almost boring: residential housing in 2015 dr. jim gilkeson, cfa cfa society of orlando april 9,...

TRANSCRIPT

Almost Boring:Residential Housing in 2015

DR. JIM GILKESON, CFA

CFA SOCIETY OF ORLANDO

APRIL 9, 2015

Jim G

ilkeson, PhD

, CFA

2Where We’ve Been

2005: Is the Sky Falling?

2007: What a Difference a Year Makes

2008: Where Do We Go From Here?

2009: Reading the Tea Leaves

2010: The Good, the Bad, and the Ugly

2012: Have We Hit Bottom?

2013: (Very) Cautious Optimism

2014: Will Slow & Steady Win the Race?

2015: Almost Boring

4/9/2015

Jim G

ilkeson, PhD

, CFA

3What We’ll Talk About Today

Price

Volume (Sales)

Delinquency/Foreclosure

Financing

Supply

Demand

Wrap Up

4/9/2015

Jim G

ilkeson, PhD

, CFA

4Prices (constant quality)4/9/2015

1999 2002 2005 2008 2011 2014$ 150,000

$ 175,000

$ 200,000

$ 225,000

$ 250,000

$ 275,000

$ 300,000

$ 325,000

$ 350,000

U.S. South

Jim G

ilkeson, PhD

, CFA

5Median Home Prices

New homes Existing homes

4/9/2015

1999 2002 2005 2008 2011 2014100.0

120.0

140.0

160.0

180.0

200.0

220.0

240.0

260.0

280.0

300.0

U.S.

South

1999 2002 2005 2008 2011 2014100.0

120.0

140.0

160.0

180.0

200.0

220.0

240.0

260.0

280.0

300.0

U.S.

South

Jim G

ilkeson, PhD

, CFA

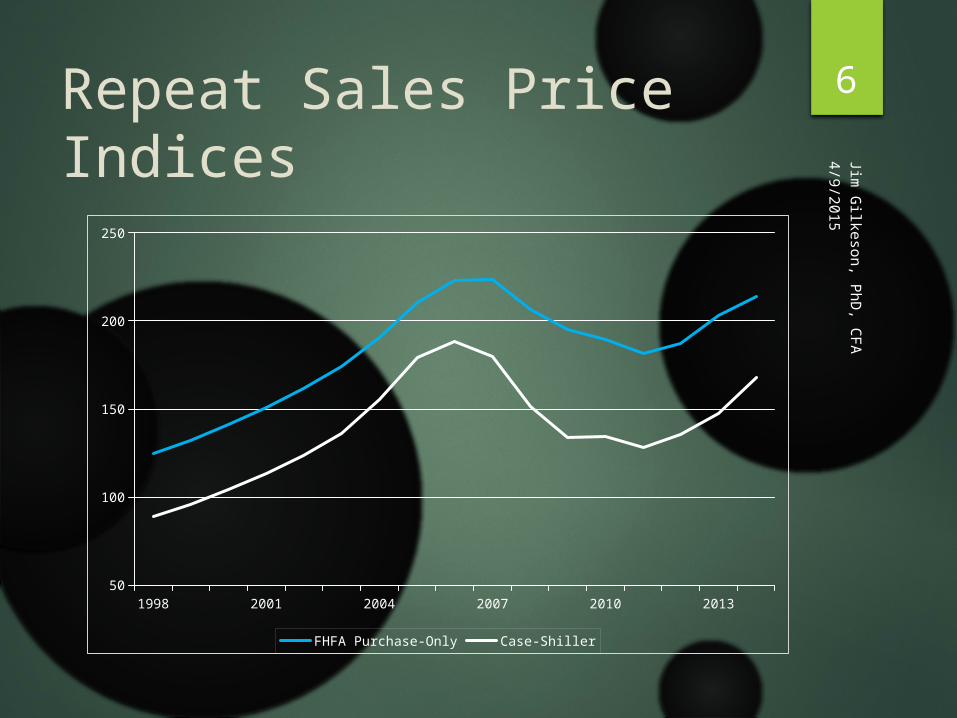

6Repeat Sales Price Indices4/9/2015

1998 2001 2004 2007 2010 201350

100

150

200

250

FHFA Purchase-Only Case-Shiller

Jim G

ilkeson, PhD

, CFA

7FHFA HPI (repeat sales)4/9/2015

2001 2004 2007 2010 2014100

150

200

250

300

350

US FL Orlando

Jim G

ilkeson, PhD

, CFA

8Florida Price Appreciation4/9/2015MSA 1-year 5-year

Miami 11.80% 25.02%

Ft Lauderdale 9.48% 32.29%

Jacksonville 8.71% 3.88%

Ft Myers 8.19% 31.74%

Tampa/St. Pete 7.41% 15.10%

West Palm Beach 7.26% 27.52%

Orlando 5.66% 9.17%

Sarasota 5.10% 19.25%

FLORIDA 7.85% 17.32%

Jim G

ilkeson, PhD

, CFA

9Sales Volume (US)4/9/2015

1998 2001 2004 2007 2010 20130

1000

2000

3000

4000

5000

6000

7000

8000

0

200

400

600

800

1000

1200

1400

existing

new

Jim G

ilkeson, PhD

, CFA

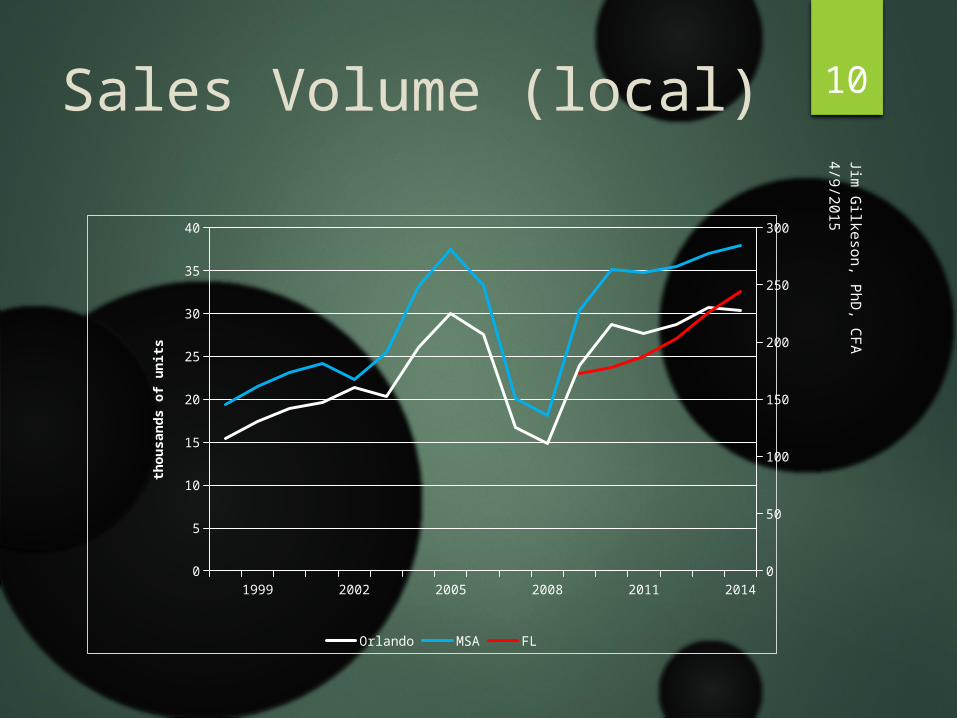

10Sales Volume (local)4/9/2015

1999 2002 2005 2008 2011 20140

5

10

15

20

25

30

35

40

0

50

100

150

200

250

300

Orlando MSA FL

tho

usa

nd

s o

f u

nit

s

Jim G

ilkeson, PhD

, CFA

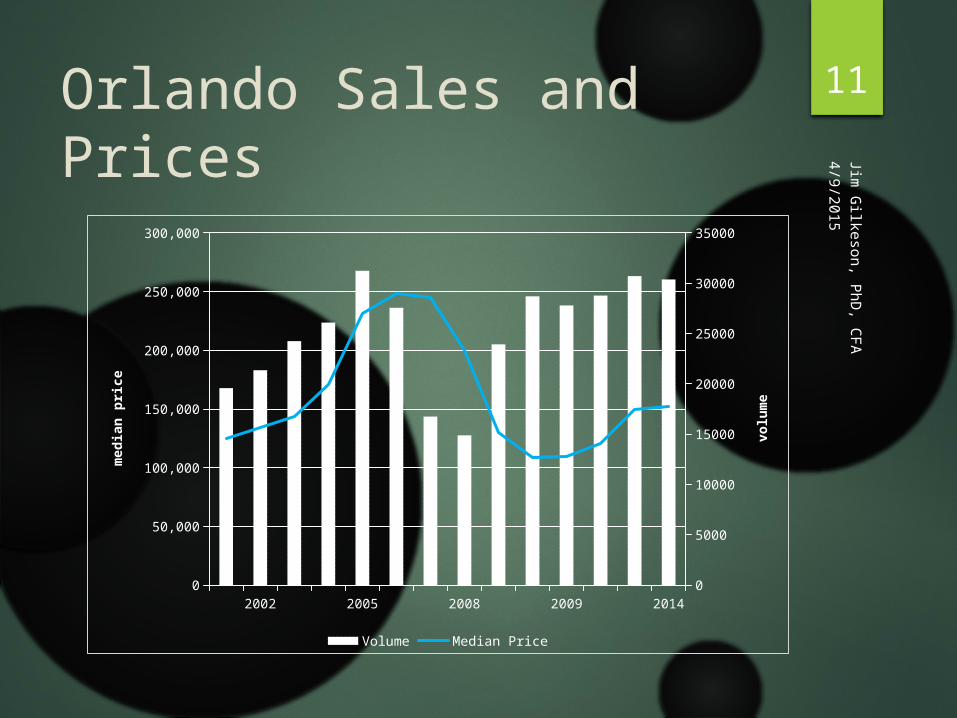

11Orlando Sales and Prices4/9/2015

2002 2005 2008 2009 20140

50,000

100,000

150,000

200,000

250,000

300,000

0

5000

10000

15000

20000

25000

30000

35000

Volume Median Price

med

ian

pri

ce

volu

me

Jim G

ilkeson, PhD

, CFA

12Bank Problem Loans:Federal Reserve Data 4/9/2015

1999 2002 2005 2008 2011 20140

2

4

6

8

10

12

Charge Offs Delinquencies

Rat

e (%

)

Jim G

ilkeson, PhD

, CFA

13Mortgage Delinquencies:U.S. banks (OCC) 4/9/2015

2008 2009 2010 2011 2012 2013 20140

1

2

3

4

5

6

7

8

Seriously Delinquent Foreclosure

Jim G

ilkeson, PhD

, CFA

14Florida Foreclosures4/9/2015

U.S. FloridaFL

rank Orlando

Foreclosure Inventory 1.4% 3.5% 3rd 3.2%

1-year change -0.6% -2.9% -3.3%

Completed foreclosures 552,048 111,321 1st 15,053

Serious Delinquency 4.0% 7.7% 2nd 7.4%

Jim G

ilkeson, PhD

, CFA

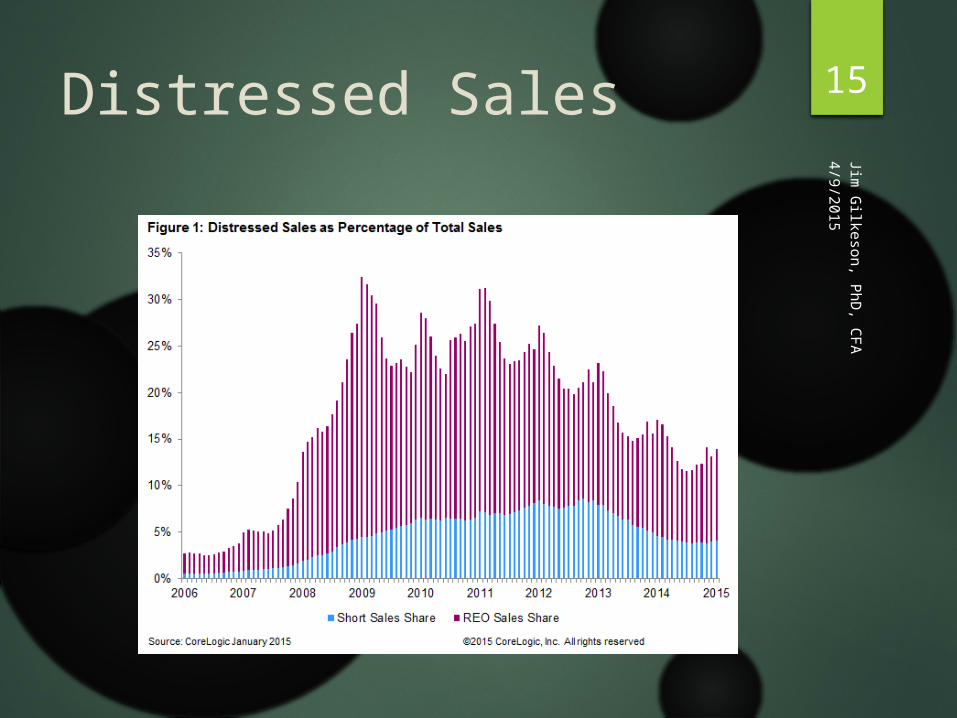

15Distressed Sales4/9/2015

Jim G

ilkeson, PhD

, CFA

16Conventional Mortgage Rate4/9/2015

99 02 05 08 11 140.00%

3.00%

6.00%

9.00%

Jim G

ilkeson, PhD

, CFA

174/9/2015

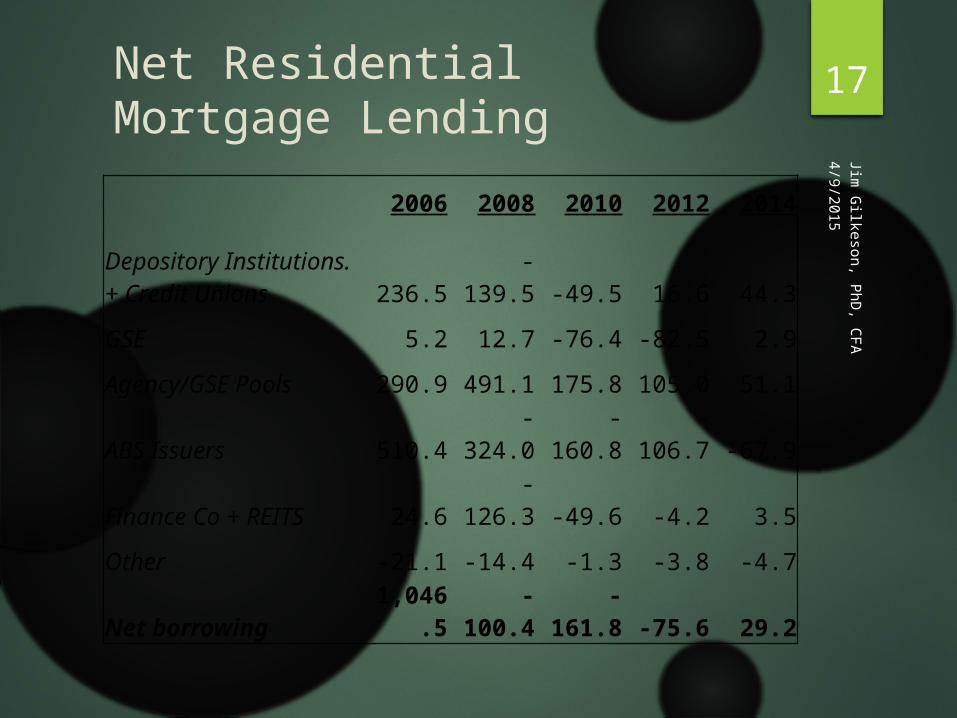

Net Residential Mortgage Lending

2006 2008 2010 2012 2014

Depository Institutions. + Credit Unions 236.5 -139.5 -49.5 16.6 44.3

GSE 5.2 12.7 -76.4 -82.5 2.9

Agency/GSE Pools 290.9 491.1 175.8 105.0 51.1

ABS Issuers 510.4 -324.0 -160.8 -106.7 -67.9

Finance Co + REITS 24.6 -126.3 -49.6 -4.2 3.5

Other -21.1 -14.4 -1.3 -3.8 -4.7

Net borrowing 1,046.5 -100.4 -161.8 -75.6 29.2

Jim G

ilkeson, PhD

, CFA

18FHA Share of Financings4/9/2015

2002 2004 2006 2008 2010 2012 20140.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

US Orlando

Jim G

ilkeson, PhD

, CFA

19Orlando Financing Sources:Cash is still King 4/9/2015

1998 2001 2004 2007 2010 20130%

20%

40%

60%

80%

100%

All Cash Conventional FHA/VA Other

Jim G

ilkeson, PhD

, CFA

20Single Family Starts4/9/2015

1998 2002 2006 2010 20140

500

1000

1500

2000

2500

0

4500

9000

13500

18000

US (000s) Orlando (units) FL (units)

Jim G

ilkeson, PhD

, CFA

21Housing Market Index4/9/2015

2005 2008 2011 20140

10

20

30

40

50

60

70

80

National South

Jim G

ilkeson, PhD

, CFA

224/9/2015

Household WealthBalance Sheet of Households & Nonprofit Organizations

(in $trillions) 2004 2009 2014 Δ04-14Assets 71.7 73.1 97.1 35.4% Tangible 28.4 23.7 29.1 2.5% Household Real Estate 22.1 16.9 20.6 -6.8% Financial 43.3 49.4 68.0 57.0% Deposits 6.2 8.1 10.2 64.5% Credit Market 3.4 5.6 3.4 0.0% Corporate Equities 8.0 7.5 13.4 67.5% Mutual Fund Shares 3.8 4.1 7.8 105.3% Businesses Owned 8.6 6.3 9.3 8.1% Pension Entitlements 11.4 15.2 20.8 82.5%Liabilities Home Mortgages 8.8 10.4 9.4 6.8% Consumer Credit 2.3 2.6 3.3 43.5%

Net Worth 59.6 59.0 77.3 29.7%

Jim G

ilkeson, PhD

, CFA

23Affordability Index (income/cost)4/9/2015

1999 2002 2005 2008 2011 20140.0

50.0

100.0

150.0

200.0

250.0

300.0

National Orlando

Jim G

ilkeson, PhD

, CFA

24Consumer Confidence4/9/2015

06 08 10 12 1494.00

95.00

96.00

97.00

98.00

99.00

100.00

101.00

102.00

0.0

20.0

40.0

60.0

80.0

100.0

120.0

OECD Indicator Univ Michigan

Jim G

ilkeson, PhD

, CFA

254/9/2015

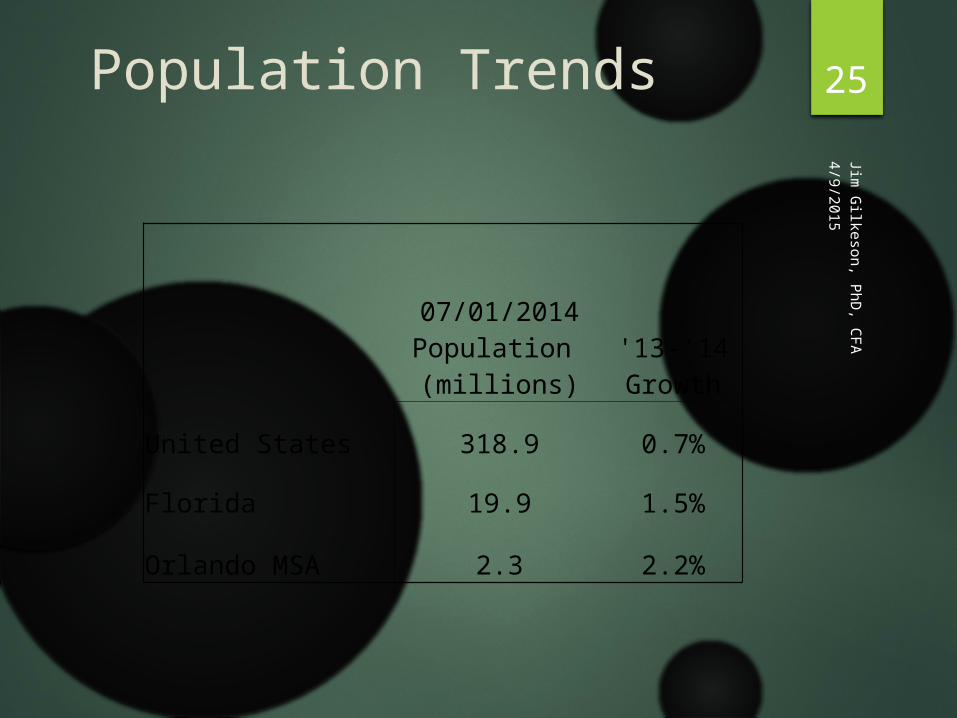

Population Trends

07/01/2014 Population (millions)

'13-'14 Growth

United States 318.9 0.7%

Florida 19.9 1.5%

Orlando MSA 2.3 2.2%

Jim G

ilkeson, PhD

, CFA

264/9/2015

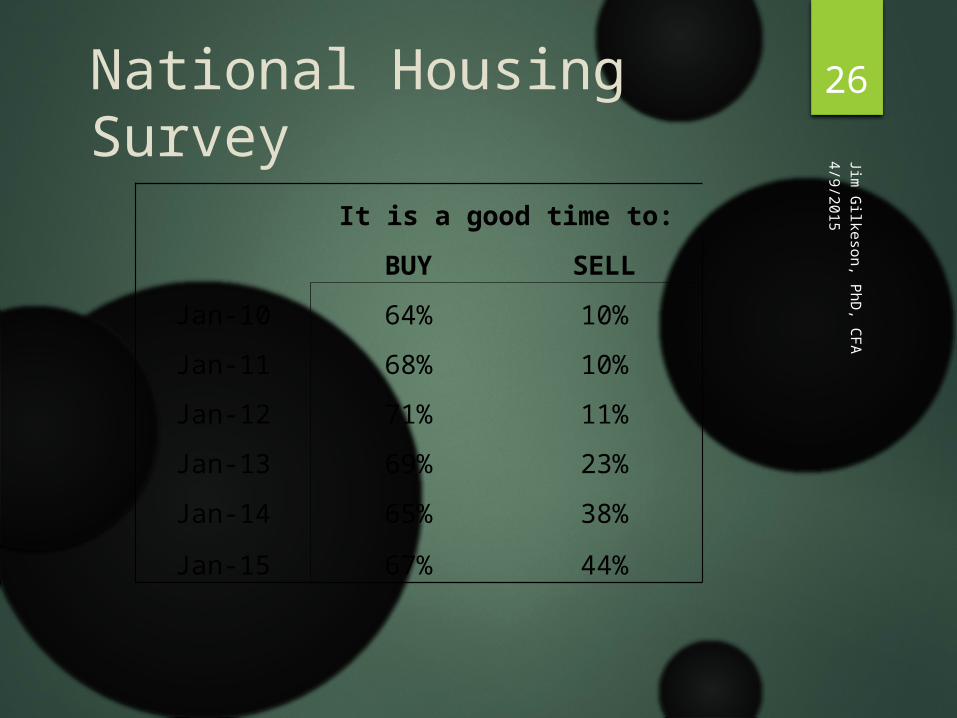

National Housing Survey

It is a good time to:

BUY SELL

Jan-10 64% 10%

Jan-11 68% 10%

Jan-12 71% 11%

Jan-13 69% 23%

Jan-14 65% 38%

Jan-15 67% 44%

Jim G

ilkeson, PhD

, CFA

274/9/2015

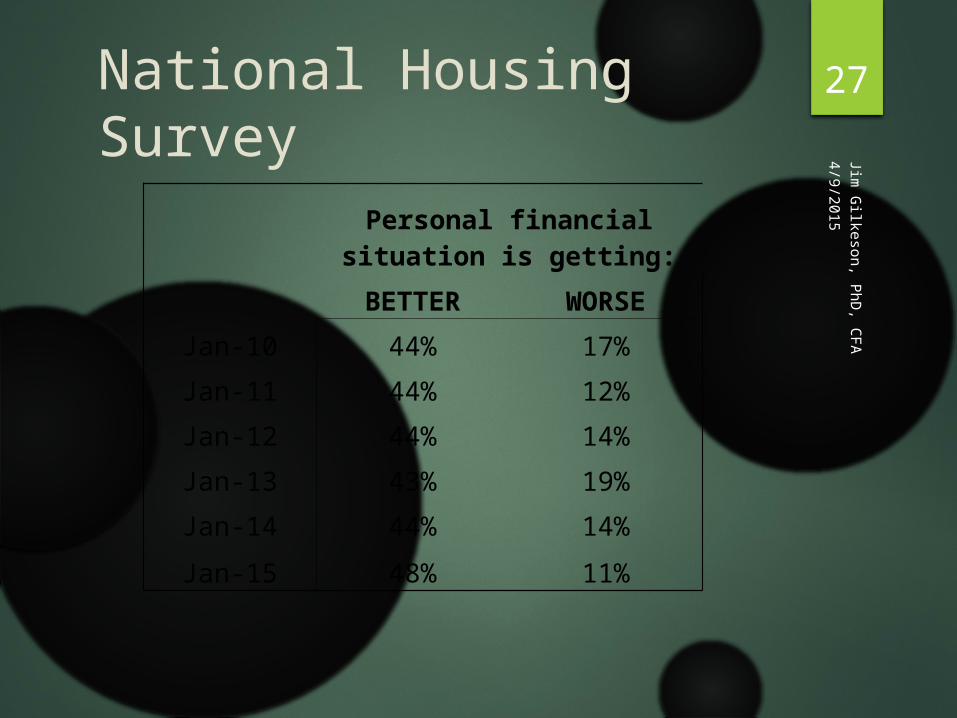

National Housing Survey

Personal financial situation is

getting:

BETTER WORSE

Jan-10 44% 17%

Jan-11 44% 12%

Jan-12 44% 14%

Jan-13 43% 19%

Jan-14 44% 14%

Jan-15 48% 11%

Jim G

ilkeson, PhD

, CFA

284/9/2015

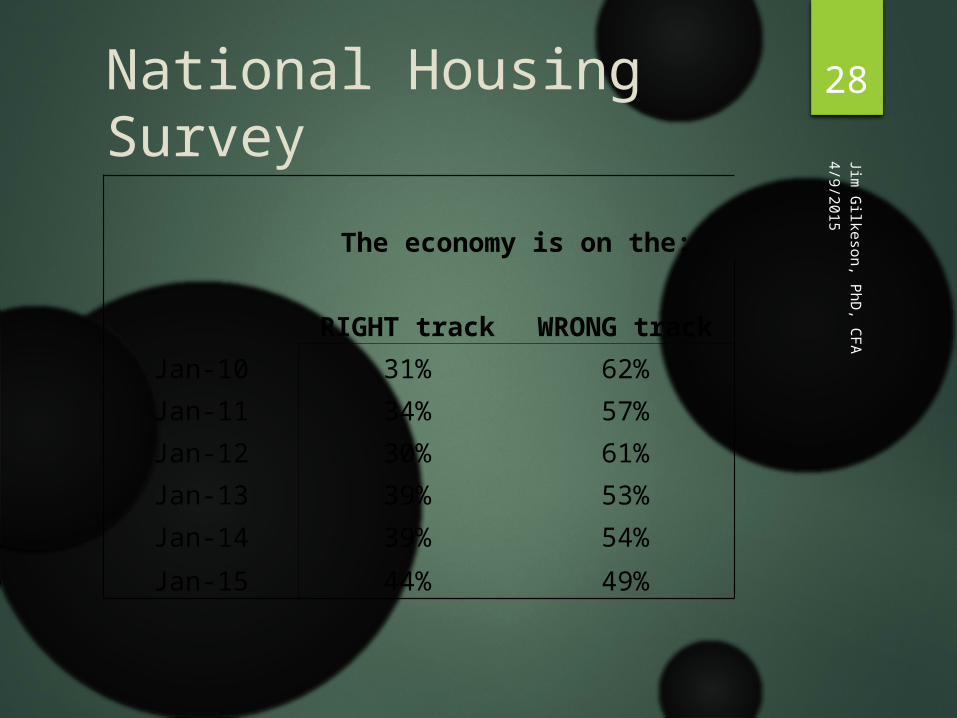

National Housing Survey

The economy is on the:

RIGHT track WRONG track

Jan-10 31% 62%

Jan-11 34% 57%

Jan-12 30% 61%

Jan-13 39% 53%

Jan-14 39% 54%

Jan-15 44% 49%

Jim G

ilkeson, PhD

, CFA

29Wrap Up

National

Housing is affordable

Mortgage rates low

Foreclosures and delinquencies back to normal

New housing starts still half of normal

Confidence is growing but not strong

4/9/2015

Jim G

ilkeson, PhD

, CFA

30Wrap Up

Orlando

Volume stable at peak but prices well below peak

Housing affordable

Population growing again

Starts half of pre-peak normal

Still quite a few problem loans

43% of 2014 sales were cash

4/9/2015