additive manufacturing meets the financial · pdf fileadditive manufacturing meets the...

TRANSCRIPT

Additive Manufacturing Meets the Financial

Markets

The Challenge for the Lasers & Photonics Sector:

Value Creation Opportunities In Additive

Lasers & Photonics Marketplace Seminar February

9, 2015 John Dexheimer

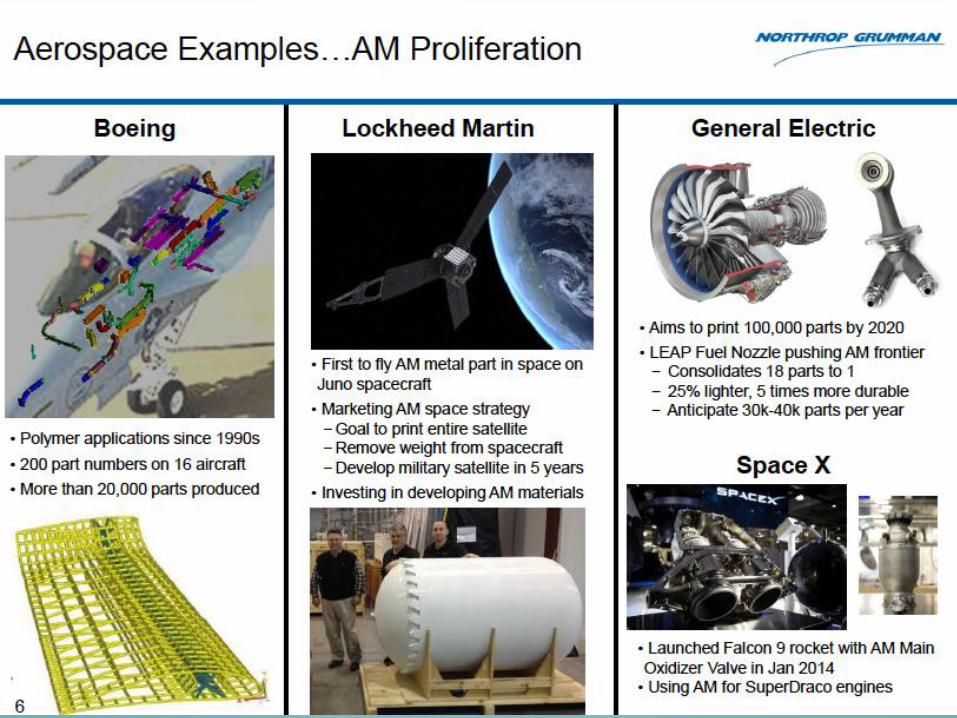

Why Additive Matters

“Eli Whitney’s standardized interchangeable parts came in the 1800s,

Henry Ford and the assembly line in 1910s,

Taylor and time and motion studies in the 1920s and 1930s,

Taiichi Ono and lean manufacturing in the 1950s.

You have those things happen every few decades that really change the way

we think about manufacturing.

~ That’s what I think additive manufacturing could be; not just a tool, but

part of a new way to think about manufacturing itself that’s sometimes

called distributed manufacturing “

~Mark Bunger, Lux Research

Manufacturing Above & Beyond Current Methods i.e.--Uber

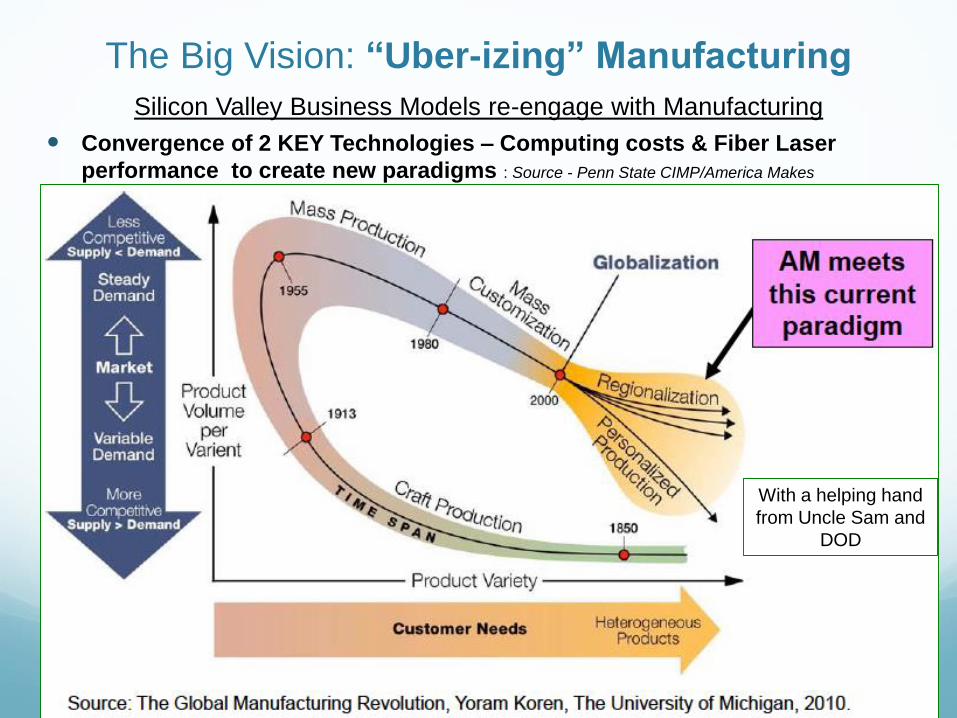

The Big Vision: “Uber-izing” Manufacturing

Silicon Valley Business Models re-engage with Manufacturing

Convergence of 2 KEY Technologies – Computing costs & Fiber Laser

performance to create new paradigms : Source - Penn State CIMP/America Makes

With a helping hand

from Uncle Sam and

DOD

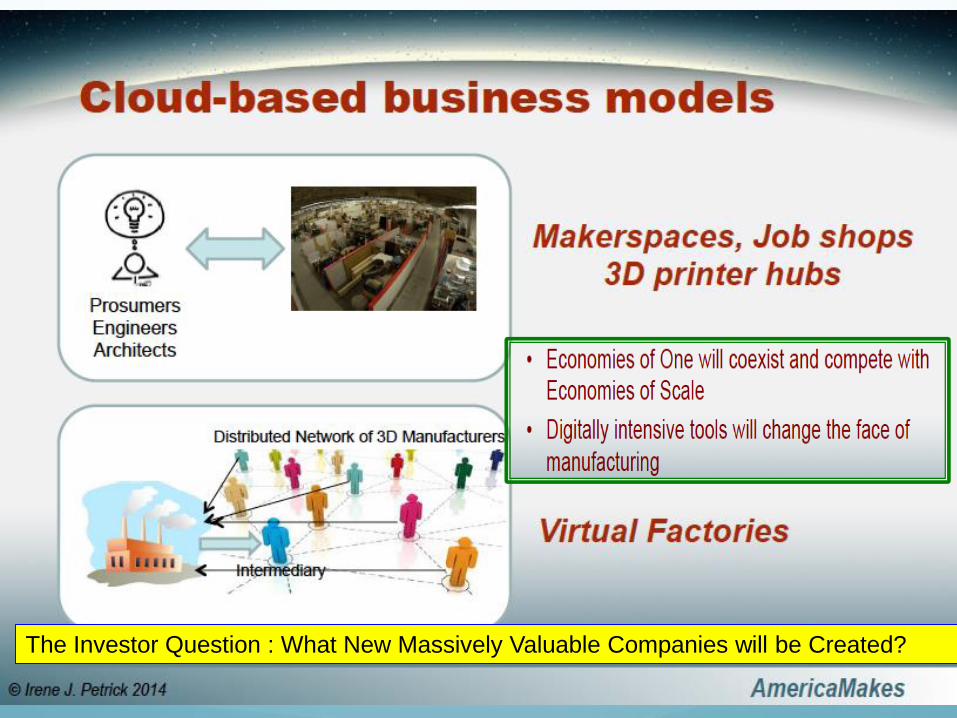

The Investor Question : What New Massively Valuable Companies will be Created?

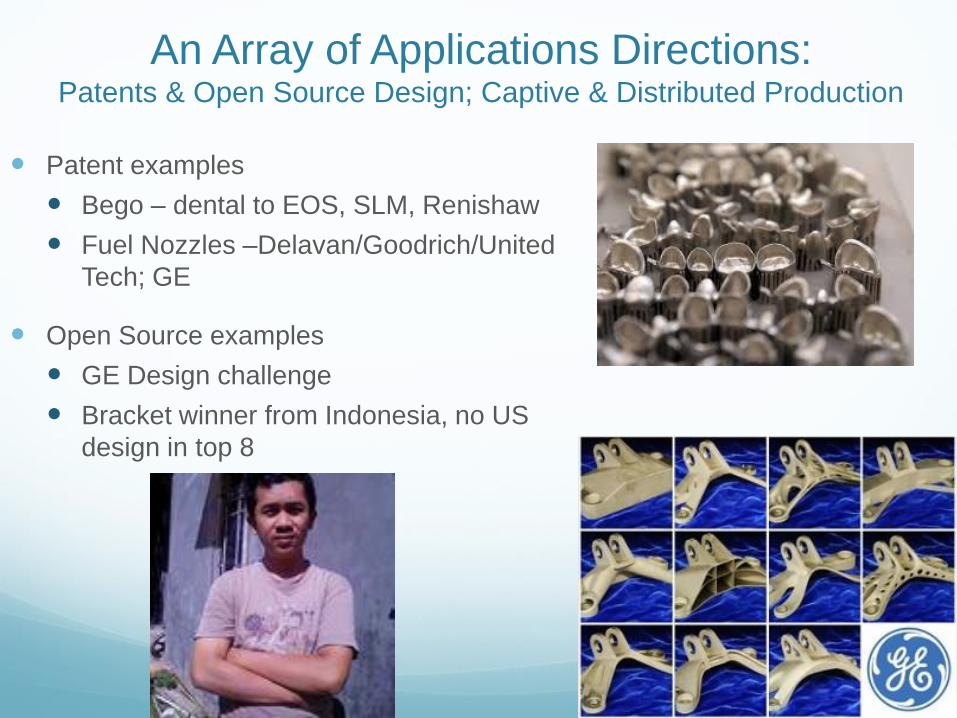

An Array of Applications Directions: Patents & Open Source Design; Captive & Distributed Production

Patent examples

Bego – dental to EOS, SLM, Renishaw

Fuel Nozzles –Delavan/Goodrich/United

Tech; GE

Open Source examples

GE Design challenge

Bracket winner from Indonesia, no US

design in top 8

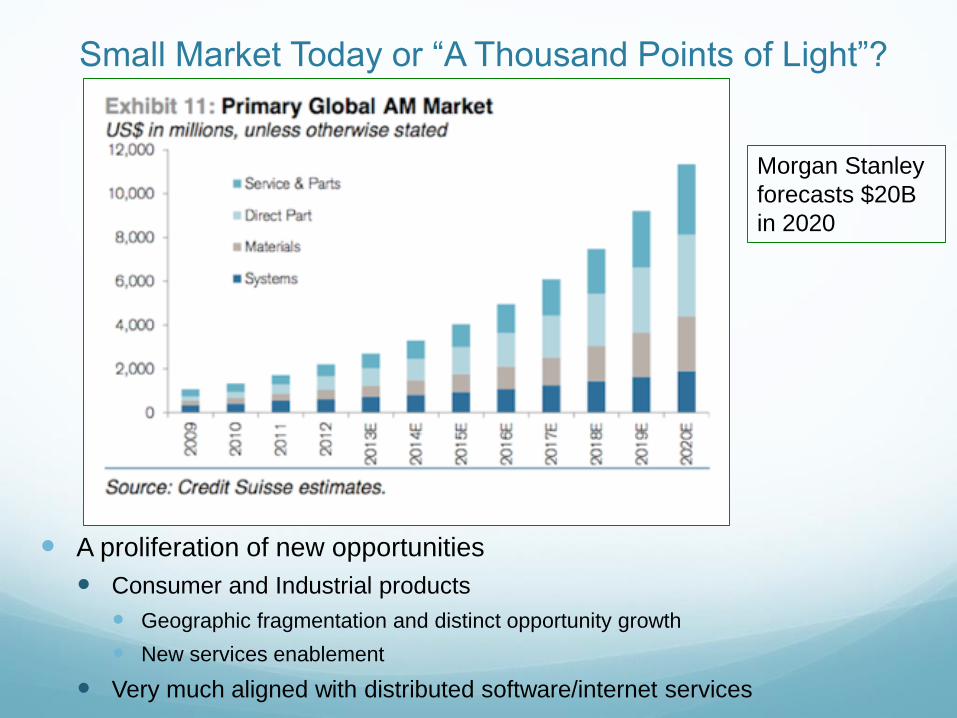

Small Market Today or “A Thousand Points of Light”?

A proliferation of new opportunities

Consumer and Industrial products

Geographic fragmentation and distinct opportunity growth

New services enablement

Very much aligned with distributed software/internet services

Morgan Stanley

forecasts $20B

in 2020

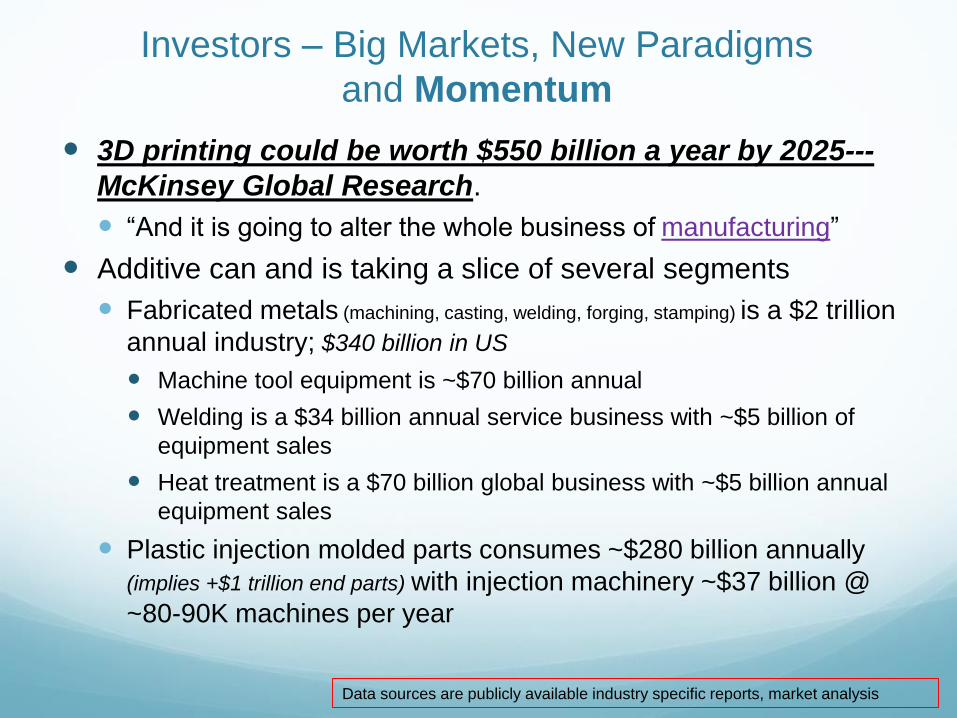

Investors – Big Markets, New Paradigms

and Momentum

3D printing could be worth $550 billion a year by 2025---

McKinsey Global Research.

“And it is going to alter the whole business of manufacturing”

Additive can and is taking a slice of several segments

Fabricated metals (machining, casting, welding, forging, stamping) is a $2 trillion

annual industry; $340 billion in US

Machine tool equipment is ~$70 billion annual

Welding is a $34 billion annual service business with ~$5 billion of

equipment sales

Heat treatment is a $70 billion global business with ~$5 billion annual

equipment sales

Plastic injection molded parts consumes ~$280 billion annually

(implies +$1 trillion end parts) with injection machinery ~$37 billion @

~80-90K machines per year

Data sources are publicly available industry specific reports, market analysis

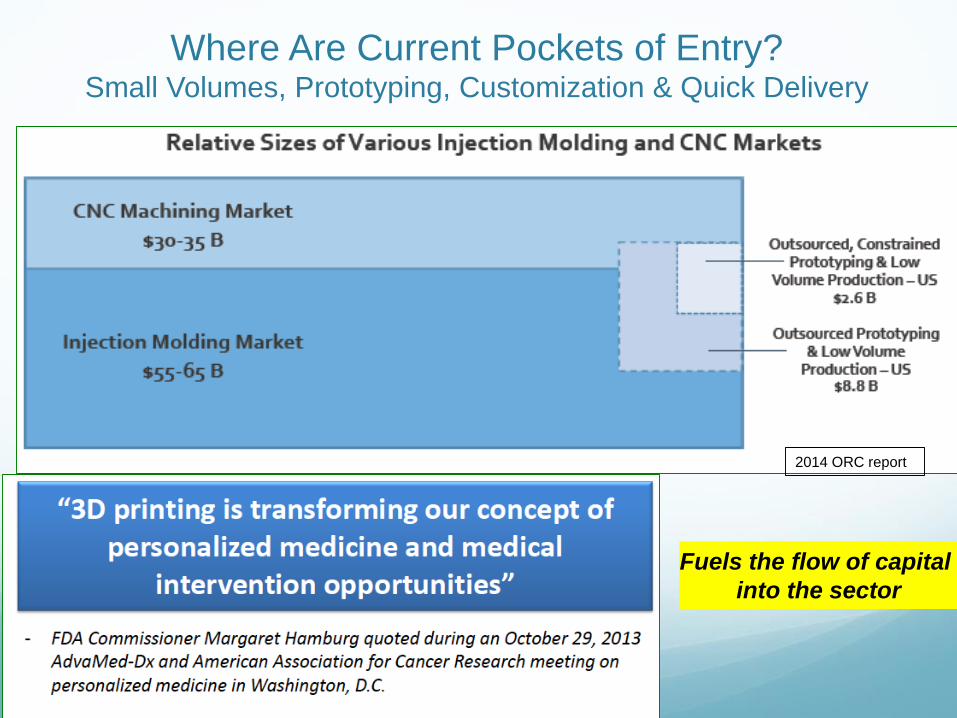

Where Are Current Pockets of Entry?Small Volumes, Prototyping, Customization & Quick Delivery

2014 ORC report

Fuels the flow of capital

into the sector

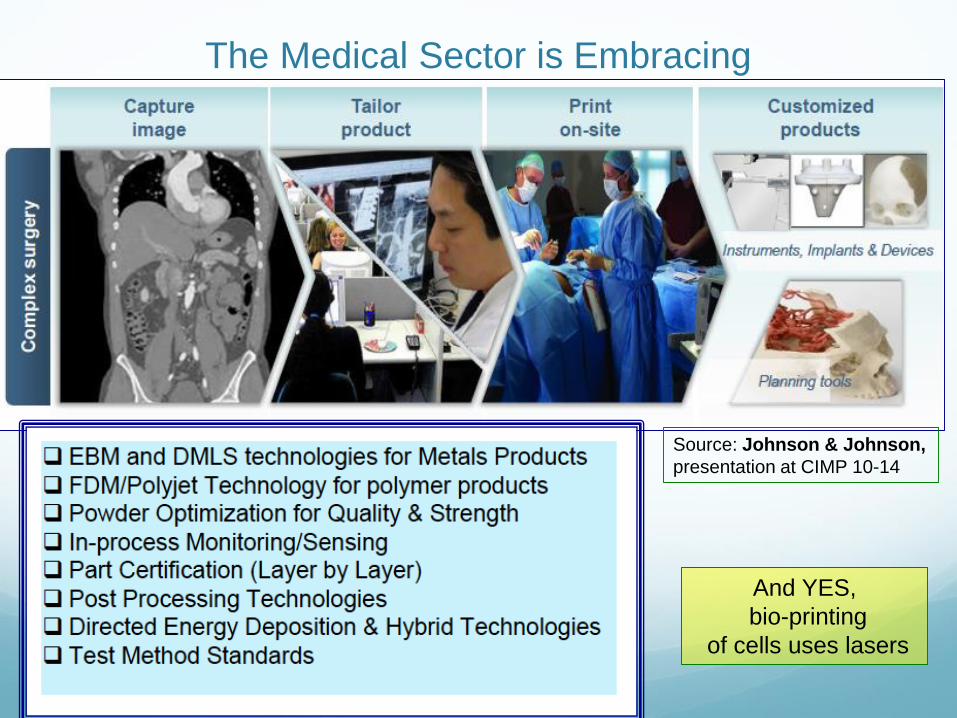

The Medical Sector is Embracing

Source: Johnson & Johnson,

presentation at CIMP 10-14

And YES,

bio-printing

of cells uses lasers

Patents

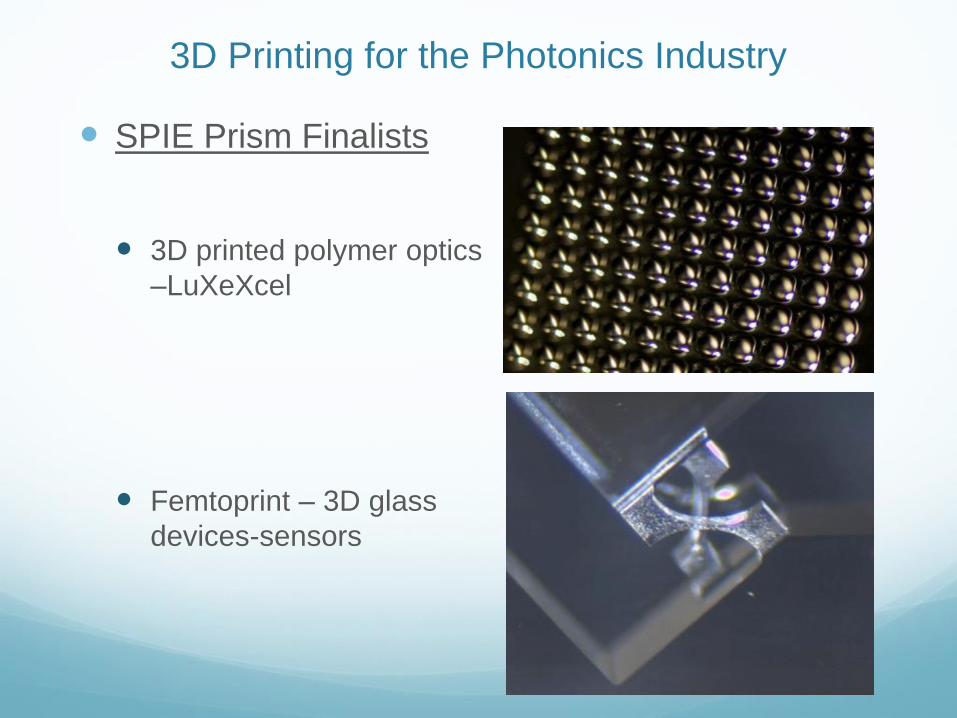

3D Printing for the Photonics Industry

SPIE Prism Finalists

3D printed polymer optics

–LuXeXcel

Femtoprint – 3D glass

devices-sensors

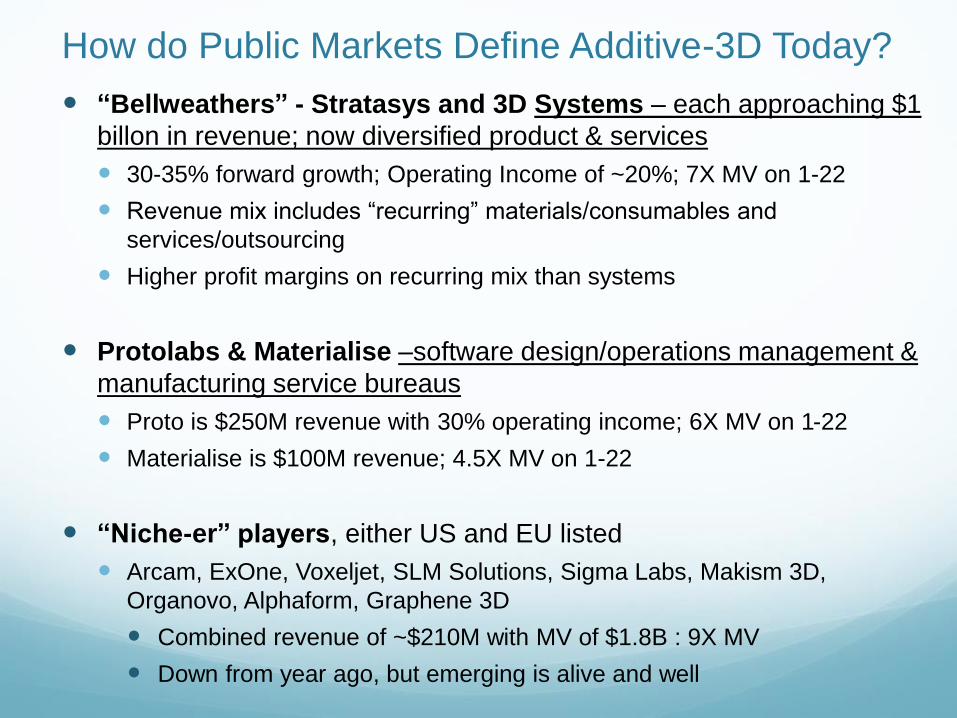

How do Public Markets Define Additive-3D Today?

“Bellweathers” - Stratasys and 3D Systems – each approaching $1

billon in revenue; now diversified product & services

30-35% forward growth; Operating Income of ~20%; 7X MV on 1-22

Revenue mix includes “recurring” materials/consumables and

services/outsourcing

Higher profit margins on recurring mix than systems

Protolabs & Materialise –software design/operations management &

manufacturing service bureaus

Proto is $250M revenue with 30% operating income; 6X MV on 1-22

Materialise is $100M revenue; 4.5X MV on 1-22

“Niche-er” players, either US and EU listed

Arcam, ExOne, Voxeljet, SLM Solutions, Sigma Labs, Makism 3D,

Organovo, Alphaform, Graphene 3D

Combined revenue of ~$210M with MV of $1.8B : 9X MV

Down from year ago, but emerging is alive and well

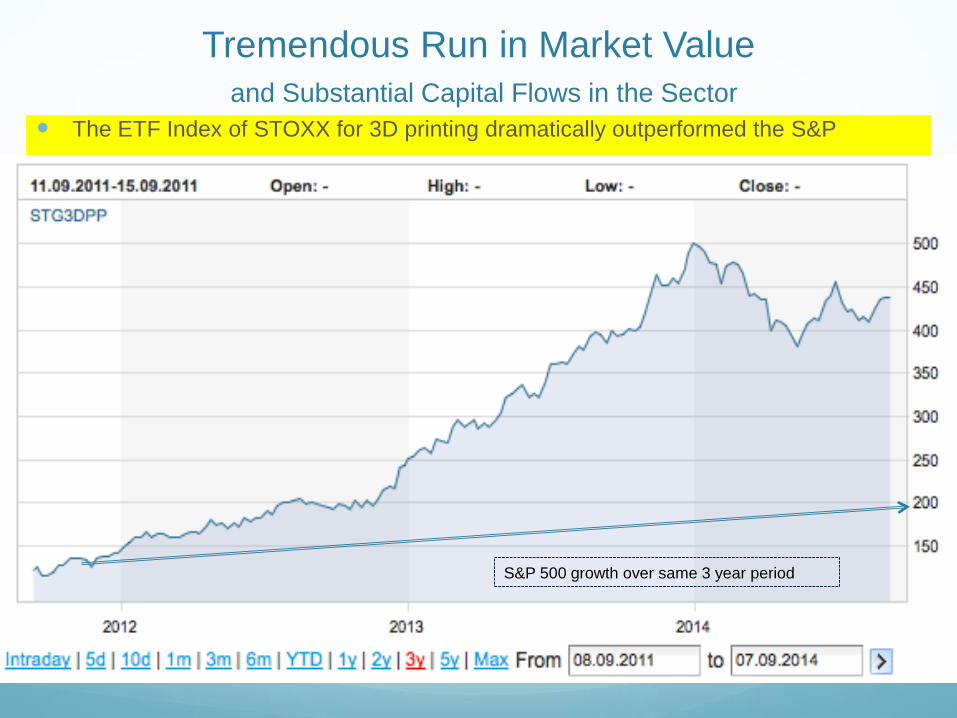

Tremendous Run in Market Value

and Substantial Capital Flows in the Sector

The ETF Index of STOXX for 3D printing dramatically outperformed the S&P

S&P 500 growth over same 3 year period

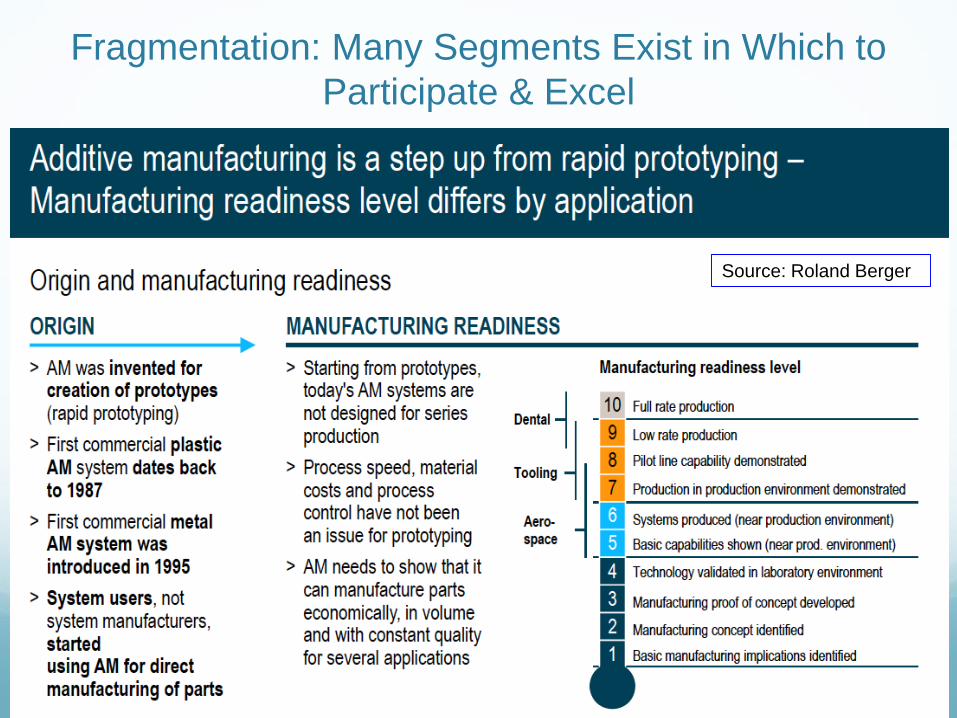

Fragmentation: Many Segments Exist in Which to

Participate & Excel

Source: Roland Berger

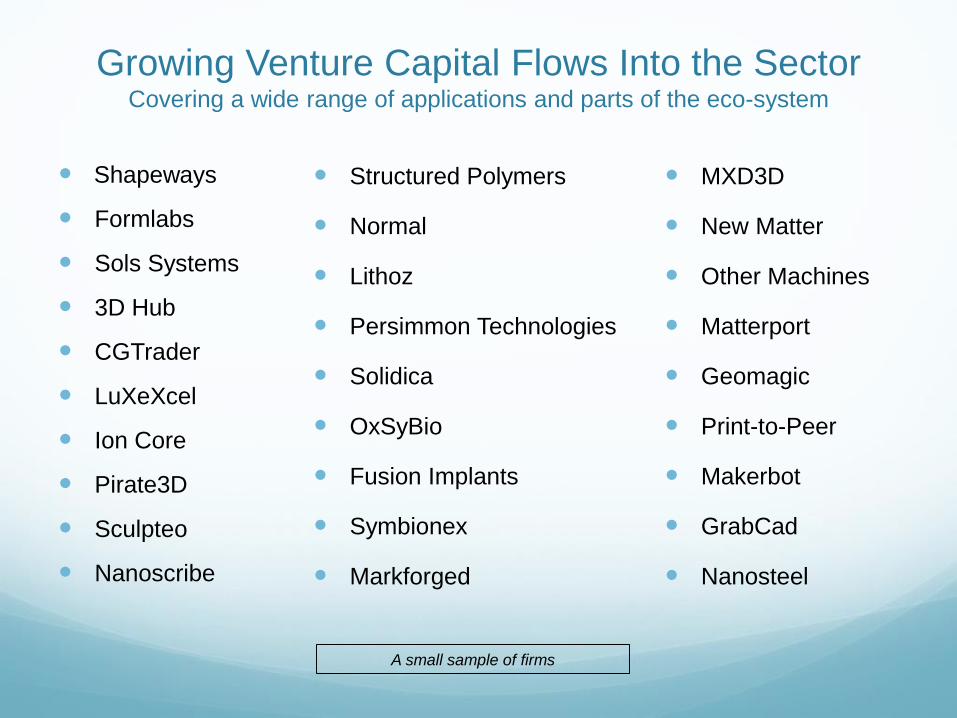

Growing Venture Capital Flows Into the SectorCovering a wide range of applications and parts of the eco-system

Shapeways

Formlabs

Sols Systems

3D Hub

CGTrader

LuXeXcel

Ion Core

Pirate3D

Sculpteo

Nanoscribe

Structured Polymers

Normal

Lithoz

Persimmon Technologies

Solidica

OxSyBio

Fusion Implants

Symbionex

Markforged

A small sample of firms

MXD3D

New Matter

Other Machines

Matterport

Geomagic

Print-to-Peer

Makerbot

GrabCad

Nanosteel

A Long Gestation to Get Stock Traction

- with High Volatility as Typical

At the peaks, both Stratasys & 3D

had market caps over $9 billion –each more than IPG, COHR, NEWP and

RSTI combined peaks of the past 5 years

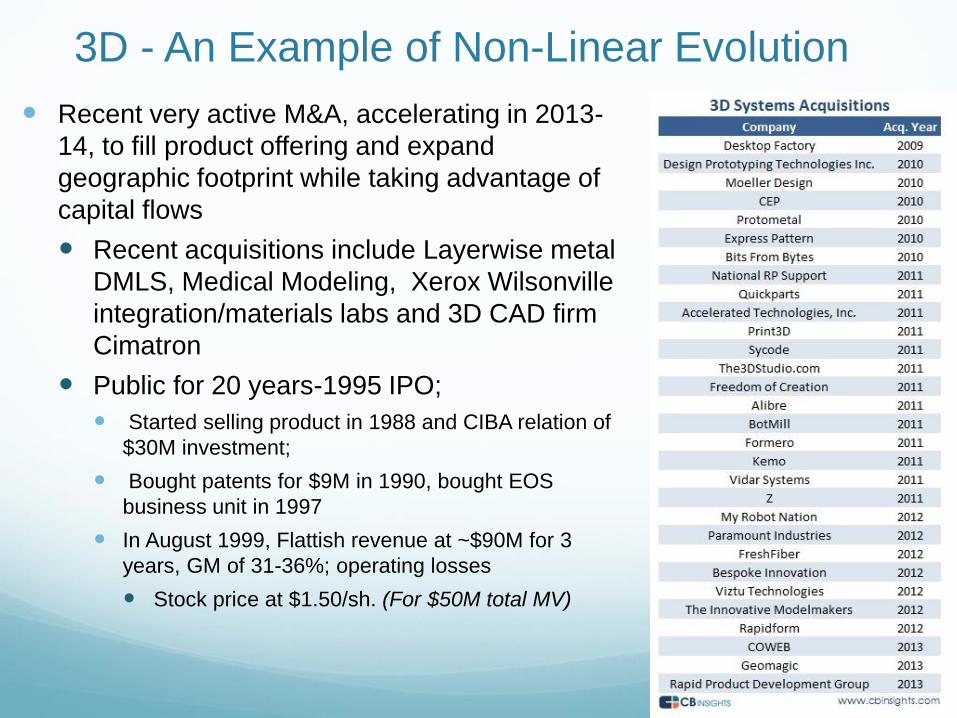

3D - An Example of Non-Linear Evolution

Recent very active M&A, accelerating in 2013-

14, to fill product offering and expand

geographic footprint while taking advantage of

capital flows

Recent acquisitions include Layerwise metal

DMLS, Medical Modeling, Xerox Wilsonville

integration/materials labs and 3D CAD firm

Cimatron

Public for 20 years-1995 IPO;

Started selling product in 1988 and CIBA relation of

$30M investment;

Bought patents for $9M in 1990, bought EOS

business unit in 1997

In August 1999, Flattish revenue at ~$90M for 3

years, GM of 31-36%; operating losses

Stock price at $1.50/sh. (For $50M total MV)

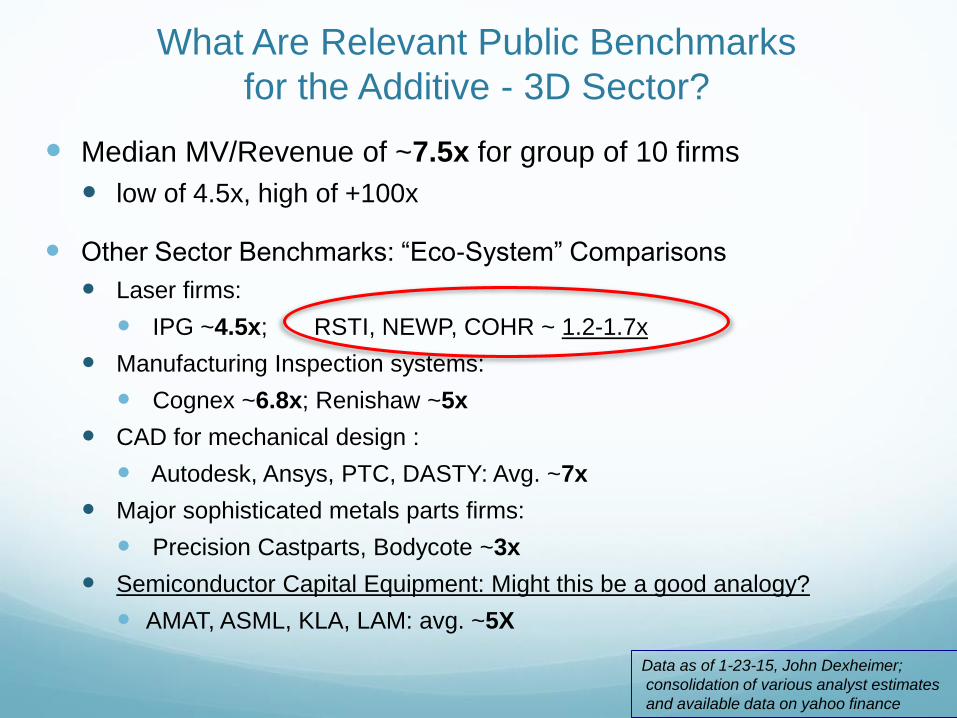

What Are Relevant Public Benchmarks

for the Additive - 3D Sector?

Median MV/Revenue of ~7.5x for group of 10 firms

low of 4.5x, high of +100x

Other Sector Benchmarks: “Eco-System” Comparisons

Laser firms:

IPG ~4.5x; RSTI, NEWP, COHR ~ 1.2-1.7x

Manufacturing Inspection systems:

Cognex ~6.8x; Renishaw ~5x

CAD for mechanical design :

Autodesk, Ansys, PTC, DASTY: Avg. ~7x

Major sophisticated metals parts firms:

Precision Castparts, Bodycote ~3x

Semiconductor Capital Equipment: Might this be a good analogy?

AMAT, ASML, KLA, LAM: avg. ~5X

Data as of 1-23-15, John Dexheimer;

consolidation of various analyst estimates

and available data on yahoo finance

The End of the Additive Stock Market Run….

…. or Just a Re-Grouping?

Feb.3, 2015 : Shares of Stratasys Ltd. plunged 28 percent Tuesday

a surprise $100 million “goodwill impairment charge”

“new phase of increased investment in its business” because more manufacturers are adopting 3-D printing into their factories.

“The investment plan is designed to implement broad product development and infrastructure which would support annual revenues of $3 billion in 2020,”

“raise its capital expenditures for 2015 to a range of $160 million to $200 million from about $50 million in 2014.”

“The industrial side of the market is the sweet side.”

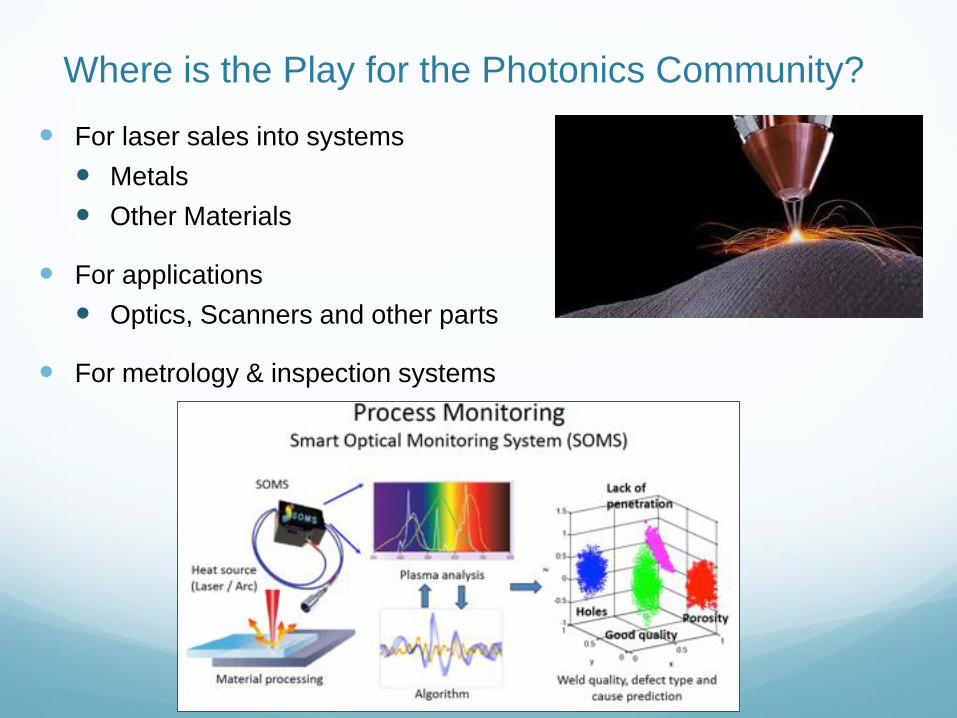

Where is the Play for the Photonics Community?

For laser sales into systems

Metals

Other Materials

For applications

Optics, Scanners and other parts

For metrology & inspection systems

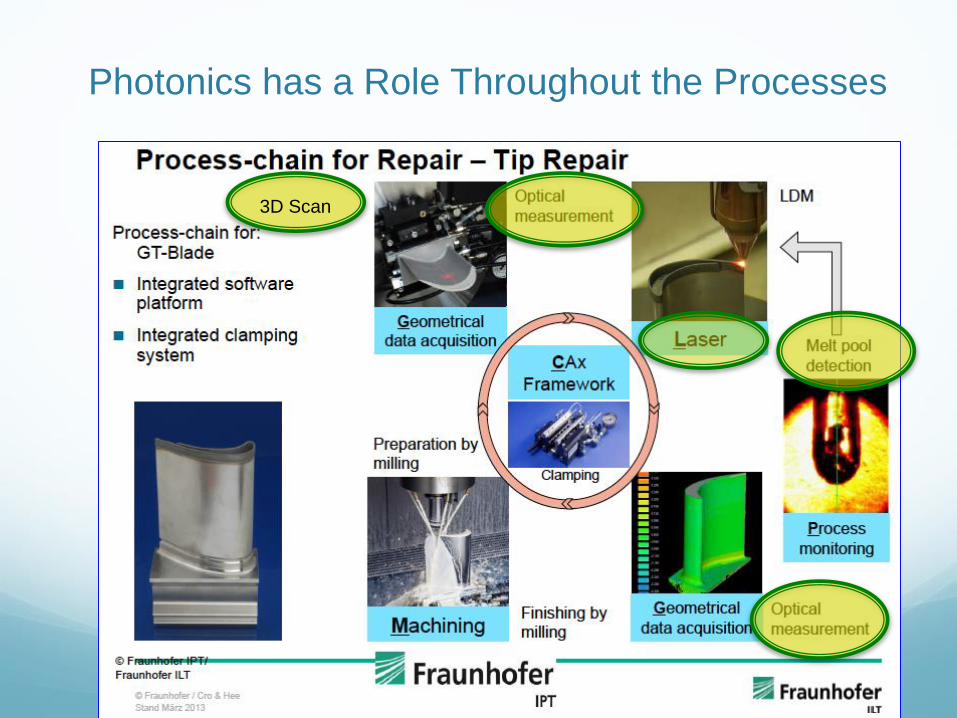

Photonics has a Role Throughout the Processes

3D Scan

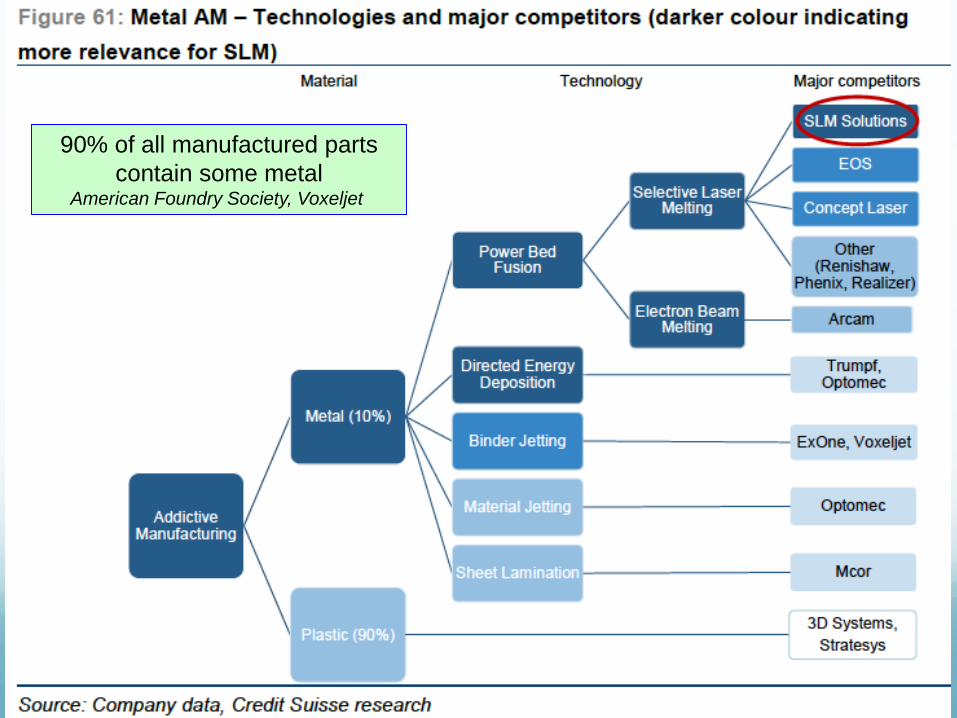

90% of all manufactured parts

contain some metalAmerican Foundry Society, Voxeljet

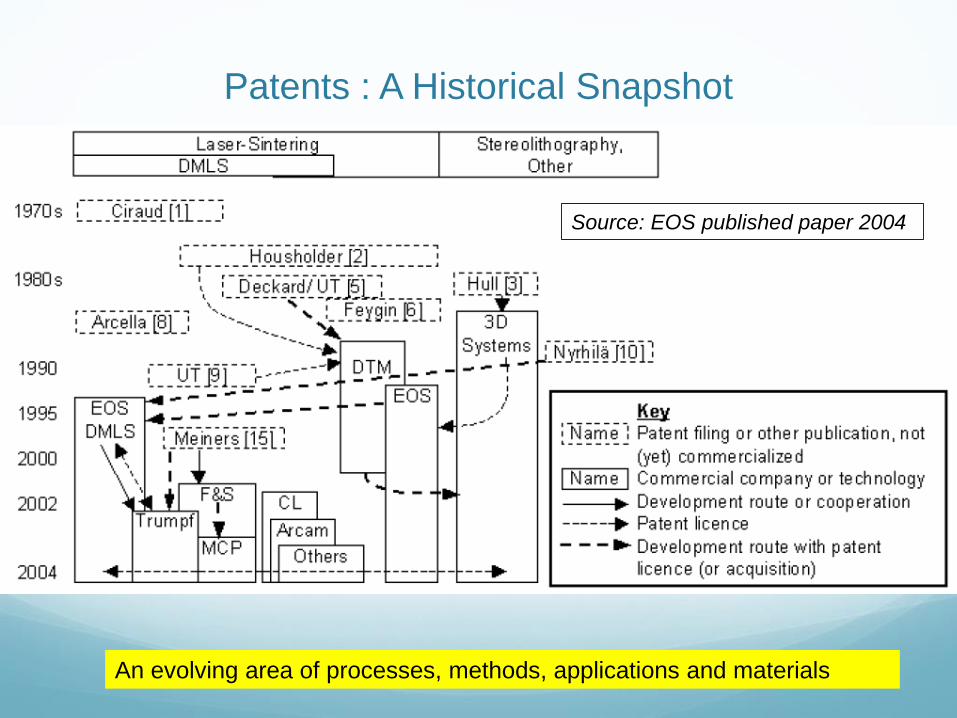

Patents : A Historical Snapshot

Source: EOS published paper 2004

An evolving area of processes, methods, applications and materials

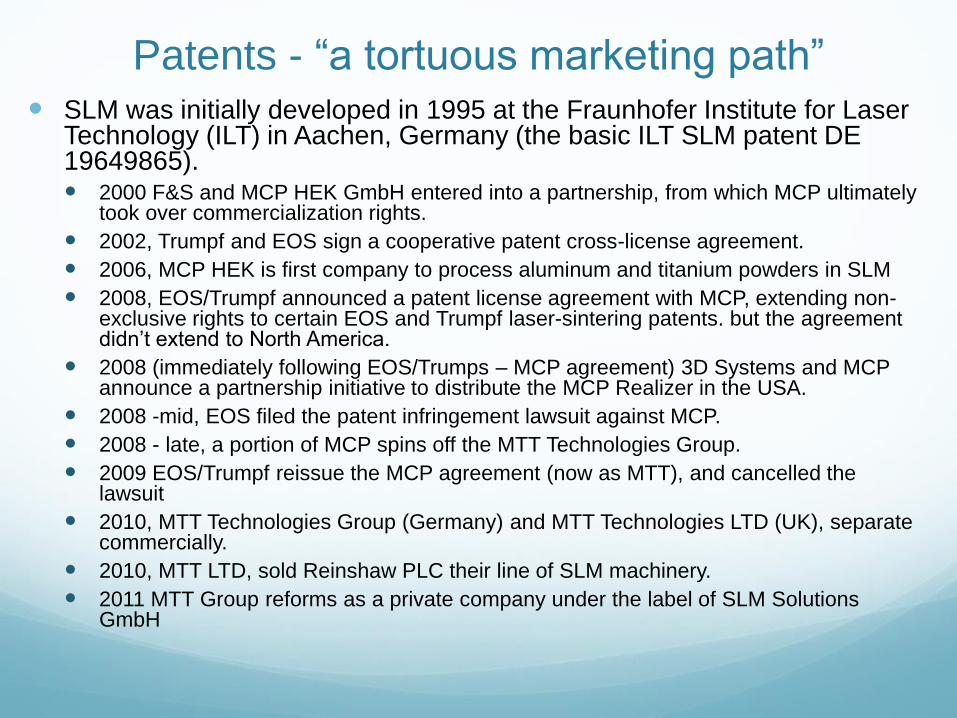

Patents - “a tortuous marketing path” SLM was initially developed in 1995 at the Fraunhofer Institute for Laser

Technology (ILT) in Aachen, Germany (the basic ILT SLM patent DE 19649865). 2000 F&S and MCP HEK GmbH entered into a partnership, from which MCP ultimately

took over commercialization rights.

2002, Trumpf and EOS sign a cooperative patent cross-license agreement.

2006, MCP HEK is first company to process aluminum and titanium powders in SLM

2008, EOS/Trumpf announced a patent license agreement with MCP, extending non-exclusive rights to certain EOS and Trumpf laser-sintering patents. but the agreement didn’t extend to North America.

2008 (immediately following EOS/Trumps – MCP agreement) 3D Systems and MCP announce a partnership initiative to distribute the MCP Realizer in the USA.

2008 -mid, EOS filed the patent infringement lawsuit against MCP.

2008 - late, a portion of MCP spins off the MTT Technologies Group.

2009 EOS/Trumpf reissue the MCP agreement (now as MTT), and cancelled the lawsuit

2010, MTT Technologies Group (Germany) and MTT Technologies LTD (UK), separate commercially.

2010, MTT LTD, sold Reinshaw PLC their line of SLM machinery.

2011 MTT Group reforms as a private company under the label of SLM Solutions GmbH

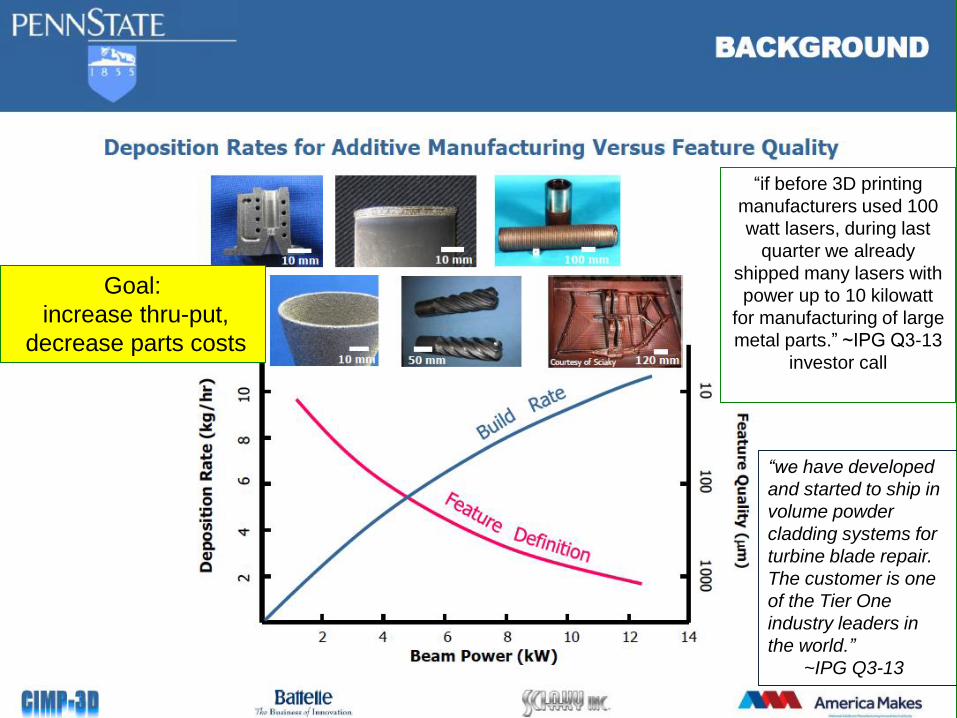

Goal:

increase thru-put,

decrease parts costs

“if before 3D printing

manufacturers used 100

watt lasers, during last

quarter we already

shipped many lasers with

power up to 10 kilowatt

for manufacturing of large

metal parts.” ~IPG Q3-13

investor call

“we have developed

and started to ship in

volume powder

cladding systems for

turbine blade repair.

The customer is one

of the Tier One

industry leaders in

the world.”

~IPG Q3-13

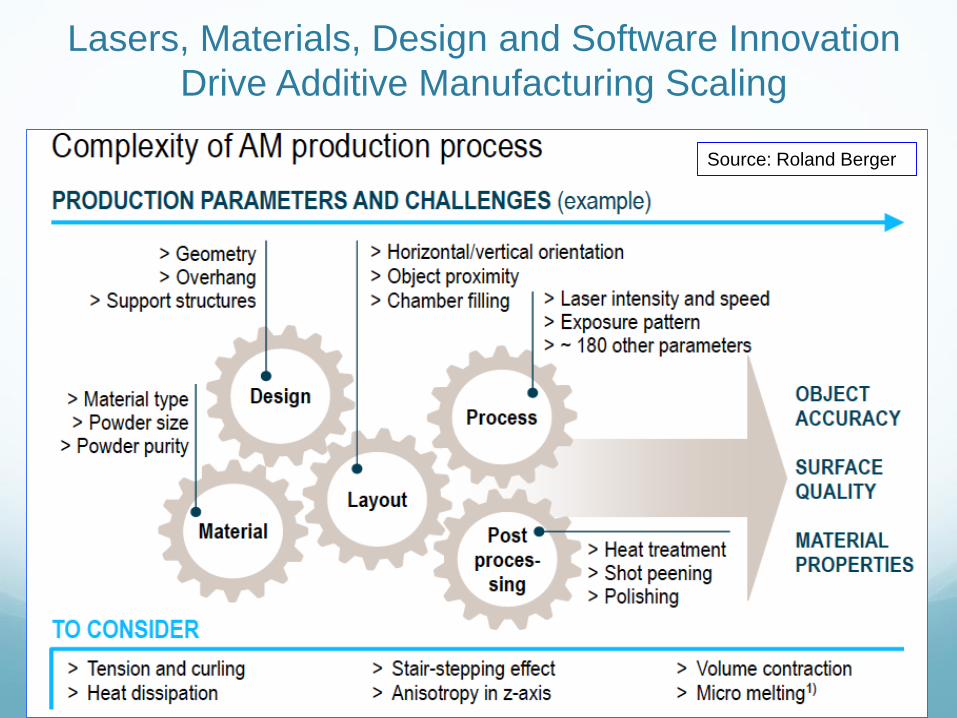

Lasers, Materials, Design and Software Innovation

Drive Additive Manufacturing Scaling

Source: Roland Berger

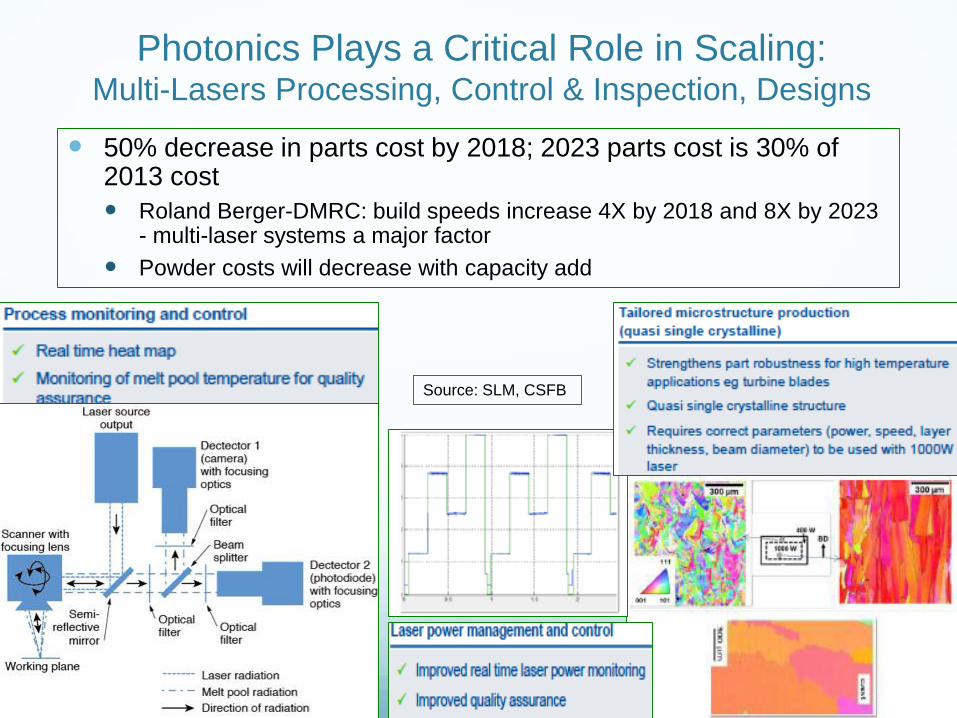

Photonics Plays a Critical Role in Scaling:Multi-Lasers Processing, Control & Inspection, Designs

50% decrease in parts cost by 2018; 2023 parts cost is 30% of 2013 cost

Roland Berger-DMRC: build speeds increase 4X by 2018 and 8X by 2023 - multi-laser systems a major factor

Powder costs will decrease with capacity add

Source: SLM, CSFB

For the Photonics Community:

Is This a Small or Big Opportunity?

OR

Metals Additive – Triangulation of Market Data

1400 installed based at end of 2012 (Codex/CSFB)

68% powder bed; 12% DLS, 10% each binder or material jetting,

EOS 2014 revenue of EU-177M; gr. of 36%, 540 employees

half of 300 machines sold in 2014 were metal; prior installed base of

1500 units is 40/60 metal

Concept Laser – all metal laser based systems; over 200 installed, 100 sold

in 2014 with 130 target in 2014; 500 employees

SLM – all metal; IPO in 2014; 133 installed based at 12-13; 53 orders in

2014 with majority having multi-lasers; CSFB “sandbag” forecast for 90

units sold in 2016 with most 2-4 lasers in each

Optomec 2014 growth of 100%; 150 customers –both metal and aerosol jet

nanomaterials; 25 new customers in Q4-2014

Other laser based players with market share : Trumpf, Renishaw,

3D/Phenix AND new entry by major machine tools firms like DMG-Mori

and Mazak

Metals Additive –More Data & Observations

40.5% annual growth in metals additive from 2014-2020 (Metal working

Magazine 7-14)

Applying 30-40% to 2014 sales of EOS and Concept implies they would sell

1930 to 3200 systems combined in 2020

If the average system has 2-4 lasers that means 6,000-12,000 lasers

consumed by these 2 alone

And competitors will consume more

Powder metal sales for additive are forecast at $520M in 2019 growing

to $930M in 2023 (SmarTech -2014) ; up from $25M in 2012- Deloitte, Wohlers, CSFB

Implies $3-5 Billion in end parts in 2019

And there is more……By many definitions and examples….

………………………. laser cladding & portions of welding is additive

Metals appears to be a much bigger & strategic market opportunity

than many have projected to date

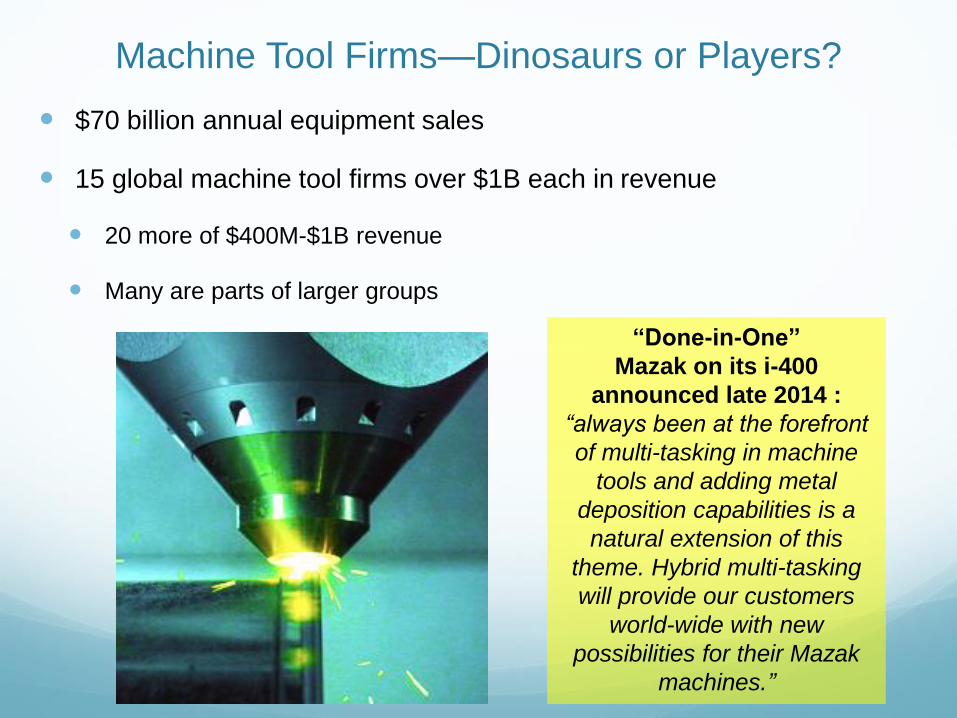

Machine Tool Firms—Dinosaurs or Players?

$70 billion annual equipment sales

15 global machine tool firms over $1B each in revenue

20 more of $400M-$1B revenue

Many are parts of larger groups

“Done-in-One”

Mazak on its i-400

announced late 2014 :

“always been at the forefront

of multi-tasking in machine

tools and adding metal

deposition capabilities is a

natural extension of this

theme. Hybrid multi-tasking

will provide our customers

world-wide with new

possibilities for their Mazak

machines.”

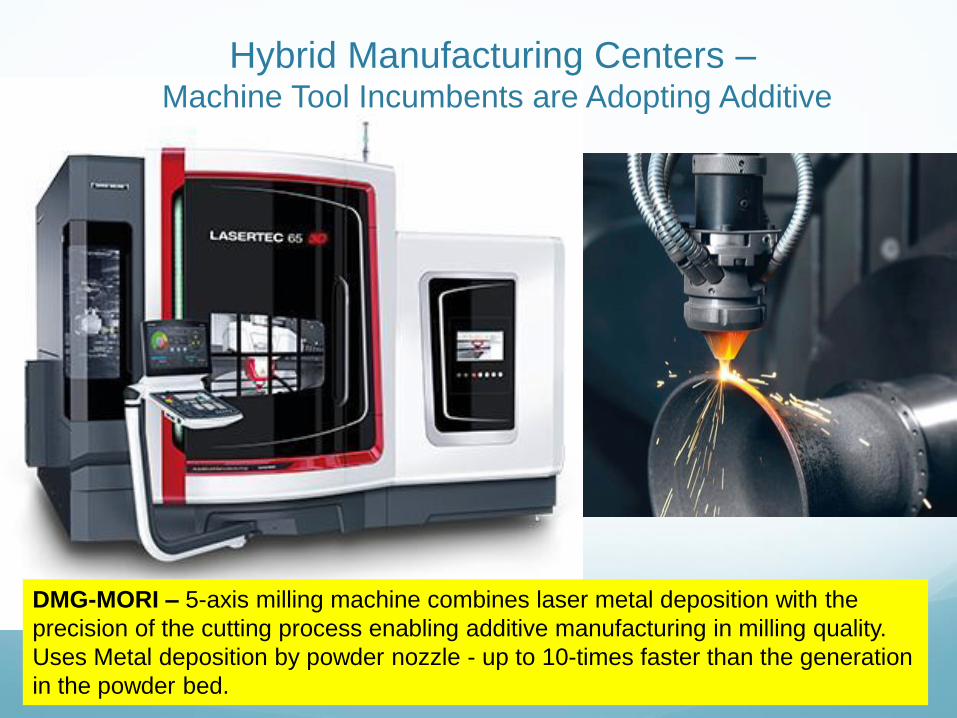

DMG-MORI – 5-axis milling machine combines laser metal deposition with the

precision of the cutting process enabling additive manufacturing in milling quality.

Uses Metal deposition by powder nozzle - up to 10-times faster than the generation

in the powder bed.

Hybrid Manufacturing Centers –Machine Tool Incumbents are Adopting Additive

Action Items

Get involved !!!

America Makes, CIMP, CCAM, ASTM, ANST

Think about the implications of evolving manufacturing eco-

systems and architectures

Think about new business model opportunities

John Dexheimer

203-952-1049

President –LightWave Advisors, Inc.

Advisory Board - Indo-US MIM TEC http://www.indo-mim.com/corpProfile.html

Yale Entrepreneurial Institute http://yei.yale.edu/

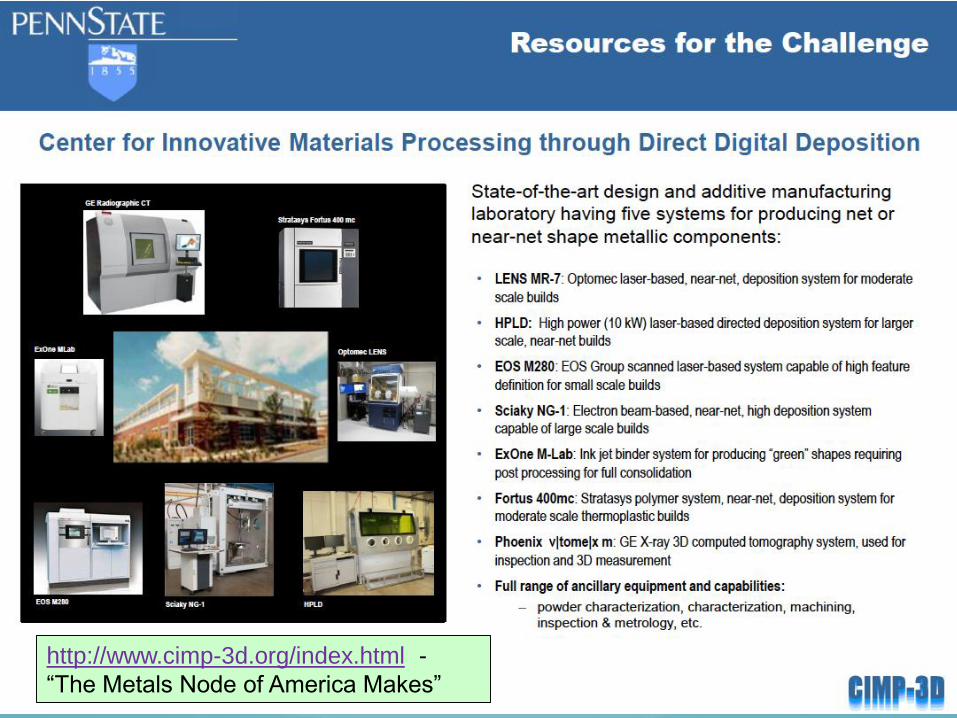

http://www.cimp-3d.org/index.html -

“The Metals Node of America Makes”

Have Vision, BE BOLD!!!

Additive can present a massive opportunity for photonics firm to

contribute to re-working the landscape of manufacturing and

capturing a substantial value created

Can you find a pocket to create hyper-growth and sustained

long term 20-30% Operating Income?

Beyond being just another supplier - that’s not the big part of the value

creation chain

Focused on contributing to transforming customer economics

It likely means reaching outside current eco-systems for collaborators

What models from other sectors may be applicable lessons to the

entrepreneurial innovation and Uber-ization of your firm?

John Dexheimer [email protected]