afs best practices leadership council webinar series ... · 2019/04/25 · commercial lending...

TRANSCRIPT

April 25, 2019

Winners and LosersCommercial Lending Dynamics

Green Lending

AFS Best Practices Leadership Council Webinar Series Presents:

Special Feature:

©2019 Automated Financial Systems, Inc. All Rights Reserved. AFS and all AFS product trademarks Are registered trademarks of Automated Financial Systems, Inc. The content of this document represents confidential and proprietary information of AFS. This information may not be disclosed to any third party, other than the direct addressee and its employees, agents, and representatives. The infringement of this prohibition may violate AFS proprietary and trade secret rights with resulting irreparable damage to AFS. Your cooperation is requested and appreciated. Thank you for your help in this matter. AFS 123 Summit Drive, Exton, Pennsylvania 19341. Telephone (610) 524‐9300 Fax (610) 524‐7977

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.2April 25, 2019

Achieving Success through Execution

Ask Questions

We want to hear from you. Please use the chat area to ask questions. We will answer your questions at the conclusion of the prepared remarks.

Please use this area to ask your questions.

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.3April 25, 2019

Achieving Success through Execution

AFS Pricing Dashboard by the Numbers

$1.2 TrillionThe Pricing Dashboard database already totals over $1.2 trillion in committed exposure, with broad coverage and depth across C&I and Commercial Real Estate product categories.

80,000 20+The database is seeded with over 80,000 new or renewed loans per quarter, creating a robust set of historical performance metrics to model and analyze.

The Pricing Dashboard contains a robust offering of measures and dimensions, allowing banks to tailor the analysis to their unique specifications and create balanced scorecards of growth, pricing, and credit risk performance.

Do you want to know… How your portfolio compares to peers? What geographies have tailwinds for loan growth? What sectors have the most pricing volatility? What are spread and fee levels for comparable credit?

The Pricing Dashboard gives you the tools and information you need to stay ahead of the curve.

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.4April 25, 2019

Achieving Success through Execution

Agenda

Balance Growth

Total commercial loan balances increased +1.6% in 1Q19, well above the pace reported in the same quarter a year earlierFor bilateral loans, balance growth trends continued to diverge between the large and small deals

New/Renewed Vol.

Spread Pricing

Fee Pricing

Special Topic

New bilateral volume continued to trend upwards in MarchTexas surpassed California as the largest state for new/renewed participation volume

Spread pricing was flat year over year for new loansThe average spread for renewals was up in March from a year ago

Total annualized fee performance in March was up slightly from a year ago

This month we examine the loan growth, spread pricing, and credit risk characteristics of “Green” industry segments

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.5April 25, 2019

Achieving Success through Execution

Markets Are Giving Mixed Signals

‐3.0‐2.0‐1.00.01.02.03.04.05.0

Chan

ge in Rea

l GDP

%

Real GDP Growth accelerated in 2018...

0.0

1.0

2.0

3.0

4.0

5.0

%

Fed Funds Interest Rate$1‐5M Fixed Loans

LIBOR‐Equ. Spread$1‐5M Fixed Loans

...and spreads remain stagnant despite rising interest rates

0.0

2.0

4.0

6.0

8.0

10.0

12.0

U.S. Nat'l Un

employmen

t %

... and unemployment remains at historic lows.

‐2.0‐1.00.01.02.03.04.05.0

10‐Yr M

inus 3‐M

th Treasury

The yield curve inverted in March...

Real GDP Source: Bureau of Economic Analysis (BEA)U.S. Unemployment Rate Source: Bureau of Labor Statistics (BLS)Yield Curve Source: Federal Reserve Bank of St. LouisInterest rate and LIBOR‐Equivalent Spread Source: AFS Pricing Dashboard

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.6April 25, 2019

Achieving Success through Execution

Commercial Lending in the News

“U.S. banks have delivered a mixed bag of first‐quarter financial results so far — but that’s probably the sector’s best this year, especially if the Federal Reserve does not increase interest rates at all.

With the Fed already signaling that it did not expect to hike interest rates this year, the banking industry’s ability to generate higher profits in the coming months may be limited.”

—CNBC, April 16, 2019

“Small‐business owners are turning to online lenders for financing much more frequently than they did even two years ago, the Federal Reserve Banks found in a new survey.

The findings suggest that more traditional lenders risk being left behind if they do not match the faster processes that many online lenders offer.

‘We’re seeing essentially low‐credit‐risk firms going to very conventional channels, and lower‐risk channels, ones that might have a longer wait time, but do offer better [lower] rates.’”

—American Banker, April 16, 2019

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.7April 25, 2019

Achieving Success through Execution

100

150

200

250

300

350New Renewed 10‐Year Treasuries

LIBOR‐Equivalent Spread (in BPS) TrendAll Loan Types

$0$5

$10$15$20$25$30$35$40

New Renewed

New and Renewed Loans Trend ($ Billions)All Loan Types

Commercial Loan Market Overview: March 2019

Source: AFS Pricing Dashboard – March 2019

Mar 20130.09%

Mar 20141.98%

Mar 20151.38%

Mar 20162.01%

Mar 2017‐0.02%

Mar 20180.33%

Mar 20191.58%

‐1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

Percen

t Growth

Growth in Outstandings ‐ Quarterly Trend(Quarter‐over‐Quarter Growth Rates)

0

5

10

15

20

25

30

35

2018* 2019*

Total Fees Upfront Fees

Total Fees Paid (in BPS) ‐ Bilateral LoansYear‐over‐Year Comparison

* Based on Comparative Jan‐Mar Periods

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.8April 25, 2019

Achieving Success through Execution

Bilateral Loan Growth Concentrated in the Larger DealsParticipations Up Broadly Across the Size Spectrum

Source: AFS Pricing Dashboard – March 2019

‐2.0%‐1.0%0.0%1.0%2.0%3.0%4.0%5.0%6.0%7.0%

Percen

t Growth

Bilateral Loans Participations

Growth in Outstandings ‐ Quarterly Trend(Quarter‐over‐Quarter Growth Rates)

‐1.45% ‐0.87%

0.86%1.96% 1.72%

‐2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

< $1M $1M to< $5M

$5M to< $25M

>= $25M CRE

Percen

t Growth

Growth in Outstandings ‐ Dec 2018 vs. Mar 2019Bilateral Loans

C&I Bilateral Loans

0.86%

8.52%

2.72%1.40%

3.18%

‐2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

< $1M $1M to< $5M

$5M to< $25M

>= $25M CRE

Percen

t Growth

Growth in Outstandings ‐ Dec 2018 vs. Mar 2019Participations

C&I Participations

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.9April 25, 2019

Achieving Success through Execution

CRE Balance Growth Accelerated in 1Q19

Source: AFS Pricing Dashboard – March 2019

‐5.0%

0.0%

5.0%

10.0%

15.0%

Percen

t Growth

Bilateral Loans Participations

Growth in Outstandings ‐ Quarterly Trend ‐ CRE(Quarter‐over‐Quarter Growth Rates)

‐0.38% ‐0.45%

1.52%

4.57%

‐10.0%

‐5.0%

0.0%

5.0%

10.0%

15.0%

< $1M $1M to< $5M

$5M to< $25M

>= $25M

Percen

t Growth

Growth in Outstandings ‐ Dec 2018 vs. Mar 2019Bilateral Loans ‐ CRE

‐5.17%

11.45%

1.96%4.21%

‐10.0%

‐5.0%

0.0%

5.0%

10.0%

15.0%

< $1M $1M to< $5M

$5M to< $25M

>= $25M

Percen

t Growth

Growth in Outstandings ‐ Dec 2018 vs. Mar 2019Participations ‐ CRE

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.10April 25, 2019

Achieving Success through Execution

Year‐Over‐Year Loan Growth Continues to Trend Upwards

Source: AFS Pricing Dashboard – March 2019

The charts below plot year‐over‐year loan growth rates for each month, allowing us to better account for seasonal effects on the loan growth trend. Year‐over‐year commercial loan balance growth in March 2019 was 5.6%, the highest growth rate seen since 2016.

‐5%

0%

5%

10%

15%

20%

25%

30%

% Growth Ye

ar‐ove

r‐Year

Growth in Outstandings Trend by Month(Year‐over‐Year Growth Rates)

All Loan Types (Bilateral Loans & Participations)

‐5%

0%

5%

10%

15%

20%

25%

30%

% Growth Ye

ar‐ove

r‐Year

Growth in Outstandings Trend by Month(Year‐over‐Year Growth Rates)

Bilateral Loans Participations

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.11April 25, 2019

Achieving Success through Execution

Texas is a High‐Growth Region for Both Bilateral Loans and Participations

Note: Geographic data refers to the location of the borrower, not necessarily the bank booking the loan. Outstandings of at least $3 billion in the base period is required. Source: AFS Pricing Dashboard – March 2019

6.5%

5.9%

2.6%

1.7%

1.5%

1.4%

‐0.3%

‐1.4%

‐2.8%

‐3.8%

‐4.6%

South Carolina

Texas

North Carolina

GeorgiaNew York

New Jersey

ColoradoWisconsin

NevadaKentucky

Growth in Outstandings ‐ Dec 2018 vs. Mar 2019All Loan Types

Nat'l Avg

3.4%

3.4%

1.9%

0.8%

0.7%

1.0%

‐1.0%

‐1.3%

‐1.4%

‐1.5%

‐4.9%

Texas

MassachusettsFlorida

New York

California

Tennessee

Oregon

OhioPennsylvania

Wisconsin

Growth in Outstandings ‐ Dec 2018 vs. Mar 2019Bilateral Loans

Nat'l Avg

8.0%

5.2%

3.9%

3.6%

3.1%

2.5%

‐1.9%

‐1.9%

‐2.1%

‐2.3%

‐5.2%

Texas

PennsylvaniaIllinoisGeorgia

New York

New JerseyColoradoCalifornia

Massachusetts

Florida

Growth in Outstandings ‐ Dec 2018 vs. Mar 2019Participations

Nat'l Avg

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.12April 25, 2019

Achieving Success through Execution

* Core Based Statistical Areas (CBSAs)Note: Geographic data refers to the location of the borrower, not necessarily the bank booking the loan.Source: AFS Pricing Dashboard – March 2019

Drilling Down to the CBSA* Level

1.94%

4.13%

1.39%

2.75%

‐0.83% ‐1.05%‐2.0%

‐1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%Pe

rcen

t Growth

Growth in Outstandings ‐ BilateralFlorida

Dec 2018 to Mar 2019

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.13April 25, 2019

Achieving Success through Execution

Note: Geographic data refers to the location of the borrower, not necessarily the bank booking the loan. Source: AFS Pricing Dashboard – March 2019

Bilateral Loans Up in 1Q19 Across Most States

Top 5 States1. Florida2. Texas3. California4. Massachusetts5. New York

Bottom 5 States1. Pennsylvania2. Ohio3. Wisconsin4. Nevada5. Iowa

ALARAZ

CA CO

CT

DCDE

FL

GA

IA

ID

IL INKS KY

LA

MA

MD

ME

MI

MN

MO

MS

MT

NC

ND

NE

NH

NJ

NM

NV

NY

OH

OK

OR

PARI

SC

SD

TN

TX

UTVA

VTWA

WI

WV

WY

Growth in OutstandingsDec 2018 vs. Mar 2019

Bilateral Loans

Negative Growth$0 to $100M$100M to $250M $250M to $500M Greater‐than $500MInsufficient Data

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.14April 25, 2019

Achieving Success through Execution

Note: Geographic data refers to the location of the borrower, not necessarily the bank booking the loan. Source: AFS Pricing Dashboard – March 2019

Participation Balances Up in 1Q19 Across the Majority of States

Top 5 States1. Texas2. New York3. Pennsylvania4. Maine5. Illinois

Bottom 5 States1. California2. Florida3. Arkansas4. Kentucky5. Massachusetts

ALARAZ

CA CO

CT

DCDE

FL

GA

IA

ID

IL INKS KY

LA

MA

MD

ME

MI

MN

MO

MS

MT

NC

ND

NE

NH

NJ

NM

NV

NY

OH

OK

OR

PARI

SC

SD

TN

TX

UTVA

VTWA

WI

WV

WY

Growth in OutstandingsDec 2018 vs. Mar 2019

Participations

Negative Growth$0 to $100M$100M to $250M $250M to $500M Greater‐than $500MInsufficient Data

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.15April 25, 2019

Achieving Success through Execution

GDP and Loan Growth: Is There a Correlation?

Total commercial loan growth for the Top 10 CBSAs* in terms of GDP remains well ahead of the rest of the country.

* Top 10 Core Based Statistical Areas (CBSAs) based on contribution to total U.S. Real GDP. Geographic data refers to the location of the borrower, not necessarily the bank booking the loan. Source: AFS Pricing Dashboard – March 2019Real GDP data sourced from the Bureau of Economic Analysis (BEA)

2.9%4.6% 5.2% 5.2% 5.6% 6.4% 7.1%

8.3% 8.9%10.9%

12.4%

15.2%

17.4%

1.3%2.5% 2.2% 2.5% 2.1% 1.9%

1.5% 1.5% 1.7% 2.3% 2.5%

4.5%5.6%

0.0%2.0%4.0%6.0%8.0%

10.0%12.0%14.0%16.0%18.0%20.0%

% Growth

Growth in Outstandings ‐ December 2015 BaselineTop 10 CBSAs vs. All Other Regions

Top 10 CBSAs

All Other Regions

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.16April 25, 2019

Achieving Success through Execution

Manufacturing Sectors Fuel Balance Growth for Both Bilateral Loans and Participations

Note: Industry categories based on North American Industry Classification System (NAICS). Outstandings of at least $3 billion in the base period is required.Source: AFS Pricing Dashboard – March 2019

8.1%

6.0%

3.6%

1.6%

1.5%

1.4%

‐0.6%

‐0.7%

‐1.8%

‐2.6%

‐7.7%

Manufacturing (Wood, Chem)

Manufacturing (Machinery, Elec)

Professional, Scientific, & Tech Retail Trade (Motor, Elec, Bldg)

Finance & Insurance

Arts, Entertainment, & Recreation

Admin, Support, Waste Mgmt Transportation (Air, Water, Truck)

Public Administration

Agriculture

Growth in Outstandings ‐ Dec 2018 vs. Mar 2019All Loan Types

All Industries Avg

10.9%

9.0%

5.8%

4.6%

1.3%

1.0%

‐1.9%

‐2.8%

‐3.1%

‐4.8%

‐9.3%

Utilities

Manufacturing (Wood, Chem)

Manufacturing (Machinery, Elec)

Professional, Scientific, & Tech

Finance & Insurance

Arts, Entertainment, & Recreation

Public Administration Admin, Support, Waste Mgmt

Manufacturing (Food, Bev, Apparel) Agriculture

Growth in Outstandings ‐ Dec 2018 vs. Mar 2019Bilateral Loans

All Industries Avg

7.4%

7.4%

7.1%

6.1%

1.8%

2.5%

1.6%

1.5%

1.5%

‐4.4%

‐6.4%

Manufacturing (Food, Bev, Apparel) Manufacturing (Wood, Chem)

Retail Trade (Motor, Elec, Bldg)

Manufacturing (Machinery, Elec) Health Care & Social Assistance

Finance & Insurance Arts, Entertainment, & Recreation

Admin, Support, Waste Mgmt

Transportation (Air, Water, Truck) Utilities

Growth in Outstandings ‐ Dec 2018 vs. Mar 2019Participations

All Industries Avg

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.17April 25, 2019

Achieving Success through Execution

Note: Industry categories based on North American Industry Classification System (NAICS).Source: AFS Pricing Dashboard – March 2019

Drilling Down to the 6‐Digit NAICS Level

5.81%

10.48%

3.72%

16.87%

‐1.85%‐5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

33Manufacturing

(Machinery, Elec)

331Primary MetalManufacturing

331210Iron & Steel Pipe

& TubeManufacturingfrom Purchased

Steel

331318Other AluminumRolling, Drawing,

& Extruding

331222Steel WireDrawing

Percen

t Growth

Growth in Outstandings ‐ BilateralManufacturing (Machinery, Elec)

Dec 2018 to Mar 2019

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.18April 25, 2019

Achieving Success through Execution

100

150

200

250

300

350

400New Renewed 10‐Year Treasuries

LIBOR‐Equivalent Spreads (in BPS) TrendBilateral Loans

$0

$5

$10

$15

$20

$25New Renewed

New and Renewed Loan Volume ($ Billions)Bilateral Loans

New Bilateral Volume Decreased from a Year Ago…While Spreads Narrowed Over the Same Period

Source: AFS Pricing Dashboard – March 2019

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.19April 25, 2019

Achieving Success through Execution

Volume vs. Spread Pricing: New/Renewed Bilateral LoansState and Industry Detail for the Most Recent 6‐Month Period

Note: Geographic data refers to the location of the borrower, not necessarily the bank booking the loan. Industry categories based on North American Industry Classification System (NAICS).Source: AFS Pricing Dashboard – March 2019

$27.3

$16.5

$7.6

$6.4

$6.4

$5.6

$5.6

$4.7

$4.1

$3.9

California

New York

Florida

Ohio

Texas

Pennsylvania

Minnesota

Maryland

New Jersey

North Carolina

Top 10 States New/Renewed Volume Oct 2018 to Mar 2019 Bilateral Loans

$29.6

$13.5

$9.4

$6.4

$5.8

$4.6

$3.9

$3.3

$2.9

$2.7

Finance & Insurance

Wholesale Trade

Manufacturing (Machinery, Elec)

Health Care & Social Assistance

Retail Trade (Motor, Elec, Bldg)

Accommodation & Food Services

Professional, Scientific, & Tech

Manufacturing (Wood, Chem)

Information Manufacturing (Food, Bev, Apparel)

Top 10 C&I Industries New/Renewed Volume Oct 2018 to Mar 2019 Bilateral Loans

201

161

170

193

207

202

242

235

185

200

159

Finance & Insurance

Wholesale Trade Manufacturing (Machinery, Elec)

Health Care & Social Assistance Retail Trade (Motor, Elec, Bldg)

Accommodation & Food Services Professional, Scientific, & Tech Manufacturing (Wood, Chem)

Information Manufacturing (Food, Bev, Apparel)

Top 10 C&I Industries New/Renewed Volume ‐ LIBOR‐Equ. Spread Bilateral Loans

All Industries Avg

210

218

214

223

220

202

218

167

184

218

226

CaliforniaNew York

Florida

OhioTexas

PennsylvaniaMinnesotaMaryland

New Jersey

North Carolina

Top 10 States New/Renewed Volume ‐ LIBOR‐Equ. Spread Bilateral Loans

Nat'l Avg

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.20April 25, 2019

Achieving Success through Execution

100

150

200

250

300

350

400New Renewed 10‐Year Treasuries

LIBOR‐Equivalent Spreads (in BPS) TrendParticipations

$0

$5

$10

$15

$20

$25New Renewed

New and Renewed Loan Volume ($ Billions)Participations

New Participation Volume Continued to Fall in 1Q19…While Spreads Increased M/M and Y/Y

Source: AFS Pricing Dashboard – March 2019

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.21April 25, 2019

Achieving Success through Execution

Volume vs. Spread Pricing: New/Renewed ParticipationsState and Industry Detail for the Most Recent 6‐Month Period

Note: Geographic data refers to the location of the borrower, not necessarily the bank booking the loan. Industry categories based on North American Industry Classification System (NAICS).Source: AFS Pricing Dashboard – March 2019

$11.1

$10.8

$8.7

$5.8

$5.3

$4.6

$4.4

$4.2

$3.2

$2.7

Texas

California

New York

Pennsylvania

Illinois

Florida

Georgia

Ohio

Massachusetts

Maryland

Top 10 States New/Renewed Volume Oct 2018 to Mar 2019 Participations

$12.2

$10.3

$6.8

$6.7

$5.4

$5.1

$5.0

$4.3

$3.4

$3.3

Finance & Insurance

Manufacturing (Machinery, Elec)

Mining, Oil & Gas

Wholesale Trade

Utilities

Information

Manufacturing (Wood, Chem)

Retail Trade (Motor, Elec, Bldg)

Transportation (Air, Water, Truck)

Professional, Scientific, & Tech

Top 10 C&I Industries New/Renewed Volume Oct 2018 to Mar 2019 Participations

230

170

184

148

148184

191

152

162

197

188

Texas

California

New YorkPennsylvania

Illinois

Florida

GeorgiaOhio

Massachusetts

Maryland

Top 10 States New/Renewed Volume ‐ LIBOR‐Equ. Spread Participations

Nat'l Avg

174140

253

174

153

184152

177

168

202

182

Finance & Insurance

Manufacturing (Machinery, Elec) Mining, Oil & Gas

Wholesale Trade

Utilities

Information Manufacturing (Wood, Chem)

Retail Trade (Motor, Elec, Bldg)

Transportation (Air, Water, Truck) Professional, Scientific, & Tech

Top 10 C&I Industries New/Renewed Volume ‐ LIBOR‐Equ. Spread Participations

All Industries Avg

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.22April 25, 2019

Achieving Success through Execution

Total Annualized Fee Performance in March Up Slightly from the Same Period a Year Ago

Note: Geographic data refers to the location of the borrower, not necessarily the bank booking the loan. Industry categories based on North American Industry Classification System (NAICS).Source: AFS Pricing Dashboard – March 2019

0

5

10

15

20

25

30

35

2018* 2019*

Total Fees Upfront Fees

Total Fees Paid (in BPS) ‐ Bilateral LoansYear‐over‐Year Comparison

* Based on Comparative Jan‐Mar Periods

05

101520253035

Eastern

Midwest

Middle

Atlantic

Northea

st

South

Southw

est

West

Western

Midwest

2018* 2019*

Total Upfront Fees Paid (in BPS) Year‐over‐Year Comparison ‐ By Geographic Region

* Based on Comparative Jan‐Mar Periods

05

101520253035

Inform

ation

Utilities

Fina

nce &

Insuranc

e

Admin, S

uppo

rt,

Waste M

gmt,

& Rem

ediatio

nMan

ufacturing

(Woo

d, Pap

er,

Plastic

)

Man

agem

ent

of Com

panies

Educationa

lSe

rvices

Agric

ulture,

Forestry, Fishing

& Hun

ting

Retail Trad

e(M

otor, E

lec,

Bldg

)

Public

Administration

2018* 2019*

Total Upfront Fees Paid (in BPS) Year‐over‐Year Comparison ‐ By Industry

* Based on Comparative Jan‐Mar Periods

Special TopicGreen Lending

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.24April 25, 2019

Achieving Success through Execution

Green Lending: Overview

Most of the major banks and many regional players have established green lending and sustainability initiatives

According to the LSTA, 2018 was a record year for green and sustainability linked loans in the syndicated loan market1

Bloomberg reported that over $12 trillion in investment is needed to support the climate goals of the Paris Agreement2

The Bureau of Labor Statistics provides criteria for identifying green industry segments3

1. LSTA Week in Review, February 1, 2019.2. Bloomberg New Energy Finance, New Energy Outlook, 2017.3. Bureau of Labor Statistics (BLS), https://www.bls.gov/green/industry_by_naics.pdf.

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.25April 25, 2019

Achieving Success through Execution

Categories of Green Lending

Agricultural and Natural Resources

Conservation0.9%

Education, Compliance,

Public Awareness, and Training

21.7%

Energy Efficiency29.5%Greenhouse

Gas Reduction0.9%

Pollution Reduction and Cleanup

6.3%

Recycling and Waste Reduction26.0%

Renewable Energy14.9%

Green and Sustainable Lending

Distribution of Outstandings by SubsectorMar 2019

See the Appendix for the NAICS mappings of the Green industries.Source: AFS Pricing Dashboard – March 2019

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.26April 25, 2019

Achieving Success through Execution

Green Lending is Already a Significant Exposure for Many Banks

Subset of participating banks in the AFS Pricing Dashboard. See the Appendix for the NAICS mappings of the Green industries.Source: AFS Pricing Dashboard – March 2019

For the Market as a whole, the Green industries represent 2.6% of total C&I and CRE exposure, although this ratio varies significantly across the participating banks.

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Percen

t of O

utstan

ding

s

Green and Sustainable LendingPercent of Total Commercial Portfolio

Bilateral Loans Participations

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.27April 25, 2019

Achieving Success through Execution

Loan Growth for Green Industries Trails Market Averages

See the Appendix for the NAICS mappings of the Green industries.Source: AFS Pricing Dashboard – March 2019

Total outstandings for Green industries were down year over year in March. However, quarter over quarter, the Green sector experienced a healthy rebound in bilateral loan growth.

0.4%

‐0.9%

1.7%

‐2.2% ‐2.5%

2.1%1.4%

5.7%

0.9%

4.7%

2.6%

8.1%

‐4.0%

‐2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

Qtr/Qtr Yr/Yr Qtr/Qtr Yr/Yr Qtr/Qtr Yr/Yr

All Loan Types Bilateral Loans Participations

Percen

t Growth

Growth in Outstandings ‐Mar 2019

Green and Sustainable Lending All Other Sectors

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.28April 25, 2019

Achieving Success through Execution

Recycling and Waste Reduction Leads Loan Growth at the Subsector Level

See the Appendix for the NAICS mappings of the Green industries.Source: AFS Pricing Dashboard – March 2019

1.4%

0.4%

0.8%

‐0.5%‐0.7%

1.2%

‐0.8%

‐1.0%

‐0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

All O

ther Sectors

Green an

d Su

staina

ble

Lend

ing

Education, Com

pliance,

Public Awaren

ess,

and Training

Energy Efficien

cy

Pollu

tion Re

duction

and Cleanu

p

Recycling

and

Waste Red

uctio

n

Rene

wab

le Ene

rgy

Percen

t Growth

Growth in OutstandingsMar 2019 Qtr/Qtr

5.7%

‐0.9%

‐8.8%‐7.2%

15.7%

11.0%

‐0.3%

‐10.0%

‐5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

All O

ther Sectors

Green an

d Su

staina

ble

Lend

ing

Education, Com

pliance,

Public Awaren

ess,

and Training

Energy Efficien

cy

Pollu

tion Re

duction

and Cleanu

p

Recycling

and

Waste Red

uctio

n

Rene

wab

le Ene

rgy

Percen

t Growth

Growth in OutstandingsMar 2019 Yr/Yr

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.29April 25, 2019

Achieving Success through Execution

The Return Relative to Risk is Better than Average for the Green Industries

Yellow bubbles represent 2‐digit NAICS industry segments.Risk ratings based on the RMA 10‐point obligor risk rating scale.See the Appendix for the NAICS mappings of the Green industries.Source: AFS Pricing Dashboard – March 2019

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.30April 25, 2019

Achieving Success through Execution

Spreads Widen Year Over Year for Green Industries

100

125

150

175

200

225

250

1Q18 2Q18 3Q18 4Q18 1Q19

Wtd Avg LIBOR‐Equivalent Spread (in BPS)New and Renewed Loans

Green and Sustainable Lending All Other Sectors

3.00

3.50

4.00

4.50

5.00

5.50

1Q18 2Q18 3Q18 4Q18 1Q19

Wtd Avg Risk Rating (10‐Pt. Scale)New and Renewed Loans

Green and Sustainable Lending All Other Sectors

Risk ratings based on the RMA 10‐point obligor risk rating scale.See the Appendix for the NAICS mappings of the Green industries.Source: AFS Pricing Dashboard – March 2019

On a year‐over‐year basis, spread pricing for the Green industries increased 44 bps, as contrasted with a decline of 9 bps for All Other Sectors. The weighted average risk rating for the Green industries trended upwards over the last year, although credit quality for this segment is comparable to that seen for All Other Sectors.

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.31April 25, 2019

Achieving Success through Execution

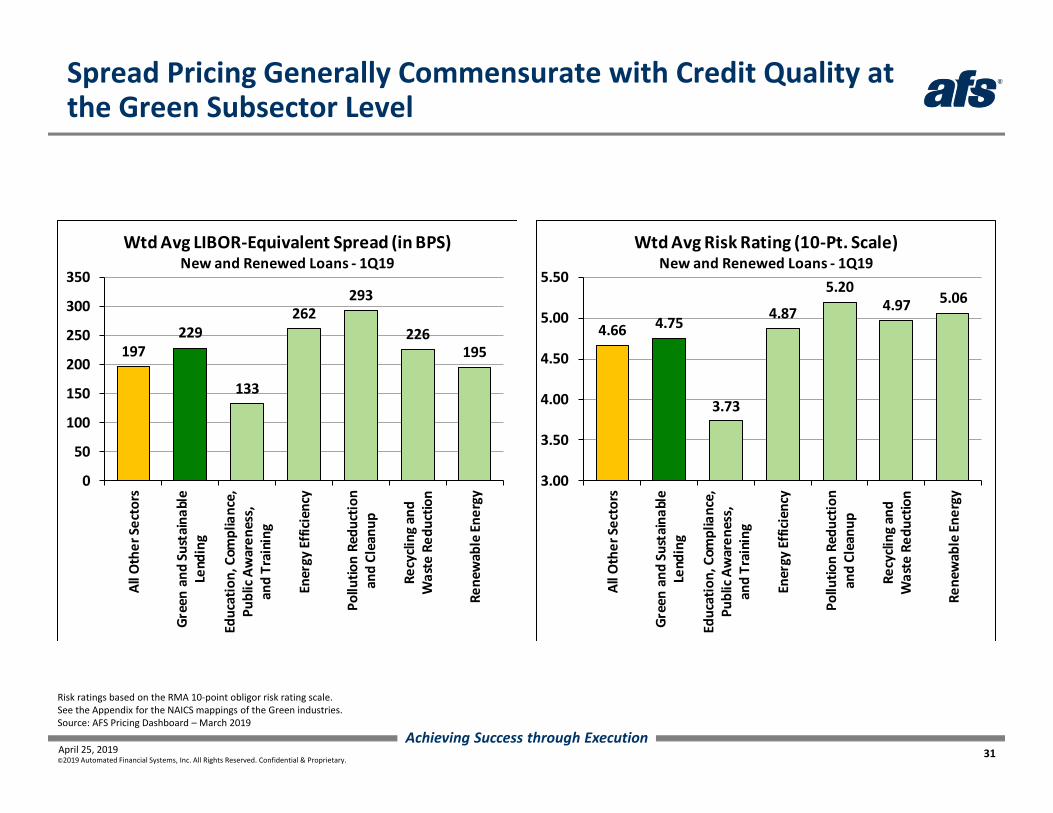

Spread Pricing Generally Commensurate with Credit Quality at the Green Subsector Level

197229

133

262293

226195

0

50

100

150

200

250

300

350

All O

ther Sectors

Green an

d Su

staina

ble

Lend

ing

Education, Com

pliance,

Public Awaren

ess,

and Training

Energy Efficien

cy

Pollu

tion Re

duction

and Cleanu

p

Recycling

and

Waste Red

uctio

n

Rene

wab

le Ene

rgy

Wtd Avg LIBOR‐Equivalent Spread (in BPS)New and Renewed Loans ‐ 1Q19

4.66 4.75

3.73

4.87

5.204.97 5.06

3.00

3.50

4.00

4.50

5.00

5.50

All O

ther Sectors

Green an

d Su

staina

ble

Lend

ing

Education, Com

pliance,

Public Awaren

ess,

and Training

Energy Efficien

cy

Pollu

tion Re

duction

and Cleanu

p

Recycling

and

Waste Red

uctio

n

Rene

wab

le Ene

rgy

Wtd Avg Risk Rating (10‐Pt. Scale)New and Renewed Loans ‐ 1Q19

Risk ratings based on the RMA 10‐point obligor risk rating scale.See the Appendix for the NAICS mappings of the Green industries.Source: AFS Pricing Dashboard – March 2019

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.32April 25, 2019

Achieving Success through Execution

Summary of Findings & Observations

Green industries are material in size in terms of current loans outstanding, although recent loan growth has been sluggish

In 1Q19, the Recycling & Waste Reduction subsector led growth in Green loans

Spread pricing increased year over year for the Green industries, correlating with an increase in credit risk over the same period for this segment

The return relative to risk is better than average for the Green industries

Demand for Green/sustainability linked loans is likely to increase in the coming years

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.33April 25, 2019

Achieving Success through Execution

Thank You for Joining Us Today

A recording and a copy of this presentation will be made available by the end of this week.

Questions?

Doug Skinner+1 484‐875‐1562

Don Dougherty+1 484‐875‐1334

Jeremy Chalson+1 484‐875‐1546

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.34April 25, 2019

Achieving Success through Execution

AFS Best Practices Leadership Council Programming

Upcoming AFS in the Industry Events

Topic Date

Fiserv Forum, Las Vegas May 6–9, 2019

LIBOR Webinar May 8, 2019

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.35April 25, 2019

Achieving Success through Execution

Stay Connected with AFS

Stay on top of all the latest news and happenings with AFS. Follow us and stay connected.

Automated Financial Systems, Inc.

@afs_vision

AFS@AFSVision

Appendix

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.37April 25, 2019

Achieving Success through Execution

How Do We Define “Best”?

Balance Growth Percent change in outstandings. Is there positive

growth momentum in the industry or region? Are banks getting their fair share of wallet?

The three criteria listed below are used to evaluate industry and regional performance in the database. Segments in the top quartile for all three categories represent sustainable growth opportunities for banks.

Spread and Fee Pricing Is spread and fee pricing above average for the

industry or region, or rather is the segment showing signs of pricing compression?

Credit Risk Are risk levels and default projections trending

downward for the segment?

$

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.38April 25, 2019

Achieving Success through Execution

NAICS Mapping of Green IndustriesAgricultural and Natural Resources Conservation

Green Subsector NAICS NAICS Description

Agricultural and natural resources conservation 113210 Forest nursery and gathering forest products

Agricultural and natural resources conservation 115310 Support activities for forestry

Agricultural and natural resources conservation 712130 Zoos and botanical gardens

Agricultural and natural resources conservation 712190 Nature parks and other similar institutions

Source: Bureau of Labor Statistics (BLS), https://www.bls.gov/green/industry_by_naics.pdf.

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.39April 25, 2019

Achieving Success through Execution

NAICS Mapping of Green IndustriesEducation, Compliance, Public Awareness, and Training

Green Subsector NAICS NAICS Description

Education, compliance, public awareness, and training 813211 Grantmaking foundations

Education, compliance, public awareness, and training 813219 Other grantmaking and giving services

Education, compliance, public awareness, and training 813312 Environment and conservation orgs

Education, compliance, public awareness, and training 813910 Business associations

Education, compliance, public awareness, and training 813920 Professional organizations

Education, compliance, public awareness, and training 813940 Political organizations

Education, compliance, public awareness, and training 924110 Air, water, and waste program administration

Education, compliance, public awareness, and training 924120 Administration of conservation programs

Education, compliance, public awareness, and training 926110 Administration of general economic programs

Education, compliance, public awareness, and training 926120 Transportation program administration

Education, compliance, public awareness, and training 926130 Utility regulation and administration

Education, compliance, public awareness, and training 926140 Agricultural market and commodity regulation

Education, compliance, public awareness, and training 926150 Licensing and regulating commercial sectors

Source: Bureau of Labor Statistics (BLS), https://www.bls.gov/green/industry_by_naics.pdf.

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.40April 25, 2019

Achieving Success through Execution

NAICS Mapping of Green IndustriesEnergy Efficiency

Green Subsector NAICS NAICS Description

Energy efficiency 236118 Residential remodelers

Energy efficiency 237210 Land subdivision

Energy efficiency 333312 Commercial laundry and drycleaning machinery

Energy efficiency 334513 Industrial process variable instruments

Energy efficiency 334514 Totalizing fluid meters and counting devices

Energy efficiency 334515 Electricity and signal testing instruments

Energy efficiency 483114 Coastal and Great Lakes passenger transport.

Energy efficiency 483212 Inland water passenger transportation

Energy efficiency 485111 Mixed mode transit systems

Energy efficiency 485112 Commuter rail systems

Energy efficiency 485113 Bus and other motor vehicle transit systems

Energy efficiency 485119 Other urban transit systems

Energy efficiency 485210 Interurban and rural bus transportation

Energy efficiency 485410 School and employee bus transportation

Energy efficiency 485991 Special needs transportation

Energy efficiency 485999 All other ground passenger transportation

Energy efficiency 511210 Software publishersSource: Bureau of Labor Statistics (BLS), https://www.bls.gov/green/industry_by_naics.pdf.

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.41April 25, 2019

Achieving Success through Execution

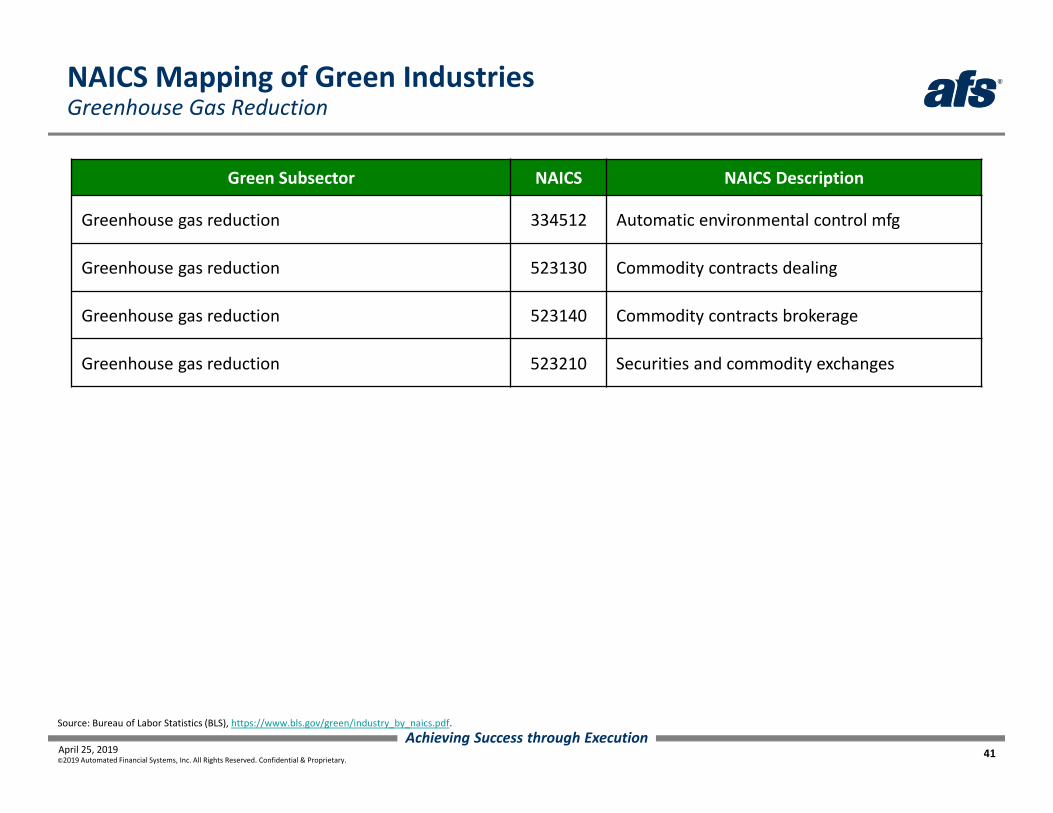

NAICS Mapping of Green IndustriesGreenhouse Gas Reduction

Green Subsector NAICS NAICS Description

Greenhouse gas reduction 334512 Automatic environmental control mfg

Greenhouse gas reduction 523130 Commodity contracts dealing

Greenhouse gas reduction 523140 Commodity contracts brokerage

Greenhouse gas reduction 523210 Securities and commodity exchanges

Source: Bureau of Labor Statistics (BLS), https://www.bls.gov/green/industry_by_naics.pdf.

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.42April 25, 2019

Achieving Success through Execution

NAICS Mapping of Green IndustriesPollution Reduction and Cleanup

Green Subsector NAICS NAICS Description

Pollution reduction and cleanup 333411 Air purification equipment mfg

Pollution reduction and cleanup 334516 Analytical laboratory instrument mfg.

Pollution reduction and cleanup 562112 Hazardous waste collection

Pollution reduction and cleanup 562211 Hazardous waste treatment and disposal

Pollution reduction and cleanup 562910 Remediation services

Pollution reduction and cleanup 562920 Materials recovery facilities

Pollution reduction and cleanup 562991 Septic tank and related services

Pollution reduction and cleanup 812320 Drycleaning and laundry services

Source: Bureau of Labor Statistics (BLS), https://www.bls.gov/green/industry_by_naics.pdf.

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.43April 25, 2019

Achieving Success through Execution

NAICS Mapping of Green IndustriesRecycling and Waste Reduction

Green Subsector NAICS NAICS Description

Recycling and waste reduction 221310 Water supply and irrigation systems

Recycling and waste reduction 221320 Sewage treatment facilities

Recycling and waste reduction 237110 Water and sewer system construction

Recycling and waste reduction 333319 Other commercial & service machinery mfg

Recycling and waste reduction 423930 Recyclable material merchant wholesalers

Recycling and waste reduction 562111 Solid waste collection

Recycling and waste reduction 562119 Other waste collection

Recycling and waste reduction 562212 Solid waste landfill

Recycling and waste reduction 562213 Solid waste combustors and incinerators

Recycling and waste reduction 562219 Other nonhazardous waste disposal

Recycling and waste reduction 562998 Miscellaneous waste management services

Source: Bureau of Labor Statistics (BLS), https://www.bls.gov/green/industry_by_naics.pdf.

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.44April 25, 2019

Achieving Success through Execution

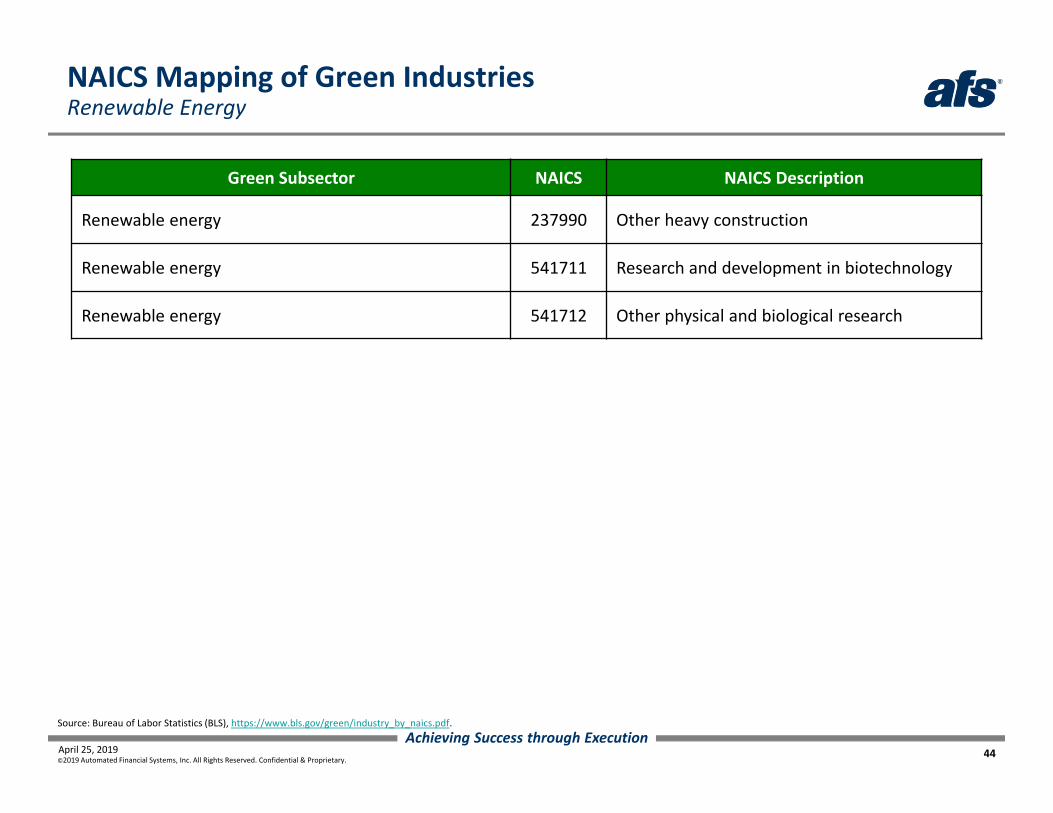

NAICS Mapping of Green IndustriesRenewable Energy

Green Subsector NAICS NAICS Description

Renewable energy 237990 Other heavy construction

Renewable energy 541711 Research and development in biotechnology

Renewable energy 541712 Other physical and biological research

Source: Bureau of Labor Statistics (BLS), https://www.bls.gov/green/industry_by_naics.pdf.

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.45April 25, 2019

Achieving Success through Execution

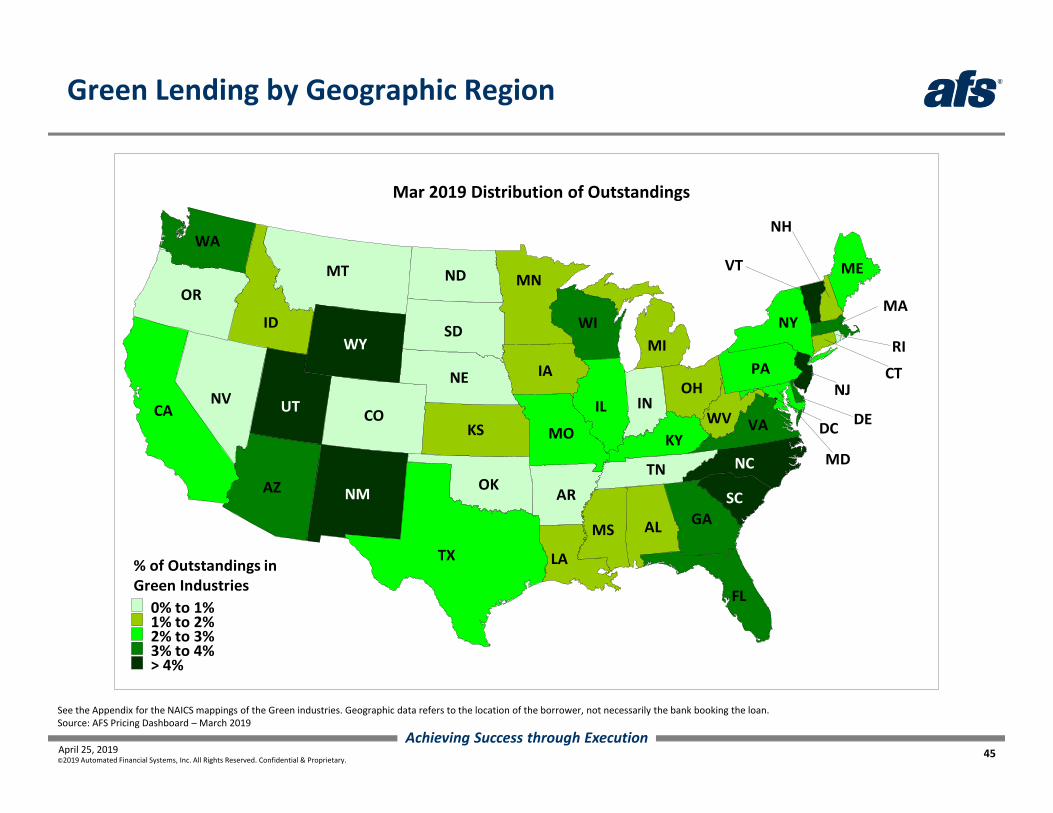

Green Lending by Geographic Region

See the Appendix for the NAICS mappings of the Green industries. Geographic data refers to the location of the borrower, not necessarily the bank booking the loan.Source: AFS Pricing Dashboard – March 2019

SD

ND

NENV

MT

TNOK

OR

IN

RI

AR

CO

MI

NH

OH

ID

MS

CT

LA

KS

AL

IA

MN

WVCA

ME

MO

NY

IL

MDKY

TX

PA

FL

AZ

WA

WI

GA

VA DE

MA

UT

NC

NJ

SCNM

DC

VT

WY

0% to 1%1% to 2%2% to 3%3% to 4%> 4%

% of Outstandings in Green Industries

Mar 2019 Distribution of Outstandings

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.46April 25, 2019

Achieving Success through Execution

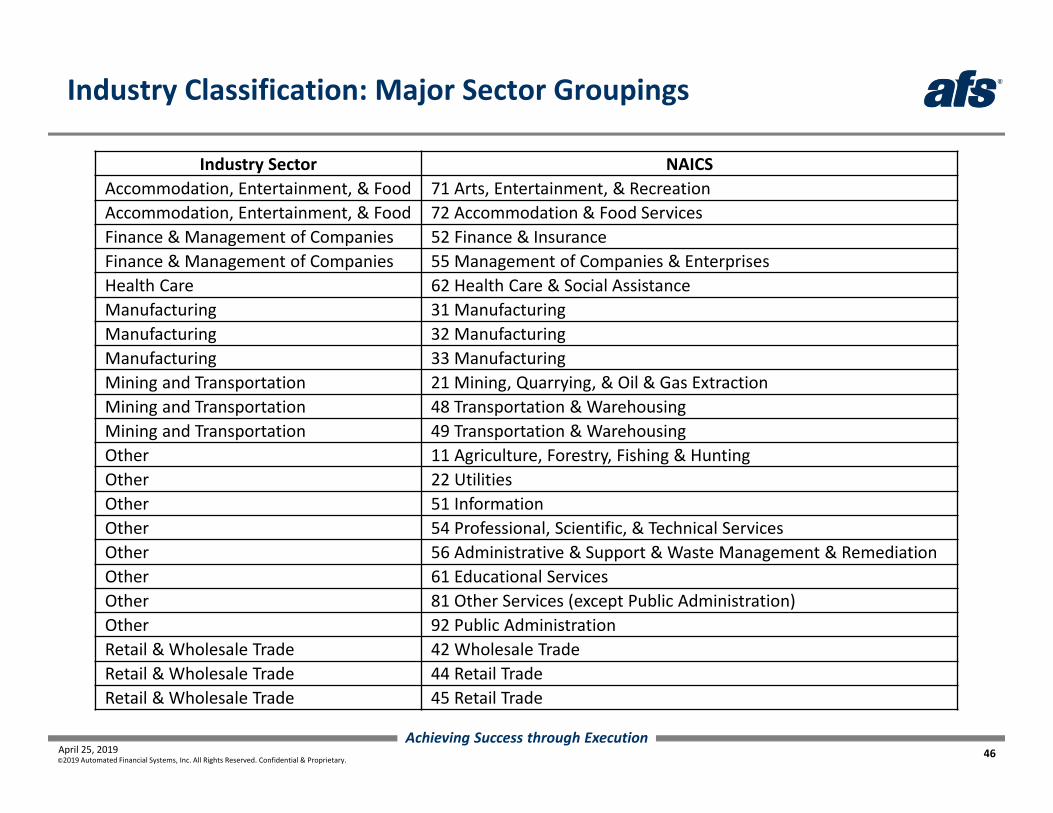

Industry Classification: Major Sector Groupings

Industry Sector NAICSAccommodation, Entertainment, & Food 71 Arts, Entertainment, & RecreationAccommodation, Entertainment, & Food 72 Accommodation & Food ServicesFinance & Management of Companies 52 Finance & InsuranceFinance & Management of Companies 55 Management of Companies & EnterprisesHealth Care 62 Health Care & Social AssistanceManufacturing 31 ManufacturingManufacturing 32 ManufacturingManufacturing 33 ManufacturingMining and Transportation 21 Mining, Quarrying, & Oil & Gas ExtractionMining and Transportation 48 Transportation & WarehousingMining and Transportation 49 Transportation & WarehousingOther 11 Agriculture, Forestry, Fishing & HuntingOther 22 UtilitiesOther 51 InformationOther 54 Professional, Scientific, & Technical ServicesOther 56 Administrative & Support & Waste Management & RemediationOther 61 Educational ServicesOther 81 Other Services (except Public Administration)Other 92 Public AdministrationRetail & Wholesale Trade 42 Wholesale TradeRetail & Wholesale Trade 44 Retail TradeRetail & Wholesale Trade 45 Retail Trade

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.47April 25, 2019

Achieving Success through Execution

Balance Growth by State and Industry: Bilateral Loans

Note: Geographic data refers to the location of the borrower, not necessarily the bank booking the loan. Industry categories based on North American Industry Classification System (NAICS).Source: AFS Pricing Dashboard – March 2019

ALARAZ

CA CO

CT

DCDE

FL

GA

IA

ID

IL INKS KY

LA

MA

MD

ME

MI

MN

MO

MS

MT

NC

ND

NE

NH

NJ

NM

NV

NY

OH

OK

OR

PARI

SC

SD

TN

TX

UTVA

VTWA

WI

WV

WY

Growth in Outstandings ‐ Predominant C&I Industries*Dec 2018 vs. Mar 2019

Bilateral Loans

Retail & Wholesale TradeHealth CareFinance & Management of CompaniesManufacturingMining and TransportationAccommodation, Entertainment, & FoodOther

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.48April 25, 2019

Achieving Success through Execution

Balance Growth by State and Industry: Participations

Note: Geographic data refers to the location of the borrower, not necessarily the bank booking the loan. Industry categories based on North American Industry Classification System (NAICS).Source: AFS Pricing Dashboard – March 2019

ALARAZ

CA CO

CT

DCDE

FL

GA

IA

ID

IL INKS KY

LA

MA

MD

ME

MI

MN

MO

MS

MT

NC

ND

NE

NH

NJ

NM

NV

NY

OH

OK

OR

PARI

SC

SD

TN

TX

UTVA

VTWA

WI

WV

WY

Growth in Outstandings ‐ Predominant C&I Industries*Dec 2018 vs. Mar 2019

Participations

Retail & Wholesale TradeHealth CareFinance & Management of CompaniesManufacturingMining and TransportationAccommodation, Entertainment, & FoodOther

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.49April 25, 2019

Achieving Success through Execution

Balance Growth: Industry Drivers by Geographic Region

The AFS Pricing Dashboard enables users to pinpoint industry loan growth drivers across their unique geographic footprints.

Note: Geographic data refers to the location of the borrower, not necessarily the bank booking the loan. Industry categories based on North American Industry Classification System (NAICS).Source: AFS Pricing Dashboard – March 2019

12.2%

‐0.2%

12.1%

6.6%

15.3%

7.3%

Manufacturing(Machinery,

Elec)

WholesaleTrade

Professional,Scientific,& Tech

Bilateral Participations

1.9% 3.7%

7.9%

2.2%

23.4%

6.6%

Real Estate Manufacturing(Machinery,

Elec)

Finance& Insurance

Bilateral Participations

0.5%2.3% 2.1%

9.5%

‐1.1%

16.1%

Finance& Insurance

Real Estate Retail Trade(Motor, Elec,

Bldg)

Bilateral Participations

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.50April 25, 2019

Achieving Success through Execution

Balance Growth: Industry Drivers by Geographic Region

Note: Geographic data refers to the location of the borrower, not necessarily the bank booking the loan. Industry categories based on North American Industry Classification System (NAICS).Source: AFS Pricing Dashboard – March 2019

2.3% 2.0%5.9%

11.0%

17.4%

‐2.2%Health Care& Social

Assistance

Accomm‐odation &

Food Services

Finance& Insurance

Bilateral Participations

16.0%

2.1%5.8%

42.6%

13.0%6.3%

Information Real Estate Finance& Insurance

Bilateral Participations

1.0%

‐1.3%

2.1%

‐2.5%

6.1%

0.0%

Real Estate Accomm‐odation &

Food Services

Manufacturing(Machinery,

Elec)

Bilateral Participations

20.0%

6.7%11.1%9.2%

29.7%

18.9%

WholesaleTrade

Finance& Insurance

Manufacturing(Machinery,

Elec)

Bilateral Participations

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.51April 25, 2019

Achieving Success through Execution

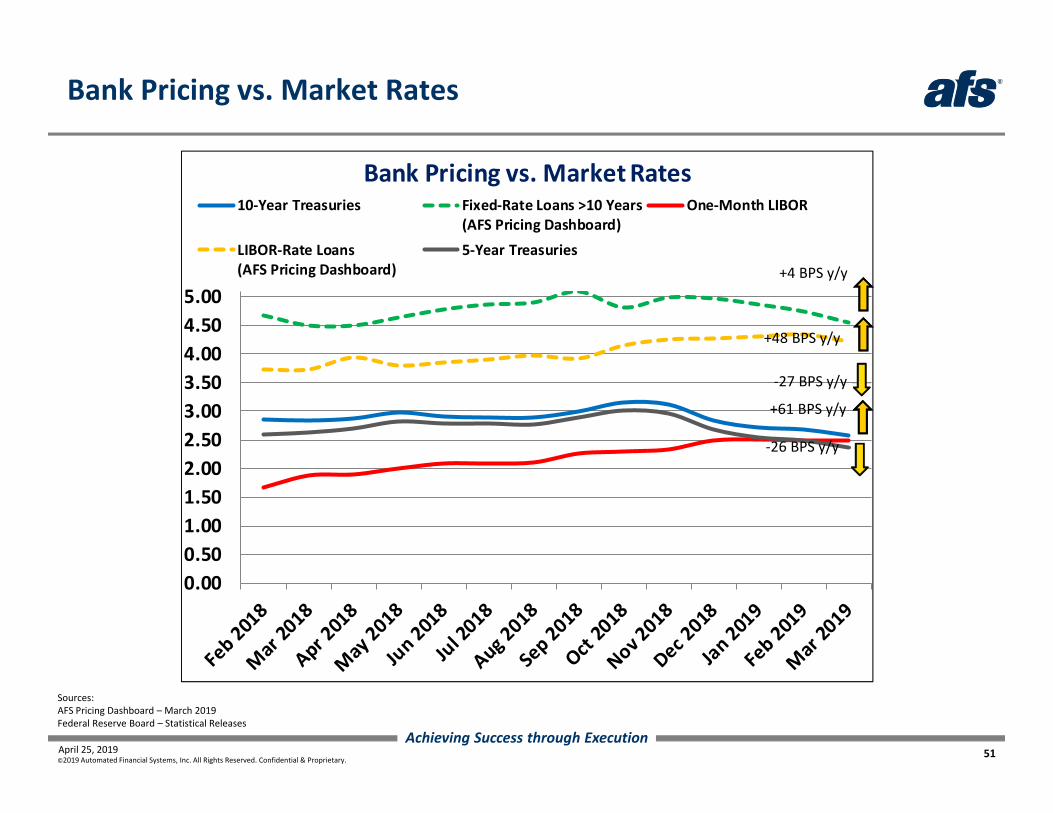

0.000.501.001.502.002.503.003.504.004.505.00

10‐Year Treasuries Fixed‐Rate Loans >10 Years(AFS Pricing Dashboard)

One‐Month LIBOR

LIBOR‐Rate Loans(AFS Pricing Dashboard)

5‐Year Treasuries

Bank Pricing vs. Market Rates

Bank Pricing vs. Market Rates

Sources: AFS Pricing Dashboard – March 2019Federal Reserve Board – Statistical Releases

+48 BPS y/y

‐26 BPS y/y

+4 BPS y/y

‐27 BPS y/y

+61 BPS y/y

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.52April 25, 2019

Achieving Success through Execution

Overall Line of Credit Utilization Remains Flat

Note: Geographic data refers to the location of the borrower, not necessarily the bank booking the loan. Industry categories based on North American Industry Classification System (NAICS).Source: AFS Pricing Dashboard – March 2019

20%

30%

40%

50%

60%Overall Line Usage < $1M $1M to < $5M

$5M to < $25M >= $25M Participations

Line of Credit Utilization Rate ‐ By Deal SizeRevolving Lines of Credit Only

51.1%

47.9%

47.0%

46.8%

45.4%

39.1%

33.8%

32.8%

31.4%

30.8%

30.1%

New HampshireUtah

Maryland

Oregon

ArkansasIndiana

WisconsinMissouri

Washington

Top 5 / Bottom 5 States ‐ Line Utilization Mar 2019 All Loan Types

Kansas

Nat'l Avg

50.8%

49.2%

45.4%

44.2%

42.0%

39.1%

34.5%

32.1%

31.5%

24.5%

20.9%

Agriculture

Retail Trade (Motor, Elec, Bldg)

Wholesale Trade Mining, Oil & Gas

Management

Public Administration

Professional, Scientific, & Tech

Retail Trade (Hobby, General)

Utilities Educational Services

Top 5 / Bottom 5 C&I Industries ‐ Line Utilization Mar 2019 All Loan Types

All Industries Avg

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.53April 25, 2019

Achieving Success through Execution

RMA 10‐Point Obligor Risk Rating Scale

Risk Key

Risk Rating

Risk Rating Category Definition and Criteria

1 Substantially Risk‐Free

High Pass Borrowers of unquestioned credit standing at the pinnacle of credit quality. Basically, governments and central banks of major industrialized countries, a few major world‐class banks, and a few multinational corporations.

2 Minimal Risk

High Pass Borrowers of the highest quality, presently and prospectively. Virtually no risk in lending to this class. Cash flows over at least five years demonstrate exceptionally large and/or stable margins of protection. Balance sheets are very conservative and strong with liquid assets. Projected cash flows, including anticipated credit extensions, exhibit strong trends in margins of protection, liquidity, and debt service coverage. Excellent asset quality and management. Access to world capital Markets under any conditions. Typically, large national companies with a significant share of a major, stable industry.

3 Modest Risk

High Pass Borrowers in the lower end of the high‐quality range but with excellent prospects. Very good asset quality and liquidity; consistently strong debt capacity and coverage; very good management. The credit extension is considered definitely sound; however, elements may be present that suggest the borrower may not be free from temporary impairments some‐time in the future. May have limited access to national capital Markets. Typically major regional companies in relatively stable industries.

4 Better than Average Risk

Moderate Pass

Borrowers in the high end of the medium range between borrowers who are definitely sound and those with minor risk characteristics. The margin of protection is good. Elements of strength are present in such areas as liquidity, stability of margins and cash flows, diversity of assets, and lack of dependence on one type of business. Reasonable access to capital Markets or bank financing is present; can always borrow at favorable rates and terms. Well‐established regional and excellent local companies operating in a reasonably stable industry that may be moderately affected by the business cycle and moderately open to changes. Management and owners have unquestioned character, as demonstrated by repeated performance.

5 Average Risk

Moderate Pass

Borrowers with smaller margins of debt service coverage and with some elements of reduced strength. Satisfactory asset quality and liquidity; good debt capacity and coverage; and good management in critical positions. These companies have good margins of protection and will definitely qualify as attractive borrowers. These borrowers will be able to obtain similar financing from other financial institutions and can generally borrow at attractive rates and terms. A loss year or a somewhat declining earnings trend may occur, but borrowers have sufficient strength and financial flexibility to offset these issues. These are typically solid companies often operating in cyclical industries that are somewhat vulnerable to change. Management and owners have unquestioned character. Depth of management may become an issue in a growing firm.

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.54April 25, 2019

Achieving Success through Execution

RMA 10‐Point Obligor Risk Rating Scale

Risk Key

Risk Rating

Risk Rating Category Definition and Criteria

6 Acceptable Risk

Low Pass Borrowers with declining earnings, strained cash flow, increasing leverage and/or weakening Market fundamentals that indicate above‐average risk. These borrowers generally have limited additional debt capacity and modest coverage and average or below average asset quality, margins, and Market share. Some management weakness exists. These borrowers should be able to obtain similar financing with comparable terms or somewhat worse, from other banks, but that ability may diminish in difficult economic times. Also, borrowers who are currently performing as agreed but could be adversely affected by such developing factors as deteriorating industry conditions, operating problems, pending litigation of a significant nature, or declining collateral quality/adequacy, and so forth. Companies with average or smaller Market shares operating in a cyclical or declining industry. Management and owners have good character, with no basis for questions.

7 Special Mention (Potential Weakness)

Criticized –Classified

Borrowers who exhibit potential credit weaknesses or downward trends deserving bank management’s close attention. If not checked or corrected, these trends will weaken the bank’s asset and position. While potentially weak, these borrowers are currently marginally acceptable; no loss of principal or interest is envisioned. As a result, special mention assets do not expose an institution to sufficient risk to warrant adverse classification. Included in special mention assets could be turnaround situations, as well as those borrowers previously rated 4–6 who have shown deterioration, for whatever reason, indicating a downgrading from the better categories. Typically companies in start‐up or deteriorating industries or with a poor and declining Market share in an average industry. An element of asset quality, financial flexibility, or management is below average. Management and owners may have limited depth and backup. Borrowers who have been or would normally be categorized special mention by regulatory authorities.

8 Substandard (Definite Weakness – Loss Unlikely)

Criticized –Classified

Borrowers with well‐defined weaknesses that jeopardize the orderly liquidation of debt. A substandard loan is inadequately protected by the current sound worth and paying capacity of the obligor or by the collateral pledged, if any. Normal repayment from the borrower is in jeopardy, although no loss of principal is envisioned. There is a distinct possibility that a partial loss of interest and/or principal will occur if the deficiencies are not corrected. Loss potential, while existing in the aggregate amount of substandard assets, does not have to exist in individual assets classified substandard. Management skills are questionable with readily identifiable voids. Borrowers that have been or would normally be classified substandard by regulatory authorities.

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.55April 25, 2019

Achieving Success through Execution

RMA 10‐Point Obligor Risk Rating Scale

Risk Key

Risk Rating

Risk Rating Category Definition and Criteria

9 Doubtful (Partial Loss Probable)

Criticized –Classified

Borrowers classified doubtful have the weaknesses found in substandard borrowers with the added provision that the weaknesses make collection of debt in full, on the basis of currently existing facts, conditions, and values, highly questionable and improbable. Serious problems exist to the point where partial loss of principal is likely. The possibility of loss is extremely high, but because of certain important, reasonably specific pending factors that may work to strengthen the assets, the loans’ classification as estimated losses are deferred until a more exact status may be determined. Pending factors include proposed merger, acquisition, or liquidation procedures; capital injection; perfecting liens on additional collateral; and refinancing plans. Reserves are generally established to provide for these uncertainties. Management has a demonstrated history of failing to live up to agreements, unethical or dishonest business practices, bankruptcy, and/or conviction on criminal charges.

10 Loss (Definite Loss)

Criticized –Classified

Borrowers deemed incapable of repayment of unsecured debt. Loans to such borrowers are considered uncollectible and of such little value that continuance as active assets of the bank is not warranted. This classification does not mean that the loans have absolutely no recovery or salvage value but, rather, it is not practical or desirable to defer writing off these basically worthless assets even though partial recovery may be effected in the future.

Additional FeaturesDelivering Market Data

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.57April 25, 2019

Achieving Success through Execution

Delivering Market Data: Simple Pricing Grid

AFS will work with the bank to define the appropriate segmentation criteria and level of granularity. This can be used for integration into other systems at the bank.

Min/Median/Max/Avg of Banks in Market

Segmentation Criteria

Sample data for illustration purposes only.

Region Collateral Pricing Index Product

New & Renewed

FlagTerm Deal Size EL Number of

Observations

Bank Minimum LIBOR

Equivalent Spread

Bank Median LIBOR

Equivalent Spread

Bank Maximum LIBOR

Equivalent Spread

Market AverageLIBOR

Equivalent Spread

South Secured Re Prime Line of Credit New <= 1 Year $100,000‐$249,999 4.0% < 8.0% 42 3.58 3.70 4.01 3.70

Eastern Midwest Secured No Fixed Line of Credit New 2‐5 Years $5,000,000‐$24,999,999 4.0% < 8.0% 20 2.03 2.03 2.03 2.03

South Secured No Prime Line of Credit New 5‐10 Years <$100,000 4.0% < 8.0% 18 5.64 5.64 5.64 5.64

Eastern Midwest Secured No Fixed Line of Credit New 1‐2 Years $5,000,000‐$24,999,999 4.0% < 8.0% 16 2.16 2.16 2.16 2.16

Eastern Midwest Secured No Fixed Line of Credit New 2‐5 Years <$100,000 4.0% < 8.0% 15 2.09 2.09 2.09 2.09

Eastern Midwest Unsecured LIBOR Line of Credit New <= 1 Year $50,000,000+ 4.0% < 8.0% 14 2.50 2.50 2.50 2.50

South Secured No Fixed Term/Time Loan New 5‐10 Years <$100,000 4.0% < 8.0% 14 4.25 5.90 7.55 4.30

Middle Atlantic Secured Re Prime Line of Credit New <= 1 Year $100,000‐$249,999 4.0% < 8.0% 9 3.77 3.77 3.77 3.77

Eastern Midwest Secured No Fixed Line of Credit New <= 1 Year $5,000,000‐$24,999,999 4.0% < 8.0% 7 2.00 2.00 2.00 2.00

South Secured No Fixed Term/Time Loan New 2‐5 Years <$100,000 4.0% < 8.0% 7 4.03 4.03 4.03 4.03

South Secured No Prime Line of Credit New Unknown/ <$100,000 4.0% < 8.0% 7 5.85 5.85 5.85 5.85

Middle Atlantic Secured Re LIBOR Term/Time Loan New <= 1 Year $1,000,000‐$4,999,999 4.0% < 8.0% 6 4.00 4.00 4.00 4.00

South Secured Re LIBOR Term/Time Loan New 1‐2 Years $5,000,000‐$24,999,999 4.0% < 8.0% 6 3.50 3.50 3.50 3.50

Middle Atlantic Secured No Prime Line of Credit New 5‐10 Years <$100,000 4.0% < 8.0% 5 5.13 5.13 5.13 5.13

Western Midwest Secured Re Prime Line of Credit New <= 1 Year $250,000‐$499,999 4.0% < 8.0% 5 2.93 2.93 2.93 2.93

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.58April 25, 2019

Achieving Success through Execution

Upcoming Renewals Report

PDB View – Includes the Upcoming Renewals Report. Business Purpose – Provides actionable data to support pricing decisions on loans coming

up for renewal. Key Insights – Provides a total market equivalent price for each obligation based on

shared loan characteristics. Allows the Bank to maximize the revenue on each deal while still maintaining its competitive advantage. From an accountability perspective, shows how the pricing of each individual obligation compares to external standards.

For the borrower circled below, the Bank can reprice at more advantageous terms while still undercutting its competitors.

Sample data for illustration purposes only.

©2019 Automated Financial Systems, Inc. All Rights Reserved. Confidential & Proprietary.59April 25, 2019

Achieving Success through Execution

Pricing Performance: Recent New and Renewed Deals

For enforcement of policy, reporting on all New and recently Renewed deals provides an audit of pricing exceptions.

Sample data for illustration purposes only.