agenda & opening comments · 2018-04-24 · federal reporting & indirect cost mark davis...

TRANSCRIPT

4/10/2018

1

FY2018 Close & FY2019 Open

Training

Higher Education Presented by:

Office of the State Controller

April 12, 2018

1

Agenda &

Opening Comments

2

4/10/2018

2

Presenters

State Controller

Bob Jaros (303) 866-3765

Financial Services Unit

Tom Gamache (303) 866-5657

Karoline Clark (303) 866-3811

Jennifer Henry (303) 866-3809

Daniel Saint (303) 866-3891

Federal Reporting & Indirect Cost

Mark Davis (303) 866-4041

Marc Burkepile (303) 866-3346

3

Agenda

• Opening Comments

• State Controller Comments

• General Information

• Calendar Highlights

• Budget Process

• Capital Construction

• Opening & Closing Procedures

• Indirect Cost & Federal Reporting Unit Update

• Financial Reporting & GASB Update

• Closing and Questions

4

4/10/2018

3

Housekeeping

• Please sign in at the registration table

• CPE will be offered for today’s training, turn in

the form before you leave today

• We will take a break about halfway through the

session • Vending machines are in the basement—turn left

off elevators • Restrooms and café (closes at 2 pm) are behind the

elevator bank

5

State Controller Comments

6

4/10/2018

4

State Controller Comments

• Fiscal Rule revision update

• NIST upgrade update

• OSC guidance on Uniform Guidance

• GASB 68 & 75

• Close calendar

• Internal receivable/payable balances • Reconcile account balances, address old balances, and

confirm valid balances to assist OSC preparation of CAFR

7

Calendar Highlights

8

4/10/2018

5

Financial Analysis & Reporting

Section

9

Director

Jeffrey Kahn

Financial Services

Tom Gamache

Reporting

Paul Reynolds

Internal Audit

Jeff Lee

Federal Reporting & Indirect Cost

Bhavna Punatar

Financial Analysis & Reporting

Section

Central Mailbox

10

4/10/2018

6

Fiscal Procedures Manual

Items of Note

Calendar Changes communicated via Controllers

distribution list Audit Risk Letter

Updates Changes communicated via Controllers

distribution list

www.colorado.gov/osc/fiscalprocedures

11

Period Close Dates

Period Purpose Close Date

12 Payment / Cash Cut Off July 20

13 Department Close August 3

14 OSC Close August 15

15 Basic Financial Statements September 20

16 CAFR / Audit Opinion December 15

12

4/10/2018

7

Calendar Highlights

June 30

• Goods must be received or services performed by this date

• Long bill, special bills, and supplemental bills interfaced from PB to CORE by this date

July 6 • Exhibit K3 due

July 13

• Last day departments can bill Institutions of Higher Education (via invoice or IET for central billing agencies)

13

Calendar Highlights

July 20

• Period 12 Close • Cash cutoff

• Last day to approve disbursement, cash receipt, and procurement documents

• Encumbrance roll job run at close of business

July 25

• OSC to provide the allocation for posting Treasury Pooled Cash Unrealized Gain/Loss to IHEs based on period 12 balances (on the assumption that cash balances will not change for the IHEs)

July 30

• Target date for OSC to provide pension and OPEB liability workbooks (GASB 68/75)

14

4/10/2018

8

Calendar Highlights

August 2 • Final date for interface feeds to core

August 3

• Period 13 Close – Department Close • Last day for regular department/IHE input into CORE

• Transfers must be in balance by this date

• IHE deadline to post Treasury Pool and Institution-Held Unrealized Gain/Losses to CORE

• Deadline for BGA documents to be approved for the continuing portion of expiring capital construction projects

• Deadline for BGA documents to be approved for the reversion portion of expiring capital construction projects

• After this date all FY18 documents route to the OSC for approval

15

Calendar Highlights

August 7

• Last day to approve capital/fixed assets before the final June 30 automated depreciation is run for period 14

• Deadline to submit transfer and overexpenditure requests to the OSC

August 15

• All exhibits due except I, J, K1, and K3

August 17

• TABOR variance analysis responses due (balances as of period 14 close)

• OSC to provide Treasury pooled cash summarized footnote to IHEs and standalone entities based on Treasury’s Exhibit N

16

4/10/2018

9

Calendar Highlights

August 24

• Cash funds uncommitted reserves turnaround report due

• Target date for IHE to submit pension and OBEB liability entries (GASB 68/75)

• Target date of cutoff of post-closing entries for the Basic Financial Statements. Entries submitted in period 15 after this date will only be posted if deemed material and/or necessary by the OSC and are considered audit adjustments

August 27

• Exhibit I due

• SNP, SRENCP, and Exhibit J due

17

Calendar Highlights

September 20

• Period 15 Close - planned publication date of the Basic Financial Statements

• Entries after this date are considered audit adjustments

• CORE document catalog to be cleared of all FY2018 and prior rejected documents

September 28

• Target date to submit MD&A to OSC

October 1

• Exhibit K1 due

18

4/10/2018

10

Calendar Highlights

December

• Copy of Management Rep Letter due to OSC

December 31

• FRAC due to OSC

19

Budget Process

20

4/10/2018

11

FY2019 Budget Structure

• FY2019 Budget lines are now available in CORE • Based on active FY2018 budget lines as of February 2

EXCEPT expiring capital construction budget lines

• BGA90/91 documents were created with department 999A in the header; difficult to find departments

• Please search the BQ90LV3 or BQ91LV3 screens, based on the fund or appropriation unit

• Any questions, contact Fiftwo

• By July 1st, all existing and new lines will be available for use in CORE

• If budget line exists that is not needed in FY2019, work with Fiftwo to get the budget line deactivated

• If a budget line does not exist that should be available in FY2019, work with Fiftwo to get the budget line activated

21

FY2019 Long Bill

• HB 18-1322 not yet signed by the Governor (May?)

• Budget data contained in Performance Budget (PB) • PB syncs with CORE via appropriation unit

• New/changed coding in PB/CORE • Coordinated by Fiftwo Baldwin and Andrew Rauch

• PB to CORE interface for Higher Ed will occur before the

start of FY2019

22

4/10/2018

12

Special & Supplemental Bills & Emergency

Supplementals • For Special and Supplemental Bills

• Interface from PB periodically based on effective date

• Contact Fiftwo if new coding is necessary

• For Emergency Supplementals • Manual budget documents (contact Fiftwo)

• Final supplemental bills have been booked; any emergency supplementals need to be reversed (contact Fiftwo)

23

Capital Construction

24

4/10/2018

13

Capital Construction – Long Bill Booking

• Process

• Fiftwo & IHEs request appropriation units for new projects (project numbers are assigned by CDC and recorded in CORE)

• CCHE enters data into PB which is interfaced into CORE

• Once budget documents are finalized in CORE, the OSC will:

• Apply restrictions which prohibit spending

• Provide the coded capital construction long bill to Fiftwo for distribution to the IHEs

• To remove a restriction, submit a BGA90/91 document and attach an approved SC4.1 or Letter of Intent

• Reminders • Ensure appropriation units and funds are correct in PB

• Capital construction appropriations are effective upon signature by the Governor, typically in May

25

Capital Construction – Six-Month Rule

• Statute requires that funds for new capital construction

projects be encumbered within 6 months from the date

the Long Bill is signed

• Rule applies to the initial appropriation only

• Rule does not apply to projects that are solely funded

from cash funds

• 6-Month Certification Form must be submitted to the

OSC by the six-month due date at

• Appropriations will be restricted for any projects not

certified

26

4/10/2018

14

Capital Construction - Spending

• For State-funded projects, budgetary compliance is

measured in the Capital Construction Fund 4610

• Process: • Spend directly in Fund 305x/320x

• Record a transfer from Fund 4610 to Fund 305x/320x • Use CORE document IET4

• Event Type XN96

• Object Code 7300 for the transfer out of Fund 4610

• Revenue Source Code 9300 for the transfer into Fund 305x/320x

27

Capital Construction - Spending

• Reminders • Funds should not be transferred out of Fund 4610 without

supporting expenditures in Fund 305x/320x

• At fiscal year end, IHEs will need to transfer funds from 4610 for any capital construction related accruals in Fund 305x/320x

28

4/10/2018

15

Capital Construction – Capital Assets

• IHEs maintain detailed records of all capital assets in

their own systems

• Data are interfaced to CORE at a summary level

• Entries for recording the asset • Some IHEs use 6610-Clearing Offset Account to record the

elimination entry for the asset and feed this entry to CORE

• Other IHEs do the eliminating entry in their own system and then feed the asset entry to CORE

• For more information on capital assets see Fiscal

Procedures Manual, Chapter 4

29

Capital Construction – Reconciliation

• Tool to help determine if Fund 4610 and 305x/320x are

in sync • InfoAdvantage Report OSC-011 - Higher Ed Capital

Construction Transfers Compared to Institutional Fund Expenditures

• “Expenditure Difference” should be $0

• “Capitalization Difference” should be $0 unless only a portion of the expense was capitalized, the amount is in CIP, or the IHE does not use the 6610-Clearing Offset Account

30

4/10/2018

16

Capital Construction – Carryforward &

Reversion • Per LB headnotes, appropriations are available upon enactment plus

three full fiscal years and for any subsequent year for the amount encumbered as of June 30

• Projects within the three years

• OSC will process the budget documents in CORE to carryforward spending authority

• Target date for the carryforward is August 31st

• Calculation is FY Budget less FY Expenditures (based on P14 balances)

• For any postclosing entries in periods 15 or 16, work with Fiftwo to ensure the carryforward is correct

• Projects outside the three years (expired projects)

• IHEs must work with Fiftwo to process the budget documents to carryforward any amount encumbered as of June 30 and attach encumbrance documentation

• IHEs process budget documents to revert unencumbered amount

• Due date is Period 13 Close (August 3rd)

• Use the infoAdvantage Report OSC-019 Continuing/Expiring Capital Construction Project to identify expiring projects

31

Capital Construction – Emergency

Maintenance Projects • DPA receives an annual appropriation for EM projects

• DPA may choose to pay for and complete an EM project at an

IHE. The expenditures are recorded by DPA, however:

Capitalizable Expenses • If the project meets the requirements of increasing the capacity,

efficiency, or extending the useful life of the asset, the IHE should capitalize the cost of the project on its books once completed

Non-Capitalizable Expenses • For TABOR purposes expenditures must also be duplicated in IHE’s Funds

(305x/320x) to support the calculation of state support

• IHE Entry: Dr: Expense and Cr: RSRC 8800-Contributed Capital

• infoAdvantage Report OSC-015 Higher Ed Non-capitalizable DPA Emergency Controlled Maintenance Projects was created to help IHEs reconcile their expenditures to DPA. By year end, expenditures should agree.

32

4/10/2018

17

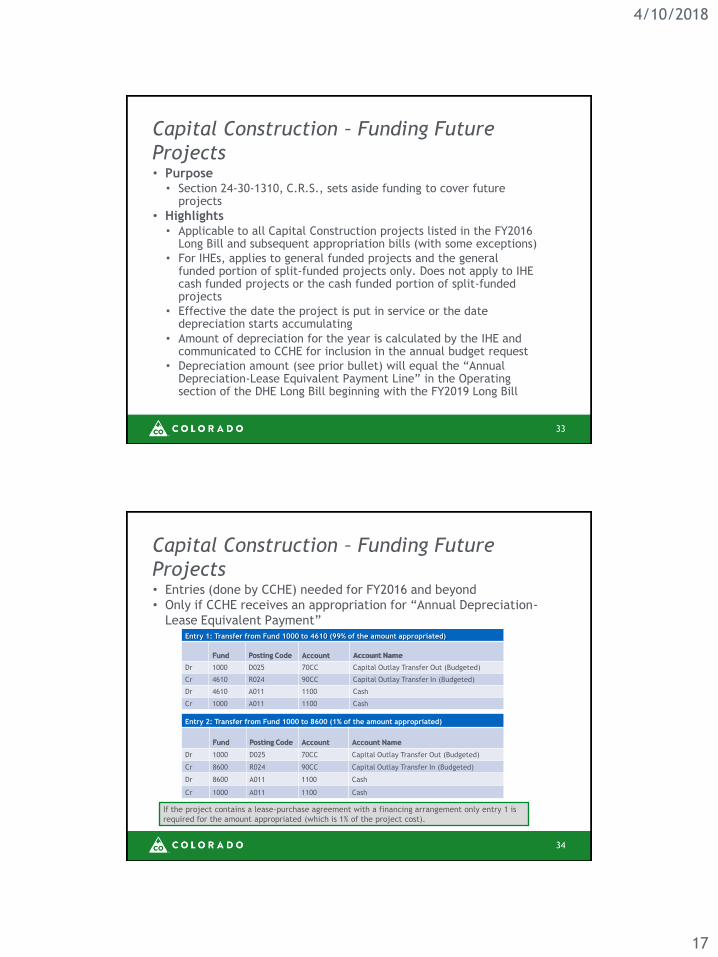

Capital Construction – Funding Future

Projects • Purpose

• Section 24-30-1310, C.R.S., sets aside funding to cover future projects

• Highlights • Applicable to all Capital Construction projects listed in the FY2016

Long Bill and subsequent appropriation bills (with some exceptions)

• For IHEs, applies to general funded projects and the general funded portion of split-funded projects only. Does not apply to IHE cash funded projects or the cash funded portion of split-funded projects

• Effective the date the project is put in service or the date depreciation starts accumulating

• Amount of depreciation for the year is calculated by the IHE and communicated to CCHE for inclusion in the annual budget request

• Depreciation amount (see prior bullet) will equal the “Annual Depreciation-Lease Equivalent Payment Line” in the Operating section of the DHE Long Bill beginning with the FY2019 Long Bill

33

Capital Construction – Funding Future

Projects • Entries (done by CCHE) needed for FY2016 and beyond

• Only if CCHE receives an appropriation for “Annual Depreciation-

Lease Equivalent Payment”

34

If the project contains a lease-purchase agreement with a financing arrangement only entry 1 is

required for the amount appropriated (which is 1% of the project cost).

Entry 1: Transfer from Fund 1000 to 4610 (99% of the amount appropriated)

Fund Posting Code Account Account Name

Dr 1000 D025 70CC Capital Outlay Transfer Out (Budgeted)

Cr 4610 R024 90CC Capital Outlay Transfer In (Budgeted)

Dr 4610 A011 1100 Cash

Cr 1000 A011 1100 Cash

Entry 2: Transfer from Fund 1000 to 8600 (1% of the amount appropriated)

Fund Posting Code Account Account Name

Dr 1000 D025 70CC Capital Outlay Transfer Out (Budgeted)

Cr 8600 R024 90CC Capital Outlay Transfer In (Budgeted)

Dr 8600 A011 1100 Cash

Cr 1000 A011 1100 Cash

4/10/2018

18

Open/Close Procedures

35

Unrealized Gain/Loss

• Treasury Pooled Cash • OSC will provide the allocation to IHEs by July 25 if IHEs

have cut off cash entries

• Allocation is based on IHE BSA 1100 balance as of period 12 close

• IHEs should feed or post allocation to CORE by August 3

• Accounts to use:

• BSA 1105 – Cumulative Unrealized Gain/Loss on Treasury Pooled Cash

• RSRC 6050 – Unrealized Gain/Loss

36

4/10/2018

19

Unrealized Gain/Loss

• Institution-Held Investments • IHEs determine allocation

• Difference between book and market value as reported on Exhibit N1

• IHEs should feed or post allocation to CORE by August 3

• Accounts to use:

• BSA 1605 – Cumulative Unrealized Gain/Loss on Investment

• RSRC 6050 – Unrealized Gain/Loss

37

Receivable/Payable Confirmations

• Same process as in the past • Seller must initiate, except CU

• Payable/Receivable confirmation forms are due to the

buyer by July 27 • If confirmation is after July 27, the buyer can refuse to

confirm

• Payable/Receivable confirmation forms are due from

the seller to the OSC by August 7 • Unconfirmed amounts may require the OSC to reclass

balances for financial statement purposes

• Please reconcile and clear old balances or move unconfirmed balances remaining in the internal accounts to other or external receivable and payable accounts

38

4/10/2018

20

Compensated Absences - PERA

• Percentage of state employees expected to retire with

PERA benefits not yet available

• Will be provided as soon as OSC receives it from PERA’s

actuary

39

Estimates

• Do not change methodology after period 14 close

• Do not submit a period 15 or 16 entry just to revise an

estimate • Estimates should be based on the best information

available as of fiscal year close

• Do submit a period 15 or 16 entry for calculation errors

• Do submit revised estimate for contingences reported on

Exhibit L, if applicable

40

4/10/2018

21

Quarterly Reporting

• Quarterly reports due within 2 weeks after quarter close

in CORE

• OSC will follow up if report is not submitted or if there

are questions

• New in FY2018: CORE security certification

• Diagnostic report training guide will be published on

Fiscal Procedures Manual website: www.colorado.gov/osc/fiscalprocedures

• This is a work in progress

• More reports will be added in the future

• Eventually will be incorporated into Fiscal Procedures Manual

41

Indirect Cost and Federal

Reporting Unit

42

4/10/2018

22

Federal Reporting Requirements (Single

Audit)

• OMB Uniform Guidance, 2 CFR 200.511 Audit Findings

Follow-up

• .511(b) Summary Schedule of Prior Audit Findings

• Auditees must report status of prior single audit findings

• OSC compiles statewide Schedule

• Exhibit K3 – Schedule of Prior Year Audit Recommendation Status

• OSC will provide Exhibit K3 to departments/IHEs, pre-populated with the recommendations required to be reported

• Due to OSC July 6

43

Federal Reporting Requirements (Single

Audit)

• OMB Uniform Guidance, 2 CFR 200.511 Audit Findings

Follow-up

• .511(c) Corrective Action Plan

• Auditee must prepare a document, separate from auditor’s reporting of findings (recommendations)

• OSC compiles statewide Plan

• At conclusion of single audit, the OSC will send departments/IHEs a list of recommendations to address

• Departments/IHEs should respond by providing Final Approved Audit Response Forms to the OSC

• Due to OSC upon request after release of Single Audit Report

44

4/10/2018

23

Federal Reporting Requirements (Single

Audit)

• OMB Uniform Guidance, 2 CFR 200.510 Financial

Statements

• .510(b) Schedule of Expenditures of Federal Awards (SEFA)

• OSC compiles statewide SEFA

• Exhibit K1 – Schedule of Federal Assistance

• Federal Award Expenditures for the State Fiscal Year

• The Exhibit validates the information reported for: o Valid values

o Completeness of required information

o Provides an Error Message if information reported is invalid or incomplete

o Due to OSC October 1

45

TABOR

• TABOR nonexempt and re-qualifying enterprises for

FY2018 • Western State Colorado University expected to re-qualify

• State Fair expected to disqualify

• Reminder: AHEC is only partially designated

• New TABOR enterprise – Colorado Healthcare

Affordability and Sustainability Enterprise in Department

UHAA (Fund 2410)

• Exhibits A1 and A2 due to OSC on August 15

• Variance analysis due to OSC on August 17

46

4/10/2018

24

Cost Allocation Plans

• OSC prepares Statewide Cost Allocation Plan (SWCAP) and negotiates agreement with the federal cognizant agency (Health and Human Services, Cost Allocation Services Department in San Francisco)

• OSC prepares Statewide Appropriations/Cash Fees Plan and answers any questions from the OSPB, JBC, legislature and budget staff

• OSC provides assistance/guidance related to the Indirect Cost Rate Proposal’s (ICRP) preparation, negotiation, applicable regulations and recovery issues

• Departments with federal grants are responsible for preparation of Cost Allocation Plan (CAP), Public Assistance Cost Allocation Plan (PACAP) or ICRP within 6 months of the Fiscal Year end. • Submit negotiated agreement to the OSC after the

agreement has been signed.

47

Financial Reporting and

GASB Pronouncements

48

4/10/2018

25

GASB Pronouncements

Effective for Fiscal Year 2018

• GASB Statement No. 75 – Accounting and Financial

Reporting for Postemployment Benefits Other Than Pensions

• GASB Statement No. 81 – Irrevocable Split-Interest Agreements

• GASB Statement No. 85 – Omnibus 2017

• GASB Statement No. 86 – Certain Debt Extinguishment Issues

49

GASB Statement No. 75 – Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions

• Regarding OPEB, GASB 75 is almost identical to GASB 68

– the pension accounting standard implemented in FY

2015.

• The standard replaces GASB 45 and is effective for the

fiscal year ending June 30, 2018.

• The principal objective of this Statement is to improve

the usefulness of information for decisions made by the

various users of the general purpose external financial

reports (CAFR) of governments whose employees—both

active and inactive employees—are provided with

postemployment benefits other than pensions.

50

4/10/2018

26

GASB Statement No. 75 – Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions

• What are Other Post-employment Benefits? • Postemployment healthcare benefits such as medical,

dental, vision, hearing, and other health-related benefits—whether provided separately from or provided through a pension plan.

• Other forms of postemployment benefits—for example, death benefits, life insurance, disability, and long-term care—when provided separately from a pension plan.

• OPEB does not include termination benefits or termination payments for sick leave.

51

GASB Statement No. 75 – Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions

• Does this standard apply to my situation? • Most definitely. The standard applies to defined benefit

and defined contribution plans provided to the employees of state and local government employers administered through a trust whereby: Contributions from employers to the OPEB plan as well as

earnings on those contributions are irrevocable.

OPEB plan assets are dedicated to providing OPEB to plan members in accordance with the benefit terms.

OPEB plan assets are legally protected from the creditors of employers, and the OPEB plan administrator. If the plan is a defined benefit OPEB plan, plan assets also are legally protected from creditors of the plan members.

• The Health Care Trust Fund administered by PERA meets the criteria as a cost-sharing, multiple employer defined benefit OPEB plan subject to GASB 75 reporting.

52

4/10/2018

27

GASB Statement No. 75 – Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions

• What is the PERA Health Care Trust Fund (HCTF)? • The HCTF provides a health care premium subsidy to

participating PERA benefit recipients and retirees who choose to enroll in one of the PERA health care plans.

• All benefit recipients under the PERA benefit structure are eligible for a premium subsidy, if enrolled in a health care plan under PERACare.

• Contribution requirements are established by statute under Section 24-51-208, C.R.S. Affiliated PERA employers must submit contributions for all PERA members equal to 1.02 percent of covered salaries.

• Employer contributions and investment earnings on the assets pay for the cost of the premium subsidies and the administrative costs incurred by the funds.

53

GASB Statement No. 75 – Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions

• What is the impact of this standard?

• The State will have to recognize on it’s financial statements a collective net OPEB liability for the difference between the value of the HCTF Plan Assets minus the amount of future OPEB benefits earned by employees and retirees. For example:

As of December 31, 2016:

Actuarial value of assets $ 270,150,000

Actuarial accrued liability 1,556,762,000

Unfunded actuarial accrued liability $1,286,612,000

• A significant portion of the approximately $1.3 trillion liability belongs to the State and Judicial Divisions, and will be added to the face of the Statement of Net Position in the CAFR.

• Similar to the GASB 68 pension standard, the OSC will calculate and book the entries required to comply with the standard.

54

4/10/2018

28

GASB Statement No. 75 – Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions

• What calculations will the OSC be making?

• Prior Period Adjustment for the net OPEB liability as of 12/31/2016.

• Updates to the net OPEB liability, recognition of deferred inflows and outflows of resources, and amortization of those deferrals to OPEB expense during Fiscal Year 2018 impacted by:

• Changes in the Plan’s economic or demographic assumptions used to project future benefits (such as longevity of retirees)

• Differences between those particular assumptions versus what was actually experienced

• Difference between the Plan’s actual versus expected investment returns.

• Change in the employer’s (i.e. department’s) allocation percentage of the OPEB liability from 2016 to 2017.

• Difference between actual contributions made by the employer versus the employer’s proportionate share of total contributions made to the Plan.

55

GASB Statement No. 75 – Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions

• What calculations will the OSC be making (cont.)? • Other adjustments include:

• Contributions made to the plan after the Plan’s measurement date of 12/31/17 (Jan – Jun 2018)

• OPEB expense adjustments:

o Current period service cost

o Interest on the OPEB liability

o Changes in benefit terms

o Projected earnings on the Plan’s investments

o Plan administrative costs

o Amortization of employer-level deferred inflows and outflows

56

4/10/2018

29

GASB Statement No. 75 – Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions

• What happens next? • The OSC has created a workbook that will calculate and

provide detailed entries that it will post on behalf of most state entities (except IHEs).

• The workbook will be provided in early August once the OSC receives the updated Schedules to be provided by PERA – after PERA’s CAFR is released in mid to late July.

• OSC will maintain statewide amortization schedules and post entries in P15, except that IHE’s will record entries on their systems and feed to CORE.

57

GASB Statement No. 75 – Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions

• What happens next (cont.)? • The OSC will request payroll contribution information

from IHEs to assist with validation entries.

• The OSC will draft suggested disclosures for IHEs and other stand-alone financial statement

• Agency controllers and staff should review the entries for their agency when distributed.

58

4/10/2018

30

GASB Statement No. 81 – Irrevocable Split-Interest

Agreements

• Split-interest agreements are a type of giving agreement

used by donors to provide resources to two or more

beneficiaries, including governments.

• Split-interest agreements can be created through

trusts—or other legally enforceable agreements with

characteristics that are equivalent to split-interest

agreements—in which a donor transfers resources to an

intermediary to hold and administer for the benefit of a

government and at least one other beneficiary.

• Examples of these types of agreements include

charitable lead trusts, charitable remainder trusts, and

life-interests in real estate.

59

GASB Statement No. 81 – Irrevocable Split-Interest

Agreements

• This Statement requires that a government that receives

resources pursuant to an irrevocable split-interest

agreement recognize assets, liabilities, and deferred

inflows of resources at the inception of the agreement.

• Furthermore, it requires that a government recognize

assets representing its beneficial interests in irrevocable

split-interest agreements that are administered by a

third party, if the government controls the present

service capacity of the beneficial interests.

• This Statement also requires that a government

recognize revenue when the resources become

applicable to the reporting period.

60

4/10/2018

31

GASB Statement No. 81 – Irrevocable Split-Interest

Agreements

• A typical irrevocable split-interest agreement has two

components: a lead interest and a remainder interest.

• A government is a lead interest when the agreement provides periodic disbursements throughout the term of the agreement.

• A government has a remainder interest when it receives the final disbursement at the termination of the agreement.

• Typically, the government is either a lead interest or has a remainder interest, and the other beneficiary serves as the opposite interest.

• Depending on the type of agreement, payments can be fixed such as in an annuity, or variable such as a percentage of fair value of the assets at each measurement period.

• A government entity may also serve as an intermediary – where

it serves to administer the resources of the agreement to the

beneficiaries.

61

GASB Statement No. 81 – Irrevocable Split-Interest

Agreements

• If the government is both the intermediary and has a remainder

interest, it must record:

• Assets for the resources

• A liability for the lead interest assigned to other beneficiaries

• A deferred inflow of resources for the government’s unconditional remainder interest.

• Changes in assets resulting from items such as interest, dividends, and changes in fair value should be recognized as increases and decreases to deferred inflows.

• If the government is both intermediary and has a lead interest,

it will record a deferred inflow for the lead interest and a

liability for the remainder interest assigned to others.

• If the government is not the intermediary, an asset and a

related deferred inflow should be recorded for the amount of

their interest – whether lead or remainder.

62

4/10/2018

32

GASB Statement No. 85 – Omnibus 2017

Covers the following: • Blending a component unit in circumstances in which the

primary government is a business-type activity that reports in a

single column for financial statement presentation.

• Reporting amounts previously reported as goodwill and

“negative” goodwill.

• Classifying real estate held by insurance entities.

• Measuring certain money market investments and participating

interest-earning investment contracts at amortized cost.

• Recognizing on-behalf payments for pensions or OPEB in

employer financial statements.

63

GASB Statement No. 85 – Omnibus 2017

Covers the following (cont.): • Timing of the measurement of pension or OPEB liabilities and

expenditures recognized in financial statements prepared using

the current financial resources measurement focus.

• Presenting payroll-related measures in required supplementary

information for purposes of reporting by OPEB plans and

employers that provide OPEB.

• Classifying employer-paid member contributions for OPEB.

• Simplifying certain aspects of the alternative measurement

method for OPEB.

• Accounting and financial reporting for OPEB provided through

certain multiple-employer defined benefit OPEB plans.

64

4/10/2018

33

GASB Statement No. 86 – Certain Debt Extinguishment

Issues

• This Statement provides guidance for transactions in which cash

and other monetary assets acquired with only existing resources

(the government’s own resources—resources other than the

proceeds of refunding debt)—are placed in an irrevocable trust

for the sole purpose of extinguishing debt.

• This Statement also improves accounting and financial reporting

for prepaid insurance on debt that is extinguished and notes to

financial statements for debt that is defeased in substance.

• The provisions of this standard likely does not apply to most

state agencies and institutions of higher education. Please reach

out to your assigned Financial Services Specialist if you think you

might have this situation at your agency.

65

Questions?

Please reach out to Jeffrey Kahn, Paul Reynolds, or your assigned FSU Financial Specialist with any questions or concerns regarding the implementation of new GASBs.

Jeffrey Kahn – Director of Financial Reporting & Analysis

(303) 866-2659

Paul Reynolds – Financial Reporting Manager

(303) 866-3468

66

4/10/2018

34

Closing

67

Closing

• Thank you for coming!

• Please sign-in on the sign in sheets if you haven’t

already done so

• Leave evaluation and CPE forms on the tables when you

leave • Remote attendees: email evaluations and CPE forms to

• CPE forms will be signed and emailed to you

68

4/10/2018

35

Contact List

Phone: (303) 866-xxxx

Email: [email protected] or [email protected]

Jeffrey Kahn, Director—2659

Financial Services Unit* Financial Reporting

Tom Gamache—5657 Paul Reynolds—3811

Karoline Clark—3811 John McIntosh—6327

Jennifer Henry—3809 Bruce Haefner—4662

Daniel Saint—3891

Donna Hocker—4058 Indirect Cost & Federal Reporting

Fifonsi Dossou—4160 Bhavna Punatar—4344

Mohamed Mashkooke—4162 Marc Burkepile—3346

Mark Davis—4041

Internal Audit

Jeff Lee—2733

Brad Treiber—5830 *FSU Assignments: www.colorado.gov/pacific/osc/fast

69