amortised cost

DESCRIPTION

IAS 39 related document explaining the effective interest ratesTRANSCRIPT

Understanding Amortised Cost & Effective interest rate

Learning Outcomes

Amortised CostEffective Interest rateEffective interest methodEffective interest rate ( Examples)Fixed and Floating Interest RateInterest Cap and FloorLIBOR

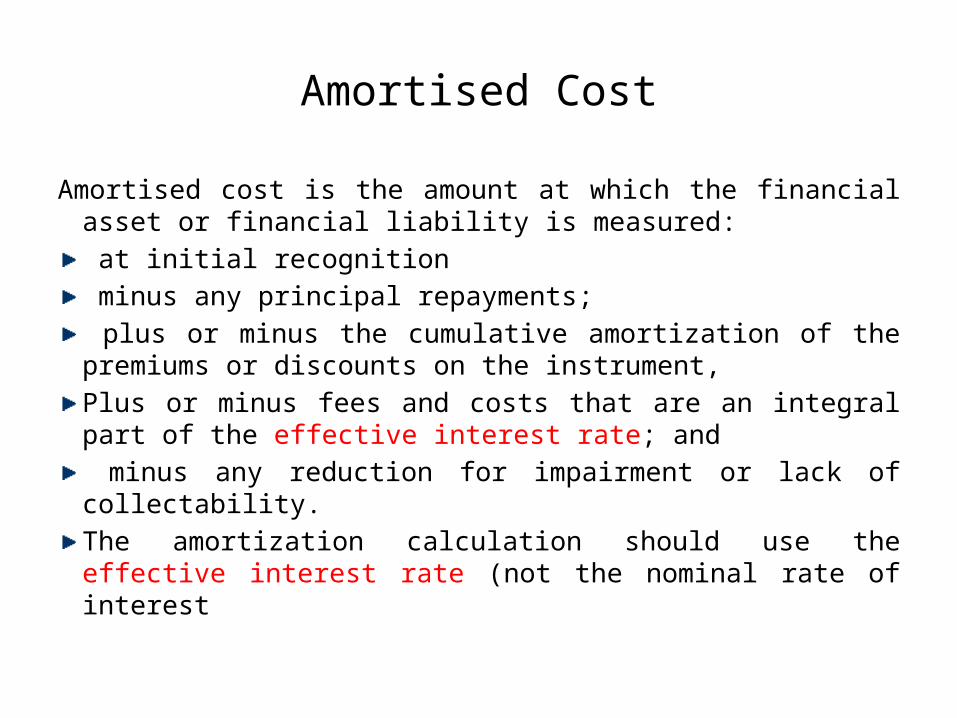

Amortised Cost

Amortised cost is the amount at which the financial asset or financial liability is measured: at initial recognition minus any principal repayments; plus or minus the cumulative amortization of the premiums or discounts on the instrument,Plus or minus fees and costs that are an integral part of the effective interest rate; and minus any reduction for impairment or lack of collectability.The amortization calculation should use the effective interest rate (not the nominal rate of interest

Effective Interest rate

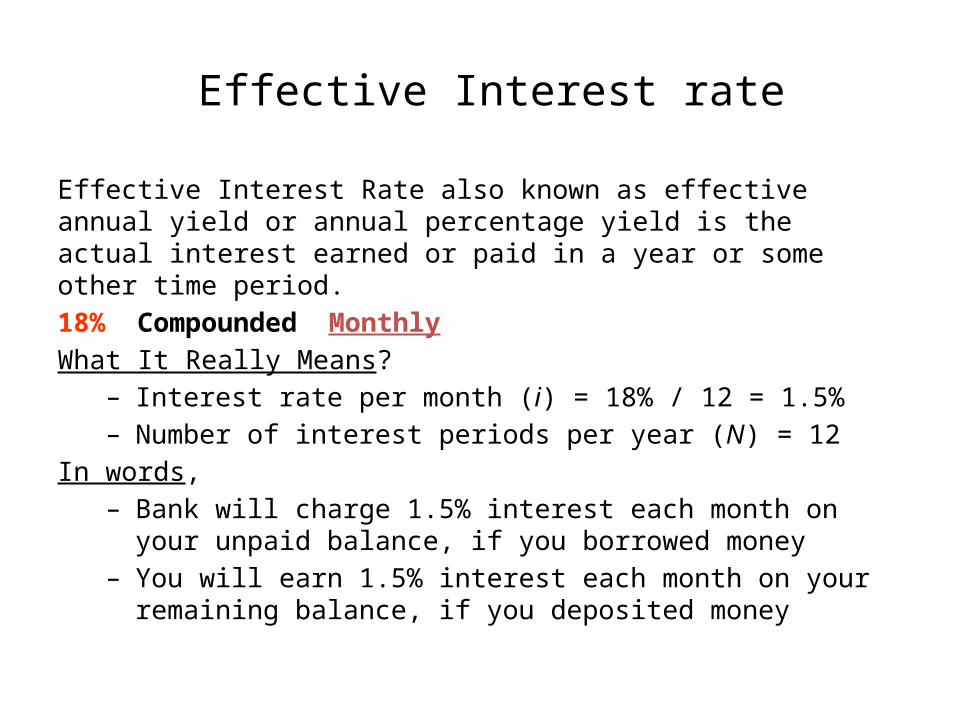

Effective Interest Rate also known as effective annual yield or annual percentage yield is the actual interest earned or paid in a year or some other time period. 18% Compounded MonthlyWhat It Really Means?

– Interest rate per month (i) = 18% / 12 = 1.5%– Number of interest periods per year (N) = 12

In words,– Bank will charge 1.5% interest each month on your unpaid balance, if

you borrowed money – You will earn 1.5% interest each month on your remaining balance, if

you deposited money

Effective Interest rate

Nominal rate- %

Semi-Annual- %

Quarterly- %

Monthly-% Daily-% Continuous-%

1 1.002 1.004 1.005 1.005 1.005

5 5.062 5.095 5.116 5.127 5.127

10 10.250 10.381 10.471 10.516 10.517

15 15.563 15.865 16.075 16.180 16.183

The formula for effective interest rate is:[1 + (i/n)]n - 1

Where:i = the nominal raten = the number of payment periods in one year

Effective Interest rate

For example, if an investor holds a bond that pays a 5% coupon semi-annually, he will actually receive two coupon payments per annum. If the investor reinvests each coupon payment then his effective yield will be greater than the stated coupon rate or nominal yield. Reinvesting the coupon will produce a higher yield, because interest is earned on the interest payments.

The formula for effective yield is:

[1 + (i/n)]n - 1

Where:i = the nominal raten = the number of payment periods in one yearLet's assume you purchase a Company XYZ bond that has a 5% coupon. The nominal rate is 5%.

If the interest is paid semiannually, number of payment periods in one year is two. Using the formula above, we can calculate that the effective yield is:

[1 + (.05/2)]2 - 1 = .05062 or 5.062%

Effective Interest rate

Effective interest rate is a more accurate measure of the investor's return than calculating a simple annual interest rate (the yield for one period times the number of periods in a year) because effective yield takes compounding into account.

However, effective yield also assumes the investor can reinvest their coupon payments at the coupon rate. In our example, this means the investor can reinvest that first coupon payment in another vehicle paying 5%. This is not always possible, especially in a falling interest-rate environment. When it is, the investor can earn interest on interest, thereby raising the investor's yield above the stated coupon rate.

Effective Interest Method in IAS 39

Effective interest method is a method of calculating the amortised cost of a financial asset or financial liability ( or group of financial assets or financial liabilities) and of allocating the interest income or the interest expense over the relevant period. The effective interest rate is the rate that exactly discounts estimated future cash payments or receipts through the expected life of the financial instruments or when appropriate, a shorter period to the net carrying amount of the financial asset or liability.Estimated cash flows shall include prepayment, call or similar options but not future credit losses.Integral part of the effective interest rate shall include all fees, transaction costs, premiums or discounts

Effective Interest Method (cont’d)

Effective interest rate is the rate that discounts the expected future cash flows on the assets to zero. The effective interest is not necessarily equal to the coupon received.

For example, if an instrument is issued at a discount the effective interest rate will take that discount into account, while the coupon received would be based on the contractual interest.

Effective Interest Rate:Actual interest earned or paid in a year or some other time periodEffective interest rate is a special case of IRR

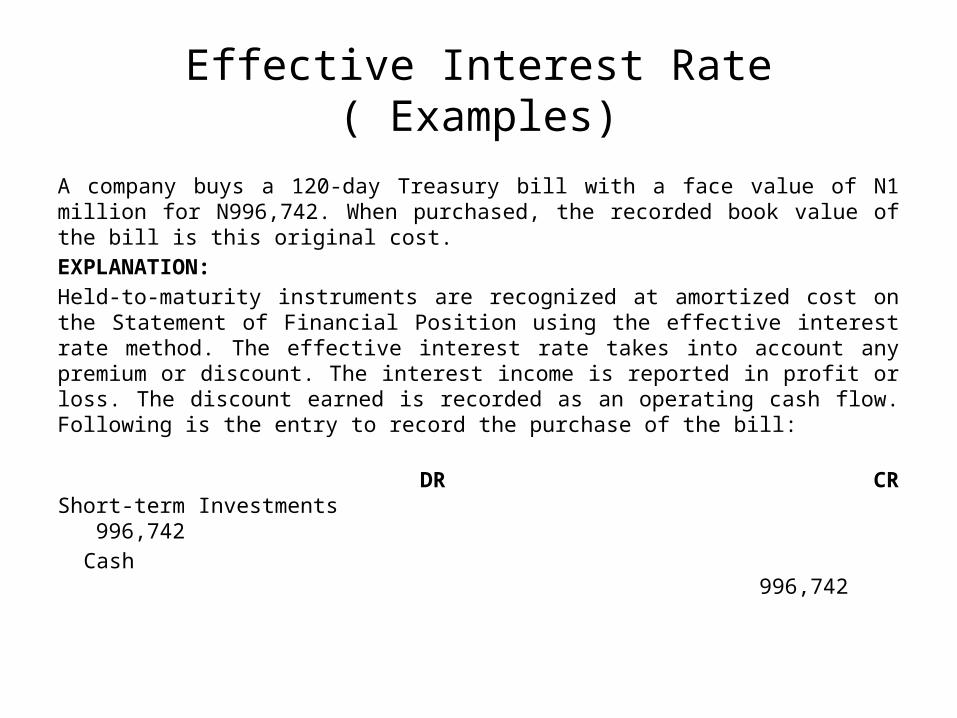

Effective Interest Rate ( Examples)

A company buys a 120-day Treasury bill with a face value of N1 million for N996,742. When purchased, the recorded book value of the bill is this original cost.EXPLANATION:Held-to-maturity instruments are recognized at amortized cost on the Statement of Financial Position using the effective interest rate method. The effective interest rate takes into account any premium or discount. The interest income is reported in profit or loss. The discount earned is recorded as an operating cash flow. Following is the entry to record the purchase of the bill: DR CR Short-term Investments 996,742 Cash 996,742

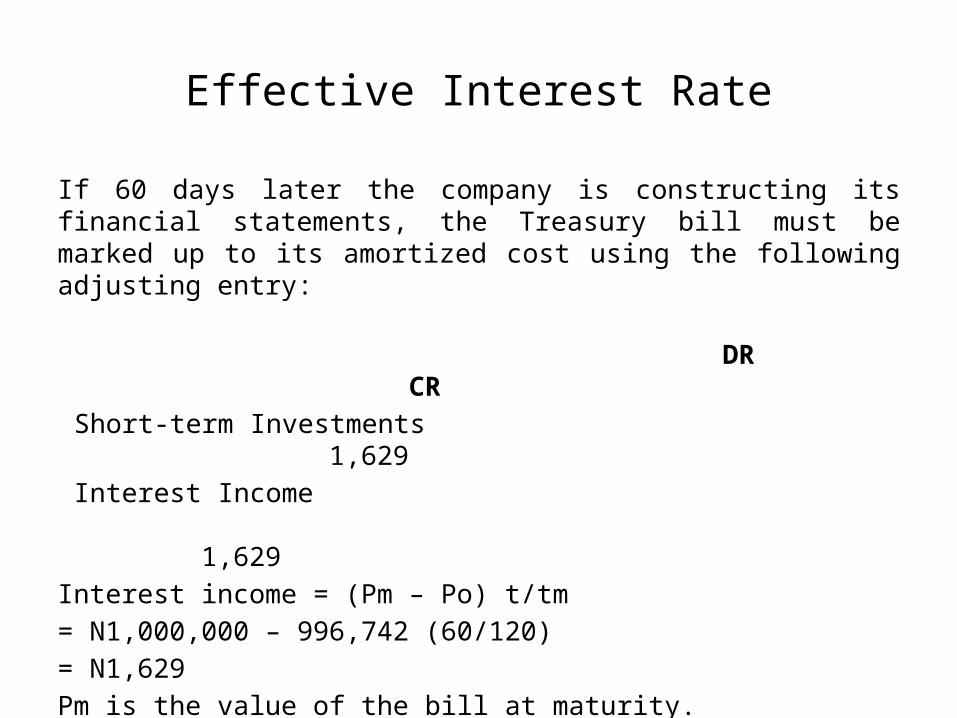

Effective Interest Rate

If 60 days later the company is constructing its financial statements, the Treasury bill must be marked up to its amortized cost using the following adjusting entry: DR CR Short-term Investments 1,629 Interest Income 1,629Interest income = (Pm – Po) t/tm= N1,000,000 – 996,742 (60/120)= N1,629Pm is the value of the bill at maturity.Po is the value of the bill when purchased.t is the number of days the bill has been held.tm is the number of days until the bill matures from when purchased.

Effective Interest Rate

The Treasury bill will be recorded on the Statement of Financial Position as a short-term investment valued at its adjusted cost of N998,371 (N996,742 + N1,629), whereas the N1,629 discount earned will be reported as interest income in profit or loss.When the Treasury bill matures, the entry is as follows: DR CR Cash 1,000,000 Short-term Investments 998,371 Interest Income 1,629**Assumes 60 days of interest on a straight-line basis as an approximation of effective interest rate.

Effective Interest Rate

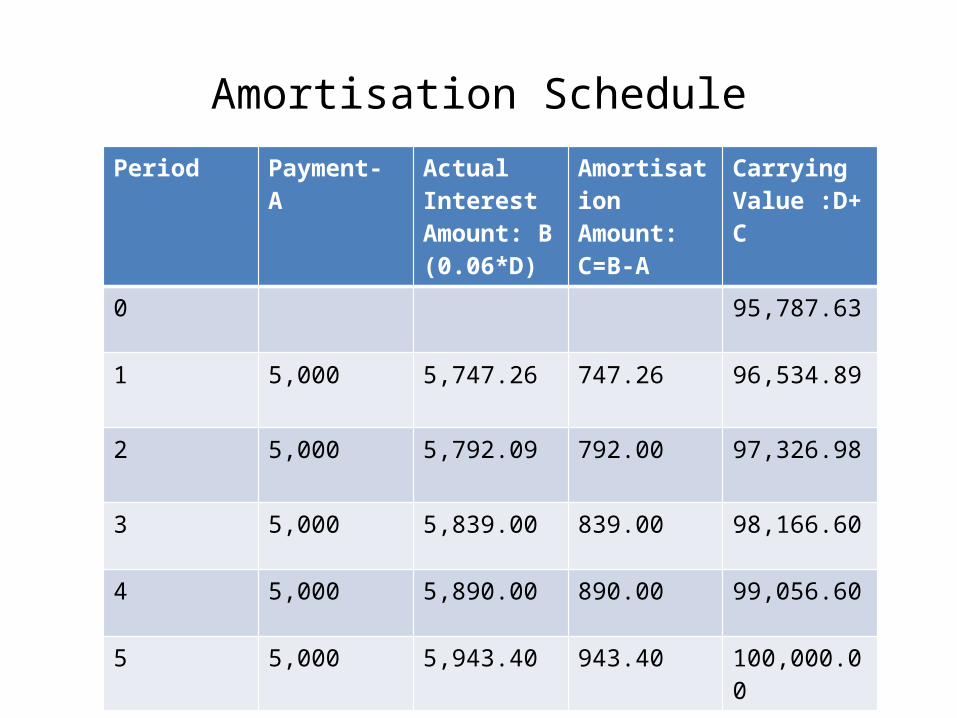

An example: A 5-year bond with a maturity value of N100,000.00, a stated annual interest rate of 5% with annual interest payments of N5,000.00 (5% x N100,000.00) is sold to yield a 6% effective rate. The initial amount of cash changing hands (present value) on the sales date would be N95,787.63 using your NPV and Annuity formula. [(N100,000.00 * 0.74725817) + (N5,000.00 * 4.21236379)] = N95,787.63. The amortization schedule shown below provides proof of the accuracy of the present value.

Calculation of the effective interest rate using the formula: Y = [ 5,000 + ( 100,000.00 – 95,787.63 ) / 5 ] / ( 100,000.00 + 95,787.63 ) / 2 Y = 5,842.474 / 97,893.815 Y = 5.968172669 % Close to effective interest rate of 6.000%

Amortisation SchedulePeriod Payment- A Actual

Interest Amount: B (0.06*D)

Amortisation Amount: C=B-A

Carrying Value :D+C

0 95,787.63

1 5,000 5,747.26 747.26 96,534.89

2 5,000 5,792.09 792.00 97,326.98

3 5,000 5,839.00 839.00 98,166.60

4 5,000 5,890.00 890.00 99,056.60

5 5,000 5,943.40 943.40 100,000.00

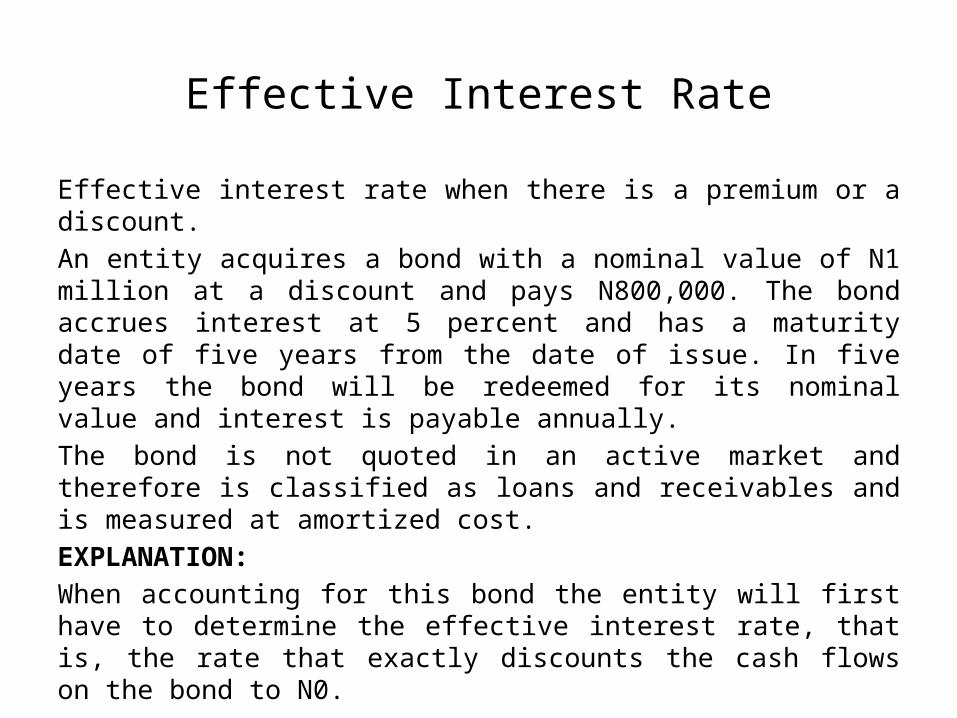

Effective Interest Rate

Effective interest rate when there is a premium or a discount.An entity acquires a bond with a nominal value of N1 million at a discount and pays N800,000. The bond accrues interest at 5 percent and has a maturity date of five years from the date of issue. In five years the bond will be redeemed for its nominal value and interest is payable annually.The bond is not quoted in an active market and therefore is classified as loans and receivables and is measured at amortized cost.EXPLANATION:When accounting for this bond the entity will first have to determine the effective interest rate, that is, the rate that exactly discounts the cash flows on the bond to N0.

Effective Interest Rate

The following cash flows are relevant:Period Cash flow N0 (800,000)1 50,0002 50,0003 50,0004 50,0005 1,050,000

Using an effective interest rate (IRR Formula) of 10.32%

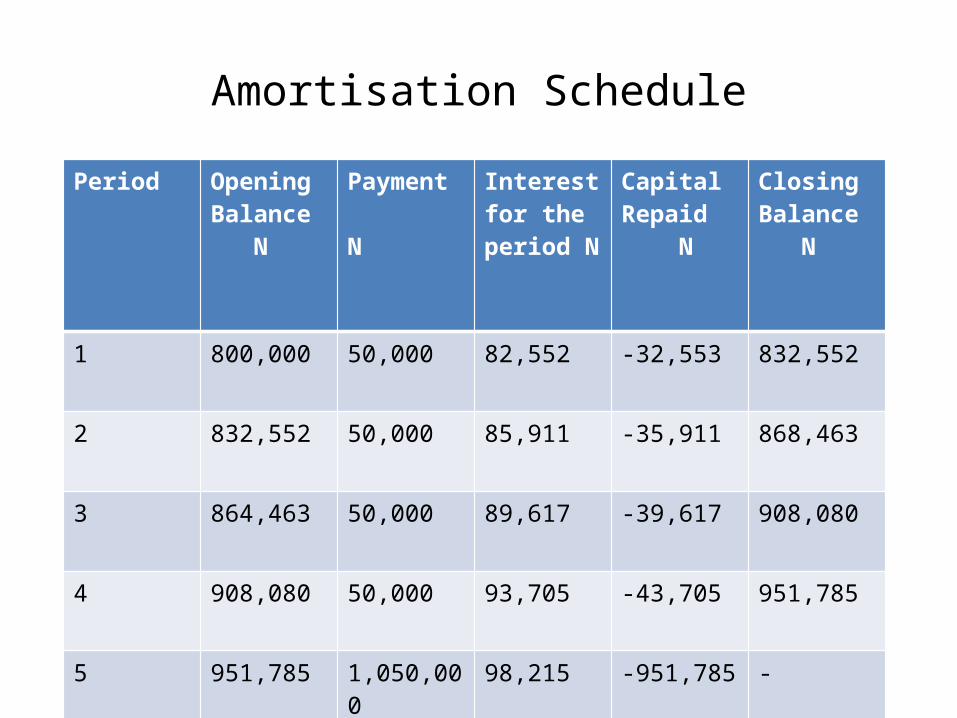

Amortisation Schedule

Period Opening Balance N

Payment

N

Interest for the period N

Capital Repaid N

Closing Balance N

1 800,000 50,000 82,552 -32,553 832,552

2 832,552 50,000 85,911 -35,911 868,463

3 864,463 50,000 89,617 -39,617 908,080

4 908,080 50,000 93,705 -43,705 951,785

5 951,785 1,050,000 98,215 -951,785 -

Effective Interest rate

Therefore the following accounting journals will be recorded at each period:Period 0 DR CR Investment in bond N800,000 Bank N800,000For acquisition of bond

Period 1 DR CR Bank N50,000Investment in bond N32,552Interest income N82,552Recognition of interest earned and received

Effective Interest rate

Period 2 DR CR Bank N50,000 Investment in bond N35,911 Interest income N85,911 Recognition of interest earned and received

Period 3 DR CR Bank N50,000 Investment in bond N39,617 Interest income N89,617Recognition of interest earned and received

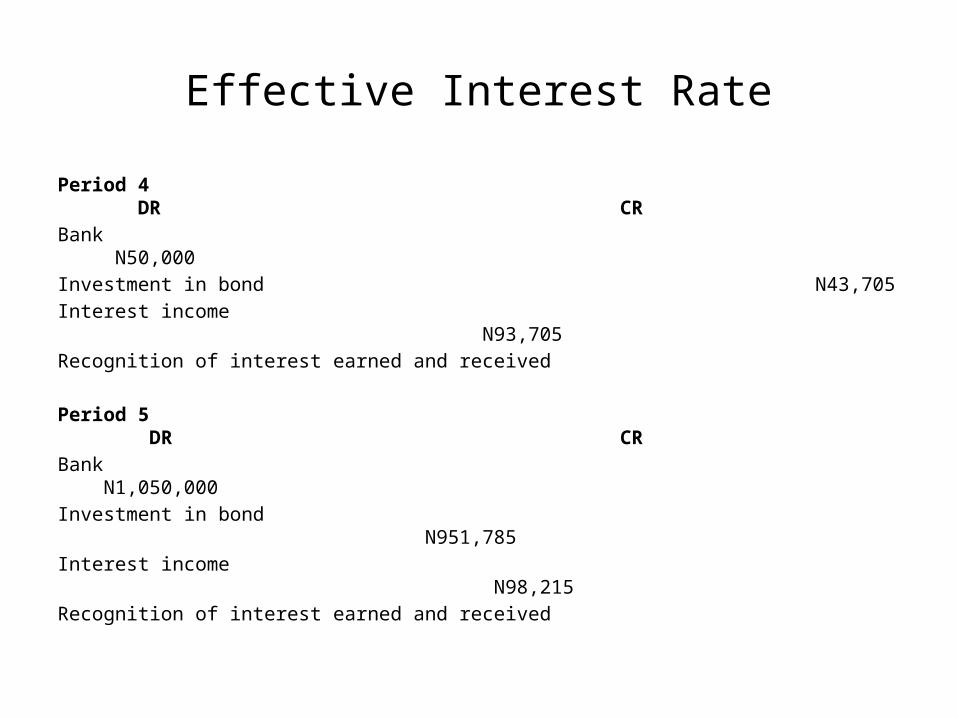

Effective Interest Rate

Period 4 DR CRBank N50,000Investment in bond N43,705Interest income N93,705Recognition of interest earned and received

Period 5 DR CRBank N1,050,000Investment in bond N951,785Interest income N98,215Recognition of interest earned and received

Fixed and Floating interest rate

Fixed interest rate is the rate on a debt obligation or investment that stays constant or static for the duration of the agreement. i.e. A mortgage that has a fixed interest rate of 5% paid annually.

A floating interest rate also known as a variable or adjustable rate, refers to any type of debt instrument such as loan, bond that does not have a fixed rate of interest over the life of the instrument. Such debt typically use an index or other base rate for establishing the interest rate for each relevant period + a certain spread ( difference between the strike price and market value). ( most used one is the LIBOR as base rate) I.e. a five year loan may be priced at six month LIBOR +2.5%, also money market rates are commonly used for commercial loans.

Interest rate cap & floor

An interest rate cap is a derivative(an instrument that receives its return from the return of another underlying asset ) in which the buyer receives payments at the end of each period in which the interest rate exceeds the agreed strike price. An example of a cap would be an agreement to receive a payment for each month the LIBOR rate exceeds 2.5%.

Similarly an interest rate floor is a derivative contract in which the buyer receives payments at the end of each period in which the interest rate is below the agreed strike price ( predetermined price at the inception of the contract).

Caps and floors can be used to hedge against interest rate fluctuations. For example a borrower who is paying the LIBOR rate on a loan can protect himself against a rise in rates by buying a cap at 2.5%. If the interest rate exceeds 2.5% in a given period the payment received from the derivative can be used to help make the interest payment for that period, thus the interest payments are effectively "capped" at 2.5% from the borrowers point of view.

Interest rate cap & floor

Interest rate options are widely used to either speculate on the future course of interest rates or to hedge the interest payments or receipts on an underlying position. This interest rate options allow an investor to benefit from changes in interest rates while also limiting any downside losses. Hence, like all options they provide insurance.

Interest rate cap is a limit on the maximum interest rate or maximum change in the interest rate allowable. An interest rate collar combines the effect of both interest rate cap and floor

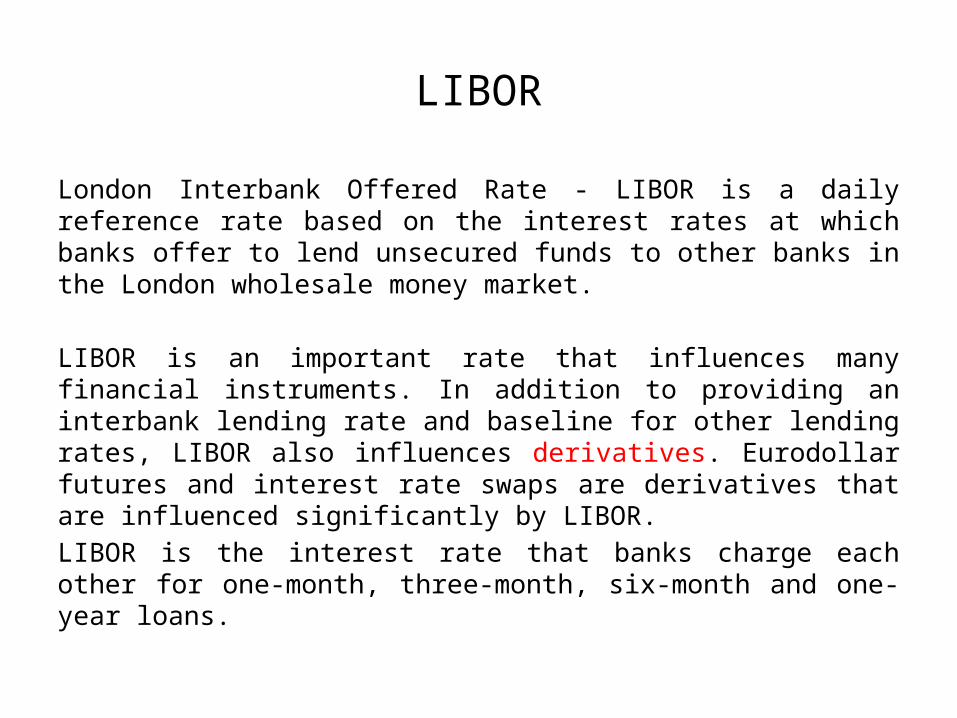

LIBOR

London Interbank Offered Rate - LIBOR is a daily reference rate based on the interest rates at which banks offer to lend unsecured funds to other banks in the London wholesale money market.

LIBOR is an important rate that influences many financial instruments. In addition to providing an interbank lending rate and baseline for other lending rates, LIBOR also influences derivatives. Eurodollar futures and interest rate swaps are derivatives that are influenced significantly by LIBOR.LIBOR is the interest rate that banks charge each other for one-month, three-month, six-month and one-year loans.

Teasers

Give two examples of financial instrument measured at amortised costOther names for effective interest rate is what?What makes effective interest rate different from nominal interest rate?Interest rate cap and floor are examples of what activities ?Can future losses be included in the calculation of effective interest rate?What is a strike Price?What is the full meaning of LIBOR?