alabama's opportunities and challenges

TRANSCRIPT

Alabama’s Opportuni1es & Challenges Observa1ons From a Site Selector

EDAA Winter Conference Feb. 3, 2014 Dennis Cuneo Fisher & Phillips LLP

Experience

• Former SVP Toyota

• Projects > $12 billion/ 20,000 jobs – Auto….heavy industry….R&D…high tech

• Board of Directors: 3 companies

• Site Selec1on: – Insider… Investor….Consultant….Board Member

Toyota Huntsville Plant

• Expanded 4 1mes since start-‐up • $850,000,000 investment….1200 jobs • Only Toyota plant building 4, 6 & 8 cylinder engines

Established 2001

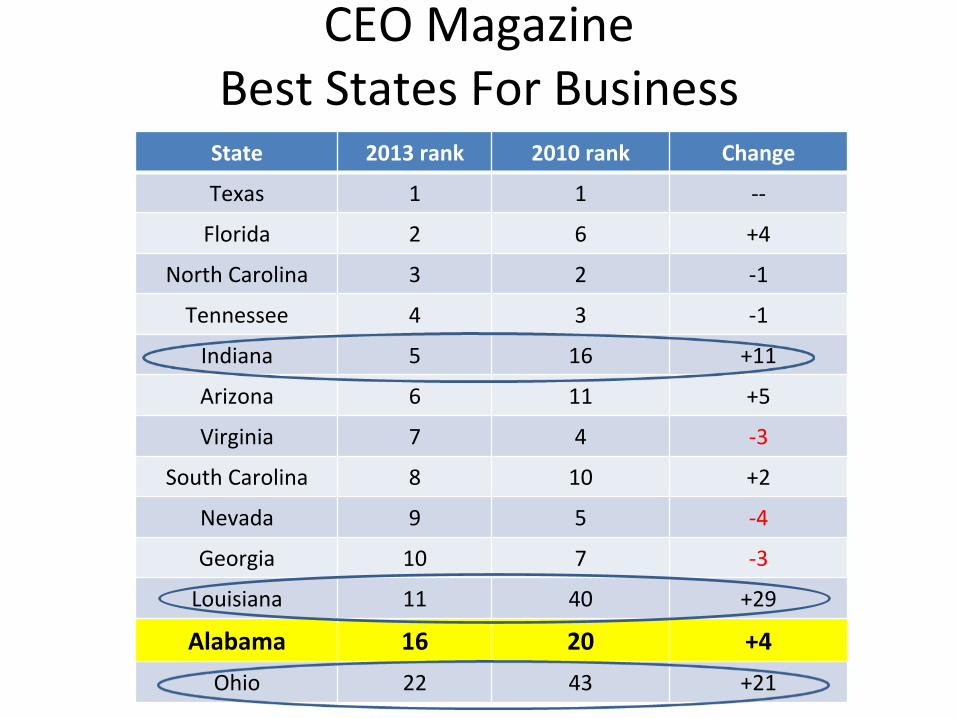

CEO Magazine Best States For Business State 2013 rank 2010 rank Change

Texas 1 1 -‐-‐

Florida 2 6 +4

North Carolina 3 2 -‐1

Tennessee 4 3 -‐1

Indiana 5 16 +11

Arizona 6 11 +5

Virginia 7 4 -‐3

South Carolina 8 10 +2

Nevada 9 5 -‐4

Georgia 10 7 -‐3

Louisiana 11 40 +29

Alabama 16 20 +4 Ohio 22 43 +21

CEO Rankings Workforce Quality

TX

FL

NC

TN

IN

AR

VA

SC

GA

LA

AL

Workforce Quality

8.1 6.9 7.7 7.4 7.7 7.1 7.7 7.0 7.2 5.9 5.8

CEO Magazine: Best & Worst States for Business 2013

Percep1ons Oden Lag Reality

Paul Krugman, New York Times, July 25, 2005 “….Japanese auto companies opening plants in the Southern U.S. have been unfavorably surprised by the work force's poor level of training.”

Response LeMer from Toyota:

"The Huntsville work force has been highly mo1vated, well trained and produc1ve. Almost 30 percent of our hourly team members are college graduates, and 97 percent are high school graduates.”

Do Incen1ves Maler

“States are more aggressive in compe1ng with one another” CEO Magazine: Best & Worst States for Business 2013

Do Incen1ves Maler?

2 Cases Studies – R&D Project – Auto Parts Project

R&D Project

• 200 jobs @ $110,000 per job ($145,000 w benefits) – 60% engineers

• Ini1al RFP sent to 12 States

• AL didn’t make final cut – Incen1ves not compe11ve

IBM Baton Rouge

• 800 sodware jobs • Incen1ves

– $30.5 million building – $29.5 million in grants – $14 million for college programs to increase computer science graduates

Source: New Orleans Times Picayune 3.17.13

Auto Parts Project

• Ini1ally 36 jobs @ $54,000 per job

– Expansion possible

• AL loca1on selected near OEM

• AL incen1ves lower than compe1ng state – Project divided with plant in compe1ng state

Opportuni1es for Alabama

• Chemical • Aerospace • Re-‐shoring • Automo1ve

– Supply Base/ R&D

Alabama Chemical Corridor

Source: Alabama Power

“…most promising development in the American economy…. discovery of oceans of natural gas in North America….” Forbes 8.21.2012

Aerospace

Airbus builds on State’s robust aerospace sector.

Re-‐shoring

-‐ Wages on the rise in China & developing countries -‐ Lower energy costs in U.S. -‐ Advanced manufacturing techniques McKinsey: 2/3 of manufacturing occurs close to demand

But There Are New Challenges As Well As New Opportuni1es

For the Southern States

Auto Industry Strong hub of Auto Produc1on in the South

2 decades of Investment by Foreign Automakers

Source: Thomas Klier, Federal Reserve Bank of Chicago

Past 20 years Alabama has become

Automo1ve Powerhouse

4th in U.S. vehicle produc1on 4th in vehicle exports: $6.6 billion in 2012 1/4 of all passenger vehicles built in the South made in Alabama. Source: amazing alabama.com

But the South & Alabama face new challenges & new opportuni1es

as Auto Industry restructures

Canada $3.2 billion

Total $51.7 billion

U.S. Great Lakes

$23.9 billion United States

$35.8 billion

Mexico $12.7 billion

South $8.2 billion

U.S. Great Lakes includes: IL, IN, KY, MI, MO, and OH South includes: AL, FL, GA, MS, SC, TN, and TX

North American Automaker Investments 2010-‐2013 Source: CAR Research, Book of Deals

Since the Great Recession Mexico Has Outpaced U.S. Southern Region

24 month comparisons Oct 2010 – Sept 2012 * States include TN, MS, AL, GA, NC, SC, FL & TX

Mexico • More trade agreements • Cheaper labor • Growing Parts Infrastructure

Automaker investments in

Mexico 2010 – 2013 $12.7 billion

Automaker Investments in Southern States 2010 – 2013 $8.2 billion

What does the future hold?

New Assembly in Mexico

• Nissan, Honda, Audi, Mazda, (w Toyota produc1on) building new plants.

• Chrysler, Ford, GM adding capacity at exis1ng plants.

• BMW & Hyundai reportedly in talks with Mexican government.

• Volkswagen: majority of $7B NA investment in Mexico.

Another Challenge for the South

UAW currently targe1ng: – Volkswagen Chalanooga – Nissan Canton – Mercedes Tuscaloosa

UAW Campaign At Nissan

UAW Campaign at Mercedes

State. Sen. Bobby Singleton at news conference about UAW campaign at the automaker's Tuscaloosa County plant.

Source: AL.com

Center for Automo1ve Research Southern Automo_ve Research Alliance

Iden1fying & Exploi1ng Opportuni1es Southern Automo1ve Industry

1. Alabama 2. Kentucky 3. Louisiana 4. Mississippi 5. South Carolina 6. Tennessee -‐ -‐ -‐ -‐ -‐ -‐ -‐ -‐ -‐ -‐ -‐ -‐ -‐ -‐ -‐ -‐ -‐ -‐ -‐ -‐ -‐ -‐ -‐ • Duke Energy • CU-‐ICAR • University of Alabama • AAMA • MAMA • SCMA • TAMA • GAMA

-‐

Par$cipa$on by six states

Suppor$ng contribu$ons and in-‐kind par$cipa$on by Duke Energy and various Universi$es & AMA’s

Southern Automo_ve Research Alliance (SARA)

Southern Automo_ve Research Alliance (SARA)

Opportuni1es to Grow Southern Auto Industry • Expand Supply Base • Enhance Automo1ve R&D in the Region

Auto Parts Suppliers S_ll Concentrated In Upper Midwest

Thomas Klier, Federal Reserve Bank of Chicago

Assembly

Tier 1

Tier 2

Tier 3

Includes Alabama, Georgia, Mississippi, North Carolina, South Carolina, and Tennessee.

Source: CAR 2010

Includes: Illinois, Indiana, Michigan, Ohio, Pennsylvania, and Wisconsin

Opportunity

Less Lower Tier Supplier Jobs in the South

Jobs US Region Outside Region

Direct 2000 2000 -‐-‐

0

Supplier 5133 2603 2530

Spin-‐off 8680 4630 4809

Totals 15,813 8474 7339

Opportunity High % out-‐of-‐region jobs

Es_mated Job Impact Southern Auto Assembly Plant

Source: Center for Automo1ve Research

Fuel Economy

Source: CAR 2013

Connec_vity/Automa_on Electronics Safety

Bio-‐Based Materials/ Fuels

Lightweigh_ng

New Automo1ve Technology Brings New Opportuni1es

Porsche

High-‐Tech Automo1ve Systems

Next genera1on high strength steels Foamed metals

Aluminum and magnesium alloys Corrosion protec1on

Bio-‐based materials Advanced plas1cs and composites Mold in color/Films/Other for plas1cs Alterna1ve automo1ve trim cover insert and/or bolster fabrics

Recycled low cost filler materials Coa1ng technology

Non-‐destruc1ve tes1ng methods Robo1cs simula1on sodware Forming high strength steels

New laser technology for trimming, piercing and cuvng

New joining technologies Tool rapid hea1ng and cooling Mul1-‐material joining technologies Low cost fine blanking alterna1ves

Materials and Processes Powertrain and Fuels Connected Vehicles Gasoline direct injec1on Turbochargers and superchargers Dual-‐clutch transmissions

Higher-‐speed automa1c transmissions (8-‐ or 9-‐speed) Con1nuously variable transmissions

Vehicle electrifica1on: motor assist, hybrid electric vehicles, plug in hybrid electric vehicles, extended range electric vehicles, or balery electric vehicles

Alterna1ve fuels: natural gas, biofuels (E85 and B20), and hydrogen

Dedicated Short Range Communica1ons (DSRC); 3G, 4G, LTE Cellular; Wi-‐Fi; Bluetooth; and Global Posi1oning System Infotainment (e.g. Sync, Uconnect, and Cue) Human machine interface Collision warning and avoidance

Lane departure warning Blind spot and pedestrian detec1on Road condi1on and event no1fica1on

Adap1ve route guidance with real-‐1me traffic informa1on Signal phase and 1ming

Tolling and E-‐payment Loca1on-‐based services

Efficiency monitoring and carbon footprint accoun1ng Infrastructure investment planning and condi1on monitoring Fleet management

Prognos1cs and diagnos1cs

Advanced Driver Assistance Radar, light detec1on and ranging (LiDAR), and cameras Forward collision warning systems

Automa1c emergency braking and steering Back-‐up and rear-‐view assistance systems

Lane departure and lane-‐keeping assistance systems Adap1ve cruise control and adap1ve cruise control with lane-‐keeping

Blind spot and pedestrian detec1on systems Parking assistance and automated parking systems Adap1ve headlights and adap1ve high beams

Source: CAR 2013

Loca1on of Automaker & Supplier R&D…Design…Engineering

Nissan HQ

Other opportuni_es???

Ques1ons Comments