annual report 2007 bank mandiri (europe) ltd annual report 2007.pdfannual report 2007 bank mandiri...

TRANSCRIPT

Annual Report 2007

Bank Mandiri (Europe) Ltd

Bank Mandiri (Europe) LtdCardinal Court, 23 Thomas More StreetLondon E1W 1YY

Tel: +44 (0)20 7553 8688Fax: +44 (0)20 7553 8699SWIFT: BEIIGB2L

www.bkmandiri.co.uk

Shared Values and Culture

TrustThrough reliability, establish confidence and positive outlook among stakeholders in open andsincere relationships.

IntegrityConsistently think, speak and behave honestly, guarding dignity and upholding the code ofprofessional ethics.

ProfessionalismCommitted to complete work with accuracy based on the highest competence and with a fullsense of responsibility.

Customer FocusContinuously position customers as main partners who can mutually benefit from sustained growth.

ExcellenceContinuously create and carry out improvements in all areas to achieve optimum value added results.

Bank Mandiri Network

PT BANK MANDIRI (PERSERO) TBK

HEAD OFFICE

Plaza Mandiri

Jl. Jend. Gatot Subroto, Kay 36–38

Jakarta 12190, Indonesia

Tel: +62–21 526 5045, 526 5095

Fax: +62–21 526 5008, 526 5017

Website: www.bankmandiri.co.id

SWIFT: BEIIIDJA

HONG KONG BRANCH

7th Fl, Far East Finance Centre

16 Harcourt Road, Queensway

Hong Kong

Tel: + 852–2527–6611

Fax: + 852–2529–8131

SWIFT: BBUDI–IKI–IH

Website: www.bankmandirihk.com

SINGAPORE BRANCH

3 Anson Road #12-01/02

Springleaf Tower

Singapore 079909

Tel: (65) 6213 5688

Fax: (65) 6438 3363

SWIFT: BEIISGSG

Website: www.ptbankmandiri.com.sg

CAYMAN ISLANDS BRANCH

Cardinal Plaza, 3rd Floor

#30 Cardinal Avenue

P0 Box 10198 APO

Grand Cayman, Cayman Islands

Tel: + 1–345–945–8891

Fax: + 1–345–945–8892

SWIFT: BEIIKYKY

SHANGHAI REPRESENTATIVE OFFICE

3401, Bank of China Tower

200 Yin Cheng (M) Road

Pudong New Area, Shanghai, 200120

People's Republic of Chiua

Tel: + 86–21–5037–2509

Fax: + 86–21–5037–2507

DILI BRANCH

Ave Presidente Nicolau Lobato No. 12,

Colmera, Dili – Timor Leste

Tel: + 670–331–7555 or + 670–331–7777

Fax: + 670–331–7444 or + 670–331–7190

SWIFT: BEIIIDJA

Bank Mandiri: Head Office, Jakarta.

< PAGE 1

Contents

Financial Highlights 2

Board of Directors and Management 3

Chairman’s Statement 5

Director’s Report 7

Board of Directors 8

Management 10

Statement of Director’s Responsibilities 11

Auditor’s Report 12

Corporate Profile and Services 13

Profit and Loss Account 17

Balance Sheet 18

Notes to the Financial Statements 19

Bank Mandiri Network Inside Back Cover

PAGE 2 >

In US$ 000's Restated

2003 2004 2005 2006 2007

US$ 000 US$ 000 US$ 000 US$ 000 US$ 000

Income Statement

Net interest income 4,197 4,019 4,942 6,298 7,692Fees & commissions receivable 3,237 3,571 3,323 3,700 4,867Operating income 7,434 7,590 8,265 9,998 12,559Overhead expenses (1) 5,261 5,375 7,380 6,488 6,399Profit before tax & provisions 2,173 2,215 885 3,510 6,160Provisions for bad debts 299 718 3,203 (2,032) (662)Provisions for commitments & contingencies – – 1,499 – –Profit (loss) before taxation 1,874 1,497 (3,817) 5,542 6,822Taxation – – – 873 (1,997)Profit after taxation 1,874 1,497 (3,817) 6,415 4,825

Balance Sheet

Loans and advances to banks 29,325 46,880 32,638 18,415 57,311Loans and advances to customers (2) 47,846 57,379 68,929 115,371 158,467Debt securities (3) 63,676 63,508 72,377 74,731 52,829Total assets 144,301 172,691 179,694 218,570 274,635Deposits from banks 58,134 68,138 73,007 104,913 141,938Customer accounts 27,382 35,616 39,708 37,283 60,981Debt securities in issue – 8,940 8,514 10,000 –Shareholder's funds (4) 57,675 59,172 55,457 62,827 67,244

Ratios

Capital adequacy ratio 71.3% 62.8% 51.9% 36.3% 29.9%Total equity to total assets 40.0% 34.3% 31.0% 28.4% 24.5%Return on average equity 3.3% 2.7% –8.2% 10.7% 10.4%Return on average assets (5) 1.6% 1.4% 0.5% 1.8% 2.7%

Financial Highlights

FY03 FY04 FY05 FY06 FY07

7,692

6,298

4,9424,0194,197

Net Interest Income (US$ 000’s)

FY03 FY04 FY05 FY06 FY07

4,867

3,7003,3233,571

3,237

Fee–Based Income (US$ 000’s)

FY03 FY04 FY05 FY06 FY07

12,559

9,998

8,2657,5907,434

Operating Income (US$ 000’s)

(1) 2005 Includes exceptional costs in respect of:(a) Staff restructuring costs US$154k(b) Premises move costs of US$528k(c) Exceptional client administration and legal costs relating to a borrower in default US$377k

(2) Net of specific provisions(3) Comparative after adoption of FRS26 to 2005(4) Shareholder's funds restated for 2005 to include reserves of available–for–sale & hedge accounting(5) Excluding tax and bad debt provisions

Basis for Calculation of the RatiosCapital Adequacy Ratio – Capital adequacy ratio is calculated in line with the format prescribed by theFinancial Services AuthorityTotal Equity to Total Assets – The total equity to total assets ratio is calculated by dividing theshareholders funds (see note 20) by the total assets after deducting specific provisions for bad debts.Return on Average Equity – The return on average equity is calculated by dividing profit before tax bythe average equity during the year.Return on Average Assets – The return on average assets is calculated by dividing profit before tax andprovisions for bad debts by the average total assets during the year.

< PAGE 3

Board of Directors and Management

Directors

Appointed Resigned

Mr G Subadio : Chairman 10/11/05 –

Mr K Widjajanto : Chief Executive 16/09/05 –

Mr M S Nasution : Non-Executive Director 09/11/07 –

Mr P J Quinn : Non-Executive Director 31/05/07 –

Mr J K Williams : Non Executive Director 02/07/07 –

Mr G Penny : Non-Executive Director 02/07/99 23/02/07

Mr E S Lacy : Non Executive Director 01/01/01 30/06/07

Management

Mr K Widjajanto : Chief Executive

Mr G Turpin : General Manager

Mr R Hutagalung : General Manager

Mr A Joshi : Deputy General Manager

Mr S Wansell : Deputy General Manager

Mr B Battle : Deputy General Manager

Company Secretary

Mr A Joshi : Deputy General Manager and Company Secretary

Auditors

Ernst & Young LLP1 More London PlaceLondon SE1 2AF

Registered Office

Cardinal Court23 Thomas More StreetLondon E1W 1YY

Registration Number: 3793679

PAGE 4 OVERLAY

TotalAssets

up 26%

OperatingIncome

up 26%

Profitbefore tax

up 23%

StrongCAR

30%

PAGE 4 OVERLAY (reverse)

PAGE 4 >

< PAGE 5

Chairman’s Statement

I am pleased to present the Report and

Accounts of Bank Mandiri (Europe)

Limited for its eighth year as a wholly

owned subsidiary of PT Bank Mandiri

(Persero) bk, Indonesia.

The Bank performed well in 2007 and

our pre–tax profits reached US$6.82

million, this was 23% higher than the

previous year and was the best result

that BMEL has ever recorded; this was

the second year in a row that we have

reported record profits.

In 2007 we wrote back US$1.37 million

of provisions for bad debts but after

new provisions of US$0.71 million for

estimated credit losses, the net write

back from the provision account to the

profit and loss account was US$0.66

FY03 FY04

FY05

FY06 FY07

6.822

5.542

-3.817

1.4971.874

Pre–Tax Profit (millions)

million. Excluding the write back of

provisions, operating profits grew by

75.6% from US3.51 million to US$6.16

million.

Tax losses carried forward from prior

years have now been fully utilised and

the Bank was obliged to make an

accrual for the payment of corporation

tax of US$1.99 million in 2007 such that

reported net profits after taxes were

US$4.83 million.

In 2007 we continued to focus on

growth in our core lending activities in

trade finance and ship finance and this

fuelled growth in our total assets by

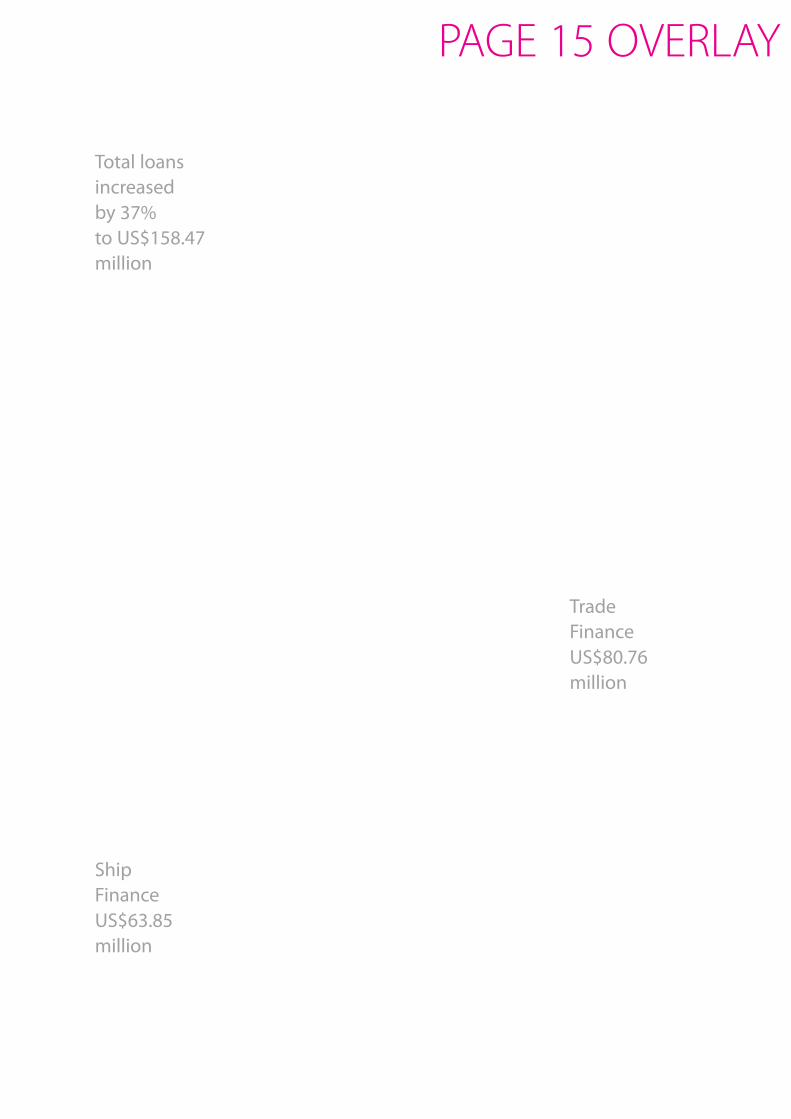

26% to US$274.63 million and 37%

growth in our loans and advances to

banks and customers to US$158.47

million. Given the turbulence in the

financial markets in the last quarter of

2007 resulting from the “sub–prime

mortgage crisis” I should like to confirm

that the Bank has no sub–prime

mortgage exposure in its balance sheet

and has never been involved in the

sub–prime mortgage market either

directly or indirectly.

The Bank actively manages its assets

and liabilities to ensure that business

growth is supported by the

appropriate level of funding and

liquidity resources; more details as to

the Bank’s liquidity management are

contained in note 24 to the accounts.

The growth in the balance sheet was

reflected in net interest income which

We could not have achieved such an excellentresult in 2007 without the hard work of all ourstaff, the continued business and co–operationfrom our customers and market counterpartiesand the support of our parent bank

“

”

FY03 FY04 FY05 FY06 FY07

7.7

6.3

4.04.24.9

Net Interest Income ( millions)

FY03 FY04 FY05 FY06 FY07

144.3172.69 179.69

218.57

274.63

Total Assets ( millions)

PAGE 6 >

grew by 22.13% to US$7.7 million. As

well as strong growth in its lending

business the Bank was also successful

in growing its fee income from off

balance sheet and customer service

activities which grew by 31.55% to

US$4.86 million.

Notwithstanding the strong growth

in assets, the Bank maintained

adequate capital resources to support

its business activities and our

capital adequacy ratio measured in

accordance with Basel 1 guidelines

was 29.91%.

This ratio is well above accepted

industry norms and gives the Bank

ample scope to further expand its

business and profitability.

during 2007 and I should like to

welcome to them to the Board.

We could not have achieved such an

excellent result in 2007 without the

hard work of all our staff, the continued

business and co–operation from our

customers and market counterparties

and the support of our parent bank. On

behalf of the Board, I should like to

thank you all and we look forward to

working with you in 2008 and the

years’ ahead.

Gatut Subadio,

Chairman

January 2008

The Bank did all things necessary to

ensure compliance with the changes in

regulatory guidelines and legislation

that came into force in 2007 and to

prepare for the implementation of

Basel 2 and the Capital Requirement

Directive with effect from 1st January

2008. As a result of these efforts, we

believe that the Bank has a solid

platform from which to grow its

business further in 2008.

Mr. Penny and Mr. Lacy retired from the

Board during 2007 and I should like to

thank them for the guidance that they

provided during their tenure as

Non–Executive Directors. Mr. Quinn,

Mr. Williams and Mr. Nasution were

appointed as Non–Executive Directors

FY03 FY04 FY05 FY06 FY07

29.9%

36.3%

62.8%

71.3%

51.9%

Capital Adequacy Ratio (US$ 000’s)

Trade Finance

Secondary Markets

Ship Finance

Trade Finance

Secondary Markets

Ship Finance

Type of Loans (US$ 000’s)

< PAGE 7

Director ’s Report

The Directors present their Report andthe Financial Statements for the yearended 31 December 2007.

Results and Dividends

The trading profit after tax for the yearamounted to US$4,825,199

The Directors do not recommend thepayment of a dividend.

Principal Activities andReview of Business

The Bank is an authorised UK Bankunder the Banking Act 1987 and carrieson international corporate andinstitutional banking business, whichincludes the following activities:

(1) Trade Finance.

(2) Ship Finance.

(3) Inter–bank Deposits.

(4) Current and Deposit Accounts.

(5) Purchase of investment Securities,Marketable Securities and Sec-ondary Market Debt.

Details of the Review of Businesshave been covered in the Chairman'sStatement.

Auditors

Ernst & Young LLP have expressed theirwillingness to continue in office asauditors. A resolution proposing theirre–appointment and giving authorityto the directors to fix theirremuneration will be tabled at the nextAnnual General Meeting.

By order of the Board

A Joshi,Company Secretary14 February 2008

Principal Risks and Uncertainties

The Board, in conjunction with SeniorManagement of the Bank, hasestablished comprehensive policiesand procedures in order to manageand mitigate the risks and uncertaintiesfacing the Bank and the on–goingimplementation of such is monitoredby management and through a robustand independent internal auditfunction. More detail as to the principalrisks and uncertainties facing the Bankand the mitigation thereof is containedin Note 24 to the Financial Statements.

Fixed Assets

Details of the Bank's fixed assets areshown in Note 12 to the financialstatements.

Disclosure of Information

So far as each Director is aware, there isno relevant audit information of whichthe Bank's auditors are unaware; andeach director has taken all steps thatthey ought to have taken as a Directorin order to make themselves aware ofany relevant audit information and toestablish that the Bank's auditors areaware of that information.

PAGE 8 >

Board of Directors

In accordance with the best principles of corporate governance the Bank’s activities are directed by a Board which is comprisedof three appointees from our parent bank and two non-executive directors, as follows:

Gatut Subadio (Chairman)

Graduated with a Bachelor Degree inIndustrial Engineering from BandungInstitute of Technology in 1984 andobtained an MBA in InternationalBusiness and Finance from theUniversity of Miami in 1992.

He is a seasoned international bankerwho started his banking career in 1984as an analyst at Bank Bumi Daya inIndonesia. In 1999 he joined Bank

Mandiri where he has held a number ofsenior international banking positions.Since 2005 he has been Head ofInternational Banking and CapitalMarket Services at Bank Mandiri,Jakarta Indonesia.

Appointed as Chairman of BankMandiri (Europe) Limited in 2005.

Ken Widjajanto (Chief Executive)

Graduated with a Bachelor Degree inEconomics from the University ofIndonesia in 1983 and obtained anMBA degree from the Cleveland StateUniversity (Ohio, USA) in 1995.

He began his banking career in 1993at Bank Dagang Negara, Indonesiawhere he gained a broad experiencein both plantation finance andcorporate lending.

In 1999 he joined Bank Mandiri as asenior manager in the loan recoveryand debt work-out unit and wassubsequently responsible for settingup and managing Bank Mandiri’sinternational branch in Timor Leste.

Appointed as Chief Executive of BankMandiri (Europe) Limited in 2005.

Patrick Quinn (Non–Executive Director)

Associate member of the CharteredInstitute of Bankers and an Associatemember of the British Institute ofManagement.

During a long banking career, whichstarted at National Westminster Bank in1960, he has held a number of seniorpositions both in London and overseas,including directorships at AMEX BankLimited, Chartered West LB andas a Director & General Manager ofYamaichi Bank Plc.

In addition to his non-executivedirectorship at Bank Mandiri (Europe)Ltd, since 2000 he has held a position asa Non-Executive Director of HabibsonsBank Ltd.

Appointed as a Non Executive Directorof Bank Mandiri (Europe) Ltd in 2007 andis Chairman of the Audit Committee.

< PAGE 9

Mr. Mansyur Syamsuri Nasution (Non–Executive Director)

Graduated from the Institute ofAgronomy Bogor (Indonesia) in 1981and completed his Master Degree inAgronomy in University of Colorado(USA) in 1991.

In 1983, he began his career in bankingby joining Bank Bumi Daya, Jakarta,Indonesia. In 1999 he joined BankMandiri, as a division head in the loanrecovery and debt work-out unit.

He is currently Head of the CorporateSecretary Group of Bank Mandiri,Jakarta, Indonesia.

Appointed as a Non-Executive Directorof Bank Mandiri (Europe) Limited inNovember 2007.

John Williams (Non–Executive Director)

Fellow of the Institute of CharteredAccountants of England and Wales;qualified as a chartered accountantin 1968. Worked for three years withPrice Waterhouse and Co in Nassau,Bahamas before joining The DeltecBanking Corporation Limited in 1973where, after working in several groupcompanies, in 1977 he became GeneralManager of the Nassau operationbefore leaving in 1980.

He returned to England to work withTrade Development Bank and joined

American Express Bank Limited, uponits purchase of Trade DevelopmentBank, as Chief Financial Officer forEurope, Middle East and Africa until hisretirement from full time employmentin 2000. Since then he has beenworking as a consultant to companiesin the financial sector.

Appointed as a Non-Executive Directorof Bank Mandiri (Europe) Ltd in 2007and is Chairman of the RemunerationReview Committee.

Board of Directors (Continued)

PAGE 10 >

Management

The management of BMEL comprises six members, consisting of the Chief Executive, two General Managers and three DeputyGeneral Managers.

Ken WidjajantoChief Executive

Gordon TurpinGeneral ManagerRisk & Operations

Rudy HutagalungGeneral ManagerCorporate & Treasury

Brendan BattleDeputy General ManagerOperations

Ajay JoshiDeputy General Manager –MISA & IT

Steve WansellDeputy General ManagerCorporate & Treasury

< PAGE 11

Statement of Directors’ Responsibilities

The Directors are responsible for

preparing the Annual Report and

the Financial Statements in accordance

with applicable United Kingdom

Generally accepted Accounting Practice.

Company Law requires the Directors to

prepare financial statements for each

financial year which give a true and fair

view of the state of affairs of the Bank

and of the profit or loss of the Bank

for that period. In preparing those

The Directors are responsible forkeeping proper accounting recordswhich disclose with reasonableaccuracy at any time the financialposition of the Bank and enable themto ensure that the financial statementscomply with the Companies Act 1985.They are also responsible forsafeguarding the assets of the Bankand hence for taking reasonable stepsfor the prevention and detection offraud and other irregularities.

financial statements, the Directors

are required to:

• Select suitable accounting policies

and then apply them consistently;

• Make judgments and estimates

that are reasonable and prudent;

and

• Prepare the financial statements on

the going concern basis unless it is

inappropriate to presume that the

Bank will continue in business.

PAGE 12 >

Auditor ’s Report

Independent Auditor's report to

the members of Bank Mandiri

(Europe) Limited

We have audited the company's

financial statements for the year ended

31 December 2007 which comprise the

Profit and Loss Account, Balance Sheet

and the related notes 1 to 27. These

financial statements have been

prepared on the basis of the

accounting policies set out therein.

This report is made solely to the

company's members, as a body, in

accordance with Section 235 of the

Companies Act 1985. Our audit work

has been undertaken so that we might

state to the company's members those

matters we are required to state to

them in an auditors' report and for no

other purpose. To the fullest extent

permitted by law, we do not accept or

assume responsibility to anyone other

than the company and the company's

members as a body, for our audit work,

for this report, or for the opinions we

have formed.

Respective responsibilities of

directors and auditors

The directors' responsibilities for

preparing the Annual Report and the

financial statements in accordance

with applicable law and United

Kingdom Accounting Standards (UK

Generally Accepted Accounting

Practice) are set out in the Statement of

Directors' Responsibilities.

Our responsibility is to audit the financial

statements in accordance with relevant

legal and regulatory requirements and

International Standards on Auditing (UK

and Ireland).

We planned and performed our auditso as to obtain all the information andexplanations which we considerednecessary in order to provide us withsufficient evidence to give reasonableassurance that the financial statementsare free from material misstatement,whether caused by fraud or otherirregularity or error. In forming ouropinion we also evaluated the overalladequacy of the presentation ofinformation in the financial statements.

Opinion• the financial statements give a true

and fair view in accordance withUnited Kingdom GenerallyAccepted Accounting Practice ofthe state of affairs of the companyas at 31 December 2007 and of itsprofit for the year then ended.

• The financial statements havebeen properly prepared inaccordance with the CompaniesAct 1985; and

• The information given in theDirector's report is consistent withthe financial statements.

Ernst & Young LLPRegistered AuditorLondon14 February 2008

We report to you our opinion as to

whether the financial statements give a

true and fair view and are properly

prepared in accordance with the

Companies Act 1985. We also report

to you, whether in our opinion, the

information given in the director's

report is consistent with the

financial statements.

In addition we report if, in our opinion,

the company has not kept proper

accounting records, if we have not

received all the information and

explanations we require for our audit,

or if information specified by law

regarding directors' remuneration and

transactions with the company is

not disclosed.

We read the Financial Highlights, the

Chairman's Statement and the

Directors' Report and consider the

implications for our report if we

become aware of any apparent

misstatements within them.

Basis of audit opinion

We conducted our audit in accordance

with International Standards on

Auditing (UK and Ireland) issued by the

Auditing Practices Board. An audit

includes examination, on a test basis,

of evidence relevant to the amounts

and disclosures in the financial

statements. It also includes an

assessment of the significant estimates

and judgments made by the directors

in the preparation of the financial

statements, and of whether the

accounting policies are appropriate to

the company's circumstances,

consistently applied and adequately

disclosed.

< PAGE 13

Corporate Profile and Services

The bank that delivers Trade Finance and Shipping Solutions Worldwide

BMEL’s Profile

Bank Mandiri (Europe) Limited (“BMEL”)was established on the 2nd August1999 and is a wholly owned subsidiaryof Bank Mandiri, Indonesia.

When BMEL was established it tookover the banking business of PT BankEkspor Impor Indonesia (Persero),London Branch which had been basedin London since 1992; and previouslysince 1983 as a representative office

BMEL is incorporated and licensed inthe United Kingdom and is a Britishbank under the regulation of the UKFinancial Service Authority (FSA) andhas a complement of 30 staff.

By virtue of its Indonesian ownership,BMEL can offer a more informed andpro-active service in Indonesian relatedbusiness than many of its competitors.

Although BMEL is Indonesian owned,its business activities are not restrictedto Indonesia and we like to considerBMEL, as the bank that delivers TradeFinance and Shipping SolutionsWorldwide.

BMEL’s Services

Some of the principal products andservices we provide are listed below:

• Import letter of credit anddocumentary collection services;

• Supplier credit financing;• Short-term refinancing loans

under import letters of credit;• Export letter of credit services

(advising, confirmation, nego-tiation, etc);

• Bill discounting and forfaiting;• Contract bonding and guarantee

facilities;• Ship financing;• Syndications.

BMEL’s primary business activities areTrade finance and ship finance.

BMEL is staffed by a team ofexperienced banking professionals whoare committed to providing an efficient,informed and personal service.

The Bank has a wide network ofcorrespondent banking contactsdeveloped over many years of servicingits customers' needs throughoutthe World.

BMEL provides tailored financialsolutions specific to individual clientrequirements which assist in the timelysettlement of transactions and cansubstantially benefit the cash flow ofour customers.

”“

TradeFinanceUS$80.76million

ShipFinanceUS$63.85million

Total loansincreasedby 37%to US$158.47million

PAGE 15 OVERLAY

PAGE 15 OVERLAY (reverse)

TradeFinanceUS$....million

ShipFinanceUS$....million

Total loansincreasedby 42.31%to US$164.180

PAGE 14 >

< PAGE 15

PAGE 16 >

Financial Statements

< PAGE 17

Profit and Loss Accountfor the year ended 31 December 2007

In US$ 000’s Notes 2007 2006

US$ 000 US$ 000

Interest receivable [3] 17,044 13,208

Interest payable (9,352) (6,910)

Net interest income 7,692 6,298

Fees and commissions receivable 4,749 3,600

Other operating Income [5] 118 100

Total operating income 12,559 9,998

Administrative expenses [6] (6,195) (6,251)

Depreciation and amortisation [12] (204) (237)

Provision for bad and doubtful debts [10] 662 2,032

Profit/(Loss) on ordinary activities before tax [4] 6,822 5,542

Tax (charge)/credit [8] (1,997) 873

Profit/(Loss) on ordinary activities after tax 4,825 6,415

Retained profit brought forward 13,438 6,355

Retained profit carried forward 18,263 12,770

There were no recognised gains or losses other than those shown above.

The accompanying notes are an integral part of these financial statements.

Bank Mandiri (Europe) Limited

PAGE 18 >

Balance Sheetas at 31 December 2007

ASSETS Notes 2007 2006

US$ 000 US$ 000

Cash and money at call and deposits with central banks 3,231 6,124

Loans and advances to banks [9] 57,311 18,415

Loans and advances to customers [10] 158,467 115,371

Debt securities [11] 52,829 74,731

Tangible fixed assets [12] 457 610

Other assets, prepayments and accrued income [13] 2,340 3,319

Total assets [14] 274,635 218,570

LIABILITIES

Deposits from banks [15] 141,938 104,913

Customer accounts [16] 60,981 37,283

Debt securities in issue [17] – 10,000

Other liabilities, accruals and deferred income [18] 4,472 3,547

Total liabilities excluding capital and other reserves [14] 207,391 155,743

SHAREHOLDER’S FUNDS

Called up share capital [19] 49,000 49,000

Cash flow hedge reserve [25] – 429

Write back of general provision [20] – 668

Available–for–sale reserve [20] (19) (40)

Profit and loss account 18,263 12,770

Total shareholder's funds – equity interests [20] 67,244 62,827

Total liabilities 274,635 218,570

MEMORANDUM ITEMS

Contingent Liabilities:

Guarantees and assets pledged as collateral security [23] 20,139 20,127

The financial statements on pages 16 to 38 were approved by the Board of Directors on 14 February 2008 and are signed on its behalf by:

Mr. Ken Widjajanto,

Chief Executive

The accompanying notes are an integral part of these financial statements.

Bank Mandiri (Europe) Limited

< PAGE 19

Notes to the Financial Statementsfor the year ended 31 December 2007

1. ACCOUNTING POLICIES

The accounting policies, all of which, unless specifically stated, have been consistently applied throughout the year, are detailed below:

a) Basis of preparationThe financial statements have been prepared under the historical cost basis of accounting except for available–for–sale investments and

derivatives financial instruments that have been measured at fair value and in accordance with the special provision of Part VII of the

Companies Act 1985, relating to banking companies, and in accordance with applicable accounting standards and with the Statements of

Recommended Accounting Practice issued by the British Bankers’ Association.

The financial statements have been prepared in US Dollars, as this is the primary currency of the economic environment in which the Bank

operates.

Changes in accounting policiesAs from 1st January 2007, the Bank adopted FRS29 Financial Instruments: Disclosures. As a result, additional disclosures are made providing

information on impairment of loans & advances, interest on impaired loans & advances and additional disclosures on Risk Management.

The change has no recognition or measurement effect for the year ending 31 December 2007.

b) CashflowsUnder Financial Reporting Standard 1 (revised 1996) the Bank is exempt from the requirement to prepare a cash flow statement on the

grounds that it is a wholly owned subsidiary of a parent undertaking that includes the Bank in its own published consolidated financial

statements, which include a consolidated cashflow report.

c) Foreign currenciesTransactions or accruals in foreign currencies are recorded in the profit and loss account at the US dollar rate of exchange applicable to the

related month–end, such that all profits are ultimately booked in US dollars. Assets and liabilities denominated in foreign currencies are

translated into US Dollars at the rates of exchange prevailing as at the Balance Sheet date. Both realised and unrealised foreign exchange

gains and losses are recognised in the profit and loss account.

d) Forward foreign exchange contracts Forward foreign exchange contracts are re–valued at market prices, and the resultant unrealised profits and losses are included in the Profit

and Loss account, unless they qualify for hedge accounting.

Hedge accountingThe Bank makes use of derivative instruments to manage exposures to foreign currency risks, including exposures arising from forecast

transactions. In order to manage particular risk, the Bank applies hedge accounting for transactions, which meet the specified criteria.

e) Fixed assetsFixed assets are included at cost less accumulated depreciation. Depreciation is provided at rates calculated to write off the cost less

estimated residual value of each asset on a straight line basis from the date of use over its estimated useful life as follows:–

Leasehold Improvement 5 years

Computer Hardware 3 years

Computer Software 3 years

Furniture and Fixtures 5 years

Office Equipment 3 years

Motor vehicles 4 years

The carrying values of the tangible fixed assets are reviewed for impairment when events or changes in circumstances indicate the carrying

value may not be recoverable.

f) PensionsThe Bank offers to its staff a money purchase arrangement. The cost to the Bank is charged to the Profit and Loss account as incurred.

Bank Mandiri (Europe) Limited

PAGE 20 >

1. ACCOUNTING POLICIES (Continued)

g) Provision for bad and doubtful debtsSpecific loan loss provisions are made by specific identification of potential losses on the collection of certain loans, advances, and debt

securities. When establishing specific provisions management consider past and expected credit losses, business and economic conditions,

their knowledge of the borrower and any other relevant factors.

h) Financial Instruments – Initial recognition and subsequent measurementsDate of recognitionThe purchase or sale of financial assets, liabilities and derivatives that require the delivery of assets within the time frame generally

established in the market place are recognised on the trade date i.e. the date that the Bank commits to purchase or sell the assets.

Initial recognition of financial instrumentsThe classification of financial instruments at initial recognition depends on the purpose for which the financial instruments were acquired

and their characteristics. All financial instruments are measured initially at their fair value less/plus any directly related costs.

Held–to–maturity financial investmentsHeld–to–maturity financial instruments are those which carry fixed or determinable payments and have fixed maturities and which the

Bank has the intention and ability to hold to maturity. After initial measurements, held–to–maturity financial investments are subsequently

measured at amortised cost using the effective interest rate method less allowance for impairment.

Available–for–sale financial investmentsFinancial investments classified as available–for–sale are measured at fair value. Unrealised gains and losses are recognized directly in equity

in the "Available–for–sale reserve". When the security is disposed of, the cumulative gain or loss previously recognized in equity is

recognised in the income statement.

Derecognition of financial assets and financial liabilitiesA financial asset is derecognised where: –

• The rights to receive cash flows from the asset have expired; or

• The Bank has transferred its right to receive cash flows from the asset or has assumed an obligation to pay the received cash flows in

full without material delay to a third party; and

• Either (a) the Bank has transferred substantially all the risks and rewards of the asset, or (b) the Bank has neither transferred nor retained

substantially all the risks and rewards of the asset, but has transferred control of the asset.

A financial liability is derecognised when the obligation under the liability is discharged or cancelled or expires.

Determination of fair valueThe determination of fair values of financial instruments is based upon quoted market prices or dealer price quotation for financial

instruments traded in active markets.

i) Impairment of financial assetsThe Bank assesses at each balance sheet date whether there is any objective evidence that a financial asset is impaired. A financial asset is

deemed to be impaired if and only, if, there is objective evidence of impairment as a result of one or more events that has occurred after

the initial recognition of the asset and the loss event has an impact on the estimated cash flows of the financial asset that can be reliably

estimated.

j) Cash flow hedgesForward foreign exchange contracts are used to hedge future sterling expenses. For these the gain or loss on the hedging instrument is

initially recognised directly in equity in the "Cash flow hedge reserve". When a forward foreign exchange contract expires, or is exercised,

or when a hedge no longer meets the criteria for hedge accounting, any cumulative gain or loss existing in equity at that time remains in

equity and is recognised when future sterling expenses are ultimately recognised in the income statement.

Notes to the Financial Statementsfor the year ended 31 December 2007

Bank Mandiri (Europe) Limited

< PAGE 21

Notes to the Financial Statementsfor the year ended 31 December 2007

1. ACCOUNTING POLICIES (Continued)

k) Loans and advancesAfter initial measurement, loans and advances are subsequently measured at amortised cost using the effective interest rate method, less

allowances for impairment. Amortised cost is calculated by taking into account any discount or premium on acquisition and fees and costs

that are an integral part of the effective interest rate. The amortisation is included in "interest income" in the profit and loss account.

l) Income recognitionInterest income is recognised in the profit and loss account as it accrues. Once the recorded value of a financial asset has been reduced due

to an impairment loss, interest income continues to be recognised using the effective interest rate applied to the new carrying amount.

Interest expense is debited to the profit and loss account on an accruals basis.

Fees earned for the provision of services over a period of time are accrued over that period. These fees include commission income. Loan

commitment fees for loans that are likely to be drawn down and other credit related fees are deferred and recognised as an adjustment to

the effective interest rate on the loan.

m) TaxationCorporation tax payable, where applicable, is provided on taxable profits at the current UK tax rate.

n) Deferred TaxationDeferred taxation is recognised in respect of all timing differences that have originated but not reversed at the balance sheet date where

transactions or events that result in an obligation to pay more, or a right to pay less, tax in the future have occurred at the balance sheet date.

Deferred Tax is measured on an undiscounted basis at the tax rates that are expected to apply in the periods in which timing differences

reverse, based on tax rates and laws enacted or substantively enacted at the balance sheet date. Deferred tax assets are recognised only to

the extent that the Directors consider it more likely than not that there will be suitable taxable profits from which the future reversal of the

underlying timing difference can be deducted.

o) Related PartiesThe Bank has taken advantage of the exemption in paragraph 3 (c) of FRS8, from disclosing transactions with related parties that are part

of the Bank Mandiri Group, as consolidated financial statements are publicly available.

p) LeasingAssets held under finance leases, which are leases where substantially all the risk and rewards of ownership of the asset have passed to the

Bank, are capitalised in the balance sheet and depreciated over their useful lives. The capital elements of future obligations under the leases

are included as liabilities in the balance sheet. The interest elements of the rental obligations are charged in the profit and loss account

over the periods of the leases and represent a constant proportion of the balance of capital repayments outstanding.

Rentals payable under operating leases are charged in the profit and loss account on a straight line basis over the lease term.

Bank Mandiri (Europe) Limited

PAGE 22 >

2. SEGMENTAL ANALYSIS

Segmental Information – By Class of BusinessThe directors consider that the Bank does not have more than one class of business namely Corporate & Institutional Banking, and therefore

a disclosure by class of business has been deemed unnecessary.

Segmental Information– By geographic segment

Region: UK & Europe Asia Others Intra–group Total

2007 2006 2007 2006 2007 2006 2007 2006 2007 2006

US$000 US$000 US$000 US$000 US$000 US$000 US$000 US$000 US$000 US$000

Interest receivable 6,313 4,902 9,424 6,015 246 936 1,061 1,355 17,044 13,208

Interest payable (6,699) (4,595) (1,572) (1,430) (252) 0 (829) (885) (9,352) (6,910)

Net interest

income (386) 307 7,852 4,585 (6) 936 232 470 7,692 6,298

Fees and

commissions

receivable 2,986 2,242 1,791 1,328 86 79 4 51 4,867 3,700

Net revenue 2,600 2,549 9,643 5,913 80 1,015 236 521 12,559 9,998

Operating

expenses (2,716) (2,741) (3,275) (2,818) (97) (389) (311) (540) (6,399) (6,488)

Operating

(loss)/profit before

provisions (116) (192) 6,368 3,095 (17) 626 (75) (19) 6,160 3,510

Provisions for

bad debts – – 662 2,032 – – – – 662 2,032

Provisions for

commitments

and contingencies – – – – – – – – – –

Profit/(Loss)

before taxation (116) (192) 7,030 5,127 (17) 626 (75) (19) 6,822 5,542

Total assets

employed 120,313 90,662 121,312 89,639 22,874 28,057 10,136 10,212 274,635 218,570

Total net

assets/(liabilities) (18,617) (9,879) 95,437 55,526 (1,910) 27,763 (7,666) (10,583) 67,244 62,827

Notes:

(i) Geographic segments are based on the ultimate market risk to which the Bank is exposed.

(ii) Operating expenses have been allocated to each geographic segment based on the percentage of income attributed to that

segment.

(iii) The Bank's Capital is not directly attributed to business lines but its benefit is evenly distributed on the basis of assets employed within

each respective segment.

Notes to the Financial Statementsfor the year ended 31 December 2007

Bank Mandiri (Europe) Limited

< PAGE 23

Notes to the Financial Statementsfor the year ended 31 December 2007

3. INTEREST RECEIVABLE 2007 2006

US$ 000 US$ 000

– Due from banks 1,902 1,304

– Debt Securities (inc AFS) 3,946 4,161

– Loans and Advances to customers 10,749 7,546

– Interest accrued on impaired Loans & Advances to customers 177 –

– Other 270 197

17,044 13,208

4. (LOSS)/PROFIT ON ORDINARY ACTIVITIES BEFORE TAX

Is stated after charging:

– Depreciation of owned fixed assets 204 233

– Depreciation of assets held under finance leases – 7

– Operating lease rentals – Buildings 389 373

– Operating lease rentals – Office Equipment 46 52

– Auditors' remuneration for audit work 134 134

– Other fee to Auditors' – taxation services 17 10

– Exceptional consultancy & legal costs incurred as a result of – 331

the administration of a borrower in default

5. OTHER OPERATING INCOME

Gains from sale of available–for–sale financial instruments 25 –

Foreign exchange profit 93 100

118 100

6. ADMINISTRATIVE EXPENSES

Staff Costs:

– wages and salaries 2,594 2,646

– social security costs 303 233

– pension costs [Note 22] 309 272

– other staff costs 1,012 854

Other administrative expenses 1,977 2,246

6,195 6,251

The average weekly number of employees during the year ended 31 December 2007 was 27 (2006–27).

Bank Mandiri (Europe) Limited

PAGE 24 >

7. EMOLUMENTS OF DIRECTORS 2007 2006

US$ 000 US$ 000

Directors' remuneration and other emoluments were:

Directors' emoluments 835 661

835 661

The emoluments of the highest paid director were US$ 659,000 – 12 month period, (2006 US$ 565,000 ).

No director received benefits in the form of pension contributions during 2006 or 2007.

8. TAX ON PROFIT/(LOSS) ON ORDINARY ACTIVITIES

a) Analysis of charge for the year:

Current Tax

Current year 1,180 –

Adjustment in respect of prior periods – –

Total current tax charge/(credit) 1,180 –

Deferred Tax

Current year 852 873

Adjustment in respect of prior periods (35) –

Total deferred tax charge/(credit) 817 873

1,997 873

b) Factors affecting tax charge for the year:

Profit/(Loss) on ordinary activities before tax 6,822 5,542

Corporation tax at 30% 2,047 1,663

Effects of:–

Expenses not deductible for tax purposes 47 22

Capital allowances in excess of depreciation (3) 11

Other Short term timing differences (48) –

Foreign Exchange movements on tax balances (66) –

Utilisation of tax losses brought forward (797) (1,696)

Current tax credit for the year 1,180 –

c) Factors that may affect future tax charges:

At the year end, the Bank has a deferred tax asset of $56,260 (31.12.2006: $873,327). The asset arises in respect of capital allowances in excess

of depreciation. As a result of a change in the headline rate of corporation tax from 30% to 28% in Finance Act 2007, which was

substantively enacted by Parliament on 26 June 2007 and becomes effective on 1 April 2008, the deferred tax asset has been recalculated

to take account of this change. The resulting decrease in the deferred tax asset ($4,019) has been accounted for as part of the current year

movement on this deferred tax balance.

Notes to the Financial Statementsfor the year ended 31 December 2007

Bank Mandiri (Europe) Limited

INK3082 PHA BML R&A07I 3/7/08 9:56 am Page 25

< PAGE 25

Notes to the Financial Statementsfor the year ended 31 December 2007

8. TAX ON PROFIT/(LOSS) ON ORDINARY ACTIVITIES (Continued) 2007 2006

US$ 000 US$ 000

d) Deferred Tax

The deferred tax asset included in the balance sheet and changes recorded

in the income tax gain are as follows:–

Provision at start of year 873 –

Prior period adjustment 35 –

Effect of change in tax rate (4) –

Other temporary differences (51) 59

(Utilisation)/recognition of tax losses (797) 814

56 873

9. LOANS AND ADVANCES TO BANKS

Loans and advances

Remaining maturity:

– Repayable on demand 52,311 17,415

Other loans and advances:

– 3 months or less – 1,000

– Between 3 months and 1 year – –

– Between 1 year and 5 years 5,000 –

57,311 18,415

Amounts Include:

Due from group undertakings – 1,000

10. LOANS AND ADVANCES TO CUSTOMERS

Remaining maturity:

– Repayable on demand or short notice 981 172

– 3 months or less (excluding demand or at short notice) 47,602 65,140

– Between 3 months and 1 year 73,139 31,151

– Between 1 year and 5 years 33,712 18,394

– Over 5 years 3,744 4,608

Less specific bad and doubtful debt provisions (711) (4,094)

158,467 115,371

Bank Mandiri (Europe) Limited

PAGE 26 >

10. LOANS AND ADVANCES TO CUSTOMERS (continued) 2007 2006

US$ 000 US$ 000

Non–performing loans and advances to customers:

– Loans and advances before provisions 13,202 4,094

– Loans and advances after provisions 12,491 –

The Bank derives and manages its loan portfolio in a risk averse manner. The Directors have agreed that the customer portfolio will

comprise principally of short–term self–liquidating trade finance exposures and medium term asset backed ship financing loans. The

factors considered during fair valuation of the loans and advances included future cash flows and collateral consisting of cash deposits

and properties.

A reconciliation of the allowance for impairment losses for loans and advances by class is as follows:

Trade Shipping

Finance Portfolio Total

2007 2007 2007

US$ 000 US$ 000 US$ 000

As at 1 January 2007 4,094 – 4,094

Charges for the year – 711 711

Recoveries (1,373) – (1,373)

(1,373) 711 (662)

Amounts written off (2,721) – (2,721)

As at 31 December 2007 – 711 711

Individual Impairment – 711 711

Trade Shipping

Finance Portfolio Total

2006 2006 2006

US$ 000 US$ 000 US$ 000

As at 1 January 2006 4,627 – 4,627

Recoveries (533) – (533)

Amounts written off – – –

As at 31 December 2006 4,094 – 4,094

Individual Impairment 4,094 – 4,094

Net (charge)/credit to profit & loss account 2,032

(Included write back of provisions of $1,499 made in respect of contingent liabilities)

Notes to the Financial Statementsfor the year ended 31 December 2007

Bank Mandiri (Europe) Limited

< PAGE 27

Notes to the Financial Statementsfor the year ended 31 December 2007

11. DEBT SECURITIES Available– Held–to– Available– Held–to–

for–sale maturity Total for–sale maturity Total

2007 2007 2007 2006 2006 2006

US$ 000 US$ 000 US$ 000 US$ 000 US$ 000 US$ 000

Investment securities

– Public sector securities – 22,249 22,249 – 18,279 18,279

– Other debt securities – banks 17,563 13,017 30,580 43,378 13,074 56,452

17,563 35,266 52,829 43,378 31,353 74,731

Investment securities

– Listed 4,969 35,266 40,235 26,819 31,353 58,172

– Unlisted 12,594 – 12,594 16,559 – 16,559

17,563 35,266 52,829 43,378 31,353 74,731

Remaining maturity:

– 3 months or less 4,527 – 4,527 11,205 – 11,205

– Between 3 months and 1 year 8,072 13,017 21,089 11,229 – 11,229

– Between 1 year and 5 years 4,965 22,249 27,214 20,944 31,353 52,297

– Over 5 years – – – – – –

17,563 35,266 52,829 43,378 31,353 74,731

Valuation: 2007 2007 2006 2006

US$ 000 US$ 000 US$ 000 US$ 000

Book Fair Book Fair

Value Value Value Value

– Floating rate notes & Fixed rate notes 40,262 40,229 58,221 58,173

– Commercial bills discounted 12,600 12,600 16,558 16,558

52,862 52,829 74,779 74,731

Amounts Include:

Issued by group undertakings 10,018 10,018 11,358 11,358

Securities are purchased with the dual purpose of complying with the necessary statutory liquidity requirements, and to provide an even

flow of floating rate interest receipts. Bills are purchased primarily as a result of the Bank's involvement in the discounting of letters of credit.

Although some paper may be traded prior to maturity, it is not the Bank's original intention to sell these assets and they are therefore

funded accordingly. The Directors consider that the book value of commercial bills is not materially different from fair value, since this is

intrinsically linked to a Libor plus margin pricing regime which is reasonably consistent throughout this market. The Bank intends to hold

the securities listed under held–to–maturity until their final maturity.

Bank Mandiri (Europe) Limited

PAGE 28 >

12. TANGIBLE FIXED ASSETS Motor Furniture,

vehicles Motor Leasehold Computer fixtures

finance vehicles improve– and other and 2007

leases owned ments equipment fittings Total

US$ 000 US$ 000 US$ 000 US$ 000 US$ 000 US$ 000

Cost:

Balance as at 31 December 2006 45 139 472 1,396 303 2,355

Additions – – 9 32 10 51

Disposals (45) – – (18) (9) (72)

At 31 December 2007 – 139 481 1,410 304 2,334

Accumulated Depreciation:

Balance as at 31 December 2006 45 91 102 1,288 219 1,745

Charge for the year – 25 95 60 24 204

Disposals (45) – – (18) (9) (72)

At 31 December 2007 – 116 197 1,330 234 1,877

Net book value at 31 December 2007 – 23 284 80 70 457

Net book value at 31 December 2006 – 48 370 108 84 610

13. OTHER ASSETS, PREPAYMENTS AND ACCRUED INCOME 2007 2006

US$ 000 US$ 000

Accrued interest receivable (net of suspended interest) 1,722 1,687

Prepaid expenses 287 213

Deferred tax asset 56 873

Other receivables 275 546

2,340 3,319

14. ASSETS AND LIABILITIES

Assets and liabilities denominated in foreign currencies

Denominated in US dollars 243,423 191,264

Denominated in currencies other than US dollars 31,212 27,306

Total assets 274,635 218,570

Denominated in US dollars 184,850 128,441

Denominated in currencies other than US dollars 22,541 27,302

Total liabilities excluding capital and other reserves 207,391 155,743

Notes to the Financial Statementsfor the year ended 31 December 2007

Bank Mandiri (Europe) Limited

< PAGE 29

Notes to the Financial Statementsfor the year ended 31 December 2007

15. DEPOSITS FROM BANKS 2007 2006

US$ 000 US$ 000

With agreed maturity dates or periods of notice, by remaining maturity of:

Repayable on demand 3,908 7,030

– 3 months or less 64,030 55,883

– Between 3 months and 1 year 34,000 28,000

– Between 1 year and 5 years 40,000 14,000

141,938 104,913

Amounts include:

Due to group undertakings 14,000 14,000

16. CUSTOMERS ACCOUNTS

With agreed maturity dates or periods of notice, by remaining maturity of:

Repayable on demand 38,597 35,026

– 3 months or less 11,950 –

– 1 year or less but over 3 months 10,434 2,257

60,981 37,283

A total of US$10.4 million ( 2006 – US$3.17 million) of deposits are frozen and held as

collateral against trade finance loan facilities.

17. DEBT SECURITIES IN ISSUE

Other debt securities in issue, by remaining maturity:

– 3 months or less – 10,000

– Between 1 year and 2 years – –

– 10,000

Bank Mandiri (Europe) Limited

PAGE 30 >

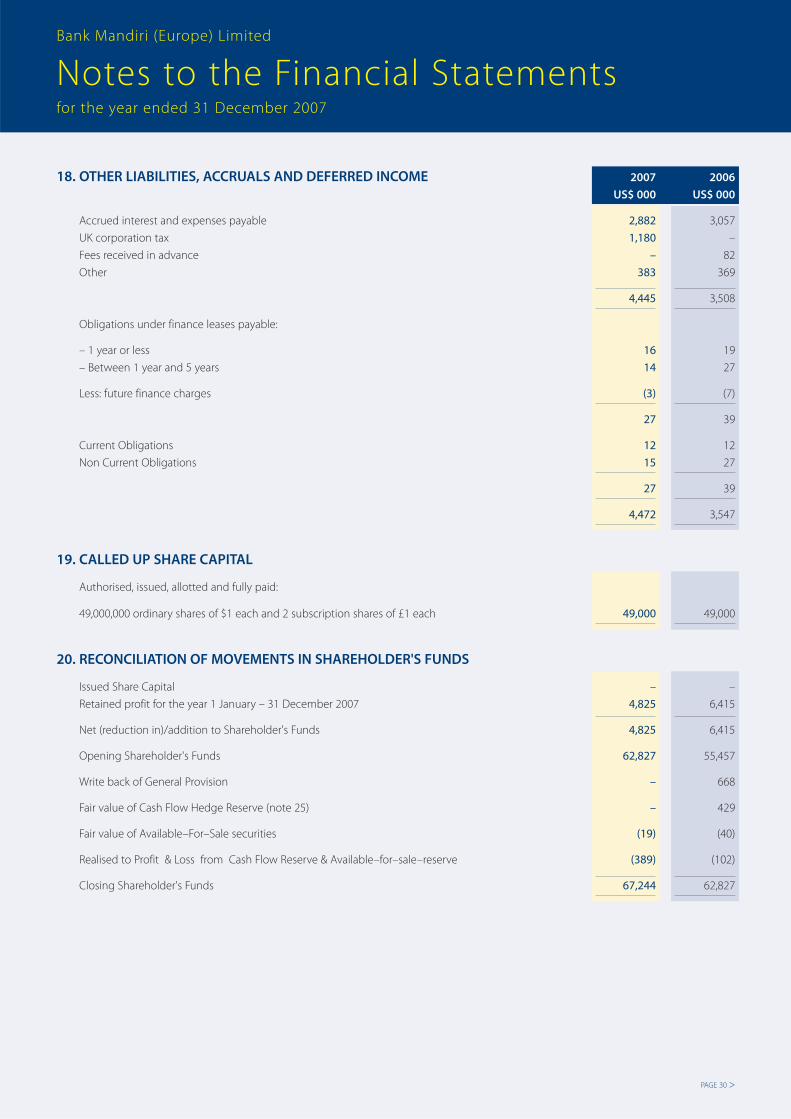

18. OTHER LIABILITIES, ACCRUALS AND DEFERRED INCOME 2007 2006

US$ 000 US$ 000

Accrued interest and expenses payable 2,882 3,057

UK corporation tax 1,180 –

Fees received in advance – 82

Other 383 369

4,445 3,508

Obligations under finance leases payable:

– 1 year or less 16 19

– Between 1 year and 5 years 14 27

Less: future finance charges (3) (7)

27 39

Current Obligations 12 12

Non Current Obligations 15 27

27 39

4,472 3,547

19. CALLED UP SHARE CAPITAL

Authorised, issued, allotted and fully paid:

49,000,000 ordinary shares of $1 each and 2 subscription shares of £1 each 49,000 49,000

20. RECONCILIATION OF MOVEMENTS IN SHAREHOLDER'S FUNDS

Issued Share Capital – –

Retained profit for the year 1 January – 31 December 2007 4,825 6,415

Net (reduction in)/addition to Shareholder's Funds 4,825 6,415

Opening Shareholder's Funds 62,827 55,457

Write back of General Provision – 668

Fair value of Cash Flow Hedge Reserve (note 25) – 429

Fair value of Available–For–Sale securities (19) (40)

Realised to Profit & Loss from Cash Flow Reserve & Available–for–sale–reserve (389) (102)

Closing Shareholder's Funds 67,244 62,827

Notes to the Financial Statementsfor the year ended 31 December 2007

Bank Mandiri (Europe) Limited

< PAGE 31

Notes to the Financial Statementsfor the year ended 31 December 2007

21. OPERATING LEASE COMMITMENTS 2007 2007 2006 2006

US$ 000 US$ 000 US$ 000 US$ 000

Buildings Other Buildings Other

At the year end, cumulative commitments under

non–cancellable operating leases were:

– Within 1 year 140 49 137 31

– Between 1 and 5 years 1,241 145 1,576 115

1,381 194 1,713 146

22. PENSION COSTS

The Bank provides each of its employees with an individual money purchase pension arrangement which is administered by the Standard

Life Assurance Company. The sums allocated into each individual's pension fund are paid on a monthly basis, and the amounts are based

on a scale linked to each staff member's age and salary.

23. MEMORANDUM ITEMS 2007 2007 2006 2006

US$ 000 US$ 000 US$ 000 US$ 000

Book Fair Book Fair

Value Value Value Value

CONTINGENT LIABILITIES:

As at 31 December :

Direct–credit substitutes:

Bank acceptances granted – – 249 249

– – 249 249

Transaction–related :

Guarantees pledged 681 681 1,935 1,935

681 681 1,935 1,935

Trade–related :

Letters of credit issued 19,458 19,458 17,943 17,943

19,458 19,458 17,943 17,943

20,139 20,139 20,127 20,127

Bank Mandiri (Europe) Limited

PAGE 32 >

24. RISK MANAGEMENT

The identification, measurement and containment of risk is integral to the management of our business. Our risk policies and procedures

are regularly updated to meet changing business requirements, and to comply with best practice. Our parent company, PT Bank Mandiri

(Persero) Tbk, conducts an in–depth review at least once a year of our loan portfolio and also conducts a review of our internal

controls/procedures. Our Audit Committee is apprised of these and other developments throughout the year to ensure adequate controls

are in place to meet our changing business requirements.

(A) – Risk Management and ControlThe Bank is firmly committed to the management of risk, recognising that sound internal risk management is essential to its prudent

operation, particularly with the growing complexity, diversity and volatility of markets, facilitated by rapid advances in technology and

communications. Risk management is given high priority throughout the Bank.

Responsibility for risk management policies, limits, and the level of risk assumed, lies with the Board of Directors. The Board charges Senior

Management with developing, presenting and implementing these policies and limits. The structure is designed to provide a reasonable

degree of assurance that no single event, or contribution of events, will materially affect the wellbeing of the Bank.

A Risk Committee comprised of Senior Management plays a key role in the identification, evaluation and management of all risks. All credit

and other new product decisions require direct Senior Management & Risk Committee approval. Management is supported by a

comprehensive structure of independent controls, analysis and reporting processes.

The Bank has strict controls and detailed procedures in place for the monitoring of the financial instruments employed in its business.

Before any new financial instrument is employed by the Bank approval must be sought from the Bank's Senior Management Committee

and as part of this approval process the Senior Management Committee ensures that the Bank has the relevant expertise, adequate

controls and operating procedures in place before the new financial instrument is initiated. Where it is deemed necessary product or sector

limits are established and monitored such that excessive concentration risk is minimised.

The Bank's Board of Directors, Asset and Liability Committee, Risk Committee and Audit Committee, assist in appraising market trends,

economic and political developments, and providing strategic direction for all aspects of risk management.

The Bank has in place an extensive number of limit controls and management information systems to facilitate effective management

overview. All limits are approved by the Board of Directors and are reviewed at least annually. Limit breaches, if any, are reported to the

Chief Executive and Senior Management on a daily basis.

The following basic elements of sound risk management are applied to all financial risk instruments, including derivatives.

This includes where appropriate:

• Review by the Board of Directors and Senior Management.

• Risk management processes with integral product risk limits.

• Measurement procedures and information systems.

• Continuous risk monitoring and frequent management reporting.

• Segregation of duties, comprehensive internal controls and audit procedures.

In the opinion of the Directors, the period end numerical disclosures are not materially unrepresentative of the entity's position during the

period or its agreed objectives, policies and strategies. In addition, the Directors have no plans, at the current time, to make any significant

changes either to the product base or to the methods employed in the management and control of the above–mentioned risks.

(B) – Market RiskMarket risk refers to the uncertainty of future earnings, resulting from changes in interest rates, foreign exchange rates, market prices and

volatility thereof. Senior Management constantly monitors market risk by a combination of reports and real time market information systems.

(C) – Interest Rate RiskInterest rate risk arises when there is a mis–match between positions which are subject to interest rate adjustments within a specific period.

In the Bank's funding/lending activities, fluctuations in interest rates are reflected in interest margins and earnings. Our interest rate risk

profile is short term and liquid and the Directors therefore feel that risks have been minimised. Hedging techniques can be applied on a

limited basis should the need arise.

Notes to the Financial Statementsfor the year ended 31 December 2007

Bank Mandiri (Europe) Limited

< PAGE 33

Notes to the Financial Statementsfor the year ended 31 December 2007

An interest rate gap is a common measure of interest rate sensitivity (note 26). A liability gap occurs when more liabilities than assets are

subject to rate changes during a prescribed future time period. Interest rate gaps are monitored by Senior Management & Asset & Liability

Committee regularly.

(D) – Currency RiskThe Bank does not actively trade in the foreign exchange markets on its own account, and foreign exchange swaps and forward foreign

exchange contracts are committed for management of Bank's expenses and Bank's assets and liabilities.

Where possible the Bank matches its currency transactions. The majority of the asset and liability positions are denominated in US Dollars

and therefore, in the opinion of the Directors, the level of currency risk is considered to be minimal.

(E) – Liquidity RiskLiquidity risk arises from fluctuations in cash flows. The liquidity risk management process ensures that the Bank is able to honour all of its

financial commitments as they fall due. Liquidity is monitored daily through specialised reports provided to Senior Management against

appropriate limits set by the Board of Directors and with reference to statutory requirements. In addition the Asset and Liability Committee

and the Risk Committee review the liquidity position periodically. The Bank has access to a variety of funding sources including bank

deposits, loan facilities, customer deposits and corporate trade finance deposits. Regular weekly reviews are conducted, via meetings of

the Asset and Liability Committee, of these sources and requirements for perusal by Senior Management. In practice, the Bank operates

well within its prescribed liquidity levels.

Analysis of financial liabilities by remaining contractual maturities

The Table below summarises the maturity profile of the Bank's financial liabilities as at 31 December 2007 based on contractual

undiscounted repayment obligations. Repayments which are subject to notice are treated as if notice were to be given immediately.

However, the Bank expects that many customers will not request repayment on the earliest date the Bank could be required to pay and

the table does not reflect the expected cash flows indicated by the Bank's deposit retention history.

Less than 3 to 12 1 to 5 Over

On Demand 3 months months years 5 years Total

US$ 000 US$ 000 US$ 000 US$ 000 US$ 000 US$ 000

As at 31 December 2007

Due to Banks 3,908 64,030 34,000 40,000 – 141,938

Customer Accounts 47,046 3,500 10,435 – – 60,981

Debt Securities in Issue – – – – – –

Other financial – – 3,087 1,385 – 4,472

Total financial liabilities 50,954 67,530 47,522 41,385 – 207,391

Less than 3 to 12 1 to 5 Over

On Demand 3 months months years 5 years Total

US$ 000 US$ 000 US$ 000 US$ 000 US$ 000 US$ 000

As at 31 December 2006

Due to Banks 7,030 55,883 28,000 14,000 – 104,913

Customer Accounts 34,113 – 3,170 – – 37,283

Debt Securities in Issue – – 10,000 – – 10,000

Other financial – – 1,857 1,690 – 3,547

Total financial liabilities 41,143 55,883 43,027 15,690 – 155,743

Bank Mandiri (Europe) Limited

PAGE 34 >

24. RISK MANAGEMENT (Continued)

Ageing for Contingent liabilities Less than 3 to 12 1 to 5 Over

On Demand 3 months months years 5 years Total

US$ 000 US$ 000 US$ 000 US$ 000 US$ 000 US$ 000

As at 31 December 2007

Guarantees – – 681 – – 681

Letters of credit issued – – 19,458 – – 19,458

Total financial liabilities – – 20,139 – – 20,139

Ageing for Contingent liabilities Less than 3 to 12 1 to 5 Over

On Demand 3 months months years 5 years Total

US$ 000 US$ 000 US$ 000 US$ 000 US$ 000 US$ 000

As at 31 December 2006

Guarantees – – 2,184 – – 2,184

Letters of credit issued – – 17,943 – – 17,943

Total financial liabilities – – 20,127 – – 20,127

(F) – Operational RiskOperational Risk is the risk that deficiencies in information systems or internal controls result in unexpected business, financial and

operating losses. Operational Risk is ultimately managed by the Board of Directors and is given the highest priority. Senior Management

are charged with applying stringent procedures to mitigate risk of error, fraud, money laundering, and other irregularities. In addition,

strong disaster recovery procedures have been formulated and are tested on at least a yearly basis. Internal Audit reviews the risk mitigation

processes to ensure that these meet the organisation's current needs and are being properly implemented and controlled.

(G) – Credit RiskThe Bank uses a formal credit process to quantify and evaluate the risk of proposed credits, and to ensure appropriate returns for assuming

risks. Relationship Managers undertake a full financial review of each client at least annually, so that the Bank remains aware of

counterparties' risk profiles. This analysis includes a review of previous historical financial data, future projections, industry reviews, broker

reports and credit analysis techniques.

Securities, Letters of Credit, Guarantees and Off–Balance Sheet instruments are managed by the same process. Settlement and any other

credit risks are restricted through product limits and counterparty netting agreements.

From time to time the Bank takes collateral to mitigate credit or transactional risks. The taking of collateral as security is governed by

detailed policies and procedures and where necessary the security is registered and perfected in the relevant jurisdictions using legal

counsel.

The table below shows the maximum exposure to credit risk for the components of the balance sheet, including derivatives. The maximum

exposure is shown gross, before the effect of mitigation through use of master netting and collateral agreements.

Notes to the Financial Statementsfor the year ended 31 December 2007

Bank Mandiri (Europe) Limited

< PAGE 35

Notes to the Financial Statementsfor the year ended 31 December 2007

Gross Gross Net Net

Maximum Maximum Maximum Maximum

exposure exposure exposure exposure

2007 2006 2007 2006

Notes US$ 000 US$ 000 US$ 000 US$ 000

Cash and money at call and deposits with central banks 3,231 6,124 3,231 6,124

Loans and advances to banks 9 57,311 18,415 57,311 18,415

Loans and advances to customers 10 159,178 119,465 158,467 115,371

Debt securities 11 52,829 74,731 52,829 74,731

Other assets, prepayments and accrued income 13 2,340 3,319 2,340 3,319

Total 274,889 222,054 274,178 217,960

Contingent Liabilities [23] 20,139 20,127 20,139 20,127

Risk concentrations of the maximum exposure to credit risk

Concentration of risk is managed by client/counterparty, by geographical region and industry sector. The maximum credit exposure to any

non–bank client during has been within our prescribed LECB by the FSA of $15.6 million before talking account of collateral or other credit

enhancements.

The Bank's financial assets, before talking into account any collateral held or other credit enhancements can be analysed by the following

geographical regions:

2007 2006

US$ 000 US$ 000

United Kingdom 99,110 88,323

Europe 10,427 15,030

Asia 146,503 109,410

North America 18,850 9,291

Total 274,889 222,054

Bank 81,137 76,037

Intergroup 10,018 12,369

Corporate Finance 22,245 18,279

Foodstuffs 22,824 23,539

Metals 18,996 14,214

Other 32,338 20,934

Pharmaceutical 8,913 8,988

Shipping 64,562 36,562

Sovereign debt 13,856 11,132

Total 274,889 222,054

Bank Mandiri (Europe) Limited

PAGE 36 >

24. RISK MANAGEMENT (Continued)

Credit Quality per Neither past

class of financial assets: due nor Past due or individually impaired

impaired

Special Sub

31 December 2007 Current Mention Standard Doubtful Loss Total

Due from Banks 81,137 – – – – 81,137

Loans and Advances 170,532 12,122 – 850 230 183,734

Intergroup 10,018 – – – – 10,018

Total 261,687 12,122 – 850 230 274,889

Credit Quality per Neither past

class of financial assets: due nor Past due or individually impaired

impaired

Special Sub

31 December 2006 Current Mention Standard Doubtful Loss Total

Due from Banks 76,037 – – – – 76,037

Loans and Advances 129,554 – – – 4,094 133,648

Other 12,369 – – – – 12,369

Total 217,960 – – – 4,094 222,054

25. HEDGE ACCOUNTING – ( Cash Flow Hedges) 2007 2006

US$ 000 US$ 000

Fair Fair

Value Value

Present values of cash inflows (Assets) – 3,965

Present value of cash outflows (Liabilities) – (3,536)

Fair value – 429

As a result of future sterling expenses, the Bank is exposed to foreign exchange risks . In 2007 foreign exchange risks which were hedged

with forward foreign exchange contracts. A schedule indicating the position of the forward foreign exchange contracts which all matured

during 2007 is listed above. The Bank was unable to cost effectively hedge its expenses for the last quarter in 2007.

Notes to the Financial Statementsfor the year ended 31 December 2007

Bank Mandiri (Europe) Limited

< PAGE 37

Notes to the Financial Statementsfor the year ended 31 December 2007

26. NON TRADING BOOK INTEREST RATE RISK

The Bank does not have a trading book. However, interest rate exposure exists within its non–trading book. Instruments have been

allocated to time bands by reference to the earlier of their next contractual interest rate repricing date and their maturity date.

As at 31 December 2007, interest rate risk comprised:–

Category of Asset/Liability Less than 3 months to 6 months 1 year to Non–Int. Total

3 months 6 months to 1 year 5 years bearing

US$ 000 US$ 000 US$ 000 US$ 000 US$ 000 US$ 000

Loans and advances to banks 57,311 – – – – 57,311

Loans and advances to customers 158,589 – – – (122) 158,467

Debt securities 22,521 8,220 – 22,000 88 52,829

Other assets – – – – 6,028 6,028

Total assets 238,421 8,220 – 22,000 5,994 274,635

Deposits by banks 121,938 20,000 – – – 141,938

Customer accounts 60,981 – – – – 60,981

Debt Securities in issue – – – – – –

Shareholder's funds – – – – 67,244 67,244

Other liabilities – – – – 4,472 4,472

Other Provisions Liab. & Chgs – – – – – –

Total Liabilities & Shareholder's Funds 182,919 20,000 – – 71,716 274,635

Gap 55,502 (11,780) – 22,000 (65,722) –

Cumulative gap 55,502 43,722 43,722 65,722 – –

The above figures do not provide the exposure of the Bank to particular interest rates as they have been consolidated across all currencies.

The majority of the Bank's balance sheet is denominated in US Dollars, with only a minor element of currencies regarded as volatile. The

Directors therefore consider that a further currency analysis of interest rate risk is not relevant.

As at 31 December 2006, interest rate risk comprised:–

Category of Asset/Liability Less than 3 months to 6 months 1 year to Non–Int. Total

3 months 6 months to 1 year 5 years bearing

US$ 000 US$ 000 US$ 000 US$ 000 US$ 000 US$ 000

Loans and advances to banks 18,415 – – – – 18,415

Loans and advances to customers 115,541 – – – (170) 115,371

Debt securities 45,176 9,520 – 20,000 35 74,731

Other assets – – – – 10,053 10,053

Total assets 179,132 9,520 – 20,000 9,918 218,570

Deposits by banks 79,914 25,000 – – – 104,914

Customer accounts 37,282 – – – – 37,282

Debt Securities in issue – – – 10,000 – 10,000

Shareholder's funds – – – – 62,827 62,827

Other liabilities – – – – 3,547 3,547

Other Provisions Liab. & Chgs – – – – – –

Total Liabilities & Shareholder's Funds 117,196 25,000 – 10,000 66,374 218,570

Gap 61,936 (15,480) – 10,000 (56,456) –

Cumulative gap 61,936 46,456 46,456 56,456 – –

Bank Mandiri (Europe) Limited

PAGE 38 >

27. ULTIMATE PARENT COMPANY

The Bank is a subsidiary undertaking of PT Bank Mandiri (Persero) Tbk, a part government owned bank incorporated in the Republic

of Indonesia.

The registered address is:

Plaza Mandiri

JL. Gatot Subroto Kav 36–38

Jakarta 12190

Indonesia

The smallest and largest group in which the results of the Bank are consolidated is that headed by PT Bank Mandiri (Persero) Tbk.

The consolidated financial statements of the group are available to the public at the Bank's registered office.

Notes to the Financial Statementsfor the year ended 31 December 2007

Bank Mandiri (Europe) Limited

< PAGE 39

NotesBank Mandiri (Europe) Limited