an update on dnb’s strategy and portfolio within shipping

TRANSCRIPT

An update on DNB’s strategy and portfolio within shipping, offshore and logistics

Stockholm, March 15, 2013

Harald Serck-Hanssen

Norway is a leading maritime nation. DNB no. 1 shipping bank globally

Shipping

strategy

Long-term

and

relationship

driven

Leading industry expertise

DNB – a one-stop bank

Mainly

larger,

leading

industrial

clients

2

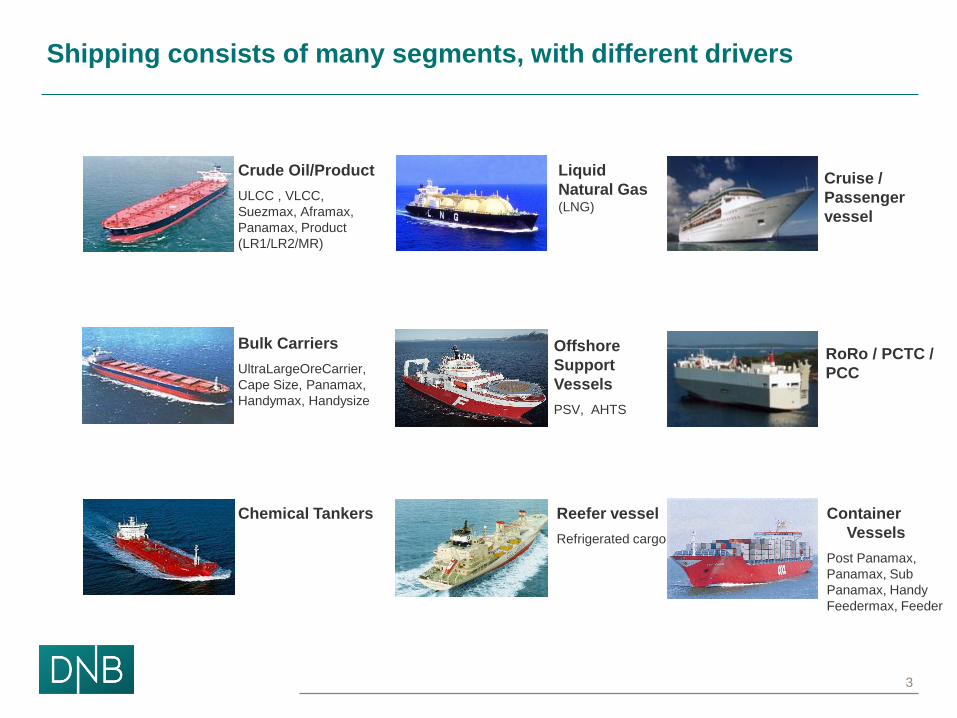

Shipping consists of many segments, with different drivers

Bulk Carriers

UltraLargeOreCarrier,

Cape Size, Panamax,

Handymax, Handysize

Crude Oil/Product

ULCC , VLCC,

Suezmax, Aframax,

Panamax, Product

(LR1/LR2/MR)

Chemical Tankers

Container

Vessels

Post Panamax,

Panamax, Sub

Panamax, Handy

Feedermax, Feeder

Liquid

Natural Gas (LNG)

Offshore

Support

Vessels

PSV, AHTS

Reefer vessel

Refrigerated cargo

RoRo / PCTC /

PCC

Cruise /

Passenger

vessel

3

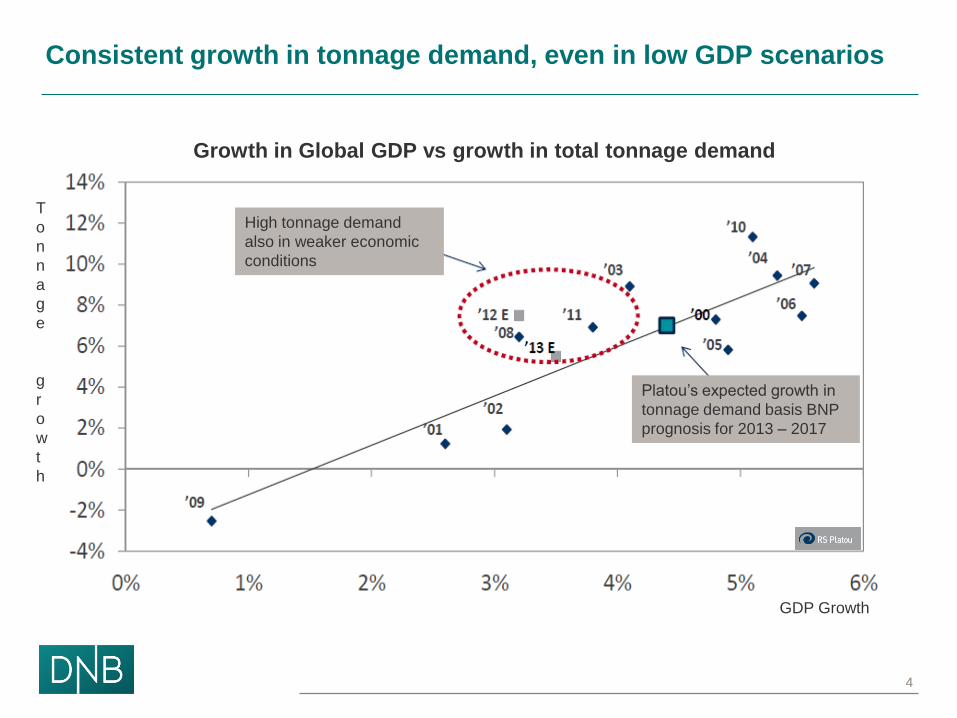

Consistent growth in tonnage demand, even in low GDP scenarios

Growth in Global GDP vs growth in total tonnage demand

High tonnage demand

also in weaker economic

conditions

Platou’s expected growth in

tonnage demand basis BNP

prognosis for 2013 – 2017

T

o

n

n

a

g

e

g

r

o

w

t

h

GDP Growth

4

Expected Worldwide Container Demand

Demand for shipping services is expected to increase further

Source: Clarkson

5

Source: Clarksons

Much lower orderbook, but challenging dry bulk and tanker markets

Orderbook now close to normal levels

► Orderbook is significantly reduced

compared with the peak in 2008

► Scrapping is increasing

► Lower increase in demand

► Spot rates expected to remain at

low levels for some time

Orderbook within the major shipping

segments as per cent of the existing fleet

6

Client selection is key to portfolio quality

► A set of financial and

minimum value covenants

► Act as early warning signals

► Used actively in client discussions

► 1st priority mortgages

► Acceptable jurisdictions

► Modern and standard tonnage

► Financial strength

► Track record & standing

► Investment horizon

► Cash flow projections

► Historical performance

► Volatility

Cash flow Client

Collateral Covenants

Client

selection

through

the 4 Cs

7

DNB maintains a diversified portfolio within shipping and offshore

► Offshore is the largest single segment

with 24%. It is comprised of drilling

rigs, support- and specialized vessels

► Industrial shipping, such as gas, ro/ro,

chemical and cruise totals 30%

► Within containers, dry bulk and

tankers the shares are 14%, 12% and

9% respectively.

Offshore is the largest segment A diversified maritime portfolio

8

Share of EaD pr. 31.12.2012

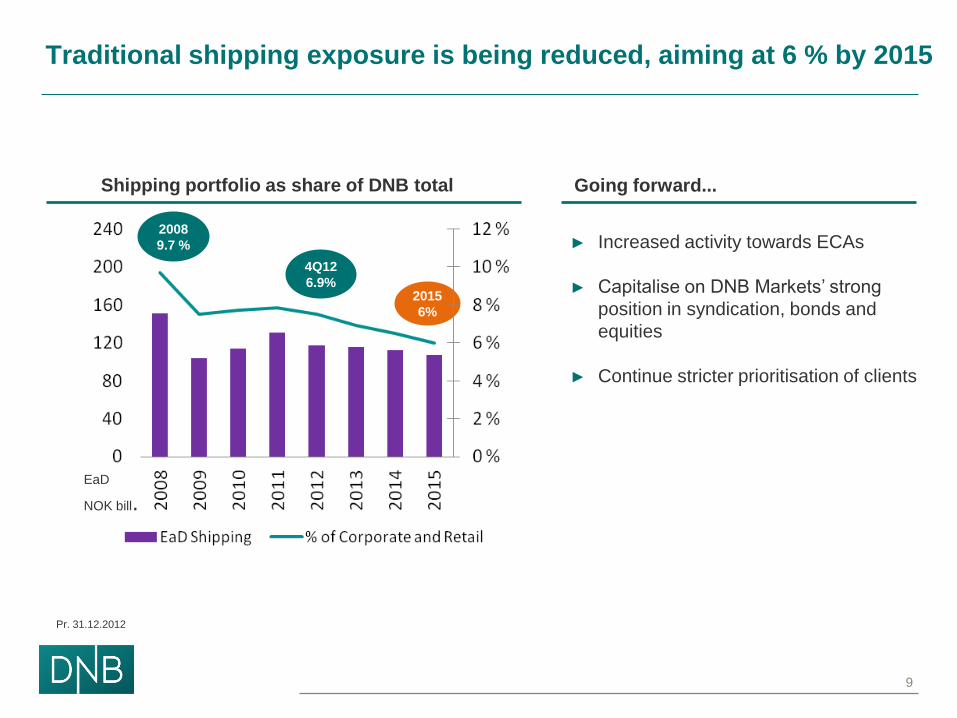

Going forward...

► Increased activity towards ECAs

► Capitalise on DNB Markets’ strong

position in syndication, bonds and

equities

► Continue stricter prioritisation of clients

Traditional shipping exposure is being reduced, aiming at 6 % by 2015

9

2008

9.7 %

4Q12

6.9% 2015

6%

Shipping portfolio as share of DNB total

EaD

NOK bill.

Pr. 31.12.2012

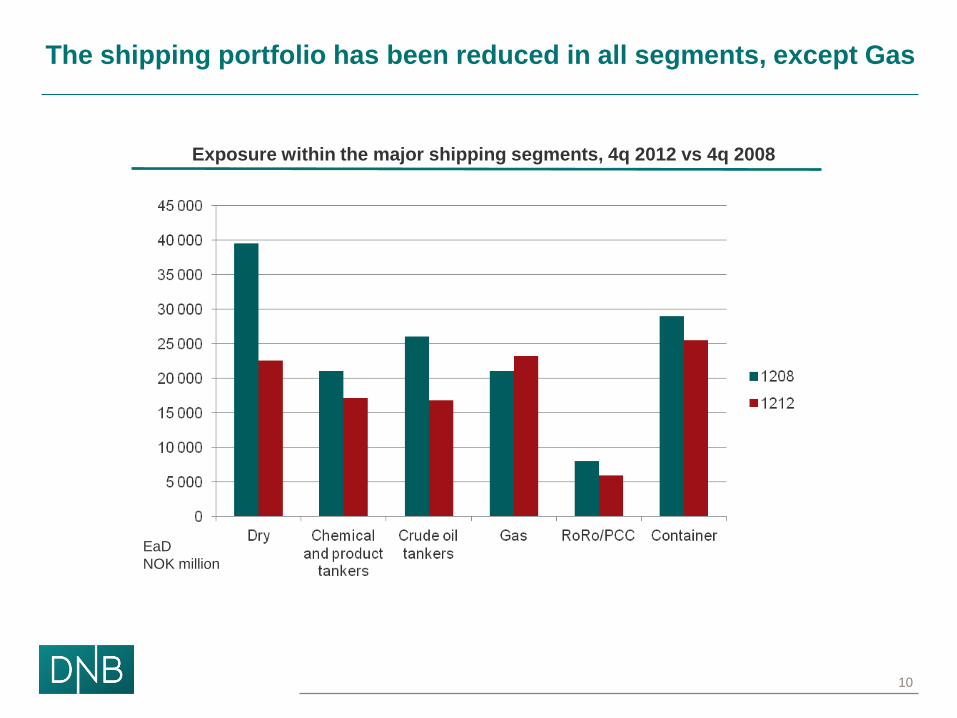

The shipping portfolio has been reduced in all segments, except Gas

Exposure within the major shipping segments, 4q 2012 vs 4q 2008

10

EaD NOK

million EaD

NOK million

Negative migration of portfolio as expected in present shipping markets

The PD

levels for

the entire

division

and within

the tanker,

dry bulk

and

container

segments

11

Shipping, Offshore and Logistics Division total The tanker segment

63

106

35

5

59

86

42

5

57

95

45

5

57

80

46

5

48

85

40

5

PD 0.01% - PD 0.75% - PD 2.0% - Net non-performingand net doubtful

commitments

NOK billion

3

13

41

4

8

41

3

10

4

03

9

5

02

9

5

0

PD 0.01% - PD 0.75% - PD 2.0% - Net non-performingand net doubtful

commitments

NOK billion

The dry bulk segment The container segment

3

14

4 33

12

633

12

633

8 74

2

8 8

3

PD 0.01% - PD 0.75% - PD 2.0% - Net non-performingand net doubtful

commitments

NOK billion

4

20

5

03

14

9

0

710 9

1

79 8

1

79 9

0

PD 0.01% - PD 0.75% - PD 2.0% - Net non-performingand net doubtful

commitments

NOK billion

31 Dec. 2011 31 March 2012 30 June 2012 30 Sept. 2012 31 Dec. 2012

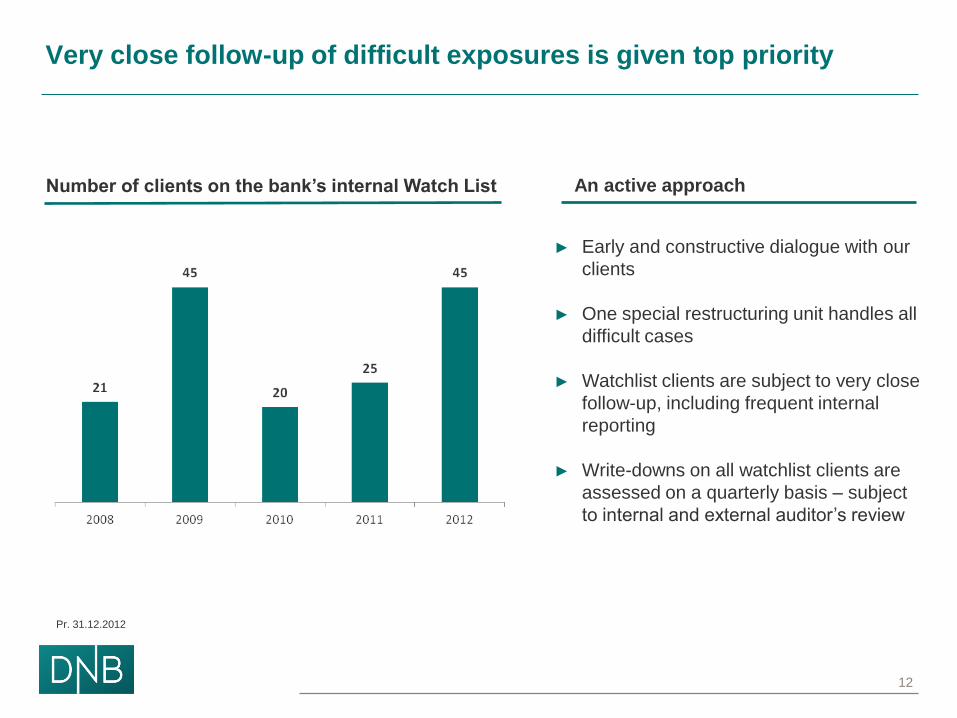

Number of clients on the bank’s internal Watch List

Very close follow-up of difficult exposures is given top priority

An active approach

12

► Early and constructive dialogue with our

clients

► One special restructuring unit handles all

difficult cases

► Watchlist clients are subject to very close

follow-up, including frequent internal

reporting

► Write-downs on all watchlist clients are

assessed on a quarterly basis – subject

to internal and external auditor’s review

Pr. 31.12.2012

Specifying the non-performing and net-doubtful commitments

Shipping’s share of non performing and net

doubtful commitments Most of the shipping loans are performing

13

► The aggregate of the Net non-performing

and Net doubtful commitments for the

DNB group totaled NOK 19.7 billion at 4Q

2012.

► The shipping share was NOK 5.2 billion.

55% was performing.

Pr. 31.12.2012

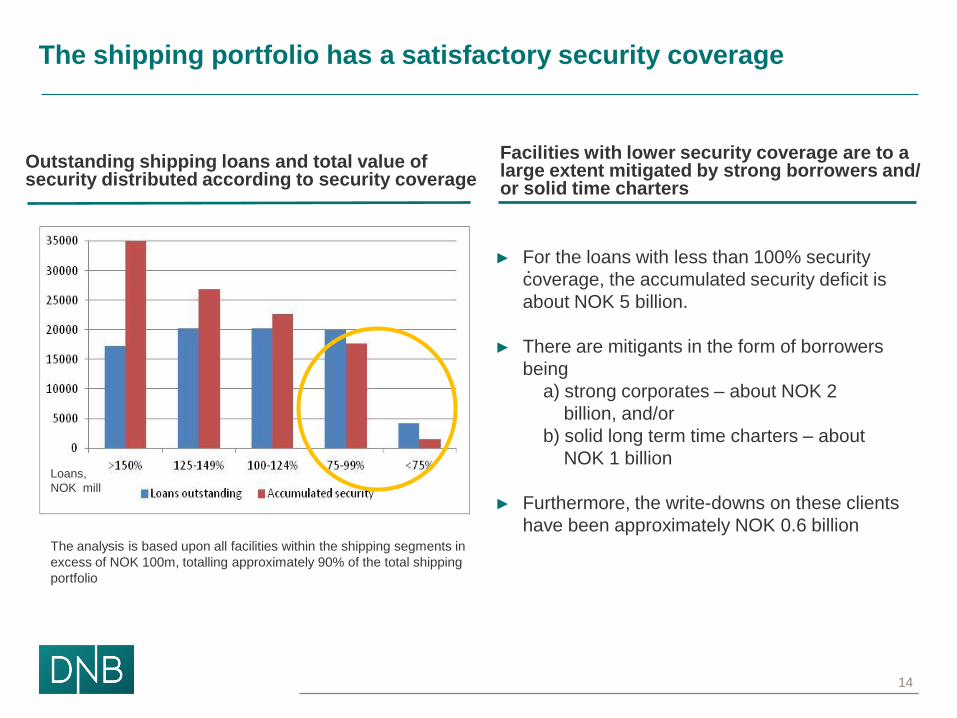

Facilities with lower security coverage are to a large extent mitigated by strong borrowers and/ or solid time charters

The shipping portfolio has a satisfactory security coverage

The analysis is based upon all facilities within the shipping segments in

excess of NOK 100m, totalling approximately 90% of the total shipping

portfolio

Loans,

NOK mill

Outstanding shipping loans and total value of security distributed according to security coverage

14

.

► For the loans with less than 100% security

coverage, the accumulated security deficit is

about NOK 5 billion.

► There are mitigants in the form of borrowers

being

a) strong corporates – about NOK 2

billion, and/or

b) solid long term time charters – about

NOK 1 billion

► Furthermore, the write-downs on these clients

have been approximately NOK 0.6 billion

A common solution is usually found to solve challenging situations

• Providing additional guarantees or

security

• Raising additional capital

• Reducing or stopping dividends

• Cancelling or postponing newbuildings

• Scrapping vessels

• Selling assets

• Cutting costs

• Modifying, postponing or waiving

covenants

• Moratorium, stretching the

repayment schedule

• "Bridge loans“ - solving temporary

liquidity challenges

• Restructuring – in several ways

Bank Contribution Shipowner Contribution

15

The average margin is increasing every quarter

16

Pr. 31.12.2012

The average margin is likely to increase further going forward

Loans distributed by margin New credits priced at around 300 bps

17

► There is a substantial repricing

potential within the division’s portfolio

► To illustrate: Repricing NOK 20 bill

with a margin of 300 bp will increase

the average margin to 205 bps.

Pr. 31.12.2012

Proven strategy contributes to low specified write-downs

NOK million

Specified write-downs 1996 - 2012 Guidance on write-downs 2012, 2013

18

► 2012 write-down level expected

to be NOK 0.8-1 billion

► Actual write-down in 2012 was

0.9 billion

► 2013 write-down level expected

to be NOK 1-1.5 billion

Pr. 31.12.2012

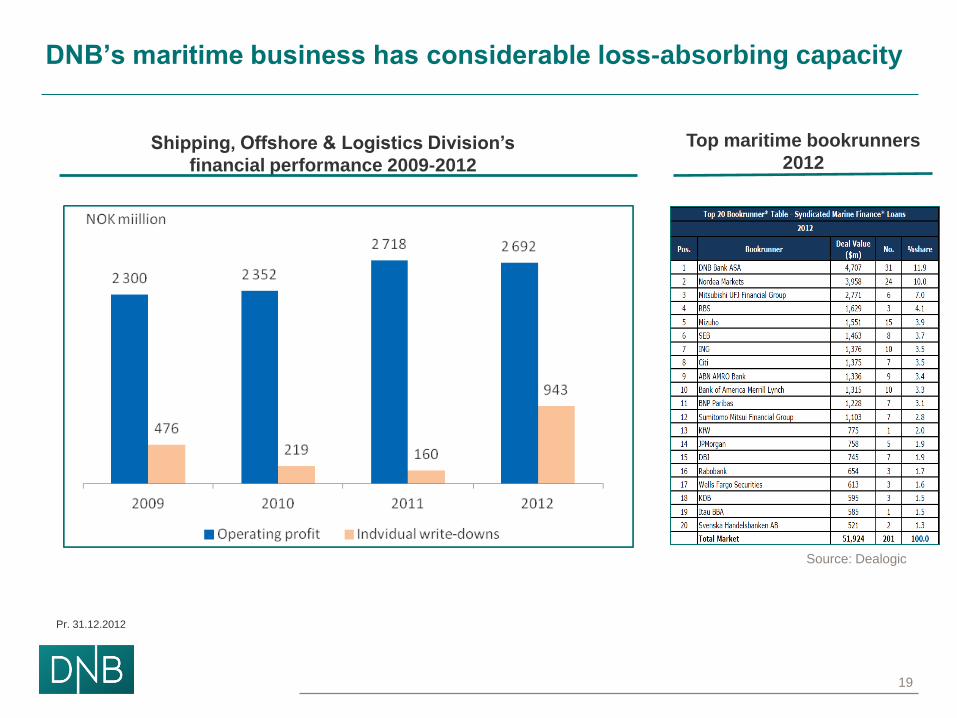

DNB’s maritime business has considerable loss-absorbing capacity

19

Top maritime bookrunners

2012

Source: Dealogic

Shipping, Offshore & Logistics Division’s

financial performance 2009-2012

Pr. 31.12.2012

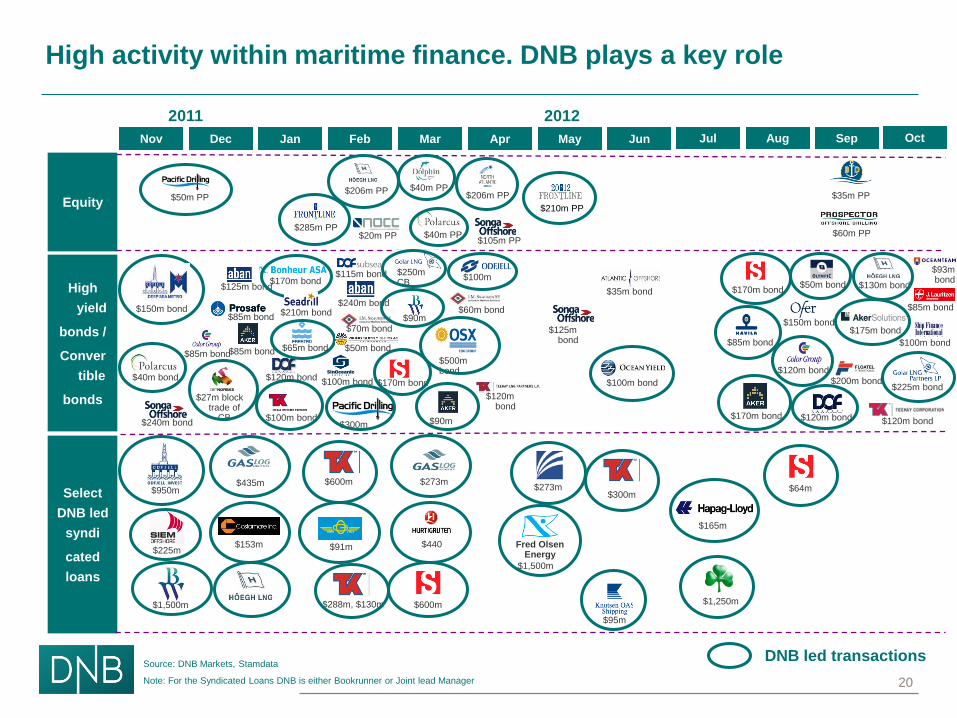

High activity within maritime finance. DNB plays a key role

Equity

High

yield

bonds /

Conver

tible

bonds

2011

Select

DNB led

syndi

cated

loans

DNB led transactions Source: DNB Markets, Stamdata

Note: For the Syndicated Loans DNB is either Bookrunner or Joint lead Manager

Jan Feb May Jun Jul Aug Sep Oct Nov

$40m bond

$150m bond

$240m bond

$950m

$1,500m

$225m

$27m block trade of

CB

$85m bond

Dec

$125m bond

$85m bond

$100m bond

$170m bond

$85m bond

$120m bond

$65m bond

$210m bond

$115m bond

2012

$435m

$153m

$288m, $130m

$285m PP

$206m PP $50m PP

$100m bond

$300m

$70m bond

Mar

$240m bond

$250m CB

$90m

$90m

$600m

$50m bond

$170m bond

$500m bond

$100m

Apr

$60m bond

$120m bond

$20m PP

$40m PP

$40m PP $105m PP

$273m

$600m

$440 $91m

$125m bond

$210m PP

$206m PP

$35m bond

$1,500m

Fred Olsen Energy

$100m bond

$95m

$300m $273m

$85m bond

$170m bond

$170m bond

$1,250m

$165m

$64m

$120m bond

$120m bond

$50m bond $130m bond

$175m bond

$225m bond

$120m bond

$150m bond

$200m bond

$35m PP

$60m PP

$100m bond

$85m bond

$93m bond

20

21

In summary...

► DNB has a proven track record within shipping,

delivering strong results each year

► By concentrating on the larger and leading

companies within each segment the risk is

acceptable. These companies have a high

demand for non-lending products

► Targeting 6 per cent shipping exposure of total

DNB Group EaD by 2015

► Write-downs expected to be NOK 0.8-1 billion in

2012, and NOK 1-1.5 billion in 2013

► DNB’s maritime business is profitable and has

considerable loss-absorbing capacity

Appendix

• Illustrative Case: USD 1 billion (70%) financing of modern vessels

22

Illustrative Case: USD 1 billion (70%) financing of modern vessels

2006: DNB’s well established client acquires a fleet of

modern vessels for USD 1.000 mill.. A bankgroup led

by DNB provides 70% financing based upon 1st pr.

mortgages and a set of covenants. DNB’s share of the

loan is 30%. It is a 7 year facility with a 15 year profile.

2008: Values are down 30%, the client cuts costs and

stops dividends. Satisfactory EBITDA next 2 years due

to contract coverage. The bank group reduces the min.

value clause (MVC) to 100% for 2 years.

2010: Values drop a further 15%, and the cash flow

is weak. The company attracts some new hybrid capital,

the banks agree to reduce the MVC for a further year

and forego installments.

2012: Values drop a further 15%. In a theoretical

WORST CASE scenario the Client gives up, and the

banks sell the assets, realizing a loss of MUSD 7, ie 1%

of the original loan amount. DNB’s share of the loss is

MUSD 2.1.

70% financing of a USD 1 billion investment

• Valued are provided by recognized brokers. DNB

finances mostly standard vessels

• Detailed cash flow analysis of the clients are based upon

conservative base- and risk case assumptions

MUSD

Vessel values drop by 50%, whereas the loan loss is

1% of the original loan amount.

23