analytical perspectives - the white house

TRANSCRIPT

Analytical PerspectivesBudget of the U.S. GovernmentFISCAL YEAR 2022

OFFICE OF MANAGEMENT AND BUDGET

Analytical PerspectivesBudget of the U.S. GovernmentFISCAL YEAR 2022

OFFICE OF MANAGEMENT AND BUDGET

THE BUDGET DOCUMENTS

Budget of the United States Government, Fiscal Year 2022 contains the Budget Message of the President, information on the President’s priori-ties, and summary tables.

Analytical Perspectives, Budget of the United States Government, Fiscal Year 2022 contains analyses that are designed to highlight specified subject areas or provide other significant presenta-tions of budget data that place the budget in perspec-tive. This volume includes economic and accounting analyses, information on Federal receipts and collec-tions, analyses of Federal spending, information on Federal borrowing and debt, baseline or current ser-vices estimates, and other technical presentations.

Supplemental tables and other materials that are part of the Analytical Perspectives vol-ume are available at https://whitehouse.gov/omb/analytical-perspectives/.

Appendix, Budget of the United States Government, Fiscal Year 2022 contains detailed information on the various appropriations and funds that constitute the budget and is designed primarily for the use of the Appropriations Committees. The Appendix contains more detailed financial infor-mation on individual programs and appropriation accounts than any of the other budget documents. It includes for each agency: the proposed text of

appropriations language; budget schedules for each account; legislative proposals; narrative explana-tions of each budget account; and proposed general provisions applicable to the appropriations of entire agencies or group of agencies. Information is also provided on certain activities whose transactions are not part of the budget totals.

BUDGET INFORMATION AVAILABLE ONLINE

The President’s Budget and supporting materials are available online at https://whitehouse.gov/omb/budget/. This link includes electronic versions of all the budget volumes, supplemental materials that are part of the Analytical Perspectives volume, spread-sheets of many of the budget tables, and a public use budget database. This link also includes Historical Tables that provide data on budget receipts, outlays, surpluses or deficits, Federal debt, and Federal em-ployment over an extended time period, generally from 1940 or earlier to 2022 or 2026. Also available are links to documents and materials from budgets of prior years.

For more information on access to electronic ver-sions of the budget documents, call (202) 512-1530 in the D.C. area or toll-free (888) 293-6498. To pur-chase the printed documents call (202) 512-1800.

GENERAL NOTES1. All years referenced for budget data are

fiscal years unless otherwise noted. All years referenced for economic data are calendar years unless otherwise noted.

2. Detail in this document may not add to the totals due to rounding.

U.S. GOVERNMENT PUBLISHING OFFICE, WASHINGTON 2021

iii

Page

TABLE OF CONTENTS

List of Charts and Tables .......................................................................................................................v

Introduction

1. Introduction .................................................................................................................................3

Economic and Budget Analyses

2. Economic Assumptions and Overview ........................................................................................7

3. Long-Term Budget Outlook .......................................................................................................17

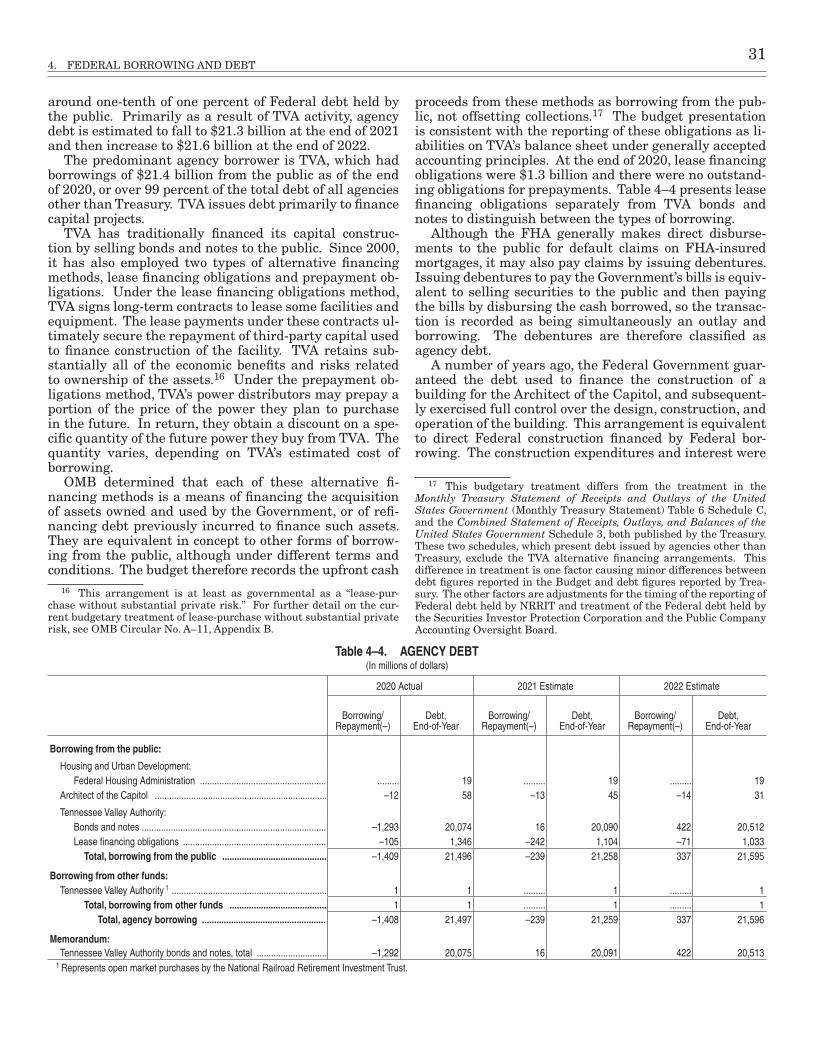

4. Federal Borrowing and Debt .....................................................................................................23

Management

5. Strengthening the Federal Workforce .......................................................................................41

Budget Concepts and Budget Process

6. Budget Concepts.........................................................................................................................55

7. Coverage of the Budget ..............................................................................................................79

Federal Receipts

8. Governmental Receipts ..............................................................................................................87

9. Offsetting Collections and Offsetting Receipts .........................................................................97

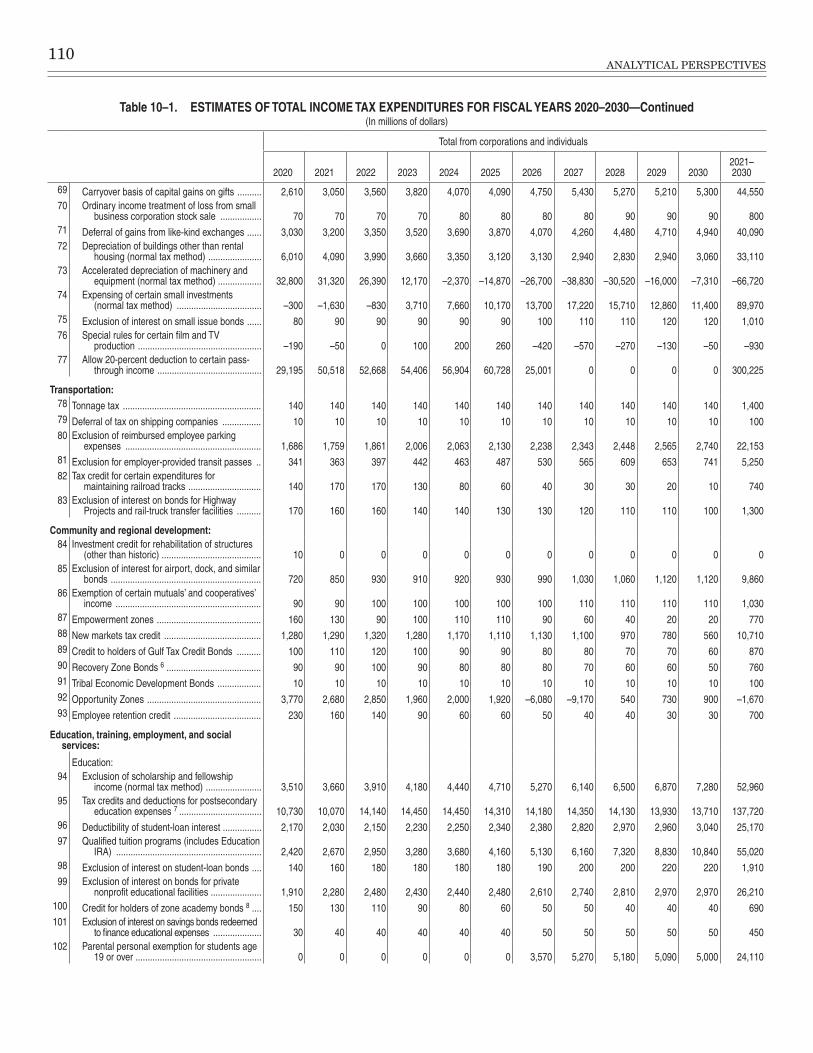

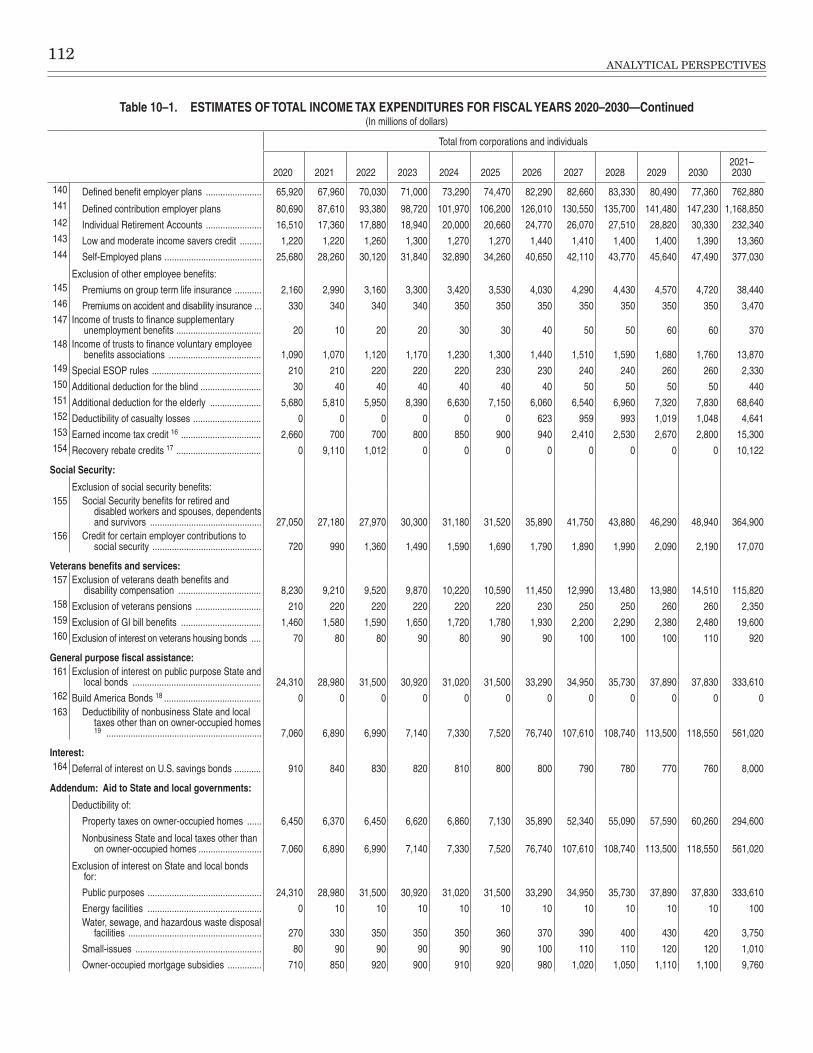

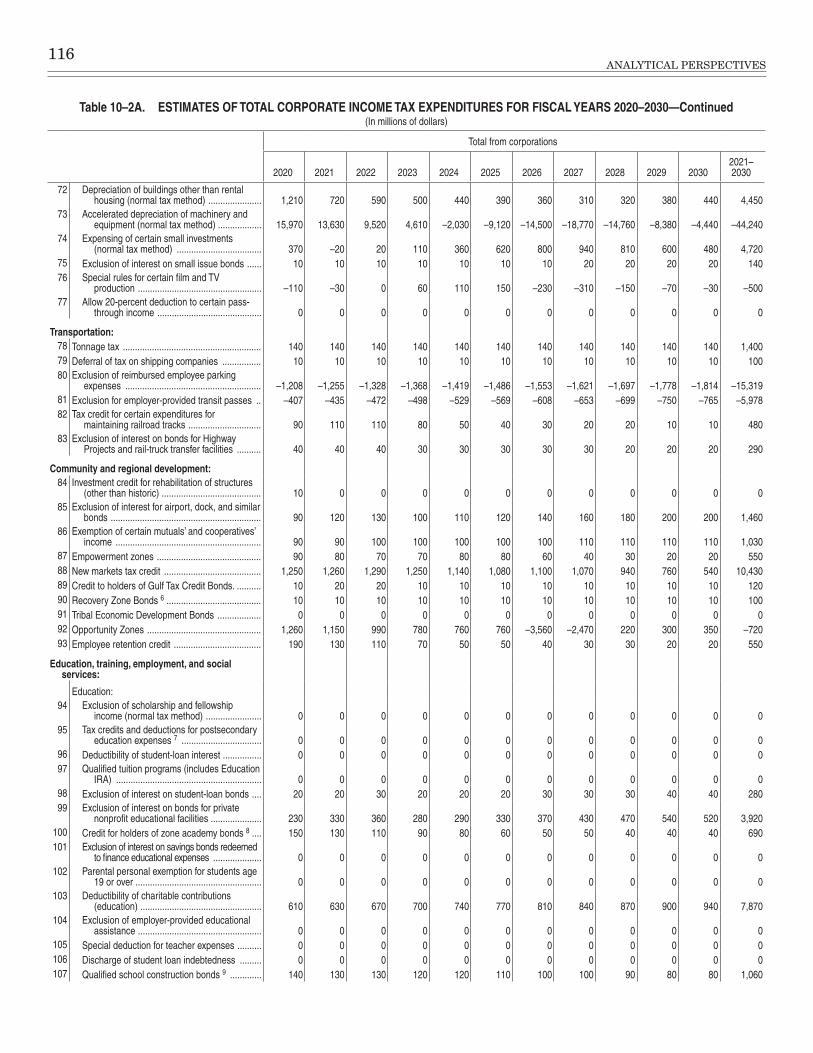

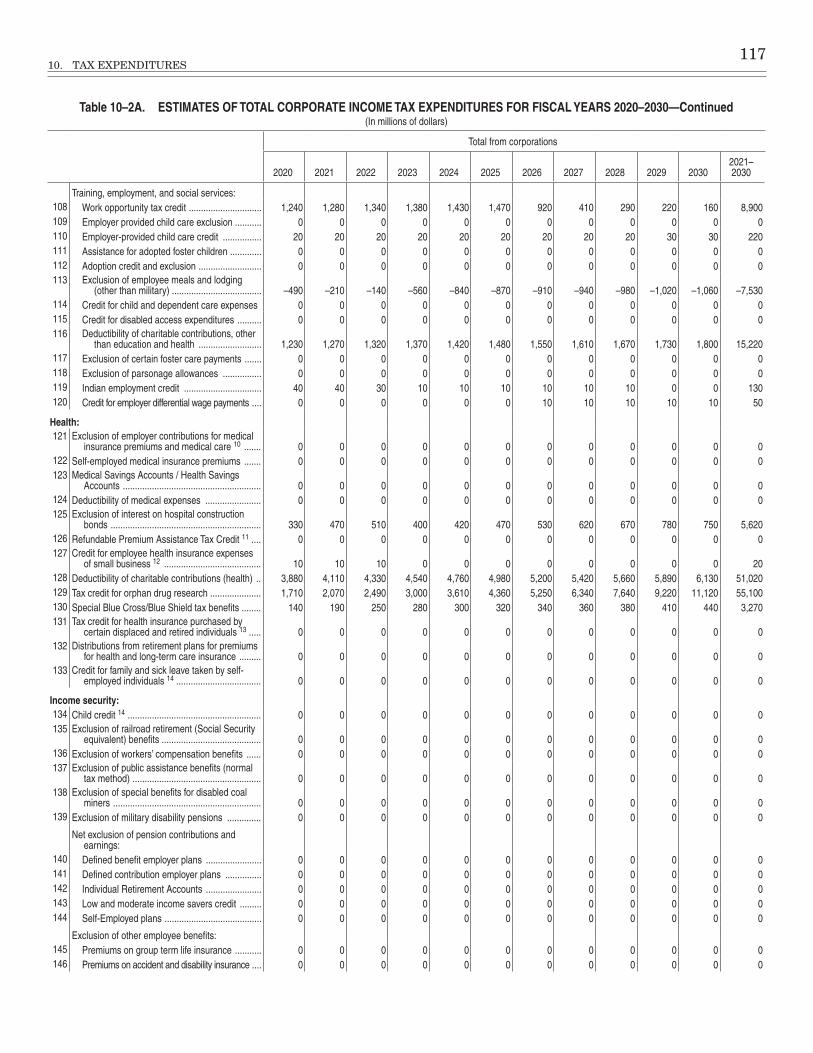

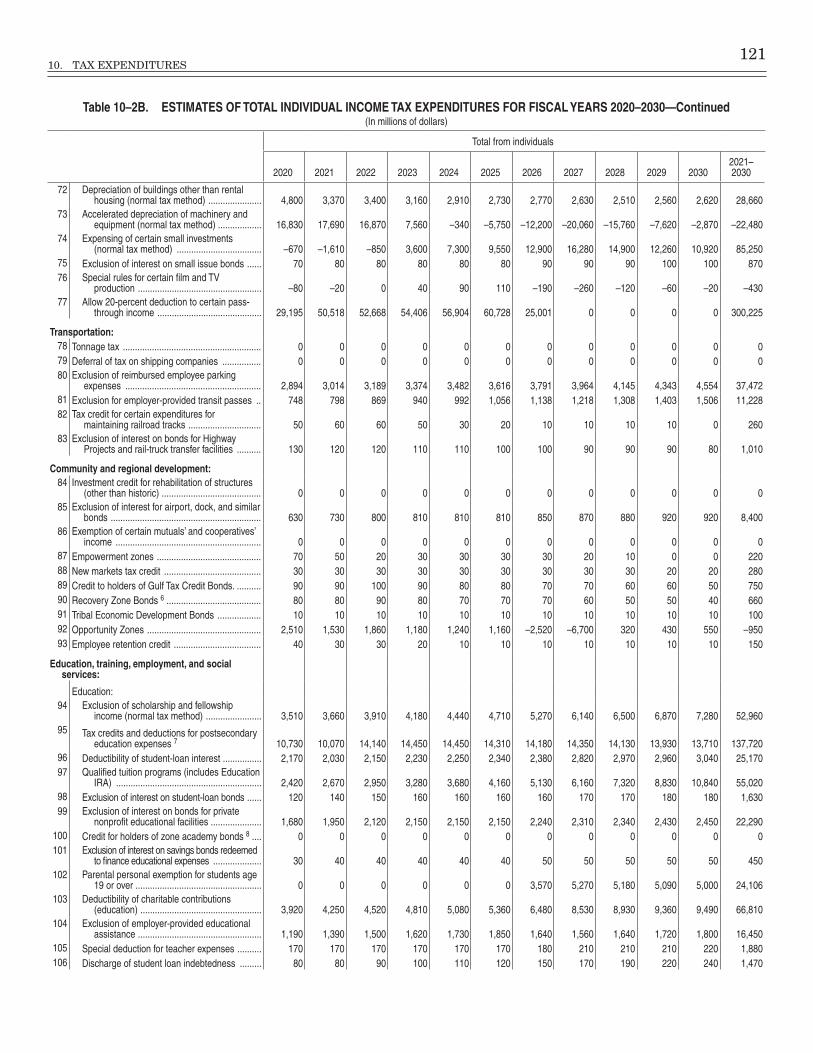

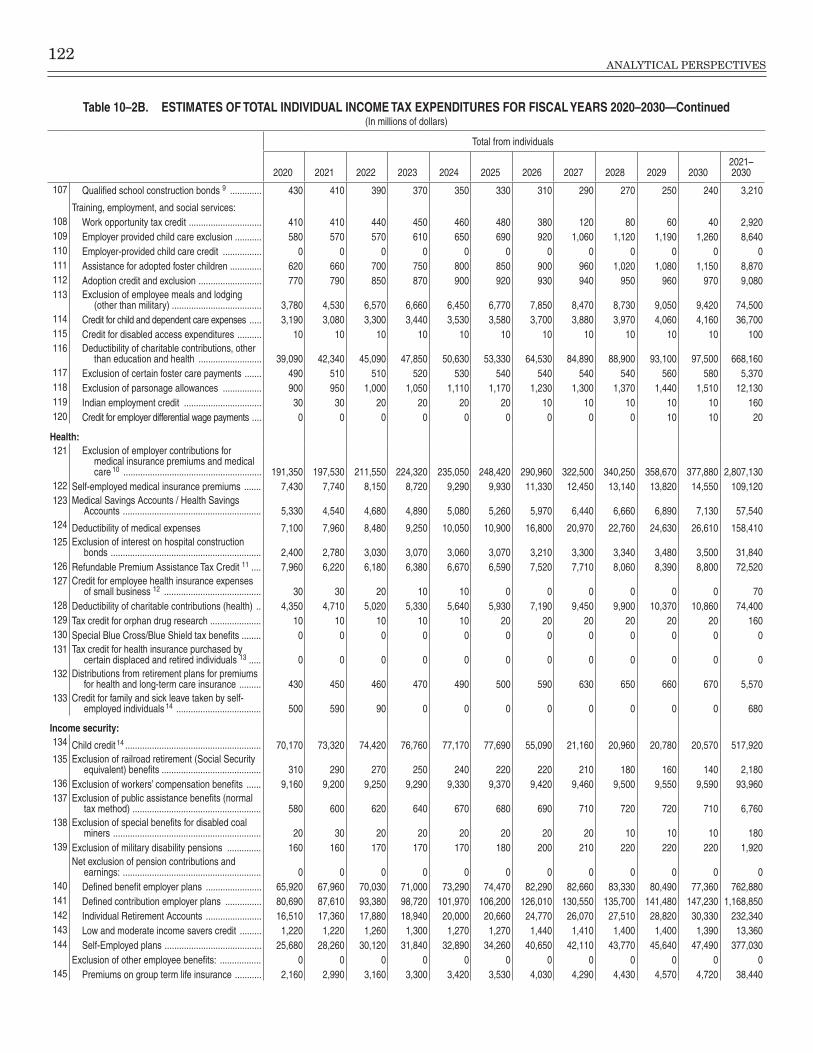

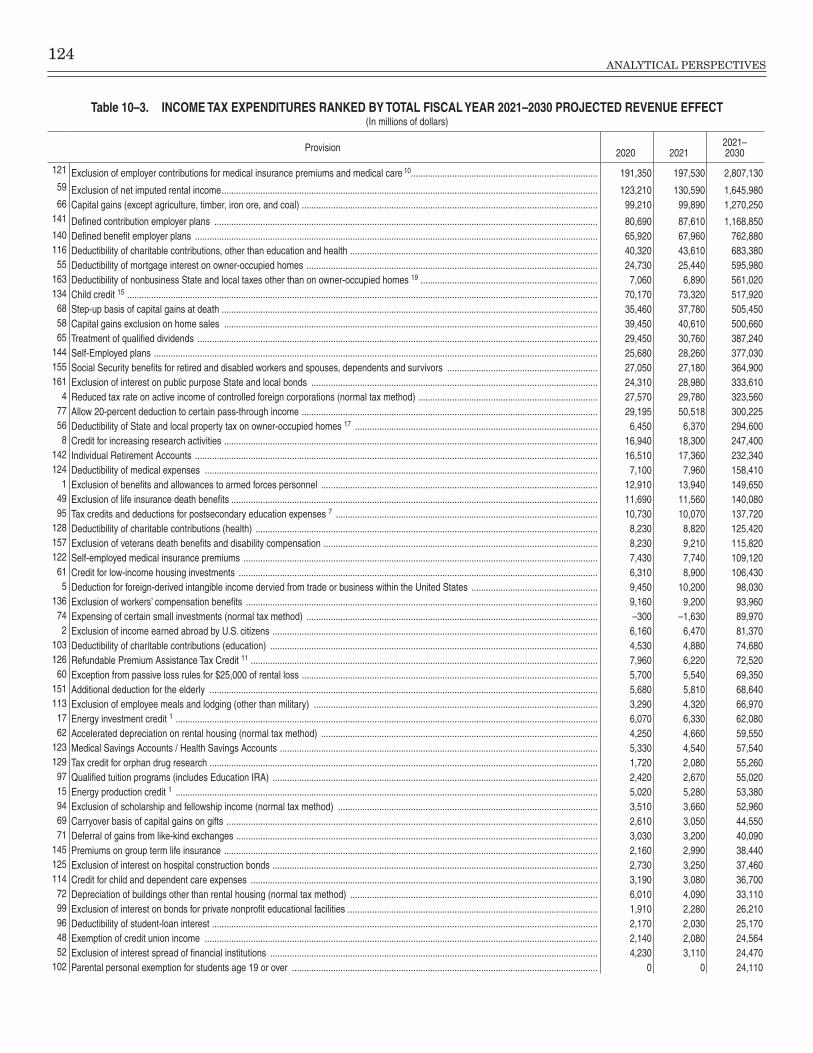

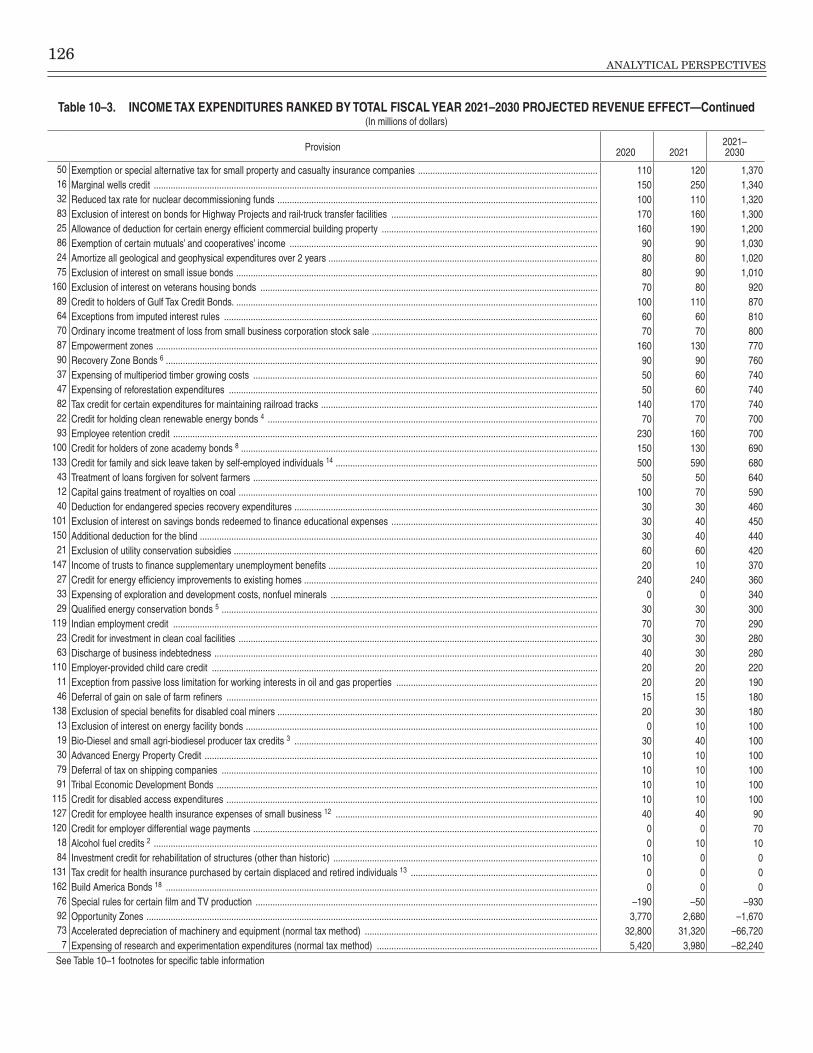

10. Tax Expenditures .....................................................................................................................105

Special Topics

11. Aid to State and Local Governments ......................................................................................149

12. Information Technology and Cybersecurity Funding .............................................................165

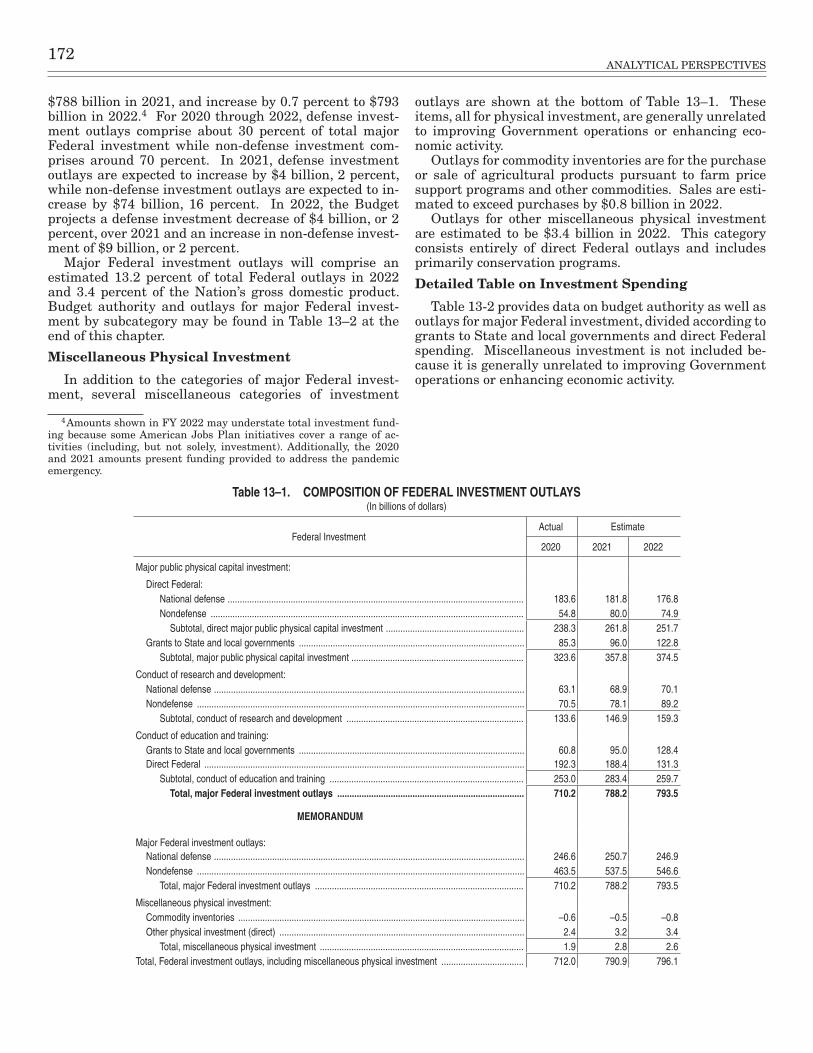

13. Federal Investment ..................................................................................................................171

14. Research and Development .....................................................................................................177

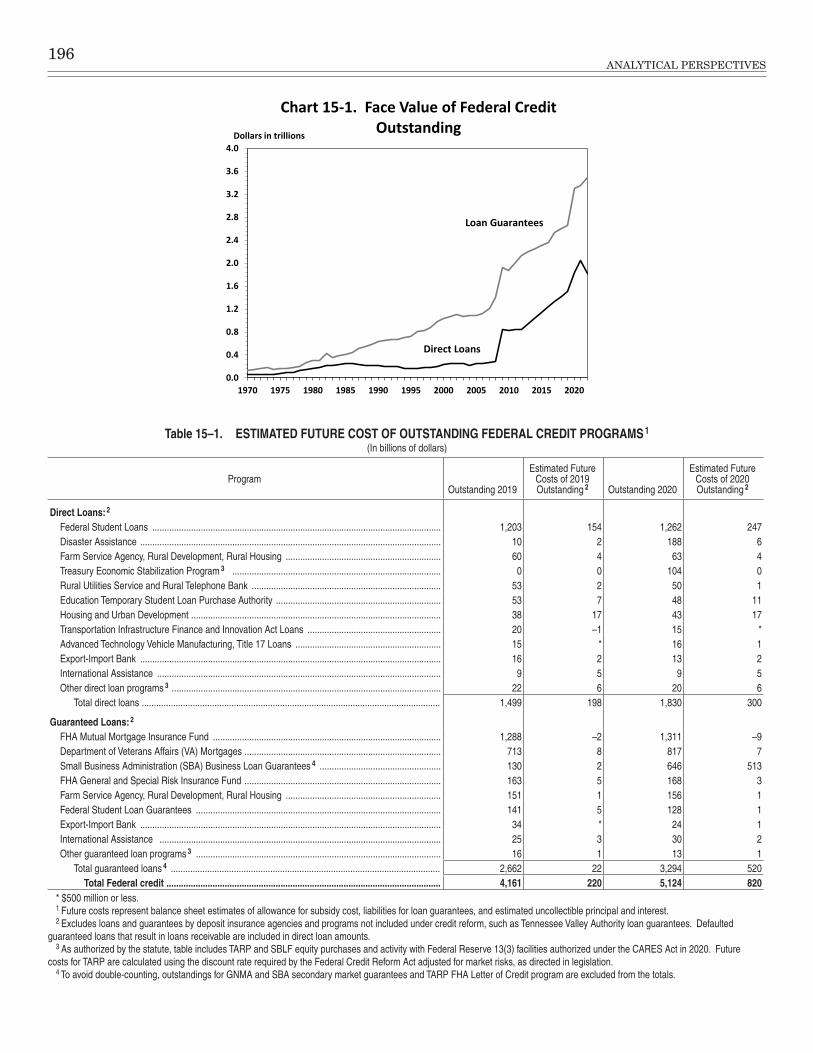

15. Credit and Insurance ...............................................................................................................181

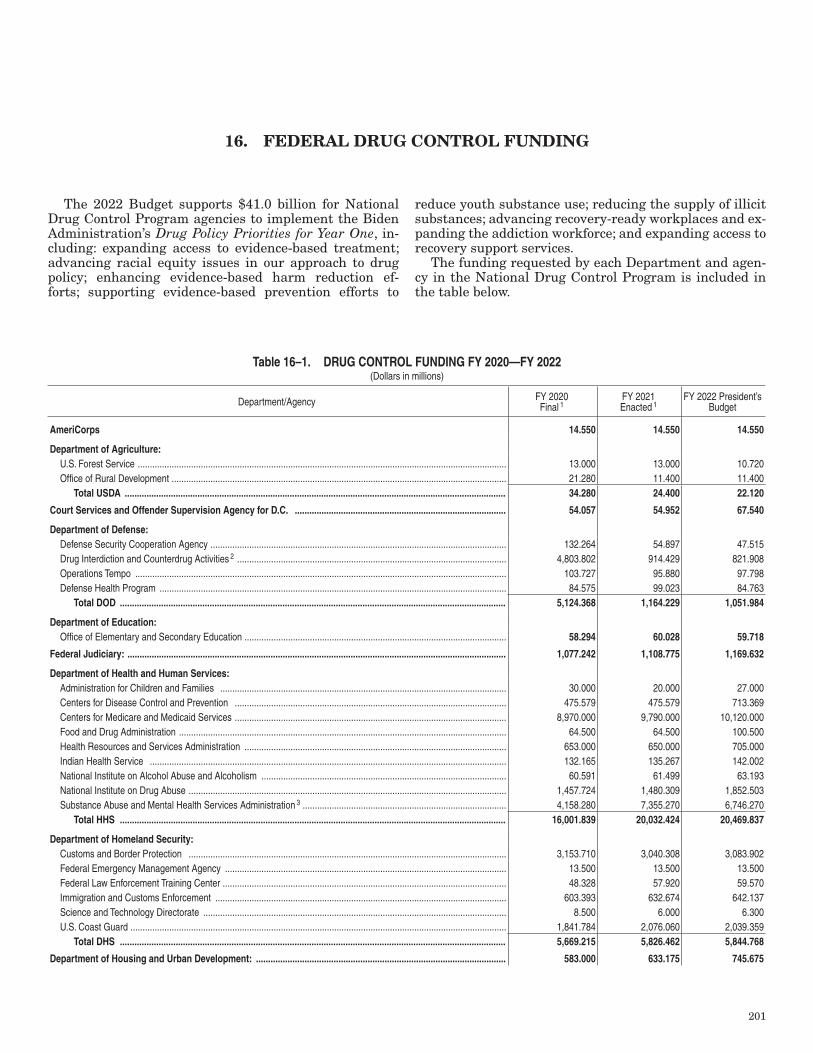

16. Federal Drug Control Funding ................................................................................................201

Technical Budget Analyses

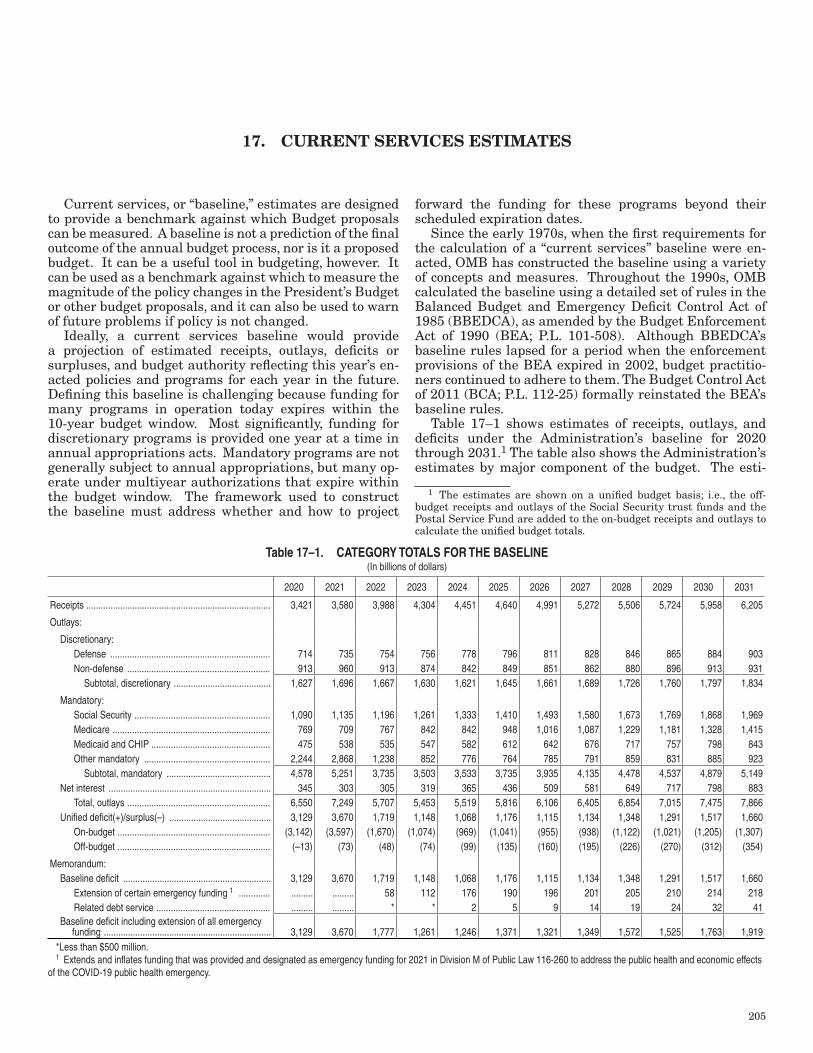

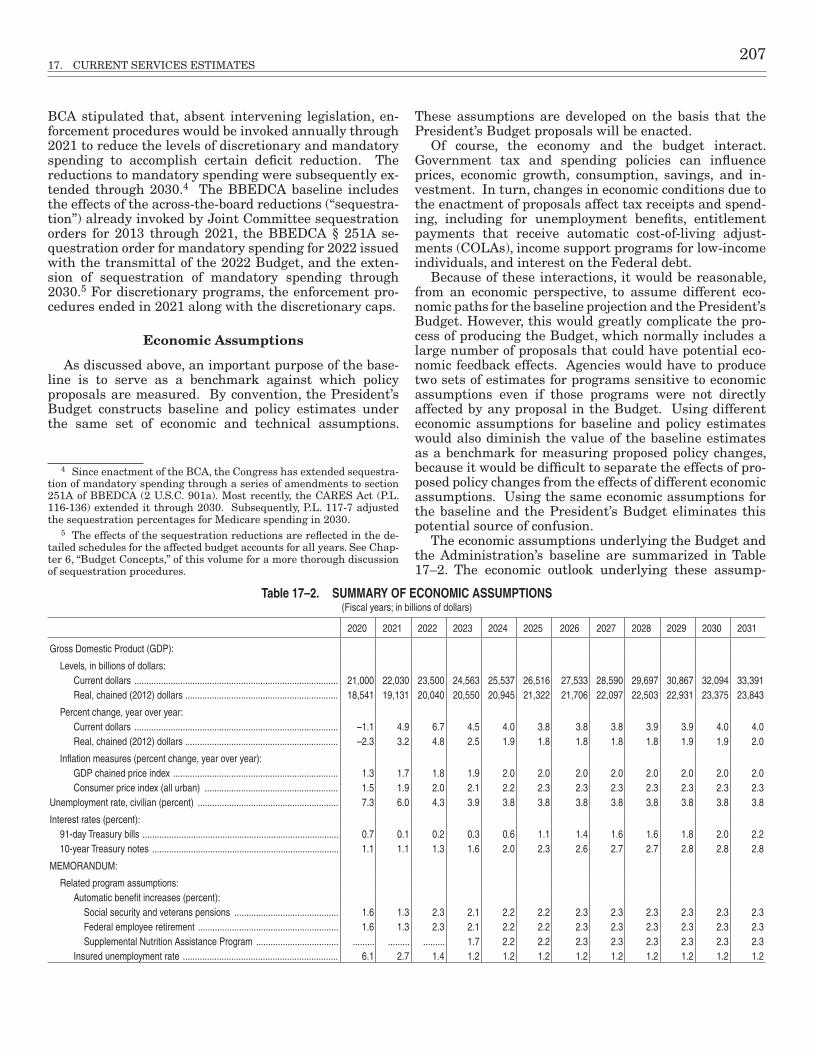

17. Current Services Estimates .....................................................................................................205

18. Trust Funds and Federal Funds ..............................................................................................215

19. Comparison of Actual to Estimated Totals .............................................................................229

v

LIST OF CHARTS AND TABLES

vii

LIST OF CHARTS AND TABLES

LIST OF CHARTS

2–1. Labor Underutilization: Alternative Measures ..........................................................................7

2–2. Contributions to Percent Change in 2020 Real GDP .................................................................8

2–3. Components of Real Personal Consumption Expenditures .......................................................8

2–4. Range of Uncertainty for the Budget Deficit ............................................................................15

3–1. Comparison of Annual Surplus/Deficit .....................................................................................18

3–2. Comparison of Publicly Held Debt ............................................................................................19

5–1. Masters Degree or Above by Year for Federal and Private Sectors .........................................48

5–2. High School Graduate or Less by Year for Federal and Private Sectors .................................48

5–3. Average Age by Year for Federal and Private Sectors ..............................................................48

5–4. Government-wide On-board U.S. Distribution 10-1-1978 ........................................................49

5–5. Government-wide On-board U.S. Distribution 1-1-2021 ..........................................................50

5–6. The Changing General Schedule Workforce .............................................................................50

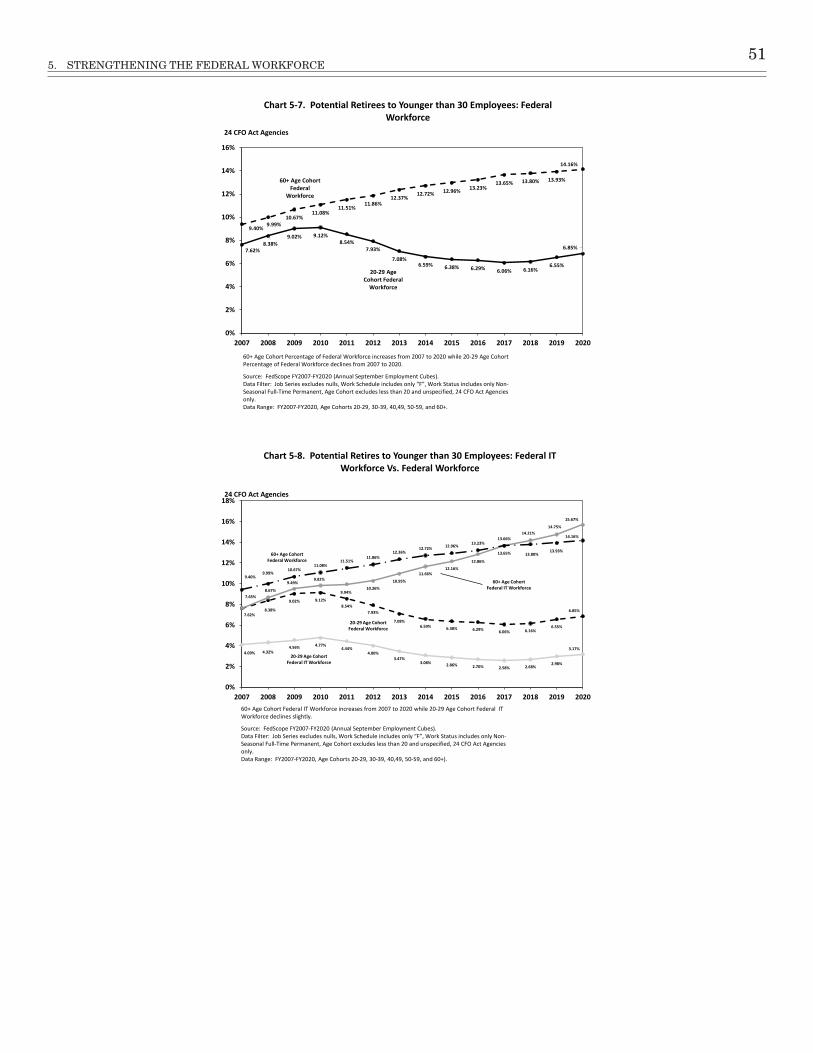

5–7. Potential Retirees to Younger than 30 Employee: Federal Workforce .....................................51

5–8. Potential Retires to Younger than 30 Employees: Federal IT Workforce Vs. Federal Workforce ..........................................................................51

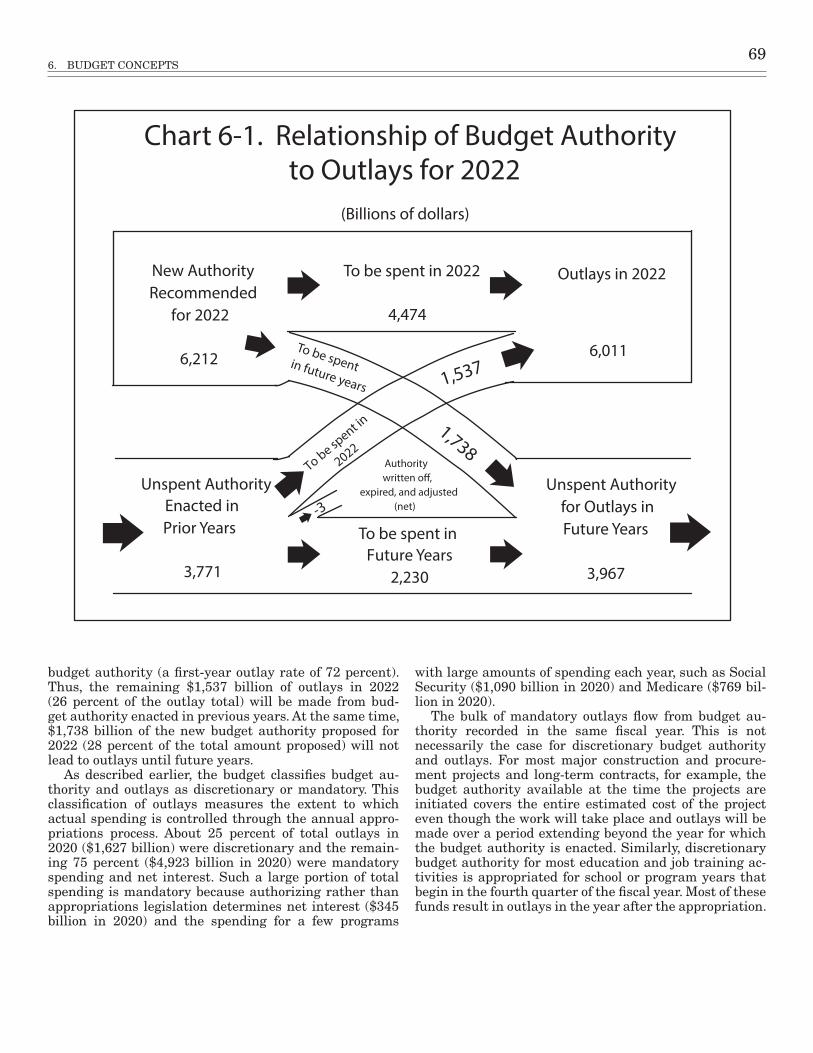

6–1. Relationship of Budget Authority to Outlays for 2022 .............................................................69

12–1. Trends in Federal Civilian IT Spending .................................................................................166

12–2. 2022 Federal Civilian IT Investment Portfolio .......................................................................166

15–1. Face Value of Federal Credit Outstanding ..............................................................................196

Page

ix

LIST OF TABLES

Economic and Budget Analyses

Economic Assumptions and Overview 2–1. Economic Assumptions ....................................................................................................... 9 2–2. Comparison of Economic Assumptions in the 2021 and 2022 Budgets .......................... 10 2–3. Comparison of Economic Assumptions ............................................................................. 11 2–4. Sensitivity of the Budget to Economic Assumptions ...................................................... 13 2–5. Forecast Errors, 2002-Present .......................................................................................... 14 2–6. Differences Between Estimated and Actual Surpluses or Deficits

for Five-Year Budget Estimates Since 1985 ................................................................ 15

Long-Term Budget Outlook 3–1. Intermediate Actuarial Projections for OASDI and HI, 2020 Trustees’ Reports ........... 19

Federal Borrowing and Debt 4–1. Trends in Federal Debt Held By the Public and Interest on the

Debt Held by the Public ................................................................................................. 24 4–2. Federal Government Financing and Debt ........................................................................ 26 4–3. Debt Held by the Public Net of Financial Assets and Liabilities .................................... 29 4–4. Agency Debt ....................................................................................................................... 31 4–5. Debt Held by Government Accounts ................................................................................. 33 4–6. Federal Funds Financing and Change in Debt Subject to Statutory Limit ................... 37 4–7. Foreign Holdings of Federal Debt ..................................................................................... 38

Management

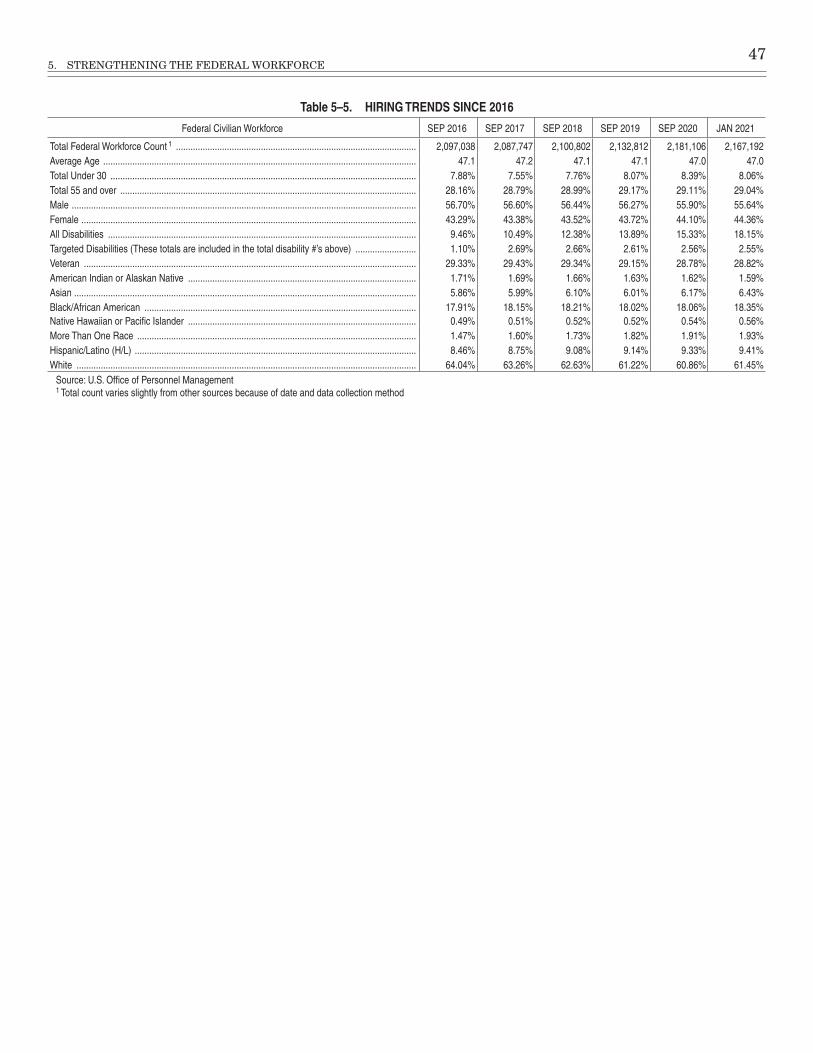

Strengthening the Federal Workforce 5–1. Federal Civilian Employment in the Executive Branch .................................................... 43 5–2. Total Federal Employment ................................................................................................ 44 5–3. Occupations of Federal and Private Sector Workforces ................................................... 45 5–4. Personnel Pay and Benefits ............................................................................................... 46 5–5. Hiring Trends Since 2016 .................................................................................................. 47

Budget Concepts and Budget Process

Budget ConceptsBudget Calendar ............................................................................................................................... 57 6–1. Totals for the Budget and the Federal Government ........................................................ 62

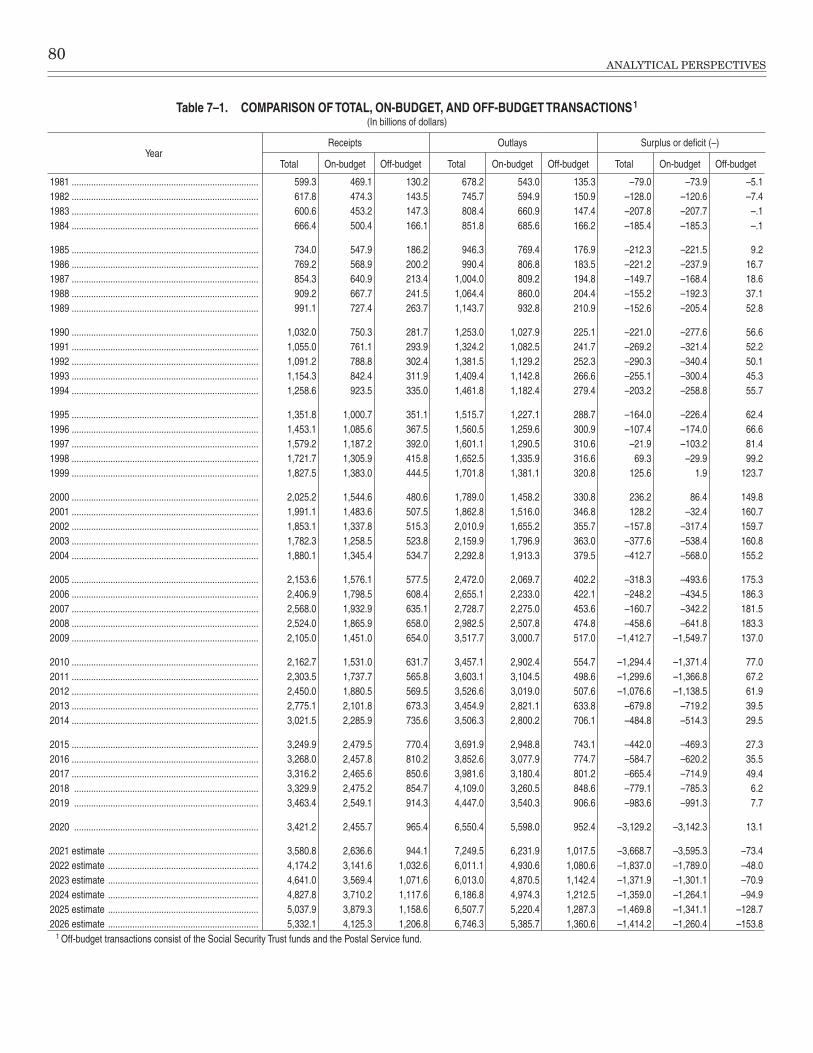

Coverage of the Budget 7–1. Comparison of Total, On-Budget, and Off-Budget Transactions ..................................... 80

Federal Receipts

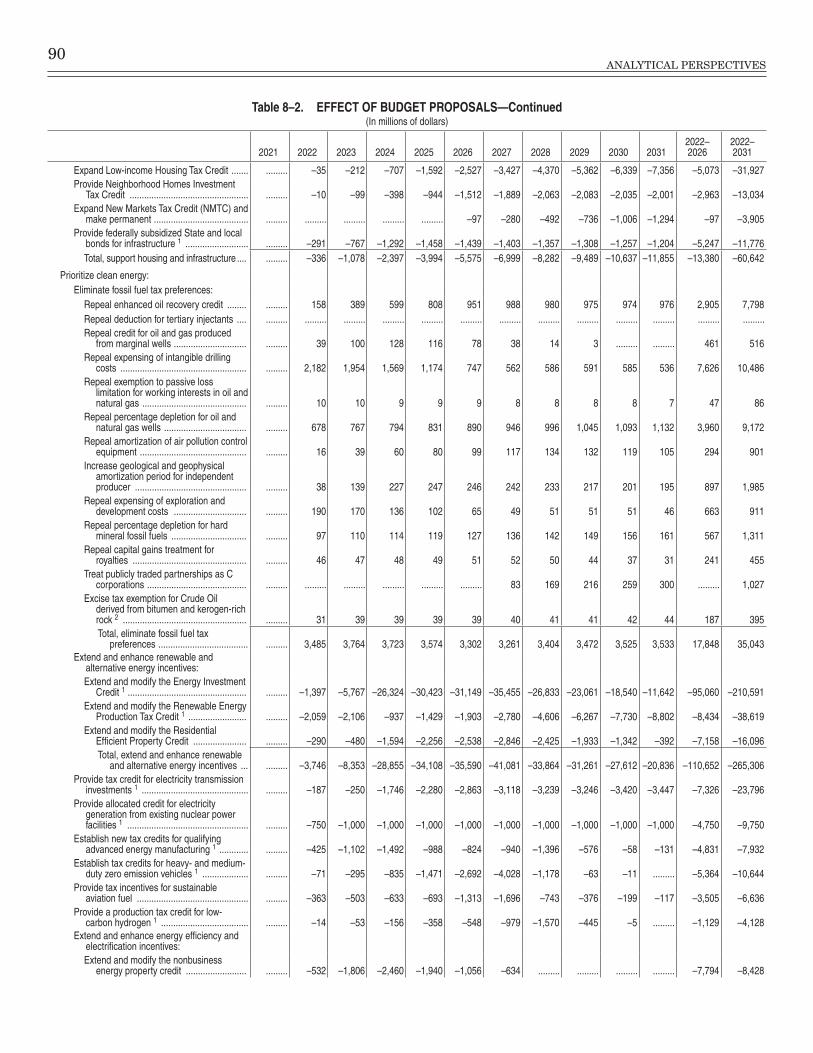

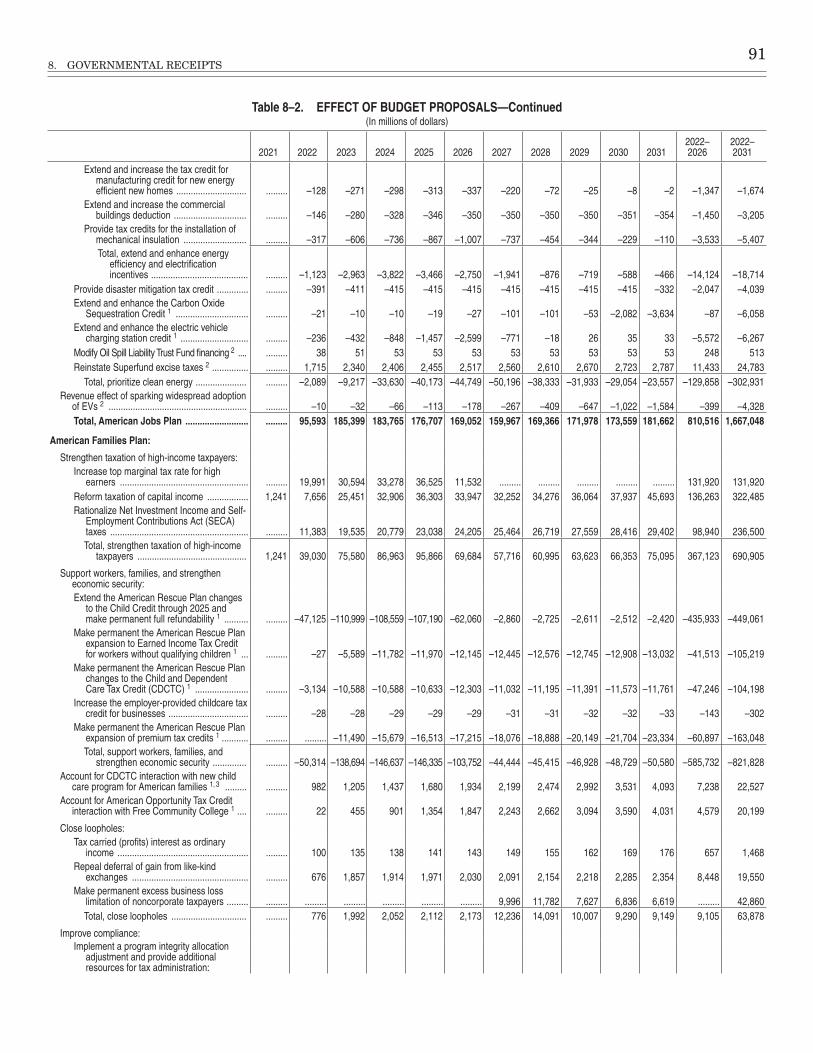

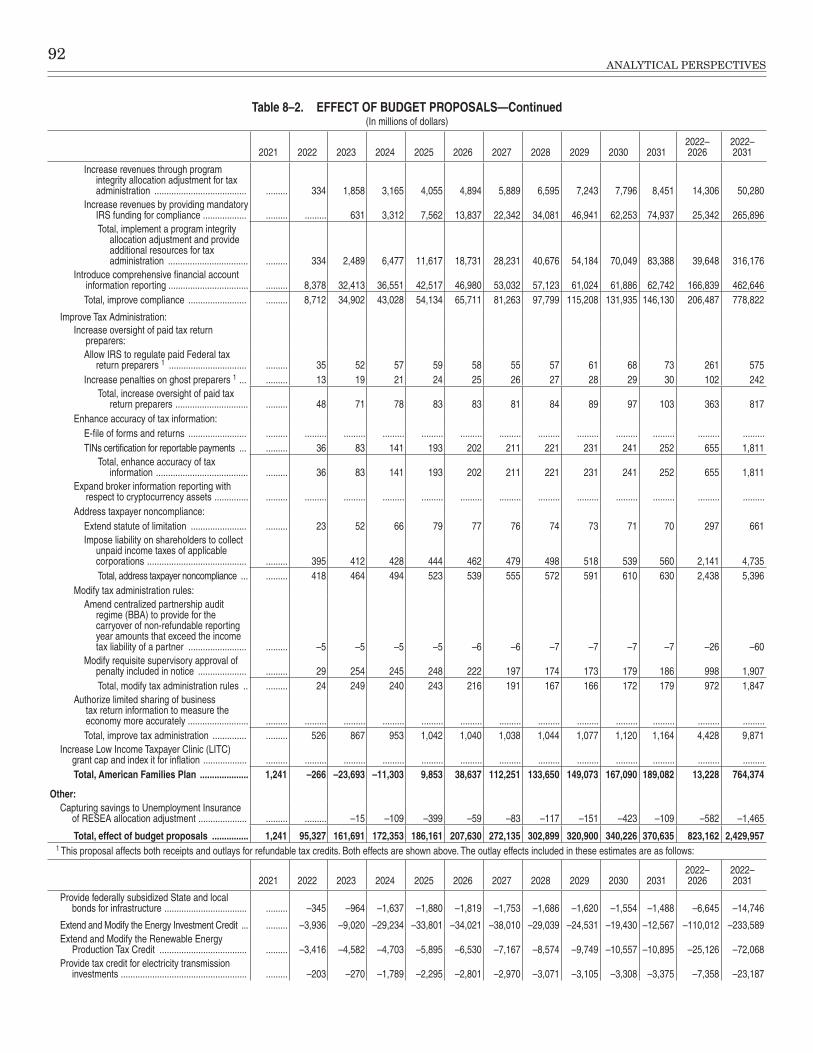

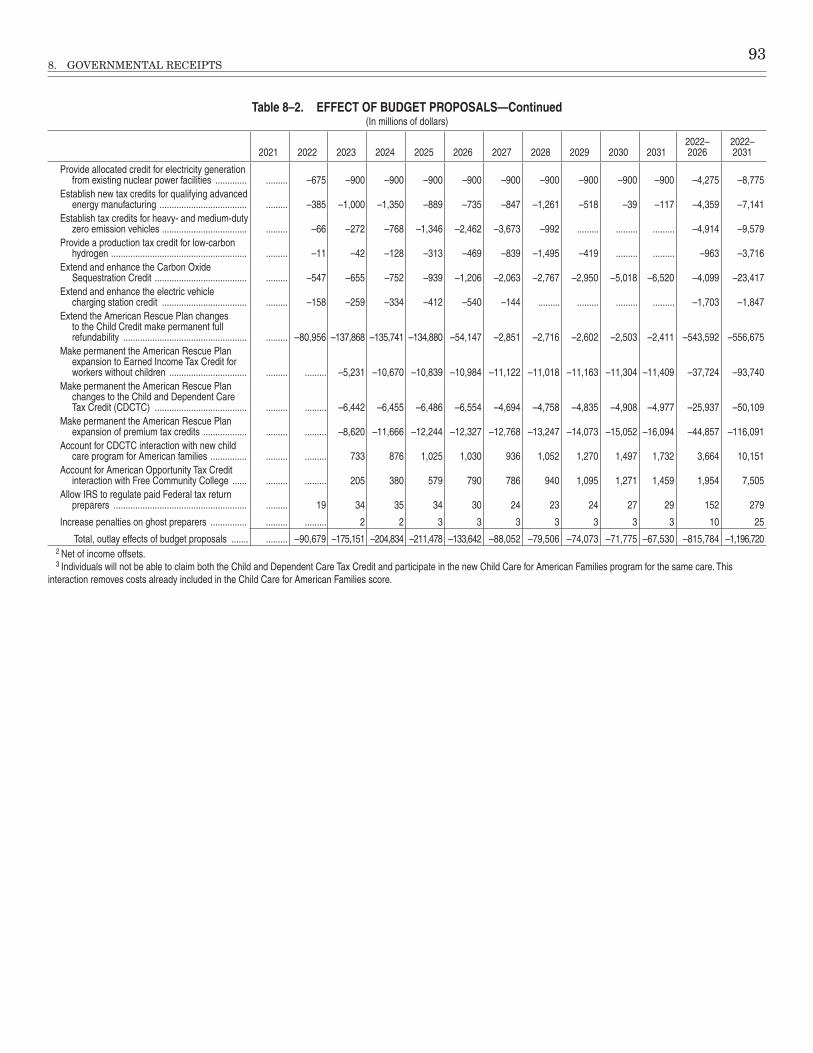

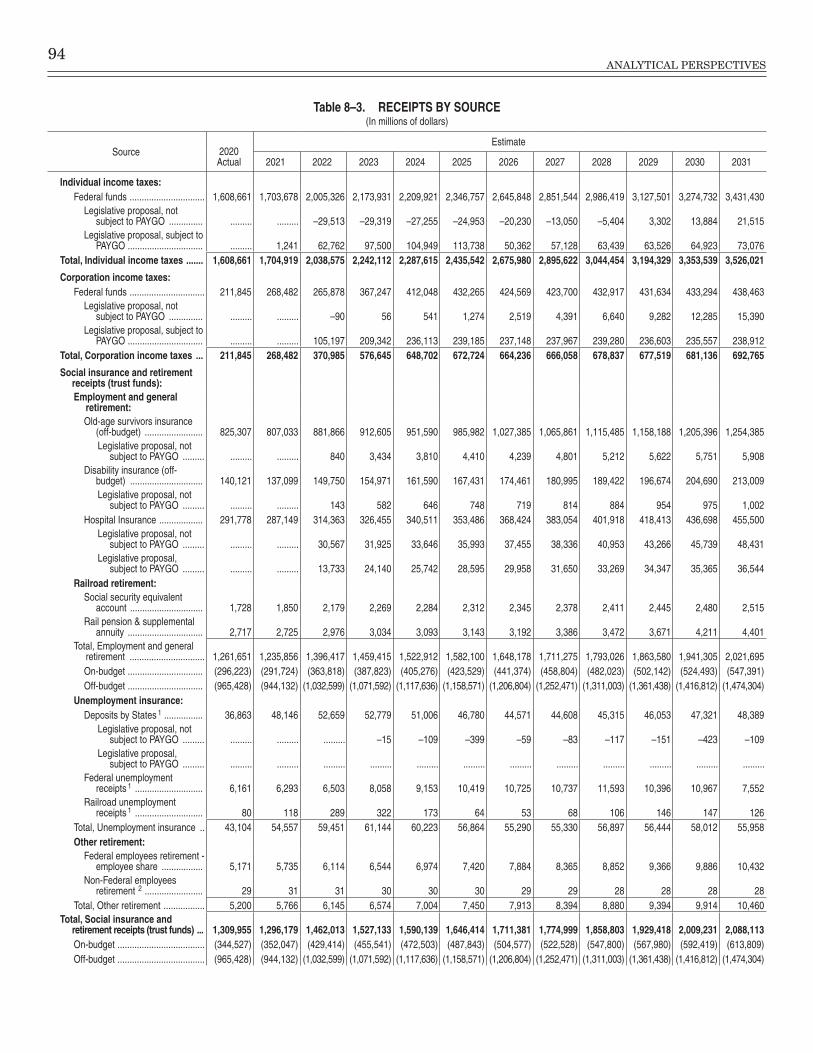

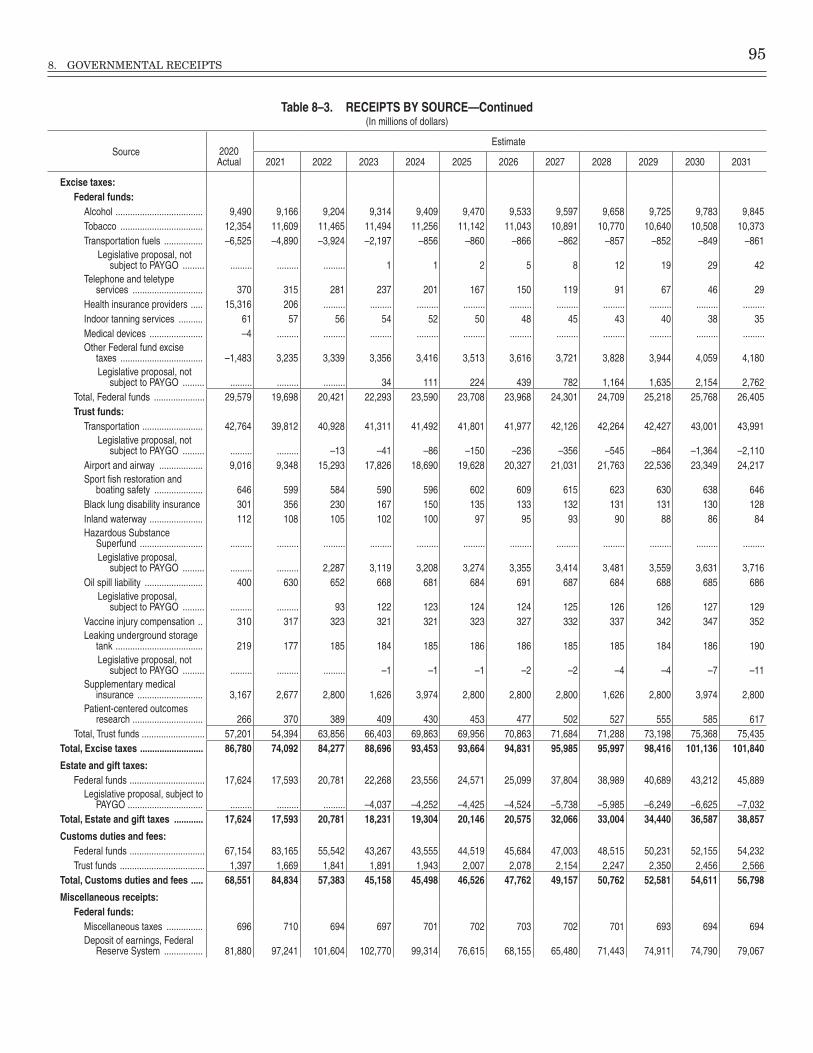

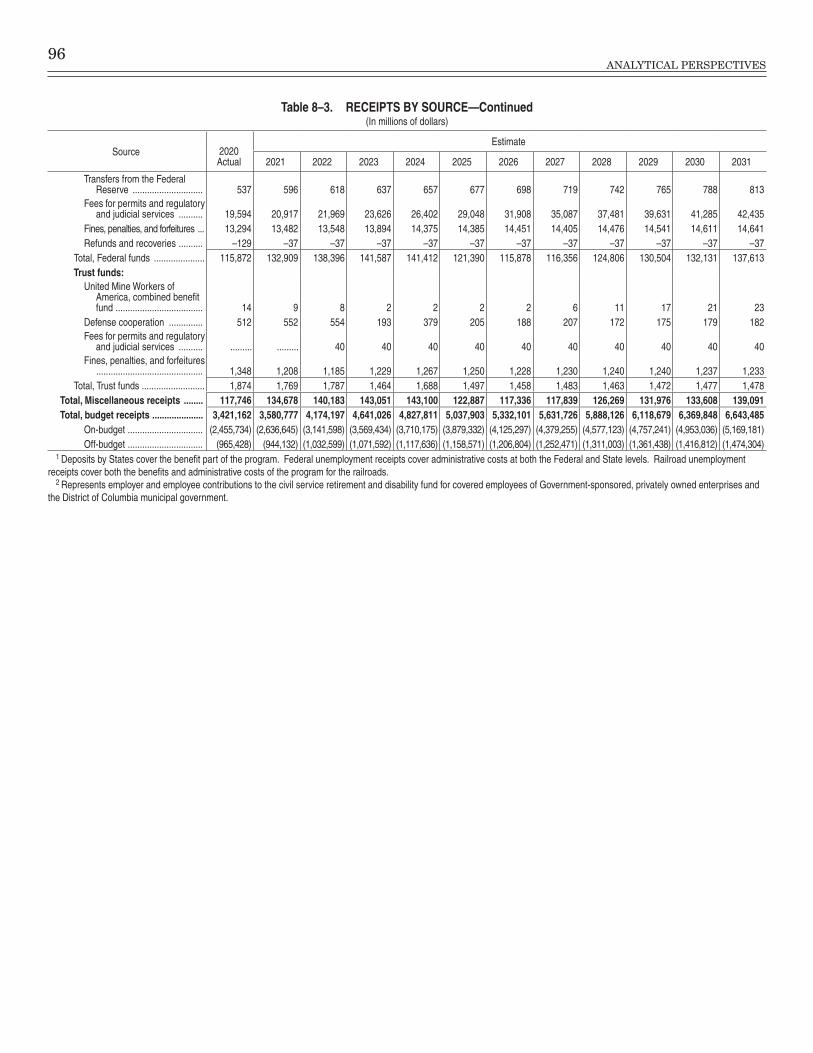

Governmental Receipts 8–1. Receipts by Source—Summary ......................................................................................... 87 8–2. Effect of Budget Proposals ................................................................................................ 89 8–3. Receipts by Source ............................................................................................................. 94

Offsetting Collections and Offsetting Receipts 9–1. Offsetting Collections and Offsetting Receipts from the Public ...................................... 99 9–2. Summary of Offsetting Receipts by Type ....................................................................... 100

Page

x

9–3. Gross Outlays, User Charges, Other Offsetting Collections and Offsetting Receipts from the Public, and Net Outlays ......................................................................................... 101

9–4. User Charge Proposals in the FY 2022 Budget ............................................................ 102 9–5. Offsetting Receipts by Type ................................................................................................. * 9–6. Offsetting Collections and Offsetting Receipts by Detail─2022 Budget ............................ *

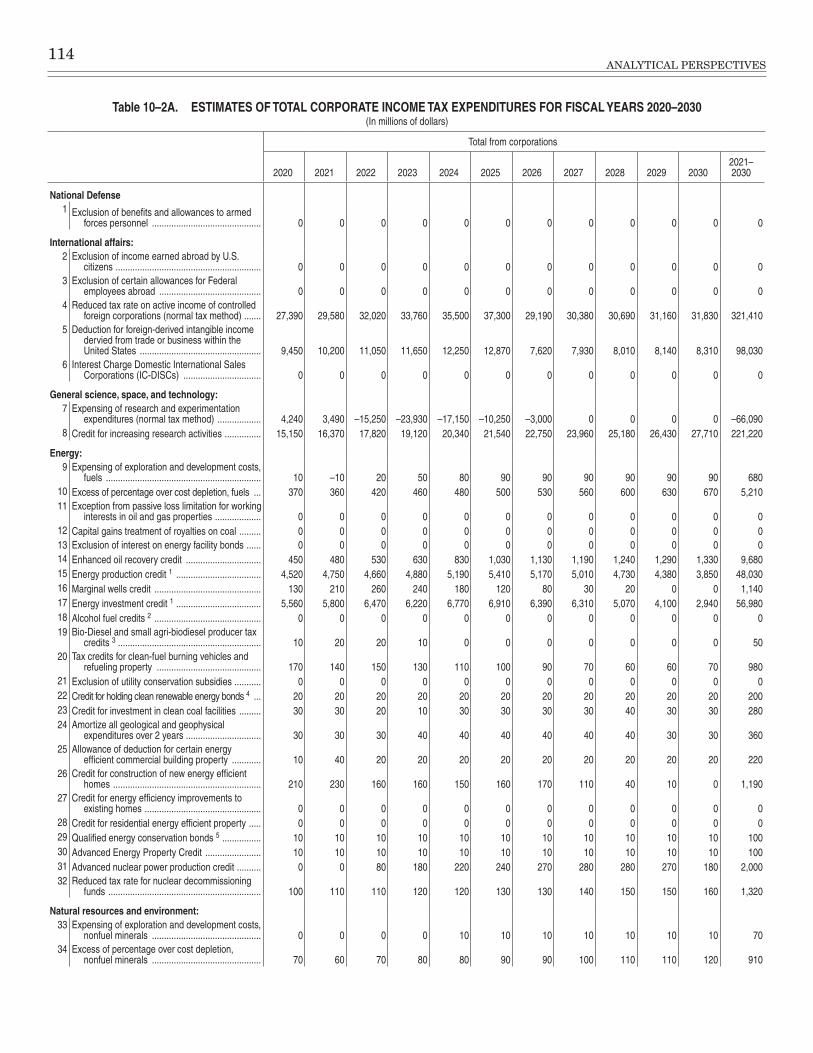

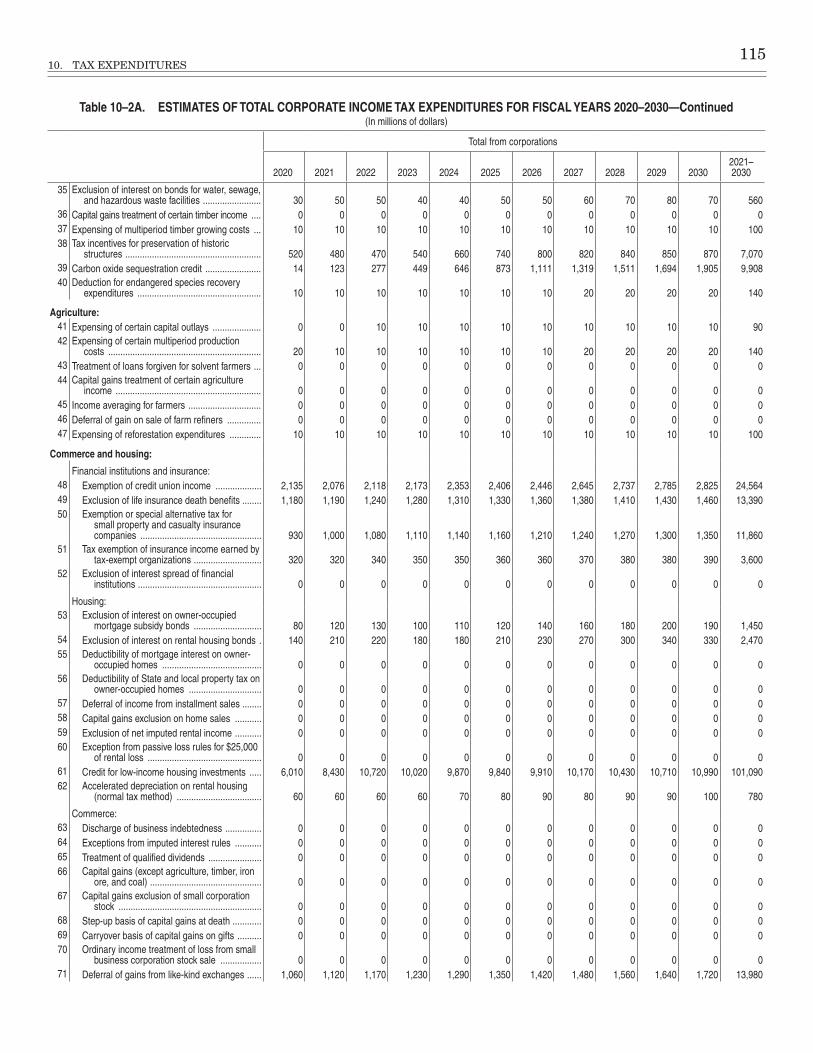

Tax Expenditures 10–1. Estimates of Total Income Tax Expenditures for Fiscal Years 2020–2030 ................... 108 10–2a. Estimates of Total Corporate Income Tax Expenditures for

Fiscal Years 2020–2030 ................................................................................................ 114 10–2b. Estimates of Total Individual Income Tax Expenditures for

Fiscal Years 2020–2030 ................................................................................................ 119 10–3. Income Tax Expenditures Ranked by Total Fiscal Year 2021–2030

Projected Revenue Effect ............................................................................................. 124 10–4. Present Value of Selected Tax Expenditures for Activity in Calendar Year 2020 ........ 127

Special Topics

Aid to State and Local Governments 11–1. Trends in Federal Grants to State and Local Governments ......................................... 152 11–2. Federal Grants to State and Local Governments—Budget Authority and Outlays .... 153 11–3. Summary of Programs by Agency, Bureau, and Program .................................................. * 11–4. Summary of Programs by State ........................................................................................... * 11–5.–11–49. 2022 Budget Program State-by-State Tables ......................................................... *

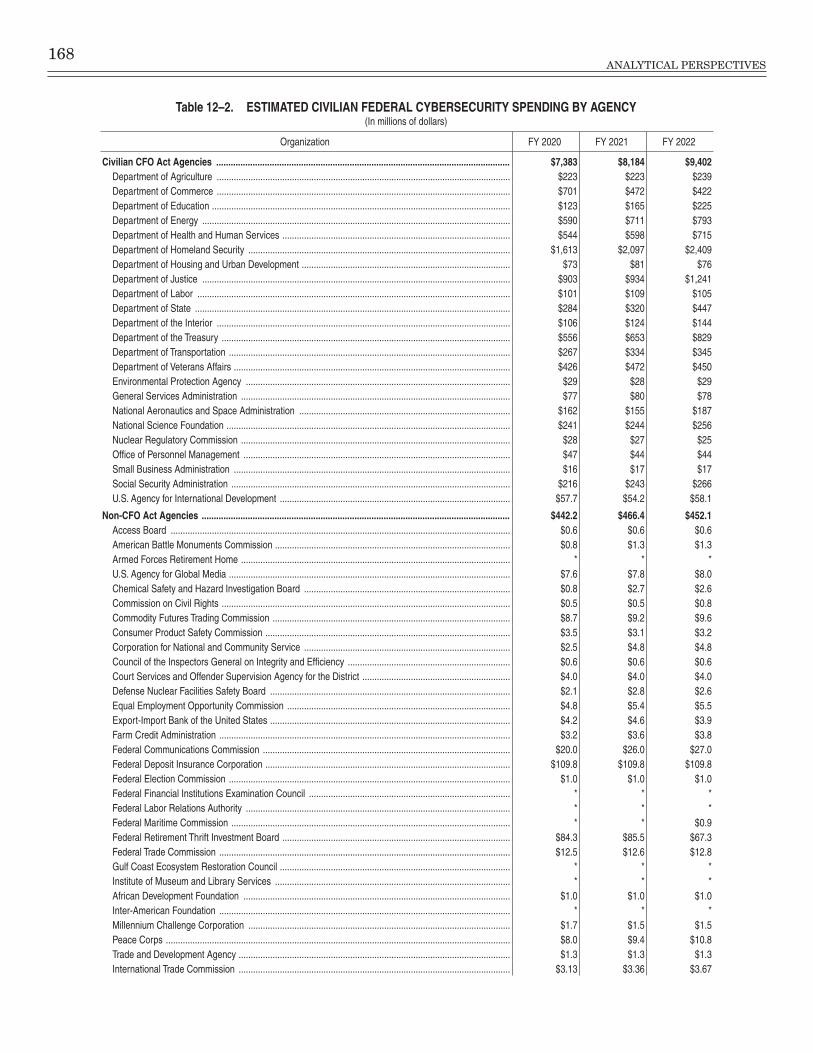

Information Technology and Cybersecurity Funding 12–1. Estimated FY 2022 Civilian Federal IT Spending and Percentage by Agency ............ 167 12–2. Estimated Civilian Federal Cybersecurity Spending by Agency .................................. 168 12–3. NIST Framework Function Civilian CFO Act Agency Funding Totals ........................ 169

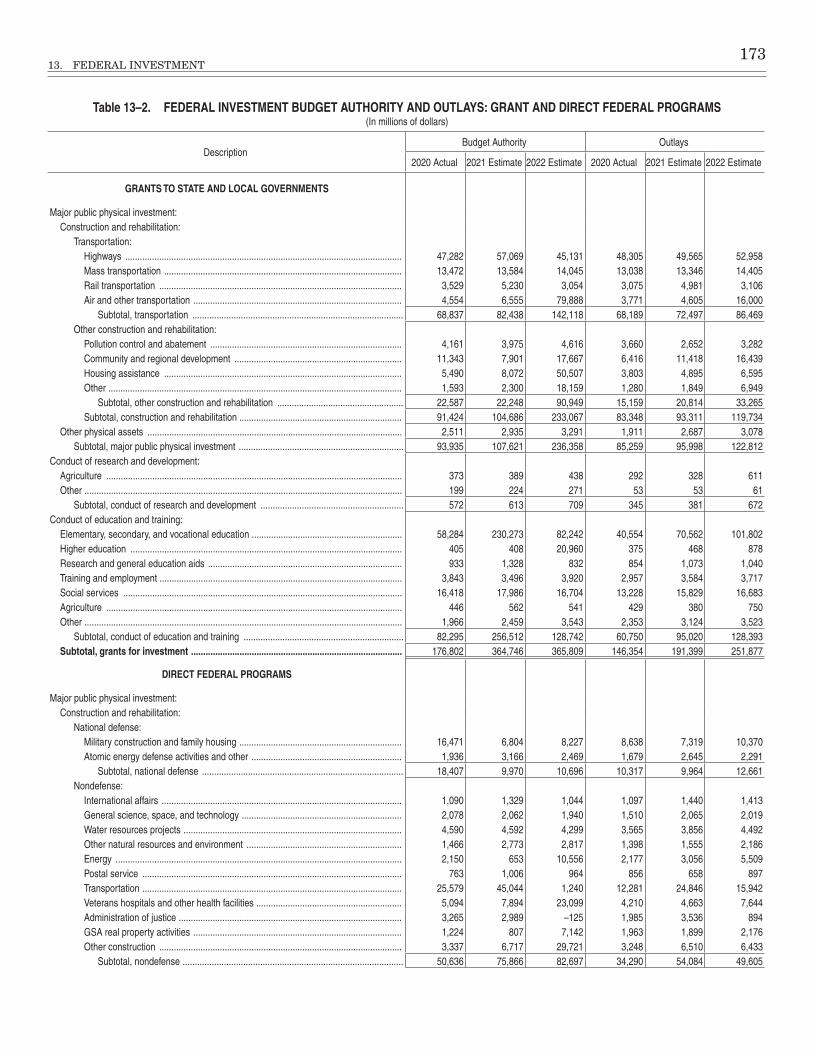

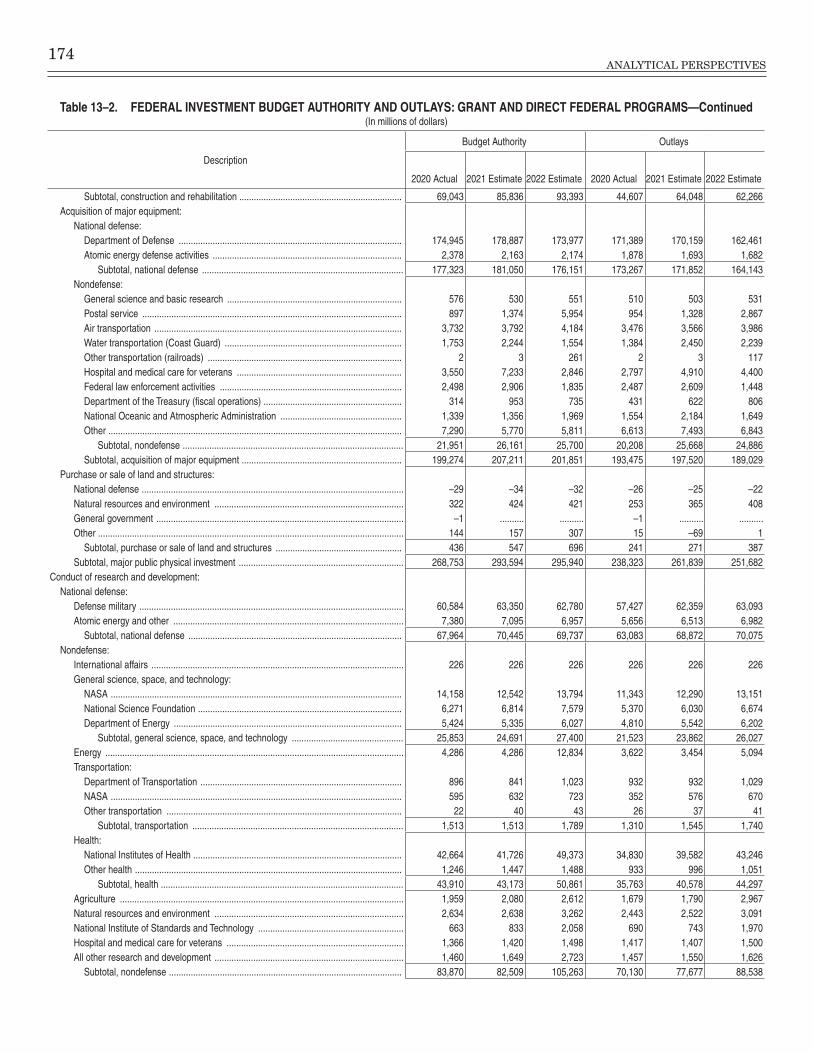

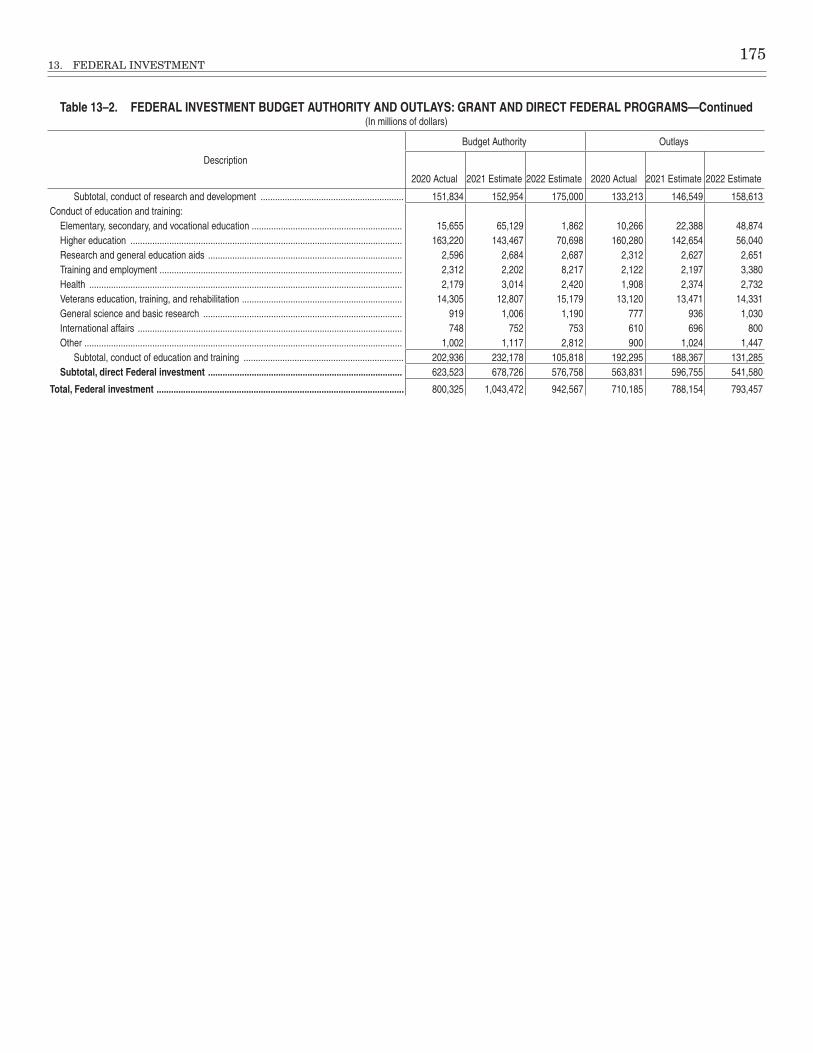

Federal Investment 13–1. Composition of Federal Investment Outlays .................................................................. 172 13–2. Federal Investment Budget Authority and Outlays: Grant

and Direct Federal Programs ...................................................................................... 173

Research and Development 14–1. Federal Research and Development Spending .............................................................. 178

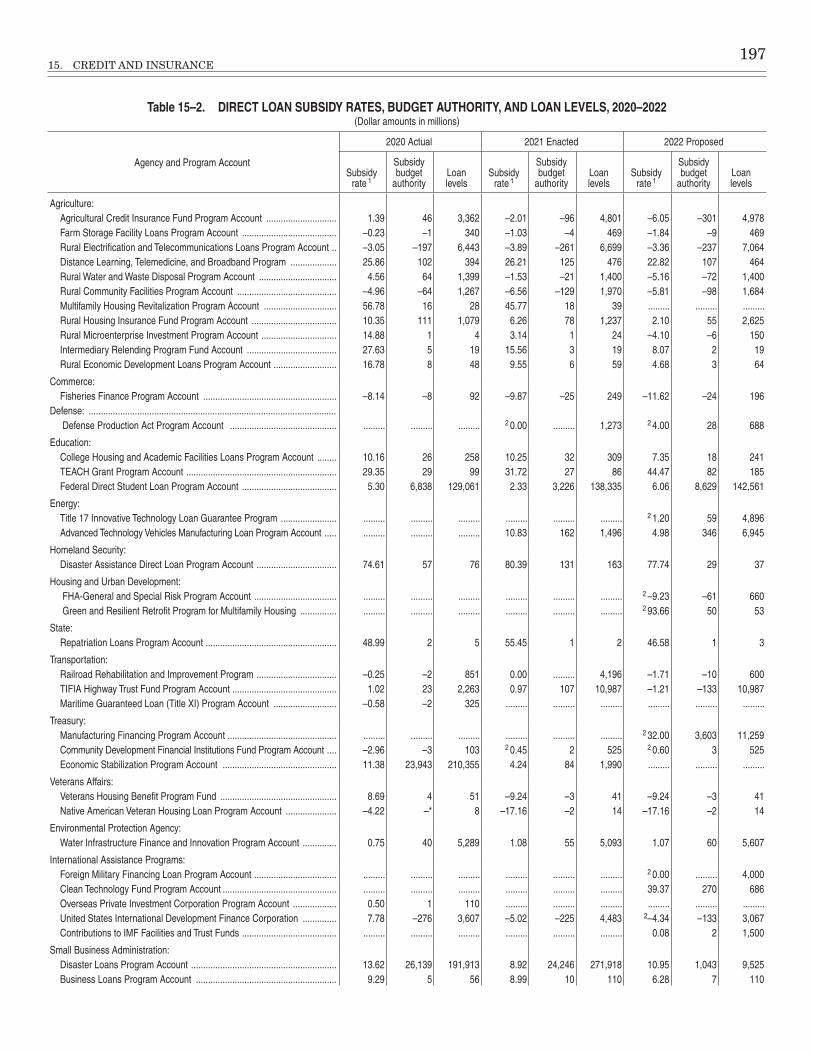

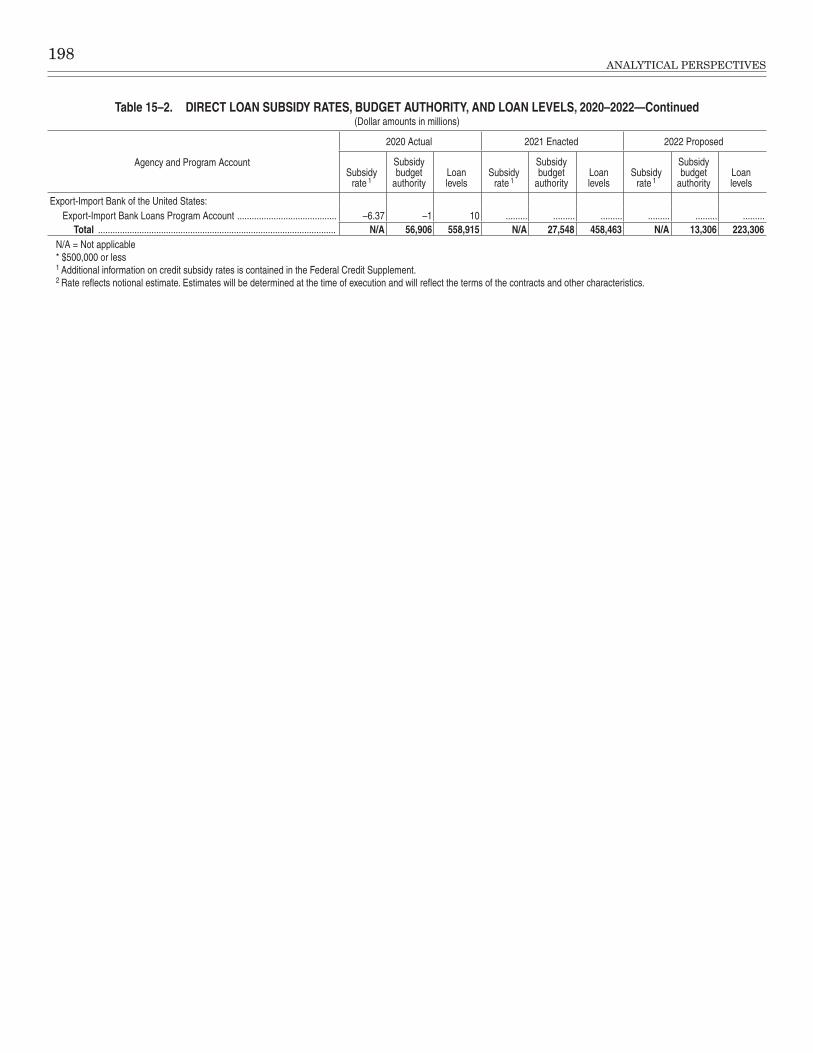

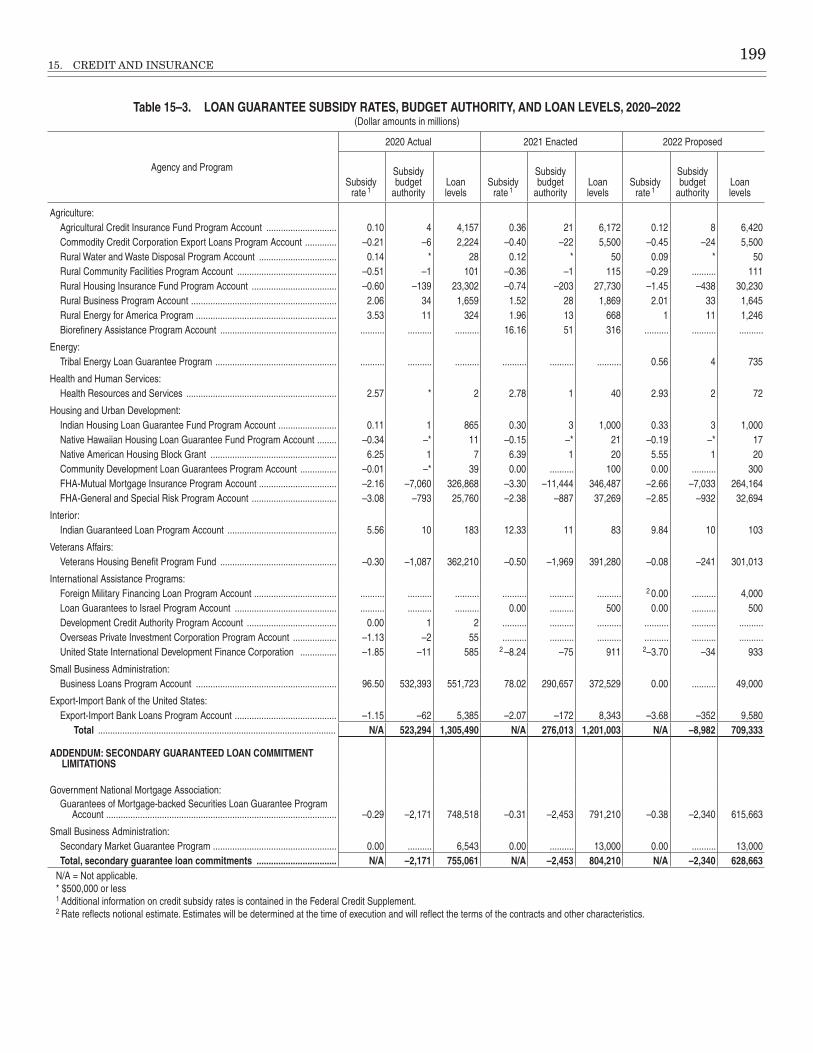

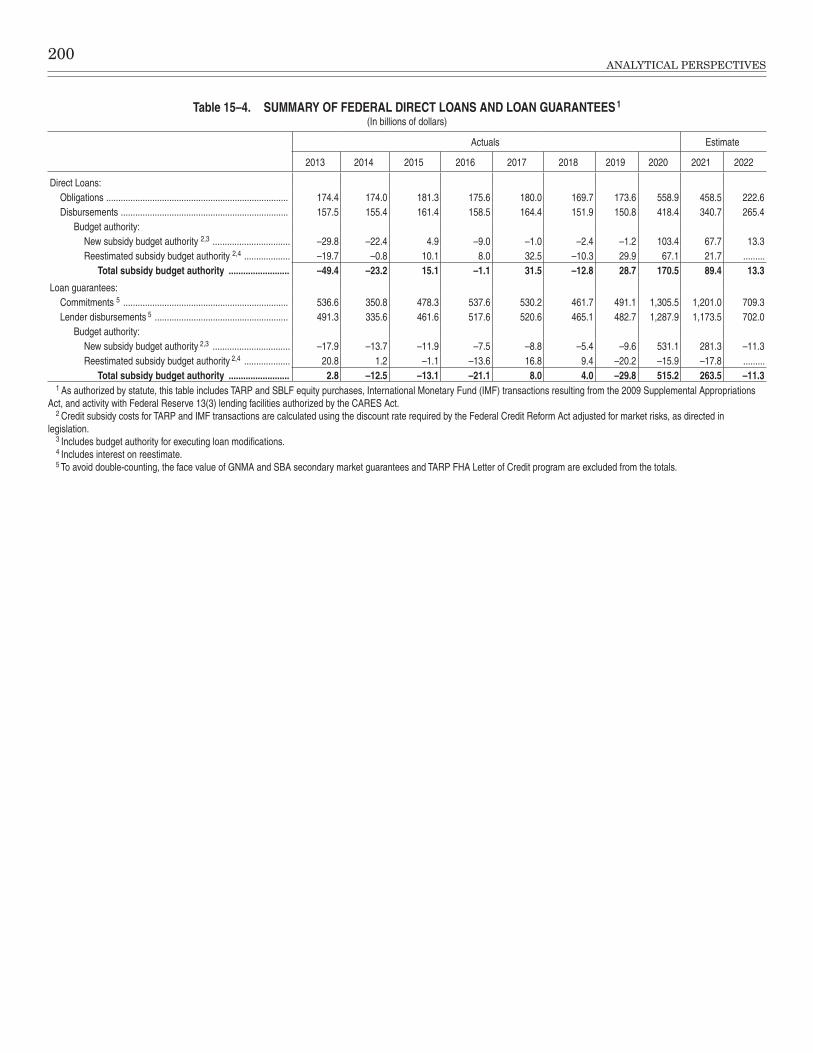

Credit and Insurance 15–1. Estimated Future Cost of Outstanding Federal Credit Programs ................................ 196 15–2. Direct Loan Subsidy Rates, Budget Authority, and Loan Levels, 2020–2022 .............. 197 15–3. Loan Guarantee Subsidy Rates, Budget Authority, and Loan Levels, 2020–2022 ....... 199 15–4. Summary of Federal Direct Loans and Loan Guarantees ............................................. 200 15–5. Reestimates of Credit Subsidies on Loans Disbursed Between 1992-2020 ....................... * 15–6. Face Value of Government-Sponsored Lending .................................................................. * 15–7. Lending and Borrowing by Government-Sponsored Enterprises (GSEs) ......................... * 15–8. Direct Loan Transactions of the Federal Government ....................................................... * 15–9. Guaranteed Loan Transactions of the Federal Government .............................................. * 15–10. Change in Programmatic Costs of Troubled Asset Relief Program ................................... * 15–11. Troubled Asset Relief Program Current Value ................................................................... *

Page

*Available on the internet at http://www.whitehouse.gov/omb/analytical-perspectives/

xi

15–12. Troubled Asset Relief Program Effects on the Deficit and Debt ........................................ * 15–13. Troubled Asset Relief Program Effects on the Deficit and

Debt Calculated on a Cash Basis ..................................................................................... * 15–14. Troubled Asset Relief Program Reestimates ....................................................................... * 15–15. Detailed TARP Program Levels and Costs .......................................................................... * 15–16. Comparison of CBO and OMB TARP Costs ........................................................................ *

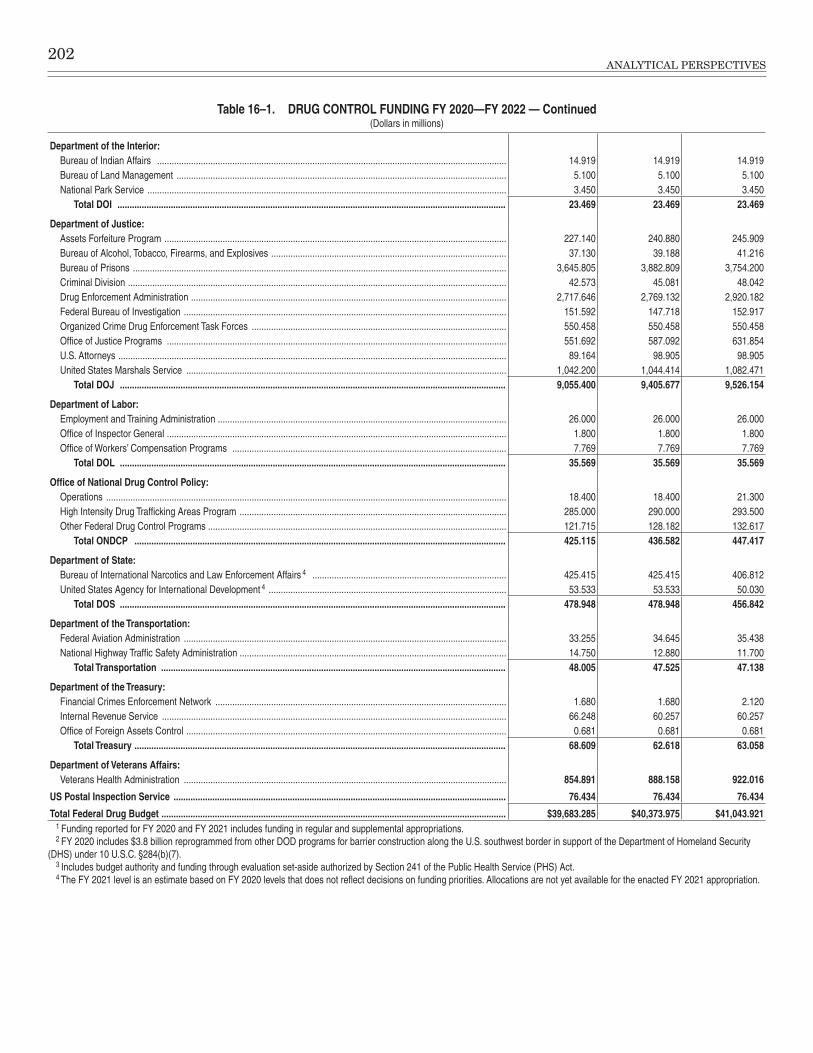

Federal Drug Control Funding 16–1. Drug Control Funding FY 2020—FY 2022 .................................................................... 201

Technical Budget Analyses

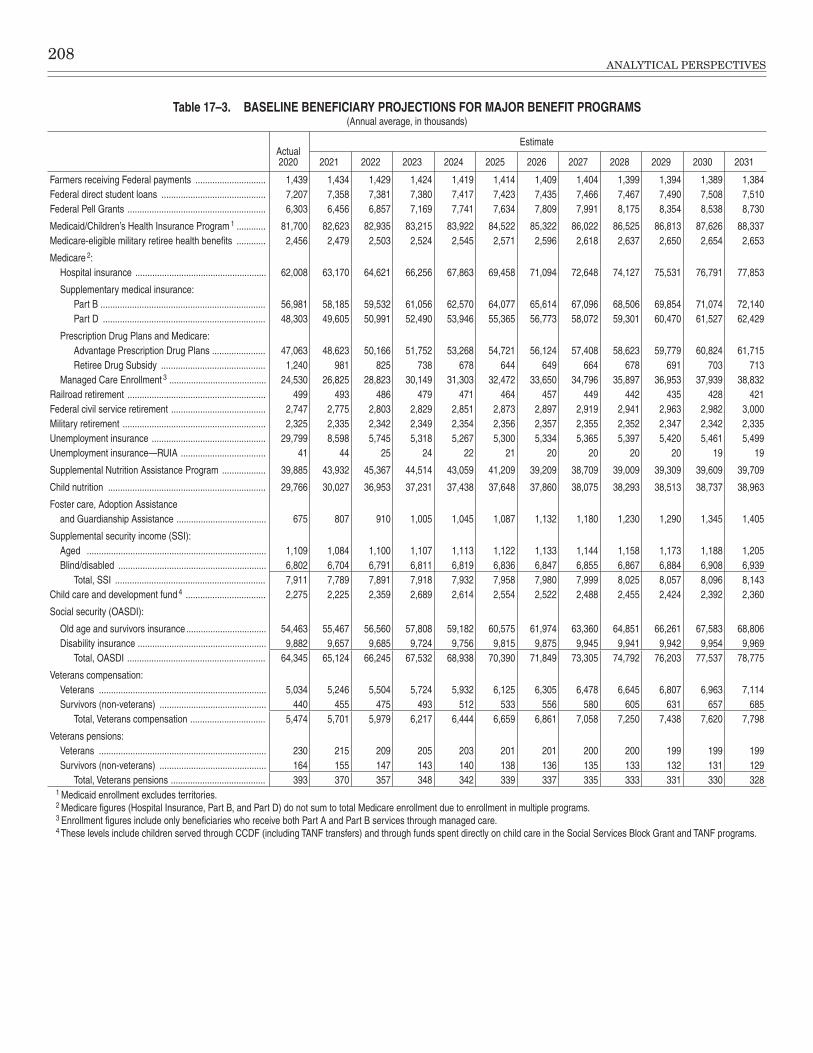

Current Services Estimates 17–1. Category Totals for the Baseline ..................................................................................... 205 17–2. Summary Of Economic Assumptions ............................................................................. 207 17–3. Baseline Beneficiary Projections for Major Benefit Programs ...................................... 208 17–4. Impact of Regulations, Expiring Authorizations, and

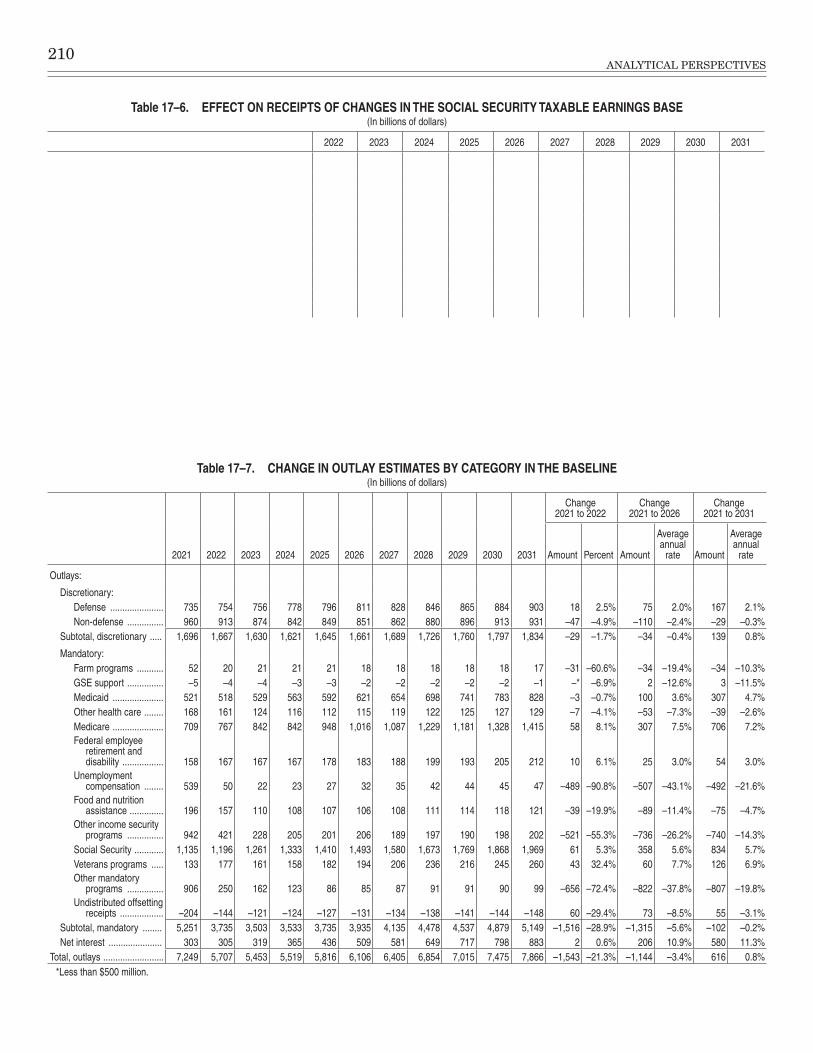

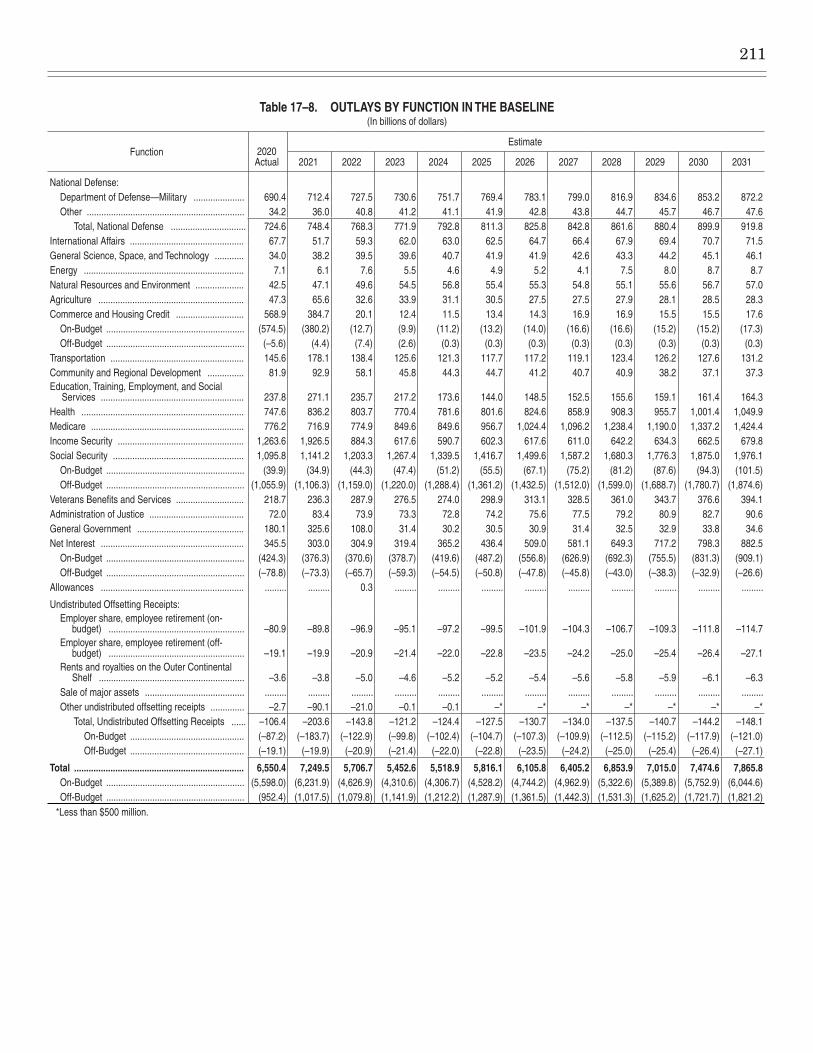

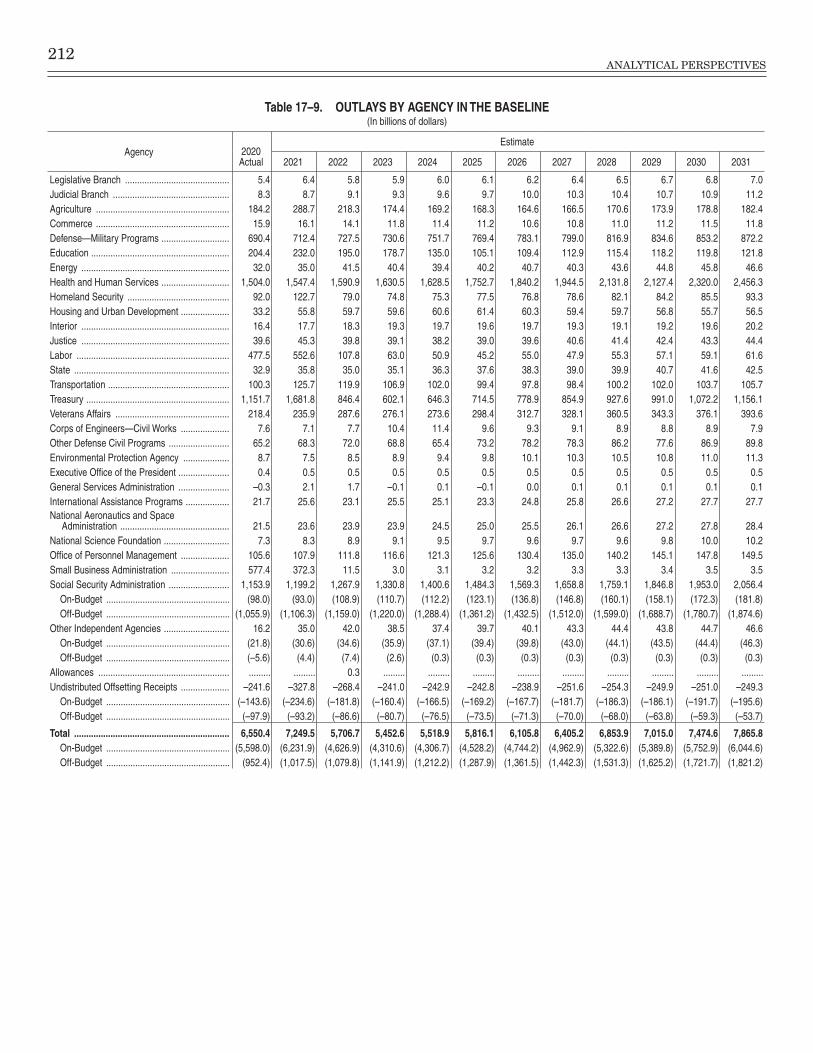

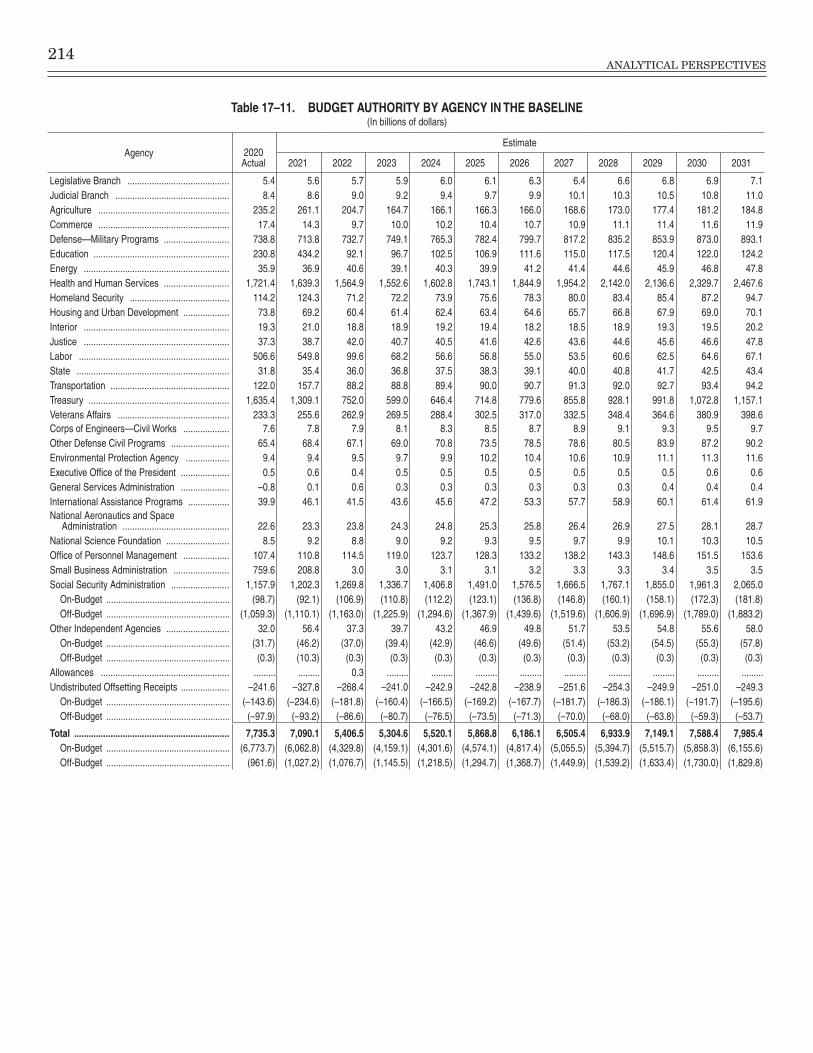

Other Assumptions in the Baseline ................................................................................. * 17–5. Receipts by Source in the Projection of Baseline ........................................................... 209 17–6. Effect on Receipts of Changes in the Social Security Taxable Earnings Base ............. 210 17–7. Change in Outlay Estimates by Category in the Baseline ............................................ 210 17–8. Outlays by Function in the Baseline .............................................................................. 211 17–9. Outlays by Agency in the Baseline ................................................................................. 212 17–10. Budget Authority by Function in the Baseline .............................................................. 213 17–11. Budget Authority by Agency in the Baseline ................................................................. 21417–12. Current Services Budget Authority and Outlays by Function, Category, and Program ... *

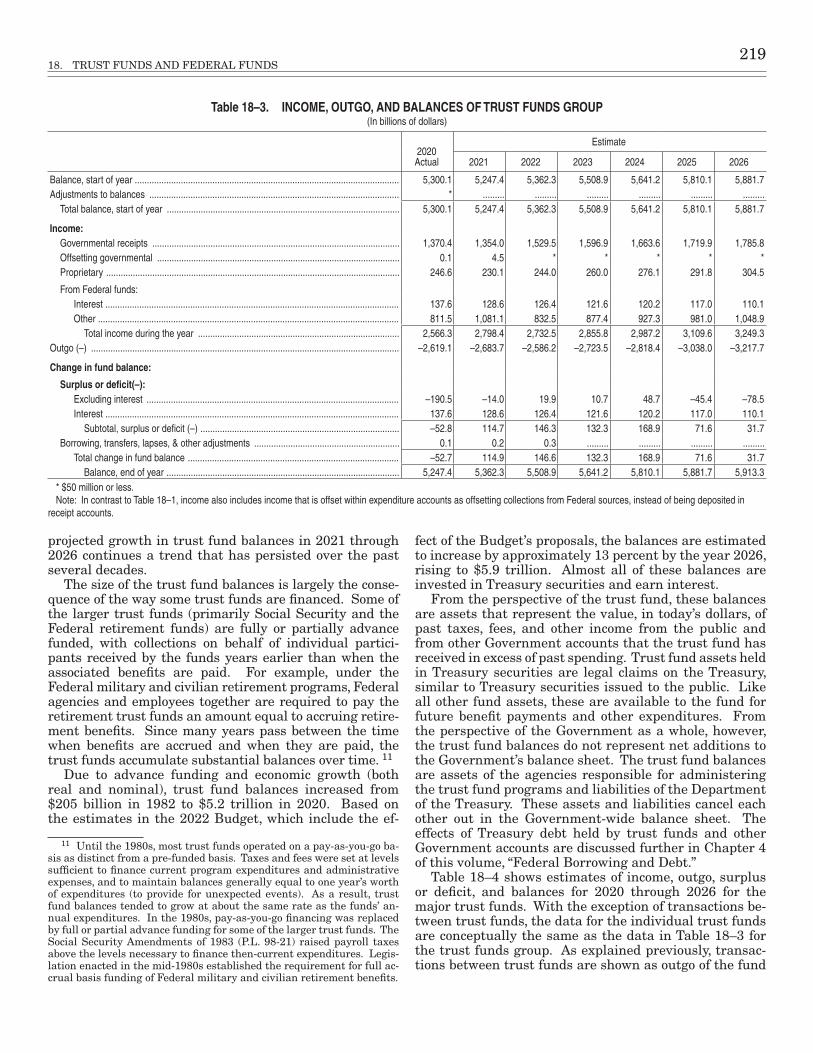

Trust Funds and Federal Funds 18–1. Receipts, Outlays and Surplus or Deficit by Fund Group ............................................. 217 18–2. Comparison of Total Federal Fund and Trust Fund Receipts to

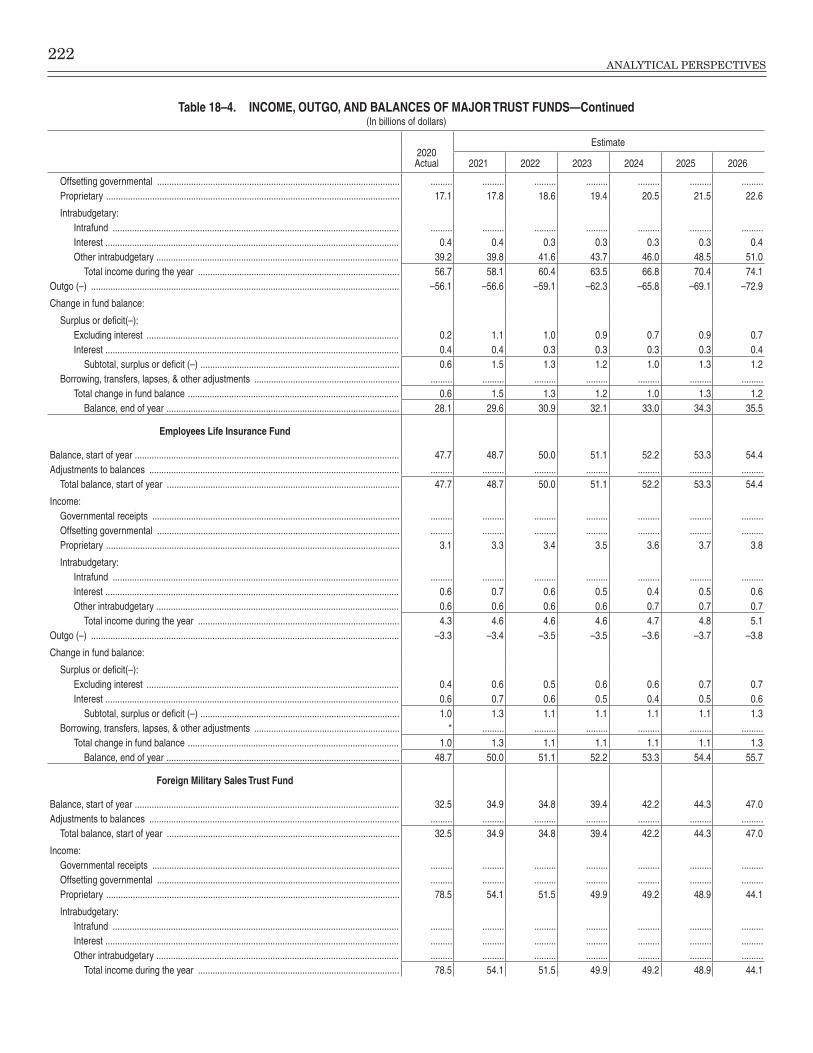

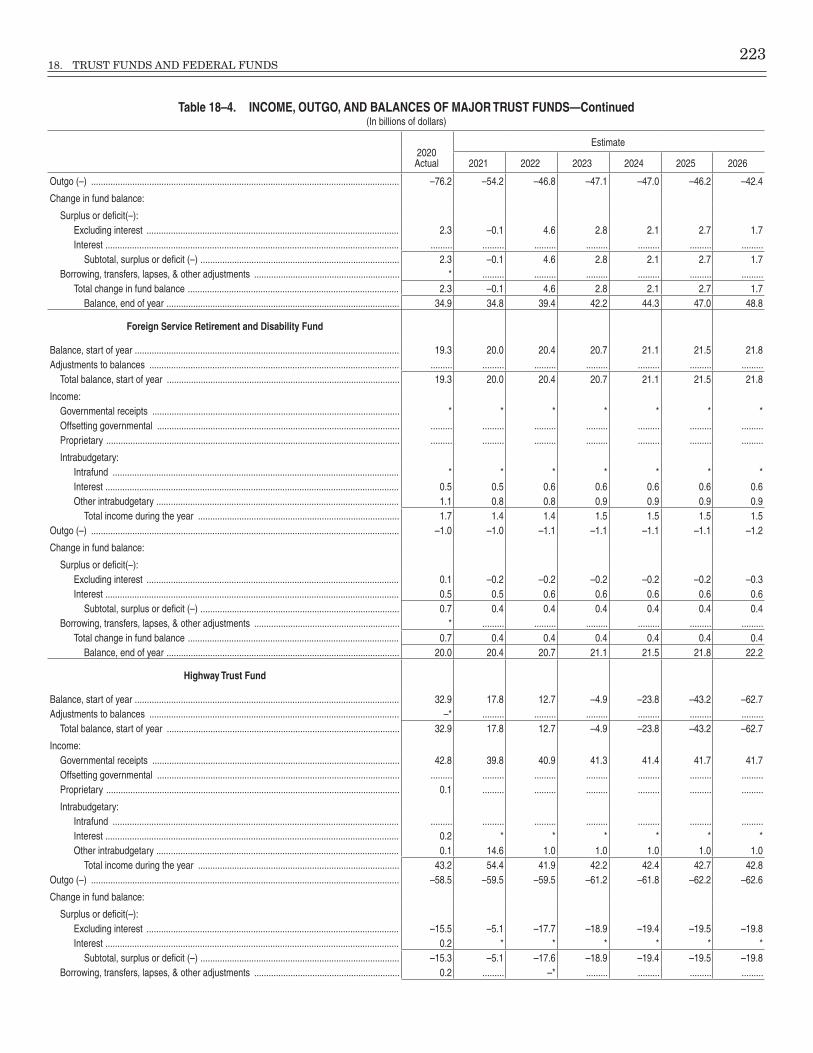

Unified Budget Receipts, Fiscal Year 2020 ................................................................. 218 18–3. Income, Outgo, and Balances of Trust Funds Group ..................................................... 219 18–4. Income, Outgo, and Balances of Major Trust Funds ...................................................... 221 18–5. Income, Outgo, and Balances of Selected Special Funds ............................................... 228

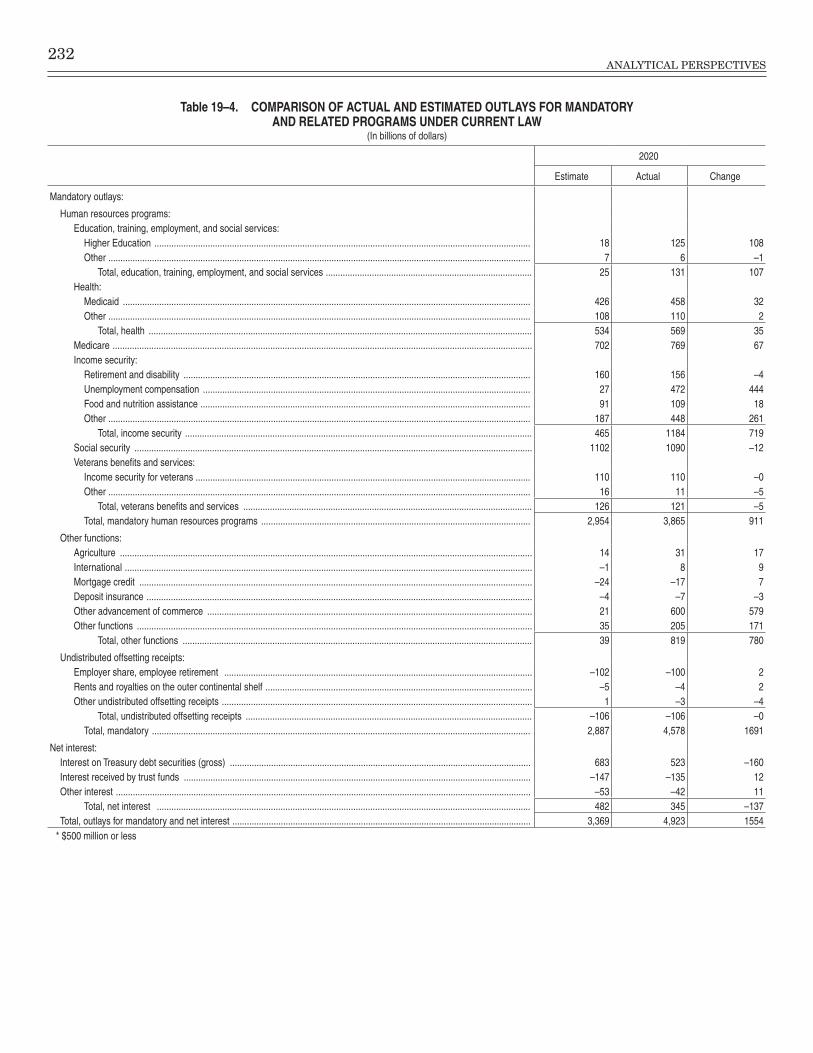

Comparison of Actual to Estimated Totals 19–1. Comparison of Actual 2020 Receipts with the Initial Current Services Estimates ..... 229 19–2. Comparison of Actual 2020 Outlays with the Initial Current Services Estimates ...... 230 19–3. Comparison of the Actual 2020 Deficit with the Initial Current Services Estimate ... 231 19–4. Comparison of Actual and Estimated Outlays for Mandatory

and Related Programs Under Current Law ............................................................... 232 19–5. Reconciliation of Final Amounts For 2020 ..................................................................... 233

Detailed Functional Tables

20–1. Budget Authority and Outlays by Function, Category and Program ................................ *

Federal Budget by Agency and Account

21–1. Federal Budget by Agency and Account .............................................................................. * Calfed Bay-Delta Federal Budget Crosscut Report ........................................................................... * Columbia River Basin Federal Budget Crosscut Report ................................................................... *

Page

*Available on the internet at http://www.whitehouse.gov/omb/analytical-perspectives/

1

INTRODUCTION

3

1. INTRODUCTION

The Analytical Perspectives volume presents analyses that highlight specific subject areas or provide other sig-nificant data that place the President’s 2022 Budget in context and assist the public, policymakers, the media, and researchers in better understanding the Budget. This volume complements the main Budget volume, which presents the President’s Budget policies and priorities, and the Budget Appendix volume, which provides ap-propriations language, schedules for budget expenditure accounts, and schedules for selected receipt accounts.

Presidential Budgets have included separate analyti-cal presentations of this kind for many years. The 1947 Budget and subsequent budgets included a separate sec-tion entitled Special Analyses and Tables that covered four, and later more, topics. For the 1952 Budget, the section was expanded to 10 analyses, including many subjects still covered today, such as receipts, investment, credit programs, and aid to State and local governments. With the 1967 Budget this material became a separate volume entitled Special Analyses, and included 13 chap-ters. The material has remained a separate volume since then, with the exception of the Budgets for 1991–1994, when all of the budget material was included in one volume. Beginning with the 1995 Budget, the volume has been named Analytical Perspectives. Since the 2022 Budget is being released following a presidential tran-sition, OMB is publishing an abbreviated Analytical Perspectives volume this year. The 2023 Budget will include a more comprehensive Analytical Perspectives vol-ume with additional key updates on areas including the Government’s mission performance goals and objectives and the President’s Management Agenda (PMA), effective utilization of Federal real property, statistics that offer a numerical picture of the United States and an overview of statistical agency budgets and priorities, and the impor-tance of using evidence, evaluation, and data to improve Government effectiveness.

In addition to the information included in this vol-ume, supplemental tables and other materials that are part of the Analytical Perspectives volume are available at http://www.whitehouse.gov/omb/analytical-perspec-tives. Tables included at this link are shown in the List of Tables in the front of this volume with an asterisk instead of a page number.

Overview of the Chapters

Economic and Budget Analyses

Economic Assumptions and Overview. This chap-ter reviews recent economic developments; presents the Administration’s assessment of the economic situation and outlook; compares the economic assumptions on

which the 2022 Budget is based with the assumptions for last year’s Budget and those of other forecasters; pro-vides sensitivity estimates for the effects on the Budget of changes in specified economic assumptions; and reviews past errors in economic projections.

Long-Term Budget Outlook. This chapter assesses the long-term budget outlook under current policies and under the Budget’s proposals. It focuses on 25-year projections of Federal deficits and debt to illustrate the long-term impact of the Administration’s proposed poli-cies. It also discusses the uncertainties of the long-term budget projections and discusses the actuarial status of the Social Security and Medicare programs.

Federal Borrowing and Debt. This chapter analyzes Federal borrowing and debt and explains the budget es-timates. It includes sections on special topics such as trends in debt, debt held by the public net of financial as-sets and liabilities, investment by Government accounts, and the statutory debt limit.

Management

Strengthening the Federal Workforce. This chapter presents summary data on Federal employment and com-pensation, and discusses the approach the Administration is taking with Federal human capital management.

Budget Concepts and Budget Process

Budget Concepts. This chapter includes a basic descrip-tion of the budget process, concepts, laws, and terminology, and includes a glossary of budget terms. It also discusses proposals specific to the 2022 Budget to improve budget-ing under certain budget concepts.

Coverage of the Budget. This chapter describes activi-ties that are included in budget receipts and outlays (and are therefore classified as “budgetary”) as well as those activities that are not included in the Budget (and are therefore classified as “non-budgetary”). The chapter also defines the terms “on-budget” and “off-budget” and in-cludes illustrative examples.

Federal Receipts

Governmental Receipts. This chapter presents informa-tion on estimates of governmental receipts, which consist of taxes and other compulsory collections. It includes descrip-tions of tax-related legislation enacted in the last year and describes proposals affecting receipts in the 2022 Budget.

Offsetting Collections and Offsetting Receipts. This chapter presents information on collections that offset outlays, including collections from transactions with the public and intragovernmental transactions. In addition, this chapter presents information on “user fees,” charges associated with market-oriented activities and regulatory fees. Detailed tables of offsetting receipts and offsetting

4ANALYTICAL PERSPECTIVES

collections in the Budget are available at the internet ad-dress cited above.

Tax Expenditures. This chapter describes and pres-ents estimates of tax expenditures, which are defined as revenue losses from special exemptions, credits, or other preferences in the tax code.

Special Topics

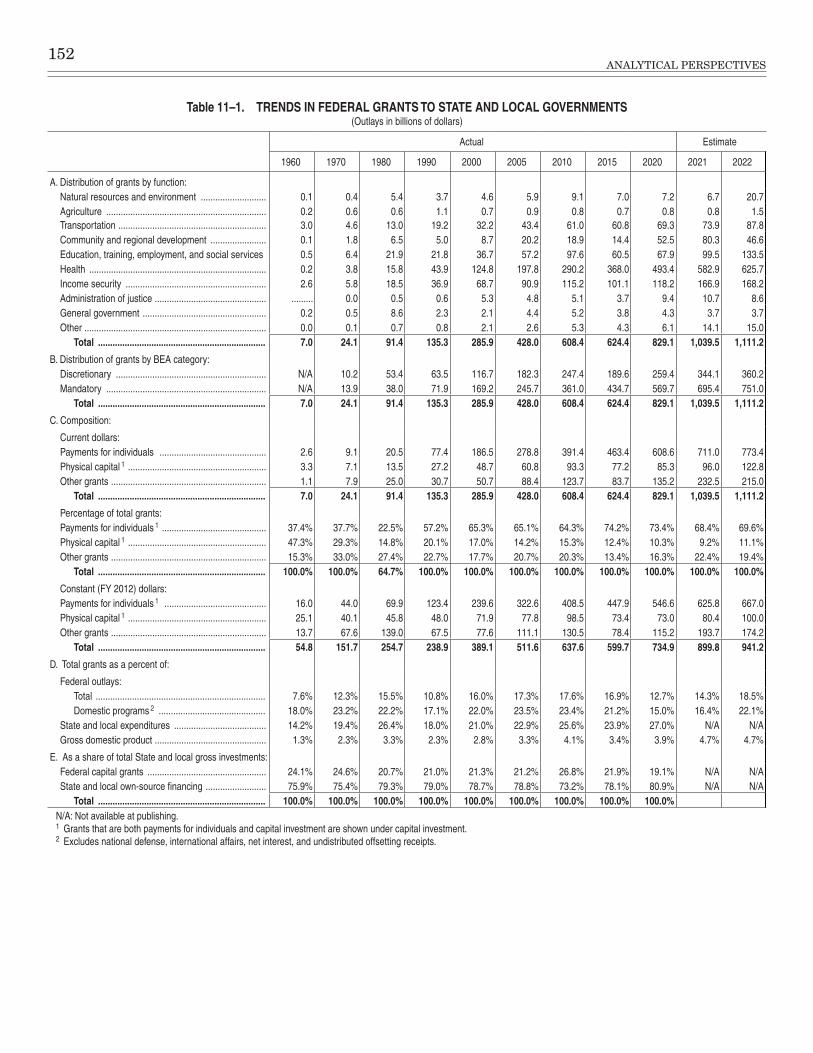

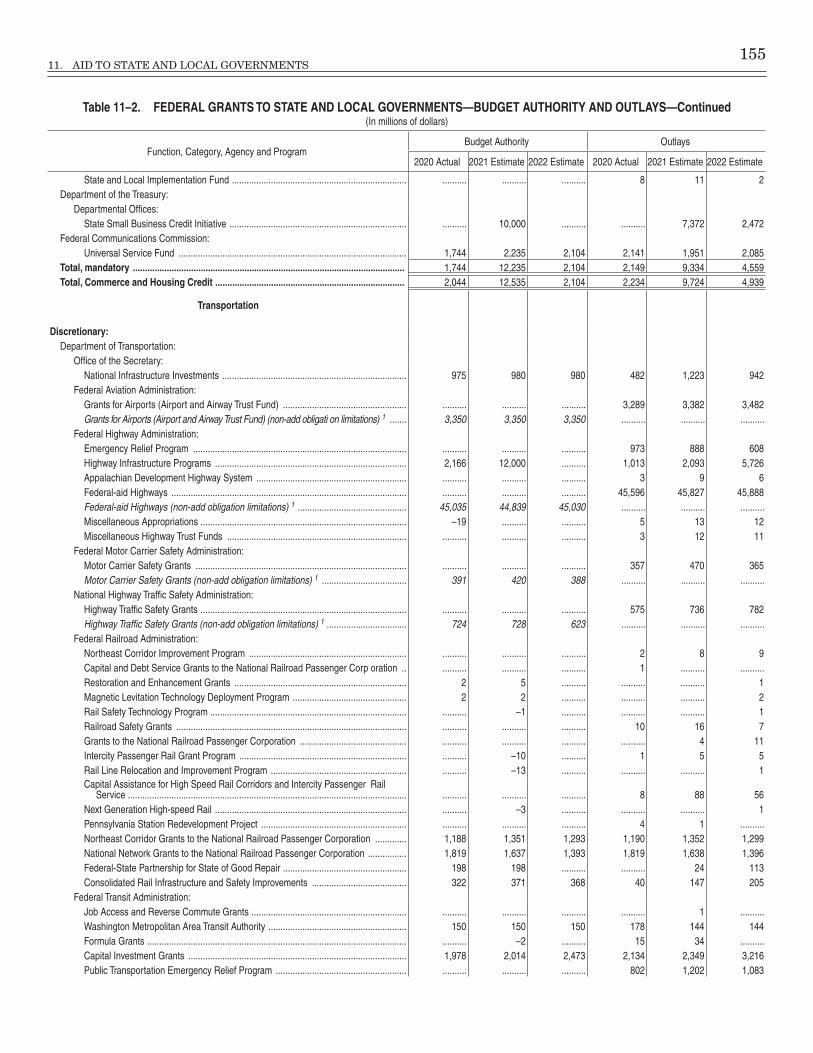

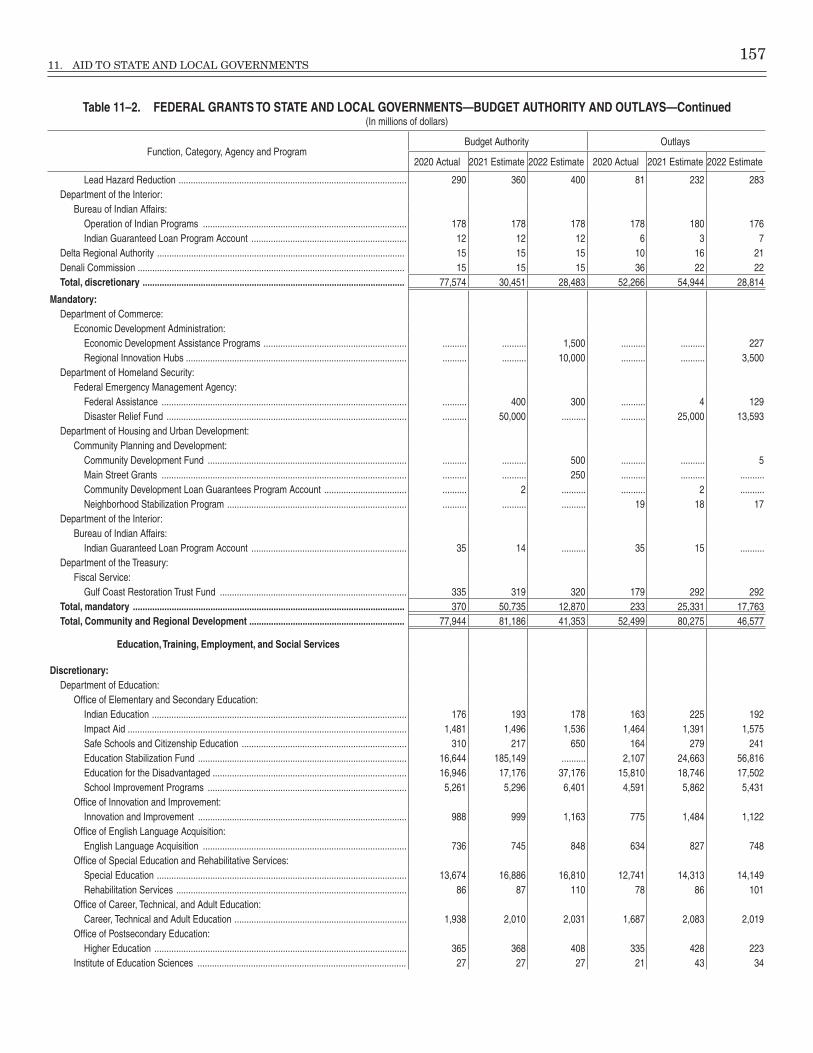

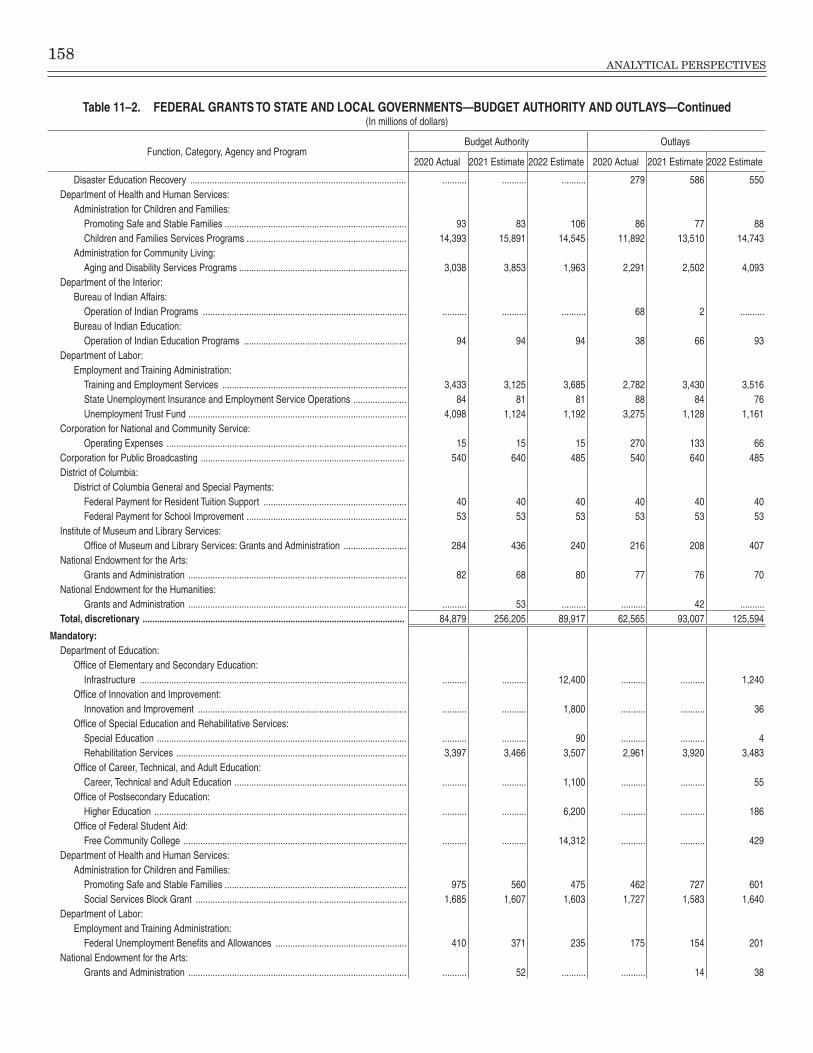

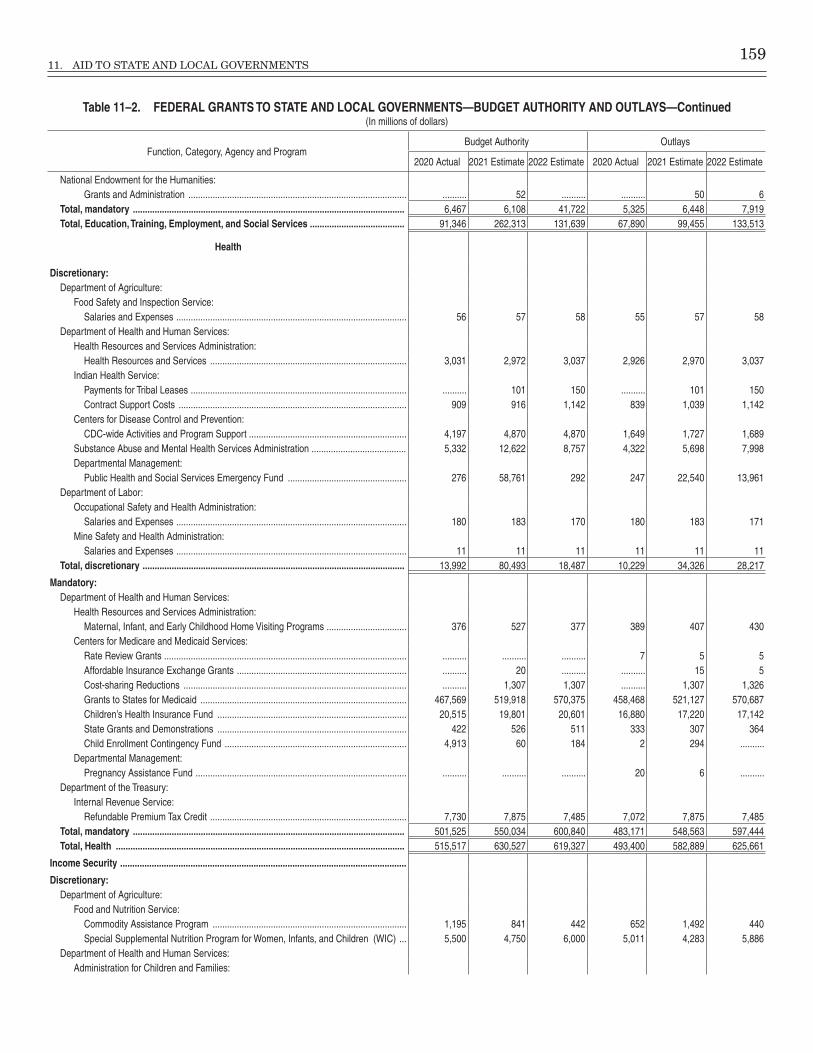

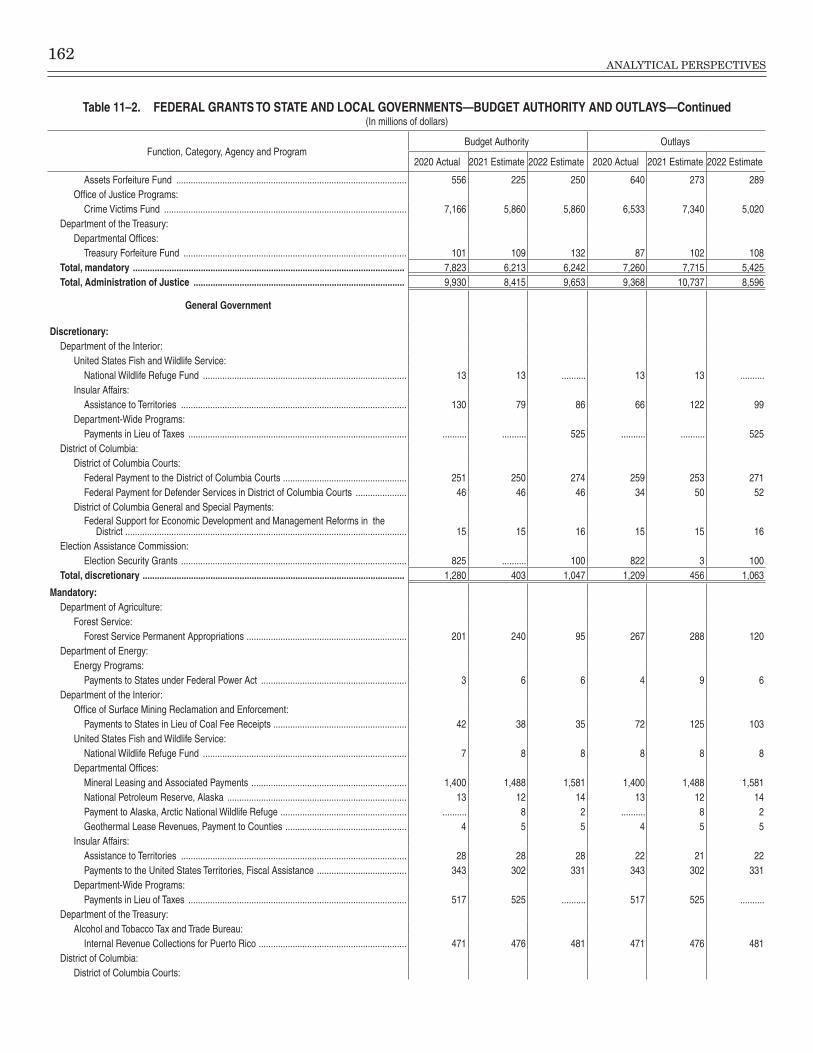

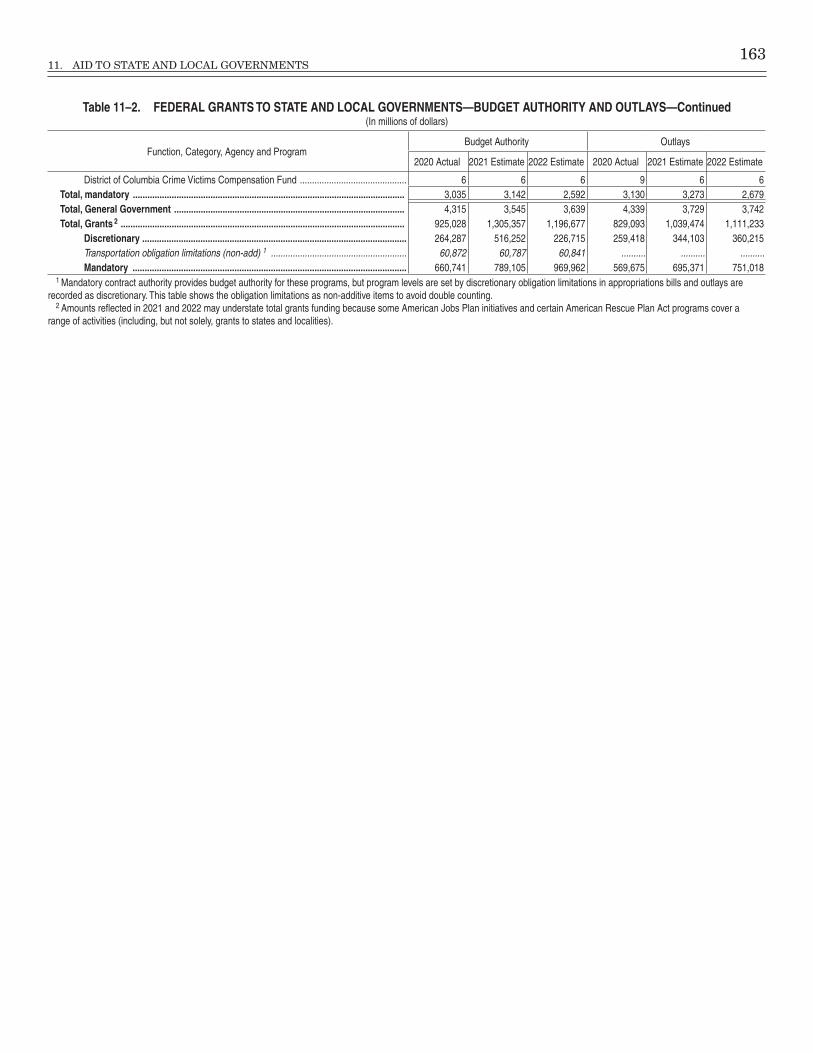

Aid to State and Local Governments. This chapter pres-ents crosscutting information on Federal grants to State and local governments. The chapter also includes a table showing historical grant spending, and a table with bud-get authority and outlays for grants in the Budget. Tables showing State-by-State spending for major grant pro-grams are available at the internet address cited above.

Information Technology and Cybersecurity. This chap-ter addresses Federal information technology (IT) and cybersecurity, highlighting initiatives and proposed fund-ing levels to deliver critical citizen services, keep sensitive data and systems secure, and further the vision of modern Government. The Administration will invest in modern, secure technologies and services to drive enhanced effi-ciency and effectiveness. This will include undertaking complex Government-wide modernization efforts, driving improved delivery of citizen-facing services, and improv-ing the overall management of the Federal IT portfolio. The Administration will also continue its efforts to fur-ther build the Federal IT workforce and seek to reduce the Federal Government’s cybersecurity risk in order to better serve and protect the American public.

Federal Investment. This chapter discusses federally financed spending that yields long-term benefits. It pres-ents information on annual spending on physical capital, research and development, and education and training.

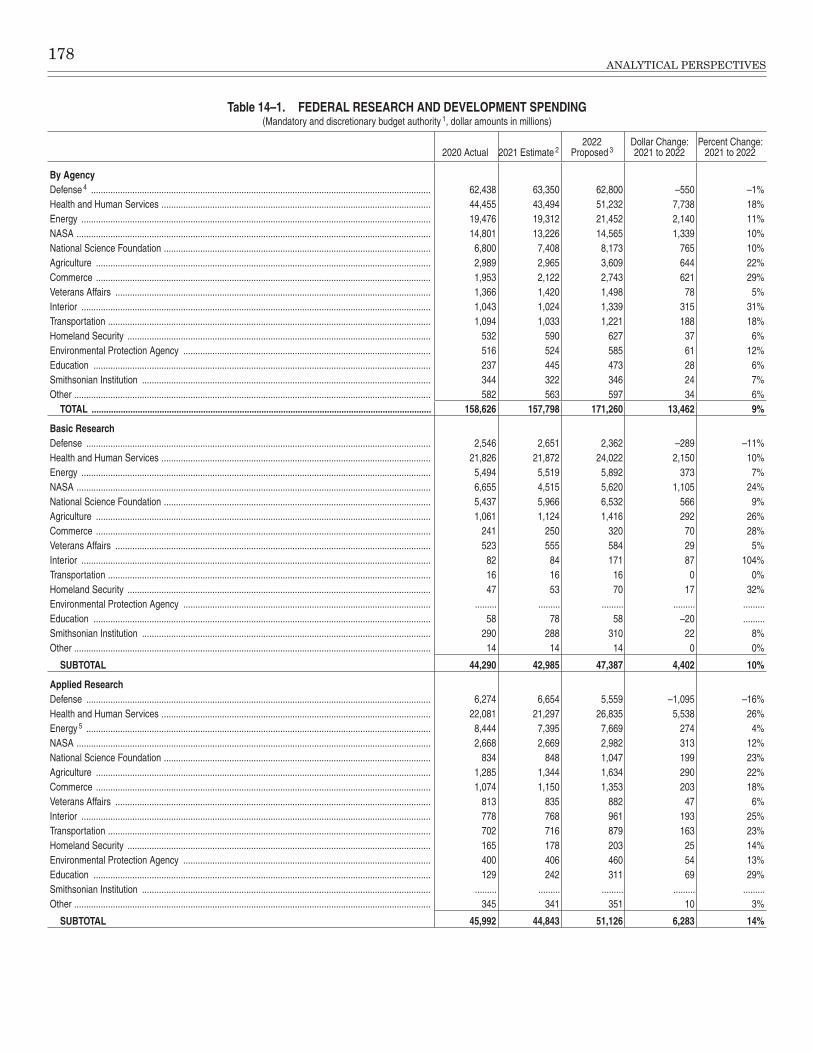

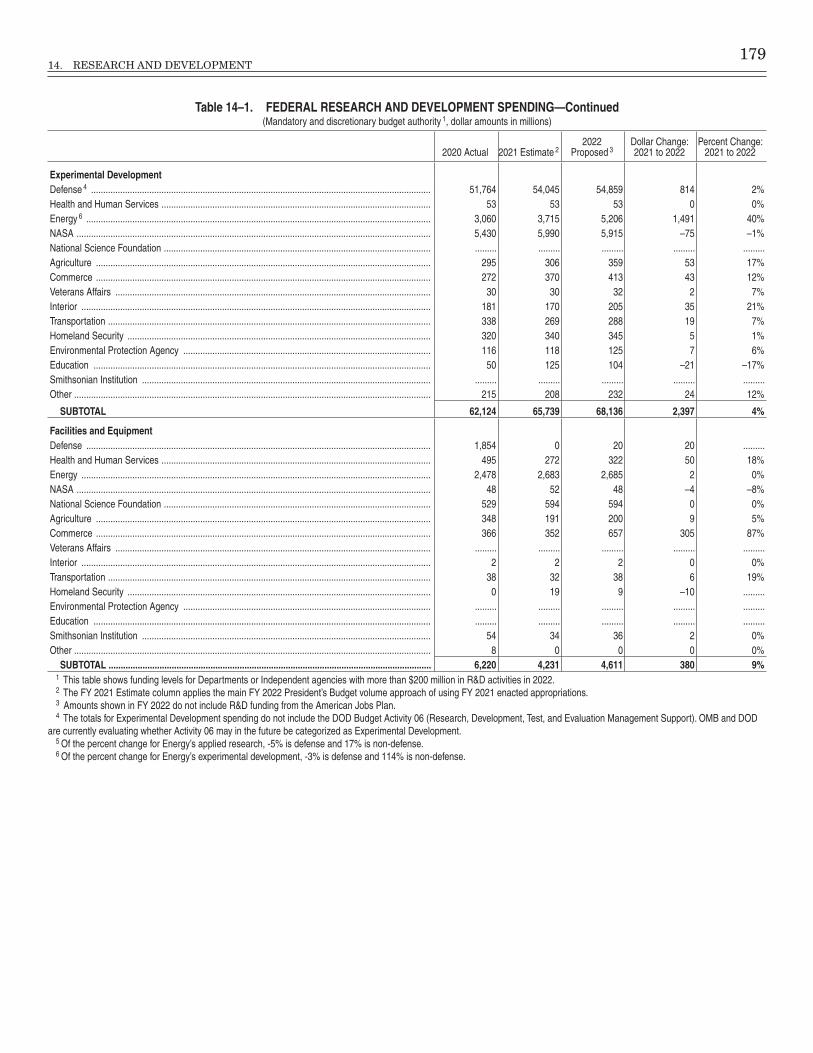

Research and Development. This chapter presents a crosscutting review of research and development funding in the Budget.

Credit and Insurance. This chapter provides cross-cutting analyses of the roles, risks, and performance of Federal credit and insurance programs and Government-sponsored enterprises (GSEs). The chapter covers the major categories of Federal credit (housing, education, small business and farming, energy and infrastructure, and international) and insurance programs (deposit in-surance, pension guarantees, disaster insurance, and insurance against terrorism-related risks). Five addi-tional tables address transactions including direct loans, guaranteed loans, and GSEs. These tables are available at the internet address cited above.

Federal Drug Control Funding. This chapter displays enacted and proposed drug control funding for Federal Departments and Agencies.

Technical Budget Analyses

Current Services Estimates. This chapter discusses the conceptual basis of the Budget’s current services, or “baseline,” estimates, which are generally consistent with the baseline rules in the Balanced Budget and Emergency

Deficit Control Act of 1985 (BBEDCA). The chapter pres-ents estimates of receipts, outlays, and the deficit under this baseline. Two detailed tables addressing factors that affect the baseline and providing details of baseline bud-get authority and outlays are available at the internet address cited above.

Trust Funds and Federal Funds. This chapter provides summary information about the two fund groups in the Budget—Federal funds and trust funds. In addition, for the major trust funds and certain Federal fund programs, the chapter provides detailed information about income, outgo, and balances.

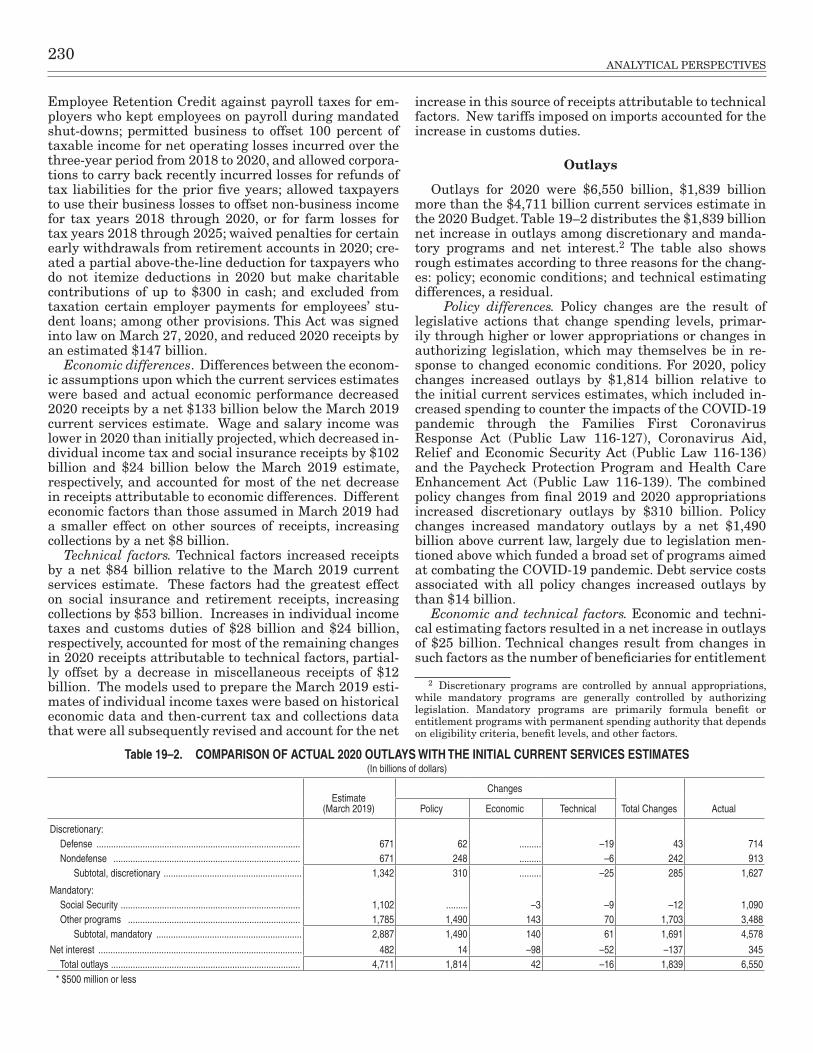

Comparison of Actual to Estimated Totals. This chap-ter compares the actual receipts, outlays, and deficit for 2020 with the estimates for that year published in the 2020 Budget, published in March 2019.

The following materials are available at the internet address cited above.

Detailed Functional Table

Detailed Functional Table. Table 20–1, “Budget Authority and Outlays by Function, Category, and Program,” displays budget authority and outlays for major Federal program categories, organized by budget function (such as healthcare, transportation, or national defense), category, and program.

Federal Budget by Agency and Account

Federal Budget by Agency and Account. Table 21–1, “Federal Budget by Agency and Account,” displays bud-get authority and outlays for each account, organized by agency, bureau, fund type, and account.

Budgets of the Federal Statistical Agencies

Budgets of the Federal Statistical Agencies. Table 22-1, “Budgets of the Federal Statistical Agencies,” displays the budgets of the Principle Statistical Agencies recognized by OMB, organized by agency.

Calfed Bay-Delta Program Federal Budget Crosscut

Calfed Bay-Delta Program Crosscut. The Calfed Bay-Delta Program interagency budget crosscut report provides an estimate of Federal funding by each of the participating Federal Agencies with authority and pro-grammatic responsibility for implementing this program, fulfilling the reporting requirements of section 106(c) of Public Law 108–361.

Columbia River Basin Federal Budget Crosscut

Columbia River Basin Federal Budget Crosscut. The Columbia River interagency budget crosscut report in-cludes an estimate of Federal funding by each of the participating Federal agencies to carry out restoration activities within the Columbia River Basin, fulfilling the reporting requirements of section 123 of the Clean Water Act (33 U.S.C. 1275).

5

ECONOMIC AND BUDGET ANALYSES

7

2. ECONOMIC ASSUMPTIONS AND OVERVIEW

This chapter presents the economic assumptions that underlie the Administration’s 2022 Budget.1 It provides an overview of the recent performance of the American economy, presents the Administration’s projections for key macroeconomic variables, compares them to forecasts prepared by other prominent institutions, and discusses the unavoidable uncertainty inherent in providing long-term forecasts.

This chapter proceeds as follows:The first section provides an overview of the recent

functioning of the U.S. economy, examining the perfor-mance of a broad array of key economic indicators.

The second section presents a detailed exposition of the Administration’s economic assumptions underlying the 2022 Budget, discussing how key macroeconomic vari-ables are expected to evolve over the years 2021 to 2031.

The third section compares the forecast of the Administration with those of the Congressional Budget Office (CBO), the Federal Open Market Committee of the Federal Reserve, and the Blue Chip panel of private-sec-tor forecasters.

The fourth section discusses the sensitivity of the Administration’s projections of Federal receipts and out-lays to alternative paths of macroeconomic variables.

The fifth section considers the errors in past Administrations’ forecasts, comparing them with the er-rors in forecasts produced by the CBO and the Blue Chip panel of private professional forecasters.

The sixth section uses information on past accuracy of Administration forecasts to provide understanding

1 Economic performance, unless otherwise specified, is discussed in terms of calendar years (January-December). Budget figures are dis-cussed in terms of fiscal years (October-September).

and insight into the uncertainty associated with the Administration’s current forecast of the budget balance.

Recent Economic Performance2

The onset of the COVID-19 pandemic was marked by a sharp recession with steep declines across all prominent U.S. economic indicators. Unlike a typical recession, the effects of the recession were most acutely felt by those in the service and retail sectors, where social distancing be-havior limited overall spending and activity. The economy plunged in the second quarter of 2020 and has partially rebounded in the quarters since, yet GDP remains below its pre-pandemic peak. Gains continue to be made in la-bor force participation while employers have added over 1.5 million jobs since the beginning of 2021.

Looking forward, consumers and businesses alike are showing increasing optimism following the passage of the American Rescue Plan Act of 2021 and significant prog-ress in controlling the pandemic. Both the University of Michigan and Conference Board indicators for con-sumer sentiment and consumer confidence, respectively, have increased substantially over the past few months. Improvements in consumer sentiment signal increased consumer spending heading into the summer months. Businesses are also exhibiting optimism, as seen in the re-cent high levels of the ISM Purchasing Managers Index, a survey of business activity at manufacturing companies.

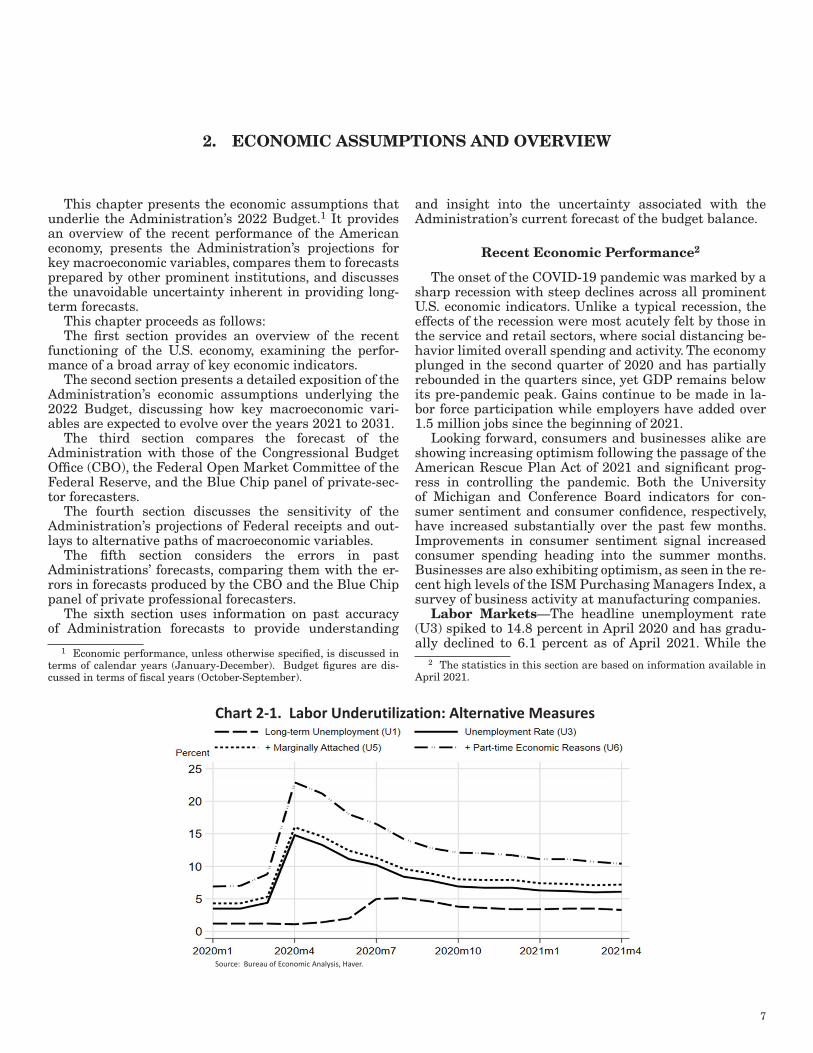

Labor Markets—The headline unemployment rate (U3) spiked to 14.8 percent in April 2020 and has gradu-ally declined to 6.1 percent as of April 2021. While the

2 The statistics in this section are based on information available in April 2021.

Chart 2-1. Labor Underutilization: Alternative Measures

Source: Bureau of Economic Analysis, Haver.

8ANALYTICAL PERSPECTIVES

decline in the unemployment rate is a positive sign for the economy, and the Blue Chip panel of professional fore-casters projects that the unemployment rate will fall to an average of 4.7 percent during 2022, several important labor market indicators still show signs of weakness.

By looking at alternative measures of labor unde-rutilization (Chart 2-1), we can get a clearer picture of the state of employment. The U5 unemployment rate, which includes those workers who identify as margin-ally attached to the workforce, is 7.2 percent as of April.3 Including workers who are working part-time for econom-ic reasons (U6), the rate is 10.4 percent. Additionally, not only do millions of Americans remain unemployed—9.8 million as of April, a 72.0 percent increase from February 2020—but the duration of unemployment remains elevat-

3 The BLS defines marginally attached workers as persons who are not in the labor force, want and are available for work, and had looked for a job sometime in the prior 12 months. They are not counted as un-employed because they had not searched for work in the prior 4 weeks.

ed as well. The long-term unemployment rate (U1), which measures the percent of the labor force unemployed for 15 weeks or longer, is 3.3 percent as of April; this is almost three times as high as the pre-pandemic rate of 1.2 per-cent from February 2020. Moreover, the median duration of unemployment in April was 19.8 weeks, which is the highest this indicator has been since October 2012.

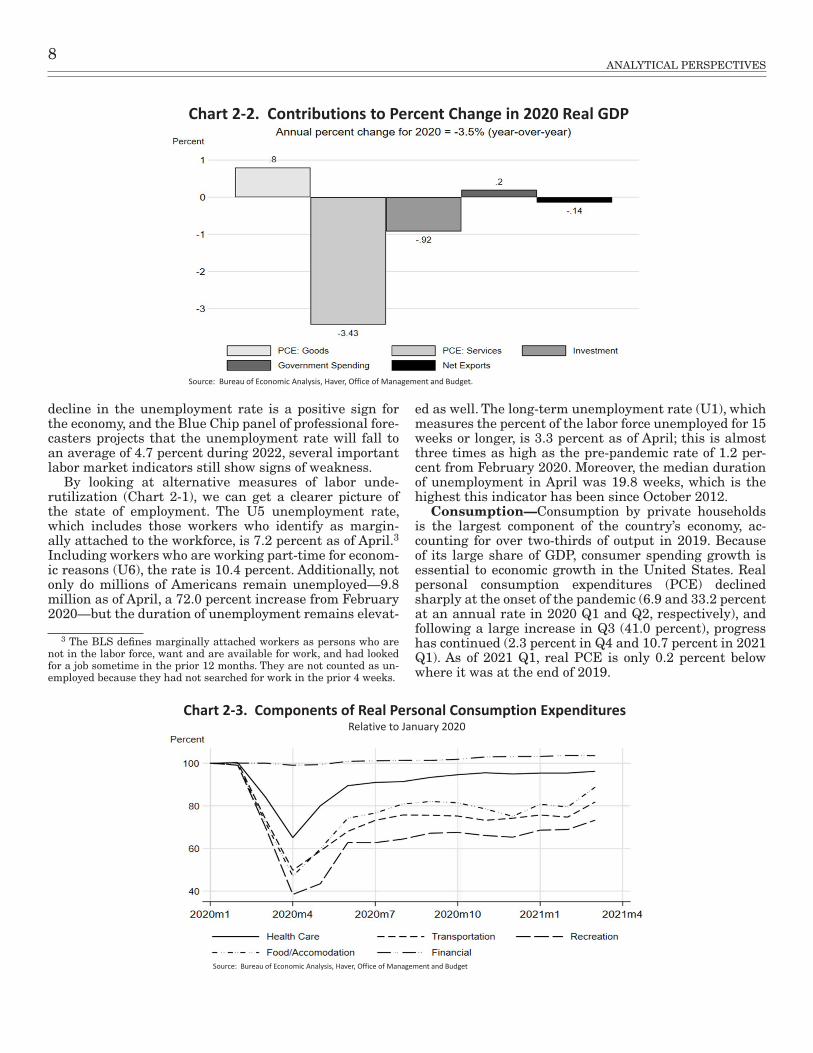

Consumption—Consumption by private households is the largest component of the country’s economy, ac-counting for over two-thirds of output in 2019. Because of its large share of GDP, consumer spending growth is essential to economic growth in the United States. Real personal consumption expenditures (PCE) declined sharply at the onset of the pandemic (6.9 and 33.2 percent at an annual rate in 2020 Q1 and Q2, respectively), and following a large increase in Q3 (41.0 percent), progress has continued (2.3 percent in Q4 and 10.7 percent in 2021 Q1). As of 2021 Q1, real PCE is only 0.2 percent below where it was at the end of 2019.

Chart 2-2. Contributions to Percent Change in 2020 Real GDP

Source: Bureau of Economic Analysis, Haver, Office of Management and Budget.

Chart 2-3. Components of Real Personal Consumption ExpendituresRelative to January 2020

Source: Bureau of Economic Analysis, Haver, Office of Management and Budget

2. ECONOMIC ASSUMPTIONS AND OVERVIEW 9

A prominent story of the pandemic has been the extent of the economic damage in specific sectors, particularly services. Chart 2-2 illustrates that a decline in the com-bined consumption of goods and services accounted for 75 percent of the total decline in real GDP for the year as a whole in 2020. Looking at the composition of services con-sumption, Chart 2-3 shows that several prominent service sectors are still considerably below pre-pandemic levels.

Nonresidential Fixed Investment—Real nonresi-dential fixed investment declined at an annual rate of 4.0 percent in 2020 (year-over-year). Equipment and intel-lectual property investment have recovered strongly in recent quarters, although business structures investment remains slow.

The Government Sector—Topline real government expenditures on consumption and investment increased 1.1 percent in 2020 (year-over-year), which includes a 4.3 percent increase in Federal spending partially offset by a 0.8 percent decline in State and Local spending. Within the Federal spending category, nondefense spending rose 5.6 percent while defense spending increased 3.5 percent.

Federal Reserve Policy—The Federal Reserve’s re-sponse to the COVID-19 pandemic can be grouped into three main categories: lowering the policy rate, stabiliz-ing financial markets, and supporting the flow of credit in the economy.4 First, the Fed’s monetary policymaking

4 See the following Fed blog post for a more detailed description of the

body—the Federal Open Market Committee (FOMC)—quickly lowered the target range for the federal funds rate. The federal funds rate, which serves as the FOMC’s policy interest rate, is the rate that banks charge each other for overnight loans. In an effort to forestall negative economic impacts from the pandemic, the FOMC rapidly lowered the federal funds rate from an average of 1.59 in January 2020 to 0.08 by the end of March 2020, and this rate currently sits within the target range of 0 to 0.25 per-cent as of April 2021. This step helped reduce borrowing costs for households and businesses.

During its March 2021 meeting the FOMC announced it would maintain the target range for the federal funds rate at 0 to 0.25 percent. In its accompanying statement, the Committee repeated that it will not raise the federal funds rate target range “until labor market conditions have reached levels consistent with the Committee’s as-sessments of maximum employment and inflation has risen to 2 percent and is on track to moderately exceed 2 percent for some time.”

Second, the Fed took a number of steps to unfreeze key financial markets and to help them run smoothly. In many cases this involved the purchases of securities and assets that were otherwise difficult to sell. These purchases con-

Fed’s policy response to the pandemic: https://www.stlouisfed.org/open-vault/2020/august/fed-response-covid19-pandemic

Table 2–1. ECONOMIC ASSUMPTIONS 1

(Calendar Years, Dollar Amounts In Billions)

Actual2019

Projections

2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031

Gross Domestic Product (GDP)Levels, Dollar Amounts in Billions:

Current Dollars �������������������������������������������������������� 21,433 20,933 22,411 23,799 24,808 25,778 26,767 27,794 28,860 29,986 31,166 32,414 33,723Real, Chained (2012) Dollars ���������������������������������� 19,092 18,423 19,375 20,200 20,652 21,039 21,418 21,803 22,196 22,609 23,039 23,491 23,961Chained Price Index (2012=100), Annual Average � 112 114 116 118 120 123 125 128 130 133 135 138 141

Percent Change, Fourth Quarter over Fourth Quarter:Current Dollars �������������������������������������������������������� 4�0 -1�2 7�1 5�2 4�0 3�8 3�8 3�8 3�8 3�9 3�9 4�0 4�0Real, Chained (2012) Dollars ���������������������������������� 2�3 -2�5 5�2 3�2 2�0 1�8 1�8 1�8 1�8 1�9 1�9 2�0 2�0Chained Price Index (2012=100) ����������������������������� 1�6 1�3 1�8 1�9 2�0 2�0 2�0 2�0 2�0 2�0 2�0 2�0 2�0

Incomes, Billions of Current DollarsDomestic Corporate Profits ������������������������������������� 1,745 1,616 1,529 1,725 1,795 1,861 1,880 1,854 1,828 1,825 1,849 1,900 1,955Employee Compensation ����������������������������������������� 11,432 11,489 12,247 12,907 13,416 13,909 14,435 15,018 15,642 16,305 17,002 17,730 18,491Wages and Salaries ������������������������������������������������ 9,309 9,369 10,047 10,491 10,918 11,383 11,818 12,296 12,812 13,352 13,930 14,526 15,159Nonwage Personal Income �������������������������������������� 5,413 5,409 5,324 5,522 5,806 6,096 6,436 6,747 7,094 7,371 7,650 7,984 8,265

Consumer Price Index (All Urban) 3:Level (1982-1984 = 100), Annual Average �������������� 249 252 258 263 269 275 281 287 294 301 307 314 321Percent Change, Fourth Quarter over Fourth

Quarter ��������������������������������������������������������������� 1�9 1�3 2�0 2�1 2�2 2�3 2�3 2�3 2�3 2�3 2�3 2�3 2�3

Unemployment Rate, Civilian, PercentAnnual Average ������������������������������������������������������� 3�7 8�1 5�5 4�1 3�8 3�8 3�8 3�8 3�8 3�8 3�8 3�8 3�8

Interest Rates, Percent91-Day Treasury Bills 2 ��������������������������������������������� 2�1 0�4 0�1 0�2 0�4 0�8 1�2 1�5 1�6 1�7 1�8 2�1 2�310-Year Treasury Notes ������������������������������������������� 2�1 0�9 1�2 1�4 1�7 2�1 2�4 2�6 2�7 2�8 2�8 2�8 2�8

1 Based on information available as of mid-February 20212 Average rate, secondary market (bank discount basis)3 Seasonally Adjusted

10ANALYTICAL PERSPECTIVES

veyed to the public that the Fed stands ready to assist important parts of the financial system.

Third, the Fed introduced several temporary lending and funding facilities to support the flow of credit to busi-nesses and households. Overall, the Fed has introduced multiple temporary facilities to support various types of funding and credit markets. Two of the commonly dis-cussed facilities are the Paycheck Protection Program Liquidity Facility, established to help small businesses keep workers on the payroll, and the Main Street Lending Program (a set of five facilities), established to support lending to both small and midsized businesses and non-profit organizations.

Economic Projections

The Administration’s forecast was finalized on February 19, with the parameters of that forecast close to the consensus prevailing at that date. The forecast in-forms the 2022 Budget and assumes implementation of the Administration’s policy proposals. Importantly, how-ever, the projections described below were formulated before the details of the American Jobs Plan (AJP) and American Families Plan (AFP) were finalized and there-fore do not incorporate the full impact of these policies. The Administration’s projections are reported in Table 2-1 and summarized below.

Real GDP—In 2021, as the economy recovers from the COVID-19 pandemic, the Administration forecast assumes a strong recovery in civilian employment, as-sociated with a rebound at a fourth quarter-over-fourth quarter rate of 5.2 percent. As noted below, growth to date in 2021 has been strong, and private forecasters

now project somewhat more rapid 2021 growth than in the Administration forecast. As the economy continues to recover and the employment picture improves, growth is projected to be 3.2 percent in 2022. Real GDP is projected to return to its long-run “potential” level by 2023 and is forecasted to grow at an average of 1.9 percent between 2024 and 2031.

Unemployment—As of December 2020, the unem-ployment rate stood at 6.7 percent, a substantial recovery from the peak rate of 14.8 percent in April 2020 but still high relative to historical levels. The Administration expects a rapid and strong recovery in unemployment coinciding with progress in controlling the pandemic, with the unemployment rate dropping to 4.7 percent by the end of 2021. The Administration then forecasts un-employment rates will drop to 4.1 percent by 2022 before leveling out at 3.8 percent from 2023-2031.

Interest Rates—Interest rates are expected to rise as the economy recovers from the recession and as infla-tion rises and then stabilizes around the Federal Reserve target rate of 2 percent. The 91-day Treasury bill rate is expected to steadily rise from an average of 0.1 percent in 2021 to 1.2 percent in 2025, then gradually increase to a terminal rate of 2.3 percent. The 10-year rate follows a similar path as it increases from 1.4 percent in 2021 to 2.4 percent by 2025, reaching 2.8 percent at the end of the budget window, which reflects both the increase in short-term rates and an increase in the term premium for investors committing to holding long-term securities.

General Inflation—The Administration’s forecast assumes that inflation will return to a long run trend. Specifically, the Administration’s forecast assumes that the Consumer Price Index for all Urban Consumers

Table 2–2. COMPARISON OF ECONOMIC ASSUMPTIONS IN THE 2021 AND 2022 BUDGETS

2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Real GDP (Percent Change)1:2021 Budget Assumptions ����������������������������������������������������������� 2�5 2�5 3�1 3�0 3�0 3�0 3�0 2�9 2�8 2�8 2�8 2�82022 Budget Assumptions ����������������������������������������������������������� 2�3 –2�5 5�2 3�2 2�0 1�8 1�8 1�8 1�8 1�9 1�9 2�0

GDP Price Index (Percent Change)1:2021 Budget Assumptions ����������������������������������������������������������� 2�3 1�8 2�0 2�0 2�0 2�0 2�0 2�0 2�0 2�0 2�0 2�02022 Budget Assumptions ����������������������������������������������������������� 1�6 1�3 1�8 1�9 2�0 2�0 2�0 2�0 2�0 2�0 2�0 2�0

Consumer Price Index (All-Urban; Percent Change)1:2021 Budget Assumptions ����������������������������������������������������������� 2�2 1�9 2�3 2�3 2�3 2�3 2�3 2�3 2�3 2�3 2�3 2�32022 Budget Assumptions ����������������������������������������������������������� 1�9 1�3 2�0 2�1 2�2 2�3 2�3 2�3 2�3 2�3 2�3 2�3

Civilian Unemployment Rate (Percent)1:2021 Budget Assumptions ����������������������������������������������������������� 3�9 3�7 3�5 3�6 3�8 4�0 4�0 4�0 4�0 4�0 4�0 4�02022 Budget Assumptions ����������������������������������������������������������� 3�7 8�1 5�5 4�1 3�8 3�8 3�8 3�8 3�8 3�8 3�8 3�8

91-Day Treasury Bill Rate (Percent)2:2021 Budget Assumptions ����������������������������������������������������������� 1�9 2�1 1�4 1�5 1�5 1�6 1�7 2�0 2�2 2�4 2�5 2�52022 Budget Assumptions ����������������������������������������������������������� 2�1 0�4 0�1 0�2 0�4 0�8 1�2 1�5 1�6 1�7 1�8 2�1

10-Year Treasury Note Rate (Percent)2:2021 Budget Assumptions ����������������������������������������������������������� 2�9 2�2 2�0 2�2 2�5 2�7 3�0 3�1 3�1 3�1 3�2 3�22022 Budget Assumptions ����������������������������������������������������������� 2�1 0�9 1�2 1�4 1�7 2�1 2�4 2�6 2�7 2�8 2�8 2�8

1 % Change 4Q2 Calendar Year Average

2. ECONOMIC ASSUMPTIONS AND OVERVIEW 11

(CPI-U) will rise from 1.2 percent in 2020 on a fourth quarter-over-fourth quarter basis to 2.0 percent in 2021 and stabilize at 2.3 percent from 2024 to 2031, a rate consistent with the Federal Open Market Committee’s inflation target for a slightly different inflation measure.

Comparison with Other Forecasts

For perspective on the Administration’s forecast, this section compares it with forecasts prepared around the same time by the CBO, the Federal Open Market Committee of the Federal Reserve (FOMC), and the Blue Chip panel of private-sector forecasters. There are impor-tant differences that should inform such comparisons.

The most important difference between these forecasts is that they make different assumptions about the imple-mentation of the Administration’s proposed policies. As

already noted, the Administration’s forecast assumes im-pacts of Administration policies, including the American Rescue Plan and components of the American Jobs and American Families Plans. In contrast, the CBO forecast assumes no changes to current law and was formulated prior to passage of the American Rescue Plan. It is not clear to what extent FOMC participants and Blue Chip panelists incorporate policy implementation expecta-tions in their respective outlooks. The Blue Chip panel, in particular, comprises a large number of private-sector forecasters, who have different expectations about the enactment of the Administration’s proposed policies and different views about the contribution of those policies to economic growth.

A second difference is that the various forecasts were published on different dates. For example, while the forecast published by the Administration is based on

Table 2–3. COMPARISON OF ECONOMIC ASSUMPTIONS 1

2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031

Real GDP (Year-over-Year):2022 Budget ���������������������������������������������������������������������������� –3�5 5�2 4�3 2�2 1�9 1�8 1�8 1�8 1�9 1�9 2�0 2�0CBO ����������������������������������������������������������������������������������������� –3�4 4�6 2�9 2�2 2�3 2�3 1�9 1�6 1�6 1�6 1�5 1�6Blue Chip 2 ������������������������������������������������������������������������������� 4�9 3�8 2�3 2�4 2�0 2�0 1�9 1�9 1�9 1�9 1�9

Real GDP (Fourth-Quarter-over-Fourth-Quarter):2022 Budget ���������������������������������������������������������������������������� –2�5 5�2 3�2 2�0 1�8 1�8 1�8 1�8 1�9 1�9 2�0 2�0Federal Reserve 3 �������������������������������������������������������������������� –2�4 4�2 3�2 2�4 1�8 1�8 1�8 1�8 1�8 1�8 1�8 1�8

Consumer Price Index (CPI-U) (Fourth-Quarter-over-Fourth-Quarter):2022 Budget ���������������������������������������������������������������������������� 1�3 2�0 2�1 2�2 2�3 2�3 2�3 2�3 2�3 2�3 2�3 2�3CBO ����������������������������������������������������������������������������������������� 1�1 1�9 2�2 2�3 2�3 2�4 2�4 2�5 2�5 2�4 2�4 2�3Blue Chip 2, 4 ���������������������������������������������������������������������������� 2�3 2�1 2�2 2�2 2�2 2�2 2�2 2�2 2�2 2�2 2�2Federal Reserve, PCE 3, 5 ������������������������������������������������������� 1�2 1�8 1�9 2�0 2�0 2�0 2�0 2�0 2�0 2�0 2�0 2�0

Unemployment Rate: (annual averages)2022 Budget ���������������������������������������������������������������������������� 8�1 5�5 4�1 3�8 3�8 3�8 3�8 3�8 3�8 3�8 3�8 3�8CBO ����������������������������������������������������������������������������������������� 8�1 5�7 5�0 4�7 4�4 4�1 3�9 3�9 4�0 4�1 4�3 4�3Blue Chip 2 ������������������������������������������������������������������������������� 5�8 4�7 4�8 4�5 4�3 4�4 4�3 4�3 4�3 4�3 4�3Federal Reserve 3, 6 ����������������������������������������������������������������� 6�7 5�0 4�2 3�7 4�1 4�1 4�1 4�1 4�1 4�1 4�1 4�1

Interest Rates:

91-Day Treasury Bills (discount basis):2022 Budget ���������������������������������������������������������������������������� 0�4 0�1 0�2 0�4 0�8 1�2 1�5 1�6 1�7 1�8 2�1 2�3CBO ����������������������������������������������������������������������������������������� 0�4 0�1 0�1 0�2 0�3 0�6 1�0 1�4 1�6 1�9 2�2 2�3

Blue Chip 2 ������������������������������������������������������������������������������� 0�1 0�2 0�6 0�9 1�1 1�3 1�7 1�7 1�7 1�7 1�7

10-Year Treasury Notes2022 Budget ���������������������������������������������������������������������������� 0�9 1�2 1�4 1�7 2�1 2�4 2�6 2�7 2�8 2�8 2�8 2�8CBO ����������������������������������������������������������������������������������������� 0�9 1�1 1�3 1�5 1�8 2�1 2�5 2�7 3�0 3�2 3�3 3�4Blue Chip 2 ������������������������������������������������������������������������������� 1�2 1�6 1�7 2�0 2�2 2�3 2�5 2�5 2�5 2�5 2�5

Sources: Administration; CBO, The Budget and Economic Outlook: 2021 to 2031, February 2021; October 2020 and February 2021 Blue Chip Economic Indicators, Aspen Publishers, Inc�; Federal Reserve Open Market Committee, December 16, 2020

1 Calendar Year2 2028-2031 are 5 year averages; 2023-2031 values derived from October 2020 report3 Median Projection4 Year-over-Year5 Personal Consumption Expenditures 6 Average rate during 4th quarter

12ANALYTICAL PERSPECTIVES

data available in February, the Blue Chip forecasts are drawn from the February survey for 2021 and 2022 val-ues and from the October 2020 survey for the long-term forecast (2023-2031). These were the latest Blue Chip forecasts available at the time the Administration fi-nalized its forecast. In addition, the FOMC projections were released in mid-March, and the CBO forecast was published in early February based on data available in January. During the months that have elapsed since the Administration’s forecast was finalized, macroeconomic, policy, and pandemic developments have been mostly positive. Consumer spending has outpaced earlier pro-jections, the Congress has passed the American Rescue Plan, and over one hundred million Americans have been vaccinated. These subsequent developments should be considered when comparing the Administration’s forecast with more recent forecasts such as the Blue Chip panel of professional economic forecasters. For example, between February and May of 2021, the Blue Chip panel revised upwards their consensus forecast for 2021 (year-over-year) real GDP growth, from 4.9 percent to 6.6 percent. Likewise, the Blue Chip consensus forecast for the av-erage 2021 unemployment rate was revised downwards from 5.8 to 5.4 percent.

In spite of differences across forecasters, the forecasts are similar in several aspects. All of them project a con-tinued economic recovery and improving labor markets. Interest rates across these various projections are consis-tent with an environment in which the Federal Reserve holds off on raising its policy rate until late 2022 or early 2023. Rates of inflation are also expected to rise but to remain in line with the Federal Reserve’s mandate on low and stable inflation. See Table 2-3 for a comparison.

Real GDP—The Administration forecasts a higher path for real GDP growth than the CBO, a 2.4 percent per year average over the forecast window versus CBO’s 2.2 percent average, though consistent with the 2.4 percent average from Blue Chip. The Administration’s forecast reflects partial effects of the Administration’s proposed policies, while the CBO is required to assume a continu-ation of current law in its forecast. The Administration’s forecast has the same average growth rate over the fore-cast window as the FOMC although the Fed’s forecast assigns more growth in 2021 than the Administration (6.5 percent compared with 5.2 percent) and slightly slower growth over the out-years of the forecast.

Unemployment—On the unemployment rate, the Administration’s expectations are largely aligned with those of the other forecasters. In particular, all forecast-ers expect unemployment to decrease over the forecast window. One minor difference is that the Administration’s forecast for unemployment plateaus at 3.8 percent as compared with 4.0 and 4.1 percent for the other projec-tions. Although slightly lower for 2021 through 2023 than the CBO and Blue Chip, the Administration’s forecast is slightly higher than the Federal Reserve’s forecast during this window.

Interest Rates—The Administration’s 91-day inter-est rate forecast is broadly consistent with the Blue Chip forecast for 2022-2025 and is slightly higher than the

CBO’s forecast. The Administration expects short-term rates to pick up slowly in 2022 and 2023 and rise from 1.2 to 1.6 percent between 2025-2027. The Blue Chip expects a rise from 1.1 to 1.7 percent, and the CBO expects a rise from 0.4 to 1.7 percent over this period. For both short- and long-term rates, all forecasters agree that they will tend to rise modestly over the coming few years.

General Inflation—Assumptions for CPI-U inflation are similar across the Administration, the CBO, and the Blue Chip. The CBO assumes a CPI-U inflation rate of 2.4 percent in the long run, while the Administration and the Blue Chip are not significantly different at 2.3 and 2.2 percent long-run rates. The Federal Reserve does not pre-dict CPI-U but rather PCE inflation. The Federal Reserve expects PCE inflation to reach the Fed’s target of 2.0 per-cent by 2023 and remain stable thereafter. PCE inflation tends to be lower than CPI-U inflation.

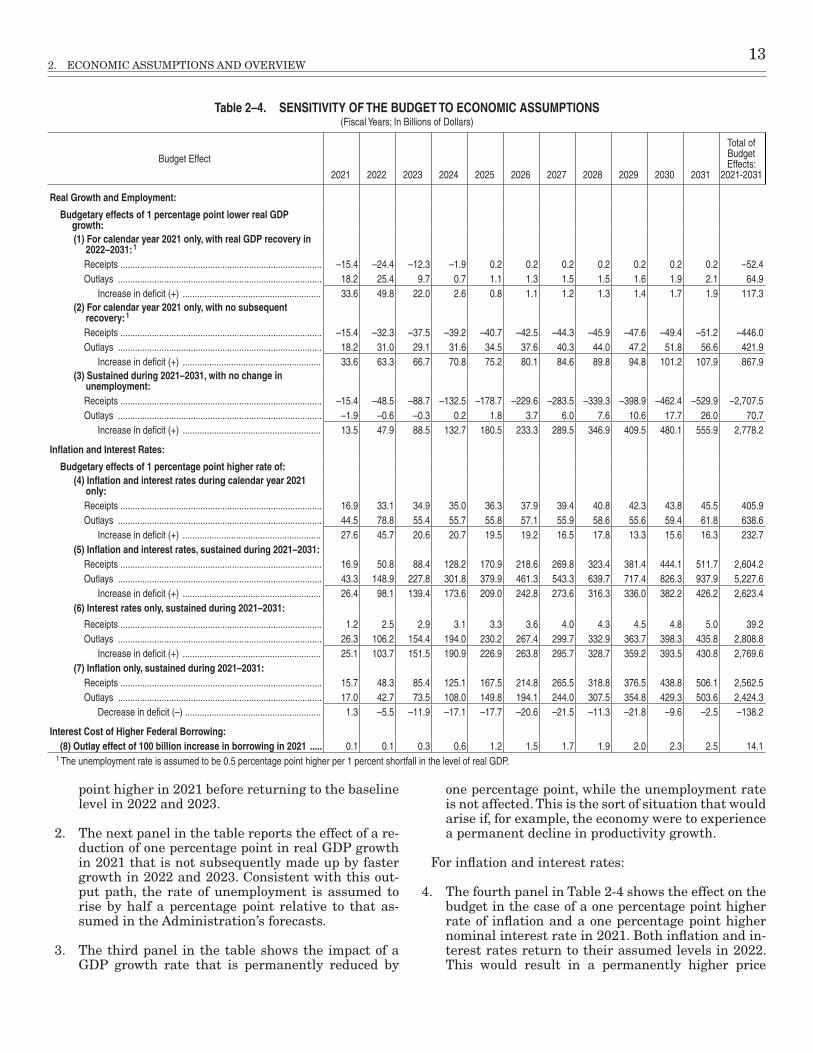

Sensitivity of the Budget to Economic Assumptions

Federal spending and tax collections are heavily in-fluenced by developments in the economy. Income tax receipts are a function of growth in incomes for house-holds and firms. Spending on social assistance programs may rise when the economy enters a downturn, while in-creases in nominal spending on Social Security and other programs are dependent on consumer price inflation. A robust set of projections for macroeconomic variables as-sists in budget planning, but unexpected developments in the economy have ripple effects for Federal spending and receipts. This section seeks to provide an understanding of the magnitude of the effects that unforeseen changes in the economy can have on the budget.

To make these assessments, the Administration relies on a set of heuristics that can predict how certain spending and receipt categories will react to a change in a given subset of macroeconomic variables, holding almost everything else constant. These sensitivity analyses provide a sense of the broad changes one would expect after a given development, but they cannot anticipate how policy makers would react and potentially change course in such an event. For exam-ple, if the economy were to suffer an unexpected recession, tax receipts would decline and spending on programs such as unemployment insurance would rise. In such a situation, however, policy makers might enact policies that stimulate the economy, leading to secondary and tertiary changes that are difficult to predict. Another caveat is that it is often un-realistic to suppose that one macroeconomic variable might change while others would remain constant. Most macro-economic variables interact with each other in complex and subtle ways. These are important considerations to bear in mind when examining Table 2-4.

For real GDP growth and employment:

1. The first panel in the table illustrates the ef-fect on the deficit resulting from a one percentage point reduction in real GDP growth, relative to the Administration’s forecast, in 2021 that is followed by a subsequent recovery in 2022 and 2023. The un-employment rate is assumed to be half a percentage

2. ECONOMIC ASSUMPTIONS AND OVERVIEW 13

point higher in 2021 before returning to the baseline level in 2022 and 2023.

2. The next panel in the table reports the effect of a re-duction of one percentage point in real GDP growth in 2021 that is not subsequently made up by faster growth in 2022 and 2023. Consistent with this out-put path, the rate of unemployment is assumed to rise by half a percentage point relative to that as-sumed in the Administration’s forecasts.

3. The third panel in the table shows the impact of a GDP growth rate that is permanently reduced by

one percentage point, while the unemployment rate is not affected. This is the sort of situation that would arise if, for example, the economy were to experience a permanent decline in productivity growth.

For inflation and interest rates:

4. The fourth panel in Table 2-4 shows the effect on the budget in the case of a one percentage point higher rate of inflation and a one percentage point higher nominal interest rate in 2021. Both inflation and in-terest rates return to their assumed levels in 2022. This would result in a permanently higher price

Table 2–4. SENSITIVITY OF THE BUDGET TO ECONOMIC ASSUMPTIONS (Fiscal Years; In Billions of Dollars)

Budget Effect

2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031

Total of Budget Effects:

2021-2031

Real Growth and Employment:

Budgetary effects of 1 percentage point lower real GDP growth:(1) For calendar year 2021 only, with real GDP recovery in

2022–2031: 1

Receipts ����������������������������������������������������������������������������������� –15�4 –24�4 –12�3 –1�9 0�2 0�2 0�2 0�2 0�2 0�2 0�2 –52�4Outlays ������������������������������������������������������������������������������������ 18�2 25�4 9�7 0�7 1�1 1�3 1�5 1�5 1�6 1�9 2�1 64�9

Increase in deficit (+) ��������������������������������������������������������� 33�6 49�8 22�0 2�6 0�8 1�1 1�2 1�3 1�4 1�7 1�9 117�3(2) For calendar year 2021 only, with no subsequent

recovery: 1

Receipts ����������������������������������������������������������������������������������� –15�4 –32�3 –37�5 –39�2 –40�7 –42�5 –44�3 –45�9 –47�6 –49�4 –51�2 –446�0Outlays ������������������������������������������������������������������������������������ 18�2 31�0 29�1 31�6 34�5 37�6 40�3 44�0 47�2 51�8 56�6 421�9

Increase in deficit (+) ��������������������������������������������������������� 33�6 63�3 66�7 70�8 75�2 80�1 84�6 89�8 94�8 101�2 107�9 867�9(3) Sustained during 2021–2031, with no change in

unemployment:Receipts ����������������������������������������������������������������������������������� –15�4 –48�5 –88�7 –132�5 –178�7 –229�6 –283�5 –339�3 –398�9 –462�4 –529�9 –2,707�5Outlays ������������������������������������������������������������������������������������ –1�9 –0�6 –0�3 0�2 1�8 3�7 6�0 7�6 10�6 17�7 26�0 70�7

Increase in deficit (+) ��������������������������������������������������������� 13�5 47�9 88�5 132�7 180�5 233�3 289�5 346�9 409�5 480�1 555�9 2,778�2

Inflation and Interest Rates:

Budgetary effects of 1 percentage point higher rate of:(4) Inflation and interest rates during calendar year 2021

only:Receipts ����������������������������������������������������������������������������������� 16�9 33�1 34�9 35�0 36�3 37�9 39�4 40�8 42�3 43�8 45�5 405�9Outlays ������������������������������������������������������������������������������������ 44�5 78�8 55�4 55�7 55�8 57�1 55�9 58�6 55�6 59�4 61�8 638�6

Increase in deficit (+) ��������������������������������������������������������� 27�6 45�7 20�6 20�7 19�5 19�2 16�5 17�8 13�3 15�6 16�3 232�7(5) Inflation and interest rates, sustained during 2021–2031:

Receipts ����������������������������������������������������������������������������������� 16�9 50�8 88�4 128�2 170�9 218�6 269�8 323�4 381�4 444�1 511�7 2,604�2Outlays ������������������������������������������������������������������������������������ 43�3 148�9 227�8 301�8 379�9 461�3 543�3 639�7 717�4 826�3 937�9 5,227�6

Increase in deficit (+) ��������������������������������������������������������� 26�4 98�1 139�4 173�6 209�0 242�8 273�6 316�3 336�0 382�2 426�2 2,623�4(6) Interest rates only, sustained during 2021–2031:

Receipts ����������������������������������������������������������������������������������� 1�2 2�5 2�9 3�1 3�3 3�6 4�0 4�3 4�5 4�8 5�0 39�2Outlays ������������������������������������������������������������������������������������ 26�3 106�2 154�4 194�0 230�2 267�4 299�7 332�9 363�7 398�3 435�8 2,808�8

Increase in deficit (+) ��������������������������������������������������������� 25�1 103�7 151�5 190�9 226�9 263�8 295�7 328�7 359�2 393�5 430�8 2,769�6(7) Inflation only, sustained during 2021–2031:

Receipts ����������������������������������������������������������������������������������� 15�7 48�3 85�4 125�1 167�5 214�8 265�5 318�8 376�5 438�8 506�1 2,562�5Outlays ������������������������������������������������������������������������������������ 17�0 42�7 73�5 108�0 149�8 194�1 244�0 307�5 354�8 429�3 503�6 2,424�3

Decrease in deficit (–) �������������������������������������������������������� 1�3 –5�5 –11�9 –17�1 –17�7 –20�6 –21�5 –11�3 –21�8 –9�6 –2�5 –138�2

Interest Cost of Higher Federal Borrowing:(8) Outlay effect of 100 billion increase in borrowing in 2021 ..... 0�1 0�1 0�3 0�6 1�2 1�5 1�7 1�9 2�0 2�3 2�5 14�1

1 The unemployment rate is assumed to be 0�5 percentage point higher per 1 percent shortfall in the level of real GDP�

14ANALYTICAL PERSPECTIVES

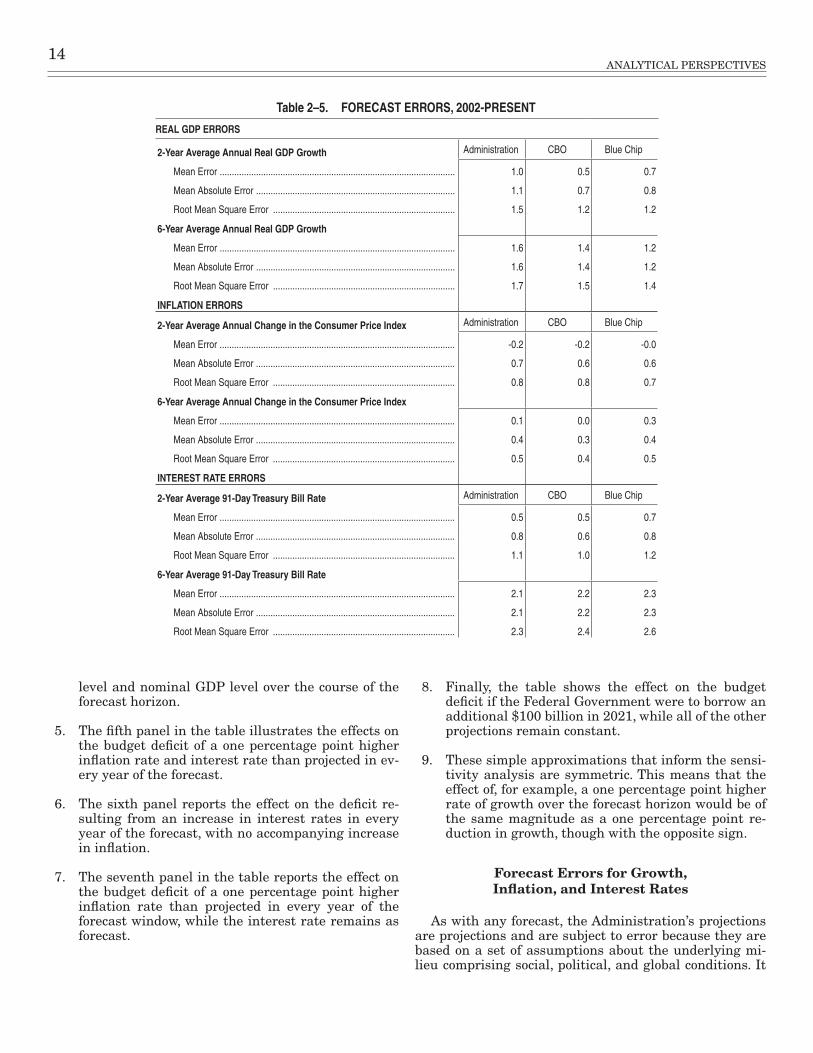

Table 2–5. FORECAST ERRORS, 2002-PRESENT

REAL GDP ERRORS

2-Year Average Annual Real GDP Growth Administration CBO Blue Chip

Mean Error ������������������������������������������������������������������������������������������������� 1�0 0�5 0�7

Mean Absolute Error ���������������������������������������������������������������������������������� 1�1 0�7 0�8

Root Mean Square Error ��������������������������������������������������������������������������� 1�5 1�2 1�2

6-Year Average Annual Real GDP Growth

Mean Error ������������������������������������������������������������������������������������������������� 1�6 1�4 1�2

Mean Absolute Error ���������������������������������������������������������������������������������� 1�6 1�4 1�2

Root Mean Square Error ��������������������������������������������������������������������������� 1�7 1�5 1�4

INFLATION ERRORS

2-Year Average Annual Change in the Consumer Price Index Administration CBO Blue Chip

Mean Error ������������������������������������������������������������������������������������������������� -0�2 -0�2 -0�0

Mean Absolute Error ���������������������������������������������������������������������������������� 0�7 0�6 0�6

Root Mean Square Error ��������������������������������������������������������������������������� 0�8 0�8 0�7

6-Year Average Annual Change in the Consumer Price Index

Mean Error ������������������������������������������������������������������������������������������������� 0�1 0�0 0�3

Mean Absolute Error ���������������������������������������������������������������������������������� 0�4 0�3 0�4

Root Mean Square Error ��������������������������������������������������������������������������� 0�5 0�4 0�5

INTEREST RATE ERRORS

2-Year Average 91-Day Treasury Bill Rate Administration CBO Blue Chip

Mean Error ������������������������������������������������������������������������������������������������� 0�5 0�5 0�7

Mean Absolute Error ���������������������������������������������������������������������������������� 0�8 0�6 0�8

Root Mean Square Error ��������������������������������������������������������������������������� 1�1 1�0 1�2

6-Year Average 91-Day Treasury Bill Rate

Mean Error ������������������������������������������������������������������������������������������������� 2�1 2�2 2�3

Mean Absolute Error ���������������������������������������������������������������������������������� 2�1 2�2 2�3

Root Mean Square Error ��������������������������������������������������������������������������� 2�3 2�4 2�6

level and nominal GDP level over the course of the forecast horizon.

5. The fifth panel in the table illustrates the effects on the budget deficit of a one percentage point higher inflation rate and interest rate than projected in ev-ery year of the forecast.

6. The sixth panel reports the effect on the deficit re-sulting from an increase in interest rates in every year of the forecast, with no accompanying increase in inflation.

7. The seventh panel in the table reports the effect on the budget deficit of a one percentage point higher inflation rate than projected in every year of the forecast window, while the interest rate remains as forecast.

8. Finally, the table shows the effect on the budget deficit if the Federal Government were to borrow an additional $100 billion in 2021, while all of the other projections remain constant.

9. These simple approximations that inform the sensi-tivity analysis are symmetric. This means that the effect of, for example, a one percentage point higher rate of growth over the forecast horizon would be of the same magnitude as a one percentage point re-duction in growth, though with the opposite sign.

Forecast Errors for Growth, Inflation, and Interest Rates

As with any forecast, the Administration’s projections are projections and are subject to error because they are based on a set of assumptions about the underlying mi-lieu comprising social, political, and global conditions. It

2. ECONOMIC ASSUMPTIONS AND OVERVIEW 15

is impossible to foresee every eventuality over a one-year horizon, much less over ten or more years. This section evaluates the historical accuracy of past Administrations’ forecasts for real GDP growth, inflation, and short-term interest rates from 2002 to the present day, especially relative to the accuracy of forecasts produced by the CBO and Blue Chip panel. For this exercise, forecasts produced by all three entities are compared with realized values of these variables.

The results of this exercise are reported in Table 2-5 and contain three different measures of accuracy. The first is the average forecast error. When a forecaster has an average forecast error of zero, it may be said that the forecast has historically been unbiased, in the sense that realized values of the variables have not been systemati-cally above or below the forecasted value. The second is the average absolute value of the forecast error, which of-fers a sense of the magnitude of errors. Even if the past forecast errors average to zero, the errors may have been of a very large magnitude, with both positive and nega-tive values. Finally, the table reports the square root of the mean of squared forecast error (RMSE). This metric applies a harsher penalty to forecasts exhibiting large er-rors. The table reports these measures of accuracy at both the 2-year and the 6-year horizons, thus evaluating the

relative success of different forecasts in the short run and in the medium run.

Past Administrations have forecast 2-year real GDP growth and interest rates that were higher than actu-ally realized, on average, by 1.0 percentage points and 0.5 percentage points, respectively. This is partly due to the assumption that Administration policy proposals contained in the Budget will be enacted, which has not always come to pass. The 2-year average forecast error for inflation is smaller, -0.2 percentage points, and similar to other forecasts.

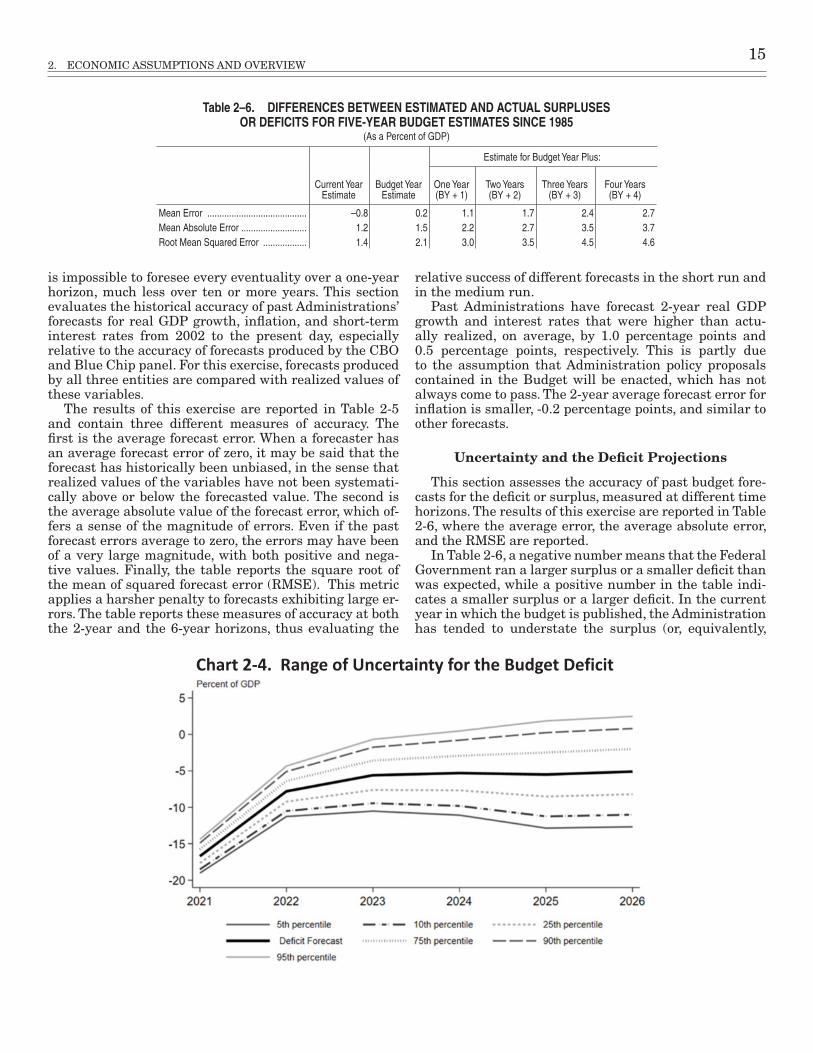

Uncertainty and the Deficit Projections

This section assesses the accuracy of past budget fore-casts for the deficit or surplus, measured at different time horizons. The results of this exercise are reported in Table 2-6, where the average error, the average absolute error, and the RMSE are reported.

In Table 2-6, a negative number means that the Federal Government ran a larger surplus or a smaller deficit than was expected, while a positive number in the table indi-cates a smaller surplus or a larger deficit. In the current year in which the budget is published, the Administration has tended to understate the surplus (or, equivalently,

Table 2–6. DIFFERENCES BETWEEN ESTIMATED AND ACTUAL SURPLUSES OR DEFICITS FOR FIVE-YEAR BUDGET ESTIMATES SINCE 1985

(As a Percent of GDP)

Current Year Estimate

Budget Year Estimate

Estimate for Budget Year Plus:

One Year (BY + 1)

Two Years (BY + 2)

Three Years (BY + 3)

Four Years (BY + 4)

Mean Error ����������������������������������������� –0�8 0�2 1�1 1�7 2�4 2�7Mean Absolute Error ��������������������������� 1�2 1�5 2�2 2�7 3�5 3�7Root Mean Squared Error ������������������ 1�4 2�1 3�0 3�5 4�5 4�6

Chart 2-4. Range of Uncertainty for the Budget Deficit

16ANALYTICAL PERSPECTIVES

overstate the deficit) by an average of 0.8 percent of GDP. For the budget year, however, the historical pattern has been for the budget to understate the deficit by an aver-age of 0.2 percent of GDP.5 One possible reason for this is that past Administrations’ policy proposals have not all been implemented. The forecast errors tend to grow with the time horizon, which is not surprising given that there is much greater uncertainty in the medium run about both the macroeconomic situation and the specific details of policy enactments.

A probabilistic range of outcomes for the deficit over the budget window can be calculated by building off of the historical forecast errors summarized in Table 2-6. This is accomplished by taking the RMSE of previous forecast errors and assuming that these errors are drawn from a

5 Additionally, the CBO has historically forecasted smaller deficits, on average, than actually materialized.

normal distribution. This exercise is undertaken at every forecast horizon from the current year through four years after the budget year. Chart 2-4 displays the projected range of possible deficits. In the chart, the middle line rep-resents the Administration’s expected fiscal balance and represents the 50th percentile outcome. The rest of the lines in the chart may be read in the following fashion. The top line reports the 95th percentile of the distribu-tion of outcomes over 2021 to 2026, meaning that there is a 95 percent probability that the actual balance in those years will be more negative than expressed by the line. Similarly, there is a 95 percent probability that the bal-ance will be more positive than suggested by the bottom line in the chart.

17

3. LONG-TERM BUDGET OUTLOOK

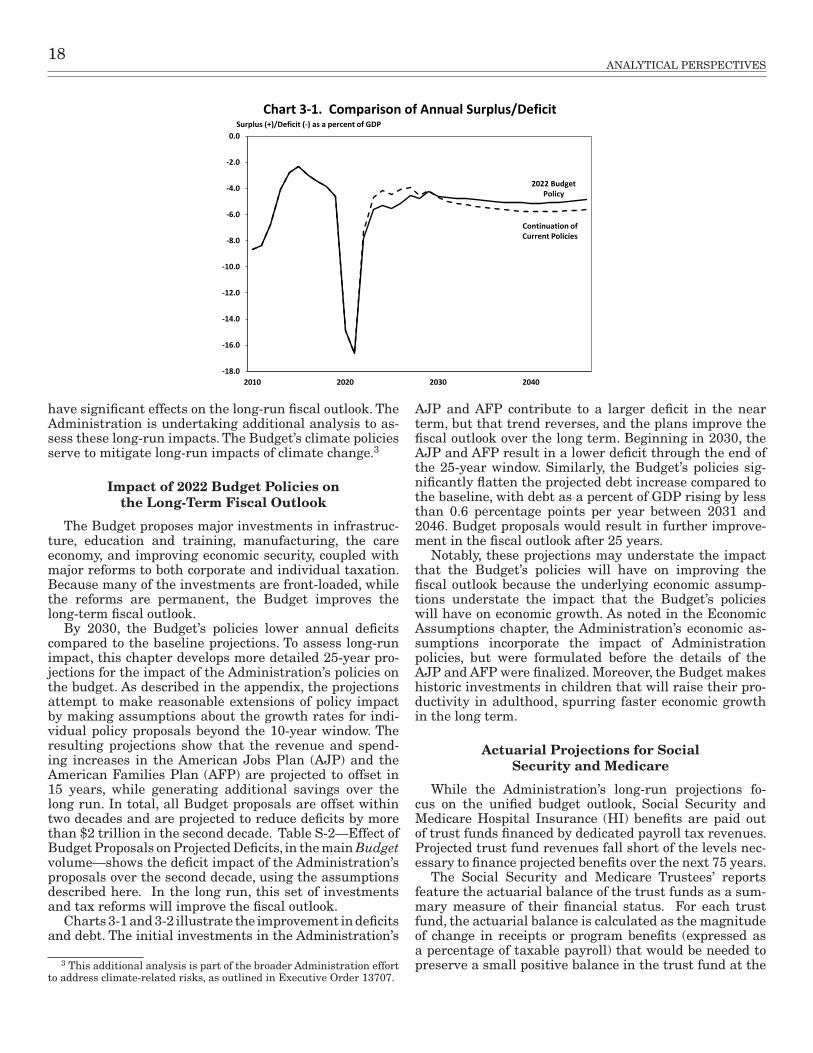

The horizon for most numbers in this Budget is 10 years. This 10-year horizon reflects a balance between the importance of considering both the current and future im-plications of budget decisions made today, and a practical limit on the construction of detailed budget projections for years in the future.

Nonetheless, it can be informative to look further into the future, despite the uncertainty surrounding the as-sumptions needed for such estimates. This chapter begins by discussing the fiscal outlook under current law over the next 25 years. The second section discusses the fiscal impact of the Administration’s policies, finding they will cut deficits and debt over the long run, compared to the baseline. The third section discusses the actuarial projec-tions for Social Security and Medicare. The appendix to this chapter provides further detail on data sources, as-sumptions, and other methods for estimation.

Long-Run Projections under Continuation of Current Policies

The baseline long-term projections assume that current policy continues for Social Security, Medicare, Medicaid, other mandatory programs, and revenues.1 Projections for all mandatory programs and revenues maintain con-sistency with other Federal agency projections. From 2032-2046, total mandatory spending grows by 4.2 per-centage points as a share of GDP (Gross Domestic Product), while revenues increase by 3.8 percent. For discretionary spending, it is less clear how to project a continuation of current policy. After the expiration of the statutory caps in 2021, the Administration’s 10-year baseline assumes that discretionary funding levels generally grow slightly below the rate of CPI (Consumer Price Index) inflation (about 2.2 percent per year). Thereafter, the baseline long-run projections assume that real per-person discretionary funding remains constant, implying an average growth rate of 2.8 percent per year. The appendix provides addi-tional detail on the methodology behind these projections.

The COVID-19 public health and economic crisis and measures taken to address them significantly increased deficits and debt for 2020 and 2021. In the baseline pro-jections (not including proposed policy), the deficit is 14.9 percent of GDP in 2020 and 16.7 percent of GDP in 2021. The deficit is then projected to fall sharply in 2022 and 2023 and then gradually fall to 4.0 percent of GDP in 2027, though it is projected to rise through the end of the

1 The long-run baseline projections are consistent with the Budget’s baseline concept, which is explained in more detail in Chapter 17, “Cur-rent Services Estimates,” in this volume. The projections assume full payment of scheduled Social Security and Medicare benefits without re-gard to the projected depletion of the trust funds for these programs. Ad-ditional baseline assumptions beyond the 10-year window are detailed in the appendix to this chapter.

10-year window and reach 5.0 percent of GDP in 2031. Debt rose to 100.1 percent of GDP in 2020 and is projected to rise to 109.7 percent of GDP in 2022 and 111.2 percent of GDP in 2023 before leveling off to a more gradual as-cent, rising to 112.9 percent of GDP in 2031.

Over the past several decades, interest rates have fall-en even as debt has risen. This has been a widespread, persistent, and global phenomenon, and it has meant that the burden associated with debt has gone down. Under the baseline projections, real net interest payments will remain at or below 0.5 percent of GDP over the 10-year window, below the approximately one percent average over the last four decades and well below the roughly two percent average level in the 1990s.

Beyond the 10-year horizon, deficits continue to rise un-der the baseline projections, reaching 5.8 percent of GDP in 2041 before falling back to 5.7 percent of GDP by the end of the 25-year window. Debt is projected to increase gradually from 112.9 percent of GDP in 2031 to 130.8 per-cent of GDP by 2046, an increase of about 1.2 percentage points per year. Real net interest steadily rises after the 10-year window, but never exceeds 0.7 percent of GDP.