alternative financing

TRANSCRIPT

1

ALTERNATIVE FINANCING

Premiere Date, July 9, 2014

ALTERNATIVE FINANCING: JULY 9, 2014

FINANCIAL POISE, A DIVISION OF DAILYDAC, LLC©2014

Practical and entertaining education for business owners and executives, Accredited Investors, and their legal and

financial advisors.For more information, visit www.financialpoise.com

2

DISCLAIMER: THE MATERIAL IN THIS PRESENTATION IS FOR INFORMATIONAL PURPOSES ONLY. IT SHOULD NOT BE CONSIDERED LEGAL ADVICE. YOU SHOULD CONSULT WITH AN ATTORNEY TO DETERMINE WHAT MAY BE

BEST FOR YOUR INDIVIDUAL NEEDS

FINANCIAL POISE, A DIVISION OF DAILYDAC, LLC©2014

ALTERNATIVE FINANCING: JULY 9, 2014

3

ABOUT THIS EPISODE OF THE SERIES

• Not every company can obtain conventional financing from a bank. Banks like well established companies and vanilla collateral. When you have neither of these and you need money, that is the time to explore alternative financing. This webinar will discuss various types of alternative financing, what to expect and how to find it.

FINANCIAL POISE, A DIVISION OF DAILYDAC, LLC©2014

ALTERNATIVE FINANCING: JULY 9, 2014

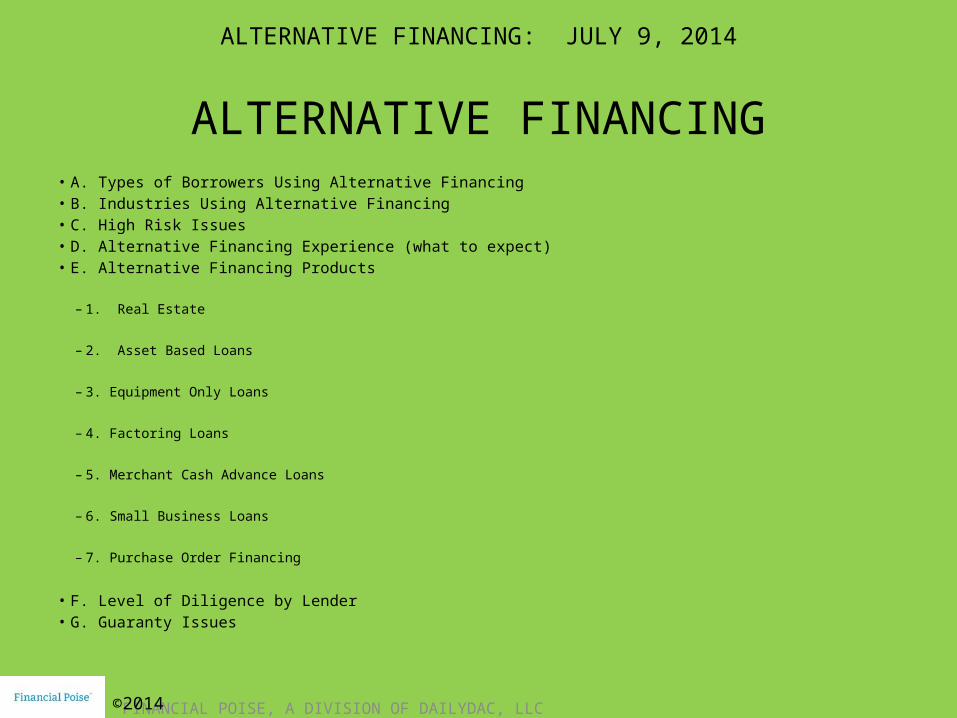

ALTERNATIVE FINANCING• A. Types of Borrowers Using Alternative Financing• B. Industries Using Alternative Financing • C. High Risk Issues• D. Alternative Financing Experience (what to expect)• E. Alternative Financing Products

– 1. Real Estate

– 2. Asset Based Loans

– 3. Equipment Only Loans

– 4. Factoring Loans

– 5. Merchant Cash Advance Loans

– 6. Small Business Loans

– 7. Purchase Order Financing

• F. Level of Diligence by Lender• G. Guaranty Issues

ALTERNATIVE FINANCING: JULY 9, 2014

FINANCIAL POISE, A DIVISION OF DAILYDAC, LLC©2014

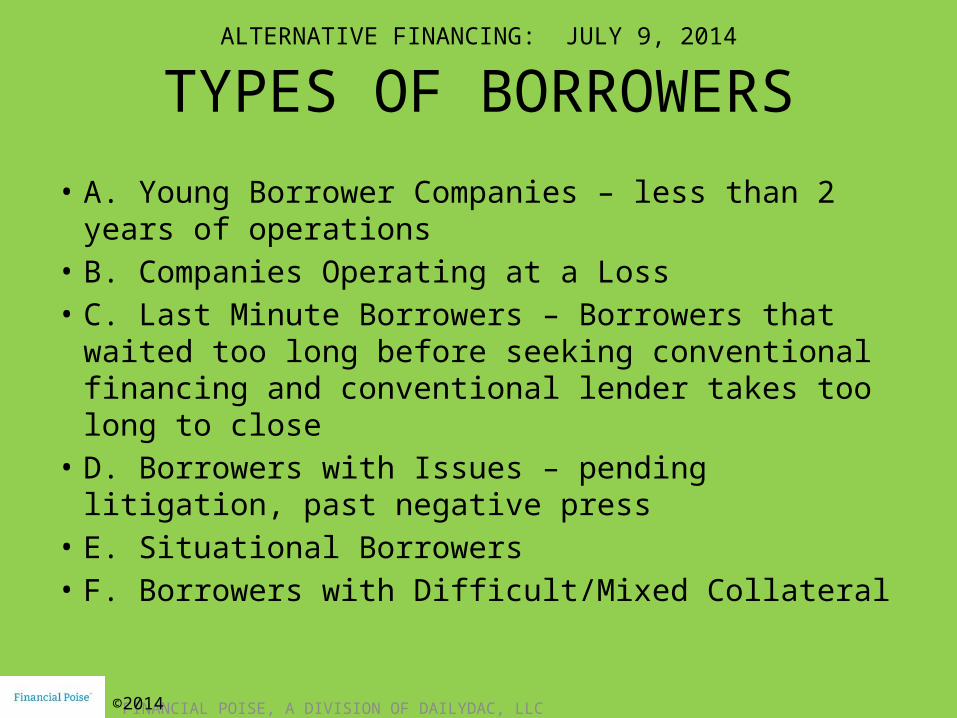

TYPES OF BORROWERS

• A. Young Borrower Companies – less than 2 years of operations

• B. Companies Operating at a Loss • C. Last Minute Borrowers – Borrowers that waited too

long before seeking conventional financing and conventional lender takes too long to close

• D. Borrowers with Issues – pending litigation, past negative press

• E. Situational Borrowers• F. Borrowers with Difficult/Mixed Collateral

ALTERNATIVE FINANCING: JULY 9, 2014

FINANCIAL POISE, A DIVISION OF DAILYDAC, LLC©2014

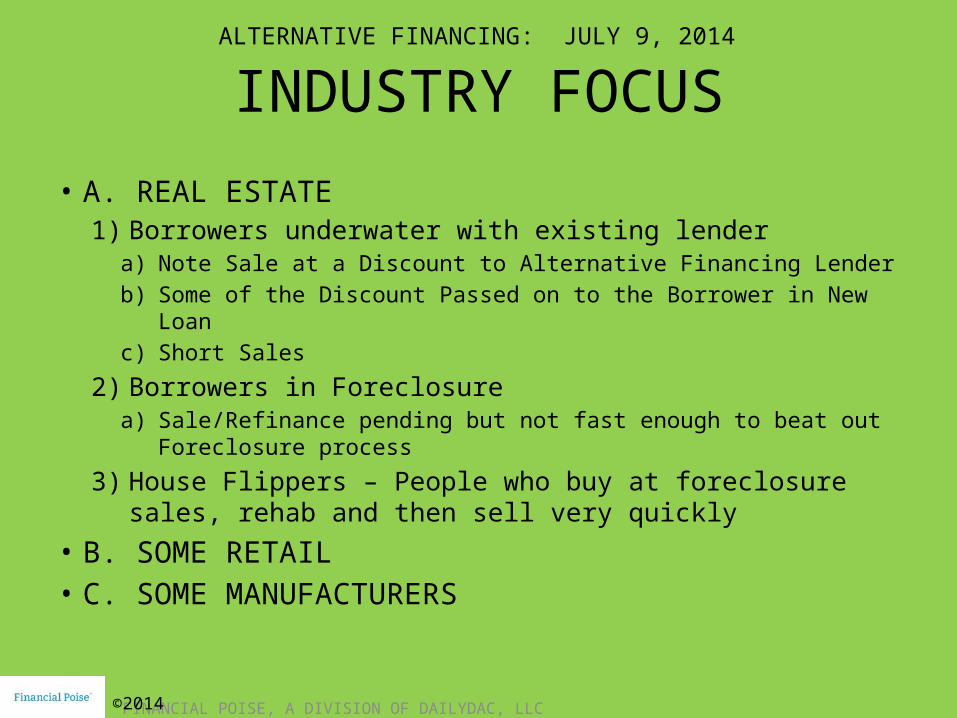

INDUSTRY FOCUS

• A. REAL ESTATE1) Borrowers underwater with existing lender

a) Note Sale at a Discount to Alternative Financing Lenderb) Some of the Discount Passed on to the Borrower in New Loanc) Short Sales

2) Borrowers in Foreclosurea) Sale/Refinance pending but not fast enough to beat out

Foreclosure process

3) House Flippers – People who buy at foreclosure sales, rehab and then sell very quickly

• B. SOME RETAIL• C. SOME MANUFACTURERS

ALTERNATIVE FINANCING: JULY 9, 2014

FINANCIAL POISE, A DIVISION OF DAILYDAC, LLC©2014

7

ALTERNATIVE FINANCING: JULY 9, 2014

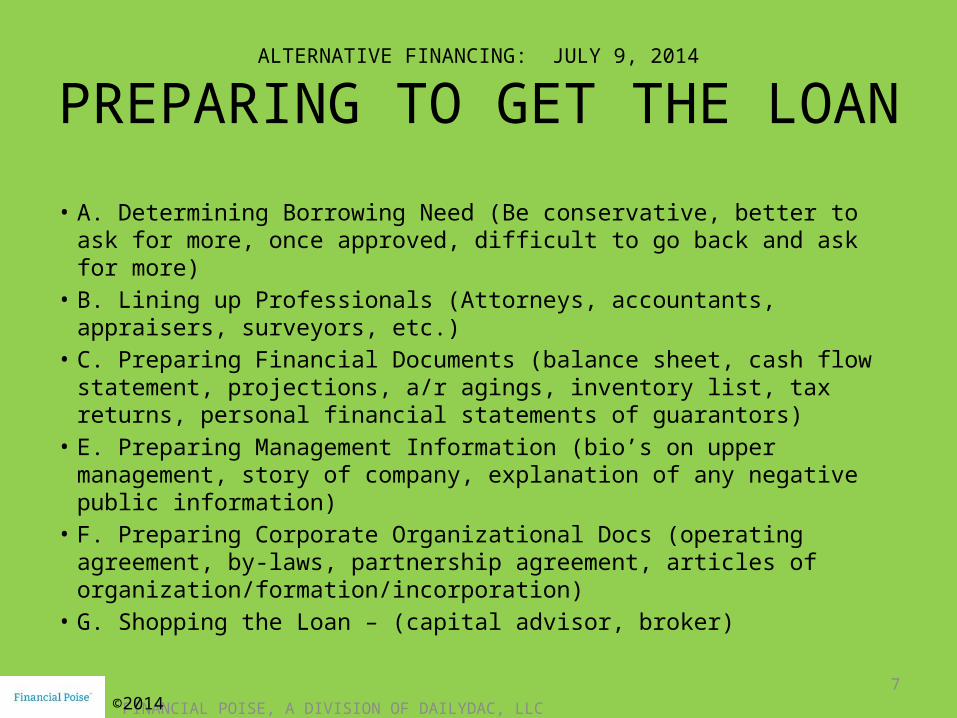

PREPARING TO GET THE LOAN

• A. Determining Borrowing Need (Be conservative, better to ask for more, once approved, difficult to go back and ask for more)

• B. Lining up Professionals (Attorneys, accountants, appraisers, surveyors, etc.)

• C. Preparing Financial Documents (balance sheet, cash flow statement, projections, a/r agings, inventory list, tax returns, personal financial statements of guarantors)

• E. Preparing Management Information (bio’s on upper management, story of company, explanation of any negative public information)

• F. Preparing Corporate Organizational Docs (operating agreement, by-laws, partnership agreement, articles of organization/formation/incorporation)

• G. Shopping the Loan – (capital advisor, broker)

FINANCIAL POISE, A DIVISION OF DAILYDAC, LLC©2014

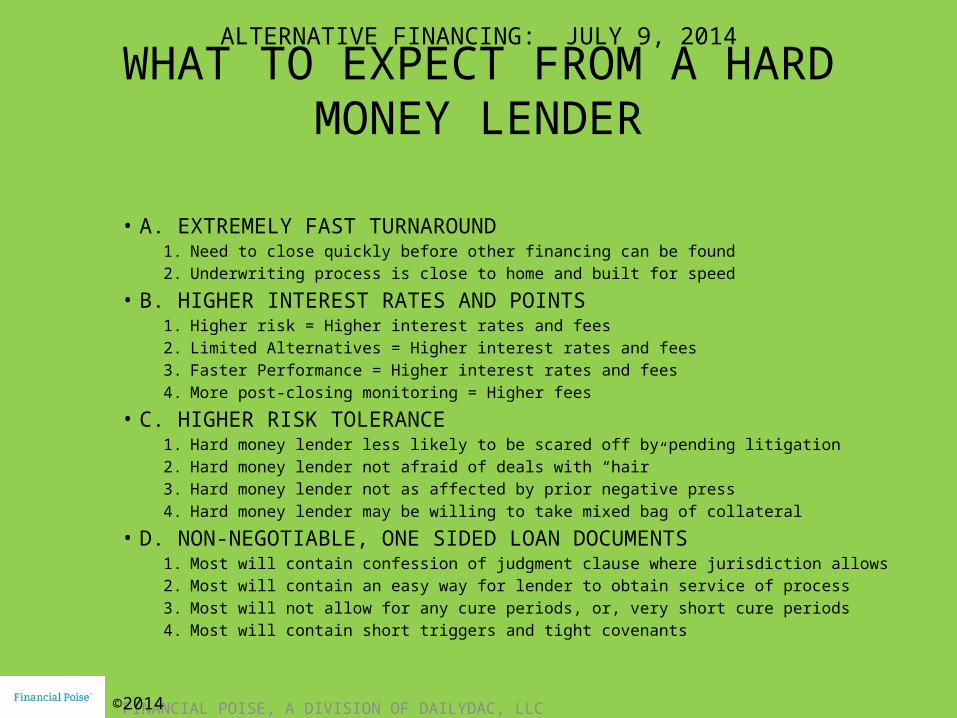

WHAT TO EXPECT FROM A HARD MONEY LENDER

• A. EXTREMELY FAST TURNAROUND1. Need to close quickly before other financing can be found2. Underwriting process is close to home and built for speed

• B. HIGHER INTEREST RATES AND POINTS1. Higher risk = Higher interest rates and fees2. Limited Alternatives = Higher interest rates and fees3. Faster Performance = Higher interest rates and fees4. More post-closing monitoring = Higher fees

• C. HIGHER RISK TOLERANCE1. Hard money lender less likely to be scared off by pending litigation2. Hard money lender not afraid of deals with “hair”3. Hard money lender not as affected by prior negative press4. Hard money lender may be willing to take mixed bag of collateral

• D. NON-NEGOTIABLE, ONE SIDED LOAN DOCUMENTS 1. Most will contain confession of judgment clause where jurisdiction allows2. Most will contain an easy way for lender to obtain service of process3. Most will not allow for any cure periods, or, very short cure periods4. Most will contain short triggers and tight covenants

ALTERNATIVE FINANCING: JULY 9, 2014

FINANCIAL POISE, A DIVISION OF DAILYDAC, LLC©2014

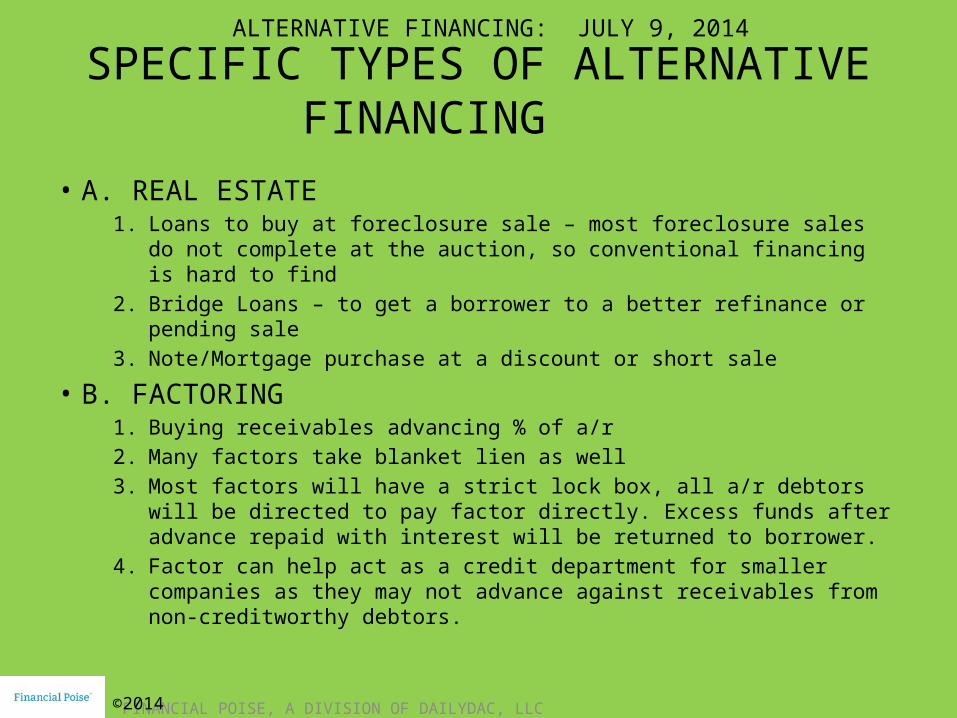

SPECIFIC TYPES OF ALTERNATIVE FINANCING

• A. REAL ESTATE1. Loans to buy at foreclosure sale – most foreclosure sales do not

complete at the auction, so conventional financing is hard to find2. Bridge Loans – to get a borrower to a better refinance or pending sale3. Note/Mortgage purchase at a discount or short sale

• B. FACTORING1. Buying receivables advancing % of a/r2. Many factors take blanket lien as well3. Most factors will have a strict lock box, all a/r debtors will be directed

to pay factor directly. Excess funds after advance repaid with interest will be returned to borrower.

4. Factor can help act as a credit department for smaller companies as they may not advance against receivables from non-creditworthy debtors.

ALTERNATIVE FINANCING: JULY 9, 2014

FINANCIAL POISE, A DIVISION OF DAILYDAC, LLC©2014

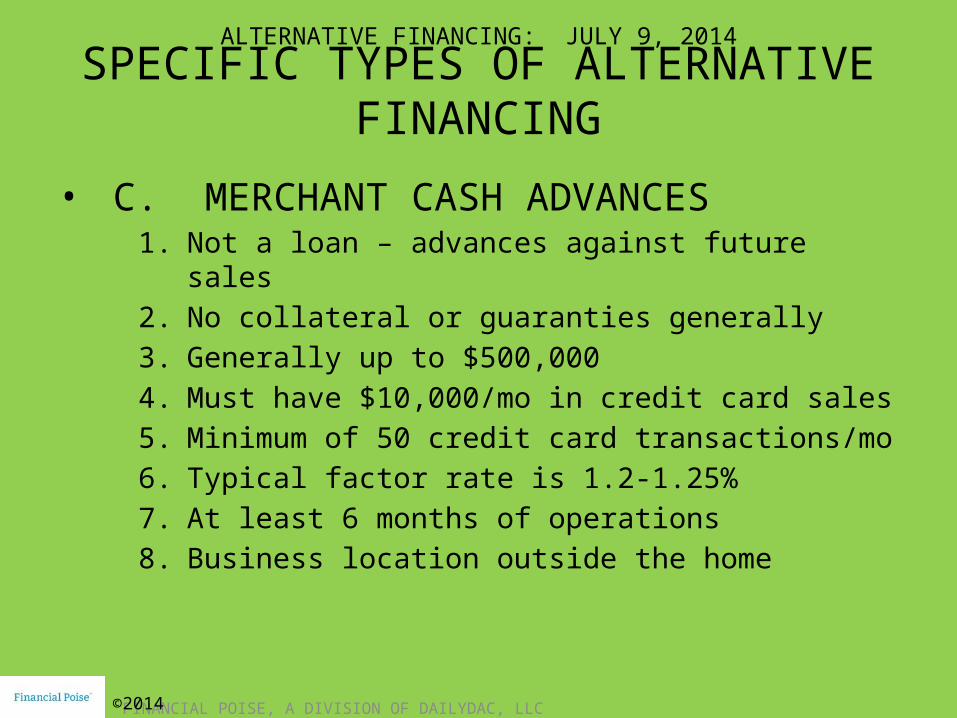

SPECIFIC TYPES OF ALTERNATIVE FINANCING

• C. MERCHANT CASH ADVANCES1. Not a loan – advances against future sales2. No collateral or guaranties generally3. Generally up to $500,0004. Must have $10,000/mo in credit card sales5. Minimum of 50 credit card transactions/mo6. Typical factor rate is 1.2-1.25%7. At least 6 months of operations8. Business location outside the home

ALTERNATIVE FINANCING: JULY 9, 2014

FINANCIAL POISE, A DIVISION OF DAILYDAC, LLC©2014

11

ALTERNATIVE FINANCING: JULY 9, 2014

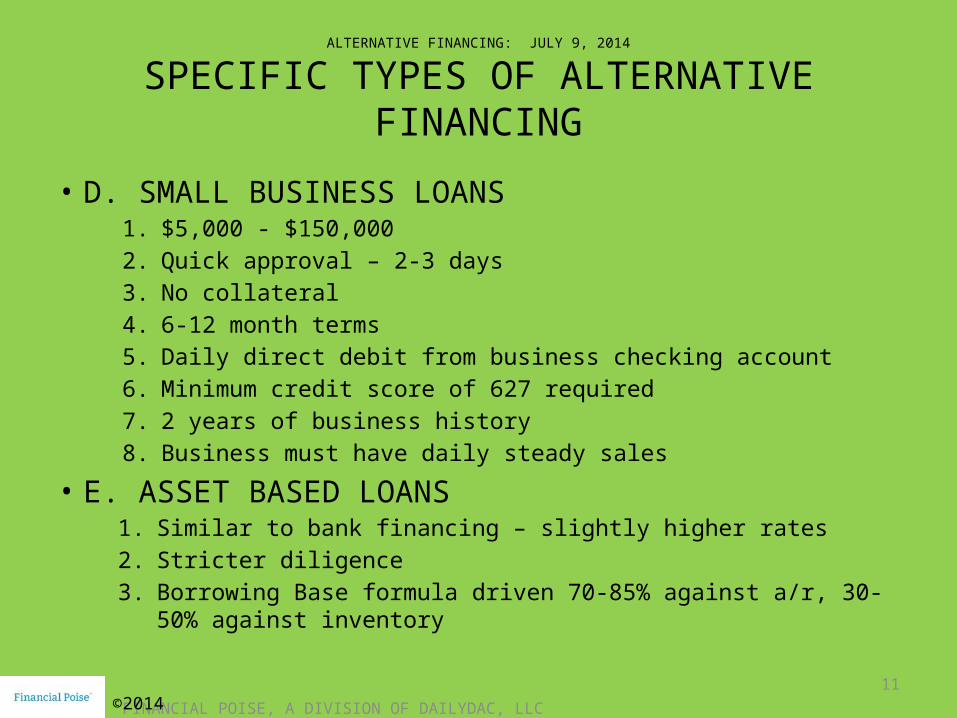

SPECIFIC TYPES OF ALTERNATIVE FINANCING

• D. SMALL BUSINESS LOANS1. $5,000 - $150,0002. Quick approval – 2-3 days3. No collateral4. 6-12 month terms5. Daily direct debit from business checking account6. Minimum credit score of 627 required7. 2 years of business history8. Business must have daily steady sales

• E. ASSET BASED LOANS1. Similar to bank financing – slightly higher rates2. Stricter diligence3. Borrowing Base formula driven 70-85% against a/r, 30-50% against

inventory

FINANCIAL POISE, A DIVISION OF DAILYDAC, LLC©2014

FINANCIAL POISE, A DIVISION OF DAILYDAC, LLC

12

ALTERNATIVE FINANCING: JULY 9, 2014

SPECIFIC TYPES OF ALTERNATIVE FINANCING

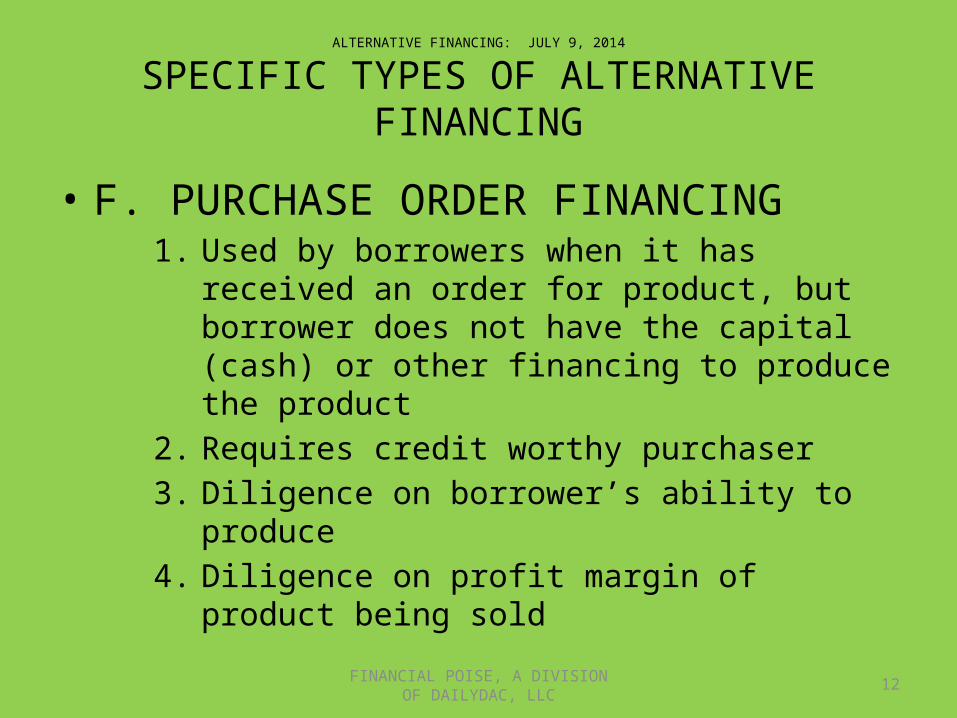

• F. PURCHASE ORDER FINANCING1. Used by borrowers when it has received an order for

product, but borrower does not have the capital (cash) or other financing to produce the product

2. Requires credit worthy purchaser3. Diligence on borrower’s ability to produce4. Diligence on profit margin of product being sold

13

ALTERNATIVE FINANCING: JULY 9, 2014

GUARANTY ISSUES• A. Most hard money loans will require a personal

guaranty• B. Most of the guaranties will contain confession of

judgment clauses if jurisdiction allows• C. A pledge of assets from the guarantor, separate from

all other collateral is also not unusual• D. Some asset based finance companies use “Validity

Guaranties”. Generally speaking, these are guaranties that have the guarantor providing a warranty that each receivable financed is accurate. If it is not accurate, the guarantor will be liable for that amount.

FINANCIAL POISE, A DIVISION OF DAILYDAC, LLC©2014

MORE ABOUT THE FACULTY:

14FINANCIAL POISE, A DIVISION OF DAILYDAC, LLC©2014

NEGOTIATING A LOAN AGREEMENT: JULY 9, 2014

William Schwartz

Bill is a partner in the Banking & Restructuring Group of Levenfeld Pearlstein, and concentrates his practice on representing borrowers and lenders in financial services, litigation (including bankruptcy) and workouts. Bill takes a complete approach to client service. He works to achieve the results his clients want, and in doing so, he also strives to make the experience of working together a positive one. Bill recognizes the time constraints facing his client, and works to reduce the distractions often caused by focusing on the “small picture.” He believes that communicating with your attorney and boredom do not have to be synonymous. As a result, he takes a real interest in his clients and strives to consistently demonstrate that in his frequent interactions. He also represents receivers in foreclosure cases, buyers and sellers at UCC sales, buyers from assignees for the benefit of creditors, and buyers of notes and mortgages. In the last few years, Bill co-authored the chapter “Federal Court Receiverships” in the book Strategic Alternatives for Distressed Businesses (Thompson-West 2012) and an article in Buyouts Magazine entitled “Buying Distressed Assets Outside of Bankruptcy” (Thomson Reuters, June, 2010).

FINANCIAL POISE, A DIVISION OF DAILYDAC, LLC15

©2014

www.financialpoise.com

NEGOTIATING A LOAN AGREEMENT: JULY 9, 2014

16FINANCIAL POISE, A DIVISION OF DAILYDAC, LLC©2014

www.accreditedinvestormarkets.com

NEGOTIATING A LOAN AGREEMENT: JULY 9, 2014

17FINANCIAL POISE, A DIVISION OF DAILYDAC, LLC©2014

www.dailydac.com

NEGOTIATING A LOAN AGREEMENT: JULY 9, 2014