aicpa professional issues update ernie almonte cpa, cfe ri auditor general and aicpa vice chair...

TRANSCRIPT

AICPA Professional Issues UpdateErnie Almonte CPA, CFE

RI Auditor General and AICPA Vice Chair

National State Auditors Association – June 2008

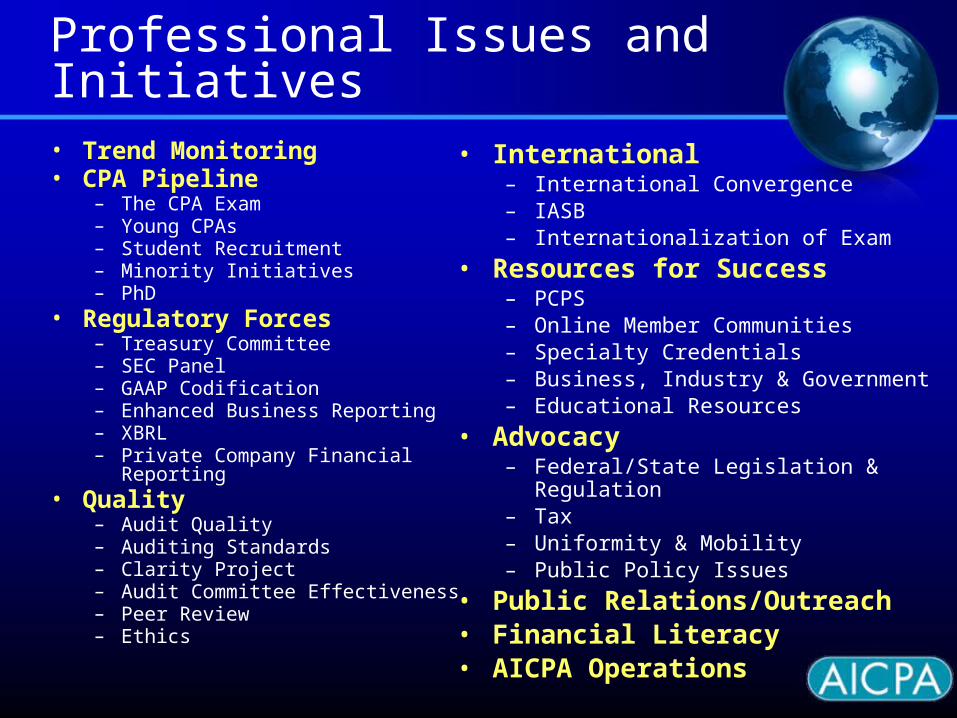

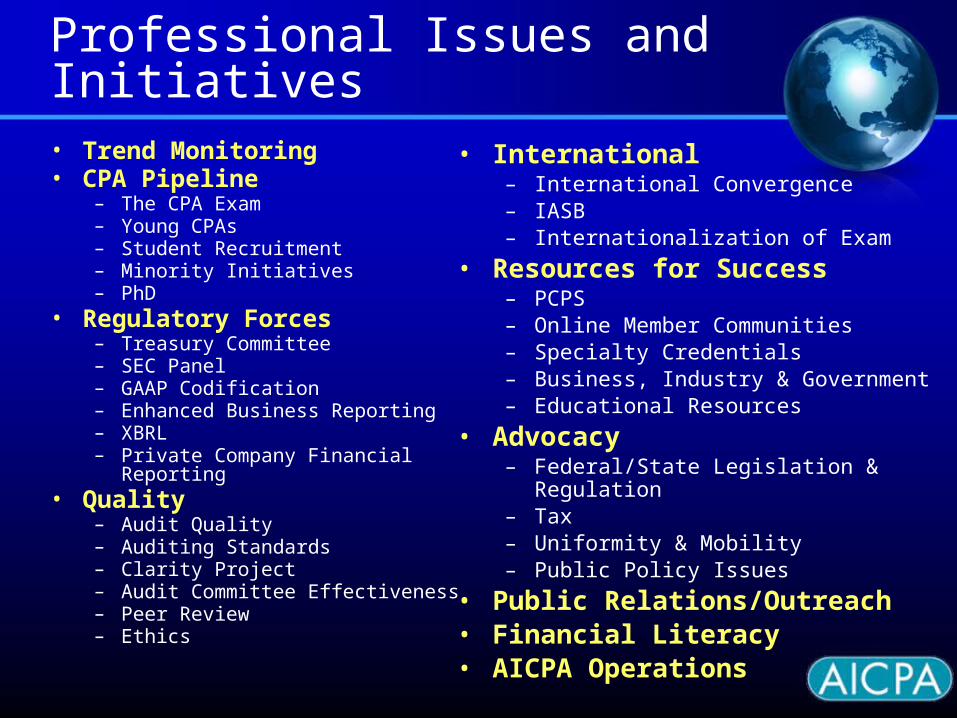

Professional Issues and Initiatives• Trend Monitoring• CPA Pipeline

– The CPA Exam– Young CPAs– Student Recruitment– Minority Initiatives– PhD

• Regulatory Forces– Treasury Committee– SEC Panel– GAAP Codification– Enhanced Business Reporting– XBRL– Private Company Financial Reporting

• Quality– Audit Quality – Auditing Standards– Clarity Project– Audit Committee Effectiveness– Peer Review– Ethics

• International– International Convergence– IASB– Internationalization of Exam

• Resources for Success– PCPS – Online Member Communities– Specialty Credentials– Business, Industry & Government– Educational Resources

• Advocacy– Federal/State Legislation & Regulation– Tax– Uniformity & Mobility– Public Policy Issues

• Public Relations/Outreach• Financial Literacy• AICPA Operations

Our World at a Glance

• Unemployment rising• Wage increases falling behind inflation• Boomers delaying retirement• Health benefits dropping• Housing market slumping• Consumer confidence declining• Gas prices soaring• Worker attitudes changing• Web 3.0 is already emerging• Accounting remains in high demand• Globalization accelerating, with convergence imminent

CPA Pipeline

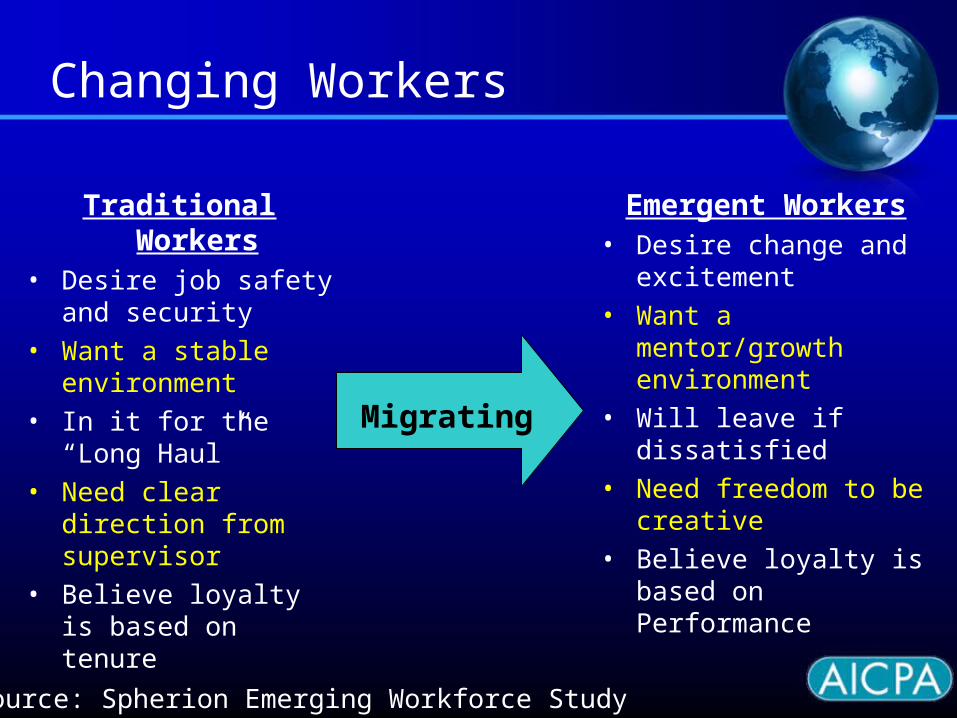

Changing Workers

Traditional Workers• Desire job safety and

security • Want a stable

environment • In it for the “Long

Haul” • Need clear direction

from supervisor• Believe loyalty is

based on tenure

Emergent Workers• Desire change and

excitement • Want a mentor/growth

environment • Will leave if dissatisfied • Need freedom to be

creative • Believe loyalty is based

on Performance

Migrating

Source: Spherion Emerging Workforce Study

2%6%

16%

0%

10%

20%

30%

High School Early College

General population SHGP members

27%

6

• SHGP high school members are 8X as likely to plan on majoring in accounting.

• SHGP early college members are 4X as likely to declare accounting as their major.

Average Percentage of Students Planning on Declaring Accounting

As Their Major, 2002-2007

StartHereGoPlaces.com

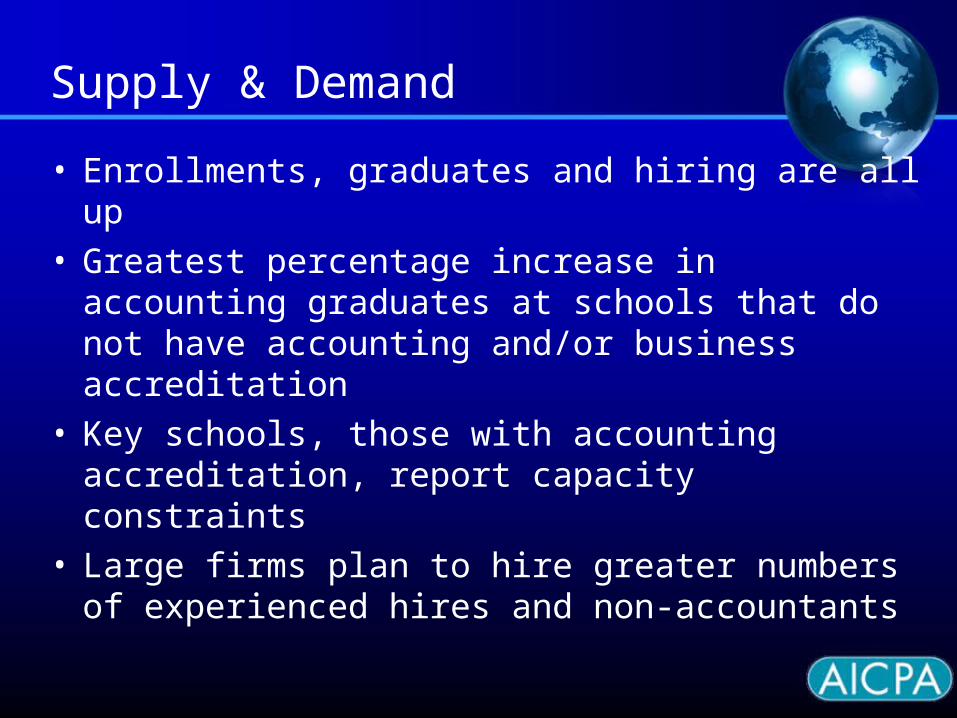

Supply & Demand

• Enrollments, graduates and hiring are all up• Greatest percentage increase in accounting

graduates at schools that do not have accounting and/or business accreditation

• Key schools, those with accounting accreditation, report capacity constraints

• Large firms plan to hire greater numbers of experienced hires and non-accountants

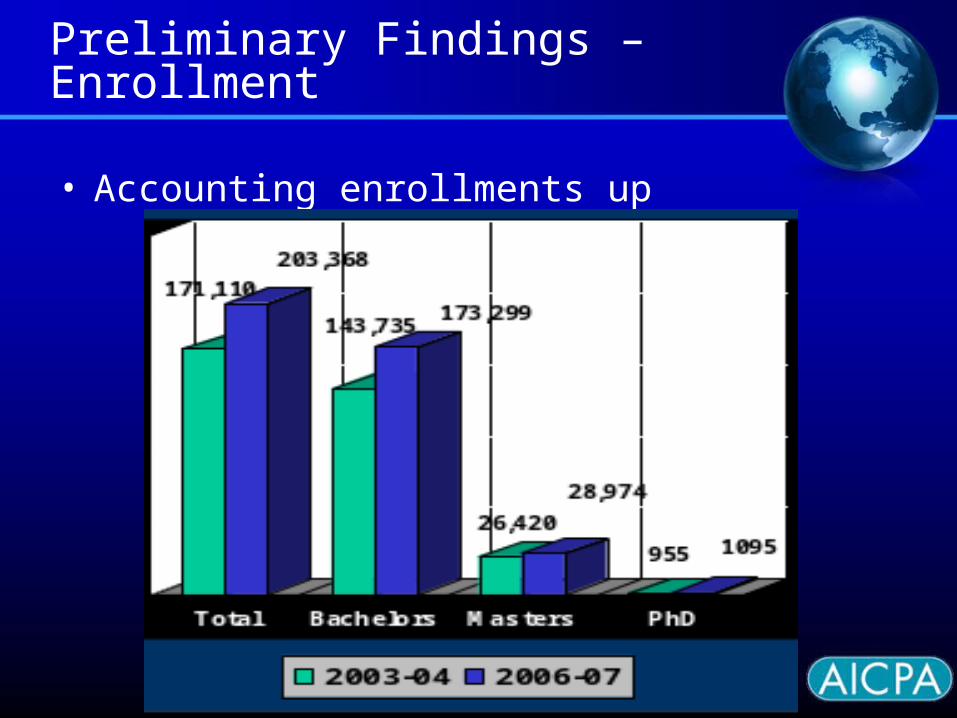

Preliminary Findings – Enrollment

• Accounting enrollments up

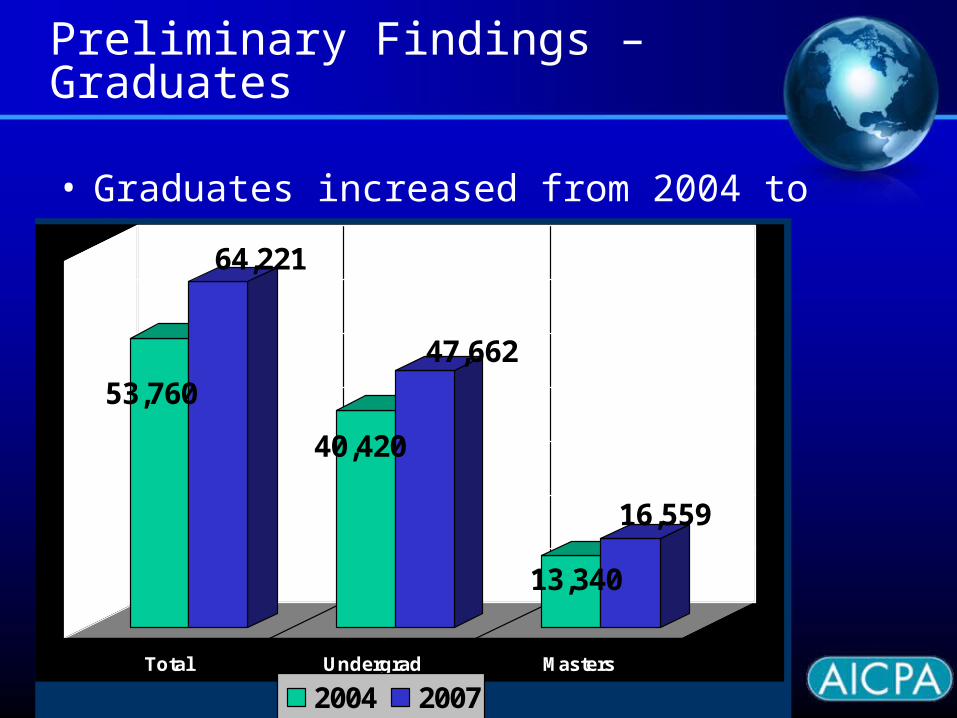

Preliminary Findings – Graduates

• Graduates increased from 2004 to 2007

53,760

64,221

40,420

47,662

13,340

16,559

Total Undergrad Masters

2004 2007

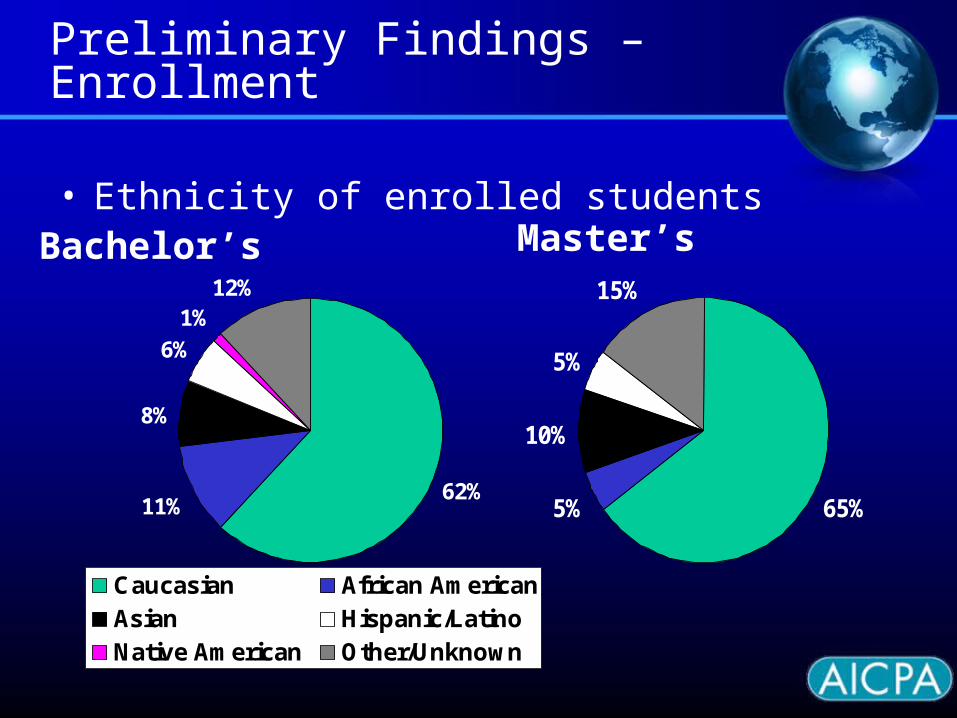

Preliminary Findings – Enrollment

• Ethnicity of enrolled students

65%5%

10%

5%

15%

62%11%

8%

6%

1%12%

Caucasian African AmericanAsian Hispanic/LatinoNative American Other/Unknown

Bachelor’s Master’s

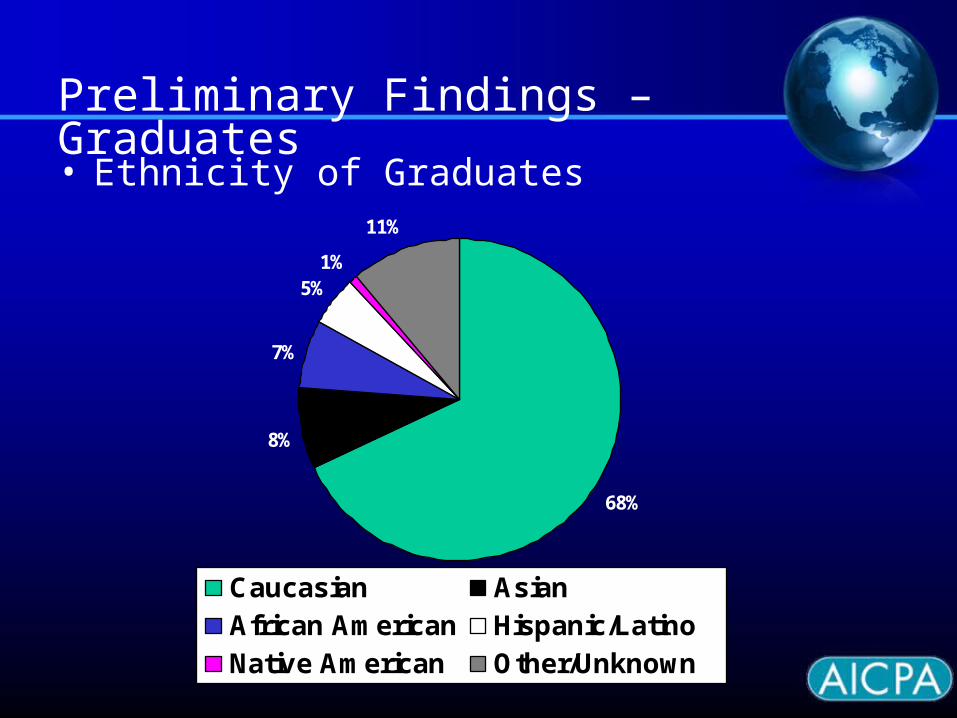

Preliminary Findings – Graduates• Ethnicity of Graduates

68%

8%

7%

1%

11%

5%

Caucasian AsianAfrican American Hispanic/LatinoNative American Other/Unknown

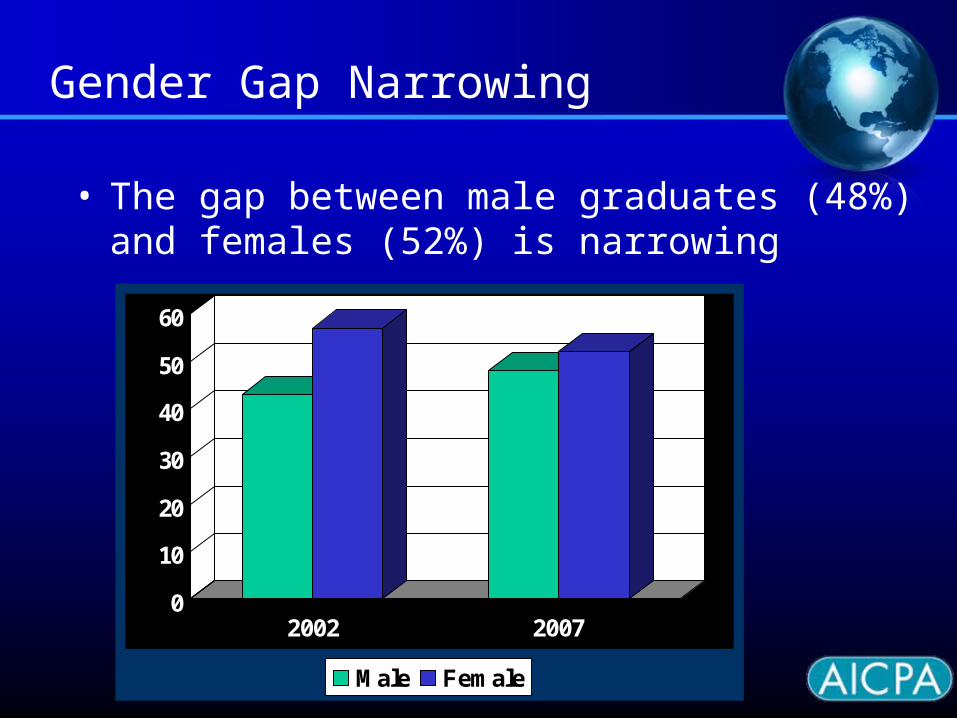

Gender Gap Narrowing

• The gap between male graduates (48%) and females (52%) is narrowing

0

10

20

30

40

50

60

2002 2007

Male Female

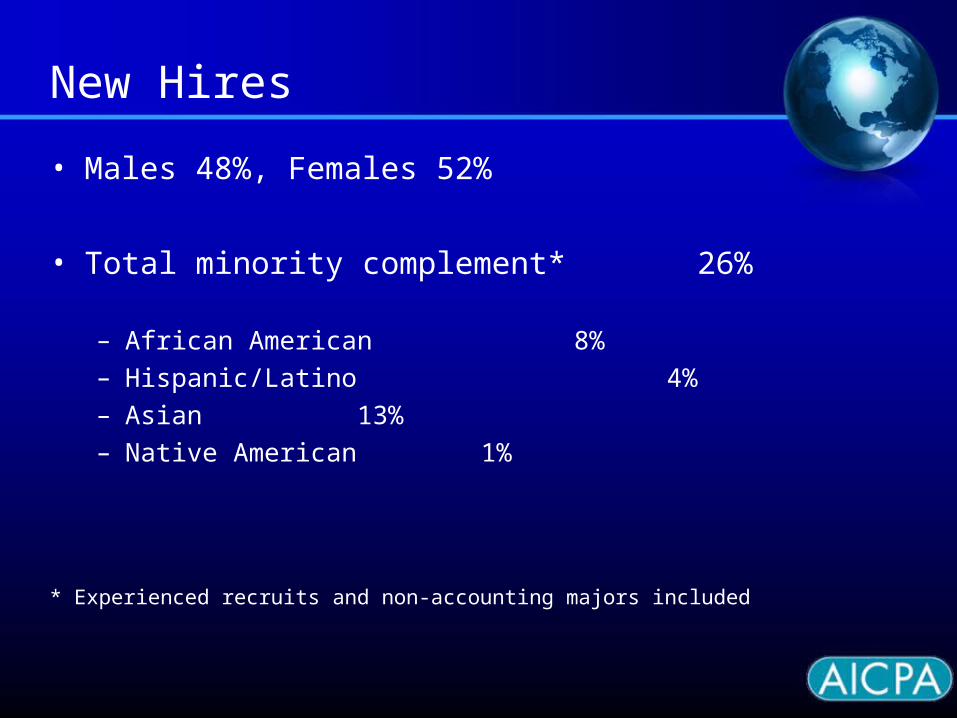

New Hires

• Males 48%, Females 52%

• Total minority complement* 26% – African American 8% – Hispanic/Latino 4% – Asian 13% – Native American 1%

* Experienced recruits and non-accounting majors included

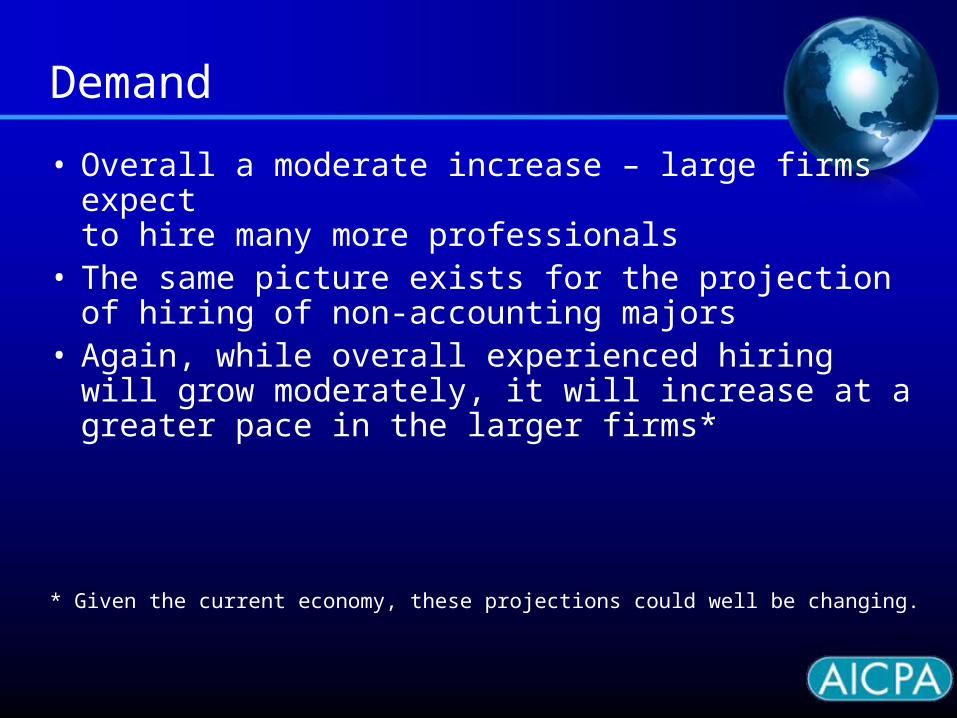

Demand

• Overall a moderate increase – large firms expect to hire many more professionals

• The same picture exists for the projection of hiring of non-accounting majors

• Again, while overall experienced hiring will grow moderately, it will increase at a greater pace in the larger firms*

* Given the current economy, these projections could well be changing.

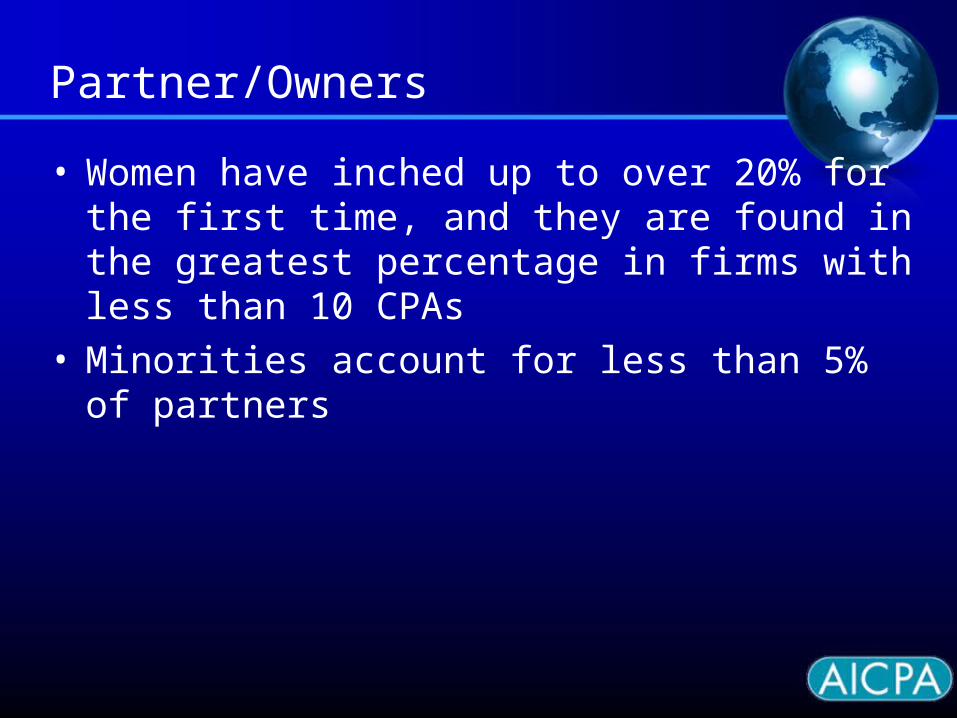

Partner/Owners

• Women have inched up to over 20% for the first time, and they are found in the greatest percentage in firms with less than 10 CPAs

• Minorities account for less than 5% of partners

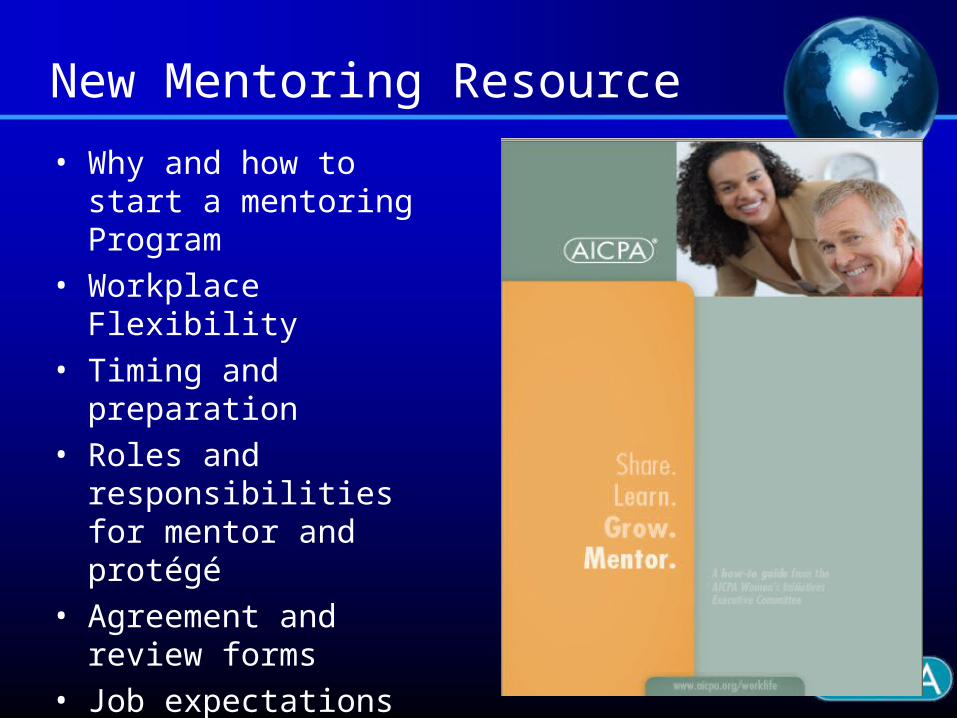

New Mentoring Resource

• Why and how to start a mentoring Program

• Workplace Flexibility• Timing and preparation• Roles and responsibilities

for mentor and protégé• Agreement and review

forms• Job expectations

checklist

Faculty Shortage Issue

• New studies confirm shortage

• Shortage approaching 20%

• Only 23% of demand for audit and 27% of demand for tax being met

• Programs may be forced to reduce enrollments in undergraduate programs

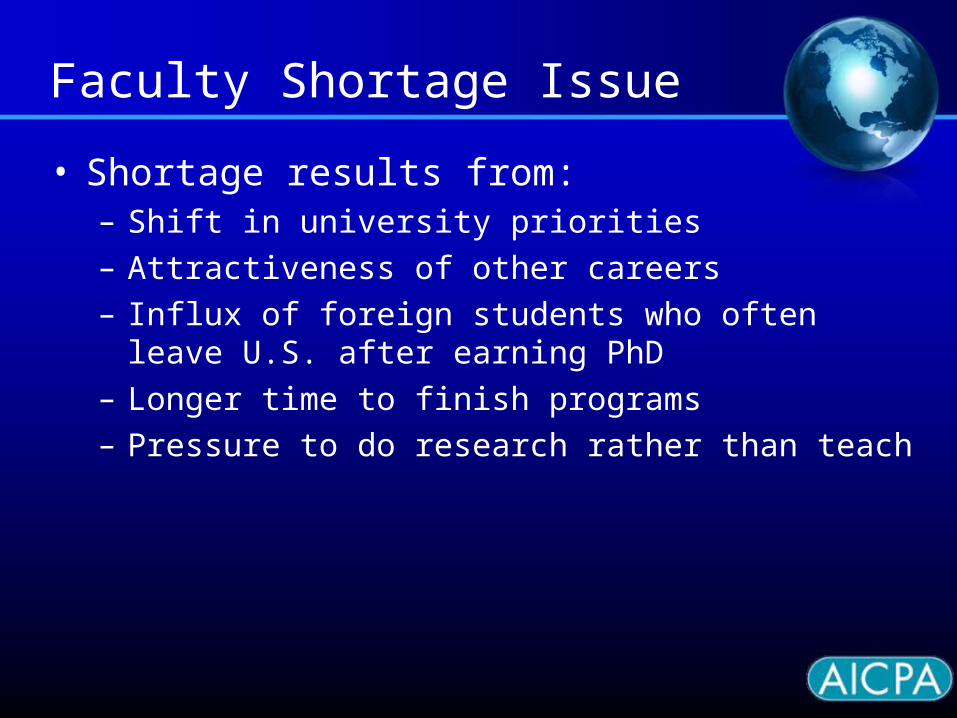

Faculty Shortage Issue

• Shortage results from:– Shift in university priorities– Attractiveness of other careers– Influx of foreign students who often leave U.S. after

earning PhD– Longer time to finish programs– Pressure to do research rather than teach

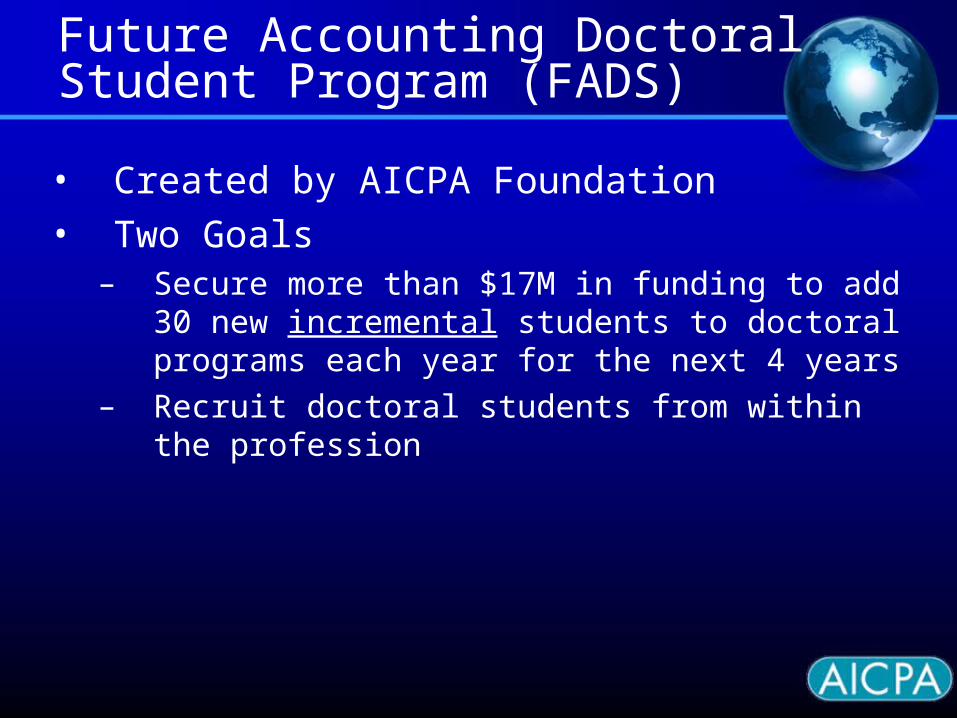

Future Accounting Doctoral Student Program (FADS)

• Created by AICPA Foundation• Two Goals

– Secure more than $17M in funding to add 30 new incremental students to doctoral programs each year for the next 4 years

– Recruit doctoral students from within the profession

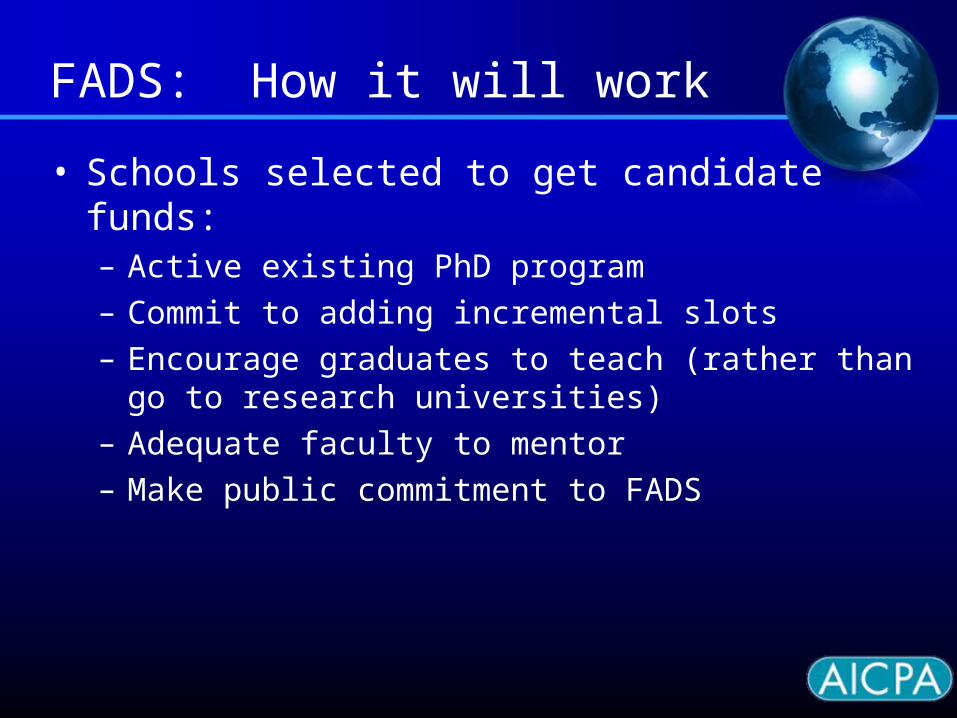

FADS: How it will work

• Schools selected to get candidate funds:– Active existing PhD program– Commit to adding incremental slots– Encourage graduates to teach (rather than go to

research universities)– Adequate faculty to mentor– Make public commitment to FADS

Regulatory Forces

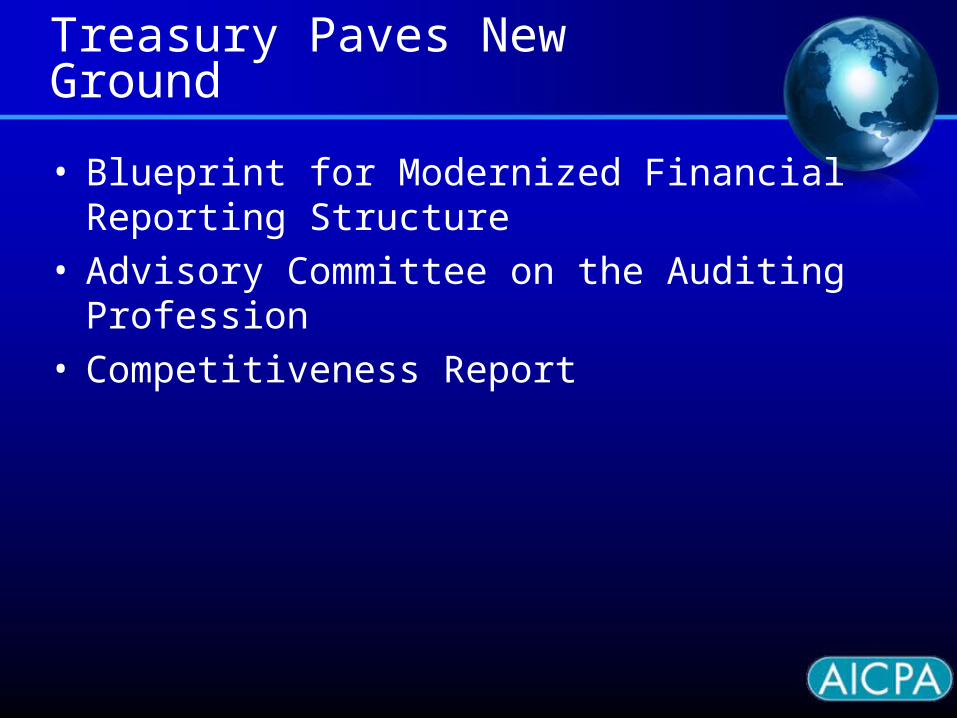

Treasury Paves New Ground

• Blueprint for Modernized Financial Reporting Structure

• Advisory Committee on the Auditing Profession• Competitiveness Report

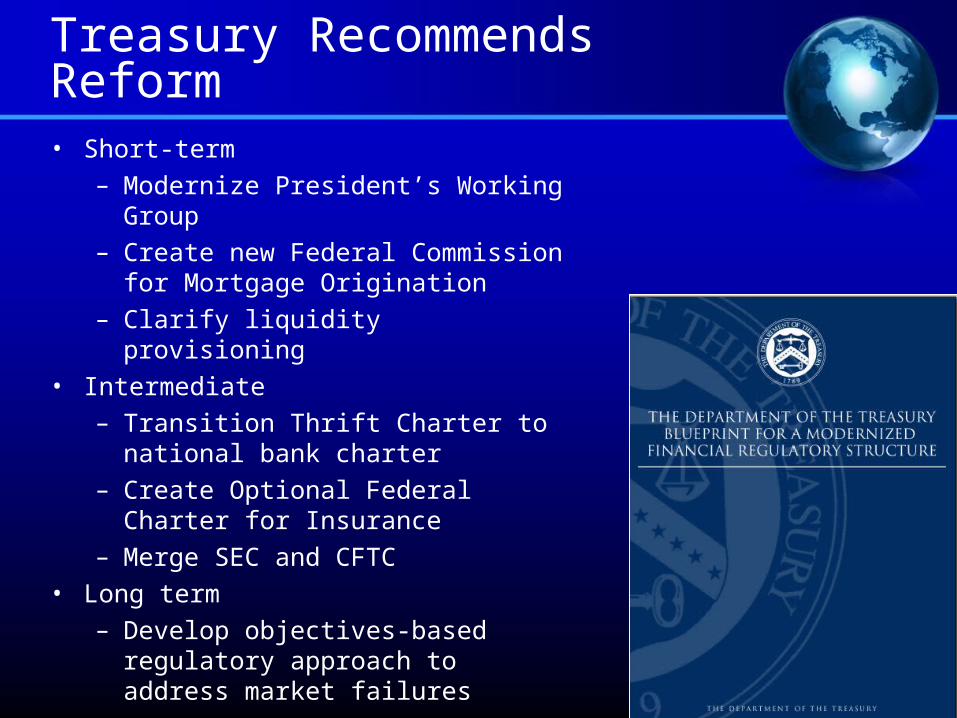

Treasury Recommends Reform• Short-term

– Modernize President’s Working Group

– Create new Federal Commission for Mortgage Origination

– Clarify liquidity provisioning • Intermediate

– Transition Thrift Charter to national bank charter

– Create Optional Federal Charter for Insurance

– Merge SEC and CFTC • Long term

– Develop objectives-based regulatory approach to address market failures

Treasury Competitiveness Study

• Investigates public company restatements 1997-2006

• Topline findings:– Restatements

started to increase before SOX

– After SOX, restatements due to fraud declined

Advisory Committee on the Auditing Profession

• 21 members + 5 observers

• Chairs: Arthur Levitt and Don Nicolaisen

• 4 meetings • 3 subcommittees:

– Human Capital– Firm Structure and

Finances– Concentration and

Competition

Preliminary Recommendations: Human Capital

• Keep curricula current by continuing to update exam, teaching materials/content, and accreditation standards

• Ensure robust faculty supply, including professionally qualified, and more sabbaticals

• Improve minority representation by reaching out to other disciplines, working with community colleges, cross-sabbaticals at HBCUs

• Capture more demographic and higher education data

Preliminary Recommendations:Firm Structure and Finances

• Create fraud center to share experiences and best practices

• Clarify auditor’s role in detecting fraud • Recommend that Congress require state adoption

of UAA mobility provisions after 2010/2011, for those states not uniform

• Encourage federal and state regulators to avoid overlapping enforcement conundrum

Preliminary Recommendations:Firm Structure and Finances

• Greater financial and operational independence of state boards of accountancy

• Encourage firms to add independent board members, or create advisory boards

• Revise Form 8-K to require more information about public company auditor changes

• Further study on firm transparency• Further study on liability issues

Preliminary Recommendations:Concentration and Competition

• Promote growth of smaller auditing firms• Require disclosure of any provisions limiting

auditor choice• PCAOB monitoring of potential sources of

catastrophic risk for public company audit firms• Mechanism to preserve and rehabilitate troubled

larger auditing firms

Preliminary Recommendations:Concentration and Competition

• Promote understanding of independence standards by creating a Web-based compilation of independence requirements

• Develop additional training materials on independence, and require PCAOB to inspect independence training within firms

• Require annual shareholder ratification of auditors• Enhance collaboration between PCAOB and

foreign regulators

GAO Report on Audit Market Concentration

• Audit market for large public companies remains highly concentrated, while smaller public company market has become significantly less concentrated

• Market concentration doesn’t appear to have significant negative impact

• Large public company audit concentration is unlikely to be reduced in the near term

• No consensus for addressing market concentration

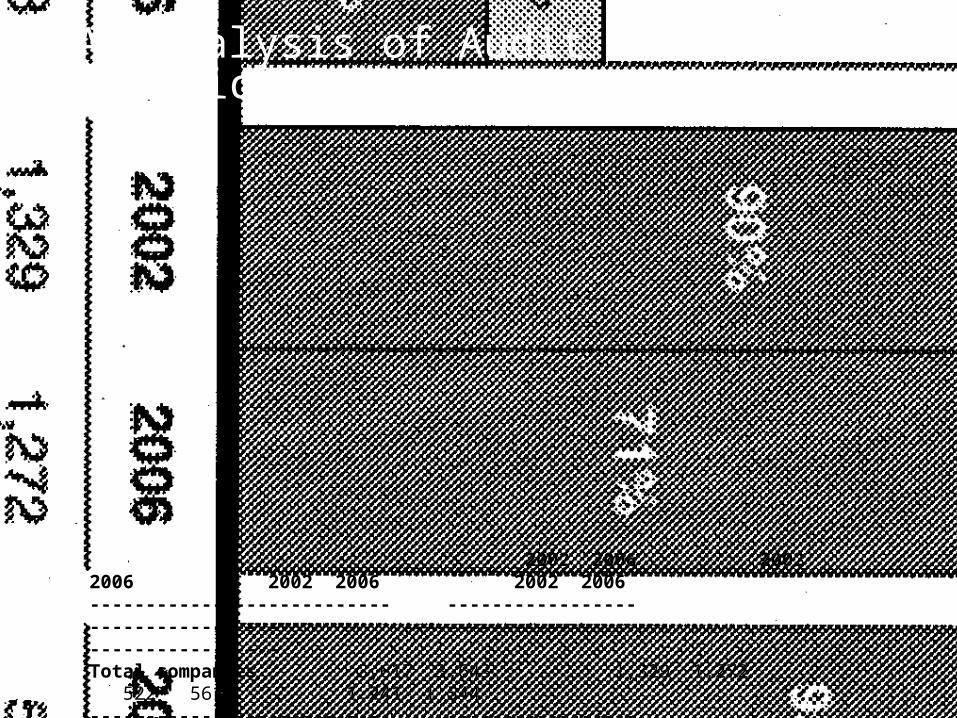

GAO Analysis of Audit Analytics Data

2002 2006 2002 2006 2002 2006 2002 2006--------------------------- ----------------- ------------------ ----------------- -----------------Total companies 3,617 3,643 1,329 1,272 522 561 1,241 1,544--------------------------- ----------------- ------------------ ----------------- ----------------- Company revenue <$100 million $100 - $500 $.5 - $1 billion >$1 billion-------------------------- ----------------- ___million__ ------------------ -----------------

• Two goals:– Reduce unnecessary

complexity– Make information more

useful and understandable for investors

• Bob Pozen – chairman• Profession well-

represented among auditors, academics, analysts, investors & preparers

Committee on Improvements to Financial Reporting—“CIFiR”

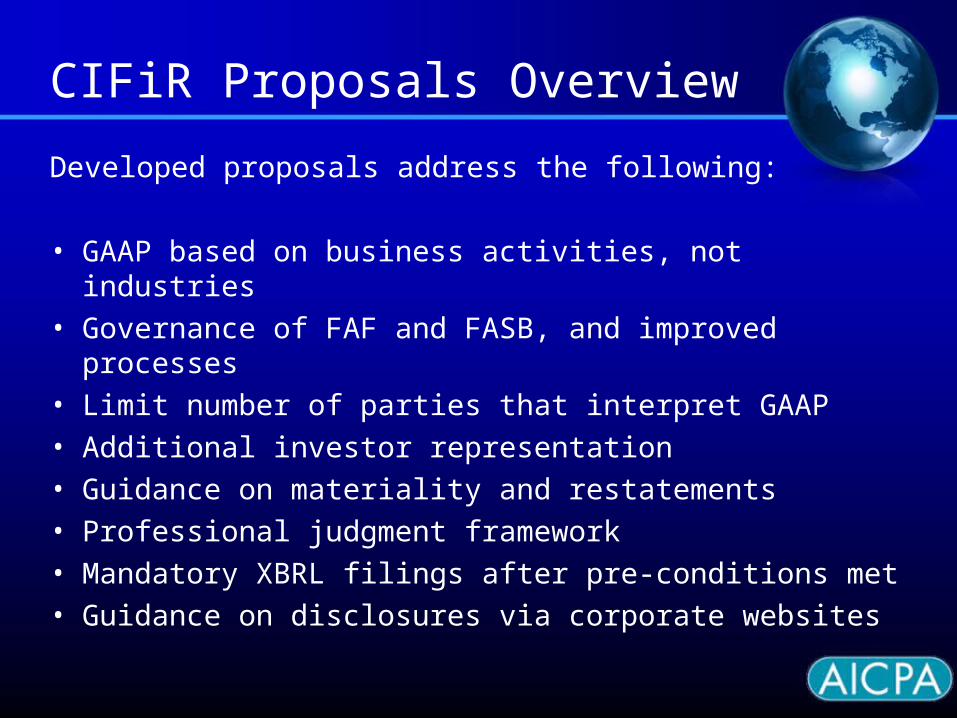

CIFiR Proposals Overview

Developed proposals address the following:

• GAAP based on business activities, not industries• Governance of FAF and FASB, and improved processes• Limit number of parties that interpret GAAP• Additional investor representation• Guidance on materiality and restatements• Professional judgment framework• Mandatory XBRL filings after pre-conditions met• Guidance on disclosures via corporate websites

Financial Reporting

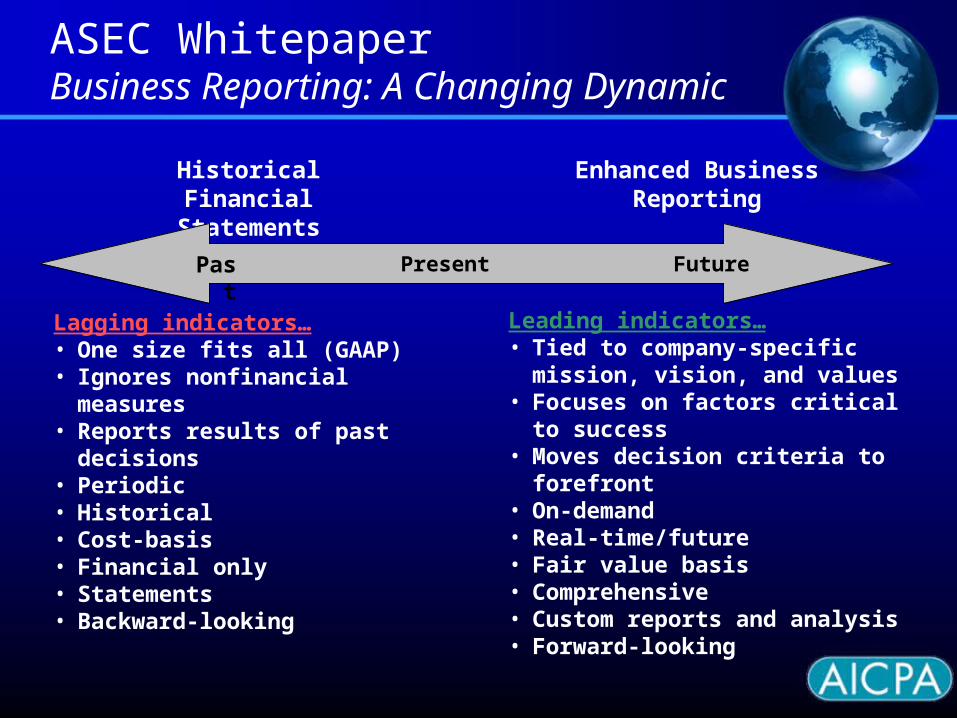

ASEC WhitepaperBusiness Reporting: A Changing Dynamic

Historical Financial Statements

Past FuturePresent

Enhanced Business Reporting

Lagging indicators…• One size fits all (GAAP)• Ignores nonfinancial measures• Reports results of past

decisions• Periodic• Historical• Cost-basis• Financial only• Statements• Backward-looking

Leading indicators…• Tied to company-specific mission,

vision, and values• Focuses on factors critical to

success• Moves decision criteria to forefront• On-demand• Real-time/future• Fair value basis• Comprehensive• Custom reports and analysis• Forward-looking

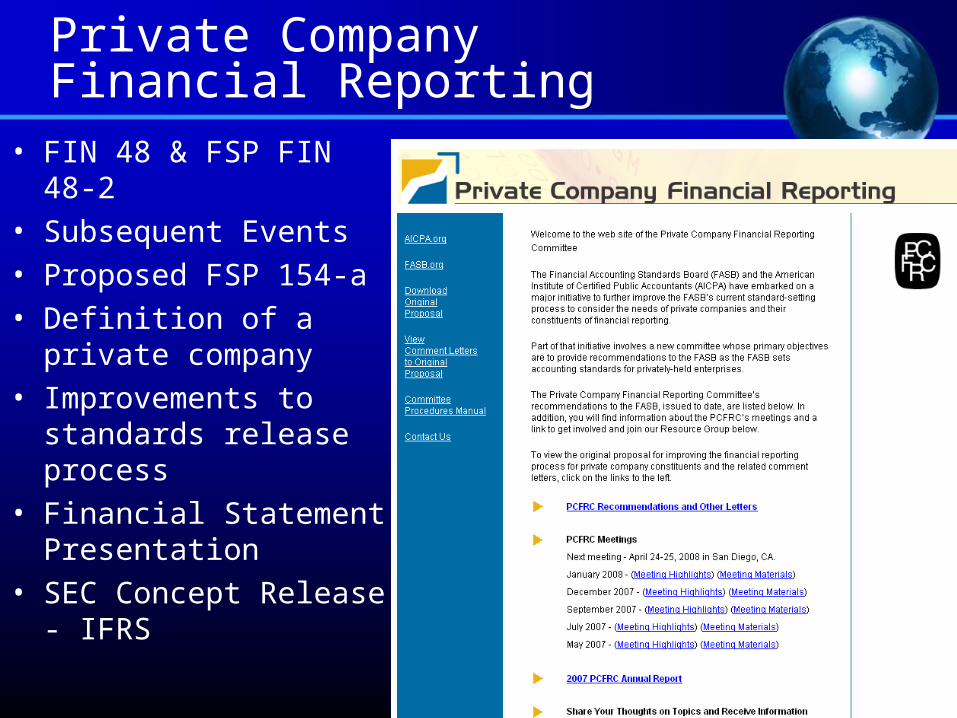

Private Company Financial Reporting

• FIN 48 & FSP FIN 48-2• Subsequent Events• Proposed FSP 154-a• Definition of a private

company• Improvements to

standards release process

• Financial Statement Presentation

• SEC Concept Release - IFRS

Existing GAAP

• PCFRC working on existing GAAP, including:– FIN 46R– FAS 123R valuation issues– Goodwill– Impairment issues

• PCFRC addressing FASB codification project.

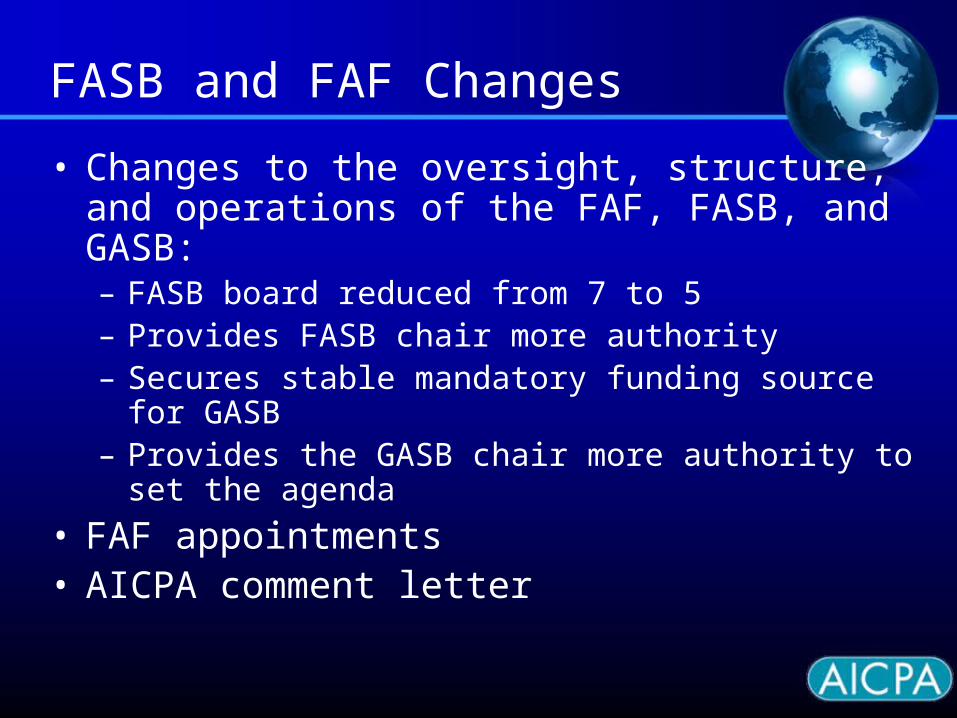

FASB and FAF Changes

• Changes to the oversight, structure, and operations of the FAF, FASB, and GASB:– FASB board reduced from 7 to 5– Provides FASB chair more authority– Secures stable mandatory funding source for GASB– Provides the GASB chair more authority to set the

agenda

• FAF appointments• AICPA comment letter

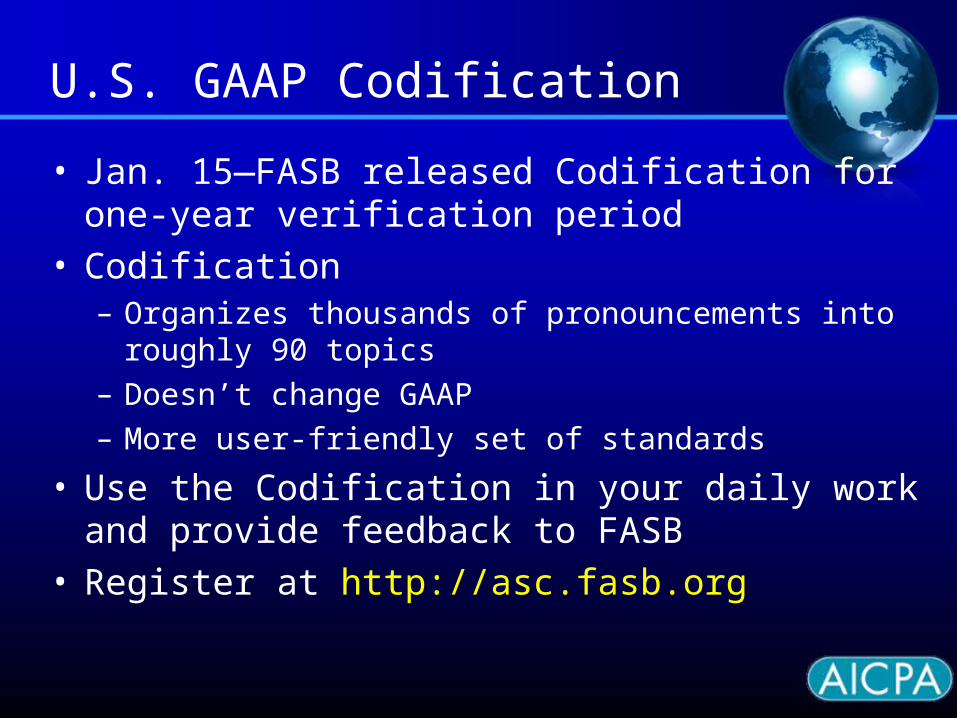

U.S. GAAP Codification

• Jan. 15—FASB released Codification for one-year verification period

• Codification – Organizes thousands of pronouncements into roughly

90 topics– Doesn’t change GAAP– More user-friendly set of standards

• Use the Codification in your daily work and provide feedback to FASB

• Register at http://asc.fasb.org

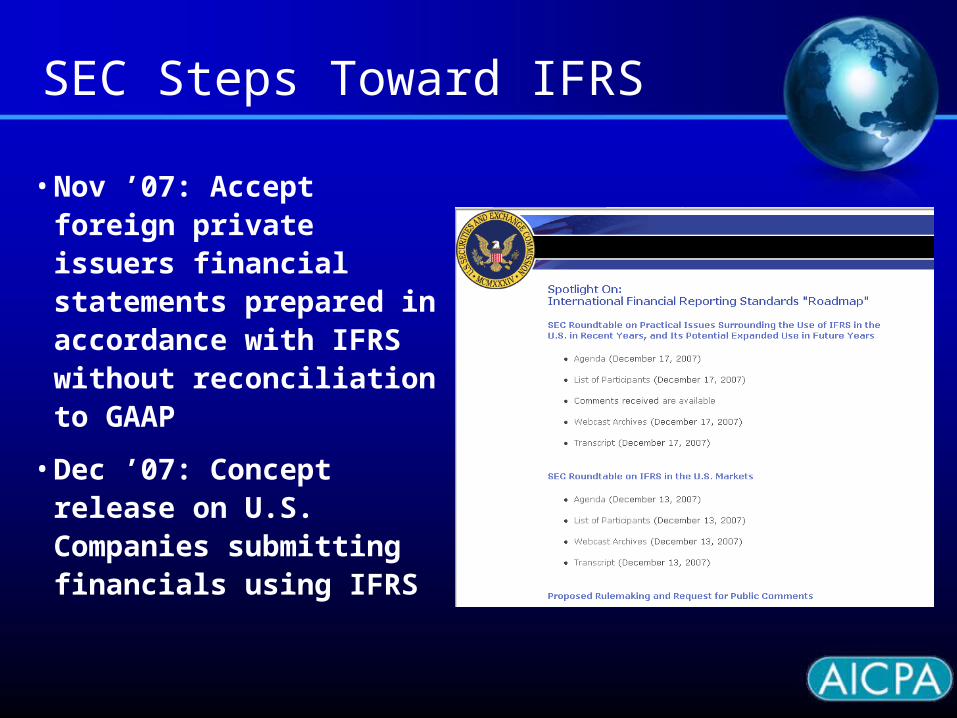

International

• Nov ’07: Accept foreign private issuers financial statements prepared in accordance with IFRS without reconciliation to GAAP

• Dec ’07: Concept release on U.S. Companies submitting financials using IFRS

SEC Steps Toward IFRS

Five Years From Now

• U.S. public companies will be following IFRS, not U.S. GAAP

• One standard setter (IASB) will promulgate IFRS• The role of FASB is uncertain

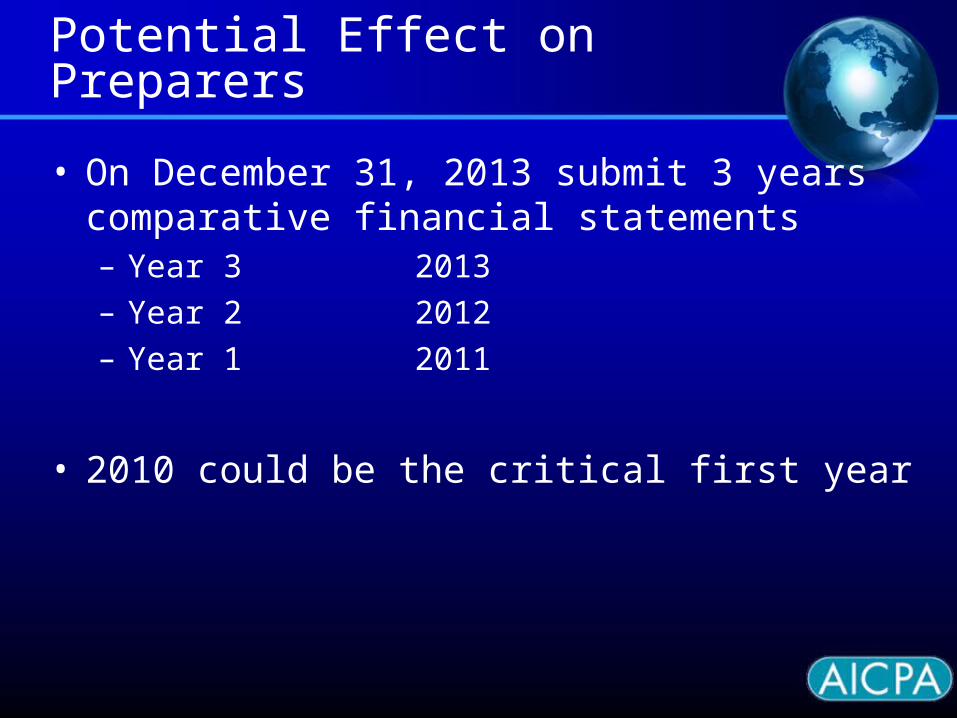

Potential Effect on Preparers

• On December 31, 2013 submit 3 years comparative financial statements– Year 3 2013– Year 2 2012– Year 1 2011

• 2010 could be the critical first year

Global Standards

• A single set of high-quality, comprehensive accounting standards involves the convergence of: – Auditing standards– Capital markets regulation– Audit oversight– Changes in the U.S. and legal environment

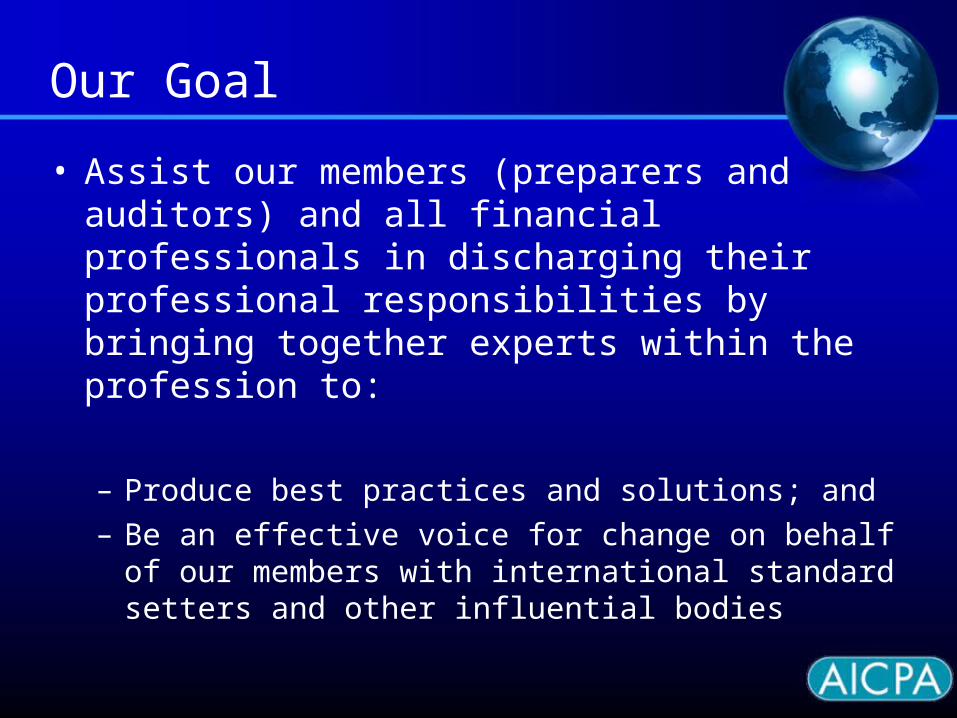

Our Goal

• Assist our members (preparers and auditors) and all financial professionals in discharging their professional responsibilities by bringing together experts within the profession to:

– Produce best practices and solutions; and– Be an effective voice for change on behalf of our

members with international standard setters and other influential bodies

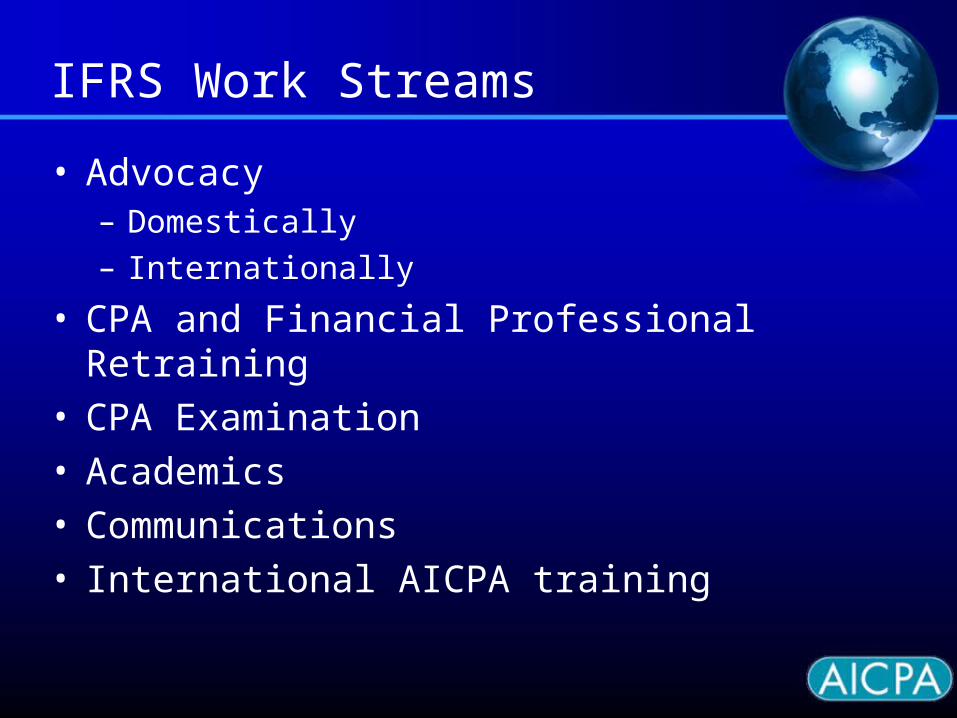

IFRS Work Streams

• Advocacy– Domestically– Internationally

• CPA and Financial Professional Retraining• CPA Examination• Academics• Communications• International AICPA training

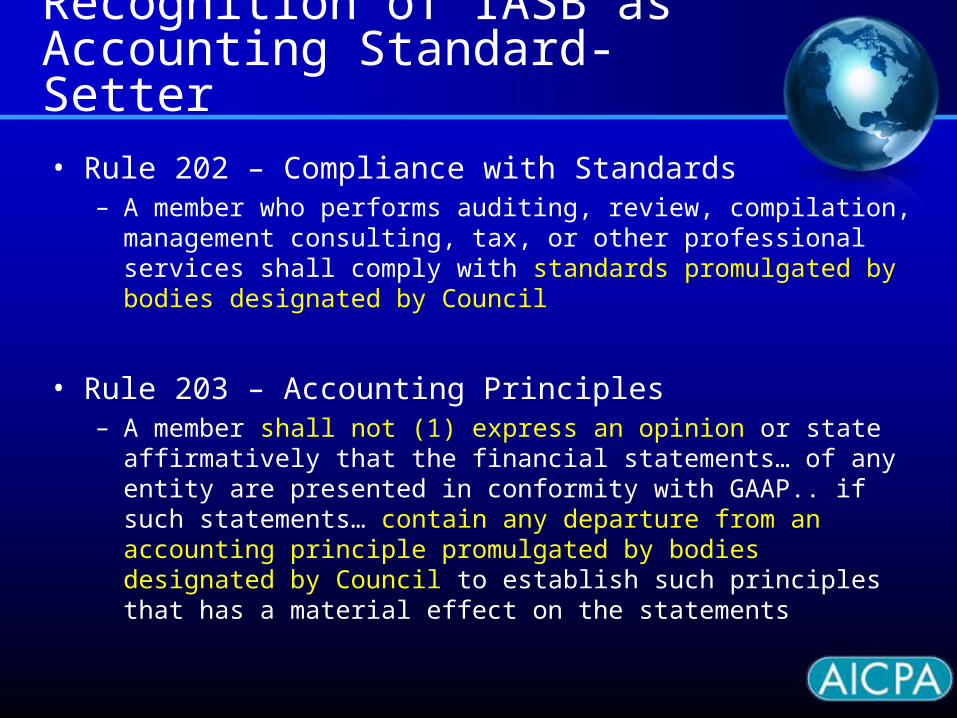

Recognition of IASB as Accounting Standard-Setter

• Rule 202 – Compliance with Standards– A member who performs auditing, review, compilation,

management consulting, tax, or other professional services shall comply with standards promulgated by bodies designated by Council

• Rule 203 – Accounting Principles– A member shall not (1) express an opinion or state affirmatively

that the financial statements… of any entity are presented in conformity with GAAP.. if such statements… contain any departure from an accounting principle promulgated by bodies designated by Council to establish such principles that has a material effect on the statements

International Offering of the Uniform CPA Examinations

Global Exam Offering

• Trends in technology and business practices• Impact of the U.S. adopting international

accounting standards• Demand for credential to differentiate oneself from

peers• Ten percent of today’s candidates are from

countries other than the U.S.– Many not seeking licensure

Current Candidate Experience

• Points of entry– Delaware– Illinois– Montana– New Hampshire– Others

• Country of Origins• Motivations-need to differentiate

– Certificate of completion– Holding Out– License to practice public accounting

AICPA’s Guiding Principles

• Recognize that we are significantly expanding international access to the CPA designation

• Protecting the public interest protects the designation

• NASBA, Prometric and the AICPA have to do this together

Benefits

• To the protection of the public– Demonstrated knowledge of professional standards– Demonstrated skills of research, analytics,

communications and other higher order skills– Lasting relationship with the U.S. accounting profession

• To the talent pipeline– Increased numbers of individuals to service business

and industry and outsourcing from the U.S.

Next Steps

• Explore offering Uniform CPA Examinationn outside of the United States– A request from NASBA’s Committee on

Internationalization of the CPA Examination– Establishment of the Joint AICPA/NASBA Committee on

International Delivery of the CPA Examination• Leslie Murphy, Former Chair of the AICPA • John Peace, Former Char of NASBA

• Complete business plan• Discuss with NASBA’s leadership

Quality

CAQ Audit Committee Survey

5% Fair

17%Good

53%Very Good

25%Excellent

• Perceptions of Audit Quality

Q9: Based on your experience as an audit committee member, how would you rate the overall quality of audits publicly traded companies being conducted today?

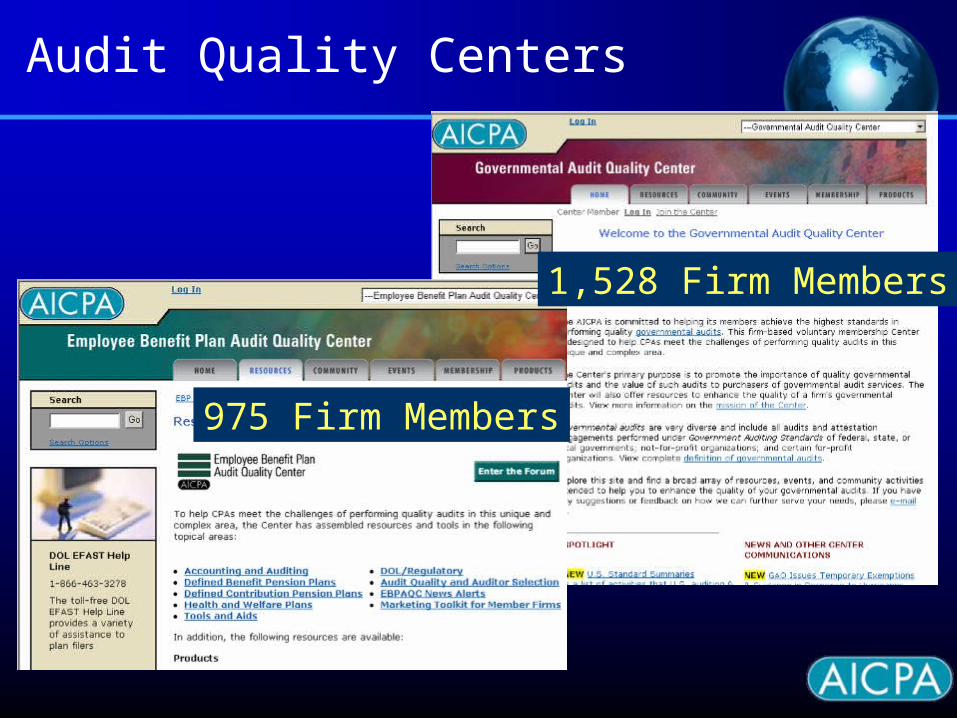

Audit Quality Centers

975 Firm Members

1,528 Firm Members

Peer Review—Facilitated State Board Access Pilot

• Ohio, Oklahoma, North Carolina, Texas, Tennessee, and South Dakota piloted the program

• Assessment of feedback is underway• Implementation will be phased in over the next 12

to 18 months

Advocacy

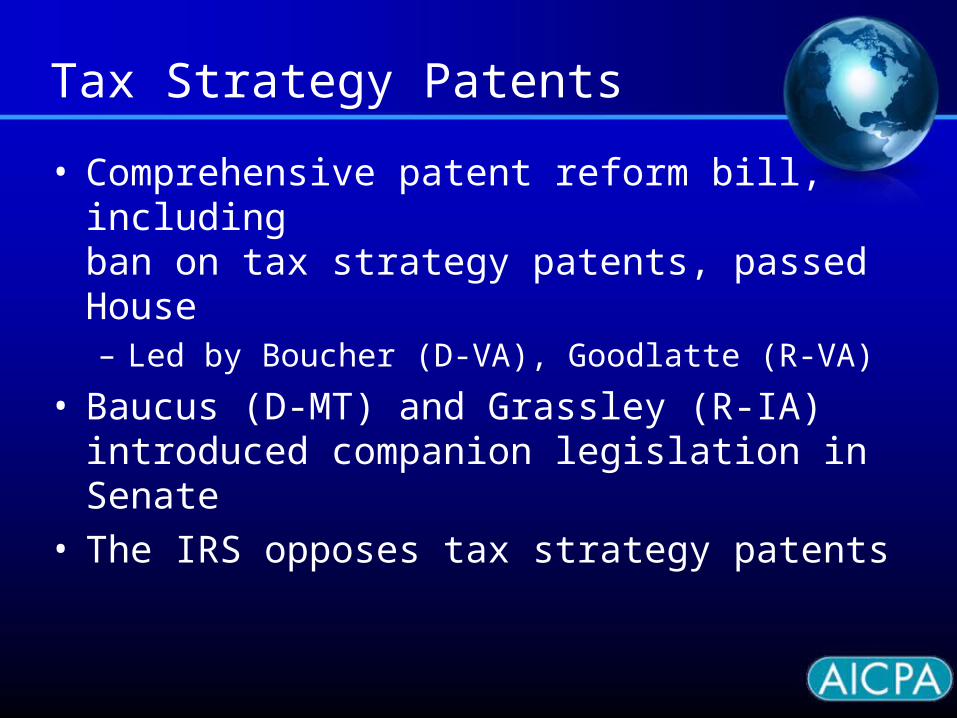

Tax Strategy Patents

• Comprehensive patent reform bill, including ban on tax strategy patents, passed House– Led by Boucher (D-VA), Goodlatte (R-VA)

• Baucus (D-MT) and Grassley (R-IA) introduced companion legislation in Senate

• The IRS opposes tax strategy patents

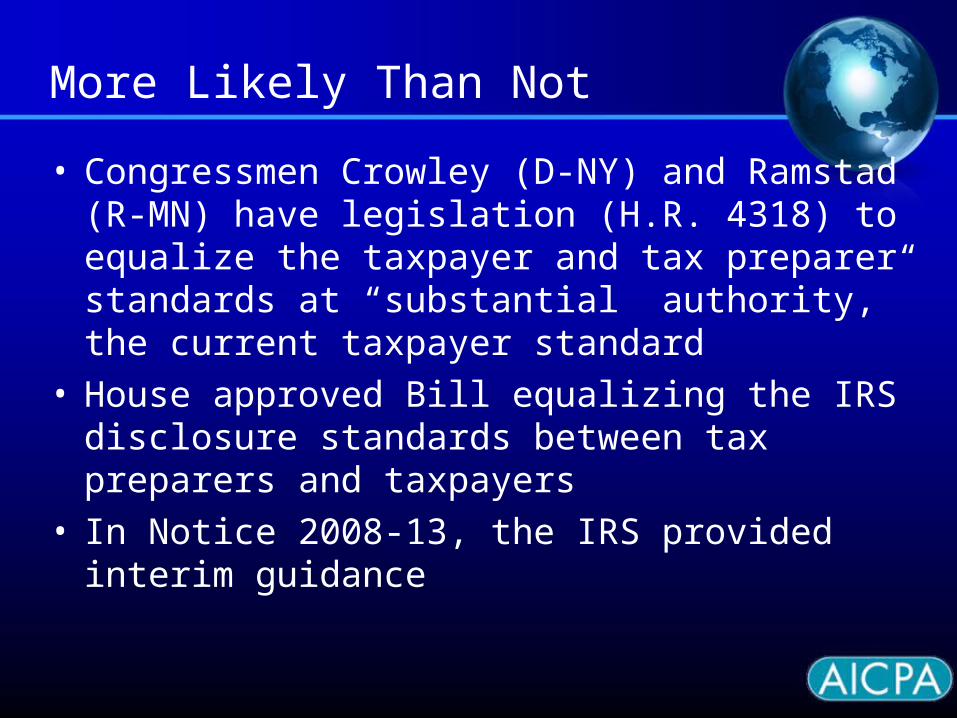

More Likely Than Not

• Congressmen Crowley (D-NY) and Ramstad (R-MN) have legislation (H.R. 4318) to equalize the taxpayer and tax preparer standards at “substantial authority,” the current taxpayer standard

• House approved Bill equalizing the IRS disclosure standards between tax preparers and taxpayers

• In Notice 2008-13, the IRS provided interim guidance

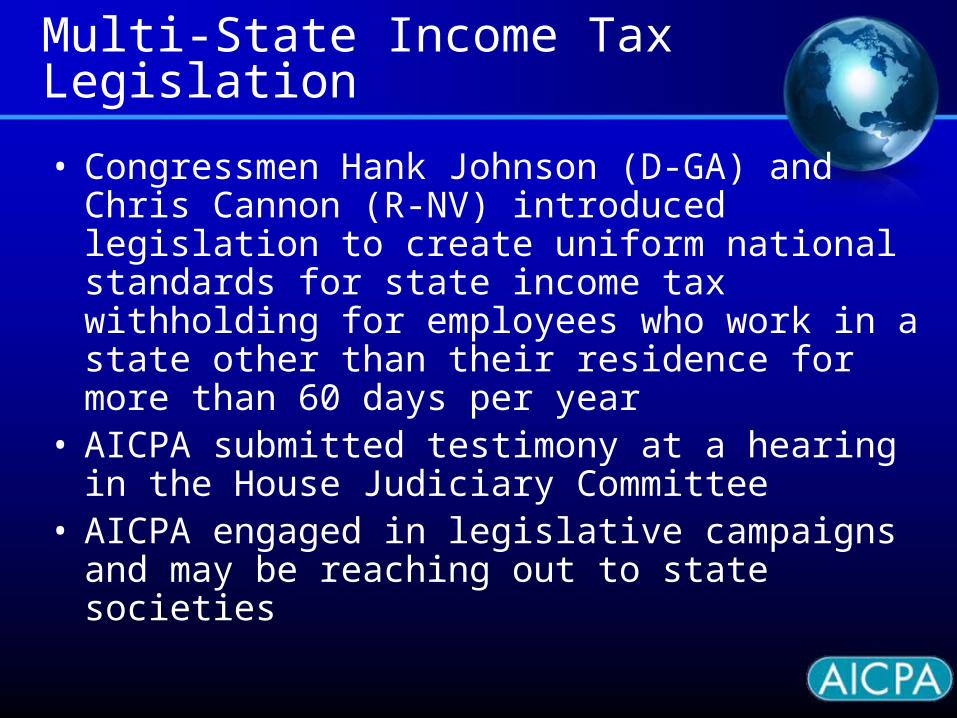

Multi-State Income Tax Legislation

• Congressmen Hank Johnson (D-GA) and Chris Cannon (R-NV) introduced legislation to create uniform national standards for state income tax withholding for employees who work in a state other than their residence for more than 60 days per year

• AICPA submitted testimony at a hearing in the House Judiciary Committee

• AICPA engaged in legislative campaigns and may be reaching out to state societies

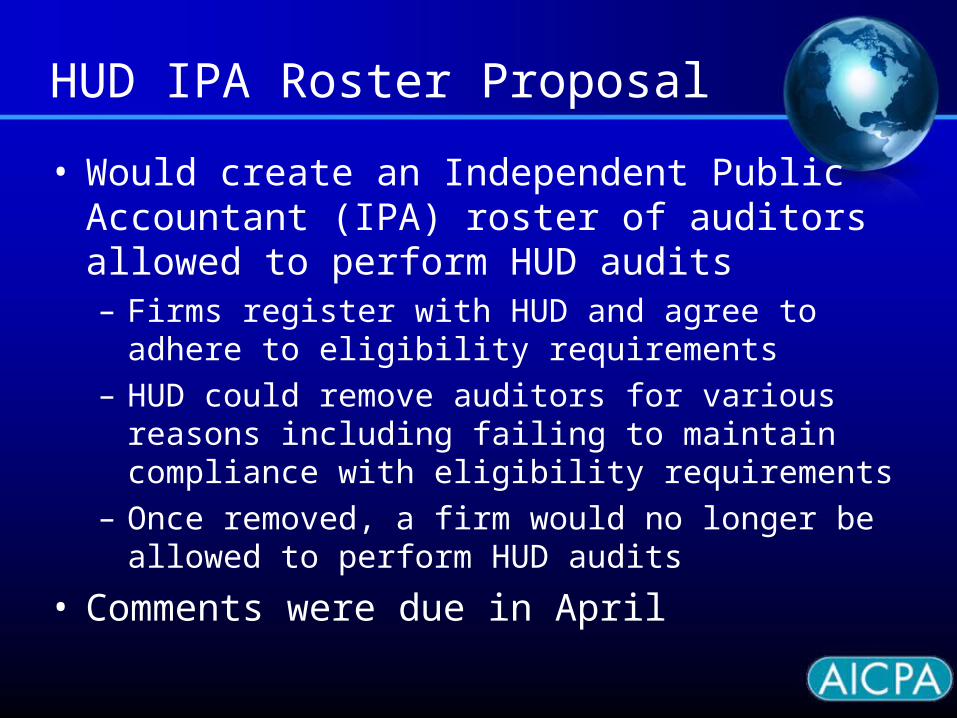

HUD IPA Roster Proposal

• Would create an Independent Public Accountant (IPA) roster of auditors allowed to perform HUD audits – Firms register with HUD and agree to adhere to

eligibility requirements– HUD could remove auditors for various reasons

including failing to maintain compliance with eligibility requirements

– Once removed, a firm would no longer be allowed to perform HUD audits

• Comments were due in April

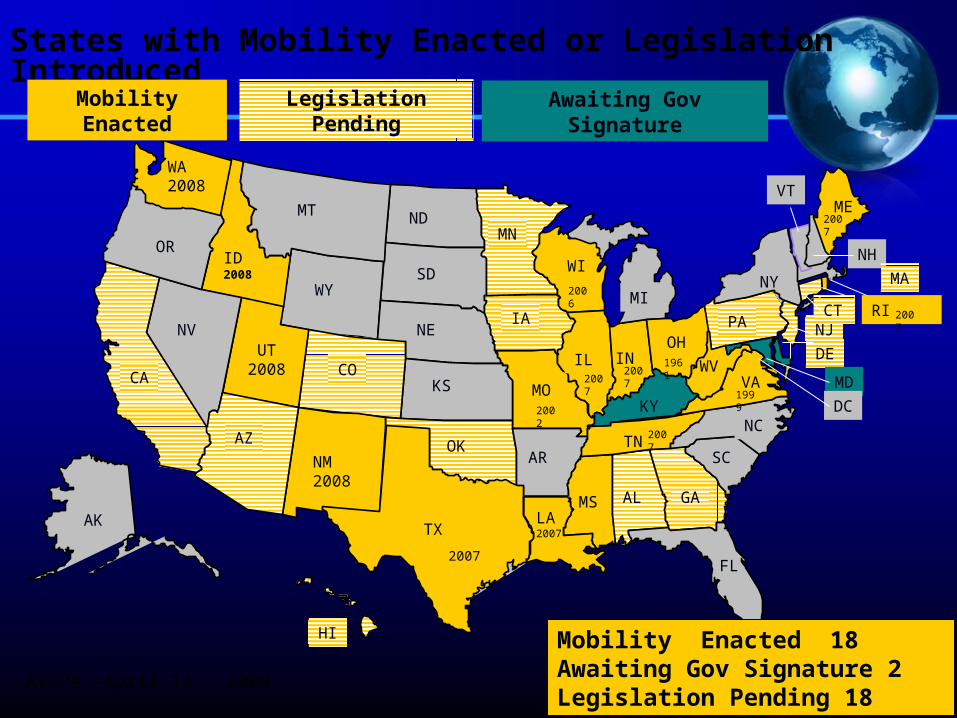

Mobility

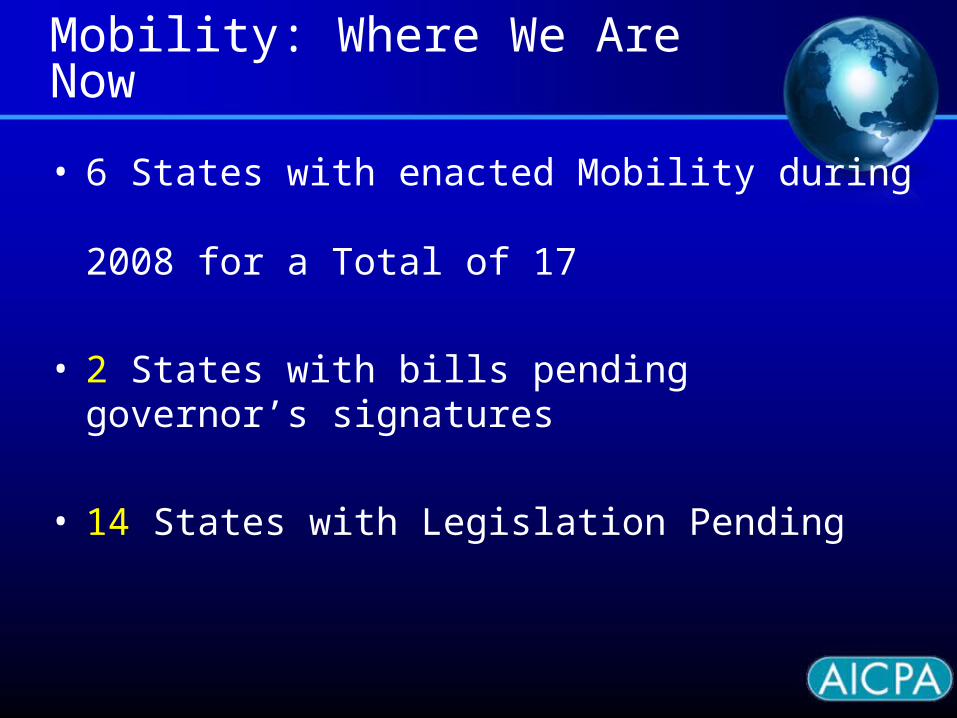

Mobility: Where We Are Now

• 6 States with enacted Mobility during 2008 for a Total of 17

• 2 States with bills pending governor’s signatures

• 14 States with Legislation Pending

WA2008

OR

CA

NV

ID2008

MT ND

SDWY

UT2008 CO

AZ

NM2008

AK

HI

TX

OK

KS

NE

MN

IA

MO

AR

LA2007

MS AL GA

FL

WI

IL

MI

IN

KY

TNSC

NC

VAWV

OHPA

NY

VTME

NH

MA

RINJ

DE

MD

CT

States with Mobility Enacted or Legislation Introduced

DC

Legislation PendingMobility Enacted

Mobility Enacted 18Awaiting Gov Signature 2Legislation Pending 18

AICPA –April 14, 2008

2007

2007

2007

2007

2007

2007

1961

2002

1999

2006

Awaiting Gov Signature

What You Can Do

• Work with your state to make sure that they are assessing how your law can be amended to align with the revised UAA provision

• Reach out to the collaborative group for assistance

• Engage neighboring states that have passed the mobility provision

• Work to avoid individual state differences to help achieve a national uniform system of mobility

Specialty Credentials

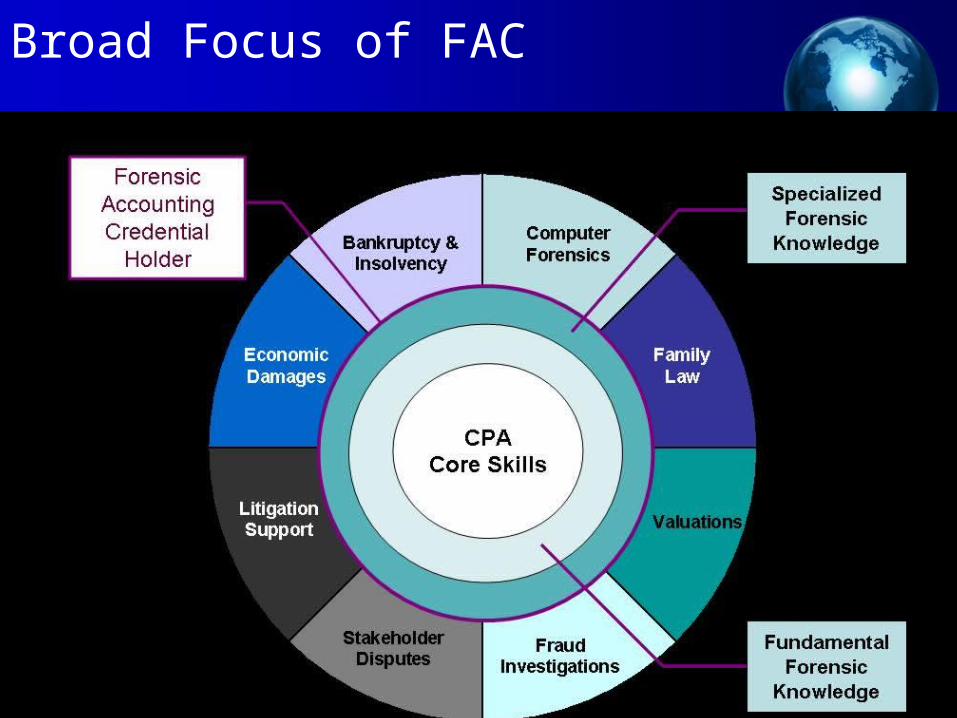

Forensic Accounting Credential-- Definition

• SAS 99 defines the auditor’s responsibilities relative to fraud

• If fraud discovered by auditor, the organization is responsible for investigation and subsequent resolution

• The FAC’s role would be to assist the organization in the investigation of, and response to, the fraud

Broad Focus of FAC

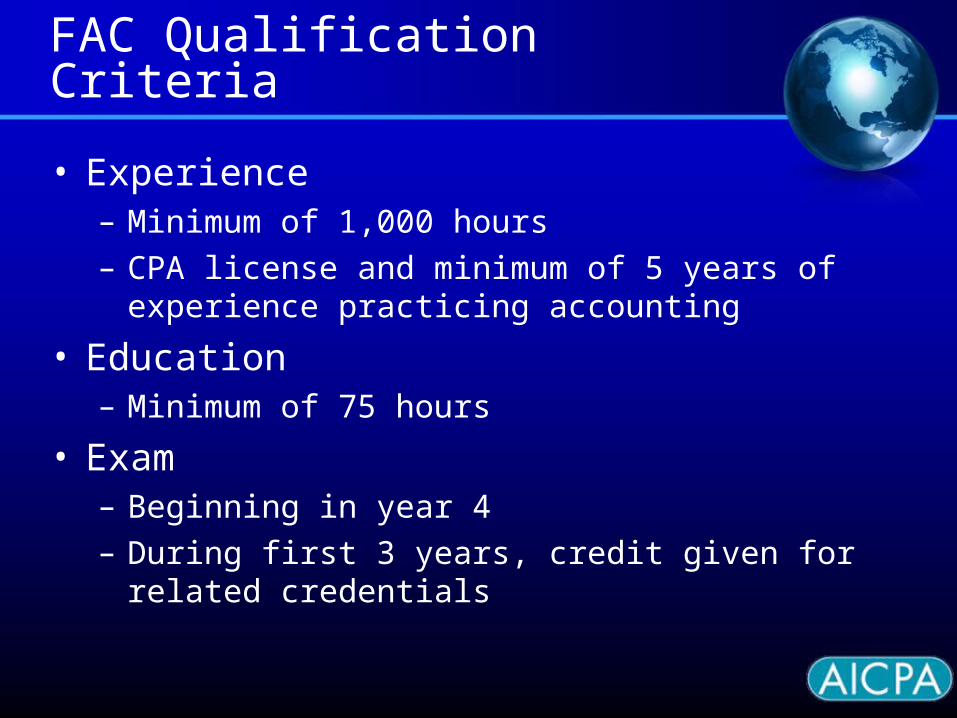

FAC Qualification Criteria

• Experience– Minimum of 1,000 hours– CPA license and minimum of 5 years of experience

practicing accounting

• Education– Minimum of 75 hours

• Exam – Beginning in year 4– During first 3 years, credit given for related credentials

Positioned for Success

• Increasing market demand for forensics• Forensic accounting top career choice for

accounting graduates• Buyers expect credential in this field• Member feedback favorable

AICPA/Moss Adams CPA Financial Planning Study

• First ever study of CPA financial planning & investment advisory practices

• 431 practices provided detailed information

• Bottom line: typical CPA financial planning practice growing faster than the broader industry and is more profitable

• www.aicpa.org/PFP

Impressive Growth Trends

• CPA financial planning & investment advisory practices have averaged high growth rates over the last two years

• Typical CPA practice dedicates 1.5 FTEs to this niche

$342,568

$462,011

$254,006

$0

$100,000

$200,000

$300,000

$400,000

$500,000

2004 2005 2006

Fiscal Year

Av

era

ge

Re

ve

nu

e

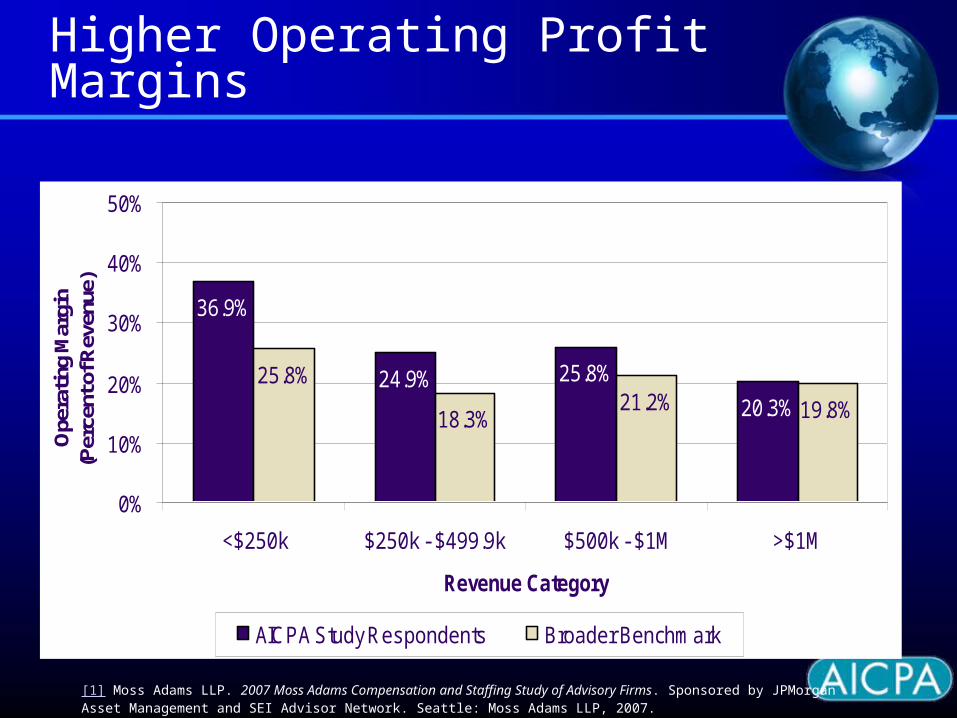

34.9%

34.9%

18.3%

25.8%24.9%

36.9%

20.3%

25.8%

19.8%21.2%

0%

10%

20%

30%

40%

50%

<$250k $250k - $499.9k $500k - $1M >$1M

Revenue Category

Ope

ratin

g M

argi

n(P

erce

nt o

f Rev

enue

)

AICPA Study Respondents Broader Benchmark

[1] Moss Adams LLP. 2007 Moss Adams Compensation and Staffing Study of Advisory Firms. Sponsored by JPMorgan Asset Management and SEI Advisor Network. Seattle: Moss Adams LLP, 2007.

Higher Operating Profit Margins

Resources for Success

PCPS Small Firm Advocacy

• Integral part of the AICPA Reliability Task Force• Integral part of the AICPA National Resource

Center Task Force• IFRS Task Force – strategic support• Various advocacy support activities in concert

with other AICPA teams and committees – Farm Credit Issue - helping rural CPA’s (with DC office)– IFAC SPIES issue - working in concert with PEEC (SPIES

would include EBP, NFP and Government entities)– Uniformity in State taxation (with DC Office)

Small Firm Advocacy

AICPA and SBA Alliance

• AICPA and the U.S. Small Business Administration signed a strategic alliance agreement giving CPAs greater access to the SBA’s programs and nationwide network.

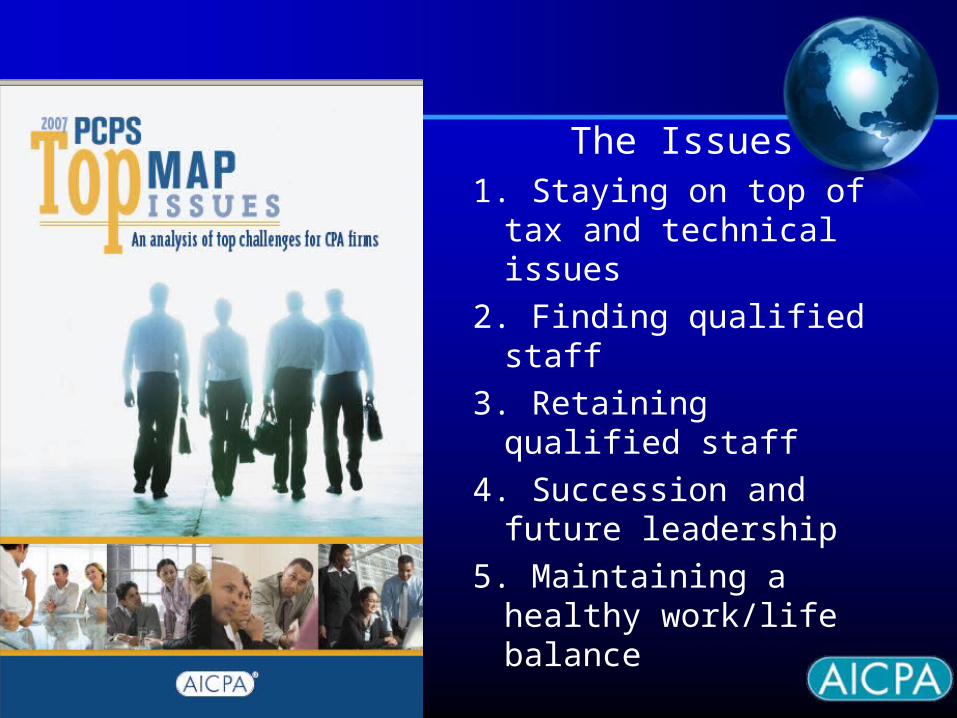

The Issues1. Staying on top of tax

and technical issues

2. Finding qualified staff

3. Retaining qualified staff

4. Succession and future leadership

5. Maintaining a healthy work/life balance

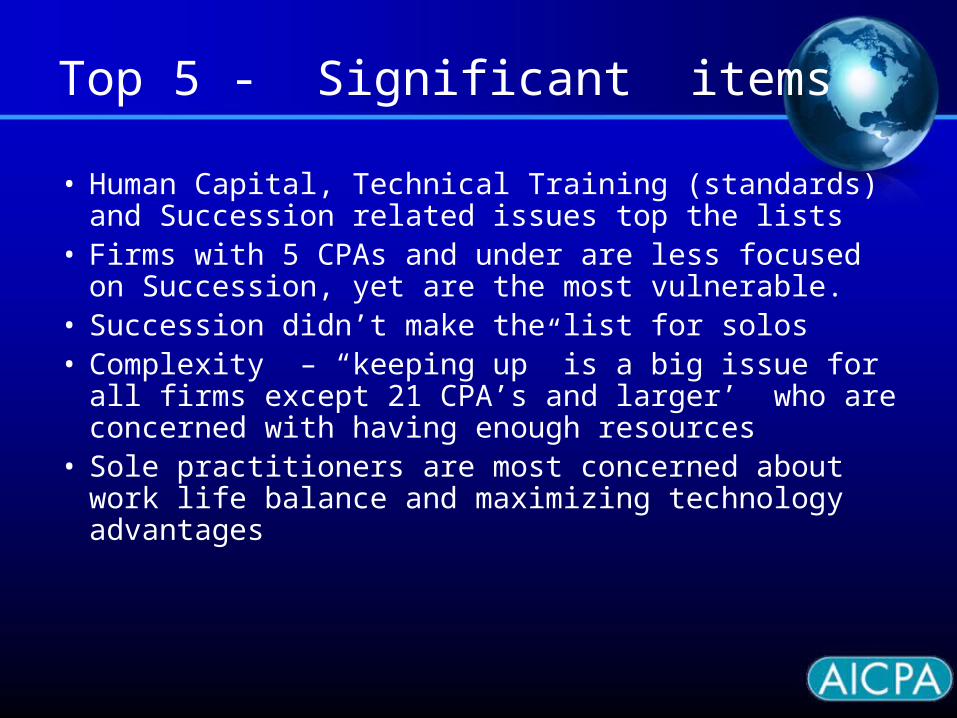

Top 5 - Significant items

• Human Capital, Technical Training (standards) and Succession related issues top the lists

• Firms with 5 CPAs and under are less focused on Succession, yet are the most vulnerable.

• Succession didn’t make the list for solos• Complexity – “keeping up” is a big issue for all

firms except 21 CPA’s and larger’ who are concerned with having enough resources

• Sole practitioners are most concerned about work life balance and maximizing technology advantages

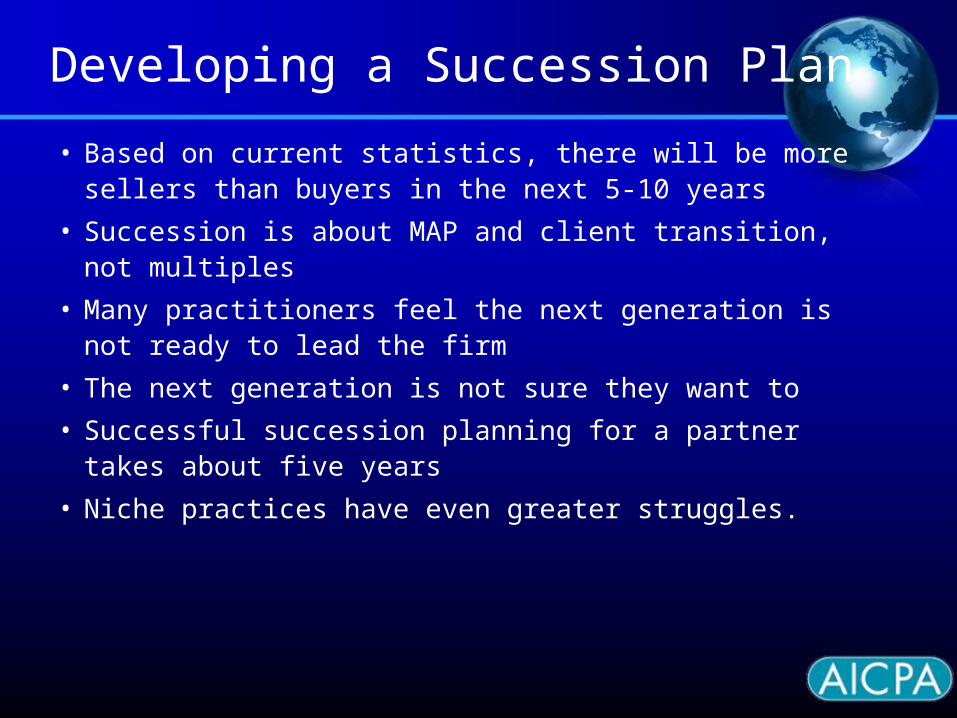

Developing a Succession Plan

• Based on current statistics, there will be more sellers than buyers in the next 5-10 years

• Succession is about MAP and client transition, not multiples

• Many practitioners feel the next generation is not ready to lead the firm

• The next generation is not sure they want to

• Successful succession planning for a partner takes about five years

• Niche practices have even greater struggles.

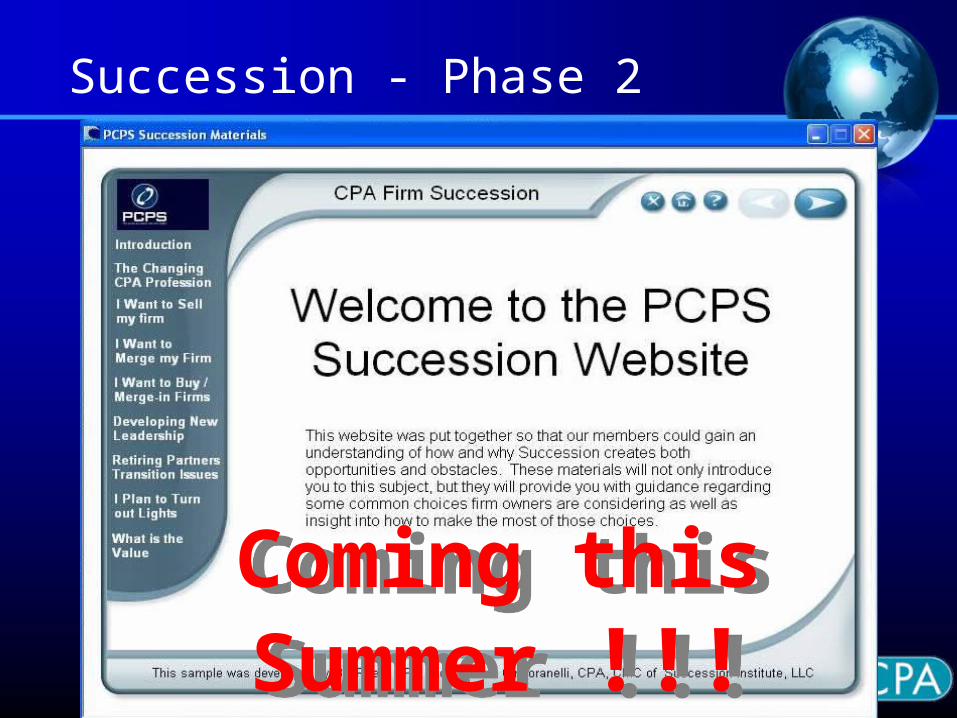

Succession - Phase 2

Coming this Summer !!!Coming this Summer !!!

Financial Literacy

The Need Is Greater Than Ever

• “The financial preparedness of our nation's youth is essential to their well-being and of vital importance to our economic future… In light of the problems that have arisen in the subprime mortgage market, we are reminded of how critically important it is for individuals to become financially literate at an early age so that they are better prepared to make decisions and navigate an increasingly complex financial marketplace.”

Ben Bernanke, Federal Reserve Chairman

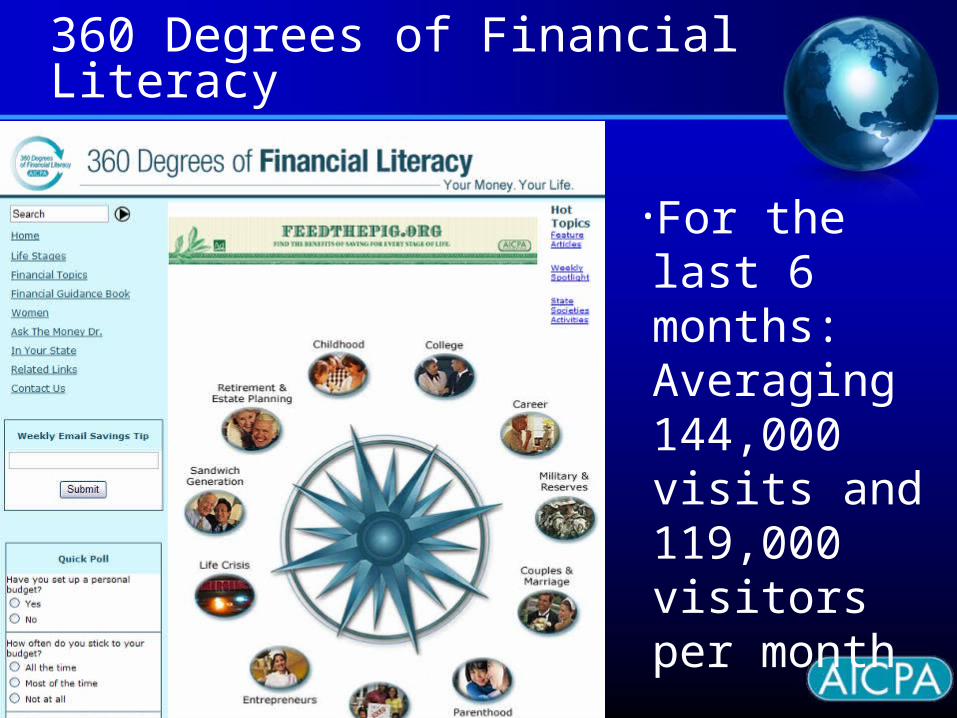

• 1.5 million visits since October ‘04 •For the last 6

months: Averaging 144,000 visits and 119,000 visitors per month

360 Degrees of Financial Literacy

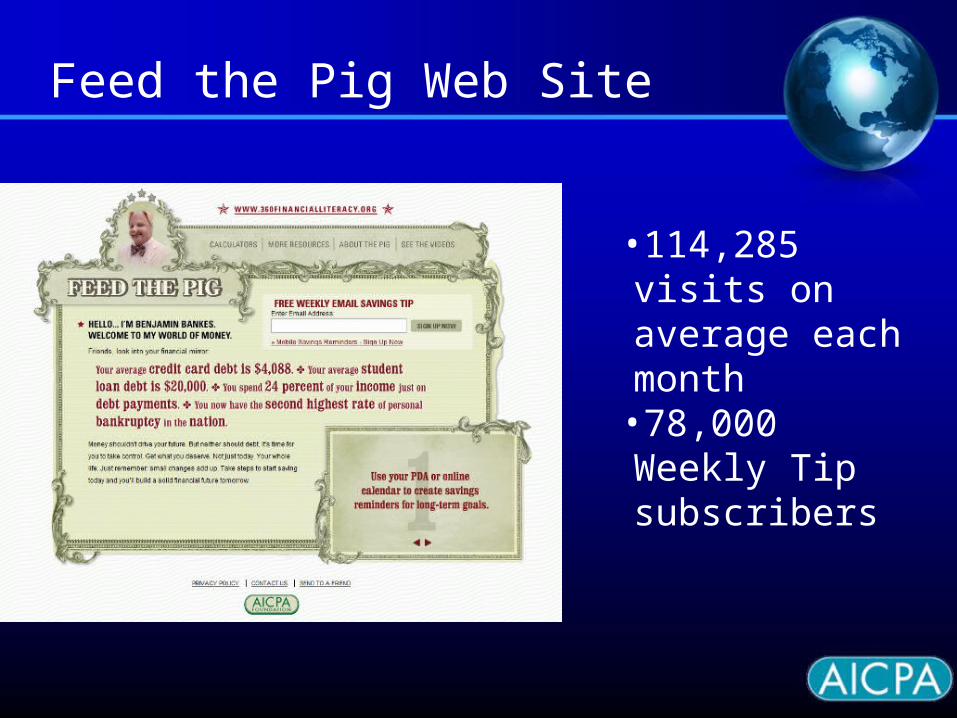

•114,285 visits on average each month

•78,000 Weekly Tip subscribers

Feed the Pig Web Site

90

Engaging Individual

Fam

iliar

Accessible

Influential

Fun

PODCASTS

TEX

T

ME

SS

AG

ES

TVR

AD

IO\/P

RIN

T/

OU

TDO

OR

INTERNET

TRA

DITIO

NA

L

ME

DIA

MY

SP

AC

E

Feed the Pig: Total DONATED media

Oct 06 – Sep 07: $46.9 Million

One of Ad Council Top 10 Campaigns

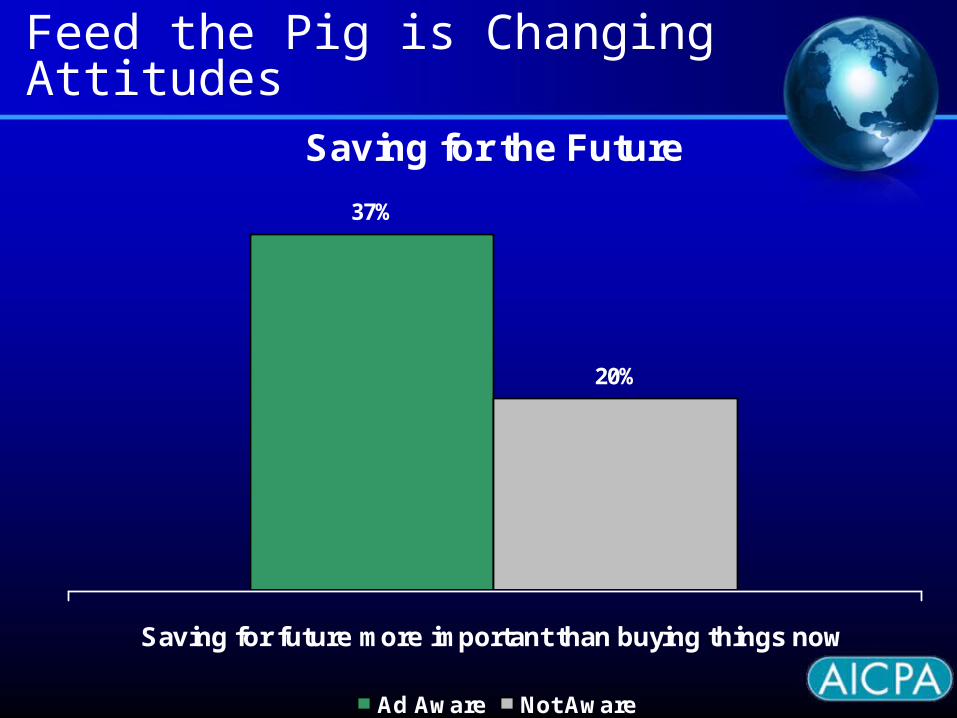

Feed the Pig is Changing AttitudesSaving for the Future

37%

20%

Saving for future more important than buying things now

Ad Aware Not Aware

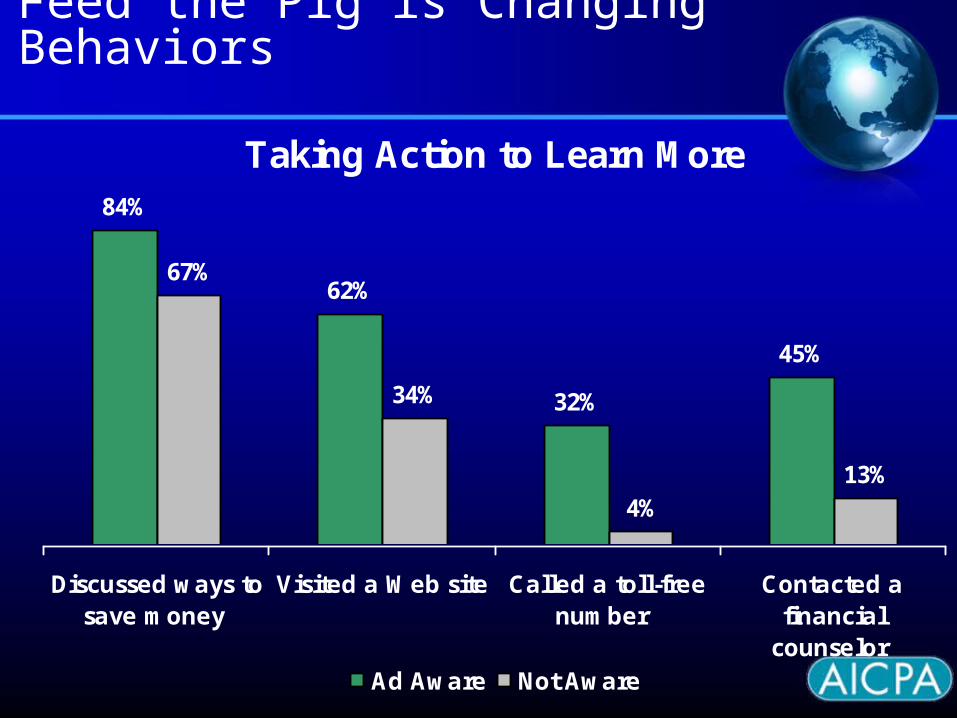

Feed the Pig is Changing Behaviors

Taking Action to Learn More84%

62%

32%

45%

67%

34%

4%13%

Discussed ways tosave money

Visited a Web site Called a toll-freenumber

Contacted afinancial

counselor Ad Aware Not Aware

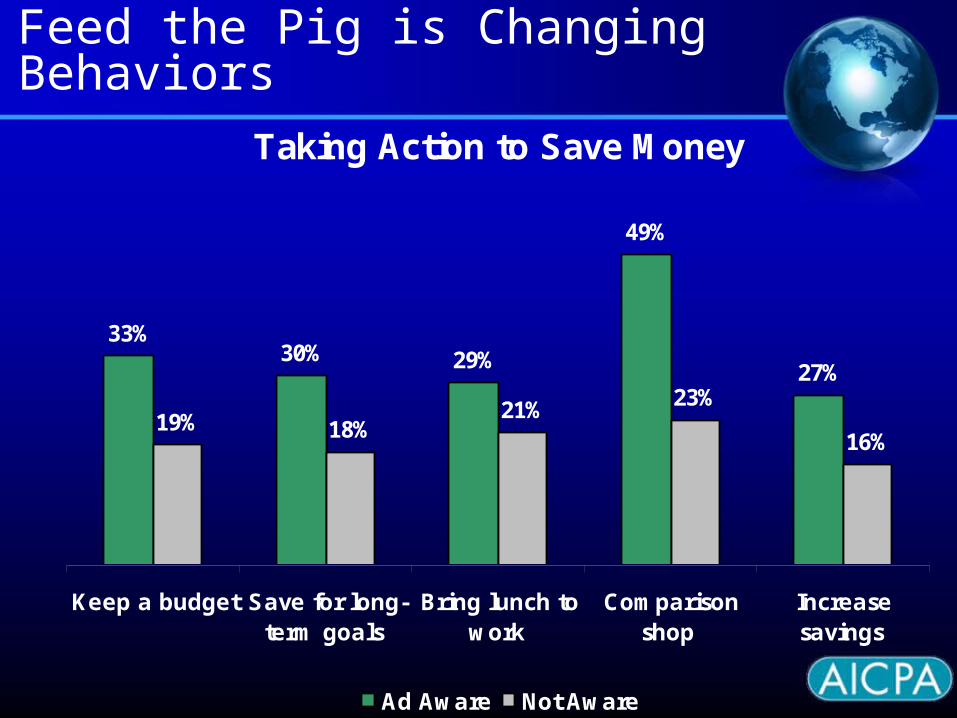

Feed the Pig is Changing BehaviorsTaking Action to Save Money

33%30% 29%

49%

27%

19% 18%21% 23%

16%

Keep a budget Save for long-term goals

Bring lunch towork

Comparisonshop

Increasesavings

Ad Aware Not Aware

Professional Issues and Initiatives• Trend Monitoring• CPA Pipeline

– The CPA Exam– Young CPAs– Student Recruitment– Minority Initiatives– PhD

• Regulatory Forces– Treasury Committee– SEC Panel– GAAP Codification– Enhanced Business Reporting– XBRL– Private Company Financial Reporting

• Quality– Audit Quality – Auditing Standards– Clarity Project– Audit Committee Effectiveness– Peer Review– Ethics

• International– International Convergence– IASB– Internationalization of Exam

• Resources for Success– PCPS – Online Member Communities– Specialty Credentials– Business, Industry & Government– Educational Resources

• Advocacy– Federal/State Legislation & Regulation– Tax– Uniformity & Mobility– Public Policy Issues

• Public Relations/Outreach• Financial Literacy• AICPA Operations

AICPA Professional Issues UpdateErnie Almonte CPA, CFERI Auditor General and AICPA Vice [email protected]