advanced financial accounting · advanced financial accounting 2nd year examination ... a possible...

TRANSCRIPT

Adv. Financial Accounting August 2015 2nd

Year Paper

Page 1 of 25 Adv. Financial Acc. A2015 (AFA)

Advanced Financial Accounting 2

nd Year Examination

August 2015

Solutions & Marking Scheme & Examiner’s Comments

Adv. Financial Accounting August 2015 2nd

Year Paper

Page 2 of 25 Adv. Financial Acc. A2015 (AFA)

NOTES TO USERS ABOUT THESE SOLUTIONS

The solutions in this document are published by Accounting Technicians Ireland. They are intended to provide

guidance to students and their teachers regarding possible answers to questions in our examinations.

Although they are published by us, we do not necessarily endorse these solutions or agree with the views expressed

by their authors.

There are often many possible approaches to the solution of questions in professional examinations. It should not be

assumed that the approach adopted in these solutions is the ideal or the one preferred by us. Alternative answers will

be marked on their own merits.

This publication is intended to serve as an educational aid. For this reason, the published solutions will often be

significantly longer than would be expected of a candidate in an examination. This will be particularly the case

where discursive answers are involved.

This publication is copyright 2015 and may not be reproduced without permission of Accounting Technicians

Ireland.

© Accounting Technicians Ireland, 2015.

Adv. Financial Accounting August 2015 2nd

Year Paper

Page 3 of 25 Adv. Financial Acc. A2015 (AFA)

Accounting Technicians Ireland

2nd

Year Examination: Autumn 2015

Paper: Advanced Financial Accounting

Monday 10 August 2015

2.30 p.m. to 5.30 p.m.

INSTRUCTIONS TO CANDIDATES

PLEASE READ CAREFULLY

Candidates must indicate clearly whether they are answering the paper in accordance with the law and

practice of Northern Ireland or the Republic of Ireland.

In this examination paper the €/£ symbol may be understood and used by candidates in Northern Ireland to

indicate the UK pound sterling and by candidates in the Republic of Ireland to indicate the Euro.

Answer ALL THREE questions in Section A and TWO of the THREE questions in Section B. If more than

TWO questions are answered in Section B, then only the first TWO questions, in the order filed, will be

corrected.

Candidates should allocate their time carefully.

All workings should be shown.

All figures should be labelled, as appropriate, e.g. €’s, £’s, units etc.

Answers should be illustrated with examples, where appropriate.

Question 1 begins on Page 2 overleaf.

Adv. Financial Accounting August 2015 2nd

Year Paper

Page 4 of 25 Adv. Financial Acc. A2015 (AFA)

Note:

This paper uses both the language of International Accounting Standards (I.A.S’s) and Financial Reporting

Standards (F.R.S’s) where appropriate (e.g. Receivables/Debtors). Examinees are permitted to use either

terminology when preparing financial statements but the use of the language of the International Accounting

Standards (e.g. Receivables rather than Debtors) is preferred.

Adv. Financial Accounting August 2015 2nd

Year Paper

Page 5 of 25 Adv. Financial Acc. A2015 (AFA)

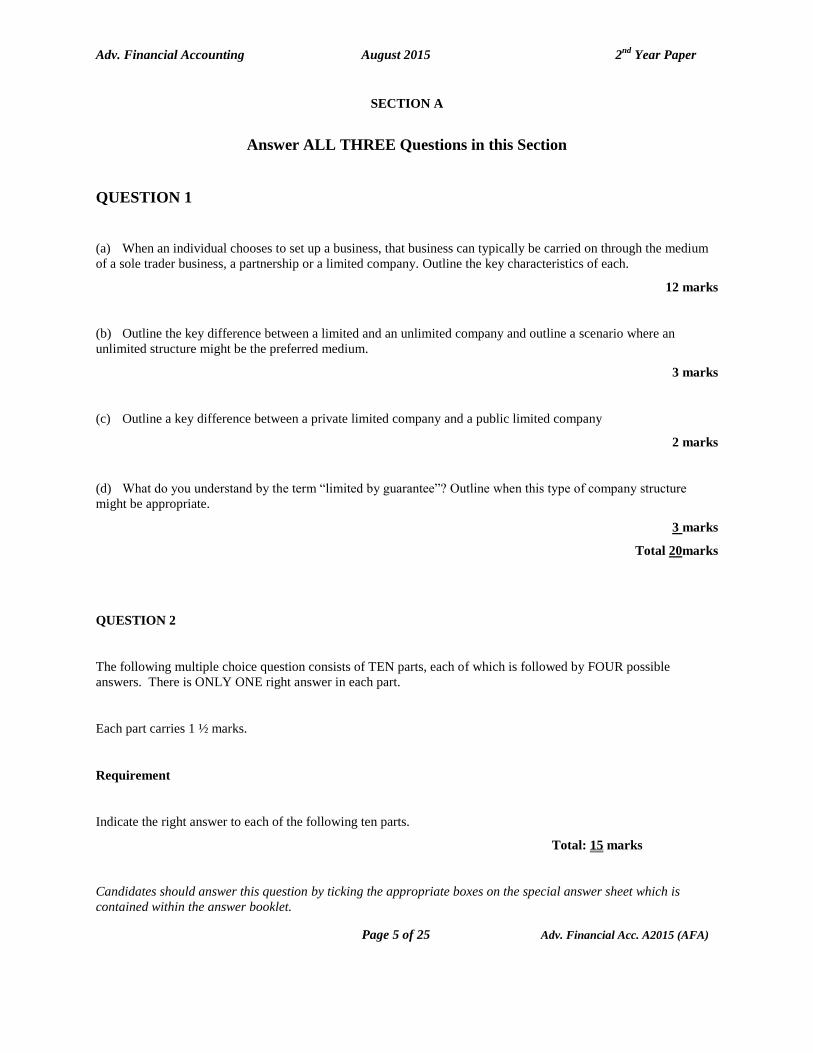

SECTION A

Answer ALL THREE Questions in this Section

QUESTION 1

(a) When an individual chooses to set up a business, that business can typically be carried on through the medium

of a sole trader business, a partnership or a limited company. Outline the key characteristics of each.

12 marks

(b) Outline the key difference between a limited and an unlimited company and outline a scenario where an

unlimited structure might be the preferred medium.

3 marks

(c) Outline a key difference between a private limited company and a public limited company

2 marks

(d) What do you understand by the term “limited by guarantee”? Outline when this type of company structure

might be appropriate.

3 marks

Total 20marks

QUESTION 2

The following multiple choice question consists of TEN parts, each of which is followed by FOUR possible

answers. There is ONLY ONE right answer in each part.

Each part carries 1 ½ marks.

Requirement

Indicate the right answer to each of the following ten parts.

Total: 15 marks

Candidates should answer this question by ticking the appropriate boxes on the special answer sheet which is

contained within the answer booklet.

Adv. Financial Accounting August 2015 2nd

Year Paper

Page 6 of 25 Adv. Financial Acc. A2015 (AFA)

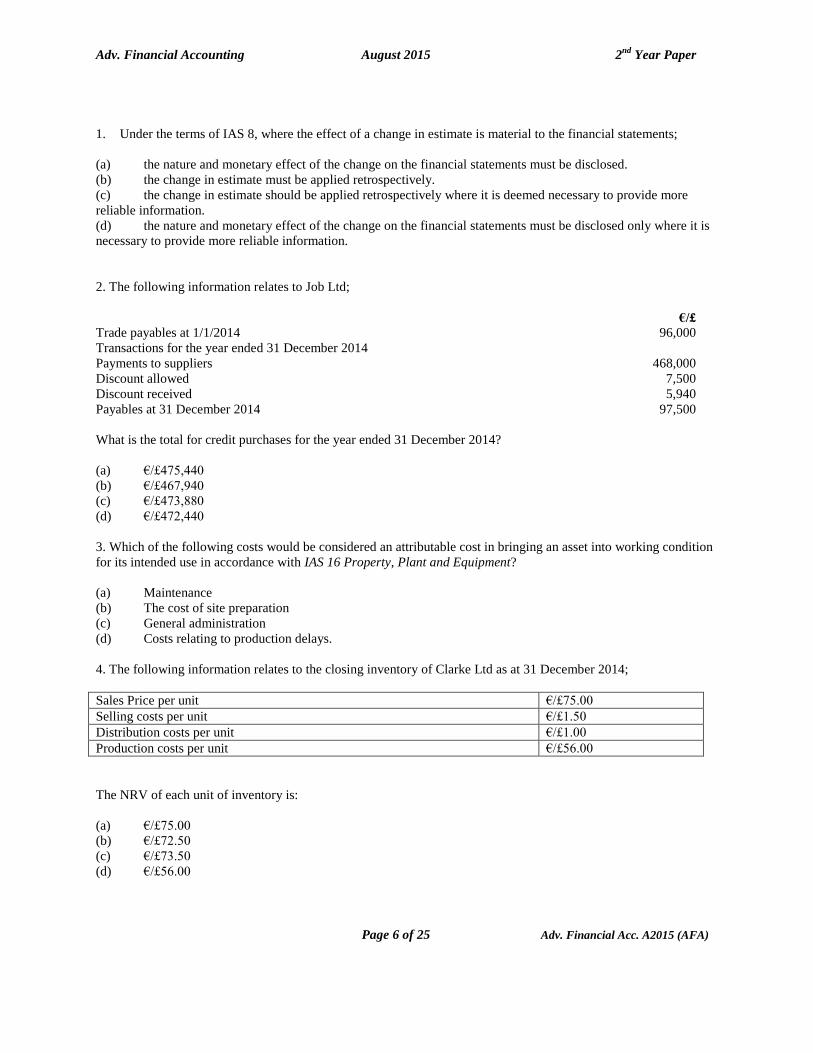

1. Under the terms of IAS 8, where the effect of a change in estimate is material to the financial statements;

(a) the nature and monetary effect of the change on the financial statements must be disclosed.

(b) the change in estimate must be applied retrospectively.

(c) the change in estimate should be applied retrospectively where it is deemed necessary to provide more

reliable information.

(d) the nature and monetary effect of the change on the financial statements must be disclosed only where it is

necessary to provide more reliable information.

2. The following information relates to Job Ltd;

€/£

Trade payables at 1/1/2014 96,000

Transactions for the year ended 31 December 2014

Payments to suppliers 468,000

Discount allowed 7,500

Discount received 5,940

Payables at 31 December 2014 97,500

What is the total for credit purchases for the year ended 31 December 2014?

(a) €/£475,440

(b) €/£467,940

(c) €/£473,880

(d) €/£472,440

3. Which of the following costs would be considered an attributable cost in bringing an asset into working condition

for its intended use in accordance with IAS 16 Property, Plant and Equipment?

(a) Maintenance

(b) The cost of site preparation

(c) General administration

(d) Costs relating to production delays.

4. The following information relates to the closing inventory of Clarke Ltd as at 31 December 2014;

Sales Price per unit €/£75.00

Selling costs per unit €/£1.50

Distribution costs per unit €/£1.00

Production costs per unit €/£56.00

The NRV of each unit of inventory is:

(a) €/£75.00

(b) €/£72.50

(c) €/£73.50

(d) €/£56.00

Adv. Financial Accounting August 2015 2nd

Year Paper

Page 7 of 25 Adv. Financial Acc. A2015 (AFA)

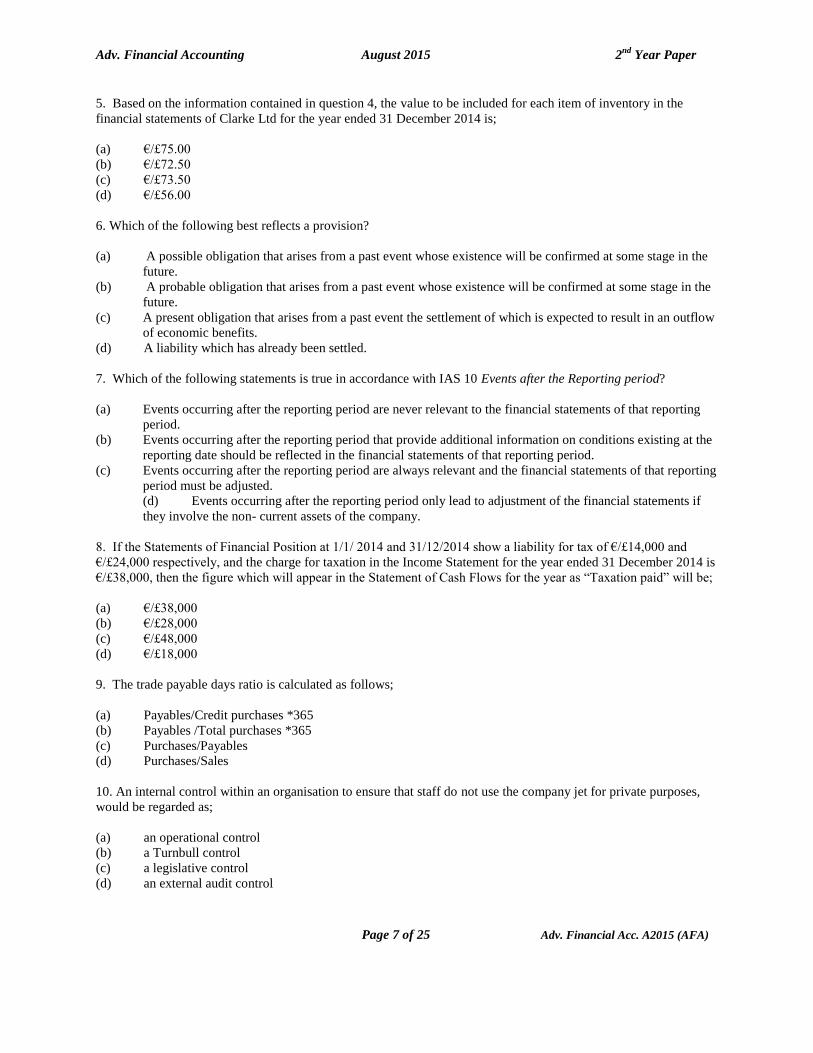

5. Based on the information contained in question 4, the value to be included for each item of inventory in the

financial statements of Clarke Ltd for the year ended 31 December 2014 is;

(a) €/£75.00

(b) €/£72.50

(c) €/£73.50

(d) €/£56.00

6. Which of the following best reflects a provision?

(a) A possible obligation that arises from a past event whose existence will be confirmed at some stage in the

future.

(b) A probable obligation that arises from a past event whose existence will be confirmed at some stage in the

future.

(c) A present obligation that arises from a past event the settlement of which is expected to result in an outflow

of economic benefits.

(d) A liability which has already been settled.

7. Which of the following statements is true in accordance with IAS 10 Events after the Reporting period?

(a) Events occurring after the reporting period are never relevant to the financial statements of that reporting

period.

(b) Events occurring after the reporting period that provide additional information on conditions existing at the

reporting date should be reflected in the financial statements of that reporting period.

(c) Events occurring after the reporting period are always relevant and the financial statements of that reporting

period must be adjusted.

(d) Events occurring after the reporting period only lead to adjustment of the financial statements if

they involve the non- current assets of the company.

8. If the Statements of Financial Position at 1/1/ 2014 and 31/12/2014 show a liability for tax of €/£14,000 and

€/£24,000 respectively, and the charge for taxation in the Income Statement for the year ended 31 December 2014 is

€/£38,000, then the figure which will appear in the Statement of Cash Flows for the year as “Taxation paid” will be;

(a) €/£38,000

(b) €/£28,000

(c) €/£48,000

(d) €/£18,000

9. The trade payable days ratio is calculated as follows;

(a) Payables/Credit purchases *365

(b) Payables /Total purchases *365

(c) Purchases/Payables

(d) Purchases/Sales

10. An internal control within an organisation to ensure that staff do not use the company jet for private purposes,

would be regarded as;

(a) an operational control

(b) a Turnbull control

(c) a legislative control

(d) an external audit control

Adv. Financial Accounting August 2015 2nd

Year Paper

Page 8 of 25 Adv. Financial Acc. A2015 (AFA)

QUESTION 3

Trial Balance of Better Tiles Ltd as at 31st December, 2014

€/£’000 €/£’000

Buildings (cost €/£2,400,000) 1,500

Plant and machinery (cost €/£1,100,000) 860

Bank 20

Trade receivables and Payables 480 360

Inventory at 31 December, 2014 140

Share capital 900

Share premium 100

Revenue reserves, 31 December, 2013 1,040

Profit for year ended 31 December, 2014 540

Prepayments and accruals 40 60

3,020 3,020

You are given the following additional information:

1. A defect was found in one particular brand of floor tiles in January 2015. These tiles had been produced in

December 2014, and were included in the inventory figure in the trial balance at their original cost of

€/£30,000. The sales director believes that these tiles can only be sold for €/£10,000. The remaining

inventory has a net realisable value of €/£300,000 and a replacement cost of €/£360,000.

2. During 2014, a sales rep, visiting the company premises, fell on the factory floor and suffered neck and

back injuries. The rep. is suing the company for €/£300,000 in damages. Better Tiles Ltd’s lawyers are still

putting the case file together and as yet are not in a position to quantify what level of damages may be

ultimately agreed on and to what extent the company’s insurance policies will cover the pay-out.

3. The following items were not recorded in arriving at the figure of profit for the year in the trial balance :

(i) Training grant approved but not received of €/£80,000

(ii) Capital grant application, lodged but not yet approved of €/£1,000,000

(iii) Depreciation;

Buildings - 2% straight line

Plant and machinery - 20% straight line

A full year’s depreciation is charged in the year of acquisition and none in the year of disposal.

(iv) Corporation tax - €/£120,000

Required

Prepare the following financial statements for Better Tiles Ltd. in accordance with the requirements of international

standards:

Adv. Financial Accounting August 2015 2nd

Year Paper

Page 9 of 25 Adv. Financial Acc. A2015 (AFA)

(a) A Statement of the corrected net profit after tax of Better Tiles Ltd for the year to 31 December 2014.

7 marks (b) A Statement of Changes in Equity for the year to 31 December 2014. 4 marks

(c) A Statement of Financial Position as at 31 December 2014. 7 marks

(d) The accompanying disclosure notes to the Financial Statements in relation to Inventories.

5 marks

Presentation: 2 marks

Total: 25 marks

SECTION B

Answer TWO of the THREE questions in this Section

QUESTION 4

Trial Balance (extract) of “Build a Brick” Ltd for year ended 31 December 2014.

€/£ €/£

Sales revenue 850,250

Returns In 4,500

Purchase of raw materials 425,651

Returns out 7,200

Carriage out 15,230

Carriage in 13,300

Inventories at 1 January 2014

Raw material 90,500

Work in progress 32,070

Finished Goods 27,250

Direct factory wages 60,790

Factory supervisors salary 37,560

Employer’s PAYE/PRSI(all factory related) 10,570

Machinery at cost 132,000

Repairs to machinery 9,700

Power( 60% production, 40% administration) 24,300

Insurance 15,000

Other admin expenses 73,500

The additional information is also available;

Adv. Financial Accounting August 2015 2nd

Year Paper

Page 10 of 25 Adv. Financial Acc. A2015 (AFA)

1. Inventory at 31 December 2014;

Raw Material - €/£96,000

Work in Progress - €/£32,320

Finished Goods - €/£24,050

2. Machinery is to be depreciated by 10% using the straight line method.

3. 40% of insurance relates to production, the remainder to distribution.

Requirement:

(a) Prepare a statement showing the factory cost of goods produced for the year ended 31 December 2014.

10 marks

(b) Calculate the gross profit for the year ended 31 December 2014.

4 marks

(c) Calculate the net profit for the year ended 31 December 2014.

4 marks

Presentation: 2 marks

Total: 20 marks

QUESTION 5

The following are the accounts of two businesses that sell sporting goods.

Income Statement

J J K K

€/£ €/£ €/£ €/£

Revenue 80,000 120,000

Less Cost of Sales

Opening inventory 25,000 22,500

Add purchases 50,000 91,000

75,000 113,500

Less closing Inventory (15,000) (60,000) (17,500) (96,000)

Gross profit 20,000 24,000

Less expenses

Depreciation 1,000 3,000

Other expenses 9,000 (10,000) 6,000 (9,000)

Net profit 10,000 15,000

Statement of Financial Position

J J K K

Non – current assets €/£ €/£ €/£ €/£

Equipment 10,000 20,000

Less depreciation to date (8,000) 2,000 (6,000) 14,000

Current assets

Inventory 15,000 17,500

Receivables 25,000 20,000

Bank 5,000 45,000 2,500 40,000

Total assets 47,000 54,000

Adv. Financial Accounting August 2015 2nd

Year Paper

Page 11 of 25 Adv. Financial Acc. A2015 (AFA)

Financed by

Capital

Balance at start of year 38,000 36,000

Add net profit 10,000 15,000

Less drawings (6,000) 42,000 (7,000) 44,000

Current Liabilities

Payables 5,000 10000

47,000 54,000

Requirement;

(a) Calculate the following ratios for each business;

i. Gross profit percentage

ii. Net profit percentage

iii. ROCE

iv. Current ratio

v. Receivable days

vi. Payable days 8 marks

(b) Comment on the relative performance of each company, based on the ratios you have calculated in (a) above.

6 marks

(c) Based on the ratios you have calculated, which business would be more attractive to a potential investor wishing

to invest in a sports business and why? 4 marks

Presentation: 2 marks

Total: 20 marks

QUESTION 6

TRAILERS Ltd., manufactures horse boxes. During the year ended 31st December 2014, TRAILERS Ltd.,

commenced manufacturing a new “double” horse box and purchased machinery costing €/£500,000, to be used for

the manufacture of the new horse box.

It is anticipated that the new machinery will have an expected useful life of ten years and will have no residual value

at that date. Depreciation is therefore to be 10% per annum using the straight line method.

During the year ended 31st December 2014, Trailers Ltd. received government grants as follows:

€/£

Training grants .............................................................................................. ... 40,000

(to assist in covering training costs of staff in the use of new machinery)

Grants related to assets …………………………………………….............................. 120,000

(to assist in covering the costs of the new machinery set out above)

Total Grants received…………………………………………………………………... 160,000

Requirement:

(a) Explain your understanding of each of the following terms in accordance with IAS 20 “Accounting for

Government Grants”.

Adv. Financial Accounting August 2015 2nd

Year Paper

Page 12 of 25 Adv. Financial Acc. A2015 (AFA)

Revenue based Grants

Capital based Grants

4 marks

(b) Outline the two possible treatments of revenue based grants and the two possible treatments of capital based

grants, allowed by IAS 20.

6 marks

(c) Prepare journal entries to show how the above transactions should be dealt with in the accounts of Trailers Ltd

for the year ended 31st December 2014 in accordance with International Accounting Standards.

8 marks

Presentation: 2 marks

Total: 20 marks

Adv. Financial Accounting August 2015 2nd

Year Paper

Page 13 of 25 Adv. Financial Acc. A2015 (AFA)

2nd Year Examination: August 2015

Advanced Financial Accounting

Suggested Solutions

and

Examiner’s Comments

Students please note: These are suggested solutions only; alternative answers may also be deemed to be correct and

will be marked on their own merits.

Statistical Analysis – By Question

Question No. 1 2 3 4 5 6

Average Mark (%) 59 65 48 56 69 47

Nos. Attempting 111 112 111 81 90 52

Statistical Analysis - Overall

Pass Rate 75%

Average Mark 57%

Range of Marks Nos. of Students

0-39 14

40-49 14

50-59 30

60-69 30

70 and over 24

Total No. Sitting Exam 112

Total Absent 26

Total Approved Absent 6

Total No. Applied for Exam 140

General Comments:

In general, the paper was well answered. No question on the paper seemed to pose particular difficulty

and most students who attempted question 5 on ratios scored very well on it.

Adv. Financial Accounting August 2015 2nd

Year Paper

Page 14 of 25 Adv. Financial Acc. A2015 (AFA)

Examiner’s Comments on Question One

Question 1.

(a)

Sole Trader

A sole trader operation is a business owned by one person only. The sole trader is ultimately solely responsible for

the running and management of the business and bears all the risks of the business and is entitled to all the profit

from the business. The sole trader has unlimited liability with regard to the debts of the business. The sole trader s’

business is not regarded as a distinct legal entity. The sole trader is taxed in full on the profits of the business

regardless of whether he withdraws any or all of the profit from the business.

Marks Allocated

4 marks

Partnership

A partnership is a business which is owned by two or more individuals. Like sole traders, most partners will have

unlimited liability with regard to the debts of the partnership. However in certain partnership arrangements some but

not all of the partners will have limited liability. The profits of the partnership are typically divided between the

partners in accordance with the terms of the partnership profit sharing agreement and each partner is taxable on

his/her share of the partnership profit.

Marks Allocated

4 marks

Limited company.

A limited company is regarded as a separate legal entity, distinct from its owners. It can therefore conduct business

in its own right and be sued or sue in its own right. The liability of the owners of a limited company – its

shareholders is limited to the amount they have invested in the company. The company is managed and controlled

on a day to day basis by its board of directors which may not necessarily consist of shareholders. The company is

taxed on any taxable profit it makes. It distributes the after tax profit to shareholders typically in the form of a

dividend.

Marks Allocated

4 marks

Most students were comfortable with part (a), but parts (b) and (c) proved trickier in many cases.

Adv. Financial Accounting August 2015 2nd

Year Paper

Page 15 of 25 Adv. Financial Acc. A2015 (AFA)

(b)

A limited company is a company where the liability of the shareholders is limited to their investment in the

company.

An unlimited company is one where the liability of the shareholders for the debts of the company is unlimited.

An unlimited structure might be used by a large corporate group to facilitate return of capital to its members.

Marks Allocated

1 mark for each of the above points

(c)

The shares in a private limited company are not available for sale to the general public. A public limited company

can sell its shares to the public.

Marks Allocated

1 mark for each point

(d)

A company limited by guarantee is a company where the liability of the members is limited to a guaranteed amount-

this is the amount the members agree to pay in the event of the company going into liquidation. This structure is

commonly used for clubs and non – trading organisations.

Marks Allocated

1.5 marks for each point.

Adv. Financial Accounting August 2015 2nd

Year Paper

Page 16 of 25 Adv. Financial Acc. A2015 (AFA)

Examiner’s Comments on Question Two

Question 2

Total

Marks

Allocated

1

(a) 1.5

2

(a) 1.5

3

(b) 1.5

4

(b) 1.5

5

(d) 1.5

6

(c) 1.5

7

(b) 1.5

8

(b) 1.5

9

(a) 1.5

10

(a) 1.5

No significant difficulties generally with this question.

Adv. Financial Accounting August 2015 2nd

Year Paper

Page 17 of 25 Adv. Financial Acc. A2015 (AFA)

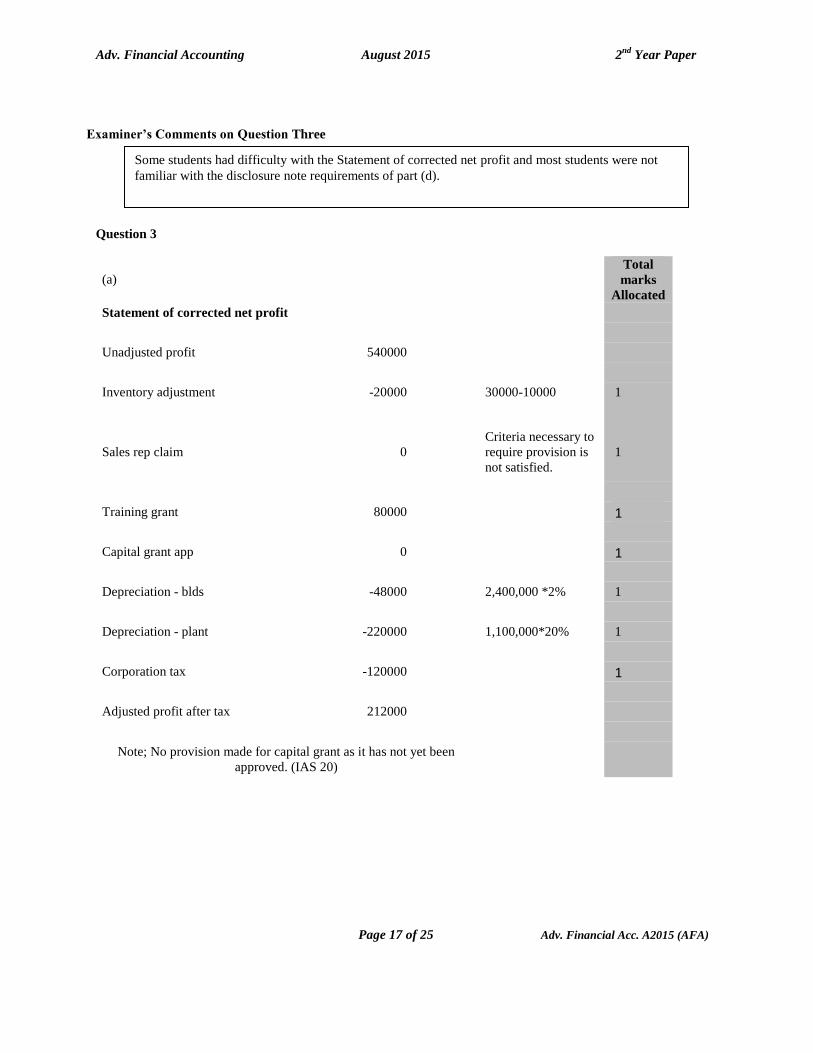

Examiner’s Comments on Question Three

Question 3

(a)

Total

marks

Allocated

Statement of corrected net profit

Unadjusted profit 540000

Inventory adjustment -20000 30000-10000 1

Sales rep claim

0

Criteria necessary to

require provision is

not satisfied.

1

Training grant 80000 1

Capital grant app 0 1

Depreciation - blds -48000 2,400,000 *2% 1

Depreciation - plant -220000 1,100,000*20% 1

Corporation tax -120000 1

Adjusted profit after tax 212000

Note; No provision made for capital grant as it has not yet been

approved. (IAS 20)

Some students had difficulty with the Statement of corrected net profit and most students were not

familiar with the disclosure note requirements of part (d).

Adv. Financial Accounting August 2015 2nd

Year Paper

Page 18 of 25 Adv. Financial Acc. A2015 (AFA)

(b)

Total Marks

Allocated

A statement of changes in Equity for the year ended 31 December 2014

Equity Share Retained

Total

share Premium Earnings

Capital

Balance at 1/1/2014

900000 100000 1040000

2040000

Profit for the year

212,000

212000

Balance at 31/12/2014 900000 100000 1252000

2252000

1mark 1mark 1mark

1mark

(c )

Statement of Financial position as at 31 December 2014.

Assets

2014 2013

Non-current assets

Land and Buildings

1452000

1,500,000-48000

Plant

640000

860,000-220000

2092000

3.5 marks

Current assets

for total assets

Inventories

120000

140000-20000

Receivables

600000

720000

Total Assets

2812000

Equity and liabilities

Equity and reserves

Issued share capital

900000

3.5 marks

Share Premium

100000

for equity

Retained earnings

1252000

And

2252000

liabilities

Current liabilities

Trade and other Payables

540000

360000+60000+120000)

Bank Overdraft

20000

560000

0

Total equity and liabilities

2812000

Adv. Financial Accounting August 2015 2nd

Year Paper

Page 19 of 25 Adv. Financial Acc. A2015 (AFA)

(d)

Disclosure notes

Accounting Policy note

Inventories

Inventories are stated at lower of cost and net realisable value.

3 marks

Cost represents invoice price and the cost of carriage in.

NRV represents selling price less any costs of marketing selling and completion.

Note to the Financial Statements

Inventories

Raw material 0

2 marks

Work in Progress 0

Finished goods 120000

2 marks for presentation

Adv. Financial Accounting August 2015 2nd

Year Paper

Page 20 of 25 Adv. Financial Acc. A2015 (AFA)

Examiner’s Comments on Question Four

Question 4

(a)Manufacturing Account of Build a Brick ltd for the year ended 31 December 2014

Total

Marks

Allocated

Cost of raw materials consumed

Opening stock of raw materials

90,500

Purchases of raw materials

425651

Carriage In

13300

less returns

-7200

431751

3 marks

for cost

of R.M.

522,251

Less closing stock of raw material

-96000

Cost of raw material consumed

426,251

Direct expenses

Production wages

60790

2 marks

for

prime

cist

Paye/Prsi

6533

Machine repairs

9700

Power

14580

91603

Prime cost

517,854

Overheads

Factory insurance

6000

Factory supervisor's salary

37560

4 marks

for o/h

Employers PRSI/PAYE

4037

Depreciation of factory machinery* 13200

60797

578,651

The answer below includes power and repairs in direct expenses. The relevant marks were awarded in

full if students included power and repairs in factory overheads rather than direct expenses as text

books have differed on the treatment.

Adv. Financial Accounting August 2015 2nd

Year Paper

Page 21 of 25 Adv. Financial Acc. A2015 (AFA)

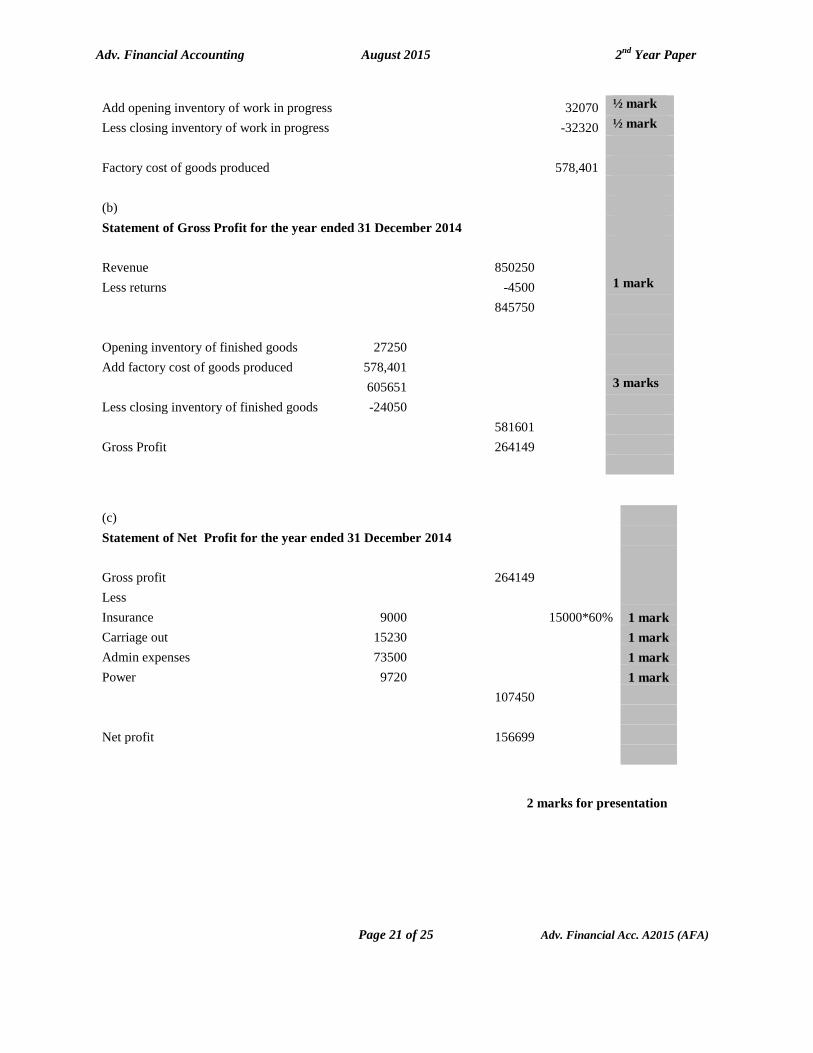

Add opening inventory of work in progress

32070 ½ mark

Less closing inventory of work in progress

-32320 ½ mark

Factory cost of goods produced

578,401

(b)

Statement of Gross Profit for the year ended 31 December 2014

Revenue

850250

Less returns

-4500

1 mark

845750

Opening inventory of finished goods 27250

Add factory cost of goods produced 578,401

605651

3 marks

Less closing inventory of finished goods -24050

581601

Gross Profit

264149

(c)

Statement of Net Profit for the year ended 31 December 2014

Gross profit

264149

Less

Insurance

9000

15000*60% 1 mark

Carriage out

15230

1 mark

Admin expenses

73500

1 mark

Power

9720

1 mark

107450

Net profit

156699

2 marks for presentation

Adv. Financial Accounting August 2015 2nd

Year Paper

Page 22 of 25 Adv. Financial Acc. A2015 (AFA)

Examiner’s Comments on Question Five

Question 5

(a)

Gross Profit Margin = Gross Profit / Sales x 100

Total

Marks

Allocated

J

K

= 20,000 / 80,000 x

100

= 24,000 / 120,000 x

100

= 25 %

= 20 %

2 marks

Net Profit Margin = Net Profit before tax / Sales x 100

J

K

= 10,000 / 80,000 x

100

= 15,000 / 120,000 x

100

= 12.5 %

= 12.5 %

1 mark

ROCE = Net Profit before int & tax/ Capital Employed x 100

J

K

= 10,000 / 40,000 x

100

= 15,000 / 40,000 x

100

= 25 %

= 35 %

2 marks

Current ratio = Current assets / current liabilities

This question produced consistently strong results across all examination centres.

In calculating the ROCE ratio, marks were awarded if the capital employed figure was taken as the

opening figure, the closing figure or an average of the two figures.

Adv. Financial Accounting August 2015 2nd

Year Paper

Page 23 of 25 Adv. Financial Acc. A2015 (AFA)

J K

= 45,000 / 5,000

= 40,000 / 10,000

09:01

04:01

1 mark

Receivables Days = Receivables / Sales x

365

J

K

= 25,000 / 80,000 x

365

= 20,000 / 120,000 x

365

= 114.06 Days

= 60.8 Days

1 mark

Payables Days = Payables / Purchases x

365

J

K

= 5,000 / 50,000 x

365

= 10,000 / 91,000 x

365

= 36.5 Days

= 40.1 Days

1 mark

(b)

Business K is more profitable, both in terms of actual net profits and return

on capital employed. K has achieved a return of €35 for every

€100 invested. J has achieved a lower return of €25 for every €100 invested.

A review of the current ratios of both businesses suggests that

K has achieved greater working capital efficiency than J. However both

businesses would appear to have credit control difficulties with receivable days

far greater than payable days.

Unchecked this could result in overtrading and cash flow difficulties.

Both businesses should strive for a current ratio of 2:1 and a quick ratio of 1:1

K has a higher investment in non current assets which may account for the higher

expense levels in J, e.g. on leasing of equipment.

2 marks for each of three valid points

Adv. Financial Accounting August 2015 2nd

Year Paper

Page 24 of 25 Adv. Financial Acc. A2015 (AFA)

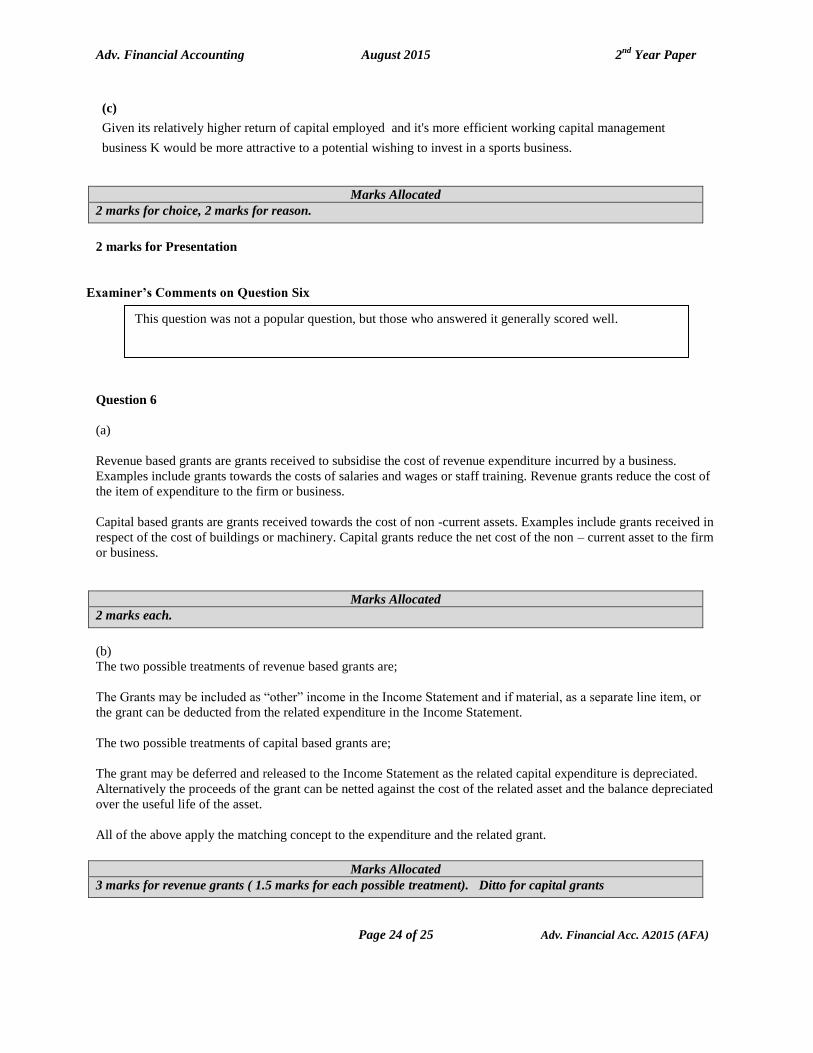

(c)

Given its relatively higher return of capital employed and it's more efficient working capital management

business K would be more attractive to a potential wishing to invest in a sports business.

Marks Allocated

2 marks for choice, 2 marks for reason.

2 marks for Presentation

Examiner’s Comments on Question Six

Question 6

(a)

Revenue based grants are grants received to subsidise the cost of revenue expenditure incurred by a business.

Examples include grants towards the costs of salaries and wages or staff training. Revenue grants reduce the cost of

the item of expenditure to the firm or business.

Capital based grants are grants received towards the cost of non -current assets. Examples include grants received in

respect of the cost of buildings or machinery. Capital grants reduce the net cost of the non – current asset to the firm

or business.

Marks Allocated

2 marks each.

(b)

The two possible treatments of revenue based grants are;

The Grants may be included as “other” income in the Income Statement and if material, as a separate line item, or

the grant can be deducted from the related expenditure in the Income Statement.

The two possible treatments of capital based grants are;

The grant may be deferred and released to the Income Statement as the related capital expenditure is depreciated.

Alternatively the proceeds of the grant can be netted against the cost of the related asset and the balance depreciated

over the useful life of the asset.

All of the above apply the matching concept to the expenditure and the related grant.

Marks Allocated

3 marks for revenue grants ( 1.5 marks for each possible treatment). Ditto for capital grants

This question was not a popular question, but those who answered it generally scored well.

Adv. Financial Accounting August 2015 2nd

Year Paper

Page 25 of 25 Adv. Financial Acc. A2015 (AFA)

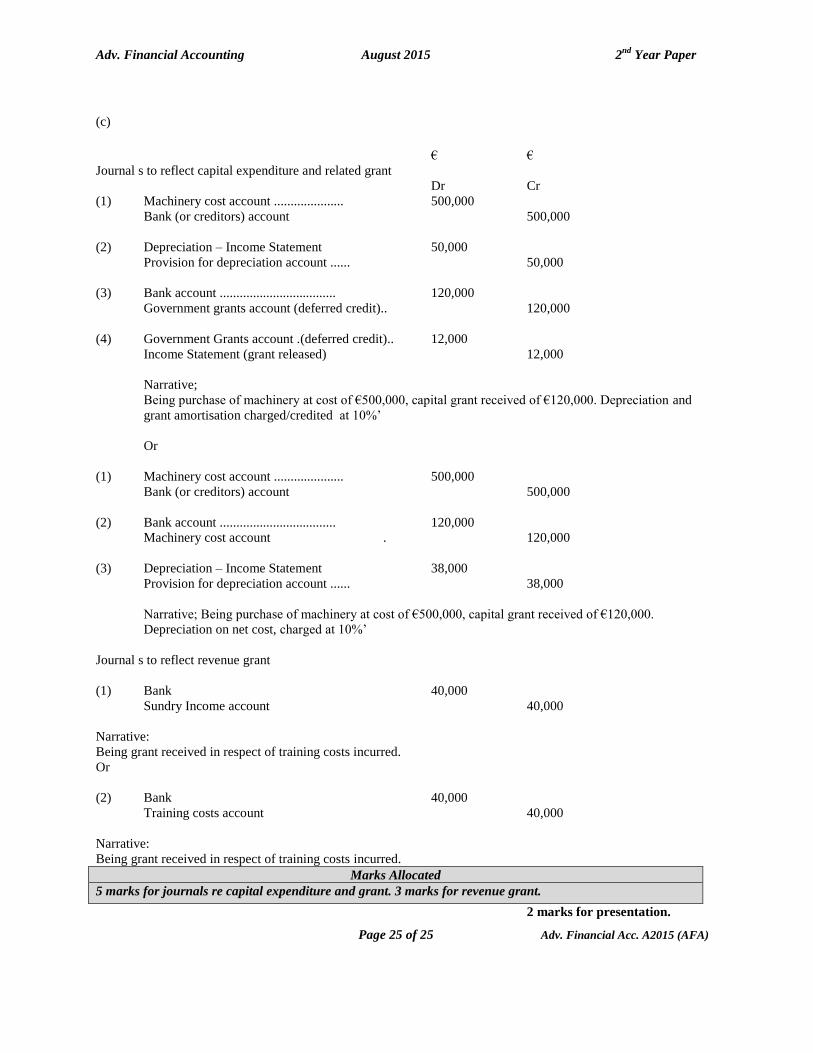

(c)

€ €

Journal s to reflect capital expenditure and related grant

Dr Cr

(1) Machinery cost account ..................... 500,000

Bank (or creditors) account 500,000

(2) Depreciation – Income Statement 50,000

Provision for depreciation account ...... 50,000

(3) Bank account ................................... 120,000

Government grants account (deferred credit).. 120,000

(4) Government Grants account .(deferred credit).. 12,000

Income Statement (grant released) 12,000

Narrative;

Being purchase of machinery at cost of €500,000, capital grant received of €120,000. Depreciation and

grant amortisation charged/credited at 10%’

Or

(1) Machinery cost account ..................... 500,000

Bank (or creditors) account 500,000

(2) Bank account ................................... 120,000

Machinery cost account . 120,000

(3) Depreciation – Income Statement 38,000

Provision for depreciation account ...... 38,000

Narrative; Being purchase of machinery at cost of €500,000, capital grant received of €120,000.

Depreciation on net cost, charged at 10%’

Journal s to reflect revenue grant

(1) Bank 40,000

Sundry Income account 40,000

Narrative:

Being grant received in respect of training costs incurred.

Or

(2) Bank 40,000

Training costs account 40,000

Narrative:

Being grant received in respect of training costs incurred.

Marks Allocated

5 marks for journals re capital expenditure and grant. 3 marks for revenue grant.

2 marks for presentation.