tesmecinvestor.tesmec.com/_docs/ir_analysis/2017.08.08-mediobanca-tortora.pdf · alessandro tortora...

TRANSCRIPT

IMPORTANT DISCLOSURE FOR U.S. INVESTORS: This document is prepared by Mediobanca Securities, the equity research department of Mediobanca S.p.A. (parent company of Mediobanca Securities USA LLC (“MBUSA”)) and it is distributed in the United States by MBUSA which accepts responsibility for its content. The research analyst(s) named on this report are not registered / qualified as research analysts with Finra. Any US person receiving this document and wishing to effect transactions in any securities discussed herein should do so with MBUSA, not Mediobanca S.p.A.. Please refer to the last pages of this document for important disclaimers.

Tesmec

08 August 2017 Diversified Industrials Change in Estimates

First signals of cash conversion Alessandro Tortora

Equity Analyst

Results in line. Full year guidance fine tuned

Tesmec reported 1H17 results in line with our estimates. The group matched its

target in terms of sales and recurring EBITDA was in line with our estimate. In

the first half, stringing equipment (+44% yoy) and railway (c.3x) reported a

positive set of numbers, while the €2m contribution at EBITDA level of Marais

and the trenching business was modest. At bottom line level, the €3.1m FX

headwind, mainly due to the USD depreciation, materially affected the result in

the first half of the year. 1H17 net debt was the positive news, dropping to

€91.5m (from €97m in 1Q17), better than our estimate of €93m, due to a more

efficient WC management that included significant destocking. Following the

results, the company fine-tuned its FY guidance and is now expecting higher top

line growth and a 1pp lower EBITDA margin (from 15% to 14%).

Bottom line burdened by USD weakness...

After a decent quarter, we expect the company to keep its double-digit top line

growth in the second half of the year, as confirmed in the guidance update. The

stringing equipment business should continue its positive momentum, thanks to

the improving quality of the backlog (focused on smaller projects) and new

orders from South America (Brazil). The railway business should be another key

growth driver, both at the top line and at operating level. Despite a slow start,

we estimate Marais will keep its double-digit revenues growth and expand its

margin in 2H17, due to stronger project execution. Trenching equipment

remains the risky part of this story, even if going forward this business should

benefit from an easy comparison yoy (extremely weak 4Q16). At the EBITDA

level, we stick to our recurring EBITDA margin forecast of c.13%. At the bottom

line level, we now expect the company to be in the red this year, factoring in

€2.5m FX losses. On 2018, we cut EPS by 20% owing chiefly to higher D&A.

...but cash conversion finally in a better shape

The improvement in FCF reported in 1H17 is more than welcome considering the

high net debt level of the company. For FY17 we expect this positive trend to

continue, closing with €89m of net debt by YE (from €96.7m in FY16). However,

the high level of the inventories remains an item to be closely monitored. We

improved our cash flow assumptions to factor in a better WC containment, with

a ratio on sales of c.42%.

Need for further delivery. Neutral confirmed with TP of €0.62/sh

On the back of the 1H17 results, we adjust our 2017-18 estimates marginally,

increasing the top line (c.3%) while keeping unchanged our overall assumptions

on recurring operating margins. Our target price lands at €0.62/share (from

€0.60) as the sum of: 1) €0.65/share based on DCF analysis; and 2) €0.58/share

from peer multiple comparison. We still attach good growth potential to the

company’s product range, however, in order to be more positive we need a

better balance between top line growth and working capital management. We

confirm our Neutral recommendation.

+39 02 8829 673

Giuseppe Grimaldi

Equity Analyst

+39 02 8829 412

Source: Mediobanca Securities

Price: € 0.50 Target price: € 0.62 Neutral

2016 2017E 2018E 2019E

EPS Adj (€) -0.06 -0.01 0.03 0.04

DPS (€) 0 0 0 0

BVPS (€) 0.45 0.43 0.45 0.50

EV/Ebitda(x) 18.0 7.5 6.0 5.3

P/E adj (x) nm nm 18.6 12.0

Div.Yield(%) 0.0% 0.0% 0.0% 0.0%

OpFCF Yield (%) -2.1% 6.1% 3.5% 5.3%

Market Data

Market Cap (€m) 54

Shares Out (m) 107

FI.IND and TTC S.r.l (%) 43%

Free Float (%) 57%

52 week range (€) 0.56-0.46

Rel Perf vs DJGL Italy DJ Total Market Italy (%)

-1m -6.2%

-3m -3.2%

-12m -23.5%

21dd Avg. Vol. 164,380

Reuters/Bloomberg TES.MI / TES IM

Una

utho

rized

redi

strib

utio

n of

this

repo

rt is

pro

hibi

ted.

Thi

s rep

ort i

s int

ende

d fo

r IR

Team

Tesmec

08 August 2017 ◆ 2

Price: € 0.50 Target price: € 0.62 Neutral

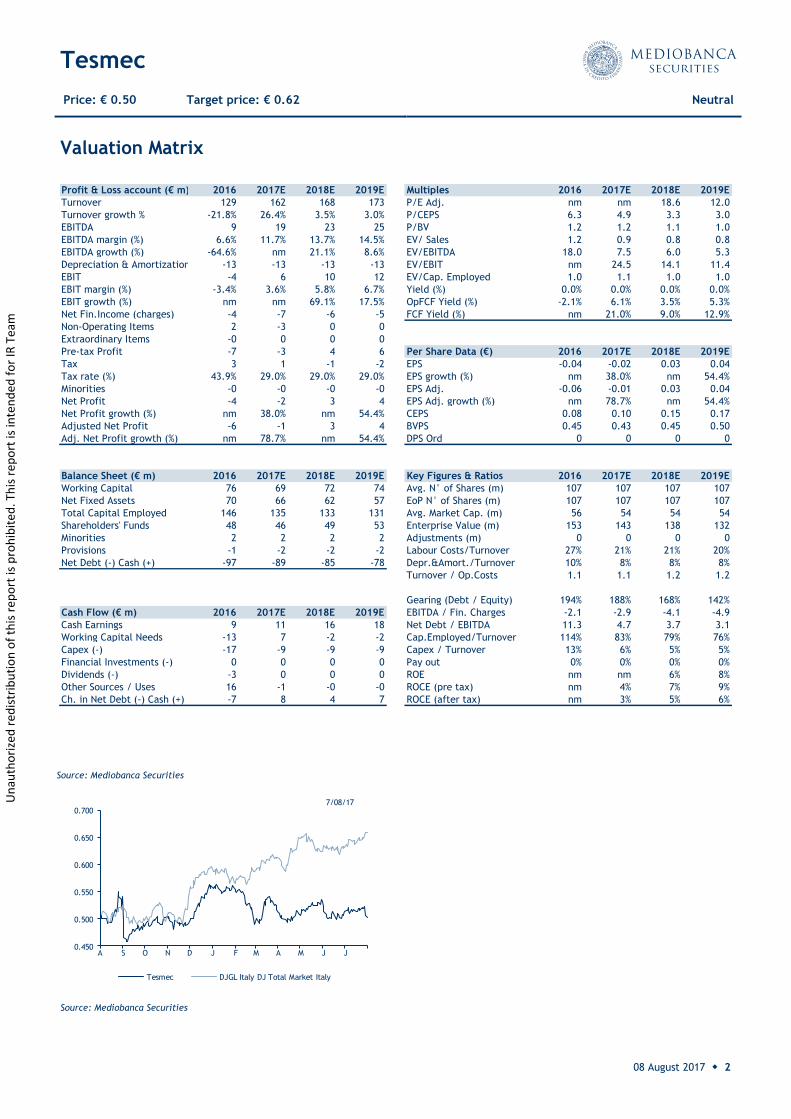

Valuation Matrix

Source: Mediobanca Securities

Source: Mediobanca Securities

Profit & Loss account (€ m) 2016 2017E 2018E 2019E Multiples 2016 2017E 2018E 2019E

Turnover 129 162 168 173 P/E Adj. nm nm 18.6 12.0

Turnover growth % -21.8% 26.4% 3.5% 3.0% P/CEPS 6.3 4.9 3.3 3.0

EBITDA 9 19 23 25 P/BV 1.2 1.2 1.1 1.0

EBITDA margin (%) 6.6% 11.7% 13.7% 14.5% EV/ Sales 1.2 0.9 0.8 0.8

EBITDA growth (%) -64.6% nm 21.1% 8.6% EV/EBITDA 18.0 7.5 6.0 5.3

Depreciation & Amortization -13 -13 -13 -13 EV/EBIT nm 24.5 14.1 11.4

EBIT -4 6 10 12 EV/Cap. Employed 1.0 1.1 1.0 1.0

EBIT margin (%) -3.4% 3.6% 5.8% 6.7% Yield (%) 0.0% 0.0% 0.0% 0.0%

EBIT growth (%) nm nm 69.1% 17.5% OpFCF Yield (%) -2.1% 6.1% 3.5% 5.3%

Net Fin.Income (charges) -4 -7 -6 -5 FCF Yield (%) nm 21.0% 9.0% 12.9%

Non-Operating Items 2 -3 0 0

Extraordinary Items -0 0 0 0

Pre-tax Profit -7 -3 4 6 Per Share Data (€) 2016 2017E 2018E 2019E

Tax 3 1 -1 -2 EPS -0.04 -0.02 0.03 0.04

Tax rate (%) 43.9% 29.0% 29.0% 29.0% EPS growth (%) nm 38.0% nm 54.4%

Minorities -0 -0 -0 -0 EPS Adj. -0.06 -0.01 0.03 0.04

Net Profit -4 -2 3 4 EPS Adj. growth (%) nm 78.7% nm 54.4%

Net Profit growth (%) nm 38.0% nm 54.4% CEPS 0.08 0.10 0.15 0.17

Adjusted Net Profit -6 -1 3 4 BVPS 0.45 0.43 0.45 0.50

Adj. Net Profit growth (%) nm 78.7% nm 54.4% DPS Ord 0 0 0 0

Balance Sheet (€ m) 2016 2017E 2018E 2019E Key Figures & Ratios 2016 2017E 2018E 2019E

Working Capital 76 69 72 74 Avg. N° of Shares (m) 107 107 107 107

Net Fixed Assets 70 66 62 57 EoP N° of Shares (m) 107 107 107 107

Total Capital Employed 146 135 133 131 Avg. Market Cap. (m) 56 54 54 54

Shareholders' Funds 48 46 49 53 Enterprise Value (m) 153 143 138 132

Minorities 2 2 2 2 Adjustments (m) 0 0 0 0

Provisions -1 -2 -2 -2 Labour Costs/Turnover 27% 21% 21% 20%

Net Debt (-) Cash (+) -97 -89 -85 -78 Depr.&Amort./Turnover 10% 8% 8% 8%

Turnover / Op.Costs 1.1 1.1 1.2 1.2

Gearing (Debt / Equity) 194% 188% 168% 142%

Cash Flow (€ m) 2016 2017E 2018E 2019E EBITDA / Fin. Charges -2.1 -2.9 -4.1 -4.9

Cash Earnings 9 11 16 18 Net Debt / EBITDA 11.3 4.7 3.7 3.1

Working Capital Needs -13 7 -2 -2 Cap.Employed/Turnover 114% 83% 79% 76%

Capex (-) -17 -9 -9 -9 Capex / Turnover 13% 6% 5% 5%

Financial Investments (-) 0 0 0 0 Pay out 0% 0% 0% 0%

Dividends (-) -3 0 0 0 ROE nm nm 6% 8%

Other Sources / Uses 16 -1 -0 -0 ROCE (pre tax) nm 4% 7% 9%

Ch. in Net Debt (-) Cash (+) -7 8 4 7 ROCE (after tax) nm 3% 5% 6%

0.450

0.500

0.550

0.600

0.650

0.700

A S O N D J F M A M J J

Tesmec DJGL Italy DJ Total Market Italy

7/08/17Una

utho

rized

redi

strib

utio

n of

this

repo

rt is

pro

hibi

ted.

Thi

s rep

ort i

s int

ende

d fo

r IR

Team

Tesmec

08 August 2017 ◆ 3

Price: € 0.50 Target price: € 0.62 Neutral

1H17: Results in line, better FCF Last Friday (4 August) the company reported its 1H17 results, updating its FY outlook.

Looking at P&L, 1H17 revenues and recurring EBITDA matched our estimates. However,

reported EBITDA fell below our estimates reflecting the impact of an unfavourable legal ruling

in the US. The bottom line was strongly affected by FX headwinds, leading to a negative

result. On the balance sheet side, we highlight the positive FCF due to an improvement in

trade working capital.

Below are the main points:

1H17 revenues were €91m (+23% yoy) in line with our estimates. In 2Q17 the company fully

matched its top line guidance with sales growing 23% yoy, confirming the trend seen in the

previous quarter. By segment, stringing equipment (+44.2% yoy) benefited from a general

recovery in investment in the energy sector as well as from the completion of the Indonesian

order production activities. Trenchers’ slight growth (+3.7% yoy) was attributable to Marais,

which more than offset the drop in traditional selling activities. Railways continued the

positive trend;

1H17 reported EBITDA of €8.7m (+18.3%) was below our estimate of €10.0m. However, the

figure has been affected by the impact of non recurring items (a €1.7m legal claim in the

US);

1H17 net loss was in line with our estimates. The bottom line has been affected negatively

by c. €3m FX losses, which were partly offset by lower taxes;

1H17 net debt was €91.5m, from €96.7m in FY16. The FCF generation was mainly due to a

better control of the net working capital (€4.4m reduction in the level of the inventories),

which more than offset the higher than expected capex linked to Marais’ fleet maintenance.

Following the 1H17 results, the company updated its FY guidance, increasing its revenue

expectations, while slightly revising down its forecasted EBITDA margin. In more detail, the positive

development of the US market and the increasing number of projects for renewable energy and

telecommunications leads to a better outlook. Tesmec now aims to exceed the €160-170m

revenues’ range for the FY17. This compares with our estimate of €162m. However, the company

revised its expectation on EBITDA margin, which is now seen 1pp down, in the 14% region (from the

previous 15%; vs MBe now at 12.8%), reflecting the impact of FX on profitability rates. A further

reduction in net debt is also expected in 2H17.

2Q17 and 1H17 results

(€m) 2Q 2017A 2Q 2016 % ch. 2Q 2017E A/E 1H 2017A 1H 2016 % ch. 1H 2017E A/E

Total sales 41.3 33.5 +23.3% 41.0 +0.8% 91.1 74.0 +23.2% 90.8 +0.4%

EBITDA recurring 4.8 2.0 +137.4% 4.4 +9.4% 10.4 9.9 +5.6% 10.0 +4.1%

EBITDA margin 11.6% 6.0%

10.7%

11.4% 13.3%

11.0%

EBITDA reported 3.1 2.0 +53.0% 4.4 -29.5% 8.7 7.4 +18.3% 10.0 -12.9%

EBITDA margin 7.5% 6.0%

10.7%

9.6% 10.0%

11.0%

EBIT (0.5) (1.0) nm 1.3 nm 2.0 1.4 +39.0% 3.8 -47.3%

EBIT margin -1.3% -3.0%

3.1%

2.2% 2.0%

4.2%

Net profit (2.6) (1.2) nm (2.4) nm (1.8) (1.3) nm (1.5) nm

Net debt 91.5 104.8

92.5

91.5 104.8

92.5 -1.1%

Source: Mediobanca Securities

Una

utho

rized

redi

strib

utio

n of

this

repo

rt is

pro

hibi

ted.

Thi

s rep

ort i

s int

ende

d fo

r IR

Team

Tesmec

08 August 2017 ◆ 4

Price: € 0.50 Target price: € 0.62 Neutral

2017-18: Change in estimates. Introducing our 2019 estimates Given the FX headwind and the material effects of non recurring items, we have changed our

FY17-FY18 estimates after the 1H17 figures, also factoring in the update on FY17 outlook

provided by the company. Note that we now present our FY19 estimates.

Below is a summary of the main changes.

Our change in estimates in detail:

Sales: We slightly increased our top line estimates for both FY17 and FY18, taking into

account the revision of the guidance and an improving outlook in all the main businesses;

EBITDA: We kept our recurring EBITDA unchanged for this year, while we cut the reported

EBITDA to €19.0m (-8.0% yoy) to reflect the negative impact of the US ruling. We also fine

tuned our EBITDA for the next year;

Net income: We revised down both our FY17-18 estimates to reflect a €2.5m negative

EBITDA impact of FX this year, while we raised our D&A estimates for next year following the

higher capex related to the Marais fleet;

Net debt: Going forward we expect the company to keep its commitment to deleveraging

following the positive results of 1H17. In our view the improvement in FCF comes from a

tighter control of the working capital due to destocking and an improvement in receivables

collection. We expect Tesmec to reach a net debt of €89m and €84m, in 2017 and 2018,

respectively.

Change in estimates

(€m) 2017E old 2017E new % Chg. 2018E old 2018E new % Chg. 2019E

Sales 158.3 162.5 2.6% 163.9 168.2 2.6% 173.2

Recurring EBITDA 20.7 20.7 0.2% 23.4 23.1 -1.3% 25.0

EBITDA margin recurring 13.1% 12.8%

14.3% 13.7%

14.5%

Reported EBITDA 20.7 19.0 -8.0% 23.4 23.1 -1.3% 25.0

EBITDA margin reported 13.1% 11.7%

14.3% 13.7%

14.5%

EBIT 8.5 5.8 -31.9% 11.0 9.8 -10.3% 11.6

EBIT margin 5.4% 3.6%

6.7% 5.8%

6.7%

Net profit 1.2 (2.4) nm 3.6 2.9 -19.6% 4.5

Net debt 93.2 89.1

86.7 84.6

78.0

Source: Mediobanca Securities

Una

utho

rized

redi

strib

utio

n of

this

repo

rt is

pro

hibi

ted.

Thi

s rep

ort i

s int

ende

d fo

r IR

Team

Tesmec

08 August 2017 ◆ 5

Price: € 0.50 Target price: € 0.62 Neutral

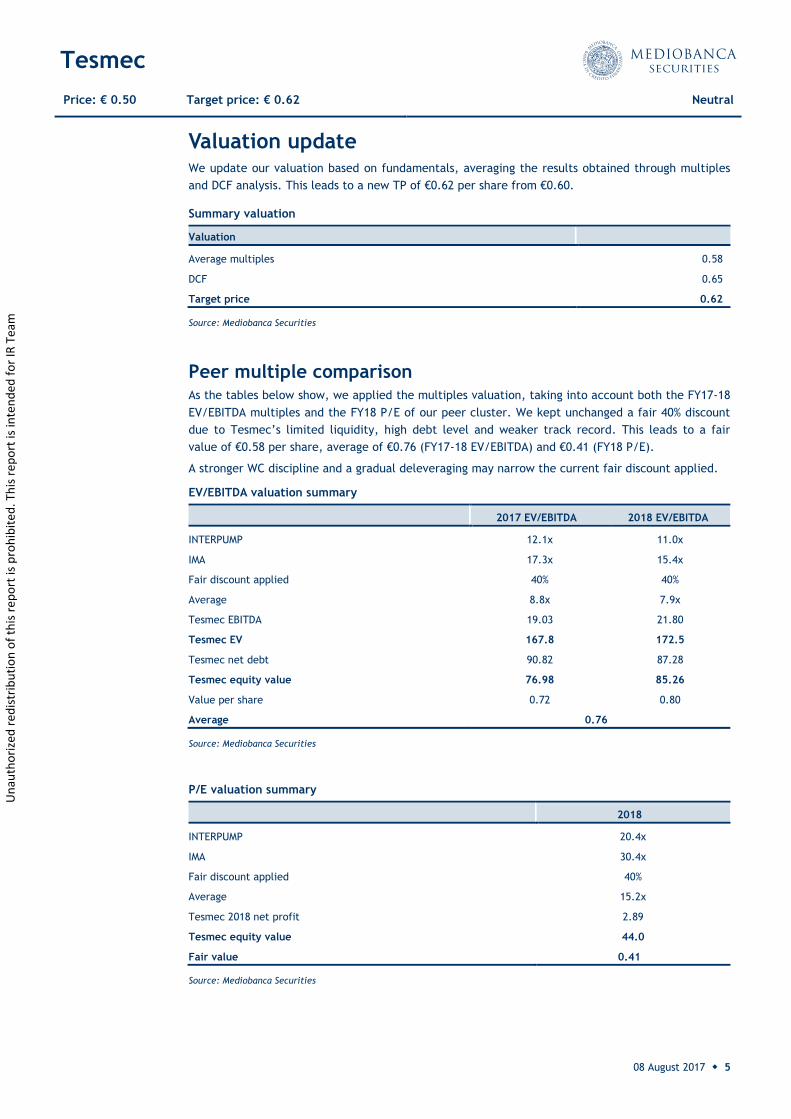

Valuation update We update our valuation based on fundamentals, averaging the results obtained through multiples

and DCF analysis. This leads to a new TP of €0.62 per share from €0.60.

Peer multiple comparison As the tables below show, we applied the multiples valuation, taking into account both the FY17-18

EV/EBITDA multiples and the FY18 P/E of our peer cluster. We kept unchanged a fair 40% discount

due to Tesmec’s limited liquidity, high debt level and weaker track record. This leads to a fair

value of €0.58 per share, average of €0.76 (FY17-18 EV/EBITDA) and €0.41 (FY18 P/E).

A stronger WC discipline and a gradual deleveraging may narrow the current fair discount applied.

Summary valuation

Valuation

Average multiples 0.58

DCF 0.65

Target price 0.62

Source: Mediobanca Securities

EV/EBITDA valuation summary

2017 EV/EBITDA 2018 EV/EBITDA

INTERPUMP 12.1x 11.0x

IMA 17.3x 15.4x

Fair discount applied 40% 40%

Average 8.8x 7.9x

Tesmec EBITDA 19.03 21.80

Tesmec EV 167.8 172.5

Tesmec net debt 90.82 87.28

Tesmec equity value 76.98 85.26

Value per share 0.72 0.80

Average 0.76

Source: Mediobanca Securities

P/E valuation summary

2018

INTERPUMP 20.4x

IMA 30.4x

Fair discount applied 40%

Average 15.2x

Tesmec 2018 net profit 2.89

Tesmec equity value 44.0

Fair value 0.41

Source: Mediobanca Securities

Una

utho

rized

redi

strib

utio

n of

this

repo

rt is

pro

hibi

ted.

Thi

s rep

ort i

s int

ende

d fo

r IR

Team

Tesmec

08 August 2017 ◆ 6

Price: € 0.50 Target price: € 0.62 Neutral

DCF analysis Based on our estimates, the DCF returns a fair value of €0.65. Our analysis is based on a WACC of

6.59% and on a perpetual growth rate of 1.0%. The table below summarises our DCF valuation.

On the back of the 1H17 results, we adjust our 2017-18 estimates, marginally increasing the top line

(c.3%) while keeping unchanged our overall assumptions on recurring operating margins. Our target

price lands at €0.62/share (from €0.60) as the sum of: 1) €0.65/share based on DCF analysis; and 2)

€0.58/share from peer multiple comparisons. We still attach a good growth potential to the

company product range, however, in order to be more positive we need a better balance between

top line growth and working capital management. We confirm our Neutral recommendation.

DCF summary

DCF ANALYSIS

Perpetual growth rate 1.00%

WACC 6.59%

Terminal value as of 31/12/21 148.0

Discounting rate of terminal value 0.77

Discounted terminal value 114.7

Cumulated DFOCF 48.9

Enterprise value (€m) 163.6

2016 net debt (96.7)

Own shares market value* 2.4

Equity value (€ mn) 69.3

Value per share (€) 0.65

Source: Mediobanca Securities,* priced as of 4 August

Una

utho

rized

redi

strib

utio

n of

this

repo

rt is

pro

hibi

ted.

Thi

s rep

ort i

s int

ende

d fo

r IR

Team

Tesmec

08 August 2017 ◆ 7

Price: € 0.50 Target price: € 0.62 Neutral

GENERAL DISCLOSURES

This research report is prepared by Mediobanca - Banca di credito finanziario S.p.A. (“Mediobanca S.p.A.”), authorized and supervised by Bank of Italy and Consob to provide financial services, and is compliant with the relevant European Directive provisions on investment and ancillary services (MiFID Directive) and with the implementing law.

Unless specified to the contrary, within EU Member States, the report is made available by Mediobanca S.p.A. The distribution of this document by Mediobanca S.p.A. in other jurisdictions may be restricted by law and persons into whose possession this document comes should inform themselves about, and observe, any such restrictions. All reports are disseminated and available to all clients simultaneously through electronic distribution and publication to our internal client websites. The recipient acknowledges that, to the extent permitted by applicable securities laws and regulations, Mediobanca S.p.A. disclaims all liability for providing this research, and accepts no liability whatsoever for any direct, indirect or consequential loss arising from the use of this document or its contents. This research report is provided for information purposes only and does not constitute or should not be construed as a provision of investment advice, an offer to buy or sell, or a solicitation of an offer to buy or sell, any financial instruments. It is not intended to represent the conclusive terms and conditions of any security or transaction, nor to notify you of any possible risks, direct or indirect, in undertaking such a transaction. Not all investment strategies are appropriate at all times, and past performance is not necessarily a guide to future performance. Mediobanca S.p.A. recommends that independent advice should be sought, and that investors should make their own independent decisions as to whether an investment or instrument is proper or appropriate based on their own individual judgment, their risk-tolerance, and after consulting their own investment advisers. Unless you notify Mediobanca S.p.A. otherwise, Mediobanca S.p.A. assumes that you have sufficient knowledge, experience and/or professional advice to undertake your own assessment. This research is intended for use only by those professional clients to whom it is made available by Mediobanca S.p.A. The information contained herein, including any expression of opinion, has been obtained from or is based upon sources believed to be reliable but is not guaranteed as to accuracy or completeness although Mediobanca S.p.A. considers it to be fair and not misleading. Any opinions or estimates expressed herein reflect the judgment of the author(s) as of the date the research was prepared and are subject to change at any time without notice. Unless otherwise stated, the information or opinions presented, or the research or analysis upon which they are based, are updated as necessary and at least annually. Mediobanca S.p.A. may provide hyperlinks to websites of entities mentioned in this document, however the inclusion of a link does not imply that Mediobanca S.p.A. endorses, recommends or approves any material on the linked page or accessible from it. Mediobanca S.p.A. does not accept responsibility whatsoever for any such material, nor for any consequences of its use. Neither Mediobanca S.p.A. nor any of its directors, officers, employees or agents shall have any liability, howsoever arising, for any error, inaccuracy or incompleteness of fact or opinion in this report or lack of care in its preparation or publication.

Our salespeople, traders, and other professionals may provide oral or written market commentary or trading strategies to our clients and our proprietary trading desks that reflect opinions that are contrary to the opinions expressed in this research. Our proprietary trading desks and investing businesses may make investment decisions that are inconsistent with the recommendations or views expressed in this research. The analysts named in this report may have from time to time discussed with our clients, including Mediobanca S.p.A. salespersons and traders, or may discuss in this report, trading strategies that reference catalysts or events that may have a near-term impact on the market price of the equity securities discussed in this report, which impact may be directionally counter to the analysts' published price target expectations for such stocks. Any such trading strategies are distinct from and do not affect the analysts' fundamental equity rating for such stocks, which rating reflects a stock's return potential relative to its coverage group as described herein.

ADDITIONAL DISCLAIMERS TO U.S. INVESTORS: This research report is prepared by Mediobanca S.p.A. and distributed in the United States by Mediobanca Securities USA LLC, which is a wholly owned subsidiary of Mediobanca S.p.A., is a member of Finra and is registered with the US Securities and Exchange Commission. 565 Fifth Avenue - New York NY 10017. Mediobanca Securities USA LLC accepts responsibility for the content of this report. Any US person receiving this report and wishing to effect any transaction in any security discussed in this report should contact Mediobanca Securities USA LLC at 001(212) 991-4745. Please refer to the contact page for additional contact information. All transactions by a US person in the securities mentioned in this report must be effected through Mediobanca Securities USA LLC and not through a non-US affiliate. The research analyst(s) named on this report are not registered / qualified as research analysts with Finra. The research analyst(s) are not associated persons of Mediobanca Securities USA LLC and therefore are not subject to NASD rule 2711 and incorporated NYSE rule 472 restrictions on communications with a subject company, public appearances and trading securities held by a research analyst.

ADDITIONAL DISCLAIMERS TO U.K. INVESTORS: Mediobanca S.p.A. provides investment services in the UK through a branch established in the UK (as well as directly from its establishment(s) in Italy) pursuant to its passporting rights under applicable EEA Banking and Financial Services Directives and in accordance with applicable Financial Services Authority requirements.

ADDITIONAL DISCLAIMERS TO U.A.E. INVESTORS: This research report has not been approved or licensed by the UAE Central Bank, the UAE Securities and Commodities Authority (SCA), the Dubai Financial Services Authority (DFSA) or any other relevant licensing authorities in the UAE, and does not constitute a public offer of securities in the UAE in accordance with the commercial companies law, Federal Law No. 8 of 1984 (as amended), SCA Resolution No.(37) of 2012 or otherwise. This research report is strictly private and confidential and is being issued to sophisticated investors.

REGULATORY DISCLOSURES

Mediobanca S.p.A. does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Mediobanca S.p.A. or its affiliates or its employees may effect transactions in the securities described herein for their own account or for the account of others, may have long or short positions with the issuer thereof, or any of its affiliates, or may perform or seek to perform securities, investment banking or other services for such issuer or its affiliates. The organisational and administrative arrangements established by Mediobanca S.p.A. for the management

Disclaimer

Una

utho

rized

redi

strib

utio

n of

this

repo

rt is

pro

hibi

ted.

Thi

s rep

ort i

s int

ende

d fo

r IR

Team

Tesmec

08 August 2017 ◆ 8

Price: € 0.50 Target price: € 0.62 Neutral

of conflicts of interest with respect to investment research are consistent with rules, regulations or codes applicable to the securities industry. The compensation of the analyst who prepared this report is determined exclusively by research management and senior management (not including investment banking). Analyst compensation is not based on investment banking revenues, however, compensation may relate to the revenues of Mediobanca S.p.A. as a whole, of which investment banking, sales and trading are a part.

For a detailed explanation of the policies and principles implemented by Mediobanca S.p.A. to guarantee the integrity and independence of researches prepared by Mediobanca's analysts, please refer to the research policy which can be found at the following link: http://www.mediobanca.it/static/upload/b5d/b5d01c423f1f84fffea37bd41ccf7d74.pdf

Unless otherwise stated in the text of the research report, target prices are based on either a discounted cash flow valuation and/or comparison of valuation ratios with companies seen by the analyst as comparable or a combination of the two methods. The result of this fundamental valuation is adjusted to reflect the analyst's views on the likely course of investor sentiment. Whichever valuation method is used there is a significant risk that the target price will not be achieved within the expected timeframe. Risk factors include unforeseen changes in competitive pressures or in the level of demand for the company's products. Such demand variations may result from changes in technology, in the overall level of economic activity or, in some cases, from changes in social values. Valuations may also be affected by changes in taxation, in exchange rates and, in certain industries, in regulations. All prices are market close prices unless differently specified.

Since 1 July 2013, Mediobanca uses a relative rating system, based on the following judgements: Outperform, Neutral, Underperform and Not Rated.

Outperform (O). The stock’s total return is expected to exceed the average total return of the analyst’s industry (or industry team’s) coverage universe, on a risk-adjusted basis, over the next 6-12 months.

Neutral (N). The stock’s total return is expected to be in line with the average total return of the analyst’s industry (or industry team’s) coverage universe, on a risk-adjusted basis, over the next 6-12 months.

Underperform (U). The stock’s total return is expected to be below the average total return of the analyst’s industry (or industry team’s) coverage universe, on a risk-adjusted basis, over the next 6-12 months.

Not Rated (NR). Currently the analyst does not have adequate confidence about the stock’s total return relative to the average total return of the analyst’s industry (or industry team’s) coverage, on a risk-adjusted basis, over the next 6-12 months. Alternatively, it is applicable pursuant to Mediobanca policy in circumstances when Mediobanca is acting in any advisory capacity in a strategic transaction involving this company or when the company is the target of a tender offer.

Our recommendation relies upon the expected relative performance of the stock considered versus its benchmark. Such an expected relative performance relies upon a valuation process that is based on the analysis of the company's business model / competitive positioning / financial forecasts. The company's valuation could change in the future as a consequence of a modification of the mentioned items.

Please consider that the above rating system also drives the portfolio selections of the Mediobanca's analysts as follows: long positions can only apply to stocks rated Outperform and Neutral; short positions can only apply to stocks rated Underperform and Neutral; portfolios selection cannot refer to Not Rated stocks; Mediobanca portfolios might follow different time horizons.

Proportion of all recommendations relating to the last quarter

Outperform Neutral Underperform Not Rated

45.96% 40.44% 12.13% 1.47%

Proportion of issuers to which Mediobanca S.p.A. has supplied material investment banking services relating to the last quarter:

Outperform Neutral Underperform Not Rated

60.94% 58.62% 23.08% 100.00%

The current stock ratings system has been used since 1 July 2013. Before then, Mediobanca S.p.A. used a different system, based on the following ratings: outperform, neutral, underperform, under review, not rated. For additional details about the old ratings system, please access research reports dated before 1 July 2013 from the restricted part of the “MB Securities” section of the Mediobanca S.p.A. website at www.mediobanca.com.

Disclaimer

Una

utho

rized

redi

strib

utio

n of

this

repo

rt is

pro

hibi

ted.

Thi

s rep

ort i

s int

ende

d fo

r IR

Team

Tesmec

08 August 2017 ◆ 9

Price: € 0.50 Target price: € 0.62 Neutral

COMPANY SPECIFIC REGULATORY DISCLOSURES

INVESTMENT AND ANCILLARY SERVICES In the last 12 months, Mediobanca S.p.A. or one or more of the companies belonging to its group has entered into agreements to deliver investment and ancillary services to Tesmec or one or more of the companies belonging to its group.

RATING The present rating in regard to Tesmec has not been changed since 06/03/2017. In the past 12 months, the rating on Tesmec has been changed. The previous rating, issued on 14/04/2015, was Outperform.

INITIAL COVERAGE

Tesmec initial coverage as of 21/09/2010.

COPYRIGHT NOTICE

No part of the content of any research material may be copied, forwarded or duplicated in any form or by any means without the prior consent of Mediobanca S.p.A., and Mediobanca S.p.A. accepts no liability whatsoever for the actions of third parties in this respect. END NOTES

The disclosures contained in research reports produced by Mediobanca S.p.A. shall be governed by and construed in accordance with Italian law. Additional information is available upon request.

The list of all recommendations disseminated in the last 12 months by Mediobanca's analysts is available here

Date of report production: 08 August 2017 - 07:31

Disclaimer Disclaimer Disclaimer Disclaimer

Una

utho

rized

redi

strib

utio

n of

this

repo

rt is

pro

hibi

ted.

Thi

s rep

ort i

s int

ende

d fo

r IR

Team

Tesmec

08 August 2017 ◆ 10

Price: € 0.50 Target price: € 0.62 Neutral

Mediobanca S.p.A.

Antonio Guglielmi – Head of Equity Markets

+44 203 0369 570

Mediobanca S.p.A.

Andrea Filtri/Javier Suarez - Co - Heads of European Equity Research

(Reporting to the Group General Manager)

ANALYSTS

European Banks

Adam Terelak IBK +44 203 0369 574 [email protected]

Alberto Nigro Spain/Italy +44 203 0369 575 [email protected]

Andrea Filtri Spain/Italy +44 203 0369 571 [email protected]

Noemi Peruch Spain/Italy +44 203 0369 645 [email protected]

Omar Fall France +44 203 0369 567 [email protected]

Riccardo Rovere Italy/Scandinavia/CEE/Germany +39 02 8829 604 [email protected]

Robin van den Broek Benelux +44 203 0369 672 [email protected]

European Insurance

Gian Luca Ferrari Global multi-liners/Italy/Asset Gatherers +39 02 8829 482 [email protected]

Robin van den Broek Benelux +44 203 0369 672 [email protected]

Vinit Malhotra Global multi-liners/Reinsurers +44 203 0369 585 [email protected]

Italian Research

Alessandro Pozzi Oil & Oil Related +44 203 0369 617 [email protected]

Alessandro Tortora Building Materials/Industrials/Capital Goods +39 02 8829 673 [email protected]

Chiara Rotelli Branded Goods/Consumers Goods +39 02 8829 931 [email protected]

Fabio Pavan Media/Telecommunications/Consumer Goods +39 02 8829 633 [email protected]

Gian Luca Ferrari Global multi-liners/Italy/Asset Gatherers +39 02 8829 482 [email protected]

Javier Suárez Utilities +39 028829 036 [email protected]

Jean Farah Utilities +44 203 0369 665 [email protected]

Massimo Vecchio Auto & Auto Components/Industrials/Holdings +39 02 8829 541 [email protected]

Niccolò Storer Auto & Auto Components/Industrials/Holdings +39 02 8829 444 [email protected]

Nicolò Pessina Consumer Goods/Infrastructure +39 02 8829 796 [email protected]

Sara Piccinini Utilities +39 02 8829 295 [email protected]

Simonetta Chiriotti Real Estate/ Financial Services/Banks +39 02 8829 933 [email protected]

FOR NON US PERSON receiving this document and wishing to effect transactions in any securities discussed herein, please contact:

Mediobanca S.p.A.

Carlo Pirri - Head of Equity Sales SALES

Angelo Vietri

+39 02 8829 989 [email protected]

Christopher Seidenfaden

+44 203 0369 610 [email protected]

Lorenzo Angeloni

+39 02 8829 507 [email protected]

Matteo Agrati

+44 203 0369 629 [email protected]

Nahid Iqbal

+44 203 0369 597 [email protected]

Pierandrea Perrone

+39 02 8829 572 [email protected]

Timothy Pedroni

+44 203 0369 635 [email protected]

Stephane Langlois

+44 203 0369 582 [email protected]

European Spec Sales

Carlo Pirri Banks/Insurance +44 203 0369 531 [email protected]

Alan Davies Banks/Insurance +44 203 0369 510 [email protected]

Colin Hector Banks/Insurance +44 203 0369 687 [email protected]

Mediobanca S.p.A.

Cedric Hanisch - Head of Equity Trading and Sales Trading

SALES/TRADERS

Andrew Westoby

+44 203 0369 513 [email protected]

Cedric Hanisch

+44 203 0369 584 [email protected]

Michael Sherry

+44 203 0369 605 [email protected]

Roberto Riboldi +39 02 8829 639 [email protected]

FOR US PERSON receiving this document and wishing to effect transactions in any securities discussed herein, please contact:

Mediobanca Securities USA LLC

Pierluigi Gastone - Head of Mediobanca Securities USA LLC

Massimiliano Pula

+1 646 839 4911 [email protected]

Pierluigi Gastone

+1 212 991 4745 [email protected]

Robert Perez

+1 646 839 4910 [email protected]

Mediobanca S.p.A.

Salvatore Guardino - Head of Corporate Broking

Enrico Baraldini

+39 02 8829 978 [email protected]

Nicolo Bottaro

+39 02 8829 429 [email protected]

Salvatore Guardino

+39 02 8829 826 [email protected]

Vito Pinto

+39 02 8829 542 [email protected]

MEDIOBANCA – Banca di Credito Finanziario S.p.A. Piazzetta Enrico Cuccia, 1 - 20121 Milano - T. +39 02 8829.1 62 Buckingham Gate, London SW1E 6AJ – T. +44 (0) 203 0369 530

Una

utho

rized

redi

strib

utio

n of

this

repo

rt is

pro

hibi

ted.

Thi

s rep

ort i

s int

ende

d fo

r IR

Team