analyzing industry structure

TRANSCRIPT

1

Source: freedigitalphotos.net

2

“If everyone can do it, it’s difficult to create and capture value from it.”

or, alternatively

“In a perfectly competitive market, no

3

In a perfectly competitive market, no firm realizes economic profits (rents).”

Monopoly Rents (Industrial Organization View)

Ricardian Rents(Resource Based View)

Schumpeterian Rents(Dynamic Capabilities View)

P

Q

S

D

S’P

Q

S

D

(Industrial Organization View)

S’P

q1

AC 2

MC 1

q2

AC 1

MC 2

P

q1

AC 2

MC 1

(Resource Based View)

q2

AC 1

MC 2

( y p )

-Barriers to entry-Industry structure matters

-Barriers to imitation-Firm structure matters

-Markets are dynamic-Innovation matters

3

The Industrial Organization Perspective:

Premise that industry structure matters most

Economic rents due to barriers to competition (i l )

P

S

S’

The Industrial Organization Perspective:

(i.e. monopoly rents)

Some industries are more profitable than others

QD

mFo

rtun

e 50

0 20

09, m

oney

.cnn

.com

6

Sour

ce:

4

Bargaining Power of Suppliers

Intensity of Rivalry

Bargaining Power of Buyers

Threat of Entry

Suppliers y

Threat of Substitutes

Buyers

Bargaining Power of Suppliers

Intensity of Rivalry

Bargaining Power of Buyers

Threat of Entry

Suppliers y

Threat of Substitutes

Buyers

5

Entry is less likely when ...

1. Entrant faces high sunk costs

sunk costs are investments that cannot be recovered

2. Incumbents have a competitive advantagepotential entrants are at a competitive disadvantage compared to existing players, simply not profitable to enter

3. Entrant faces retaliation potential entrants are likely to be forced out of business by strategic (pricing) behavior of incumbents

Point: For sunk costs, emphasize non-recoverability (vs. large recoverable capital investment)large recoverable capital investment)Ex: R&D, hotel vs. big boxCounter Example:Leasing airplanes

Slide: Potential BarriersEx: Patents, etc: Taxis, Doctors, LawyersEx: Pioneering Brands: Quicken, Coke & Pepsi,

Foundations of Strategy

Ex: Pioneering Brands: Quicken, Coke & Pepsi, NikeEx: Pre-commitment: SWA in Detroit

6

Entry is less likely when ...

1. Entrant faces high sunk costs

sunk costs are investments that cannot be recovered

2. Incumbents have a competitive advantagepotential entrants are at a competitive disadvantage compared to existing players, simply not profitable to enter

3. Entrant faces retaliation potential entrants are likely to be forced out of business by strategic (pricing) behavior of incumbents

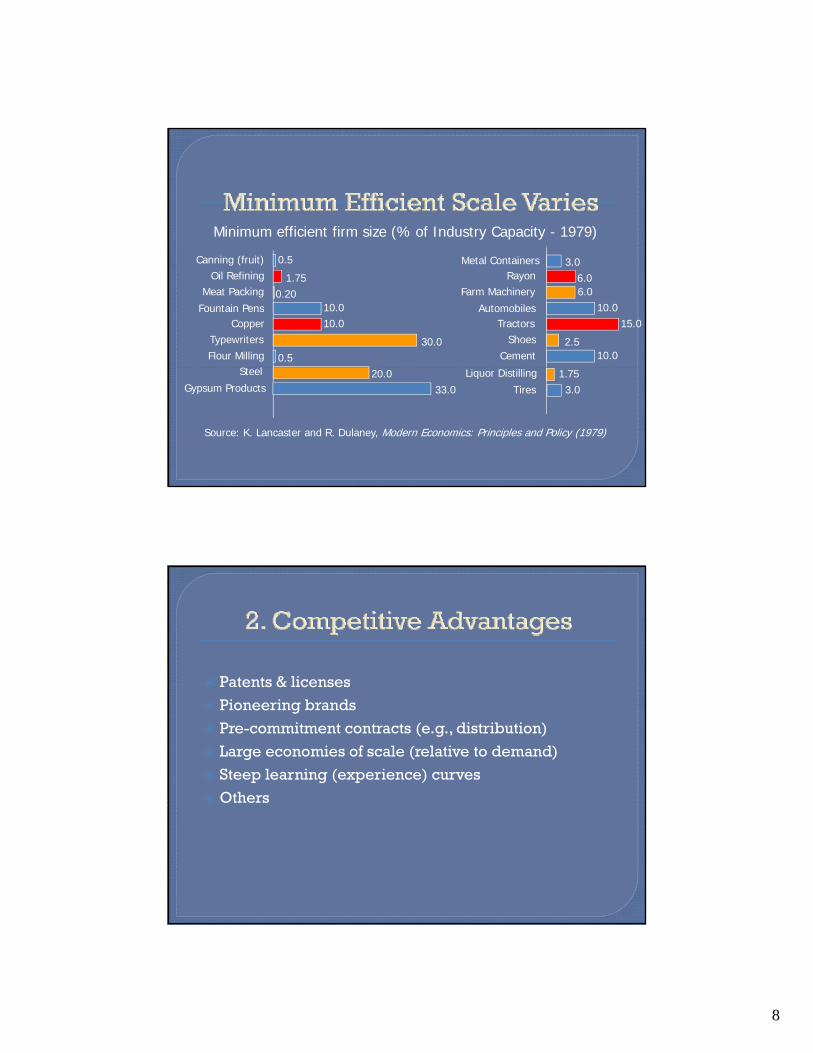

Patents & licensesPatents & licenses

Pioneering brands

Pre-commitment contracts (e.g., distribution)

Large economies of scale (relative to demand)

Steep learning (experience) curves

Others

7

Slide: Economies of scalePoint: C = αqβ : calculate using regression ln C = ln α + β Point: C = αqβ : calculate using regression ln C = ln α + β

ln qPoint: Talk about slope

Slide: MESPoint: Expressed as market share, could change as

market grows

Foundations of Strategy

Slide: Learning curvesPoint: Similar to EOS, could be qualityEx: Far better at working with team by Term 2!

$

AC

OutputMES

8

Minimum efficient firm size (% of Industry Capacity - 1979)

Canning (fruit)Oil Refining

Meat Packing

Fountain PensCopper

TypewritersFlour Milling

Metal Containers0.5

1.750.20

10.010.0

30.00.5

3.06.06.0

10.015.0

2.510.0

RayonFarm Machinery

AutomobilesTractors

ShoesCement

S l Liquor Distilling 1.753.0

20.033.0 Tires

Steel

Gypsum Products

Source: K. Lancaster and R. Dulaney, Modern Economics: Principles and Policy (1979)

Patents & licensesPatents & licenses

Pioneering brands

Pre-commitment contracts (e.g., distribution)

Large economies of scale (relative to demand)

Steep learning (experience) curves

Others

9

Unit cost

Cumulative output over time

10

Entry is less likely when ...

1. Entrant faces high sunk costs

sunk costs are investments that cannot be recovered

2. Incumbents have a competitive advantagepotential entrants are at a competitive disadvantage compared to existing players, simply not profitable to enter

3. Entrant faces retaliation potential entrants are likely to be forced out of business by strategic (pricing) behavior of incumbents

Excess capacity of incumbentsp y

Economies of scale or other cost advantage

Substantial exit costs

• Exit costs are payments that must be made upon exit

• Exit costs provide an incentive to fight

Aggressive reputation of incumbents

• Must be credible

• Suffers from free-riding problem

11

Slide: Likelihood of retaliation (for example, price cutting)Ex: Excess Capacity: airlines during recession Ex: Excess Capacity: airlines during recession,

semiconductor cycles & PC memory prices, fiber optic lines

Ex: EOS: Wal*Mart (war of attrition)Ex: Exit Costs: polluters, pensionsEx: Reputation: Microsoft

(Simpson’s example =

Foundations of Strategy

(Simpson s example CompuGlobalHyperMegaNet)

Bargaining Power of Suppliers

Intensity of Rivalry

Bargaining Power of Buyers

Threat of Entry

Suppliers y

Threat of Substitutes

Buyers

12

Substitute products are less of a threat when ...

1. Cross-price elasticity of demand is low

2. Switching costs are highone-time costs customers incur when switching to a new product or service

Slide: Cross-Price ElasticityEx: Cellular vs landline 10 yrs ago & now; more Ex: Cellular vs. landline, 10 yrs ago & now; more

generally, digital convergenceEx: butter vs. margarine VS gas vs. alternatives

Note: Negative CPE implies complements

Slide: Switching CostsEx: Cellular vs. landline & number portability

Foundations of Strategy

Ex: Cellular vs. landline & number portabilityEx: car rentals vs. public transport

13

The ratio of the % change in demand for one good given a 1% increase in price of another good

P1 P1P1

given a 1% increase in price of another good.

Q2Perfectly /Infinitely

Elastic Demand

Q2Perfectly

Inelastic Demand

Q2

“Moderately” Elastic Demand

The ratio of the % change in demand for one good given a 1% increase in price of another good

P1 P1P1

given a 1% increase in price of another good.

Q2Perfectly /Infinitely

Elastic Demand

Q2Perfectly

Inelastic Demand

Q2

“Moderately” Elastic Demand

14

Substitute products are less of a threat when ...

1. Cross-price elasticity of demand is low

2. Switching costs are highone-time costs customers incur when switching to a new product or service

Bargaining Power of Suppliers

Intensity of Rivalry

Bargaining Power of Buyers

Threat of Entry

Suppliers y

Threat of Substitutes

Buyers

15

Slide: Buyer BP, point 1 (buyers not concentrated) Ex: Counter example McDonald’s & CokeEx: Counter example -- McDonald s & Coke

Slide: Relative Concentration Ex: Monopoly = Wintel

Competitive = PCMonopsony = Hops in mass beerMutual = military aircraft

Foundations of Strategy

Buyers have less power when ...

1. Buyers are not concentrated (no monopsony)• Many potential buyers• Each accounts for a small fraction of sales

2. Buyers have few options• Products are differentiated (low intra-industry CPE)• High switching costs (relationship-specific assets)• Buyer cannot backward integrate

3. Buyers are segmented• Price information is not widely available• Price discrimination possible• Bundling possible

16

Buyer

Many

Few

MonopolyPower

MonopsonyPower

Competitive

MutualDependence

Supplier

ManyFew

Slide: Buyer BP, point 2 (few buyer options) Ex: Differentiation: Coke & PepsiE S i hi M Wi l Ex: Switching costs: Mac vs. Wintel, contract

manufacturersEx: B. Integration: large industrial customers &

electricity

Slide: Buyer BP, point 3 (segmentation)Ex: Information not widely available: Mattress modelsSlide: Price DiscriminationEx: 1st degree: Auto sales, college tuition, auctions

2nd degree: Airlines w/ travel dates

Foundations of Strategy

17

Buyers have less power when ...

1. Buyers are not concentrated (no monopsony)• Many potential buyers• Each accounts for a small fraction of sales

2. Buyers have few options• Products are differentiated (low intra-industry CPE)• High switching costs (relationship-specific assets)• Buyer cannot backward integrate

3. Buyers are segmented• Price information is not widely available• Price discrimination possible• Bundling possible

Buyers have less power when ...

1. Buyers are not concentrated (no monopsony)• Many potential buyers• Each accounts for a small fraction of sales

2. Buyers have few options• Products are differentiated (low intra-industry CPE)• High switching costs (relationship-specific assets)• Buyer cannot backward integrate

3. Buyers are segmented• Price information is not widely available• Price discrimination possible• Bundling possible

18

PP

D

S

Producer Surplus

pc

ConsumerSurplus

Q

D

qc

P i $60Profits = $60M

Price

$20

$40

$60

Profits = $100M

Profits = $60M

Demand (Millions)

1 2 3

Profits = $60M

19

WTP for Product TypeConsumer Type A B C D Total

HR $100 $90 $70 $20 $280

Engineers $60 $120 $70 $70 $290

Sales $100 $80 $140 $60 $380

Consultants $70 $100 $60 $80 $310

Min. WTP for product $60 $80 $60 $20 $220

Bargaining Power of Suppliers

Intensity of Rivalry

Bargaining Power of Buyers

Threat of Entry

Suppliers y

Threat of Substitutes

Buyers

20

Suppliers are less of a threat when ...

1. Sellers are not concentrated (no monopoly)

2. Firms have many alternatives• many substitutes for supplier’s products• firms face low switching costs• supplier cannot forward integrate

3. Sellers may not treat segments differently• price information is widely available• price discrimination not possible

Bargaining Power of Suppliers

Intensity of Rivalry

Bargaining Power of Buyers

Threat of Entry

Suppliers y

Threat of Substitutes

Buyers

21

Note: Big issue is concentration. Economists have long been interested in this issue…

Slid B t d C tSlide: Bertrand vs CournotNote: Both are “one-shot” games with simultaneous

moves

Note: In the end, there is wide variance across industries.Note: Consider duopolies,

Coke vs. Pepsi (favorable)Bud vs. Miller (favorable)B i Ai b ( t ti )Boeing vs. Airbus (contentious)

Note: More useful to think about two broad conditions….

Foundations of Strategy

Slide: Intensity of rivalryNote: Catch 22 -- many of the factor that lower the y

incentives to “fight” also lower barriers to entryEx: Cyclical demand (autos, hotels in college towns,

PCs)

Slide: Value of coordinationPoint: So reduce output, raise priceSlide: Illegal forms of coordination, Crandall exampleA k Wh i OPEC i ?Ask: Why is OPEC not anti-trust?Note: What is allowed is various forms of tacit collusion…

Foundations of Strategy

22

Rivalry is less intense when ...

1. The number of competitors is small !!!!!

2. Incentives to “fight” are low• Substantial market growth (especially if capacity constrained)• Opportunities to differentiate• Low exit costs• Little excess capacity (demand is not cyclical)

3. Coordination is feasible• Explicit price / market fixing (antitrust violation!)

• Tacit coordination (implicitly holding prices high, differentiating)

ACMCACMC

Price Taker Monopolist (or Cartel)

AC

PM

qM

DMR

PC

qC

AC

qM

MCqqPPqqPPMR

MCMR

=∂∂+∂∂+=

=→

*/*/

maxπ

MCPPMR

MCMR

==

=→maxπ

23

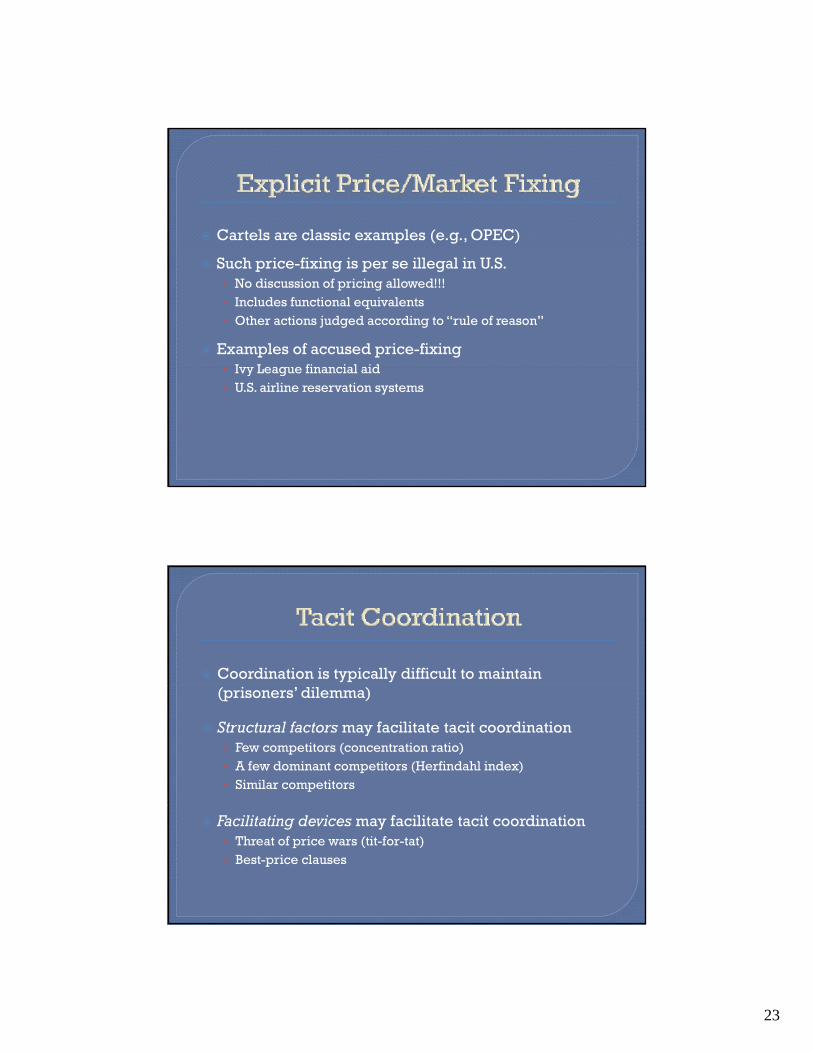

Cartels are classic examples (e.g., OPEC)

Such price-fixing is per se illegal in U.S.• No discussion of pricing allowed!!!• Includes functional equivalents• Other actions judged according to “rule of reason”

Examples of accused price-fixingIvy League financial aid• Ivy League financial aid

• U.S. airline reservation systems

Coordination is typically difficult to maintain (prisoners’ dilemma)

Structural factors may facilitate tacit coordination• Few competitors (concentration ratio)• A few dominant competitors (Herfindahl index)• Similar competitors

Facilitating devices may facilitate tacit coordination • Threat of price wars (tit-for-tat)• Best-price clauses

24

Bargaining Power of Suppliers

Intensity of Rivalry

Bargaining Power of Buyers

Threat of Entry

Suppliers y

Threat of Substitutes

Buyers

Bargaining Power of Suppliers

Intensity of Rivalry

Bargaining Power of Buyers

Threat of Entry

Suppliers

Role of Compliments

y

Threat of Substitutes

Buyers

Role of Institutions

25

Complements are products for which a decrease in price will increase demand for the target product (i.e., p g p ( ,negative cross-price elasticity)Examples: computers and software, VCRs and video tapes, bread and butter (?), guns and bullets

Important issues:• Who controls complementary products?• Who has bargaining power firms in the industry • Who has bargaining power, firms in the industry

or providers of complementary products?

Institutions set “the rules of the game”• Antitrust law and enforcement• Legal barriers to entry, trade (“natural”

monopolies)• Policymaking institutions (policy stability)• Institutions may be influenced by players

26

Raise switching costs (e.g., frequent flyer programs)Differentiate (e.g., Swatch watches)Coordinate – tacitly of course (e.g., best-price clauses)Consolidate (e.g., telecoms industry)Integrate – vertically, that is (e.g., M&A in media)Innovate (e.g., CFCs to HCFCs)Certify / Lobby (e.g., lawyers, doctors)y y ( g , y , )

A key task in a strategic analysis is to identify and dd h i i f h li i i address the competitive forces that limit economic

rents:

• Entry is less likely when incumbent firms have a competitive advantage and can credibly retaliate against new entrants.

• Substitution is less likely when switching costs are high and cross-price elasticity is low.

• Buyer and supplier power depend on relative concentration, the viability of alternatives, and information availability.

• Rivalry is more intense when incentives to fight are large and tacit coordination is difficult.

52