annual report 2001 - e+s rück · gerd kettler chairman of the executive board of ... hannover of...

TRANSCRIPT

Annual

e+s rück

REPORT

2001

Gross written premiums 1 904.5 +22.8% 1 550.4 1 272.3

Net premiums earned 1 041.3 +15.1% 904.6 727.0

Underwriting result (148.6) (24.9%) (119.0) (57.5)

Change in the equalisation reserve and similar provisions (23.1) (232.8%) 17.4 19.5

Investment result 223.3 (2.7%) 229.6 160.1

Pre-tax profit 27.8 – 27.8 19.0

Profit or loss for the financial year 12.0 +650.0% 1.6 9.8

Investments 3 603.3 +13.8% 3 166.8 3 074.2

Capital and reserves incl. surplus debenture (Genussrechtskapital) 161.2 – 161.2 161.2

Equalisation reserve and similar provisions 270.1 (7.9%) 293.2 275.8

Net technical provisions 2 952.0 +16.1% 2 543.1 2 372.1

Total capital, reserves and technical provisions 3 383.3 +12.9% 2 997.5 2 809.1

Number of employees 198 +5 193 207

Retention 57.0% 59.6% 56.9%

Loss ratio* 91.7% 78.4% 83.1%

Expense ratio* 23.9% 26.9% 25.1%

Combined ratio* 115.6% 105.3% 108.2%

* excluding life reinsurance

Figures in EUR million +/(-)previousyear2001 19992000

KEY FIGURES of E+S Rück

1 Foreword

3 Boards and officers

5 Executive Board

8 Management report

8 Economic climate

10 Business development

11 Premium growth and results

21 Investments

23 Risk report

27 Human resources

28 Outlook

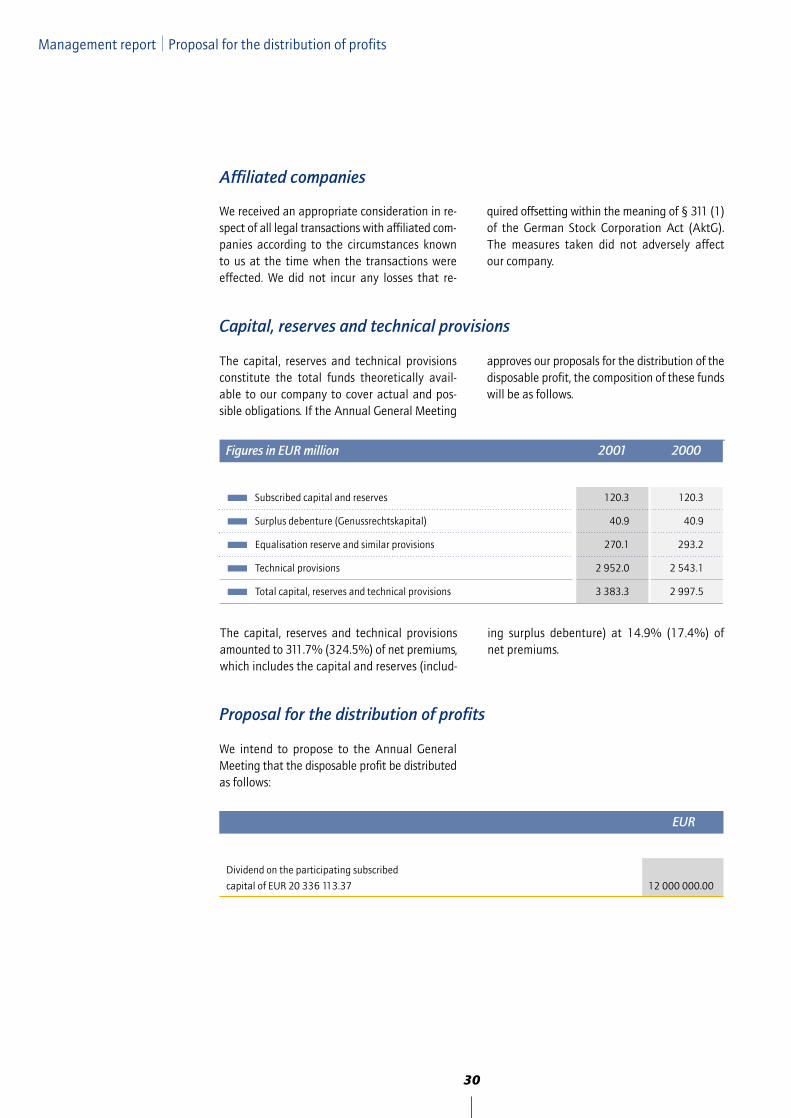

30 Proposal for the distribution of profits

31 Annual financial statements

32 Balance sheet as at 31 December 2001

36 Profit and loss account for the 2001 financial year

38 Notes

41 Notes on assets

46 Notes on liabilities

50 Notes on the profit and loss account

54 Auditors' report

55 Report of the Supervisory Board

57 Glossary

CONTENTS

Dear clients and shareholders of E+S Rück,

We are pleased to report that our company enjoyed another successful financial year.

For the insurance industry 2001 was a year of upheaval, triggered by an extraordinary

incidence of major losses. The most devastating event occurred on 11 September in the

United States – the horrific images of that day will take a long time to fade. On the

German market, too, the losses caused by the terrorist attacks as well as further sizeable

major losses prompted an appreciably heightened level of risk awareness and a review of

existing coverages – especially those for major risks. Whilst the 2001 treaty renewals had

already produced improvements, the loss experience in the year under review necessitated

significant premium increases and limitations of liability. This was most apparent in in-

dustrial fire and liability insurance, lines that had been under strain for years and where

premiums were not commensurate with the risk. In the present annual report we would

like to explain how we pursued our anti-cyclical approach in this difficult year.

We enlarged our total gross premium income in the year under review by an impressive

22.8% to EUR 1.9 billion. Disproportionately strong growth was generated once again in

our strategic segment of life and health reinsurance, which now accounts for 33% of our

overall premium volume. The German life insurance market showed further sustained

growth and was given added impetus by the launch of state-subsidised, private old-age

provision. Our acceptances in property and casualty reinsurance are guided by strict

profitability considerations, as a consequence of which premium income showed growth

in absolute terms but was further reduced in the context of its share of our total port-

folio. It goes without saying that our profit and loss account – like that of other market

players – was impacted by the major losses of the year under review. We are therefore

particularly proud to report that even in such a difficult market climate we actually

generated an increased profit for the year, which we intend to distribute in full to our

shareholders.

For some years now you have been accustomed to the importance that we not only

attach to the profit-oriented management of our underwriting business but also to the

areas of quality management and individual customer care. In the year under review we

conducted our activities in this respect under the motto "standing still is a step back-

wards". In the previous year we were the first reinsurer in the world to obtain ISO 9001

certification confirming the efficiency of our quality management system. In the year

under review we underwent our first annual review. The results were highly satisfactory

and produced fresh insights that we look forward to acting on within our organisation.

We also set great store by enhancing our Customer Relationship Management in life and

1

Wilhelm Zeller

Dr. Wolf S. Becke

Dr. Michael Pickel

2

health reinsurance. By pursuing an approach that goes above and beyond traditional mar-

keting concepts, our goal here is to enter into long-term, mutually beneficial partnerships

with our loyal customers. Last but not least it may be noted that E+S Rück was the only

reinsurer in the German market to keep up its treaty quotations without interruption in

the wake of 11 September. As a specialist reinsurer for the German market, we thus sent

out a clear signal that we stand by our clients even – or more accurately – especially in

difficult times.

Summing up, 2001 was in many respects a turbulent year in which we systematically

moved forward on our chosen path and equipped ourselves well for future challenges as

your reinsurer serving the German market.

Yours sincerely,

Wilhelm Zeller Dr. Wolf S. Becke Dr. Michael Pickel

Chairman of the Member of the Member of the

Executive Board Executive Board Executive Board

3

BOARDS AND OFFICERS of E+S Rückversicherungs-AG

Wolf-Dieter Baumgartl Chairman of the Board of Management ofHannover HDI Haftpflichtverband derChairman Deutschen Industrie V.a.G.

Gerd Kettler Chairman of the Executive Board ofMünster LVM Landwirtschaftlicher Versicherungs-Deputy Chairman verein Münster a.G.

Manfred BieberHannover*

R. Claus Bingemer Former Chairman of the Executive Boards Hannover of Hannover Rückversicherungs-AG,

E+S Rückversicherungs-AG

Dr. Heinrich Dickmann Chairman of the Executive Board ofBurgwedel Vereinigte Haftpflichtversicherung V.a.G.

Ass. jur. Tilman HessHannover*

Rolf-Peter Hoenen Speaker of the Executive Boards ofCoburg HUK-Coburg Versicherungsgruppe

Dr. Ing. Manfred Mücke Chairman of the Executive Boards ofHamburg - KRAVAG-SACH VaG,

- KRAVAG-LOGISTIC Versicherungs-AG,

Member of the Executive Board of - R+V Versicherung AG- R+V Allgemeine Versicherung AG

Anita Suing-HopingGodshorn*

Supervisory Board (Aufsichtsrat)

*Staff representative

Dr. Edo Benedetti President of the Trient ITAS Istituto Trentino-Alto Adige

per Assicurazioni, Italy

Wolfgang Bitter Chairman of the Executive Board ofItzehoe Itzehoer Versicherungsverein –

Brandgilde von 1691 VVaG

Dieter Holl Chairman of the Executive Board ofStuttgart Württembergische Gemeinde-Versicherung a.G.

Ernst Köller General Director and Chairman of Hannover the Executive Board of

CONCORDIA Versicherungs-Gesellschaft a.G.(until 28 February 2002)

Dr. Erwin Möller Member of the Board of Management of Hannover HDI Haftpflichtverband der

Deutschen Industrie V.a.G.and Talanx AG

Adolf Morsbach Former Chairman of the Board of ManagementWedemark of HDI Haftpflichtverband der

Deutschen Industrie V.a.G.

Advisory Board (Beirat)

4

Executive Board (Vorstand)

Wilhelm Zeller Program business; Planning/Controlling,Burgwedel Investor Relations, Public Relations, InternalChairman Auditing; Underwriting Services and Controlling;

Human Resources; Corporate Development

Dr. Wolf Becke Life and Health reinsurance worldwideHannover

Jürgen Gräber Coordination of all non-life reinsurance;Ronnenberg international Property and Casualty treaty

reinsurance, Credit and Surety business world-wide; Financial reinsurance worldwide

Herbert K. Haas Finance and Accounting;Burgwedel Capital Markets; Information Technology;(until 31 January 2002) General Administration

Dr. Andreas-Peter Hecker Hannover(until 31 August 2001)

Dr. Michael Pickel German Property and Casualty treaty Gehrden reinsurance; non-life reinsurance of the HDI (Full Member Group, Retrocessions; Claims Service;since 1 January 2002) Legal Department

Dr. Detlef Steiner Hannover(until 31 August 2001)

André Arrago International Property and Hannover Casualty treaty reinsuranceDeputy Member(since 1 September 2001)

Dr. Elke König Finance and Accounting;Hannover Capital Markets; Information Technology;Deputy Member General Administration(since 1 January 2001)

Ulrich Wallin Specialty Division (worldwide facultativeHannover business in Casualty and Property lines;Deputy Member worldwide treaty and facultative business(since 1 September 2001) in aviation, space and marine insurance world-

wide) international Property and Casualtytreaty reinsurance

5

From left to right:

Dr. Michael Pickel

André Arrago

Jürgen Gräber

Wilhelm Zeller

Dr. Elke König

Ulrich Wallin

Dr. Wolf Becke

8

The cyclical trend in the global economy showeda marked downturn in the year under review. Thiswas especially true of the major industrial nations,with the USA and Japan actually going into re-cession. The strains in the USA were primarilytriggered by the muted growth expectationsand the low personal savings ratio of privatehouseholds. The economies of the developingand emerging countries also declined, with Asiaparticularly impacted by the tense state of thetechnology sector. Macroeconomic expansion inthe Eurozone similarly fell away sharply in theyear under review. Particularly notable here wasthe abrupt fall in manufacturing output, triggeredon the demand side by the deteriorating globaleconomy and the associated contraction in ex-port and domestic demand. The terrorist attacksof 11 September exacerbated the already appre-ciable economic problems on a worldwide scale.

Economic growth in Germany was in the orderof just 0.6% in the year under review, an unex-pectedly large decline compared to the previousyear. While a mood of optimism still prevailedat the beginning of the year due to extensivetax cuts, adverse factors increasingly gained theupper hand as the year progressed. The level ofprices rose sharply as the cost of petrol and foodincreased. What is more, growing unemploymentserved to reduce disposable incomes, thus ham-pering personal consumption and again curbingdomestic demand. Furthermore, industry's will-ingness to make capital investments sufferedunder the deterioration in the general businessoutlook as well as the drop in incoming orders.The growth in real gross domestic product thuscame to a virtual standstill in the summer of

The German insurance industry

The German insurance industry experienced an-other difficult year in 2001. While premium in-come in property and casualty insurance is fore-cast to have risen by around 3% to EUR 50billion, this growth does not constitute improvedincome in real terms once the increase in insuredvalues is taken into account. Most strikingly, thesituation in German industrial property insurance

remained under considerable strain. Predatorycompetition continued to prevail in this segment.It was at least gratifying to note that total pre-mium income increased – the first rise since1994. Yet this higher income was offset by alarger burden of losses. On balance, the loss ratiofor the financial year was around 100% (previ-ous year: 98.5%). Allowing for run-off profits and

2001. Most notably, export demand – the de-cisive motor for economic growth in recent years– lost impetus as the global cyclical trend tookan increasingly downward turn.

The economic slowdown also took a heavy tollon capital markets, making 2001 one of the mostdifficult years in stock market history. Alarmingcorporate announcements warning of – some-times multiple – downward revisions in profitexpectations provoked a general mood of uncer-tainty and caused stock prices to decline acrossvirtually all sectors. Against the backdrop of thisalready very tense environment, the terroristattacks of 11 September unleashed near-panicselling on the equity markets. Although the cru-cial national and international indices had re-covered appreciably by year-end, the Dax showeda decline of more than 20% for the year as awhole. Movements on interest rate markets werealso impacted by the flagging economy. The mostdrastic reaction came from the US Federal Re-serve Board, which in the course of the year –and prompted in part by the terrorist attacks –incrementally cut the prime rate by a total of475 basis points to 1.75%. The European Cen-tral Bank, by contrast, was relatively slow to startcutting rates and did so in less pronounced fash-ion. Overall, it reduced base rates by 150 basispoints to 3.25% by year-end. These interest ratecuts of course gave bond markets a correspondingimpetus, with securities issued by first-rate bor-rowers showing the greatest gains. The develop-ment of the euro was unsatisfactory: despite amodest upswing early in the second half of theyear it continued to depreciate, especially againstthe US dollar.

Economic climate

of E+S RückMANAGEMENT REPORT

9

losses of previous years, the resulting marketloss is expected to be in the order of EUR 0.6billion (previous year: EUR 0.5 billion). The situ-ation in fire and liability insurance remainedespecially critical – with both lines additionallyburdened by large major claims which cut heav-ily into profits. The consistently unacceptablelevel of profitability compelled insurers to im-prove premiums and conditions. The develop-ment of German motor insurance was morefavourable from a profitability standpoint. Pre-mium increases in this line combined with a de-creased claims frequency – due to higher petrolprices and lower usage of motor vehicles – gen-erated surprisingly good results.

Marked hardening could be observed on theGerman reinsurance market in the course of theyear under review. This was triggered by thepoor – in some areas intolerable – results of theprevious years in conjunction with sharply lowerinvestment income. The renewal season for 2001thus showed a clear tendency towards more ad-equate pricing as well as conditions that weremore commensurate with the risk. Furthermore,the heavy burden of major losses intensified thepressure on reinsurers to obtain improved termsand conditions or withdraw the accustomed levelof capacity from the markets – a trend that wasgiven significant added impetus by the terror-ist attacks of 11 September in the USA. For theGerman reinsurance industry, as was true of re-insurers around the world, these loss eventssignalled a decisive turning point that trans-formed the market. On the one hand, reinsurers– first and foremost international players – tem-porarily or even permanently suspended theirunderwriting activities on the German market.On the other hand, this unprecedented lossunderlined the significant role played by reinsur-ers as vital risk-carriers and highlighted the im-portance of adequate reinsurance cover. Where-as in past years the pricing component wasvirtually the sole focus of attention, consider-ations of quality, security and continuity havenow reclaimed greater importance.

Since the effects of the 11 September terroristattacks did not make themselves felt until thefourth quarter, they did not give rise to any dra-matic improvements in the accounting figures

reported for the year under review. The decisivefactors continued to be the strained state of themarket in German property and casualty (re-)in-surance and the large burden of major losses.The depressed situation in industrial fire andliability insurance – both as regards premiumsand claims – particularly impacted the reinsur-ers' results. Yet as the year progressed, these linesalso showed the most far-reaching rehabilitationsuccesses, and the prospects for the current fi-nancial year are therefore considerably brighter.The performance of German motor insurance,on the other hand, was exceptionally favourablefor the reinsurance industry. In this line reinsurerswere able to share in the premium increases onthe original market and they generated substan-tially improved results.

German life insurance continued to be attract-ive, both in the insurance and reinsurance sec-tors. Following a decline in new business in theprevious year the number of new policies takenout increased in the year under review. Premiumincome grew by around 8%. Pension and terminsurance products as well as unit-linked life in-surance continued to be high-growth areas. Yetthe greatest impetus derived from disability in-surance, which profited from the reduced pro-tection afforded younger employees under thestatutory pension scheme. The most significantevent in the 2001 financial year was the passageof legislation relating to the so-called "Riesterpension" and the introduction of state-subsid-ised, private old-age provision. Although thefavourable implications of this aspect of pen-sion reform did not make themselves felt in theyear under review, they open up the prospectof enormous growth potential for the Germanlife insurance industry.

Stronger emphasison quality, securityand continuity

Marked hardening of the Germanreinsurance market

Management report Economic climate

10

Business development

E+S Rück bears exclusive responsibility for Ger-man business within the Hannover Re Group.We are the specialist reinsurer for the Germanmarket. For its part, Hannover Re – together withits subsidiaries – writes the international business.In order to safeguard advantageous internation-al risk spreading, the two companies participatein each other's respective business segments. Ourtechnical account thus continues to be influ-enced by developments in the international re-insurance markets via these retrocessions.

Our gross premium income posted a highly grat-ifying increase of 22.8% compared to the pre-vious year to reach a total of EUR 1.9 billion.Growth derived from the expansion of both prop-erty/casualty and life/health reinsurance. In ab-solute terms gross premium income in the lattersegment grew by EUR 144.5 million to EUR625.8 million, and the proportion of our totalportfolio attributable to life and health reinsur-ance now stands at 32.9% (previous year:31.0%). The key driver of growth here was sus-tained strong demand for products in the areaof old-age provision, especially pension and terminsurance policies as well as unit-linked life in-surance. In these subsegments we support ourclients with reinsurance solutions designed tofinance their new business.

The state of the market in German property andcasualty reinsurance remained tense in the yearunder review. Inadequate premiums and inappro-priate conditions were most striking in indus-trial fire and liability insurance. This continuedto be the case despite the fact that premiumsand conditions were improved – sometimes sub-stantially – in the course of the year in responseto the heavy burden of major losses. Motor in-surance, however, where a good premium leveland favourable claims situation facilitated sur-prisingly positive results, produced a gratifyingperformance. Whilst our internal standard ofwriting business only in accordance with strictprofitability considerations thus permitted anoverall expansion of the premium volume inabsolute terms, it consequently caused the pro-

portion of our total portfolio attributable toproperty and casualty reinsurance to contractfurther to 67.1% (previous year: 69.0%).

Owing to a slightly lower retention, our net pre-miums grew in the year under review by 15.1%to EUR 1.0 billion.

The loss expenditure climbed sharply by 29.2%year-on-year to EUR 838.6 million. The key fac-tors here were the major loss incidence and es-pecially the terrorist attacks of 11 September inthe USA, which also impacted our profit and lossaccount through intra-group risk spreading withHannover Re. The loss ratio excluding life in-surance thus increased to 91.7% (previous year:78.4%). Operating expenses, on the other hand,were reduced from EUR 328.1 million to EUR269.2 million. This decrease was primarily at-tributable to earnings that accrued back to ourtechnical account from securitisation transac-tions – i.e. from the transfer of reinsurance risksto the capital markets – concluded jointly withHannover Re. The heavy losses of the year underreview resulted in reimbursements under thesecontracts. Overall, the net underwriting resultbefore changes in the equalisation reserve de-teriorated to -EUR 148.6 million (previous year:-EUR 119.0 million).

On the basis of the loss experience in the yearunder review an amount of EUR 23.1 million(previous year: allocation of EUR 17.4 million)was withdrawn from the equalisation reserve,and the net underwriting result consequentlyimproved slightly year-on-year to -EUR 125.5million (previous year: -EUR 136.4 million).

We also strengthened the IBNR reserve in theyear under review with an allocation of EUR 35.6million (previous year: EUR 34.5 million) fromthe non-technical account.

Even given the difficult conditions prevailing onthe capital markets, we succeeded in generatingan investment result of EUR 223.3 million – afigure almost on a par with the previous year

Investment resultalmost on a par with

the previous year

Gratifying rise inpremium income

Higher loss burden

due to increased major losses

Management report Business development

11

Capital, reserves and technical provisions

Technical provisions

Net premiums

Equalisation reserve and similar provisions

Capital and reserves (excl. disposable profit)

500

1 000

1 500

2 000

2 500

0

Growth in capital, reserves, technical provisions and in net premiums

in EUR million

3 000

19921994

19951996

19971998

19992001

20001993

(EUR 229.6 million). The main positive factorshere were the increased portfolio of investmentsas well as credits on deposits under life and fi-nancial reinsurance treaties. Particularly due tothe tense state of the stock markets, however, thehidden reserves in our securities portfolio de-creased from EUR 282.2 million to EUR 165.7million.

After tax expenditure of EUR 15.8 million, wethus generated a profit for the financial year ofEUR 12.0 million. We intend to distribute thisamount in full to our shareholders.

Our gross premium income increased by 22.8%to EUR 1.9 billion in the year under review. Thisgrowth derived from the expansion of our owndirectly written German business and an increasein the foreign business accepted from HannoverRe. We assume the latter under an internal retro-cession agreement that enables us – by addingforeign risks – to improve the geographicalspread and risk diversification of our portfolioacross all lines of business. However, this internalbalancing of risks within the Group – which overthe years has proven advantageous and helpedstabilise profits – placed a considerable strainon our results in the year under review. This wasdue to the heavy international major losses, most

notably those associated with the terrorist attackson 11 September in the USA. We reserved in fullthe burden of losses resulting from these attacksin the year under review. Furthermore, since wehave no reason to doubt the stability of our retro-cession arrangements, we do not expect theseevents to have any further adverse impacts onsubsequent years.

Our German business, on the other hand, showeda more satisfactory development and recorded aslightly improved underwriting result*. It should,however, be borne in mind that the strong growthin our domestic life portfolio and the associatedprefinancing expenditures – the full amount of

Management report Premium growth and results

Premium growth and results

* Underwriting result: gross before internal administrative expenses, allocatedinvestment return and the change in the equalisation reserve

12

which must be booked as expenses in the firstyear under German accounting requirements –of course place a drag on the reported earn-ings. We attach considerable importance to ourretrocession facilities in order to be able to shoul-

der these prefinancing components. In conjunc-tion with Hannover Re these investment-orientedexpenditures were transferred to the capital mar-kets by way of securitisations.

Management report Premium growth and results

* Underwriting result: gross before internal administrative expenses, allocatedinvestment return and the change in the equalisation reserve

The following sections explain the developmentof each line of business. Due to our orientationas a specialist reinsurer for the German market,we have subdivided our management report ontechnical business. The following commentarieson the various lines of business refer solely to

our German portfolio; we then provide a sum-mary of our international business accepted fromHannover Re under retrocession arrangements.Due to the international nature of aviation busi-ness, this is also described within the foreignsection.

Development of underwriting results* – breakdowninto German and foreign business

100

0

(100)

(200)

(300)

(400)

(500)

(600)

in EUR million

Development of gross premium income – breakdowninto German and foreign business

200

400

1 200

800

600

1 000

1 400

1 600

1 800

2 000

0

in EUR million

2000 2001 2000 2001

940 1 061

610 844

Germany

Foreign

1 550 1 905 Total

(165) (157)

(40) (361)

Germany

Foreign

(205) (518)Total

Development of the individual lines of business in Germany

13

Fire

The state of the German fire insurance marketremained tense in the year under review. Pre-mium income in the traditional lines of indus-trial fire and fire loss of profits is expected toshow another substantial decline of around 9%to EUR 0.9 billion. With loss expenditure for thetwo segments virtually unchanged year-on-yearat approximately EUR 1.2 billion, the loss ratioclimbed markedly to 128% (previous year:117.8%). The situation in industrial fire insur-ance – which had been unsatisfactory for a num-ber of years – prompted the implementation ofurgent remedial action in the course of 2001.Primary insurers initiated this rehabilitation byrestricting their available capacity, exerting asqueeze on the market which made initial rateincreases possible. Insurance conditions alsoshowed a favourable trend, as exemplified by theintroduction of special limitations of liability fornatural hazards.

In the reinsurance sector the poor results of pre-vious years coupled with a sharply higher burdenof major losses in the year under review gaveadded impetus to the trend towards non-pro-portional types of coverage. Particularly in indus-trial fire insurance, lower layers virtually ceasedto be reinsured because they could only havebeen written with substantial premium increasesowing to the heavy burden of losses. Mid-rangeand higher layers continued to be accepted,albeit only with appreciable premium adjust-ments. Progress was also made with regard toterms and conditions. For example, it is now virtu-ally impossible to place multi-year policies on thereinsurance market. The terrorist attacks of 11September and the ensuing reappraisal of therisk situation considerably boosted these effortsto restore business to profitability. German firebusiness thus showed pleasing improvementsin the course of the year, although these werenot yet sufficient to offset the dramatic pricecuts and deteriorations in terms and conditionswitnessed over the past eight years.

In response to the unsatisfactory state of Ger-man fire insurance we only accepted new riskson a highly selective basis. As a consequence ourgross premium income posted a merely modestincrease of EUR 4.7 million. In keeping with themarket-wide trend, we emphasised the expan-sion of our non-proportional portfolio. The num-ber of treaties written rose by 5% compared tothe previous year. In this context, we primarilysupported companies that have demonstratedtheir special commitment to a long-term partner-ship. In proportional fire business, too, the heavylosses of the previous years brought about im-provements in terms and conditions. In this area,for example, we were able to obtain reductionsin commissions and include loss participationclauses. In cases where it appeared impossibleto attain the break-even point in the mediumterm, we consciously decided against treaty re-newal. The number of proportional treaties con-sequently decreased by around 20%.

This cautious approach hasenabled us to limit the ad-verse effects of the alto-gether still unsatisfactorysituation in German fire in-surance. Nevertheless, evenour portfolio experienced adeterioration of 12.3 per-centage points in the lossratio, closing with an under-writing deficit. It was, how-ever, gratifying to note that our loss ratio wasstill above average compared to other marketplayers, since with few exceptions we had noparticipations in the significant major losses re-corded in the year under review.

In contrast to other large professional reinsur-ers we – very deliberately – maintained ourquotation service in the wake of the terroristattacks of 11 September. In the continuity-ori-ented environment of the German market, this

in EUR million 2001 2000

Fire

Gross writtenpremiums 35.3 30.6

Loss ratio (%) 77.6 65.3

Underwriting result(gross) (3.7) 0.9

Management report Premium growth and results

14

was an opportunity for us to live up to ourpromise that E+S Rück – as a specialist reinsurerfor German clients – stands ready as a reliablepartner even in difficult times. Thanks to this pol-icy, we were able to establish extensive new busi-ness relationships and we succeeded in con-solidating and expanding our positioning in themarket. With an eye to the changed significanceof the terrorism risk, we implemented the neces-sary adjustments to terms and conditions. To a

Liability

Following the slight premium decline in the pre-vious year, German liability insurance expects togrow by a modest 1.5% to around EUR 6.0 bil-lion in the year under review. Yet the market cli-mate in liability business remained tense in the2001 financial year and was further burdened byan exceptional claims experience. Whilst the over-

all level of loss expenditure isforecast to remain roughly un-changed year-on-year at EUR4.7 billion, the year under reviewwas enormously impacted bymajor claims under US-relatedpharmaceutical covers. The mostprominent examples for the Ger-man market were the Lipobay

group of claims as well as product liability claimsresulting from contaminated implants, whichgave rise to extensive claims for damages. Takentogether, these two events produced a marketloss in the order of almost EUR 1 billion. Yet theselosses ushered in a trend towards market hard-ening, causing the price of (re-)insurance coverfor pharmaceutical and other major risks to risesharply. In response to this changed market situ-ation many policyholders were compelled to dras-tically increase their deductibles, with the resultthat in some cases they now carry a not insignifi-cant portion of individual risks themselves.

Against the backdrop of this unsatisfactory en-vironment we continued to withdraw from prob-lematic segments of German liability business. Atthe same time we did not renew a number ofspecial treaties written in the previous year,thus causing our premium income to contract

slightly. Nevertheless, the strained situation thathas prevailed in recent years in German liabilityinsurance and the major losses recorded in2001 enabled us to implement initial premiumincreases in the course of the year. The mostmarked effects were felt in non-proportional re-insurance, most notably industrial liability. It wasgratifying to see that the deterioration in termsand conditions also observed in previous yearsdid not continue. The return towards more risk-appropriate conditions that was thereby set inmotion for our portfolio was fostered by theterrorist attacks of 11 September, which triggereda fundamental review of the situation with cor-responding adjustments of premiums and con-ditions. What is more, these loss events promptedour clients to focus more closely on the qualityand security of our company; preference wasgiven market-wide to reinsurers equipped witha sound capital structure and long-standing ex-pertise in liability business. As a seasoned re-insurer that has concentrated exclusively on thespecial requirements of the German market, wemeet these criteria and were therefore able tofurther enhance our competitive position.

Yet the positive changes which set in during theyear were not sufficient to offset the unfavour-able experience of the previous years and theheavy burden of major losses incurred in the yearunder review. The two most significant majorlosses for our account alone produced a grossstrain of around EUR 130 million for our port-folio. Overall, our liability business closed with aconsiderably poorer loss ratio and a markedunderwriting deficit for gross account, although

very large extent our modified reinsurancetreaties contain an exclusion for terrorism-re-lated losses or damage with respect to all fireand industrial risks with total sums insured inexcess of EUR 50 million. Lower sums insuredare subject to event limits in the obligatory re-insurance treaties. Furthermore, terrorism risksare now reinsured only on a non-proportionalbasis against payment of a separate premiumand with a limitation of liability.

in EUR million 2001 2000

Liability

Gross writtenpremiums 105.5 105.6

Loss ratio (%) 212.6 55.0

Underwriting result(gross) (141.4) 23.4

Management report Premium growth and results

mium increases and improvements in terms andconditions, and we therefore anticipate a far-reaching recovery for the current financial year.

it was substantially more favourable in net terms.Furthermore, the treaty renewals for 2002 en-abled us to generate additional sizeable pre-

Personal accident

German personal accident insurance showed an-other increase in its market-wide premium in-come in the year under review, although thegrowth of around 1% to approximately EUR 5.5billion was less than in previous years. Thehighest-growth areas continued to be personalaccident insurance with a premium refund andpersonal accident annuities. The loss ratio is ex-pected to reach 55% due to a moderate increasein the burden of losses, and it will therefore bevirtually unchanged from the gratifying level ofthe previous year. Since the competitive climateremained favourable, 2001 can be rated as apositive year for German personal accident insur-ance.

Owing to the relatively small share of the totalvolume of the German (re-)insurance market at-tributable to personal accident business, thisline is clearly not of pre-eminent importance inour portfolio. In view of the sustained attractivetrend and earnings situation, however, we againstepped up our involvement in this segment inthe year under review. By offering services spe-cifically tailored to support our clients, our goalhere was to acquire new market shares in ac-cordance with profitability considerations. We ad-vise ceding companies on personal accident prod-ucts for children as well as on underwriting and

claims investigation. In addition, we expandedour range of services in the area of personal ac-cident products for senior citizens. In cooper-ation with welfare and nursingorganisations we developed apackage of measures that com-plements pure claims handlingwith assistance componentssuch as the organisation ofcare and the provision of ad-vice and support during illness.On the basis of these specialservices we succeeded in estab-lishing new business relationships in the yearunder review and paving the way for furtherexpansion of our portfolio.

Overall, our portfolio showed a premium increaseof 18.3% in the year under review – growth thatwas well in excess of the market average. Thequality of our personal accident business as re-flected in the gratifying loss ratio was also morethan satisfactory. The deterioration in the under-writing result derived from increased commis-sions, although these essentially take the form ofprefinancing expenditures that will accrue to ouraccount in the coming financial years and boostearnings then.

in EUR million 2001 2000

Personal accident

Gross writtenpremiums 39.4 33.3

Loss ratio (%) 53.8 56.5

Underwriting result(gross) (1.1) 0.4

15

Motor

In the year under review motor business wasthe line that showed the most far-reaching im-provements within German property and casu-alty (re-)insurance. Premium income market-wideis expected to climb by a sizeable 5% to morethan EUR 21 billion. Notwithstanding a slight in-crease in the insured risks, this growth derivedprimarily from the tariff increases implementedby insurers. The reduction of numerous discounts– some of which were unjustifiable from the

underwriting standpoint – also had a favourableimpact. On the claims side the experience in theyear under review was satisfactory: claims ex-penditure decreased by around 3 percentagepoints overall, producing a remarkably low lossratio of around 93% (previous year: 99.8%). Itshould be pointed out, however, that some of thisreduction in the claims expenditure will probablyonly be of a temporary nature: the higher priceof transportation fuel and the associated cut-

Management report Premium growth and results

16

backs in vehicle usage – especially in the firsthalf of the year – resulted in a decreased claimsfrequency. This trend had already begun to mod-erate later in the year.

Since retentions in proportional business wereonly increased in isolated cases, the recovery ofGerman motor insurance also had implicationsfor the reinsurance market. Further positive

tendencies could be discernedin the non-proportional sector.Particularly in motor third partyliability insurance, premium in-creases were achieved despite areduced burden of major losses.

Our portfolio also benefited fromthe favourable state of the mar-ket in German motor insurance.

This was true despite an 8.5% reduction in pre-mium volume compared to the previous year.This decrease bears witness to our selectiveunderwriting policy and reflects the cancella-tion of unattractive treaties. Most notably, wemaintained our cautious stance with respect tocommercial fleet business. Leaving aside these

portfolio optimisation measures, the traditional-ly high importance attached to proportionalreinsurance in our portfolio enabled us to shareunreservedly in the growth and improved qual-ity of the insurance market.

The attractive general market conditions simi-larly had a favourable effect on our non-pro-portional acceptances.We were able to secureslight premium increases in this sector, whichled to a modest overall rise in our premium in-come despite higher priorities in some instances.This upward trend in premiums was even morepronounced in the 2002 renewals. Compared toprevious years, the volume of claims that werereported very belatedly under excess of losstreaties for motor third party liability insurancewas also considerably lower. This even led to ap-preciable run-off profits in some portfolios andgenerated positive underwriting results – some-times of sizeable dimensions. Overall, our loss ex-penditure showed a highly satisfactory decreaseof 14.8 percentage points. We were thus suc-cessful in achieving a good result in the yearunder review that surpassed our expectations.

Marine

Following a decline in premium income in theprevious year, German marine insurance gen-erated modest growth of around 2% to reach avolume of approximately EUR 1.7 billion. The bur-

den of losses also improved, andwith lower claims expenditure ofaround EUR 1.4 billion (previousyear: EUR 1.5 billion) the lossratio contracted to roughly 81%(previous year: 89.3%). Fiercecompetition and excess cap-acities continued to be the hall-marks of the German marineinsurance market. It was thus im-possible to secure the desired

level of premium increases that would haveprovided the basis for more satisfactory pricing.Positive developments were limited in scope,although offshore business showed the mostsignificant advances.

The situation in German marine reinsurance wasalso strained, although a large burden of majorlosses prompted a turnaround in the course ofthe year under review. This was primarily trueof non-proportional business, where premiumsincreased by more than 20% in some areas.

In the year under review we stood by our re-strained underwriting policy in German marineinsurance business. Furthermore, we stepped upour strategically defined orientation towards non-proportional business with the goal of divorcingourselves as far as possible from original rateson the primary insurance market. The number ofthese treaties in our portfolio increased again andthey now account for considerably more thantwo-thirds of our total inventory. Responding tochanges in the market, we also stepped up ouroffshore acceptances in order to profit from themore favourable premiums and conditions. Our

Management report Premium growth and results

in EUR million 2001 2000

Motor

Gross writtenpremiums 382.1 417.5

Loss ratio (%) 70.3 85.1

Underwriting result(gross) 62.0 19.6

in EUR million 2001 2000

Marine

Gross writtenpremiums 9.2 11.2

Loss ratio (%) 93.4 108.9

Underwriting result (gross) (2.2) ( 3.5)

17

facultative acceptances, in particular, were con-centrated on this segment. Elsewhere, however,we were highly conservative in our facultativeunderwriting.

Overall, premium income declined by 17.9% dueto our restrictive underwriting policy. Neverthe-

Life

The German life insurance industry generatedrenewed growth in new business in the yearunder review. Following the record year in 1999and a decline in 2000, around 8.4 million (pre-vious year: 7.3 million) new policies are antici-pated for the year under review. New businesspremium is also likely to grow by around 8% tomore than EUR 13 billion. This growth derivedprimarily from pension and term insurance prod-ucts. In unit-linked life insurance the expansionof previous years also continued, although withpremium growth of 5% at a less vigorous pace.However, this development came as no surprisesince in recent years the rates of increase hadbeen outstanding; furthermore, the depressedstate of the stock markets in the year underreview had created a mood of uncertainty. Themarket share of endowment insurance, on theother hand, declined again with below-averagepremium growth of around 1.8%. A key event inthe year under review was the enactment oflegislation relating to the state-subsidised, pri-vate supplementary pension. The launch of pri-vate old-age provision initiated by this so-called"Riester pension" opened up new growth areasfor the German life insurance industry. The figuresfor the 2001 financial year were only minimallyaffected, however, since certification of "Riester-compliant" products did not occur until year-endand state support only began in 2002.

Against this backdrop we further enlarged ourstrategic priority segment of life reinsurance inthe year under review. Our activities remainedfocused on financing our clients' new businessand supporting their growth with specificallydesigned reinsurance concepts. In this contextwe concentrated especially on financing solu-tions for pension insurance and unit-linked life

insurance. The sustained strong demand for ourfinancing products combined with the above-average growth generated by our clients enabledus to achieve another gratifying premium in-crease for our portfolio. Additionally, we com-pleted a number of block assumption transactions– a special type of financing arrangement thatenables our clients to realise the value of a port-folio before its actual maturity. Overall, the lossexperience of our portfolio was once again veryfavourable and the persistency of the businessin force also remained withthe anticipated actuarial par-ameters.

The year under review alsoclearly demonstrated that ourlife reinsurance business willprofit from the restructuringof the German pension sys-tem. Firstly, the so-called "Riester" products willcreate additional demand for financing assist-ance; secondly, we anticipate that notable bene-ficiaries of this reform will be bancassurers – acustomer group that we have especially focusedon.

We set particularly great store in the year underreview in the intensification of our Customer Re-lationship Management (CRM). The philosophyto which we adhere in this context is a deliberatedeparture from traditional marketing approach-es. For us, Customer Relationship Managementmeans that formation of a reinsurance treaty isno longer considered to mark the end of a purelyprice-driven and product-oriented marketingtransaction. On the contrary, we strive for long-term, evolving relationships. We devote particu-lar attention to clients who demonstrate their

less, our cautious approach enabled us to con-siderably ease the strain on our loss ratio, andthe underwriting result consequently improvedby EUR 1.3 million.

Management report Premium growth and results

in EUR million 2001 2000

Life

Gross written premiums 362.3 246.7

Technical result (gross) (46.1) (219.2)

18

loyalty to us and generate above-average valueadded within our portfolio. These core customersare offered preferred access to our financial andknowledge resources.

With growth of 46.9% the development of pre-mium income was once again gratifying in theyear under review. The continuing lively demandfor our financing products is of course directlyreflected in accounting losses in our profit andloss statement, since under German accountingrequirements the full amount of the prefinancingprovided must be written off in the first year. How-ever, due to substantial earnings which accruedback to our account from prefinancing transac-tions of earlier years, the underwriting deficit was

significantly lower than in the previous year.

It should generally be borne in mind that thenegative result of our life business must be con-sidered an investment which will be amortised bycorresponding repayments in the coming yearsand thereby boost our earnings. We continuedto retrocede substantial portions of these invest-ment-oriented financing expenditures, a factor,which further improved the underwriting resultfor net account. The "allocated investment re-turn" item in our profit and loss account is alsoof great significance in life reinsurance. Of thetotal reported amount of EUR 15.4 million, thelargest portion is attributable to our German lifebusiness.

Other lines

The following lines of business are shown com-bined under other lines: health, legal protection,burglary and robbery, water damage, plate glass,windstorm, householder's comprehensive (con-tents), householder's comprehensive (buildings),hail, livestock, engineering, omnium, credit and

surety, extended coverage, travelassistance benefits, nuclear plantproperty, other property damage,fire loss of profits, other and engin-eering loss of profits, other purefinancial losses and fidelity.

German credit and surety businessis one of our strongest sources ofpremium income among the other

lines. In the year under review this segmentsuffered under the generally adverse economicconditions, which were the primary cause of aconspicuously high number of insolvencies – es-pecially in the areas of trade and logistics. Over-all, the German insurance and reinsurance sectorswere faced with rising loss ratios and worseningresults. Our acceptances were also impacted bythese developments. On the one hand, the reper-cussions of a generally ongoing soft marketplaced a strain on the 2001 renewals, and for themost part we were only able to obtain premiumincreases and improved conditions in non-propor-

tional business. On the other hand, the majorclaims resulting from insolvencies also left theirmark on our portfolio. In the second half of theyear, however, these events induced hardening inthe market, which enabled us to secure appre-ciable premium increases and improvements inconditions. Against this backdrop we enlargedour premium income by EUR 5.5 million to EUR32.1 million. However, the heavy burden of lossesin the year under review produced an under-writing deficit of EUR 2.0 million.

German windstorm insurance experienced quiteliterally a quiet year. On the insurance marketboth premiums and claims continued on at rough-ly the same level as the previous year, and ac-ceptable results were thus once again possible.On the reinsurance side the picture varied:treaties burdened by heavy losses in past yearsshowed substantial premium increases, where-as loss-free risks posted only modest gains. As faras the burden of losses was concerned, the re-insurance sector profited from the higher reten-tions run by ceding companies, which absorbedthe bulk of the claims in the year under review.In this environment we stood by our tried andtested underwriting policy of previous years. Ourwindstorm portfolio is traditionally dominated bynon-proportional covers, under which we prefer

Management report Premium growth and results

in EUR million 2001 2000

Other lines

Gross writtenpremiums 98.4 84.1

Loss ratio (%) 50.8 56.2

Underwriting result (gross) 16.3 12.5

19

to participate in the less loss-prone middle andupper layers. In this segment too we were success-ful in obtaining improvements – sometimes mark-edly so – in programmes that had suffered heavylosses in past years, as a consequence of whichour premium income in the year under reviewgrew by 32.4% to EUR 8.7 million. With a highlygratifying loss experience we recorded a goodprofit of EUR 5.8 million for our portfolio.

In overall terms, we achieved a year-on-yearincrease of 17.0% in gross premium income forthe other lines in the year under review. Sincethe loss ratio also decreased by 5.4 percentagepoints, we were pleased to generate anotherclearly positive underwriting result.

As a member of the Hannover Re Group, we sharein the experience of the international (re-)insur-ance markets via internal retrocessions withinthe Group. By adding blocks of foreign businessto our portfolio we are able to ensure better geo-graphical diversification, which serves to stabiliseresults from the medium- to long-term perspec-tive. In the year under review, however, the inter-national markets were severely impacted by theterrorist attacks of 11 September. For the Han-nover Re Group, too, these events produced a sub-stantial loss that is reflected in our profit andloss account. Overall, then, with a gross under-writing deficit of EUR 360.7 million the inter-national portion of our business deterioratedconsiderably compared to the previous year. Yetthe events in the USA triggered a hitherto un-precedented market hardening with massive in-creases in premiums and deductibles as well asfar-reaching exclusions and limitations of liability.We are therefore confident that over the next twoto three years we can recoup our losses in theyear under review through a very favourableresults trend in foreign business, provided the lossexperience at least remains in line with the multi-year average.

In the wake of the terrorist attacks of 11 Sep-tember the following tendencies could be ob-served on our key international markets:

Insurance and reinsurance markets in Europerevived appreciably in the year under review. Inthe United Kingdom the reinsurance sector im-proved disproportionately strongly, and premiumincreases were attained in virtually all lines. Many

companies intensified their concentration ontheir true core business, consequently leading tothe relinquishing of non-strategic segments. Thewithdrawal of some market players followingthe events of 11 September – amongst others,some Lloyd's syndicates stopped writing busi-ness or at least heavily reduced their accept-ances – further cut into the volume of avail-able reinsurance capacity and made additionalpremium increases possible. Hannover Re ex-ploited these positive changes to expand its port-folio, continuing to prefer middle and higherlayers of non-proportional programmes.

The French insurance industry was still over-shadowed in the year under review by the after-effects of the 1999 winter storms. Since they oc-curred so late in the year these events did notsignificantly impact the 2000 renewals, and itwas not until the year under review that appre-ciable premium increases – from which our port-folio also benefited – were achieved. The 2001financial year also witnessed two large corpor-ate mergers, as part of which highly active re-insurers on the French market were absorbedinto larger groups. The drop in reinsurance cap-acity triggered further premium increases. Themost prominent local loss event was the explosionat a fertiliser plant in Toulouse, which caused eco-nomic losses in the order of EUR 1.5 billion. Thisevent similarly constituted a sizeable major lossfor our account. Following the terrorist attacks of11 September in the USA the French insuranceand reinsurance industry joined forces with theFrench government to set up a pool for terrorismrisks in which Hannover Re also participated.

Results of our foreign business

Management report Premium growth and results

20

In the North American insurance market risingloss ratios provided a good basis for sweepingpremium increases, which averaged around 30%in the reinsurance sector. Yet these increaseswere not sufficient to significantly improveresults in all lines of business. Many marketplayers responded by cutting their proportionalcapacity. 2001 also witnessed substantial majorloss events, of which tropical storm "Allison" –with insured losses of almost USD 5 billion – wasthe most prominent. In the year under reviewwe benefited from our adherence to a profit-oriented underwriting policy in the previousyears and our strict orientation towards non-proportional covers. Hannover Re expanded itsportfolio in sharply hardening lines, such as li-ability business. The terrorist attacks of 11 Sep-tember further transformed the US market. Pre-mium increases in some cases reached levelscomparable to the mid-1980s during the liabilityinsurance and reinsurance crisis in the UnitedStates. Furthermore, terrorism risks were excludedfrom most reinsurance treaties and transferredto non-proportional treaties priced on a basiscommensurate with the risk. Hannover Re wasone of the leading reinsurers to offer these covers.

Asian business was hampered by soft insuranceand reinsurance markets. The price level for na-tural hazard coverage, in particular, remained un-satisfactory. In response to the market situationHannover Re continued to prioritise non-propor-tional treaties in the year under review, since itwas able here to achieve adequate premiums.It also focused on improving the diversificationof the portfolio in order to bring about moreeffective risk spreading. Unprofitable partici-pations, on the other hand, were reduced. It isgratifying to note that in Malaysia Hannover Rewas able to expand its market position via its ownbranch office. Satisfactory results were postedthanks to the absence of conspicuous majorlosses.

The international aviation market, which Han-nover Re serves from a central division bearingworldwide responsibility, was heavily impactedin the year under review by the terrorist attacksof 11 September. While premium increases could

already be discerned at the beginning of theyear in both the insurance and reinsurance sec-tors, the terrorist attacks in the USA fundamen-tally changed the aviation market. The losses re-sulting from these events surpassed all previousloss events many times over and placed a heavystrain on results – including those of HannoverRe. Aviation insurers reacted immediately withmassive premium increases and a limitation ofliability for third-party losses on the ground toUSD 50 million. Furthermore, additional pre-miums were required for the war and terrorismrisks under liability policies. Substantial premiumincreases were also implemented in aviationproduct liability and general aviation insurance,with the result that premiums and conditionsimproved markedly in the aviation sector as awhole. Hannover Re optimally exploited this mar-ket situation with its underwriting policy and –compared to the market in general – gener-ated disproportionately strong premium growthin its treaty renewals while at the same timeobtaining considerably more satisfactory condi-tions. The most notable loss event subsequent to11 September was the crash of an Airbus pas-senger jet over New York, although our accountwas only minimally affected.

Management report Premium growth and results

21

Management report Investments

Satisfactory growth in net investment income

Investments

The year under review was once again remark-able in many respects for the worldwide financialmarkets. While the forecasts of economic growthin the leading national economies were still posi-tive at the beginning of the year, clear signs of aslowdown – including in Germany – very quicklyemerged and steadily grew over the course ofthe year. The terrorist attacks on 11 Septemberin the USA added considerably to the strain. Theinternational central banks reacted to the gen-eral cyclical downturn with massive interest ratecuts. In contrast to the numerous sweeping inter-est rate reductions by the US Federal ReserveBoard, the European Central Bank was relativelyslow to cut interest rates and took less aggressiveaction. Overall, it trimmed prime rates by a mere150 basis points to 3.25% as at year-end. Theflagging economy and repeated interest ratecuts naturally gave corresponding impetus tobond markets in the short to intermediate ma-turity range. Uncertainty among investors, espe-cially in the wake of 11 September, prompted aflight to quality, as a consequence of which thestrongest price gains were on securities issued byfirst-rate borrowers and government bonds.

On the international equity markets 2001 will godown as one of the most difficult years in history.Falling capital market rates as well as tax andpension reforms in Europe created a fundamen-tally favourable environment. Yet alarming cor-porate news in the course of the year – withsome companies repeatedly compelled to revisedownwards their profit expectations – gave riseto dramatic price declines on all major stock ex-changes. In this general climate the terrorist at-tacks in the USA triggered virtual panic selling,causing stocks to nosedive to new record lowsfor the year. Although equity markets had re-covered appreciably by year-end, the major na-tional and international indices still closed withheavy losses; the Dax and the Euro Stoxx 50, forexample, gave up around 20% of their value onthe year. The euro continued to depreciate in thecourse of the year, especially against the USdollar. This held true despite a rally in the sum-

mer months, since August subsequently usheredin another protracted downslide.

Given these extremely difficult circumstances, ourinvestment portfolio and the net investment in-come generated from these holdings developedhighly satisfactorily in the year under review.

Our total portfolio of self-managed assets (i.e. ex-cluding deposits with ceding companies) in-creased in the reporting period by an impres-sive 9.5% or EUR 245.0 million to EUR 2,832.8million. This growth was due not only to move-ments in exchange rates but also to the higherinflow of liquidity from the technical account.Extraordinary cash outflows, on the other hand,were booked in merely a moderate amount.Claims payments associated with the terroristattacks in the USA did not significantly impactthe development of our investment portfolio inthe year under review.

In light of our unfavourable assessment of thestock markets, we systematically continued thereduction of our equity holdings that we hadinitiated towards the end of the previous year.The volume of dividend-carrying securities in ourtotal investment portfolio therefore decreasedsignificantly by EUR 103.8 million to EUR 298.6million as at year-end. The equity allocation con-sequently fell by around 5.0 percentage pointsto 10.5% as at 31 December 2001. We continueto limit our equity exposure to liquid Blue Chipslisted on major indices such as the Euro Stoxx50, S&P 500 etc. In the year under review weagain did not make any stock purchases on theNew Market or in comparable market segments.

The focus of our self-managed assets continuedto be on fixed-income securities, which accountedfor a share of 66.2% (previous year: 65%). Whenselecting securities we always ensure that issuershave a first-class rating. The proportion of highlyliquid fixed-income securities with a rating of AAor better – of whom 72% were rated AAA – thusincreased by 4% year-on-year to 91% of our total

22

Management report Investments

portfolio of fixed-income securities. We used thesometimes very drastic declines in yields on fixed-income securities – especially in the wake of theevents of 11 September – to realise profits andshorten the maturity pattern of the portfolio.Realised price gains on the disposal of fixed-

income securities consequentlytotalled EUR 49.3 million andwere clearly in excess of the pre-vious year (EUR 6.3 million).

With the implementation into lawof § 341b German CommercialCode, the insurance industry wasfor the first time permitted tosubdivide investments into fixedassets and current assets in theyear under review. The companymade partial use of the opportun-ity to apply the associated mod-

ified lower-of-cost-or-market principle in the caseof asset items allocated to fixed assets. The totalportfolio of investments valued as fixed assetsamounted to EUR 533.8 million. Had these hold-ings been valued in accordance with the provi-sions relating to current assets, the additionalvolume of depreciation would have totalled EUR21.1 million.

Bearing in mind the loss payments that we stillhave to meet for major losses incurred in the yearunder review, most notably those associated withthe terrorist attacks in the USA, we substantiallyincreased our short-term investments. As at year-end 2001 we held a total amount of EUR 92.0million (previous year: EUR 65.8 million) in short-term assets, including overnight money and timedeposits.

The volatile state of the financial markets hadcorresponding implications for the unrealisedgains remaining in our investment portfolio asat year-end. While unrealised price gains in ourportfolio of fixed-income securities decreased toEUR 35.0 million (previous year: EUR 61.6 mil-lion), the valuation reserves in our equity port-folio shrank by EUR 109.8 million to EUR 19.4million. This decline contrasted with realisedgains from active portfolio management. On bal-ance, therefore, unrealised price gains for ourtotal investment portfolio stood at EUR 165.7

million as against EUR 282.8 million in the pre-vious year.

Despite the decreased average yield on invest-ments and the shortening of the maturity pat-tern, ordinary investment income fell by a mereEUR 1.5 million to EUR 259.1 million in the yearunder review. This modest decline was due notonly to exchange rate factors and the increasedinvestment portfolio, but also – and most import-antly – to considerably higher deposit interestcredited principally under life and financial re-insurance treaties. These credits are generallyopposed by corresponding expenditures, whichare booked to the technical account.

In view of the tense state of the financial mar-kets, we were highly satisfied with the extraor-dinary income from investments. Realised profitson disposals of EUR 102.1 million contrasted withlosses on the disposal of investments totallingEUR 7.9 million, thus generating another posi-tive balance (including appreciation/depreci-ation) of EUR 75.0 million (previous year: EUR60.4 million).

Overall, then, we generated a gratifying net in-vestment result of EUR 223.3 million (previousyear: EUR 229.6 million). Excluding deposits withceding companies and interest on deposits, thiscorresponded to a net return of 7.7% on our in-vestment portfolio.

AA19%

AAA72%

A3%

< BBB3%

BBB3%

Rating of fixed-income securities

23

As a reinsurer, our business naturally involveseconomic risks of various types in our individualbusiness segments. The acceptance of risks andthe professional management of this risk port-folio constitute the core business of a reinsurancecompany. Our risk management is based upon acorporate strategy geared to generating a sus-tained increase in the value of the company. Thismeans that we purposefully enter into entrepre-neurial risks provided the associated opportun-ities promise an appropriate increase in the valueof the company. We have at our disposal a largenumber of efficient management and controlsystems, which vary in their design and degreeof reporting detail. The core risk management

elements are set out in guidelines that apply toall areas of E+S Rück. Within the scope of our riskmanagement system all conceivable risks fromthe current perspective which could jeopardisethe performance and survival of our company arerecorded systematically and comprehensively.The up-to-date status of our risk portfolio, bothon the level of individual risks and accumulationrisks, is ensured by means of defined reportingprocedures and an annual risk inventory. Risksare quantified with an eye to their probability ofoccurrence and the potential loss. This approachalso takes into consideration the effectivenessof the implemented control measures.

1 000

500

1 500

2 000

2 500

3 000

3 500

4 000

0

19921993

19941995

19961997

19982000

20011999

Investments

in EUR million

Total

Shares, units in unit trusts and other variable-yieldsecurities as well as bearerdebt securities and otherfixed-income securities

Deposits retained

Loans to affiliated companiesand other loans

Other investments

Management report Risk report

Risk report

Overall system of risk monitoring and management

24

Overall responsibility for risk management isdetermined according to the specific strategicsegments, within which the responsible boardmembers define the operating objectives. Riskmanagement is locally integrated into our or-ganisation. This local allocation of responsibility isintended to ensure that risks can be identified,reported and managed as quickly as possible. Tothis end, we use a number of different indicatorsthat are tailored to individual risks and provideprompt information about any potentially unde-sirable developments.

A central risk coordinator ensures that all riskmanagement activities are monitored, documen-ted and coordinated; the coordinator also bearsresponsibility for describing the risk situation ofthe company as a whole within the scope of thereporting system.

Risk categories

Global risks

We understand global risks to mean externalrisks upon which we are unable to exert anydirect influence. They may arise, for example, asa result of changes in the legal framework (in-cluding changes in the general regulatory or taxsituation), through social trends or as a conse-quence of developments in the insurance indus-try.

By way of illustration, a significant decline in de-mand for reinsurance coverage would constitutea major risk for our company. In life reinsurance,for example, this could be caused by the elim-ination of tax assistance for old-age provision.We therefore systematically monitor, inter alia,the tendencies in legislation as well as the newbusiness statistics (number of policies, sums in-sured, and annual premiums).

Strategic risks

Strategic risks refer to specific factors that mayjeopardise achievement of our strategic object-

ives in the individual business segments. Theparamount goal is to safeguard our stable pos-itioning as a reinsurer of above-average profit-ability. Our profit target is to generate an above-average return on the equity made available tous by our shareholders. A system of agreementson targets has been introduced for our manager-ial staff in order to ensure that the various stra-tegic objectives are also pursued on the operatinglevel. Under this system, individual targets arederived from the higher-order strategic objectives.We used company-wide ratios in order to mea-sure objectively the profit contribution made byeach segment or unit to the overall corporateperformance. These key figures facilitate perform-ance controlling and hence are also reflected inthe remuneration received by our managerialstaff.

Technical operating risks

Technical operating risks are of special signifi-cance to reinsurance companies. The technicalrisk lies primarily in the fact that cash flows,which are vital to the insurance business, may

The efficiency of the risk management system isregularly reviewed by internal and external in-stances and adjusted according to the constantlychanging economic environment. Our company'srisk situation can be comprehensively describedby the following risk categories:

• global/external risks,

• strategic risks,

• operating risks, which we subdivide into– technical risks,– investment risks and– operational risks.

Management report Risk report

Indicators tailored to individual risks

provide promptinformation about

potentially undesir-able developments

Stable positioning asa reinsurer of above-average profitability

25

Investment structureoptimised by meansof soundly basedasset/liability man-agement

Management report Risk report

deviate from their expected values. Possible rea-sons here may be inaccurate pricing assump-tions, incorrect estimations of the claims experi-ence – especially with respect to the so-calledrisk of random fluctuations and change – or fail-ures in accumulation controlling.

We have at our disposal various sets of rules inorder to counteract technical risks. In life andhealth reinsurance these include the use of re-liable biometric actuarial bases with statisticallyadequate safety margins. For example, the mor-bidity risk (e.g. for health and critical illness risks)is assessed and monitored on the basis of actu-arial studies of the morbidity experience.

Retrocession is a further key instrument of risklimitation. The business that we accept is notalways carried entirely in our own retention butis retroceded where necessary. Written risks arescrutinised in order to ascertain the extent towhich they promote a balance within a givenportfolio. Our retentions and retrocessions arecalculated and structured accordingly. Whereaspremiums are always payable at the beginningof a contract, risks chiefly derive from the factthat long periods may elapse until we can callon our retrocessionaires and collect on the losses.This entails the risk that retrocessionaires maydefault on payment. When ceding business it istherefore essential to carefully select our retro-cession partners with an eye to their long-termability to meet such financial obligations.

In recent years roughly 93% of our retroces-sionaires on average have received a so-calledinvestment grade rating – with around 89% ofthem being rated A or better. In this context itshould, however, be added that the remaining7% of our retrocessionaires are not all rated assub-investment grade; many of them do not havea rating because they transact only a minimalvolume of reinsurance or have discontinued suchbusiness.

Our assessment of our retrocessionaires is guidedby the opinions of internationally recognised rat-ing agencies and supported by our own research

based on market knowledge and balance sheetanalyses.

Investment operating risks

The consistent principle underlying our invest-ment strategy is the goal of generating an op-timal contribution to the business result. This isprimarily accomplished by means of soundlybased asset/liability management. Risks in theinvestment sector consist most notably of mar-ket, credit and liquidity risks. Company-wide in-vestment guidelines are in force throughoutHannover Re, and compliance is subject to con-stant monitoring. The principle of separationof functions – i.e. keeping a strict distinctionbetween trading, settlement and risk controlling– is applied up to the level of management andconstitutes a further integral element of our riskmanagement. Risks in the investment sectorare countered using a broad range of efficientmanagement and control mechanisms whichare geared to the rules adopted by the FederalBanking Supervisory Office and the Federal Super-visory Office for Securities Trading.

26

The rating structure of our fixed-income securities was as follows:

Subject to the following assumptions as at thebalance sheet date, the fair market value of ourinvestments would develop as follows:

Operational risks

By operational risks we have in mind unexpectedlosses attributable to operational hazards suchas human error, criminal intent, inadequate con-trols or organisational shortcomings. The failureof technical equipment, especially in the case ofthe data processing infrastructure and the avail-ability of the applications it provides also poses asignificant risk to our company. In order to min-imise these risks we invest systematically in im-

Assessment of the risk situation

Given the information currently available to us,we do not perceive any risks which could jeop-ardise the continued existence of our company

in the short or medium term or which could im-pair the assets, financial position or net incomein a significant or sustained manner.

proving the security and availability of our infor-mation technology. This includes, for example,the comprehensive use of virus protection andfiltering software as well as measures to optimisenetwork stability. We shall continue to meet theexacting security standards to which our infor-mation processing is subject, and with this aim inmind the position of IT Security Officer has beencreated to coordinate all security-related ITissues.

Management report Risk report

AAA 77.1 917 311 6.3 25 383 82.6 325 331

AA 21.5 255 687 47.9 193 727 0.5 2 127

A 0.8 9 494 17.3 69 908 8.8 34 655

BBB – – 10.4 41 958 – –

< BBB 0.6 6 918 18.1 73 730 8.1 31 951

Total 100.0 1 189 410 100.0 404 706 100.0 394 064

Rating Government bonds Corporate bonds Other fixed-income securities

in % in EUR thousand in % in EUR thousand in % in EUR thousand

Equities Stock prices -20% (76 294)

Fixed-income securities Yield increase +1 percentage point (65 040)

Fixed-income securities Yield decrease - 1 percentage point 68 853

Portfolio Scenario Portfolio change based on fair value

in EUR thousand

27

Human resources

As a reinsurer and highly specialised financialservices provider, skilled and motivated staff area crucial success factor for our company. We con-sequently implemented further improvements inour personnel advancement and assessment sys-tems in the year under review.

We set great store in the further training of ouremployees. Our internal training programmeslargely cover the requirements pinpointed atthe annual staff interviews. In this context, our"pool of experts" once more proved its worth inthe year under review – especially with regardto training in specific reinsurance topics. The aimis that experienced staff should pass on theirexpertise to new employees in a modular seriesof seminars. In addition to these reinsurancecourses increasing importance is attached toseminars on so-called "soft skills" such as pre-sentation techniques, project management andteam leadership. We draw upon outside special-ists to provide these courses. Our executive simu-lation game has evolved into a particularly popu-lar component within our overall advancedtraining scheme. Further enhanced over the pastyear, this simulation of real situations in the cor-porate world confronts groups of employees,each representing a reinsurance company, withthe complex issues that abound on the reinsur-ance market. This alternative mode of learningteaches both specialist expertise and manage-ment qualities.

As a further step, we improved the opportunitiesfor our staff to structure their working environ-ment on a flexible basis. In this connection, weenlarged the scope of our telecommuting. Ourpositive experiences of the previous year encour-aged us to offer this type of "out-of-office" workto a larger group of employees – an alternativethat was once again well received. We also ex-panded our online job service. This in-house em-ployment market makes it easier for all em-ployees to obtain information about vacantpositions and perhaps to move into a new areaof responsibility.

In the year under review we also refined ourpersonnel development tools for our managerialstaff. As a first step, we set up an employee feed-back system: in a process that is transparent forboth staff and managers, the executive first as-sesses him- or herself in order to arrive at a self-image. This is then compared with the findingsof the employee survey, thereby revealing dis-crepancies, which are then analysed in a feed-back discussion between the manager and hisor her staff – under the auspices of an impartialfacilitator. As a special measure aimed at thetwo upper levels of management, we also con-ducted a skill analysis in which managerial staffand the entire executive board assessed eachother's competencies. The final outcome pro-duced a point score that was incorporated as anew criterion into our remuneration system.