al huda presentation on micro health takaful

DESCRIPTION

TRANSCRIPT

MicroTakaful

( Islamic Micro Insurance )Presented by:

Muhammad Zubair Mughal

Regional Head

TAKAFUL PAKISTAN LIMITED

Contents

• Introduction• Microtakaful defined• Historical perspective • MicroTakaful schemes in other countries • Prospects in Pakistan• Incremental values – The Takaful advantage• Takaful Pakistan’s initiative• The way forward• Conclusion

Introduction

Micro-insurance defined:“Generally, micro-insurance is viewed just like other normal

insurance on small scale for low-income people”

MicroTakaful redefined:“A mechanism to provide Shariah-based protection to the blue collared, under-privileged individuals at an affordable cost”.

Introduction Cont’d. …• MicroTakaful can help people improve.

• Microtakaful will help them sustain their financial well being.

• Feeling of togetherness & security.

• Opens avenues for joint efforts for mutual benefits.

• Cooperative approach and outlook.

• Result oriented

• Society benefits at large.

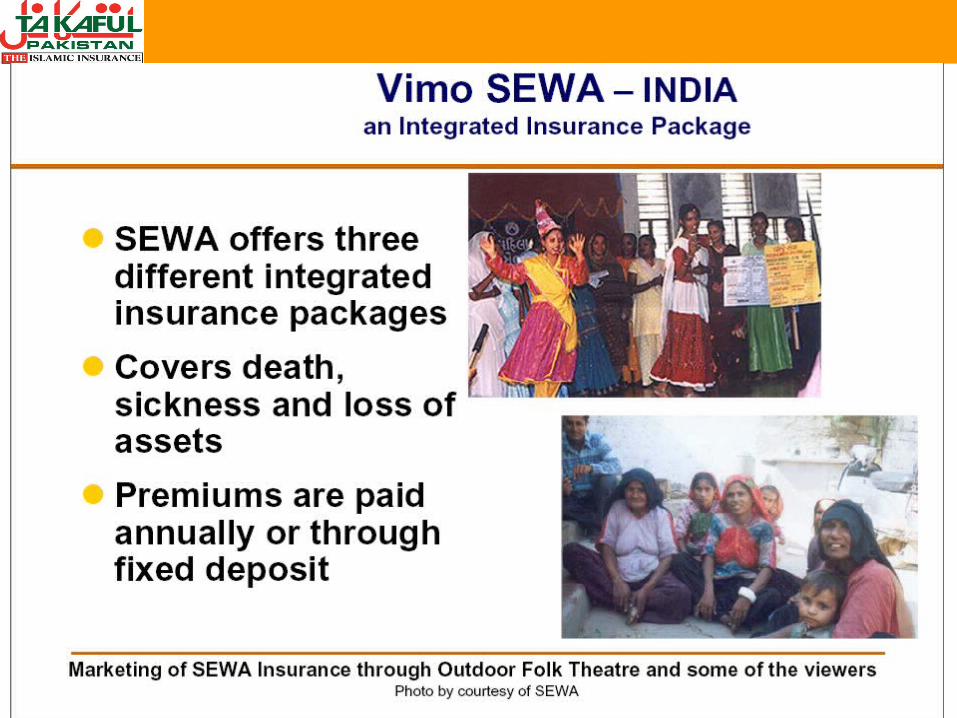

Global Landscape of Microinsurance

• Only eighty million out of the world's 2.5 billion poor are currently covered by some form of micro insurance.

• Only 3% of poor lives are insured in India and China.

• Only 0.3% of the poor are insured in Africa.

• In 23 of the poorest 100 countries in the world, there is currently no identified micro insurance activity.

Prospects in Pakistan

• Serious efforts at national level only picked up

during the last decade.

• Advent of Microfinance banks.

• Large rural/urban divide (65% : 35%)

• 40% population below poverty level.

• Scope for extensive work.

• Mushroom growth of NGOs.

Prospects in Pakistan (Cont’d. …)• Government’s initiatives – Rural support programs.

• SMEDA.

• Financial Support from ADB, WB, etc.

• State Bank’s initiative – 20% branches of commercial banks required in rural areas.

• Agriculture/Crop & Livestock Finance and Takaful.

• Benefit of economies of scale to make these viable ventures.

Fire TheftRainfall Floods

Agriculture

Property

Prices

Hospitalisation

Dental

Opt

ical

Dread Disease

Out-patient

Health

SurgicalDisability

Dismemberment

Partial

Permanent

Temporary

Total

Credit Disability

Life Insurance

Credit Life

FuneralEndowments

“Transition funds”

Pensions

Education Life

Types of MicroTakaful Products

Benefits of MicroTakaful

Health

Marriage

Death

Prolonged Illness

Education of Children

Business Failure/Loss of Job

Birth of ChildrenImp

ort

an

ce o

f R

isk/E

con

om

ic S

tress

Potential areas of action

Takaful Pakistan’s initiatives• Coverage to over 100,000 low-cost houses.

• Synergy with NGOs.

• Micro Takaful Health Products – CWCD & Sungi

• Students Healthcare/Campus care cover

• Factory workers’ & Daily wagers

• Crop Takaful

• Credit coverage for Islamic Microfinance.

• Covers tailored for SMEs financing.

• All above at ‘no profit basis’.

Takaful Pakistan’s MicroHealth Products

Center for Women Center for Women Cooperative Development. Cooperative Development.

(CWCD). (CWCD). No of Lives covered 14000 Beneficiaries ( Husband and Wife )

Benefits:Benefits:Hospitalization Rs. 35,000Daily Room Limit Rs. 500Maternity Rs. 5,000 (Sub limit)Rate per family Rs. 570

Takaful Pakistan’s MicroHealth Products

Ministry of Zakat & Ushar No of Lives covered 100,000,0 Beneficiaries (Husband, Wife and 3

Children's) Benefits:Benefits:Hospitalization Rs. 150,000Individual Limit Rs. 25,000Daily Room Limit Rs. 500Maternity Rs. 5,000 (Sub limit)Rate per family Rs. 695/-

Basic Elements of Takaful• Mutuality and cooperation. • Takaful contract pertains to Tabarru’at as against mu’awadat

in case of conventional insurance.• Payments made with the intention of Tabarru (contribution)• Eliminates the elements of Gharrar, Maisir and Riba.• Wakalah/Modarabah basis of operations.• Joint Guarantee / Indemnity amongst participants – shared

responsibility.• Constitution of separate “Participants’ Takaful Fund”.• Constitution of “Shariah Supervisory Board.” • Investments as per Shariah.

InvestmentIncome

Operational Cost of Takaful

/ ReTakaful

Claims &Reserves Surplus

(Balance)

P A R T I C I P A N T S’ T A K A F U L F U N D (P.T.F.)

Mudarib’s Share of PTF’s

Investment Income

Wakalah Fee

InvestmentIncome

Management Expense of

the Company

Profit/Loss

S H A R E H O L D E R S’ F U N D (S.H.F.)

Participant

WAQF

Takaful Operator

Share Holder

Investment by the Company

The Takaful Advantage

Comparing Takaful to Conventional InsuranceIssueIssue Conventional Conventional

InsuranceInsuranceTakafulTakaful

Organization PrincipleOrganization Principle Profit for shareholdersProfit for shareholders Mutual for participantsMutual for participants

BasisBasis Risk TransferRisk Transfer Co-operative risk sharingCo-operative risk sharing

Value PropositionValue Proposition Profits maximizationProfits maximization Affordability and spiritualAffordability and spiritual

satisfactionsatisfaction

LawsLaws Secular/RegulationsSecular/Regulations Sharia plus regulationsSharia plus regulations

OwnershipOwnership ShareholdersShareholders ParticipantsParticipants

Management statusManagement status Company ManagementCompany Management OperatorOperator

Form of ContractForm of Contract Contract of Sale Contract of Sale Cooperative,Cooperative,

Islamic contracts of Wakala orIslamic contracts of Wakala or

Mudarbah with Tabar’ruMudarbah with Tabar’ru

(contributions)(contributions)

InvestmentsInvestments Interest basedInterest based Sharia compliant, Riba-freeSharia compliant, Riba-free

SurplusSurplus Shareholders’ accountShareholders’ account Participants’ accountParticipants’ account

Takaful through Time• Origins in the First Constitution of Madina.

• The first Takaful company was set up in Sudan in 1979, almost simultaneously followed by another one set up in Bahrain.

• There are now around 179 Takaful companies in over 40 countries.

• Poor Insurance rate in the Muslim countries (<1% of GDP).

• Average growth rate higher than conventional insurance companies (around 25%).

• Non–Muslims increasingly opting for Takaful products for commercial benefits.

About Takaful Pakitan Limited Takaful Pakistan is a joint venture of prestigious local & foreign institutions, including:

•Emirates Investment Group (Sharjah).

•Al-Buhaira National Insurance Co. (U.A.E.)

•Al-Rajhi Banking Group – Saudia Arbia

•House Building Finance Corporation.

•Emirates Global Islamic Bank.

•Arif Habib Securities.

•Sitara Chemicals.

Large initial paid-up Capital.

What is required?

When there is a will, there is way!