accounting i. proving the ledger trial balance transposition error slide error correcting entry

TRANSCRIPT

Trial BalanceAccounting I

Proving the Ledger Trial Balance Transposition Error Slide Error Correcting Entry

Key Vocabulary

Adding all the debit balances and adding all the credit balances and then comparing the two totals to see whether they are equal.

A list of all the account names and the current balances.

When two digits within an amount are accidentally reversed. This error is divisible by 9.

When the decimal place is moved ( or add or subtract a zero)

An entry made to correct an error in a journal entry discovered AFTER posting.

Definitions:

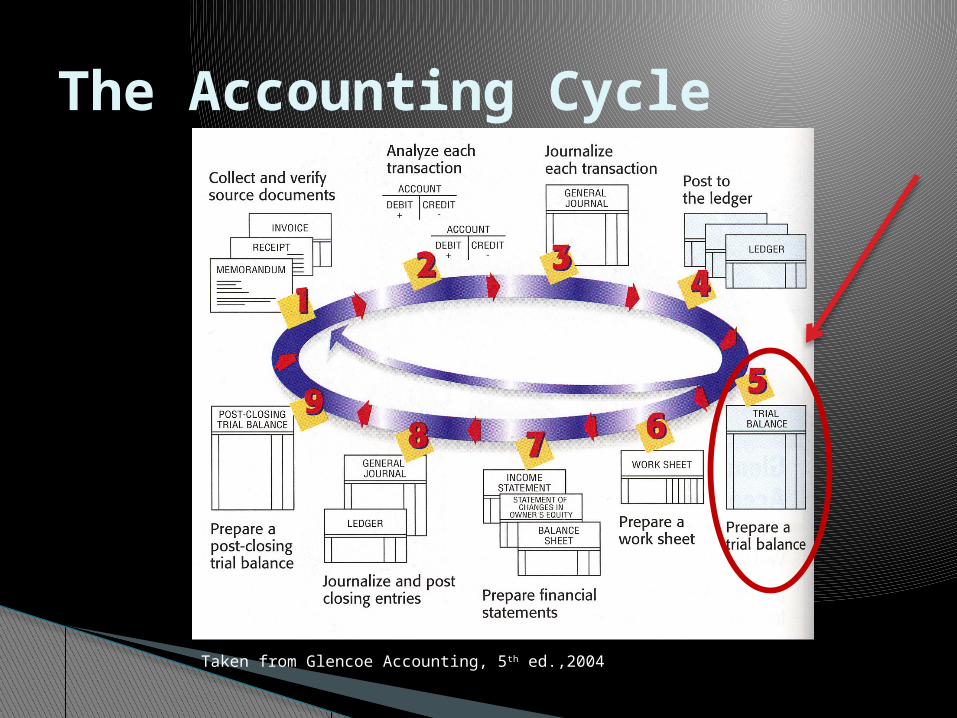

The Accounting Cycle

Taken from Glencoe Accounting, 5th ed.,2004

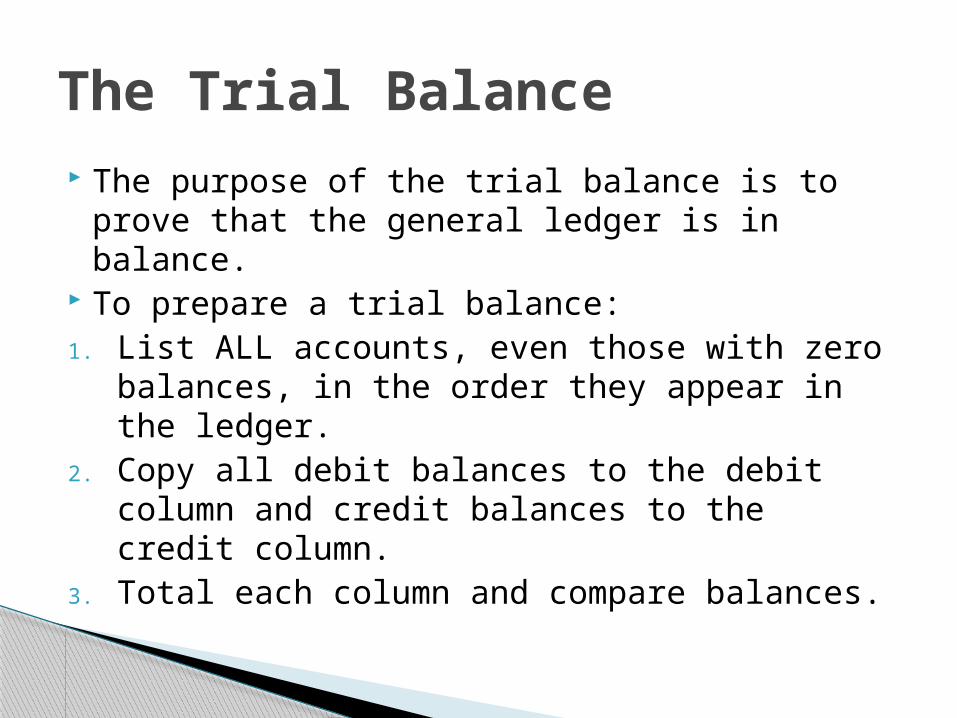

The purpose of the trial balance is to prove that the general ledger is in balance.

To prepare a trial balance: 1. List ALL accounts, even those with zero

balances, in the order they appear in the ledger.

2. Copy all debit balances to the debit column and credit balances to the credit column.

3. Total each column and compare balances.

The Trial Balance

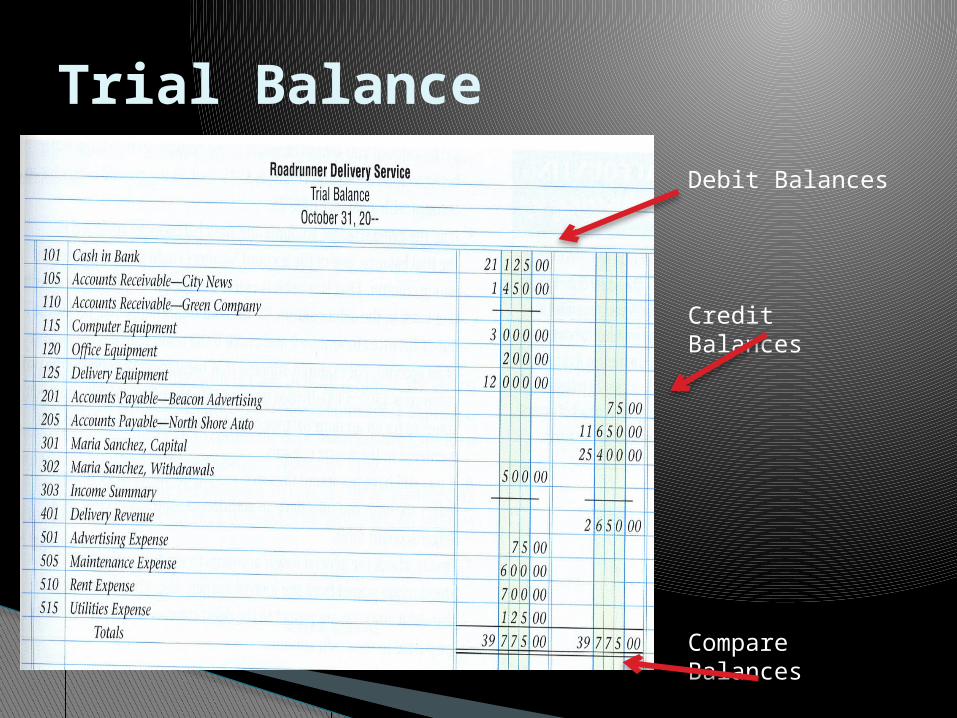

Trial Balance

Debit Balances

Credit Balances

Compare Balances

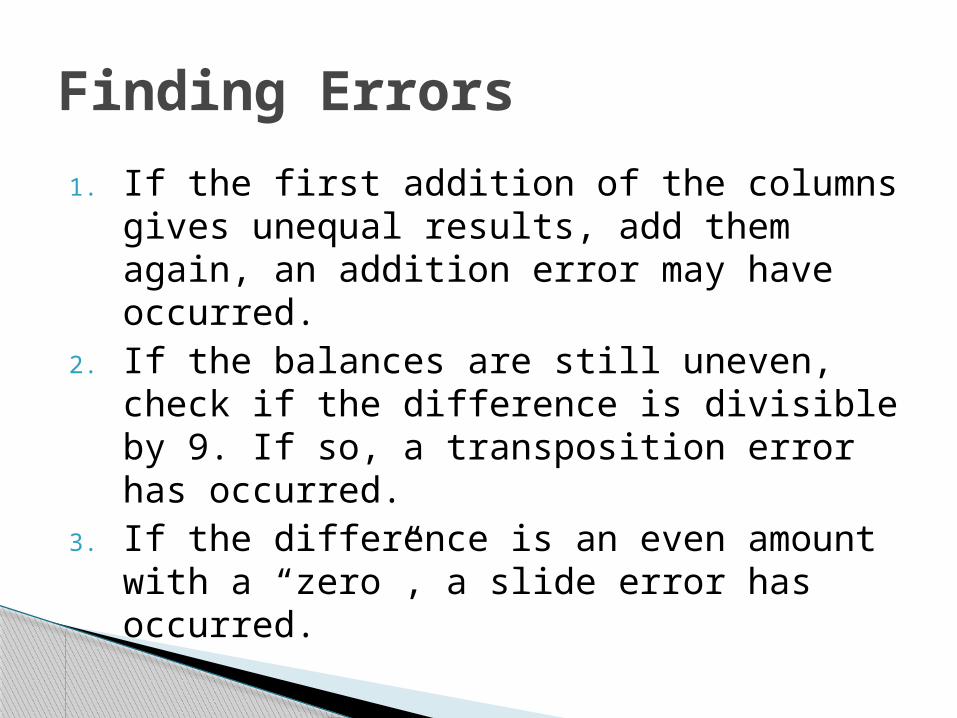

1. If the first addition of the columns gives unequal results, add them again, an addition error may have occurred.

2. If the balances are still uneven, check if the difference is divisible by 9. If so, a transposition error has occurred.

3. If the difference is an even amount with a “zero”, a slide error has occurred.

Finding Errors

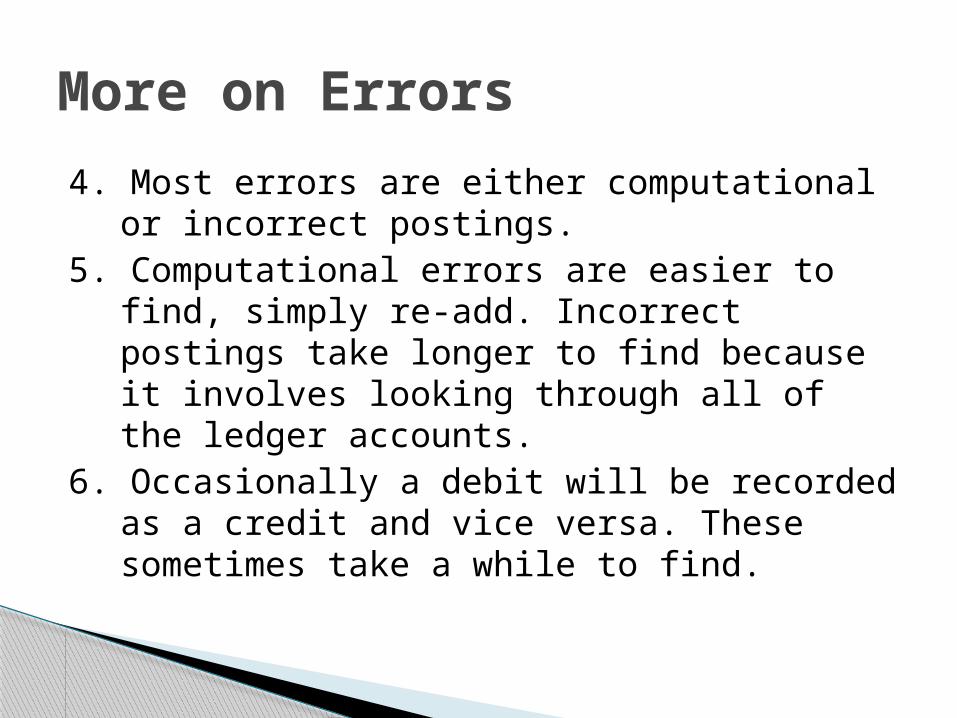

4. Most errors are either computational or incorrect postings.

5. Computational errors are easier to find, simply re-add. Incorrect postings take longer to find because it involves looking through all of the ledger accounts.

6. Occasionally a debit will be recorded as a credit and vice versa. These sometimes take a while to find.

More on Errors

Anyone who works in accounting understands the saying “ To err is human…” When mistakes are made in accounting, however, one rule applies: NEVER erase an error.Three types of errors:Error in journal entry that is not posted.Error in posting to the ledger when the journal entry is correct.Error in journal entry that is posted.

Correcting Entries

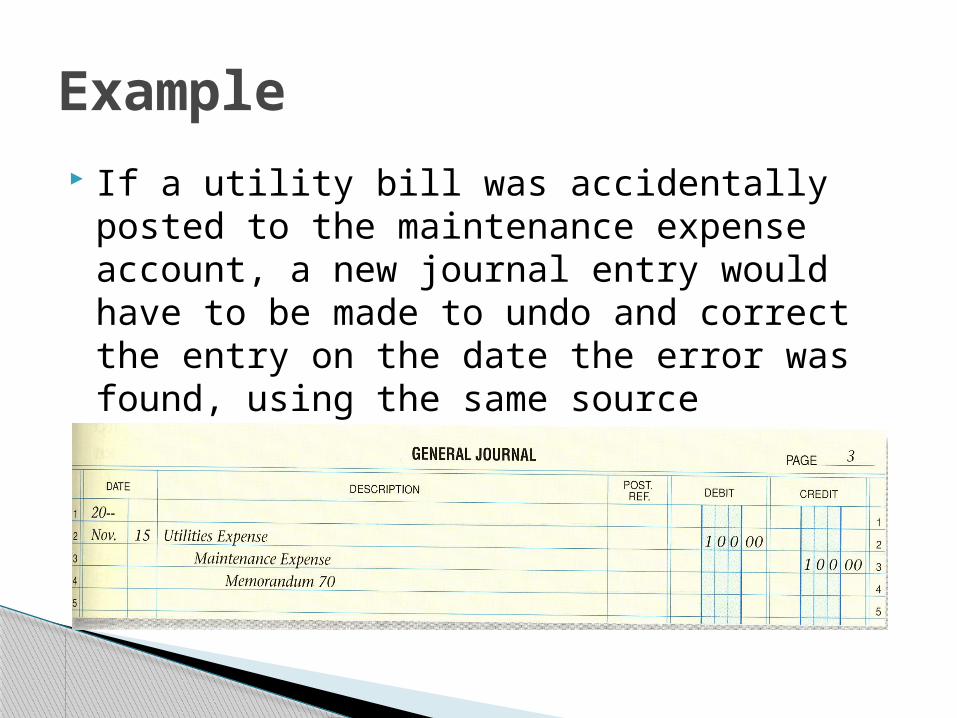

If a utility bill was accidentally posted to the maintenance expense account, a new journal entry would have to be made to undo and correct the entry on the date the error was found, using the same source document:

Example

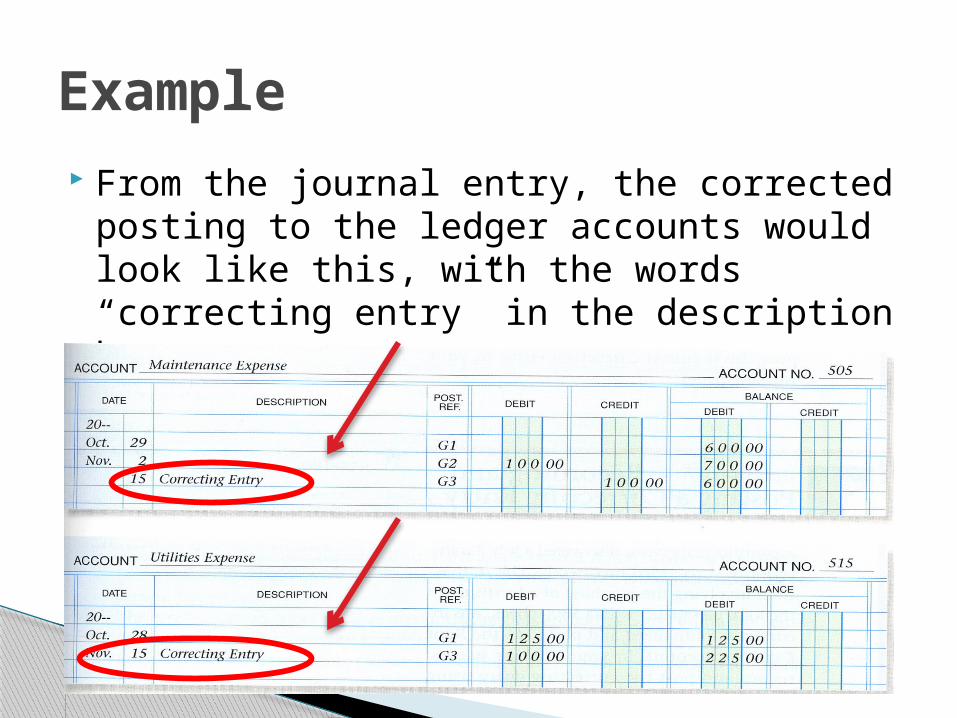

From the journal entry, the corrected posting to the ledger accounts would look like this, with the words “correcting entry” in the description box:

Example

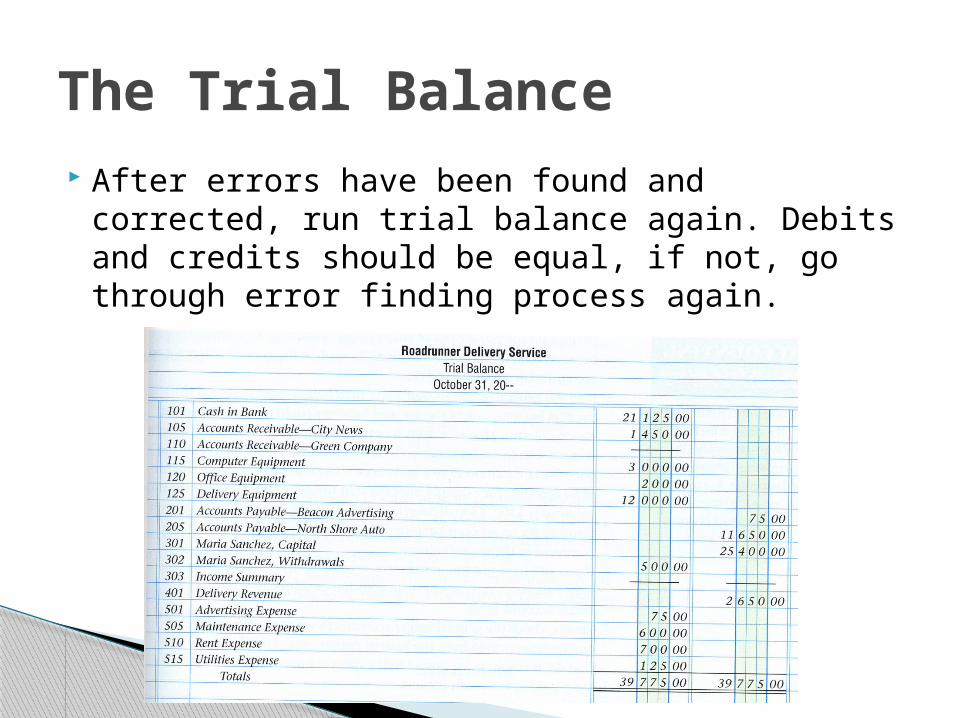

After errors have been found and corrected, run trial balance again. Debits and credits should be equal, if not, go through error finding process again.

The Trial Balance

Guerrieri, Haber, Hoyt, & Turner. (2004) Glencoe Accounting: Real-World Applications & Connections. (5th ed.) Woodland Hills, CA: Glencoe McGraw Hill.

References