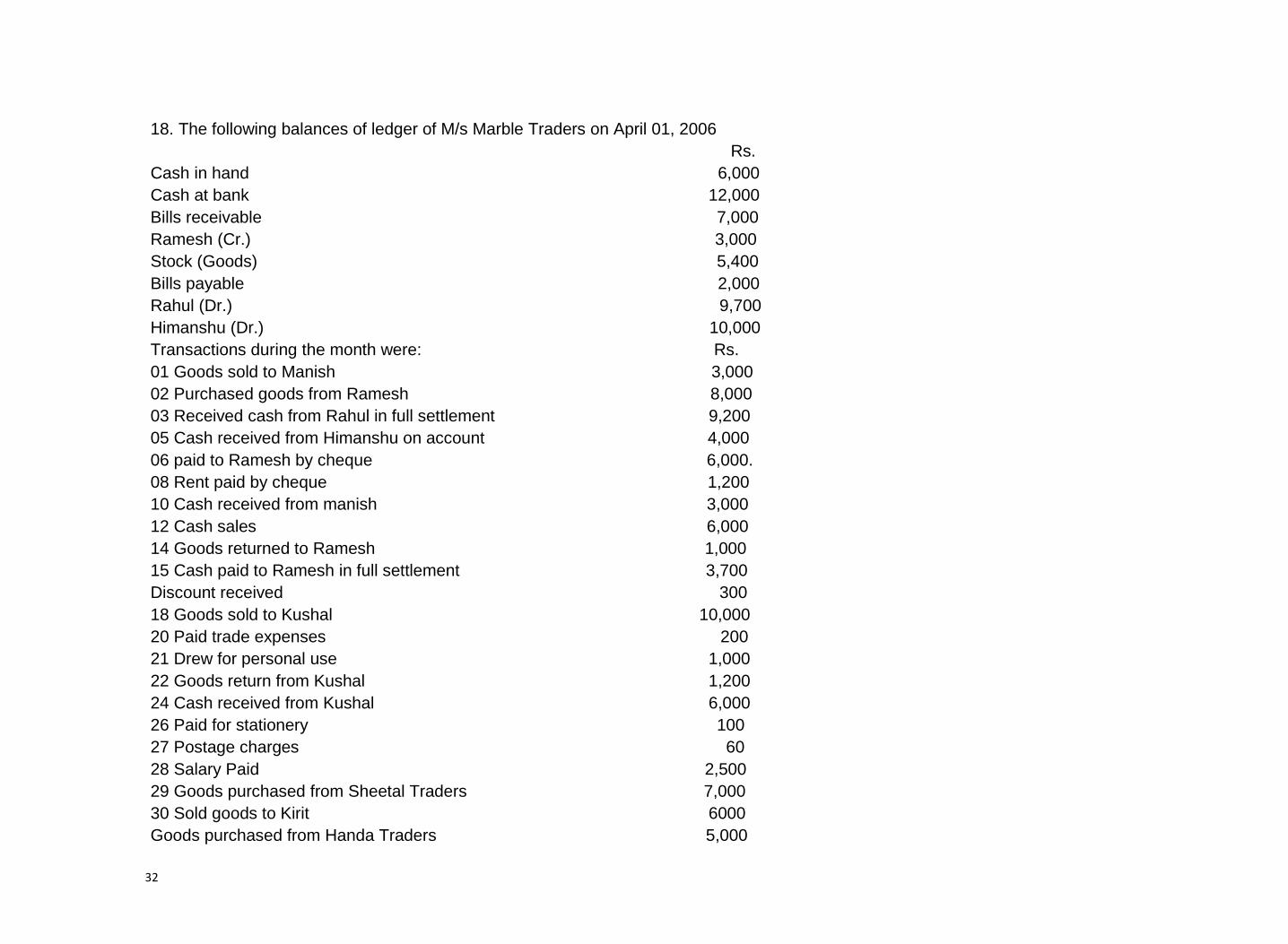

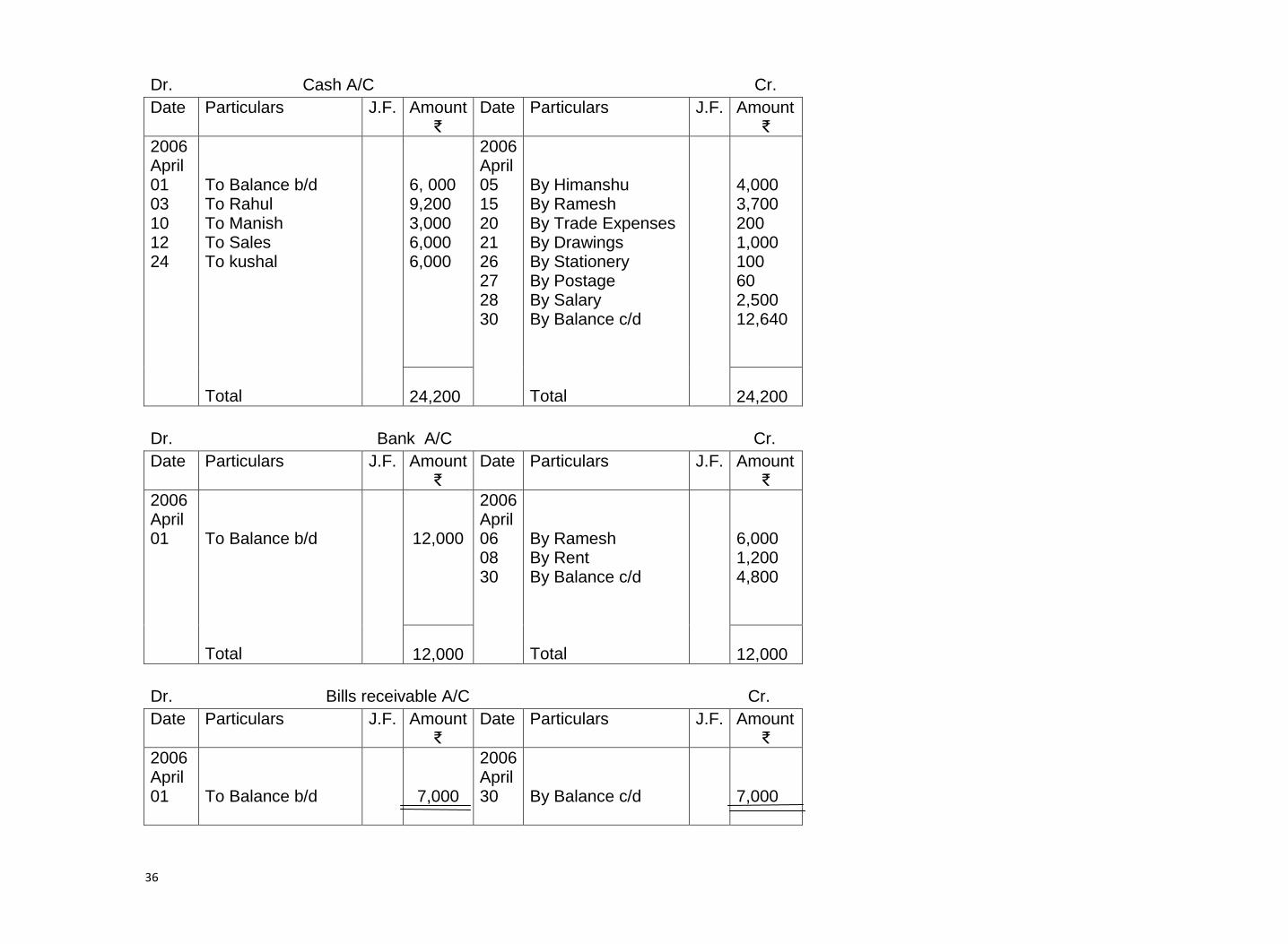

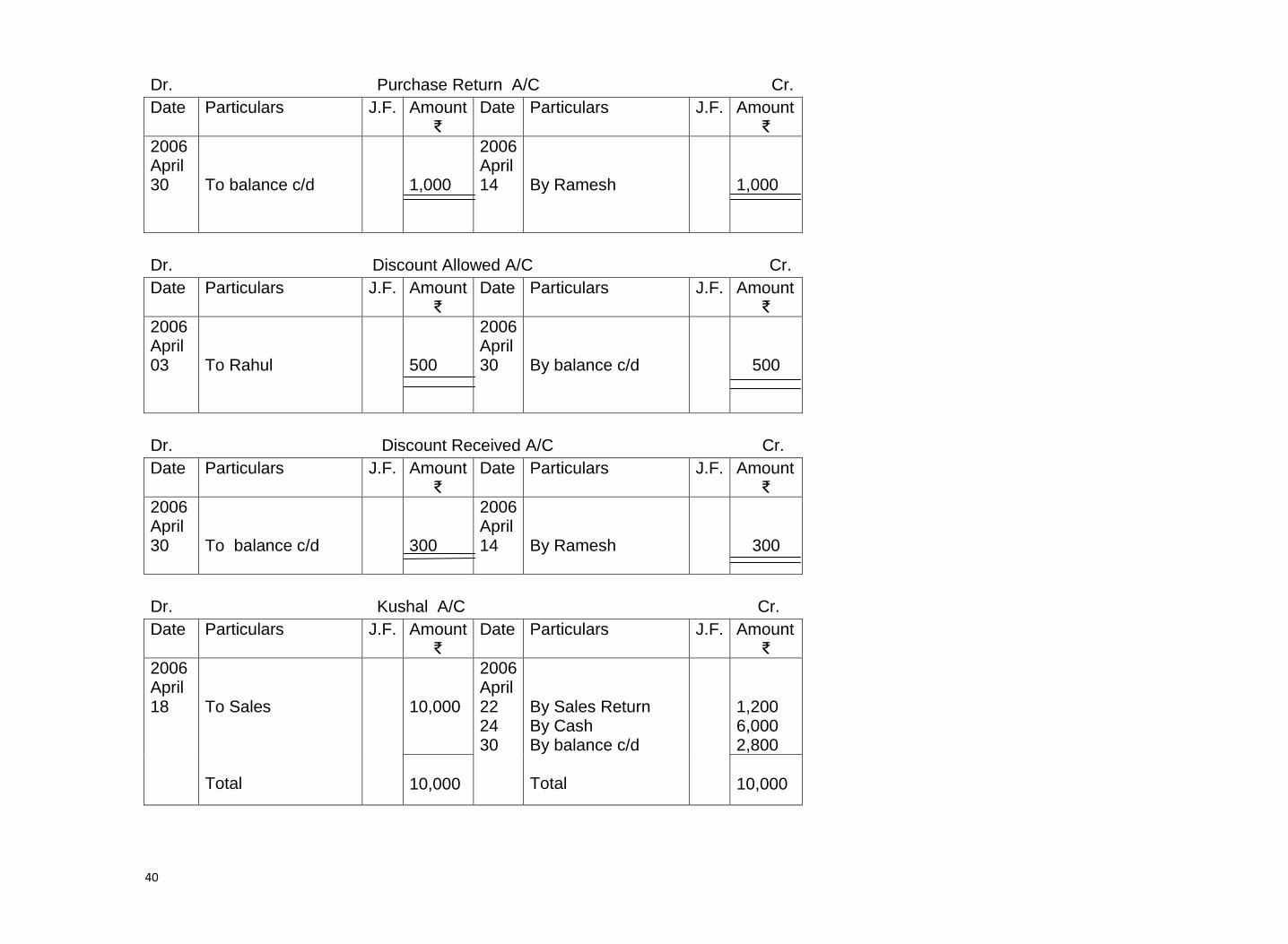

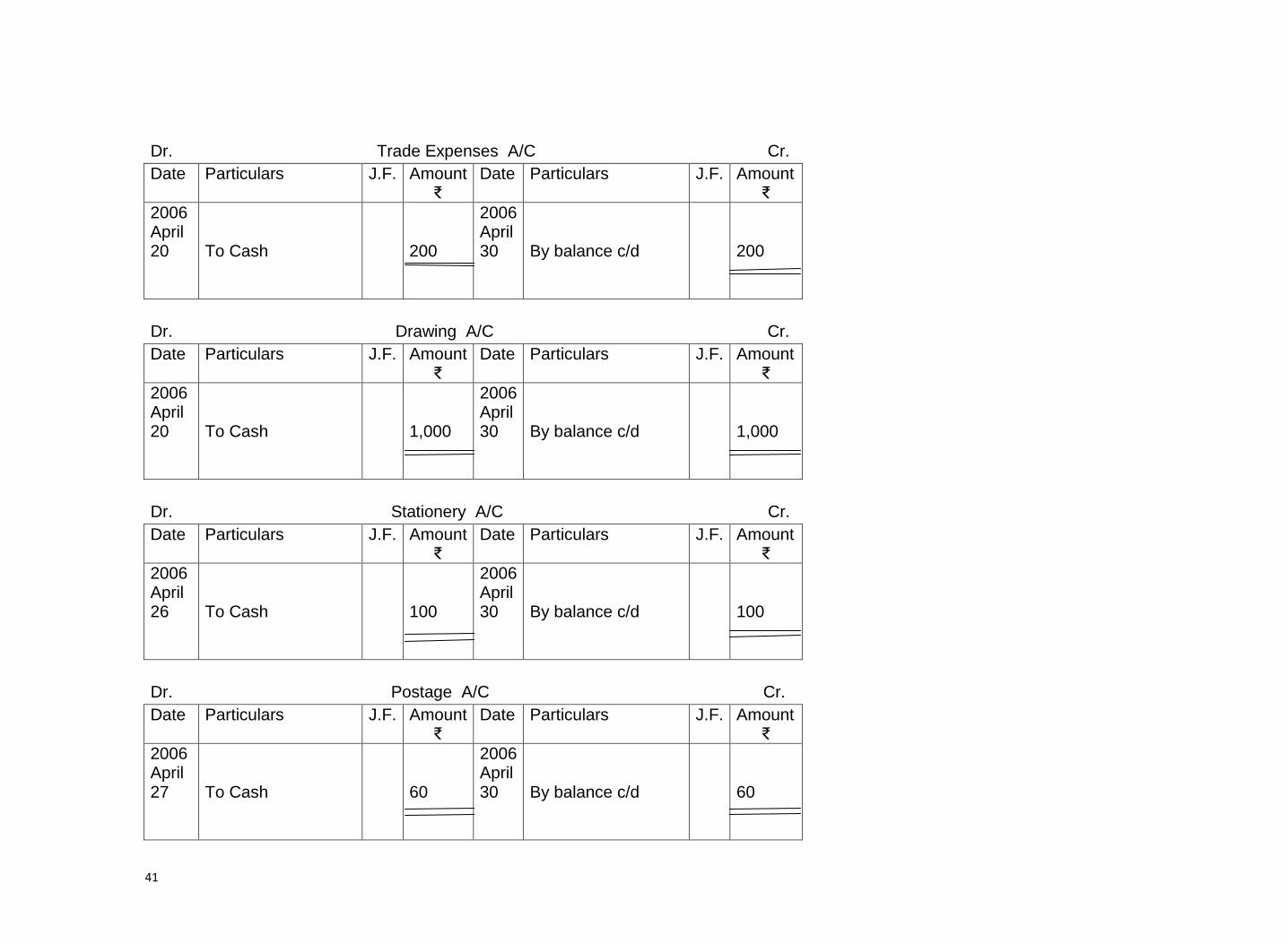

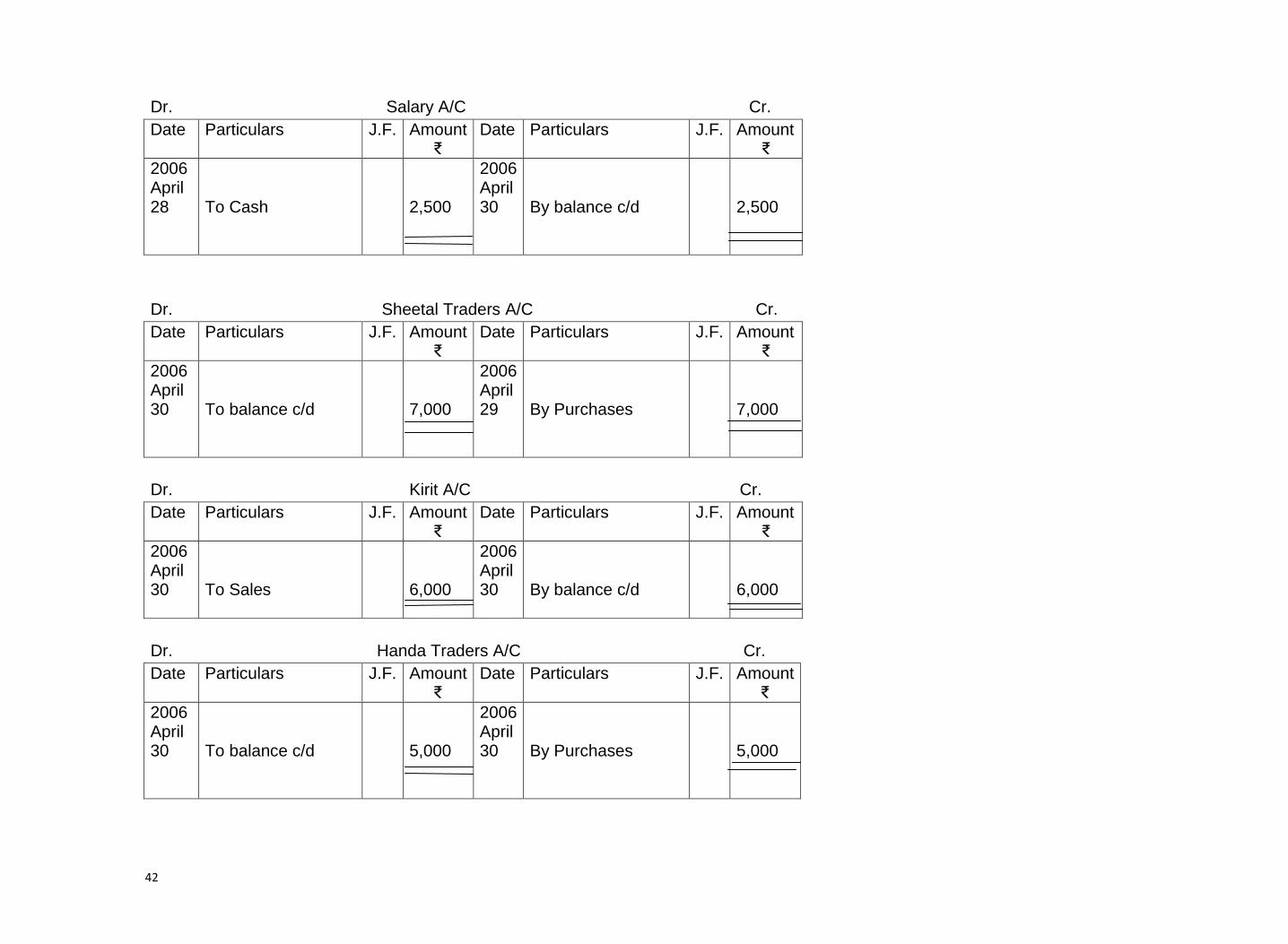

18. The following balances of ledger of M/s Marble Traders on April 01, 2006

Rs.

Cash in hand 6,000

Cash at bank 12,000

Bills receivable 7,000

Ramesh (Cr.) 3,000

Stock (Goods) 5,400

Bills payable 2,000

Rahul (Dr.) 9,700

Himanshu (Dr.) 10,000

Transactions during the month were: Rs.

01 Goods sold to Manish 3,000

02 Purchased goods from Ramesh 8,000

03 Received cash from Rahul in full settlement 9,200

05 Cash received from Himanshu on account 4,000

06 paid to Ramesh by cheque 6,000.

08 Rent paid by cheque 1,200

10 Cash received from manish 3,000

12 Cash sales 6,000

14 Goods returned to Ramesh 1,000

15 Cash paid to Ramesh in full settlement 3,700

Discount received 300

18 Goods sold to Kushal 10,000

20 Paid trade expenses 200

21 Drew for personal use 1,000

22 Goods return from Kushal 1,200

24 Cash received from Kushal 6,000

26 Paid for stationery 100

27 Postage charges 60

28 Salary Paid 2,500

29 Goods purchased from Sheetal Traders 7,000

30 Sold goods to Kirit 6000

Goods purchased from Handa Traders 5,000

33

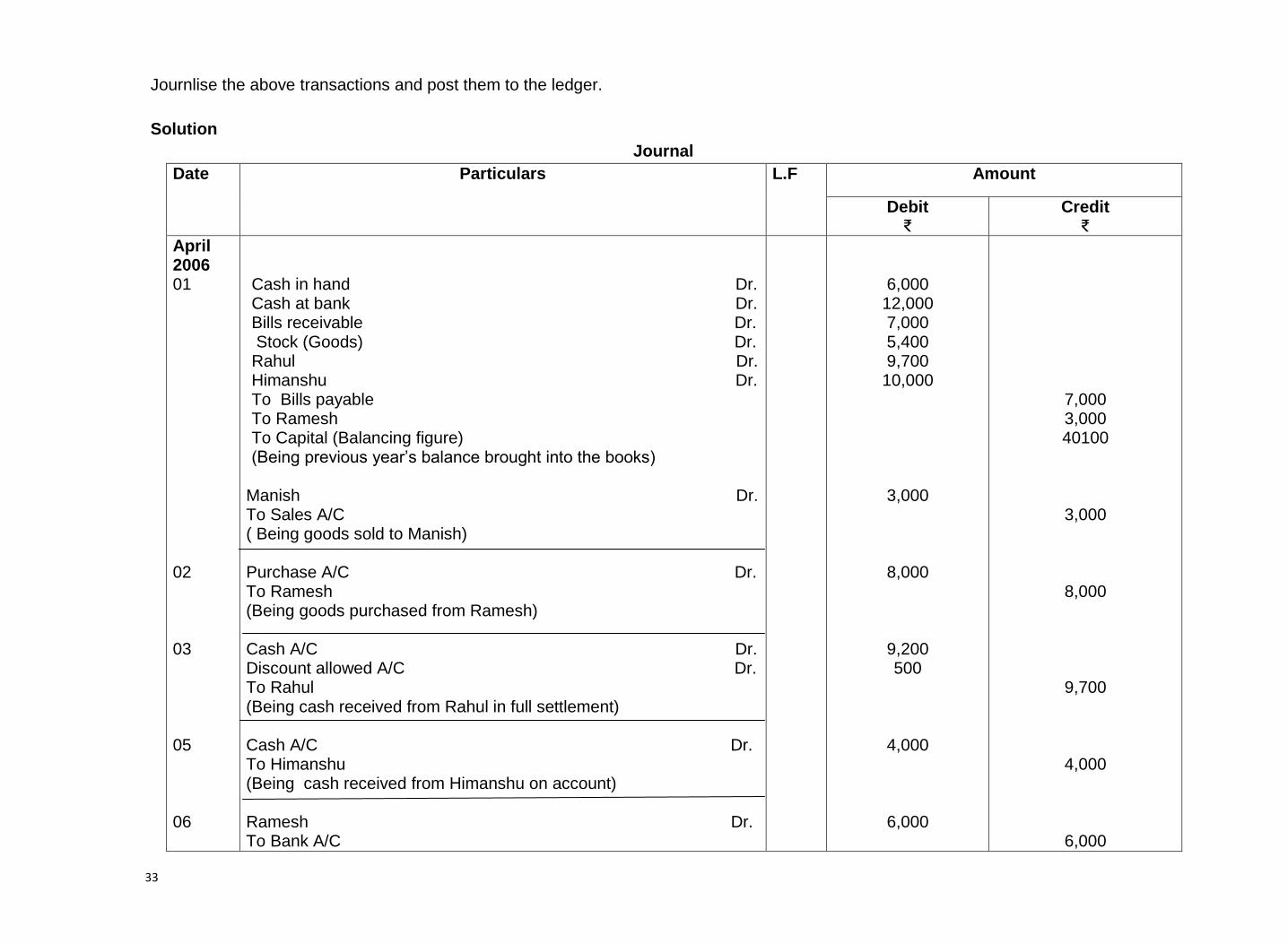

Journlise the above transactions and post them to the ledger.

Solution

Journal

Date Particulars L.F Amount

Debit ₹

Credit ₹

April 2006 01 02 03 05 06

Cash in hand Dr. Cash at bank Dr. Bills receivable Dr. Stock (Goods) Dr. Rahul Dr. Himanshu Dr. To Bills payable To Ramesh To Capital (Balancing figure) (Being previous year’s balance brought into the books)

Manish Dr. To Sales A/C ( Being goods sold to Manish) Purchase A/C Dr. To Ramesh (Being goods purchased from Ramesh) Cash A/C Dr. Discount allowed A/C Dr. To Rahul (Being cash received from Rahul in full settlement) Cash A/C Dr. To Himanshu (Being cash received from Himanshu on account) Ramesh Dr. To Bank A/C

6,000 12,000 7,000 5,400 9,700 10,000

3,000

8,000

9,200 500

4,000

6,000

7,000 3,000 40100

3,000

8,000

9,700

4,000

6,000

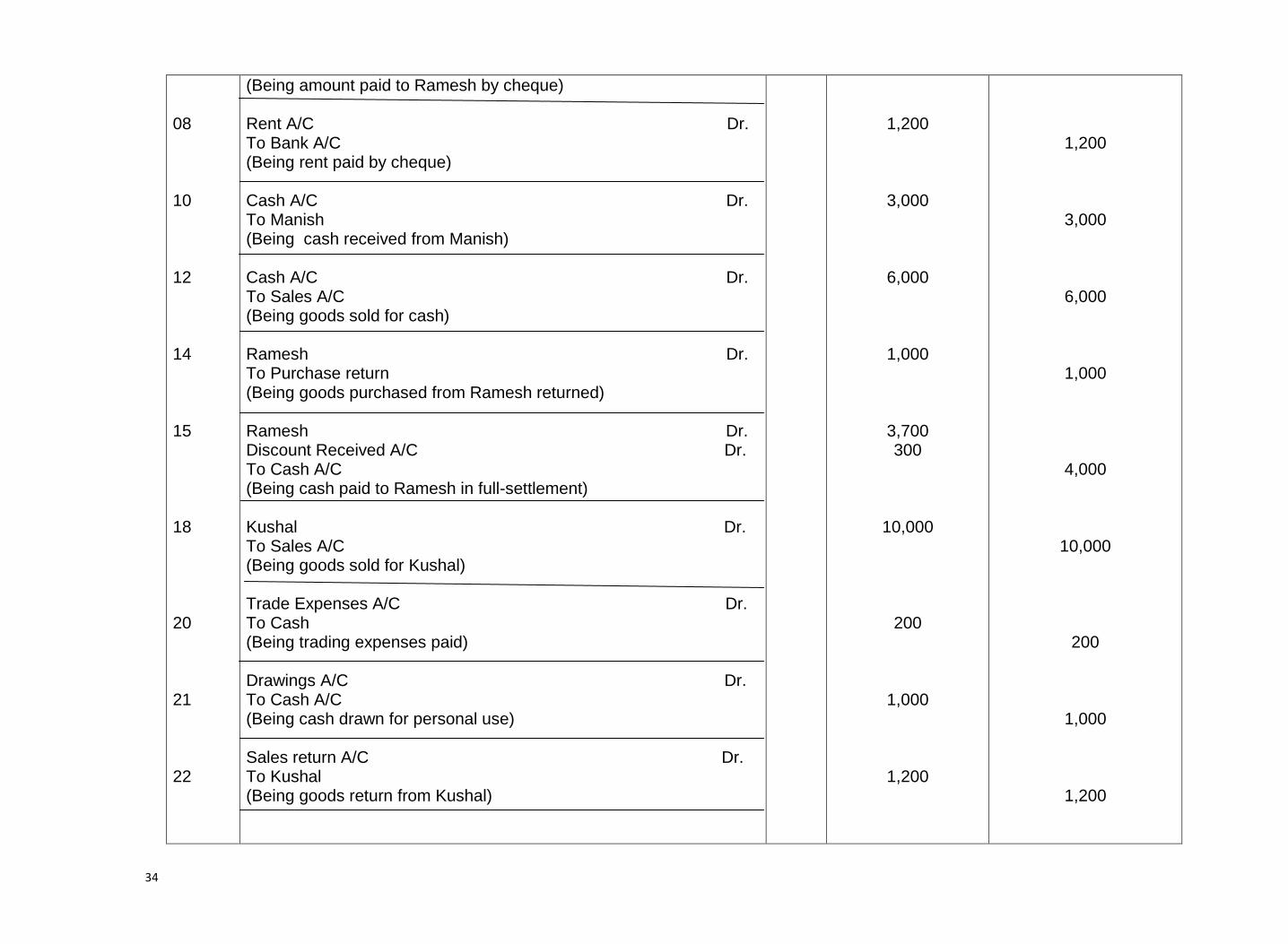

34

08 10 12 14 15 18 20 21 22

(Being amount paid to Ramesh by cheque) Rent A/C Dr. To Bank A/C (Being rent paid by cheque) Cash A/C Dr. To Manish (Being cash received from Manish) Cash A/C Dr. To Sales A/C (Being goods sold for cash) Ramesh Dr. To Purchase return (Being goods purchased from Ramesh returned) Ramesh Dr. Discount Received A/C Dr. To Cash A/C (Being cash paid to Ramesh in full-settlement) Kushal Dr. To Sales A/C (Being goods sold for Kushal) Trade Expenses A/C Dr. To Cash (Being trading expenses paid) Drawings A/C Dr. To Cash A/C (Being cash drawn for personal use) Sales return A/C Dr. To Kushal (Being goods return from Kushal)

1,200

3,000

6,000

1,000

3,700 300

10,000

200

1,000

1,200

1,200

3,000

6,000

1,000

4,000

10,000

200

1,000

1,200

35

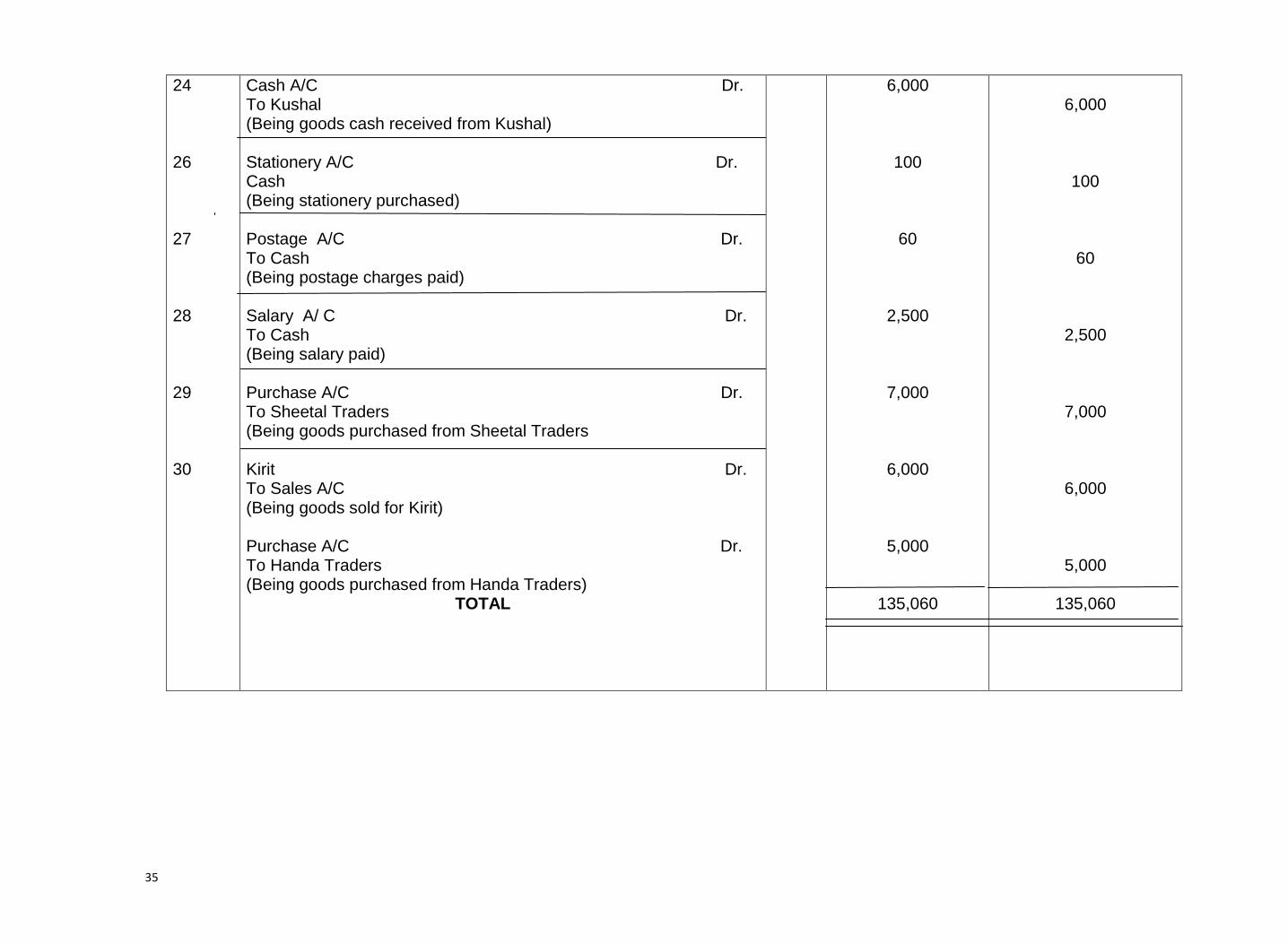

24 26 27 28 29 30

Cash A/C Dr. To Kushal (Being goods cash received from Kushal) Stationery A/C Dr. Cash (Being stationery purchased) Postage A/C Dr. To Cash (Being postage charges paid) Salary A/ C Dr. To Cash (Being salary paid) Purchase A/C Dr. To Sheetal Traders (Being goods purchased from Sheetal Traders Kirit Dr. To Sales A/C (Being goods sold for Kirit) Purchase A/C Dr. To Handa Traders (Being goods purchased from Handa Traders) TOTAL

6,000

100

60

2,500

7,000

6,000

5,000

135,060

6,000

100

60

2,500

7,000

6,000

5,000

135,060

36

Dr. Cash A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 April 01 03 10 12 24

To Balance b/d To Rahul To Manish To Sales To kushal Total

6, 000 9,200 3,000 6,000 6,000

2006 April 05 15 20 21 26 27 28 30

By Himanshu By Ramesh By Trade Expenses By Drawings By Stationery By Postage By Salary By Balance c/d Total

4,000 3,700 200 1,000 100 60 2,500 12,640

24,200

24,200

Dr. Bank A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 April 01

To Balance b/d Total

12,000

2006 April 06 08 30

By Ramesh By Rent By Balance c/d Total

6,000 1,200 4,800

12,000

12,000

Dr. Bills receivable A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 April 01

To Balance b/d

7,000

2006 April 30

By Balance c/d

7,000

37

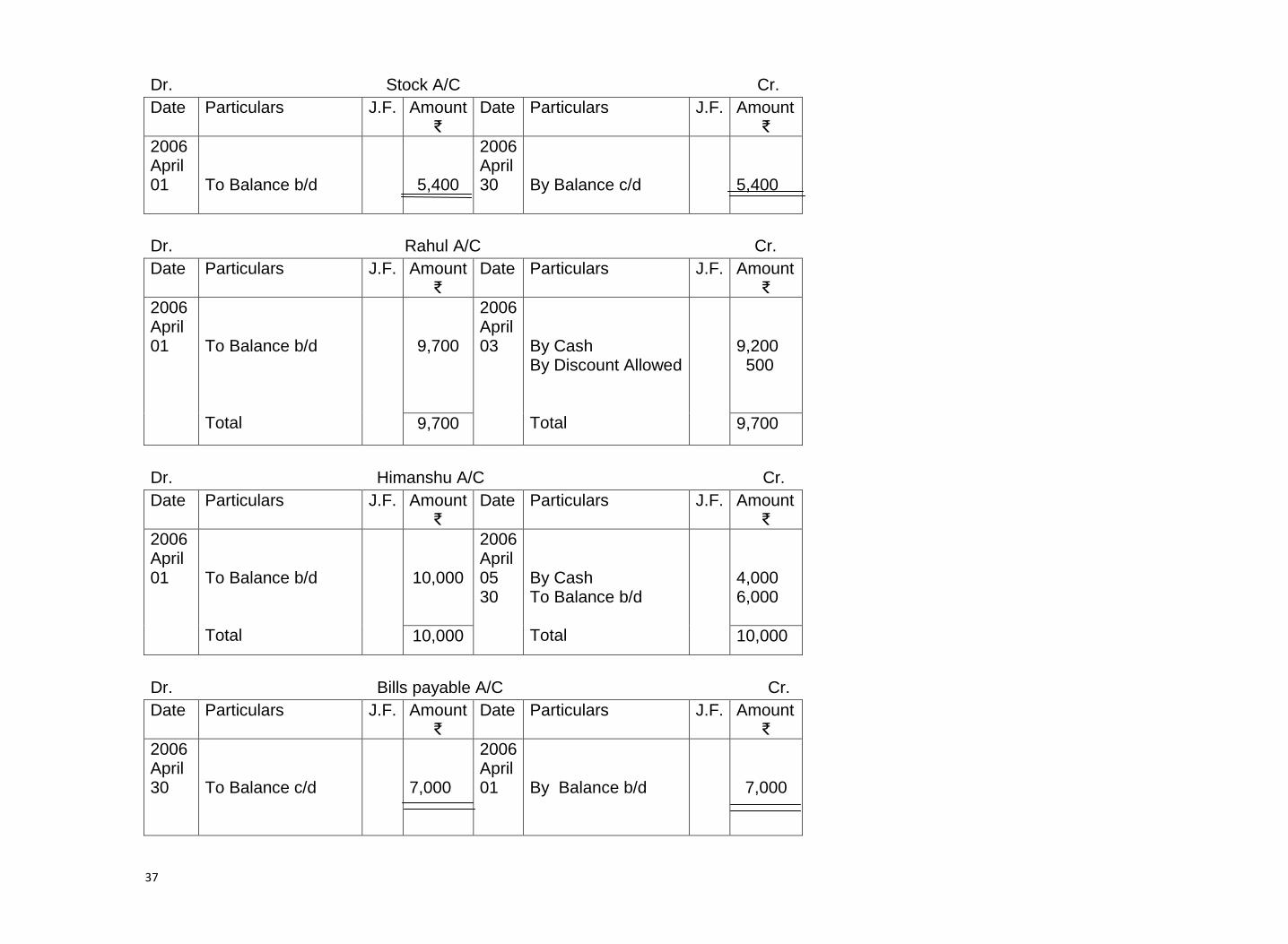

Dr. Stock A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 April 01

To Balance b/d

5,400

2006 April 30

By Balance c/d

5,400

Dr. Rahul A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 April 01

To Balance b/d Total

9,700

2006 April 03

By Cash By Discount Allowed Total

9,200 500

9,700 9,700

Dr. Himanshu A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 April 01

To Balance b/d Total

10,000

2006 April 05 30

By Cash To Balance b/d Total

4,000 6,000

10,000 10,000

Dr. Bills payable A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 April 30

To Balance c/d

7,000

2006 April 01

By Balance b/d

7,000

38

Dr. Tarun A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 April 30

To Balance c/d

3,000

2006 April 01

By Balance b/d

3,000

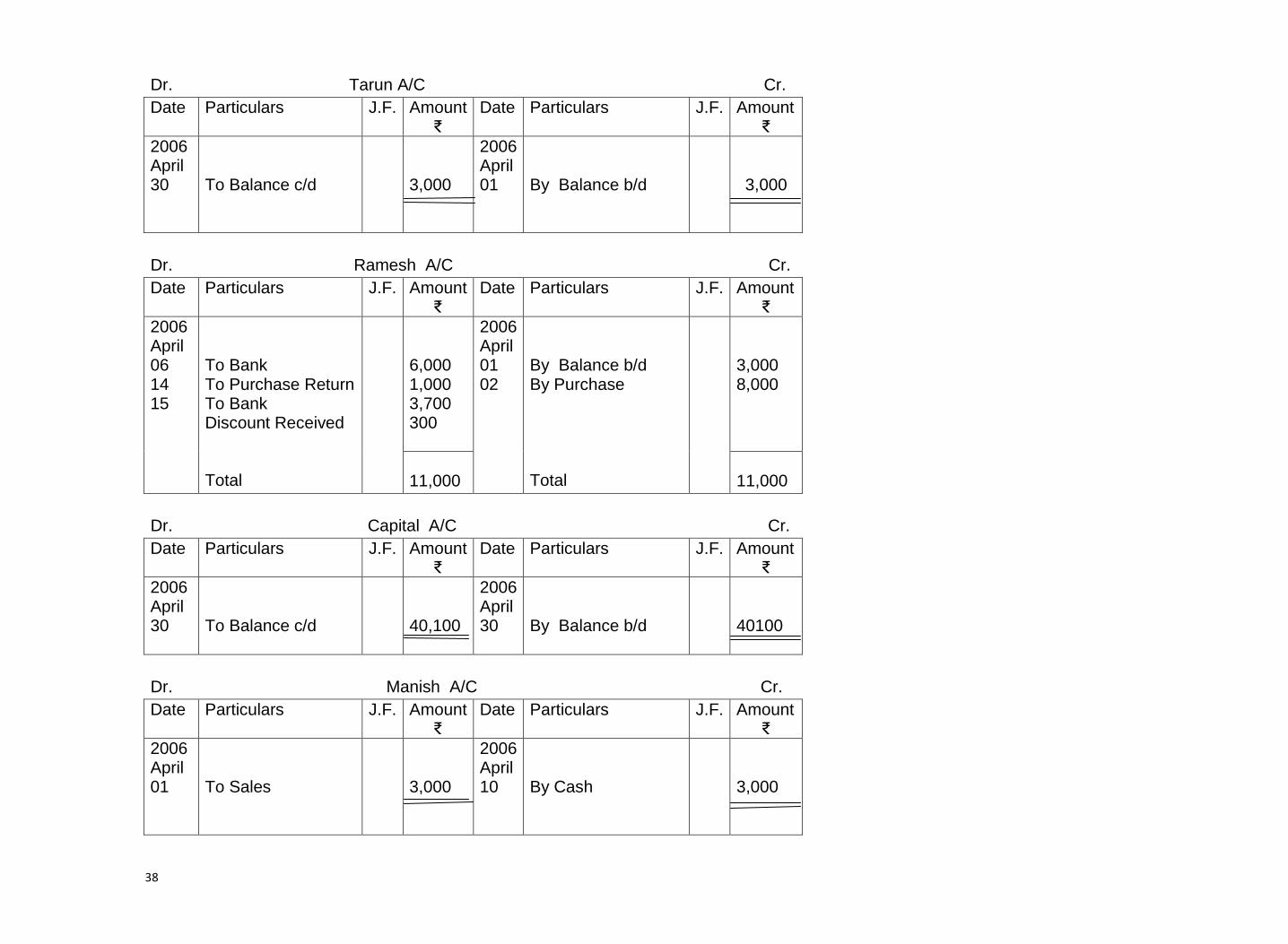

Dr. Ramesh A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 April 06 14 15

To Bank To Purchase Return To Bank Discount Received Total

6,000 1,000 3,700 300

2006 April 01 02

By Balance b/d By Purchase Total

3,000 8,000

11,000

11,000

Dr. Capital A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 April 30

To Balance c/d

40,100

2006 April 30

By Balance b/d

40100

Dr. Manish A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 April 01

To Sales

3,000

2006 April 10

By Cash

3,000

39

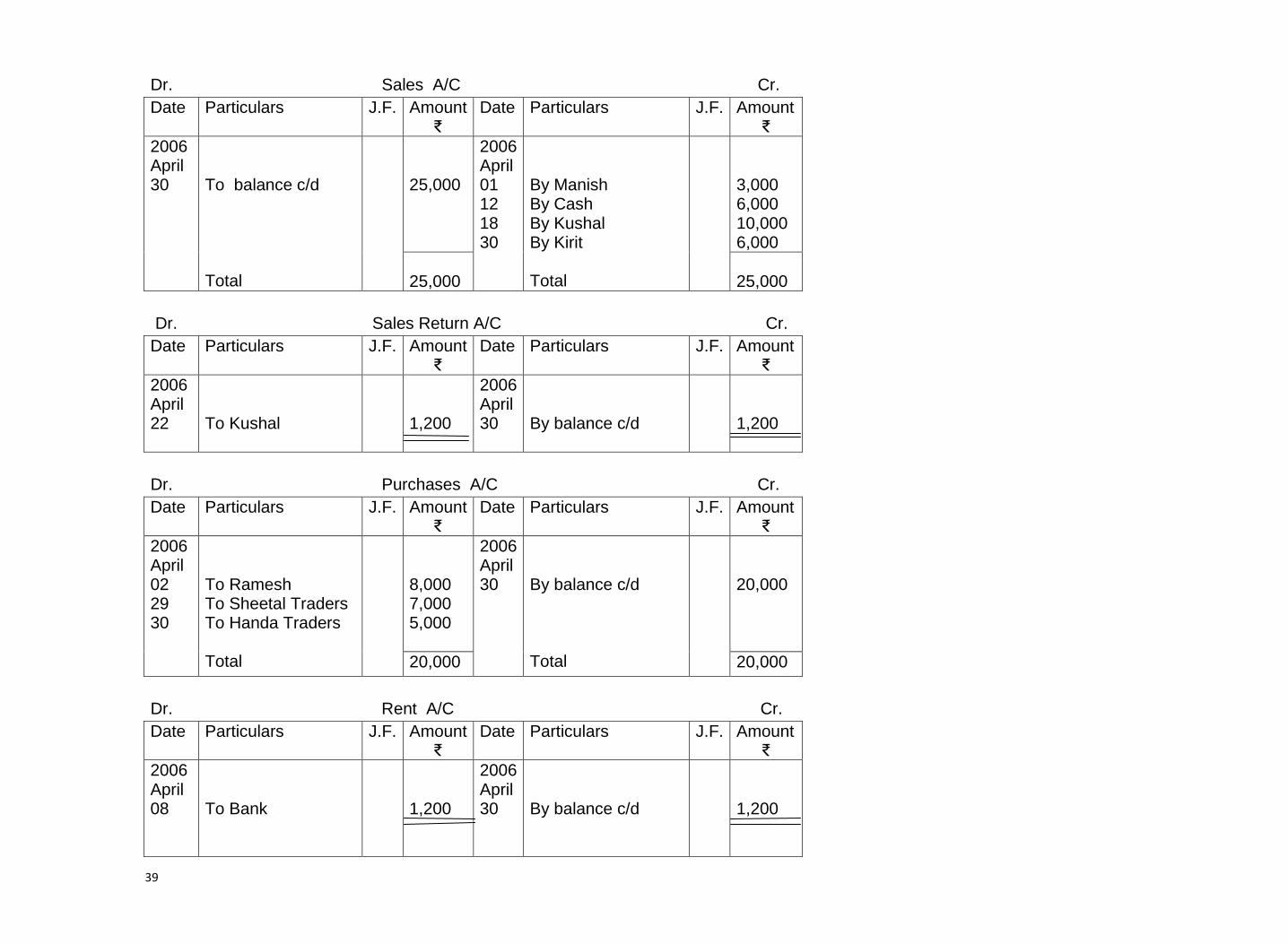

Dr. Sales A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 April 30

To balance c/d Total

25,000

2006 April 01 12 18 30

By Manish By Cash By Kushal By Kirit Total

3,000 6,000 10,000 6,000

25,000

25,000

Dr. Sales Return A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 April 22

To Kushal

1,200

2006 April 30

By balance c/d

1,200

Dr. Purchases A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 April 02 29 30

To Ramesh To Sheetal Traders To Handa Traders Total

8,000 7,000 5,000

2006 April 30

By balance c/d Total

20,000

20,000 20,000

Dr. Rent A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 April 08

To Bank

1,200

2006 April 30

By balance c/d

1,200

40

Dr. Purchase Return A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 April 30

To balance c/d

1,000

2006 April 14

By Ramesh

1,000

Dr. Discount Allowed A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 April 03

To Rahul

500

2006 April 30

By balance c/d

500

Dr. Discount Received A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 April 30

To balance c/d

300

2006 April 14

By Ramesh

300

Dr. Kushal A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 April 18

To Sales Total

10,000

2006 April 22 24 30

By Sales Return By Cash By balance c/d Total

1,200 6,000 2,800

10,000

10,000

41

Dr. Trade Expenses A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 April 20

To Cash

200

2006 April 30

By balance c/d

200

Dr. Drawing A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 April 20

To Cash

1,000

2006 April 30

By balance c/d

1,000

Dr. Stationery A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 April 26

To Cash

100

2006 April 30

By balance c/d

100

Dr. Postage A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 April 27

To Cash

60

2006 April 30

By balance c/d

60

42

Dr. Salary A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 April 28

To Cash

2,500

2006 April 30

By balance c/d

2,500

Dr. Sheetal Traders A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 April 30

To balance c/d

7,000

2006 April 29

By Purchases

7,000

Dr. Kirit A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 April 30

To Sales

6,000

2006 April 30

By balance c/d

6,000

Dr. Handa Traders A/C Cr.

Date Particulars J.F. Amount ₹

Date Particulars J.F. Amount ₹

2006 April 30

To balance c/d

5,000

2006 April 30

By Purchases

5,000