alnoor ebrahim, associate professor, harvard business school kelly mccarthy, senior manager, global...

TRANSCRIPT

Alnoor Ebrahim, Associate Professor, Harvard Business SchoolKelly McCarthy, Senior Manager, Global Impact Investing NetworkDaniel Brown, Doctoral Candidate, Harvard Business School

Correspondence to: [email protected]

The State of Impact Measurement

An update for theSocial Impact Investment TaskforceGuildhall, London, July 9, 2015

At a Glance: G7+1Mobilizing• Convene diverse players

(Canada, France)• Influence legislation (Aus,

Italy, Japan)• Build knowledge base via

investor surveys & academic centers (Aus, Italy, US)

Standardizing• Process guides (Japan,

UK, Germany)• Process/assurance

standards (Germany, UK)

• Outcome standards by industry (France, UK)

• Transparency/reporting (Germany, UK, US) Financing

• Pay for Success/SIBs (Aus, Canada)

• Bank of unclaimed assets (Japan)

• Catalyze philanthropic support (US)

Source: National Advisory Board updates to Social Impact Investment Taskforce (2015)

It is early days (still)…

• Though there is increasing understanding of social impact measurement, the practice is still under development. (Japan)

• [Need] to develop an impact measurement culture before setting impact objectives to measure. (Italy)

• Measurement of impact … continues to vary on a deal-by-deal basis. (Canada)

Source: National Advisory Board updates to Social Impact Investment Taskforce (2015)

I. MethodsII. AdoptionIII. Ecosystem

Guidance (process)

Impact Measurement Working GroupSocial Impact Investment Taskforce (2014)

JP Morgan (2015)

EVPA (2013)

Methods for different stagesEstimating Impactfor due diligence

1 Monitoring Impactto improve program

3 Evaluating Impactto prove social value

4Planning Impactthrough strategy

2

Expected Return

• SROI

Theory of Change

• Logic Model

Mission Alignment

• Social Value Criteria

• Scorecards

Quasi-Experimental & Experimental Methods

• RCT

• Historical baseline

• Pre/post test

• Regression discontinuity design

• Difference in differences

Post-InvestmentPre-ApprovalDue DiligenceProcess Alignment:

Source: Ivy So & Alina Staskevicius, (2015), “Measuring the ‘impact’ in impact investing,” Harvard Business School, MBA independent project. http://www.hbs.edu/socialenterprise/pdf/MeasuringImpact.pdf

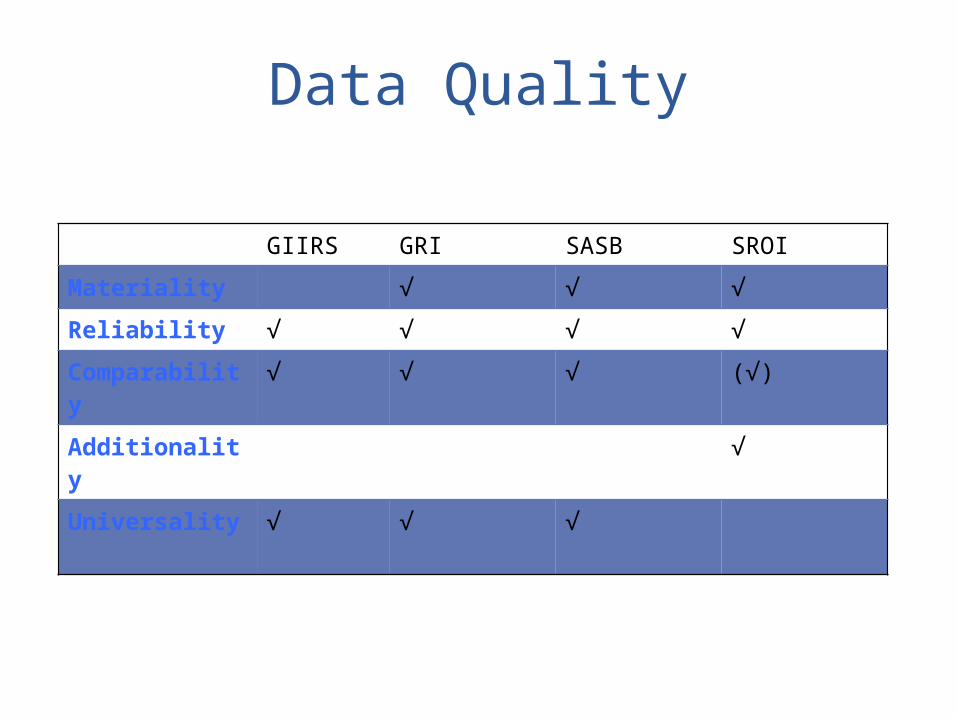

Data Quality

GIIRS GRI SASB SROI

Materiality

Reliability

Comparability

Additionality

Universality

Data Quality

GIIRS GRI SASB SROI

Materiality √ √ √

Reliability √ √ √ √

Comparability

√ √ √ (√)

Additionality √

Universality √ √ √

I. MethodsII. AdoptionIII. Ecosystem

EVPA Guidance Adoption

How social/environmental performance of investees is measured

IRIS Metrics Adoption

So…

Investors appear to be seeking and using general guidance and some standardized metrics

But…

What are they actually measuring?

How are they judging performance?

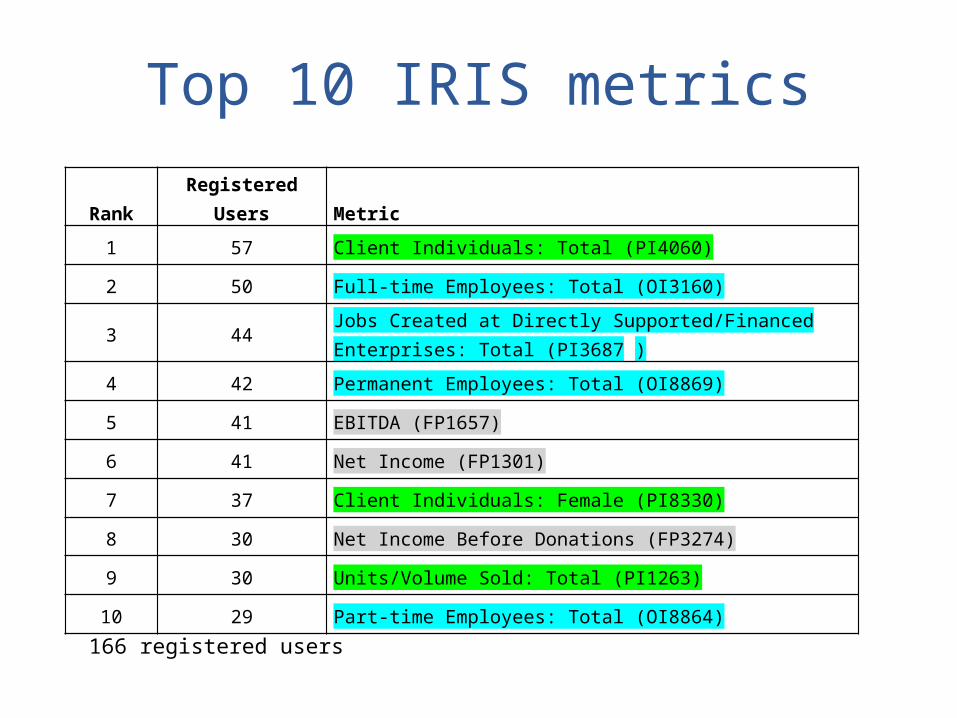

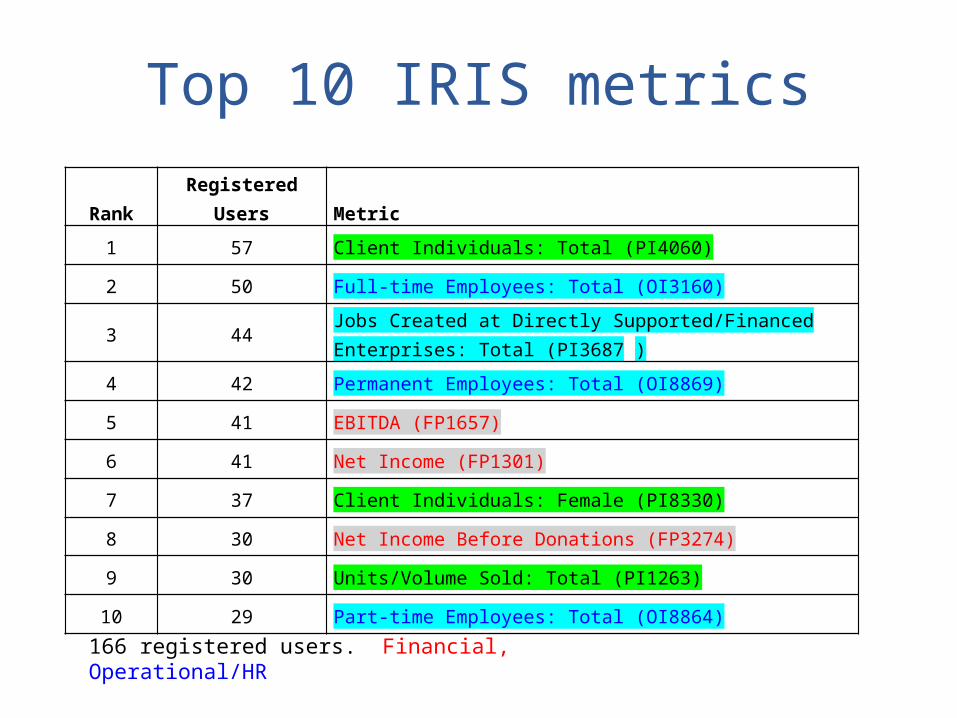

Top 10 IRIS metrics

RankRegistered

Users Metric

1 57 Client Individuals: Total (PI4060)

2 50 Full-time Employees: Total (OI3160)

3 44Jobs Created at Directly Supported/Financed Enterprises: Total (PI3687 )

4 42 Permanent Employees: Total (OI8869)

5 41 EBITDA (FP1657)

6 41 Net Income (FP1301)

7 37 Client Individuals: Female (PI8330)

8 30 Net Income Before Donations (FP3274)

9 30 Units/Volume Sold: Total (PI1263)

10 29 Part-time Employees: Total (OI8864)

166 registered users

Top 10 IRIS metrics

RankRegistered

Users Metric

1 57 Client Individuals: Total (PI4060)

2 50 Full-time Employees: Total (OI3160)

3 44Jobs Created at Directly Supported/Financed Enterprises: Total (PI3687 )

4 42 Permanent Employees: Total (OI8869)

5 41 EBITDA (FP1657)

6 41 Net Income (FP1301)

7 37 Client Individuals: Female (PI8330)

8 30 Net Income Before Donations (FP3274)

9 30 Units/Volume Sold: Total (PI1263)

10 29 Part-time Employees: Total (OI8864)

166 registered users. Financial

Top 10 IRIS metrics

RankRegistered

Users Metric

1 57 Client Individuals: Total (PI4060)

2 50 Full-time Employees: Total (OI3160)

3 44Jobs Created at Directly Supported/Financed Enterprises: Total (PI3687 )

4 42 Permanent Employees: Total (OI8869)

5 41 EBITDA (FP1657)

6 41 Net Income (FP1301)

7 37 Client Individuals: Female (PI8330)

8 30 Net Income Before Donations (FP3274)

9 30 Units/Volume Sold: Total (PI1263)

10 29 Part-time Employees: Total (OI8864)

166 registered users. Financial, Operational/HR

Top 10 IRIS metrics

RankRegistered

Users Metric

1 57 Client Individuals: Total (PI4060)

2 50 Full-time Employees: Total (OI3160)

3 44Jobs Created at Directly Supported/Financed Enterprises: Total (PI3687 )

4 42 Permanent Employees: Total (OI8869)

5 41 EBITDA (FP1657)

6 41 Net Income (FP1301)

7 37 Client Individuals: Female (PI8330)

8 30 Net Income Before Donations (FP3274)

9 30 Units/Volume Sold: Total (PI1263)

10 29 Part-time Employees: Total (OI8864)

166 registered users. Financial, Operational/HR, Social (output)

Top 10 IRIS metrics

RankRegistered

Users Metric

1 57 Client Individuals: Total (PI4060)

2 50 Full-time Employees: Total (OI3160)

3 44Jobs Created at Directly Supported/Financed Enterprises: Total (PI3687 )

4 42 Permanent Employees: Total (OI8869)

5 41 EBITDA (FP1657)

6 41 Net Income (FP1301)

7 37 Client Individuals: Female (PI8330)

8 30 Net Income Before Donations (FP3274)

9 30 Units/Volume Sold: Total (PI1263)

10 29 Part-time Employees: Total (OI8864)

166 registered users. Financial, Operational/HR, Social (output/outcome)

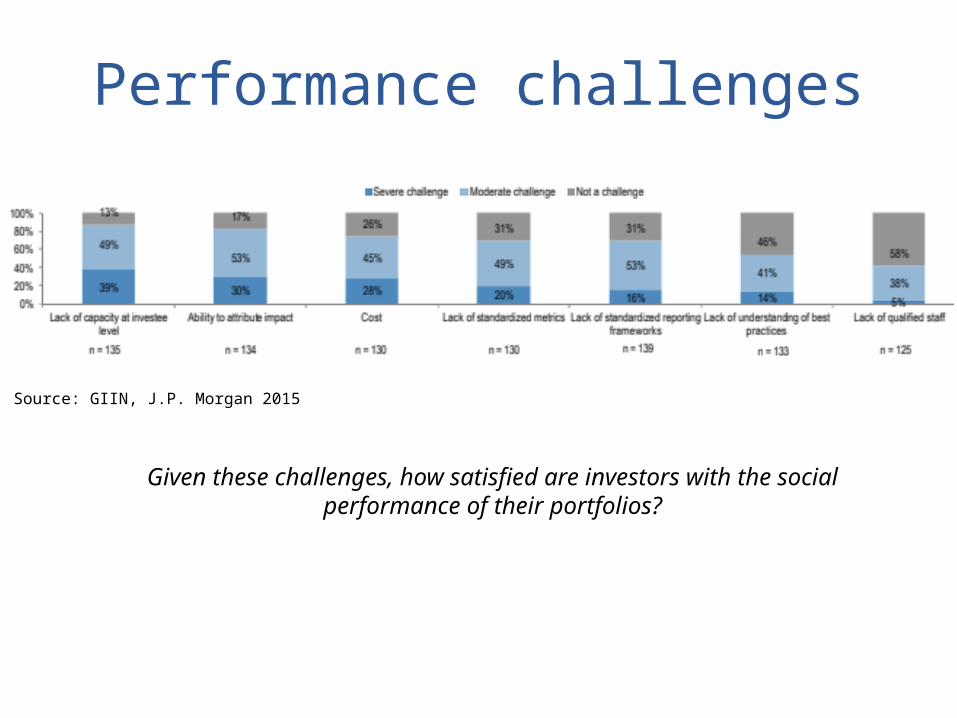

Performance challenges

Source: GIIN, J.P. Morgan 2015

Given these challenges, how satisfied are investors with the social performance of their portfolios?

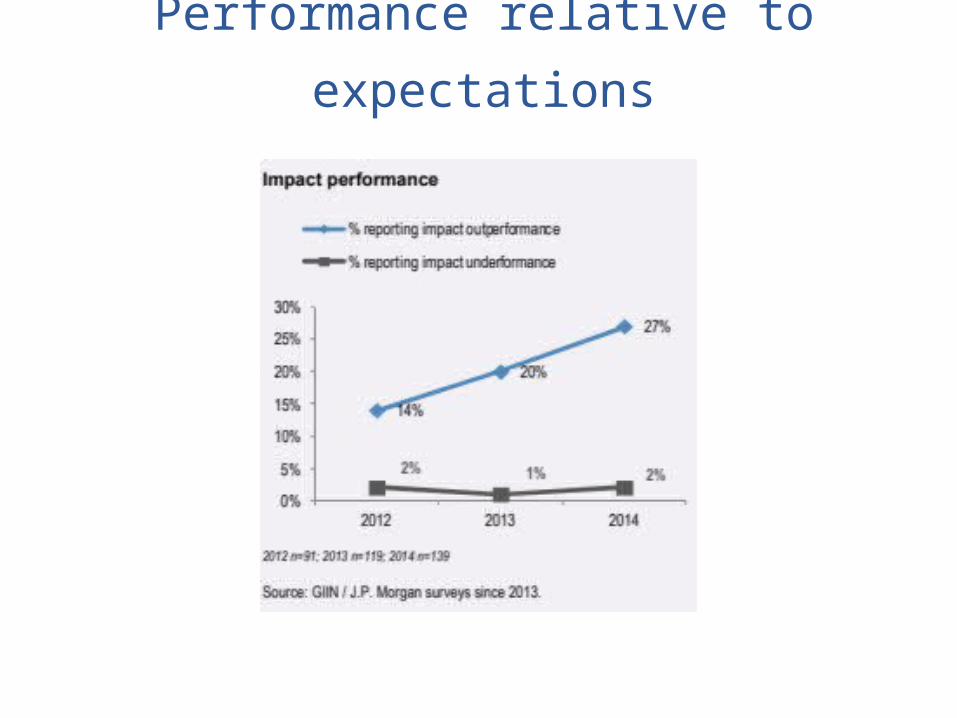

Performance relative to expectations

Measurement ConundrumMany challenges to measuring social impact…

Yet investors are satisfied with social performance!

o Highly idiosyncratic practice; limited convergenceo Little external scrutiny or reporting obligationso Few incentives or demands for systematized information

See: GIIN/J.P. Morgan 2015; EVPA 2014. • Investing for Good, Esmée Fairbairn, Big Society Capital (2015), “Oranges and Lemons.”• New Philanthropy Capital (2014), “Smart Money: Understanding the Impact of Social Investment.”

I. MethodsII. AdoptionIII. Ecosystem

A Growing Ecosystem

Standards & Ratings

Guidance

Metrics

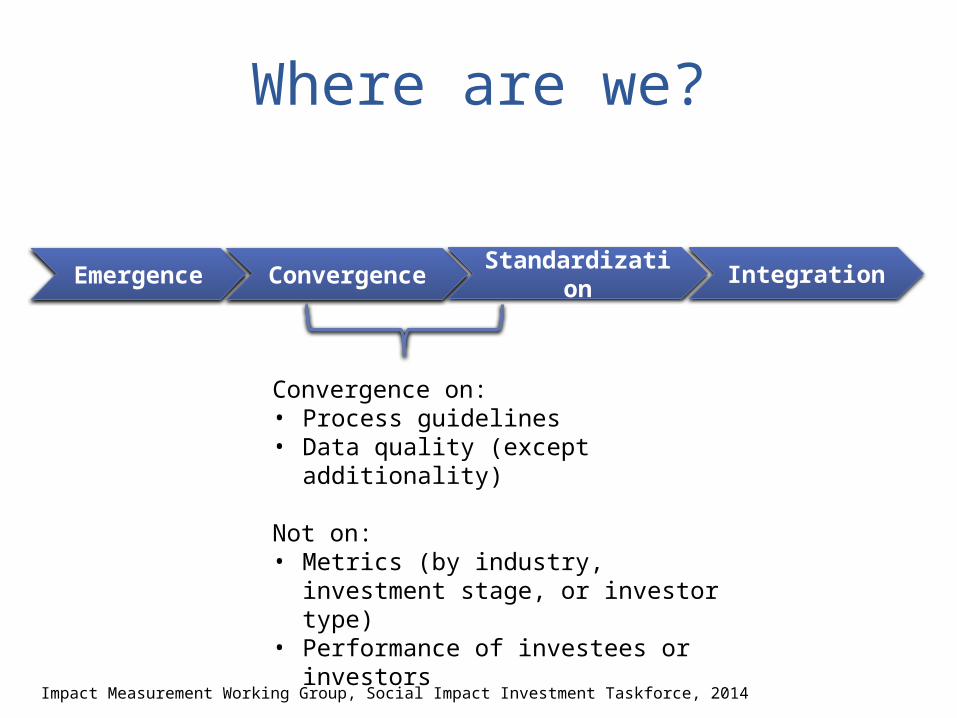

Where are we?

Impact Measurement Working Group, Social Impact Investment Taskforce, 2014

Emergence

Convergence

Standardization

Integration

Convergence on:• Process guidelines• Data quality (except additionality)

Not on:• Metrics (by industry, investment

stage, or investor type)• Performance of investees or

investors