an evaluation of the cooperative system in the philippines

TRANSCRIPT

Journal of Philippine DevelopmentNumber Twenty.Five, Volume XIV, No. 2, 1987

AN EVALUATION OF THE COOPERATIVESYSTEM IN THE PHILIPPINES

Victor A. Tan

I. INTRODUCTION

The cooperative system in the Philippines has been character-ized by stories of success and failure. While the system has beena recipient of all-out government support, it seems that it hasremained meek and docile.

This paper looks into the reasons for such situation. It examinesthe problems and their implications on the cooperative movementas a whole. It also looks into other rural-based organizations andtheir performance. The study also attempts to be as comprehensiveas possible, by way of reviewing the various studies in existenceregarding the subject matter.

A compilation of recommendations and the writer's own viewsare likewise included here. The state of things at present indicatesthat the cooperative structure in the Philippines deserves a shotin the arm in some instances and a blow in others if only to promotethe development of the more deserving cooperatives.

II. MAJOR FINDINGS

A. Studies on the Rural Credit System

1. The Rural and Farm Credit System

The rapid growth of the rural population has put pressure on the

Tan Research House and Consultancy; Technical Consultant to the Assistant Secretaryfor Planning and Comprehensive Agrarian Reform Program of the Department of AgrarianReform.

321

322 JOURNALOF PHILIPPINE DEVELOPMENT

land-man ratio and has given rise to burgeoning food needs. Thecountry's development plan hasaddressed this concern and hasarti-culated the objectives of increased food production, the expansionand creation of employment opportunities, enhanced rural incomesand nutritional level, increased agricultural exports, the develop-ment of agro-based energy sources, and conservation of naturalresou rces.

In trying to achieve these objectives, severalrural credit programswere launched which were meant primarily for the small producers.These programs cover a host of commodities and activities thatinclude rice, corn, feedgrains, livestock and poultry, fruits and vege-tables, cotton, fisheries and cottage industries. They also includeon-farm capital investments and integrated agricultural financing.

Despite these programs, though, there has not been much flow ofrural credit into the .countryside. Most of the current credit supplyin the countryside is provided by the private nonformal money-lenders. This was true in the late 1970s when informal sourcesroseto prominence as fund suppliers,contributing some 64-78 percentof all farm credit during the period. The formal sourcesof ruralcredit showed their importance only in the mid-19?0s with their64-6-/ percent contribution as a result of the emergence of thegovernment's massive supervised credit programs. But this laterpetered out due to high loan arrearageswhich compelled financialinstitutions to be selective in their lending to agricultural and ruralbusinessundertakings (TBAC 1980).

Loan biases in agricultural lending are evident among formalinstitutions in favor of export and commercial crops. Loans aremostly short term and concentrated in developed regions.This hasresulted in a "vacuum" among other agricultural prodt_cts andunderdevelopedregions(TBAC 1981).

Aside from these biases, there is a seeming institutional biasagainst lending to the rural sector due to risk-return considera-tions involving uncertainties in physical output as well as in themarket value of the output. The output risks include the weather,land and man productivity. While the weather risks are essentiallybeyond man's control and can be considered as constraints, manand land productivity could be managed through breakthroughsin researchand extension programs.

Financial institutions could help in intermediating betweengroups of farmers and other segmentsof the rural population who

TAN : COOPERATIVE SYSTEM 323

have excess liquidity. The seasonalnature of the farm productionprocess causes varying supplies and shortages of cash. Throughintermediation, financial institutions could assist in managing thecash flow of several disjointed operations in the rural areas.Thecredit functions of financial institutions are necessary not onlyto smooth seasonalliquidity but also to increasethe rate of capitalinvestmentsin the rural sector.

It is fair to assumethat there might be indivisibilities in the fac-tor proportions between capital and labor in agriculture. Irrigationand fertilizers could fall under this category. No amount of extraman-days could increase production if irrigation and fertilizers arenot provided. Small farmers, however, think otherwise, asevidencedby the fact that they keep a large householdsize for the purposeofproviding additional labor which the farm may need to increaseproductivity,

The rural credit system is a dichotomy between large fund pro-ducers and small fund producers. Based on this structure, smallproducers are only able to get loans from small fund suppliers dueto the former's credit absorptive capacity. Small funders, however,usually end up with low repayment problems, and their Ioanablefunds are eaten up by operational expenses. Moreover, most smallfunders' loan portfolio is concentrated on special borrower groups,and when these groups default on their loans, the small funders'viability and profitability position becomesprecarious (TBAC 1979).

The farm and rural credit system, therefore, has become dys-functional in carrying out its objectivessuch as the enhancement ofthe transfer of technology through the provision of funds for in-creased demand for borrowed funds; the facilitation of commod-ity flows, through the market mechanism, from the producersdownto the final consumers:and the allocationof funds, through financialintermediation, to individuals and institutions that could use thesefunds productively. The low volume of credit trickling down to therural sectoris reflective of the flows in the rural credit system.

2. Agricultural Credit Policies

The major underlying objectives of the agricultural credit policyare anchored on the progressiveinstitutionalization of credit andthe allocation of an increasingly larger share for the small farmer

324 JOURNAL OF PHILIPPINE DEVELOPMENT

producers and weaker sections of the peasantry. These aims arereflected in the government's strategy of establishing financial in-stitutions in the countryside such as rural banks, the Land Bank ofthe Philippines, and the like, with the end in view of influencing theflow of credit to the rural sector, in general, and to the small-scaleproducers, in particular.

The agricultural lending policies on small farmer lending programscan be categorized into: (a) general policies on small farmer lendingprograms; (b) Central Bank policies affecting rural bank loans tosmall farmers and entrepreneurs; and (c) Central Bank policies onrediscounting of rural banks' eligible papers.

(a) General Policies

The general policies on small farmer lending programs include:(1) supervised credit schemes which introduce three importantfeatures, namely, farm plan and budget, Packageof Technology(POT), and extension services; (2) group lending; (3) guaranteecoverage wherein guarantee feesof 1 percent and 2 percent for short-term and medium�long-term loans, respectively, are charged to therural banks so as to cover the unsecured portions of loans caused bynonpayment due to reasons of force ma/eure; (4) accelerated fundassistance which provides for a fund of some t=450 million to enablerural banks to avail themselves anew of rediscounting privileges;(5) crop insurance which assuresthe farmer of some funds to financehis next production expenses if his previous crop is destroyed,through a 2.0 percent premium payment contribution by the farmer,1.5 percent by the lending institution, and 7.5 percent by the govern-ment in case the farmer is the borrower; (6) rediscounting at pre-ferential rates where the loan value is equivalent to 90 percent ofthe outstanding balance on the unpaid portion of eligible instru-ments at the time of rediscounting for supervised credits, and 80percent of the outstanding balance for nonsupervised credits; (7)collateral requirements relaxation in conformity with PresidentialDecree 315 promulgated on 22 October 1973 that asked all finan-cial institutions participating in agricultural credit programs toaccept a certificate of land transfer (CLT) as a collateral for loanwith a maximum loan value of 60 percent of the value of the farmholding; (8) marketing arrangements wherein the farmer-borroweragrees to deliver a portion of his produce to the marketing agent

TAN: COOPERATIVE SYSTEM 325

equivalent to the amount of his loan inclusive of the interest rateand the marketing agent purchasesthe farmer-borrower's produceand pays the said borrower's loan directly to the lending institutionwithin a specified number of days, and where the lending institu-tion accepts the loan payment made by the marketing agent in be-half of the borrower andcredits any excessamount to the borrower'ssavings account; (9) restructuring of past due loans whereby theCentral Bank may allow the rural banks to restructure their redis-counting arrears for a period of one year if these arrearsare due toforce majeure and for a maximum period of three years for itsmeritorious cases. For their part, rural banks may alsoallow therestructuring of the farmer-borrower's past due loans for similarperiods for similar reasons;(10) decentralization schemesfor Spe-cial Time Deposits (STD) availment wherein the Central Bankempowers the Regional Loan Teams in Central Bank Regional Offi-ces and the Department of loans and Credit (D/C) units in theregions to accept and processSTD applications and releasethe pro-ceeds immediately; (11) agricultural credit quota policy whichrequiresall banks, either private or public, to allocate 25 percentoftheir Ioanable funds for agricultural credit (15 percent for agricul-ture in general and 10 percent for agrarian reform credit): (12)integrated approach in agricultural financing whereby the CentralBank redesignsits lending scheme by simplifying lending proceduresto benefit both borrowersand lenders, dovetailing it to the conceptof Integrated Agricultural Financing initiated by the National Foodand Agriculture Council; and (13) integrated rural financing, whichis a supervisedrural credit program characterized by the adoptionof an area-basedcomprehensivefinancing schemeand area manage-ment approach, and whose major thrust focuses on the selectivesite-specific implementation approach and on participative area plan-ning,amongothers.

(b) Central Banh Policies Affecting Rural Banh Loans to .SmallFarmers and Entrepreneurs

Central Bank policies affecting rural bank loans to small farmersand entrepreneurs touch on the eligibility of borrowers, the purposeof the loan, loan ceiling, terms of loan, loan releases,interest rates,service fees and other charges,collateral requirement and loan repay-ment.

326 JOURNAL OF PHILIPPINE DEVELOPMENT

On the question of eligibility, the qualifications depend on theduration of the loan, whether short_, medium-, or long-term, Forshort-term loans, the qualified borrowersare small farmers/operatorswho own or till lessthan sevenhectaresof viable agricultural land;agrarian reform beneficiarieswho own no more than three irrigatedand five unirrigated hectares; previous borrowers under any of thesupervisedcredit programswhose experience, background and faci-lities have been proven as effective; residents of the locality as cer-tified by the barangay captain or the municipal government; thosewhose repayment rate records warrant eligibility for another project;vocational students whose parents are willing to co-sign as loan gua-rantors and whose teachers are amenable to being supervised credittechnicians; municipal fishermen who operate no more than 3-tonmotorized or nonmotorized bancas; and members of agriculturalcooperativeswho are qualified for financing.

For medium- and long-term financing, the qualified borrowersare (1) farmers who own or till not more than SO hectares; (2)operators who are engagedor intend to engage in a cottage or agro-industry with a capital investment not exceeding t=300,000 exclud-ing land; (3)operators Who are engaged or intend to engage intransporation enterprises for cargo or mixed cargo and passengers;(4) persons who are engaged or intend to engage in poultry, swineor cattle breeding/fattening projects; and (5) persons who areengaged in the development of fishpond/fishpens or in coastal fish-ing with a capital investment not exceeding t=300,000 excludingland.

Short-term loans are usually for (1) the purchaseof seeds,ferti-lizer, chemicals, work animals, and implements/equipment used infarm operations or for the hiring of such animals, implements/equipment, and the purchaseof stocks such as cattle, poultry swineand fingerlings; (2) farm expensessuch as labor in relation to landpreparation, planting, plant care and harvesting, minor repairs,construction or improvements in the farm/fishpond/fishpen forincreased productivity purposes; and payments for current taxes/irrigation fees. For medium- and long-term loans, the loan pur-poses cover all activities related to agriculture, cottage or agro-industry whose production cycles are more than one year and which

require the acquisition of machinery/tools/equipment needed intheir undertakings.

Meanwhile, the loan ceiling of the project dependson the type of

TAN: COOPERATIVE SYSTEM 327

the project and on the implementing guidelines of the credit pro-gPam, as well as on the viability and actual needs of the project,the borrower's creditwothiness and repayment capacity, and thecollateralsoffered.

Regarding loan terms, for short-term loans, the loan maturitydoes not exceed 360 days while for medium- and long-term loans,the maturity period varies in accordancewith the economic life ofthe project and the projected cash flows. However, in each case, itshould not exceed the specified maturity period stipulated in theimplementing guidelines.

Loan proceeds under the ordinary lending scheme are releasedto the borrower in full. The loan amount under the supervisedcreditprogram is deposited in the special savingsdeposit account of theborrower. Amounts are then released by the depository bank inaccordance with the farm plan a_d budget. This usually holds forshort-term loans. For medium- and long-term loans, the loanamounts releaseddepend on the project plan.

On the matter of interest rate, for short-term loans, it dependsonthe prevailing interest rate asdetermined by market forces. For ordi-nary loans with a maturity period of 730 days or less,the interestrate is placed as 16 percent per annum if secured,and 18 percentper annum if unsecured. For loans which mature in more than 730days, the interest rate is 21 percent per annum, excluding commis-sionsand other charges.

Service fees and other chargesdepend on the discretion of thelending institution. Up to 2 percent per annum may be assessedbythe borrower on the loan pr'ncipal or outstanding balance, which-ever is lower, under the ordinary loans and 3 percent on the loanbalance of CB-IBRD loans. Nevertheless, for a loan not exceeding_=2,000, a T=20.00 service charge is collected. For Agrarian Reformbeneficiaries borrowers, the minimum charge shall not exceed 2percentor t=150.00 per annum, whichever is lower.

Initially, no collateral is required for short-term loans under thesupervised credit programs. Recently, however, lending institutionswere allowed to impose a collateral requirement in the form ofunencumbered real/personal property, chattel mortgage on stand-ing crops or object of financing, pledge of bonded warehousereceipts, acceptable co-makers and joint liability or guaranteecoverage.

For ordinary and supervised medium- and long-term loans, the

328 JOURNAL OF PHI LIPPINE DEVELOPMENT

collateral may assume the form of first mortgage on titled anduntitled immovable property and bonds securities. However, loansof agrarian reform beneficiaries and small fishing boat operators maybe secured with a guarantee by the "Agricultural Guarantee Fund"to the extent that their loans are not secured.

Repayment of short-term loans usually is made at a time whenthe borrower has the highest income or when the principal incomeof the borrower is available. Payment of loans may be in cash or inkind as in the caseof Masagana99 loans.

For medium- and long-term loans, repayment is scheduled inequal installments inclusive of principal and interest On an annual,semiannual or shorter-period basis except in cases where deferred

payments have been granted by the lending institutions.

(c) Central Bank Policies on Rediscounting of Rural Banks Eligi-ble Papers

Central Bank policies on the rediscounting of rural banks' eligiblepapers involve at least three major aspects, namely: credit ceiling,arrearagesratio, and risk-asset ratio.

The ceiling for rediscounting is set at 500 percent of net worthand 300 percent of monthly average savings-cum-time deposit lia-bilities during the four months immediately preceding the date ofloan application. Rural Banks (RBs) may avail themselves of redis-counts from the Central Bank for any number of years during theyear subject, however, to the RBs' operating capital.

The arrearages ratio, meanwhile, which enables the rural banks torediscount with the Central Bank and to participate in special finan-ing programs is set at 25 percent. Exceptions, however, apply tocertain special credit programs, provided that the financial assist-ance granted by the Central Bank is to be utilized solely for the par-ticular program for which such assistance is provided. If the redis-counting appears were incurred due to natural calamities, the ruralbanks may submit to the Central Bank a capital buildup program andconversion scheme.

For banks to be able to rediscount with the Central Bank and to

participate in special financing programs, the ratio of capitalaccounts to their total risk assets should not be less th_n ]0 per-cent.

Numerous problems accompany the agricultural credit policies.

TAN: COOPERATI VE SYSTEM 329

Despite the positive salient features of the supervisedcredit schemes,•the beneficiaries appear not to have improved their economic lot.This may be due to the many risks in agriculture brought about bythe vagariesof weather, uncertain packageof technolo_ and inade-quate price support. The situation has created another unlikelysituation where the loan absorptivecapacity of borrowers is low andarrears are high, compounded further by the seemingly acceptableloan default syndrome and poor collection mechanismon the part oflending institutions.

Group lendings through such groups as the seldas or damayanshave been failures. The lack of discipline among members and the"to each his own" attitude has substantially eroded the groups'confidence in eachother.

To protect the interest rate spreadfrom beingeaten up under thesupervisedcredit program, the Agricultural Guarantee Fund (AGF)wasput up, but so far, statistics revealthat it has not lived up to itsrole due to factors beyond the Fund's liability.

Meanwhile, Presidential Decree No. 717 expresslyprovides prior-ity to agrarian reform beneficiaries. While financial institutionshaveovercomplied with the 25 percent of Ioanable funds, compliancewith the agrarian reform credit subquota through direct lending hasbeen minimal. Despite general overcompliance, the decree has hada negligible effect on banks' investment portfolio as evidenced byvery slight positive, if not negative, changesin the ratios of agricul-tural loans to total loans outstanding as well as of agricultural loansto net Ioanable funds outstanding after the decree took effect. Nordid compliance have any significant impact on bank profitabilitylevels because the conditions for the effective implementation ofthe decree are not, in the first place, adequately present. First, thereare no Agrarian Reform Beneficiaries (ARBs) to provide loans toin particular areas. Second, many financial institutions are urban-based and are not oriented towards lending to the rural sector orto the ARBs, for that matter. Third, there is a lack of identifiedviable projects for potential borrowers.Fourth, financial institutionsrarely find support and encouragementto lend directly to loan bene-ficiaries due to the presence of alternative compliance vehiclesthrough the purchase of Central Bank Certificates of Indebtedness(CBCI). Fifth, other bond instruments and government protectionmeasuresand incentivesare inadequate. Sixth, there is a lack of veri-fication of compliance at the field level. And finally, sanctionsfor

330 JOURNAL OF PHILIPPINE DEVELOPMENT

noncompliance are rarely carried out.Central bank's policies affecting rural banks' loan to small farms

and the policiesaffecting the rediscounting of eligible papers of therural banks are stringent and some are also unrealistic. For instance,the fundability of loans once these are in the hands of the ruralbanks poses one big problem of verification, rendering the pur-pose for the loan academic. Many rural banks have been foundguilty of diversion of funds while their investment activities in alliedservicesare largely constricted or limited.

3. Review of Institutions/Lenders

At the forefront of the rural and agricultural credit system whichprovides loans to small producers and entrepreneurs are the ruralbanks. But they, too, have to contend with severalproblems.

Under the Masagana 99 program alone, it is estimated that thecritical repayment level, below which profits would assume a nega-tive figure, is 98.?- percent. For rural banks, an average repaymentrate of 98.2 percent is a tall order, considering that agriculturallending is a.Costly proposition.

The rural banking, system is also confronted with the following:(1) most rural banks operate on an uneconomic size: (2) their

•. growth in resources is impressive at first glance, but a closer lookat the growth structure reveals that resource accretions are due tothe addition of new rural banks rather than to internally gene-rated resources; (3) rural banks can hardly mobilize savings. Thebulk of their resources come from government equity counter-part and borrowings from the government; (4) delinquent accountsand poor loan and investment quality portfolios have substantiallyeroded the system's profitability and viability; (5) mismanagement,inadequate personnel capability and poor salary structure have alsocontributed to the rural banks' unprofitable state: (6) Central Bank's

paternalistic approach by pampering and overprotection also didmuch to make the rural banks too dependent on the CB;. and (7)engaging in too many supervised credit programs has resulted inoverexposure, poor quality portfolio and, thus, poor repayment.

Government banks such as the Land Bank of the Philippines, the

Development Bank of the Philippines and the Philippine NationalBank lend to small farmers only intermittently. The bulk of theirlending portfolio is focused on plantation type farms, large farmers/

'TAN : COOPERATIVE SYSTEM 331

traders andcommercial loans.Private commercial banks and other types of banks lend either

on a commercial basis or to large borrowers, nonfarmers and bigproducers.

Several bottlenecks plague rural and agricultural lenders, amongwhich are the following: (a) the high specialization of banks leadsto a dearth of medium- and long-term funds for agriculture, and tocompartmentalized services and segmentation of the agriculturalclientele. The latter segments,among others, big and small peasant-farmers, agrarianreform farmers and sugarfarmers, and bigand smalltraders: (b) bank government funding agenciescannot sustain thenoncredit needs of the less privileged sector of the borrower-spec-trum. Nonbank government financing agencieswhich form part ofthe rural financial system include the Farm Systems DevelopmentCorporation (FSDC), Philippine Tobacco Association (PTA), Minis-try of Agrarian Reform (MAR), and Cooperative Development LoanFund (CDLF). The CDLF lends directly to small marginal farmers,resettlers, landlessrural workers and agricultural cooperatives. How-ever, it only providesa negligible share (lessthan one-half of a per-cent) of total loans, with most of thesegovernment funding institu-tions depending on government sourcesand funds which are most-ly treated as dole-outs; (c) Apparently, there is no coordinationamong financial institutions at the grassrootslevel, resulting in multi-ple financing for the same borrower; (c) since severalfinancing insti-tutions are persuaded to lend to the rural and agricultural sectors,there exists no link among them to promote loan syndication forreasonsof lack of identified bankable projectsand the absenceof alead bank for loan consortium purposes;(e) informal lenderswhocharge high interest rates also lend loans to small producersto thelatter's disadvantage. Most of these lenders, who are also traders,own adequate facilities to service the marketing needsof the smallproducersat depressedprices. Some government marketing outfitssuch as the National Food Authority (NFA) and the AgriculturalMarketing Cooperatives (AMCs) absorb the marketing needsof thesmall farmer producers, but the former absorbsonly up to 15 per-cent of the market while the latter are saddledwith severalproblems,suchasthe lack of capital.

Recently, informal lenders also becameselective in their loaningoperations. They have followed the lending strategy of institutionallending institutions, ruling out the possibility of loaning to marginal

i'

332 JOURNAL OF PHILIPPINE DEVELOPMENT

and submarginalproducers.

4. Review of Borrowers

Most farmers and food producers are small, and most (61 percent)farm holdings are less than three hectares. Due to the smallness offarmers and to high production risks and insufficient marketing sup-port, farmers are faced with cash flow problems as income competeswith funds for production and household upkeep purposes.

Several studies support the notion that rural credit borrowers are

hardly bankable and hardly get loans. Tan (1978), for instance,analyzed the cash flow balances of a typical agrarian reform benefi-ciary under various assumptions of land size, family size, householdexpenditures, type of labor utilization, sources and amount ofloans, etc.

Permutations of sot_rce of loans and type of labor used in the farmwere combined with the usual socioeconomic conditions and frame-

work of operations of an ordinary rice farmer to create six models.to determine his cash flow position at the end of each month andyear. One-year cash flows were simulated from these models and themonthly and year-end cash balances were noted. The effect of varia-tions in factors such as land size, loan size and effect of typhoondamage were analyzed through sensitivity analysis. Simulationresults revealed that, in almost all cases, months with negative cashbalances outnumber months with positive cash flow balances andthat the various assumptions and conditions under which a farmercan have a positive year-end balance seem rare and infeasible. A far-mer owning one hectare of irrigated land should have no loans otherthan _=1,200 from a formal source per cropping season and shouldnot utilize labor outside the family while following the Masagana99 recommended package of technology. One who uses labor bothfrom within and outside the family and has the same credit positionsas above should own at least 1.25 hectares of irrigated land to beable to have a positive cash balance. One who avails himself of loansfrom informal sources should have bigger landholdings to end upwith favorable cash balances. Such findings reveal that, despite the

success of government agricultural credit programs in increasingfood production, they had little beneficial effects on the socioeco-nomic status of the producers.

A survey on the socioeconomic profile of landless agricultural

TAN : COOPERATIVE SYSTEM 333

workers in three selected barangay was aimed at documenting theirsocioeconomic profile. It determined the basic needs and creditrequirements of this particular group and gave insignts into thisgroup's perception of credit, banks, the government and their con-dition.

The study, which covered the barangays of Abangay, lloilo,Bahaypare, Pampanga, and Tinawagan, Camarines Sur, found thatthe rural workers are a very disadvantagedgroup in the agriculturalsector. The group is very impoverished,with income levelsthat arelow and seasonal.The group's major activities are mainly personalservices, making these landless rural workers uncompetitive in thehighly competitive agricultural labor market. Interview results

revealed that the government showed lessattention by not creatingproblems addressed to their problem. In fact, the agrarian reformprogram hashada negativeeffect on them (TBAC 1978).

In a surveymade by the TBAC in 1982, field resultsindicatedthatabout a third borrowed during the survey year. Paddy irrigated far-mers, large farm operators, and agrarian reform beneficiarieshada relatively high level of indebtedness. Informal sources, mostlypalay traders, accountedfor close to two-thirds of the total numberof loans while formal sourcesdominated the lending arena in termsof lending, with about three.fifths of total loan volume.

A finding of the study that one out of ten farmers was a formalborrower and three out of ten farmers borrowed from either theformal or informal sourcesisa clear indication that the flow of cred-

it to the agricultural sector is assuming miniscule proportions inrelation to the required rural credit needs.

The study concluded that the main bottlenecks in rural credit arethe bankability of small farmers/producers, the secondary role ofcredit in improving farm productivity and income,and the limitedaccessof farmers to formal credit.

TBAC (1981), using a sample of 34 farmer respondents(lease-holders, full amortizing owners and CLT holding tenurial classes)in Nueva Ecija in 1981 observed that, without the use of loans,almost all sample respondents would have had deficit runs fromthe planting to the maturing phaseof the crop. Without loans, therewould be a probable decline in harvestand farm income becauseof

the lack of proper inputs, the reduction in the scale of operations,and the lack of financial resources.Other resultswere an improve-ment through land ownership in the equity position of farmers,

334 JOURNAL OF PHILIPPINE DEVELOPMENT

an improvement through multiple cropping of the income flow andrepayment capacity of farmers, and the inability of sample farmersto settle their total current and carryover obligations.

Other reasons why small producers were not able to pay theirloans were the inadequate loan amounts, the lack of discipline, andthe lack of a conscious effort_to saveto finance farm activities.

Farmers who obtained loans in proportion to their farm size orwhose loans were the actual amounts ailowed did not fare wellbecause the amounts were not the funds needed or required. Inother instances, many farmers had borrowed funds in excess ofwhat they needed or required, letting them accumulate some "sav-ings" which they spent elsewhere. In the meantime, they had somehard time repaying their loan (Castillo 1982). This reinforces thegeneral impression that credit ceilings are not based on requiredneeds of the borrowers, stymying the opportunities of the produ-cers to attain maximum productivity. Meanwhile, farmers whooverborrow do not religiously apply the recommended package oftechnology due to inadequate extension and verification services.

The average propensity to save has been found to be a low 7 per-cent among sample respondents in Iloilo, Nueva Ecija and Davao delSur (IbaSez 1978). The marginal propensity to save which is higherat 13 percent implies that increasing incomes will result in furtherincreases in the average proportion of income saved. About 80percent of asset accumulation is in the form of capital formation,livestock and poultry and farm implements. Assets held in financialinstruments constitute a negligible 3 percent. The primary determi-nant of savings is income, with the latter influenced by size of cul-tivated land area, level of liquid assets,land ownership and averageeducation. Rural households appear to be generally responsivetothe opportunity cost of high consumption levels. Most of the ruralhouseholds surveyed were not aware of the functions of financialinstitutions. The general perception was that banks were acting asconduits for leading and not for savings. For forced savingspro-grams, however, the BSF and BGF have been growing at relativelyhigh rates. Nevertheless, voluntary savingshave rarely set in therural areas except among school children through the "school sav-ings campaign program." Perhaps the lack of savingsconsciousnessamong rural householdsmay be ascribed to the lack of incentivesto save and to the absence of a vigorous campaign to tap ruralsavingscapacity.

TAN. COOPERATIVE SYSTEM

5. Summary of Recommendations

1. A recommendation for the institutional credit delivery systemand lending institutions is to continue the present multiagencyapproach to rural financing and also to adopt an effectiveinformation exchange.network among such institutions at thefield level to eliminate overlapping of lending services.This wasdone during the launching of the Kilusang Kabuhayan saKaunlaran (KKK) programwherein past-duetswere not allowedto borrow from the KKK-designated banks. Another recom-mendation is for them to continue functioning as conduits forreal financial intermediation and to allow a viable loan programalong with a social loan program. The latter can be addressedtothe nonbank government entities especially since they arecapable of reaching marginal farmers and other nonbankablerural projects.To abate lending operation inefficiencies,trainingprograms,upgradingof personneland a regularmonitoring andevaluation of these social loan programsshould be conducted.The rural banking system should also encourage mergers andconsolidation on a provincewide or regionwide basisto makethe new groupings more competitive and efficient, and toimprove their economic size stature. The provincial or regionalrural bank may rediscount with the CB, thus eliminating theretail nature of individual rural bank rediscounting.As soon asthe system matures, it can subsequentlychange into a nationalbank. For cooperative rural banks, mergeror consolidation isalso suggested. The consolidated CRB should assume thepostureof a purely private commercial bank with existingCRBsas brancheswith expanded servicenetworks in the rural areas.Land Bank could buy into the equity sharesof the rural banksand make thesebanks its own branches.

Many rural banks have in fact consolidated, such as the 14rural banks in Bohol, equitizin_gmany CRBs and RBs at :F1million each. Another suggestion in formulating an effectiveinstitutional credit delivery system is by upgrading the criteriafor the openingof new rural banks, putting more emphasis oncapital requirements by way of raising the minimum capital to__i million, developingbank managementexpertise,and check-ing the potential of the area where the rural bank is to be Ioca.ted. Another option is to encouragethe putting up of bra_.ches

3_ JOURNAL OF PHILIPPINE DEVELOPMENT

in the rural areasfor every two branchesopened in urban areasby stronger banks such as the large commercial banks. Incen-tives should be provided, and these include a reduction in the5 percent grossmargin tax, a reduction in the tax on interestincome of depositorsservicedby the branch, or tax exemptionon the operations of the particular branch during the firstthree to five years of existence. Since rural informal lendershave been found to be more efficient and to have developeda strong Clientele basein the countryside, they may be insti-tutionalized, subjectto certain conditions.

2. A retention of the quota policy is suggested to lessen theineffectivenessof the agricultural credit quota policy and theunresponsivenessof hanks to the weaker section of the pea-antry. However, it should be modified to make it more effec-

• tire, so that the small farmer will not find himself at the losingend due to high risk and the high cost of lending to him. Thequota policy could cushion this fear; there is thus a necessityfor the moral suasioneffects of the quota system. Sufficientguaranteessuch as a 50 percent all-risk guaranteemay also beenforced to attract high-riskloans.

3. For agricultural credit programs to proliferate an integratedand development approach to agricultural financing is recom-mended. The experience gained in commodity-specific programformulation and implementation shouldserveasbuilding•blocksfor integrated area development planning. The integrated RuralFinancing (I RF), which is an ongoing project that features theoperationalization of the area management interagencyapproach and area-specific, comprehensive area development,and many activity financing schemes, could be considered.So far, a total of twelve development siteshavebeen identifiedin 1984.

4. Activities addressing client-related problems such as small-scale farmers' cash flow problems, unavailability and bank-ability, improvement of small-scale farming system, farmtechnology, infrastructure, and markets and favorable pricesforfarmers' produce to increase•their absorptive capacity for cre-dit and repayment capability; accessto or provision of other

TAN : COOPERATIVE SYSTEM 337

employment opportunities either within or outside agriculturesuch as rural home industriesand other home-basedundertak-

ings to buoy up the farm households' income levels,enhancerepayment capability, and subsequently reducerisks of lendingto small-scale farmers; and the provision of skills training,better accessto educational facilities for the children of farmersespecially those who till at the margin, it is also.suggestedthat,in relation to the farmers' capacity to pay, the farms and far-mars should be categorized and differentiated accordingto pro-ductivity size, location, availability of irrigation, term statusincluding sharingarrangement or lease rental, capital and laborresource availability, credit utilization, family size, accesstofavorable market price, etc.

5. Some recommendationsfor the less privileged groups such asthe agrarian reform beneficiariesare: (1) intensify and speedupland transfer operations under the agrarian reform program inorder to strengthenthe financial makeup of the farm leasehold;(2) promote growth in farm leaseholdequity and furnish thesmall farmers with an endowment level from which long-termfarm development may proceed; (3) encourage the adoptionof multi-cropping activities to provide small farmers with addi-tional sourcesof income and improve their cashflow structure;(4) evaluate the debt burdenand financial capacity of potentialfarmer-borrowers rather than basing credit lending decisionson the cost of the package of technology or the financial needof the farmer to enable him to diversify his farm and non-farm undertakings; and (5) introduce farmer self-help pro-grams or village.level mutual benefit schemesfor small farmercredit programs.There is a need to expand the credit deliverysystem by expandingthe existing institutional network.

B. Cooperative Performance

Samahang Nayons

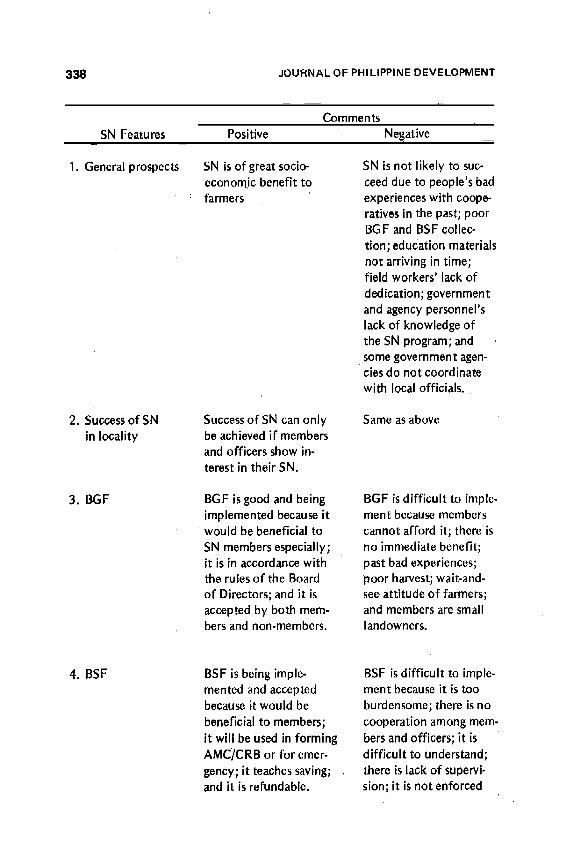

Studies on the performance and problems of Samahang Nayonsabound in Philippine literature. Foremost of these is the study byCastillo (1982) which elicited the following commentsfrom farmers,implementors, program participants and others on the SN's features:

:338 JOURNALOF PHILIPPINEDEVELOPMENT

Comments

SN Features Positive Negative

1. Generalprospects SN is of great socio- SN is not likely to suc-economic benefit to ceeddue to people'sbad

: farmers experienceswith coope-ratives in the past; poorBGF and BSF collec-

tion; education materialsnot arriving in time;field workers' lack of

dedication; governmentand agencypersonnel'slack of knowledge ofthe SN program;and

•somegovernment agen-ciesdo not coordinatewith local officials.

2. Successof SN Successof SN canonly Same asabovein locality be achievedif members

andofficersshowin-terestin their SN.

3. BGF BGF isgood andbeing BGF isdifficult to imple-implementedbecauseit ment becausemembers

• wouldbe beneficialto cannotafford it; there isSN membersespecially; no immediatebenefit;it is in accordancewith pastbadexperiences;the rulesof the Board poor harvest;wait-and-of Directors;andit is see,attitude of farmers;accep_d by both mere- andmembersaresmallbersand non-members, landowners.

4. BSF BSF is being imple- BSF is difficult to imple-mented and accepted ment becauseit is toobecauseit would be burdensome; there is nobeneficial to members; cooperation among mem-it will be used in forming bers andofficers; it isAMC/CRB or for emer- difficult to understand;gency; it teachessaving; there is lack of supervi-and it is refundable, sion; it isnot enforced

TAN: COOPERATIVESYSTEM 339

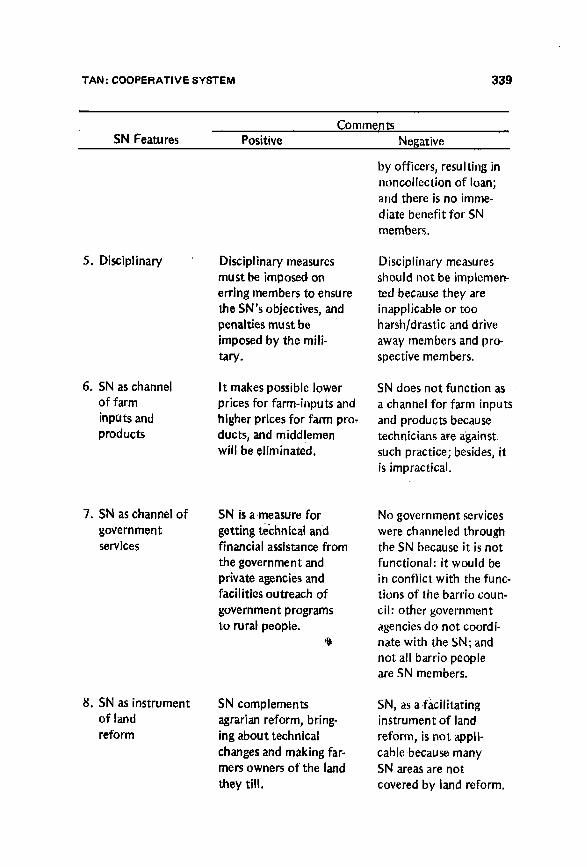

Comments

SN Features Positive Negative

by officers, resultinginnoncollectionof loan;and there isno imme-diatebenefit for SNmembers.

5. Disciplinary Disciplinarymeasures Disciplinary measuresmustbe imposedon shouldnot be implemen-erringmembersto ensure ted becausethey arethe SN's objectives,and inapplicableor toopenaltiesmustbe harsh/drasticanddriveimposedby the mill- away membersandpro-tary. spectivemembers.

6. SN aschannel It makespossiblelower SN doesnot functionasof farm pricesfor farm-inputsand a channelfor farm inputsinputsand higherpricesfor farm pro, and productsbecauseproducts ducts,andmiddlemen techniciansare against

will be eliminated, suchpractice;besides,itis impractical.

7. SN aschannelof SN isameasurefor No governmentservicesgovernment gettingtechnicaland were channeledthroughservices financialassistancefrom the SN becauseit isnot

the governmentand functional: it would beprivateagenciesand in conflict with the rune-facilitiesoutreachof tionsof the barrio coun-

governmentprograms cil: other governmentto ruralpeople, agenciesdo not coordi-

nate with the SN; andnot all barriopeopleare SN members.

8. SN asinstrument SN complements SN, asafacilitatingof land agrarianreform, bring- instrumentof landreform ingabout technical reform, is not appli-

changesand makingfar- cable.becausemanymersownersof the land SN areasare notthey till. coveredby land reform.

340 JOURNAL OF PHILIPPINE DEVELOPMENT

Actual conduct was abbreviated and only more than a half of SNscompleted their training courses. Agrarian reform message wasbetter absorbed than SN principles, and concept learning was notactually translated into actual behavior. In the area of capital build-up, despite some level of compliance with the savingprogram, prac-tically 90 percent of SNs regardedBSF and BGF collection asa prob-lem. Despite the trend in capital mobilization, SN is the only pro-gram which has succeeded in generating funds from farmers. Fort_20 per annum, with almost a million members, it had been possi-ble to raise nearly t=100 million in five years. Among the otherSN features, discipline was the least implemented, followed bylearning and saving.

Assessingthe SNs in general, 40 percent of SN members believedthat the SN movement was a success,11 percent thought it a failiJrewhile almost half were unsure. For thosewho saidthat the SN move-ment was a success,about one-third reasoned that the externalinput from the government such as the efficiency of the MunicipalDevelopment Officer (MDO), Bureau of Cooperative Development(BCOD) workers and the technician and the inspiring governmentattention and incentives for rural development contributed muchto the movement's success.About 70 percent attributed the successto themselves, to the wholehearted cooperation of members, andto the efficiency of officers and their honesty and integrity. About82 percent of the respondentsblamed the failure on the unwilling-ness and low capacity of members to settle their financial obliga-tions, on nonattendance in meetings, and on the inefficiency anddishonesty of SN officers. In general, an assessmentby local offi-cials and field workers showed that only a little over one-half ofthem were definitely positive about the SN project's successin thelocalities.

One successful cooperative is the Quinlogan Samahang Nayon.According to a study mad_ by the Special Task Force Division,Bureau of Cooperative Development of the Ministry of Local Go-vernment and Community Development, the successof the group(composed of 94 farmers) was due to the active role played bythe leaders of the SN; the participation of the members in everystageof program planning and implementation; the self-reliant spiritof the group members;and the timely extension assistanceprovidedby the government. The latter factor hasbeen recognizedasan indis-pensable component of a development program and a dominating

TAN: COOPERATIVE SYSTEM 341

factor in the successfuloperations of some SamahangNayons (Spe-cial Task Force Division, 1978).

Development Specialists international, Inc. (1981)found thatthe majority (72 percent) of the M-99 SN-farmers considered thetechnicians indispensableto the program. More than 80 percent ofM-99 and non M-99 farmers believed in the technicians becauseof

their credibility in providing advice on the choice of input andfarming techniques. Moreover, about 60 percent thought that far-mers should get production loans only when there is a technicianto supervisethe useof the loan.

The presenceof live-in technicians alsocontributed to the successof the Malatgao Samahan Nayon of Malatgao, Narra. Palawan. It wasnoted that one of its successfactors was the development of thecooperative spirit among the farmers (Qui_ones Jr. and Acasio1981). In consultation with the live.in technician, farmers agreedon What crop to raise in a given season, set the schedule of farmactivities from land preparation to harvesting, and implementedtheir common plan through group farming. Production on the 75-hectare farm was quite impressive.Rice stalksgrew at a uniform rate,pests were effectively controlled, water was efficiently managed,fertilizer application was uniform and harvests were bountiful.Becauseof this, this was the only SN among the sevenSNs that wasable to fully repay its loan for production inputs of t=6,630.00which it got from the Palawan National Agricultural College Per-sonnel Cooperative Credit Union, Inc. (PNACPCCUI) while theother six which got loans from the same source had total arrearsof over t=60,000.0U.

Perhapsit is assumedthat successfulSNs utilize or need a com-bination of inputs: credit, extension, participation by members inany aspectof SN activity, and a self-reliant spirit.

The Agricultural Marketing Cooperative (AMCs). The AMCsserve as the marketing arm of the Samahang Nayons but have notsufficiently participated in marketing activities to sustain the mar.keting needsof their SN constituents. The reasonsfrequently citedinclude the lack of capital, inadequate discipline and training, thelack of patronage by SNs, stiff competition posed by private traders,and the lack of competent personnel.Cegarial (1978), who studiedextensively the performance of AMCs, asserted that the level ofperformance of AMCs depended on five (5) major factors: (a) Ioc_tion wherein most AMCs were located along or near the main high-

342 JOURNAL OF PHI LIPPINE DEVELOPMENT

way and away from commercialcenters. While location is consideredstrategic, AMCs are not ableto put up outlets to service members infar-away places due to business uncertainty and lack of capital; (b)total amount of capital, in which the lack of capital could mean thesmall contribution of members and lack of responsibility of the mem-

bers in paying their loans and for the goods tl_ey acquired from theAMC on credit. Capital inadequacy could force the AMCs to special-ize in the sale of inputs, thus neglecting the marketing of the mem-bers' produce. Fund insufficiency could also force the AMCs to bor-

•row at usually high interest rates; (c) profitability of the business,wherein nonprofitability could mean the offering of AMCs at aprice sale of farm inputs lower than that of their competitors. Thissituation is further aggravated by high administrative expense; (d)members' participation, in which nonparticipation of some AMCmembers is due to stringent operating policies of the AMCs and thelack of coordination of the different agricultural programs. AMC'slack of capital could be a result of the small membership contribu-tions; (e) qualification of the manager and members of the Boardof Directors. Some 10 percent of the membership of the Board ofDirector's had not finished intermediate• education. Considering the

duties and responsibilities they are supposed to perform, their edu-cation did not give them a stamp of managerial competence andability.

A study of 15 AMCs and eight CRBs in 1980 revealed that fiveproblems beset the AMCs despite their Iocational advantages, theirpromising arrangement profile and conventional business practicesand procedures (ACCI 1980). These problems were the lack ofoperating capital, inadequate discipline and education among farmer-members, the generally weak support of 5N members, inadequatetraining and processing facilities, and the lack of extension personnel.

The Cooperative Rural Banhs (CRBs). The CRBs are the lendingarm of the SNs and the AMCs. Like•the AMCs, however, the CRBsfind themselves in difficult financial straits. According to TBAC

(1981), the uncertainty of the CRBs is brought on by their charac-teristics as follows: (a) small resources and uneconomic size of ope-rations; (b) paid-up capital, which comprises only about 20 per-cent of authorized capital and half of the CRBs, is still without coun-terpart equity from the government; (c) high borrowing costs•consti-tuting 64 percent of total resources; (d) generally profitable opera-

TAN: COOPERATIVE SYSTEM 343

tions, wherein return on evenues is negative at 2 percent, renderingeight of 28 in a precarious liquidity situation: (a) only 40 percent ofCRBs generated a net income during the period 1978-80 and almost

all incurred excessive expenses; (f).a half of the CRBs had pastdue ratios exceeding 25 percent, and the systemwide collection ratewas a low 57 percent; (g). insufficient loanable resources such asdeposits, capital and borrowings; (h) inability to effectively compete:(i) high incidence of mismanagement problems and conflicts, andlack of professionalism in managing most CRBs; and (j) lack of

•strong cooperative base and institutional linkages, lukewarm atti-tude of SN members in patronizing CRBs, and improper concept ofrole as owners and as borrowers.

Problems centered on the inadequate number of staff, the inade-quate loanable funds due to generally weak investment support givento member-SNs; increasing past-due loans dueto difficulty in obtain-ing a closer coordination with full support from SNs and AMCs ineffecting a systematized collection scheme, and the dole-out mental-ity of 5N members-borrowers; and the lack of farmers' generalknowledge or negative attitude towards normal loaning policies andprocedures of the bank so much so that these farmers resist normalprocedures of submitting basic documents, question the CRB'ssystem of appraising collaterals, and get impatient when loan releasesare delayed.

Other Types of Cooperatives. Mixed trends characterize the per-formance of the other farmer-based or rural-based cooperatives.Some have miserably failed while others succeeded.

Among the cooperatives that failed is the moshav-type GeneralRicarte Agricultural Cooperative, Inc. (GRACI)in Nueva Ecija.Started in 1975 with the technical assistance of Israeli consultants

and massivegovernment management and credit support, it focusedon rice and poultry production. It fared well in its first few yearsbut began to taper off a few years later. Failure could be attributedto the following factors; (a) the Ricarte farmers were not able torespond well to the sudden inflow of wealth. With savingsawarenessunknown to them, household appliances and unnecessary items werebought during their buying sprees, (b) with the initial successof thepoultry business, the farmers poured their resources into this activityat the expense of their crops. As a result, when the poultry businessfailed due to poor quality of feeds, diseaseand poor marketing, the

344 JOURNAL OF PHI LIPPINE DEVELOPMENT

farmers had no way of bailingthemselvesout; (c) the government, inits effort to aid the farrners, unwittingly introduced to them the"dole-out" mentality; (d) due to the multiplicity of agenciesin thearea, the source of the problem could not be pinpointed; (e) fundswere reportedly diverted to other purposes by the cooperative'sofficers, leading to a complete lack of interest on the farmers'side;(f) the technology brought by the Israelis was not completely ab-sorbed by the farmers such that, when the former left, most of theprojects had to be abandoned; (g) there wasa basicconflict betweenthe Barangay Council and the cooperative officers, resulting in mu-tual distrust; and (h) there was no binding force among memberssuch that the cooperatives were organized only during good timesand by-passedduring bad timeswithin the cooperativecycle.

Montemayor studied the Kalasungay Free Farmers' Cooperative,Inc., located in Malaybalay Bukidnon. It is a credit cooperativewhich later on branched into other activities by establishinga con-sumer cooperative store and a marketing section to service theinput and output marketing needs of its members. It was foundedas a small credit union of 16 members in 1969 but after three yearsbecame a registeredcooperative with t=13,800 in fixed savingsdepo-sits to start with and 75 membersin its fold. It wasduringthe period1973-82 that the cooperativegrew at a considerablepacein termsofits volume of loans granted and repayment and marketing andcooperative store sales.

In early 1983, however, the cooperative slowly failed. Membercontributions dwindled to low levels, marketing and store salesvolume dipped substantially and the repayment rate was a measly49 percent. Montemayor attributed the failure to the following rea-sons: Fund mismanagement. When two of the top cooperative offi-cers were sent to Manila to conduct training on financial and busi-ness management, they failed to formally relegate their functionsto appropriate persons. During their absence, there was rampantfund misuse by those at the helm of operations. Although the twoeventually turned the operations around on their return, the damagehad been done and could not be rectified in a short period of time;Shrinking land size. As early as 1980, a large coffee-based food com-pany started leasingthe lands of farmer-members. By 1982, almost60 percentof farmer-members' total landholdingsalready were in thehands of the food firm, leaving the farmers with no more than ahomelot to plant something on. With no more lands to till, there was

TAN: COOPERATIVE SYSTEM

no steady source of income to rely on; Fundissue. Farmers areentitled to a large sum of money payable every five years as pay-ment for the leaseof their landsby the food company. The farmers,however, lured by the illusion of money, began a wanton spendingspree upon receiPt of the first payment in 1980 with the hope that

• their jobs as casual workers in the coffee company would tide themover. It was too late becauseafter they had spent their leasepro-ceeds, they suddenly felt that their wagesfrom the food outfit werebarely enough for them. In the meantime, nothing wasadded to theircontributions. In fact, they becamenet borrowers; Thin distributionof time and efforts by cooperative officers. During the 1981 ba-rangay elections, many .of the cooperative officers ran and won asbarangay captains and councilmen or Kagawad.This, however, wasultimately inimical to the cooperative as the officers became busywith their new posts and neglected the cooperatives; Drought.The protracted eight-month brought from October 1.982 to May1983 exacted a heavy toll on the farmers' produce. There was nocorn harvestedand abaca wilted away, thus leavingthe farmers withno other recoursebut to borrow from the union which by then wasitself running out of funds.

Other cooperativesthat failed were the farmer-basedcooperativesin the towns of Narra and Aborlan, Palawan.TBAC (1981) conduc-ted severalcasestudiesof someof these cooperativesin two towns in1981.

The Car-Gum Credit Cooperative was set up in 1969 starting withthree members only. In early 1975, its members grew to 1972, and

they believed that they were about to scale greater heights. Theunion expanded its businessby enagagingin the sari-saristore busi-nesswith wares provided by the PNAC Cooperative Store, and byacquiringa solar and mechanicaldrier, a warehouse,a rice mill andathresher. Suddenly in mid-1975, the cooperative's membershipthinned out and lanquishedin painful failure. It all started with onedeal involving a t=15,000 loan from the PalawanNational Agricultu-ral College (PNAC) for the purchaseof farm inputs. A similar dealfor _=11,000 was hatched earlier in 1974 but wasfully paid in early1975; hence the second loaning line. The full amount oft=15,000was used for fertilizers, and the transaction was proper except thatthe fertilizers were fake. This wasa self-destructingendeavoras farmcrops began to wilt, feeling the catastrophic impact of the bogusfertilizers. Because of these, the farmer-members lost interest in

346 JOURNAL OF PHILIPPINE DEVELOPMENT

their cooperative and the latter wasnever the sameagain.The Narra Proper CooperatiVe Credit Union (NPCCU) seems to

be an adjunct failure of the Car-Gum Credit Cooperative. Establishedin 1972, it operated briefly before it disintegrated ih 1975. Sincethen, membership meetihgs became scarceand far between until, in1980, the union was nothin_ more than a skeleton haunted by anoutstanding debt of over ]=15,000 in favor of PNAC from an origi-nal loan of ]=12,880 in 1972. The cooperative union failed to re-register in 1975, for reasonsof lack of interest among its membersand lossof confidence in the leadership,arising from the dissipa-tion of funds without thorough explanation. Some of the reasonswhy this cooperative failed were: (1)dishonesty of incorporatorsand board membersJofflcers. The monthly, amortizations or contri-butions of members were channeled to personaluseby incorporatorsand union officers; (2) lack of cooperative training among coope-rative members. Most farmer-members had not kept tabs on theirrole _.scooperative members either because they were ill-trained,lacked trainors or were simply indifferent. Farmers join to. get achance to make a loan; (3) inadequate loan capacity and fundsmismanagement; lneffectivit_.y of extension. Extension workers werenot full-time workers since most of them had businessconcerns of

their own. (4) overselling of the cooperative movement. Championsof PNAC-motivated cooperative movements allegedly promised alot to would-be union members only to renege during hard times.However, not all cooperatives were failures. Many nonagricultraland even agricultural cooperatives attained some measureof success.

Montemayor (1983) conduc_teda case study on the Davao delNorte Free Farmers'Cooperative , Inc., which is situated in _asmalltown in Tubod, Davao del Nofte. The study attributed the successof the DFFCl cash bond program to the following: timely creditaccessibility, implemcntors' credibility, effective repayment scheme,provision of allied services,'staff support, and continuous member-ship education and organization. From a limited participation ofonly 18 depositorsand 20 borrowers in 1980, the program grew toaccommodate 148 members and 103 borrowers in 1982. Loans

increasedsignificantly from only t=8,000 in 1980 to a high ?=224,000in 1982 with a respectable repayment rate of 95.0 percent duringthe three-year period. The DFFCI cash bond program, while onlyabout three years old, promised to be a reliable sourceof credit inthe countryside. The. program could have become a showcaseof

TAN : COOPERATIVE SYSTEM 347

farmer-contrived lending and of a savingsscheme had the DFFCIbeen able to Competewith private traders on the purchaseof mem-bers' produce. Lack of marketing facilities and serviceshindered thecooperative in its marketing operations.

2. Summary of Recommendations

1. One of the major lessonswhich can be learned from the failuresof SNs and other cooperative is that, in areas where there islittle economic activity, cooperativesengaged in trade are notlikely to succeeddue to the smallnessof the economic base.Thus, before embarking on a cooperativedevelopment scheme,an assessmentof the influence area, as well asof the feasibilityof the business proposed to be established, should first bemade. Another lessonis the lack of preparation of cooperativemembers to assumeresponsibility. Lack of disciplineand train-ing has also hampered their operation. Thus, an honest-to-goodness discipline-oriented program should be faithfullyundertaken before even forming a cooperative.

2. Suggestionsfor the AMCs and CRBs are: minimization of redtape in program implementation and aid to cooperatives;reduc-tion in the extension of credit to membersand regular auditingof the accounts; lessgovernment control on the internal affairsof the cooperative; continuous education on the part of themembers as well as personnel of the cooperative; continuousfinancial and technical aid; and government action on erringofficials and the creation of the Ministry of Cooperatives.

3. Villamin (1982) believes that the cooperatives will generatecapital from the government sector for its implementation.He noted that funds for cooperativesare accumulating in bankaccountsand have reachedsubstantial proportions.

4. Another recommendation is the integration of the nonagricul-tural cooperatives in the government lending schemefor coope-ratives.

It would seem that, on the basis of longer-term market poten-tial, there are a number of other cooperatives classified as non-agricultural which are in need of financial assistance.Thesealsoserve

farmers, fishermen and agri-businessprojects, have a sounder finan-cial condition, andare in a more advancedstageof development than

348 JOURNAL OF PHILIPPINE DEVELOPMENT

are agriculturalcooperatives to which the CMP isdirected.

C. Studieson Other Rural-BasedOrganizations

1. Focus or Credit and Credit-Reloted Aspects

Some rural-basedorganizationsare farming well while otherscould not perform creditably.

The United States Agency for International Development(1983) and the Bicol River BasinDevelopment Project did anextensive evaluation of three irrigation projects within the BicolRiver Basin Development Project influence area. These are the

• Libmanan-Cabusao, Bula-Minalabac and Rinconada-Buhi/Laloirrigation projects.

The study was on (1) the capability of the various farmer• groups to eventually, take over the management of the water

systems, (2) the viability of farmer organi_cations,and (3) bot-tom.up participatory planning and credit use. The three irri-gation projects started at different times - the Libmanan-Cabusao in. 1975, the Bula-Minalabacin 1978, and the Rinco-nada-Buhi/Lalo in 1979. Despite an early lead, the Libmanan.Cabusao is trailing behind the other two in many respects.The Libmanan-Cabusaoproject also has the highest•costover-run from the originally approved costing confirmation. Theestimate is that it will in•cura cost overrun of 84.97 percentwhen finally completed. Bula-Minalabac's overrun will be at alower 65.28 percent while Rinconada.Buhi/Lalo's would benegligibleat 12.15 percent.

The major objective of the three projects was to increaseproduction and the income of farmers through efficient deli-very of water, improved crop•production techniquesand timelyapplication of inputs and credit and the.sufficient availabilityof extension services and marketing facilities. Some positiveand negative impacts have been noted due to the projects in-cluding: (a) increasedcollection rates for both property andbusinesstaxes in the, municipalities affected by the projects.The records •show that these increasescoincided with the in-troduction of the irrigation, systems: (b) readily apparenthousing improvements in the areas. In addition, there wasevidence of increased backyard farming, mainly in livestock

TAN: COOPERATIVE SYSTEM 349

production, including a proliferation of ducks; (c) land valuesappear to have increased, e.g., from an estimated preprojectvalue in Libmanan-Cabusaoof_=3,S00 per ha. to a current valueof t=12,000 per ha.; (d) increased, businessand employmentopportunities, both in terms of farm employment and sup-porting services, with small private enterprises sprouting;(e) greater variety and amounts of consumerdurablesand capi-tal investment in stores and homes; (f) strengthenedtransportstructure with more vehicles and a much reduced transportcost; (g) greater availability of water for bathing, drinking,watering, livestock, and the like; and (h) improvedfish suppliesand lessproblems of flooding, drainage, soil erosion and salini-zation.

The farmer-group badly needed more credit support to furtherdiversify farm activities. The evaluation also noted that the farmers'incomesoutside the project areasdeclined in real terms vis-a_-vistheconsumer price index. While the evaluation did not mention the realincomesvis._-visthe consumer price index insidethe project areas, itmay be assumedthat the problem wasalso true insidethese projectareas although to a lesserdegree.This setback shows that the pricesystem did not improve the farmers' incomesfrom rice production.It should be noted that, due to the project, some private enter-prisessprouted. Given the right planning and management, the proj-ect site may yet become a showcasefor successfulintegrated area-specific financing and development. Casesof conflicts among bene-ficiaries and lack of discipline and leadership are well highlightedin a case study conducted by Plana (1983). She observed that thelow irrigation fee collection in the Walang Tanggihan IntegratedService Association Service area was due to the poor disciplineamong farmers. The problem of poor cooperation and lack ofdiscipline by farmers was aggravatedby the lack of strong leader-ship and inadequate NIA supervision.Because of this, the tractorfor communal use that was being amortized was foreclosed bythe bank since it could not be paid due to low fund levelsgenera-ted by the group. Many were not willing to pay due to conflicts ininterest rate in the useof irrigation.

Experiencesof the Philippine Businessfor Social Progress(PBSP)financing rural-basedgroups are worth mentioning (Paz Cruz, Valera1979). The PBSP has given financial and technical management

350 JOURNAL OF PHILIPPINE DEVELOPMENT

assistanceto more than 25 agribusiness projects, one of which is the

group made up of 44 farmer-members of the Bisig ng MagsasakainBiEan, Laguna. In addition to a financial advance of P87,000, thePBSP would initially manage the project. The project involves theorganization and operation of a "Farm Service Center" to be man-aged by the farmers themselves. The center envisions to promoteimproved farm practices, input and output marketing, and incresedagribusiness knowledge. After one and a half years of operations,the average family income of farm-households increased fromP5,289 to _7,764.00 per year and savings increased from P24.30to P_6"/.07per month.

Another project worth noting is the Sta. Cruz, Davao del Sur smallfishermen development project, which was successfully implementedin 1973 with the construction and sale of 2.4 fishing boats to 24fishermen through a P20,O00 PBSP financial assistance. This loanwas completely repaid in April 1978. Also in the area of fishing,eighteen fishermen in General Santos City, South Cotabato, got someP_31,200 from the PBSP for the purchase of six fishing boat_ plusP20,O00 in grant for educational program purposes. Fishing opera-tions commenced in October 19"/4. From September 1975 to Feb-

ruary 1976, fishing boat operations improved, resulting in a 51.3percent increase in gross production and a 23.0 percent increase insales compared to 1974. The following year, however, saw a steepdrop in production due to bad weather piracy. Fishermen wereconstrained to amortize the boats which they bought. In the mean-time, they launched a massive capital buildup campaign by deduct-ing 5 percent of the net sales of fishermen through the fixed andsavings deposits made by the fishermen with the associations untilthey can pay off their amortization.

Other informal farm-based groups are the compact farms whichare the handiwork of the Agricultural Credit Administration (ACA).Studies show that the compact farm program suffers from severalweaknessesand constraints (TBAC 1981 ). The volume of operationsis not large enough to enable farm management to generate econ-omies of scale for the members' benefit. Diversification through

forward and backward linkages is not feasible due to limitedresources. Production yield, however, has improved considerably,ranging from 74 cavans/ha, to 113 cavans/ha. This is due primarilyto efficient farm management, provision of extension services bythe MA and ACA technicians, and timely release of loans. Despite

TAN: COOPERATIVE SYSTEM 351

this, nonetheless, farmers at times suffer low returns due to risinginput prices, inadequate postharvest facilities, low output prices,andsometimesevenlack of markets.

Castillo (1978) also studied compact farms, and observedthat there was evidence of group participation among compactfarm members when it came time to obtain loans. The most fie-

quently mentioned reasons for joining the compact farm were:availability of low interest loans and farm supplies, the desire toincreaseproduction, the chanceto learn modern methodsof farming,and the availability of technical assistance.Decision of members tostay on depended on the continuing availability of these advantagesof credit, efficient farm management, technical assistanceand desireto increaseproduction. Another reasoncited was the pleasant com-pany of other members. Disagreement among members, inefficientmanagement and compulsion to pay loans and buy unnecessaryinputs were some reasonsfor quitting.

For seldas which are loosely-organizedsmall farmer groups, Mon-temayor comparatively studied five compact farms in Nueva Ecija,Bulacan and Iloilo and five seldas in Infanta, Quezon. In his study,most farmer-members in compact farms experienced decreasesrather than increasesin harvests due to high costs of productionand natural calamities. Farmers belonging to the seldas increasedtheir net income levelsunlike before, suggestingthat inadequatepricesupport negatively affected compact farm operations and that theselda'sproduction levelsmay haveoffset increasesin farm inputs.

2. Summary of Recommendations

With respect to other rural-based groups, the following are sug-gested: (a) project implementation should include the project bene-ficiaries even during the project planning stage, implying that thebeneficiaries themselvesshould be aware of what the project hopesto achieve. Discipline and identification of a strong leader to bechosen by the farmers themselvesshould be instilled; (b) follow-upof the project, educational and skills training and the provision oftechnical and credit assistancecould play a major role in the project,as in the experience of the PBSP; (c) credit alone is not "the" mainfactor in project development. Production may increaseand man-agement capability may have improved but the members' soci_economic status may remain the same or deteriorate due to the proj-

352 JOURNAL OF PHILIPPINE DEVELOPMENT

ect. Pricing and marketing support and their importation, again,cannot be overemphasized.The compact farm experience should bean eye-opener; (d) a savingscampaign should be an integral part ofthe project especially in caseswhere credit is not forthcoming, asin the case of the PBSP-funded fishing boat project in Davao delSur.

III. CONCLUSION

Evidences suggest that cooperatives and other rural-based organi-zations can still becomea potent set of small producer associationscapable of developing income-generating activities for the benefitof their members, provided they get assistanceand benefit froman appropriate policy mix.

The new dispensationhascontinued to show concern for the devel-opment of rural-based cooperatives and farmers' organizations.This is underscored in the country's national development plan(1987-1992) where the cooperatives will remain to play a majorrole in the advancementof their members' interests.

Government policies to promote cooperatives have proven tobe viable. As a result, various cooperative development programs,notably the Cooperative Development Loan Fund (CDLF), were asuspendeddue to low repayment rate on loans and to insufficientviability of the cooperatives' economic activities. One factor thatstands out after a review and analysis of cooperatives' failures isthe need for extensive training among cooperative members on thenuanceson how to get a cooperative system going.Thus_the govern-ment thrust in this regard is to make certain such training needsaremet.

REFERENCES

AgriculturalCreditCooperativeInstitute."An Evaluationof Area MarketingCooperativesandCooperativeRuralBanks."LosBa_os,Laguna,1980.

Castillo,Gelia. "ChangingRural InstitutionsandParticipatoryDevelopment:Reviewof PhilippineExperience."PhilippineInstitutefor DevelopmentStudies,1982.• "SarnahangNayon: A New Designfor CooperativeDevelopment."Makati1979.

Cigaral,Domingo,"Short-TermAgriculturalCredit Repaymentin CentralLuzon."LosBaEos,Laguna,1974.

TAN:COOPERATIVESYSTEM 353

DevelopmentSpecialistsInternational, Inc. "An Evaluation of the ExtensionSystemin the Philippines."Manila, 1981•

Ibafiez, Roy. "Savings Mobilization and Capital Formation in Three SelectedProvincesin the Philippines." University of the PhilippinesBusinessFoundation,QuezonCity, 1978.

Montemayor, Raul. "A CaseStudy of the Davaodel Norte FreeFarmers'Coop-erative,Inc." Central Bank, 1983•

. "A CaseStudy of the KalasungayFree Farmers'Cooperative." Manila,1983.

Plana, Teresita• "A Case Study of the Walang Tanggihan Integrated ServiceAssociation."1983.

QuiEones, Benjamin Jr., and Ellen Acasio. "A CaseStudy of the MalatgaoSamahangNayon." Central Bank, 1981•

Special Task Force Division, Bureau of CooperativeDevelopment. "A CaseStudy of the QuinloganSamahangNayon." QuezonCity, 1978.

Tan, Victor A. "Loan Portfolio Analysisof a Typical AgrarianReform Bene-ficiary in the Philippines:A CaseStudy." In Proceedingsof the Interna-tional Conferenceon SystemsModeling, Bangkok,Thailand, 8-11 May1978.

Technical Boardfor AgriculturalCredit (TBAC). "Agricultural Financingin thePhilippines."CentralBank, 1980.. "A Study on the Nonrepayment of Agricultural Loans in the Philip-pines." Manila, 1978.• "A Study on the Informal Rural FinancialMarkets in Three SelectedProvincesof the Philippines."Manila, 1981.• "Case Studies of Farmer Organizations in Selected Areas." CentralBank,1981.. "Socio-EconomicSurvey on LandlessRural Workersin Three SelectedBarangays."Manila, 1983.• "Study of CooperativeFinancein the Philippines.."Manila, 1983.

United StatesAgency for InternationalDevelopment. "An Evaluationof ThreeIrrigationSystemsin the BicolRiver Basin."Pili, CamarinesSur, 1983.

Valera, Paz Cruz, ed. PhilippineBusinessfor Social ProgressAnnual Report,Makati, 1979.

Villamin, Romulo. "Toward a Banking System for Cooperatives." QuezonCity, 1982.