announcement 09-34 respa-gfe-hud - mimutualhome.michiganmutual.com/forms/announcements/announcement...

TRANSCRIPT

1

ANNOUNCEMENT………………………#09-34, December 29, 2009 To: All Michigan Mutual Brokers Re: RESPA Changes to the Good Faith Estimate and HUD-1

RESPA Changes to Good Faith Estimate and HUD-1 Table of Contents Important Updates on the Good Faith Estimate .................................................................. 1 Changed Circumstances ...................................................................................................... 1 Fee Disclosure & Accuracy ................................................................................................ 2 Fee Tolerances .................................................................................................................... 3

Important Updates on the Good Faith Estimate/HUD-1

RESPA Reg. X mandates significant changes to the mortgage loan disclosure process. Michigan Mutual, Inc. (MMI) will require all Mortgage Brokers to be in full compliance with the changes effective January 1, 2010. The following updates highlight new requirements for Mortgage Brokers pertaining to the Good Faith Estimate.

All loans with an application taken on or after January 1, 2010, must contain the new GFE form, at time of application and the HUD-1 at closing.

Note: Michigan Mutual, Inc. will not fund any loans if the new HUD-1 or HUD-1A was not used; these loans cannot be cured.

Mortgage Brokers are responsible for providing the initial GFE and Settlement Service Provider (SSP) list to the borrower within three business days of completing their application. Both documents must be included with initial submission to MMI.

The GFE must be accurate as the Mortgage Broker will be held to the fees disclosed on the initial GFE.

The initial GFE is a binding GFE, subject to any changed circumstances. Please refer to the next section for additional information on “changed circumstances.”

After the borrower has received the initial GFE and SSP, the Mortgage Broker is responsible for obtaining and documenting the borrower’s expressed intent to proceed with the transaction. The Intent to Proceed acknowledgment form must be included with initial submission.

Changed Circumstances

The Mortgage Broker must issue a re-disclosed GFE and SSP list to the borrower within the required time frame of three business days of the Broker receiving the changed circumstance information.

NOTE: MMI requires immediate submission of all redisclosed GFE’s and accompanied Changed Circumstance form. (updated 3/18/10)

2

If a changed circumstance occurs, only those fees affected by the changed circumstance may change.

If the estimates within the GFE are inaccurate and a valid changed circumstance does not occur, the Mortgage Broker is bound to the amounts shown on the most recent disclosed GFE.

If a changed circumstance occurs, the Mortgage Broker must re-disclose within three business days after receipt of the information regarding the changed circumstance or the ability to re-disclose (and increase a fee) is lost.

Mortgage Brokers must retain documentation relating to the changed circumstance and fee change, if re-disclosed, for three years.

A “changed circumstance” is defined as follows:

Acts of God, war or disaster

Changes or inaccuracies in information relating to the borrower or the transaction that was relied upon in providing the GFE

Changes to the loan amount or estimated value of the property

New information regarding the borrower or transaction not relied upon when the initial disclosure was provided

A revised GFE must be issued upon a lock event (locking the rate or expiration of the lock) and may be issued in the event the borrower requests a change in the mortgage loan that was identified in the GFE and that changes the settlement charges or terms of the loan.

Please Note: changes in YSP cannot affect Origination charges in Box 1 of GFE. Changes in YSP will impact (+/-) Box 2 and A (Your Adjusted Origination Charge).

Fee Disclosure & Accuracy

The accuracy of initial GFE is critical.

The following applies to wholesale transactions:

All broker origination fees, including broker compensation, disclosed on the GFE should match those fees listed on the Mortgage Broker Fee Agreement (MBFA) form.

Under no circumstances can the broker compensation disclosed in Box 1 (“Our Origination Charge”) increase from the amount disclosed on the initial GFE. Please Note: Box 1 to include MMI’s underwriting fee of $775 and the actual 4506T processing fee (see MMI’s website for a detailed 4506T processing fee schedule).

It is essential that the MBFA and the GFE align throughout the loan process and at loan closing.

o Brokers are responsible for ensuring that the MBFA is kept current with the GFE should any changed circumstance occur that impacts the fees on the MBFA.

o Broker compensation disclosed in Box 2 (“Your Credit or Charge for the Specific Interest Rate Chosen”) on the GFE can only increase if the Loan Program or Product changes; the Rate changes as the result of a lock or re-lock; or if the borrower requests changes to the loan amount or terms.

3

o With the RESPA amendments, the MBFA is critical as the new GFE does not provide a breakdown of broker fees and compensation. The MBFA supplements the GFE – and it will help ensure the borrower can clearly determine broker fees and compensation.

The following applies to all transactions:

For all services where the borrower may select the provider, Mortgage Brokers must provide borrowers with a list of Settlement Service Providers (SSP) in the borrowers’ geographic area along with the costs for the services. At least one vendor for each potential service must be provided.

Fee Tolerances

Page 3 of the HUD-1 will reflect a reconciliation between the settlement charges disclosed on the GFE and the actual charges reflected on pages 1 & 2 of the HUD-1. All charges and fees will be subject to the tolerances defined below.

1. Charges that cannot increase at settlement (ZERO tolerance):

Origination Charges shown in Box 1 on GFE

Credit or charges for the specific interest rate selected (Box 2 on GFE).

Adjusted origination charges (after the interest rate is locked), reflected in Box A on GFE.

Transfer taxes shown in Box 8 on GFE

2. Charges that cannot increase in the aggregate by more than 10% at settlement:

Required settlement services that the lender selects, such as appraisal services

Title services and lender’s title insurance (if selected by lender or if the borrower uses a company identified on the Settlement Services Provider List)

Owner’s title insurance (if the borrower uses a company identified on the Settlement Services Provider List).

Required settlement services (such as Pest Inspections) that the borrower selects from the Settlement Services Provider List

Government recording charges

3. Charges that can increase at settlement (not subject to limitation):

Required settlement services that the borrower can select, if the borrower selects a service provider not listed on the Settlement Services Provider List

Title services and lender’s title insurance, if the borrower selects a service provider not listed on the Settlement Services Provider List

Owner’s title insurance, if the borrower selects a service provider not listed on the Settlement Services Provider List

Initial deposit for borrower escrow account

Daily interest charges

4

Homeowner’s insurance

Please note: For 1 and 2 above, should a changed circumstance occur that directly impacts the fee effected by the change circumstance and a revised GFE be provided within three business days after receipt of the information regarding the changed circumstance, the tolerance is determined by reference to the fees disclosed on the most recent GFE as compared to the fees at closing. Only fees directly impacted by the change circumstance can be added and/or increased and re-disclosed.

Please contact your account executive should you have any questions.

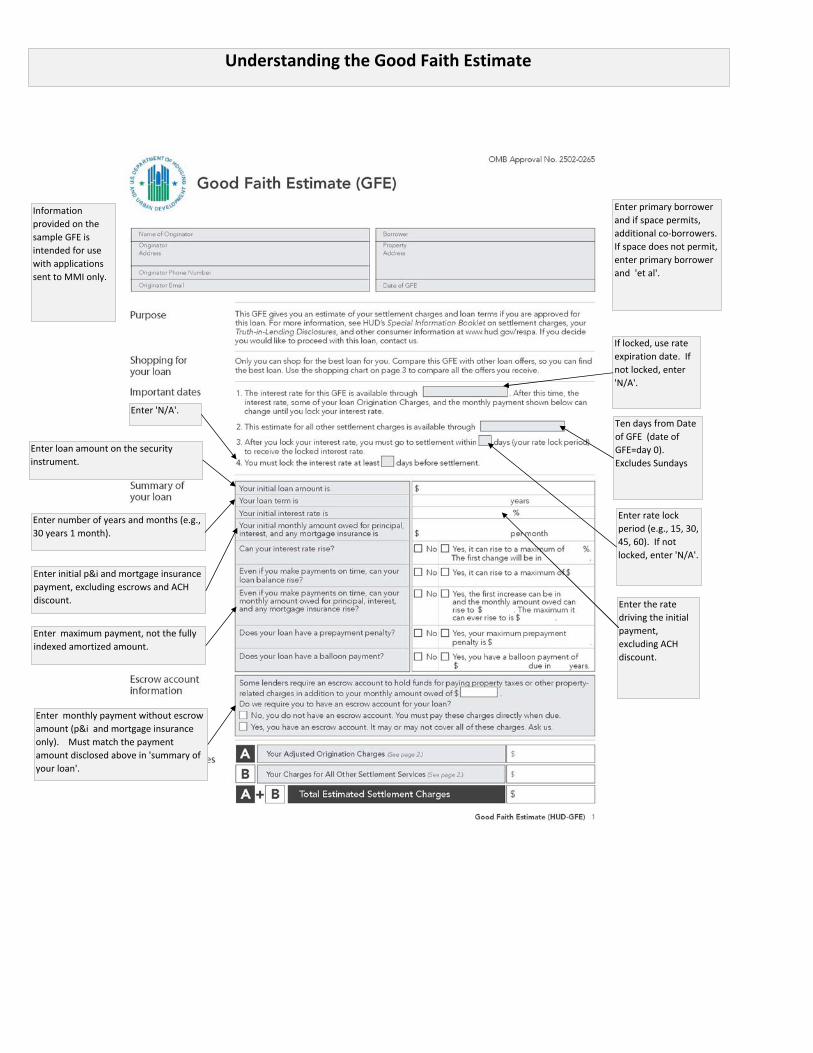

Information provided on the sample GFE is intended for use with applications sent to MMI only.

Enter primary borrower and if space permits, additional co‐borrowers. If space does not permit, enter primary borrower and 'et al'.

Enter 'N/A'.

Enter loan amount on the security instrument.

Enter number of years and months (e.g., 30 years 1 month).

Enter initial p&i and mortgage insurance payment, excluding escrows and ACH discount.

Enter maximum payment, not the fully indexed amortized amount.

Enter monthly payment without escrow amount (p&i and mortgage insurance only). Must match the payment amount disclosed above in 'summary of your loan'.

If locked, use rate expiration date. If not locked, enter 'N/A'.

Ten days from Date of GFE (date of GFE=day 0). Excludes Sundays

Enter rate lock period (e.g., 15, 30, 45, 60). If not locked, enter 'N/A'.

Enter the rate driving the initial payment, excluding ACH discount.

Understanding the Good Faith Estimate

Check only one box. There cannot be both a credit and a charge in the same transaction.

Par pricing.

Over par pricing, such as YSP.

Under par pricing, such as discount points used to buy down the rate.

Enter the service, not the name of the service provider.

Enter fees, if charged by the title company, related to the settlement.

Enter the service, not the name of the service provider.

Enter 0 if no fees are charged.

The total of all fees paid to BOTH the lender & broker, including YSP, but excluding discount points used to buy down the rate.

Total of sections 1 and 2.

This is required to be disclosed on all purchase transactions, regardless of intent to purchase.

If the transaction includes an ownership of property transfer between parties, enter the charge for transfer tax. Charge cannot be added later or be increased absent a Changed Circumstance.

Enter insurance to be purchased at or before settlement.

If no escrows, enter '0' in the fee column.

Understanding the Good Faith Estimate

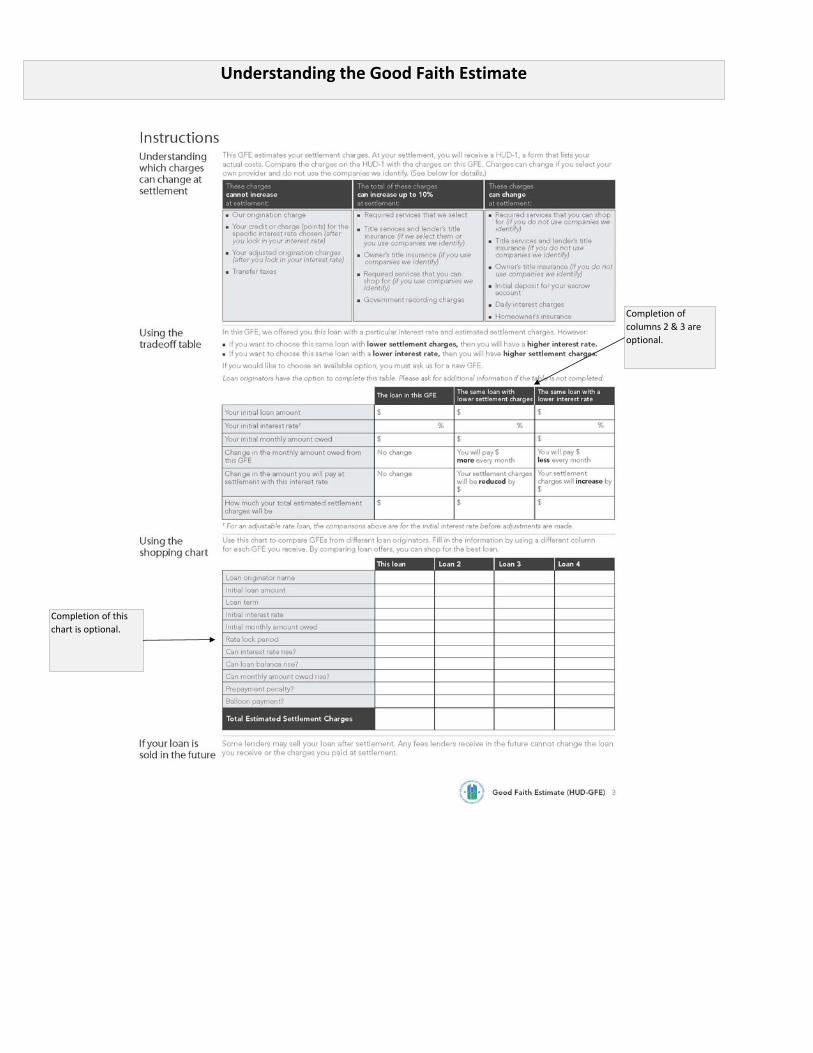

Completion of columns 2 & 3 are optional.

Completion of this chart is optional.

Understanding the Good Faith Estimate

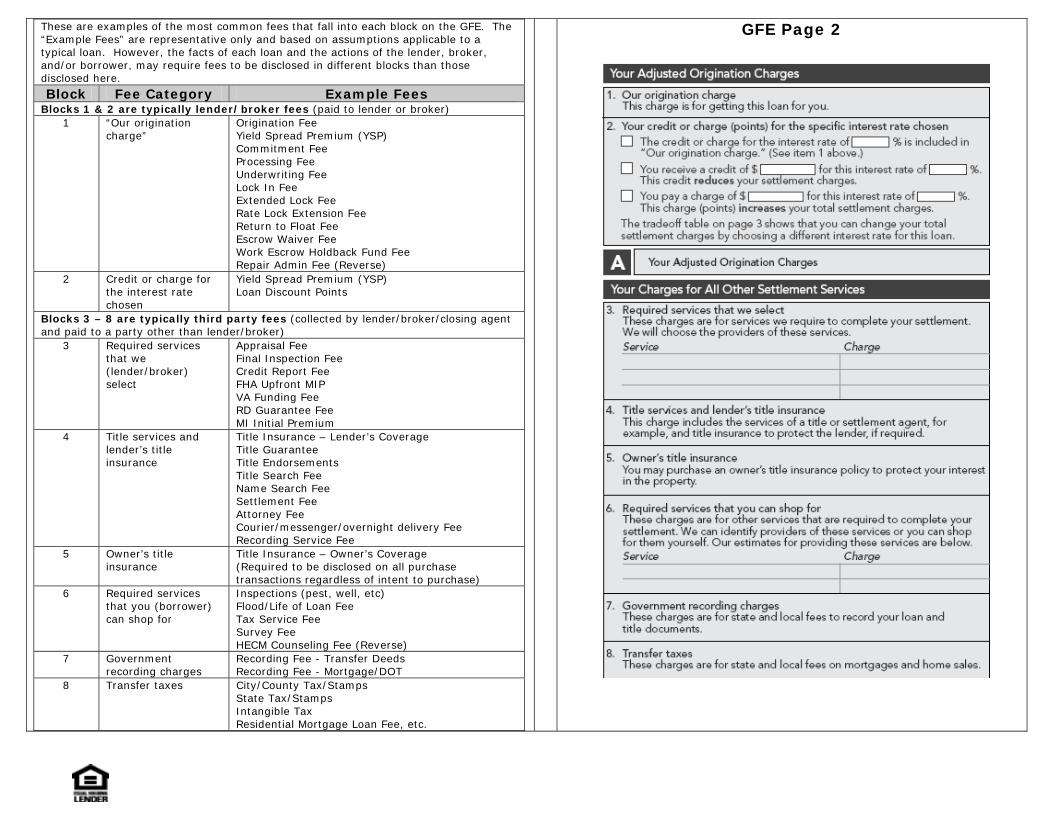

These are examples of the most common fees that fall into each block on the GFE. The “Example Fees” are representative only and based on assumptions applicable to a typical loan. However, the facts of each loan and the actions of the lender, broker, and/or borrower, may require fees to be disclosed in different blocks than those disclosed here. Block Fee Category Example Fees

Blocks 1 & 2 are typically lender/broker fees (paid to lender or broker) 1 “Our origination

charge” Origination Fee Yield Spread Premium (YSP) Commitment Fee Processing Fee Underwriting Fee Lock In Fee Extended Lock Fee Rate Lock Extension Fee Return to Float Fee Escrow Waiver Fee Work Escrow Holdback Fund Fee Repair Admin Fee (Reverse)

2 Credit or charge for the interest rate chosen

Yield Spread Premium (YSP) Loan Discount Points

Blocks 3 – 8 are typically third party fees (collected by lender/broker/closing agent and paid to a party other than lender/broker)

3 Required services that we (lender/broker) select

Appraisal Fee Final Inspection Fee Credit Report Fee FHA Upfront MIP VA Funding Fee RD Guarantee Fee MI Initial Premium

4 Title services and lender’s title insurance

Title Insurance – Lender’s Coverage Title Guarantee Title Endorsements Title Search Fee Name Search Fee Settlement Fee Attorney Fee Courier/messenger/overnight delivery Fee Recording Service Fee

5 Owner’s title insurance

Title Insurance – Owner’s Coverage (Required to be disclosed on all purchase transactions regardless of intent to purchase)

6 Required services that you (borrower) can shop for

Inspections (pest, well, etc) Flood/Life of Loan Fee Tax Service Fee Survey Fee HECM Counseling Fee (Reverse)

7 Government recording charges

Recording Fee - Transfer Deeds Recording Fee - Mortgage/DOT

8 Transfer taxes City/County Tax/Stamps State Tax/Stamps Intangible Tax Residential Mortgage Loan Fee, etc.

GFE Page 2

The New HUD‐1 must be used if the new GFE has been issued.

Understanding the HUD‐1

The New HUD‐1 now consists of 3 pages.

It is required that the HUD‐1 is signed by all borrowers and sellers. They may sign anywhere on the HUD‐1 or a signature page may be provided.

Lines 207 & 208: Enter the credit paid by lender/broker and GFE refund amount, if applicable.

Understanding the HUD‐1

Many line items have been re‐numbered and some settlement charges are grouped together.

Settlement charges are displayed in dollar amounts, not percentages.

The GFE line numbers are nowreferenced on the HUD‐1.

Changes to ANY settlement charge cannot be made once Michigan Mutual has approved the HUD‐1.

All settlement charges listed on HUD‐1 must be accurate and within the tolerance limits in comparison to the amount disclosed on the most recent GFE.

Enter tax service and flood certification amounts in lines 1302 & 1303, as opposed to lines 806 & 807.

Understanding the HUD‐1

Comparison of GFE and HUD‐1 settlement charges enables the borrowers to compare settlement charges disclosed on the most recent GFE to the actual settlement charges shown on the final HUD‐1.

If more lines are needed for charges, the HUD‐1 Supplement document would reflect any additional charges that exceed the number of lines provided.

HUD‐1 now groups settlement charges into 3 categories:1) Charges that cannot increase at settlement.2) Charges that in total cannot increase more than 10% at settlement.3) Charges that can change.

Settlement charges listed on the HUD‐1 are the cost to do the transaction, not necessarily the borrower's cost.

Loan Terms section of the HUD‐1 must match the terms disclosed on the most recent GFE.

NOTE: A HUD‐1 Supplement document is available to provide additional lines for settlement charges that may not fit on pages 2 and 3, as mentioned above.

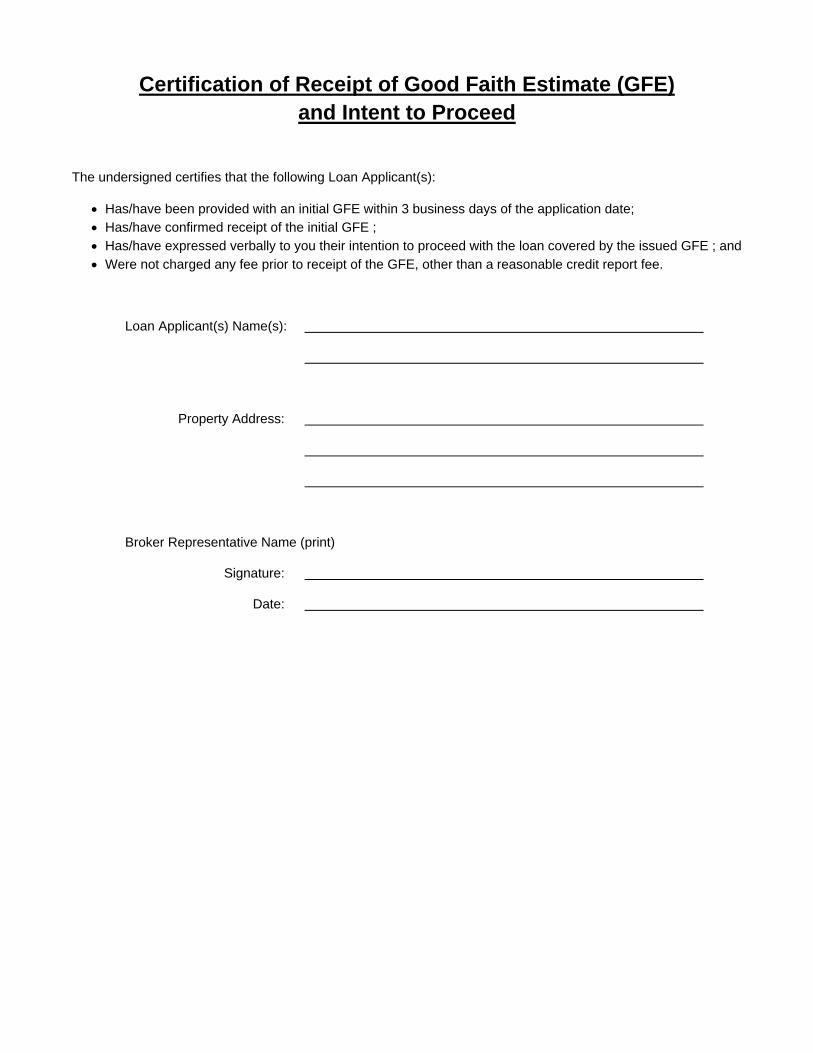

Certification of Receipt of Good Faith Estimate (GFE) and Intent to Proceed

The undersigned certifies that the following Loan Applicant(s):

• Has/have been provided with an initial GFE within 3 business days of the application date; • Has/have confirmed receipt of the initial GFE ; • Has/have expressed verbally to you their intention to proceed with the loan covered by the issued GFE ; and • Were not charged any fee prior to receipt of the GFE, other than a reasonable credit report fee.

Loan Applicant(s) Name(s):

Property Address:

Broker Representative Name (print)

Signature:

Date:

RESPA Change Circumstance Form Complete this form for each re-disclosure GFE and include the revised GFE: Date of Change: _________________________________________ Date of GFE Re-Disclosure: _________________________________________ Details of Change: _________________________________________ ________________________________________________________________________ ________________________________________________________________________ ________________________________________________________________________ ________________________________________________________________________ ________________________________________________________________________ ________________________________________________________________________ Changes associated with Changed Circumstance: $______________________ $______________________ $______________________ $______________________ $______________________ $______________________ $______________________ $______________________ Borrower Signature ______________________________________ (If borrower requested change)

This Mortgage Broker Fee Agreement and Disclosure (“Agreement”) is by and between

2. YOUR MORTGAGE LOAN

You are currently applying for a mortgage loan in the amount of $

MAXIMUM BROKER FEE (1) - All fees that are paid to us for arranging your loan with a mortgage lender. This amount is included in the “Our origination charge” of Block 1 of your Good Faith Estimate. The “Our origination charge” amount represents the total sum of all origination charges and fees for your loan from the mortgage broker, mortgage lender and other third parties, as applicable.

Amount

NOTE: You may not be charged any fee, other than a reasonable credit report fee (if applicable), prior to (i) receiving your Good Faith Estimate from us, (ii) expressing your intent to proceed with the loan transaction and (iii) receiving the initial disclosures from the mortgage lender.

,a mortgage broker (“we,” “us,” “our”) and the Borrower(s) who sign(s) below (“you,” “your”). This Agreement discloses and governs the overall fees that will be paid to your mortgage broker for the origination of your loan.

may increase if the loan amount increases, or decrease if the loan amount decreases. The fees in this Agreement are for broker services only and do not include other closing costs or credits from us or other parties for non-broker related services.

3. BROKER FEES: Depending on the loan program you select and subject to applicable legal requirements, our fees may be paid by you directly or indirectly, or a combination of both. For the portion of our fees paid directly, you will pay our fees from your own funds at or prior to the loan closing. For the portion of our fees paid indirectly, you may elect to include our fees in your loan amount and pay us at closing out of your loan proceeds. In addition, you may pay our fees by electing to pay the mortgage lender a higher interest. When you elect to pay a higher interest rate, the mortgage lender will provide you with a credit which will be applied against and reduce your settlement charges, including our fees. Paying our fees directly versus indirectly may result in a lower interest rate. We have discussed these fee payment options with you. In addition to our fees, estimates of other fees you will pay in connection with your loan will be shown on your Good Faith Estimate. Once your interest rate is locked and your loan amount and terms are finalized, we will be able to tell you the exact amount of all fees.

Mortgage Broker Fee Agreement and Disclosure

(Must be completed)

(1) In Wisconsin, this fee shall constitute a “broker administration fee.” In Iowa, this fee shall constitute a “broker administration fee.” In all other states, this fee shall constitute a broker origination fee.

1. OUR SERVICES: A mortgage broker charges fees to arrange a loan from a mortgage lender who will fund the loan. As your mortgage broker, we will assist you in obtaining a loan, but we do not offer the products of all mortgage lenders, and so we cannot guarantee you the lowest price or best loan terms available. Be sure that you understand and are satisfied with the mortgage loan product and terms we arrange for you. By signing below, you request us to arrange a mortgage loan from a mortgage lender and you agree to the fees listed below for our services.

1

If this box is checked, the form has been amended. All amendments must be initialed by borrower,or a new agreement must be completed.

Signature: Signature:

Date: Date:

Broker Name: By: Signature:(Printed Name)

Date:ver. 1/10

Borrower: Co-Borrower:

YOUR ADJUSTED BROKER FEE - The portion of our fees that will be paid by you to us directly after applying the above credit of the mortgage lender, if applicable. This amount is included in the “Your Adjusted Origination Charges” of Block A of your Good Faith Estimate. The “Your Adjusted Origination Charges” amount represents the total sum difference of Box 1 and Box 2 of your Good Faith Estimate.:

By signing below, you acknowledge that:(i) You have received an initial Good Faith Estimate within three (3) business days of the mortgage loan application date and you intend to proceed with the loan transaction.(ii) The Agreement has been explained to you and you understand it. (iii) You have not been charged any fees, other than a reasonable credit fee (if applicable), prior to entering into this Agreement(iv) You voluntarily enter into this Agreement and agree to the fees above.(v) The fees above are based on current market rates and your current loan request.

(Must be completed)

(Must be completed)

CREDIT FOR SETTLEMENT COSTS FROM THE MORTGAGE LENDER IN EXCHANGE FOR YOUR SELECTED INTEREST RATE – This will be reflected as a credit to you on Block 2 of your Good Faith Estimate:

1