annual report 2012 - kbc bank · 4 | kbc annual report 2012 5 jan feb mar apr may jun smart access...

TRANSCRIPT

Annual Report 2012

1

About KBC 2Board of Directors 8 Chairman’s Statement 12 Chief Executive’s Review 14Income Statement 18Statement of Financial Position 19 Auditors’ Statement 20Corporate Governance 21 Corporate Social Responsibility 22 Management 24Regional Offices 26Other KBC Companies in Ireland 27Company Information 28

CONTENTSKBC is dedicated to Ireland. The photography in this 2012 annual report provides a snapshot of Ireland focused around our employees, customers and communities. These have been the heart of our business for the last 40 years and will continue to be long into the future.

2 | KBC ANNUAL REPORT 2012 3

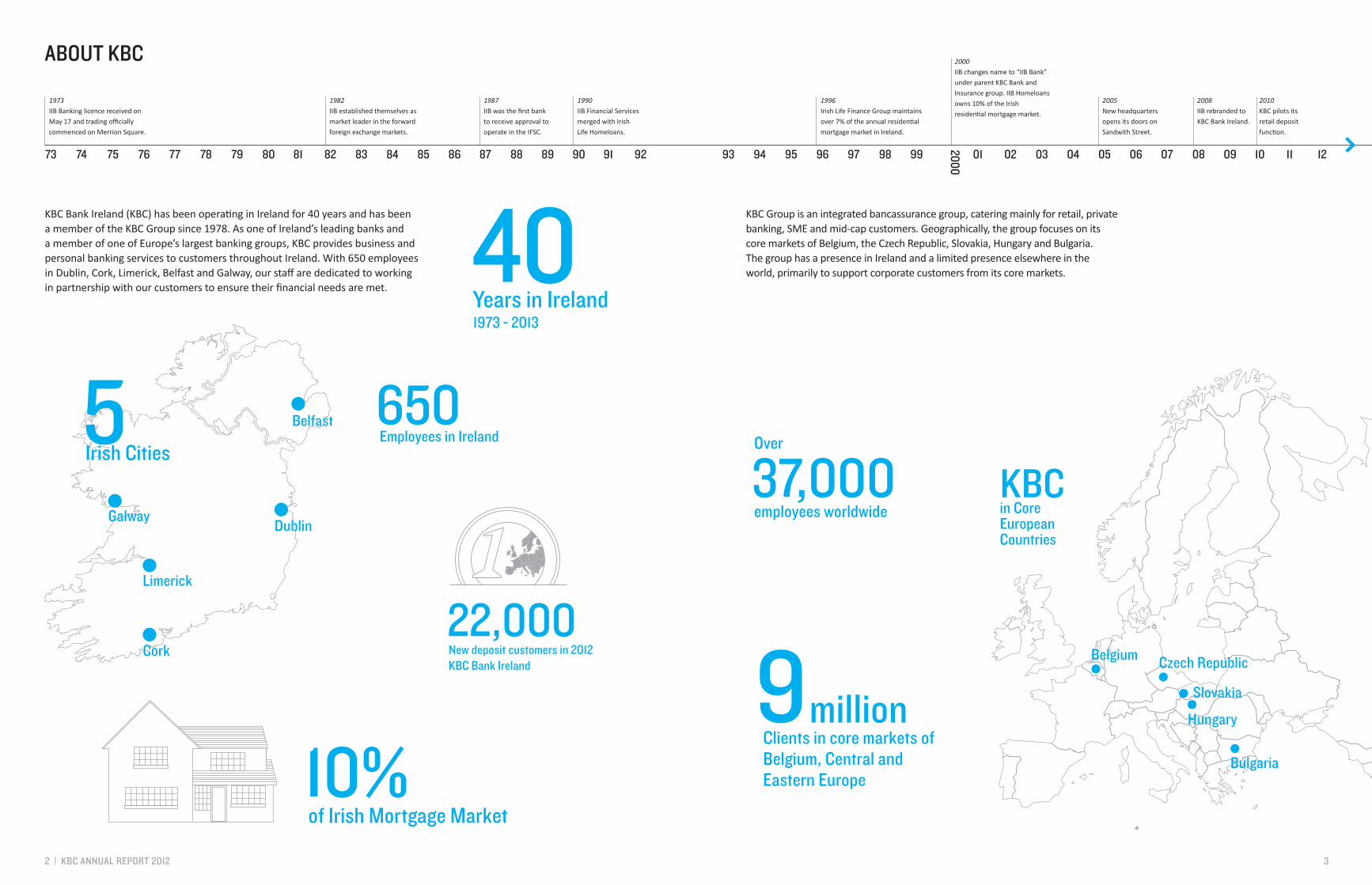

22,000New deposit customers in 2012 KBC Bank Ireland

40Years in Ireland1973 - 2013

KBC in Core European Countries

73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99

2000

01 02 03 04 05 06 07 08 09 10 11 12

1973 IIB Banking licence received on May 17 and trading officially commenced on Merrion Square.

2005New headquarters opens its doors on Sandwith Street.

2008IIB rebranded to KBC Bank Ireland.

2010KBC pilots its retail deposit function.

1982IIB established themselves as market leader in the forward foreign exchange markets.

1987IIB was the first bank to receive approval to operate in the IFSC.

1990IIB Financial Services merged with Irish Life Homeloans.

1996Irish Life Finance Group maintains over 7% of the annual residential mortgage market in Ireland.

2000IIB changes name to “IIB Bank” under parent KBC Bank and Insurance group. IIB Homeloans owns 10% of the Irish residential mortgage market.

ABOUT KBC

KBC Bank Ireland (KBC) has been operating in Ireland for 40 years and has been a member of the KBC Group since 1978. As one of Ireland’s leading banks and a member of one of Europe’s largest banking groups, KBC provides business and personal banking services to customers throughout Ireland. With 650 employees in Dublin, Cork, Limerick, Belfast and Galway, our staff are dedicated to working in partnership with our customers to ensure their financial needs are met.

KBC Group is an integrated bancassurance group, catering mainly for retail, private banking, SME and mid-cap customers. Geographically, the group focuses on its core markets of Belgium, the Czech Republic, Slovakia, Hungary and Bulgaria. The group has a presence in Ireland and a limited presence elsewhere in the world, primarily to support corporate customers from its core markets.

5Irish Cities

Belfast

Limerick

Cork

DublinGalway

650Employees in Ireland

9 Clients in core markets of Belgium, Central and Eastern Europe

million

37,000employees worldwide

Over

Belgium Czech Republic

Slovakia

Hungary

Bulgaria10%of Irish Mortgage Market

4 | KBC ANNUAL REPORT 2012 5

Jan Feb Mar Apr May Jun

Smart Access Account launched to market.

KBC launches online videos to help mortgage customers in difficulty.

Launch of first Sterling Deposit Account.

KBC named Bank with the best corporate reputation in Ireland by RepTrak.

2012

Jul Aug Sep Oct Nov Dec

KBC announce new home insurance offer with Zurich.

KBC launches Interest UpFront Savings Account.

KBC wins prestigious national award for its long term support of the Arts.

KBC opens its first ‘pop up’ in Dundrum Town Centre, Dublin.

KBC opens flagship retail office in Dublin city centre.

KBC make sense of the budget with simple infographic from Austin Hughes.

Engaging and Listening to Customers At KBC Bank Ireland (KBC) we recognise how important it is to really listen to customers and understand their needs better. That’s why in 2012 we established our customer engagement function within the Bank that allows us to have that conversation. Over the last 12 months we have met with KBC customers in Cork, Galway and Dublin through our customer forum and asked them for their views on new products, services and initiatives. As a result we have made a number of improvements to products and communications and introduced some new initiatives that make the overall experience of being a customer of KBC that much better. Should you wish to get involved in our customer forum you can seek more details to apply by emailing [email protected]

Helping Customers in DifficultyRecognising that these are difficult times for many of our customers we are ensuring that the service and engagement we provide to those customers experiencing financial difficulty is second to none. Our employees are fully trained and experienced in dealing with those experiencing financial difficulty with the main aim to help our customers get on the right path to recovery. We have developed a number of online videos and tools that help customers guide themselves through the process and we reach out to all mortgage customers to make them aware that we are available to talk to them should they find themselves in financial difficulty.

Growing for the FutureIn 2012 we had over 22,000 new deposit customers join KBC. We developed four new deposit products that support our fixed term deposits range, including the Smart Access demand account, Top-Up deposit account and Interest UpFront savings account. We partnered with Zurich to provide KBC customers with a leading home insurance product and we had over 100 new employees join the Bank. KBC was shortlisted for its employee wellbeing programme at the 2012 Chambers Ireland Corporate Social Responsibility awards. The programme developed in conjunction with employees strives to ensure that employees achieve a healthy work life balance.

Making things Simple

We realise that financial products can be complex and difficult to understand for many. This is something you have told us through your feedback. As a result we are now trying to make the world of finances as simple as possible for consumers to understand. In 2012 we redesigned and simplified our application forms for deposit products so that they were easier to understand. We made the process easier for you to apply and we now make a ‘welcome call’ to all new deposit customers a few weeks after their deposit account has opened to see if they have any further queries or we can do anything else for them.

Improving our capability

We understand that as we move towards a technology driven world, our ability to provide that technology and innovation to our customers as part of our offering will be key. Over the course of 2012, as we introduced new products and services, we improved our capability in our online banking service to customers. A number of new facilities were introduced to make online banking easier and more secure. We plan to introduce further improvements over the course of 2013 as we introduce more products.

KBC Great Music in Irish HousesKBC has been a long term supporter of the Arts in Ireland. Our key partnership with the KBC Great Music in Irish Houses Festival has grown from strength to strength as we and the festival make world class musicians accessible to Irish audiences. This partnership was recognised by the prestigious Business2Arts awards in 2012 when KBC was awarded the Best Long Term Arts Sponsorship for its commitment to the arts and the annual festival. As part of our commitment to the community and the Arts, and recognising our 40 years in Ireland, we look forward to working with the festival again in 2013 and thrilling music lovers and Irish audiences with more world class and home grown music talent.

40 years in IrelandKBC has been proudly serving customers in Ireland now for 40 years. The Bank originally started trading on the 17 May in 1973 on Merrion Square before moving to its current headquarters on Sandwith Street in 2005. Trust is very important for consumers when it comes to financial services and we were delighted to be awarded the Bank with the best reputation in Ireland in our sector in 2012 by the annual RepTrak Survey which surveys nearly 4,000 consumers on industry and organisation reputations.

Bringing the bank closer to youIn October of 2012 we launched a new concept of banking to the Irish customer which we call the KBC ‘Pop up’. The ‘Pop up’ allows KBC to travel around Ireland to meet with customers and tell them more about the products and services we provide. It also gives customers the opportunity to engage with our experienced advisors should they have any questions or queries about any of the financial products that we provide. To find out if a KBC ‘Pop up’ will be coming your way in 2013, log onto www.kbc.ie for more details.

KBC launches Top-Up Deposit Account to market.

6 | KBC ANNUAL REPORT 2012 7

2013 marks our 40th year of serving customers in Ireland. As we enter our fifth decade in Ireland and as part of a larger Banking Group with a vision to creating a new alternative Retail Bank in the future, I look forward to many years ahead to realising our ambition and our commitment to Ireland. John H. Reynolds Chief Executive

IRELAND

Cup Café, South Leinster Street, D2

8 | KBC ANNUAL REPORT 2012 9

BOARD OF DIRECTORS

John Reynolds Chief Executive

John Reynolds is Chief Executive Officer of KBC Bank Ireland and his career in banking began in 1980 when he joined ICC, the state development bank. Five years later, John moved to KBC Bank Ireland, where he has held various roles over the years, joining the Bank’s Board in 1996 and taking up the CEO position in 2009.

A native of Culdaff in Donegal, John is an Economics graduate of Trinity College and holds a Masters Degree in Banking and Finance from UCD.

John is the current president of the Irish Banking Federation (IBF) for a two year term and sits on the Board of the Brussels based European Banking Federation of which IBF is a member.

Danny De Raymaeker Chairman*

Born on 10 December 1959, Danny De Raymaeker graduated as a Commercial and Business Engineer from the Katholieke Universiteit Leuven in 1983 and obtained a Masters Degree in Internal Auditing from the IPO-UFSIA Management School (University of Antwerp) in 1986.

He began his professional career as an internal auditor with the Kredietbank in 1984. In 1990, he was appointed Head of the Control Department, charged with the task of supervising market activities in Belgium and abroad, before taking responsibility for planning and budgets within Kredietbank in 1991. Between 1994 and the end of 1995, he filled the post of Deputy Regional Manager of the Leuven Retail Banking Office. On 1 January 1996, he was appointed General Manager of the Domestic Payments and Electronic Banking Division.

In 1997, he became General Manager of the Payments Directorate, a position he continued to hold after the merger which led to the creation of KBC. In 2002, he took charge of the Retail & Private Bancassurance Distribution Directorate. In 2008, he became Chief Executive of the Belgium Business Unit before becoming Chief Operating Officer of KBC Group in 2009.

He is a member of the Executive Committee of KBC Group since 2008. Since 1 January 2013, he is responsible for the International Markets Business Unit of KBC Group.

Ian Black Executive Director

Ian Black is Chief Financial Officer and Chief Operations Officer for KBC Bank Ireland and is a member of the Bank’s Executive Committee and Board of Directors. Ian is responsible for the development and execution of the Finance and Operations strategy for the institution. Ian joined the Bank in 1998 as a qualified accountant and has held a number of positions within Finance and Operations throughout his career with KBC. Ian was appointed to the Board in 2009. A Chartered Accountant and Associate of the Irish Taxation Institute, Ian holds an MBA from DCU and is a member of the UK Association of Corporate Treasurers.

Cameron Marr Executive Director

Cameron was appointed Chief Risk Officer (CRO) of KBC Bank Ireland in May 2011 and is a member of the Bank’s Executive Committee and Board of Directors. Cameron is responsible for the risk management strategy of the bank covering all types of risk across the institution’s activities. In 2006, Cameron took charge of KBC Bank London Branch as General Manager where he was responsible for KBC Bank’s banking operations throughout the UK. In 2009, he joined KBC Group’s Head Office in Brussels as Head of the Project Management Office for the Merchant Banking Business Unit to assist in implementing KBC’s strategic refocus. A British national, Cameron holds a Bachelor of Commerce Honours Degree in Business Studies from the University of Edinburgh.

Dara Deering Executive Director

Dara Deering is an Executive Director and Head of Retail Banking at KBC Bank Ireland. Dara was appointed Executive Director with responsibility for Retail Banking in February 2012. She is a member of the Bank’s Executive Committee and Board of Directors. The bank sees real opportunities in the retail market with customers seeking choice for their core financial products and Dara will lead KBC’s plans to introduce a broader range of products and increase its physical presence over the medium term. Currently chair of the Irish Mortgage Council, part of the Irish Banking Federation, Dara has also worked in leadership positions in the retail financial services industry for a number of years. She holds an MBA from Smurfit Business School and a Bachelor of Science Management from Trinity College Dublin.

Christine Moran Executive Director

Christine Moran is Director of Corporate and Institutional Banking and Recovery for KBC Bank Ireland and is a member of the Executive Committee and Board of Directors. Christine is responsible for the Corporate Portfolio and Homeloans Collections strategy for the Institution. Having started her career with PwC, Christine joined KBC in 1988 and has held a number of positions throughout her career with the institution. Christine was appointed an Executive Director and joined the Board in 2008. A Chartered Accountant, Christine holds a Bachelor of Commerce Honours Degree from UCD.

* Appointed in 2013

10 | KBC ANNUAL REPORT 2012 11

Robert Power Independent Non Executive Director

Robert Power was appointed as a Non Executive Director of KBC Bank Ireland in May 2010. In 1981 Mr. Power joined Cornmarket Group Financial Services Ltd (now an Irish Life Company) which provides personal financial services tailored for members of public sector unions. Mr. Power held a number of roles with the company, in Finance, Sales, Project Management and Marketing and was appointed as a Director in 1988. Mr. Power resigned in 2009 in order to develop Global Schoolroom, a world teacher training project. He is a member of the Board of Image Publications Ltd. Mr. Power is a Legal Science graduate of Trinity College (1980) and also holds a Masters Degree in Economics from the London School of Economics (1981). Mr. Power is a member of the Risk Committee and the Audit Committee.

Bart Guns Non Executive Director*

Bart Guns was appointed Senior General Manager of CRO Credits in January 2013 having previously held the position of Senior General Manager of Global Head of Payments, Cash Management and Trade Finance since September 2008. He started his career with the shipbuilding group Rijn-Schelde-Verolme Machinefabrieken in 1982 but moved to the Belgian tennis manufacturer Snauwaert & Depla in 1983 where he stayed until 1988 where he served in a number of positions including Production Director in Portugal. Since joining Kredietbank in 1989 he has worked in credit and finance as well as holding a number of managerial roles.

Mr. Guns recently completed a senior executive program in London Business School.

He is Deputy Chairman of the Board, Chairman of the Risk Committee and a member of the Audit Committee.

Damian O’Neill Company Secretary

Damian O’Neill was appointed the Company Secretary of KBC Bank Ireland in January 2010. He joined the Bank in 1990 as a qualified accountant and has held a number of positions in Finance, Risk Management and Compliance. He previously worked in PwC in Australia. He is a Fellow of the Institute of Chartered Accountants in Ireland. He is also a member of the Association of Compliance Officers Ireland and the Corporate Governance Association of Ireland. He is a Law graduate of UCD and holds a diploma in Corporate Governance from UCD.

Jan Gysels Non Executive Director*

Jan Gysels is a graduate of Katholieke Universiteit Leuven in Law and began his career with the graduate programme in KBC Belgium. His roles within the organisation to date include Relationship Manager for Turnhout Corporate Centre and Antwerp Corporate Centre. Mr. Gysels is now General Manager Banking Communities. This role is responsible for the group’s entire communication policy in Belgium including advertising, sponsoring, internal and external communication, corporate communication and language services. Mr. Gysels is Deputy Chairman of the Risk Committee and a member of the Audit Committee.

John C. Malone Independent Non Executive Director

John Malone was appointed as a Non Executive Director of KBC Bank Ireland in October 2009. Mr. Malone joined the Public Service as an Executive with the Department of Agriculture in 1969. He held many senior roles within the Department of Agriculture culminating in his appointment in 1997 as Secretary General of the Department of Agriculture and Food. Mr. Malone retired from the Public Service in 2005 and established John Malone Consulting Limited. Mr. Malone has carried out a number of assignments in the public and private sector. He was a member of the Board of Bord Bia (the Irish Food Board), a member of the Audit Committee of the Comptroller and Auditor General’s Office and Chairman of the Audit Committee of the Department of the Taoiseach (Irish Prime Minister). He is currently Chairman of the Irish Equine Foundation Ltd and a member of the Board of Dairygold Co-operative Society and Road Safety Management Ltd. Mr. Malone holds a BA in Politics and Economics from University College Dublin (1974). Mr. Malone is Chairman of the Audit Committee and a member of the Risk Committee.

Gary Britton Independent Non Executive Director

Gary Britton was appointed as a Non Executive Director of KBC Bank Ireland in January 2012. Mr. Britton is a Chartered Accountant and began his career in 1975 with Finlay-Mulligan & Co. Chartered Accountants. He joined KPMG Chartered Accountants in 1981 where he served in a number of senior positions including the firm’s Board, the firm’s Risk Committee and as head of the firm’s Audit Practice until his retirement from KPMG in 2011. With KPMG he advised blue chip Irish public companies and multinational companies. He is a Fellow of the Institute of Chartered Accountants in Ireland. He is currently a member of the Board of the Irish Stock Exchange and the Cheshire Foundation of Ireland. Mr. Britton is Deputy Chairman of the Audit Committee and a member of the Risk Committee.

BOARD OF DIRECTORS CONTINUED

* Appointed in 2013

12 | KBC ANNUAL REPORT 2012 13

2012 presented further challenges to both the Irish economy and wider Eurozone area. The global financial climate remained difficult and while there has been some modest improvement in market sentiment towards Ireland, the domestic economy remains under pressure with high, albeit stabilising rates of unemployment, reduced consumer spending and a weakening in consumer confidence. Credit markets remain difficult and there is continued financial pressure in Irish households. These key economic drivers continue to affect the overall financial performance of KBC Bank Ireland plc (the “Bank”) as it continues to navigate through the global financial crisis.

The Bank had a disappointing performance in 2012, with the Bank reporting a loss of €306 million after tax following further loan impairment costs of €547 million. This is a disappointing but expected outcome for the Bank. For 2013, we anticipate increased stability and more sustainable economic conditions for the Bank that will help return the business to profitability over the medium term. The Bank’s funding base continued to grow

from strength to strength through both retail and corporate deposits and the capital base remained strong providing a core Tier 1 ratio of 11.14% at year end.

The last twelve months however have been significant in terms of KBC’s Group Strategy and the Bank’s role within that, as it becomes a member of the new International Markets Business Unit. In October 2012, Group CEO Johan Thijs outlined the Group’s Strategy, explaining how KBC Group will address the challenges presented by the changed business environment it now faces. The KBC Group is committed to becoming the reference in banking and insurance in its core markets, focusing on activities that serve client relationships in a sustainable way. The Bank will now be managed to maximise its value contribution through its retail banking business.

As we head into 2013, the Bank looks forward with confidence. The support and commitment for Ireland from our parent means that it is well positioned to become a real competitive force in Irish retail banking in the future. To this end in 2012, the Bank started the delivery of the capability required to achieve our vision for Ireland. Our retail deposits book grew significantly as 22,000 new deposit customers joined the Bank with the introduction of a range of deposit options for consumers. We also opened our first high street retail presence in Dublin.

The Bank through its retail division expects to achieve strong growth that will contribute to the Bank’s performance and profitability over the medium term. There is a significant opportunity for an alternative retail banking brand in Ireland and I believe KBC will be able to provide that choice for customers. The KBC Group will continue to

support the Management Team and staff in Ireland as they endeavour to realise this ambition.

I would like to acknowledge the contribution made by Mr. Luc Gijsens who retired as Chairman in March of this year and Mr. Wim Eraly, Mr. Dirk Mampaey and Mr. Luc Popelier who retired from the Board of Directors of the Bank in February of this year. I also wish to acknowledge the contribution made by Mr. Ted Marah who retired from the Board of Directors of the Bank in December 2012. I welcome Mr. Bart Guns and Mr. Jan Gysels who have joined as directors of the Bank in February of this year.

I would also like to acknowledge the contribution of the management team and staff in extremely difficult circumstances under the leadership of our Chief Executive, John Reynolds.

I look forward to the Bank rising to the challenges that will present themselves over the course of 2013 as we continue to build a retail banking business in a responsible and sustainable way for the future.

Danny de Raymaeker Chairman March 2013

CHAIRMAN’S STATEMENT

14 | KBC ANNUAL REPORT 2012 15

The Irish economy remained challenging through 2012. This we had anticipated and signalled, and it has unfortunately proven to be the case. It too was a year of continued heightened credit costs for the Bank as mortgage arrears in its residential loan book continued to increase, albeit at a slower pace than heretofore. The majority of our customers continue to repay their mortgages in full and the Bank is seeing signs of success in the implementation of short and longer term resolution options for its mortgage arrears customers.

Overall, the Bank reported a loss of €306 million after tax and impairment costs for 2012. The Bank recorded a charge of €547million for loan impairment costs for the full year. This performance, while disappointing, was expected, given the continued difficult environment facing Banks in Ireland. Reflecting the muted economic activity and limited new business demand, as well as increased loan repayments and redemptions, the

overall loan portfolio reduced to €16.0 billion from €16.9 billion in 2011. The Bank’s capital base remained solid in a very challenging credit environment with a Tier 1 Capital Ratio of 11.14% as at 31 December 2012. Tier 1 capital investment by KBC Group in 2012 was €380 million.

During 2012, the Bank built on its funding base in Ireland in particular developing further its retail funding franchise with total retail deposits at the end of 2012 of approximately €2 billion (2011: €0.9 billion). This was principally generated in personal deposits, with competitive interest rates and the introduction of a range of new products for Irish customers. The Bank also developed its franchise among Credit Unions, Small and Medium sized Businesses and large Corporates. Sources of external (i.e. non-Irish) deposits also grew strongly during the year. The Bank benefits from and has access to the strong liquidity position and retail and corporate deposit capacity of KBC Group NV (“KBC Group” or “the Group”) as part of the Group’s integrated global liquidity policy.

There have been many challenges over the last twelve months but it has also been a significant year for the Bank. The announcement by Group CEO, Mr Johan Thijs in October 2012 of the updated strategic focus of KBC Group truly reflects this with the establishment of the International Markets Division of which we are a significant component. The Bank’s new place within the KBC Group has put us on a forward looking footing and the Group itself performed strongly by repaying a substantial portion of its state aid before the end of last year. The Bank’s Belgian parent, KBC Group

CHIEF EXECUTIVE’S REVIEW

recorded a strong performance for the year, reporting net profits of €612 million. With continued support from the parent to adapt our operating model, we will strive towards our ambition of being a leading retail bank in Ireland in the future.

In 2012 the Bank further developed its proposition for new retail customers. To meet customers evolving needs we introduced a broader range of deposit products and continued to build on our strong performance in this area of business in 2012. Over the year we attracted over 22,000 new savers to the organisation who recognised the value of our offering of making products ‘simple and sensible’. The Bank’s insurance business expanded this year too with the announcement of our fully branded home insurance offering.

We continued to innovate in the way customers experience KBC as an organisation. We made ourselves more accessible by introducing the concept of ‘pop up’ banking. Our new high street retail presence on Baggot Street in Dublin was designed with customers at the heart of the process and as more customers wish to deal with us online, we have also improved our capability and core service. Overall, we plan to bring this fresh thinking in retail banking to more customers throughout Ireland over the next number of years.

The mortgage market remains very challenging for both lenders and potential buyers. During times of financial difficulty for many, it is more important than ever to put the customer at the centre of what we do. The Bank has played a leading role in Ireland in supporting customers in difficulty. This means that we are responding to customer requirements in a

16 | KBC ANNUAL REPORT 2012 17

prompt, professional way and acting at all times in a diligent and compliant manner. Treating customers well is good business, as well as good behaviour and this has always been a hallmark of our approach.

Delivering a great customer experience is all about people. I would like to thank all of my colleagues in the Bank for their commitment, diligence and hard work over 2012. I am delighted to welcome the many new employees that have joined the Bank, which has been a very positive experience. I am particularly proud too that we have created a vibrant workplace for them which was recognised this year at the Chambers Ireland CSR Awards.

We anticipate increasing economic stability that will lead to more sustainable conditions in 2013 with the Bank in Ireland hoping to return to profitability in the medium term. 2013 will see further investment in the Bank with new retail branches and distribution platforms; continued expansion of our product portfolio and a commitment to supporting Irish homeowners, whether through the writing of new business or continuing to support mortgage arrears customers with workable solutions. We recognise the opportunity in Ireland’s recovery and are positioning ourselves to play a part in that recovery.

In December 2012 Mr. Edward Marah retired from his position as a Director of the Bank, following a 38 year association both in an executive and non executive capacity. In February 2013, Mr. Wim Eraly, Mr. Dirk Mampaey, and Mr. Luc Popelier retired from their positions as Directors of the Bank. Mr. Luc Gijsens retired from his position as Chairman of the Bank in March 2013. I would like to take this opportunity to thank each of them for their service to the Bank and wish them well for the future.

I would also like to welcome Mr. Danny De Raymaeker our newly appointed Chairman of the Bank and Mr. Bart Guns and Mr. Jan Gysels, all who have recently joined the Board of the Bank as directors.

While 2012 has presented its difficulties, we have also had many significant achievements as we strive towards our new end goal. We are enthused with optimism about the future.

2013 marks our 40th year of serving customers in Ireland. As we enter our fifth decade in Ireland and as part of a larger Banking Group with a vision to creating a new alternative Retail Bank in the future, I look forward to many years ahead to realising our ambition and our commitment to Ireland.

John H. Reynolds Chief Executive March 2013

CHIEF EXECUTIVE’S REVIEW CONTINUED

18 | KBC ANNUAL REPORT 2012 19

INCOME STATEMENT STATEMENT OF FINANCIAL POSITION

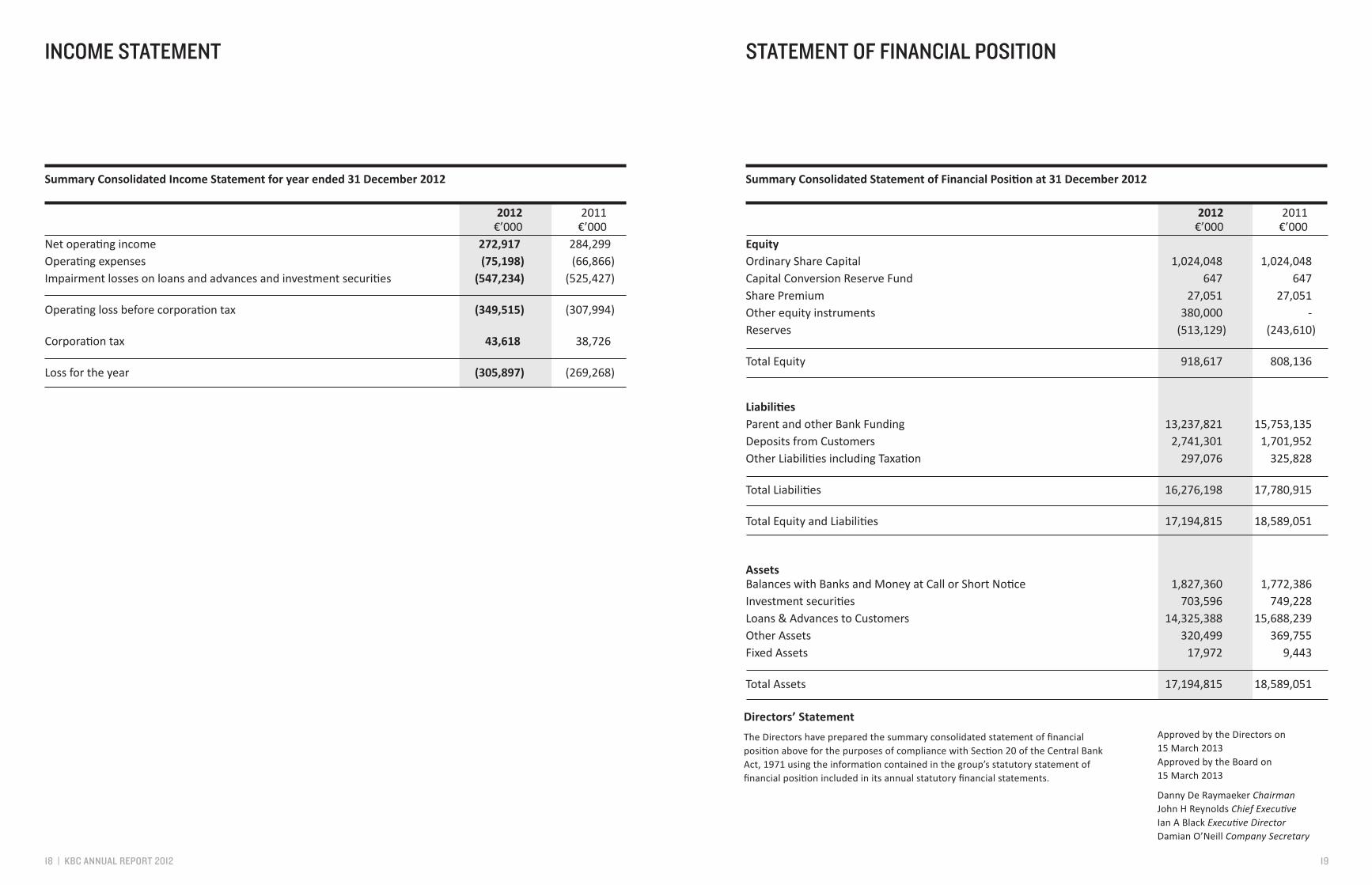

2012 2011 €’000 €’000 Net operating income 272,917 284,299Operating expenses (75,198) (66,866)Impairment losses on loans and advances and investment securities (547,234) (525,427) Operating loss before corporation tax (349,515) (307,994) Corporation tax 43,618 38,726 Loss for the year (305,897) (269,268)

Summary Consolidated Income Statement for year ended 31 December 2012 Summary Consolidated Statement of Financial Position at 31 December 2012

2012 2011 €’000 €’000 Equity Ordinary Share Capital 1,024,048 1,024,048 Capital Conversion Reserve Fund 647 647 Share Premium 27,051 27,051 Other equity instruments 380,000 - Reserves (513,129) (243,610) Total Equity 918,617 808,136 Liabilities Parent and other Bank Funding 13,237,821 15,753,135Deposits from Customers 2,741,301 1,701,952 Other Liabilities including Taxation 297,076 325,828 Total Liabilities 16,276,198 17,780,915 Total Equity and Liabilities 17,194,815 18,589,051 Assets Balances with Banks and Money at Call or Short Notice 1,827,360 1,772,386 Investment securities 703,596 749,228 Loans & Advances to Customers 14,325,388 15,688,239 Other Assets 320,499 369,755 Fixed Assets 17,972 9,443 Total Assets 17,194,815 18,589,051

Directors’ Statement

The Directors have prepared the summary consolidated statement of financial position above for the purposes of compliance with Section 20 of the Central Bank Act, 1971 using the information contained in the group’s statutory statement of financial position included in its annual statutory financial statements.

Approved by the Directors on 15 March 2013 Approved by the Board on 15 March 2013

Danny De Raymaeker Chairman John H Reynolds Chief Executive Ian A Black Executive Director Damian O’Neill Company Secretary

20 | KBC ANNUAL REPORT 2012 21

Internal Control and Risk Management

The Board acknowledges its overall responsibility for the Bank’s system of internal control and for reviewing its effectiveness. The Board has established a process for the identification, evaluation and management of the significant risks faced by the Bank, and regularly reviews this process. Line management has primary responsibility for risk management. It ensures that risk management relating to the business is embedded in the business through policies and procedures. The Bank has established a risk management function reporting to the Chief Risk Officer to assist the Bank in monitoring and assessing significant risks. The Bank has also established specialised risk management committees to monitor and assess significant risks, including business, operational, financial and compliance risks, and to review the effectiveness of internal control.

AUDITORS’ STATEMENT

Respective Responsibilities of Directors and Auditors

The Directors are responsible for the preparation of the summary consolidated financial statements for the purposes of compliance with Section 20 of the Central Bank Act, 1971.

Our responsibility is to report to you our opinion on the consistency of the Summary Consolidated Financial Statement within the summary annual report with the full annual Consolidated Financial Statements, on which we reported on 15 March 2013.

We also read the other information contained in the Summary Consolidated Financial Statement and consider the implications for our report if we become aware of any apparent misstatements or material inconsistencies with the Summary Consolidated Financial Statement. The other information comprises only the Chairman’s Statement and the Chief Executive’s Review.

Our report on the company’s full annual Consolidated Financial Statements describes the basis of our opinion on those Consolidated Financial Statements and on the Directors’ Report.

Opinion

In our opinion, the Summary Consolidated Financial Statement is consistent with the full annual Consolidated Financial Statements for the year ended 31 December 2012.

Ernst & Young Chartered Accountants and Registered Auditors Dublin 15 March 2013

Independent Auditors’ Statement to the members of KBC Bank Ireland plc on the Summary Consolidated Financial Statements for the year ended 31 December 2012

We have examined the Summary Consolidated Financial Statements for the year ended 31 December 2012, which comprise the Summary Consolidated Income Statement and Summary Consolidated Statement of Financial Position.

This statement is made solely to the company’s members, as a body. Our audit work has been undertaken so that we might state to the company’s member those matters we are required to state to them in an auditors’ statement and for no other purpose. To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other than the company and the company’s members as a body, for our audit work, for this statement, or for the opinions we have formed.

CORPORATE GOVERNANCE

Commitment to integrity is a cornerstone of our mission statement. KBC Bank Ireland (‘The Bank’) is committed to maintaining the highest standards of corporate governance, ethics, business integrity and professionalism in all of our activities. These standards are embedded in the corporate culture, reflected in our code of conduct, and reinforced through continuing communication and training.

The Bank is subject to the Central Bank of Ireland’s Corporate Governance Code for Credit Institutions and Insurance Undertakings (which is available on www.centralbank.ie). The Bank is not required to comply with the additional requirements for “major institutions”.

Role of the Board

The Board is the principal decision making forum for the Bank and is responsible to the Shareholder and other stakeholders for the leadership, direction and control of the Bank. It establishes the strategic objectives, corporate values and ethical standards that drive the activities of the Bank.

Audit Committee

The Audit Committee assists the Board by supervising the integrity, efficiency and effectiveness of the internal control measures and compliance rules in place and monitoring the effectiveness and adequacy of the Bank’s internal audit and IT systems. The Audit Committee is comprised of non-executive directors, the majority of whom are independent.

Risk Committee

The Risk Committee assists the Board in discharging its responsibilities of ensuring that risks are properly identified,reported, assessed and controlled. The Risk Committee is comprised of an appropriate representation of non executive and executive directors which is commensurate with the nature, scale and complexity of the business of the Bank.

22 | KBC ANNUAL REPORT 2012 23

Corporate Social Responsibility

The Corporate Social Responsibility (CSR) Team at KBC Bank Ireland (KBC) work together to drive socially responsible initiatives and ensure that CSR is at the heart of everything that happens within the organisation.

We attach great importance to the work of the 4 key teams who help create and deliver our CSR programme; our Wellbeing team, Green team, Community team and Sports and Social team. This commitment is evident in the daily life of the business, but also at a strategic level and through our corporate values. Below are some of the many highlights from our CSR activities in 2012.

Volunteering We actively encourage volunteering within the KBC community. 137 KBC staff volunteered their time for various initiatives last year and engaged in charity and community events. In 2012 volunteers partnered with the Lambert Puppet Theatre and brought a fun filled day to children from disadvantaged areas and those with special needs. We have many plans to engage in even more volunteer activity within the community in 2013. A volunteer policy has been implemented to raise the profile of our volunteering initiatives internally and a dedicated Volunteer Officer will organise all volunteering events.

Wellbeing and Sports & Social In September 2012, KBC was shortlisted for the Chambers Ireland National CSR Awards for Excellence in the Workplace. This reflects our commitment to delivering initiatives to assist employees in achieving a work/life balance, managing stress, promoting a healthy lifestyle and managing personal finances. Plans for 2013 include a roll out of a leading edge wellbeing programme for employees.

Employee Fundraising KBC charity partners have been carefully selected by KBC staff. Our charity partners for 2012 were Barretstown and Barnardo’s. Our Community team work throughout the year to raise much needed funds and organise staff volunteers to help these charities. We will continue this support throughout 2013 and have a full calendar of activities planned to meet our fundraising targets.

Environment The Green team focus on identifying, implementing and supporting initiatives which have a positive effect on the environment. Over the last 12 months they have delivered a significant number of environmental recycling initiatives and the focus now has turned towards the measurement and identification of sustainable and improved processes for energy usage. In the future we plan to implement a number of specific initiatives to monitor energy usage and reduce CO2 emissions to below industry average by the end of June 2014.

24 | KBC ANNUAL REPORT 2012 25

Danny De Raymaeker Chairman (Belgian) John Reynolds Chief Executive Ian Black Executive Director Dara Deering Executive Director Cameron Marr Executive Director (British) Christine Moran Executive Director Bart Guns Non-Executive Director (Belgian) Jan Gysels Non-Executive Director (Belgian) Gary Britton Non-Executive Director* John Malone Non-Executive Director* Robert Power Non-Executive Director* Damian O’Neill Company Secretary

MANAGEMENT

* Independent Non-Executive Director

John Reynolds Chief ExecutiveIan Black Chief Financial Officer/Chief Operations OfficerDara Deering Retail BankingCameron Marr Chief Risk Officer Christine Moran Corporate and Institutional Banking and Recovery

Board of DirectorsBrian Austen Compliance Tony Barnes Wholesale Operations Sinéad Brennan Human Resources Noelle Condon Finance Edward Dillon Retail Products Hugo Doherty Retail Recovery Portfolio Management Brian Dunne Legal Services Grant Hourigan Internal Audit Austin Hughes Chief Economist Darragh Lennon Banking

Siobhán Lynch Credit Acceptance Anne Marie Malone Risk Oversight Michael Martin Information Technology Rickard Mills Corporate Affairs Joseph Moore Retail Recovery Strategy Feargal O’Riagain Corporate and Institutional Markets Aidan Power Brand Marketing and e-Channels Frank Stokes Retail Recovery Operations Terry Sullivan Treasurer Pat Watt Distribution

Honorary Life President Patrick C. McEvoy

Executive Committee

Management

26 | KBC ANNUAL REPORT 2012 27

KBC Fund Management LimitedJoshua Dawson House,Dawson Street, Dublin 2.Tel: (353 1) 514 8800Fax: (353 1) 514 8701Email: [email protected]

KBC Bank NV Dublin BranchKBC House,4 George’s Dock,IFSC, Dublin 1.Tel: (353 1) 670 0888Fax: (353 1) 603 5490Email: [email protected]

KBC Finance IrelandKBC House,4 George’s Dock,IFSC, Custom House Dock, Dublin 1.Tel: (353 1) 670 0888Fax: (353 1) 670 0855Email: [email protected]

Belfast Number One Lanyon Quay, Belfast BT1 3LG. Tel: (44 28) 9044 6100 Fax: (44 28) 9044 6120 Email: [email protected]

Cork52 South Mall, Cork. Tel: (353 21) 422 2600 Fax: (353 21) 422 2693 Email: [email protected]

Galway4 Dockgate, Dock Road, Galway. Tel: (353 91) 567 744 Fax: (353 91) 567 754 Email: [email protected]

Limerick8th Floor, Riverpoint Bishops Quay, Limerick. Tel: (353 61) 448 600 Fax: (353 61) 468 468 Email: [email protected]

Dublin Sandwith Street, Dublin 2.Tel: (353 1) 664 6000Fax: (353 1) 664 6099Email: [email protected]

142 - 143 Baggot Street, Lower Baggot Street, Dublin 2.Tel: (353 1) 639 2000Email: [email protected]

OTHER KBC COMPANIES IN IRELAND

REGIONAL OFFICES

Galway Dublin

Limerick

Cork

Belfast

28 | KBC ANNUAL REPORT 2012 29

KBC Bank Ireland plc

Share Capital €’000

Authorised 2,500,000

Issued Ordinary 1,024,048

Held by KBC Group 100%

Registered Office Sandwith Street, Dublin 2.

Registered in the Republic of Ireland Number 40537. Tel: (353 1) 664 6000 Fax: (353 1) 664 6099 Email: [email protected] Swift Code ICON IE2D Website: www.kbc.ie

Auditors Ernst and Young, Harcourt Centre, Harcourt Street, Dublin 2. Solicitors Arthur Cox, Arthur Cox Building, Earlsfort Terrace, Dublin 2.

COMPANY INFORMATION

www.kbc.ie

KBC Bank Ireland PLC is regulated by the Central Bank of Ireland