actg 4310 contemporary cost/managerial practices

TRANSCRIPT

ACTG 4310

Contemporary Cost/Managerial Practices

Contemporary Topics in Cost and Managerial Accounting

• Lean Accounting• Sustainability Reporting• Intellectual Capital Management• Knowledge Management• Global Business Services• Customer Value Management

Lean Accounting

• Lean Manufacturing– A management strategy that requires everyone in the

value stream to have one common vision for the company of reducing waste, resulting in improvements in quality and production/service time as well as reduction in costs.

• Continuous improvement is emphasized• Customers are the main focus• Pioneered by Toyota in the 1950s

Contemporary Lean Accounting

• The objective is to eliminate waste, free up capacity, speed up the process, eliminate errors and defects, and make the process clear and understandable.

• Fundamentally change the accounting control, and measurement processes so they motivate lean change and improvement, provide information that is suitable for control and decision-making, provide an understanding of customer value, correctly assess the financial impact of lean improvement, and are themselves, simple, visual, and low-waste.

Lean Accounting

• Key tool in Lean Accounting – Value Stream Costing– Direct costing by value streams– Typically collected weekly – Little or no allocation of “overheads”.– Provides financial information that can be clearly

understood by everybody in the value stream which in turn • Leads to good decisions• Motivates employees to improve across the entire value

stream• Assigns clear accountability for cost and profitability

Value Stream Costing

• Weekly reporting provides excellent control and management of costs because they can be reviewed by the value stream manager while the information is still current.

• Modify chart-of-accounts structure to value stream groupings rather than by traditional departments.

Watlow Electric

• Replaced month-end variance reports with daily operator generated reporting

• Has been very satisfied with lean accounting

• Attributes 15% increase in sales and sales margins to lean accounting

Sustainability

• The new buzz word for social/environmental accounting.

• Puts dollars to the social/environmental accounting agenda.

• Focuses on doing the right thing for employees, consumers, society and the government.

• Incorporates profits into doing the right thing.

Triple Bottom Line (TPL or 3BL)

• Created by John Elkington in 1994• Triple Bottom Line accounting means

expanding the traditional reporting framework to take into account ecological and social performance in addition to financial performance –

• People, planet, and profit.

People Bottom Line

• Known as human capital.• It relates beneficial business practices

toward labor, the community and region.• Includes good labor practices, human

rights, and product responsibility.• It also posits that the company should give

part of its profit to the surrounding community in donations.

Planet Bottom Line

• Known as natural capital and includes water, air, energy, waste produced, etc.

• Evaluated by how well a company includes environmental consideration into its activities.

• A company should try to minimize its impact on nature among all its operations.

Profit Bottom Line

• The organizational economic impact on the environment.

• Can include traditional financial measures.• Refers to an “honest” profit, frowning upon

excessive profits with excessive job losses.• It must be made in agreement with the other

two bottom lines.• 3BL views people, plant and profits together,

not separately, as opportunities for the better.

Financial Examples

• 73% of the Top 100 U.S. Companies issued stand-alone Sustainability Reports in 2008

• Examples of companies:– Johnson & Johnson (began reporting in 1993 –

declared IMA leader in sustainability reporting)– FedEx– WalMart – Pepsico

Environmental Cost Calculators

• Carbon Footprint Calculator – www.carbonfootprint.com• Nature Conservancy carbon footprint -www.nature.org• Terrapass calculator for travel emissions-www.terrapass.com• EPA – individual emissions, household emissions –

epa.gov/climatechange/emissions/ind_calculator.html • PG&E – Climate Change –

www.pge.com/myhome/environment/calculator • Berkeley Institute of the Environment -coolclimate.berkeley.edu

• Paul Hawken, environmental activist and founder of Smith and Hawken, estimates that 1 -2 million organizations worldwide are actively doing something to implement sustainability.

Management Control

• Management accounting can play a role in implementing corporate sustainability in the following areas:– Budgeting– Capital investments– Life cycle costing– Responsibility accounting– Performance evaluation/reward systems– Balanced scorecard applications

Intellectual Capital Management

Facts

• We are a knowledge-based economy– In the 1980s, about 60% of assets were

tangible assets like property, plant and equipment.

– Currently, only 10% - 50% of a company’s assets are tangible.

– Most of the value of a business comes from their intellectual capital.

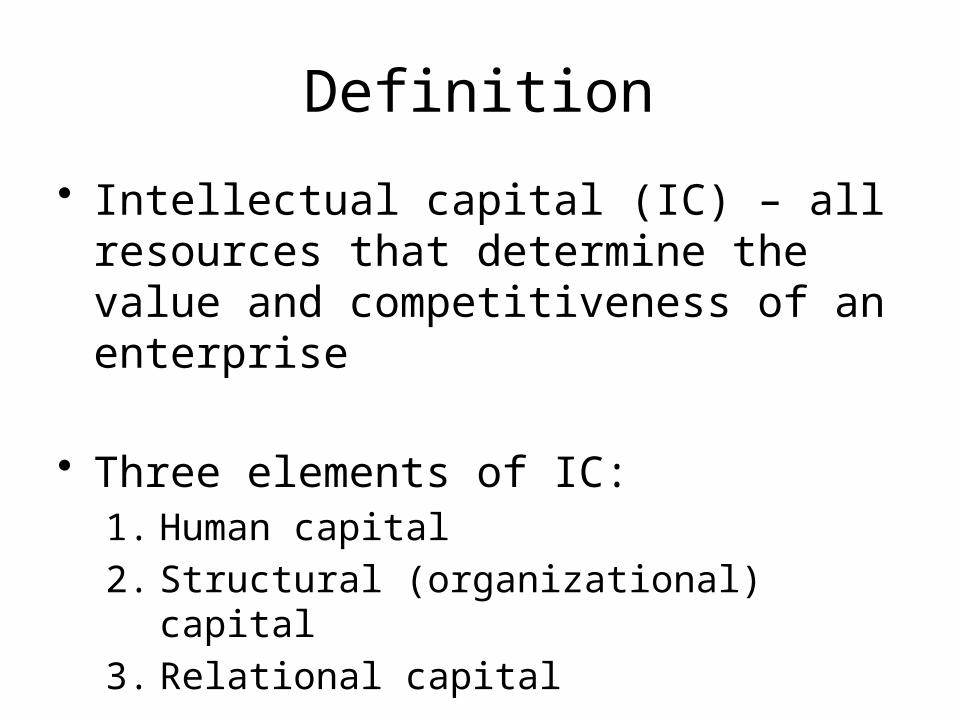

Definition

• Intellectual capital (IC) – all resources that determine the value and competitiveness of an enterprise

• Three elements of IC:1. Human capital

2. Structural (organizational) capital

3. Relational capital

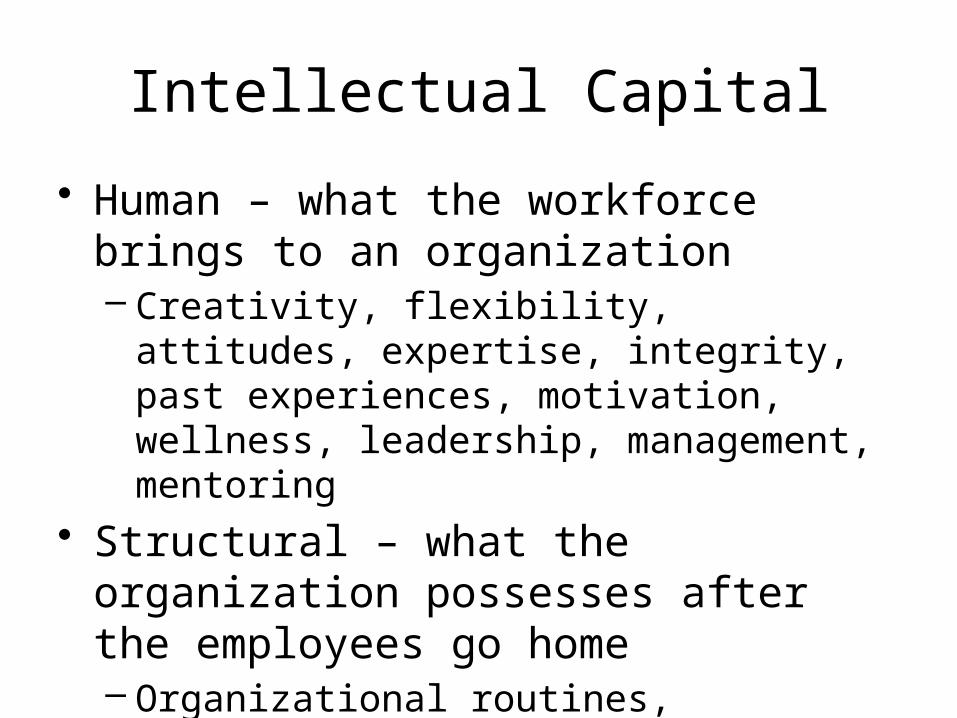

Intellectual Capital

• Human – what the workforce brings to an organization– Creativity, flexibility, attitudes, expertise,

integrity, past experiences, motivation, wellness, leadership, management, mentoring

• Structural – what the organization possesses after the employees go home– Organizational routines, procedures, manuals,

strategies, systems, databases, corporate cultures

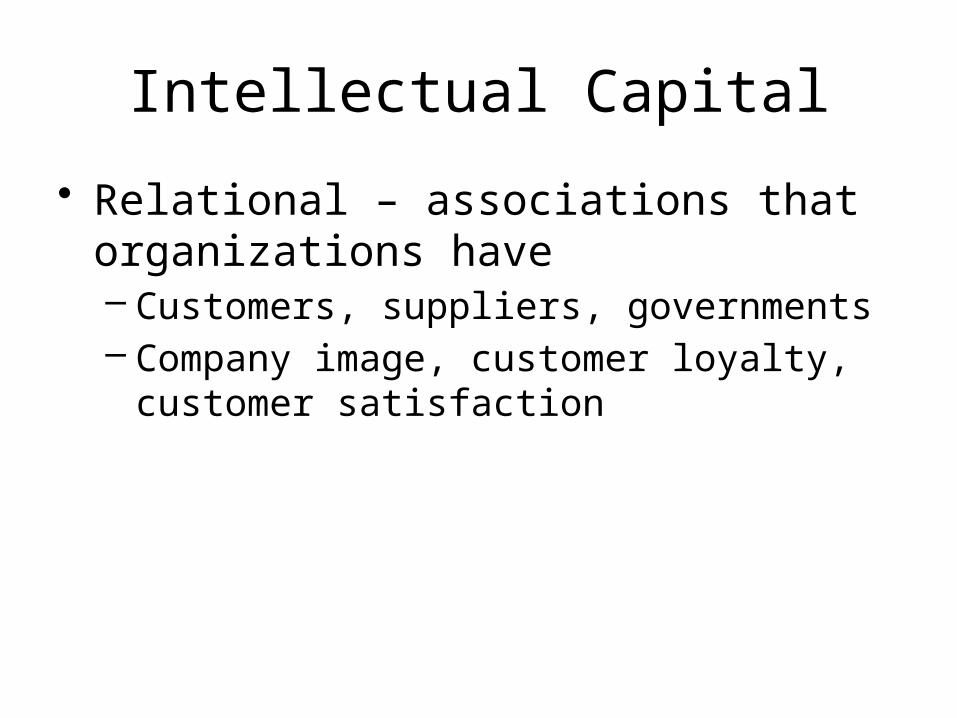

Intellectual Capital

• Relational – associations that organizations have– Customers, suppliers, governments– Company image, customer loyalty, customer

satisfaction

Knowledge Management (KM)

Definition

• The process through which organizations generate value from their intellectual and knowledge-based assets

• Knowledge – Can be described as the awareness of what

one knows through study, reasoning, experience or association, or through various types of learning.

– Should not be confused with data or information

– Is a process and is always changing

Knowledge Management

• KM is a procedure used to identify, create, represent, and distribute the explicit and tacit knowledge of individuals in the organization.

• Tools – information technology and training for:– Determining “Best Practices”– Sharing of lessons learned– Continuous improvement of the organization

Global Business Services (Shared Services)

Global Business Services (GBS)

• Are essentially shared business services where– a service is controlled by one part of an organization – the funding and resourcing of the services is funded by all

the other departments– creating an internal service provider for the entire

organization. • Is used by companies with multiple geographic

locations• IMPORTANT TO NOTE

– GBS is not OUTSOURCING because with outsourcing a third party external vendor provides the service whereas GBS are kept in the company.

Functional Aspects of GBS

1. More controllership of functions

2. Flexibility with operationsa) All sectors and departments within an organization

(sales, marketing, finance, human resources, etc.) can be included

3. Reduces need for redundant accounting operations

Customer Value Management (CVM)

Customer Value Management (CVM)

• Managing each customer relationship with the goal of achieving maximum lifetime profit from the entire customer base.

• Two basic goals:1. Deliver superior value to targeted market

segments.

2. Receive an equitable return on the value delivered.

Importance of CVM

• Current Economy:– A company’s ability to attract and retain

customers has been a key component of success. In the current economic downturn, customers have become a scarce resource to some companies.

– It is cheaper to keep a customer than to get a new one. This has caused many organizations to move towards becoming more customer-oriented and less product/service-oriented.

Customer’s Lifetime Value (LTV)

• LTV = Purchase size X Frequency X

Duration

• Goal is to increase each part of the equation

Strategies

• For profitable customers– Offer price incentives and discounts– Provide customized support– Offer customer rewards programs

• For less profitable and non-profitable customers:– Charge additional fees for services– Increase prices or reduce costs to the

customer– Eliminate relationships

Customer Retention

• It is important to keep profitable customers• It is also important to keep customers that

are not as profitable but tend to be loyal over time (LTV).

• The goal is to maintain the most valuable customers, NOT ALL OF YOUR CUSTOMERS.

• Loyal customers are more profitable because they are less price sensitive than others.

Conclusion• Lean Accounting – quicker response time that

adds value• Sustainability – do the right thing and let

everyone know about it!• Intellectual Capital Management – Find excellent

employees and keep them!• Knowledge Management – Determine best

company practices and share them throughout the company

Conclusion

• Global Business Services – consider combining services throughout your organization to save money and be consistent

• Customer Value Management – Maximize the lifetime values of our customers.

• ALL OF THESE TOOLS CAN HELP YOU CHANGE AND IMPROVE THE MANAGEMENT OF YOUR COMPANY!!!!