africa connected a telecommunications growth story

TRANSCRIPT

!@#

Africa connectedA telecommunicationsgrowth story

forward >

About Ernst & Young’s Global Telecommunications Center

In a rapidly changing environment, telecommunications operators are facing

challenges of growth, operational efficiency, convergence, technology and

increasing regulatory pressures. Ernst & Young’s Global Telecommunications

Center brings together a worldwide team of professionals to help you achieve your

potential a team with deep technical experience in providing assurance, tax,

transaction and advisory services. The Center works to anticipate market trends,

identify the implications and develop points of view on relevant industry issues.

Ultimately, it enables us to help you meet your goals and compete more

effectively. It’s how Ernst & Young makes a difference.

ey.com/telecommunications

Contacts

Vincent de La Bachelerie

Global Telecommunications LeaderTel: +33 1 4693 [email protected]

Marc Chaya

Global Telecommunications Markets LeaderTel: +33 1 4693 [email protected]

Holger Forst

EMEIA Telecommunications LeaderTel: +49 221 2779 20171 [email protected]

Julia Lamberth

Global Telecommunications Center – AfricaTel: +27 11 772 [email protected],com

Serge Thiemelé

Global Telecommunications Center – AfricaTel: +225 2030 [email protected]

Jonathan Dharmapalan

Global Telecommunications Center – BeijingTel: +86 10 5815 [email protected]

< back | forward >

Africa connected - A telecommunication’s growth story

Shifting markets in global telecoms has seen Africa becoming a significant market forinternational operators. Recognizing the increasing importance of telecommunicationinvestments in Africa and the fast growing telecommunications industry on thecontinent, Ernst & Young has conducted its first industry study on the region.

Senior executives from 28 major telecommunications operators right across Africaparticipated in the study by giving us their first-hand industry perspectives. Weconducted in-depth interviews with all these participants, supported by research,analysis, and insights from our global analyst team and industry professionals.

We hope you find this report relevant and thought-provoking, whether you come to itas a participant in the African telecommunications market or as a customer, investor,regulator, or informed observer. We would like to thank once again all the participantswho have given their time to help us produce it.

Vincent de La BachelerieGlobal Telecommunications Leader

Welcome to Ernst & Young’sfirst telecommunications studyfocused on the African region.This is one of the ongoingseries of major studiesconducted by Ernst & Young tomonitor and analyze theevolving views of businessleaders across the globaltelecommunications industry.

Foreword

Africa connected A telecommunications growth story2

< back | forward >

Research Methodology . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1

Executive summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .2

African telecommunications in context . . . . . . . . . . . . . . . . . . . . . . . . . .4

Challenges in the African market . . . . . . . . . . . . . . . . . . . . . . . . . . . . .14

Telecommunications industry response . . . . . . . . . . . . . . . . . . . . . . . .22

The way forward in the African telecommunications market . . . . . . . .32

Key success factors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .34

Glossary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .36

Notes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .38

References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .39

Contents

< back | forward >

Research methodology

ParticipantsMichel Aka-AnghuiChief Financial Officer, Atlantique Telecom

Heiko SchlittkeActing Managing Director, Zain Tanzania Ltd

Nigel WilliamsFinance Director, Zain Uganda Ltd

François CouturierChief Financial Officer, Côte d’Ivoire Telecom

Dag-Finn WernerVice President Central Africa, Detecon Consulting

Christophe EouzanFinance Director, AMEA, France Telecom

Brefo KwakyeMarketing & Communication Officer, Ghana Telecom

Christian Serriere Chief Financial Officer, MTN Congo Ltd

About the reportThis research is based on in-depth, questionnaire-led interviews conducted in the third quarter of 2008 with 28 senior figures anddecision-makers active in the African telecommunications industries who have country-wide, regional or pan-Africanresponsibilities. The respondent organizations include telecommunications operators at a local, regional and global level. The reportis a synthesis of our interviewees’ perspectives, and the analysis and insights of our Ernst & Young telecommunications industryprofessionals. All comments have been kept unattributed to enable respondents to speak freely.

Percy GrundyManaging Director, Millicom Ghana Limited

Zul JavidCountry General Manager, Warid Telecom

Macsud IsmailFinance Director, mCel

Steven Jurgens Cluster Manager, French Africa, Millicom International Cellular

Leonidas SkarlatosChief Financial Officer, MTN Ghana Ltd

Noel MeierChief Executive Officer, MTN Uganda Ltd

Pablo Guardia Chief Executive Officer, Millicom Tanzania Limited

Tumba Bob MatambaChairman, TIGO, Democratic Republic of Congo

Zhu LinlangChief Financial Officer, Congo ChineTelecom

Nazir PatelGroup Executive: Finance, MTN Group Limited

Justin RamayiaChief Executive Officer, Multilinks Telecommunications

Dominique DespoisseChief Financial Officer, Sentel

Mamudo IbraimoChief Executive Officer,Telecomunicacões de Mozambique

Deon FredericksActing Group Chief Financial Officer,Telkom South Africa

Malick GueyeChief Executive Officer, Teylium Telecom

Abdulbaset Elazzabi Managing Director, Uganda Telecom Limited

And four other African operators.

Africa connected – A telecommunication’s growth story 1

Africa connected – A telecommunication’s growth story2

Executive summary

Telecommunications has transformed AfricaFrom a continent where you would struggle to find a phone ten years ago to one that ison the forefront of a telecommnunications revolution, Africa is very much the mobilecontinent.

During the period from 2002, the French telecommunications market grew at acompound annual growth rate (CAGR) of 7.5% and the Brazilian market at 28%,1 whilethe African market experienced 49.3% growth.

This growth has been powered by an African economy that has been thriving on theback of the commodities boom and increased liberalization. Even with the currenteconomic downturn, it is expected that the African telecommunications market willcontinue to grow faster than any other region over the next three to five years.2

Data set to make an appearance as a revenuegeneratorVoice services should remain the largest contributor to operator revenues in themedium term, but data could start to play an important role. The catalyst of thischange should be the arrival of the new submarine cable systems.

These cables are expected to be a force for change in both the voice and data marketsfor the countries that the new cables reach. At the same time, many operators andgovernments are building national and metropolitan fiber networks to enable easyaccess to the new services.

The low average revenue per user (ARPU)market beckonsOperators are looking at two areas to continue revenue growth. The first is deliveringservices to people that have not had access to mobile services before. Profitablyaddressing this low-ARPU market is a challenge for most operators across thecontinent. Some have dedicated programs to offer communications in underservicedrural areas, while others are relying on their standard offerings to target this market.

The second area that operators are targeting to increase revenues is the introductionof value-added services, with mobile banking at the forefront of these applications.

1 International Telecommunications Union2 Wireless Intelligence

< back | forward >

Africa connected – A telecommunication’s growth story 3

Competition escalates, innovation is keyThe telecommunications market is becoming ever more competitive. Despite theglobal slowdown, the number of new licenses issued and mergers and acquisitions hascontinued apace in Africa during the last year. As competition increases, operationalefficiency should take on added importance for telecommunications operators

Multinational operators are on the lookout for acquisition targets to enable geographicexpansion. Consolidation seems inevitable, with moves into new segments being a keydefensive strategy for many players.

Operators are using innovation to maximize market share and the stage is set for acontest between converged, value-added operators and low-cost voice-focusedoperators.

Networks in more mature African markets are starting to reposition themselves asbroad spectrum information and communication technology (ICT) providers ratherthan simply telecommunications providers.

Still a challenging environment While an understanding of how to effectively operate telecommunications companiesin Africa is growing, significant challenges still need to be overcome by operators.

These include regulatory and political uncertainty. While political stability in Africa onthe whole has improved, Operators are wary of the ability of governments to interferein the regulatory process. The need for regulatory independence has never beenhigher.

Operators continue to be challenged by infrastructure problems, including unreliableelectricity supply. Also, the reluctance of some governments to relinquish their hold oninternational gateways has made it difficult for non-state owned entities to get equalaccess to bandwidth in certain countries.

Operators are struggling to find and retain talent. This is not a challenge unique toAfrican operators, as across the globe operators are struggling to attract talent to fillkey technical and management positions.

| Exexutive summary

< back | forward >

Africa connected - A telecommunication’s growth story4

African telecommunications incontext

African markets are at different stages ofevolutionAfrican markets are at differing stages of evolution, not just in the telecommunicationsfield, but across the broader economic and social spectrum. From countries like SouthAfrica and Egypt, which have the largest economies, to countries like Somalia, whichhas a limited formal economy, the differences are significant.

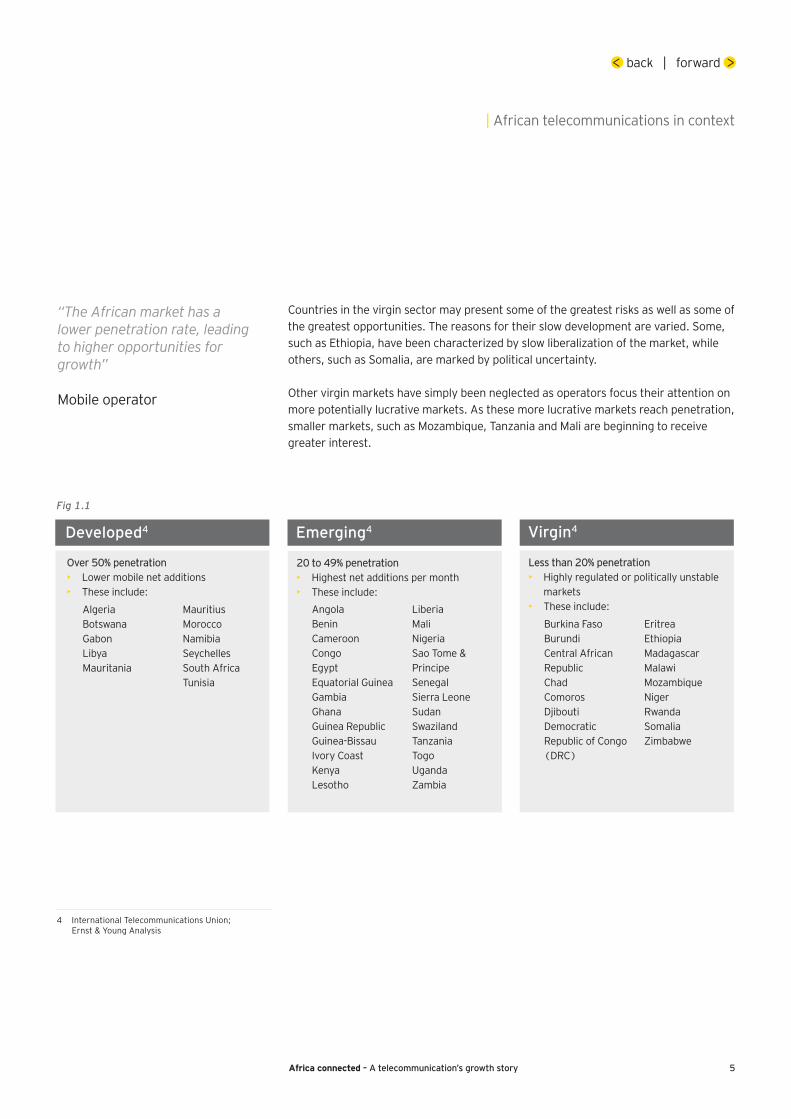

In telecommunications, the pace of development has been equally varied. In 2008,Libya became the first African country to pass the 100% mobile penetration mark, withSouth Africa not far behind at 98%. (See Fig 1.1)

A deeper look into these figures reveals that only 6 countries (Libya, Tunisia, Algeria,Gabon, Seychelles and South Africa) have penetration levels higher than 80%, while24 fall below the 20% penetration mark and 17 have mobile penetration levels of lessthan 10%. (See Fig 1.1)

Demographics have a key influence on the speed at which penetration increases.Countries like Seychelles (108% penetration) and Gabon (91% penetration), whichhave smaller populations (82,000 in the case of Seychelles and 1.4 million forGabon), will typically have elevated penetration levels. Larger countries such asNigeria, with almost 150 million people, should take longer to reach high penetrationlevels. (See Fig 1.1)

In the sub-categories of developed, emerging and virgin markets, there are stillsubstantial differences between individual countries. However, the potential foradditional growth even in the developed markets remains strong, as operators move tobroaden the set of services that they offer.

Countries in the emerging market category are currently the source of greatest focus,as operators look to enter these markets or aggressively entrench their positions tofend off competitors and new entrants. Licenses in this segment are at a premium andattract the attention of many of the prominent regional players. This is evidenced bythe recent attention garnered by the privatization of Malian incumbent operatorSotelma.

Angola has seen an annual GDP growth rate of 20%. Mobile penetration in the countryhas grown from 14% in 2006 to 31% in 2008.4 It is expected that the Angolan marketwill double from its current penetration rate over the next two years. With only oneGSM operator dominating the market, this could become a key battleground in thenext 12-18 months should the regulator license another GSM operator as expected.3

“Markets in Africa are notuniform. There are marketswhere significant marketderegulation and liberalizationhas taken place. Othermarkets in Africa continue tohave restrictive regulationwith very limited competitionor even market monopolies”

Fixed line operator

3 BMI-T Communications Technologies Handbook2008

< back | forward >

Africa connected – A telecommunication’s growth story 5

Countries in the virgin sector may present some of the greatest risks as well as some ofthe greatest opportunities. The reasons for their slow development are varied. Some,such as Ethiopia, have been characterized by slow liberalization of the market, whileothers, such as Somalia, are marked by political uncertainty.

Other virgin markets have simply been neglected as operators focus their attention onmore potentially lucrative markets. As these more lucrative markets reach penetration,smaller markets, such as Mozambique, Tanzania and Mali are beginning to receivegreater interest.

| African telecommunications in context

< back | forward >

4 International Telecommunications Union;Ernst & Young Analysis

“The African market has alower penetration rate, leadingto higher opportunities forgrowth”

Mobile operator

Developed4

Over 50% penetration• Lower mobile net additions• These include:

AlgeriaBotswanaGabonLibyaMauritania

MauritiusMoroccoNamibiaSeychellesSouth AfricaTunisia

20 to 49% penetration• Highest net additions per month• These include:

Emerging4

Less than 20% penetration• Highly regulated or politically unstable

markets• These include:

Virgin4

Angola Benin Cameroon CongoEgypt Equatorial Guinea Gambia Ghana Guinea Republic Guinea-Bissau Ivory CoastKenya Lesotho

Liberia Mali Nigeria Sao Tome &Principe Senegal Sierra Leone Sudan Swaziland Tanzania Togo Uganda Zambia

Burkina FasoBurundi Central AfricanRepublic Chad Comoros Djibouti DemocraticRepublic of Congo(DRC)

Eritrea Ethiopia MadagascarMalawi MozambiqueNiger Rwanda Somalia Zimbabwe

Fig 1.1

Africa connected - A telecommunication’s growth story6

| African telecommunications in context

< back | forward >

5 Wireless Intelligence

AlgeriaLibya

Egypt

Cape Verde

Gambia

Mauritania

Mali

IvoryCoast

Gabon

Equatorial GuineaCongo

Central African RepublicCameroon

Nigeria

Niger

ChadSudan

Eritrea

Ethiopia

Somalia

KenyaUgan

da

Democratic Republicof Congo

RwandaBurundi

Tanzania Seychelles

Comoros

MalawiZambia

Mauritius

Mad

agas

car

Reunion

Moz

ambi

que

Zimbabwe

Angola

Namibia

Botswana

South Africa Lesotho

Swaziland

Senegal

Guinea

Sao Tome & Principe

Djibouti

Moroc

co

Liberia

Tuni

sia

Western Sahara

Burkina Faso

Gha

na

Togo

Beni

nSierra Leone

Guinea-Bissau

Less than 20%

20% to 50%

Above 50%

Key

Fig 1.2: African mobile markets – 2007 penetration(%)5

Africa connected – A telecommunication’s growth story 7

Regional snapshot

| African telecommunications in context

< back | forward >

6 Ernst & Young Analysis

West Africa has seen its growth driven primarily by developmentin its largest market, Nigeria. 2008 saw Nigeria overtake SouthAfrica as the largest mobile market on the continent. The regionis expected to continue to be the fastest growing region withNigeria and Ghana showing the strongest subscriber growth.

Growth in Southern Africa, however, is beginning to slow as theSouth African market starts to reach saturation point. The moreliberalized markets in both Southern and Eastern Africa havemade these regions attractive to investors and both haveexperienced high levels of foreign direct investment.

With the South African market aproaching saturation, operatorsare working quickly to broaden their offerings and move into theenterprise services field.

East Africa is moving ahead, with countries such as Kenya andTanzania reporting rapid growth. Kenya, with the resurgence ofTelkom Kenya under the ownership of France Telecom, and thelaunch of Econet’s Yu service, is one of the most competitivemarkets on the continent. Uganda, Burundi and Rwanda, while

small markets, are moving aggressively to usetelecommunications as a catalyst for broader economic growth.

The Horn of Africa remains under-penetrated. Because ofpolitical uncertainty in Somalia, mobile penetration remains low.In Ethiopia, limited competition has resulted in mobilepenetration remaining below the 2% mark.

North Africa has a reputation for having the most maturemarkets on the continent but the delayed privatizations inAlgeria and Tunisia are holding them back. The closure of thesecond fixed-line operator in Algeria in late 2008 is testament tothe status of competiveness in that market.

The greater than 100% penetration in Libya, along with thepolitical dispensation, may limit the options fortelecommunications growth in the territory.

The slow deployment of 3G services has put most countries inthe region behind a number of other African countries, in termsof technical advancement.

Fig 1.3: Mobile penetration by African region6

60%

50%

40%

30%

20%

10%

0%Q2 06 Q2 07 Q2 08

Northern Western Central Eastern

Africa connected - A telecommunication’s growth story8

| African telecommunications in context

< back | forward >

7 International Telecommunications Union8 Wireless Intelligence9 Wireless Intelligence10 Wireless Intelligence

Fig 1.4: African mobile subscribers 2000-1210

Q4 2000

700,000,000

600,000,000

500,000,000

400,000,000

300,000,000

200,000,000

100,000,000

0

Medium growthphase

High growthphase

Q4 2001

Q4 2002

Q4 2003

Q4 2004

Q4 2005

Q4 2006

Q4 2007

Q4 2008

Q4 2009

Q4 2010

Q4 2011

Q4 2012

Africa is the fastest growing mobile market in theworldThe last five years have been a golden age for mobile telephony on the continent. Between2002 and 2007, the mobile phone market in Africa grew by 49.3% (CAGR) as opposed toAsia which grew at 27.4%.7

Even with the great disparities between individual African countries, the average mobilepenetration for the continent stands at 37% and this is expected to rise to 61% by 2012.8

Compared with Asia, where mobile penetration is already at 53% and Europe, wherepenetration has topped 125%, it is clear where the fastest growth is likely to be over the nextfive years.8

Pre-paid mobile services continue to be the dominant form of transaction on the continentaccounting for 96% of users.8 Only South Africa, with a 13% contract customer base, hasless than 90% of its market on pre-paid.8 As operators strive to bring low APRU subscribersonto their networks, pre-paid should continue to be the preferred method of payment.

Telecommunications growth should continue to be driven by voice services, but within a fewyears, data is expected to become an increasing part of the income of operators across thecontinent.

While the GSM family of technologies – based on wideband CDMA (W-CDMA) – are likely todominate the market, there are challenges in the form of CDMA EVDO and WiMAX. Atpresent, there are only 14 W-CDMA networks on the continent, with three of these in SouthAfrica. This is clearly a market still in its infancy, but it is estimated that by the end of 2012there will be 63 million W-CDMA connections on the continent as opposed to 7.6 millionCDMA EVDO connections.9

“The opportunity for sustainedgrowth in Africa may be higherthan those in other emergingmarkets”

Mobile operator

“Strong growth is stillexpected in the telecommarket: first with voice, thenwith data when voice becomesmore mature”

Mobile operator

Africa connected – A telecommunication’s growth story 9

| African telecommunications in context

< back | forward >

11 State of World Population 2007 UNDP 12 International Telecommunications Union

The “digital divide” still needs to be crossedWith 70% of the population of sub-Saharan Africa still living in rural areas, the challengeto operators is to reach remote pockets of potential consumers in a cost-effective way.11

Figure 1.6 illustrates how low the overall coverage of the population remains across thecontinent. While North Africa or countries like South Africa are approaching 100%population coverage, the average across sub-Saharan Africa is just over 50%. Thisfigure has only increased by 10% in the last four years, at a time when penetrationlevels have more than doubled.11

Until now, operators have been able to concentrate their efforts on urban areas, but asgrowth from these areas starts to slow, there is likely to be a need to look further afield.

These rural initiatives carry their own challenges, with the provision of infrastructure tosupport telecommunications services especially pertinent. The focus has been onensuring that communities, rather than individuals, are connected and this is unlikely tochange in the short term. Governments across the continent are particularly concernedwith driving telecommunications into areas that have not had access in the past. Manyof the public projects underway at the moment, including the deployment of fiber inBotswana, Malawi and Rwanda, are about increasing accessibility to rural communities.

“Our main investment is goingfor geographical coverage(from big cities to rural areas)rather than for newtechnologies”

Mobile operator

Fig 1.5: Proportion of rural population by region 200711

% population

90

80

70

60

50

40

30

20

10

0

Easte

rn A

frica

Sout

h Cen

tral A

siaAfri

caAsia

Sout

h Eas

tern A

sia

North

ern A

frica

Arab st

ates

Sout

hern

Afri

ca

Middle

Africa

Fig 1.6: Mobile population coverage in Africa 200612

% population

100

90

80

70

60

50

40

30

20

10

0Sub-Saharan

AfricaAfrica North

AfricaSouthAfrica

Africa connected - A telecommunication’s growth story10

Fixed line is seeing increased investmentHistorically, protracted under-investment in public telecommunications has renderedfixed line telecommunications largely insignificant. Egypt, with the highest fixed linepenetration on the continent, only has a 15% penetration, while mobile penetrationrates approach 100% in some countries, as illustrated by figure 1.7. Mobile phonesoutnumber fixed lines by 10 times in Africa, with the gap widening.

This figure is unlikely to change dramatically, as fixed line services will not be in aposition to challenge mobile services as the preferred method of connectingconsumers to networks in the short to medium term.

However, the investment into new fixed networks to provide backhaul and corenetwork services is seeing rapid growth. This investment is coming from individualoperators looking to access more cost-effective and reliable networks. These next-generation networks also provide the foundation for delivering high-speed networkaccess for businesses and consumers.

| African telecommunications in context

“We also expect an increaseddeployment of fiber opticnetwork for national andmetropolitan areatransmission networks”

Fixed line operator

13 International Telecommunications Union;Ernst & Young Analysis

< back | forward >

Fig 1.7: Africa fixed and mobile penetration levels 200713

% fixed line penetration

15

10

5

010 20 30 40 50 60 70 80 90

Nigeria

Gambia

Ghana

Namibia

South Africa

Senegal

Kenya

Egypt

Morocco

Gabon

Swaziland

Tunisia

ChadMozambique

Tanzania

Botswana

Ivory Coast

% mobilepenetration

Africa connected – A telecommunication’s growth story 11

The fixed broadband market remains smallAfrica has the lowest internet penetration in the world at 5.4% with only 12 countrieshaving a penetration rate of over 1%. In comparison, Asia only has five countries belowthe 1% penetration mark.14 Broadband adoption is also low, with Egypt having thehighest penetration at 8%.14

Various efforts to address this issue, such as the NEPAD eSchools initiative to providecomputers in schools, with pilot projects in 17 countries, have met with mixed success,mainly due to the high cost of bandwidth within almost every African country. InAngola, for example, the cost of the cheapest broadband package is equivalent to 78%of the gross national income (GNI) per capita.15

The high cost of bandwidth is often a result of the reluctance of some countries toderegulate their international gateways, and the reliance of many countries on satellitelinks for international connectivity. Most of the countries in the eastern region of thecontinent are completely dependent on satellite as a backhaul mechanism, as is almostevery landlocked country. It is this dependence that has stimulated the participation ofoperators and governments in the laying of submarine cable systems.

| African telecommunications in context

“Broadband does have afuture in Africa… becausethere will be strongcompetition among bigcompanies which willeventually drive the pricedown”

Mobile operator

< back | forward >

14 www.internetworldstats.com15 World Bank, Ernst & Young Analysis16 International Telecommunications Union;

Ernst & Young Analysis

Fig 1.8: Internet and broadband population penetration 200716

% population penetration

16

14

12

10

8

6

4

2

0Egypt Algeria South

AfricaBotswanaKenya Cote

d’Ivoire

Internet users

Broadband subscribers

Africa averageinternet penetration5.4% (2007)

Africa connected - A telecommunication’s growth story12

Mobile licensing has helped to unlock growthThe initial wave of GSM licenses issued during the 1990s, such as Vodacom and MTNin South Africa and Safaricom in Kenya, ignited the mobile flame in Africa. However,our research shows that it wasn’t until the second wave of licenses were issued in thelate 1990s and early 2000 that mobile penetration across the continent started tobecome a mass market phenomenon.

The awarding of new licenses in 2009 is likely to be dominated by the licenseconversion process in South Africa which should see a substantial number of value-added network services providers permitted to run their own networks. The numberthat actually launch services is likely to be much smaller.

As regulators across the continent look to increase competition, the awarding of newlicenses will continue. Already the governments of Morocco and Mozambique haveindicated that they intend to issue a license for an additional mobile operator duringthe course of 2009.

The introduction of unified licenses in countries such as Ghana, Uganda and Nigeriahas resulted in greater opportunities for operators. These licenses allow operators tochoose the technology most suited to their needs and allow mobile operators theopportunity to venture into the fixed line environment, as well as offering value-addedservices.

| African telecommunications in context

“We are noticing theemergence of a number ofcountries who have adopted aconverged/unified licenseregime. This blurs the olddistinction between fixed andmobile services”

Fixed line operator

< back | forward >

Africa connected – A telecommunication’s growth story 13

| African telecommunications in context

< back | forward >

17 United Nations Statistics Division18 Global Mobile Tax Review 2006-2007 GSM Association, Deloitte

Drivers of the African growth storyAfrican economies have benefited significantly from the recentboom in commodity prices, driven largely by demand fromChina. Much of this additional revenue has been re-invested intoinfrastructure projects, including improving healthcare andeducation.

Increased government expenditure has seen a correspondingincrease in disposable income.17 This increase in consumerspending has been mirrored by a period of relative politicalstability on the continent, with Africa more open to businessthan at any point in the past.

Consolidation in the telecommunications market and the growthof regional operators has driven efficiencies, enabled economiesof scale and delivered greater growth potential. The pureAfrican operator, however, is largely a thing of the past, withalmost all of the regional operators having expanded beyond thecontinent, wither organically or by acquisition.

Apart from isolated hot spots, Africa has enjoyed a period ofrelative political and economic stability over the past five years.This stability, combined with declining revenues in developedmarkets, has attracted a new wave of global operators to thecontinent.

Telecommunications growth has also been encouraged by theeasing of regulatory restrictions by African governments andincreased liberalization across the market.

Telecommunications is pivotal toAfrican economicsGrowing at an average of 14.5% since 2003, Africa’s economyhas seen substantial development since the turn of thecentury.17

As a critical element of the modern information society,telecommunications has a direct influence on the performanceof an economy. It is estimated that a 10% increase in telephonepenetration results in a 1.2% increase in GDP in emergingmarkets, and a 0.6% increase in developed markets.18

The introduction of private mobile operators to the continent hasunlocked new growth opportunities for many African economies.The investment by mobile operators has also brought significantforeign direct investment and increased opportunities for formalemployment in countries where the informal economy dwarfsthe formal.

The global economic crisis is expected to have a limited impacton the region’s telecommunications market. Relative marketmaturity and limited exposure to global markets should seeAfrican telecommunications continue on its current growth path.

There may be some short-term impact caused by currencyfluctuations and lower commodity prices. The biggest impact ofthe current economic slowdown may come from the increasedconsolidation of the market, as operators looking to fundoperational and capital expenditure may find it harder to gainaccess to finance.

Africa connected - A telecommunication’s growth story14

Challenges in the Africanmarket

In our research, political uncertainty topped the list of external factors faced byoperators in Africa. This indicates that although the political environment has beenrelatively stable for the last few years, operators are still mindful of the potential forserious conflicts. Even in reasonably stable democracies, simmering hostilities or localdisputes may make conducting business difficult.

Operators also identified the rise in competition as one of their chief concerns. Thiscompetition, fostered by demand and government involvement across the region, hasresulted in decreasing ARPUs. Operators view this level of competition asunsustainable in the medium term with consolidation inevitable.

Another key concern identified by operators was the lack of reliable infrastructure,especially surrounding the supply of power to base stations. Power supply can beunreliable, forcing operators to explore alternative sources of power like solar, wind orgenerators.

According to a recent report Nigeria produces only 10% of the power it requires on adaily basis, leaving many companies and facilities without power for long stretches oftime.19 This forces operators to make contingencies, including generators at everybase station, to ensure consistent operation. Having to maintain and fuel thesegenerators adds to operational costs.

“Governance, includingregulatory authority andpolitical structure, in Africa isvolatile”

Mobile operator

“We are consideringalternative sources of powerlike solar energy”

Mobile operator

19 University World News20 Ernst & Young Analysis

< back | forward >

Fig 2.1: The biggest external challenges facing telecommunications operators in Africa20

% of operators who listed it as a challenge

Politic

al un

certa

inty

50

45

40

35

30

25

20

15

10

5

0

Costs

Compe

tition

Tech

nolog

y infa

struc

ture

Regula

tory e

nviro

nmen

t

Power

Corru

ption

Africa connected – A telecommunication’s growth story 15

Regulatory and policy challenges remainDespite moves to establish independent regulators across the continent, 88% of theoperators interviewed felt that regulatory bodies in Africa were not robust enough. Ofparticular concern to operators is a perceived level of political interference in theregulatory process.

Regulators have, however, increasingly been taking their consumer protection rolemore seriously, with networks across the continent being taken to task for poor serviceprovision. Zambia, Nigeria and Senegal are just three examples where large operatorshave been compelled to address weaknesses in their offerings under the threat of finesor being barred from advertising their products and services.

The continued existence of fixed line monopolies, which typically keep pricing high inmany countries, remains an obstacle to growth, as does monopoly access tointernational gateways.

| Challenges in the African market

“A high level of governmentintervention has a significantimpact on the policies of theregulator, with differentpolicies from one governmentregime to another”

Mobile operator

< back | forward >

Fig 2.2: Competition levels (%) in telecommunications sub-segments21

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%Fixedlocal

services

Internationalfixed longdistance

Mobile Internationalgateways

Internetservices

No data

Fullcompetition

Partialcompetition

Monopoly

21 International Telecommunications Union

Africa connected - A telecommunication’s growth story16

Talent is the biggest operational challengeOur research highlighted the issue of a chronic shortage of talent which extends acrossall skill sets, from technical through to management. While operators acknowledgedthe importance of training, it was noted on several occasions that the issue of staffbeing head-hunted by other operators was an on going challenge.

Difficulties of running operations across multiple countries create a unique set ofinternal challenges for operators. The complexity of internal processes and systemscan make it difficult for operators to respond quickly to market demands andcompetitive threats.

| Challenges in the African market

“Our biggest internalchallenge is key skills, not onlytechnical but managerial aswell”

Mobile operator

“Training and knowledge ofthe employees are essential toreach the objectives of thecompany”

Mobile operator

< back | forward >

Fig 2.3: The biggest internal challenges facing telecommunications operators in Africa22

% of operators who listed it as a challenge

Staff

ing

90

80

70

60

50

40

30

20

10

0

Inter

nal p

roce

sses

Finan

cing

Speed

to m

arke

t

Cost o

f ope

ration

s

22 Ernst & Young Analysis

Africa connected – A telecommunication’s growth story 17

“Price sensitivity in Africa isvery high; one user has severalSIM cards in order to benefitfrom best prices”

Mobile operator

“Low-cost solutions need to befound and implemented tobring a larger number of thepopulation into the market”

Fixed line operator

< back | forward >

Despite the success of telecoms operators,our research indicated that the cost oftelecoms remains high. Annual fixed linesubscriptions are 10.6% of GDP per capitaas opposed to the 4.2% global average.24

The high cost has been perpetuated asincumbent fixed line operators try tomaintain revenues in the face of increasedcompetition.

Mobile pricing also remains higher thanthe international average when comparedwith earning potential. While the cost of100 minutes of mobile use internationallycosts 30% of GNI, for African consumers itcosts 77% of GNI.23

In some markets this is changing. Thereare indications that operators are lookingto use pricing as a competitivedifferentiator. Pan-African operators havebegun to standardize their tariffs acrossborders and the acquisition of Africanoperators by large multinational groupshas resulted in increased price pressure.

We are also beginning to see innovativecustomer relationship programs beingintroduced to reduce churn and leverageregional ownership. Initiatives such ascross-border roaming services encourageusers to remain loyal, as well as reducingincome lost through roaming agreements.

Operators are also looking to find newways to package their services to makethem accessible to the lower end of themarket. In South Africa, a government -mandated, lower interconnect fee hasbeen used to minimize the cost ofcommunity phones in underservicedareas, and Vodacom and MTN have bothintroduced services that offer discounts tosubscribers based on the load on thenetwork at that point in time.

The arrival of the real low-cost operator inAfrica, however, remains a new frontier.

Fig 2.4: Africa and India ARPU development24

US$ per month

30

25

20

15

10

5

0Q101

Q301

Q102

Q302

Q103

Q303

Q104

Q304

Q105

Q305

Q106

Q306

Q107

Q307

Q108

Africa

India

23 State of World Population 2007 UNDP24 International Telecommunications Union

Affordability is a key issue on the continent

| Challenges in the African market

Africa connected - A telecommunication’s growth story18

Infrastructure weakness in data connectivity isa continent-wide concernAfrica has limited inter-continent and global connectivity, which means structurallyhigh broadband prices and poor enterprise service levels. In the current situation two-thirds of inter-African data has to travel outside the continent to peering points inEurope in order to return to its African destination.25

With cable landing points controlled by incumbent monopolies, the cost of a 1Mbps link(US$7000) is substantially higher than in other regions. This is opposed to a costprice to the operators of $2000 per Mbps.26

Access to international gateways and the reliance of countries on satellite connectivityhas also contributed to the cost of data connectivity across the continent.

| Challenges in the African market

“There is huge pressure bystakeholders (governments,regulators and consumers) toreduce tariffs in environmentswhere operators have toprovide their owninfrastructure”

Mobile operator

< back | forward >

25 African Renewal26 Tectonic27 Ernst & Young Analysis

Fig 2.5: External factors inhibiting ICT growth in Africa27

ICTinhibitors

Under-prioritization ofopen access in

backboneenvironment

Lack of public sectorresources and private

sector investment

Lack of skilled staffand management

policies

Lack of regionalregulatory co-

ordination

Africa connected – A telecommunication’s growth story 19

| Challenges in the African market

“Competition here is currentlymoderate, although within thenext six months three newcompetitors are entering thecompetitive market. This willput competition on a level toohigh to be sustainable for amedium-sized country”

Mobile operator

“In future, our market willbecome hyper competitive asone or two licenses are in theoffing. It will mean too muchcompetition in GSM”

Mobile operator

< back | forward >

Competitive intensity is increasing across thecontinentUsing the Herfindhahl Hirschmann Index, it is possible to chart the increase incompetition across the continent. Our analysis indicates that while competition isincreasing across the surveyed territories, the tendency is for competitors to avoidgetting caught in a price war. This is the case in Nigeria where the index is relativelystable even though there are six operators in the market.

In South Africa, the impact of Cell C as a competitor is beginning to be felt as the indexmoved sharply downwards in 2008. The Egyptian index was flat from 2004 to 2006,but the launch of 3G services and the entry of Etisalat in 2007 has raised the level ofcompetition. While the Kenyan market was relatively flat in this analysis, more recentdevelopments, including the price war triggered by acquisitions by global operatorsand the launch of a fourth mobile operator should see this change.

While increased competition is viewed favorably by regulators and consumers, ourresearch indicated that operators in highly contested markets were uneasy about thesustainability of the level of competition and the effect on ARPUs.

Fig 2.6: Market concentration in selected African mobile markets28

Herfindhahl Hirshmann (HH) Index

8,500

7,500

6,500

5,500

4,500

3,500

2,500Q2 2004 Q2 2005 Q2 2006 Q2 2007 Q2 2008

Egypt (3 operators)South Africa(3 operators)Ghana (4 operators)Uganda (5 operators)

Nigeria (6 operators)

Kenya (3 operators)

Tanzania (4 operators)

28 Ernst & Young Analysis, Wireless Intelligence

There is a heavy tax burden on both consumersand operatorsAcross the continent, taxation is a key concern for operators with the average taxationon operator profits at 30%. Governments have chosen to place a heavy tax burden onmobile operators in terms of a tax on profits as well as higher license fees to bringmore money into the fiscus.

Kenyans, for example, pay a tax of 26% on mobile communicationsand Safaricom hasbeen acknowledged as the highest corporate tax payer in the country for 2007.29 InNamibia, the incumbent operator absorbed a 15% tax increase on pre-paid airtime,allegedly to reduce the impact on students and the elderly.

In our research, respondents also raised the issue of excise duties on handsets as aroadblock to getting the lower end of the market on the network. Operators believetheir efforts to roll out lower-cost handsets have been stifled by high taxes.

Respondents interviewed favored the use of indirect taxes such as VAT as the methodof taxation. This would allow operators to drive costs lower and allow government torecoup lost tax revenues through increased usage of mobile services. VAT rates on thecontinent range from 5% to 23%.30

29 IDG News Service30 Taxation and the Growth of Mobile in East Africa

GSM Association 31 Taxation and the growth of mobile services in

sub-Saharan Africa GSM Association

Africa connected - A telecommunication’s growth story20

| Challenges in the African market

“We see governments askingfor more and more taxeswhich in the end impactairtime and pricing”

Mobile operator

“On the continent, telecomcompanies are considered ascash cows and used as taxcollectors of indirect tax ratherthan taxing the consumerdirectly. Telecom companieshave embarked on educatingthe government on the needto reduce taxes on tariffs inorder to boost growth indemand. The process is slow”

Mobile operator

< back | forward >

Fig 2.7: Total taxes as a share of total revenue by mobile operators - 200631

%

Zambia

60

50

40

30

20

10

0

Tanz

ania

Camero

onKen

ya

Ugand

a

Ghana

Sene

gal

Gabon

Nigeria

Rwanda

Sout

h Afri

ca

Swaz

iland

Africa connected – A telecommunication’s growth story 21

< back | forward >

Return on investment (ROI) profiles in theregion are encouragingDelivering ROI in the African environment can be delayed due to the cost ofinfrastructure, coverage requirements and the low ARPU profiles of consumers.However, established African players which can benefit from economies of scale due toa large portfolio on the continent, have encouraging ROI profiles. This may indicatethat even with ARPUs below US$15 a month, operators can recoup their investmentwithin a reasonable amount of time.

Profitability can be enhanced by an “informal economy” effect that helps producehigher ARPUs than expected, given the low per capita GDP of African consumers. Alarge prepaid market also means that marginal costs involved in new customers arequickly covered to allow them to become lucrative to operators.

Site sharing and tower companies could offer African operators increased economiesof scale and improved profitability, although operators have shown resistance to thisidea up to now.

A profitable enterpriseTelecommunications companies have historically had high EBITDA margins. Themargins recorded by some African operators place them high up on the world rankingswhen it comes to profitability, with at least five African operators having EBITDAmargins above 50%.32

Not all African operators are seeing this kind of positive margin, and operatorsstruggling to compete in markets that are dominated by a single operator mayexperience significantly lower EBITDA margins.

| Challenges in the African market

32 Wireless Intelligence

Africa connected - A telecommunication’s growth story22

Telecommunicationsindustry response

African assets are attracting local and foreigninterestsEven with the challenges presented by the business environment on the continent,operators are keen to acquire assets and licenses.

The race to dominate the African market is being driven not only by potential growth,but also the ability to build synergies across a continent-wide network. However, ouranalysis shows that it may be challenging for those operators looking to enter Africa forthe first time. For those operators that have established themselves on the continent, thebusiness processes required to successfully operate a network and service the varyingneeds of the market, is institutional knowledge that will be hard to replicate.

The scale of regional operators also allows them to extract economies of scale thatenable them to procure infrastructure at costs that smaller operators can not.

From our research, market position across the continent is considered the key tosurvival. It is clear that the primary focus for operators at present is the acquisition ofcustomers. This acquisitive trend is likely to last for the next few years as more licensesbecome available and both established operators and new entrants vie to grow marketshare.

“The focus in Africa is onacquiring other players with aportfolio of network assets inorder to extend thegeographical footprint”

Mobile operator

< back | forward >

Africa connected – A telecommunication’s growth story 23

Consolidation is already happeningAfrican telecommunications has already seen some consolidation, with more expectedin the future. The market remains fragmented with less than 10 large operators andmore than 80 smaller operations (40% of the networks account for only 1% of thecontinent’s subscriber base).33 This suggests a large potential for consolidation, bothcross-border and within territories.

Markets that have five or more operators are likely to see some consolidation, either aslarge regional players compete for access to lucrative markets or as the number ofoperators is cut down through in-country consolidation.

Consolidation will not be confined to the mobile environment, even though this iswhere most of the activity will be concentrated. Mobile operators looking to buildconverged networks are acquiring fixed-line operators, as with the case with MTN’srecent acquistion of Ivory Coast landline operator Arobase Telecom.

There is also broader consolidation as telecoms operators look to expand their operationsinto related technology areas. This includes buying into ISPs as well as IT companies.

While we have seen the emergence of operators with considerable African coverage,no single operator has secured a dominant position on the continent. Even MTN andZain, which have the largest African footprint, have less than 20 territories each.There are, however, only 14 countries where none of the operators with the largestnumber of African networks have a presence.34

| Telecommunications industry response

“Due to the large number ofoperators in Africa, we will seevery soon a consolidation andthere will surely be operatorswho will try to joininternational operators. Biginternational operators likeMTN, Vodafone and Orangewill probably actively take partin this consolidation”

Mobile operator

“We have already seenconsolidation begin to takeplace. Although there are stillnew licenses being issued inmany African markets, andnew operators are coming tothe market, we expectconsolidation to gainmomentum. A number of largepan-African operators willdominate many of themarkets, but there will beroom for niche operators,addressing specific marketsegments and remainingprofitable”

Fixed line operator

33 Blycroft34 These large operators include MTN,

Vodafone/Vodacom/Safaricom, Zain, Millicom,Etisalat, Orascom, France Telecom/Orange

< back | forward >

Africa connected - A telecommunication’s growth story24

< back | forward >

“We foresee moreinfrastructure sharing in thefuture due to cost sensitivityon the part of new operatorscoming into markets. Manyoperators may choose totransfer the capex they wouldhave to incur into opex, andregulators may begin to forceor enable operators tocollaborate to a greaterdegree”

Mobile operator

“We believe that the Africanmarkets are each different,and therefore synergiesbetween countries are verydifficult to achieve and sharedservices will not work. This isvery different from our modelin other geographies where wesee more opportunities forshared services”

Mobile operator

The outsourcing model has not yet taken off inAfricaAccording to respondents interviewed, African operators wish to retain control of theirinfrastructure and are resistant to outsourcing their non-core activities.

However, there is some acceptance that in order to reach some of the outlying areas itmay be necessary to share physical infrastructure such as towers. To make theseventures more viable, operators may be forced to initially create a commoninfrastructure while estimating the viability of individual areas.

Operators with operations in multiple territories are also hesitant to centralizeoperations because of the potential for job losses in individual operations. The use ofoutsourced services is more prevalent in more mature markets as vendors look toreduce costs rather than simply acquire more customers.

The emergence of pure infrastructure companies demonstrates that infrastructureservices can be shared among a number of operators. However, our researchhighlights this is not the preferred route for growing companies as they require moredirect control over their base infrastructure. This may change in the future as marginpressure starts to impact and operators seek ways to reduce costs.

Alternative models to outsourcing present an opportunity for emerging operators toforge a broad coalition with some of the more vertically integrated vendors. Byleveraging a relationship with vendors able to control the supply chain, it should bepossible to cut the cost of deploying a network, introducing a low-cost model to theAfrican arena.

The cost advantage that Chinese vendors, for example, are bringing to the market canhelp address the issues surrounding rural infrastructure deployment. Already thesecompanies are winning deals across the continent with end-to-end contracts starting toemerge. This kind of service may gain in popularity as competition increases andoperators look for ways to boost their competitiveness.

| Telecommunications industry response

< back | forward >

Africa connected – A telecommunication’s growth story 25

| Telecommunications industry response

35 MTN Annual Report 2007

Operators are investing heavily ininfrastructure Due to lower maturity levels in market development, when compared with otherregions, a 20% ratio of capital expenditure to revenue is higher than Europe or theMiddle East (See Fig 3.1).

The difference, however, between Africa and Eastern Europe is not disproportionate,indicating that operators on the continent are investing the appropriate amount inrelation to the income they are receiving.

The scale of networks necessary to cover many of the more rural areas means thatoperators are expected to have to continue to invest heavily in the short term. Thisinvestment is part of the strategy required to deliver services to a rising subscriberbase and is essential for the continued success of the operators.

Our research shows that the biggest players on the continent are spending heavily inorder to ensure that their networks can cope with increased demand. MTN has raisedits capex/revenue rate from 19% in 2006 to 21% in 2007.35 Considering that this is onthe back of rising revenues, the monetary value of this investment has increasedsignificantly.

Operators are also contributing heavily to the development of undersea cables.

Africa connected - A telecommunication’s growth story26

| Telecommunications industry response

“In Europe, the decrease ofturnover per minute isassociated with highersubsidies and is compensatedby a rise in interconnectionearnings. In Africa, thedecrease of turnover perminute is associated to a risein the number of subscribers,which requires importantinvestments. Consequently,the capex on turnover ratio ishigher”

Mobile operator

< back | forward >

Fig 3.1: Quarterly mobile capex/revenue by region(%)36

30

25

20

15

10

5

0Q2

2006Q3

2006Q4

2006Q1

2007Q2

2007Q3

2007Q4

2007Q1

2008Q2

2008

Africa

Eastern Europe

Middle EastWestern Europe

Fig 3.2: Mobile operator capex per subscriber 200737

Operators Subscribers (m) Countries Capex/subMTN 49.8 16 US$35.7Vodacom 33.0 5 US$28.1Orascom 32.4 4 US$30.2Zain 30.2 15 US$42.1Vodafone 22.6 2 US$23.4

36 Wireless Intelligence37 Ernst & Young Analysis

Africa connected – A telecommunication’s growth story 27

| Telecommunications industry response

< back | forward >

Moves to improve ICT are taking place at alllevelsThe arrival of at least two, but probably three or more, undersea cable systems in thenext two to three years, should have a key impact on African telecommunications andon the broader African ICT market.

While SAT-3 provided a taste of the advantages of proper access to countries on thewest coast, East African countries have had limited access to reliable and cost-effectivebandwidth. The east coast of Africa is expected to benefit from new infrastructure withthe TEAMS cable system linking Kenya to the United Arab Emirates and the Seacomcable which will run down the eastern seaboard of the continent and link South Africa,Mozambique, Madagascar, Tanzania and Kenya with India and Europe.

Both the TEAMS and the Seacom cable systems should provide the impetus for vitalprice reductions in the cost of access to international bandwidth for both operatorsand customers alike. The open nature of these systems, where no single organizationcontrols access, may prove to be the single most important aspect oftelecommunication growth in Africa, as a lack of international gateways has inhibitedgrowth to date.

Down the west coast there is the Glo-One cable system linking Ghana and Nigeria andpotentially other countries to Europe. There are a number of other projects in variousstages of completion including the EASSy cable system down the east coast and theWest African Cable system.

The building of terrestrial links into these systems is equally important as it shouldeliminate the dependence of landlocked countries on satellite connectivity. However,satellite is expected to continue to play a part in connecting the continent, especially inremote areas where access to the fiber backbone will be challenging.

The amount of voice and data that will be carried by satellite should drop from the 80%that it stands at today. The final quantity carried by satellite will be determined by anumber of factors, including the pricing of fiber access, as well as the extent andreliability of networks inside individual African countries.

Africa connected - A telecommunication’s growth story28

| Telecommunications industry response

< back | forward >

“NGN’s will allow us to deploya wider range of products andservices for various marketsegments, moving towardstriple/quadruple-play serviceoffering and over time alsoconvergence”

Mobile operator

“Business customers’investment into fiber networkswill show high growthpotential. Given the new seacables in Western and EasternAfrica, even land lockedcountries are investing in fiberrings with access to the sea-cables as this is seen ascritical for growth bybusiness customers.

However, we do observe thatthe current activities in thisarea will lead to someovercapacities which will leadto a severe price competitionand, again, at the end of it wewill see consolidation”

Telecommunicationsconsultant

38 www.manypossibilities.net39 Ernst & Young Analysis

LondonEngland

MarseilleFrance

ChipionaSpain

SesimbraPortugal

CasablancaMorocco

AltavistaCanary Islands

DakarSenegal

Port SudanSudan

MassiwaEritrea

Djiboutu

MogadishuSomalia

MombasaKenya

Dar Es SalaamTanzania

MaputoMozambique

MtunziniSouth Africa

ToliaraMadagascar

Baie du JacobetMauritius

St PaulReunion

MelkbosstrandSouth Africa

FujairahUnited AradEmirates

MumbaiIndia

CochinIndia

DoualaCameroonLibrevileGabon

Pointe NoirCongo

Abi

jan,

Cot

e D

’Ivoi

reAc

cra,

Gha

naCo

tono

u, B

enin

Lago

s, Nige

ria

Bonny

, Nige

ria

Cacuaco, AngolaLuanda, Angola

Sub-Saharan Africaundersea cables (2010)

SAT3/SAFE

TEAMs

Seacom

MaIN OnE

EASSy

WACS

120 gigabits

120/1200 gigabits

1280 gigabits

1280 gigabits

1400 gigabits

3840 gigabits

Fig 3.3: Prospective African submarine cables38

Fig 3.4: TImeline of submarine cables with landing points39

Early2009

Mid2009

Mid2010

Late2010

Glo One: UK, Senegal, Nigeria

EASSy: Sudan, Djibouti, SomaliaKenya, Tanzania, Madagascar,Mozambique, South AfricaAWCC: UK, South AfricaMaIN OnE: Portugal, Ghana,Nigeria

Seacom: Europe, India, Kenya,Tanzania, Mozambique,Madagascar, South Africa

Infinity: Portugal, Senegal,Ghana, Nigeria, Cameroon,Angola, South Africa

TEAMS: Kenya, UAE

Africa connected – A telecommunication’s growth story 29

| Telecommunications industry response

< back | forward >

40 Ernst & Young Analysis

“3G has the biggest growthpotential in African countries,but in four to five years’ time”

Mobile operator

3G technologies have the greatest potentialThe strong investment by operators in GSM technologies should make W-CDMA thenatural choice for rolling out broadband access to the wider population. It is expected,however, that operators will choose a variety of technologies to meet the needs of theindividual markets. This could include a mixture of W-CDMA, CDMA EVDO and WiMAXtechnologies, depending on the individual specifics of each country. These could includelicense conditions as well as spectrum availability. The Ugandan regulator has revealedthat the country is running out of space in the GSM bands and if this is replicated inother countries, it could create opportunities for other wireless broadbandtechnologies.

While WiMAX is garnering attention at the moment, it is not expected to have a large-scale impact on the market. In particular, it has been hampered by the cost of thetechnology, which can not yet compete with GSM or CDMA, as well as by the failure ofthe WiMAX vendors to meet their own deadlines for delivering mobile WiMAX devices.

There are concerns that over-licensing on the part of regulators in some countries mayresult in the creation of sub-scale markets. It is expected that operators will divide intotwo main groups, those looking to offer a converged service and those that will retain avoice-only offering. This may evolve into a contest between low-cost operators on oneside and converged, value-added operators on the other.

Date

Aug-08

Apr-08

Mar-08

Sep-07Sep-07Jul-07Jul-06

Country

Malawi

Ghana

Kenya

EgyptUgandaUgandaMauritania

Operator

Orascom Tech

Globacom

Safaricom

EgyNet Warid TelecomMTN UgandaChinguetel

Notes

Network connects drilling rigs to homeofficeUS$50.1m license cost; plans to investUS$200m in the networkLong-standing client/vendor relationship

Deployment in Sharm-El-SheikhCommercial by YE 2007National networkUnified license at US$32 per head

Fig 3.5: Recent wireless broadband 3G license awards in selected markets40

Africa connected - A telecommunication’s growth story30

| Telecommunications industry response

“20% of people have a bankaccount in Senegal and I thinkservices such as micropayments could be quitepopular in near future”

Mobile operator

“Mobile banking, or morespecifically mobile moneytransfer, holds great potentialas a converged service”

Mobile operator

< back | forward >

41 Consultative Group to Assist the Poor/The WorldBank and United Nations Foundation

Africa has led the way in mobile paymentsThe failure of the formal banking sector to penetrate the mass African market hasopened the door for mobile operators to build sophisticated and successful mobilepayment services. In this respect, Africa has taken the lead internationally and the M-Pesa service launched by Safaricom in Kenya and Wizzit in South Africa are twoexamples of this.

Mobile banking offers a number of key advantages to users, specifically a lowtransaction cost and the removal of the need for a physical banking infrastructure. Thestrong brand presence that mobile operators have throughout their coverage areasmakes it easier for them to engage potential clients than is the case with traditionalbanks. Handsets can also be configured to deal with payments and existing mobilebilling systems are especially suited to micro-transactions.

In order to offer these services, operators need to collaborate with existing financialservices companies. These services usually combine a mobile element with atraditional banking instrument such as a debit card.

Value-added services can also include the provision of content, as well as morepractical services such as education and healthcare information. The mobile channeloffers one of the greatest opportunities for content providers to deliver music andvideo in digital format to the market. However, the sophistication of the averagehandset on the continent may prove to be an obstacle in providing this kind of service.

Fig 3.6: M-banking as a new banking channel41

Banking activities of WIZZIT users by % channel type

Money transfer

Balance checking

Electronic bank transfer

Airtime purchase

Pay for electricity

Pay store accounts

0% 20% 40% 60% 80% 100%

Handset ATM Bank Store/office

Africa connected – A telecommunication’s growth story 31

< back | forward >

Africa connected - A telecommunication’s growth story32

The way forward in theAfrican telecommunicationsmarket

Lifting the veil on AfricaAfrica is expected to be a key focus of global telecommunications operators andvendors over the next five years. This is being assisted by the realization that thecontinent is open for business and not simply a market where only the brave venture.

Operators that have African experience should have a decided advantage over newentrants. Complexities in dealing with multiple regulatory environments and rolling outand maintaining infrastructure in challenging environments is not something that canbe learned overnight.

There are relatively few countries that do not have one of the big regional or globaloperators already present, so the chance that new entrants would have to competedirectly with an established player is high. Additionally, with these operators looking toexpand their reach, any new license is likely to attract their attention and competingagainst them for licenses may be difficult.

Those countries that have established independent regulators and switched to unifiedlicenses are likely to find themselves at the forefront of African telecommunications.

The second coming of the fixed lineThe time is coming for operators in many parts of the continent to disregard theirexisting fixed line infrastructure and embrace the next generation of convergednetworks.

With the imminent launch of several submarine cable systems over the next threeyears, the bandwidth drought that has plagued the continent should be over. There isalready tremendous investment in new fiber optic networks across the continent.These networks, in conjunction with next generation wireless technologies, may renderalmost all legacy wireline infrastructure obsolete.

The opportunity will be there for larger consumers of bandwidth, such as banks andgovernment, to access the fiber networks directly, with almost every other user beingable to get sufficient bandwidth via wireless links.

< back | forward >

< back | forward >

Unified licensing takes holdRegulators in Africa need to move away from technology-specific licensing systemsand towards unified licenses. These licenses will allow all operators to compete on anequal footing, choose the most appropriate system for the environment where theyare looking to operate and counteract the propensity of incumbent operators tohamper the growth of their rivals.

Unified licenses will allow mobile operators to branch out into converged telecoms bybuilding out their own fixed-line networks. This form of licensing also frees upresources within the regulatory environment as it moves the focus of regulation awayfrom the judging and issuing of licenses and refocuses their attention on spectrummanagement and consumer protection.

Low-cost telecommunicationsThe existence of large numbers of people that are not able to afford the current cost oftelecommunications has set the stage for the emergence of true low-cost operators.The new low cost operator will have to outsource extensively and leverage offrelationships with its vendors in order to reduce costs.

Currently, emerging low-cost operators are more focused on the providing communityservices than full mobile services, as much of their target audience is rural anduniversal coverage is not economically viable. However, as urbanization continues,these low-cost operators may expand their operations and compete directly withexisting networks.

The winners in this space should be those operators able to keep their costs at anabsolute minimum while still growing their subscriber base. The emergence of asuccessful low-cost operator in Africa should force many of the other operators tofundamentally rethink their approach to doing business on the continent.

33

| The way forward in the African telecommunications market

Africa connected – A telecommunication’s growth story

Africa connected - A telecommunication’s growth story34

Key success factors

< back | forward >

Operators have a clear understanding of the African markets and have developed theiroperating models accordingly while they continue to look for new opportunities.However, operators do face challenges going forward including regulatory compliance,pricing issues, convergence and consolidation.

Operational efficiency of growing importanceOperational efficiency is critical to long-term success as voice ARPUs decline underincreasing pressure from the competition and there is uncertain demand for newservices. Even though many operators are benefiting from high margins at present,those that are able to practice cost efficiency while still investing in infrastructure, areexpected to prove to be the most successful.

Going forward, African operators will need to optimize performance, cut costs, preventrevenue leakage and increase operational efficiency to maintain profit margins.

Operators experiencing high growth, undertaking aggressive consolidation andacquisitions and outsourcing non-core activities may be at risk of suffering internalcontrol failures. This needs to be addressed with enterprise-wide risk assessments andthe appropriate processes and systems to avoid the threat of organizationalbreakdown.

As markets reach saturation, the need to share facilities should become more urgent.While this is likely to start with the sharing of towers in rural areas, as marketpressures increase and coverage becomes less of a competitive advantage, operatorsmay start looking at sharing infrastructure as a means of containing costs.

Increasing investment from telecommunications vendors in alternative energysolutions could prove to be beneficial for operators as they will be able to deploycoverage in areas that do not have power without having to rely completely on dieselgenerators.

Government must play its partAfrican governments will need to play their part to encourage continued growth in thetelecommunications sector across the continent. The institution of independentregulators should create the foundation for business, as regulators inevitably play arole in setting the competitive environment. Tax burdens in the region need to bereduced to help operators minimise costs and increase the potential market.

Africa connected – A telecommunication’s growth story 35

| Key success factors

< back | forward >

Current State

• Cost sensitive• Immature customer base• Little loyalty to network• Predominantly pre-paid

• Availability of airtime• Delivery of low-cost voice services• Cross border roaming services• Embryonic value added services

• Voice focused• Coverage is competitive differentiator

• State and private• Diverse set of small and large operators

• Talent scarce in technical and management fields

Future State

• Mature, demanding customers• Performance sensitive• Increased brand loyalty• Consuming both voice and data services• Larger post paid base

• Value-added services• Converged offering• Sophisticated customer retention strategies• Enterprise services

• Fixed and wireless networks• Data and voice play complementary roles• Quality of service seen as competitive

differentiator

• Almost entirely private with some state shareholding

• Market dominated by large operators

• Long-term staff retained, training akey focus

Customer

Proposition

Network

Ownership

People

Mergers and consolidation need to beaddressedThe African telecommunications market is characterized by increasing transactionand acquisition activity, and operators can come under intensive competitivepressures to find the right partner or target quickly.

In a market that includes a very diverse set of countries, it is crucial that operatorsunderstand the operating environment that they are acquiring and accurately valuethe transaction. They are also challenged to extract post-merger synergies timeouslywithout compromising operational efficiency.

3GPP (3rd Generation Partnership Project) is a collaboration between groups oftelecommunications associations, to produce globally applicable 3G mobile phonesystem technical specifications based on evolved GSM core networks and radio accesstechnologies.

ARPU (Average Revenue Per User) is a key performance indicator used by mobileoperators. ARPU represents total revenue divided by the weighted average number ofcustomers during the same period, expressed monthly.

CDMA (Code Division Multiple Access) is a second generation mobile technologystandard for digital transmission of radio signals that uses digital encoding and spread-spectrum RF techniques to let multiple users share the same RF channel.

Converged ICT operators are those offering voice and data services including value-added network services.

Fiber optic cable is a bundle of thin filaments of glass or other transparent materialsused as the medium for transmitting coded light pulses that represent data, images orsound.

GSM (Global System for Mobile Communications) is an open digital cellular technologyused for transmitting mobile voice and data services. It is the most widely used 2Gmobile technology standard in Africa and worldwide.

ICT refers to information and communication technology.

International gateway is a telephone switch that forms the gateway between a nationaltelephone network and one or more other international gateway exchanges, thusproviding cross-border connectivity.

Africa connected - A telecommunication’s growth story36

Glossary

< back | forward >

Africa connected – A telecommunication’s growth story 37

< back | forward >

| Glossary

Mobile phone penetration rate is a term generally used to describe the number ofactive mobile phone numbers (usually as a percentage) within a specific population.

NEPAD is the New Partnership for Africa Development, a development programdesigned to provide an overarching vision and policy framework for acceleratingeconomic co-operation and integration among African countries.

NGN (Next-Generation Network) represents the convergence of traditional publicswitched telephone networks (PSTN), and data networks, into a common packageinfrastructure. The architecture reconfigures the central office functionality of abusiness, pushing it to the edge of the network, thereby creating a distributedinfrastructure that can incorporate new services.

Roaming is using a mobile phone outside a subscriber’s home service area.

SNO (Second Network Operator) is a fixed line operator licensed to providecompetition to an incumbent operator.

WiMAX (Worldwide interoperability for Microwave Access) is a wireless accesstechnology based on IEEE 802.16 standards, that offers greater speed and coveragecompared to WiFi (wireless fidelity), which in turn is based on an earlier 802.11standard. Mobile WiMAX is an amendment of WiMAX that includes better support forquality of service.

Wireless is a method of transmission other than along wirelines, including, forexample, cellular, satellite and microwave.

Wireline is traditional telecommunications transmitted and received via, for example,traditional telephone lines and cables.

Africa connected – A telecommunication’s growth story38

< back | forward >

Notes

Africa connected – A telecommunication’s growth story 39

References

1. International Telecommunications Union2. Wireless Intelligence3. United Nations Statistics division4. Global Mobile Tax Review 2006 -2007, GSM Association, Deloitte5. Starcomms Analysis, CSL Research & Strategy 6. Communications Technologies Handbook, BMI-T, 20087. Vodacom Annual Report 20088. Blycroft9. State of World Population 2007, United Nations Development

Programme 10. Uganda legislators approve US$75 million for data backbone,

Computerworld Africa, 10 December 2008 11. Usage and population statistics, Internet World Stats12. World Bank13. Poor electricity supply hits ICT growth, University World

News, 27 April 200814. MTN May Introduce $12 Branded Handsets in Africa Next

Year, Bloomberg, 18 November 200815. Harnessing the Internet for development, Africa Renewal,

July 200616. Will EASSy make African bandwidth affordable?,

Tectonic, 9 March 200617. Mobile Price War in Kenya Reaches Fever Pitch, IDG

News Service, 21 May 2008 18. Taxation and the Growth of Mobile in East Africa, GSM

Association19. Taxation and the growth of mobile services in

sub-Saharan Africa, GSM Association20. MTN Annual Report 200721. www.manypossibilities.net22. Consultative Group to Assist the Poor/The World

Bank and United Nations Foundation

< back

Ernst & Young

Assurance | Tax | Transactions | Advisory

About Ernst & YoungErnst & Young is a global leader in assurance, tax,transaction and advisory services. Worldwide, our130,000 people are united by our shared valuesand an unwavering commitment to quality. Wemake a difference by helping our people, ourclients and our wider communities achievepotential.