accounting & reporting conversion us gaap - ifrs · equity ratio in % 44 ifrs: ... other...

TRANSCRIPT

01/081

Accounting & Reporting Conversion US GAAP – IFRS

Accounting & Reporting ConversionUS GAAP – IFRS

January 2008

01/082

Accounting & Reporting Conversion US GAAP – IFRS

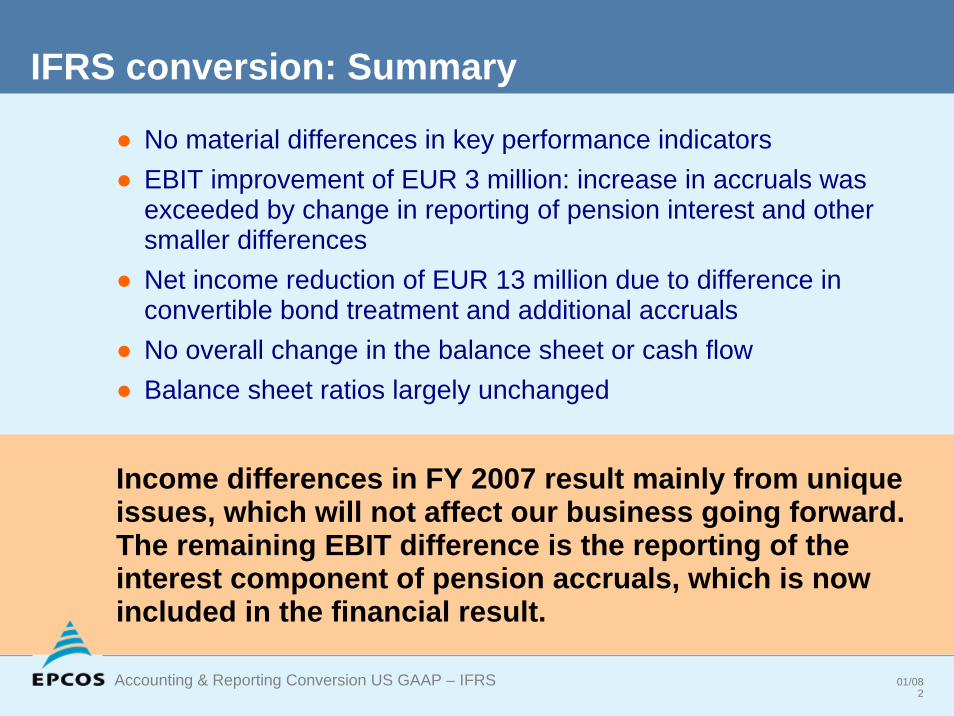

IFRS conversion: Summary

● No material differences in key performance indicators● EBIT improvement of EUR 3 million: increase in accruals was

exceeded by change in reporting of pension interest and other smaller differences

● Net income reduction of EUR 13 million due to difference in convertible bond treatment and additional accruals

● No overall change in the balance sheet or cash flow● Balance sheet ratios largely unchanged

Income differences in FY 2007 result mainly from unique issues, which will not affect our business going forward. The remaining EBIT difference is the reporting of the interest component of pension accruals, which is now included in the financial result.

01/083

Accounting & Reporting Conversion US GAAP – IFRS

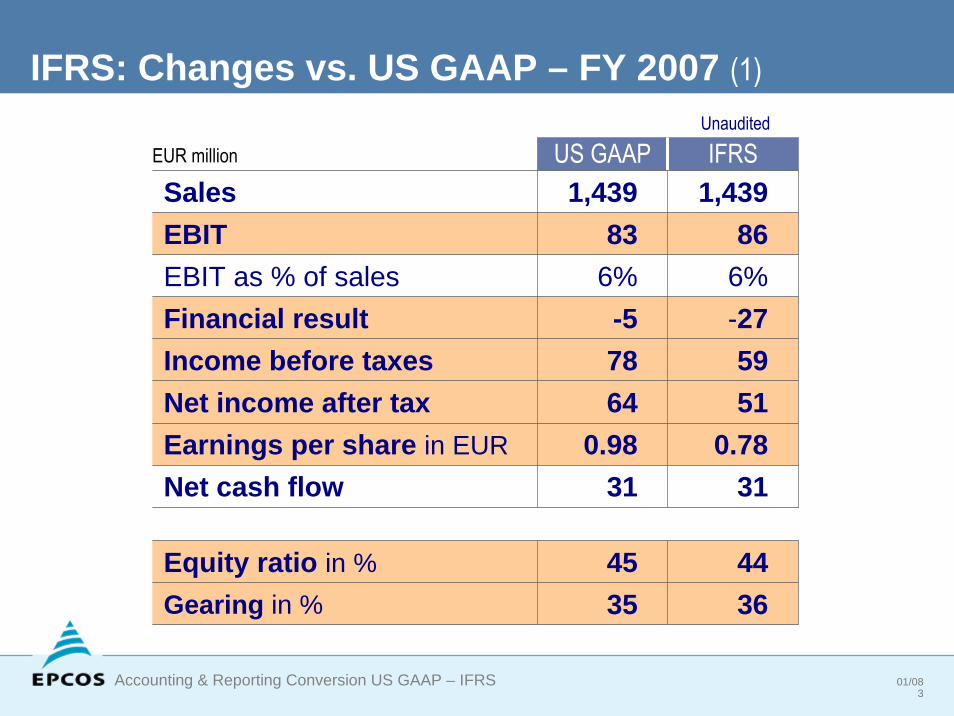

EUR million US GAAP IFRSSales 1,439

83EBIT as % of sales 6% 6%

Gearing in % 35 36

-578

Net income after tax 64 51Earnings per share in EUR 0.98 0.78

31

45

1,439EBIT 86

Financial result -27Income before taxes 59

Net cash flow 31

Equity ratio in % 44

IFRS: Changes vs. US GAAP – FY 2007 (1)Unaudited

01/084

Accounting & Reporting Conversion US GAAP – IFRS

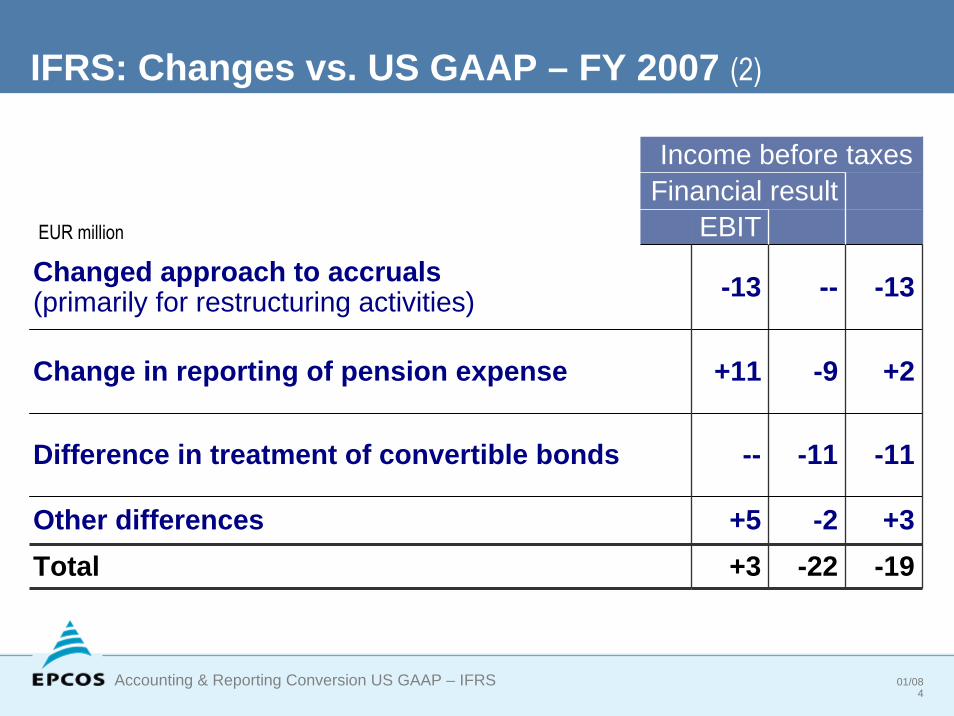

Income before taxesFinancial result

in Mio. EUR EBITChanged approach to accruals(primarily for restructuring activities) -13 -- -13

Change in reporting of pension expense +11 -9 +2

Difference in treatment of convertible bonds -- -11 -11

Other differences +5 -2 +3Total +3 -22 -19

IFRS: Changes vs. US GAAP – FY 2007 (2)

EUR million

01/085

Accounting & Reporting Conversion US GAAP – IFRS

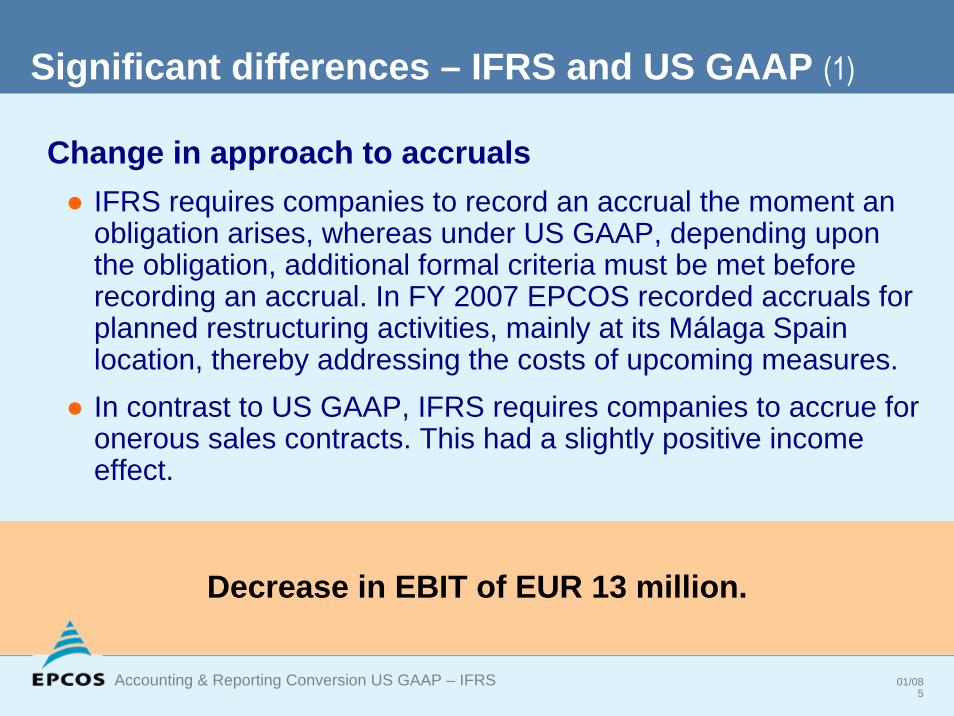

Significant differences – IFRS and US GAAP (1)

Change in approach to accruals● IFRS requires companies to record an accrual the moment an

obligation arises, whereas under US GAAP, depending upon the obligation, additional formal criteria must be met beforerecording an accrual. In FY 2007 EPCOS recorded accruals forplanned restructuring activities, mainly at its Málaga Spain location, thereby addressing the costs of upcoming measures.

● In contrast to US GAAP, IFRS requires companies to accrue for onerous sales contracts. This had a slightly positive income effect.

Decrease in EBIT of EUR 13 million.

01/086

Accounting & Reporting Conversion US GAAP – IFRS

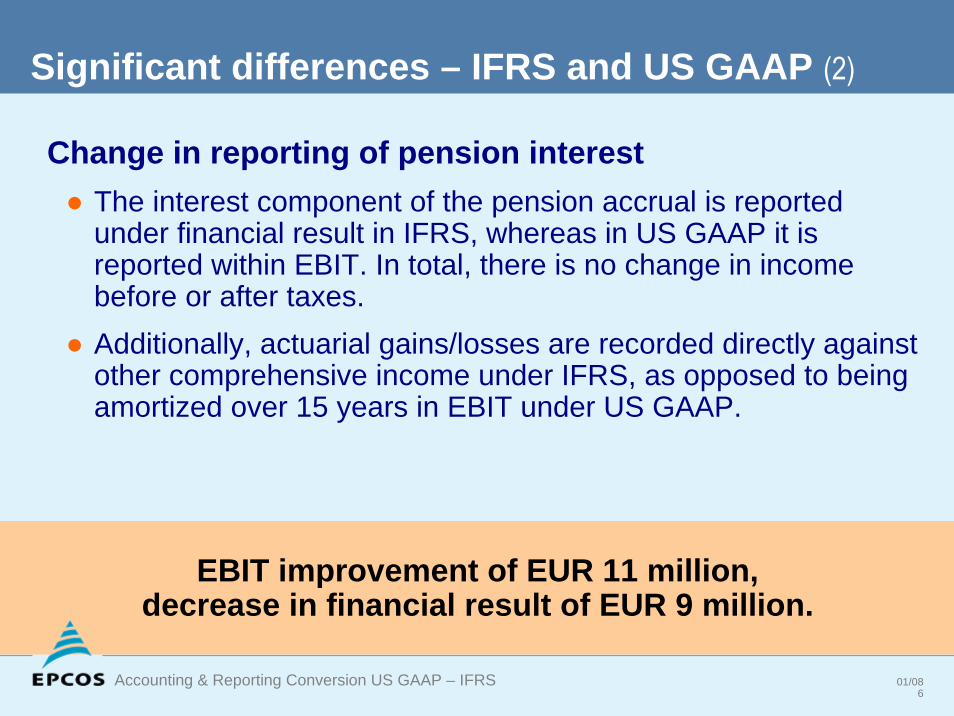

Significant differences – IFRS and US GAAP (2)

Change in reporting of pension interest● The interest component of the pension accrual is reported

under financial result in IFRS, whereas in US GAAP it is reported within EBIT. In total, there is no change in income before or after taxes.

● Additionally, actuarial gains/losses are recorded directly against other comprehensive income under IFRS, as opposed to being amortized over 15 years in EBIT under US GAAP.

EBIT improvement of EUR 11 million,decrease in financial result of EUR 9 million.

01/087

Accounting & Reporting Conversion US GAAP – IFRS

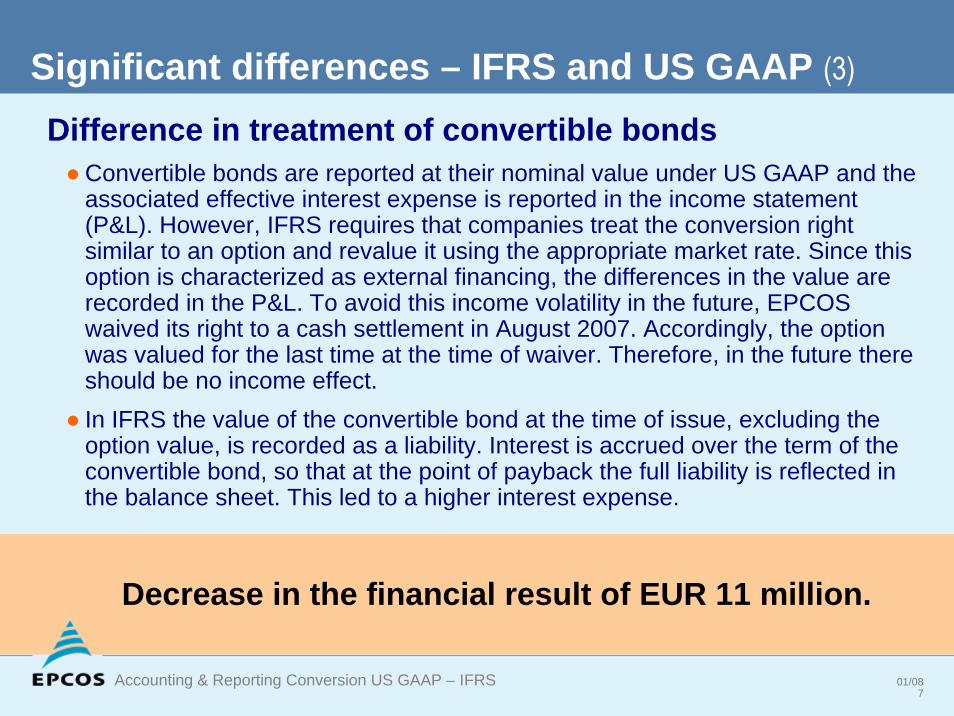

Significant differences – IFRS and US GAAP (3)

Difference in treatment of convertible bonds● Convertible bonds are reported at their nominal value under US GAAP and the

associated effective interest expense is reported in the income statement(P&L). However, IFRS requires that companies treat the conversion right similar to an option and revalue it using the appropriate market rate. Since thisoption is characterized as external financing, the differences in the value arerecorded in the P&L. To avoid this income volatility in the future, EPCOS waived its right to a cash settlement in August 2007. Accordingly, the optionwas valued for the last time at the time of waiver. Therefore, in the future thereshould be no income effect.

● In IFRS the value of the convertible bond at the time of issue, excluding the option value, is recorded as a liability. Interest is accrued over the term of the convertible bond, so that at the point of payback the full liability is reflected in the balance sheet. This led to a higher interest expense.

Decrease in the financial result of EUR 11 million.

01/088

Accounting & Reporting Conversion US GAAP – IFRS

Significant differences – IFRS and US GAAP (4)

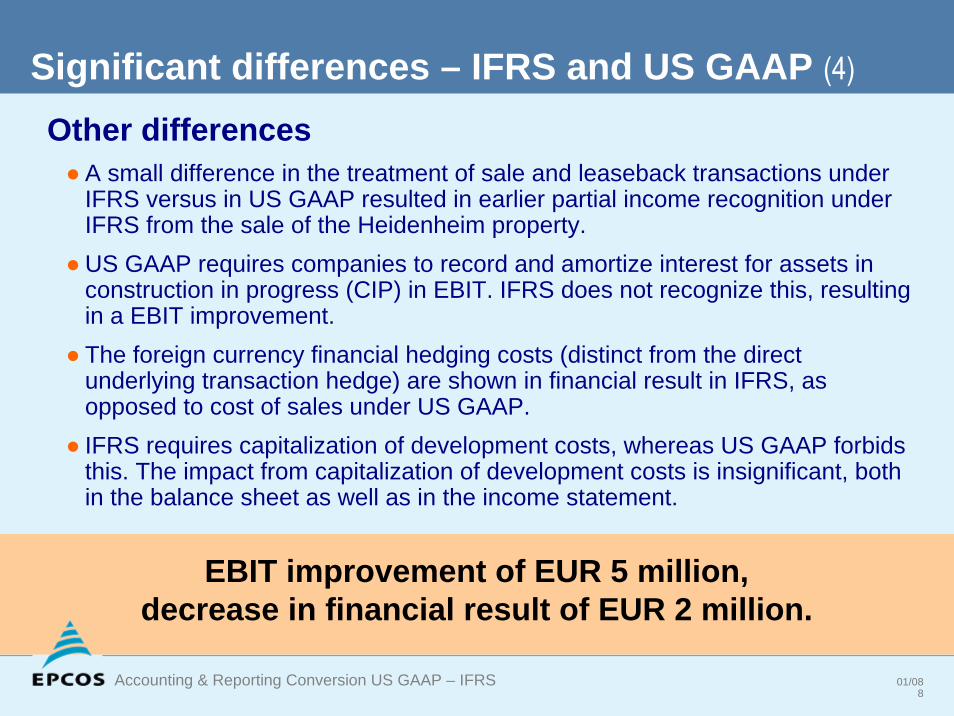

Other differences● A small difference in the treatment of sale and leaseback transactions under

IFRS versus in US GAAP resulted in earlier partial income recognition under IFRS from the sale of the Heidenheim property.

● US GAAP requires companies to record and amortize interest for assets in construction in progress (CIP) in EBIT. IFRS does not recognize this, resulting in a EBIT improvement.

● The foreign currency financial hedging costs (distinct from the direct underlying transaction hedge) are shown in financial result in IFRS, as opposed to cost of sales under US GAAP.

● IFRS requires capitalization of development costs, whereas US GAAP forbids this. The impact from capitalization of development costs is insignificant, both in the balance sheet as well as in the income statement.

EBIT improvement of EUR 5 million,decrease in financial result of EUR 2 million.

01/089

Accounting & Reporting Conversion US GAAP – IFRS

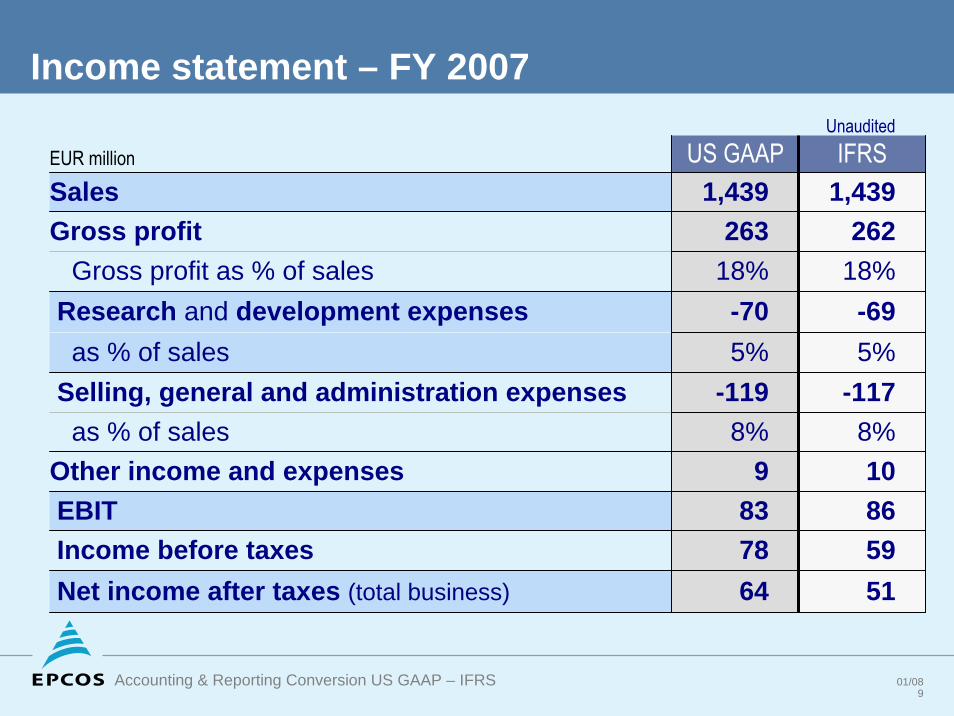

Income statement – FY 2007

EUR million US GAAP IFRSSales 1,439Gross profit 263 262

Other income and expenses 9 10

Gross profit as % of sales 18% 18%Research and development expenses -70 -69as % of sales 5% 5%

Selling, general and administration expenses -119 -117as % of sales 8% 8%

837864

1,439

EBIT 86Income before taxes 59Net income after taxes (total business) 51

Unaudited

01/0810

Accounting & Reporting Conversion US GAAP – IFRS

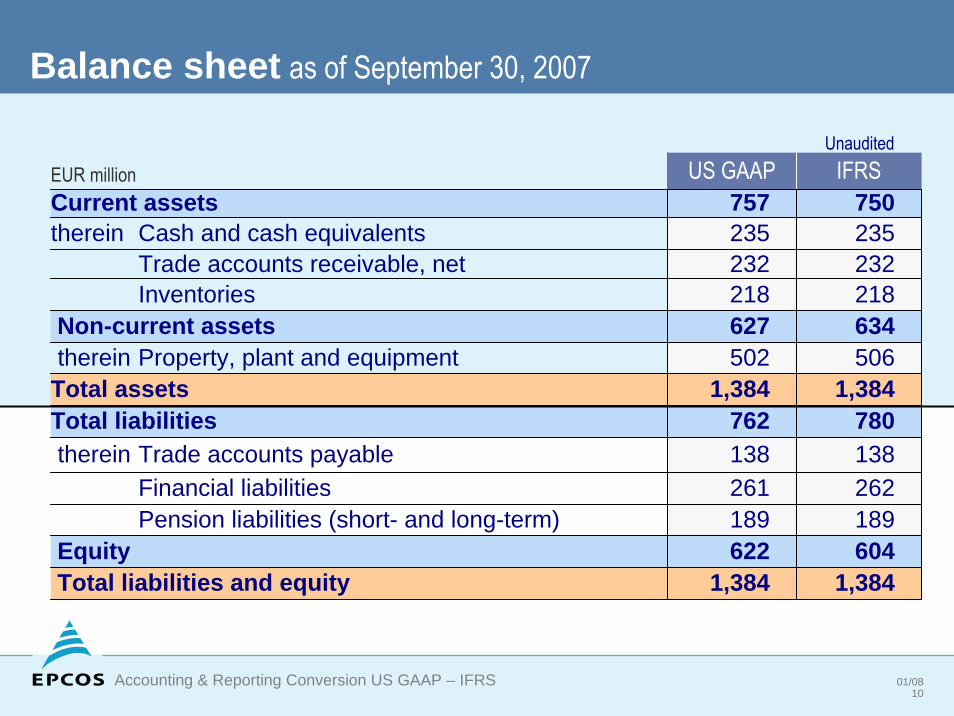

EUR million US GAAP IFRSCurrent assets 757 750therein Cash and cash equivalents 235 235

Trade accounts receivable, net 232 232Inventories 218 218

Non-current assets 627 634therein Property, plant and equipment 502 506

Total assets 1,384 1,384Total liabilities 762 780therein Trade accounts payable 138 138

Financial liabilities 261 262Pension liabilities (short- and long-term) 189 189

Equity 622 604Total liabilities and equity 1,384 1,384

Balance sheet as of September 30, 2007

Unaudited

01/0811

Accounting & Reporting Conversion US GAAP – IFRS

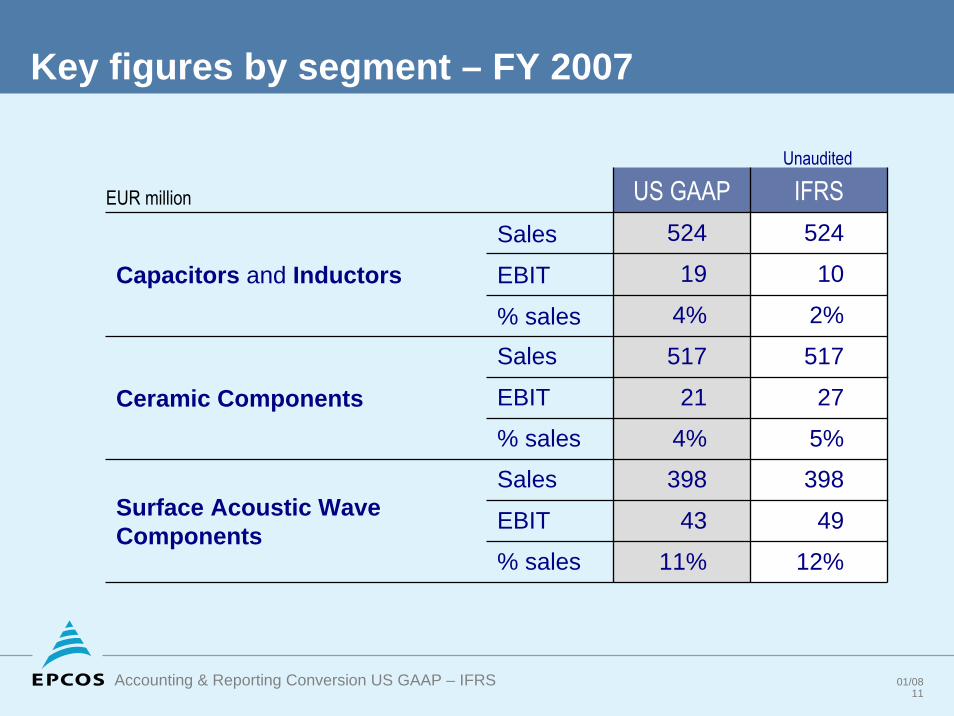

Key figures by segment – FY 2007

EUR million US GAAP IFRSSales 524 524

EBIT 19 10

% sales 4% 2%

Sales 517 517

Sales 398 398

EBIT 43 49Surface Acoustic Wave Components

% sales 11% 12%

EBIT 21 27Ceramic Components% sales 4% 5%

Capacitors and Inductors

Unaudited