anglo coal - angloamerican.com/media/files/a/anglo-american-plc-v... · from 1999 to 2004 2004...

TRANSCRIPT

1

Presentation to Analysts: June 2005 1

Anglo CoalPresentation to Analysts

June 2005

2

Presentation to Analysts: June 2005 2

Agenda and Participants► Anglo Coal Overview

Ken Bell SVP International Business Development

► Anglo Coal Australia OverviewEric Ford CEO Anglo Coal Australia

► Dawson OverviewMike O’Brien GM Dawson

Rod Elliott GM Marketing and Transportation

3

Presentation to Analysts: June 2005 3

Overview of Anglo CoalKen Bell

4

Presentation to Analysts: June 2005 4

Overview of Anglo Coal ► Operations in:

• South Africa: 9 mines• Australia: 6 mines

1 equity mine• Colombia: 1 mine• Venezuela: 1 mine

► Long life mines► Good quality reserves ► Exposure to export and domestic thermal

coal market and export metallurgical coal market

► Contributed 13% to AA plc's 2004 headline earnings

► Generated US$1.8 billion in free cash from 1999 to 2004

2004 Saleable Tonnes (Mt) By Region

5526

10

South AfricaAustraliaSouth America

5

Presentation to Analysts: June 2005 5

Anglo Coal Location Map

Beijing

Representative Office

LondonMarketing Office

ColombiaExport Export Domestic

Met ThermalCerrejon X

8 Mt3983

US$185 m

Attributable Production (2004)EmployeesAttributable EBITA (2004)

Mine

VenezuelaExport Export Domestic

Met ThermalCdG X X

2 Mt1059

US$20 m

Attributable Production (2004)EmployeesAttributable EBITDA (2004)

Mine

AustraliaExport Export Domestic

Met ThermalGerman Creek XMoranbah North XJellinbah X XDawson X XDartbrook X XDrayton X XCallide X

26 Mt2120

US$184m

Attributable Production (2004)EmployeesAttributable EBITDA (2004)

Mine

South AfricaExport Export Domestic

Met ThermalGoedehoop X XKleinkopje X X XBank X X XGreenside X XLandau X XIsibonelo XKriel XMafube XNew Denmark XNew Vaal X

55 MT7275

US$297m

Attributable Production (2004)EmployeesAttributable EBITDA (2004)

Mine

6

Presentation to Analysts: June 2005 6

Anglo Coal’s Market Share

5%

5%

24%

10%4%

52%

Anglo CoalXstrataBHPB (includes Mitsubishi)Canada (Fording & Teck)Rio TintoOthers

Anglo Coal has a competitive share in both markets

SOURCE: PUBLICLY AVAILABLE DATA & ANGLO COAL ANALYSIS

6%

7%

7%

7%

4%

69%

Anglo Coal Xstrata BHPBPT Bumi Rio Tinto Others

Export Thermal Coal Export Metallurgical Coal

7

Presentation to Analysts: June 2005 7

Anglo Coal’s Product Portfolio and Customer Destination

37

18

10

710

8

South African DomesticSouth African Thermal ExportsAustralian DomesticAustralian Thermal ExportsAustralian Metallurgical ExportsSouth American Exports

52%

31%

17%

Domestic MarketMed-Atlantic Market

Indo-Pacific Market

2004 Actual Saleable CoalBy Product Million Tonnes

2004 Actual Product Destination90 Million Tonnes

8

Presentation to Analysts: June 2005 8

0

20

40

60

80

100

120

140

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

US$/T FOBExport Hard Coking Coal (Goonyella Benchmark)

Export Thermal Coal (Japan/Newcastle Benchmarkbasis 6322 GAR)

Coal Price History & Projection

9

Presentation to Analysts: June 2005 9

Key Financials 2003 Vs. 2004

► Revenue up 29% to US$2.4 bn

► Operating Profit up 46% to US$487m

► Headline Earnings up 51% to US$351m

► Free Cash Flow up 38% to US$445m

► Total Free Cash of US$1.8 bn generated from 1999 to 2004

Solid Results

10

Presentation to Analysts: June 2005 10

EBITDA

Good EBITDA Returns

0100200300400500600700800

2002 2003 20040%5%10%15%20%25%30%35%40%

South Africa Australia South America EBITDA Margin

Significant growth in EBITDA - CAGR 33% since 1999

Average EBITDA margin ~ 30% (1999 to 2004)US$m

11

Presentation to Analysts: June 2005 11

2004 Regional ResultsRevenue (US$m)

1109

433

840

EBITDA (US$m)

297205

184

South Africa Australia South America

Operating Profit (US$m)

244164

79

Headline Earnings (US$m)

162116

73

Capex (US$m)*

137

4581

*Annual Financial Statements exclude Anglo Coal’s share of Associates’

Net Operating Assets (US$m)*

1634

398923

12

Presentation to Analysts: June 2005 12

Outlook 2005

► Anticipate sound operating performance across operations in all regions

► Higher costs•Inflationary pressures continue across

all regions•Weaker US Dollar impacting on South

African Rand and Australian Dollar► Higher average realised prices versus 2004

Anglo Coal has sold significant amount of 2005 tonnage at current high prices

13

Presentation to Analysts: June 2005 13

Project Pipeline

Cerrejon Expansion

China

Russia

Mafube

WesternComplex

Isibonelo LakeLindsay Moranbah

South

Dawson

Grasstree

Saddlers Creek

GrosvenorMonash Energy

14

Presentation to Analysts: June 2005 14

New Business Development

► Coal Bed/Mine Methane• Dawson (Australia)• Waterberg (South Africa)• German Creek (Australia)

► Monash Energy • Power and low sulphur diesel• Carbon capture & storage • Government support

► Coal Gasification• China – Xiwan• Chemical and Power• Emissions reduction

Long lead timeHigh capitalNew skills

Potential high returns

15

Presentation to Analysts: June 2005 15

In Conclusion..

► Significant earnings and cash flow contributor to AA plc

► Exposed to domestic and export coal markets► Good quality long life reserves► Diversified geographical base► Proven track record for operating in existing

and new geographies► Good growth opportunities within existing

operations► Continue to optimise existing operations and

develop new assets and business initiatives

16

Presentation to Analysts: June 2005 16

Overview of Anglo Coal Australia

Eric Ford

17

Presentation to Analysts: June 2005 17

Anglo Coal in Australia

Long LifeQualityReservesGrowthStrategy

18

Presentation to Analysts: June 2005 18

2004 Sales by Coal Type

10.1

10.414.5

Domestic Thermal Coal Export Thermal CoalExport Metallurgical Coal

35 Million Tonnes

19

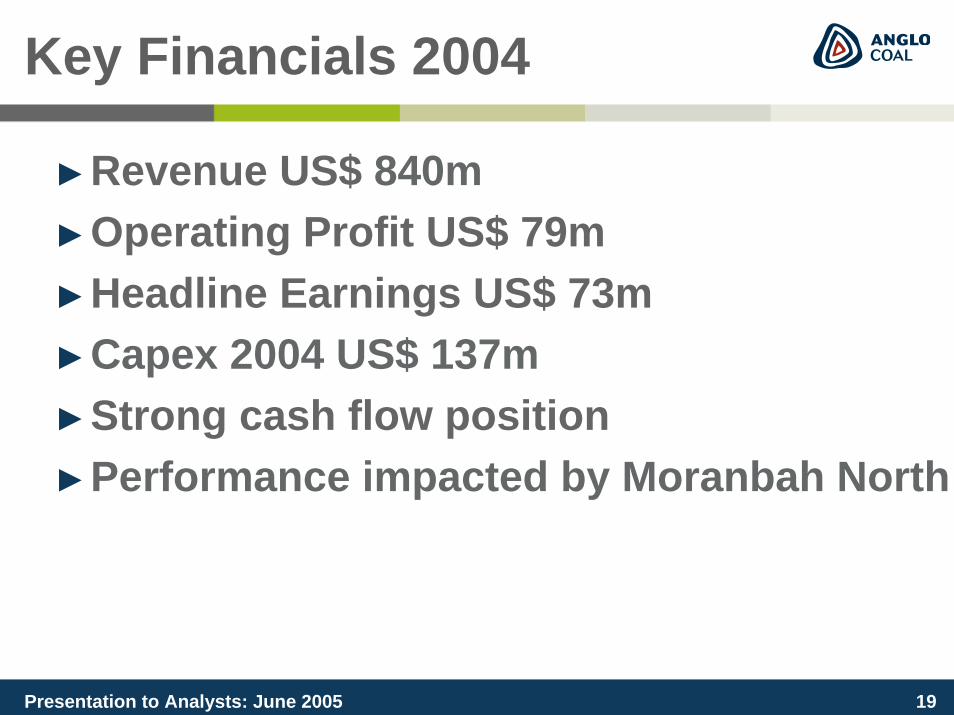

Presentation to Analysts: June 2005 19

Key Financials 2004

►Revenue US$ 840m►Operating Profit US$ 79m►Headline Earnings US$ 73m ►Capex 2004 US$ 137m►Strong cash flow position►Performance impacted by Moranbah North

20

Presentation to Analysts: June 2005 20

Coal Sales Projection

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

2004 2005 2006 2007 2008 2009Domestic E xport ThermalE xport Metallurgical E xpansions (inc luding Dawson)

Anglo Share Of Coal Sales (Mtpa)

21

Presentation to Analysts: June 2005 21

Projects

► Significant growth ahead:•Brownfield

•Grasstree•Dawson•Coal Seam Methane

•Greenfield•Lake Lindsay•Moranbah South•Grosvenor •Saddlers Creek•Monash Energy

22

Presentation to Analysts: June 2005 22

Outlook 2005

►Metallurgical►Export Thermal►Domestic Thermal►Coal Seam Methane►Skills►Materials►Contractors►Legislation

23

Presentation to Analysts: June 2005 23

Conclusion

►Strong global environment

►Good expansion projects

►Operational excellence

►M & A opportunities

24

Presentation to Analysts: June 2005 24

Dawson Overview

Mike O’Brien

25

Presentation to Analysts: June 2005 25

Dawson Location

26

Presentation to Analysts: June 2005 26

Historic Slide

0

200

400

600

800

1,000

1,200

1,400

62 63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04

Number of Employees

0

1

2

3

4

5

6

7

8

Sales Million's Tonnes

Thiess Peabody Mitsui Coal formed BHP acquires 58% BHP acquires further 22%Peabody / Mitsui JV CNA /

Mitsui JV

Anglo / Mitsui JV

Underground Mining ceasesAug 94

Annual Tonnes

Employees

Rail line to Gladstone

DL4BE 1370

DL5Marion8200

DL6Marion8200

Highw all Mining

27

Presentation to Analysts: June 2005 27

Reserves

0

50,000,000

100,000,000

150,000,000

200,000,000

250,000,000

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

Proven Probable Other250

200

150

100

50

0

Payback: April 2011

Mt

28

Presentation to Analysts: June 2005 28

Coal Rank

► Well understood rank trend dictates coal quality and products

► Rank reduces from ~ 1.6 in north to 0.7 in south

► Ranges from: ► sub-anthracite in north► hard coking in the

centre ► to thermal in the south

29

Presentation to Analysts: June 2005 29

Dawson Pit 68

30

Presentation to Analysts: June 2005 30

Dawson Pit 68

31

Presentation to Analysts: June 2005 31

Capital Expenditure

► Total capital expenditure is US$653m• US$225m mining equipment• US$294m conveyors,coal handling and

preparation infrastructure• US$134m Infrastructure and land

► Agreements for the provision of port and rail infrastructure in place

32

Presentation to Analysts: June 2005 32

Operating Costs

► The expansion and recapitalisation of Dawson will deliver improvements in unit operating costs of 15%

► This is achieved through a combination of economies of scale, improved mining schedules, and the use of larger more efficient equipment

33

Presentation to Analysts: June 2005 33

Seam Gas

Moura is currently contracted to produce 6.5 PJ per annum (approximately 5% of the Queensland market)

The extraction and sale of seam gas may provide future carbon credits

Overburden

C Seam

D Seam

D Lower Seam

A Seam

(approx 800m in coal)

Source: Geogas Systems

34

Presentation to Analysts: June 2005 34

Environment and Community

► Strong community support► Agreements with traditional owners► Special Act Lease complies with

mainstream environmental management practices

► New mining plan addresses historically approved rehabilitation liability

► ISO14001 and AS4801 compliant► Nature refuge ‘Willawa’ established

35

Presentation to Analysts: June 2005 35

Dawson Overview

Rod Elliott

36

Presentation to Analysts: June 2005 36

► Metallurgical Coal• Moura C• Dawson HV• Dawson LV

• Moura ‘K’• Soft coking

► Thermal• Moura

Coal Brands

Prime Coking

Soft Coking

Thermal

37

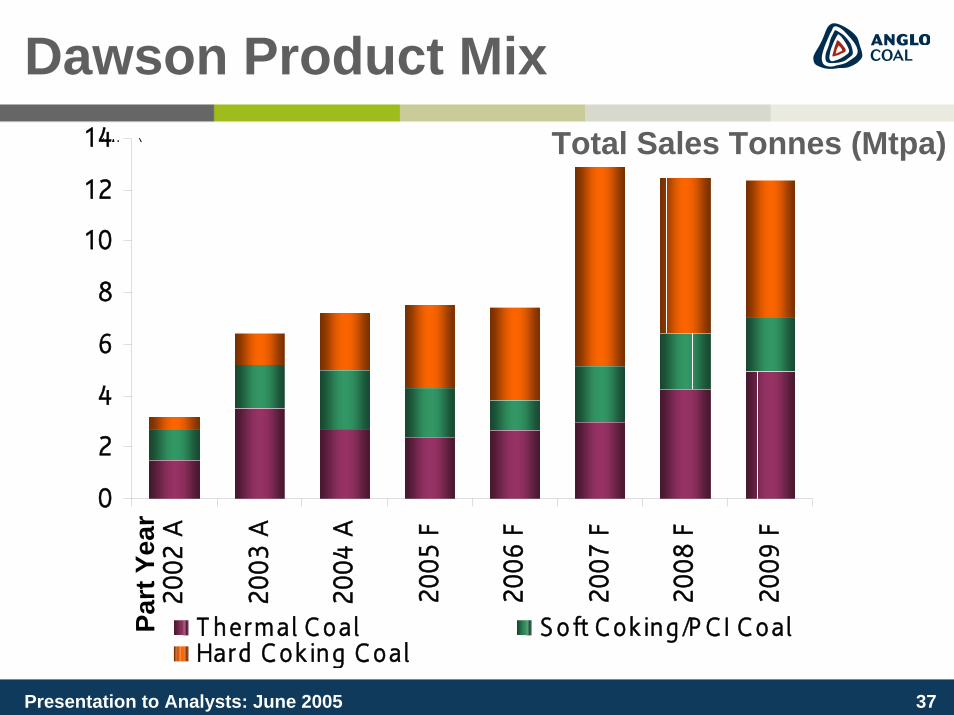

Presentation to Analysts: June 2005 37

Dawson Product MixTotal Sales Tonnes (Mtpa)

0

2

4

6

8

10

12

1420

02 A

2003

A

2004

A

2005

F

2006

F

2007

F

2008

F

2009

F

T hermal Coal Soft Cok ing /P C I CoalHard Cok ing Coal

(Mtpa)Pa

rt Y

ear

38

Presentation to Analysts: June 2005 38

Marketing Strategy

► Established brands and market presence► Term contracts covering thermal and

metallurgical coal► Strong portfolio of buyers:

• Asian thermal coal focus• Diversified metallurgical coal sales strategy

► Reliable infrastructure:• Queensland Rail• Port of Gladstone

► Anglo and Mitsui global marketing strength

39

Presentation to Analysts: June 2005 39

Dawson

40

Presentation to Analysts: June 2005 40

Questions & Answers