analysis of alcoholic drinks market in vietnam · alcoholic drinks market in vietnam. that's...

TRANSCRIPT

1

ANALYSIS OF ALCOHOLIC

DRINKS MARKET IN VIETNAM

T.Q.NGUYEN and F.SEYTE

LAMETA University Montpellier1

2

INTRODUCTION

• From Fama (1970) an efficient market is a market on

which prices reflect simultaneously and completely all

the information available and relevant: the best predictor

of course tomorrow is today's lesson.

• The aim of this paper is to analyze the efficiency of the

alcoholic drinks market in Vietnam. That's what we will

analyze segmentation of the market in the first part and

market efficiency in the second part.

PART1

ANALISIS OF SEGMENTATION

PART2

ANALISIS

OF MARKET EFFICIENCY

3

PART 1

ANALYSIS OF SEGMENTATION

4

The demand for beer and wine in

Vietnam forecast to 2015(million

liters)

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

2009 2010 2011 2012 2013 2014 2015

Year

Mill

ion liters

Demand on Beer

Demand on Alcohol

5

• the current average consumption of beer

of the people of our country is 15.8 liters

per year, in 2 / 3 compared with the

consumption of the world

• Average consumption of alcohol was 3.9

liters in which the demand is 6 liters

6

The number of manufacturing

enterprises in Beer - Alcohol -

Beverage by specialization:Specializat

ionNumber of enterprises Evolution(%/year)

2000 2005 2006 2007 2000-

2005

2006-

2007

Beer 137 163 167 151 3,54 -3,75

Alcohol 28 77 75 78 22,42 0,65

Soft Drink 602 727 771 1013 3,85 14,04

Total 767 967 1013 1242 4,74 13,33

7

• the number of enterprises of the industry

increased rapidly, especially in the period

2006-2007 more than 13% per year

• the beverage manufacturing industry has

the largest number of enterprises, then to

the beer industry

• Wine industry is at the least number of

enterprises

8

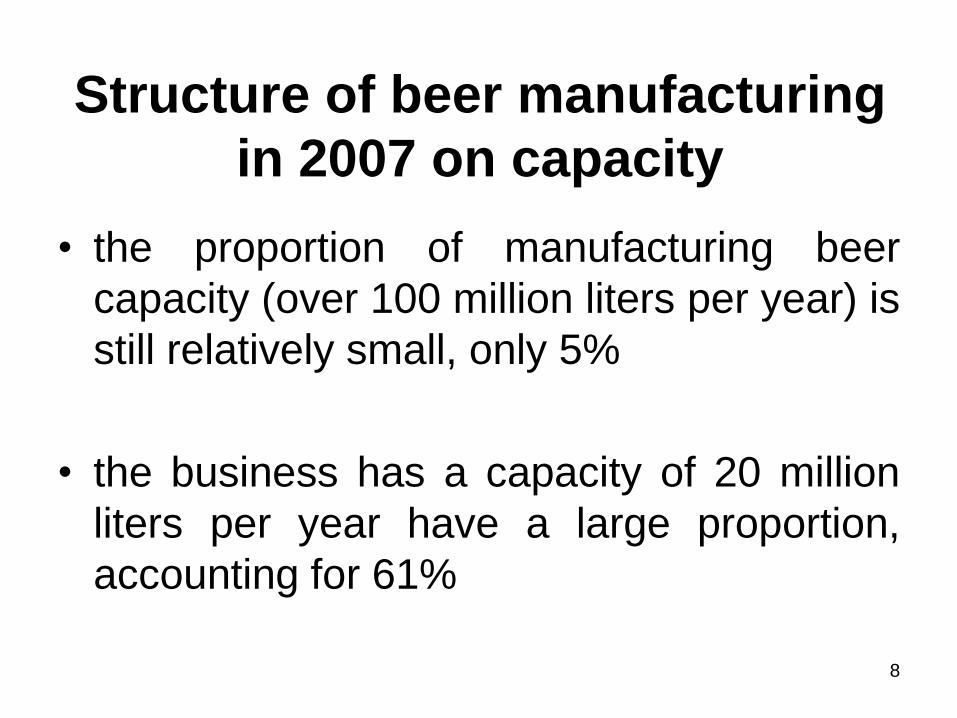

Structure of beer manufacturing

in 2007 on capacity

• the proportion of manufacturing beer

capacity (over 100 million liters per year) is

still relatively small, only 5%

• the business has a capacity of 20 million

liters per year have a large proportion,

accounting for 61%

9

5% 13%

21%61%

>100 million liters

50-100 million liters

20-50 million liters

<20 million liters

10

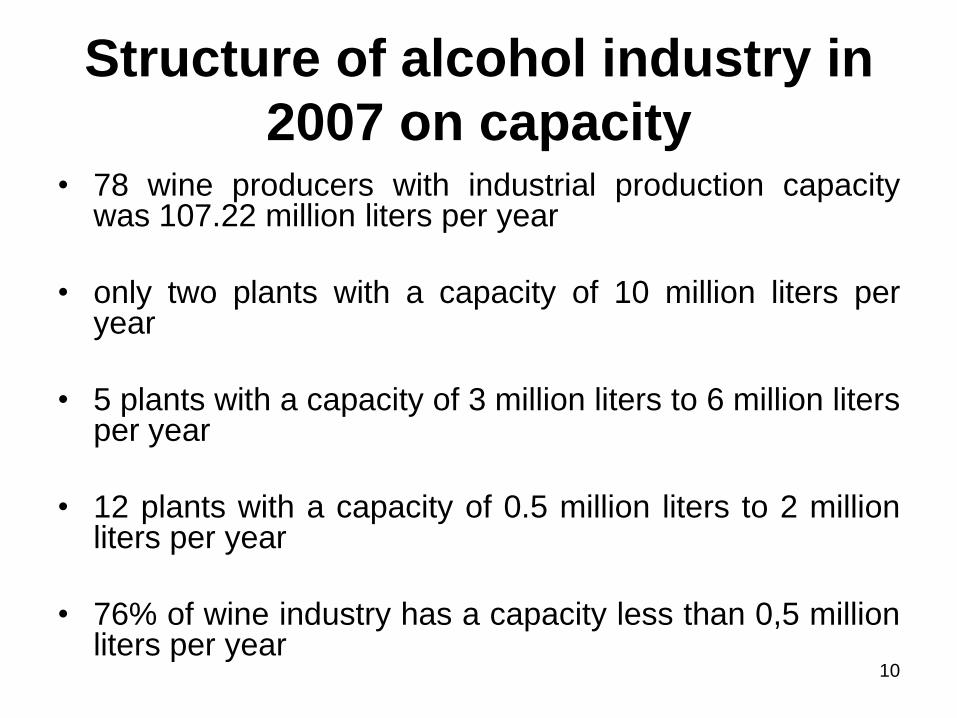

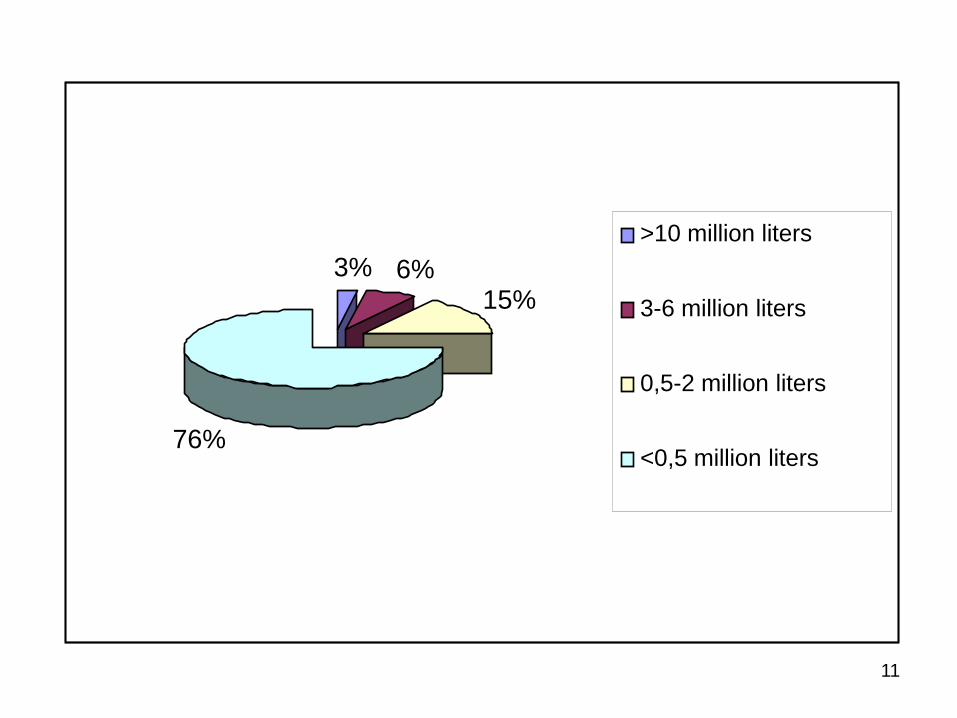

Structure of alcohol industry in

2007 on capacity• 78 wine producers with industrial production capacity

was 107.22 million liters per year

• only two plants with a capacity of 10 million liters peryear

• 5 plants with a capacity of 3 million liters to 6 million litersper year

• 12 plants with a capacity of 0.5 million liters to 2 millionliters per year

• 76% of wine industry has a capacity less than 0,5 millionliters per year

11

3% 6%15%

76%

>10 million liters

3-6 million liters

0,5-2 million liters

<0,5 million liters

12

Structure of production enterprises in all

economic sectors (%)

2000 2005 2006 2007

State

enterprises32,72 3,93 3,06 2,66

Non state

enterprises65,58 92,24 93,39 95,01

Foreign –

invested

enterprises

1,69 3,83 3,55 2,33

13

• the state enterprise is the largest scale(445 billion Vietnam dong / enterprise; 242people / business)

• then to the area of foreign investmentcapital (384 billion Vietnam dong /enterprise; 226 people per enterprise)

• and after the sector non-state (9 billionVietnam dong per enterprise, 18 persons /company)

14

Structure of productions by region (%):

2000 2005 2006 2007

Red River

Delta

14,08 24,41 26,65 23,35

Central

Northern

mountainous

4,30 4,55 4,64 4,75

Central Coast 15,91 22,54 16,88 21,01

Highlands

(Tay Nguyen)

0,65 2,79 3,06 3,46

Southeast

region

21,90 35,16 38,01 33,82

Cửu Long

River Delta

43,16 10,55 10,76 13,61

Total 100 100 100 100

15

• production capacity is mainly concentrated

in central cities

• For the brewing industry, Hanoi accounted

for 19.53% of total national production

capacity, Ho Chi Minh City (19.7%)

• Production value of the Beer - Alcohol -

Beverage increase continuously in the

period from 2000 to 2007 with average

growth rate of over 15% per year

16

Structuring and restructuring of products

(%)

Beer 2000 2005 2006 2007

Bottled beer 56,43 56,50 55,60 55,11

Beer cans 10,29 15,23 15,45 17,08

Draught beer 33,27 28,27 28,95 27,81

17

• bottled beer accounts for the largest

proportion (over 55%) also beer cans has

lowest proportion in all years

• The proportion of beer cans tend to

increase while the draught beer tends to

decrease

18

Structuring and restructuring of products

(%)

Alcohol

production

2000 2005 2006 2007

White wine

>25°

3,76 5,93 11,58 11,90

Colored

wine>25°

2,85 0,96 1,60 1,40

Sparkling

wine

0,24 0,13 0,17 0,16

Wine from

fresh fruit

5,08 3,91 4,22 4,3

Bulk Alcohol 88,07 89,07 82,43 82,25

19

• the largest proportion is bulk alcohol; the

proportion of this alcohol is 82%.

• fresh fruit decreased slowly

20

• As forecast, the demand for beer, wine, soft drinks in thecountry and around the world are still large; this is agood opportunity for industry development in the future.

• Despite the conditions and opportunities for developmentbut the last time beer and wine industry meet basicneeds in the mass market, not export. The Beverageindustry has some high-end products but is very strongcompetition by products of the leading beveragecompany in the world.

• Industrial production of beer, wine, soft drinks are stillgrowing strongly. Especially in the near future, theindustry tends to focus in Asia and Southeast Asia; thisis just the opportunity but also creates enormouspressure for the beer - alcohol - water in Vietnam.

21

PART 2

ANALISIS OF MARKET EFFICIENCY

22

We have 7 categories of products most consumed(annual series 1960-2010)

Rice wine to 35 °

Rice wine Lua Moi 40 °

Wine Thang Long

Draught beer Hanoi

Bottled beer Ha Noi

Tiger Beer

Heineken Beer

23

Data characteristics and unit root tests

LAL LLM LHE LPH LTI LHN LTL

Mean 6.69 9.06 8.06 7.29 7.83 7.71 7.70

Median 6.55 8.73 7.83 7.39 7.57 7.46 7.30

Std.Dev 1.30 0.75 0.72 0.73 0.75 0.81 1.16

Skewness

Normality

test

0.29

1.59

0.59

2.24

0.55

2.17

-0.51

2.10

0.55

2.16

0.35

1.72

0.41

1.88

Kurtosis

Normality

test

1.94

-1.52

1.95

-1.52

2.05

-1.37

2.70

-0.43

2.06

-1.36

1.96

-1.51

1.97

-1.50

Jarque-Bera 3.12 5.33 4.53 2.48 4.44 3.33 3.74

Dickey-

Fuller

augmented

-0.32

(4r)

-3.51

-1.93

(4r)

-3.51

0.13

(6r)

-3.51

-1.40

(6r)

-3.51

-0.75

(8r)

-3.52

-1.26

(8r)

-3.52

0.19

(10r)

-3.52

Philips-

Perron

-1.08

(1r)

-3.50

-1.14

(1r)

-3.50

-0.13

(1r)

-3.50

-1.46

(1r)

-3.50

0.04

(1r)

-3.50

-2.30

(1r)

-3.50

3.83

(1r)

-3.50

Dickey-

pentula

-0.74

-3.19

-1.21

-3.19

-0.59

-3.19

-1.49

-3.19

-0.66

-3.19

-2.69

-3.19

-1.06

-3.19

24

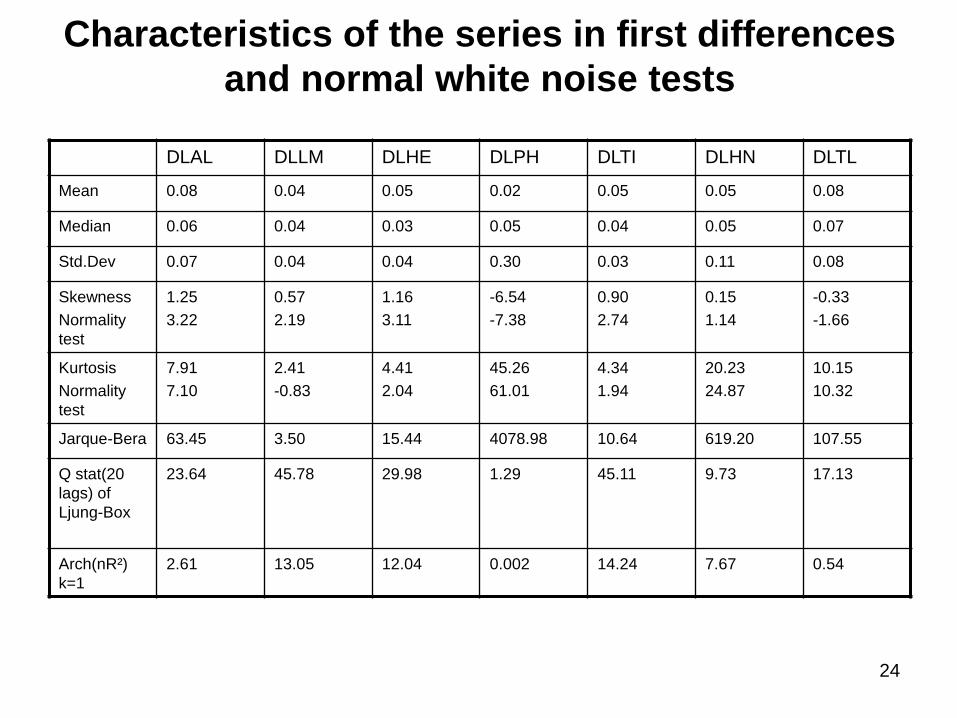

Characteristics of the series in first differences

and normal white noise tests

DLAL DLLM DLHE DLPH DLTI DLHN DLTL

Mean 0.08 0.04 0.05 0.02 0.05 0.05 0.08

Median 0.06 0.04 0.03 0.05 0.04 0.05 0.07

Std.Dev 0.07 0.04 0.04 0.30 0.03 0.11 0.08

Skewness

Normality

test

1.25

3.22

0.57

2.19

1.16

3.11

-6.54

-7.38

0.90

2.74

0.15

1.14

-0.33

-1.66

Kurtosis

Normality

test

7.91

7.10

2.41

-0.83

4.41

2.04

45.26

61.01

4.34

1.94

20.23

24.87

10.15

10.32

Jarque-Bera 63.45 3.50 15.44 4078.98 10.64 619.20 107.55

Q stat(20

lags) of

Ljung-Box

23.64 45.78 29.98 1.29 45.11 9.73 17.13

Arch(nR²)

k=1

2.61 13.05 12.04 0.002 14.24 7.67 0.54

25

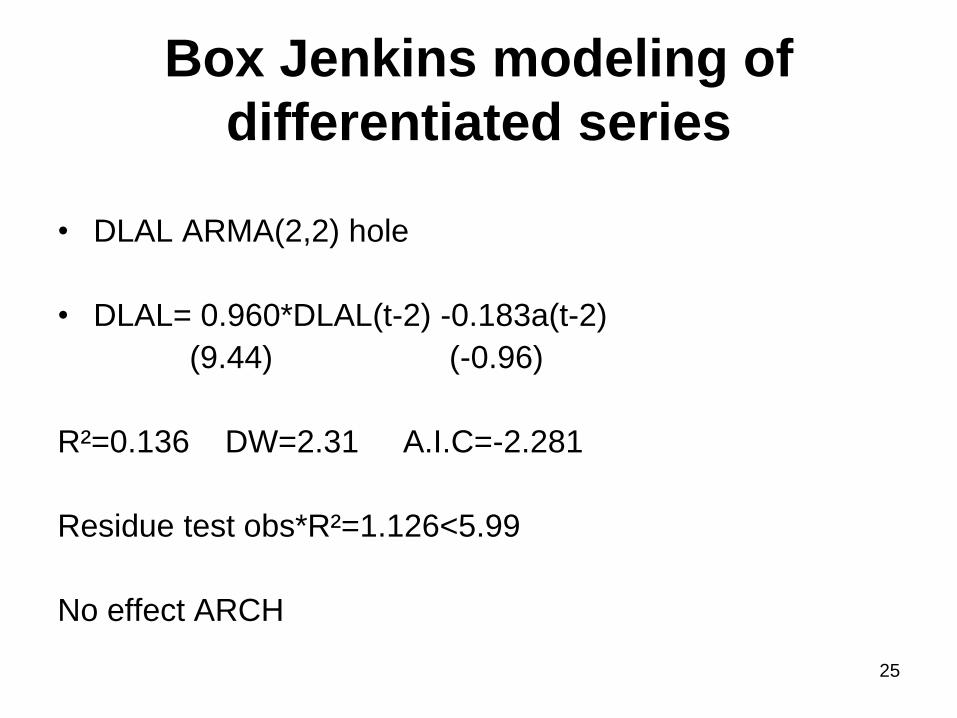

Box Jenkins modeling of

differentiated series

• DLAL ARMA(2,2) hole

• DLAL= 0.960*DLAL(t-2) -0.183a(t-2)

(9.44) (-0.96)

R²=0.136 DW=2.31 A.I.C=-2.281

Residue test obs*R²=1.126<5.99

No effect ARCH

26

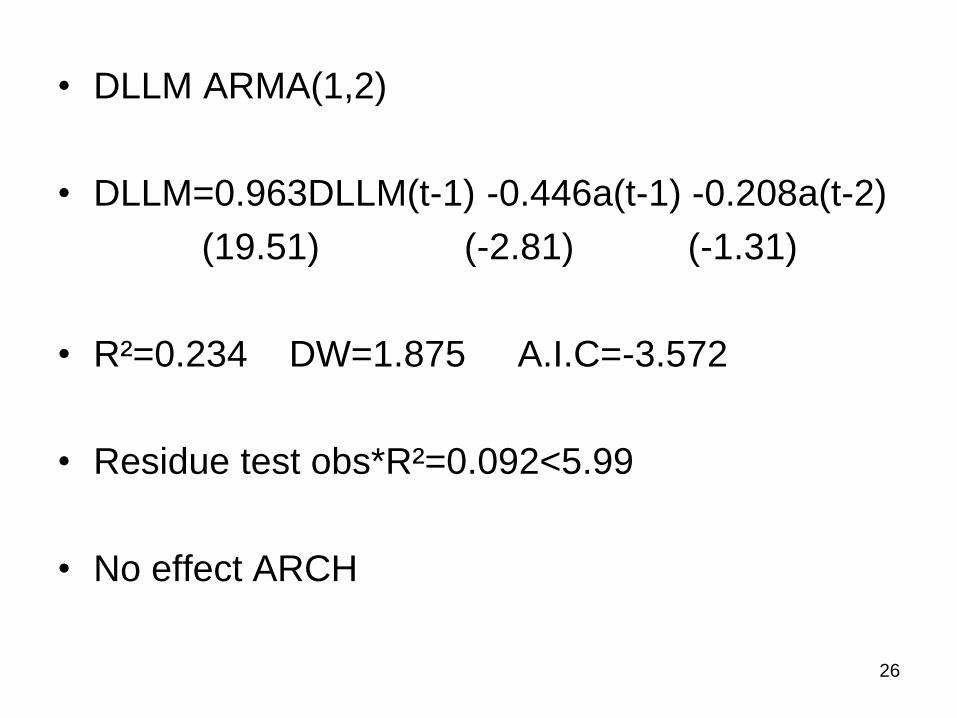

• DLLM ARMA(1,2)

• DLLM=0.963DLLM(t-1) -0.446a(t-1) -0.208a(t-2)

(19.51) (-2.81) (-1.31)

• R²=0.234 DW=1.875 A.I.C=-3.572

• Residue test obs*R²=0.092<5.99

• No effect ARCH

27

• DLHE ARMA(2,2) hole

• DLHE=0.926DLHE(t-2) +0.556a(t-1) -0.439a(t-2)

(8.27) (0.55) (-0.43)

• R²=0.221 DW=2.05 A.I.C=-3.705

• Residue test obs*R²=0.254<5.99

• No effect ARCH

28

• DLPH ARMA(10,10)

• R²=0.791 DW=0.367 A.I.C=-0.088

• Residue test obs*R²=14.621>5.99

• Effect ARCH

29

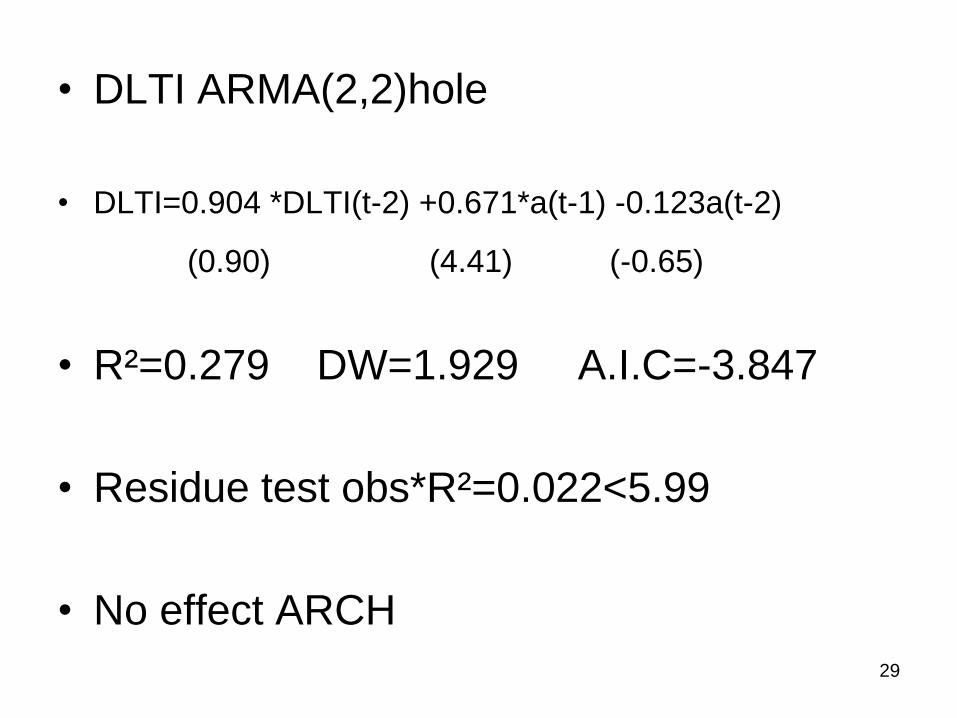

• DLTI ARMA(2,2)hole

• DLTI=0.904 *DLTI(t-2) +0.671*a(t-1) -0.123a(t-2)

(0.90) (4.41) (-0.65)

• R²=0.279 DW=1.929 A.I.C=-3.847

• Residue test obs*R²=0.022<5.99

• No effect ARCH

30

• DLHN ARMA(7,1)hole

• R²=0.145 DW=1.94 A.I.C=-1.177

• Residue test obs*R²=2.202<5.99

• No effect ARCH

31

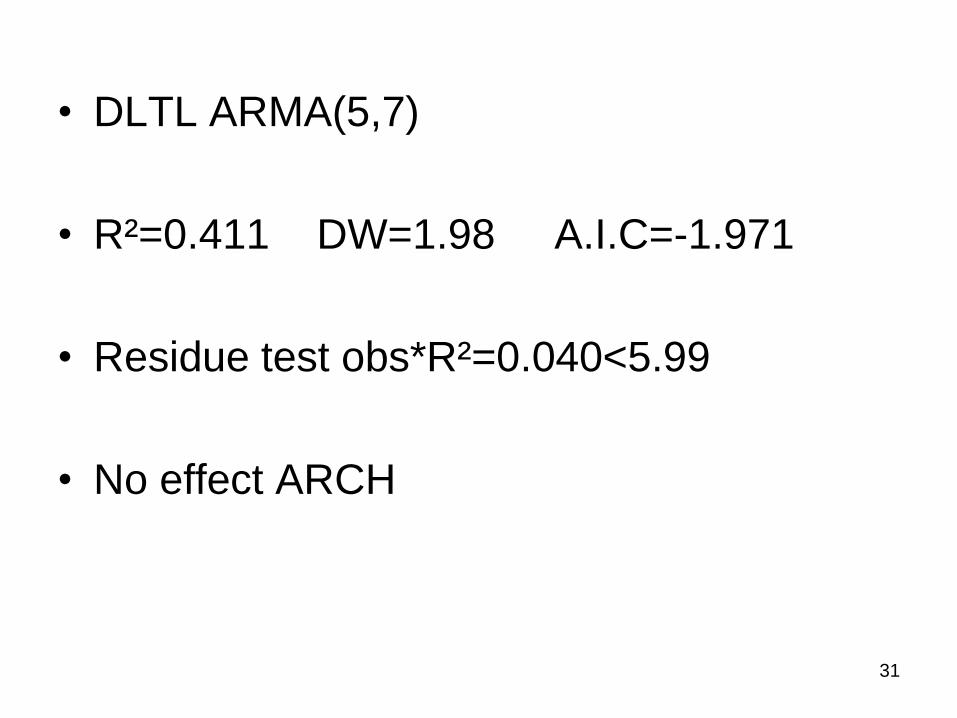

• DLTL ARMA(5,7)

• R²=0.411 DW=1.98 A.I.C=-1.971

• Residue test obs*R²=0.040<5.99

• No effect ARCH

32

• DLPH ARMA(10,10) error Garch(1,1)

• a(t)=u(t)*h(t) where h(t)→N(0,1)

• h²(t)=0.064964-0.050664a²(t-1) +0.552116h²(t-1)

33

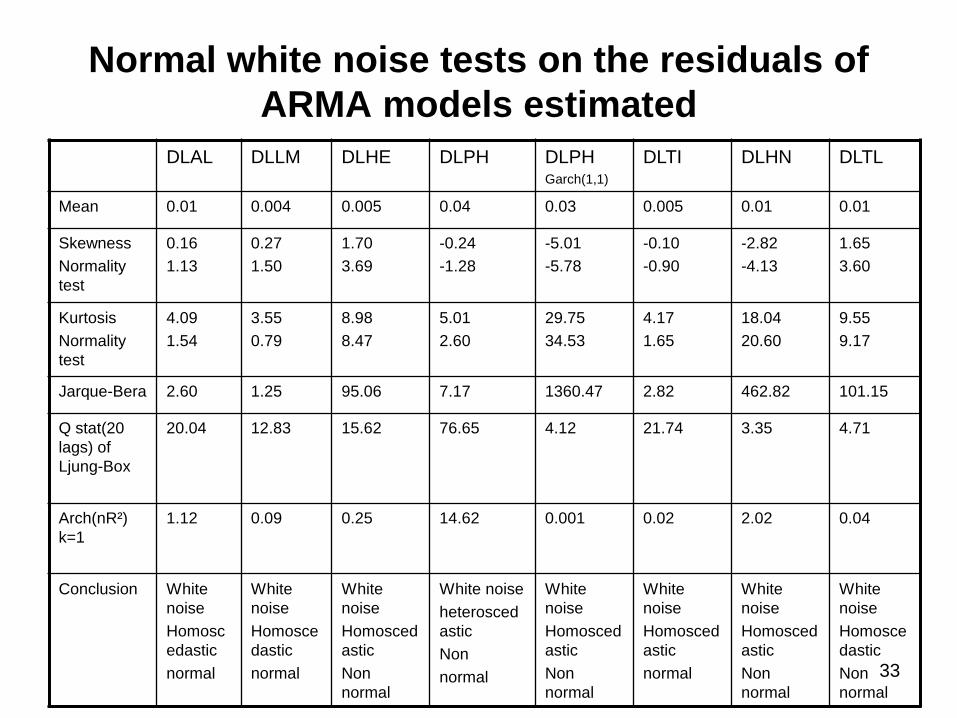

Normal white noise tests on the residuals of

ARMA models estimated

DLAL DLLM DLHE DLPH DLPHGarch(1,1)

DLTI DLHN DLTL

Mean 0.01 0.004 0.005 0.04 0.03 0.005 0.01 0.01

Skewness

Normality

test

0.16

1.13

0.27

1.50

1.70

3.69

-0.24

-1.28

-5.01

-5.78

-0.10

-0.90

-2.82

-4.13

1.65

3.60

Kurtosis

Normality

test

4.09

1.54

3.55

0.79

8.98

8.47

5.01

2.60

29.75

34.53

4.17

1.65

18.04

20.60

9.55

9.17

Jarque-Bera 2.60 1.25 95.06 7.17 1360.47 2.82 462.82 101.15

Q stat(20

lags) of

Ljung-Box

20.04 12.83 15.62 76.65 4.12 21.74 3.35 4.71

Arch(nR²)

k=1

1.12 0.09 0.25 14.62 0.001 0.02 2.02 0.04

Conclusion White

noise

Homosc

edastic

normal

White

noise

Homosce

dastic

normal

White

noise

Homosced

astic

Non

normal

White noise

heterosced

astic

Non

normal

White

noise

Homosced

astic

Non

normal

White

noise

Homosced

astic

normal

White

noise

Homosced

astic

Non

normal

White

noise

Homosce

dastic

Non

normal

34

CONCLUSION

• The series are not directly modeled by an ARMAprocess or TS. Logarithms of prices have unitroots but their first differences are oftenautocorrelated and Homoscedastic, theassumption of normal white noise can not bealways verified

• The results of the alcohol market allows us toconfirm the hypothesis of efficiency. Sets pricesAlcohol bulk, Alcohol Lua Moi, and Tiger beerare martingales with normal white noise.

• The markets for beer and wine are consideredas quasi-efficient: series of the price of beer andwine to follow martingale processes not normal