an audit on non current assets of pakistan cables

TRANSCRIPT

1

“An Audit of Non-Current

Assets of Pakistan Cables”

2

Table of Contents Introduction of Pakistan Cables ...................................................................................................... 4

Founder of Pakistan Cables ............................................................................................................ 5

Background of Pakistan Cables ...................................................................................................... 6

Vision Statement of Pakistan Cables .............................................................................................. 7

Mission Statement of Pakistan Cables ............................................................................................ 7

Factors Considered Before Accepting the New Audit Client ......................................................... 8

Type Of Business ........................................................................................................................ 8

Industry ....................................................................................................................................... 8

Expertise ..................................................................................................................................... 8

Scope of Audit ............................................................................................................................ 8

Fees ............................................................................................................................................. 9

Contact with KPMG ................................................................................................................... 9

Information Source ..................................................................................................................... 9

Appointment Procedure .............................................................................................................. 9

Audit Engagement Letter .............................................................................................................. 10

Internal Control System ................................................................................................................ 13

Approval Process for Capital Expenditure ............................................................................... 13

Estimation ................................................................................................................................. 13

If Capitalize Expense On Which Basis ..................................................................................... 13

Valuation of an asset ................................................................................................................. 13

Insurance Coverage ................................................................................................................... 14

Audit Methodology to Gather Audit Evidence and Assertions .................................................... 14

Property Plant and Equipment .................................................................................................. 14

Leasehold land ...................................................................................................................... 14

3

Leasehold Building ............................................................................................................... 15

Leasehold improvement ........................................................................................................ 16

Machinery ............................................................................................................................. 16

Office Equipment and Appliances ........................................................................................ 17

Vehicle .................................................................................................................................. 18

Furniture and Fittings ............................................................................................................ 19

Loose Tools ........................................................................................................................... 20

Long Term Loans .................................................................................................................. 20

Investment in Associates....................................................................................................... 21

Audit Report.................................................................................................................................. 23

Balance Sheet and Notes to the Accounts..................................................................................... 24

4

Introduction of Pakistan Cables

Pakistan Cables, the country's oldest and most reputable cable manufacturer, was established

over 5 decades ago in 1953 under the sponsorship of BICC, UK and the Chinoy family. In the

subsequent five decades, Pakistan Cables has earned a reputation as a market leader in the

industry and a company that does not compromise on quality. Consequently, the company has

gained a position as being the premier cable manufacturer in the country. Pakistan Cables has

been listed on the Karachi Stock Exchange since 1955. In 2010 General Cable Corporation, a

Fortune 500 company and global leader in cable manufacturing invested in Pakistan Cables by

taking up a 25% equity stake in the company. Pakistan Cables' manufacturing facilities and head

office are located in Karachi on an 11.5 acre site. This site also houses a 2MW co-generation

power plant, which allows the company to be self-reliant for its electricity needs. Pakistan Cables

presently employs over 400 people. It has regional office in Lahore and branch offices in

Rawalpindi, Multan, Abbottabad, Peshawar and Quetta. The company's distribution network

covers more than 55 cities and towns all over Pakistan. Pakistan Cables is engaged in the

manufacture of wires, cables and conductors in both copper and aluminum. In addition, Pakistan

Cables also produces aluminum sections for architectural applications under the brand name of

Alum-Ex. The company has two other product lines, namely PVC Compound and Copper Rod.

Given its focus on quality, Pakistan Cables continuously reviews and improves the effectiveness

of its Quality Management System in line with objectives of achieving higher productivity,

uncompromising quality and maximum customer satisfaction. Pakistan Cables was the first cable

manufacturer and amongst the first 5 companies in Pakistan to be ISO 9001 certified. It has

recently updated its certification to the ISO 9001:2008 version.

Pakistan Cables Limited is the country’s oldest cables manufacturer engaged in manufacturing of

wires and cables and other engineering products.

The Company was established in 1953 in collaboration with BICC, United Kingdom.

The Company manufactures General Wiring Cables in the range of 250/750 volts. These cables

manufactured in conformity with national and international standards that provides safety and

saving in electricity consumption because of the use of pure copper and cable grade PVC (Plastic

Compound Vanile).

5

The Company provides overhead conductors to the utility companies WAPDA and KESC which

are manufactured from EC grade Aluminum Rod and Copper Rod.

PCL also manufactures telephone, intercom, coaxial cables and various types of special cables

which include air field lighting, control cables, etc.

Alum-Ex is the brand name under which Pakistan Cables manufactures aluminum sections for

the construction and architectural industry.

PCL has also set up a plant to manufacture High Conductivity Oxygen Free 8mm Copper Rod.

In 2010 / 11, Pakistan Cables had a total turnover of USD 46 million. The Company has been a

regular winner of the Karachi Stock Exchange’s Top 25 Companies Award, most recently

winning the award in 2004, 2006 & 2007. Pakistan Cables has also been recognized as a winner

of the Brands of the Year Award in 2007 & 2008. Protecting the health and safety of our people

and ensuring a healthy working environment is also of great importance to Pakistan Cables. The

Company is committed to working towards designing a workplace that minimizes work related

risks and occupational health and safety. Pakistan Cables also lays great stress on environment

protection. Plant operations are strictly controlled to maintain safe environment for workers, as

well as the surrounding community. Several measures have been taken to control pollution and

to maintain a clean, green and healthy environment. Pakistan Cables has also achieved in January

2011 certification for its HSE Management Systems conforming to ISO 14001:2004 EMS and

OHSAS 18001:2007.

Founder of Pakistan Cables

Mr. Amir. S. Chinoy is the founder of Pakistan cables limited. He was born in Bombay on 21st

September 1921. He migrated to Pakistan in 1948. He played a pioneering role in the

industrialization of Pakistan by introducing and establishing concerns in heavy chemicals (Pak

Chemical Limited), electrical cables (Pakistan Cables Limited) and galvanized steel pipes

(International Industries Limited). His commercial interests also extended to trading

(representing major European and American companies), contracting and distribution.

6

Mr. Amir S. Chinoy was president of Sind Club (1973 ~ 75), Rotary Club (1968 ~ 69) and

Steward of the Karachi and Lahore Race Clubs. In his lifetime, he also wrote a book “The

Chinoys”. He passed away peacefully on 23rd Ramazan 1418.

Background of Pakistan Cables

Pakistan Cables history can be traced back to the early 20th Century with the formation of F.M.

Chinoy & Co. In 1904 F.M. Chinoy & Co. were appointed the sole agency for Shell Petrol in

India and by 1916 F.M. Chinoy & Co. had obtained the agency for Chevrolet. F.M. Chinoy &

Co. eventually expanded to include agencies for Armstrong Siddeley, Oakland, Pontiac,

Lanchester and Vauxhall. During this period F.M. Chinoy & Co. began operating The Bombay

Garage in Bombay and in a short span of time The Bombay Garage’s footprint expanded to

cover most of India.

After the Independence of Pakistan in August 1947, the founder of Pakistan Cables, Mr. Amir S.

Chinoy migrated across to Karachi. He established a number of businesses following his

migration, including Pak Chemicals, International Industries and Pakistan Cables.

Pakistan Cables, the country’s oldest and most reputable cable manufacturer, was established

over 5 decades ago in 1953 as a joint venture with BICC. In the subsequent six decades,

Pakistan Cables has earned a reputation as a market leader and premier cable manufacturer in the

country and a company that does not compromise on quality. Pakistan Cables has been listed on

the Karachi Stock Exchange since 1955. In 2010 General Cable Corporation, a Fortune 500

company and global leader in cable manufacturing invested in Pakistan Cables by taking up a

25% equity stake in the company.

Pakistan Cables is an affiliate of General Cable, which is amongst the world’s largest cable

companies with revenue in 2011 of USD 5.8 billion. General Cable has a global presence with

57 plants in 26 countries including the US, Canada, France, Germany, Spain, Brazil, China,

Thailand, South Africa, and the Philippines.

The affiliation with General Cable gives Pakistan Cables several advantages over its competitors,

including the ability to source almost any type of cable for customers, access to cutting edge

7

technology, technical support & management best practices, procurement advantages and export

opportunities. Hence Pakistan Cables is the only cable company in Pakistan with multinational

affiliation and product quality to match the best in the world.

Vision Statement of Pakistan Cables

The vision of Pakistan cable is to be the company of first choice for the customers and partners

for wire, cables and other engineering products. Pakistan cables vision is to be the best cables

and wires manufacturer and also remain best in the aluminum section/profiles. Pakistan cables

set up a plant to manufacture high conductivity oxygen free 8mm copper rod.

Mission Statement of Pakistan Cables

Pakistan cables mission statement is to strengthen company leadership in manufacturing and

marketing of wire and cables. To have a strong presence in engineering products market while,

retaining the options to participate in other profitable business.

Pakistan cables achieving consistent, long term financial growth and profitability for its

shareholders. The growth of the company and shares its success.

Pakistan cables is to operate ethically while maximizing profits and satisfying customers “need

and stakeholders” interest.

The mission of Pakistan cables is also to assist in the socio-economic development of Pakistan

by being good corporate citizens. Pakistan cables is taking a long-term view of business

relationships. It is practicing the highest standards of integrity and professionalism.

8

Factors Considered Before Accepting the New Audit Client

In this we will discuss the factors which we have to consider before going to a new client for

audit. The factors which we are considering before going to the Pakistan cables company for the

audit of Non-Current Assets of the company

Type Of Business

Pakistan Cables Company is a public limited company. So our team will know how to

design the financial statement of the business and how to disclose the information in the

balance sheet of the company. We know about the financial requirement which are

compulsion by the SECP (Security and Exchange Commission of Pakistan)

Industry

Pakistan Cables Company is the electric conductor goods. We have identify the industry

of the Pakistan cables company so it will be easy to identify the assets of the company

according to the definition given by the International Accounting Standards and GAAP

(General Accepted Accounting Principle)

Expertise

We have expertise in the field of the Non-Current Assets valuation and their estimation.

If we will audit the Non-Current Assets we will do it ease and confident about our

working.

Scope of Audit

The scope of our audit is defined which is on non-current assets of Pakistan cables

company limited. So we will do audit on the non-current assets of the Pakistan cables

limited

9

Fees

Our fees has been fixed and confirmed by the management of the Pakistan cables

company limited and if other review will be conducted they have to decide the firstly

before getting into the contract for other services

Contact with KPMG

We have to contact with the KPMG audit firm because they are the previous auditor of

the Pakistan Cables Company limited. Which have conducted the audit on non-current

assets of Pakistan cables limited company. Which tell us about the calculations and

estimation of the non-current assets and also provide information about the past records

and data of the non-current assets.

Information Source

Our information sources is the management of Pakistan cables limited will provide also

the information which is necessary to perform the audit on non-current assets of the

company and the estimation which are taken by the management of the Pakistan cables

company limited.

Appointment Procedure

We have to see that we are appointed by the proper rules and procedures. Proper rules

and procedures means that we are appointed on the vacant post of auditor which are

approved by the shareholder in the annual general meeting.

10

Audit Engagement Letter

To,

1 July 2013

The Chairman of Pakistan Cables Limited

Mr. Amir Chinoy

1. We are pleased to act as the auditor of the Pakistan Cables limited and we are writing this

letter to confirm our appointment agreement with terms and condition

2. The purpose of our letter is to confirm our audit procedure with accompanied term and

condition for carrying out the work.

3. We are bound to act according with ethical code and conduct of Chartered Accountants

(Pakistan) and ISA (International Auditing Standards)

Period of Engagement

1. This letter will be effected from 1 July 2015

2. We will deal with matter arising in this period

3. We will not be responsible for the past event/matters arising from the previous period.

Any matters which are arising from the past KPMG audit firm will be responsible.

Scope of Our Audit

We will give our opinion on the Non-Current Asset whether they are giving true and fair

view.

Our Responsibility

We have set out our scope of audit with your requirement. If any changes will be occurred

we will draft the new audit engagement letter. We will rely on you start our audit procedure.

If we want any information from past and if it is incorrect or inaccurate we will not be

11

responsible. We will give our opinion on the basis of IAS,IFRS and GAAP whether the Non-

Current Assets are giving true and fair view or not

Your Responsibility

As we relying on you any information given by you or by third party with your permission. If

any changes happens which you feel is important and alteration is needed tell us or advise us.

Otherwise we are not responsible for any cause.

Statutory Responsibility

As chairman this your responsibility to maintain the books of accounts and apply the rules

and standards of International Financial Reporting Standards.

1. This is your responsibility to make the estimation

2. It is your responsibility to maintain the asset ledgers

3. This is your responsibility to detect the error and fraud

4. This is your responsibility to show the proper disclosure and break-up of the assets

5. This is your responsibility to implement the IAS-16

6. You have to address the shareholder with the audited report

7. We will give the opinion on the non-current assets of the company

8. We will deliver you a report before time

9. This our professional and statutory responsibility that we have to check whether the

Standard is properly implemented or not

10. This your responsibility to record the subsequent expenditure which are directed by

the Standards.

11. If we want any information from your management this your responsibility to provide

us

12. It’s your responsibility to maintain the revaluation surplus account

Our Services to You

1. We are providing services to you according to the ISA and SECP rules and

regulations

12

2. We will gather the evidence with the help of internal control and other techniques

which are used to proceed the audit work due to lack of time if any misstatement will

be undiscovered we will not be responsible

3. We will tell you about any weakness in the internal control system on the non-

current assets

4. We will found out any irregularities in recording the noncurrent assets

5. Our report will be issued with the accompanied of account balances

6. Once we have issued the report we are not responsible for it

7. We will not leak any information related with you

Fees

We will charged the fees of an audit according with the market rate means the fees which

are charged by the other firms in the market. We will charged the 1million rupees by

providing our services. If any other services you want from us we will alter the fee.

Agreement of Terms

1. Once the agreement is accepted it will be affected till it is replaced

2. If the new service will also provide you this letter will be terminated

3. This letter we are sending you with the scope if any changes want to make let us

know

4. This letter should be read in accordance with the firm standards

Your sincerely,

Signature

Friends Charted Firm

13

Internal Control System

Internal control system of the Pakistan cables limited is as discussed under

Approval Process for Capital Expenditure

In Pakistan cables limited whenever the company want to incur they have to take the

approval for purchase or expansion of an asset. They have to take the approval from Board

of Director if the (BOD) has approved they will convey it to the Chief Financial Officer.

Estimation

They management of Pakistan Cable Limited make estimations for the assets which are as

Useful life

Salvage value

Cost of an asset

If Capitalize Expense On Which Basis

The management of Pakistan cable capital the expenditure on its nature. They will see

whether this expenditure is on regular basis or this expense will enhance the capacity or

useful life of any asset

Valuation of an asset

The management team of Pakistan cables limited making the revaluation of an asset on the

regular basis. The company has policy about the revaluation which is

Building will be revalued after every two year

Leasehold land will be revalued every year

14

Insurance Coverage

Any insurance which is taken against any asset should be capitalized to the asset because

the insurance is specific taken foe the asset. It should be capitalized to the amount of an

asset

Audit Methodology to Gather Audit Evidence and Assertions

Property Plant and Equipment

Leasehold land

Assertions for the Leasehold Land are;

1. Valuation

The land valuation technique used by the management is the revaluation of the

asset so we will see the value of the asset in the market at the time of audit.

2. Completeness

The revalued land should be complete in every regard of the asset in aspects of

the revaluation account and the revaluation is to be mentioned in retained earning

of the company equity

The following described below is the type of test which we are going to use;

1. Comparative Analysis

We will compare the value of land last year and value of current year any

difference between the values will be charged to revaluation surplus account

15

Leasehold Building

Assertions for the Leasehold Building are;

1. Estimation

For leasehold building we have to estimate about the depreciation of the building

and to calculation basis for depreciation

2. Segregation

We have to segregate the depreciation into two different parts which are;

Asset Control Account

Revaluation Surplus Account

The following described below is the type of test which we are going to use;

Test of Control

We will rely on the internal policy of the Pakistan cables limited because we have

taken;

Book Value

Revaluation

Depreciation

Reporting date book value

As we have gone through it we have found that all the things are reported fairly

enough and all the treatment according to it

16

Leasehold improvement

Assertions for the Leasehold Improvement are;

1. Estimation

First of all we will estimate the cost of leasehold improvement on which price it

was included in the balance sheet to charge the depreciation on it

2. Recognition

On which price the leasehold improvement was included/recorded in the ledger

are they have include the attributable cost in it

The following described below is the type of test which we are going to use;

Test of Details

We will test the leasehold improvement with the procedures which are as under;

At which time it`s purchase we will see the date

We get the evidence from cash flow statement in investing

activities

The useful life of an asset estimated by the management

How it has been depreciated

The depreciation rate on leasehold improvement

Depreciation method is straight line

Machinery

Assertions for the Machinery are;

1. Break-up

We will see the break-up of machinery, how many machinery are old and any

new machinery is purchased so we will take into the account for audit because

there will be ease to identify the machinery

2. Segregation

17

There will be segregation of the machinery in which areas the machinery are used

by the organization in which areas and to allocate the expense accordingly

3. Estimation

In estimation we will how much useful life is estimated by the organization for

the machinery because useful life of machinery is depend on the nature and

technology of a machinery

The following described below is the type of test which we are going to use;

Test of Controls

We will discuss the test which we are going to apply on the machinery. First of all

we have to see the things as under;

The depreciation rate

Calculate depreciation

Charge the depreciation

Different depreciation rates for different machinery

Balance of machinery at the reporting date

Any addition in the machinery

Office Equipment and Appliances

Assertions for the Machinery are;

1. Completeness

We have to go for the completeness in each aspects of the asset because in office

equipment’s because there is more use of technology in it which is the major

thing/point for it

18

2. Estimation

We will estimate the useful life of an asset because there is more technological

innovations in it and the depreciation is more than any asset

The following described below is the type of test which we are going to use;

Test of Controls

We will rely on the internal controls which are adopted by the Pakistan Cables

Limited. In this we will see the following points;

Useful life of asset

Depreciation rate

Depreciation calculation

Any addition in the asset

Total depreciation expense

Book value at the end of year

Vehicle

Assertions for the Vehicle are;

1. Valuation

First of all in the vehicles value of the vehicle reported in the balance sheet

because this asset has a risk of damage as compare to other asset and any

insurance which is taken by the Pakistan Cable Limited is included in it or not.

2. Completeness

The vehicle should be complete in each aspect if any addition make are included

in the ledger cost account of vehicle

The following described below is the type of test which we are going to use;

19

Test of Control

For this asset we will rely on the internal control policy in which we will see the

following points;

Break-up of vehicle

Any addition

Depreciation rate

Depreciation amount

Book value at the start

Book value at the end

Calculate the depreciation

Any attributable expenses

Furniture and Fittings

Assertions for the Furniture and Fittings are;

1. Completeness

We have examine the completeness of asset in the term of asset which means we

have to look towards the addition or any sale of the furniture

The following described below is the type of test which we are going to use;

Test of Details

We will collect the evidence in the following way;

When the furniture is purchased

Type of wood used in it

Life of wood

Break up of furniture

Salvage value at the end of life

Depreciation rate

20

Depreciation amount

Where these furniture are used

Allocate the depreciation expense

Loose Tools

Assertions for the Loose Tools are;

1. Valuation

The valuation of Loose tools are important because the loose tools can be lost

easily because most of them are in small size which can be misplaced and value

of loose tools can over valued

The following described below is the type of test which we are going to use;

Test of Controls

We will rely on the test of controls and we will see the following elements;

Where the tools are used

Types of tools

Moveable/Immovable tools

Depreciation rate

Depreciation amount

Any addition

Any sale

Long Term Loans

The long term loan in the asset side of balance sheet means the loans are provided by

the Pakistan Cables Limited to their employees. The loan is given according to the

scale of an employee in an organization

21

Assertions for the Long Term Loans are;

Segregation

The loan should be segregated into the two parts;

1. Long term loan

2. Short term assets (Receivables)

The long term loan should be categorized into the time period of the loan given to

the employee of company how much time is gone when the loan is advances to the

employee of the company so it will be easy to assess the condition of long term loans

The following described below is the type of test which we are going to use;

Test of Details

We will collect the evidence in following ways;

Segregation of loan

Break ups

Estimations

Received in the year

Receivable in the year

Collection charges

Cash flow statement

Balance at the start of year

Balance at the end of year

Investment in Associates

The investment in associates means the Pakistan Cables Limited has invested or

purchased the share of other company more than 20% and less than 50%.

Assertions for Investment in Associates are;

22

1. Valuation

The value of an investment at the time of purchase and at the time of reporting

date. The investment will be taken into account on fair market value basis

The following described below is the type of test which we are going to use;

Test of Control

We will rely on the internal controls of Pakistan Cables Limited. They are;

At the date of acquisition

At the date of reporting

Non-controlling Interest

Fair value Adjustment

Share of profit

Value of goodwill

Value shown in the balance sheet

23

Audit Report

To,

The Shareholders of Pakistan Cables Limited,

Karachi

1. Our Responsibility

Our responsibility is to give the opinion on the Non-Current assets of Pakistan cables

limited company whether the Non-Current assets are giving true and fair view or not.

As we have gone through the audit procedure on the Non-Current Assets if misstatement

remains incorrect or inaccurate because we have done our audit on the basis of sample so

we are not responsible for it.

2. Management Responsibility

It is the responsibility of the management to prepare the financial statement of the

company which gives true and fair view according to International Financial Reporting

Standards and which are directed by the Companies Ordinance 1984. It will also include

the designing maintaining and implementing the internal control system for the

preparation of Financial Statement according to the standards and the Ordinance

3. Report On The Non-Current Asset

As we have audited the non-current assets of the Pakistan Cables Limited we are

reporting that the non-current assets of the company are giving true and fair view. As the

samples which are chosen by our team we have not found any misstatement in it. Non-

Current Assets are recorded according to the International Accounting Standards

24

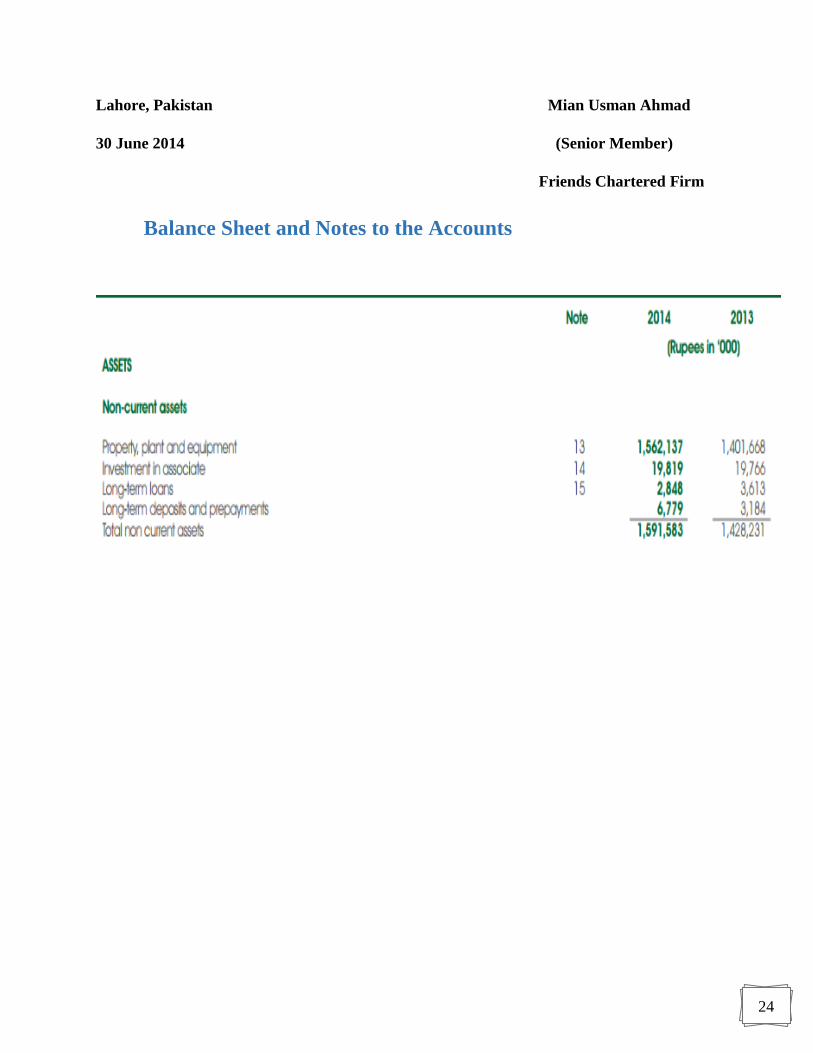

Lahore, Pakistan Mian Usman Ahmad

30 June 2014 (Senior Member)

Friends Chartered Firm

Balance Sheet and Notes to the Accounts

25

26

27