an overview of fdi concepts and the significance of fdi in...

TRANSCRIPT

An Overview of FDI Concepts and the Significance of FDI in BRIC and in

India

43

CHAPTER III

AN OVERVIEW OF FDI CONCEPTS AND THE SIGNIFICANCE OF

FDI IN BRIC AND IN INDIA

3.1 Conceptual Understanding of Foreign Direct Investment

Trade has always been a vital part of economy and with the concept of

globalization it reaches to the international level. Foreign direct investment (FDI) has

proved to be resilient during financial crises. The role of Foreign Direct Investment (FDI)

in this development is very crucial. It is widely recognized that foreign direct investment

(FDI) produces economic benefits to the recipient countries by providing capital, foreign

exchange, technology and by enhancing competition and access to foreign markets.

Foreign Direct Investment take place when an investor based in one country acquires

asset in another country in this process, the company investing in the host country also

transfers assets such as technology, management and marketing.

In addition to this the investing company also get chances of power to exercise

control over decision making in a foreign land enterprise to the extent of which it held

equity control such investment could also be in the form of reinvestment of earning in the

shape of retained earnings by the host country‘s enterprises that also strengthen the

control of foreign investors.

3.1.1 Definition of FDI as per IMF and OECD

According to the IMF and OECD definitions, direct investment reflects the aim of

obtaining a lasting interest by a resident entity of one economy (direct investor) in an enterprise

that is resident in another economy (the direct investment enterprise). The ―lasting interest‖

implies the existence of a long-term relationship between the direct investor and the direct

investment enterprise and a significant degree of influence on the management of the latter.

Direct investment involves both the initial transaction establishing the relationship between the

investor and the enterprise and all subsequent capital transactions between them and among

affiliated enterprises, both incorporated and unincorporated. It should be noted that capital

transactions which do not give rise to any settlement, like an interchange of shares among

affiliated companies, must also be recorded in the Balance of Payments and in the IIP.

44

The fifth Edition of the IMF‘s Balance of Payment Manual defines the owner of

10 percent or more of a company‘s capital as a direct investor. This guideline is not a

fast rule, as it acknowledges that smaller percentage may entail a controlling interest in

the company (and, conversely, that a share of more than 10 percent may not signify

control). But the IMF recommends using this percentage as the basic dividing line

between direct investment and portfolio investment in the form of shareholdings.

Thus when a non-resident who previously had no equity in a resident enterprise,

purchases 10 % or more of the shares of that enterprise from a resident, the price of

equity holdings acquired should be recorded as direct investment. From this moment, any

further capital transactions between these two companies should be recorded as a direct

investment. When a non-resident holds less than 10 per cent of the shares of an enterprise

as portfolio investment, and subsequently acquires additional shares resulting in a direct

investment (10 per cent of more), only the purchase of additional shares is recorded as

direct investment in the Balance of Payments. The holdings that were acquired previously

should not be reclassified from portfolio to direct investment in the Balance of Payments

but the total holdings should be reclassified in the IIP.

Concerning the terms direct investor and direct investment enterprise, the IMF

and the OECD define them as follows.

Direct Investor: A direct investor may be an individual, an incorporated or

unincorporated private or public enterprise, a government, a group of related

individuals, or a group of related incorporated and/or unincorporated enterprises

which have a direct investment enterprise, operating in a country other than the

country of residence of the direct investor.

Direct Investment Enterprise: A direct investment enterprise is an incorporated or

unincorporated enterprise in which a foreign investor owns 10 per cent or more of the

ordinary shares or voting power of an incorporated enterprise or the equivalent of an

unincorporated enterprise.

Direct investment enterprises may be subsidiaries, associates or branches that

could establish in the foreign country.

45

A subsidiary is an incorporated enterprise in which the foreign investor controls

directly or indirectly (through another subsidiary) more than 50 percent of the

shareholders‘ voting power. An associate is an enterprise where the direct investor and its

subsidiaries control between 10 percent and 50 percent of the voting shares. A branch is

a wholly or jointly owned unincorporated enterprise such as general partnerships and

limited partnerships.

It should be noted that the choice between setting up either a

subsidiary/associate or a branch in a foreign country is dependent, among other factors,

upon the existing regulations in the host country (and sometimes in its own country, too).

National regulations are often more restrictive for subsidiaries than for branches but this

is not always the case.

In the case of affiliated banks (depository institutions) and affiliated financial

intermediaries such as securities dealers, transactions recorded under direct investment

are those associated with permanent debt (loan capital representing a permanent

interest) and equity (share capital) investment.

In the case of branches, they are fixed assets. Deposits, loans and other claims

and liabilities related to usual banking transactions of depository institutions and of other

financial intermediaries are classified, as appropriate, under portfolio investment or

―other investment‖, but never as direct investment. The stock of foreign assets and

liabilities of banks and other financial intermediaries should be treated in a parallel

manner.

The OECD recommends in its Benchmark definition that for the existence of a

direct investment relationship the ―full consolidated system‖ should be followed. In other

words, it means that when there is a cascade of participations, the percentage of the parent

company in any affiliated companies should be calculated assuming the 100 percent of the

subsidiaries and the corresponding percentage of the associates. This criterion does not

correspond with the consolidation concept in the accounting statement.

From an accounting standpoint, bank branches are wholly considered as being an

integral part of their parent company and, therefore, do not have separate accounts.

However, the requirement for affiliated companies to be included in banks’ consolidated

46

financial statements is two fold: (i) they themselves must carry out a financial activity;

and (ii) at least 20 percent of their capital must be owned by their parent bank, together

with the latter‘s exerting an effective control over them. Non-compliance with any of

these requisites entails that the affiliated company is not consolidated, although it should

be valued according to the ―equity method‖ in its parent bank‘s financial statements.

In accordance with these consolidation rules, a bank will not include in its consolidated

statements the assets and liabilities of all its associates, despite the fact that such

associates may obviously be direct investment enterprises from a BOP/IIP viewpoint.

3.1.2 Valuation of FDI flows and stocks and relations between both of them

The Balance of Payments and the International Investment Position are compiled

under the same framework of methodological rules laid down in the Fifth edition of the

IMF Balance of Payments Manual. According to this, FDI transactions should be

recorded in the Balance of Payments at the accrued value, i.e. ―transactions are

recorded when economic value is created, transformed, exchanged, transferred, or

extinguished”. Thus, the flows recorded do not necessarily coincide with the liquid

proceeds and payments generated. In practice, it is very difficult to apply the accrued

principle to all transactions and many of them are therefore recorded at the time when the

proceeds or payments are generated.

3.1.3 Motives of FDI

One way of viewing FDI is in terms of natural (unskilled workers)

or created (skilled, professional workers) assets.

FDI can be either vertical (investing in suppliers, distributors, retailers) or

horizontal (investing in the same type of firm).

There are a variety of motives for a firm to engage in FDI:

Resource-seeking (location-specific)

Market-seeking (more about responding to market need than reducing costs)

Efficiency-seeking (choosing element in vertical FDI which will be most

beneficial to the company)

47

Strategic asset-seeking (created assets)

Trade/import substituting (requiring FDI to direct trade to avoid customs etc.)

3.1.4 FDI and Entry Modes

The choice of entry mode is considered a strategic decision by the foreign

investor. The key driving forces in such decisions depend on the investor‘s interest in

seeking resources, markets, and efficiency or strategic asset ownership in the host

country. While the major motive of any investment is profit, a firm may opt for a

particular entry strategy best suited to its short- or long-term interests. Basically, FDI can

be wholly owned or joint ventures and Foreign Direct Investment (FDI) inflows can take

place through any of the following entry modes:

Greenfield investment: Direct entry of foreign firms into host country is known as

―Greenfield‖ investment. A form of foreign direct investment where a parent company

starts a new venture in a foreign country by constructing new operational facilities from

the ground up. In addition to building new facilities, most parent companies also create

new long-term jobs in the foreign country by hiring new employees.

Cross Border Merger and Acquisition (M&A): A cross-border merger is a transaction

in which the assets and operation of two firms belonging to or registered in two different

countries are combined to establish a new legal entity. In a cross-border acquisition, the

control of assets and operations is transferred from a local to a foreign company, with the

former becoming an affiliate of the latter. The acquisition of existing domestic firms is

known as ―Cross Border Merger and Acquisition (M&A)‖ investment. The motives of

Cross-border Merger & Acquisitions include: the search for new markets, increased

market power and market dominance; access to proprietary assets; efficiency gains

through synergies; greater size; diversification (spreading of risks); financial motivations;

and personal (behavioural) motivations.

In a cross-border merger, the assets and operations of two different firms

belonging to two different countries join together to form a new legal entity. The stocks

of the companies are surrendered during the amalgamation process and the new

company‘s stocks are issued in the process. One such example is the merger of Essar and

48

Hutchison to form Hutchison Essar. As another example, Daimler-Benz and Chrysler

ceased to exist when the two firms merged, and a new company, Daimler Chrysler, was

created.

In a cross-border acquisition, the control of assets and operations is transferred

from a local to a foreign company. The local company ceases to exist and becomes an

affiliate of the foreign company. An acquisition can be forced through a majority interest

in the management, by purchasing shares in the open market, or by offering a take-over

proposal to the general body of the shareholders. For instance, Ranbaxy Labouratories as

part of its expansion strategy in the US market acquired the New Jersey-based Ohm

Labouratories in 1995. Vodafone‘s acquisition of Hutchinson Essar and Lenova‘s

takeover of IBM´s PC business are more recent examples.

Equity FDI may also include ―Brownfield investment‖, a term often used in the

FDI literature. This represents a hybrid of Greenfield and M&A foreign investment. Such

investment formally appears as M&A, though its effect resembles Greenfield investment.

In Brownfield investment, the foreign investor acquires a firm and undertakes near-

complete renovation of plant and equipment, labour and product lines (UNCTAD 2000).

Other primary modes of FDI entry including wholly Owned Enterprises (WOEs),

Equity Joint Ventures (EJVs), Contractual Joint Ventures (CJVs) and Joint Stock

Companies (JSCs) according to a mode of entry study carried out in China by Wei, Liu

and Liu, 2004. As already seen foreign direct investment (FDI) constitutes three

components; viz., equity; reinvested earnings; and other capital. These are the modes of

FDI that comes into a country under equity FDI.

3.1.5 Discrepancies in FDI data

As for the international comparison of data, despite a common international

methodological framework, discrepancies between countries do occur. In fact, the

worldwide discrepancy between outward and inward direct investment flows should be

zero, if all flows were recorded fully and consistently by both sides. Nevertheless,

according to Lipsey (2001) “the asymmetries have been no higher than 8 percent in any

year from 1993 to 1999, as contrasted with 40 or 50 percent for portfolio investment”.

49

Discrepancies are mainly due to the use of different criteria for valuation or for

geographical allocation of transactions. The increasing complexity of enterprise groups

poses a further challenge to the correct application of the directional principle for

accurately assessing FDI. Similarly, it is rather difficult to consistently capture loans

granted to or received from related enterprises and they are often incorrectly considered

as ―other investment‖, rather than as ―direct investment‖. This problem does not arise,

however, in the case of loans between banks since they are not considered as ―direct

investment‖. Additional circumstances resulting in discrepancies between countries are,

among others: the lack of information on reinvested earnings, the use of a percentage-

ownership threshold different from the recommended 10 percent level for identifying an

investment as direct, and the use of different reporting systems and exemption threshold

by countries for collecting and aggregating data on international transactions. Most

countries use a combination of sources to compile their balance of payments and

international investment position statistics. Data collection may be based on the

compulsory reporting of individual transactions or on aggregates, or alternatively data

may be collected by the statistical agency from an intermediary (such as a dealer that

handles security transactions for clients) or directly from the transactor by means of

mandatory surveys.

3.1.6 FDI and Economic development

FDI plays an important role in the transmission of capital and technology across

home and host countries. FDI inflows benefit the economic development of the host

country at large especially to developing economies which need more capital for its

economic development. These benefits are expected to be positive, although not

automatic and it may impact growth either directly of indirectly. Also these benefits may

have different levels of impact for different countries based on the sector of investment,

its quality and volume. The working assumption nowadays is that in a relatively

non-distorted domestic policy environment, foreign direct investment (FDI) brings in

much-needed capital, technical know-how, organisational, managerial and marketing

practices and global production networks, thus facilitating the process of economic

growth and development in host countries.

50

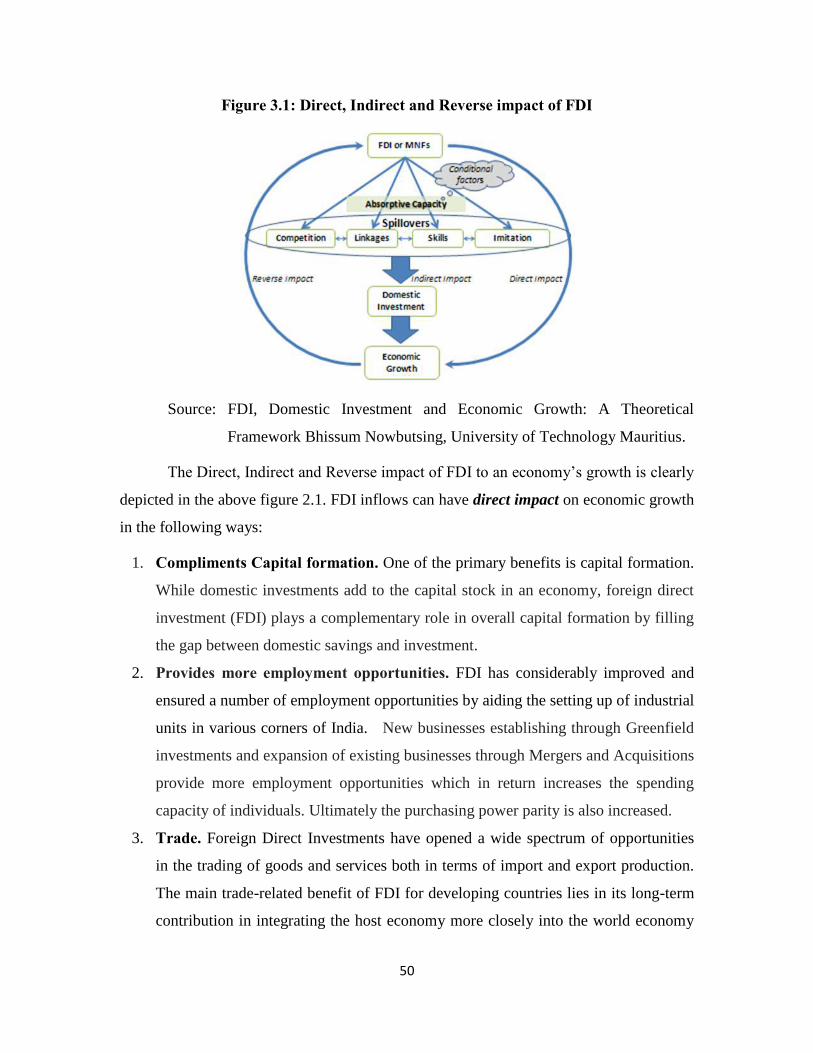

Figure 3.1: Direct, Indirect and Reverse impact of FDI

Source: FDI, Domestic Investment and Economic Growth: A Theoretical

Framework Bhissum Nowbutsing, University of Technology Mauritius.

The Direct, Indirect and Reverse impact of FDI to an economy‘s growth is clearly

depicted in the above figure 2.1. FDI inflows can have direct impact on economic growth

in the following ways:

1. Compliments Capital formation. One of the primary benefits is capital formation.

While domestic investments add to the capital stock in an economy, foreign direct

investment (FDI) plays a complementary role in overall capital formation by filling

the gap between domestic savings and investment.

2. Provides more employment opportunities. FDI has considerably improved and

ensured a number of employment opportunities by aiding the setting up of industrial

units in various corners of India. New businesses establishing through Greenfield

investments and expansion of existing businesses through Mergers and Acquisitions

provide more employment opportunities which in return increases the spending

capacity of individuals. Ultimately the purchasing power parity is also increased.

3. Trade. Foreign Direct Investments have opened a wide spectrum of opportunities

in the trading of goods and services both in terms of import and export production.

The main trade-related benefit of FDI for developing countries lies in its long-term

contribution in integrating the host economy more closely into the world economy

51

through higher imports as well as exports. In other words, trade and investment are

increasingly recognized as mutually reinforcing channels for cross-border activities.

When domestic savings and investment are incremented by foreign investments it

results in increased trade and productivity which will in turn provide more employment

and growth in foreign exchange earnings of a country. Ultimately contributes to an

increase in the Gross Domestic Product and thereby ensuring economic growth.

The indirect impact of FDI inflows to a country can be in the form of:

The indirect benefits are otherwise called as spillover benefits. The most common

factors are:

1. Competition. FDI and the presence of MNEs may exert a significant influence on

competition in host-country markets. However, since there is no commonly

accepted way of measuring the degree of competition in a given market, few firm

conclusions may be drawn from empirical evidence. The presence of foreign

enterprises may greatly assist economic development by spurring domestic

competition and thereby leading eventually to higher productivity, lower prices and

more efficient resource allocation.

2. Linkages. Vertical (backward and forward) linkages with suppliers or purchasers in

the host countries and horizontal linkages with competing or complementary

companies in the same industry will improve the efficiency of domestic suppliers

and enhances the domestic competitor‘s quality of business.

3. Technological and Managerial skills. FDI apparently benefits indirectly through

knowledge spillovers like; managerial skills and latest technology acquired from

foreign enterprises. This may result in domestic businesses and also enhances the

quality of domestic human capital.

4. Imitations. FDI has the potential to bring social and environmental benefits to host

economies through the imitation and dissemination of good practices and

technologies within MNEs, and through their subsequent spillovers to domestic

enterprises.

52

5. Improves the standard of living. Higher tax revenue from the foreign firms will

increase government spending on people‘s benefit. And the new jobs created

increases the purchasing power and thereby acquiring better standards of life.

6. Human capital enhancement. The major impact of FDI on human capital in

developing countries appears to be indirect, when the host country individuals are

employed by MNE subsidiaries, their human capital may be enhanced further

through training and on-the-job learning. Those subsidiaries may also have a

positive influence on human capital enhancement in other enterprises with which

they develop links, including suppliers. Such enhancement can have further effects

as that labour moves to other firms and as some employees become entrepreneurs.

Thus, the issue of human capital development is intimately related with other,

broader development issues.

These benefits happen only when the host country possess the appropriate

absorptive capacity of the economy. Which is depicted clearly in the above figure no.2.1

as conditional factors therefore a host economy welcoming FDI should also make

necessary environmental changes in such a way to absorb the fullest benefits of FDI and

reach economic development. More interestingly one of the most required factors for

attracting FDI to a country is its economic growth. Therefore economic growth attained

through FDI in turn serves to have a reverse impact on attracting further FDI inflows.

It can be rightly stated that this is a viscous cycle and countries have become more

competitive to advertise themselves on their FDI attractive factors.

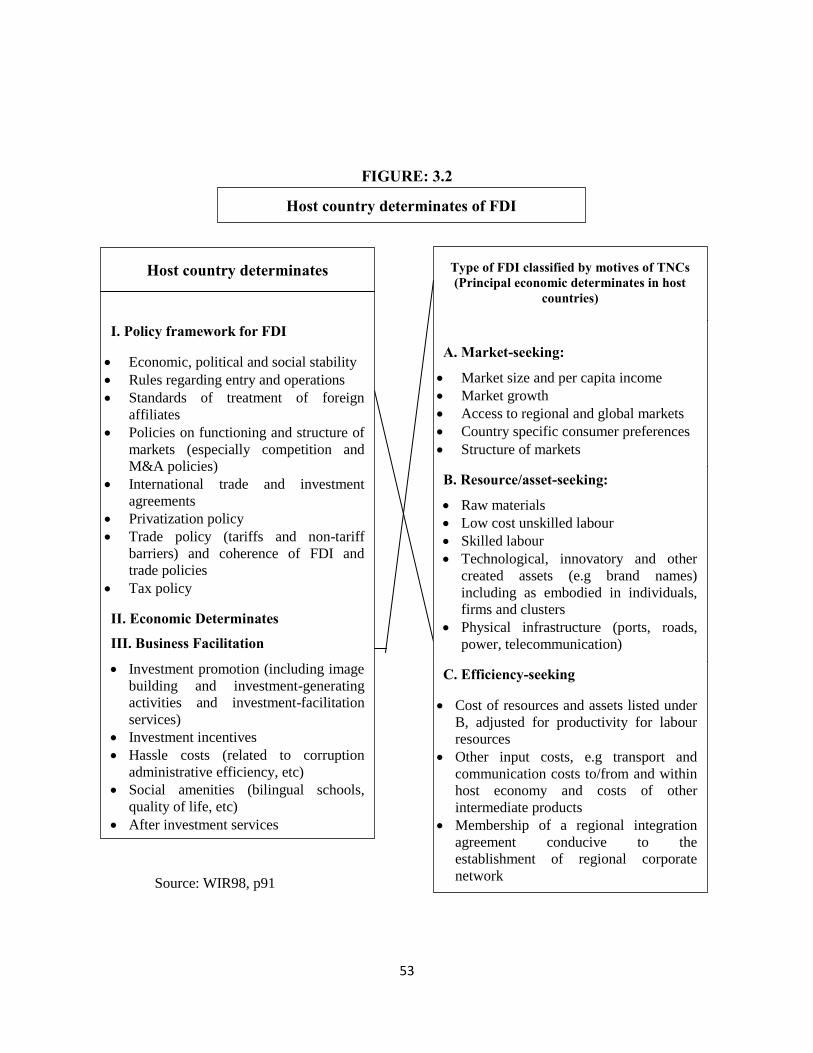

3.1.7 Determinants of FDI

The host country determinants of the FDI may be broadly grouped into three

categories: policy framework for the FDI, economic conditions and business

facilitations.

53

FIGURE: 3.2

Source: WIR98, p91

Host country determinates of FDI

Host country determinates

I. Policy framework for FDI

Economic, political and social stability

Rules regarding entry and operations

Standards of treatment of foreign

affiliates

Policies on functioning and structure of

markets (especially competition and

M&A policies)

International trade and investment

agreements

Privatization policy

Trade policy (tariffs and non-tariff

barriers) and coherence of FDI and

trade policies

Tax policy

II. Economic Determinates

III. Business Facilitation

Investment promotion (including image

building and investment-generating

activities and investment-facilitation

services)

Investment incentives

Hassle costs (related to corruption

administrative efficiency, etc)

Social amenities (bilingual schools,

quality of life, etc)

After investment services

Type of FDI classified by motives of TNCs (Principal economic determinates in host

countries)

A. Market-seeking:

Market size and per capita income

Market growth

Access to regional and global markets

Country specific consumer preferences

Structure of markets

B. Resource/asset-seeking:

Raw materials

Low cost unskilled labour

Skilled labour

Technological, innovatory and other

created assets (e.g brand names)

including as embodied in individuals,

firms and clusters

Physical infrastructure (ports, roads,

power, telecommunication)

C. Efficiency-seeking

Cost of resources and assets listed under

B, adjusted for productivity for labour

resources

Other input costs, e.g transport and

communication costs to/from and within

host economy and costs of other

intermediate products

Membership of a regional integration

agreement conducive to the

establishment of regional corporate

network

54

In an economic sense, direct investments depend on different aspects of

investments: the motive for investment (market-seeking, resource-seeking and efficiency-

seeking), type of investment (greenfield or brownfield), the sector of investment

(manufacturing or services) and the size of multinational company or investor. However,

one must also include location–specific factors, which are more stable over the period.

According to the above mentioned, the principal economic determinants of the FDI in

specific case could be different.

The market seeking FDI aims at penetrating the local markets of host countries

and is usually connected with: market size and per capita income, market growth, access

to regional and global markets, consumer preferences and structure of domestic market.

The resource-asset seeking FDI depends on prices of raw materials, lower unit

labour cost of unskilled labour force and the pool of skilled labour, physical infrastructure

(ports, roads, power, and telecommunication), However, there have been many changes

in the international finance since the publication of the manual, IMF has recently taken

steps to update it in accordance with those changes. Dunning (Dunning, 1993), stressed

that FDI takes place when three sets of factors exist simultaneously: ownership specific

advantage, location specific advantage and exploiting both advantages through

internationalization and the level of technology.

The efficiency-seeking FDI is motivated by creating new sources of

competitiveness for firms and it goes where the costs of production are lower. In this last

case, prior to decision, foreign investors consider price of factors of production (adjusted

for productivity differences) and the membership in regional integration agreement

(UNCTAD, 1998). Consequently, the efficiency-seeking FDI covers both previously

mentioned types of the FDI. It is necessary to stress that is not possible to distinguish

exactly between firm specific and country-specific determinants of the FDI, or to

determine motives of small versus large foreign affiliates. In recent years, the

determinants of and motivation for the FDI in developing countries have changed in the

process of globalization.

55

3.1.8 Constraints of Foreign Direct Investment

Apart from the wide array of positive impacts of FDI inflows to a country‘s

economic growth it also has some constraints which is debatable such as:

Exploitation of Resources: Exploitation of natural resources of a host country is not a

very uncommon phenomenon in the case of FDI. MNCs of other countries have been

known to indiscriminately exploit the resources of host countries in order to get short run

gains and profits and have even chosen to ignore the sustainability factors associated with

the local communities and local habitat, very much like what happened in the 17th

century

colonialism.

Threaten Small Scale Industries: MNCs have large economic and pricing power due to

their large sizes. They do not have much problem with regards to financial capital and

can hence resort to using lavish advertisements. Also, these companies are global players

who have their operations spread across countries and have effective supply chains which

enable them to have economies of scale which smaller players in the domestic market of

the host country cannot compete with. All this results in the MNC having cheaper

products and more visibility due to the higher amounts of advertising and have been

known to push out smaller industries out of business.

Technology: Although, the MNCs have access to new and cutting edge technology, they

do not transfer the latest technology to the host country with a fear that their home

country may loose its competitive advantage. Hence the maximum potential of the host

economy cannot be achieved as a result of old technology transferred.

Stimulates inappropriate consumption: Foreign firms stimulate inappropriate

consumption pattens through excessive advertising, creating a false status issues by

consuming international brands and monopolistic market power. The products made by

Multinationals for the domestic markets are not necessaryily low in price and high in

quality. Their technology is generally capital intensive which does not suit the needs of a

labour surplus economy.

Foreign firms may influence political decisions in developing countries: In view of

their large size and power, national sovereignty and control over economic policies may

56

be jeoparadised. In extreme cases, foreign firms may bribe public officials at the highest

levels to secure undue favours. Similarly they may contribute to friendly political parties

and subvert the political process of the host country.

Ambiguity in providing desired impact to the economic growth: It may or may not

have the desired and expected growth-enhancing impact on the economy. FDI might

enter a labour-abundant country with capital-intensive technologies; but, if the labour

laws are not flexible, this would have a relatively lesser impact on employment

generation.

Therefore the host country should be cautious in making promotional activities

and framing investment policies in such a way that it invites a quality FDI and in required

sector.

3.2 An Overview of World FDI

One of the most prominent and striking feature of today‘s globalised world is the

exponential growth of FDI in both developed and developing countries. In the last two

decades the pace of FDI flows are rising faster than almost all other indicators of

economic activity worldwide. Before 1990, Global FDI inflows more than quintupled

from 1990 to 2009, rising from US$208 billion to US$1.1 trillion, resulting in a

cumulative stock of nearly US$18 trillion by end-2009. Global FDI inflows in 2010

reached an estimated $1,244 billion, a small increase from 2009‘s level of $1,185 billion.

Global foreign direct investment (FDI) flows exceeded the pre-crisis average in 2011,

reaching $1.5 trillion despite turmoil in the global economy. However, they still remained

some 23 per cent below their 2007 peak. UNCTAD predicted slower FDI growth in 2012,

with flows levelling off at about $1.6 trillion. Longer-term projections show a moderate

but steady rise, with global FDI reaching $1.8 trillion in 2013 and $1.9 trillion in 2014,

barring any macroeconomic shocks. FDI inflows increased across all major economic

groupings in 2011.

57

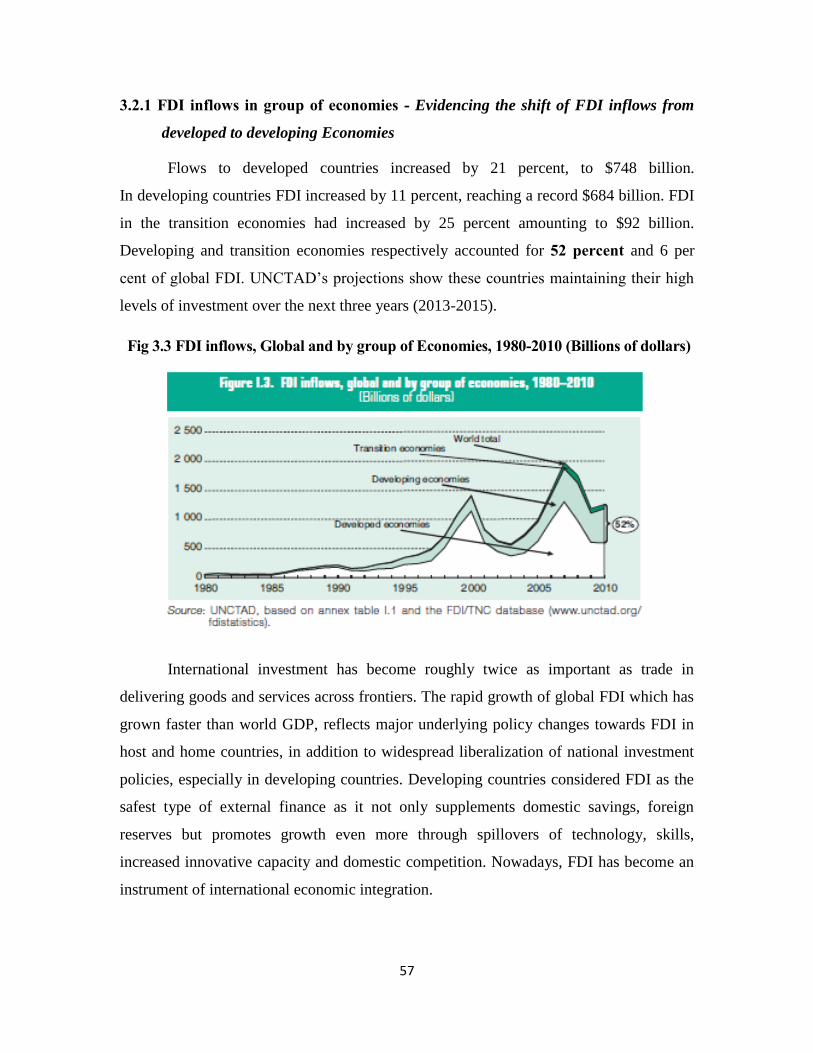

3.2.1 FDI inflows in group of economies - Evidencing the shift of FDI inflows from

developed to developing Economies

Flows to developed countries increased by 21 percent, to $748 billion.

In developing countries FDI increased by 11 percent, reaching a record $684 billion. FDI

in the transition economies had increased by 25 percent amounting to $92 billion.

Developing and transition economies respectively accounted for 52 percent and 6 per

cent of global FDI. UNCTAD‘s projections show these countries maintaining their high

levels of investment over the next three years (2013-2015).

International investment has become roughly twice as important as trade in

delivering goods and services across frontiers. The rapid growth of global FDI which has

grown faster than world GDP, reflects major underlying policy changes towards FDI in

host and home countries, in addition to widespread liberalization of national investment

policies, especially in developing countries. Developing countries considered FDI as the

safest type of external finance as it not only supplements domestic savings, foreign

reserves but promotes growth even more through spillovers of technology, skills,

increased innovative capacity and domestic competition. Nowadays, FDI has become an

instrument of international economic integration.

Fig 3.3 FDI inflows, Global and by group of Economies, 1980-2010 (Billions of dollars)

58

3.3 BRICs and the significance of FDI in BRICs

3.3.1 Evolution of BRICs

On the desk of Jim O‘Neill, chief economist for Goldman Sachs, stand four

flimsy flags, these flags hint at a more interesting story – of the latest way in which

money and ideas are reshaping the world. And almost a decade ago, O‘Neill decided to

start thinking of them as a group – which he gave the acronym BRIC. It was a simple

mental prop. The bolder move was to predict – publicly, and in Goldman‘s name – that

by 2041 (later revised to 2039, then 2032) the Brics would overtake the six largest

western economies in terms of economic might. The four flags would come to represent

the pillars of the 21st-century economy.

Separated geographically and culturally; they had never acted as a bloc in any

way, never conceived of themselves as a unit. Yet what they all shared in 2001 were large

populations, underdeveloped economies and governments that appeared willing to

embrace global markets and some elements of globalisation. To O‘Neill, these

characteristics made them natural sisters: they all had the potential for rapid future

growth.

3.3.2 The collective strengths of BRICs

Economic and social development of BRICs: The rapidly emergent powers of Brazil,

Russia, India and China (BRIC) are in the process of changing the political and economic

map of the 21st century. In particular, the historically unprecedented economic growth

observed since the 1990s in the ―awakening giants‖ China, India and Brazil has not only

aroused the interest of investors in these future markets, it has astonished the worlds of

politics, science, economics and the media. The global economic significance of the

BRICs nations is undisputed.

59

The population growth of BRICs: Over the past 50 years, the population of the BRICs

has more than doubled. There are 6.8 billion people in the world and 42 percent currently

live in the BRIC countries However, population growth is expected to slow in the BRICs

over the next few decades, pushing down their aggregate share of the global population.

The age structure of the BRICs will also continue to shift progressively towards older

populations. In the process each of the BRICs will encounter or is already encountering

an advantageous ‗demographic window‘ in which the working-age population is

disproportionately large. With an appropriate policy framework, this could provide a

boost to growth in Brazil, China and India for several years. Russia‘s window of

opportunity has probably been shut due to the decreasing rate of population.

Increase in demand and consumption: As household incomes rise, so do sales on

discretionary items such as automobiles and cellular phones. Among the BRIC countries,

China and India show the greatest increase in demand and consumption, while Russia

followed by Brazil reflects higher levels of wealth.

The rise of middle income population Vs Power of Productivity: The other essential

driver of growth is productivity. The rise in middle age population is also an important

reason for the expected rise in productivity. It is believed that the middle class is rising in

BRIC countries and estimate 2 billion will join it by 2030. In August 2009, China passed

the US as the world‘s single largest car market and it is believed that India will surpass

China in the next few decades. (BRICs brochure by GS) Countries with young and

expanded labour forces, which are becoming increasingly efficient, will show the largest

gains in the real GDP. Dominic Wilson and Roopa Purushothaman in their follow-up

paper ―Dreaming with BRICs to 2050‖ they had written in less than 40 years the BRICs

economies together could be larger than G6 in dollar terms.

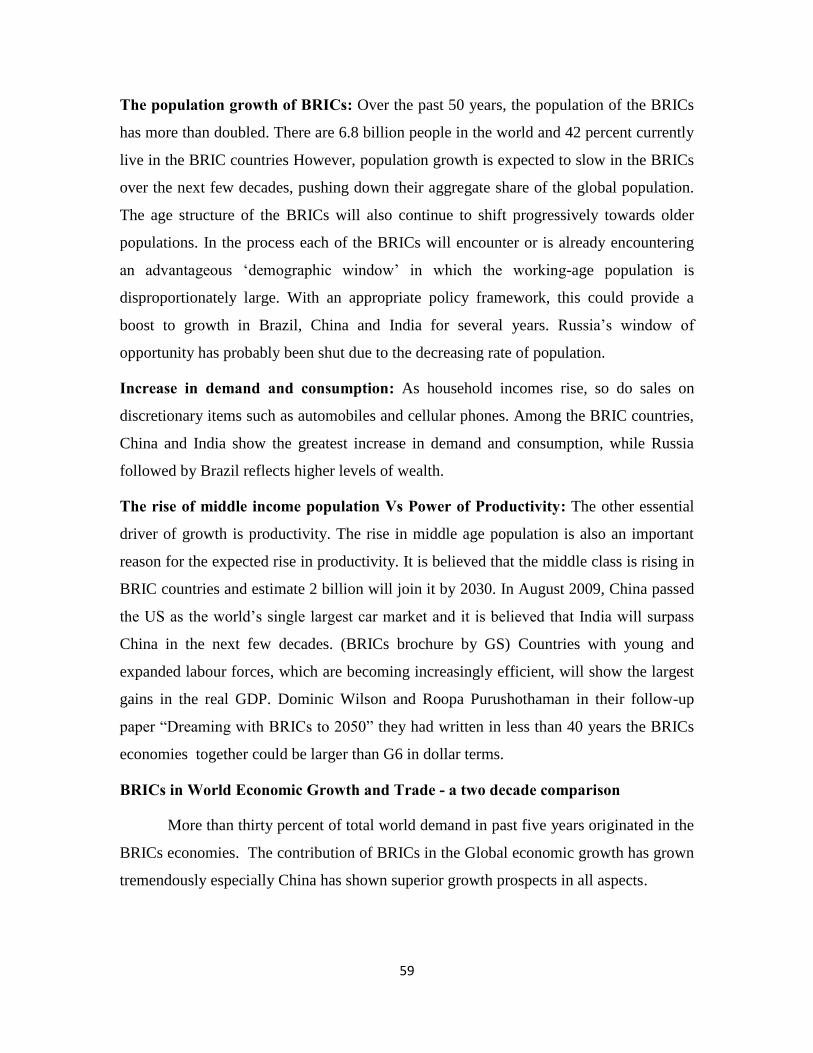

BRICs in World Economic Growth and Trade - a two decade comparison

More than thirty percent of total world demand in past five years originated in the

BRICs economies. The contribution of BRICs in the Global economic growth has grown

tremendously especially China has shown superior growth prospects in all aspects.

60

Figure 3.4. The Contribution of BRIC in Global Economic Growth & Trade

Source: IMF database

More than thirty percent of total world demand in past five years originated in the

BRIC economies. Over the last few years the importance of these countries became even

more evident as China took a lead role in world economic growth. The share of BRIC in

World GDP has shown a considerable increase for Russia and India. China has shown a

more than three fold increment in its share of World GDP, in contrast Brazil has shown a

decline from 3.3% in 1990 to 2.9% in 2010. The Share of BRIC in Global Trade has

continued to grow at a rapid pace. Their share in world export increased substantially

over the past two decades, mostly through broad-based diversification, both in

commodities and regions of trade. In case of Global FDI inflows BRIC economies

remained steady even during the recent crisis, reflecting the longer term views on the

growth potentials of the BRIC and the soundness of their financial systems.

0

5

10

15

1990 2010 1990 2010 1990 2010

Brazil

Russia

India

China

InPe

rcen

t

Share in World GDP

Share in Global Trade

Share in Global FDI inflows

61

3.3.3 BRICs economic reforms which accelerated its foreign investments and growth

– a few milestones…

There is a new era arising in international relations. The rise of the BRIC

countries (Brazil, Russia, India and China) is changing power dynamics in world affairs.

For China, India and Russia the transformation towards a market-based economy

deregulation and the opening-up towards the global economy marked the start of

economic acceleration. In China, a rather gradual reform process started in 1978 with the

introduction of the opening-up policy by its leader Deng Xiaoping. Policy changes are

often tested in smaller regions before being fully implemented. By western standards,

China is still far off from a well-functioning market economy. Since 2005, under the

leadership of President Hu Jintao and Prime Minister Wen Jiabao, the process of

liberalization has been gradually continued. An interesting feature of the liberalization

process in China is that, in contrast to Russia, it has occurred without a thorough attempt

to democratization. Even though recent growth is increasingly driven by domestic

demand, growth in the early years was led by an export-oriented policy and later the

inflow of foreign capital. In the latter, there is a large similarity with the earlier success of

other Asian economies, like Japan, South Korea and Taiwan.

Even though the Indian economy started to accelerate in the early 1980s, substantial

policy reform did not occur until a decade later. Before the 1980s, this could best be

characterized as downright hostility, whereas in the early 1980s the economic environment

abruptly changed towards business friendly. During the 1980s, the Indian economy remained

relatively closed, and economic growth was mainly driven by domestic factors. Drastic

market-based economic reform started first in 1991. Many areas of economic activity were

opened to private firms, while investment decisions in most industries did no longer require

government approval. Up to the 1990s, banking was mostly restricted to government

operated firms. Therefore, investment decisions were often politically rather than

economically motivated. Furthermore, from the late 1990s onwards trade restrictions were

gradually removed (even though trade remains more restrictive than in most OECD

countries) and the integration of India into the world economy began. As was the case in

China, this transformation resulted in the inflow of foreign capital.

62

In contrast to China and India, economic reform in Russia occurred in a big bang

fashion rather than gradual, following the collapse of the Soviet Union. Reforms started

in 1987 under Michail Gorbatsjov, with the decision to allow firms to determine output

levels based on demand. Furthermore, companies (although still being state-owned)

became financially independent and were allowed to negotiate prices, such that the

transfer of funds from profitable to unprofitable companies came to an end. Another

reform was that foreign investment became legal. In 1991, in the first year of the

presidency of Boris Yeltsin, Russia implemented what was known as the shock therapy

led by Jegor Gaidar which aimed at a rapid and radical transformation towards a market

economy. The first effects of this policy where disastrous. A full economic collapse

occurred, with GDP declining by about 50 percent between 1991 and 1995. The sudden

removal of price controls resulted in an episode of hyperinflation. After a short period of

recovery, the 1998 financial crisis resulted in a new recession and hyperinflation.

After the financial crisis in 1998, the economy started to recover. Since then, economic

growth has been continuously high, large sums of foreign direct investments have been

attracted, and inflation has remained relatively low. The total stock of FDI originating

from the EU invested in Russia has quadrupled in the five years between 2004 and 2009.

GDP growth is spurred by high revenues from the availability of natural resources,

especially oil and gas.

In the early 1980s, the Brazilian economy experienced a period of economic crisis

that was the result of bad governance and a high dependency on foreign debt. As the

government attempted to reduce indebtedness by reducing imports and economic growth

and the introduction of an import substitution program, the economy entered a deep

recession in 1981. In the mid-1980s this program resulted in a trade surplus, but at that

time the domestic public debt had become problematic and a loose monetary policy had

resulted in hyperinflation. While it took until the early 1990s before fiscal stabilization

was achieved, early attempts to improve macroeconomic stability relied on a price freeze.

While upon introduction in 1986 this was successful initially, supply was soon reduced

such that many goods became scarce. In the late 1980s Brazil returned to hyperinflation.

In 1990, under the presidency of Fernando Collor de Mello, a new attempt was made to

ensure macroeconomic stability. A new prize freeze was implemented, most financial

63

assets were frozen, and fiscal reforms were carried out. This plan failed as well, however,

and the economy entered a new period of recession. It took until 1994 before the crisis

came to an end, when the Brazilian currency (the real) was pegged to the US dollar. Since

then, economic growth has remained generally high and Brazil has succeeded to attract

high levels of FDI. For the EU, Brazil is the second most important destination for FDI of

all BRIC countries.

Therefore, the combined economic strength of the BRICs is undeniable. The

countries will continue to attract foreign direct investment as corporations hope to gain

access to their growing middle class markets. These countries are also increasingly

rebalancing their domestic consumption to achieve more sustainable growth models.

3.3.4 Foreign Direct Investments in BRICs

A Historical background of FDI inflows

Foreign Direct Investment (FDI) is an important source for the development of

strategic sectors of the BRIC countries. Until 1984, Brazil was the major FDI recipient

country among the BRICs, overtaken by China in 1985 and since then China continues to

be a major destiny of FDI, especially in the automotive and consumer durable sectors,

China became the world major recipient of FDI in the 1990s, matching with country‘s

efforts to integrate with the world economy, many multinational companies have moved

their operations to China to take advantage of its low labour costs and huge domestic

market. India received an almost constant and small part of the world total FDI flows

during last two decades.

In Brazil, since the late 19th

century, FDI became more and more important, after

the II world war, FDI played a key role during the Brazilian industrialization process.

Much of the Brazilian history shows that the country has relied upon foreign capital to

finance its development and economic growth. In recent years, foreign investments

inflows are attracted by the large Brazilian market and the rapid economic growth of the

country, besides the fact that Brazil will host the 2014 World cup and 2016 Olympics.

In Russia until the 1990s, the amount of FDI flowing into Russia remained

relatively flat. At the opening of this new millennium, Russia emerges as a country of

64

opportunities for FDI. In fact, FDI inflows has increased over the last years in Russia

thanks to its tremendous natural resources and growing domestic markets. Russia‘s new

status as WTO member will also complement its internal economic reforms and improve

foreign investment climate towards transparency and predictability in business

transactions in the country.

During the course of 1990s, the government of India initiated economic and

financial reforms aimed to progressively integrate Indian economy with the global

economy. FDI is recognized by the Indian government as an important driver of

economic growth and development. As a result of the various policy initiatives taken,

India has rapidly changes from a restrictive regime for Foreign Investments to a more

liberal one.

China has shifted from a closed, state-planned economy to an increasingly open

and internationally integrated market place over the past three decades. During the

1980‘s FDI inflows grew steadily but remained relatively low mainly confined to Joint

ventures with Chinese-State-Owned Enterprises. In the mid-1990‘s, FDI became quite

important for the chinese economy and new rules and regulations have been issued

accordingly. When Chna became member of the WTO in 2001, many new laws and

regulations have been issued after. FDIs in China have benefited from this liberalization

trend, specially the distribution, logistics, financial services and telecommunications

sectors. Given China‘s projection on the global arena, this movement is only expected to

increase in the near future, as China continues to establish its position as one of the

world‘s foremost economic growing power nations.

FDI in BRIC countries still remains bureaucratic and complex, however every

BRIC country shows the same serious intent to make the investment climate and more

and more favourable in the near future. Notably China and Brazil have become powerful

magnets of FDI. Consumption and FDI are the components of GDP and for a developing

economy it is a good predictor of stability and long term growth.

3.3.5 Major investors in BRICs

The EU is among the main investors in each of the BRICs and the dominant

investor in Brazil and Russia. In China and India, the EU has less weight. But, after

65

correcting for particularities in FDI data, such as the prominent role of Hong Kong and

off-shore centers in Chinese FDI and of Mauritius in Indian FDI, the EU ranks higher

also in these countries. In a direct comparison with the US and Japan, the EU emerges as

the leading investor among the Triad countries.

3.3.6 Potential factors determining FDI inflows in BRIC

The most important determinants establishing a congenial environment that attract

FDI and a strong business and investment climate have been mentioned in UNCTAD

study which was a general overview of possible determinants based on the investor‘s

motive. Based on the discussed literature review, there are a set of potential determinant

variables that influence the FDI flows in BRIC economies. The various broad categories

of determinants have been discussed below:

The Economic indicators Economic conditions such as: prospective GDP, Large

population, increase in trade, a positive current account balance, ample labour etc., plays

an important role in determining a country‘s FDI inflows.

Economic stability and growth prospects: A country which has a stable macroeconomic

condition with high and sustained growth rates will receive more FDI inflows than a

more volatile economy. The proxies measuring growth rate would include: GDP growth

rates, Trade volume, Current account balance, Interest rates and Inflation rates.

Contradicting, when inflation is taken as proxy for the level of economic stability, then

the classic symptoms of fiscal or monetary control will result in unbridled inflation.

In connection with this, investors prefer to invest in more stable economies that reflect a

lesser degree of uncertainty. Therefore, it is expected that GDP growth rate, Industrial

production index, Interest rates would influence FDI flows positively and the Inflation

rate would influence positively or negatively.

Market size and Growth: Larger market size should receive more inflows than that of

smaller countries having lesser market size. Market size is generally measured by Gross

Domestic Product and purchasing power parity of the population. It is expected to be a

positive and significant determinant of FDI inflows. Thus, an economy with a large

market size (along with other factors) should attract more FDI if capturing market is the

firm‘s motive. Market size is important for FDI as it provides potential for local sales,

66

greater profitability of local sales to export sales and relatively diverse resources, which

make local sourcing more feasible. Thus, a large market size provides more opportunities

for sales and also profits to foreign firms and therefore attracts FDI. However, market

size and growth impact may differ under different conditions.

Trade: Volume of Trade is considered to be a key determinant of FDI as represented in

the previous literature. Much of FDI is export oriented and may also require the import of

complementary, intermediate and capital goods. In either case, volume of trade is

enhanced and thus trade openness is generally expected to be a positive and significant

determinant of FDI.

Labour: Cheap labour is another important determinant of FDI inflow to developing

countries. A high wage-adjusted productivity of labour attracts efficiency-seeking FDI

both aiming to produce for the host economy as well as for export from host countries.

Countries with a large supply of skilled human capital attract more FDI, particularly in

sectors that are relatively skill intensive. Higher labour cost would result in higher cost of

production and is expected to limit the FDI inflows; therefore, we expect the negative and

significant relationship between labour cost and FDI.

Business Environment: Business environment factors such as Government efficiency,

Legal structure, monetary stability, effective Business regulations, technology readiness

and innovation of a country were considered to be the most important factors that would

determine a country‘s competitiveness for investment decisions.

Government Efficiency: Government‘s attitudes toward markets and the efficiency of its

operations are very important. Excessive bureaucracy and red tape, over regulation,

corruption, dishonesty in dealing with public contracts, lack of transparency and trust

worthiness, inability to provide appropriate services for the business sector, and political

dependence of the judicial system impose significant economic costs to businesses and

slow the process of economic development. The government policies in terms of public

finance, fiscal policy, institutional framework, business legislation and societal

framework can directly and indirectly affect FDI through their effects on market

imperfections. The same government policy can increase and/or decrease market

imperfections and thereby increase and/or decrease FDI inflows. The evidences of the

67

empirical evidence on the impact of government policies on FDI inflows are ambiguous.

Some of them find a positive effect of investment incentives. For example, UNCTAD (1996)

report shows that incentives can have an effect on attracting FDI only at the margin.

A number of previous studies find that fiscal incentives do affect location decisions,

especially for export oriented FDI. On the other hand, the study of Contractor (1991)

finds that changes in policy may have a weak influence on FDI inflows. Caves (1996)

concludes that incentives are generally ineffective once the role of fundamental

determinants of FDI taken into account.

Technology readiness and innovation: In today‘s globalized world, technology is

increasingly essential for firms to compete and prosper. The technological readiness pillar

measures the agility with which an economy adopts existing technologies to enhance the

productivity of its industries, with specific emphasis on its capacity to fully leverage

information and communication technologies (ICT) in daily activities and production

processes for increased efficiency and enabling innovation for competitiveness. ICT has

evolved into the ―general purpose technology‖ of our time, given the critical spillovers to

the other economic sectors and their role as industry-wide enabling infrastructure.

Therefore ICT access and usage are key enablers of country‘s overall technological

readiness. Whether the technology used has or has not been developed within national

borders is irrelevant for its ability to enhance productivity. The central point is that the firms

operating in the country need to have access to advanced products and blueprints and the

ability to absorb and use them. Among the main sources of foreign technology, FDI often

plays a key role, especially for countries at a lower stage of technological development. It is

important to note that, in this context, the level of technology available to firms in a country

needs to be distinguished from the country‘s ability to conduct blue-sky research and develop

new technologies for innovation that expand the frontiers of knowledge.

Legal Structure: Foreign investor must believe that investment is safe, that fair and

equitable treatment is assured, and that disputes can be resolved in a fair and expedient

manner. Without investor protections, equity markets fail to develop and banks become

the only source of finance. Yet weak collateral or property registration systems block

many businesses in developing countries from obtaining even bank loans.

68

Legislative Stability: Consistency in government legislation and policies are important

for attracting MNEs to invest in a country. For example, consistency of the Fiscal (Tax)

Code for longer period build investor‘s confidence and knowledge on the host country,

on the type of taxes an investor has to pay. To attract FDI legislative stability is

necessary. OECD study suggests that foreign companies may be willing to invest into

countries with sound legal and regulatory frameworks that would not otherwise be

considered as ―investor friendly‖ provided they are able to obtain a reasonable degree of

clarity about the environment in which they will be operating. An unstable legislative

environment may give investors the feeling that there is too great a risk of unfavorable

conditions arising, which may dissuade them from investing.

Infrastructure facilities: The availability of quality infrastructure, particularly electricity,

water, transportation and telecommunications, is an important determinant of FDI. When

developing countries compete for FDI, the country that is best prepared to address

infrastructure bottlenecks will secure a greater amount of FDI. The previous literature

shows the positive impact of infrastructure facilities on FDI inflows. A country which has

opportunity to attract FDI flows will stimulate a country to equip with good Infrastructure

facilities. The availability of quality Infrastructure can be related to public expenditure on

capital to acquire fixed capital assets, land, intangible assets and non-financial and non-

military assets for Infrastructure.

Regulations: The previous literature shows the impact of government regulations including

labour regulations, credit regulation and business regulations has significant impact on FDI

inflows into a host country. Though investment incentives are considered another determinant

for FDI, the investment incentives alone are generally not an efficient way to increase national

welfare. Policies to promote FDI take a variety of forms, but the most common are partial or

complete exemptions from corporate taxes and import duties. Standard policies to attract FDI

include tax holidays, import duty exemptions, and different kinds of direct subsidies. FDI

inflows are also affected by corporate tax rate differentiation. Subsidizing FDI helps

multinational firms reduce production costs, improves incentives to create patents, trademarks,

and enhances the relative attractiveness of locating production facilities in the country offering

incentives and raises the economic benefits of FDI relative to exporting.

69

Monetary Stability: A weaker real exchange rate might be expected to increase vertical FDI

as firms take advantage of relatively low prices in host markets to purchase facilities or, if

production is re-exported, to increase home-country profits on goods sent to a third market.

A ―firm-specific asset‖ argument shows that exchange rate depreciation in host countries tend

to increase FDI inflows. But on the other hand, a stronger real exchange rate might be expected

to strengthen the incentive of foreign companies to produce domestically. The exchange rate is

in a sense a barrier to entry in the market that could lead to more horizontal FDI.

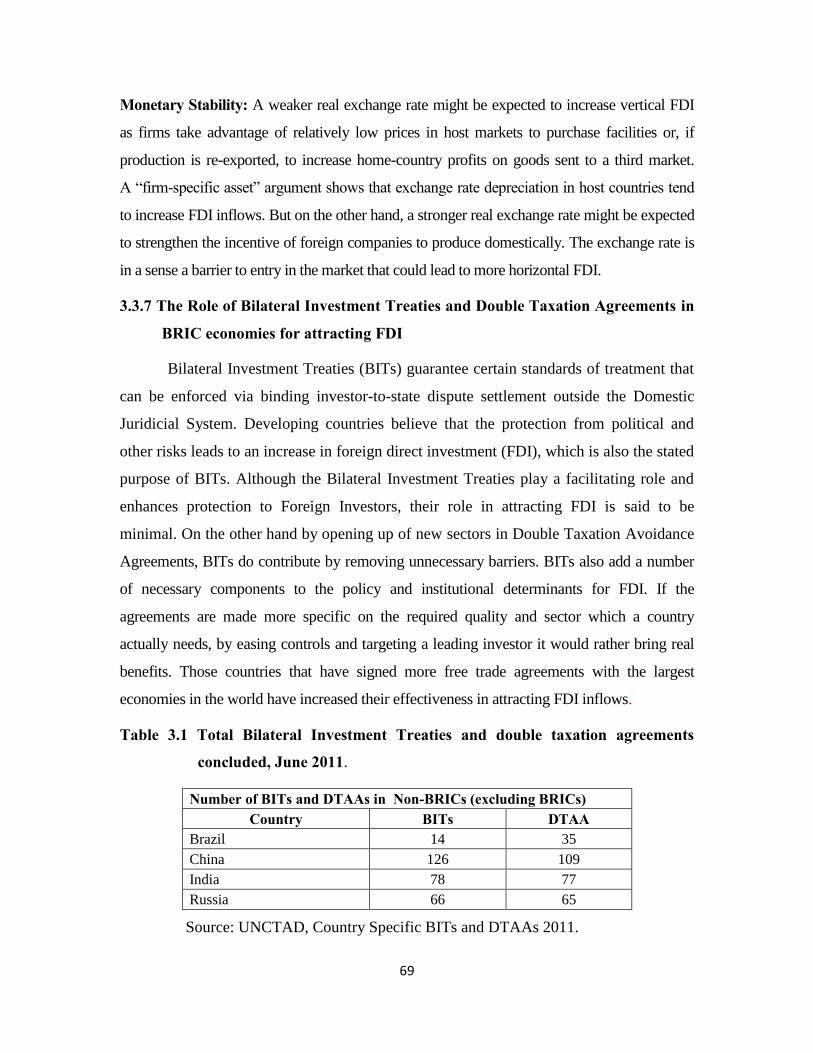

3.3.7 The Role of Bilateral Investment Treaties and Double Taxation Agreements in

BRIC economies for attracting FDI

Bilateral Investment Treaties (BITs) guarantee certain standards of treatment that

can be enforced via binding investor-to-state dispute settlement outside the Domestic

Juridicial System. Developing countries believe that the protection from political and

other risks leads to an increase in foreign direct investment (FDI), which is also the stated

purpose of BITs. Although the Bilateral Investment Treaties play a facilitating role and

enhances protection to Foreign Investors, their role in attracting FDI is said to be

minimal. On the other hand by opening up of new sectors in Double Taxation Avoidance

Agreements, BITs do contribute by removing unnecessary barriers. BITs also add a number

of necessary components to the policy and institutional determinants for FDI. If the

agreements are made more specific on the required quality and sector which a country

actually needs, by easing controls and targeting a leading investor it would rather bring real

benefits. Those countries that have signed more free trade agreements with the largest

economies in the world have increased their effectiveness in attracting FDI inflows.

Table 3.1 Total Bilateral Investment Treaties and double taxation agreements

concluded, June 2011.

Number of BITs and DTAAs in Non-BRICs (excluding BRICs) Country BITs DTAA

Brazil 14 35

China 126 109

India 78 77

Russia 66 65

Source: UNCTAD, Country Specific BITs and DTAAs 2011.

70

The above table brings out the total number of BITs and DTAAs signed by Brazil,

Russia, India and China until 2011. As revealed in other areas of growth, China seems to

have signed 126 BITs and 109 DTAAs highest among other three BRIC nations. Though

Brazil shows least number of BITs and DTAAs the growth in FDI is very positive which

is vice versa in the case of Russia. India has signed a fair number of BITs and DTAAs.

This scenario reveals the fact that investment treaties may be one of the element in

investment decisions of foreign investors whereas market size, infrastructure, economic

stability and regulations are more important for attracting FDI as stated by UNCTAD in

its series on International Investment Policies for Development.

3.3.8 World’s Top 20 FDI recipients and the position of BRICs

Table 3.4 depicts a clear picture on worlds top 20 FDI destinations. It is a world

known fact and a topic of appreciation, that China has been successful in retaining its

position in the top five, except the year 2001. It maintained its global second place until

2004, but its position went down from four, seven and third until 2008. From the year

2009 onwards it has been sustaining its second place till date, further it is expected to

reach the first place replacing the US in the coming years. Brazil has sustained its twelfth

place in the world‘s top destinations especially 2001 & 2002, but underwent a setback in

2003 -2005. It is noteworthy that Brazil missed its top twenty positions in the FDI

attraction in the year 2006. However it reached back its fifteenth place in 2007 and

gradually improved to twelfth, fourteenth, eight and fifth place as of 2011. This is the

first time in the whole period Brazil have reached top five position in FDI inflows.

71

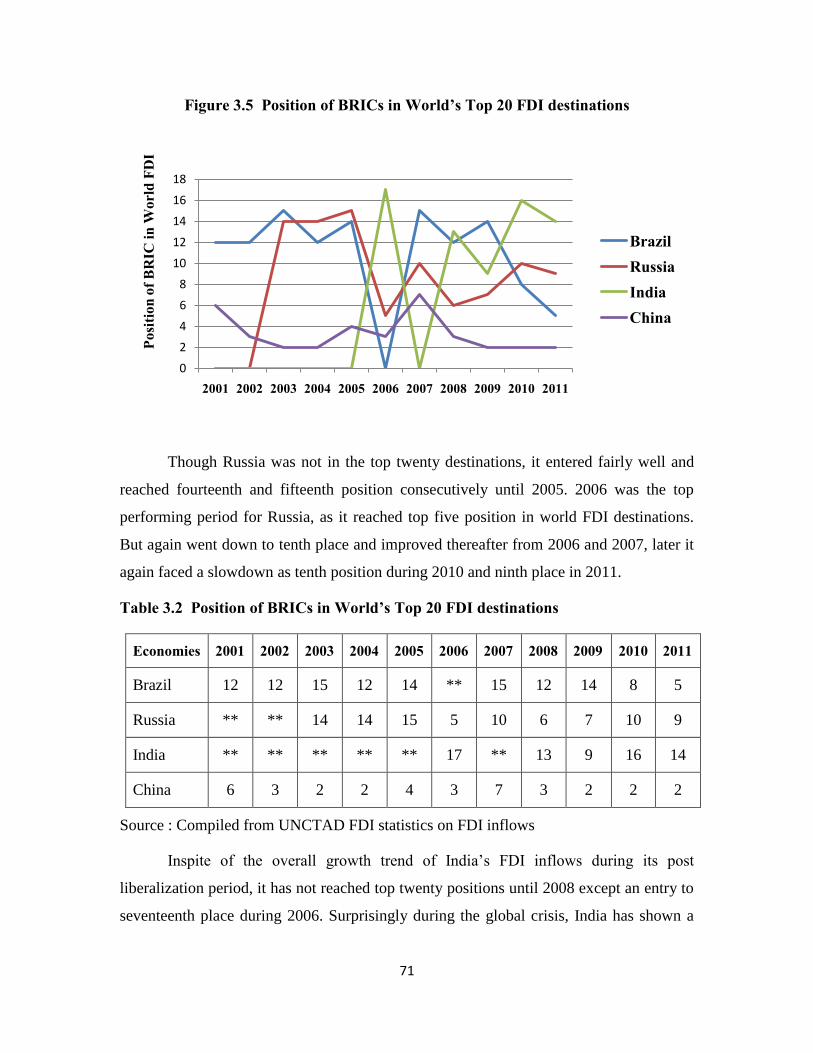

Figure 3.5 Position of BRICs in World’s Top 20 FDI destinations

Though Russia was not in the top twenty destinations, it entered fairly well and

reached fourteenth and fifteenth position consecutively until 2005. 2006 was the top

performing period for Russia, as it reached top five position in world FDI destinations.

But again went down to tenth place and improved thereafter from 2006 and 2007, later it

again faced a slowdown as tenth position during 2010 and ninth place in 2011.

Table 3.2 Position of BRICs in World’s Top 20 FDI destinations

Economies 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Brazil 12 12 15 12 14 ** 15 12 14 8 5

Russia ** ** 14 14 15 5 10 6 7 10 9

India ** ** ** ** ** 17 ** 13 9 16 14

China 6 3 2 2 4 3 7 3 2 2 2

Source : Compiled from UNCTAD FDI statistics on FDI inflows

Inspite of the overall growth trend of India‘s FDI inflows during its post

liberalization period, it has not reached top twenty positions until 2008 except an entry to

seventeenth place during 2006. Surprisingly during the global crisis, India has shown a

0

2

4

6

8

10

12

14

16

18

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

BrazilRussiaIndiaChina

Posi

tion

of B

RIC

in W

orld

FD

I

72

competitive performance in 2009 as occupying ninth position in world FDI destinations.

India‘s position showed a highly disappointing trend, coming down to sixteenth place in

2010 but improved a little in 2011 by reaching fourteenth place.

3.3.9 BRICs in Global Competitiveness

A Nation‘s prosperity depends on its competitiveness which is based on the

productivity, with which it produced goods and services. Competitiveness is rooted in a

nation‘s macroeconomic and microeconomic environment. Macroeconomic factors create

the potential for competitiveness, where as microeconomic factors increases productivity.

Macroeconomic factors include: Government policies, economic growth, stable political

and legal institutions. Microeconomic factors include: business environment factors such

as infrastructure, technology, business regulations, market size, trade etc., Hence the

competitiveness of a nation can be better analysed by studying both micro-economic and

macro-economic factors. The Global Competitiveness Reports (World Economic Forum)

have a solid theoretical foundation and combines publicly available information and

measures many critical factors like set of institutions, policies and set of sustainable

current and medium term levels of economic prosperity. It is built around twelve different

pillars, each of which is critical to driving productivity and competitiveness in national

economies. These pillars are : 1. Institutions, 2. Infrastructure, 3. Macro-economy,

4. Health and primary education, 5. Higher education and training, 6. Market efficiency,

7. Technological readiness, 8. Business sophistication, 9. Innovation, 10. Labour market

efficiency, 11. Financial market development and 12. Market size.

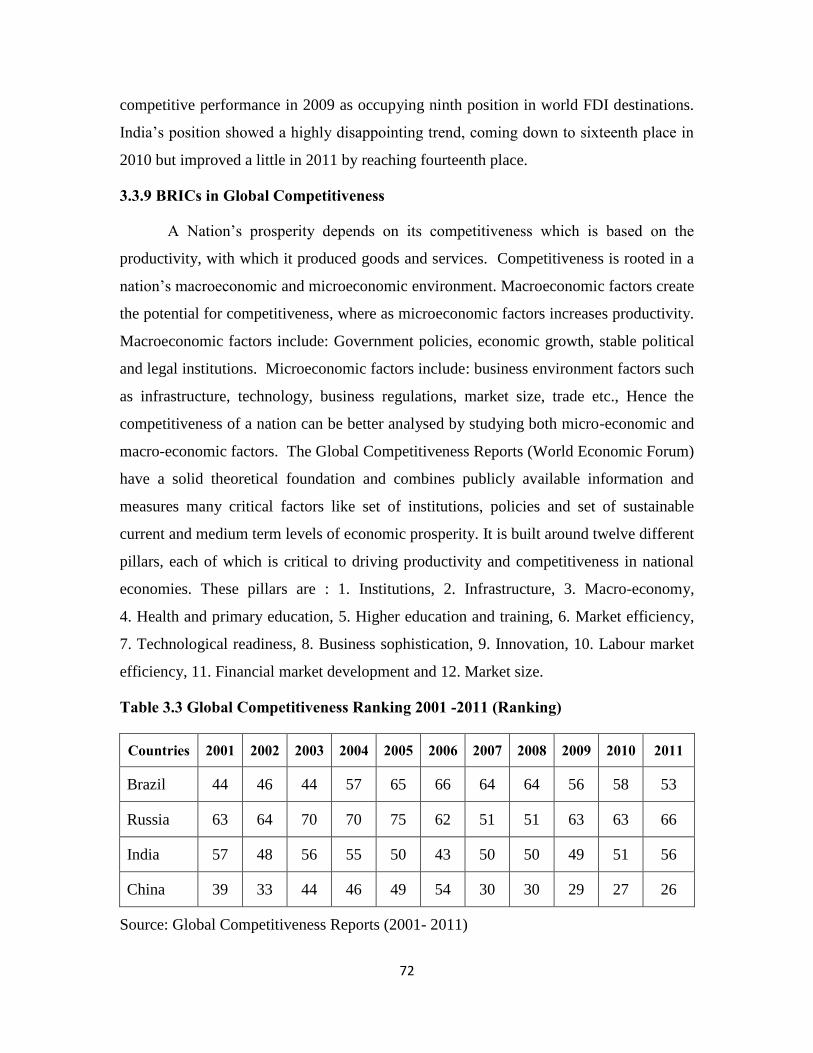

Table 3.3 Global Competitiveness Ranking 2001 -2011 (Ranking)

Countries 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Brazil 44 46 44 57 65 66 64 64 56 58 53

Russia 63 64 70 70 75 62 51 51 63 63 66

India 57 48 56 55 50 43 50 50 49 51 56

China 39 33 44 46 49 54 30 30 29 27 26

Source: Global Competitiveness Reports (2001- 2011)

73

Global Competitiveness ranking of Brazil shows a decline in its position from 44th

in 2001 to 64th

in 2008 and had started improving its competitiveness beyond 2008 again

showing a little decline in the year but recovered healthy in the year 2011 reaching

53rd

position recorded as the most attractive ranking in the past decade. Russia too seems

to have a declining trend in 2005 but surprisingly improved its position in the very next

year by ascending seven positions and shows a stagnant level of global competition

during the year 2007 and 2008. Disappointing during 2010 and 2011 may be due to

government and political instability. Unlike the other two India shows a fluctuating trend

in global competitiveness ranking after an appreciable improvement in the year 2002 it

declined to 56th

position the very next, however recovered to 43rd

position in the year

2006. Showing a decline from thereafter until 2011. On the other hand China showed a

decline from 39th

position in 2001 to 54th

position in 2006 and brilliantly jumped up to

30th

position going ahead 24 positions which show a remarkable hike and more

importantly it managed to sustain and further improved to 26th

position in the year 2011.

Since there are twelve pillars and several sub factors for determining each pillar‘s

score and ranking the overall position may be affected due to any one or few factors. So it

is difficult to come to a conclusion about the area of concern. A country which is

competitive in market efficiency may not be so in infrastructure and vice versa. Therefore in

the present study to analyze the competitiveness of a country in FDI attraction those potential

factors have been taken individually and the impact is determined based on the analysis.

3.4. FDI IN INDIA

3.4.1 FII Vs FDI: International standards and Indian definition

According to IMF and OECD definitions, the acquisition of at least ten percent of

the ordinary shares or voting power in a public or private enterprise by non-resident

investors makes it eligible to be categorized as foreign direct investment (FDI). (OECD

benchmark definition) In India, a particular FII is allowed to invest up to 10% of the paid

up capital of a company, which implies that any investment above 10% will be

considered as FDI, though officially such a definition does not exist. However, it may be

noted that there is no minimum amount of capital to be brought in by the foreign direct

investor to get the same categorized as FDI.

74

The classification of FDI in India under Foreign Investments: Foreign

Institutional Investor (FII) means an institution established or incorporated outside India

which proposes to make investment in securities in India. They are registered as FIIs in

accordance with Section 2 (f) of the SEBI (FII) Regulations 1995. FDI is a form of

investment which comes through Automatic Route, Government Route and NRI route.

This is just one form of foreign investments in India, as may be seen from the graph

below:

Figure 3.6. Foreign Investments in India – Schematic Representation

Source: www.in-investment.com

3.4.2 Legal and Regulatory Framework of FDI in India

Foreign Direct Investments under Automatic Approval and Government Approval

are regulated by the Foreign Exchange Management Act, 1999 (FEMA vide Reserve

Bank‘s Notification FEMA. 20/2000-RB dated May 3, 2000 as amended from time to

time). If a foreigner or foreign company or a person resident outside India wants to invest

in India either in the manufacturing sector or service sector, including the housing sector,

insurance, banking, telecommunications, etc., the foreigner, foreign company or a person

75

resident outside India has to pay due attention to the conditions, regulations and

procedures which are laid down in different notifications by the Reserve Bank of India

issued in terms of Section 6 of FEMA.

Foreign Investment Policy

Foreign investment is permitted in virtually every sector, except those of strategic

concern such as defense (opened up recently to a limited extent) and rail transport.

Foreign companies are permitted to set up 100 per cent subsidiaries in India. No prior

approval from the exchange control authorities (RBI) is required, except for certain

specified activities. According to the current policy, FDI can come into India in two

ways.

Routes of FDI

Automatic route: FDI in sectors/activities to the extent permitted under the

automatic route does not require any prior approval either by the government or the

Reserve Bank of India (RBI). The investors are only required to notify the concerned

regional office of the RBI within 30 days of receipt of inward remittances and file the

required documents with that office within 30 days of issue of shares to foreign investors.

Prior Government Approval route: In the limited category of sectors requiring

prior government approval, the proposals are considered in a time-bound and transparent

manner by the Foreign Investment Promotion Board (FIPB) under the Department of

Economic Affairs, Ministry of Finance. Approvals of composite proposals involving

foreign investment/foreign technical collabouration are also granted on the

recommendations of the FIPB.

3.4.3 FDI in India in Pre and Post reform period

In India, FDI is considered as a developmental tool, which can help in achieving

self-reliance in various sectors of the economy. The historical background of FDI in India

can be traced back with the establishment of East India Company of Britain. British

capital came to India during the colonial era of Britain in India. However, researchers

could not portray the complete history of FDI pouring in India due to lack of abundant

and authentic data. Before independence major amount of FDI came from the British

76

companies. British companies setup their units in mining sector and in those sectors that

suits their own economic and business interest. After Second World War, Japanese

companies entered Indian market and enhanced their trade with India, yet U.K. remained

the most dominant investor in India.

Further, after Independence issues relating to foreign capital, operations of

MNCs, gained attention of the policy makers. Keeping in mind the national interests the

policy makers designed the FDI policy which aims FDI as a medium for acquiring

advanced technology and to mobilize foreign exchange resources. In the due course of

time the economic and political regimes have been changed in the FDI policy too.

The industrial policy of 1965, allowed MNCs to venture through technical collabouration

in India. However, the country faced two severe crisis in the form of foreign exchange

and financial resource mobilization during the second five year plan (1956-61).

Therefore, the government adopted a liberal attitude by allowing more frequent equity

participation to foreign enterprises, and to accept equity capital in technical

collabourations. The government also provided many incentives such as tax concessions,

simplification of licensing procedures and de- reserving some industries such as drugs,

aluminum, heavy electrical equipments, fertilizers, etc in order to further boost the FDI

inflows in the country.

Under the new foreign investment policy Government of India constituted FIPB

(Foreign Investment Promotion Board) whose main function was to invite and facilitate

foreign investment through single window system from the Prime Minister‘s Office. The

foreign equity cap was raised to 51 percent for the existing companies. Government had

allowed the use of foreign brand names for domestically produced products which was

restricted earlier. India also became the member of MIGA (Multilateral Investment

Guarantee Agency) for protection of foreign investments. Government lifted restrictions

on the operations of MNCs by revising the FERA Act 1973. New sectors such as mining,

banking, telecommunications, highway construction and management were open to

foreign investors as well as to private sector.FDI inflows are welcomed in 63 sectors in

2008 as compared to 16 sectors in 1991.

77

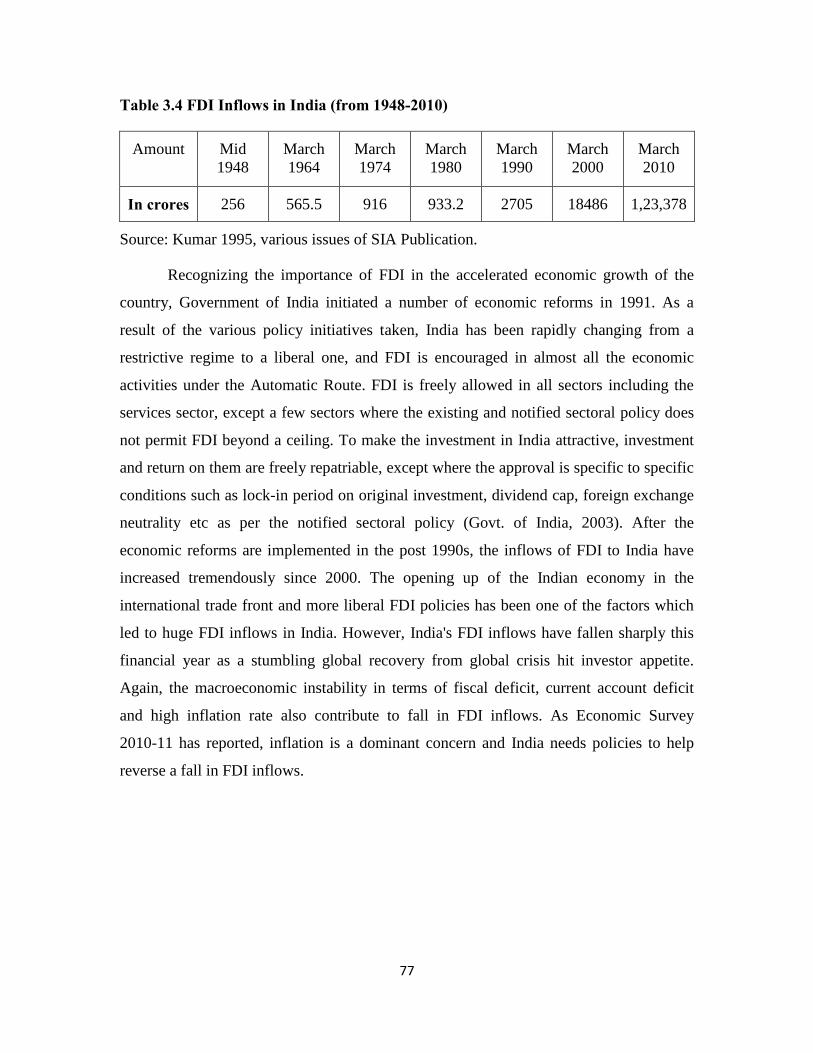

Table 3.4 FDI Inflows in India (from 1948-2010)

Amount Mid

1948

March

1964

March

1974

March

1980

March

1990

March

2000

March

2010

In crores 256 565.5 916 933.2 2705 18486 1,23,378

Source: Kumar 1995, various issues of SIA Publication.

Recognizing the importance of FDI in the accelerated economic growth of the

country, Government of India initiated a number of economic reforms in 1991. As a

result of the various policy initiatives taken, India has been rapidly changing from a

restrictive regime to a liberal one, and FDI is encouraged in almost all the economic

activities under the Automatic Route. FDI is freely allowed in all sectors including the

services sector, except a few sectors where the existing and notified sectoral policy does

not permit FDI beyond a ceiling. To make the investment in India attractive, investment

and return on them are freely repatriable, except where the approval is specific to specific

conditions such as lock-in period on original investment, dividend cap, foreign exchange

neutrality etc as per the notified sectoral policy (Govt. of India, 2003). After the

economic reforms are implemented in the post 1990s, the inflows of FDI to India have

increased tremendously since 2000. The opening up of the Indian economy in the

international trade front and more liberal FDI policies has been one of the factors which

led to huge FDI inflows in India. However, India's FDI inflows have fallen sharply this

financial year as a stumbling global recovery from global crisis hit investor appetite.

Again, the macroeconomic instability in terms of fiscal deficit, current account deficit

and high inflation rate also contribute to fall in FDI inflows. As Economic Survey

2010-11 has reported, inflation is a dominant concern and India needs policies to help

reverse a fall in FDI inflows.

78

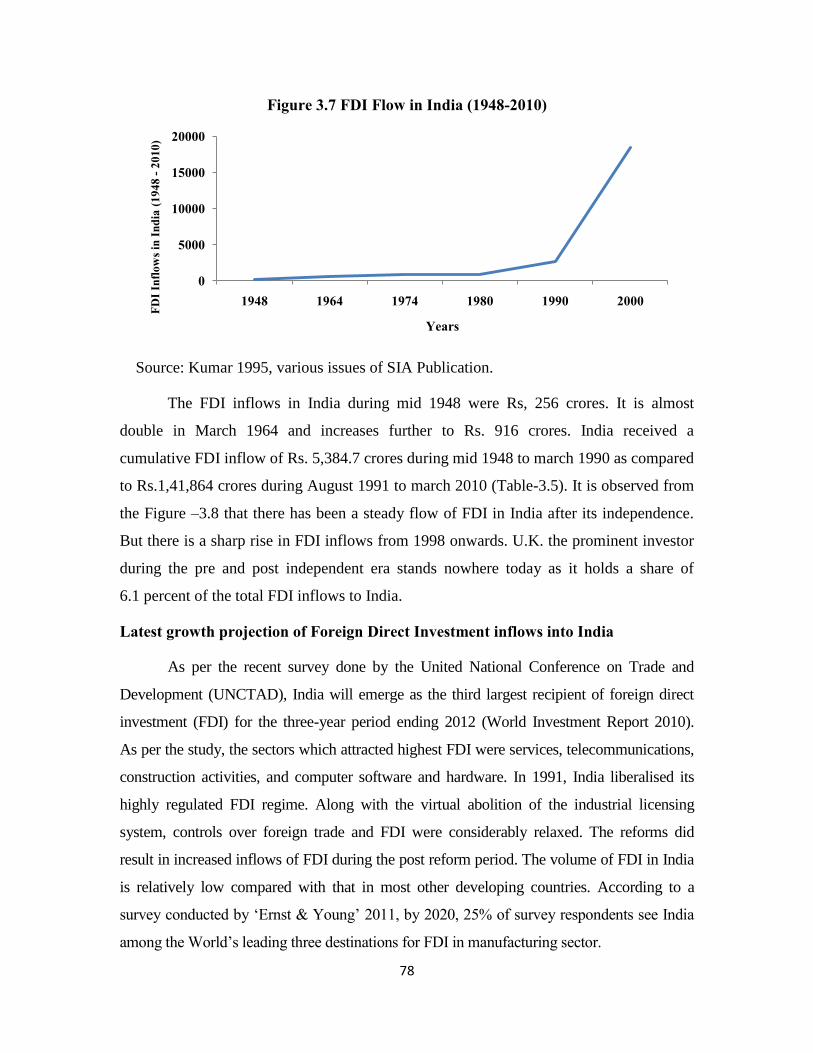

Figure 3.7 FDI Flow in India (1948-2010)

Source: Kumar 1995, various issues of SIA Publication.

The FDI inflows in India during mid 1948 were Rs, 256 crores. It is almost

double in March 1964 and increases further to Rs. 916 crores. India received a

cumulative FDI inflow of Rs. 5,384.7 crores during mid 1948 to march 1990 as compared

to Rs.1,41,864 crores during August 1991 to march 2010 (Table-3.5). It is observed from

the Figure –3.8 that there has been a steady flow of FDI in India after its independence.

But there is a sharp rise in FDI inflows from 1998 onwards. U.K. the prominent investor

during the pre and post independent era stands nowhere today as it holds a share of

6.1 percent of the total FDI inflows to India.

Latest growth projection of Foreign Direct Investment inflows into India

As per the recent survey done by the United National Conference on Trade and